Pollution Exclusion in CGL Policies - Strafford...

43

Pollution Exclusion in CGL Policies Navigating Scope of the Exclusion in Light of Differing Court Interpretations Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. THURSDAY, JULY 12, 2012 Presenting a live 90-minute webinar with interactive Q&A Carl A. Salisbury, Partner, Kilpatrick Townsend & Stockton, New York Louis A. Chiafullo, Partner, McCarter & English, Newark, N.J. Jonathan T. Viner, Partner, Bates Carey Nicolaides, Chicago

-

Upload

phungxuyen -

Category

Documents

-

view

219 -

download

0

Transcript of Pollution Exclusion in CGL Policies - Strafford...

Pollution Exclusion in CGL Policies Navigating Scope of the Exclusion in Light of Differing Court Interpretations

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, JULY 12, 2012

Presenting a live 90-minute webinar with interactive Q&A

Carl A. Salisbury, Partner, Kilpatrick Townsend & Stockton, New York

Louis A. Chiafullo, Partner, McCarter & English, Newark, N.J.

Jonathan T. Viner, Partner, Bates Carey Nicolaides, Chicago

Sound Quality

If you are listening via your computer speakers, please note that the quality of

your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory and you are listening via your computer

speakers, you may listen via the phone: dial 1-866-927-5568 and enter your

PIN -when prompted. Otherwise, please send us a chat or e-mail

[email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Pollution Exclusion in CGL Policies

History/Evolution of the CGL

Pollution Exclusion Jonathan T. Viner, Partner

Bates Carey Nicolaides LLP

191 N. Wacker Drive, Suite 2400

Chicago, Illinois 60606

312-762-3143

5

History/Evolution of the CGL Pollution Exclusion

Sudden and Accidental Pollution Exclusion

– 1973 ISO Form

– Excludes coverage for • Bodily injury or property damage arising out of the

discharge, dispersal, release or escape of smoke, vapor, soot, fumes, acids, alkalis, toxic chemicals, liquids or gases, waste materials or other irritants, contaminants or pollutants into or upon the land, the atmosphere, or any other water course or body of water, but this exclusion does not apply if such discharge, dispersal, release or escape is sudden and accidental.

6

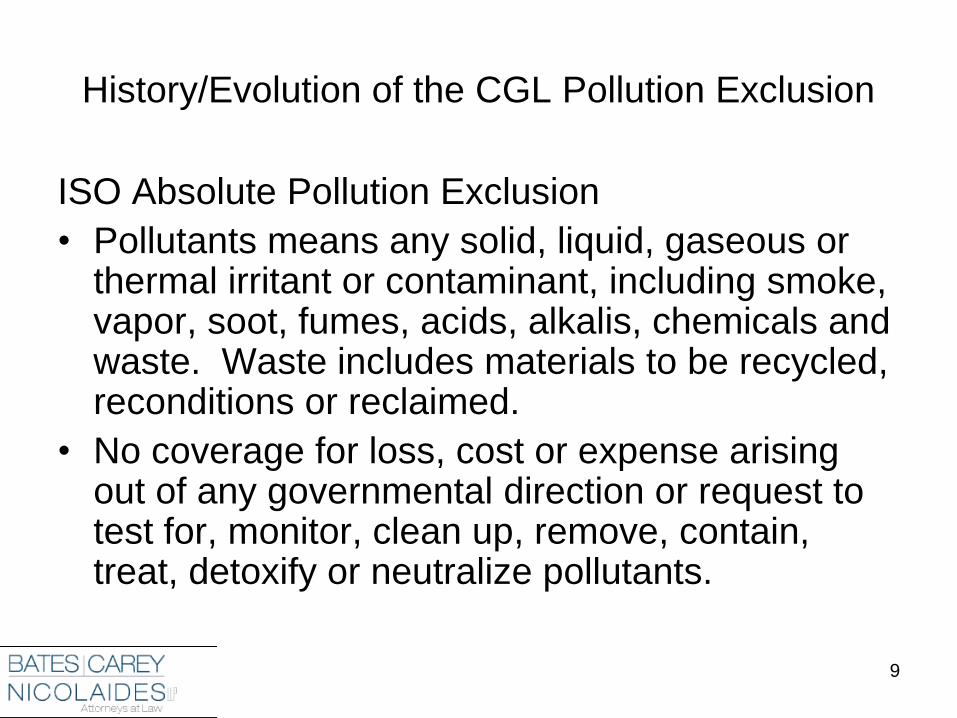

History/Evolution of the CGL Pollution Exclusion

ISO Absolute Pollution Exclusion

• Introduced into 1984 ISO form (Exclusion f)

• Excludes coverage for:

– bodily injury or property damage arising out of

the actual, alleged or threatened discharge,

dispersal, seepage, migration, release or

escape of “pollutants” under enumerated

conditions

7

History/Evolution of the CGL Pollution Exclusion

ISO Absolute Pollution Exclusion

• Applicable conditions include: – At or from premises insured owns, rents or occupies

– At or from any site or location used by insured or others for handling, storing, disposing processing or treating waste

– Pollutants that are at any time transported, handled, stored, treated, disposed of or processed as waste by insured or someone for whom insured has liability

– At or from a site or location on which insured or its (sub)contractors are performing operations, if pollutants brought onto the site for such operations

8

History/Evolution of the CGL Pollution Exclusion

ISO Absolute Pollution Exclusion

• Pollutants means any solid, liquid, gaseous or thermal irritant or contaminant, including smoke, vapor, soot, fumes, acids, alkalis, chemicals and waste. Waste includes materials to be recycled, reconditions or reclaimed.

• No coverage for loss, cost or expense arising out of any governmental direction or request to test for, monitor, clean up, remove, contain, treat, detoxify or neutralize pollutants.

9

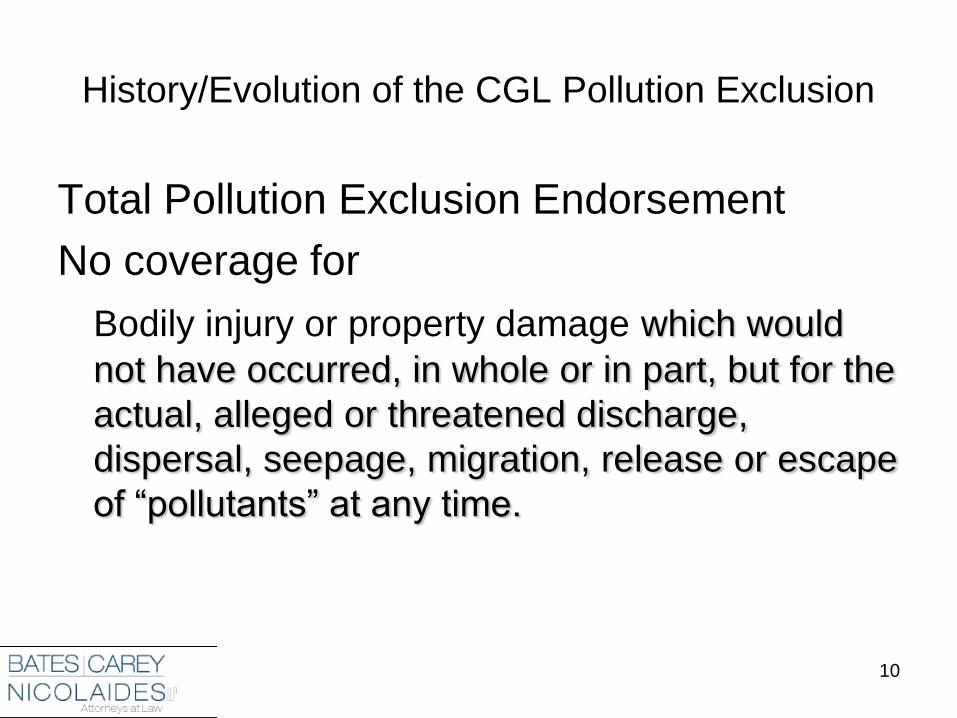

History/Evolution of the CGL Pollution Exclusion

Total Pollution Exclusion Endorsement

No coverage for

Bodily injury or property damage which would

not have occurred, in whole or in part, but for the

actual, alleged or threatened discharge,

dispersal, seepage, migration, release or escape

of “pollutants” at any time.

10

CARL A. SALISBURY

[email protected] 212.775.8779

Carl Salisbury is a partner on the Insurance Recovery Team at Kilpatrick Townsend &

Stockton. He has more than 20 years of experience in the litigation and trial of

complex commercial disputes. In addition to handling general commercial matters, Mr.

Salisbury has more than 20 years of courtroom and trial experience in complex

commercial insurance cases and has represented the full gamut of companies in

disputes involving large insurance claims, from small and middle-market corporations,

condominium associations, restaurants, and non-profit institutions, to Fortune 100

companies. He has helped corporate policyholders recover for insurance claims

involving environmental pollution, workplace discrimination, bodily injuries and property

damage, mold contamination, construction defects, and a variety of other commercial

disputes.

He received is law degree at Wake Forest University School of Law, where he was

Managing Editor of the Wake Forest University Law Review. He also served as a

judicial clerk to the Hon. Reynaldo G. Garza on the United States Court of Appeals for

the Fifth Circuit. He is admitted to practice in New York; New Jersey; the U.S. District

Court for the District of New York; the U.S. District Court for the District of New Jersey;

the U.S. Court of Appeals for the Third Circuit; and the Supreme Court of New Jersey.

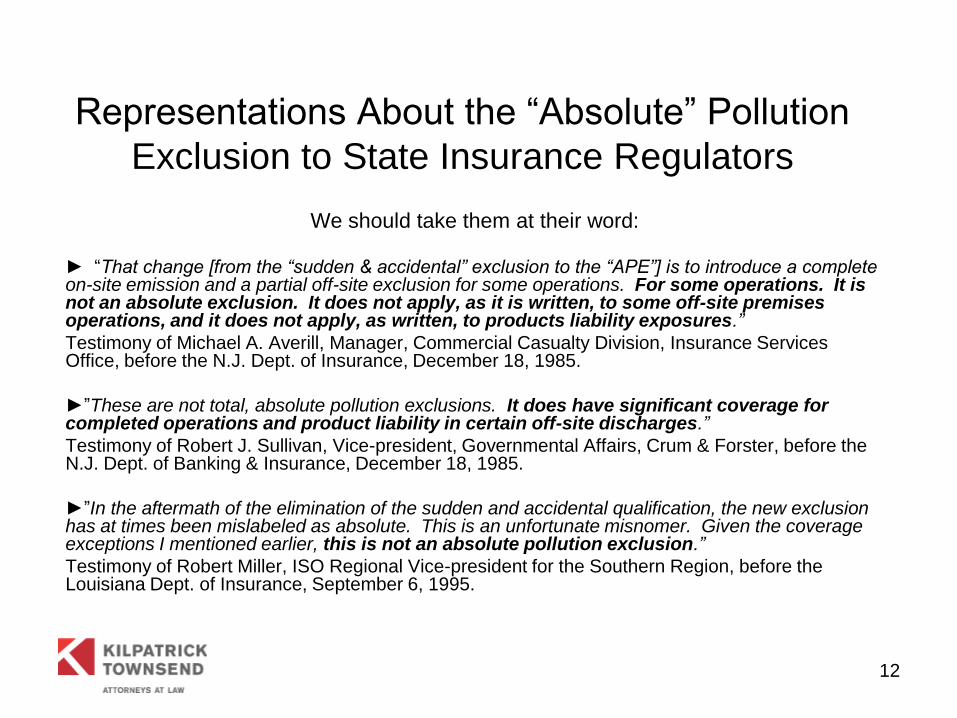

Representations About the “Absolute” Pollution

Exclusion to State Insurance Regulators

We should take them at their word:

► “That change [from the “sudden & accidental” exclusion to the “APE”] is to introduce a complete on-site emission and a partial off-site exclusion for some operations. For some operations. It is not an absolute exclusion. It does not apply, as it is written, to some off-site premises operations, and it does not apply, as written, to products liability exposures.”

Testimony of Michael A. Averill, Manager, Commercial Casualty Division, Insurance Services Office, before the N.J. Dept. of Insurance, December 18, 1985.

►”These are not total, absolute pollution exclusions. It does have significant coverage for completed operations and product liability in certain off-site discharges.”

Testimony of Robert J. Sullivan, Vice-president, Governmental Affairs, Crum & Forster, before the N.J. Dept. of Banking & Insurance, December 18, 1985.

►”In the aftermath of the elimination of the sudden and accidental qualification, the new exclusion has at times been mislabeled as absolute. This is an unfortunate misnomer. Given the coverage exceptions I mentioned earlier, this is not an absolute pollution exclusion.”

Testimony of Robert Miller, ISO Regional Vice-president for the Southern Region, before the Louisiana Dept. of Insurance, September 6, 1995.

12

Representations About the “Absolute”

Pollution Exclusion to Courts

Maybe we can’t take them at their word: ► Herbicide used by pest management company on a golf course was a “pollutant.”

Nationwide Mut. Ins. Co. v. Lang, Case No. 09-14258 (S.D.Fl. 2010).

► Dust generated from construction project at an airport was a “pollutant.”

Devcon Int’l. Corp. v. Reliance Ins. Co., Nos. 07-4602/08-1996, 2010 U.S. App. LEXIS 11619 (3d Cir. June 8, 2010).

► Damage from water and soil escaping from insured’s property was excluded by the

APE.

Builders Mut. Ins. Co. v. Half Court Press, LLC, No. 6:09-cv-0046, 2010 WL 3033911

(W.D.Va. Aug. 3, 2010).

► APE excludes coverage for manufacturer of filter that failed, causing oil leak.

Westwood Prods. Corp. v. Great American E&S Ins. Co., No. 3:10-cv-03605-MLC-DEA

(D.N.J. 2010).

13

Is Pure Drinking Water a “Pollutant”?

An underwriter testifies about the scope of the “Absolute Pollution Exclusion.”

If “pure spring drinking water” causes property damage, it can be considered a “pollutant.”

What about the expectations of “Joe Average” Insured?

If the underwriter is correct, is the APE ambiguous?

Deposition of Underwriter in Westwood Prods. Corp. v. Great American E&S Ins. Co., No. 3:10-cv-03605-MLC-DEA (D.N.J. 2010).

14

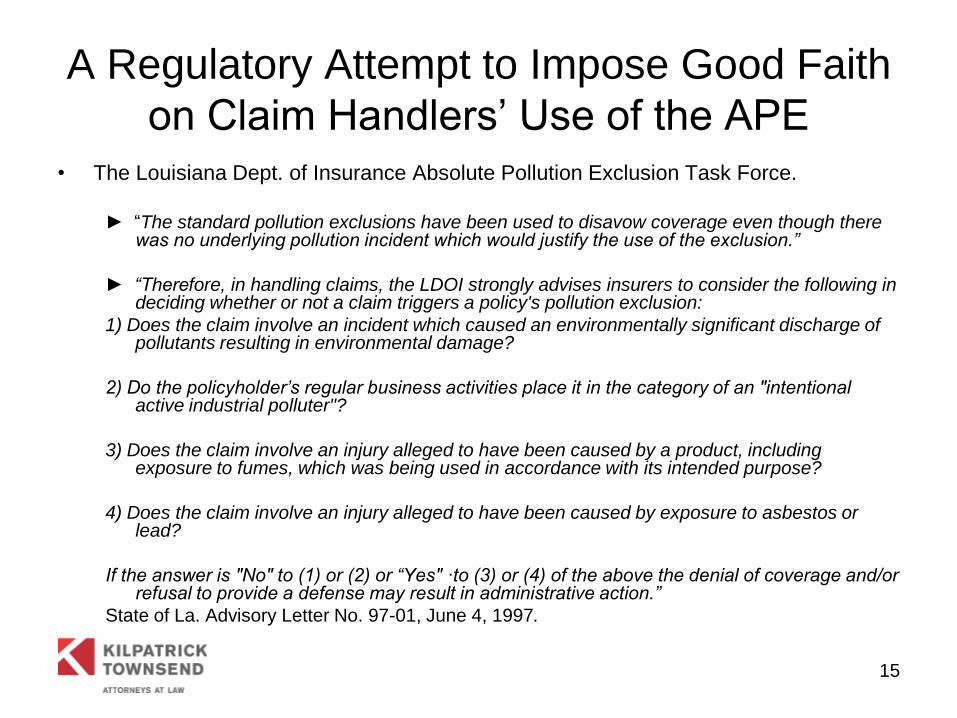

A Regulatory Attempt to Impose Good Faith

on Claim Handlers’ Use of the APE

• The Louisiana Dept. of Insurance Absolute Pollution Exclusion Task Force.

► “The standard pollution exclusions have been used to disavow coverage even though there

was no underlying pollution incident which would justify the use of the exclusion.”

► “Therefore, in handling claims, the LDOI strongly advises insurers to consider the following in deciding whether or not a claim triggers a policy's pollution exclusion:

1) Does the claim involve an incident which caused an environmentally significant discharge of pollutants resulting in environmental damage?

2) Do the policyholder’s regular business activities place it in the category of an "intentional active industrial polluter"?

3) Does the claim involve an injury alleged to have been caused by a product, including exposure to fumes, which was being used in accordance with its intended purpose?

4) Does the claim involve an injury alleged to have been caused by exposure to asbestos or lead?

If the answer is "No" to (1) or (2) or “Yes" ·to (3) or (4) of the above the denial of coverage and/or refusal to provide a defense may result in administrative action.”

State of La. Advisory Letter No. 97-01, June 4, 1997.

15

When Courts Consider the

Regulatory History of the APE

• Remembering Morton Int’l v. General Accident Ins. Co., 134 N.J. 1 (1993).

• Textron, Inc. v. Aetna Cas. & Surety Co., 754 A.2d. 742 (R.I. 2000).

• Doerr v. Mobil Oil Corp., 774 So. 2d 119 (La. 2000).

• American States Ins. Co. v. Koloms, 177 Ill. 2d 472, 687 N.E.2d 72 (1997).

• Keggi v. Northbrook Property & Cas. Co., 13 P.3d 785 (Ariz. 2000).

16

Pollution Exclusion in CGL Policies

Insurer Perspective

Jonathan T. Viner, Partner

Bates Carey Nicolaides LLP

191 N. Wacker Drive, Suite 2400

Chicago, Illinois 60606

312-762-3143

17

CGL Pollution Exclusion

Hypothetical:

Insured transport company provides metal

tanker trucks to take claimant’s milk from

farms to its central processing location,

where it is discovered – after some of the

milk is pumped into huge process tanks –

that metal particles from the tanker lining

got into the milk during transport.

18

CGL Pollution Exclusion

Figuli v. State Farm, 2012 WL 1036064 (Colo. App.)

• Injuries because of toxic mold and raw sewage in

rental property

• Court focused on term “waste”

• Reference to dictionary definition of sewage as

waste and waste as including the components of

sewage

• Reliance on statutory definition of raw sewage as a

pollutant under Water Quality Control Act

19

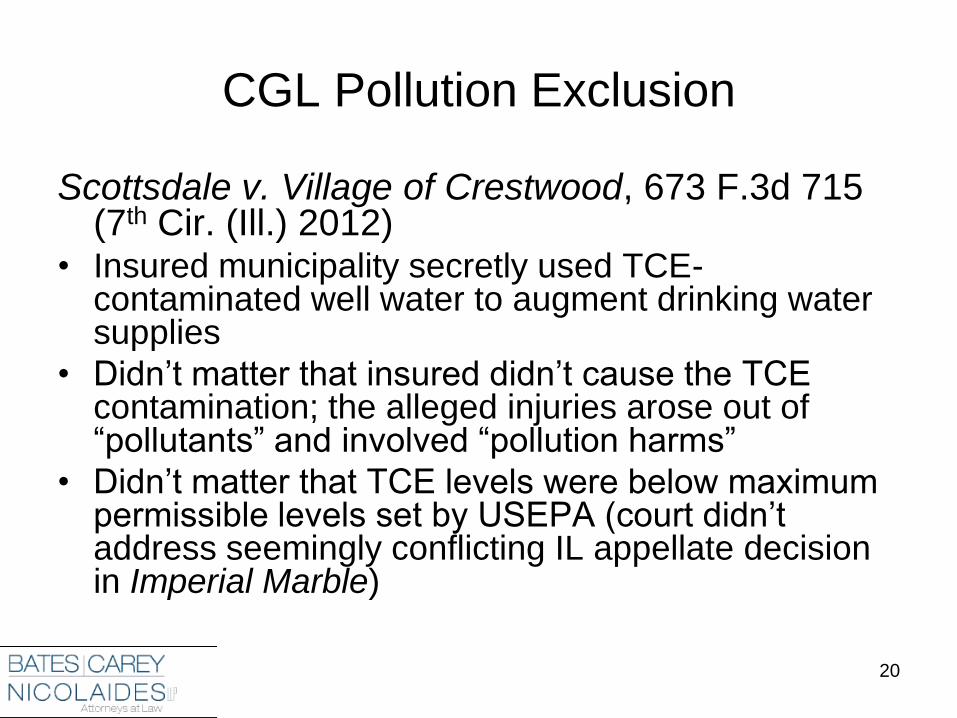

CGL Pollution Exclusion

Scottsdale v. Village of Crestwood, 673 F.3d 715 (7th Cir. (Ill.) 2012)

• Insured municipality secretly used TCE-contaminated well water to augment drinking water supplies

• Didn’t matter that insured didn’t cause the TCE contamination; the alleged injuries arose out of “pollutants” and involved “pollution harms”

• Didn’t matter that TCE levels were below maximum permissible levels set by USEPA (court didn’t address seemingly conflicting IL appellate decision in Imperial Marble)

20

CGL Pollution Exclusion

Racetrac Petroleum v. ACE American Ins. Co., 2011 WL 5299647 (11th Cir. (Ga.))

• Injury claims arising out of exposure to insured convenience store’s gasoline

• Slightly different pollution exclusion – didn’t use term “pollutants”

• Court rejected “illusory coverage” argument, which forms the basis for Indiana law – court held that the policy covers “countless other risks” faced by insured

21

CGL Pollution Exclusion

Markel Intl. Ins. Co. v. Florida West, 2011 WL

3505217 (11th Cir. (Fla.))

• Injuries from wading through bacteria-infested flood

water to retrieve property from insured’s self-storage

facility; bacteria was from wood millings on property

• A product that causes no harm when used properly

can still be classified as a pollutant; “contaminant”

and “irritant” are very broad terms

• Didn’t matter that complaint didn’t use terms like

irritant, contaminant, pollution or pollutant

22

CGL Pollution Exclusion

Certain Underwriters v. B3, Inc., 262 P.3d

397 (Ct. App. Okla. 2011)

• Injury claims due to purposeful discharge of

sewage from POTW into creek, to permit

renovation work

• Reliance on statute to define sewage as waste,

even where allegations referenced items such

as rancid food and discarded drugs

23

CGL Pollution Exclusion

RLI Ins. Co. v. Gonzalez, 2011 WL 69085

(5th Cir. (Tex.))

• Injury claims based on work-related silica

exposure

• Silica is a “pollutant” because OSHA classifies

silica dust as an air contaminant

• Existence of separate exclusion in policy for

asbestos-related injuries did not render pollution

exclusion ambiguous

24

CGL Pollution Exclusion

Union Ins. Co. v. Mendoza, 2010 WL 5065116 (10th Cir. (Kan.))

• Injuries from exposure to anhydrous ammonia mist used to fertilize farmland; mist was redirected during repair of mister

• Rejecting reasoning similar to that of the 7th Circuit in Pipefitters, holding that breadth of pollution exclusion, by itself, does not render it ambiguous

• Reliance on Kansas district court decision, Gerdes, to reject Kiger-type of analysis

• Dangerous qualities of ammonia fertilizer, as reflected in MSDS, rendered it a “pollutant”

25

CGL Pollution Exclusion

Scottsdale v. Universal Crop, 620 F.3d 926 (8th Cir. (Minn.) 2010)

• PD to claimants’ cotton crop when insured’s herbicide migrated to claimants’ property;

• Allegation that dried-up herbicide became airborne, landing on cotton plants and prevented photosynthesis

• “Relofting” theory of liability did not alter court’s conclusion that pollution exclusion barred coverage – damage to cotton was still caused by migration of chemicals, even though damage was not necessarily related to “polluting” aspect of those chemicals

26

CGL Pollution Exclusion

Hussey Copper v. Arrowood Ind., 2010 WL

3297246 (3d Cir. (Pa.))

• Deteriorated copper roof paneling results in

copper runoff into retention pond; insured

required by EPA to clean up

• Fact that claim involves product liability doesn’t

take it outside the exclusion

• Court didn’t buy regulatory estoppel argument

27

CGL Pollution Exclusion

PBM Nutritionals v. Lexington, 724 S.E.2d 708

(Va. 2012)

• Actually first-party coverage case, but notable

because it involves contamination of baby

formula during manufacturing

• Despite non-environmental nature of damage,

exclusion for loss caused by release, discharge,

escape or dispersal of contaminants or

pollutants barred coverage

28

CGL Pollution Exclusion

Travelers v. Chubb, 2012 WL 1071202 (E.D.Pa.)

• Nuisance claims premised on noxious odors

emanating from insured’s hog farms; alleged

physical harm and property damage due to

“odors, hazardous substances and

contaminated wastewater”

• Odors due to pig excrement fits squarely within

definition of “pollutants” as waste

29

CGL Pollution Exclusion

Maxine Furs v. Auto-Owners, 2011 WL 1197466

(11th Cir. (Ala.)

• Costs incurred to get rid of curry aroma in

claimant’s furs, from insured’s restaurant

• Curry aroma was a contaminant; otherwise there

would have been no need to clean the furs

• Unreasonable of insured to assert that claim did

not involve PD caused by migration, seepage or

escape of a “pollutant”

30

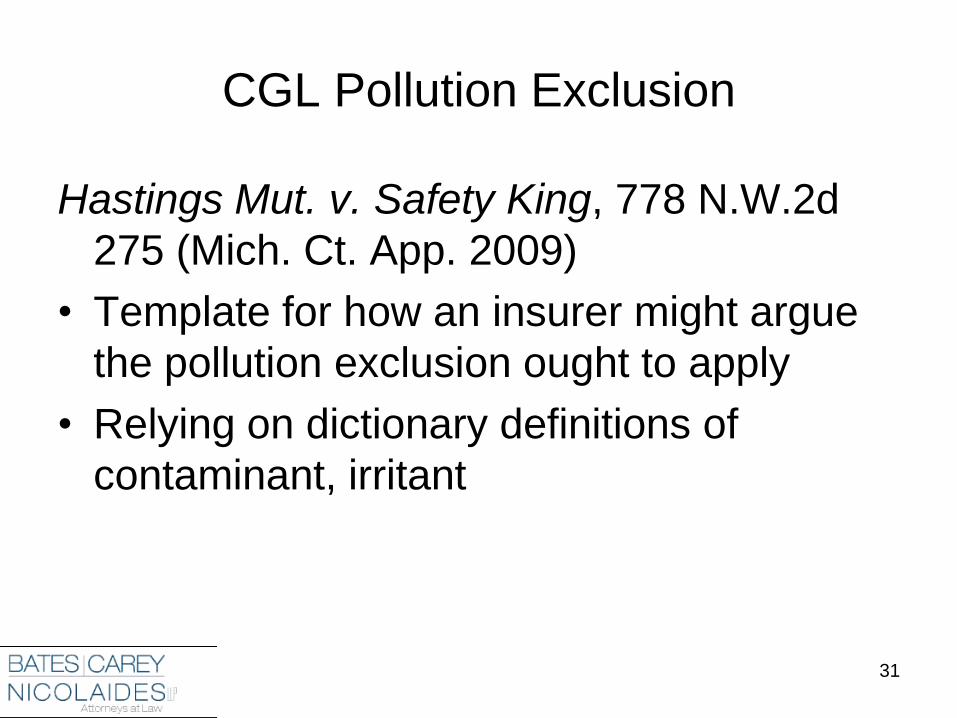

CGL Pollution Exclusion

Hastings Mut. v. Safety King, 778 N.W.2d

275 (Mich. Ct. App. 2009)

• Template for how an insurer might argue

the pollution exclusion ought to apply

• Relying on dictionary definitions of

contaminant, irritant

31

CGL Pollution Exclusion

Back to hypothetical: Metal particles in milk

• Milk was allegedly “contaminated” and was “adulterated” preventing sale

• Stainless steel particles “contaminated” milk under the dictionary definition

• The stainless particles were released into the milk and were subsequently dispersed into giant tanks by way of pumps

• Pollution Exclusion bars coverage?

32

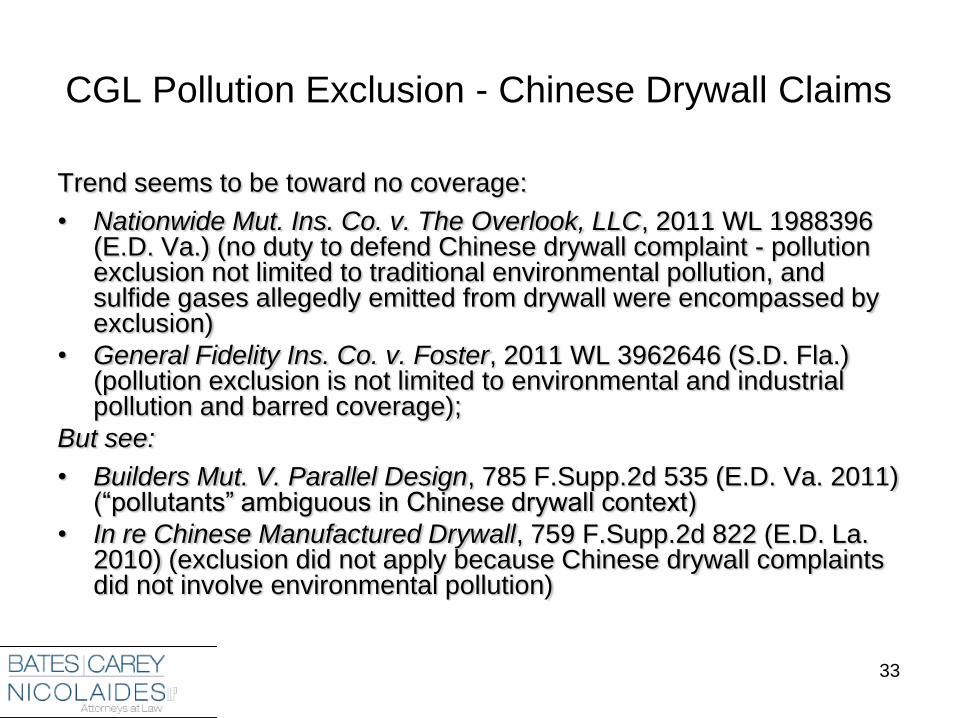

CGL Pollution Exclusion - Chinese Drywall Claims

Trend seems to be toward no coverage:

• Nationwide Mut. Ins. Co. v. The Overlook, LLC, 2011 WL 1988396 (E.D. Va.) (no duty to defend Chinese drywall complaint - pollution exclusion not limited to traditional environmental pollution, and sulfide gases allegedly emitted from drywall were encompassed by exclusion)

• General Fidelity Ins. Co. v. Foster, 2011 WL 3962646 (S.D. Fla.) (pollution exclusion is not limited to environmental and industrial pollution and barred coverage);

But see:

• Builders Mut. V. Parallel Design, 785 F.Supp.2d 535 (E.D. Va. 2011) (“pollutants” ambiguous in Chinese drywall context)

• In re Chinese Manufactured Drywall, 759 F.Supp.2d 822 (E.D. La. 2010) (exclusion did not apply because Chinese drywall complaints did not involve environmental pollution)

33

Pollution Exclusion in CGL

Policies: Navigating the Scope of the

Exclusion in Light of Differing Court

Interpretations

Lou Chiafullo, Esq.

July 12, 2012

www.mccarter.com

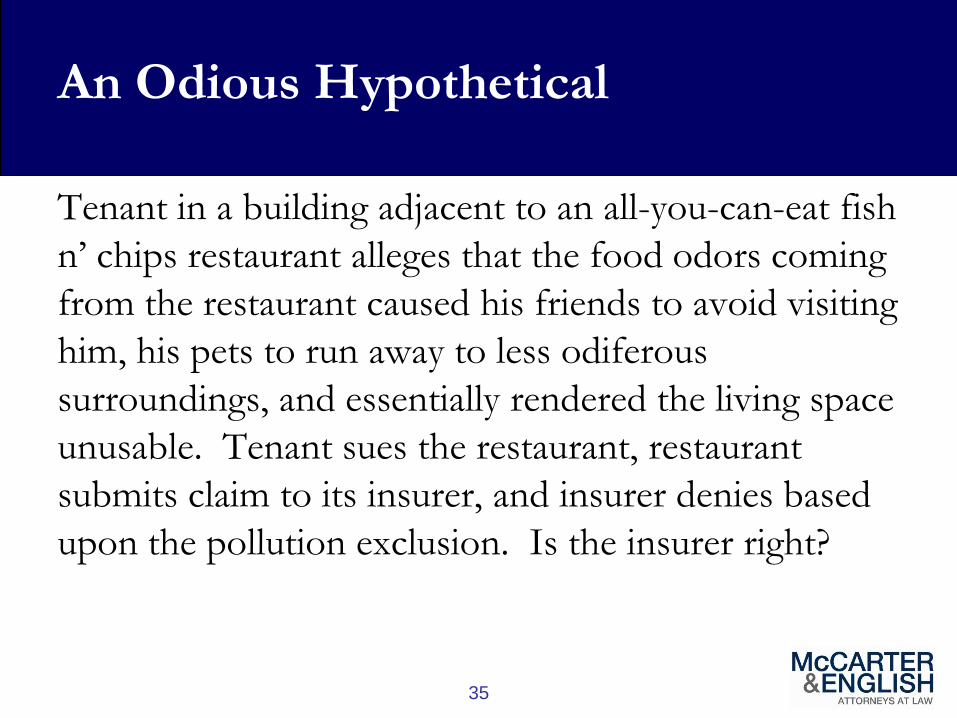

An Odious Hypothetical

Tenant in a building adjacent to an all-you-can-eat fish

n’ chips restaurant alleges that the food odors coming

from the restaurant caused his friends to avoid visiting

him, his pets to run away to less odiferous

surroundings, and essentially rendered the living space

unusable. Tenant sues the restaurant, restaurant

submits claim to its insurer, and insurer denies based

upon the pollution exclusion. Is the insurer right?

35

Barney Greengrass, Inc. v. Lumbermens Mut. Cas. Co.

2010 U.S. Dist. LEXIS 76781 (S.D.N.Y. 2010)

♦ Claimant alleged overpowering food odors and

smoke emanating from deli rendered living space

unusable

♦ SDNY found smoke probably was a pollutant

♦ However, applying exclusion to restaurant odors

violated reasonable expectations of a

businessperson, who understands exclusion to

apply to environmental harms

36

Meridian Mut. Ins. Co. v. Kellman

197 F.3d 1178 (6th Cir. 1999)

♦ Teacher sued contractor for alleged injuries from

exposure to sealant fumes

♦ 6th Circuit held absolute pollution exclusion did not

bar injuries from toxic substances confined to

general area of intended use

♦ “No reasonable person could find” exclusion

unambiguously applied to employee’s injuries when

legitimately within vicinity of chemicals

37

In re IdleAire Tech. Corp.

2009 Bankr. LEXIS 343 (D. Del. Bankr. 2009)

♦ Truck drivers inhaled carbon monoxide while using

HVAC systems at a rest stop

♦ Reasonable expectation of coverage b/c:

– Insurance industry represented to regulators that

exclusion applied only to traditional pollution;

– Insured was not a “polluter,” but HVAC producer

♦ Applying exclusion would “lead to an absurd result”

38

Belt Painting Corp. v. TIG Ins. Co.

795 N.E.2d 15 (N.Y. 2003)

♦ Worker inhaled paint or solvent fumes

♦ NY Court of Appeals found exclusion ambiguous

♦ Exclusion did not unambiguously apply to ordinary

paint or solvent fumes that injured a bystander

♦ “Reluctant to … infinitely enlarge the scope of the

term ‘pollutants’”

39

Quadrant Corp. v. Am. States Ins. Co.

110 P.3d 733 (Wash. 2005)

♦ Tenant exposed to fumes when sealant applied to

deck

♦ Sealant composed of toxic irritants, which

unambiguously fell within definition of “pollutant”

♦ Court found it “difficult to see how a reasonable

person” could find the exclusion did not apply

40

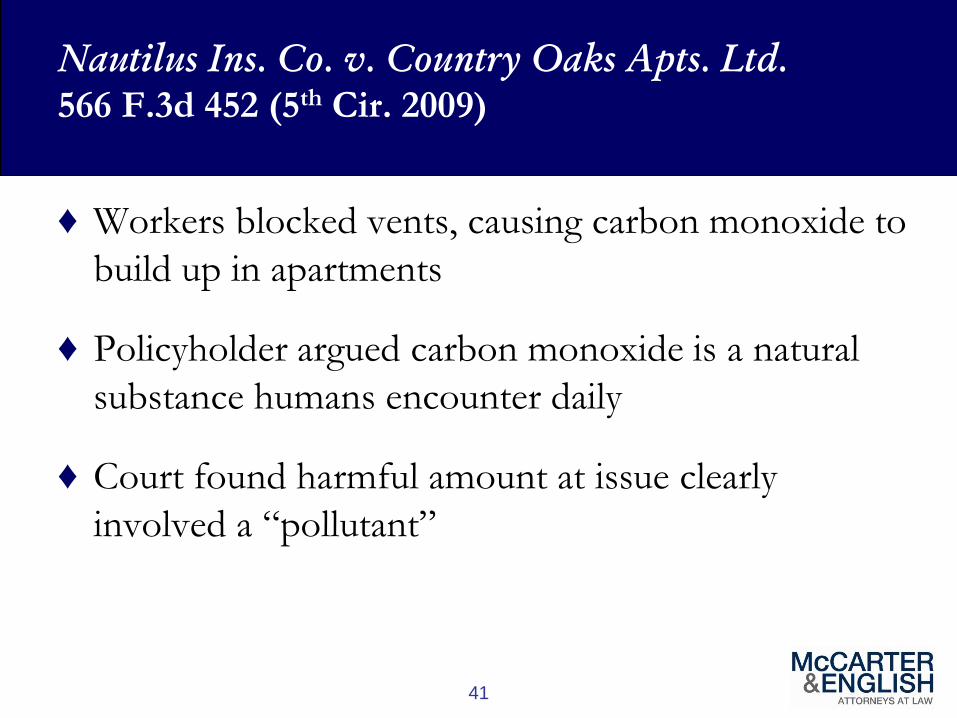

Nautilus Ins. Co. v. Country Oaks Apts. Ltd.

566 F.3d 452 (5th Cir. 2009)

♦ Workers blocked vents, causing carbon monoxide to

build up in apartments

♦ Policyholder argued carbon monoxide is a natural

substance humans encounter daily

♦ Court found harmful amount at issue clearly

involved a “pollutant”

41

Fireman’s Ins. Co. v. Kline & Son Cement Repair Inc.

474 F. Supp. 2d 779 (E.D. Va. 2007)

♦ Warehouse employee allegedly developed respiratory

problems after application of sealant to concrete

floor

♦ Definition of “pollutant” unambiguous

♦ District court found sealant was an “irritant” or

“contaminant” within definition of “pollutant”

42