Premium Tax Credit Basics Internal Revenue · PDF fileFPL used for APTC is based on projection...

78

National Governors Association Conference: Gearing Up for 2015 and Beyond: Key State Options in a Federally-Facilitated Health Insurance Marketplace July 29, 2014 -- Washington, DC Premium Tax Credit Basics Internal Revenue Service

Transcript of Premium Tax Credit Basics Internal Revenue · PDF fileFPL used for APTC is based on projection...

National Governors Association Conference: Gearing Up for 2015 and Beyond: Key State Options in a Federally-Facilitated Health Insurance MarketplaceJuly 29, 2014 -- Washington, DC

Premium Tax Credit BasicsInternal Revenue Service

Premium Tax Credit - Acronyms

EIN = employer identification numberTIN = taxpayer identification numberEHB = essential health benefitsMEC = minimum essential coverageQHP = qualified health planSLCSP = second lowest cost silver planSP = silver level qualified health planAPTC = advance payment of the premium tax creditPTC = premium tax creditFPL = federal poverty line

2

Basic Concepts

Tax family: individuals for whom the taxpayer claims a personal exemption deduction

Household income (HHI): combined modified adjusted gross income (MAGI) of all members of the tax family who must file a tax return

MAGI: AGI plus certain nontaxable income (foreign earned income, tax exempt interest, some Social Security)

Coverage family: Subset of tax family - members of the tax family who have a coverage month (enrolled in a QHP as of the first of the month and not eligible for MEC)

3

Tax Family versus Coverage Family

Tax Family--The taxpayer whose name is at the top of the tax return, plus the spouse named on the return, plus the dependents named on the return. Together with HHI, determines FPL. FPL determines whether

TP is an AT and what is the contribution amount Annual concept-- PTC uses HHI and FS (and therefore FPL)

for the entire year as shown on the tax return FPL used for APTC is based on projection of FS and HHI for

the year Coverage Family--The members of the tax family who have

coverage months; who enroll in a QHP and are not eligible for other MEC Determines what is the “applicable” SLCSP for computing

PTC Monthly concept--the coverage family may change (enroll or

disenroll, get or lose MEC, leave or join the tax family, move)4

Basic Concepts

What is the difference between APTC and PTC? There is only one PTC for a year for a taxpayer

Taxpayer must claim PTC on the tax return

PTC is based on actual HHI and FS for the year as reported on the tax return

APTC is advance payment of the estimated (projected) PTC for the year, based on estimated (projected) HHI and FS

5

Eligibility to Claim the Premium Tax Credit

Who is an applicable taxpayer? Household income for family size for the year is

between 100-400% of FPL Family size = ALL claimed exemptions For purposes of determining FPL, family size never

changes, because it is determined by exemptions on the tax return

Household income – Modified adjusted gross income (MAGI) for family members who must file MAGI= AGI + tax exempt interest & amounts

excluded under § 911 (foreign-earned income) + Social Security

6

Eligibility to Claim the Premium Tax Credit

Who is an applicable taxpayer?

Married taxpayers must file joint return except as provided in temporary regulations (abused or abandoned spouses)

Taxpayer married under law is not married for tax purposes if:

Lives apart from spouse last 6 months of year Pays more than ½ of cost of maintaining a home Home is the main home of a dependent child for

more than ½ of the year Does not file joint return with spouse

Cannot be claimed as a dependent 7

Eligibility to Claim the Premium Tax Credit

Applicable taxpayer special rules

Lawfully present alien with HHI below 100% of FPL

Marketplace projects taxpayer will be at 100-400% of FPL but ends up below 100%

Unlawfully present or incarcerated person may not enroll but may be an applicable taxpayer and claim PTC for an eligible family member

8

Eligibility to Claim the Premium Tax Credit

Taxpayer or at least one member of TP’s family has a coverage month:

Enrolled in QHP through a Marketplace

Not eligible for MEC except individual market

A United States citizen, national, or lawfully present and not incarcerated (because can’t enroll in a QHP)

Individual share of premium is paid (by someone) 9

What Is MEC?

Defined in § 5000A(f)

Government-sponsored coverageMedicaid, CHIP, Medicare, TRICARE, VA, Peace Corps, Nonappropriated Fund Health Benefits Program

Employer-sponsored coverage

Individual market

Miscellaneous MEC (designated by HHS)10

What Is MEC: Government-Sponsored Coverage

Eligible = meets the criteria for the program Special eligibility rules—treated as eligible only if

enrolled (VA, some Tricare, some Medicaid and Medicare)

Timing Eligible as of first day of first month can receive

benefits Have 2 months to submit paperwork to get

benefits (except for eligible only if enrolled) Medicaid may be retroactive--can have overlap

Medicaid and CHIP lock in rule—will not be treated as eligible based on information on the return if Marketplace determines not eligible

11

What Is MEC: Employer-Sponsored Coverage

A taxpayer and family are eligible for employer-sponsored coverage (ESI) only if it is-- Affordable, and Provides minimum value

Eligible for ESI if could have enrolled during open season

Eligible for ESI if actually enroll even if not affordable or no MV

Special eligibility rules– eligible for ESI only if enroll (retirees, continuation coverage for former employees and families)

Family does not have ESI if employee does not have ESI (unless enrolled) 12

What Is MEC: Employer-Sponsored Coverage

Affordable

Coverage is not affordable for the employee if the employee’s share of the premium for self-only coverage is more than 9.5% of HHI for the year

Coverage is not affordable for the employee’s family if the employee’s share of the premium for self-only coverage is more than 9.5% of HHI for the year

9.5% to be indexed

Lock-in rule--ESI is not affordable for the year if the Marketplace determines it will be unaffordable based on its projection of HHI

13

What Is MEC: Employer-Sponsored Coverage

Minimum value

A plan’s share of the total allowed costs of benefits provided under the plan is at least 60%

Addresses deductibles, co-pays

Based on a standard population and a defined set of benefits (pick one state’s EHB benchmark)

MV calculator on HHS website

14

Calculating the Premium Tax Credit

Determine contribution amount (theoretically, what the taxpayer should be able to pay) -- multiply taxpayer’s HHI by an applicable percentage from 2 to 9.5 based on taxpayer’s FPL (indexed after 2014)

Subtract this amount from the premium for an applicable SLCSP (the benchmark plan) (not the QHP in which the family enrolls)

The credit can be no more than the premium for the QHP in which the family enrolls (enrollment premium)

If enrollees end coverage mid-month and receive partial premium refund, each amount is prorated for the number of days of coverage

15

Contribution Amount

Hypothetical amount the taxpayer is able to pay for premiums

Percentage of the taxpayer’s HHI, based on the taxpayer’s FPL

Multiply HHI by a number from the table (2 to 9.5)

Is an annual amount because HHI and FPL are determined for the year

Divide annual contribution amount by 12 to determine amount for a coverage month

16

Contribution Amount—Applicable Percentage Table ( to be indexed)

17

Household income percentage Initial percentage Final percentage of Federal poverty line

Less than 133% 2.0% 2.0%

At least 133% but less than 150% 3.0% 4.0%

At least 150% but less than 200% 4.0% 6.3%

At least 200% but less than 250% 6.3% 8.05%

At least 250% but less than 300% 8.05% 9.5%

At least 300% but not more than 400% 9.5% 9.5%

Calculating the Premium Tax Credit -- Determining the Contribution Amount -- Scenario

Taxpayer X’s tax family is two adults (X and spouse Y) and two dependent children. The HHI for family XY is $71,550 (300% of the FPL). At 300% of the FPL, family XY’s applicable percentage is 9.5.Multiplying this applicable percentage by the HHI of $71,550, the contribution amount for family XY is $6797 ($566 per month).

At the Marketplace where family XY resides, the monthly premium for the applicable SLCSP is $1041. Therefore, the “tentative” monthly APTC amount is $1041 less $566, or $475.

HHI= $71,550% multiple= x 9.5%

Contribution for HH= $6,797 (6,797/12 months = 566 per month)

Applicable SLCSP amount= $1,041Monthly Contribution for HH= 566

Tentative monthly APTC= $475

18

Calculating the Premium Tax Credit -- Determining the Contribution Amount – Scenario (cont.)

XY and their two dependents enroll in a QHP with a monthly premium of $800. Because this premium is more than the contribution amount minus the SLCSP premium ($475), the APTC amount is $475.

The Marketplace reports the following monthly data elements: APTC: $475 SLCSP premium: $1041 Enrollment premium: $800

19

Calculating the Premium Tax Credit -- Determining the Contribution Amount – Scenario (cont.)

Alternatively, XY and their two dependents enroll in a QHP with a premium of $400. Because this premium is less than the contribution amount minus the SLCSP premium ($475), the APTC amount is $400.

The Marketplace reports the following monthly data elements: APTC: $400 SLCSP premium: $1041 Enrollment premium: $400

20

Applicable Benchmark Plan

The “applicable” SCLSP in the “rating area” where the taxpayer resides “Applicable:” the SLCSP that applies to the members

of the coverage family (enrolled in the QHP and not eligible for MEC)

Must be open to enrollment to all members of the coverage family

“Rating area” means address: Issuers offer QHPs based on service area not rating area, therefore look to the address of the taxpayer or primary subscriber

21

Applicable Benchmark Plan -- Identifying the SLCSP -- Scenario 1

22

SLCSP determined by taxpayer’s (primary subscriber’s) residence

D lives in State K. All of State K is one rating area.

Issuer P offers QHPs in State K, however, P offers QHPs based on service areas, which equal counties.

P accepts enrollments in a QHP only from individuals who live in the service area where the QHP is offered.

P offers silver level plans T, U, V, W, X, and Y in State K, but only offers plans T, V, and W in the service area where D resides.

Applicable Benchmark Plan -- Identifying the SLCSP -- Scenario 1 (cont.)

23

SLCSP determined by taxpayer’s (primary subscriber’s) residence

The monthly premiums for these QHPs are as follows:T $225 W $310U $250 X $325V $290 Y $335

Because D can enroll only in QHPs T, V, or W, only those QHPs are considered in determining D’s applicable benchmark plan.

QHPs U, X, and Y are disregarded.

Considering only T, V, and W, V is the SLCSP.

The Marketplace reports $290, the premium for V, as the premium for the SLCSP for D.

Applicable Benchmark Plan -- Identifying the SLCSP -- Scenario 2

24

SLCSP determined by taxpayer’s residence, plan not open to enrollment for some family members

Taxpayer F’s tax family is two adults (F and spouse G) and two dependents, J and K.

J is F and G’s child and K is G’s niece.

Issuer P offers silver level QHPs T, U, V, W, X, and Y for enrollment where the FG family resides, however only T, V, and W will accept a niece in family coverage.

Applicable Benchmark Plan -- Identifying the SLCSP -- Scenario 2 (cont.)

25

SLCSP determined by taxpayer’s residence, plan not open to enrollment for some family members

The monthly premiums for these QHPs are as follows:

T $225 W $310U $250 X $325V $270 Y $335

Because the entire FG household can enroll only in QHPs T, V, or W, only those QHPs are considered in determining their applicable benchmark plan.

QHPs U, X, and Y are disregarded.

Considering only T, V, and W, V is the SLCSP.

The Marketplace reports $270, the premium for V, as the premium for the SLCSP for household FG.

Applicable Benchmark Plan -- Identifying the SLCSP -- Scenarios 3 and 4

SLCSP determined by the coverage family

M, her spouse N, and their dependent P enroll in a qualified health plan. The applicable benchmark plan for their coverage is the second lowest cost silver plan covering M, N, and P.

Enrollee not in the tax family and coverage family O resides with his daughter, K, but may not claim K as a

dependent. O and K enroll in a QHP. Because K is not O’s dependent K is not in O’s tax family and if K

is not in O’s tax family she cannot be in the coverage family. O’s applicable benchmark plan is the SLCSP that applies to O. If K can claim PTC her SLCSP is the one that applies only to K.

26

Applicable Benchmark Plan -- Identifying the SLCSP -- Scenario 5

27

Enrollee not in the coverage family

Married couple J and K enroll in a QHP with their two dependent children, M and N. K is 65 years old and is eligible for Medicare. Because K is eligible for MEC he is not in the coverage family. The monthly premium for the SLCSP that applies to J, K, M, and

N is $465. The monthly premium for the SLCSP that applies to J, M, and N

is $275. The Marketplace reports $275, the premium that applies to only

J, M, and N, as the premium for the applicable SLCSP for their coverage, even though K also is enrolled in the coverage.

Applicable Benchmark Plan Issues -- Family Does Not Request APTC

An individual who does not request APTC (individual in the short line) may claim PTC on the tax return.

Taxpayer and IRS must know certain information Marketplace usually provides: premium for the SLCSP and the enrollment premium

Marketplace reports enrollment premium for all enrollments

Marketplace reports the premium for what would be the SLCSP that applies to all enrollees, OR establishes another reasonable method to determine this information at filing (lookup tool)

28

29

Applicable Benchmark Plan Issues—Family Does Not Request APTCApplicable Benchmark Plan Issues—Family Does not Request APTC--District of Columbia Health Benefits Exchange SLCSP look-up table

Applicable Benchmark Plan Issues -- Family Does Not Request APTC -- Scenario

X and Y and their two dependents enroll in a QHP with a monthly premium of $900. They do not request APTC. If all members of the tax family are in the coverage family (no one is eligible for MEC), the monthly premium for their applicable SLCSP would be $1041.

The Marketplace reports the following monthly data elements: APTC: 0 SLCSP premium: $1041 Enrollment premium: $900

30

Applicable Benchmark Plan Issues --Changes in Coverage Family

Child born, member disenrolls, member gets MEC

Family reports the change to the Marketplace —determine new SLCSP and recompute APTC

Coverage month begins on the first of the month, new APTC amount effective for the next month (in general)

Newborns – HHS rule requires effective date of coverage of child born, adopted, or placed in foster care to be date of birth (etc.); newborns are treated as enrolled as of the first of the month (in coverage family for entire month)

31

Applicable Benchmark Plan Issues -- Changes in Coverage Family -- Scenario 1

Change in the tax family and therefore the coverage family

Married couple R and S have no dependents when they enroll in a QHP during open season.

The following August they adopt a child, T, whom they will claim as a dependent.

R, S, and T enroll together in a QHP covering R, S, and T effective September 1.

The premium for the applicable SLCSP covering R and S is $390

The premium for the applicable SLCSP covering R, S, and T is $410

32

Applicable Benchmark Plan Issues -- Changes in Coverage Family -- Scenario 1 (cont.)

Change in the tax family and therefore the coverage family

The Marketplace reports $390 (for 8 months) as the premium for the applicable SLCSP for January through August.

The Marketplace reports $410 (for 4 months) as the premium for the applicable SLCSP for September through December.

*Note: because R’s and S’s family size changed, the Marketplace also must recompute R’s and S’s FPL, contribution amount, the amount of the benchmark premium less the contribution amount, and the enrollment premium.

33

Applicable Benchmark Plan Issues -- Changes in Coverage Family -- Scenario 2

Change in the coverage family but not the tax family

Married couple J and K enroll in a QHP with their two dependent children, M and N.

The monthly premium for the SLCSP that applies to J, K, M, and N is $465.

On June 1 K turns 65 years old and is eligible for Medicare. Therefore, for June through December, K s not in the coverage

family. The monthly premium for the SLCSP that applies to J, M, and

N is $275. The Marketplace reports $465 (for 5 months) as the premium

for the SLCSP for January through May and reports $275 (for 7 months) as the premium for the SLCSP for June through December.

34

Applicable Benchmark Plan Issues -- Plan Closes to Enrollment

In determining the applicable SLCSP, disregard any QHP not open to enrollment to all members of the coverage family at enrollment

SLCSP does not change if that QHP or the cheapest SP closes to enrollment or terminates after the coverage family enrolls

35

Applicable Benchmark Plan Issues -- Plan Closes to Enrollment -- Scenario 1

QHP not open at enrollment

Y has two dependents, R and S. Y, R, and S enroll in a QHP

The Marketplace where the family resides offers silver level plans 1, 2, 3, and 4, which are the first, second, third, and fourth lowest cost silver plans covering the Y family.

When the Y family enrolls, Plan 1 is closed to enrollment.

Plan 1 is disregarded in determining Y’s applicable SLCSP.

The Marketplace reports the premium for Plan 3 as the premium for Y’s SLCSP.

36

Applicable Benchmark Plan Issues -- Plan Closes to Enrollment -- Scenario 2

QHP closes to enrollment during the year

X, Y, and Z each have 2 adults in the coverage family.

Where X, Y, and Z reside, Plan 2 is the SCLSP and Plan 3 is the third LCSP covering the two adults in each coverage family.

The X and Y families each enroll in Plan 4, a QHP that is not the applicable SLCSP, during the open enrollment period.

Plan 2 closes to new enrollees the following June.

Thus, on July 1, Plan 3 is the SLCSP available to new enrollees.

37

Applicable Benchmark Plan Issues -- Plan Closes to Enrollment -- Scenario 2 (cont.)

QHP closes to enrollment during the year

The Z family enrolls in Plan 4 in July during a special enrollment period.

The Marketplace reports the premium for Plan 2 as the premium for the applicable SLCSP for X and Y for all coverage months during the year.

The Marketplace reports the premium for Plan 3 as the premium for the applicable SLCSP for Z, because Plan 2 is not open when the Z family enrolls.

38

Applicable Benchmark Plan Issues -- Plan Closes to Enrollment -- Scenario 3

QHP terminates during the year

Instead of closing to enrollment, Plan 2terminates for all enrollees in June.

Nonetheless, Plan 2 is the applicable SLCSP for X and Y for all coverage months during the year, and Plan 3 is the applicable SLCSP for Z.

39

SLCSP (Benchmark) Premium

Premium for the applicable SLCSP (benchmark plan), excluding premiums for benefits exceeding the EHBs

Allocate the premiums for benefits exceeding EHBs, then rank the silver plans

Under HHS rules issuers must report amounts allocated to excess benefits when applying for certification

Tobacco surcharges disregarded

Benchmark premium may be the sum of premiums for more than one SLCSP

40

Benchmark Premium Issue -- One Family Enrolls in Two Policies

General rule--the benchmark premium is the premium for the SLCSP that applies to the entire coverage family.

Exception--if not all QHPs will cover the entire family and the family members enroll in two or more policies, the benchmark premium may be the premium for a single policy or the combined premiums for more than one policy, whichever is the SLCSP option.

41

Benchmark Premium Issue -- One Family Enrolls in Two Policies -- Scenario 1Family chooses to enroll in two policiesTaxpayers P and Q, who are married, reside with Q’s two teenage daughters, M and N, whom they claim as dependents. P enrolls in a QHP and Q, M, and N enroll in a different QHP.

The SLCSP premiums are: $400 for covering P $550 for covering Q, M, and N $900 for covering P, Q, M, and N

The Marketplace reports $900, which is the premium for the SLCSP covering P, Q, M, and N, as the benchmark premium for the PQ family.

42

Benchmark Premium Issue -- One Family Enrolls in Two Policies -- Scenario 2SLCSP will not cover the entire coverage family

V and W are married and live with W's mother, K, whom they claim as a dependent. Issuers A, B, and C each offer one silver level plan. Issuer A charges V and W a monthly premium of $900 and Issuer B charges $700 to cover V and W. Issuers A and B do not allow adult children to enroll with a parent in one policy (except for children under age 26).

Issuers A and B respectively charge $600 and $400 for coverage for K. Issuer C offers a QHP that covers V, W, and K under one policy for a $1,200 monthly premium.

43

Benchmark Premium Issue -- One Family Enrolls in Two Policies -- Scenario 2 (cont.)SLCSP will not cover the entire coverage family

Thus, these are the silver level options for covering V’s and W’s coverage family:

Issuer A: $1,500 for premiums for two policies ($900 for V and W, $600 for K)

Issuer B: $1,100 for premiums for two policies ($700 for V and W, $400 for K)

Issuer C: $1,200 for premiums for one policy covering V, W, and K

44

Benchmark Premium Issue -- One Family Enrolls in Two Policies -- Scenario 2 (cont.)SLCSP will not cover the entire coverage family

Because some silver level qualified health plans for family coverage offered on the Marketplace do not cover all members of their coverage family under one policy, the premium for V’s and W’s applicable benchmark plan may be the premium for a single policy or for more than one policy.

The coverage offered by Issuer C is the second lowest cost silver level option for covering the VW family.

The Marketplace reports $1,200, the premium for the Issuer C coverage, as the benchmark premium.

45

Benchmark Premium Issue -- One Family Enrolls in Two Policies -- Scenario 2.5SLCSP will not cover the entire coverage family

Change the facts so that B will cover V, W, and K in one policy but C will not. A, B, and C offer the following silver level options for covering V’s and W’s coverage family:

Issuer A: $1,500 for premiums for two policies ($900 for V and W, $600 for K)

Issuer B: $1,200 for premiums for two policies ($700 for V and W, $500 for K)

Issuer C: $1,100 for premiums for one policy covering V, W, and K

46

Benchmark Premium Issue -- One Family Enrolls in Two Policies -- Scenario 2.5 (cont.)SLCSP will not cover the entire coverage family

In this case, the second lowest cost silver level option is combining the premiums for two SLCSPs. The coverage offered by Issuer B is the second lowest cost silver level option for covering the VW family.

The Marketplace reports $1,200, the premium for the Issuer B coverage, as the benchmark premium.

47

Benchmark Premium Issue -- Family Members Enroll in Different States

Each Marketplace determines SLCSP for the coverage family enrolling at that Marketplace

Taxpayer determines the benchmark premium at filing by adding the premiums for the SLCSPs that apply to each family group

48

Benchmark Premium Issue -- Family Members Enroll in Different States -- Scenario 1

J and K are married and have two dependents, R and S. J, K, and R live in New York and S attends college in California.

Although S lives in California for most of the year, J, K, R, and S enroll in a QHP through the New York Marketplace. Their monthly benchmark premium is $1,150, the benchmark premium less $300 contribution amount is $850, and their enrollment premium is $925. Their monthly APTC is $850.

The New York Marketplace reports: $1,150 as the benchmark premium $925 as the enrollment premium $850 as the APTC

49

Benchmark Premium Issue -- Family Members Enroll in Different States -- Scenario 2

Change the facts so that J, K, and R enroll together and S enrolls separately

J, K, and R enroll in a QHP through the New York Marketplace. Their monthly benchmark premium is $1,000, the benchmark premium less $300 contribution amount is $700, and their enrollment premium is $800. Their monthly APTC is $700.

S enrolls in a QHP through the California Marketplace but because she is J’s and K’s dependent J is the application filer. J applies for APTC. The California Marketplace determines that S’s monthly benchmark premium is $150 and, based on the JK family’s HHI and family size, the benchmark premium less $300 contribution amount is 0. Therefore the Marketplace does not approve APTC for S’s coverage. S enrolls in a QHP with a premium of $125.

50

Benchmark Premium Issue -- Family Members Enroll in Different States -- Scenario 2 (cont.)

The New York Marketplace reports for the JKR coverage: $1,000 as the benchmark premium $800 as the enrollment premium $700 as the APTC

The California Marketplace reports for the S coverage: $150 as the benchmark premium $125 as the enrollment premium $0 as the APTC

When J and K file their tax return, they compute their PTC using $1,150 as the benchmark premium and $925 as the enrollment premium. If their contribution amount remains $300, their monthly PTC would be $850.

51

Premiums for the Enrollment QHP

Premiums for the QHP in which the family enrolls adjusted by-- Reducing for premiums allocated to benefits exceeding

EHBs Increasing by premiums for a standalone dental plan

allocated to pediatric dental benefits

Not adjusted for tobacco surcharge

If family is enrolled in more than one QHP add pediatric dental to the premium for only one QHP

Do not reduce premiums by amount of APTC52

Adjusting Premiums for Benefits Exceeding EHBs -- Scenario 1

B enrolls in a qualified health plan that provides benefits in addition to the essential health benefits (additional benefits).

The monthly premium for the plan in which B enrolls is $385, of which $50 is allocable to the additional benefits. The premium for B’s applicable benchmark plan is $440, of which $40 is allocable to the additional benefits. The excess of the premium for B’s applicable benchmark plan over B’s $60 contribution amount is $340 per month.

53

Adjusting Premiums for Benefits Exceeding EHBs -- Scenario 1(cont.) The enrollment premium and the applicable benchmark

premium each is reduced by the portion of the premium that is allocable to the additional benefits provided under that plan.

Total Without non-EHBs Less cont. amountBenchmark premium: $440 $400 $340Enrollment premium: $385 $335

After allocating premiums to non-EHBs, the smaller of the benchmark premium less contribution amount or the enrollment premium is $335 the enrollment premium.

The Marketplace reports: $400 as the benchmark premium $335 as the enrollment premium $335 as the APTC.

54

Adjusting Premiums for Benefits Exceeding EHBs -- Scenario 1.5 Same facts except that the plan in which B enrolls provides no

additional benefits. Total W/o non-EHBs Less cont. amount

Benchmark premium: $440 $400 $340Enrollment premium: $385 $385

After allocating premiums to non-EHBs, the smaller of the benchmark premium less contribution amount or the enrollment premium is $340.

The Marketplace reports: $400 as the benchmark premium $385 as the enrollment premium $340 as the APTC.

55

Adjusting Premiums for Pediatric Dental Benefits -- Scenario

C and C’s dependent, R, enroll in a QHP. The monthly premium for the QHP in which C and R enroll is $390. The QHP does not provide dental coverage and C enrolls in a stand-alone dental plan covering C and R.

The portion of the monthly premium for the dental plan allocable to pediatric dental benefits is $50. The benchmark premium is $465 and the excess of the benchmark premium over C’s $60 contribution amount is $405/month.

56

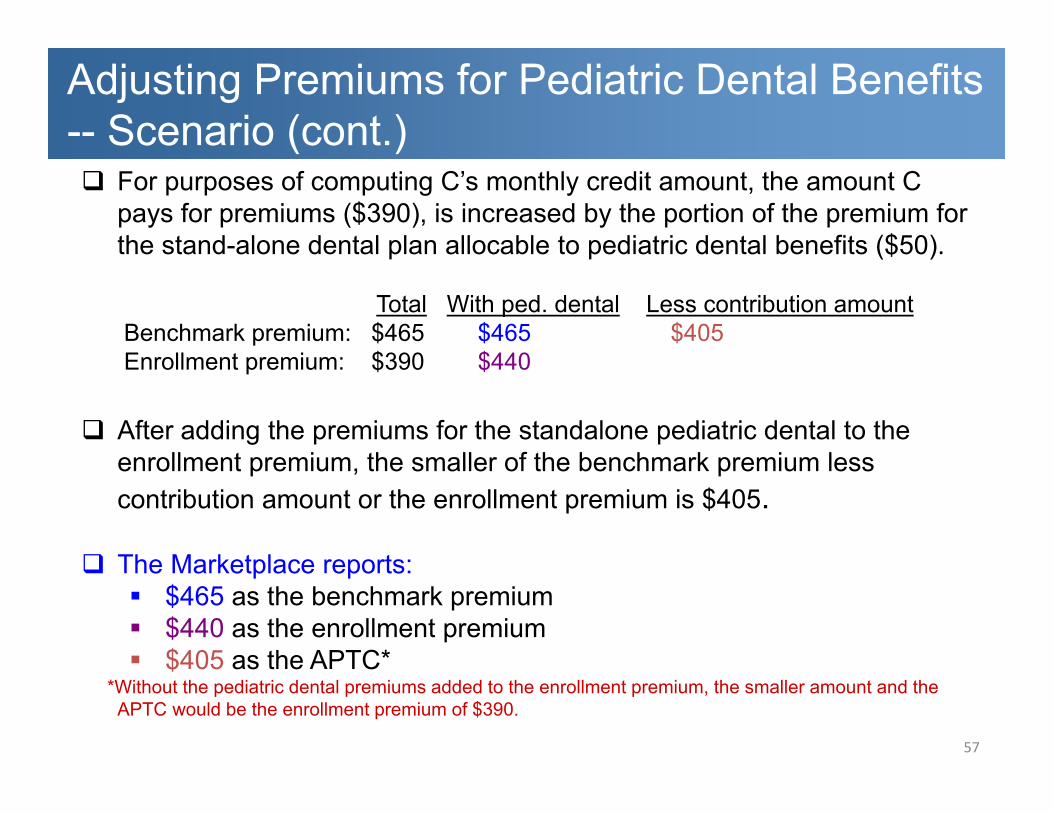

Adjusting Premiums for Pediatric Dental Benefits -- Scenario (cont.) For purposes of computing C’s monthly credit amount, the amount C

pays for premiums ($390), is increased by the portion of the premium for the stand-alone dental plan allocable to pediatric dental benefits ($50).

Total With ped. dental Less contribution amountBenchmark premium: $465 $465 $405Enrollment premium: $390 $440

After adding the premiums for the standalone pediatric dental to the enrollment premium, the smaller of the benchmark premium less contribution amount or the enrollment premium is $405.

The Marketplace reports: $465 as the benchmark premium $440 as the enrollment premium $405 as the APTC*

*Without the pediatric dental premiums added to the enrollment premium, the smaller amount and the APTC would be the enrollment premium of $390.

57

Two Tax Families Enroll in one QHP

The taxpayer of each family may claim PTC (and be provided APTC) based on that taxpayer’s separate tax family, HHI, and benchmark plan

The enrollment premium, which is the only one amount that applies to both families, must be allocated to each family based on their benchmark premiums

What if only one family gets APTC?

58

Two Tax Families Enroll in one QHP -- Scenario 1-- Both Get APTC

A, B, C, and D enroll together in a QHP. D is A’s 25-year old child who is not A’s dependent. B and C are A’s two children who are A’s dependents. B has no dependents. The premium for the plan in which A and D enroll is $15,000. The premium for the SLCSP covering only A, B, and C is $12,000. The premium for the SLCSP covering D is $6,000.

A and D request APTC. A computes her credit using her household income, a family size of three, and a benchmark premium of $12,000. A’s benchmark premium less her contribution amount is $11,000.

59

Two Tax Families Enroll in one QHP -- Scenario 1 (cont.) -- Both Get APTC D computes his credit using his household income, a family size

of one, and a benchmark plan premium of $6,000. D’s benchmark premium less his contribution amount is $4,000.

A DBenchmark premium: $12,000 $6,000Less contribution amount: $11,000 $4,000Enrollment premium: ? ?

The $15,000 enrollment premium is allocated to A and D in proportion to their benchmark premiums.

Total benchmark premiums = 18,000 A’s benchmark premium is 12,000, 2/3 of 18,000 Multiply 15,000 enrollment premium by 2/3 = 10,000 D’s benchmark premium is 6,000, 1/3 of 18,000 Multiply 15,000 enrollment premium by 1/3 = 5,000

60

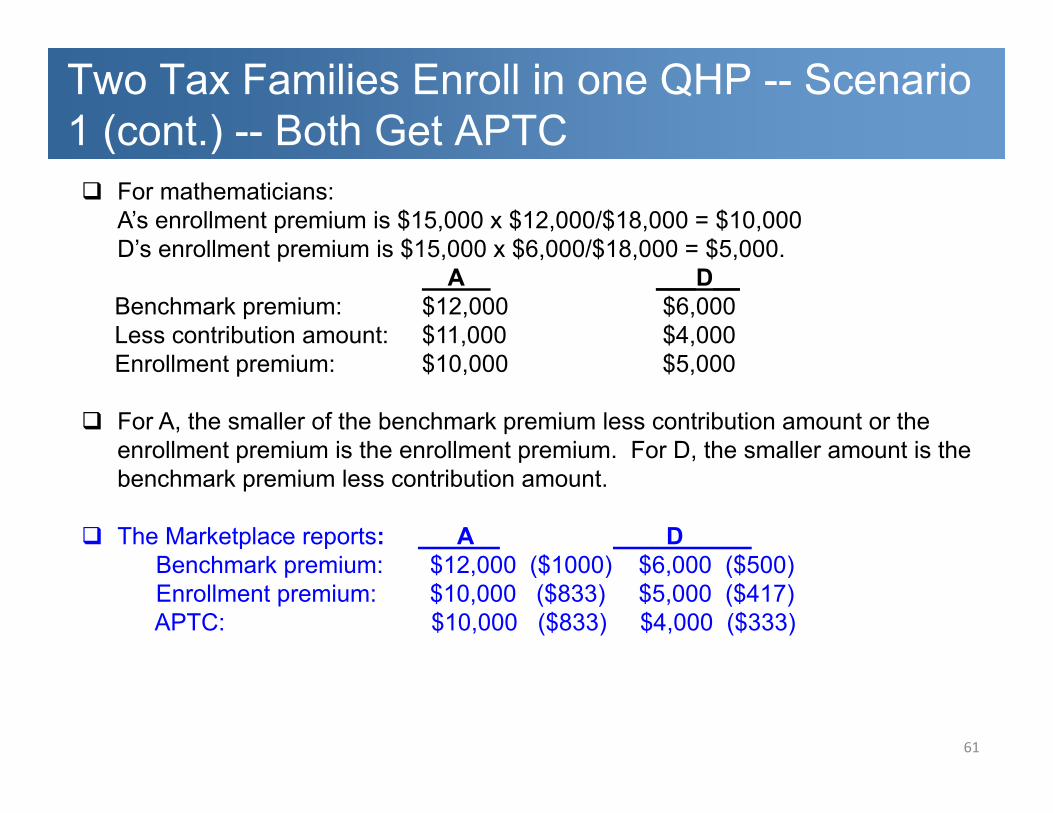

Two Tax Families Enroll in one QHP -- Scenario 1 (cont.) -- Both Get APTC For mathematicians:

A’s enrollment premium is $15,000 x $12,000/$18,000 = $10,000D’s enrollment premium is $15,000 x $6,000/$18,000 = $5,000.

A ___D__Benchmark premium: $12,000 $6,000Less contribution amount: $11,000 $4,000Enrollment premium: $10,000 $5,000

For A, the smaller of the benchmark premium less contribution amount or the enrollment premium is the enrollment premium. For D, the smaller amount is the benchmark premium less contribution amount.

The Marketplace reports: A DBenchmark premium: $12,000 ($1000) $6,000 ($500)Enrollment premium: $10,000 ($833) $5,000 ($417) APTC: $10,000 ($833) $4,000 ($333)

61

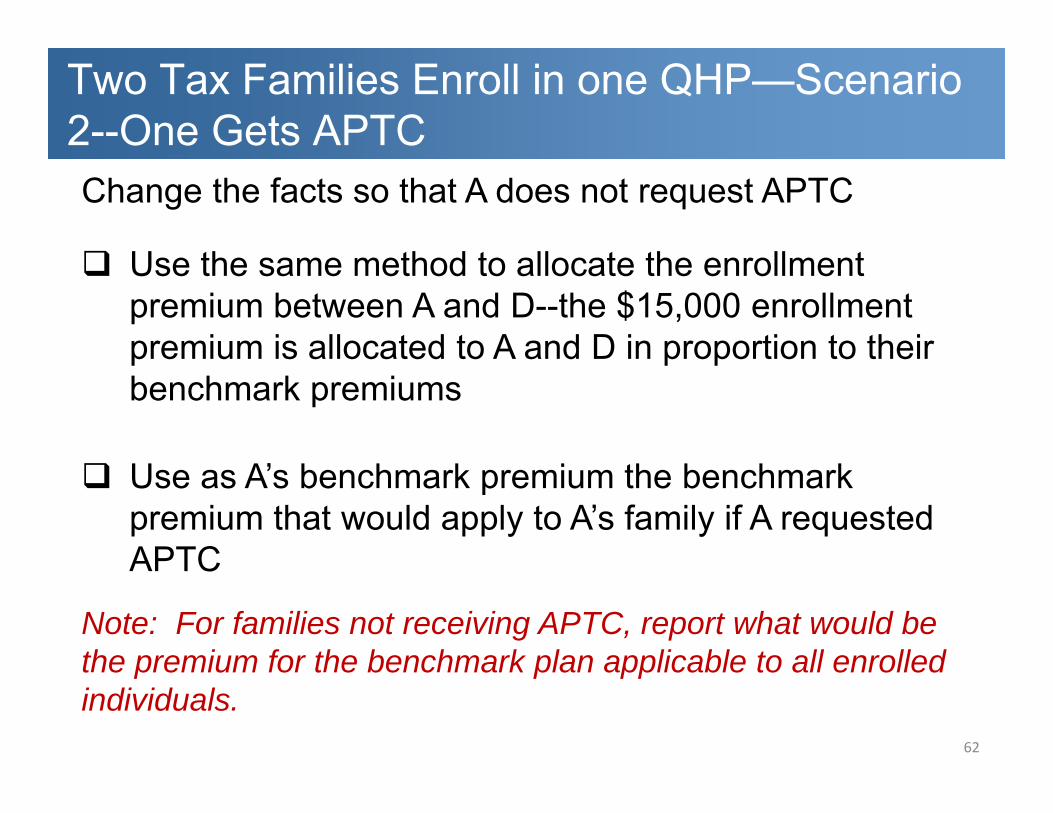

Two Tax Families Enroll in one QHP—Scenario 2--One Gets APTCChange the facts so that A does not request APTC

Use the same method to allocate the enrollment premium between A and D--the $15,000 enrollment premium is allocated to A and D in proportion to their benchmark premiums

Use as A’s benchmark premium the benchmark premium that would apply to A’s family if A requested APTC

Note: For families not receiving APTC, report what would be the premium for the benchmark plan applicable to all enrolled individuals.

62

Two Tax Families Enroll in one QHP—Scenario 2 (cont.)--One Gets APTC For mathematicians:

A’s enrollment premium is $15,000 x $12,000/$18,000 = $10,000D’s enrollment premium is $15,000 x $6,000/$18,000 = $5,000.

A D Benchmark premium: $12,000 $6,000Less contribution amount: $5,000Enrollment premium: $10,000 $5,000

D’s APTC is limited by the enrollment premium, which is less that the benchmark premium less contribution amount

The Marketplace reports: A D Benchmark premium: $12,000 ($1000) $6,000 ($500)Enrollment premium: $10,000 ($833) $5,000 ($417) APTC: $5,000 ($417)

63

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Enrollment Taxpayer and/or family members apply for coverage in a qualified health plan

through a Marketplace and request financial assistance.

Family members evaluated for eligibility for Medicaid or Children’s Health Insurance Program. Marketplace requests information from other agencies on eligibility for other government coverage.

Marketplace considers if family members have qualifying employer coverage (affordability and cost-sharing).

Marketplace estimates what will be HHI, family size, and FPL at end of year, determines if taxpayer is eligible for PTC (must be 100% to 400% FPL, except certain immigrants who may be under 100% FPL); if so, Marketplace identifies the applicable SLCSP and calculates the maximum APTC.

Consumers select one or more qualified health plans and decide whether to apply entire maximum APTC or less.

Marketplace notifies issuer of enrollment and notifies appropriate agency to begin APTC payments to issuer. 64

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Calculating the Premium Tax Credit

Determine contribution amount—theoretical estimate of what the taxpayer should be able to pay-- multiply taxpayer’s HHI by an applicable percentage based on taxpayer’s FPL

Subtract this amount from the premium for an applicable SLCSP (the benchmark plan) (not the QHP in which the family enrolls)

The credit can be no more than the premium for the plan in which the family enrolls (enrollment premium)

Changes to any of these amounts from what Marketplace used to compute APTC will result in PTC amount on return that is more or less than APTC

65

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Calculating the Premium Tax Credit

Tax Family vs. Coverage Family

Tax Family--The taxpayer whose name is at the top of the tax return, plus the spouse named on the return, plus the dependents named on the return. Together with HHI, determines FPL. FPL determines whether TP is

an AT and what is the contribution amount Annual concept-- PTC uses HHI and FS (and therefore FPL) for the

entire year as shown on the tax return FPL is only estimated at enrollment (open or special)

Coverage Family--The members of the tax family who have coverage months; who enroll in a QHP and are not eligible for other MEC Determines what is the “applicable” SLCSP for computing PTC Monthly concept--the coverage family may change (enroll or

disenroll, get or lose MEC, leave or join the tax family)

66

Reconciliation of Advance Credit Payments and Premium Tax Credit --Tax Filing

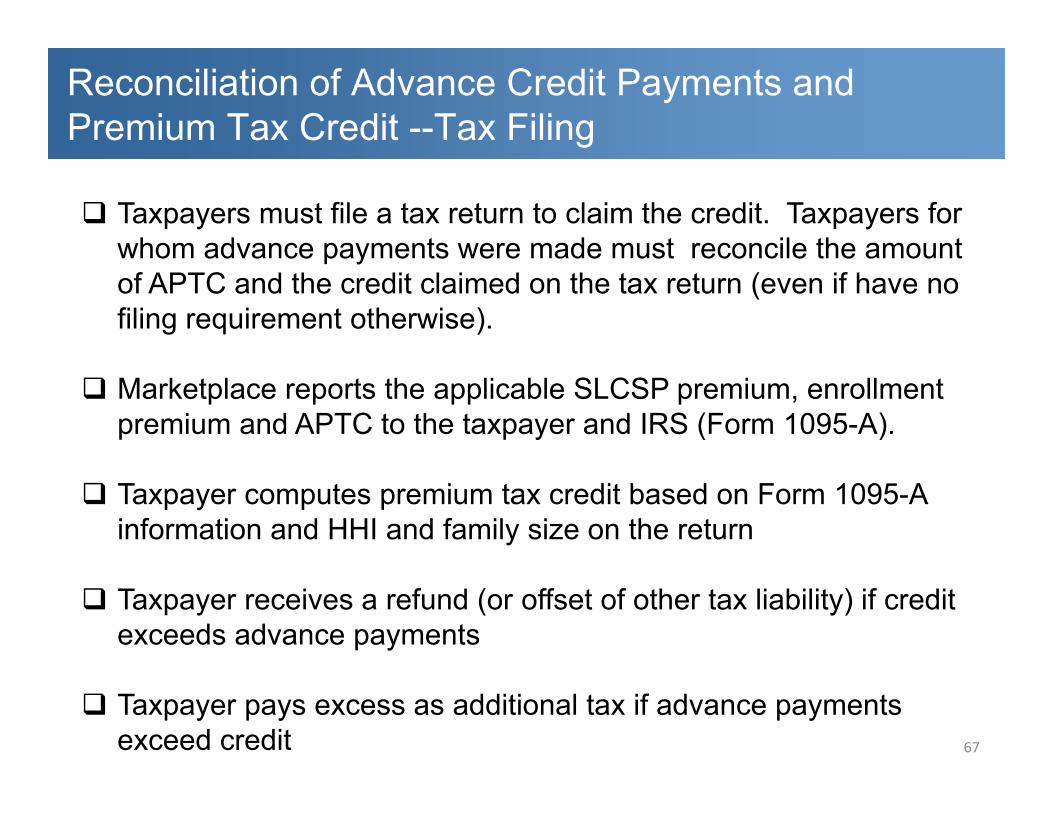

Taxpayers must file a tax return to claim the credit. Taxpayers for whom advance payments were made must reconcile the amount of APTC and the credit claimed on the tax return (even if have no filing requirement otherwise).

Marketplace reports the applicable SLCSP premium, enrollment premium and APTC to the taxpayer and IRS (Form 1095-A).

Taxpayer computes premium tax credit based on Form 1095-A information and HHI and family size on the return

Taxpayer receives a refund (or offset of other tax liability) if credit exceeds advance payments

Taxpayer pays excess as additional tax if advance payments exceed credit 67

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Changed Circumstances

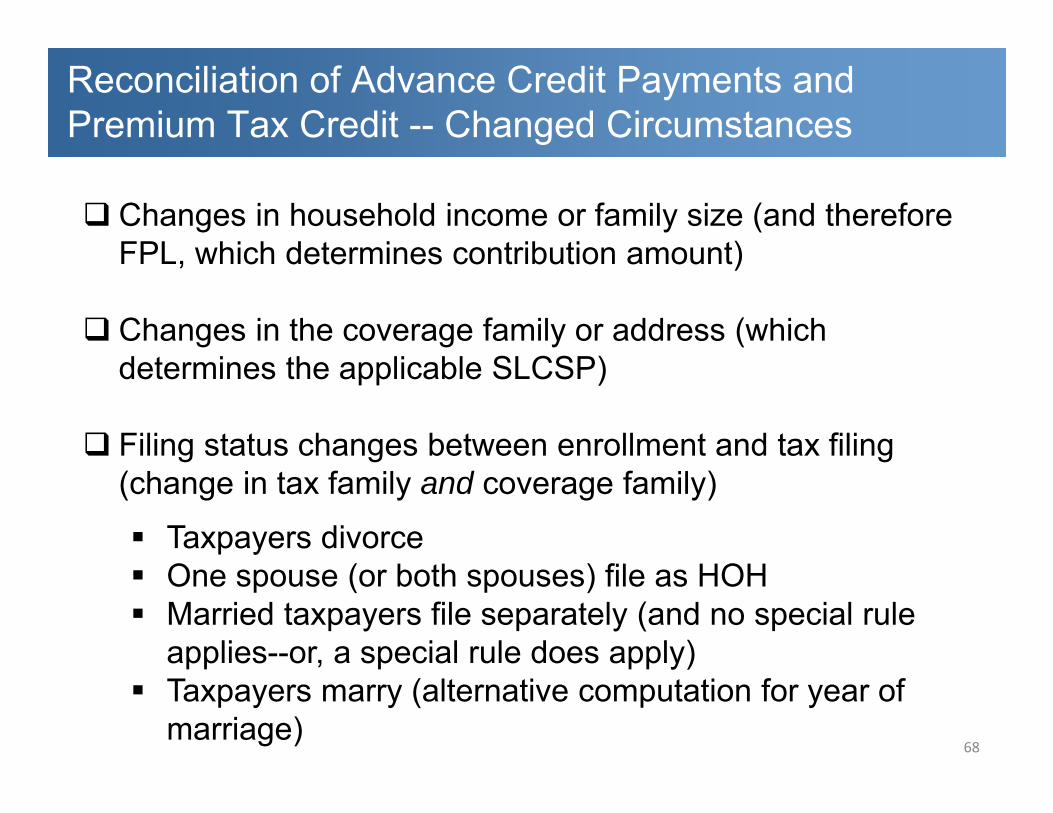

Changes in household income or family size (and therefore FPL, which determines contribution amount)

Changes in the coverage family or address (which determines the applicable SLCSP)

Filing status changes between enrollment and tax filing (change in tax family and coverage family) Taxpayers divorce One spouse (or both spouses) file as HOH Married taxpayers file separately (and no special rule

applies--or, a special rule does apply) Taxpayers marry (alternative computation for year of

marriage)68

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Changed Circumstances -- Consequences

Change in tax family size (gain or lose a family member, change in dependency status) or expected HHI

• Could result in higher FPL and lower PTC• Could result in losing applicable taxpayer status

(must repay all APTC with no cap)

Change in coverage family (family member gains or loses MEC eligibility; family member enrolls or disenrolls) Changes the SLCSP that applies for computing PTC Move to another rating area (may change applicable

SLCSP)

69

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Changed Circumstances -- Consequences

Encourage recipients of APTC to report changes in circumstances to the Marketplace as they happen and discontinue APTC or adjust amount

If don’t report changed circumstances, Taxpayer cannot rely on information reported on Form 1095-A

If coverage family has changed Taxpayer will have to identify applicable SLCSP premium at filing (FFM and states may have lookup tools)

70

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Special Issue (No APTC)

APTC is optional; taxpayer may claim PTC on the tax return although no APTC was paid

Marketplace must report information on Form 1095-A for all enrollments but requests less information from applicants not requesting financial assistance

Marketplace cannot identify the coverage family and reports applicable SLCSP premium based on all enrollees

Taxpayer must determine correct applicable SLCSP at filing (lookup tools)

71

72

Applicable Benchmark Plan Issues—Family Does Not Request APTCDistrict of Columbia Health Benefits Exchange SLCSP look-up table

Reconciliation of Advance Credit Payments and Premium Tax Credit--Changed Circumstances -- Filing Status Changes

Special rules and examples describe how to compute PTC when filing status changes between enrollment and filing

Married -- divorced Single -- married (alternative calculation

for year of marriage may reduce excess APTC) Married -- HOH Married -- married filing separately

73

Reconciliation of Advance Credit Payments and Premium Tax Credit--Changed Circumstances -- Alternative Calculation for Year of Marriage

Optional alternative method for computing PTC for taxpayers who marry during the year

Allows taxpayers to compute premium assistance amounts for the single months using ½ annual HHI and actual family size during those months (instead of HHI and FS on tax return)

May reduce amount of excess APTC to be repaid; may not be used if PTC exceeds APTC, thus taxpayers must first compute PTC the standard way

74

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Allocation Situations

If a taxpayer or dependent (at end of year, whether or not identified at enrollment) is enrolled in a policy at some time in the year with another taxpayer, the taxpayers may be required to allocate between themselves one or more amounts for SLSCP premiums, enrollment premiums, and APTC

Divorce HOH or MFS filing status Child enrolled by and with one parent and claimed as a

dependent by other parent Taxpayer enrolled with child intended to claim as a

dependent and does not claim Two taxpayers enrolled in one policy

75

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Protection Against Changes in Circumstances --Limitation on Repayment

There is a limitation (cap) on repayment of excess APTC for taxpayers with HHI less than 400% of FPL (not at 400%)

FPL Single* All others*

Less than 200% $ 300 $ 600

200% to less than 300% $ 750 $1,500

300% to less than 400% $1,250 $2,500

*Refers to filing status.

76

Reconciliation of Advance Credit Payments and Premium Tax Credit -- Protection Against Changes in Circumstances -- Lock-in Rules

Three “lock-in” rules protect taxpayers from receiving less credit or losing PTC eligibility entirely

Applicable taxpayer lock-in: if Marketplace determines that taxpayer’s FPL will be between 100% and 400% based on projected HHI and family size, taxpayer will not lose eligibility for PTC if FPL is less than 100% based on return information.

Medicaid eligibility lock-in: if Marketplace determines that taxpayer’s FPL will be above Medicaid eligibility standard, taxpayer will not be treated as eligible for Medicaid because FPL based on tax return is within Medicaid standards.

Employer coverage affordability lock-in: if Marketplace determines that available employer coverage will not be affordable based on taxpayer’s required contribution and HHI, taxpayer will not be treated as eligible for employer coverage if it would have been affordable based on income on tax return.

77

IRS Support

IRS guidance, including frequently asked questions, may be found on the irs.gov website(www.irs.gov/aca)

Please contact [email protected], IRS liaison with the states, with questions or comments.

78