Planning and Budgeting Tools Andrew Graham School of Policy Studies Queens University MPA 827 2015.

80

Planning and Budgeting Tools Andrew Graham Andrew Graham School of Policy Studies School of Policy Studies Queens University Queens University MPA 827 2015 MPA 827 2015

-

Upload

madlyn-beasley -

Category

Documents

-

view

220 -

download

0

Transcript of Planning and Budgeting Tools Andrew Graham School of Policy Studies Queens University MPA 827 2015.

Planning and Budgeting Tools

Andrew GrahamAndrew GrahamSchool of Policy StudiesSchool of Policy Studies

Queens UniversityQueens UniversityMPA 827 2015MPA 827 2015

2

Today Building budget success Business case development Capital budgeting Cost behaviour Cost benefit and the cost benefit thereof Time value of money or temporal shell game

3

So, you need more money, So, you need more money, staff and equipmentstaff and equipment You understand how the budget is set You understand how the budget is set

in the your organizationin the your organization You have some ideas that would really You have some ideas that would really

improve things (so do your improve things (so do your colleagues, but the way)colleagues, but the way)

Your managers have to sort out these Your managers have to sort out these ideas and weight them against what ideas and weight them against what they have and what they can sellthey have and what they can sell

4

How Priorities are SetHow Priorities are Set

Bottom up and top down: what are the Bottom up and top down: what are the elements of this process?elements of this process?

5

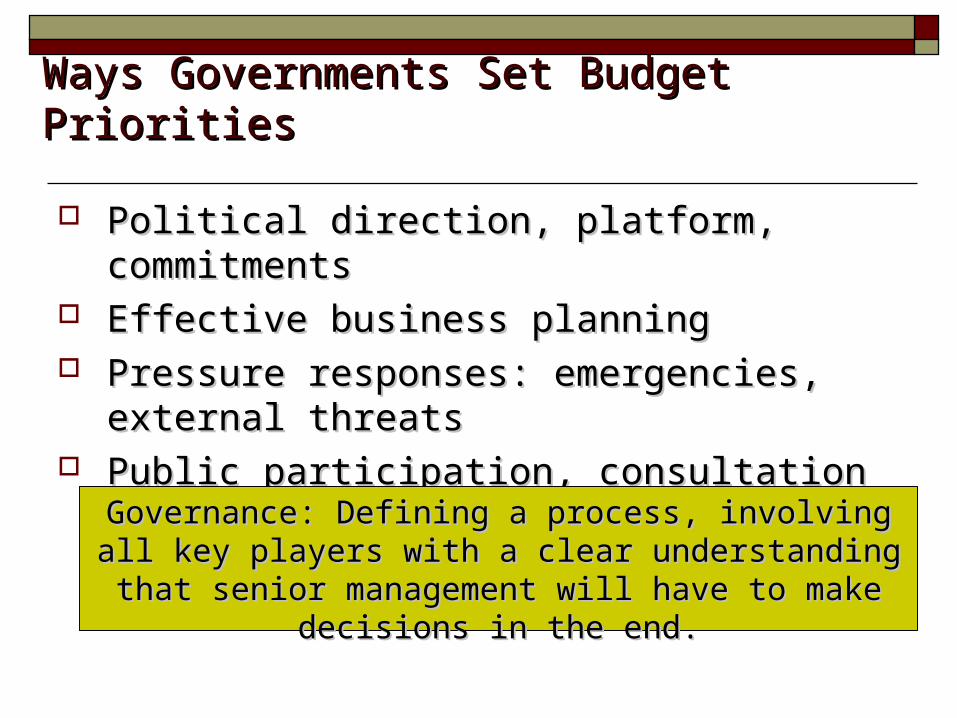

Ways Governments Set Budget Ways Governments Set Budget PrioritiesPriorities

Political direction, platform, commitmentsPolitical direction, platform, commitments Effective business planningEffective business planning Pressure responses: emergencies, Pressure responses: emergencies,

external threatsexternal threats Public participation, consultationPublic participation, consultation

6

Governance: Defining a process, involving all key Governance: Defining a process, involving all key players with a clear understanding that senior players with a clear understanding that senior

management will have to make decisions in the management will have to make decisions in the end.end.

Key Drivers for Budget IncreasesKey Drivers for Budget Increases External forces: External forces:

Legal requirementsLegal requirements Political imperatives: more cops on the Political imperatives: more cops on the

streetstreet Collective bargaining – salary costsCollective bargaining – salary costs New standardsNew standards Population growth – do you have an Population growth – do you have an

established formula?established formula? Technology and equipment turnoverTechnology and equipment turnover

7

Various approaches to the budget process……

8

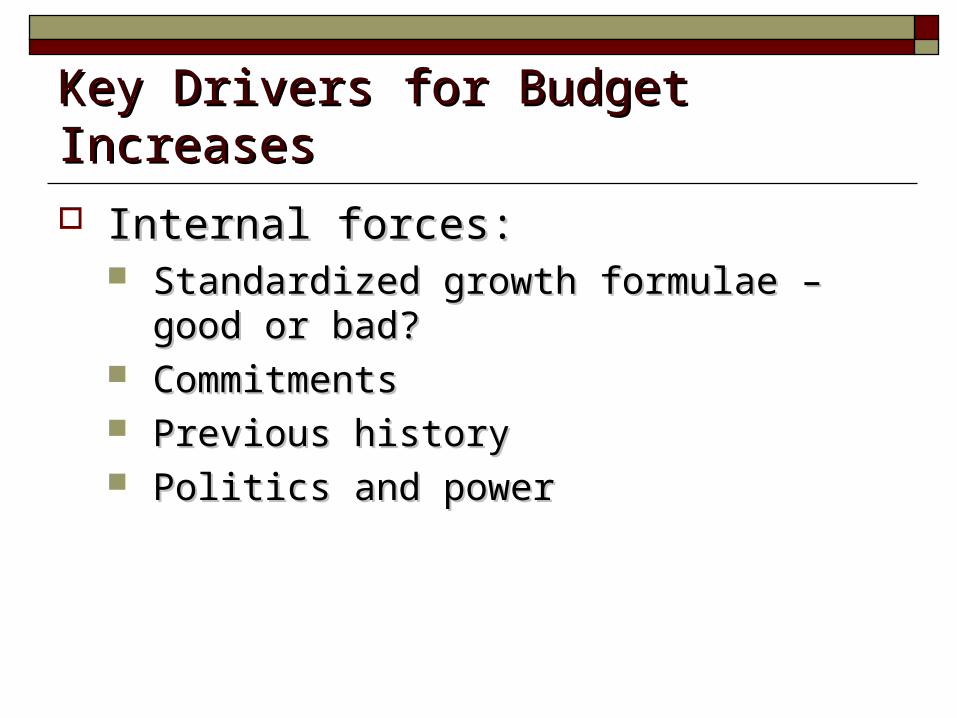

Key Drivers for Budget IncreasesKey Drivers for Budget Increases Internal forces: Internal forces:

Standardized growth formulae – good Standardized growth formulae – good or bad?or bad?

CommitmentsCommitments Previous historyPrevious history Politics and powerPolitics and power

9

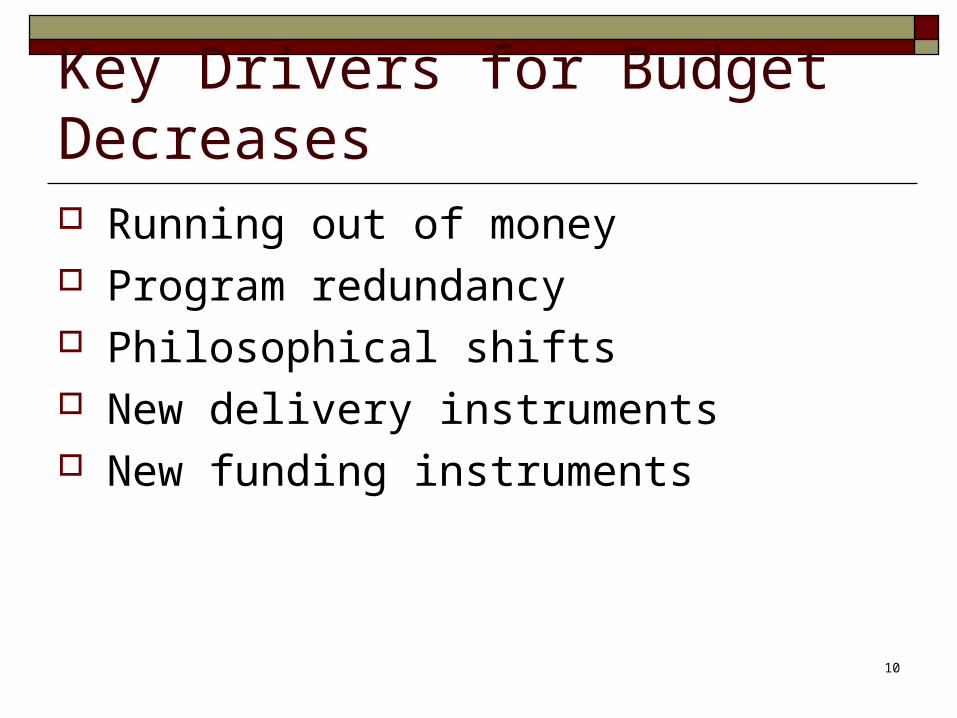

Key Drivers for Budget Decreases Running out of money Program redundancy Philosophical shifts New delivery instruments New funding instruments

10

Defining Budget SuccessDefining Budget Success Is it just getting more money?Is it just getting more money? Other factors come into play as Other factors come into play as

competition for scarce resources competition for scarce resources never endsnever ends

One time win can create One time win can create downstream costs. How?downstream costs. How?

There is always a tomorrow.There is always a tomorrow.

11

Elements of Success: Elements of Success: InternalInternal Good planningGood planning Building strategic linkageBuilding strategic linkage Knowing how the systems works – Knowing how the systems works –

formal and informalformal and informal Building a constituency and Building a constituency and

coalitions – getting the corporate/ coalitions – getting the corporate/ financial and senior management on financial and senior management on sideside

12

Elements of Success: Elements of Success: InternalInternal Doing your homeworkDoing your homework Understanding alternative delivery Understanding alternative delivery

optionsoptions Good understanding of cost and cost Good understanding of cost and cost

driversdrivers Building a good business case as a tool Building a good business case as a tool

not an end in itselfnot an end in itself Creating a distinctive productCreating a distinctive product Take a mature time perspectiveTake a mature time perspective

13

Business Cases

14

Building the Case: Why? To demonstrate the strategic alignment and

sense of urgency of the project in question. (Does this project make sense?)

To define the scope of the proposed project. To show the financial and operational benefits

associated with the proposed project.

15

A good business case or proposal should serve as the foundation for an implementation plan or roadmap.

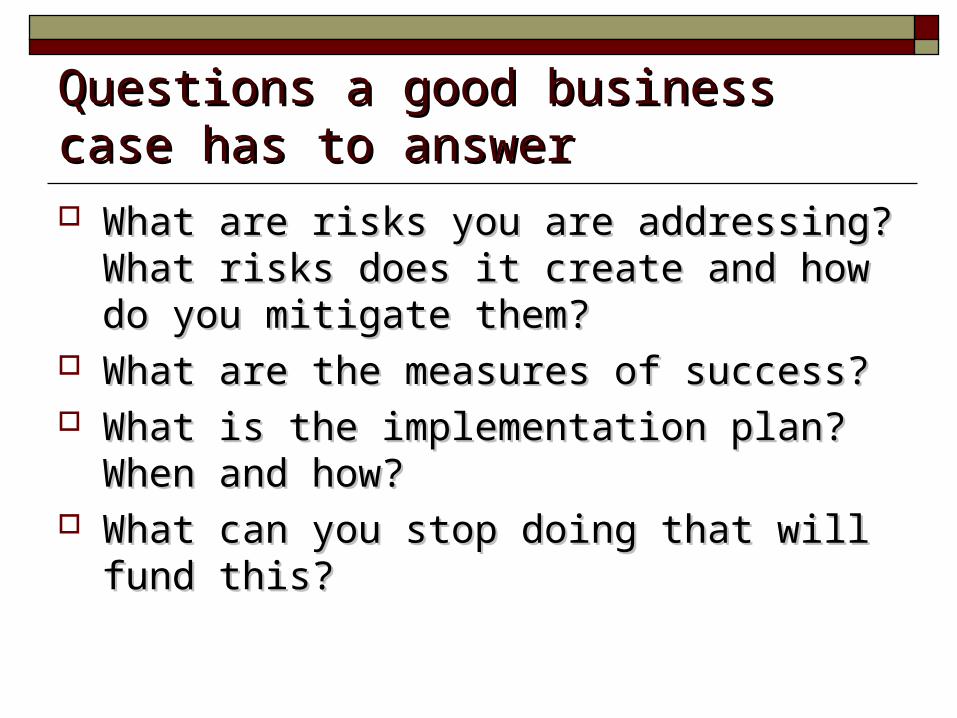

Questions a good business Questions a good business case has to answercase has to answer What exactly do you want to do?What exactly do you want to do? How does it link to what we want to do?How does it link to what we want to do? What is the history behind this idea, how What is the history behind this idea, how

does it link to what is happening now, does it link to what is happening now, what we have tried before?what we have tried before?

How much will it cost? Are these costs How much will it cost? Are these costs fully inclusive and for how long?fully inclusive and for how long?

16

Questions a good business case Questions a good business case has to answerhas to answer What are risks you are addressing? What are risks you are addressing?

What risks does it create and how do What risks does it create and how do you mitigate them?you mitigate them?

What are the measures of success?What are the measures of success? What is the implementation plan? What is the implementation plan?

When and how?When and how? What can you stop doing that will What can you stop doing that will

fund this? fund this? 17

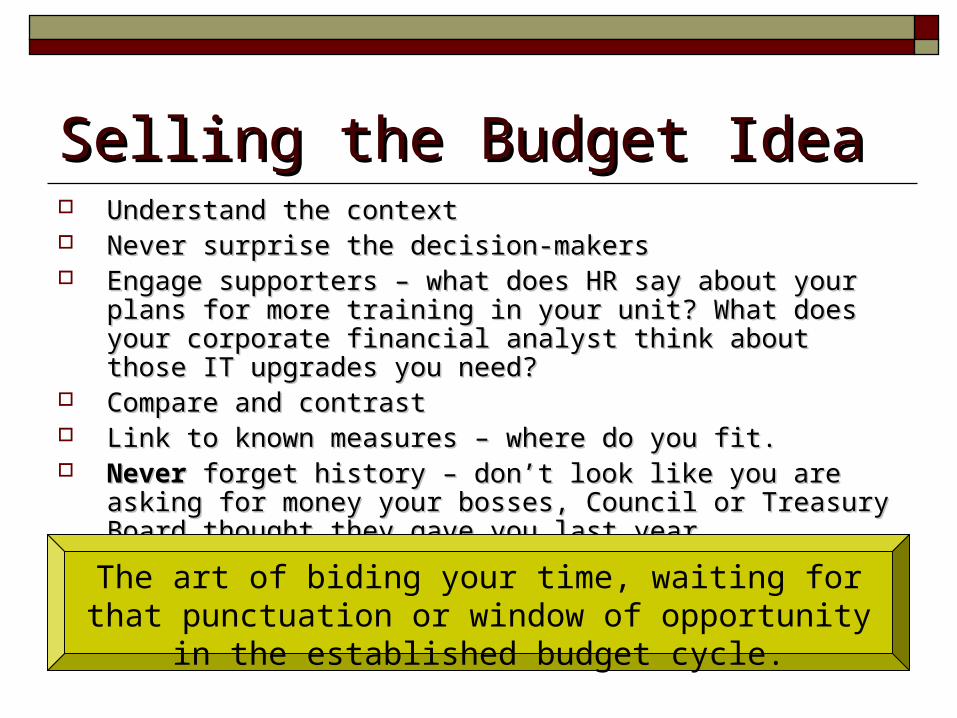

Selling the Budget IdeaSelling the Budget Idea Understand the contextUnderstand the context Never surprise the decision-makersNever surprise the decision-makers Engage supporters – what does HR say about your plans Engage supporters – what does HR say about your plans

for more training in your unit? What does your corporate for more training in your unit? What does your corporate financial analyst think about those IT upgrades you need?financial analyst think about those IT upgrades you need?

Compare and contrastCompare and contrast Link to known measures – where do you fit.Link to known measures – where do you fit. NeverNever forget history – don forget history – don’’t look like you are asking for t look like you are asking for

money your bosses, Council or Treasury Board thought money your bosses, Council or Treasury Board thought they gave you last year they gave you last year

18

The art of biding your time, waiting for that punctuation or window of opportunity in the established budget cycle.

Fault Lines and Dangers for the Fault Lines and Dangers for the Budget AdvocateBudget Advocate Avoid one-time money that creates long-term Avoid one-time money that creates long-term

commitmentscommitments Check the conditions of approvalsCheck the conditions of approvals What makes sense to you may be nonsense to What makes sense to you may be nonsense to

others.others. Assume that the business case sells itselfAssume that the business case sells itself Overpromising – you may be fooling yourselfOverpromising – you may be fooling yourself Track record Track record Threats and wolf cryingThreats and wolf crying

19

Be careful about what you agree to do to get more funds.

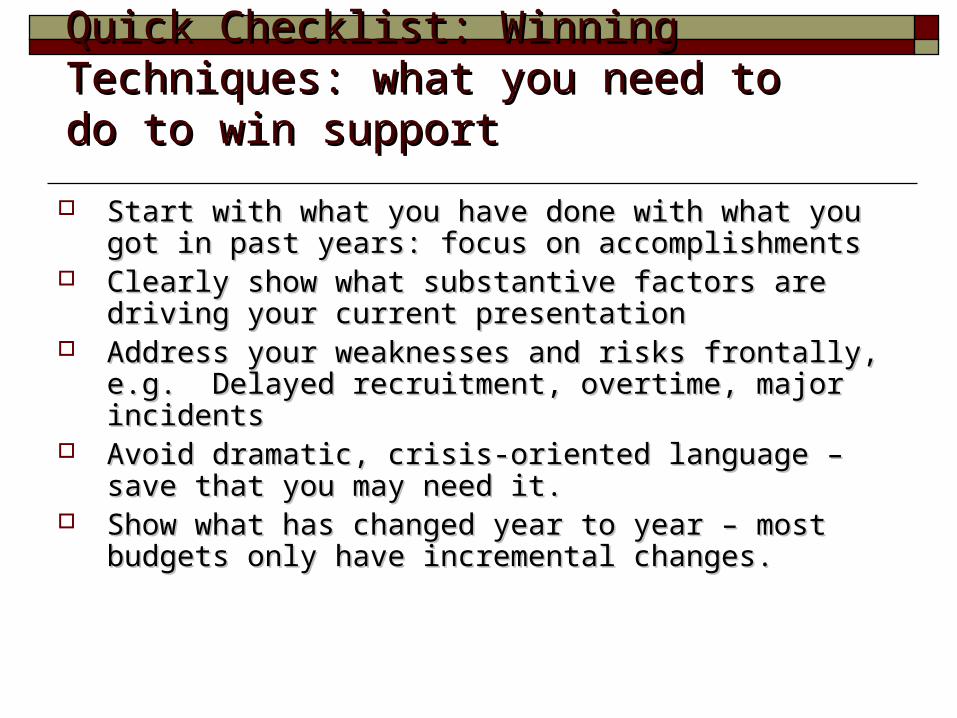

Quick Checklist: Winning Quick Checklist: Winning Techniques: what you need to do to Techniques: what you need to do to win supportwin support

Start with what you have done with what you got in Start with what you have done with what you got in past years: focus on accomplishmentspast years: focus on accomplishments

Clearly show what substantive factors are driving Clearly show what substantive factors are driving your current presentation your current presentation

Address your weaknesses and risks frontally, e.g. Address your weaknesses and risks frontally, e.g. Delayed recruitment, overtime, major incidentsDelayed recruitment, overtime, major incidents

Avoid dramatic, crisis-oriented language – save that Avoid dramatic, crisis-oriented language – save that you may need it.you may need it.

Show what has changed year to year – most budgets Show what has changed year to year – most budgets only have incremental changes.only have incremental changes.

20

Quick Checklist: Winning Quick Checklist: Winning Techniques: what you need to do to Techniques: what you need to do to win supportwin support

Focus on the good management of resources Focus on the good management of resources and what efficiencies you have achieved – and what efficiencies you have achieved – everybody but you think you can do more with everybody but you think you can do more with what you havewhat you have

Avoid detail – use graphics (but be ready with Avoid detail – use graphics (but be ready with answers to questions)answers to questions)

Make it concrete – numbers scare people, but Make it concrete – numbers scare people, but the number of new officers or cost per household the number of new officers or cost per household of the increase are a nice focusof the increase are a nice focus

Show the impact of what you are proposingShow the impact of what you are proposing Signal future issues – you will be back.Signal future issues – you will be back.

21

Sorting Out Business CasesSorting Out Business Cases Your are the ChiefYour are the Chief’’s budget groups budget group Review and discuss these business casesReview and discuss these business cases You need to do two things, You need to do two things, neither of which is neither of which is

directly related to the merits of each casedirectly related to the merits of each case: : Suggest a set of criteria that you would put in Suggest a set of criteria that you would put in

place to assess these business casesplace to assess these business cases Indicate what other information you would Indicate what other information you would

need about the Serviceneed about the Service’’s financial situation to s financial situation to recommend approval of the cases, andrecommend approval of the cases, and

What other work needs to be done to improve What other work needs to be done to improve these cases. these cases.

22

Build it and build it again

23

24

The Challenge of Capital Budgeting Think of a continuum of spending to impact

If I hire a teacher, I get an output immediately If I budget to build a school I get a school in say two years time If I budget to build a power plant, I get power in seven years time If I under-maintain an asset, I see a deterioration in public services in

ten to fifteen years time

This introduces an inherent bias against capital spending Benefits not visible immediately or costs of not investing only visible

in the long term Tougher to cut recurrent spending Easier to cut maintenance spending than fire teachers

25

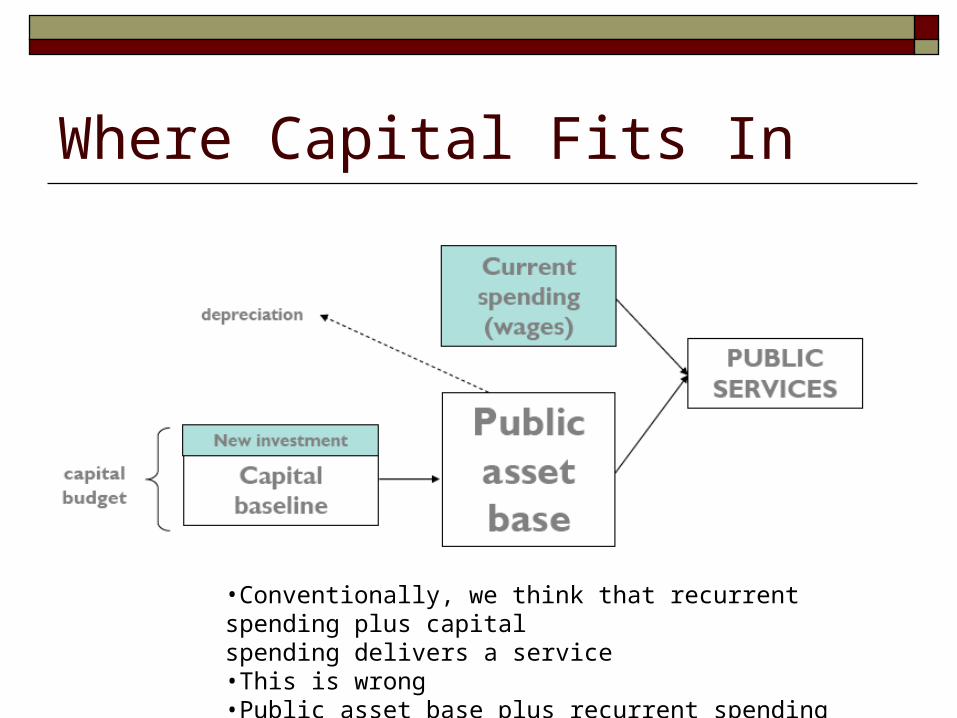

Where Capital Fits In

•Conventionally, we think that recurrent spending plus capitalspending delivers a service•This is wrong•Public asset base plus recurrent spending delivers service

Definition

27

Tangible Capital Assets, Section PS 3150:Tangible capital assets are non-financial assets having physical substance that:

a) are held for use in the production or supply of goods and services, for rental to others, for administrative purposes or for the development, construction, maintenance or repair of other tangible capital assets;b) have useful economic lives extending beyond an accounting period;c) are used on a continuing basis; andd) are not for resale in the ordinary course of operations. (PS 3150.05)

28

Capital BudgetingCapital Budgeting

Capital Budgeting is a process used to evaluate investments in long-term or capital assets.

Capital Assets have useful lives of more than one year;

analysis requires focus on the life of the asset;

low-cost, long-lived assets are not usually subjected to theCapital Budgeting process;

cost often makes it necessary for the organization tofinance the asset using long-term financing from capitalcampaigns, mortgages, long-term loans, leases, and equityofferings.

29

Unique Features Capital budgeting decisions have

long-term implications. These decisions involve

substantial commitment of funds. These decisions are irreversible

and require analysis of minute details.

These decisions determine and affect the future capacity of the agency.

30

Types of Capital Budget Actions

CapitalAcquisitions

CapitalImprovements/

BettermentsMaintenance

31

Capital budgeting:Analyzing alternative long-

term investments and deciding which assets to acquire, eliminate or renovate

Capital budgeting:Analyzing alternative long-

term investments and deciding which assets to acquire, eliminate or renovate

Outcomeis uncertain.

Outcomeis uncertain.

Large amounts ofmoney are usually

involved.

Large amounts ofmoney are usually

involved.

Investment involves along-term commitment. Investment involves a

long-term commitment.

Decision may bedifficult or impossible

to reverse.

Decision may bedifficult or impossible

to reverse.

Risk in Capital Investment Decisions

32

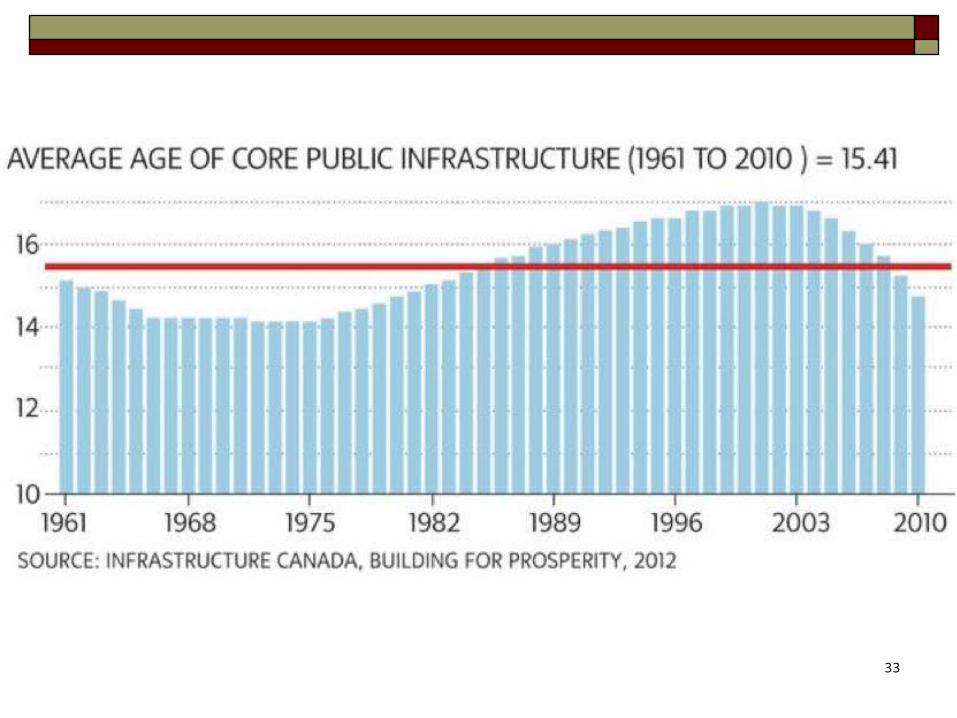

Why Prepare a Capital Plan?Why Prepare a Capital Plan?

Investments are large, Mistakes can be costly. Capital acquisitions lock the organization in for many years, Capital assets have long lives, The organization uses to buy the capital

asset flows over time and at different costs..

33

34

35

36

Steps in the Development of a Capital BudgetSteps in the Development of a Capital Budget

37

Inventory of Capital AssetsInventory of Capital Assets Life cycle assessments – replacement plans Depreciation schedules: accrued value or

replacement value Provides information on the capacity of the

infrastructure in place

38

Capital Investment PlanCapital Investment Plan

Primarily a planning document – not necessarily fully funded

Relating it to the agency’s or government’s overall objectives and priorities

Danger of ‘hidden’ capital costs not attracting public or political attention: replacing computers, buildings, sewers

Danger in ‘all to obvious’ capital renewal costs getting priorities: potholes

39

Developing a Multi-Year PlanDeveloping a Multi-Year Plan

Reinforces the cyclical nature of capital costs – recurring expenses

Permits inclusion of maintenance and preventive costs of capital

Permits some entities to consider various longer-term funding strategies

40

Development of a Financing PlanDevelopment of a Financing Plan

Complexity varies dramatically Ranges from drawing on appropriated

funds completely right through to public-private partnerships, bonds issues, specialized financing strategies such as user fees (airports)

Increasing trend to look at creative options

Financing Capital Projects: Options Special capital reserves General expenditures Special fees, levies, charges Borrowing Private financing

41

42

Danger of Optimism Bias in CostingDanger of Optimism Bias in Costing Departments may under-budget for costs because they think

that if they are honest with the costs, money will not be allocated

Poor risk analysis or using only preliminary costings Project overruns are a nightmare for spending control, yet

they are endemic in the public sector

Problems in Capital Budgeting Full costing versus buy and build new only –

renewal, maintenance, staff, skills, secondary capital (power source, support systems)

Accrual pushes for fuller costing

43

Challenges in Capital Budgeting Failure to look at secondary and opportunity

cost impacts Capital projects are long term: politics in

short term New means of financing: PPPs, new financing

schemes, build-buy-operate

44

Cost Behaviour

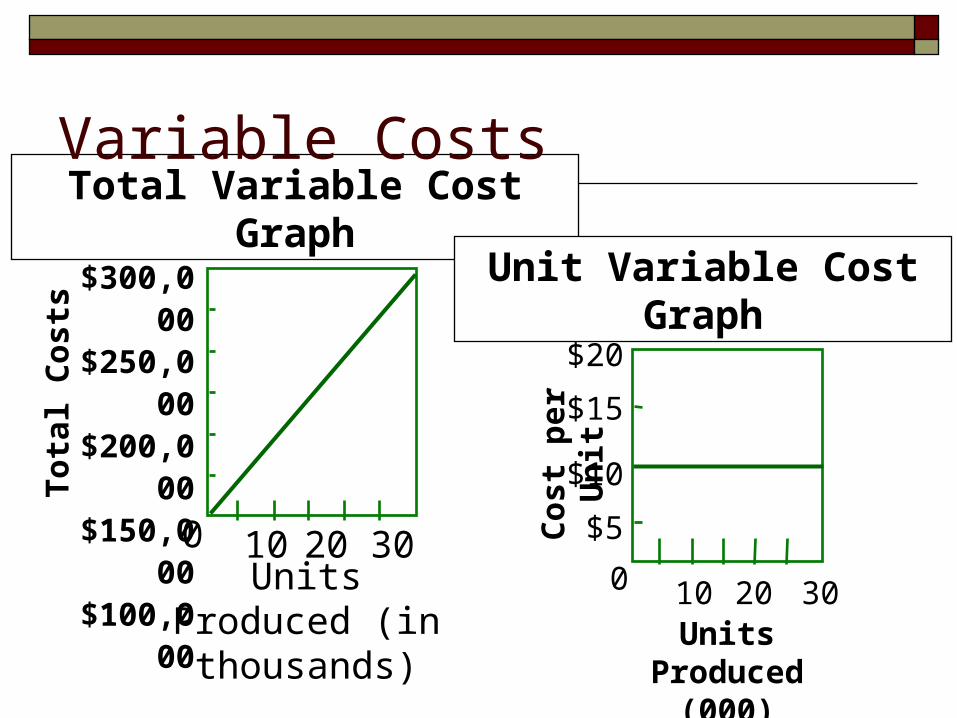

Jason Inc. produces stereo sound systems under the brand name of J-Sound. The parts for the stereo are purchased from an outside supplier for $10 per unit (a variable cost).

Variable CostVariable Cost

Total Variable Cost Graph

Tot

al C

osts

$300,000$250,000$200,000$150,000$100,000 $50,000

10 20 300Units Produced (in thousands)

Unit Variable Cost Graph

$20

$15

$10

$5

0C

ost

per

Un

it10 20 30

Units Produced (000)

Variable Costs

Tot

al C

osts

Tot

al C

osts

$300,000$250,000$200,000$150,000$100,000 $50,000

10 20 300

$20$15$10

$5

0

Cos

t per

Uni

t

10 20 30

Number ofUnits

Produced

Units Produced (000)

Units Produced (000)

Direct Materials

Cost per Unit

Total Direct Materials

Cost

5,000 units $10 $ 50,00010,000 10 l00,00015,000 10 150,00020,000 10 200,00025,000 10 250,00030,000 10 300,000

Variable Costs

The production supervisor for the Minton Company Mississauga plant is Jane

Sovissi. She is paid $75,000 per year. The plant produces from 50,000 to 300,000

bottles of air freshener depending on sales.

Fixed Costs

Number ofBottles

Produced

Total Salary for Jane Sovissi

50,000 bottles $75,000 $1.500100,000 75,000 0.750150,000 75,000 0.500200,000 75,000 0.375250,000 75,000 0.300300,000 75,000 0.250

Salary per Bottle

Produced

Fixed Costs

Total Fixed CostTotal Fixed CostT

otal

Cos

tsT

otal

Cos

ts

$150,000$125,000$100,000$75,000$50,000

$25,000

100 200 3000

Unit Fixed CostUnit Fixed Cost

Bottles Produced (000)

Number ofBottles

Produced

Cos

t per

Uni

t $1.50$1.25$1.00

$.75$.50

$.25

100 200 3000

Units Produced (000)

Total Salary for Jane Sovissi

50,000 bottles $75,000 $1.500100,000 75,000 0.75015,000 75,000 0.50020,000 75,000 0.37525,000 75,000 0.30030,000 75,000 0.250

Salary per Bottle

Produced

Simpson and Associates out of Kingston Ontario manufactures sails using rented

equipment. The rental charges are $15,000 per year, plus $1 for each machine hour used over

10,000 hours.

Mixed Costs

Total Mixed Cost Total Mixed Cost

Tot

al C

osts

Tot

al C

osts

0

Total Machine Hours (000)

$45,000$40,000 $35,000$30,000$25,000$20,000$15,000$10,000 $5,000

10 20 30 40

Mixed costs are usually separated into their fixed and variable components for management analysis.

Mixed costs are sometimes called semi-variable or semi-fixed costs.

54

Cost Benefit Analysis Tools

What is Cost Benefit Analysis?

CBA is an analytical tool used to assess the benefits and costs of regulatory proposals

Given sufficient information, CBA can:

calculate the net benefits for each proposal

rank proposals by their net benefits

recommend the proposal with the greatest net benefit

56

Cost/Benefit AnalysisCost/Benefit Analysis

Uses: Comparing benefits and costs of a particular project to

see if benefits exceed costs Comparing costs of two or more products to determine

lowest cost

Why is CBA useful?

CBA examines costs and benefits from the perspective of the proposal as a whole:

it forces a wider view on decision makers

promotes comparability and encourages consistent decision making

its aim is to maximize net benefits

CBA includes all costs and benefits – it tells the whole story

Why is CBA useful?

CBA provides a summary of the efficiency effects of a policy

But CBA can draw attention to equity issues

by identifying who gains and who loses from a regulatory proposal

but it is up to decision makers to decide whether distributional impacts/equity issues are important and need addressing

59

The Process of Cost/Benefit Analysis

Calculate the costs

•One time costs

•Ongoing or Repeated

Costs

•Opportunity costs

Calculate the Benefits

•One time benefits

•Ongoing or Benefits

•Savings

•Improved Services

Calculate the Return on Investment = ROI

Benefits/Costs × 100% = ROI

60

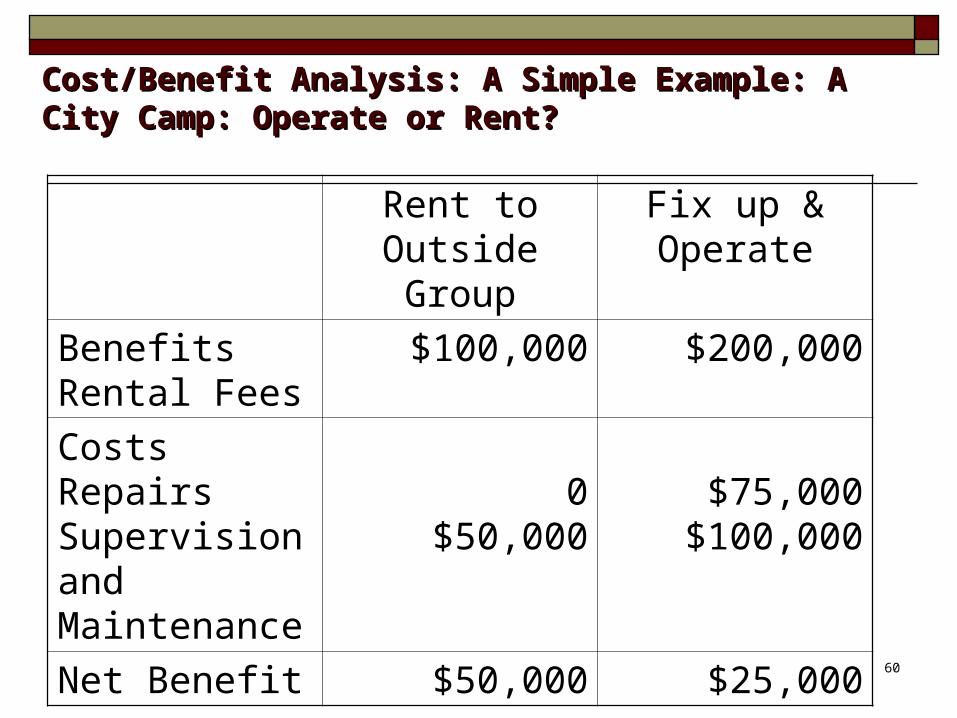

Cost/Benefit Analysis: A Simple Example: A City Camp: Cost/Benefit Analysis: A Simple Example: A City Camp: Operate or Rent?Operate or Rent?

Rent to Outside Group

Fix up & Operate

BenefitsRental Fees

$100,000 $200,000

CostsRepairsSupervision and Maintenance

0$50,000

$75,000$100,000

Net Benefit $50,000 $25,000

61

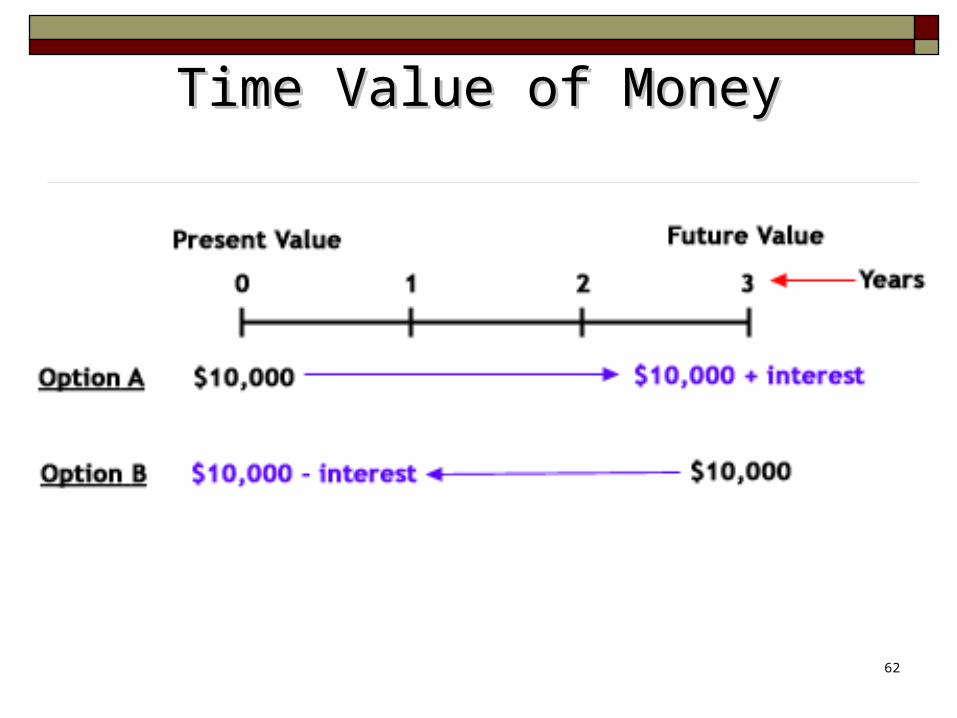

Time Value of MoneyTime Value of Money

Previous example ignores the role of time in deciding on alternatives

More complex issues seldom play out in one year

62

Time Value of MoneyTime Value of Money

63

Present Value

Project evaluation usually requires comparing costs and benefits from different time periods

Dollars across time periods are not immediately comparable, because of inflation and returns in the market.

64

Present Value:Present Dollars into the Future

Suppose you invest $100 today in the bank At the end of year 1, it is worth

(1+.05)x$100, or $105 At the end of year 2, it is worth

(1+.05)x$105, or $110.25 The interest compounds over time, that is the

interest is also earning interest

65

Present Value:Present Dollars into the Future

Define R=initial investment amount r=rate of return on investment T=years of investment

The future value (FV) of the investment is:

FV R rT 1

66

Present Value:Future Dollars into the Present

Suppose someone promises to pay you $100 one year from now.

What is the maximum amount you should be willing to pay today for such a promise?

You are forgoing the interest that you could earn on the money that is being loaned.

67

Present Value:Future Dollars into the Present

The present value of a future amount of money is the maximum amount you would be willing to pay today for the right to receive the money in the future.

68

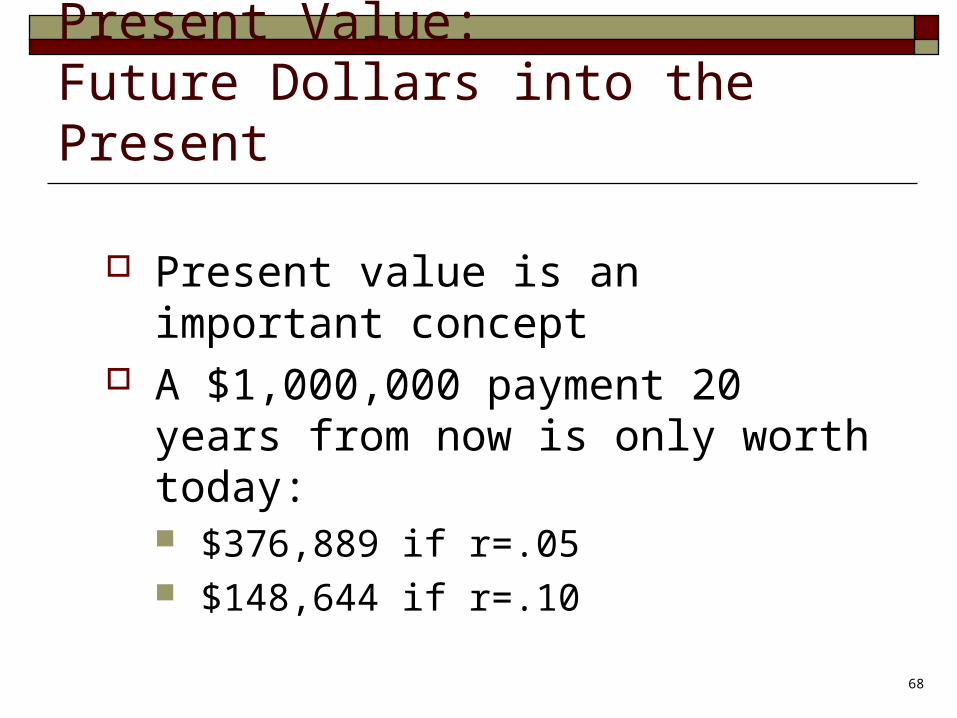

Present Value:Future Dollars into the Present

Present value is an important concept A $1,000,000 payment 20 years from now

is only worth today: $376,889 if r=.05 $148,644 if r=.10

69

Time Value of Money PrincipleTime Value of Money Principle

Money in hand now is worth more than the right to receive money in the

future because money in hand now can be invested to earn interest.

70

Time Value of Money: measuring Time Value of Money: measuring present valuepresent value

Major impact on intergenerational equity issues

Where it really matters for the public sector is in its use in forward costing and cost benefit analysis of projects that derive actual costs and benefits of a project

Also, how cash will flow becomes crucial in terms of final value

71

Net Present ValueNet Present Value (NPV) is a means to calculate whether the public sector organization will be better or worse off if it make a capital investment. It does so by adding the present value of outflows and the present value of inflows. It shows the value of a stream of future cash flows discounted back to the present by some percentage that represents the minimum desired rate of return, often called the cost of capital.

NPV = PV Inflows – PV Outflows

Need to Perform Sensitivity Analysis

There is usually considerable uncertainty about predicted costs and benefits

Sensitivity analysis shows how these uncertainties affect the CBA results

Three types of sensitivity analysis:

worst/best case analysis partial sensitivity analysis Monte Carlo sensitivity analysis

If the sign of the net benefits does not change after considering the range of scenarios, there can be confidence in the CBA results

73

Sensitivity Analysis

Projects do not always run to plan. Costs and benefits estimated at an early stage of a project may indicate a profitable project, but this profit could be eroded by an increase in costs or a decrease in the value of the benefits (the revenue).

Sensitivity analysis provides a means of determining the financial impact of this type of fluctuation.

By entering an anticipated percentage increase in costs or decrease in revenue the financial impact on the project can be identified by looking at the change to the NPV or IRR measures.

Need to Perform Sensitivity Analysis

There is usually considerable uncertainty about predicted costs and benefits

Sensitivity analysis shows how these uncertainties affect the CBA results

Three types of sensitivity analysis:

worst/best case analysis partial sensitivity analysis Monte Carlo sensitivity analysis

If the sign of the net benefits does not change after considering the range of scenarios, there can be confidence in the CBA results

75

General decision rule in applying NPV

If the Net Present Value is . . . Then the Project is . . .

Positive . . . Acceptable, since it promises a return greater than the required

rate of return.

Zero . . . Acceptable, since it promises a return equal to the required rate

of return.

Negative . . . Not acceptable, since it

promises a return less than the required rate of return.

76

Cost-Benefit Gaming

Chain-Reaction game Include secondary benefits to make a proposal appear more

favorable, without also including the secondary costs Labor game

Wages are viewed as benefits rather than costs of the project Double counting game

Benefits are erroneously counted twice Phony Quantification Ignoring soft costs and soft benefits Certainty in the face of uncertainty. Downplaying or ignoring non-financial social benefits and costs

77

Cost-Benefit Gaming

Double counting benefits

‘Before/after’ rather than ‘with/without’

Selecting a discount rate to deliver a particular result

Ignoring uncertainty – no sensitivity analysis

78

A sobering thought …

There are significant challenges in using CBA

Mainly because it is inherently difficult to accurately measure benefits and costs in dollar terms

In so much of government, we are dealing with a mix of goals, high potential risks and many unknowns, e.g. the rather foolish effort to establish the value of a statistical life

But even when it is difficult to measure benefits and costs with any precision, applying the CBA framework is important and useful

Limitations of Life Cycle Costing

79

“ The probability of a cost estimate becoming a reality, when expressed as a single number is precisely zero.”- NATO document, Methods and Models of Life Cycle Costing.”

Warning: Some things just don’t add up