PNW WOOD MARKETS - Forest Resources

42

©2016, Forest2Market, Inc. PNW WOOD MARKETS: A CLOSER LOOK AT DOMESTIC & GLOBAL EFFECTS ON OUR INDUSTRY FRA – WESTERN REGION SPRING “WORK LOCAL, THINK GLOBAL” MAY 27, 2016 SUNRIVER RESORT SUNRIVER, OREGON GREG FROHN [email protected]

Transcript of PNW WOOD MARKETS - Forest Resources

©2016, Forest2Market, Inc.

PNW WOOD MARKETS: A CLOSER LOOK AT DOMESTIC &

GLOBAL EFFECTS ON OUR INDUSTRY

FRA – WESTERN REGION SPRING “WORK LOCAL, THINK GLOBAL”

MAY 27, 2016 SUNRIVER RESORT

SUNRIVER, OREGON GREG FROHN

©2016, Forest2Market, Inc. Slide 2

TODAY’S TOPICS

1. US Housing Trends

2. The future for building with wood

3. “Softwood Lumber Agreement”

4. North American lumber production

5. The forest product export business

6. Pulp, Paper, and Pellets, a global perspective

7. Conclusion and some predictions

©2016, Forest2Market, Inc. Slide 3

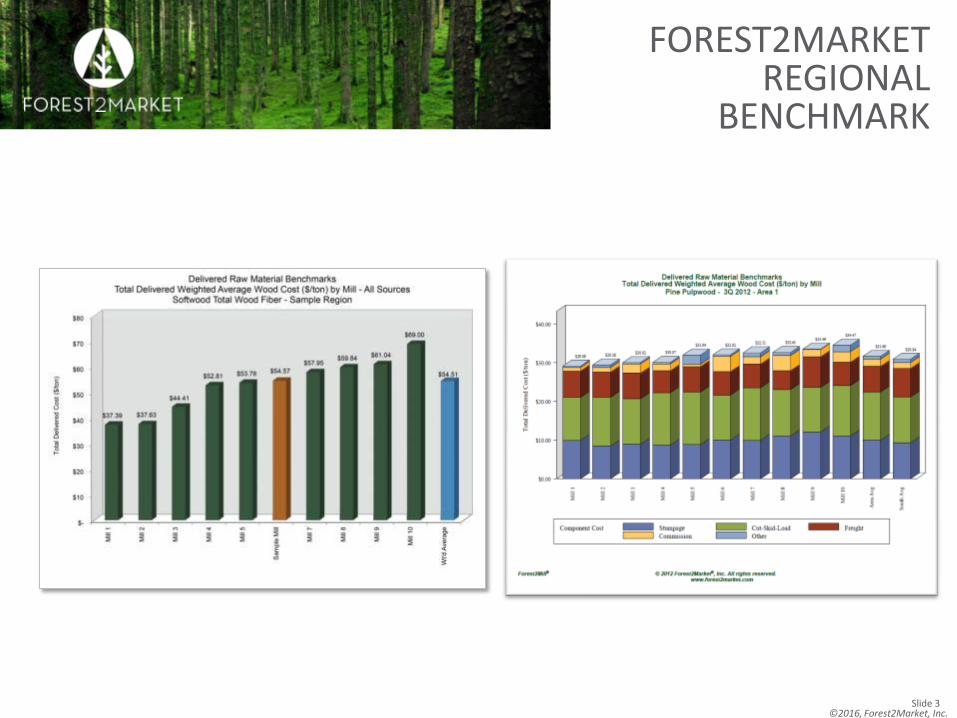

FOREST2MARKET REGIONAL

BENCHMARK

©2016, Forest2Market, Inc. Slide 4

MARKET COVERAGE

©2016, Forest2Market, Inc. Slide 5

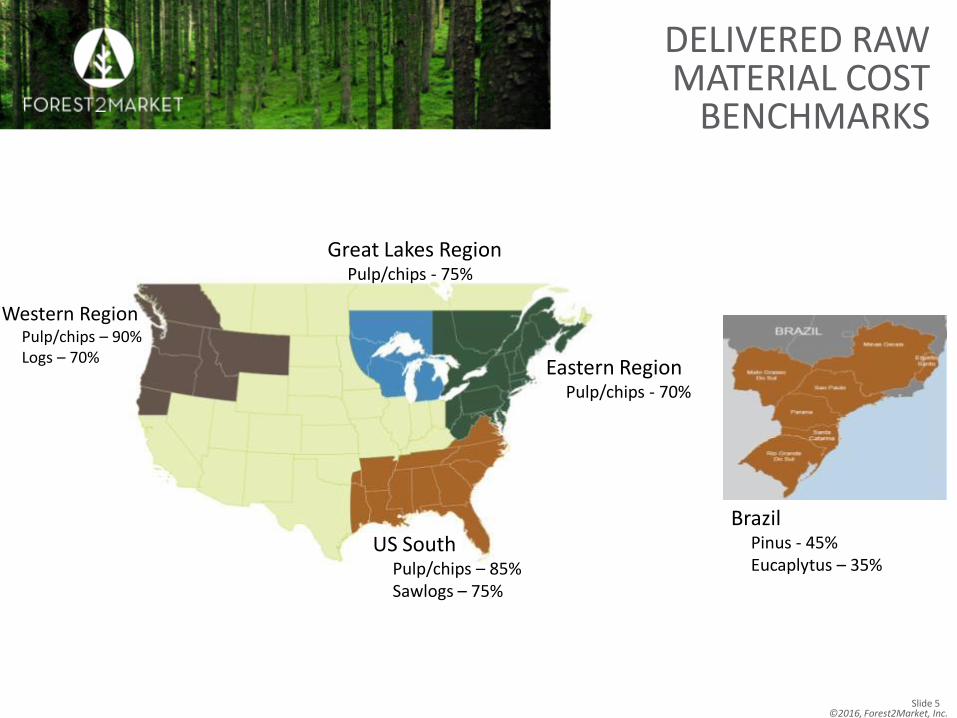

DELIVERED RAW MATERIAL COST

BENCHMARKS

Western Region Pulp/chips – 90% Logs – 70%

Great Lakes Region Pulp/chips - 75%

US South Pulp/chips – 85% Sawlogs – 75%

Brazil Pinus - 45% Eucaplytus – 35%

Eastern Region Pulp/chips - 70%

©2016, Forest2Market, Inc. Slide 6

ECONOMIC DRIVERS IN THE US FOREST

PRODUCTS INDUSTRY

WOOD IS GOOD! Le bois est bon! La madera es Buena!

©2016, Forest2Market, Inc. Slide 7

US HOUSING DRIVES NA PRODUCTION — ON THE

RISE BUT BUMPY

Source: US Census & Forest2Market

0

500

1,000

1,500

2,000

2,500

A shallow recession looms due to global economy. Real wage growth is stagnant - part time jobs. Home prices and rents are increasing. Home equity loans from subprime era linger. Conservative outlook.

©2016, Forest2Market, Inc. Slide 8

0

500

1,000

1,500

2,000

2,500

Total starts Single family Linear (Total starts) Poly. (Single family)

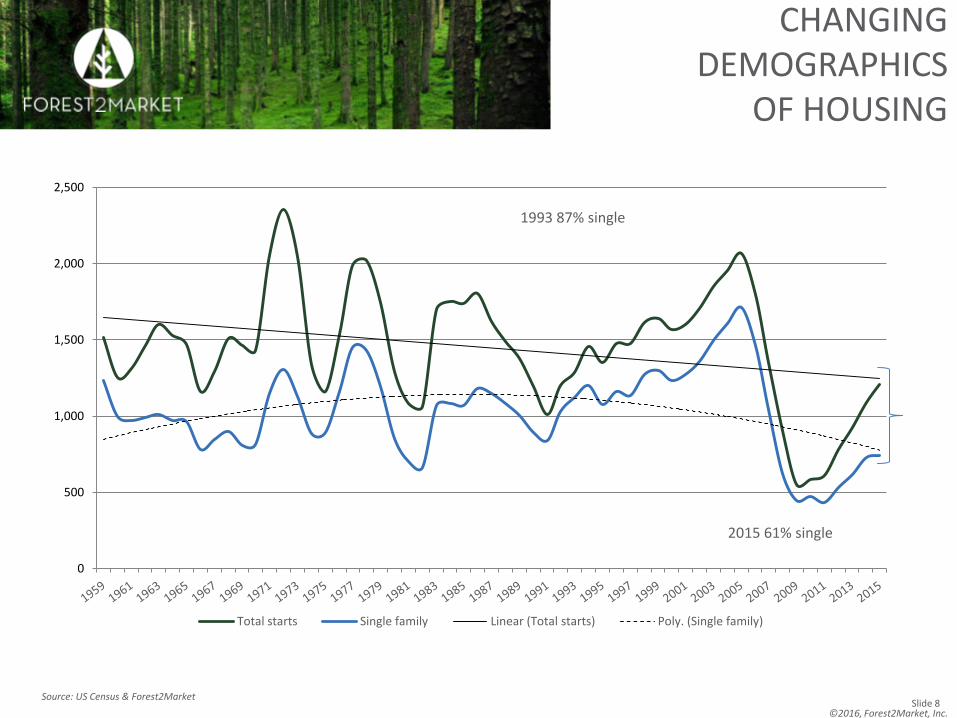

CHANGING DEMOGRAPHICS

OF HOUSING

1993 87% single

2015 61% single

Source: US Census & Forest2Market

©2016, Forest2Market, Inc. Slide 9

HOUSING THE MILLENNIALS:

92 MILLION BETWEEN 15-35

• Peak home buying years: 25-45 years

• Marriage (averages)

• 1970: 23 years old

• 2010: 30 years old

• Married and own a home (18-31 years)

• 1968: 56%

• 1981: 43%

• 2012: 23%

• Urban Centric

• 93% want to own their own homes, but the financials may not make sense:

• 41% work full-time

• 50% have less than $5,000 in savings

• Average student loan debt $33,000

©2016, Forest2Market, Inc. Slide 10

WHO’S DRIVING WHAT?

©2016, Forest2Market, Inc. Slide 11

KEY ECONOMIC INDICATORS ARE

IMPROVING

©2016, Forest2Market, Inc. Slide 12

NORTH AMERICAN LUMBER PRODUCTION

TOPICS

©2016, Forest2Market, Inc. Slide 13

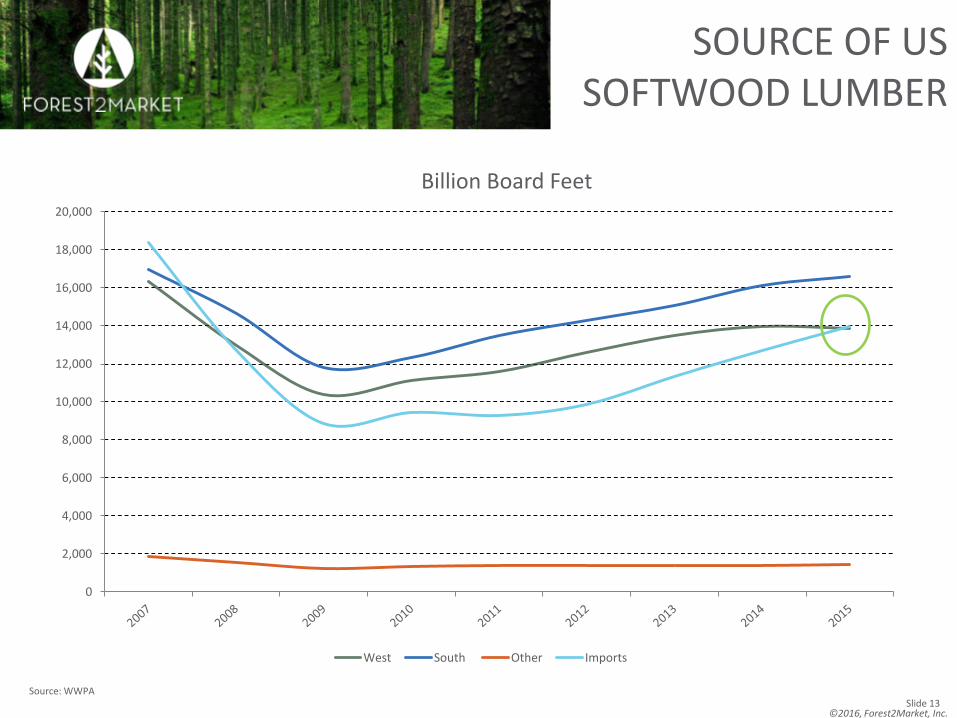

SOURCE OF US SOFTWOOD LUMBER

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

West South Other Imports

Source: WWPA

Billion Board Feet

©2016, Forest2Market, Inc. Slide 14

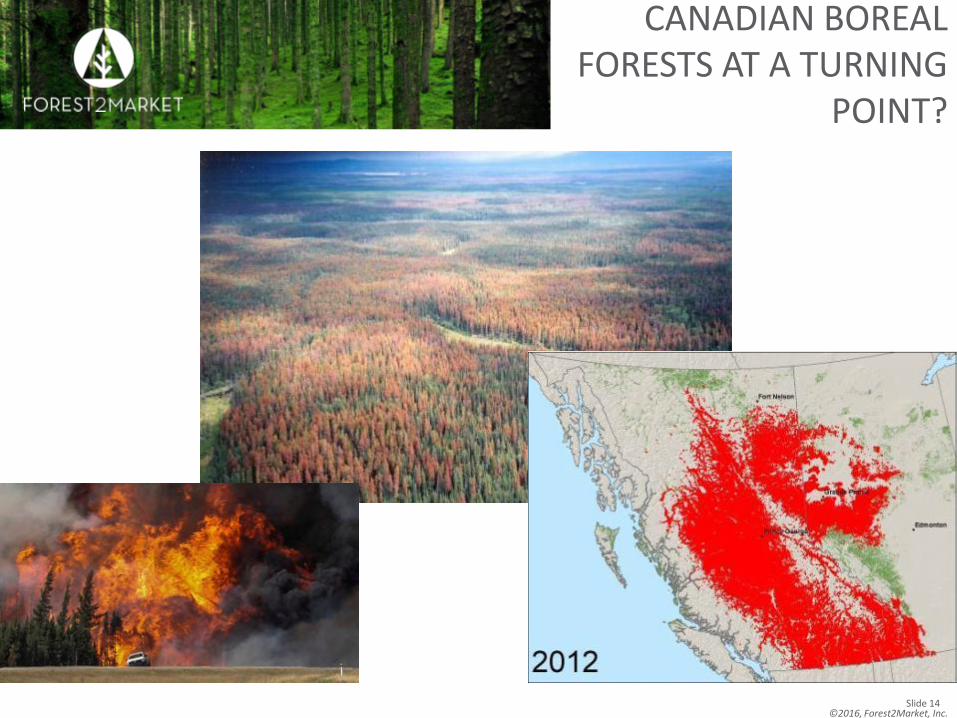

CANADIAN BOREAL FORESTS AT A TURNING

POINT?

©2016, Forest2Market, Inc. Slide 15

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

BC prod BC imports East Canada prod East Canada imports

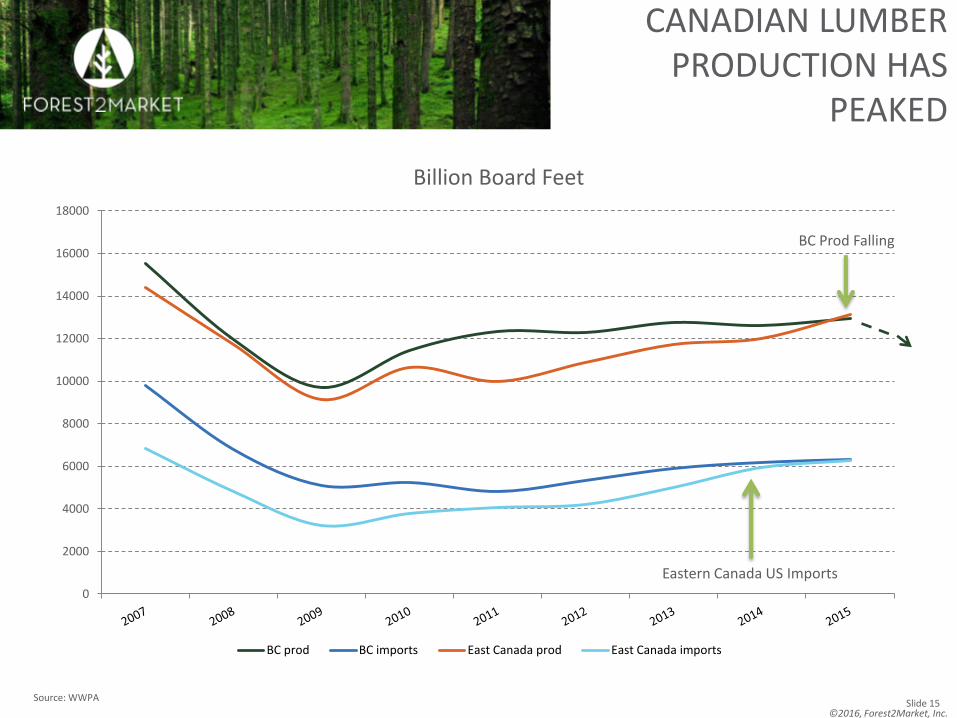

CANADIAN LUMBER PRODUCTION HAS

PEAKED

BC Prod Falling

Eastern Canada US Imports

Source: WWPA

Billion Board Feet

©2016, Forest2Market, Inc. Slide 16

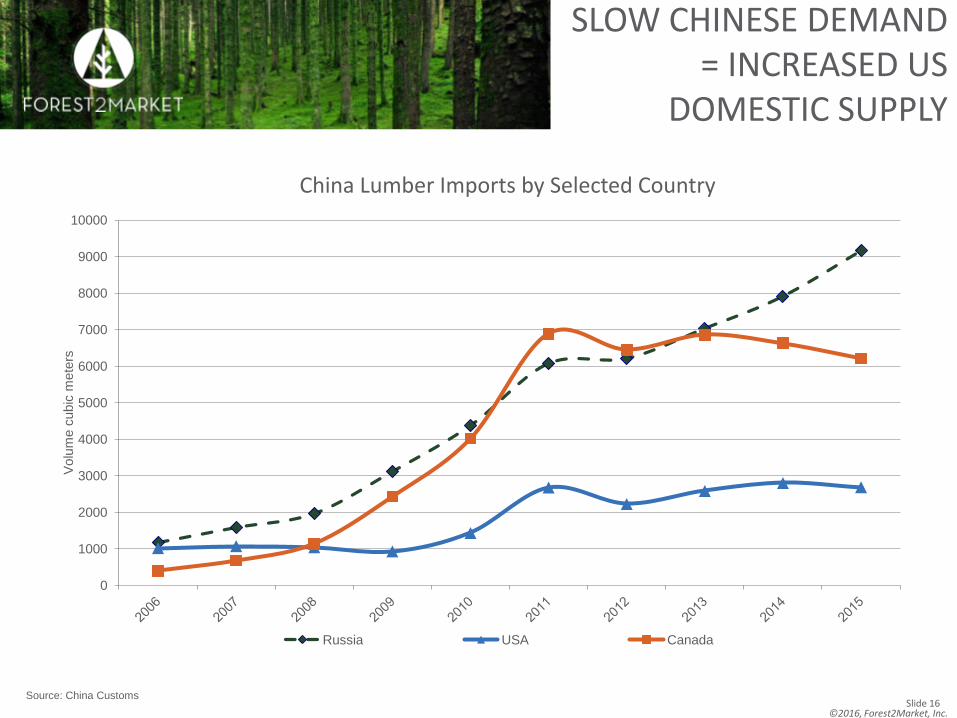

SLOW CHINESE DEMAND = INCREASED US

DOMESTIC SUPPLY

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Volu

me c

ubic

mete

rs

China Lumber Imports by Selected Country

Russia USA Canada

Source: China Customs

©2016, Forest2Market, Inc. Slide 17

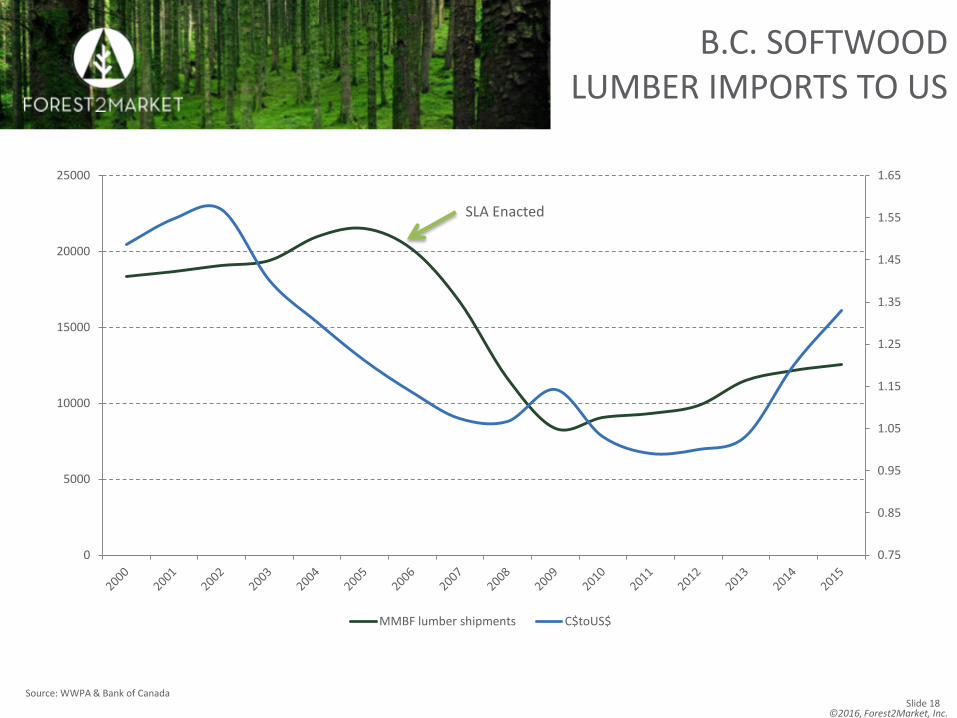

SLA SUMMARY

• Adopted in 2006, the result of a disagreement over whether Canadian stumpage pricing process constituted an unfair subsidy that disadvantaged the US lumber industry.

• SLA expired in October 2015.

• What has changed? Mountain pine beetle infestation in BC, Canadian producers supply China’s demand for wood products, Canadian industry now owns a large stake in US lumber production.

• Strong US $ makes Canadian lumber imports attractive.

• As demand from China falls, US producers have been concerned about a “wall of wood” from across the border. So far in 2016 CDN import volume is up significantly

• Canadian producers see new trade restrictions as an unnecessary intrusion on free trade, an effort to prop up values of US private forests and fear further duties could be retroactive.

• Not much progress since PM Trudeau’s White House visit in April

©2016, Forest2Market, Inc. Slide 18

0.75

0.85

0.95

1.05

1.15

1.25

1.35

1.45

1.55

1.65

0

5000

10000

15000

20000

25000

MMBF lumber shipments C$toUS$

B.C. SOFTWOOD LUMBER IMPORTS TO US

Source: WWPA & Bank of Canada

SLA Enacted

©2016, Forest2Market, Inc. Slide 19

US PACIFIC NORTHWEST EXPORT/DOMESTIC

©2016, Forest2Market, Inc. Slide 20

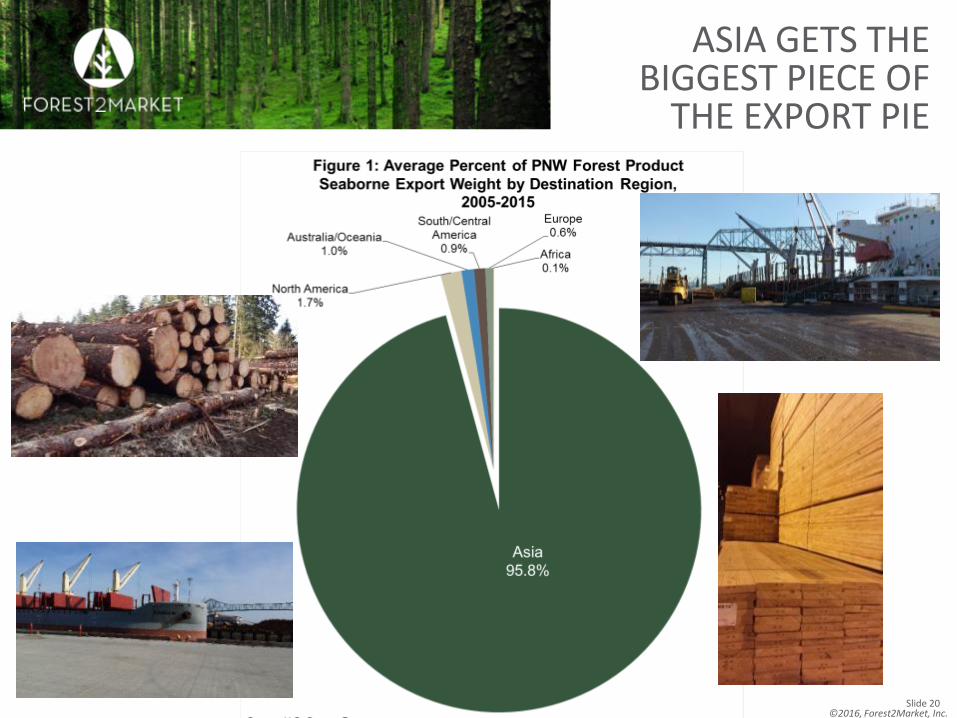

ASIA GETS THE BIGGEST PIECE OF

THE EXPORT PIE

©2016, Forest2Market, Inc. Slide 21

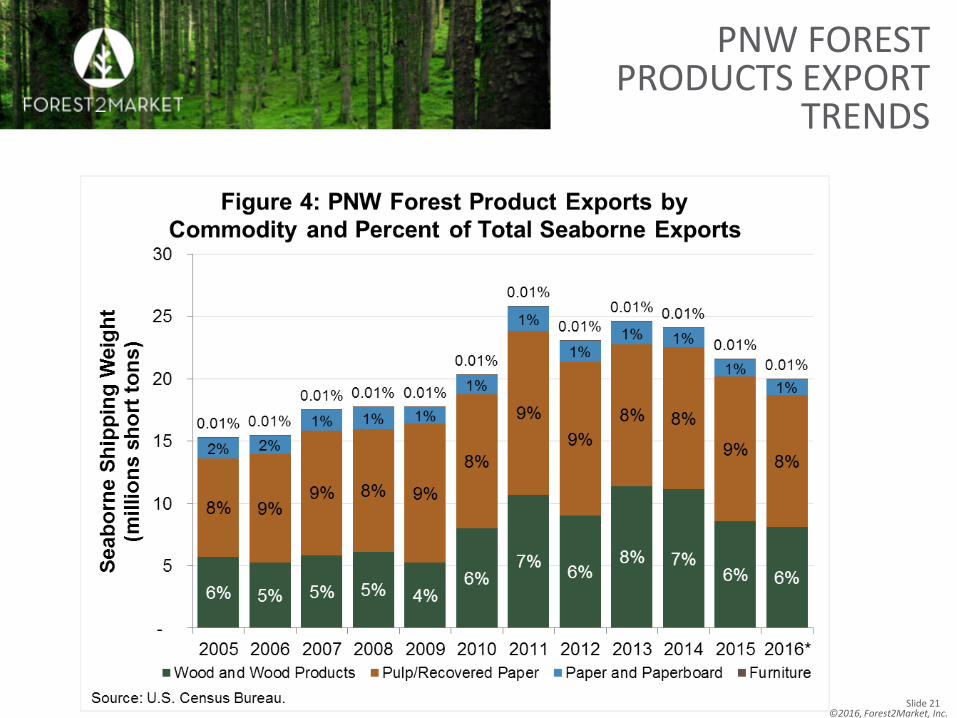

PNW FOREST PRODUCTS EXPORT

TRENDS

©2016, Forest2Market, Inc. Slide 22

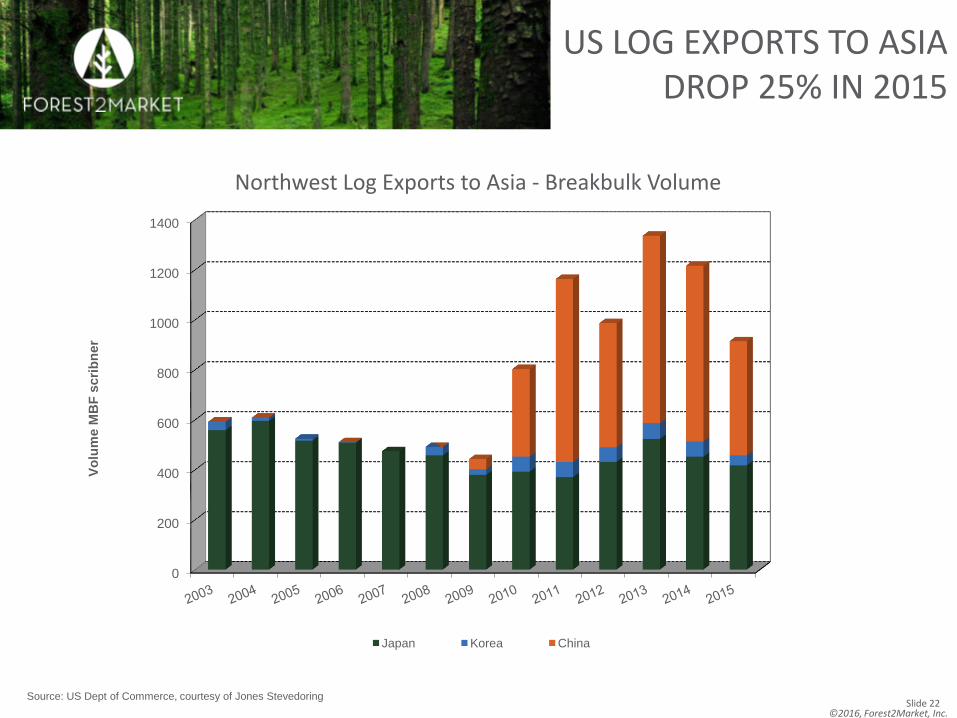

US LOG EXPORTS TO ASIA DROP 25% IN 2015

0

200

400

600

800

1000

1200

1400

Vo

lum

e M

BF

scri

bn

er

Northwest Log Exports to Asia - Breakbulk Volume

Japan Korea China

Source: US Dept of Commerce, courtesy of Jones Stevedoring

©2016, Forest2Market, Inc.

©2016, Forest2Market, Inc. Slide 24

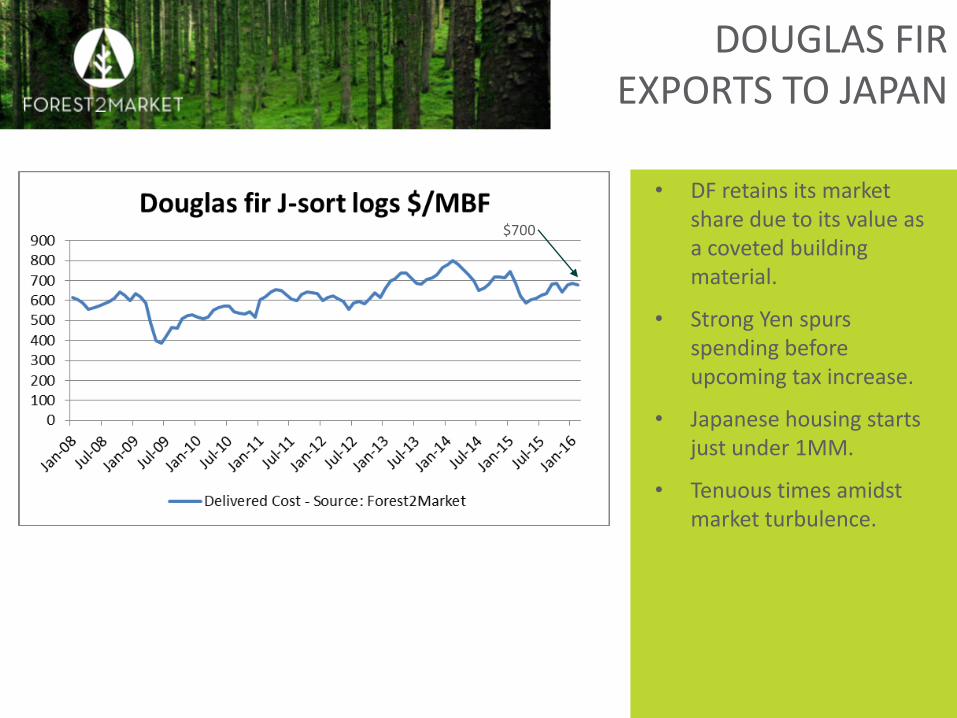

DOUGLAS FIR EXPORTS TO JAPAN

• DF retains its market share due to its value as a coveted building material.

• Strong Yen spurs spending before upcoming tax increase.

• Japanese housing starts just under 1MM.

• Tenuous times amidst market turbulence.

$700

©2016, Forest2Market, Inc. Slide 25

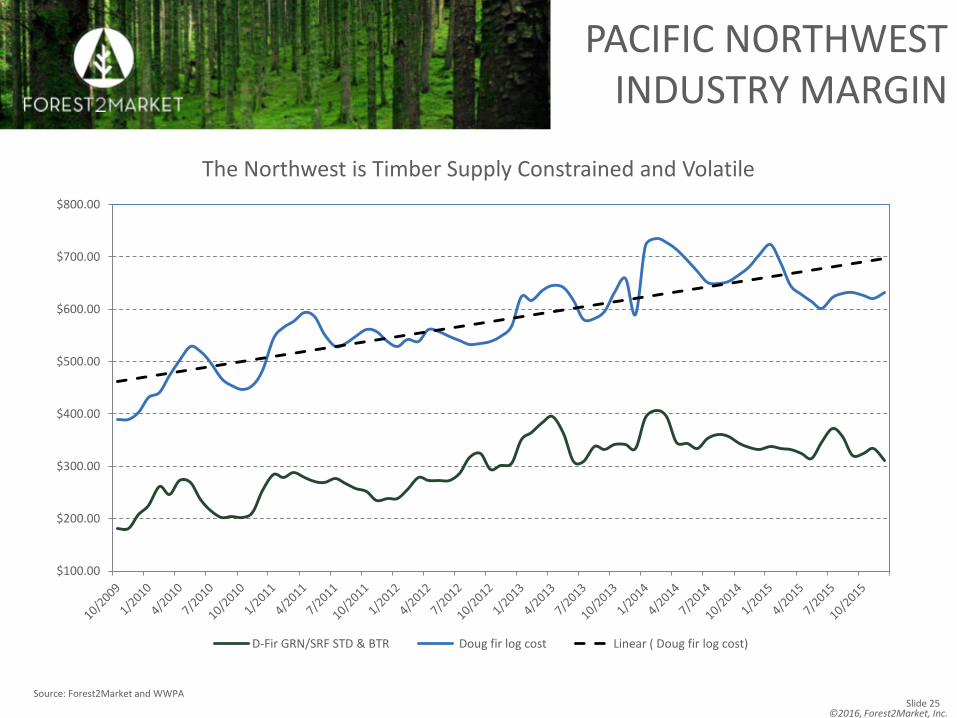

PACIFIC NORTHWEST INDUSTRY MARGIN

$100.00

$200.00

$300.00

$400.00

$500.00

$600.00

$700.00

$800.00

D-Fir GRN/SRF STD & BTR Doug fir log cost Linear ( Doug fir log cost)

Source: Forest2Market and WWPA

The Northwest is Timber Supply Constrained and Volatile

©2016, Forest2Market, Inc. Slide 26

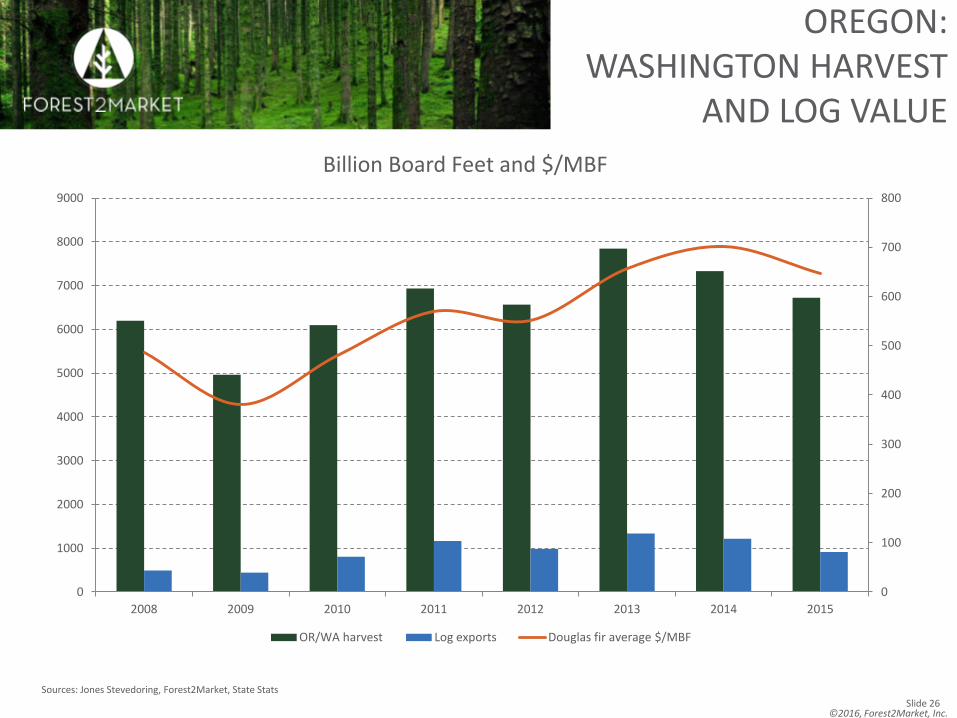

OREGON: WASHINGTON HARVEST

AND LOG VALUE

0

100

200

300

400

500

600

700

800

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2008 2009 2010 2011 2012 2013 2014 2015

OR/WA harvest Log exports Douglas fir average $/MBF

Billion Board Feet and $/MBF

Sources: Jones Stevedoring, Forest2Market, State Stats

©2016, Forest2Market, Inc. Slide 27

US SOUTHERN PINE MOSTLY A DOMESTIC

INFLUENCE

©2016, Forest2Market, Inc. Slide 28

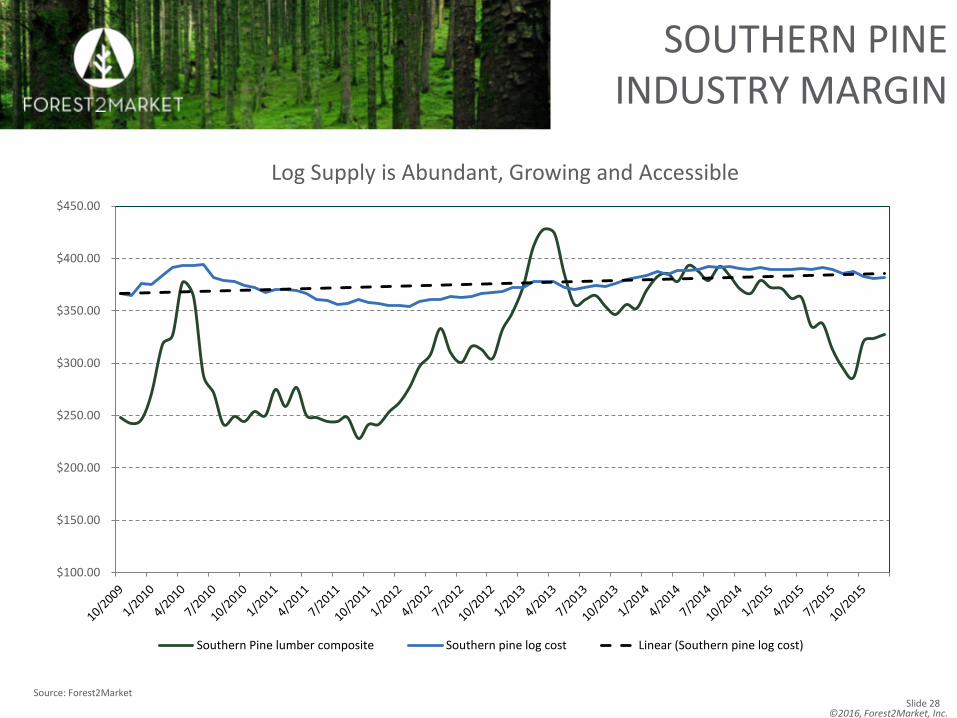

SOUTHERN PINE INDUSTRY MARGIN

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$450.00

Southern Pine lumber composite Southern pine log cost Linear (Southern pine log cost)

Source: Forest2Market

Log Supply is Abundant, Growing and Accessible

©2016, Forest2Market, Inc. Slide 29

SOUTHERN FORESTRY & AGRICULTURE

©2016, Forest2Market, Inc. Slide 30

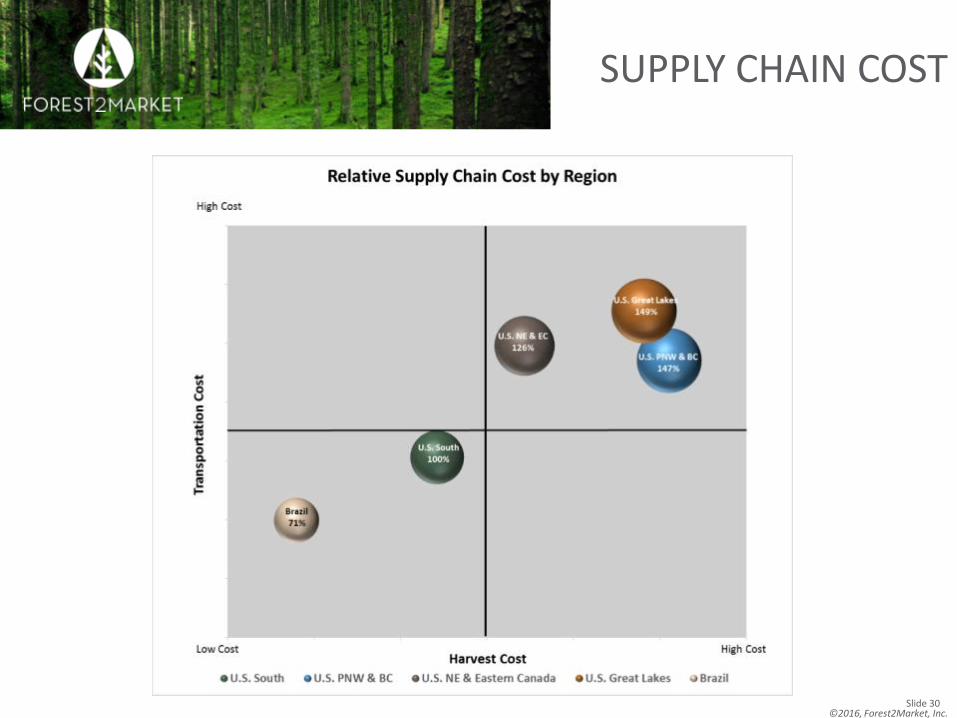

SUPPLY CHAIN COST

©2016, Forest2Market, Inc. Slide 31

CANADIAN INVESTMENT IN SOUTHERN PINE

SAWMILLS

$0

$100

$200

$300

$400

$500

$600

$700

$800 Ja

n-0

8

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

DF Westside Domestic SYP MBF Linear (DF Westside Domestic)

Source: Forest2Market

DF to SYP Pricing Volatility

©2016, Forest2Market, Inc. Slide 32

CANADIAN FOREST INDUSTRY MOVES

SOUTH

• The Southern US pine region has abundant, low cost timber from productive, well managed private forests.

• Canfor, West Fraser and Interfor, leading Canadian forest products companies, hedge their bets, moving out of Beetle kill into more lucrative business environment.

• 35 SYP sawmills in Texas, Arkansas, Louisiana, Mississippi, Alabama, Georgia, South Carolina, North Carolina and Florida are now owned by these three companies.

• 4.5 billion board feet of production capacity, mostly framing lumber. Studs remain a NW and Northern product due to strength characteristics.

• Roughly half of 2015’s housing starts were in the South.

©2016, Forest2Market, Inc. Slide 33

PULP & PAPER and… PELLETS?

©2016, Forest2Market, Inc. Slide 34

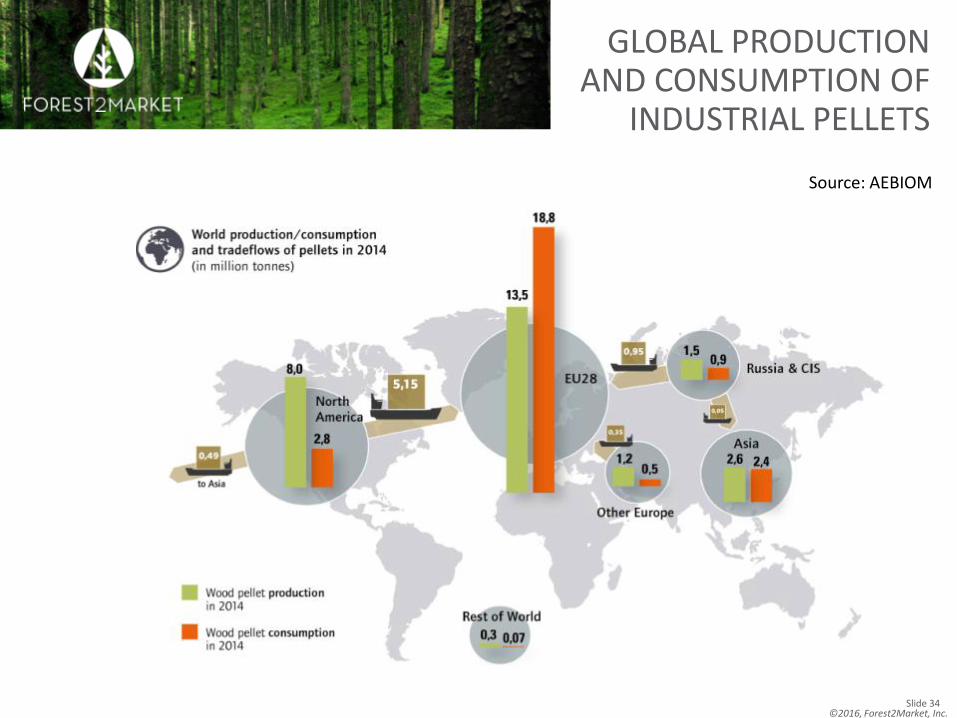

GLOBAL PRODUCTION AND CONSUMPTION OF

INDUSTRIAL PELLETS

Source: AEBIOM

©2016, Forest2Market, Inc. Slide 35

Growing Bioenergy Demand in Asia

Japan will strive to replace nuclear power generation with more sustainable bio-energy in the future • Plant size will be in the 50 MW range • Feedstock procurement will be from green certified

production sources • Focus will be on more sustainable long term supply

contracts

Korea currently has less stringent environmental constraints • Currently this allows them to source much cheaper pellets from un-certified sources

such as Vietnam. • Focus more towards “spot market” supply chain metrics

©2016, Forest2Market, Inc.

©2016, Forest2Market, Inc. Slide 37

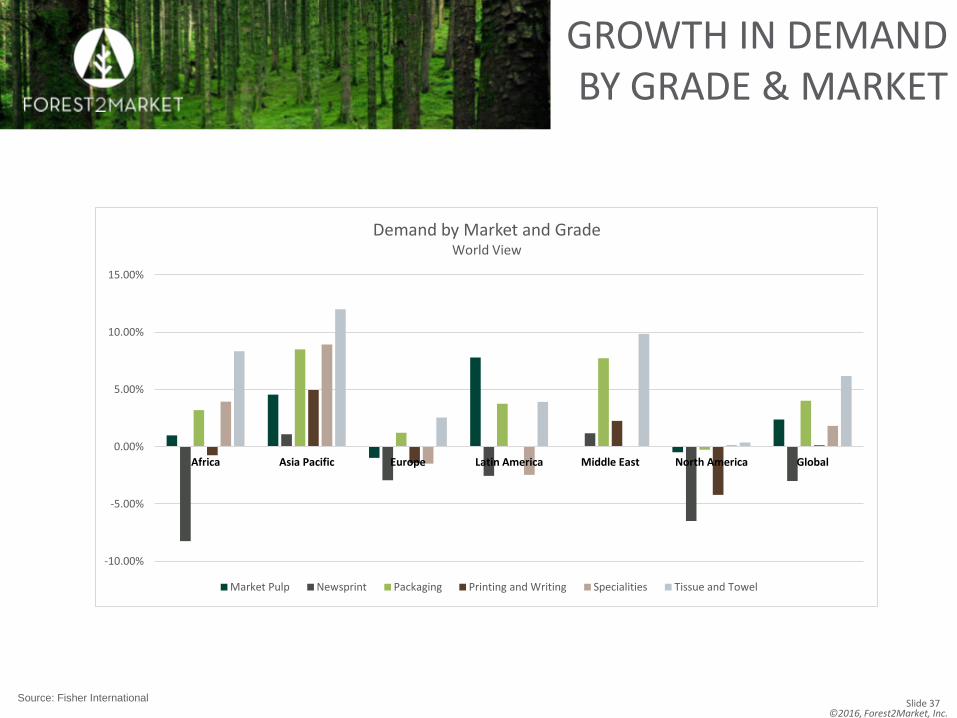

GROWTH IN DEMAND BY GRADE & MARKET

Source: Fisher International

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Africa Asia Pacific Europe Latin America Middle East North America Global

Demand by Market and Grade World View

Market Pulp Newsprint Packaging Printing and Writing Specialities Tissue and Towel

©2016, Forest2Market, Inc. Slide 38

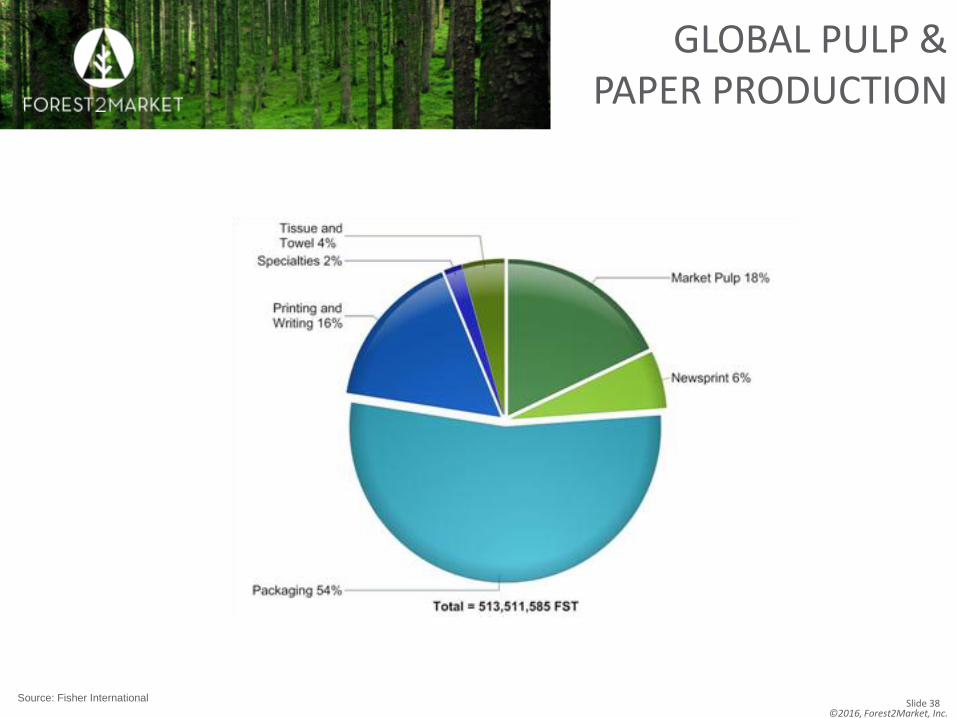

GLOBAL PULP & PAPER PRODUCTION

Source: Fisher International

©2016, Forest2Market, Inc. Slide 39

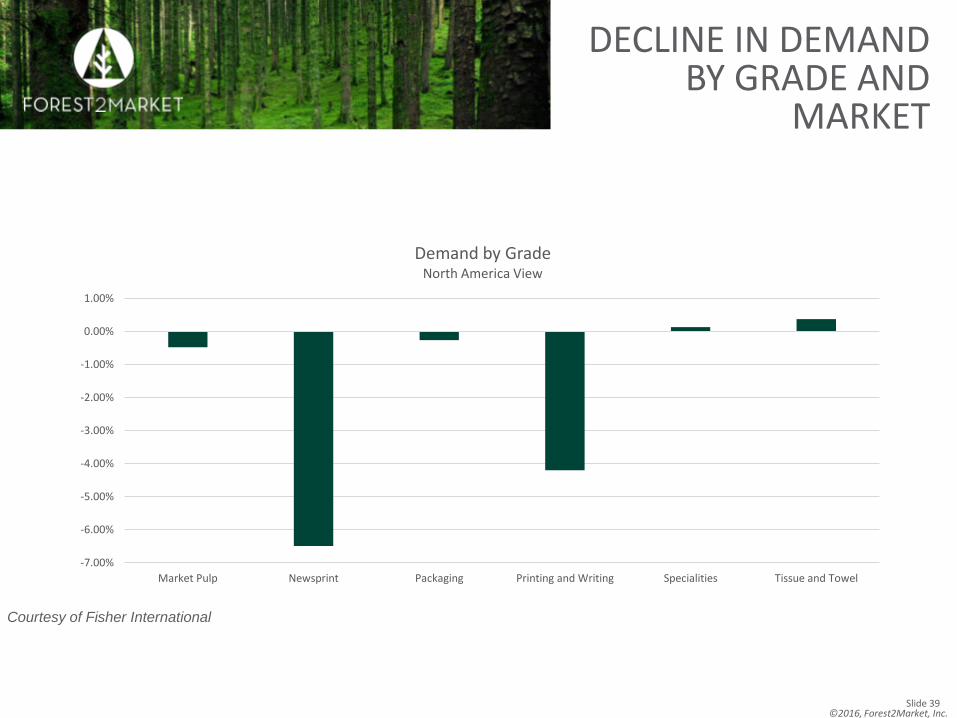

DECLINE IN DEMAND BY GRADE AND

MARKET

-7.00%

-6.00%

-5.00%

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

Market Pulp Newsprint Packaging Printing and Writing Specialities Tissue and Towel

Demand by Grade North America View

Courtesy of Fisher International

©2016, Forest2Market, Inc. Slide 40

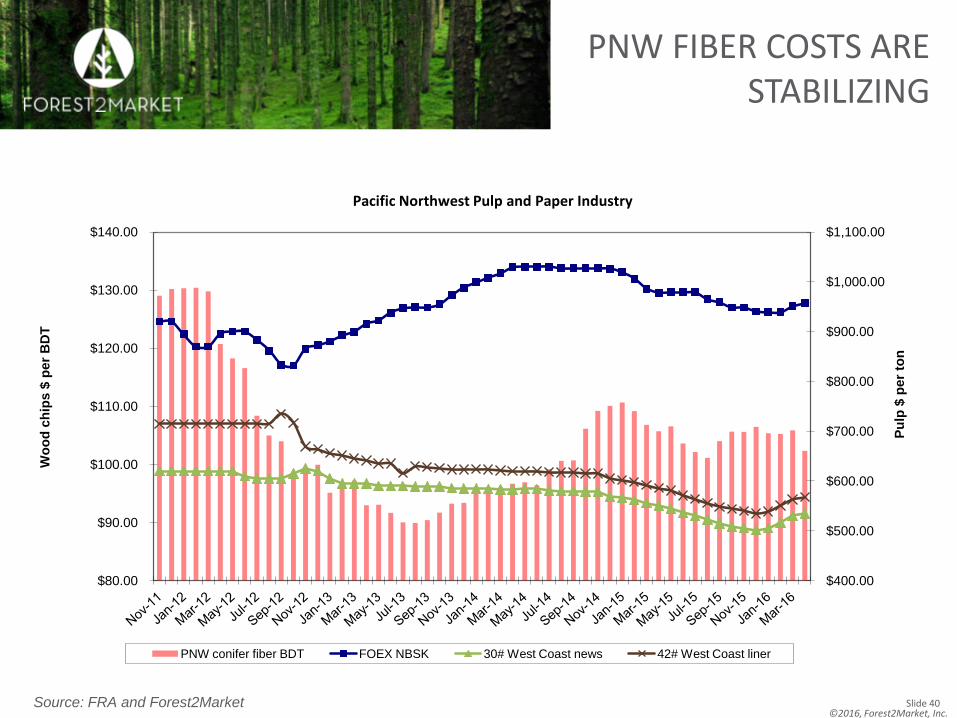

PNW FIBER COSTS ARE STABILIZING

Source: FRA and Forest2Market

$400.00

$500.00

$600.00

$700.00

$800.00

$900.00

$1,000.00

$1,100.00

$80.00

$90.00

$100.00

$110.00

$120.00

$130.00

$140.00

Pu

lp $

per

ton

Wo

od

ch

ips $

per

BD

T

PNW conifer fiber BDT FOEX NBSK 30# West Coast news 42# West Coast liner

Pacific Northwest Pulp and Paper Industry

©2016, Forest2Market, Inc. Slide 41

CONCLUDING THOUGHTS

• Slow but steady recovery for the US housing market

• Low interest rates, cheap fuel and yet a sluggish economy

• Potential for multi-level building with wood will continue

• Watch for additional mill closures and/or consolidation to continue as PNW log supply is constrained

• As British Columbia Interior production and exports decline — opportunity for the PNW-US to fill the gap. In the meantime, lumber will flow from Canada.

• Major growth in the Southern US pine industry underway

• Continuing influence of strong US $ on wood imports and exports

• Less demand for NA wood products in China = more supply and competition into domestic lumber markets

• Western harvest levels flat in near-term though harvests increase as housing and exports increase; fire mitigation efforts will open new fiber supply opportunity

• At the end of the day, the PNW — still the most sought after source of sustainable high quality conifer and hardwood products locally, regionally and globally!!!

©2016, Forest2Market, Inc. Slide 42

Forest2Market: The highest quality wood raw material analysis available

Greg Frohn Manager, PNW Market Sales Hayden Lake, ID +1.360.477.6242 [email protected]

Forest2Market

15720 Brixham Hill Ave

Suite 550

Charlotte, NC 28277

CONTACT