Premium Financing - RD Marketing Group Premium Financing Sample... · publicly traded stock, ......

23

TransACE® TRANSAMERICA LIFE INSURANCE COMPANY Life Insurance Supplemental Illustration Valued Client Transamerica 1150 S Olive Street Los Angeles, CA 90015 Prepared For: Prepared By: Financing Life Insurance Premiums with a Third-Party Lender Premium Financing: Leveraging Your Net Worth THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE. ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000 Transamerica Life Insurance Company This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 1 of 16

Transcript of Premium Financing - RD Marketing Group Premium Financing Sample... · publicly traded stock, ......

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Valued ClientTransamerica

1150 S Olive Street

Los Angeles, CA 90015

Prepared For: Prepared By:

Financing Life Insurance Premiums

with a Third-Party Lender

Premium Financing:

Leveraging Your Net Worth

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 1 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Table of Contents

Table of Contents

I. Leveraging Assets with Life Insurance and Premium Financing

II. Nuts & Bolts: How Does Premium Financing Work?

III. Why Premium Financing Could Be the Right Choice for You

IV. Typical Loan Characteristics

V. Your Snapshot: Financing vs. Non-Financing Comparison

VI. Charting Your Loan

VII. Exit Strategies: Making the Best Choice for Loan Repayment

VIII. The Transamerica Advantage

IX. Frequently Asked Questions

X. Disclosures

Appendix

A. Premium Finance Proposal

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 2 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Leveraging Assets with Life Insurance and Premium Financing

Purchasing life insurance is an ideal way to help you provide a legacy to your family or favorite charity. However, the

idea of liquidating high-yielding investments in order to pay the premiums of a life insurance policy may not be an

appealing one. The good news is that there is a way to get the quality Transamerica life insurance you need by

leveraging those assets and securing a loan while not disrupting the growth of your portfolio. It’s known as premium

financing, and Transamerica has the expertise to help you find just the right provider to allow you to take full

advantage of it.

The Challenge: Large Premiums and Gift Tax Liability

You’ve worked hard to achieve financial success, accumulating a sizeable estate that you hope to leave as a legacy to

your loved ones. You recognize the vital role that life insurance plays in helping you achieve this goal. However,

adequate life insurance coverage for a high-net-worth individual tends to require significant premium payments.

Furthermore, annual “gifts” of premiums to a Legacy Trust set up as an Irrevocable Life Insurance Trust (ILIT) may be

subject to gift taxes. And the more your money is taxed, the less there is to leave to those you care about most.

The Strategy: Borrow Premiums from a Third-Party Lender

If the idea of liquidating assets to buy a life insurance policy doesn’t appeal to you, you may consider financing the

premiums through a third-party lender. Here’s how it would work: Your Legacy Trust trustee, rather than you

personally, can apply for the loan using the policy itself and some other asset(s) as collateral. Because the lender will

advance the funds to the insurance provider to pay the premium, the trustee will only be responsible for paying the

interest on the loan. In other words, you will not need to make annual gifts to the Legacy Trust to cover the premium.

Instead, you need only make annual gifts to the Legacy Trust in the amount of interest due, which will likely be less

than the cumulative premium.[F1] Smaller gifts mean a potentially smaller amount of gift tax. Once it comes time to

repay the premium loan, you may have several options, including simply allowing the repayment to come from your

beneficiaries' proceeds.

[F1] Loan interest in some future year or years may exceed the cost of premiums in those years. However, the

cumulative outlay for interest may generally be less than the cumulative outlay for premiums.

I. Leveraging Assets

with Life Insurance and Premium Financing

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 3 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Using premium financing to purchase life insurance through your Legacy Trust may be an attractive alternative for

getting the benefits of life insurance without potentially jeopardizing your assets' ability to earn interest. The following

diagram demonstrates how the premium financing process generally works.

II. Nuts & Bolts:

How Does Premium Financing Work?

* Process requires that the insured provide among other things the following documents: (1) tax returns; (2) personal financial

statements; (3) brokerage statements, if any. The reason for this is that the insured/grantor is providing the collateral on behalf of the

trust which is borrowing the premiums. Therefore it is necessary for the insured/grantor to have adequate assets and a strong balance

sheet to qualify for the loan.

** Typically, cash surrender value of a life insurance policy will serve as primary collateral for the loan. However, new policies may not

have much cash surrender value in early years. So, you may need to make up for any shortfall between the loan balance and cash

surrender value by pledging some other assets as collateral. Acceptable forms of collateral generally include cash, cash equivalents,

publicly traded stock, other life insurance cash surrender value, letters of credit and personal guarantees.

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 4 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Using premium financing to purchase a Transamerica life insurance policy and further leverage certain of your assets may

make a lot of sense. Take a moment to review the candidate profile, benefits and special considerations to help you decide if

premium financing is right for you.

Ideal Candidates

Should typically be 60-80 years of age [F2] and have one or more of the following:

§ Have a tangible net worth of greater than $5 million (excluding the residence)

§ Require life insurance with an annual premium of $100,000 or more

§ Be a business owner, with the majority of assets fully invested and illiquid

§ Business owners looking to fund key-person coverage or a buy-sell agreement

Benefits of Premium Financing

§ High-Performing Assets Kept Intact: With a premium financed policy you can get the life insurance coverage you need

without liquidating as many high-performing investments and incurring any attendant income taxes.

§ Out-of-Pocket Expense: With a premium financed policy your required annual outlay will be loan interest only, which may

likely be less than the full amount of the premium that would be due annually and cumulatively on a non-financed policy.

§ Reduced or Eliminated Gift Tax Liability: Because you are gifting to your trust only the funds needed to cover the annual

interest (as opposed to the full premium), you may be able to reduce or potentially eliminate any gift tax liability on those

funds used to pay premiums.

§ Interest Rate Arbitrage: A low interest rate environment means it is more likely for you to obtain a loan with

interest rates that are less than the rate of return you can expect to earn on your currently invested assets.

Considerations

§ Loan Repayment: You may be able to rely on the death benefit to repay your loan, but if that is not feasible then an

alternate loan exit strategy should be considered.

§ Interest Deferral: Keep in mind that deferring payment of interest on your loan will quickly increase the amount of that loan

and therefore will reduce the net death benefit if you do not create a plan for repaying the loan.

§ Fluctuations in Interest Rate: The interest rate for a premium finance loan is typically based on a benchmark (for

example, LIBOR or the Prime Rate) plus a spread. It is important to note that although the spread is usually fixed for the

term of the loan, the benchmark fluctuates, making the amount of your required interest payments fluctuate as well.

§ Loan Interest Is Generally Not Deductible: However, if a business owns the policy, interest may be deductible in

limited circumstances as determined by a tax professional.

[F2] Ideal candidates are not limited to this specific age group. Premium financing may also be suitable for candidates in their 40s and

50s.

III. Why Premium Financing

Could Be the Right Choice for You

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 5 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

The elements of a premium-financed policy are similar to those of any loan, including term, collateral, interest rate

and repayment considerations. The following information provides additional information about each aspect of this

type of loan and how it can be used to purchase a life insurance policy.

TermsPremium financing loans are either annually renewable or fixed for a term of years. Regardless of the term of the

loan, a lender will require the loan to either be repaid or refinanced upon maturity.

CollateralWhen financing a life insurance policy with a loan, the cash surrender value of the policy will always be the primary

collateral. Any deficit between the loan balance and the policy cash value can be resolved by providing other

asset(s) as additional collateral.

Other assets may include cash, cash equivalents, publicly traded stock, cash values of other life insurance policies,

letters of credit and personal guarantees.

When using other assets, please note:

§ The cash value of any policies may not be available during the time it is collateral for the loan.

§ The collateral value of stocks and other securities is usually discounted to reflect fluctuations in their market

value.

§ Real estate and privately held stock may not be acceptable as collateral. Some lenders, however, will use

these assets as consideration for a letter of credit, which can be used as collateral. In some cases your

collateral will need to be managed or held by the lender for the duration of the loan.

Personal GuaranteeSome lenders may ask you to personally guarantee the loan. There is some concern that simply providing a

guarantee could be considered a taxable gift. The Internal Revenue Service (IRS) has issued and withdrawn a

private letter ruling on this subject, and it remains a gray area. Alternatively, there may be no taxable gift until

obligations are paid under the guarantee. [F3]

[F3] It has become accepted practice in the industry to allow the personal guarantees as a form of collateral. However,

you and your qualified advisors should consider the tax implications.

IV. Typical Loan Characteristics

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 6 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Interest Rates

Interest rates vary by lender. Generally, the interest rate is made up of two elements, an index and a spread. The

12-month LIBOR (London Interbank Offered Rate) and the Prime Rate are commonly used indices. While both fixed

and variable interest loans may be available, variable interest loans are more common.

The following graphs show the individual performances of both the LIBOR and the Prime Rate indices over the past

few years. This information should offer you a good snapshot of how these indices have performed historically and

indicate the volatility involved in interest rates going forward.

IV. Typical Loan Characteristics

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 7 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Using premium financing to fund a Transamerica life insurance policy not only allows your other assets to remain

intact and earning interest, but also may shield more of your money from gift taxes. Take a look at how you could

benefit from a premium-financing strategy to fund a Transamerica life insurance policy. Below is an example of how

much money premium financing can save you over 20 years. [F4]

Annual Premium

Initial Loan Amount

Cumulative Loan through year 20

Total Loan Interest paid through year 20

N/A

N/A

N/A

N/A

Cumulative Out-of-Pocket Expenses

through year 20

Cumulative Gifts through year 20

Initial Gift Amount

Gross Death Benefit in year 20

Death Benefit Net of Loan in year 20

[F4] The planning year was determined when designing this illustration. The highlighted planning year can be changed at any point at

your direction. The year used as the planning year may coincide with life expectancy based on the IRA required minimum

distribution tables provided by the Treasury, or may be a year that was preselected based on your planning objectives.

[F5] Any increase in the premium located in the premium financing column may reflect the cost of the Return of Premium

(ROP) feature.

$800,000

$6,775,000

$5,609,625

$5,609,625 $5,782,700

$5,609,625 $5,782,700

$16,775,000

$10,000,000

$800,000

$0

Premium Financing [F5] No Financing

$289,135

$289,135

$10,000,000

V. Your Snapshot:

Financing vs. Non-Financing Comparison

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 8 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Cumulative Loan

through Year 20:

$6,775,000

Cumulative Interest

through Year 20:

$5,609,625

Valued Client

* If in a given year the amount gifted to the trust exceeds the amount of interest due in that year, the excess gift will grow

by a rate of return. Any excess gifts and the interest earned may be used to pay loan interest in future years and offset

future gifts to the trust from the insured/grantor.

Cumulative Gifts

through Year 20:

$5,609,625

Cumulative

Premiums

through Year 20:

$6,775,000

Death Benefit Net of

Loan in Year 20:

$10,000,000

Gross Death Benefit

in Year 20:

$16,775,000

Required Collateral (Outside of Policy Cash

Values) in Year 20: $3,244,463

VI. Charting Your Loan

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 9 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

Repayment

Creating an exit strategy is essential when you are considering financing life insurance premiums, and is something that

should be implemented before the cumulative loan balance becomes unwieldy. You may choose from a number of

strategies including:

Pay Off the Loan

Liquidate Assets - The most obvious way to repay your loan would be to liquidate assets while you’re still living to cover the

cost of the loan.

Withdraw from the Policy Cash Value - You may also withdraw from the cash value of the policy itself to pay off the loan.

The challenge with this approach, however, is that most lenders require approval before any withdrawals are allowed. In

addition, the policy may not perform as expected, resulting in insufficient cash values and a potential lapse in coverage.

Use Policy’s Death Benefits - Another option is to simply repay the loan from the life insurance policy’s death benefit.

However, in doing so, you will decrease the amount of the death benefit left to your beneficiaries.

Return of Premium Option

A borrower who wants to ensure a certain death benefit may have the option of electing a return of premium (ROP)

feature. Electing ROP and paying all loan interest as it comes due will help to ensure that the desired amount of death

benefit will be available for your beneficiaries.

Establish a Grantor Retained Annuity Trust

A more sophisticated exit strategy is to establish a Grantor Retained Annuity Trust (GRAT). A GRAT is an estate-planning

device that allows you to reduce your taxable estate by making a deferred gift to beneficiaries that’s been discounted for

gift tax purposes.[F6] You can use a GRAT as a loan exit strategy by designating your Legacy Trust as your GRAT

beneficiary.

[F6] It is important to note that if you fail to survive the selected term of the GRAT, the assets left in the trust at the time of death

will be subject to estate taxes--resulting in no worse a situation than if the transfer never occurred, except for the

administrative costs and fees of establishing the GRAT.

VII. Exit Strategies: Making the Best Choice

for Loan Repayment

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 10 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

VII. Exit Strategies: Making the Best Choice

for Loan RepaymentEstate Tax Exposure & Finding the Right Loan Repayment Plan

You’ve worked hard to build a large estate, but it may be currently exposed to estate tax. If you’ve decided to finance the

premiums of a life insurance policy to provide the liquidity necessary to pay these taxes, you also realize the importance of

implementing a plan to pay off the premium finance loan before the cumulative loan balance becomes unwieldy. In some

circumstances use of the policy proceeds may be applied to repay the loan, while in other cases lifetime planning requires

an exit strategy involving the use of other assets.

If you require estate planning and a premium finance loan exit strategy, you can solve both problems with a Grantor

Retained Annuity Trust ("GRAT"). A GRAT pays you an annuity for the term of the trust and is an estate-planning device

that allows you to reduce your taxable estate by making a deferred gift through the trust to beneficiaries at a discount for gift

tax purposes.[F7] It is a trust for a specified term of years to which you make a one-time transfer of an asset. At the end of

this term, the remaining trust assets will be distributed to beneficiaries.

You can use a GRAT as a loan exit strategy by designating your Legacy Trust as the GRAT beneficiary. You can select a

shortened premium payment schedule so that you will know the exact loan balance at the end of the short pay period

(assuming that interest is paid annually). The term of the GRAT should coincide with the short-pay period so that the

remainder interest, once distributed to the Legacy Trust, can be used to repay the outstanding loan balance.

[F7] It is important to note that if you fail to survive the selected term of the GRAT, the assets left in the trust at the time of

death may be subject to estate taxes--resulting in no worse a situation than if the transfer never occurred, except

for the administrative costs and fees of establishing the GRAT.

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 11 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

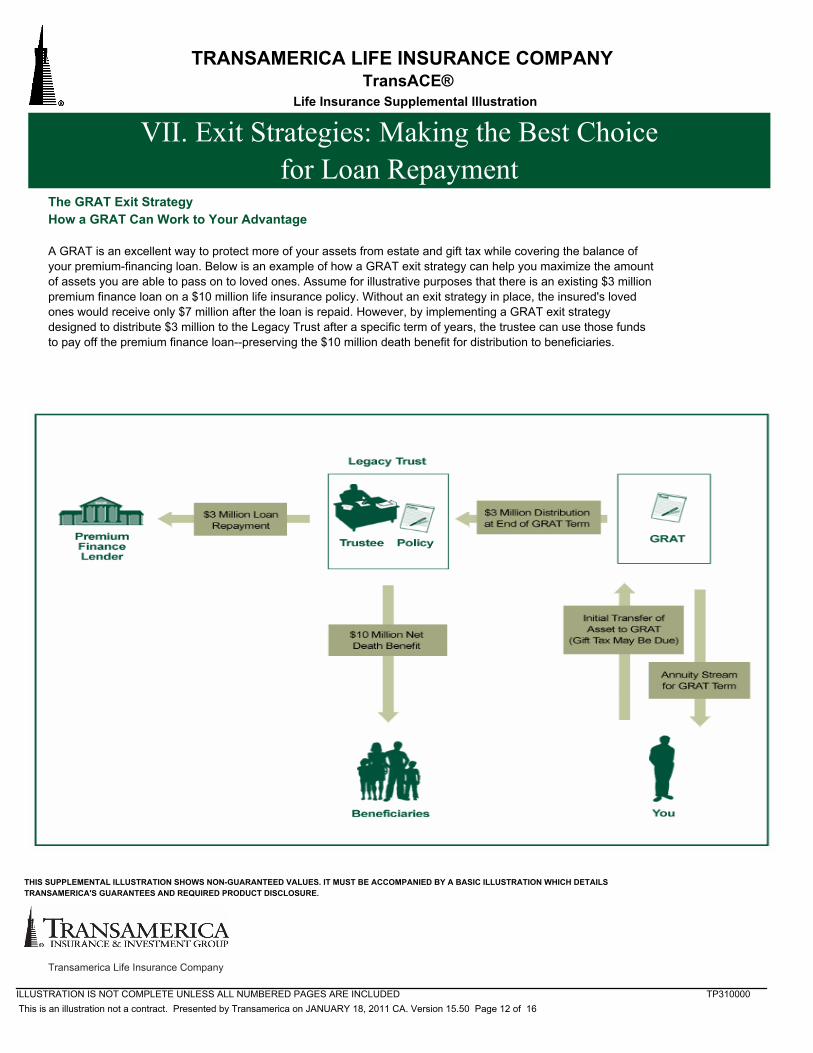

The GRAT Exit Strategy

How a GRAT Can Work to Your Advantage

A GRAT is an excellent way to protect more of your assets from estate and gift tax while covering the balance of

your premium-financing loan. Below is an example of how a GRAT exit strategy can help you maximize the amount

of assets you are able to pass on to loved ones. Assume for illustrative purposes that there is an existing $3 million

premium finance loan on a $10 million life insurance policy. Without an exit strategy in place, the insured's loved

ones would receive only $7 million after the loan is repaid. However, by implementing a GRAT exit strategy

designed to distribute $3 million to the Legacy Trust after a specific term of years, the trustee can use those funds

to pay off the premium finance loan--preserving the $10 million death benefit for distribution to beneficiaries.

VII. Exit Strategies: Making the Best Choice

for Loan Repayment

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 12 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

The Transamerica Advantage

Transamerica offers you not only outstanding expertise in the areas of premium-financed life insurance policies and

innovative estate planning, but also a reputation of strength and stability.

For over a century, Transamerica companies have been leading providers of insurance and investment products for

individuals and companies and have built a reputation on solid management, sound decisions and consumer

confidence. In 1999, Transamerica was acquired by AEGON, one of the world’s leading life insurance and pension

groups. With headquarters in The Hague, the Netherlands, AEGON’s businesses serve millions of customers

throughout the Americas, Europe and Asia.

For information about AEGON and Transamerica, please visit www.aegon.com and www.transamerica.com.

VIII. The Transamerica Advantage

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 13 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

IX. Frequently Asked Questions

1. What are the minimum financing requirements?

All premium finance lenders have their own set of requirements. Generally, the minimum annual premium for a financed

policy is $100,000. In addition, borrowers must meet a minimum net-worth requirement. Generally, a client’s total net

worth must exceed $5 million.

2. How does the collateral work?

Cash surrender value of a life insurance policy will always serve as primary collateral; however, you may be required to

make up any shortfall between the loan balance and the policy cash value by pledging other asset(s) as collateral.

Acceptable forms of collateral typically include cash, cash equivalents, publicly traded stock, other life insurance cash

values, letters of credit and personal guarantees.

3. What is the term of a premium-financing loan?

Premium financing loans are either annually renewable or fixed for a number of years. If the loan is for a fixed number of

years, rather than for the life of the insured, the lender will require the balance to be repaid at maturity if the loan is not

refinanced.

4. What interest rate will I be charged?

Interest rates vary according to lender. Generally, the interest rate is made up of two elements, an index and a spread.

The 12-month LIBOR (London Interbank Offered Rate) and the Prime Rate are commonly used indices. While both fixed

and variable interest loans are generally available, variable interest loans are more common.

5. Will I be required to pay interest?

Many lenders require that interest be paid annually, while other lenders will allow the borrower to accrue interest. Some

lenders may impose time restrictions on how long interest can be accrued (e.g., five years) and may set additional

financial requirements for the borrower (e.g., higher net worth or additional collateral requirements).

6. Is prepayment an option?

Some lenders impose a “breakage” fee for paying off the loan before the scheduled maturity date. It is important to check

with each lender regarding prepayment penalties.

7. Can a premium-financing loan ever be called?

Generally, lenders will only call a loan in the event of default, as defined by the loan documents. Some lenders do retain

the right to call the loan at any time if the financial condition of the borrower has deteriorated.

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 14 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

IX. Frequently Asked Questions

8. What types of life insurance products are typically financed? Why?

A universal life insurance policy with a no lapse guarantee is typically the best fit for premium financing. The reason for

this is that so long as premiums are paid the death benefit will be guaranteed regardless of the policy cash value. This

removes one of the potential risks involved with premium financing, policy crediting rate risk, which is the risk that cash

value may be less than anticipated due to a decrease in the currently assumed policy crediting rate. While cash value

is the primary collateral in a premium finance loan, any reduction to cash value while not impacting the death benefit will

require additional other collateral be posted by the insured. Typically, high-net-worth individuals buy a life insurance

policy to solve an estate liquidity problem. With a guaranteed product, high-net-worth individuals can eliminate variables

and ensure that their estate will have sufficient cash to pay any estate tax liability.

9. What are my options for repaying the loan premiums?

You may choose to repay the loan while still living, choose to have the premium be covered by the death benefits of the

life insurance policy, or choose to fund the premiums (and shield more of your income from gift tax) through an additional

trust known as a GRAT.

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 15 of 16

TransACE®

TRANSAMERICA LIFE INSURANCE COMPANY

Life Insurance Supplemental Illustration

The Full Policy Surrender Penalty Waiver Endorsement (Honeymoon Provision) waives company-imposed surrender

charges for a full surrender of a policy during the first five policy years. The Honeymoon Provision of a universal life

insurance policy may reduce the premium finance collateral requirements by substituting accumulated value for cash values

for policy years one through five. Surrender charges will continue to apply to partial surrenders, loan amounts, and face

reductions. The Honeymoon Provision is only available at issue on policies with a minimum required premium of $100,000

each year for five years.

TransACE® is a non-participating flexible-premium universal life insurance policy issued by Transamerica Life Insurance

Company, Cedar Rapids, IA 52499 (Policy Form #1-12611107 (CVAT), Group Certificate #2-72336107 (CVAT) for

certificates issued under a group policy issued to the Rhode Island National Consumer Protection Trust). Policy form and

number may vary, and this policy may not be available in all jurisdictions.

This material was not intended or written to be used, and cannot be used, to avoid penalties imposed under the Internal

Revenue Code. This material was written to support the promotion or marketing of the products, services, and/or concepts

addressed in this material. Anyone to whom this material is promoted, marketed, or recommended should consult with and

rely solely on their own independent advisors regarding their particular situation and the concepts presented here.

Transamerica Life Insurance Company (“Transamerica”), and its representatives do not give tax or legal advice. This

material and the concepts presented here are provided for informational purposes only and should not be construed as tax

or legal advice.

Discussions of the various planning strategies and issues are based on our understanding of the applicable federal income,

gift, and estate tax laws in effect at the time of publication. However, these laws are subject to interpretation and change,

and there is no guarantee that the relevant tax authorities will accept Transamerica’s interpretations. Additionally, the

information presented here does not consider the impact of applicable state laws upon clients and prospects.

Although care is taken in preparing this material and presenting it accurately, Transamerica disclaims any express or

implied warranty as to the accuracy of any material contained herein and any liability with respect to it. This information is

current as of December 2010.

X. Disclosures

OLA 2033 1210

THIS SUPPLEMENTAL ILLUSTRATION SHOWS NON-GUARANTEED VALUES. IT MUST BE ACCOMPANIED BY A BASIC ILLUSTRATION WHICH DETAILS

TRANSAMERICA'S GUARANTEES AND REQUIRED PRODUCT DISCLOSURE.

ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED TP310000

Transamerica Life Insurance Company

This is an illustration not a contract. Presented by Transamerica on JANUARY 18, 2011 CA. Version 15.50 Page 16 of 16

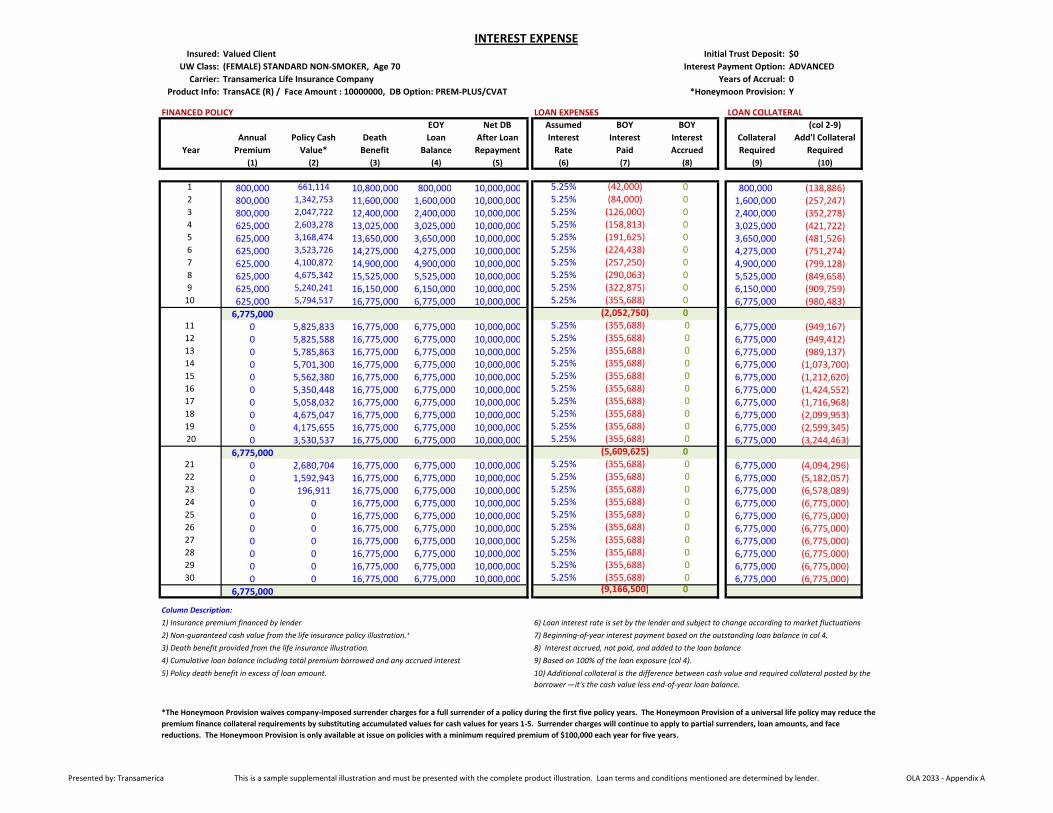

INTEREST EXPENSEValued Client Initial Trust Deposit: $0(FEMALE) STANDARD NON‐SMOKER, Age 70 Interest Payment Option: ADVANCEDTransamerica Life Insurance Company Years of Accrual: 0TransACE (R) / Face Amount : 10000000, DB Option: PREM‐PLUS/CVAT *Honeymoon Provision: Y

FINANCED POLICY LOAN EXPENSES LOAN COLLATERALEOY Net DB Assumed BOY BOY (col 2‐9)

Annual Policy Cash Death Loan After Loan Interest Interest Interest Collateral Add'l CollateralYear Premium Value* Benefit Balance Repayment Rate Paid Accrued Required Required

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 800,000 661,114 10,800,000 800,000 10,000,000 5.25% (42,000) 0 800,000 (138,886)2 800,000 1,342,753 11,600,000 1,600,000 10,000,000 5.25% (84,000) 0 1,600,000 (257,247)3 800,000 2,047,722 12,400,000 2,400,000 10,000,000 5.25% (126,000) 0 2,400,000 (352,278)4 625,000 2,603,278 13,025,000 3,025,000 10,000,000 5.25% (158,813) 0 3,025,000 (421,722)5 625,000 3,168,474 13,650,000 3,650,000 10,000,000 5.25% (191,625) 0 3,650,000 (481,526)6 625,000 3,523,726 14,275,000 4,275,000 10,000,000 5.25% (224,438) 0 4,275,000 (751,274)7 625,000 4,100,872 14,900,000 4,900,000 10,000,000 5.25% (257,250) 0 4,900,000 (799,128)8 625,000 4,675,342 15,525,000 5,525,000 10,000,000 5.25% (290,063) 0 5,525,000 (849,658)9 625,000 5,240,241 16,150,000 6,150,000 10,000,000 5.25% (322,875) 0 6,150,000 (909,759)10 625,000 5,794,517 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (980,483)

6,775,000 (2,052,750) 011 0 5,825,833 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (949,167)12 0 5,825,588 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (949,412)13 0 5,785,863 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (989,137)14 0 5,701,300 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (1,073,700)15 0 5,562,380 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (1,212,620)16 0 5,350,448 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (1,424,552)17 0 5,058,032 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (1,716,968)18 0 4,675,047 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (2,099,953)19 0 4,175,655 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (2,599,345)20 0 3,530,537 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (3,244,463)

6,775,000 (5,609,625) 021 0 2,680,704 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (4,094,296)22 0 1,592,943 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (5,182,057)23 0 196,911 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,578,089)24 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)25 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)26 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)27 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)28 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)29 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)30 0 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 6,775,000 (6,775,000)

6,775,000 (9,166,500) 0

1) Insurance premium financed by lender. 6) Loan interest rate is set by the lender and subject to change according to market fluctuations.

2) Non‐guaranteed cash value from the life insurance policy illustration.* 7) Beginning‐of‐year interest payment based on the outstanding loan balance in col 4.

3) Death benefit provided from the life insurance illustration. 8) Interest accrued, not paid, and added to the loan balance.

4) Cumulative loan balance including total premium borrowed and any accrued interest. 9) Based on 100% of the loan exposure (col 4).

5) Policy death benefit in excess of loan amount. 10) Additional collateral is the difference between cash value and required collateral posted by the borrower—it's the cash value less end‐of‐year loan balance.

*The Honeymoon Provision waives company‐imposed surrender charges for a full surrender of a policy during the first five policy years. The Honeymoon Provision of a universal life policy may reduce the premium finance collateral requirements by substituting accumulated values for cash values for years 1‐5. Surrender charges will continue to apply to partial surrenders, loan amounts, and face reductions. The Honeymoon Provision is only available at issue on policies with a minimum required premium of $100,000 each year for five years.

Insured:UW Class:

Carrier:Product Info:

Column Description:

Presented by: Transamerica This is a sample supplemental illustration and must be presented with the complete product illustration. Loan terms and conditions mentioned are determined by lender. OLA 2033 ‐ Appendix A

GIFT ‐ ANNUAL VS. INITIALValued Client Initial Trust Deposit: $0(FEMALE) STANDARD NON‐SMOKER, Age 70 Interest Payment Option: ADVANCEDTransamerica Life Insurance Company Years of Accrual: 0TransACE (R) / Face Amount : 10000000, DB Option: PREM‐PLUS/CVAT *Honeymoon Provision: Y

FINANCED POLICY ANNUAL GIFT INITIAL GIFT TO TRUSTAssumed BOY BOY EOY Annual Amount Gift Trust Account

Annual Interest Interest Interest Loan Gift of of With Growth WithdrawalYear Premium Rate Paid Accrued Balance Loan Interest Gift(s) At 0% to Pay Interest

(1) (2) (3) (4) (5) (6) (7) (8) (9)

1 800,000 5.25% (42,000) 0 800,000 (42,000) 0 0 02 800,000 5.25% (84,000) 0 1,600,000 (84,000) 0 0 03 800,000 5.25% (126,000) 0 2,400,000 (126,000) 0 0 04 625,000 5.25% (158,813) 0 3,025,000 (158,813) 0 0 05 625,000 5.25% (191,625) 0 3,650,000 (191,625) 0 0 06 625,000 5.25% (224,438) 0 4,275,000 (224,438) 0 0 07 625,000 5.25% (257,250) 0 4,900,000 (257,250) 0 0 08 625,000 5.25% (290,063) 0 5,525,000 (290,063) 0 0 09 625,000 5.25% (322,875) 0 6,150,000 (322,875) 0 0 010 625,000 5.25% (355,688) 0 6,775,000 (355,688) 0 0 0

6,775,000 (2,052,750) 0 (2,052,750) 011 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 012 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 013 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 014 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 015 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 016 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 017 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 018 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 019 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 020 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 0

6,775,000 (5,609,625) 0 (5,609,625) 021 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 022 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 023 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 024 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 025 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 026 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 027 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 028 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 029 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 030 0 5.25% (355,688) 0 6,775,000 (355,688) 0 0 0

6,775,000 (9,166,500) 0 (9,166,500) 0

1) Insurance premium financed by lender. 5) Cumulative loan balance including total premium borrowed and any accrued interest.2) Loan interest rate is set by lender and subject to change according to market fluctuations. 6) Annual gift of loan interest to trust.3) Beginning‐of‐year interest payment based on the outstanding loan balance in col 5. 7) Initial gift(s) to trust.4) Interest accrued, not paid, and added to the loan balance. 8) Trust growth with a hypothetical investment rate.

9) Trust account withdrawals to pay the loan interest.

*The Honeymoon Provision waives company‐imposed surrender charges for a full surrender of a policy during the first five policy years. The Honeymoon Provision of a universal life policy may reduce the premium finance collateral requirements by substituting accumulated values for cash values for years 1‐5. Surrender charges will continue to apply to partial surrenders, loan amounts, and face reductions. The Honeymoon Provision is only available at issue on policies with a minimum required premium of $100,000 each year for five years.

Insured:UW Class:

Carrier:Product Info:

Column Description:

Presented by: Transamerica This is a sample supplemental illustration and must be presented with the complete product illustration. Loan terms and conditions mentioned are determined by lender. OLA 2033 ‐ Appendix A

BENEFIT OF FINANCINGValued Client Initial Trust Deposit: $0(FEMALE) STANDARD NON‐SMOKER, Age 70 Interest Payment Option: ADVANCEDTransamerica Life Insurance Company Years of Accrual: 0TransACE (R) / Face Amount : 10000000, DB Option: PREM‐PLUS/CVAT *Honeymoon Provision: Y

FINANCED POLICY LOAN EXPENSES NON‐FINANCED POLICY SAVINGS DUE TO FINANCINGEOY Net DB Assumed BOY BOY Annual Cumulative

Annual Death Loan After Loan Interest Interest Interest Annual Death Cash Cash

Year Premium Benefit Balance Repayment Rate Paid Accrued Premium Benefit Savings Savings(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

1 800,000 10,800,000 800,000 10,000,000 5.25% (42,000) 0 289,135 10,000,000 247,135 247,1352 800,000 11,600,000 1,600,000 10,000,000 5.25% (84,000) 0 289,135 10,000,000 205,135 452,2703 800,000 12,400,000 2,400,000 10,000,000 5.25% (126,000) 0 289,135 10,000,000 163,135 615,4054 625,000 13,025,000 3,025,000 10,000,000 5.25% (158,813) 0 289,135 10,000,000 130,323 745,7285 625,000 13,650,000 3,650,000 10,000,000 5.25% (191,625) 0 289,135 10,000,000 97,510 843,2386 625,000 14,275,000 4,275,000 10,000,000 5.25% (224,438) 0 289,135 10,000,000 64,698 907,9357 625,000 14,900,000 4,900,000 10,000,000 5.25% (257,250) 0 289,135 10,000,000 31,885 939,8208 625,000 15,525,000 5,525,000 10,000,000 5.25% (290,063) 0 289,135 10,000,000 (928) 938,8939 625,000 16,150,000 6,150,000 10,000,000 5.25% (322,875) 0 289,135 10,000,000 (33,740) 905,15310 625,000 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 838,600

6,775,000 (2,052,750) 0 2,891,350 838,60011 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 772,04812 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 705,49513 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 638,94314 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 572,39015 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 505,83816 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 439,28517 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 372,73318 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 306,18019 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 239,62820 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 173,075

6,775,000 (5,609,625) 0 5,782,700 173,07521 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 106,52322 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) 39,97023 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (26,583)24 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (93,135)25 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (159,688)26 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (226,240)27 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (292,793)28 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (359,345)29 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (425,898)30 0 16,775,000 6,775,000 10,000,000 5.25% (355,688) 0 289,135 10,000,000 (66,553) (492,450)

6,775,000 (9,166,500) 0 8,674,050 (492,450)

6) Beginning of year interest payment based on the outstanding loan balance shown in col 3. 7) Interest accrued, not paid, and added to the loan balance.8) This premium maybe lower based on level death benefit option.9) Level death benefit of non‐financed insurance policy.

11) Cumulative cash flow comparison of out of pocket cost of paying premium to financing premium.

*The Honeymoon Provision waives company‐imposed surrender charges for a full surrender of a policy during the first five policy years. The Honeymoon Provision of a universal life policy may reduce the premium finance collateral requirements by substituting accumulated values for cash values for years 1‐5. Surrender charges will continue to apply to partial surrenders, loan amounts, and face reductions. The Honeymoon Provision is only available at issue on policies with a minimum required premium of $100,000 each year for five years.

1) Insurance premium financed by lender.

Insured:UW Class:

Carrier:Product Info:

Column Description:

2) Death benefit provided from life insurance policy illustration.3) Cumulative loan balance including total premium borrowed and any accrued interest.4) Net death benefit available after loan repayment.

5) Loan interest rate is set by the lender and subject to change according to market fluctuations. 10) Comparison of cash outlay between loan interest upon financing premium vs. non‐financing of annual premium. Col 6 lessCol 8.

Presented by: Transamerica This is a sample supplemental illustration and must be presented with the complete product illustration. Loan terms and conditions mentioned are determined by lender. OLA 2033 ‐ Appendix A

CAPITAL GROWTH DUE TO SAVINGSValued Client Initial Trust Deposit: $0(FEMALE) STANDARD NON‐SMOKER, Age 70 Interest Payment Option: ADVANCEDTransamerica Life Insurance Company Years of Accrual: 0TransACE (R) / Face Amount : 10000000, DB Option: PREM‐PLUS/CVAT *Honeymoon Provision: Y

FINANCED POLICY NON‐FINANCED POLICY CAPITAL GROWTH DUE TO SAVINGSEOY Assumed BOY BOY Net DB Annual Assumed Capital

Annual Loan Interest Interest Interest Death After Loan Annual Death Cash Investment GrowthYear Premium Balance Rate Paid Accrued Benefit Repayment Premium Benefit Savings Rate of Return Account

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

1 800,000 800,000 5.25% (42,000) 0 10,800,000 10,000,000 289,135 10,000,000 247,135 6.00% 261,9632 800,000 1,600,000 5.25% (84,000) 0 11,600,000 10,000,000 289,135 10,000,000 205,135 6.00% 495,1243 800,000 2,400,000 5.25% (126,000) 0 12,400,000 10,000,000 289,135 10,000,000 163,135 6.00% 697,7554 625,000 3,025,000 5.25% (158,813) 0 13,025,000 10,000,000 289,135 10,000,000 130,323 6.00% 877,7625 625,000 3,650,000 5.25% (191,625) 0 13,650,000 10,000,000 289,135 10,000,000 97,510 6.00% 1,033,7886 625,000 4,275,000 5.25% (224,438) 0 14,275,000 10,000,000 289,135 10,000,000 64,698 6.00% 1,164,3957 625,000 4,900,000 5.25% (257,250) 0 14,900,000 10,000,000 289,135 10,000,000 31,885 6.00% 1,268,0568 625,000 5,525,000 5.25% (290,063) 0 15,525,000 10,000,000 289,135 10,000,000 (928) 6.00% 1,343,1579 625,000 6,150,000 5.25% (322,875) 0 16,150,000 10,000,000 289,135 10,000,000 (33,740) 6.00% 1,387,98210 625,000 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,400,715

6,775,000 (2,052,750) 0 2,891,350 838,60011 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,414,21212 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,428,51913 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,443,68514 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,459,76015 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,476,80016 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,494,86217 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,514,00818 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,534,30319 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,555,81620 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,578,619

6,775,000 (5,609,625) 0 5,782,700 173,07521 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,602,79122 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,628,41223 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,655,57224 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,684,36025 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,714,87626 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,747,22327 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,781,51128 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,817,85629 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,856,38130 0 6,775,000 5.25% (355,688) 0 16,775,000 10,000,000 289,135 10,000,000 (66,553) 6.00% 1,897,219

6,775,000 (9,166,500) 0 8,674,050 (492,450)

Column Description:

1) Insurance premium financed by lender. 7) Net death benefit available after loan repayment.2) Cumulative loan balance including current year premium and any accrued interest. 8) This premium maybe lower based on level death benefit option.3) Loan interest rate is set by the lender and subject to change according to market fluctuations. 9) Level death benefit of non‐financed insurance policy.4) Beginning‐of‐year interest payment based on the outstanding loan balance shown in col 2. 10) Comparison of cash outlay between financing (loan interest) vs. non‐financing (annual premium). Col 4 minus Col 8.5) Interest accrued, not paid, and added to the loan balance. 11) The hypothetical investment growth rate.6) Death benefit provided from the life insurance policy illustration. 12) Cumulative annual cash savings from financing; the amount saved growing at the assumed rate under col 11.

Insured:UW Class:

Carrier:Product Info:

*The Honeymoon Provision waives company‐imposed surrender charges for a full surrender of a policy during the first five policy years. The Honeymoon Provision of a universal life policy may reduce the premium finance collateral requirements by substituting accumulated values for cash values for years 1‐5. Surrender charges will continue to apply to partial surrenders, loan amounts, and face reductions. The Honeymoon Provision is only available at issue on policies with a minimum required premium of $100,000 each year for five years.

Presented by: Transamerica This is a sample supplemental illustration and must be presented with the complete product illustration. Loan terms and conditions mentioned are determined by lender. OLA 2033 ‐ Appendix A

LOAN EXIT STRATEGYValued Client Initial Trust Deposit: $0(FEMALE) STANDARD NON‐SMOKER, Age 70 Interest Payment Option: ADVANCEDTransamerica Life Insurance Company Years of Accrual: 0TransACE (R) / Face Amount : 10000000, DB Option: PREM‐PLUS/CVAT *Honeymoon Provision: Y

EOY Net DB EOY Loan EOY Loan GRAT Loan Annual Policy Cash Death Loan After Loan Repaid From Repaid From Distribution Repayment GRAT Term: 0%

Year Premium Value* Benefit Balance Repayment Policy Values Other Source to Trust From GRAT Initial Deposit: $0(1) (2) (3) (4) (5) (6) (7) (8) (9) Taxable Gift: $0

Growth Rate: 0.00%1 800,000 661,114 10,800,000 800,000 10,000,000 0 0 0 Annual Pymt: $02 800,000 1,342,753 11,600,000 1,600,000 10,000,000 0 0 0 Remainder: $03 800,000 2,047,722 12,400,000 2,400,000 10,000,000 0 0 04 625,000 2,603,278 13,025,000 3,025,000 10,000,000 0 0 05 625,000 3,168,474 13,650,000 3,650,000 10,000,000 0 0 06 625,000 3,523,726 14,275,000 4,275,000 10,000,000 0 0 07 625,000 4,100,872 14,900,000 4,900,000 10,000,000 0 0 08 625,000 4,675,342 15,525,000 5,525,000 10,000,000 0 0 09 625,000 5,240,241 16,150,000 6,150,000 10,000,000 0 0 010 625,000 5,794,517 16,775,000 6,775,000 10,000,000 0 0 0

6,775,00011 0 5,825,833 16,775,000 6,775,000 10,000,000 0 0 012 0 5,825,588 16,775,000 6,775,000 10,000,000 0 0 013 0 5,785,863 16,775,000 6,775,000 10,000,000 0 0 014 0 5,701,300 16,775,000 6,775,000 10,000,000 0 0 015 0 5,562,380 16,775,000 6,775,000 10,000,000 0 0 016 0 5,350,448 16,775,000 6,775,000 10,000,000 0 0 017 0 5,058,032 16,775,000 6,775,000 10,000,000 0 0 018 0 4,675,047 16,775,000 6,775,000 10,000,000 0 0 0

GRAT SNAPSHOT

Insured:UW Class:Carrier:

Product Info:

FINANCED POLICY LOAN REPAYMENT STRATEGIES

19 0 4,175,655 16,775,000 6,775,000 10,000,000 0 0 020 0 3,530,537 16,775,000 6,775,000 10,000,000 0 0 0

6,775,00021 0 2,680,704 16,775,000 6,775,000 10,000,000 0 0 022 0 1,592,943 16,775,000 6,775,000 10,000,000 0 0 023 0 196,911 16,775,000 6,775,000 10,000,000 0 0 024 0 0 16,775,000 6,775,000 10,000,000 0 0 025 0 0 16,775,000 6,775,000 10,000,000 0 0 026 0 0 16,775,000 6,775,000 10,000,000 0 0 027 0 0 16,775,000 6,775,000 10,000,000 0 0 028 0 0 16,775,000 6,775,000 10,000,000 0 0 029 0 0 16,775,000 6,775,000 10,000,000 0 0 030 0 0 16,775,000 6,775,000 10,000,000 0 0 0

6,775,000

*The Honeymoon Provision waives company‐imposed surrender charges for a full surrender of a policy during the first five policy years. The Honeymoon Provision of a universal life policy may reduce the premium finance collateral requirements by substituting accumulated values for cash values for years 1‐5. Surrender charges will continue to apply to partial surrenders, loan amounts, and face reductions. The Honeymoon Provision is only available at issue on policies with a minimum required premium of $100,000 each year for five years.

Column Descriptions:1) Insurance premium financed by lender.2) Non‐guaranteed cash value from the life insurance illustration.3) Death benefit provided from the life insurance policy illustration.4) Cumulative loan balance including total premium borrowed and any accrued interest.5) Policy death benefit in excess of loan repayment.

6) Loan repayment from policy cash value withdrawal, if applicable.7) Loan repayment from outside source, if applicable.8) GRAT proceeds transfer to trust at the end of the GRAT term, if applicable.9) Loan repaid from Grantor Retained Annuity Trust (GRAT), if applicable.

Presented by: Transamerica This is a sample supplemental illustration and must be presented with the complete product illustration. Loan terms and conditions mentioned are determined by lender. OLA 2033 ‐ Appendix A

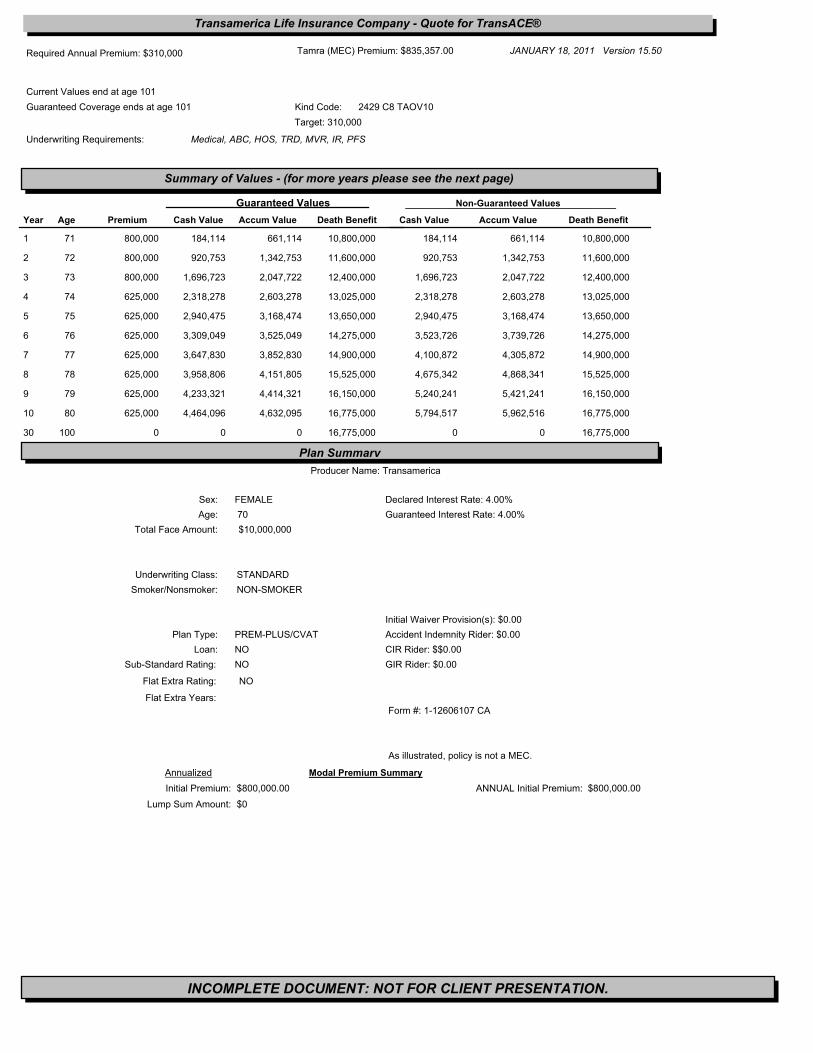

Kind Code: 2429 C8 TAOV10

Medical, ABC, HOS, TRD, MVR, IR, PFS

Tamra (MEC) Premium: $835,357.00Required Annual Premium: $310,000

Current Values end at age 101

Guaranteed Coverage ends at age 101

Transamerica Life Insurance Company - Quote for TransACE®

Underwriting Requirements:

Target: 310,000

JANUARY 18, 2011 Version 15.50

AgeYear Cash Value Death BenefitCash Value Accum Value Death Benefit

Summary of Values - (for more years please see the next page)

Premium

Guaranteed Values Non-Guaranteed Values____________________________________

Accum Value

71 800,0001 10,800,000 10,800,000661,114661,114184,114 184,114

72 800,0002 11,600,000 11,600,0001,342,7531,342,753920,753 920,753

73 800,0003 12,400,000 12,400,0002,047,7222,047,7221,696,723 1,696,723

74 625,0004 13,025,000 13,025,0002,603,2782,603,2782,318,278 2,318,278

75 625,0005 13,650,000 13,650,0003,168,4743,168,4742,940,475 2,940,475

76 625,0006 14,275,000 14,275,0003,739,7263,525,0493,309,049 3,523,726

77 625,0007 14,900,000 14,900,0004,305,8723,852,8303,647,830 4,100,872

78 625,0008 15,525,000 15,525,0004,868,3414,151,8053,958,806 4,675,342

79 625,0009 16,150,000 16,150,0005,421,2414,414,3214,233,321 5,240,241

80 625,00010 16,775,000 16,775,0005,962,5164,632,0954,464,096 5,794,517

100 030 16,775,000 16,775,000000 0

Plan Summary

Sex: FEMALE

Age: 70

Smoker/Nonsmoker: NON-SMOKER

Underwriting Class: STANDARD

Plan Type: PREM-PLUS/CVAT

Loan: NO

NO

NO

Declared Interest Rate: 4.00%

Guaranteed Interest Rate: 4.00%

Initial Waiver Provision(s): $0.00

Accident Indemnity Rider: $0.00

CIR Rider: $$0.00

GIR Rider: $0.00

Modal Premium SummaryAnnualized

Initial Premium: $800,000.00

Lump Sum Amount: $0

$800,000.00

Sub-Standard Rating:

Flat Extra Rating:

Flat Extra Years:

Producer Name: Transamerica

Form #: 1-12606107 CA

Total Face Amount:

ANNUAL Initial Premium:

As illustrated, policy is not a MEC.

$10,000,000

INCOMPLETE DOCUMENT: NOT FOR CLIENT PRESENTATION.

Annual

Premium

Annual

Withdrawal

Non-Guar.

Interest

Rate

Cash

Values

Accumulation

Values

Death

BenefitYear Age

Cash

Values

Death

Benefit

Transamerica Life Insurance Company - Quote for TransACE®

Values Calculated at Guaranteed

Rates

Values Calculated at Non

Guaranteed Rates

Accumulation

Values

4.00 800,000 71 1 0 661,114 10,800,000 184,114 661,114 10,800,000 184,114

& 4.00 800,000 72 2 0 1,342,753 11,600,000 920,753 1,342,753 11,600,000 920,753

& 4.00 800,000 73 3 0 2,047,722 12,400,000 1,696,723 2,047,722 12,400,000 1,696,723

& 4.00 625,000 74 4 0 2,603,278 13,025,000 2,318,278 2,603,278 13,025,000 2,318,278

& 4.00 625,000 75 5 0 3,168,474 13,650,000 2,940,475 3,168,474 13,650,000 2,940,475

3,650,000SUBTOTAL 0

& 4.00 625,000 76 6 0 3,525,049 14,275,000 3,523,726 3,739,726 14,275,000 3,309,049

4.00 625,000 77 7 0 3,852,830 14,900,000 4,100,872 4,305,872 14,900,000 3,647,830

4.00 625,000 78 8 0 4,151,805 15,525,000 4,675,342 4,868,341 15,525,000 3,958,806

4.00 625,000 79 9 0 4,414,321 16,150,000 5,240,241 5,421,241 16,150,000 4,233,321

4.00 625,000 80 10 0 4,632,095 16,775,000 5,794,517 5,962,516 16,775,000 4,464,096

6,775,000SUBTOTAL 0

4.00 0 81 11 0 4,190,453 16,775,000 5,825,833 5,981,833 16,775,000 4,034,453

4.00 0 82 12 0 3,642,314 16,775,000 5,825,588 5,967,587 16,775,000 3,500,315

4.00 0 83 13 0 2,962,872 16,775,000 5,785,863 5,914,862 16,775,000 2,833,873

4.00 0 84 14 0 2,131,456 16,775,000 5,701,300 5,816,300 16,775,000 2,016,456

4.00 0 85 15 0 1,112,595 16,775,000 5,562,380 5,662,380 16,775,000 1,012,595

6,775,000SUBTOTAL 0

A 4.00 0 86 16 0 0 16,775,000 5,350,448 5,433,448 16,775,000 0

A 4.00 0 87 17 0 0 16,775,000 5,058,032 5,124,031 16,775,000 0

A 4.00 0 88 18 0 0 16,775,000 4,675,047 4,722,046 16,775,000 0

A 4.00 0 89 19 0 0 16,775,000 4,175,655 4,200,655 16,775,000 0

A 4.00 0 90 20 0 0 16,775,000 3,530,537 3,530,537 16,775,000 0

6,775,000SUBTOTAL 0

A 4.00 0 91 21 0 0 16,775,000 2,680,704 2,680,704 16,775,000 0

A 4.00 0 92 22 0 0 16,775,000 1,592,943 1,592,943 16,775,000 0

A 4.00 0 93 23 0 0 16,775,000 196,911 196,911 16,775,000 0

A A 4.00 0 94 24 0 0 16,775,000 0 0 16,775,000 0

A A 4.00 0 95 25 0 0 16,775,000 0 0 16,775,000 0

6,775,000SUBTOTAL 0

A A 4.00 0 96 26 0 0 16,775,000 0 0 16,775,000 0

A A 4.00 0 97 27 0 0 16,775,000 0 0 16,775,000 0

A A 4.00 0 98 28 0 0 16,775,000 0 0 16,775,000 0

A A 4.00 0 99 29 0 0 16,775,000 0 0 16,775,000 0

A A 4.00 0 100 30 0 0 16,775,000 0 0 16,775,000 0

6,775,000SUBTOTAL 0

INCOMPLETE DOCUMENT: NOT FOR CLIENT PRESENTATION.