PowerPoint Presentationfilecache.drivetheweb.com/ir1_vaalco/227/download/... · All statements...

26

NYSE:EGY March 2015

-

Upload

nguyenxuyen -

Category

Documents

-

view

215 -

download

1

Transcript of PowerPoint Presentationfilecache.drivetheweb.com/ir1_vaalco/227/download/... · All statements...

NYSE:EGY

March 2015

2

This presentation includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. All statements included in this presentation that address activities, events or developments that VAALCO

expects, believes or anticipates will or may occur in the future are forward-looking statements. These statements include expected capital expenditures, future

drilling plans, objectives and operations, prospect evaluations, negotiations and relations with governments and third parties, expectations regarding processing

facilities, reserve growth, estimated revenues and losses, and projected costs, timing and amount of future production. These statements are based on

assumptions made by VAALCO based on its experience perception of historical trends, current conditions, expected future developments and other factors it

believes are appropriate in the circumstances. Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond

VAALCO's control. These risks include, but are not limited to, oil and gas price volatility, inflation, general economic conditions, VAALCO's success in

discovering, developing and producing reserves, lack of availability drilling equipment and services, availability of and capital, environmental risks, drilling risks,

foreign operational risks, the existence of H2S in production, regulatory changes, the uncertainty inherent in estimating reserves and in projecting future rates of

production, cash flow and access to capital, the timing of development expenditures, and other risks. Additional information on risks and uncertainties that could

affect our business prospects and performance are provided in the most recent reports of VAALCO filed with the Securities and Exchange Commission. These

forward-looking statements are based on VAALCO’s current expectations and assumptions about future events and are based on currently available information

as to the outcome and timing of future events. VAALCO cautions you that forward-looking statements are not guarantees of future performance and that actual

results or developments may differ materially from those projected in the forward-looking statements. VAALCO disclaims any intention or obligation to update or

revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

The SEC requires oil and gas companies, in their filings with the SEC, to disclose proved reserves that a company has demonstrated by actual production or

conclusive formation tests to be economically and legally producible under existing economic and operating conditions. VAALCO uses the terms “estimated

ultimate recovery,” “EUR,” “probable,” “3P,” “possible,” and “non-proven” reserves, reserve “potential” or “upside,” “unrisked potential” or other descriptions of

volumes of reserves potentially recoverable through additional drilling or recovery techniques that are not classified as proved reserves, may not have been

calculated as defined by SEC regulations and that the SEC’s guidelines may prohibit us from including in any future filings with the SEC. These estimates are by

their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of being actually realized by the

company. VAALCO believes these estimates are reasonable, but such estimates have not been reviewed by independent engineers. Estimates may change

significantly as development provides additional data, and actual quantities that are ultimately recovered may differ substantially from prior estimates. Production

forecasts are dependent upon many assumptions, including estimates of production decline rates from existing wells and the outcome of future drilling activity.

Although VAALCO believes the forecasts are reasonable, VAALCO can give no assurance they will prove to have been correct. They can be affected by

inaccurate assumptions and data or by known or unknown risks and uncertainties.

Market and industry data and forecasts used in this presentation have been obtained from independent industry sources as well as from research reports

prepared for other purposes. Although VAALCO believes these third-party sources to be reliable, VAALCO has not independently verified the data obtained from

these sources and VAALCO cannot assure you of the accuracy or completeness of the data. Forecasts and other forward-looking information obtained from

these sources are subject to the same qualifications and uncertainties as the other forward looking statements in this presentation.

Inquiries:

VAALCO Energy, Inc.

Attn: Gregory R. Hullinger

9800 Richmond Avenue

Houston, TX 77042

Ph: 713-623-0801

www.vaalco.com

Safe Harbor Statement

3

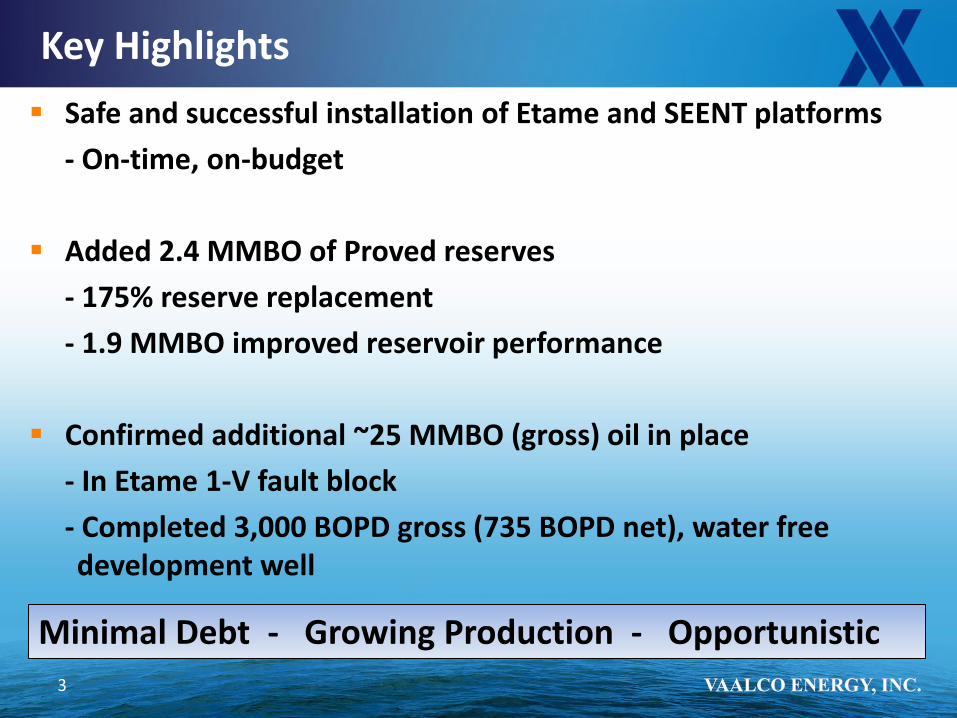

Key Highlights

Safe and successful installation of Etame and SEENT platforms

- On-time, on-budget

Added 2.4 MMBO of Proved reserves

- 175% reserve replacement

- 1.9 MMBO improved reservoir performance

Confirmed additional ~25 MMBO (gross) oil in place

- In Etame 1-V fault block

- Completed 3,000 BOPD gross (735 BOPD net), water free development well

Minimal Debt - Growing Production - Opportunistic

West Africa Focus

4

Block 5 Working Interest 40.0%

1,400,000 gross acres 560,000 net acres

Offshore Exploration

Etame Marin Permit Working Interest 28.1%

28,700 gross acres 8,100 net acres

Offshore Production and Exploration

Mutamba Iroru Permit Working Interest 41.0%

270,000 gross acres 111,000 net acres

Onshore Exploration & Development

Block P Working Interest 31.0%

57,000 gross acres 18,000 net acres

Offshore Exploration & Development

GABON Port Gentil

Libreville

Luanda

ANGOLA

EQUATORIAL GUINEA

Bata

Company Profile

5

Key Metrics

Share Price(1) $3.08

52-Week Range(1) $3.00 - $9.67

Market Capitalization(1) $178 million

Cash Balance including restricted(2) $ 92 million

Revolving Debt Facility(2)

Current Capacity(2) Current Borrowings(2)

$ 65 $ 25 $ 15

Net Production(1) 4,150 BOPD

2014 EBITDAX(3) $ 79 million

Reserves (2P)(2) 11.6 MMBOE

% Oil (Brent Based Pricing) 97%

% Operated 100%

Employees(2)

Corporate International

113 45 68

(1) As of 3/20/2015 (2) As of 12/31/2014 (3) See detail in

appendix

million

million

million

Etame Marin Permit (Production / Reserves)

6

Historical growth in EUR

Development drilling - 2015

Reversing production decline

0

5

10

15

20

25

30

2010 2011 2012 2013 2014

Estimated Net EUR 1P Reserves

-

1,000

2,000

3,000

4,000

5,000

6,000

2010 2011 2012 2013 2014 2015

Net Production (BOPD)

Estimate

Full Year Guidance

3,900 – 4,600 BOPD

First Quarter 2015 Guidance

~4,150 BOPD

Etame Marin Reserves

7

2014 Reserve Replacement Ratio of 175%

2014 Reserve Add of 2.4 MMBO 1.9 PDP (Improved Performance)

2015 Drilling program – reserve upside

8.2

3.1

2P Reserves 11.3 MMBO

Proved Probable

3.0

0.2

5.0

1P Reserves 8.2 MMBO

PDP PDNP PUD

7.2 8.2

2.3

0.1

(1.4)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

YE 2013 Reserves Production Revisions Extensions YE 2014 SECReserves

YE 2014 Proved Reserves Reconciliation (MMBO)

Operator with a 28.1% net W.I. Partners: Sinopec (Addax), Sasol, Sojitz , PetroEnergy and Tullow

2014 production averaged – 15,890 gross (3,880 net) BOPD

Current production 17,000 gross (4,150 net) BOPD*

Cumulative production through 12/31/2014 – 82.6 million barrels

Installation of two new platforms completed in 3Q 2014

Re-established Ebouri platform production in 4Q 2014

2015 development drilling program underway

Offshore Gabon – Etame Marin Permit

8

GABON Port Gentil

Libreville

Etame Marin Permit Working Interest 28.1%

Ebouri

SE Etame

Etame

South Tchibala & Avouma

North Tchibala

FPSO “Petroleo Nautipa” Long-term contract with Tinworth through 2020

Capacity: 30,000 bbls of total fluids per day Capacity: 25,000 bbls of oil per day

* As of March 2015

Export Pipeline

Etame Field Expansion Project

9

New Etame Platform

On-time, on-budget

4 pile, 8 slot platform in water depth of 85 meters

Targeting 10 MMBOE gross reserves

Transocean “Constellation II” jackup rig

Initial 3 well development $25.0 - $27.0 million gross ($7.0 - $7.6 million net) per well

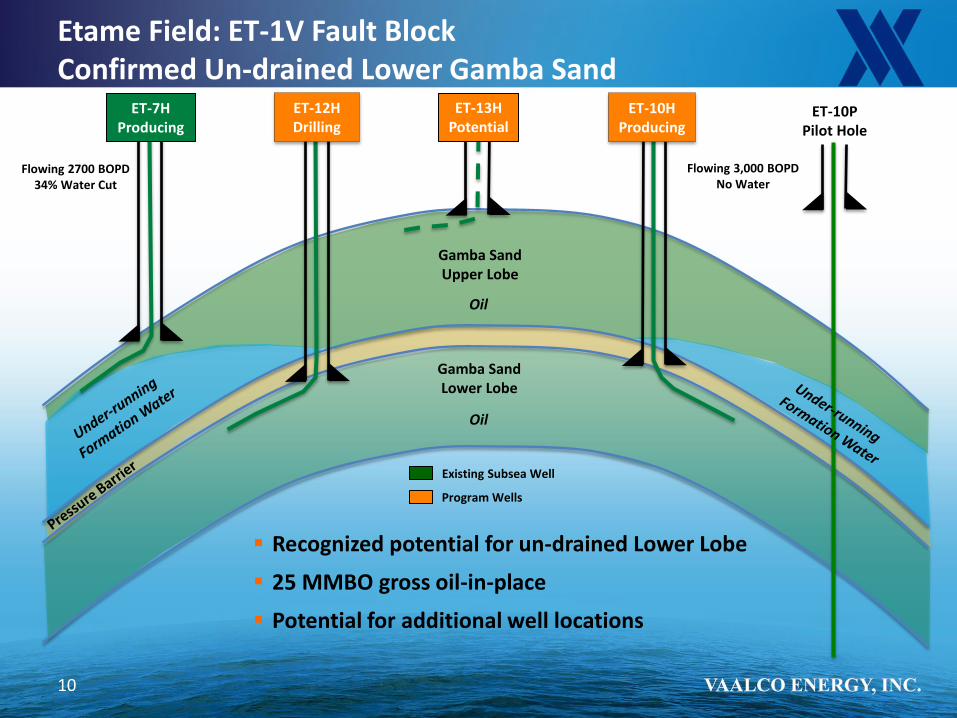

Encouraging results from the 1-V fault block - Etame 10-H producing ~3,000 BOPD - Etame 12-H well currently drilling

Etame 8-H well shut in due to H2S - Flow test scheduled shortly

Subsea Wells

Initial Planned Wells

Etame

SE Etame

ET-4H ET-5H

ET-7H

ET-6H ST

ET-1V Fault Block ET-12H

ET-10H

ET-8H ET-9H

Etame Field: ET-1V Fault Block Confirmed Un-drained Lower Gamba Sand

ET-10P Pilot Hole

Gamba Sand Upper Lobe

Gamba Sand Lower Lobe

Flowing 2700 BOPD 34% Water Cut

Flowing 3,000 BOPD No Water

Oil

Oil

Recognized potential for un-drained Lower Lobe

25 MMBO gross oil-in-place

Potential for additional well locations

10

Existing Subsea Well

Program Wells

ET-7H Producing

ET-12H Drilling

ET-13H Potential

ET-10H Producing

SE Etame & North Tchibala Fields Project

11

New SEENT Platform

On-time, on-budget

4 pile, 8 slot platform in water depth of 85 meters

Targeting 7 MMBO gross reserves

Initial 3 well development $25.0 - $28.5 million gross ($7.0 - $8.0 million net) per well - Post drilling at Etame platform

Spud initial well 2Q 2015

SE Etame Gamba well depth ~1,900 meters

North Tchibala Dentale well depth ~2,750 meters

Initial Planned Wells

SE Etame

North Tchibala

Stratigraphic Column

Crude Sweetening Project

12

Ebouri

SE Etame

Etame

South Tchibala & Avouma

North Tchibala

Targeting sour oil reserves at Ebouri and Etame fields

Due to significant fall in oil prices, re-evaluating project scope and design

Some options being considered:

Chemical removal Install facilities on existing structures Use of surplus equipment Potential to retrofit mobile drilling unit

Timing should be known as early as Q4 2015

Reserves associated with this project were booked prior to 2014

Reclassification of these reserves would not likely lead to an additional impairment

Remain committed to finding the most economic way to develop the reserve

Export Pipeline

13

Onshore Gabon- Mutamba Iroru Permit

VAALCO operated with 41% working interest

N’Gongui discovery well drilled in Q4 2012

Encountered 49 feet of oil pay in the Gamba Formation

Revised production sharing contract term sheet was signed in 3Q 2014

Development slowed while costs and design re-evaluated to improve returns

Shell Rabi Kounga Field Cum: 840 MMBO EUR 900 MMBO

TOTAL Atora Field

Cum: 38 MMBO

VAALCO N’Gongui Discovery

Shell Bende Field

Shell Gamba-Ivinga Field

Cum: 286 MMBO & 568 BCF EUR 350 MMBO Discoveries

Rabi Kounga Pipeline

VAALCO Permit

14

Offshore Equatorial Guinea - Block P

VAALCO 31% working interest

Block P Partners have agreed to the development of the Venus discovery prior to the drilling of exploration wells

Revising the JOA to reflect joint operatorship

Development slowed while costs and design re-evaluated to improve returns

17-21 million BOE gross EUR

Marathon 1,100 mmboe

Exxon 1,300 mmboe

Hess 600 mmboe

VAALCO Block P

PDA

Noble 210 mmboe

Oil Blocks

VAALCO Block

Atlantic

Atlantic Ocean

Block P PDA

A’

A

Venus

Europa

SW Grande

Marte

Exploration Program

15

Angola Block 5 – Identified Exploration Upside

16

Maersk AZUL-1

Cobalt Mavinga-1

Cobalt CAMEIA-1 & CAMEIA-2

Cobalt Lontra-1

VAALCO Loengo Prospect

VAALCO Ombundi Lead

Mobil Baleia-1A

VAALCO Block 5

Prospects

Oil Discoveries

Cobalt Bicuar-1A

KWANZA BASIN

Cobalt Orca-1

Pre-Salt Leads

Post-Salt Prospects & Leads

Post-Salt Discovery

2015 New PSDM Reprocessing (2233 km²)

50 Kilometers

Kindele

B Lead

A Lead

Ombundi

E Lead

Loengo

Jack

Mubafo

Expanded lead inventory - Derived from new 3-D seismic reprocessing

VAALCO operated with 40% WI, 10% Govt. carry

Sonangol P&P 40% WI, 10% Govt. carry

Angola Block 5 – Kindele Post Salt Prospect

Kindele Prospect

Dry Hole Costs - ~ $38 - $42 million gross ($19 - $21 million net to VAALCO)

Spud March 2, 2015

Mucanzo sand primary target

Currently drilling at 1,250 meters

Planned total depth 2,250 meters

Kindele-1

Mubafo Discovery Kindele Prospect Discovery

Prospects

Gross Reserves Min Mid Max

(MMBOE) 20 28 49

A

A’

A A’

Salt

Sag

Syn-Rift

Basement

Mucanzo

~2 miles

Water Depth = 101 m

Mubafo-1 1988 Conoco

Discovery Tested 1100

BOPD

SW NE

17

Loengo A A’

Block 5 Block 20

Ombundi

Possible Oil Zone

Confirmed Oil Zone

VAALCO Prospect

VAALCO Lead

Offshore Angola - Block 5 Regional X-section

Salt

Maersk AZUL-1

Cobalt Mavinga-1

Cobalt CAMEIA-1 & CAMEIA-2

Cobalt Lontra-1

VAALCO Loengo Prospect

VAALCO Ombundi Lead

Mobil Baleia-1A

VAALCO Block 5

Prospects

Oil Discoveries

Cobalt Bicuar-1A

KWANZA BASIN

Cobalt Orca-1

~15 miles ~65 miles

Salt

Basement

Basement

Cobalt Discovery

Orca -1

Mobil Discovery

Baleia -1A

18

Large pre-salt structures in the Kwanza Basin

VAALCO’s leads are located approximately 65 miles from the Orca Field (Block 20)

VAALCO’s leads are in much shallower water depths (100 m – 500 m)

2015 – Full Year Guidance (As of March 17, 2015)

19

BOPD 3,900 – 4,600

OPEX ($MM) $30.0 MM - $33.0 MM

Workovers ($MM) $3.0 MM - $6.0 MM

G&A ($MM) $12.5 MM - $15.0 MM (1)

DD&A ($/bbl) $15.0 - $18.0

CAPEX ($MM) $65.0 - $75.0

(1) Includes ~$3.5MM non-cash compensation

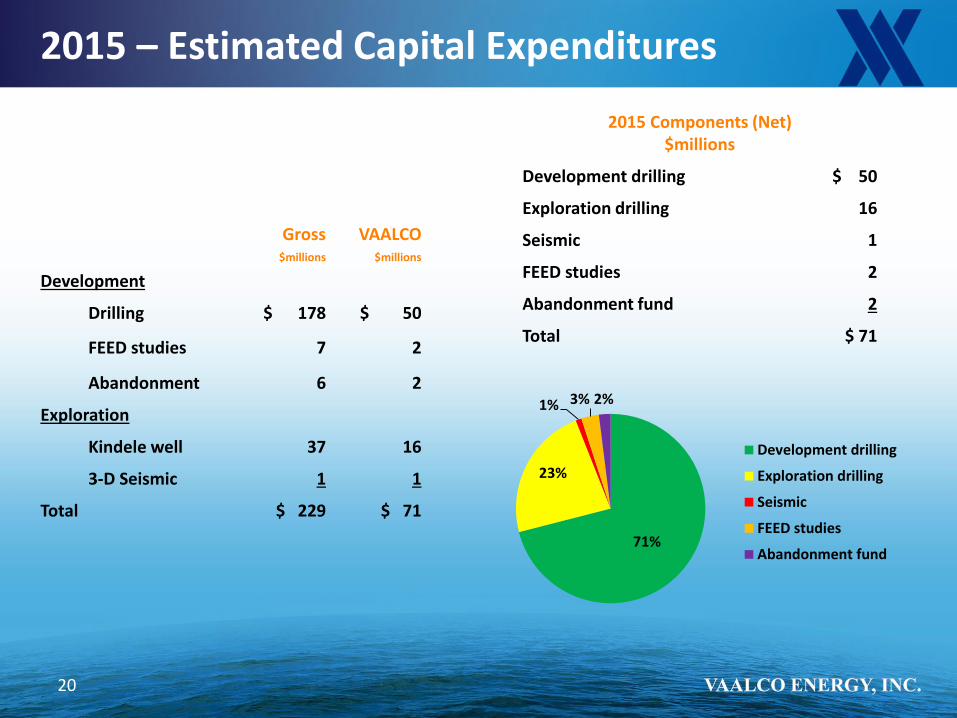

2015 – Estimated Capital Expenditures

20

Gross $millions

VAALCO

$millions

Development

Drilling $ 178 $ 50

FEED studies 7 2

Abandonment 6 2

Exploration

Kindele well 37 16

3-D Seismic 1 1

Total $ 229 $ 71

2015 Components (Net) $millions

Development drilling $ 50

Exploration drilling 16

Seismic 1

FEED studies 2

Abandonment fund 2

Total $ 71

71%

23%

1% 3% 2%

Development drilling

Exploration drilling

Seismic

FEED studies

Abandonment fund

21

Why Invest in VAALCO Now?

Near term catalysts Drilling Kindele Continued Development Program at Etame – reversing production decline Analyzing recently processed pre-salt seismic on Block 5

Proven West Africa Operator 100% operated In 3 out of top 4 West Africa producing countries Projects on time, on budget

Solid Financial Position Increasing production profile in 2015 Unrestricted Cash Position + Borrowing Base Internally funding development and exploration activities

High Impact Exploration Prospects Significant exposure to lower cost pre-salt opportunities

Identifying Potential Discovered Resource Acquisition Acquisition would balance development / exploration portfolio

22

APPENDIX

23

Strong Financial Position

($’s in millions)

Financial Position 12/31/2014

Cash Balance (Includes Restricted) $ 92

Working Capital (Includes Restricted) 95

Net PP&E 108

Current Borrowing Balance (IFC Loan) 15

Retained Earnings 147

Financial Performance (Year Ended 2014)

Revenues 128

Operating Income -54

Tax Expense -22

Net Loss (includes non-cash impairment of $98 MM) -78

EBITDAX(1) 79

Funds Available for Growth

Working Capital 95

Current Borrowing Capacity (IFC Loan) 10

Total Funds Available for Growth $ 105

Basic Shares Outstanding 12/31/2014 (in millions) 57.2

Earnings Per Share (12 Months Ended 2014) $ -1.36 (1) See detail in appendix

EBITDAX Reconciliation

24

12 months

ended

12/31/2014

12 months

ended

12/31/2013

Revenues $ 169,277 $

Operating costs and expenses (182,097) (92,052)

Operating income (loss) (54,406) $ 77,225 $

Depreciation, depletion and amortization 20,086 16,929

Exploration expenses 15,358 23,928

Total add backs 133,785 $

40,857 $

EBITDAX (Amounts in thousands)

79,379 $ 118,082 $

127,691

Impairment of proved properties 98,341 ---

Syn-Rift

Sag

Basement

NE

VAALCO

~3 miles

SW

Lead A VAALCO Lead B

Salt

Offshore Angola - Block 5: Leads A & B

Potential Carbonate Buildup areas

New leads identified from the new seismic processing

Cross-section over 2 leads utilizing re-processed 3D

Well imaged basement highs

Basement highs are prone to carbonate build-ups

Leads are ~3 miles apart

Water depth ~ 150m

25

Biography on Key Executives Mr. Guidry assumed the role of Chief Executive Officer for VAALCO Energy, Inc. on October 21, 2013. At that time, he was also appointed to our Board of Directors and became Chairman of the Board on June 4, 2014. Prior to joining VAALCO, Mr. Guidry was Vice President of Business Development for Marathon Oil Corporation since July 2011, where he was responsible for acquisitions of strategic opportunities for value growth. Mr. Guidry also held numerous executive management positions, including President of Marathon Oil Libya Limited from October 2008 to July 2011. Prior to the Libya assignment, he was Regional Vice President for Marathon Oil’s North American Production Operations. Mr. Guidry oversaw all of the company’s exploration and production activities onshore and offshore U.S. He also spent five years leading Marathon Oil’s Central Africa Business Unit, overseeing project expansions and operations in Equatorial Guinea, Gabon and Angola. Throughout his career, he has held challenging technical, staff and managerial positions in the company’s domestic and international production organizations. Mr. Guidry graduated from the University of Louisiana Lafayette in 1980 with a bachelor’s degree in petroleum engineering. He is a member of the Society of Petroleum Engineers, and served on the board of directors for the Corporate Council on Africa, the Independent Petroleum Association of America, the U.S. Oil and Gas Association and was a member of the Upstream Committee of the American Petroleum Institute. We believe Mr. Guidry’s strong operational background and experience, particularly in the international arena, is a valuable asset to our Board.

In October of 2008, Mr. Scheirman was appointed Chief Operating Officer following his overseeing of the planning, fabrication, and installation of the Avouma Field and Ebouri Field production platforms offshore Gabon. Mr. Scheirman continues to serve as President of VAALCO Energy, Inc., a position held since 1992. Mr. Scheirman served as Chief Financial Officer from 1991 to 2008. From 1991 to 1992, Mr. Scheirman served as Executive Vice President of the Company. Prior to joining VAALCO Energy, Inc., Mr. Scheirman was an Associate at McKinsey & Company, Inc. from 1989 to 1991, an investment banker with Copeland, Wickersham and Wiley from 1984 to 1989, and a Petroleum Reservoir Engineer for Exxon Company, U.S.A. from 1978 to 1984. Mr. Scheirman holds a B.S. (Summa Cum Laude) and M.S. in Mechanical Engineering from Duke University (1977 and 1978, respectively) and an M.B.A. from California Lutheran University (1984).

Mr. Hullinger joined VAALCO as our Chief Financial Officer in October 2008 after more than 30 years of finance and accounting experience at Shell Oil Company and its parent company, Royal Dutch Shell. Notable positions held by Mr. Hullinger at Shell Oil include Controller, Treasurer, CFO – Shell Deer Park Refining Company and CFO – Pecten Cameroon Company (West Africa). For Royal Dutch Shell, Mr. Hullinger held the positions of International Audit Manager and as the Manager for Group Accounting, the unit responsible for the financial consolidations, results and reporting. Mr. Hullinger was twice elected Chairman of the Accounting Committee of the American Petroleum Institute. He holds a B.S. in Accounting from Louisiana State University.

26