PPT Currencies

43

Welcome to the world of currencies

-

Upload

ankush-shrivastava -

Category

Documents

-

view

245 -

download

6

Transcript of PPT Currencies

Welcome to the

world of currencies

What is a currency?

• A generally accepted medium of exchange for goods and services, issued by a government and circulated within an economy.

World currencies

• Different countries have different currencies.

What is currency exchange rate?

• Each currency of a country is valued with other currency, the net ratio is called exchange rate.

Currency exchange rates

• Each currency exchange rate represents a pair of currency.

• Examples of currency pairs: USD/INR - US Dollar against Indian Rupee

EUR/USD - Euro against US Dollar

EUR/GBP - Euro against British Pound

GBP/INR - British Pound against Indian Rupee

How is currency quoted?

• Each currency is quoted/paired/valued with another currency.

• Quote of USD/INR = 55.60 means for every 1 USD paid, INR 55.60 will be received.

• Quote of EUR/USD = 1.2745 means for every 1 Euro paid, 1.2745 USD will be received.

USD/INR = 55.60

Base currency Quote currency

Understanding appreciation & depreciation of currency

• How valuation of rupee changes?

$`

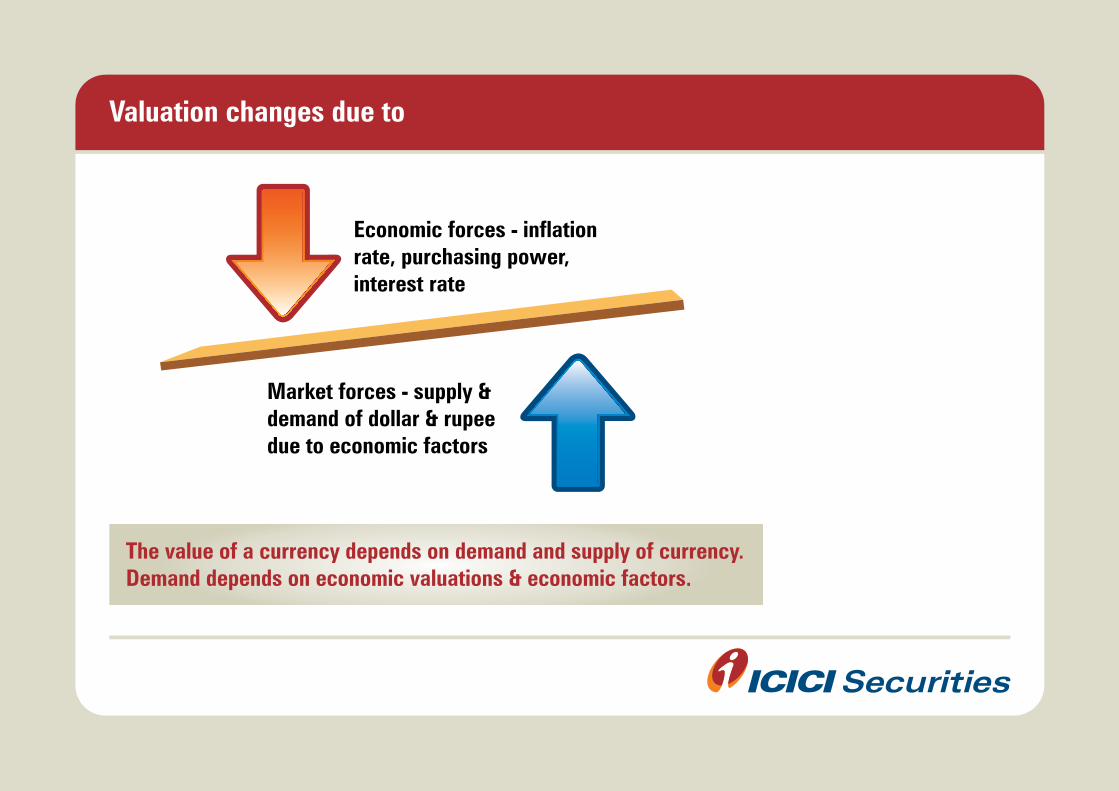

Valuation changes due to

The value of a currency depends on demand and supply of currency. Demand depends on economic valuations & economic factors.

Economic forces - inflationrate, purchasing power,interest rate

Market forces - supply &demand of dollar & rupeedue to economic factors

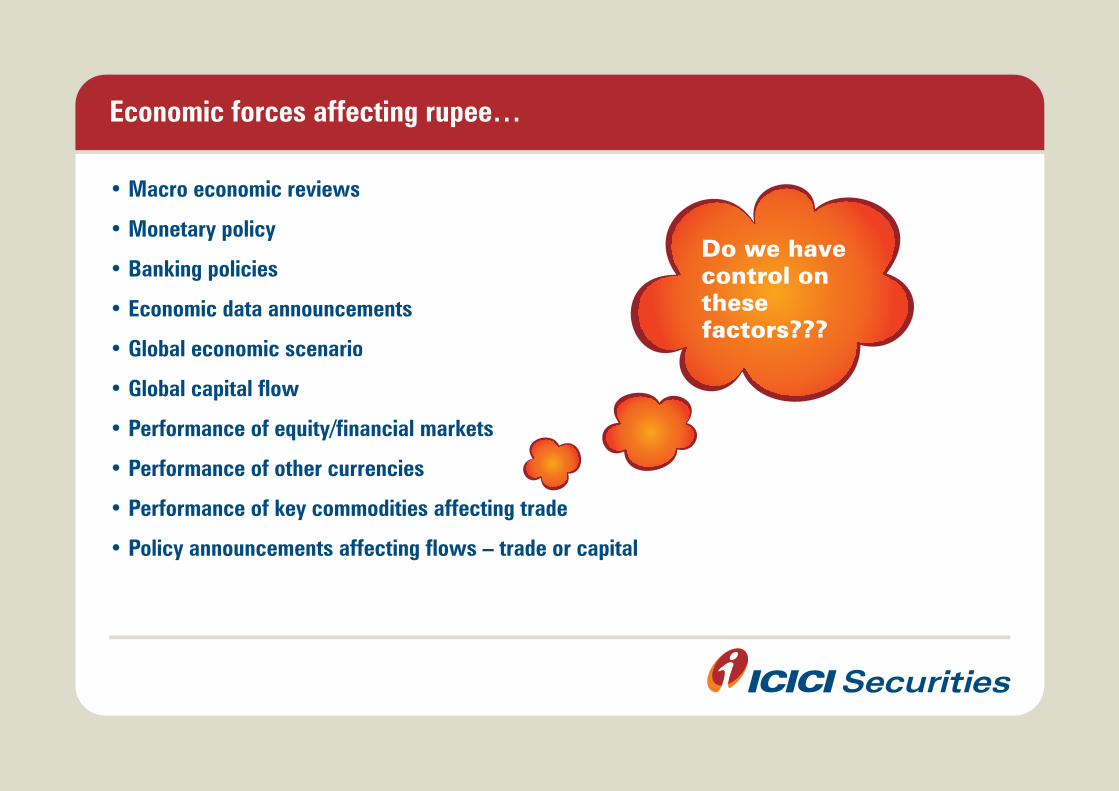

Economic forces affecting rupee…

• Macro economic reviews

• Monetary policy

• Banking policies

• Economic data announcements

• Global economic scenario

• Global capital flow

• Performance of equity/financial markets

• Performance of other currencies

• Performance of key commodities affecting trade

• Policy announcements affecting flows – trade or capital

ws

cements

rio

Do we havecontrol onthesefactors???

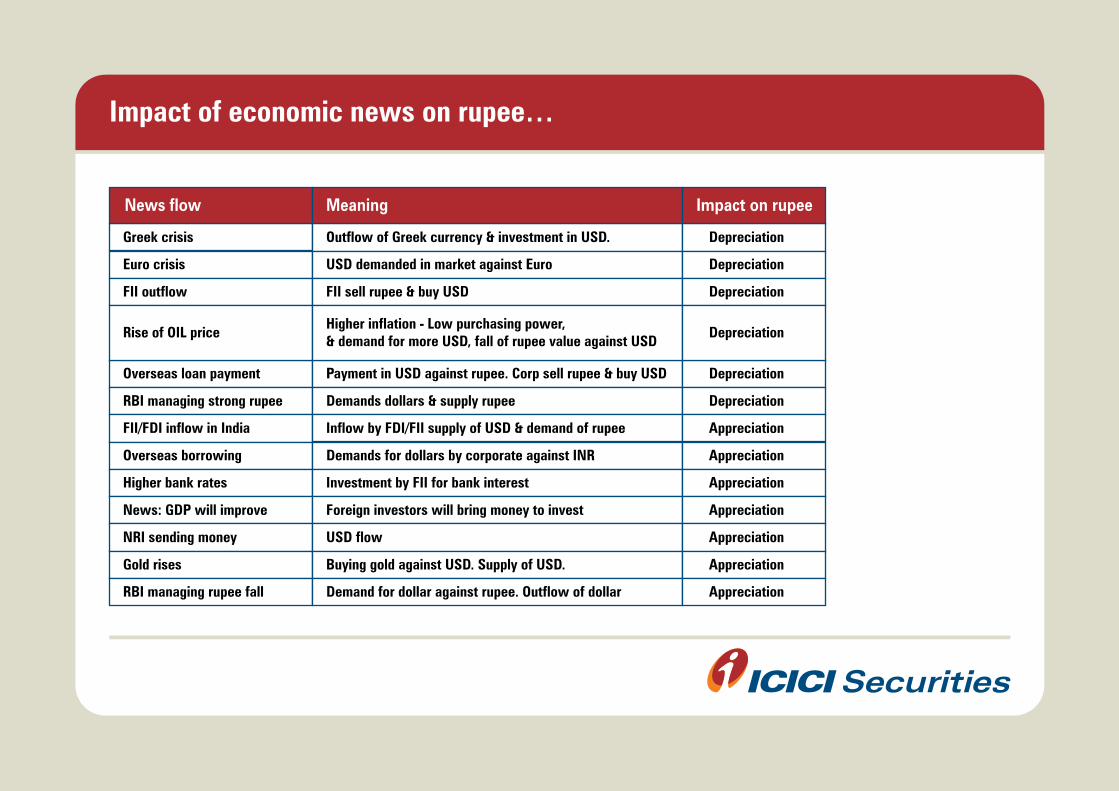

Impact of economic news on rupee…

News flow Meaning Impact on rupee

Greek crisis Depreciation

Depreciation

Depreciation

Depreciation

Depreciation

Depreciation

Appreciation

Appreciation

Appreciation

Appreciation

Appreciation

Appreciation

Appreciation

Euro crisis

FII outflow

Rise of OIL price

Overseas loan payment

RBI managing strong rupee

FII/FDI inflow in India

Overseas borrowing

Higher bank rates

News: GDP will improve

NRI sending money

Gold rises

RBI managing rupee fall

Outflow of Greek currency & investment in USD.

USD demanded in market against Euro

FII sell rupee & buy USD

Payment in USD against rupee. Corp sell rupee & buy USD

Demands dollars & supply rupee

Inflow by FDI/FII supply of USD & demand of rupee

Demands for dollars by corporate against INR

Demand for dollar against rupee. Outflow of dollar

Investment by FII for bank interest

Foreign investors will bring money to invest

USD flow

Buying gold against USD. Supply of USD.

Higher inflation - Low purchasing power, & demand for more USD, fall of rupee value against USD

How is change in currency rate a financial risk?

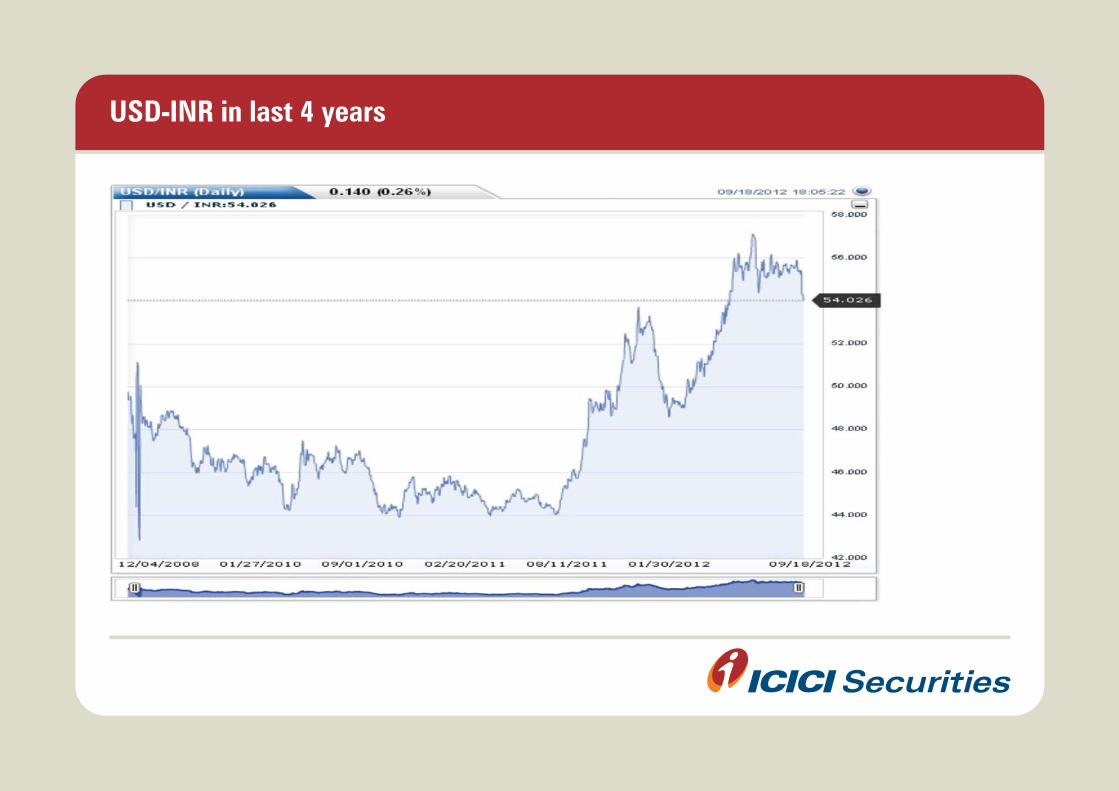

USD-INR in last 4 years

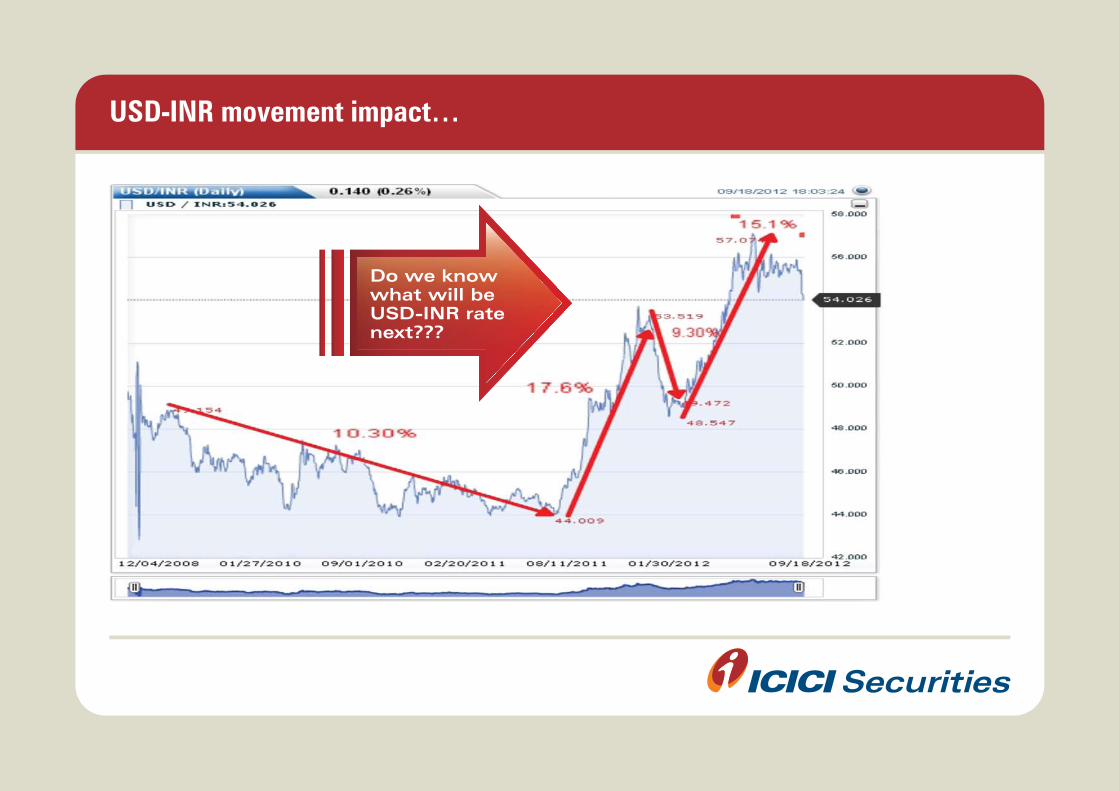

USD-INR movement impact…

Do we knowwhat will be USD-INR ratenext???

What is currency risk?

When rise or fall in value of one currency against another currency has direct

or indirect impact on financial statements, it is a currency risk.

When is currency a risk?

• Currency risk occurs when

- transactions undertaken by entity involves international currencies.

- rate of exchange has direct or indirect impact on its financial statements.

• Transactions may be

- receivable or payable fx instruments.

- purchase/sale commitments in fx.

- future transactions in a foreign currency.

- speculative transactions.

Who is affected by currency market?

Corporate, exporters, importers, governments, central & other banks,

financial markets, individuals - travellers, students

How is exchange rate a financial risk?

• Mr. ABC is an exporter and has to receive USD 5 million as payment for his exported

goods next month. If today USD-INR rate is 55.60, Mr. ABC is expecting to receive

INR 27.8 Crs. (5*10^6*55.60 = 27.8 Cr).

• By the time of payment delivery, if USD-INR moves to 57.30, Mr. ABC will receive

INR 28.65 Cr. He will gain additional INR 0.85 Cr.

• In a situation, USD-INR changes to 53.50 at the time of delivery, Mr. ABC will receive

INR 26.75 Cr. A loss of INR 1.05 Cr.

• In above situations, Mr. ABC will hugely gain or lose basis exchange rate

movement in USD-INR, for which he has no control.

How is currency a risk – more examples...

• Mr. XYZ imports goods. He is expecting delivery of his contract next month and has to

pay USD 10 million at the time of goods delivered.

• If today USD-INR rate is 55.60, XYZ has to pay INR 55.60 Cr. (10*10^6*55.60 = 55.6 Cr).

• By the time of payment, if USD-INR moves to 57.30, Mr. XYZ will have to pay INR 57.30

Cr. He will have to pay additional INR 1.70 Cr.

• In a situation, USD-INR changes to 53.50 at the time of delivery, Mr. XYZ will have to pay

INR 53.50 Cr. A gain of INR 2.10 Cr.

• In above situations, Mr. XYZ will gain or lose basis exchange rate movement in

USD-INR, for which he has no control.

Some more situations -

• Anjali Jewellers is importing 100 KG of Gold, worth INR 30 Cr from US.

• Ruchi Soya has entered in a contract to export Soya Oil to US worth INR 20,000 Cr next year.

• Indian importer ABC partners has deposited USD 5 Million as refundable guarantee deposit

to tie up with US Company for 5 Years.

• Same ABC partners is sourcing business from US every month worth INR 25 Cr every year.

• Indo-Call runs 1000-seat BPO in India and US. Receives $100 per day as servicing fee.

• What happens if the INR depreciates against USD - rate moves from $50 to &52 in a month

And the fx risks -

• Anjali Jewellers’ operating profit falls with Rs 1.2 Cr every month.

• Ruchi Soya’s net income rises by 800 Cr a year.

• ABC partners will receive INR 10 Million extra on conversion of his deposit.

• Same ABC partners’ profit for the year increases to 1Cr for the year.

• Indo-Call receives Rs 60 Lakh additional gain each month.

Problem - currency exposure risk solution - hedging

Problem -

• Firms involved in international transactions face a risk, an unknown gain/loss,

on account of unanticipated changes in exchange rates.

• These transactions are quantified in terms of ‘international exposure’.

• Un-hedged exposures adversely affects P&L of companies and creates

operational hitches like cash flow requirements etc.

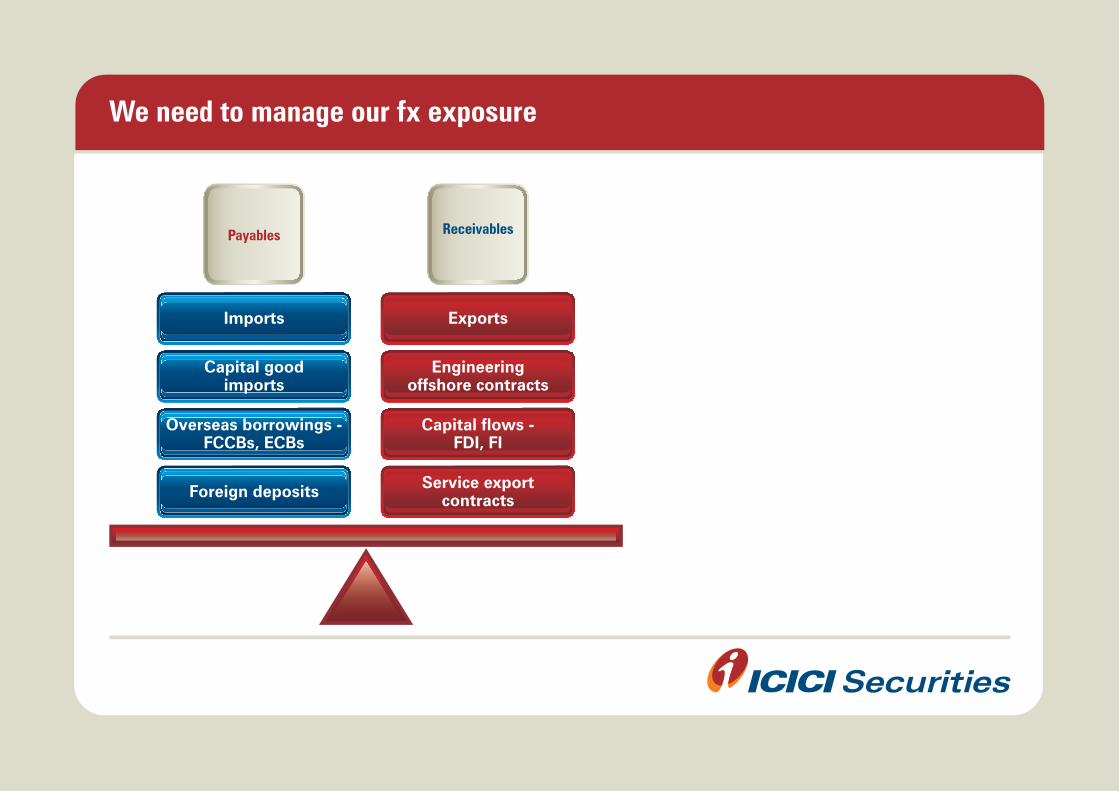

We need to manage our fx exposure

Foreign deposits

Overseas borrowings -FCCBs, ECBs

Capital goodimports

Imports Exports

Service exportcontracts

Capital flows -FDI, FI

Engineeringoffshore contracts

Payables Receivables

Solution on fx risk - hedging

• Hedging is a position established in one market in an attempt to offset

exposure in some opposite position in another market.

• The goal is to minimize one's exposure to unwanted risk.

• Hedging is thus taking of a position, either acquiring a cash flow or an asset

or a contract(including a forward contract) that will rise(fall) in value to

offset a fall(rise) in value of an existing position.

What is hedging – overview & concept?

• Hedging is a position established in one market in an attempt to offset

exposure in some opposite position in another market.

• The goal is to minimize one's exposure to unwanted risk.

• Hedging is thus taking of a position, either acquiring a cash flow or an asset

or a contract(including a forward contract) that will rise(fall) in value to

offset a fall(rise) in value of an existing position.

Keeping it simple - how to hedge?

Forex receivable Forex payable

• Short/Sell futures • Long/Buy futures

Cost of hedging & management of hedge

• Set price for transacting a foreign currency in the future

• Hedge forex exposure

• Cost to “lock in” this exchange rate

- margin deposits

- premium related to future rate for currency

- brokerage fee to obtain contract

- mark to market cash flow

- net settlement cash flow

Problem - Currency Exposure Risk

Solution - Hedging

Best Tool - Currency Derivatives

Problem - currency exposure risk

Solution - hedging

Best Tool - currency derivatives

What are currency derivatives?

• The term 'Derivatives' indicates it derives its value from some underlying i.e. it has

no independent value. Underlying can be securities, stock market index,

commodities, bullion, currency etc.

• Currency derivatives implies contracts where underlying would be the currency

exchange rate.

• Examples of currency trading pairs:

- USD-INR – US Dollar against Indian Rupee

- USD-EUR – US Dollar against Euro

- EUR-GBP – Euro against British Pound

Currency derivatives @ ICICIdirect.com

Currency trading @ ICICIdirect.com

• Products offered

- 4 currency pairs

• USD-INR – 6 month forward contracts available for trading

• GBP-INR – 3 month forward contracts available for trading

• EUR-INR - 3 month forward contracts available for trading

• JPY-INR – 2 month forward contracts available for trading

- Only futures

- Option trading not available

• Trading screens

- Online through web-trading

- Call n trade facility

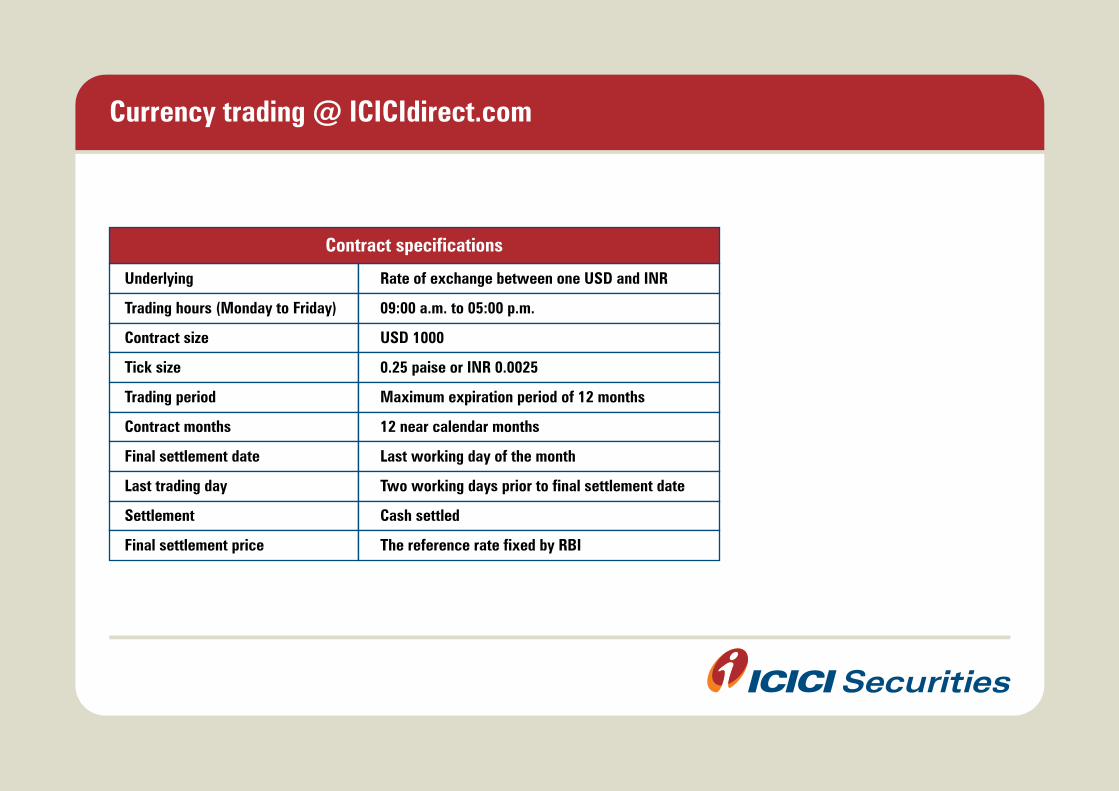

Currency trading @ ICICIdirect.com

Underlying

Trading hours (Monday to Friday)

Contract size

Tick size

Trading period

Contract months

Final settlement date

Last trading day

Settlement

Final settlement price

Rate of exchange between one USD and INR

09:00 a.m. to 05:00 p.m.

USD 1000

0.25 paise or INR 0.0025

Maximum expiration period of 12 months

12 near calendar months

Last working day of the month

Two working days prior to final settlement date

Cash settled

The reference rate fixed by RBI

Contract specifications

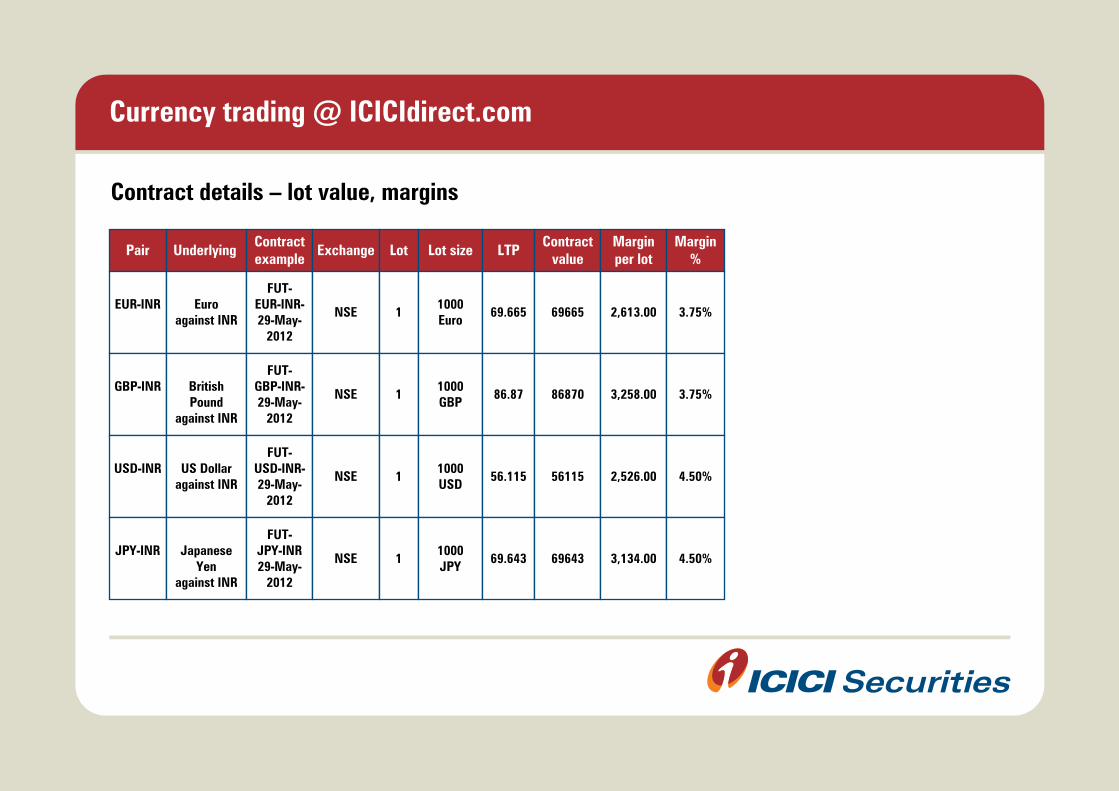

Currency trading @ ICICIdirect.com

Contract details – lot value, margins

Pair UnderlyingContractexample

Contractvalue

Marginper lot

Margin%

Exchange Lot Lot size LTP

NSEEuro

against INREUR-INR

11000Euro

FUT-EUR-INR-29-May-

2012

69.665 69665 2,613.00 3.75%

NSEBritishPound

against INR

GBP-INR1

1000GBP

FUT-GBP-INR-29-May-

2012

86.87 86870 3,258.00 3.75%

NSEUS Dollar

against INRUSD-INR

11000USD

FUT-USD-INR-29-May-

2012

56.115 56115 2,526.00 4.50%

NSEJapanese

Yenagainst INR

JPY-INR1

1000JPY

FUT-JPY-INR29-May-

2012

69.643 69643 3,134.00 4.50%

Equity Currency

Derivatives

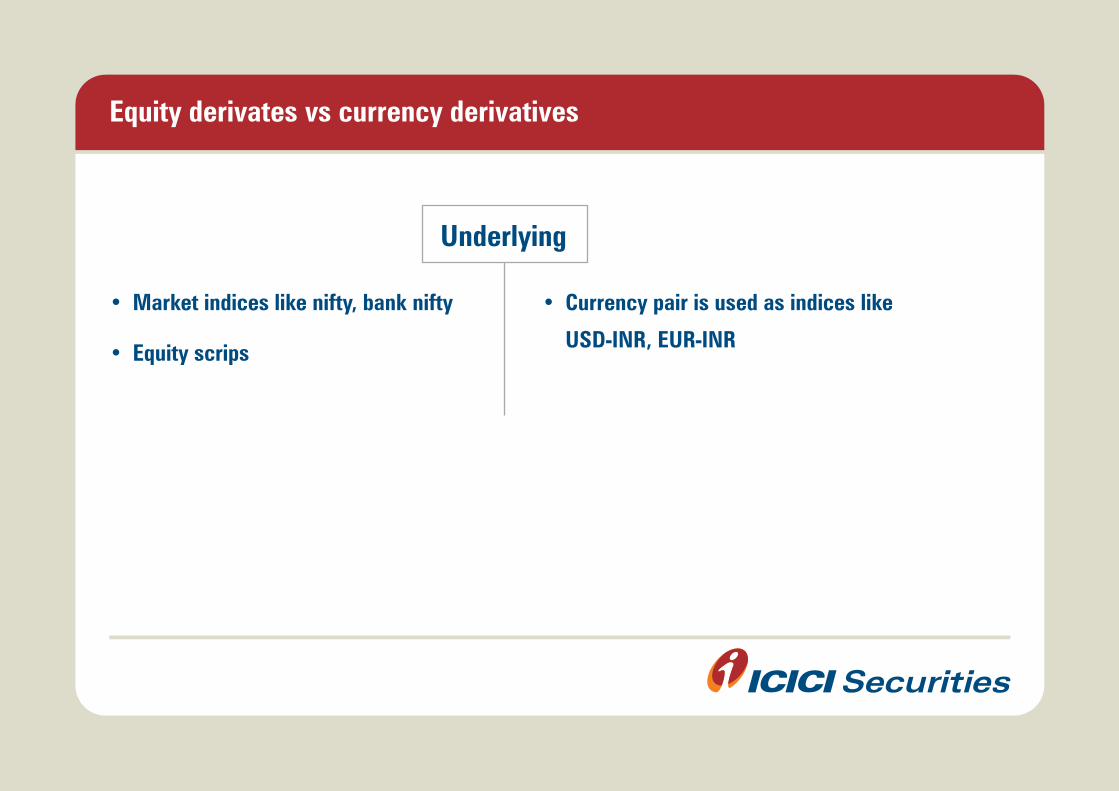

Equity derivates vs currency derivatives

• Market indices like nifty, bank nifty

• Equity scrips

• Currency pair is used as indices like

USD-INR, EUR-INR

Underlying

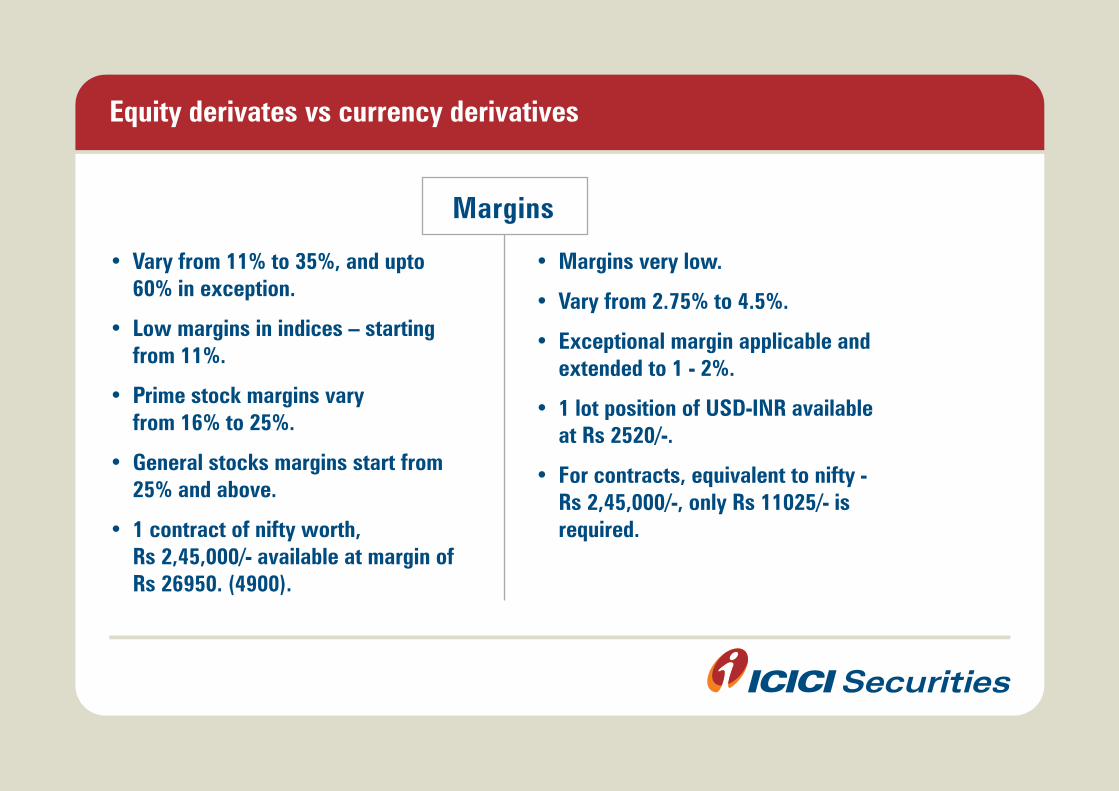

Equity derivates vs currency derivatives

Margins

• Vary from 11% to 35%, and upto 60% in exception.

• Low margins in indices – starting from 11%.

• Prime stock margins vary from 16% to 25%.

• General stocks margins start from 25% and above.

• 1 contract of nifty worth, Rs 2,45,000/- available at margin of Rs 26950. (4900).

• Margins very low.

• Vary from 2.75% to 4.5%.

• Exceptional margin applicable and extended to 1 - 2%.

• 1 lot position of USD-INR available at Rs 2520/-.

• For contracts, equivalent to nifty - Rs 2,45,000/-, only Rs 11025/- is required.

Equity derivates vs currency derivatives

Lot size

• Lot size is based on contract value.

• Standard value set by NSE is Rs 2.5 Lakhs.

• Number of units in lot vary as per market price of scrip at the time of initiating the contract by NSE.

• Lot size is based on number of units of underlying in contract.

• Standard is 1000 Units of currency.

• Lot value is not the set standard.

Equity derivates vs currency derivatives

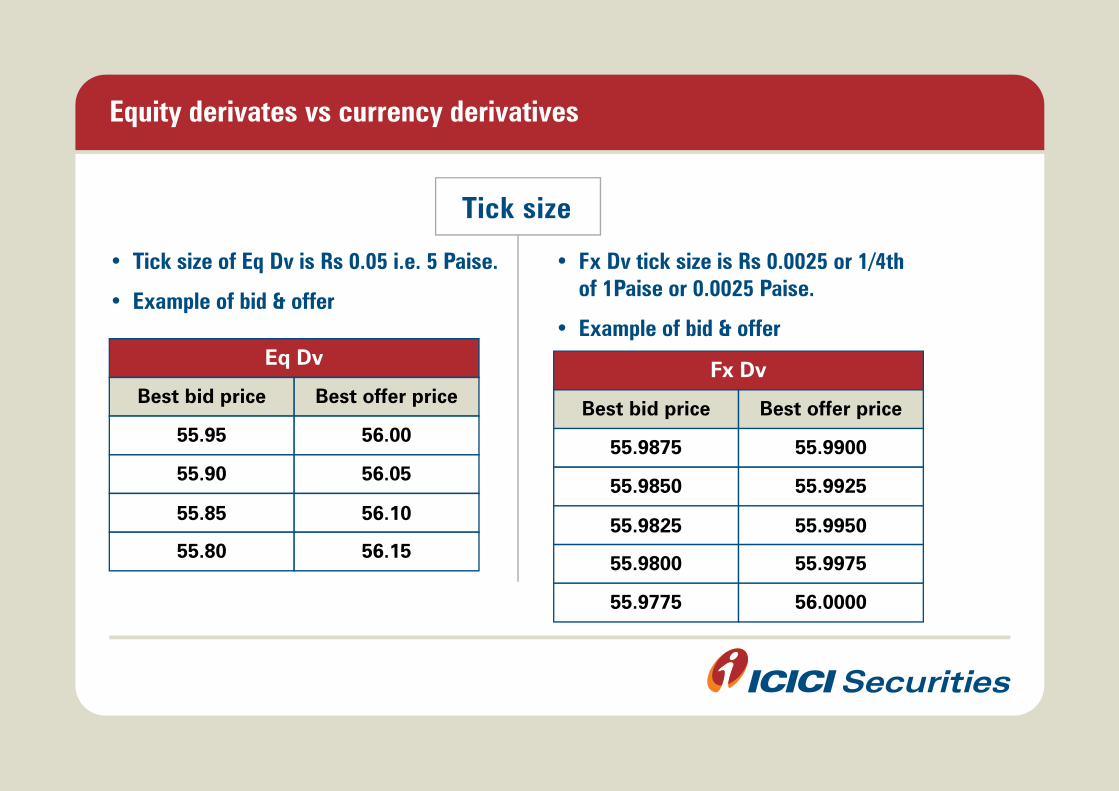

Tick size

• Tick size of Eq Dv is Rs 0.05 i.e. 5 Paise.

• Example of bid & offer

• Fx Dv tick size is Rs 0.0025 or 1/4th of 1Paise or 0.0025 Paise.

• Example of bid & offerEq Dv

Best bid price Best offer price

55.95 56.00

55.90 56.05

55.85 56.10

55.80 56.15

Fx Dv

Best bid price Best offer price

55.9875 55.9900

55.9850 55.9925

55.9825 55.9950

55.9800 55.9975

55.9775 56.0000

Equity derivates Vs currency derivatives

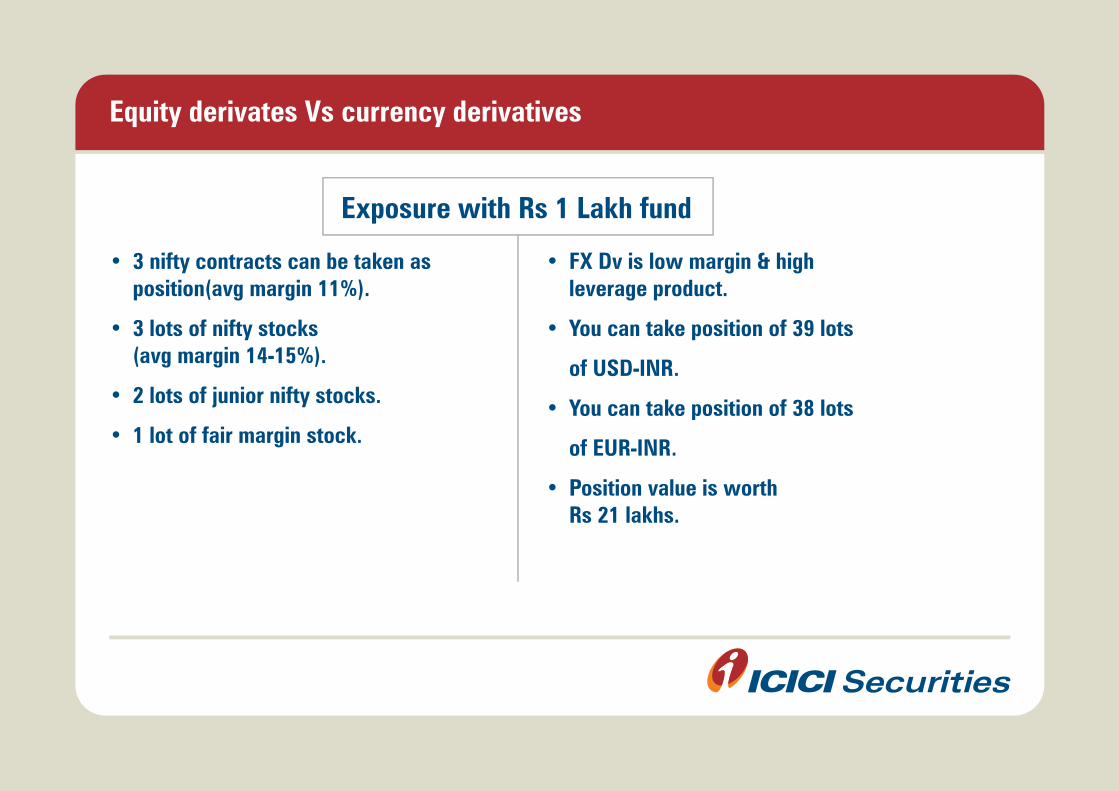

Exposure with Rs 1 Lakh fund

• 3 nifty contracts can be taken as position(avg margin 11%).

• 3 lots of nifty stocks (avg margin 14-15%).

• 2 lots of junior nifty stocks.

• 1 lot of fair margin stock.

• FX Dv is low margin & high leverage product.

• You can take position of 39 lots

of USD-INR.

• You can take position of 38 lots

of EUR-INR.

• Position value is worth Rs 21 lakhs.

Equity derivates vs currency derivatives

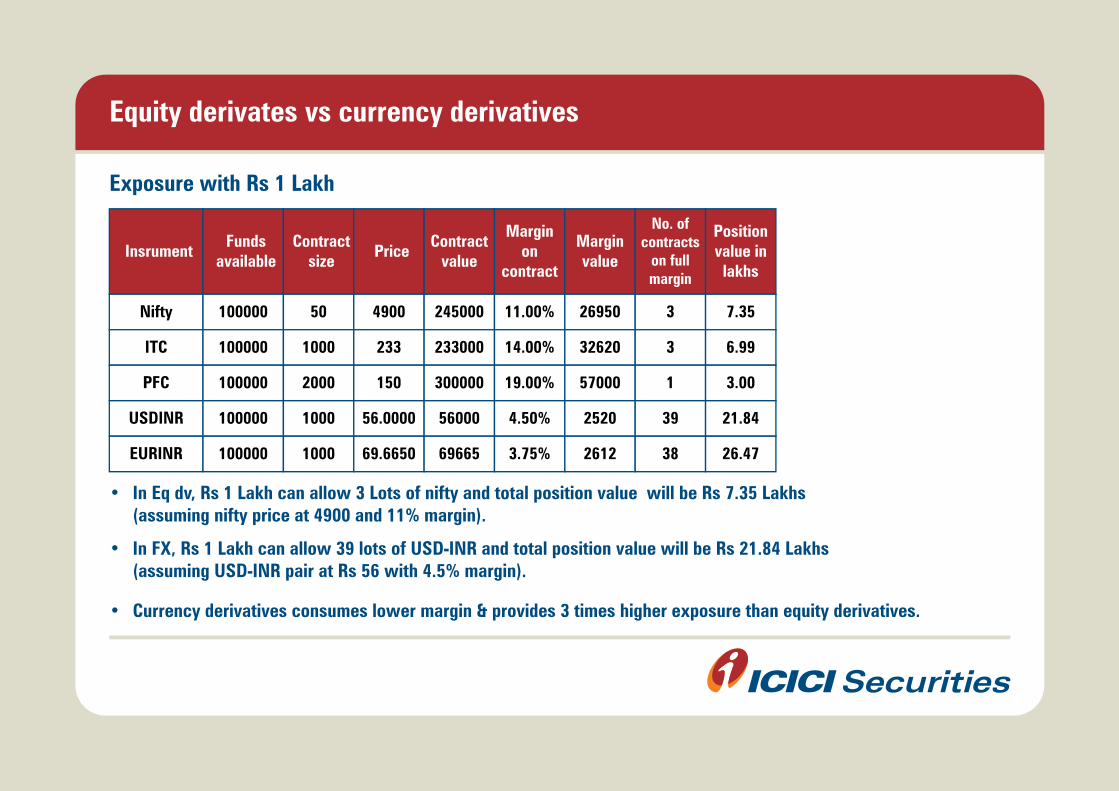

Exposure with Rs 1 Lakh

• In Eq dv, Rs 1 Lakh can allow 3 Lots of nifty and total position value will be Rs 7.35 Lakhs (assuming nifty price at 4900 and 11% margin).

• In FX, Rs 1 Lakh can allow 39 lots of USD-INR and total position value will be Rs 21.84 Lakhs (assuming USD-INR pair at Rs 56 with 4.5% margin).

• Currency derivatives consumes lower margin & provides 3 times higher exposure than equity derivatives.

Insrument

Nifty 100000 50 4900 245000 11.00% 26950 3 7.35

ITC 100000 1000 233 233000 14.00% 32620 3 6.99

PFC 100000 2000 150 300000 19.00% 57000 1 3.00

USDINR 100000 1000 56.0000 56000 4.50% 2520 39 21.84

EURINR 100000 1000 69.6650 69665 3.75% 2612 38 26.47

Fundsavailable

Contractsize

Contractvalue

Marginon

contract

Marginvalue

No. ofcontracts

on fullmargin

Positionvalue inlakhs

Price

Daily currency report, provided by ICICI Securities research

Disclaimer

ICICI Securities Ltd.( I-Sec). Registered office of I-Sec is at ICICI Securities Ltd. - ICICI Centre, H. T. Parekh Marg, Churchgate, Mumbai - 400020, India, Tel No : 022 - 2288 2460, 022 - 2288 2470. I-Sec is a Member of National Stock Exchange of India Ltd., SEBI Regn. No. INB 230773037 (CM), SEBI Regn. No. INF 230773037 (F&O), SEBI Regn No. INE230773037 (CD), Bombay Stock Exchange Ltd., SEBI Regn. No. INB011286854 (CM), SEBI Regn No. INF010773035 (F&O). Name of the Compliance officer: Ms. Mamta Jayaram Shetty, Contact number: 022-40701000, E-mail address: [email protected]. Kindly read the Risk Disclosure Documents carefully before investing in Equity Shares, Derivatives or other instruments traded on the Stock Exchanges. The contents herein above shall not be considered as an invitation or persuasion to trade or invest. Investors should make independent judgment with regard suitability, profitability, and fitness of any product or service offered herein above. I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of any actions taken in reliance thereon.The contents of this presentation are solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments or any other product. While due care has been taken in preparing this presentation, I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of any inaccurate, delayed or incomplete information nor for any actions taken in reliance thereon.

Thank You