Pipavav Shipyard Limited - Money Control

393

DRAFT RED HERRING PROSPECTUS Dated January 16, 2008 Please read Section 60B of the Companies Act, 1956 (This Draft Red Herring Prospectus will be updated upon filing with the RoC) 100% Book Built Issue Pipavav Shipyard Limited (The Company was incorporated as Pipavav Ship Dismantling and Engineering Limited on October 17, 1997 under the Companies Act, 1956, as amended (the “Companies Act”). Pursuant to a special resolution of the shareholders of the Company at an extraordinary general meeting held on April 19, 2005, the name of the Company was changed to Pipavav Shipyard Limited. The fresh certificate of incorporation to reflect the new name was issued on April 29, 2005 by the Registrar of Companies, Gujarat, Dadra and Nagar Haveli, located at Ahmedabad (the “RoC”). For details of change in name and registered office, see the section “History and Certain Corporate Matters” beginning on page [●] of the Draft Red Herring Prospectus.) Registered Office: Pipavav Port, Post Ucchaya, Via Rajula, Rajula – 365 560, Gujarat, India; Telephone: +91 2794 286200; Facsimile: +91 2794 286373 Corporate Office: SKIL House, 209 Bank Street Cross Lane, Fort, Mumbai – 400 023, Maharashtra, India; Telephone: +91 22 6619 9000; Facsimile: +91 22 2265 6022 Contact Person: Mr. Ajit Dabholkar, Company Secretary and Compliance Officer; Email: [email protected] Website: www.pipavavshipyard.com PUBLIC ISSUE OF 86,850,000 EQUITY SHARES OF RS.10 EACH (“EQUITY SHARES”) OF PIPAVAV SHIPYARD LIMITED (THE “COMPANY” OR THE “ISSUER”) FOR CASH AT A PRICE OF RS.[●] PER EQUITY SHARE, AGGREGATING RS.[●] MILLION (THE “ISSUE”). THE ISSUE WILL CONSTITUTE 13.04% OF THE FULLY DILUTED POST-ISSUE EQUITY SHARE CAPITAL OF THE COMPANY. 2,600,000 EQUITY SHARES OF RS.10 EACH WILL BE RESERVED IN THE ISSUE FOR SUBSCRIPTION BY EMPLOYEES (AS SPECIFICALLY DEFINED HEREIN IN THE SECTION “DEFINITIONS AND ABBREVIATIONS”) AT THE ISSUE PRICE (THE “EMPLOYEE RESERVATION PORTION”). THE ISSUE LESS THE EMPLOYEE RESERVATION PORTION SHALL BE HEREINAFTER REFERRED TO AS THE “NET ISSUE”. THE COMPANY ALSO PROPOSES TO MAKE A PRE-IPO PLACING. IF SUCH PRE-IPO PLACING IS COMPLETED, THE NUMBER OF EQUITY SHARES ISSUED PURSUANT TO THE PRE-IPO PLACING WILL BE REDUCED FROM THE NET ISSUE SUBJECT TO A MINIMUM NET ISSUE SIZE OF 10% OF THE POST-ISSUE PAID-UP SHARE CAPITAL. PRICE BAND: RS.[●] TO RS.[●] PER EQUITY SHARE OF FACE VALUE RS.10 EACH. THE ISSUE PRICE IS [●] TIMES THE FACE VALUE AT THE LOWER END OF THE PRICE BAND AND [●] TIMES THE FACE VALUE AT THE HIGHER END OF THE PRICE BAND. In case of revision in the Price Band, the Bidding Period shall be extended for three additional working days after such revision, subject to the Bidding Period not exceeding 10 working days. Any revision in the Price Band, and the revised Bidding Period, if applicable, shall be widely disseminated by notification to the Bombay Stock Exchange Limited (the “BSE”) and the National Stock Exchange of India Limited (the “NSE”), by issuing a press release and also by indicating the change on the website of the Book Running Lead Managers (“BRLMs”), the Co-Book Running Lead Managers (“CBRLMs”) and at the terminals of the other members of the Syndicate. Pursuant to Rule 19(2)(b) of the Securities Contract (Regulation) Rules, 1957, as amended (“SCCR”), this Issue is for less than 25% of the post-Issue share capital of the Company and is therefore being made through a 100% Book Building Process wherein at least 60% of the Net Issue shall be allocated on a proportionate basis to Qualified Institutional Buyers (“QIBs”), out of which 5% shall be available for allocation on a proportionate basis to Mutual Funds only and the remainder shall be available for allocation on a proportionate basis to all QIBs, including Mutual Funds, subject to valid Bids being received at or above the Issue Price. In addition, in accordance with Rule 19(2)(b) of the SCRR, a minimum of two million securities are being offered to the public and the size of the Issue shall aggregate at least Rs.1,000 million. If at least 60% of the Net Issue cannot be allotted to QIBs, then the entire application money will be refunded forthwith. Further, not less than 10% of the Net Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 30% of the Net Issue shall be available for allocation on a proportionate basis to Retail Individual Bidders, subject to valid Bids being received at or above the Issue Price. Further, 2,600,000 Equity Shares shall be available for allocation on a proportionate basis to Employees, subject to valid Bids being received at or above the Issue Price. RISKS IN RELATION TO FIRST ISSUE This being the first public issue of Equity Shares of the Company, there has been no formal market for the Equity Shares of the Company. The face value of the Equity Shares is Rs.10 per Equity Share and the Issue Price is [●] times the face value. The Issue Price (as determined by the Company, in consultation with the BRLMs and the CBRLMs, on the basis of the assessment of market demand for the Equity Shares by way of the book building process) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active and/or sustained trading in the Equity Shares of the Company or regarding the price at which the Equity Shares will be traded after listing. GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on their own examination of the Company and the Issue, including the risks involved. The Equity Shares offered in the Issue have not been recommended or approved by SEBI, nor does SEBI guarantee the accuracy or adequacy of the contents of the Draft Red Herring Prospectus. Specific attention of the investors is invited to the statements in the section “Risk Factors” beginning on page [●] of the Draft Red Herring Prospectus. COMPANY’S ABSOLUTE RESPONSIBILITY The Company, having made all reasonable inquiries, accepts responsibility for and confirms that the Draft Red Herring Prospectus contains all information with regard to the Company and the Issue that is material in the context of the Issue, that the information contained in the Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes the Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. IPO GRADING This Issue has been graded by [●] and has been assigned the “IPO Grade [●]” indicating [●], through its letter dated [●]. The IPO grading is assigned on a five point scale from 1 to 5 with an “IPO Grade 5” indicating strong fundamentals and an “IPO Grade 1” indicating poor fundamentals. For details regarding the grading of the Issue, see the section “General Information” beginning on page [●] of the Draft Red Herring Prospectus. LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. The Company has received in-principle approvals from the BSE and the NSE for the listing of the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of this Issue, the [•] shall be the Designated Stock Exchange. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

Transcript of Pipavav Shipyard Limited - Money Control

DRAFT RED HERRING PROSPECTUS Dated January 16, 2008

Please read Section 60B of the Companies Act, 1956 (This Draft Red Herring Prospectus will be updated upon filing with the RoC)

100% Book Built Issue

Pipavav Shipyard Limited

(The Company was incorporated as Pipavav Ship Dismantling and Engineering Limited on October 17, 1997 under the Companies Act, 1956, as amended (the “Companies Act”). Pursuant to a special resolution of the shareholders of the Company at an extraordinary general meeting held on April 19, 2005, the name of the Company was changed to Pipavav Shipyard Limited. The fresh certificate of incorporation to reflect the new name was issued on April 29, 2005 by the Registrar of Companies, Gujarat, Dadra and Nagar Haveli, located at Ahmedabad (the “RoC”). For details of change in name and registered office, see the section “History and Certain Corporate Matters” beginning on page [●] of the Draft Red Herring Prospectus.)

Registered Office: Pipavav Port, Post Ucchaya, Via Rajula, Rajula – 365 560, Gujarat, India; Telephone: +91 2794 286200; Facsimile: +91 2794 286373

Corporate Office: SKIL House, 209 Bank Street Cross Lane, Fort, Mumbai – 400 023, Maharashtra, India; Telephone: +91 22 6619 9000; Facsimile: +91 22 2265 6022 Contact Person: Mr. Ajit Dabholkar, Company Secretary and Compliance Officer; Email: [email protected]

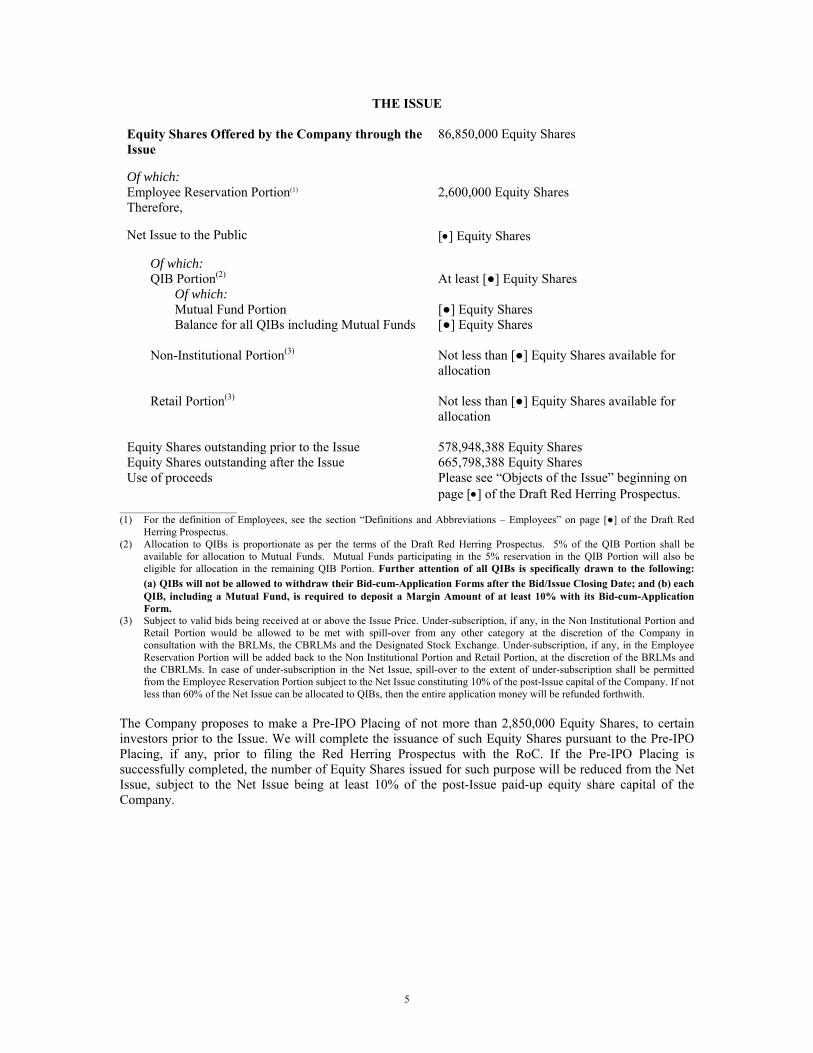

Website: www.pipavavshipyard.com PUBLIC ISSUE OF 86,850,000 EQUITY SHARES OF RS.10 EACH (“EQUITY SHARES”) OF PIPAVAV SHIPYARD LIMITED (THE “COMPANY” OR THE “ISSUER”) FOR CASH AT A PRICE OF RS.[●] PER EQUITY SHARE, AGGREGATING RS.[●] MILLION (THE “ISSUE”). THE ISSUE WILL CONSTITUTE 13.04% OF THE FULLY DILUTED POST-ISSUE EQUITY SHARE CAPITAL OF THE COMPANY. 2,600,000 EQUITY SHARES OF RS.10 EACH WILL BE RESERVED IN THE ISSUE FOR SUBSCRIPTION BY EMPLOYEES (AS SPECIFICALLY DEFINED HEREIN IN THE SECTION “DEFINITIONS AND ABBREVIATIONS”) AT THE ISSUE PRICE (THE “EMPLOYEE RESERVATION PORTION”). THE ISSUE LESS THE EMPLOYEE RESERVATION PORTION SHALL BE HEREINAFTER REFERRED TO AS THE “NET ISSUE”. THE COMPANY ALSO PROPOSES TO MAKE A PRE-IPO PLACING. IF SUCH PRE-IPO PLACING IS COMPLETED, THE NUMBER OF EQUITY SHARES ISSUED PURSUANT TO THE PRE-IPO PLACING WILL BE REDUCED FROM THE NET ISSUE SUBJECT TO A MINIMUM NET ISSUE SIZE OF 10% OF THE POST-ISSUE PAID-UP SHARE CAPITAL.

PRICE BAND: RS.[●] TO RS.[●] PER EQUITY SHARE OF FACE VALUE RS.10 EACH.

THE ISSUE PRICE IS [●] TIMES THE FACE VALUE AT THE LOWER END OF THE PRICE BAND AND [●] TIMES THE FACE VALUE AT THE HIGHER END OF THE PRICE BAND.

In case of revision in the Price Band, the Bidding Period shall be extended for three additional working days after such revision, subject to the Bidding Period not exceeding 10 working days. Any revision in the Price Band, and the revised Bidding Period, if applicable, shall be widely disseminated by notification to the Bombay Stock Exchange Limited (the “BSE”) and the National Stock Exchange of India Limited (the “NSE”), by issuing a press release and also by indicating the change on the website of the Book Running Lead Managers (“BRLMs”), the Co-Book Running Lead Managers (“CBRLMs”) and at the terminals of the other members of the Syndicate.

Pursuant to Rule 19(2)(b) of the Securities Contract (Regulation) Rules, 1957, as amended (“SCCR”), this Issue is for less than 25% of the post-Issue share capital of the Company and is therefore being made through a 100% Book Building Process wherein at least 60% of the Net Issue shall be allocated on a proportionate basis to Qualified Institutional Buyers (“QIBs”), out of which 5% shall be available for allocation on a proportionate basis to Mutual Funds only and the remainder shall be available for allocation on a proportionate basis to all QIBs, including Mutual Funds, subject to valid Bids being received at or above the Issue Price. In addition, in accordance with Rule 19(2)(b) of the SCRR, a minimum of two million securities are being offered to the public and the size of the Issue shall aggregate at least Rs.1,000 million. If at least 60% of the Net Issue cannot be allotted to QIBs, then the entire application money will be refunded forthwith. Further, not less than 10% of the Net Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 30% of the Net Issue shall be available for allocation on a proportionate basis to Retail Individual Bidders, subject to valid Bids being received at or above the Issue Price. Further, 2,600,000 Equity Shares shall be available for allocation on a proportionate basis to Employees, subject to valid Bids being received at or above the Issue Price.

RISKS IN RELATION TO FIRST ISSUE This being the first public issue of Equity Shares of the Company, there has been no formal market for the Equity Shares of the Company. The face value of the Equity Shares is Rs.10 per Equity Share and the Issue Price is [●] times the face value. The Issue Price (as determined by the Company, in consultation with the BRLMs and the CBRLMs, on the basis of the assessment of market demand for the Equity Shares by way of the book building process) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active and/or sustained trading in the Equity Shares of the Company or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on their own examination of the Company and the Issue, including the risks involved. The Equity Shares offered in the Issue have not been recommended or approved by SEBI, nor does SEBI guarantee the accuracy or adequacy of the contents of the Draft Red Herring Prospectus. Specific attention of the investors is invited to the statements in the section “Risk Factors” beginning on page [●] of the Draft Red Herring Prospectus.

COMPANY’S ABSOLUTE RESPONSIBILITY The Company, having made all reasonable inquiries, accepts responsibility for and confirms that the Draft Red Herring Prospectus contains all information with regard to the Company and the Issue that is material in the context of the Issue, that the information contained in the Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes the Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

IPO GRADING This Issue has been graded by [●] and has been assigned the “IPO Grade [●]” indicating [●], through its letter dated [●]. The IPO grading is assigned on a five point scale from 1 to 5 with an “IPO Grade 5” indicating strong fundamentals and an “IPO Grade 1” indicating poor fundamentals. For details regarding the grading of the Issue, see the section “General Information” beginning on page [●] of the Draft Red Herring Prospectus.

LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. The Company has received in-principle approvals from the BSE and the NSE for the listing of the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of this Issue, the [•] shall be the Designated Stock Exchange.

BOOK RUNNING LEAD MANAGERS

REGISTRAR TO THE ISSUE

JM Financial Consultants Private Limited 141, Maker Chambers III Nariman Point Mumbai - 400 021, India Tel: +91 22 6630 3030 Fax: +91 22 2204 7185 E-mail: [email protected] Investor Grievance ID: [email protected] Contact Person: Ms. Poonam Karande Website: www.jmfinancial.in SEBI registration number: INM000010361

Citigroup Global Markets India Private Limited 12th Floor, Bakhtawar Nariman Point Mumbai - 400 021, India Tel: +91 22 6631 9999 Fax: +91 22 6646 6669 Email: [email protected] Investor Grievance ID: [email protected] Contact Person: Ms. Ayesha Gupta Website: www.citibank.co.in SEBI registration number: INM000010718

Enam Securities Private Limited 801/802, Dalamal Towers Nariman Point Mumbai - 400 021, India Tel: +91 22 6638 1800 Fax: +91 22 2284 6824 Email and Investor Grievance ID: [email protected] Contact Person: Ms. Dipali Dalal Website: www.enam.com SEBI registration number: INM000006856

Karvy Computershare Private Limited Plot No. 17-24, Vithalrao Nagar Madhapura Hyderabad - 500 086 India Tel: +91 40 2342 0815 Fax: +91 40 2342 0814 Email: [email protected] Contact Person: Mr. M. Murali Krishna Website: www.karvy.com SEBI registration number: INR000000221

CO-BOOK RUNNING LEAD MANAGERS

SBI Capital Markets Limited 202, Maker Towers “E” Cuffe Parade Mumbai - 400 005, India Tel: +91 22 2218 9166 Fax: +91 22 2218 8332 Email: [email protected] Investor Grievance ID: [email protected] Contact Person: Mr. Nishit Mathur Website: www.sbicaps.com SEBI registration number: INM000003531

Kotak Mahindra Capital Company Limited 3rd Floor, Bakhtawar 229, Nariman Point Mumbai - 400 021, India Tel: +91 22 6634 1100 Fax: +91 22 2284 0492 Email: [email protected] Investor Grievance ID: [email protected] Contact Person: Mr. Chandrakant Bhole Website: www.kotak.com SEBI registration number: INM000008704

Motilal Oswal Investment Advisors Private Limited 113/114, Bajaj Bhawan 11th Floor, Nariman Point Mumbai - 400 0021, India Tel: +91 22 3980 4380 Fax: +91 22 3980 4315 Email and Investor Grievance ID: [email protected] Contact Person: Ms. Nisha Shah Website: www.motilaloswal.com SEBI registration number: INM000011005

BID/ISSUE PROGRAM BID/ISSUE OPENING ON [●] BID/ISSUE CLOSING ON [●]

TABLE OF CONTENTS

Page

SECTION I: GENERAL .................................................................................................................................................................................................. i DEFINITIONS AND ABBREVIATIONS .............................................................................................................................................................. i CERTAIN CONVENTIONS, PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA, CURRENCY OF

PRESENTATION AND EXCHANGE RATES...................................................................................................................................................... ix FORWARD LOOKING STATEMENTS................................................................................................................................................................ xi SECTION II: RISK FACTORS ...................................................................................................................................................................................... xii RISK FACTORS ...................................................................................................................................................................................................... xii SECTION III: INTRODUCTION .................................................................................................................................................................................. 1 SUMMARY.............................................................................................................................................................................................................. 1 THE ISSUE .............................................................................................................................................................................................................. 5 SUMMARY FINANCIAL INFORMATION.......................................................................................................................................................... 6 GENERAL INFORMATION .................................................................................................................................................................................. 8 CAPITAL STRUCTURE......................................................................................................................................................................................... 20 OBJECTS OF THE ISSUE ...................................................................................................................................................................................... 36 BASIS FOR ISSUE PRICE...................................................................................................................................................................................... 44 STATEMENT OF TAX BENEFITS ....................................................................................................................................................................... 47 SECTION IV: ABOUT THE COMPANY ..................................................................................................................................................................... 59 SHIPBUILDING AND OFFSHORE FABRICATION INDUSTRY...................................................................................................................... 59 OUR BUSINESS...................................................................................................................................................................................................... 68 REGULATIONS AND POLICIES.......................................................................................................................................................................... 85 HISTORY AND CERTAIN CORPORATE MATTERS ........................................................................................................................................ 90 OUR MANAGEMENT............................................................................................................................................................................................ 105 OUR PROMOTERS AND PROMOTER GROUP COMPANIES ......................................................................................................................... 122 RELATED PARTY TRANSACTIONS .................................................................................................................................................................. 163 DIVIDEND POLICY ............................................................................................................................................................................................... 164 SECTION V: FINANCIAL INFORMATION............................................................................................................................................................... F-1 FINANCIAL STATEMENTS.................................................................................................................................................................................. F-1 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS .......................... 165 SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND US GAAP ...................................................................... 176 FINANCIAL INDEBTEDNESS.............................................................................................................................................................................. 189 SECTION VI: LEGAL AND OTHER INFORMATION............................................................................................................................................. 192 OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS ............................................................................................................. 192 GOVERNMENT AND OTHER APPROVALS...................................................................................................................................................... 211 OTHER REGULATORY AND STATUTORY DISCLOSURES .......................................................................................................................... 217 SECTION VII: ISSUE INFORMATION....................................................................................................................................................................... 228 TERMS OF THE ISSUE.......................................................................................................................................................................................... 228 ISSUE STRUCTURE............................................................................................................................................................................................... 231 ISSUE PROCEDURE .............................................................................................................................................................................................. 235 SECTION VIII: MAIN PROVISIONS OF THE ARTICLES OF ASSOCIATION ................................................................................................. 264 MAIN PROVISIONS OF THE ARTICLES OF ASSOCIATION.......................................................................................................................... 264 SECTION IX: OTHER INFORMATION ..................................................................................................................................................................... 307 MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION................................................................................................................ 307 DECLARATION...................................................................................................................................................................................................... 310

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS Unless the context otherwise indicates or requires in the Draft Red Herring Prospectus, the following terms have the meanings given below. Company Related Terms Term Description The Company, the Issuer, Pipavav Shipyard Limited or PSL

Pipavav Shipyard Limited, a public limited company incorporated under the Companies Act and whose registered office is at Pipavav Port, Post Ucchaya, Via Rajula, Rajula - 365 560, Gujarat, India.

We, our or us The Company, and where the context requires, its Subsidiary, on a consolidated basis.

ABN AMRO ABN AMRO Asia Merchant Bank (Singapore) Limited. Articles or Articles of Association

The articles of association of the Company, as amended.

Auditors GPS & Associates, Chartered Accountants, the statutory auditors of the Company.

Board of Directors or Board The board of directors of the Company or a committee constituted thereof.

Director(s) The director(s) on the Board of the Company. Citadel Citadel Equity Fund Limited. Equity Shares Equity shares of the Company with a face value of Rs.10 each. EXIM Bank Export-Import Bank of India. GPPL Gujarat Pipavav Port Limited. Grevek Investments Grevek Investments and Finance Private Limited, a private limited

company incorporated under the Companies Act and a Promoter of the Company.

HUDCO Housing and Urban Development Corporation Limited. IDBI Industrial Development Bank of India Limited. IL&FS Infrastructure Leasing & Financial Services Limited. Memorandum or Memorandum of Association

The memorandum of association of the Company, as amended.

New York Life New York Life Investment Management India Fund (FVCI) II, LLC. Offshore Business The business of fabrication or construction of offshore platforms, rigs,

jackets, vessels, etc., for the upstream oil and gas sector excluding all kinds of sub-sea pipelines.

Order book Contracts entered into by the Company with its customers for construction and repair of ships and other products, including for the Offshore Business.

Pipavav Shipyard A shipbuilding, ship repair and offshore fabrication complex being constructed by the Company at Pipavav in the State of Gujarat, India. The construction of the Pipavav Shipyard includes:

• conversion of one existing wet basin into a 651 meters long and 65 meters wide dry dock, capable of accommodating ships of up to 400,000 DWT and/or multiple combinations of smaller vessels;

• the construction of a fabrication and block assembly facility for shipyard operations;

• the establishment of dryland facilities comprising a fabrication area for the Offshore Business products; and

• the installation of a shiplift facility, including multiple land berths, for building and repairing small to medium sized ships, including

i

Term Description naval vessels.

Promoters The promoters of the Company specified in the section “Our Promoters and Promoter Group Companies” beginning on page [●] of the Draft Red Herring Prospectus.

Promoter Group or Promoter Group Companies

The companies, entities or individuals mentioned in the section “Our Promoters and Promoter Group Companies” beginning on page [●] of the Draft Red Herring Prospectus.

Punj Lloyd or PLL Punj Lloyd Limited, a public limited company incorporated under the Companies Act and a Promoter of the Company.

Registered Office The registered office of the Company, which is at Pipavav Port, Post Ucchaya, Via Rajula, Rajula - 365 560, Gujarat, India.

SembCorp SembCorp Marine Limited. SKIL SKIL Infrastructure Limited, a public limited company incorporated

under the Companies Act and a Promoter of the Company. Sneha Metals Sneha Metals Private Limited. Subsidiary or E Complex E Complex Private Limited, a private limited company incorporated

under the Companies Act and a wholly-owned subsidiary of the Company.

Trinity Trinity Capital (Nine) Limited. Issue Related Terms Term Description Advisor to the Issue IL&FS Investsmart Securities Limited. Allot, Allotment, Allotted, allot or allotment

Unless the context otherwise requires or implies, the issue or allotment pursuant to the Issue.

Allottee A successful Bidder to whom Equity Shares are Allotted. Banker(s) to the Issue [●]. Bid An indication to make an offer during the Bidding Period by a

prospective investor to subscribe for or purchase the Equity Shares at a price within the Price Band, including all revisions and modifications thereto.

Bid Amount The highest value of the optional Bids indicated in the Bid-cum-Application Form and payable by the Bidder upon submission of the Bid.

Bid-cum-Application Form The form in terms of which the Bidder shall make an offer to subscribe for or purchase the Equity Shares and which will be considered as the application for Allotment pursuant to the terms of the Red Herring Prospectus and the Prospectus.

Bid/Issue Closing Date The date after which the members of the Syndicate shall not accept any Bids for the Issue, which shall be notified in a widely circulated English national newspaper, a widely circulated Hindi national newspaper and a widely circulated Gujarati newspaper.

Bid/Issue Opening Date The date on which the members of the Syndicate start accepting Bids for the Issue, which date shall be notified in a widely circulated English national newspaper, a widely circulated Hindi national newspaper and a widely circulated Gujarati newspaper.

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring Prospectus and the Bid-cum-Application Form.

Bidding Period The period between the Bid/Issue Opening Date and the Bid/Issue Closing Date (inclusive of both days) and during which prospective Bidders can submit their Bids.

Book Building Process The book building process as described in Chapter XI of the SEBI Guidelines, in terms of which the Issue is being made.

BRLMs or Book Running JM Financial Consultants Private Limited, Citigroup Global Markets

ii

Term Description Lead Managers India Private Limited and Enam Securities Private Limited. BSE Bombay Stock Exchange Limited. Business Day Any day other than a Saturday or Sunday on which commercial banks in

Mumbai are open for business. CAN or Confirmation of Allocation Note

The note, advice or intimation of allocation of Equity Shares sent to the Bidders who have been allocated Equity Shares after discovery of the Issue Price in accordance with the Book Building Process.

Cap Price The higher end of the Price Band, above which the Issue Price will not be finalized and above which no Bids will be accepted.

CBRLMs or the Co-Book Running Lead Managers

Kotak Mahindra Capital Company Limited, SBI Capital Markets Limited and Motilal Oswal Investment Advisors Private Limited.

CDSL Central Depository Services (India) Limited. Citi Citigroup Global Markets India Private Limited. Companies Act The Companies Act, 1956, as amended. Cut-off Price Any price within the Price Band finalized by the Company, in

consultation with the BRLMs and the CBRLMs. A Bid submitted at the Cut-off Price by a Retail Individual Bidder is a valid Bid. Only Retail Individual Bidders are entitled to Bid at the Cut-off Price for a Bid Amount not exceeding Rs.100,000. QIBs and Non-Institutional Bidders are not entitled to Bid at the Cut-off Price.

Depositories NSDL and CDSL. Depositories Act The Depositories Act, 1996, as amended. Depository A depository registered with SEBI under the Securities and Exchange

Board of India (Depositories and Participants) Regulations, 1996, as amended.

Depository Participant or DP A depository participant as defined under the Depositories Act. Designated Date The date on which the Escrow Collection Banks transfer the funds from

the Escrow Account to the Public Issue Account, after the Prospectus is filed with the RoC, following which the Board may approve the Allotment of Equity Shares to successful Bidders.

Designated Stock Exchange The [●]. Draft Red Herring Prospectus

This draft red herring prospectus issued in accordance with Section 60B of the Companies Act, which does not have complete particulars of the price at which the Equity Shares are offered and the size of the Issue.

ECS Electronic Clearing System. EEFC Account The Exchange Earner’s Foreign Currency Account, as specified under

FEMA. Eligible NRIs NRIs from such jurisdictions outside India where it is not unlawful to

make an offer or invitation under the Issue and in relation to whom the Red Herring Prospectus constitutes an invitation to purchase the Equity Shares offered thereby.

Employee, Employees or Eligible Employees (in the Employee Reservation Portion)

A permanent employee or a Director of the Company, as on the date of filing of the Red Herring Prospectus, who is a resident in India and who continues to be in the employment of the Company, until submission of the Bid-cum-Application Form. It would not include employees of the Promoters and Promoter Group entities.

Employee Reservation Portion

The portion of the Issue, being a maximum of 2,600,000 Equity Shares, available for allocation to the Employees.

Enam Enam Securities Private Limited. Escrow Account The account opened with Escrow Collection Bank(s) for the Issue and in

whose favour the Bidder will issue cheques or drafts in respect of the Margin Amount when submitting a Bid and the remainder of the Bid Amount, if any, collected thereafter.

Escrow Agreement The agreement to be entered into among the Company, the Registrar to

iii

Term Description the Issue, the BRLMs, the CBRLMs, the Syndicate Members and the Escrow Collection Bank(s) for collection of the Bid Amounts and where applicable, for remitting refunds of the amounts collected to the Bidders on the terms and conditions thereof.

Escrow Collection Bank(s) The banks that are clearing members and registered with SEBI as Bankers to the Issue with whom the Escrow Account(s) will be opened, comprising [●].

FCNR Account Foreign Currency Non-Resident Account. FDI Foreign Direct Investment, as understood under applicable laws and

regulations in India. FEMA The Foreign Exchange Management Act, 1999, as amended, and the

regulations framed thereunder. FIIs Foreign Institutional Investors (as defined under the Securities and

Exchange Board of India (Foreign Institutional Investors) Regulations, 1995, as amended) registered with SEBI.

First Bidder The Bidder whose name appears first in the Bid-cum-Application Form or Revision Form.

Fiscal, Financial Year or FY A period of twelve months ended March 31 of that particular year, unless otherwise stated.

Floor Price The lower end of the Price Band, below which the Issue Price will not be finalized and below which no Bids will be accepted.

FVCIs Foreign Venture Capital Investors (as defined under the Securities and Exchange Board of India (Foreign Venture Capital Investor) Regulations, 2000, as amended) registered with SEBI.

GIR Number General Index Registry Number. Indian GAAP Generally accepted accounting principles in India. Indian National As used in the context of the Employee Reservation Portion, a citizen of

India as defined under the Indian Citizenship Act, 1955, as amended, who is not an NRI.

Industrial Policy The policy and guidelines relating to industrial activity in India issued by the Ministry of Commerce and Industry, Government of India, as updated, modified or amended from time to time.

IFSC Indian Financial System Code. Issue The public issue of an aggregate of 86,250,000 Equity Shares. Issue Price The final price at which Equity Shares will be Allotted in the Issue, as

determined by the Company, in consultation with the BRLMs and the CBRLMs, on the Pricing Date.

JM Financial JM Financial Consultants Private Limited. KMCC Kotak Mahindra Capital Company Limited. Margin Amount The amount paid by the Bidder at the time of submission of the Bid,

which may range between 10% and 100% of the Bid Amount, as applicable.

MFs or Mutual Funds Mutual funds registered with SEBI under the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, as amended.

MICR Magnetic Ink Character Recognition. Monitoring Agency Industrial Development Bank of India Limited. Motilal Oswal Motilal Oswal Investment Advisors Private Limited. Mutual Fund Portion 5% of the QIB Portion, equal to a minimum of [●] Equity Shares,

available for allocation to Mutual Funds from the QIB Portion. NEFT National Electronic Fund Transfer. Net Issue The Issue other than the Equity Shares included in the Employee

Reservation Portion, aggregating [●] Equity Shares. Non-Institutional Bidders All Bidders that are not Qualified Institutional Buyers or Retail Individual

Bidders and have bid for an amount greater than Rs.100,000.

iv

Term Description Non-Institutional Portion The portion of the Issue being not less than 10% of the Net Issue

consisting of [●] Equity Shares, available for allocation to Non-Institutional Bidders.

Non-Residents All eligible Bidders that are persons resident outside India, as defined under FEMA, including Eligible NRIs, FIIs and FVCIs.

NRE Account Non-Resident External Account. NRI or Non-Resident Indian A person resident outside India, as defined under FEMA, and who is a

citizen of India or a person of Indian origin, as such terms are defined under the Foreign Exchange Management (Deposit) Regulations, 2000, as amended.

NRO Account Non-Resident Ordinary Account. NSDL National Securities Depository Limited. NSE The National Stock Exchange of India Limited. OCB or Overseas Corporate Body

A company, partnership, society or other corporate body owned directly or indirectly to the extent of at least 60% by NRIs including overseas trusts, in which not less than 60% of beneficial interest is irrevocably held by NRIs directly or indirectly and which was in existence on October 3, 2003 and immediately before such date had taken benefits under the general permission granted to OCBs under the FEMA. OCBs are not permitted to invest in the Issue.

PAN Permanent Account Number. Pay-in Date The Bid/Issue Closing Date with respect to the Bidders whose Margin

Amount is 100% of the Bid Amount and the last date specified in the CAN with respect to the Bidders whose Margin Amount is less than 100% of the Bid Amount.

Pay-in Period (i) With respect to Bidders whose Margin Amount is 100% of the Bid Amount, the period commencing on the Bid/Issue Opening Date and extending until the Bid Closing Date; and

(ii) With respect to Bidders whose Margin Amount is less than 100% of the Bid Amount, the period commencing on the Bid/Issue Opening Date and extending until the closure of the Pay-in Date specified in the CAN.

Pre-IPO Placing The private placement of not more than 2,850,000 Equity Shares for cash consideration in Indian Rupees to selected investors to be completed prior to filing the Red Herring Prospectus with the RoC. The details of such Pre-IPO Placing, if any, will be included in the Red Herring Prospectus.

Price Band The price band with a minimum price (Floor Price) of Rs.[●] per Equity Share and the maximum price (Cap Price) of Rs.[●] per Equity Share, and any revision to such Floor Price or Cap Price as permitted under the SEBI Guidelines.

Pricing Date The date on which the Issue Price is finalized by the Company, in consultation with the BRLMs and the CBRLMs.

Prospectus The prospectus to be filed with the RoC after the Pricing Date containing, inter alia, the Issue Price, the size of the Issue and certain other information.

Public Issue Account The account opened with the Bankers to the Issue to receive monies from the Escrow Account(s) on the Designated Date.

QIBs or Qualified Institutional Buyers

As defined under the SEBI Guidelines and includes public financial institutions (defined under Section 4A of the Companies Act), FIIs, scheduled commercial banks, mutual funds, multilateral and bilateral development financial institutions, VCFs, FVCIs, state industrial development corporations, insurance companies registered with the Insurance Regulatory and Development Authority, provident funds with a

v

Term Description minimum corpus of Rs.250 million and pension funds with a minimum corpus of Rs.250 million.

QIB Margin Amount An amount representing at least 10% of the Bid Amount, which QIBs are required to pay at the time of submission of a Bid.

QIB Portion The portion of the Issue being at least 60% of the Net Issue consisting of [●] Equity Shares, to be allotted to QIBs on a proportionate basis.

Refund Account An account opened with the Refund Bank, from which refunds of the whole or part of the Bid Amount, if any, shall be made.

Refund Bank [●]. Registrar or Registrar to the Issue

Karvy Computershare Private Limited.

Retail Individual Bidders Bidders (including HUFs) who have bid for an amount less than or equal to Rs.100,000.

Retail Portion The portion of the Issue being not less than 30% of the Net Issue consisting of [●] Equity Shares, available for allocation to Retail Individual Bidder(s).

Revision Form The form used by the Bidders to modify the quantity of Equity Shares or the Bid Price in any of their Bid-cum-Application Form or any previous Revision Form.

RHP or Red Herring Prospectus

The red herring prospectus dated [●], issued in accordance with Section 60B of the Companies Act, which does not have complete particulars of the price at which the Equity Shares are offered, and the size of the Issue. The Red Herring Prospectus will be filed with the RoC at least three days before the Bid/Issue Opening Date.

RoC The Registrar of Companies, Gujarat, Dadra and Nagar Haveli located at Ahmedabad.

RTGS Real Time Gross Settlement. SBI CAPS SBI Capital Markets Limited. SCRA The Securities Contracts (Regulation) Act, 1956, as amended. SCRR The Securities Contracts (Regulation) Rules, 1957, as amended. SEBI The Securities and Exchange Board of India, constituted under the SEBI

Act. SEBI Act The Securities and Exchange Board of India Act, 1992, as amended. SEBI Guidelines The Securities and Exchange Board of India (Disclosure and Investor

Protection) Guidelines, 2000, as amended. Securities Act The U.S. Securities Act of 1933, as amended. SICA The Sick Industrial Companies (Special Provisions) Act, 1985, as

amended. Stock Exchanges The BSE and the NSE. Syndicate Agreement The agreement to be entered into among the Company and the members

of the Syndicate, in relation to the collection of Bids in this Issue. Syndicate Members [●]. Syndicate or members of the Syndicate

The BRLMs, the CBRLMs and the Syndicate Members.

Takeover Code The Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 1997, as amended.

TRS or Transaction Registration Slip

The slip or document issued by any of the members of the Syndicate to a Bidder as proof of registration of the Bid.

Underwriters The BRLMs, the CBRLMs and the Syndicate Members. Underwriting Agreement The agreement among the Underwriters and the Company to be entered

into on or after the Pricing Date. US GAAP Generally accepted accounting principles in the United States of America. VCFs Venture Capital Funds (as defined under the Securities and Exchange

vi

Term Description Board of India (Venture Capital Funds) Regulations, 1996, as amended) registered with SEBI.

Industry Related Terms

Term Description Aframax An oil tanker with capacity between 80,000 DWT and 120,000 DWT

largely used in the basins of the Black Sea, the North Sea, the Caribbean Sea, the China Sea and the Mediterranean.

AHTS Anchor Handling Tug Supply. Capesize Cargo ships that are too large to traverse either the Suez Canal or the

Panama Canal, and that have to traverse either through the Cape of Good Hope or Cape Horn.

DWT Dead weight tonnage. GMB Gujarat Maritime Board, an authority constituted by the Government of

Gujarat pursuant to the Gujarat Maritime Board Act, 1981. IMO International Maritime Organization. KOMAC Korea Maritime Consultants Co. Limited. LNG Liquefied Natural Gas. Malaccamax The maximum size of a ship capable of transiting the straits of Malacca. NMDP National Maritime Development Programme. OSV Offshore supply vessel. Panamax The maximum size of a ship capable of transiting the Panama Canal. Suezmax The maximum size of a ship capable of transiting the Suez Canal. ULCC Ultra large crude carrier. VLCC Very large crude carrier.

Other Abbreviations/Terms

Term Description A/c Account. AGM Annual general meeting. Air Act The Air (Prevention and Control of Pollution) Act, 1981, as amended. AS Accounting Standards as issued by the Institute of Chartered Accountants

of India. Bonus Act The Payment of Bonus Act, 1965, as amended. BPLR Below Prime Lending Rate. CAGR Compound annual growth rate. CLRA The Contract Labour (Regulation and Abolition) Act, 1970, as amended. EBITDA Earnings Before Interest, Tax, Depreciation and Amortization. EGM Extraordinary general meeting. EPS Earnings per share. ESI Act The Employees State Insurance Act, 1948, as amended. Factories Act The Factories Act, 1948, as amended. FIPB The Foreign Investment Promotion Board of the Government of India. GOI or Government Government of India. Gratuity Act The Payment of Gratuity Act, 1972, as amended. HUF Hindu Undivided Family. IPO Initial Public Offering. IT Information technology. I.T. Act The Income Tax Act, 1961, as amended. I.T. Rules The Income Tax Rules, 1962, as amended. LIBOR London Interbank Offered Rate.

vii

Term Description NA Not Applicable. NAV Net Asset Value. p.a. Per annum. P/E Ratio Price/Earnings Ratio. PLR Prime Lending Rate. RBI The Reserve Bank of India. RoNW Return on Net Worth. Water Act The Water (Prevention and Control of Pollution) Act 1974, as amended.

viii

CERTAIN CONVENTIONS, PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET

DATA, CURRENCY OF PRESENTATION AND EXCHANGE RATES Certain Conventions Unless otherwise specified or the context otherwise requires, all references to “India” in the Draft Red Herring Prospectus are to the Republic of India, together with its territories and possessions, all references to the “US”, the “USA”, the “United States” or the “U.S.” are to the United States of America, together with its territories and possessions and all references to “UK” or “U.K.” are to the United Kingdom of Great Britain and Northern Ireland, together with its territories and possessions. Financial Data Unless indicated otherwise, the financial data in the Draft Red Herring Prospectus is derived from our restated stand alone financial statements prepared in accordance with Indian GAAP, the Companies Act and the SEBI Guidelines included in the section “Financial Statements” beginning on page F-1 of the Draft Red Herring Prospectus. Our fiscal year commences on April 1 and ends on March 31 of the next year, so all references to a particular fiscal year are to the twelve month period ended on March 31 of that year. In the Draft Red Herring Prospectus, any discrepancies in any table between the totals and the sum of the amounts listed are due to rounding off. There are significant differences between Indian GAAP and US GAAP; accordingly, the degree to which the Indian GAAP financial statements (consolidated or unconsolidated) included in the Draft Red Herring Prospectus will provide meaningful information is entirely dependent on the reader’s level of familiarity with Indian accounting practices, Indian GAAP, the Companies Act and the SEBI Guidelines. Any reliance by persons not familiar with Indian accounting practices, Indian GAAP, the Companies Act and the SEBI Guidelines on the financial disclosures presented in the Draft Red Herring Prospectus should accordingly be limited. The Company has not attempted to quantify those differences or their impact on the financial data included herein, and you should consult your own advisors regarding such differences and their impact on our financial data. For more information on these differences, see the section “Summary of Significant Differences between Indian GAAP and US GAAP” beginning on page [●] of the Draft Red Herring Prospectus. Industry and Market Data Unless stated otherwise, market and industry related data used in the Draft Red Herring Prospectus has been obtained or derived from publicly available documents and other industry sources. Industry sources and publications generally state that the information contained therein has been obtained from sources generally believed to be reliable, but their accuracy, completeness and underlying assumptions are not guaranteed and their reliability cannot be assured and accordingly, investment decisions should not be based on such information. Although the Company believes that the industry data used in the Draft Red Herring Prospectus is reliable, it has not been verified by us or any other person connected with the Issue. Further, the extent to which the market and industry data used in the Draft Red Herring Prospectus is meaningful depends on the reader’s familiarity with and understanding of the methodologies used in compiling such data. There are no standard data gathering methodologies in the industry in which we conduct our business and methodologies and assumptions may vary widely among different industry sources.

ix

Currency of presentation All references to “Rupees”, “Rs.” or “INR” are to Indian Rupees, the official currency of the Republic of India. All references to “$”, “US$”, “USD” or “U.S. Dollars” are to United States Dollars, the official currency of the United States of America. All references to “EURO”, “euro” or “Euro” are to the official currency of the European Union. All references to “KZT” are to Kazakhstan Tenge, the official currency of the Republic of Kazakhstan. All references to “SGD” are to Singapore Dollars, the official currency of the Republic of Singapore. All references to “GBP” are to the Pound Sterling, the official currency of the United Kingdom. All references to “Riyal” are to the official currency of the Kingdom of Saudi Arabia. Exchange Rates The Draft Red Herring Prospectus contains translations of certain U.S. Dollar, Euro and other currency amounts into Indian Rupees. These have been presented solely to comply with the requirements of Clause 6.9.7.1 of the SEBI Guidelines. These translations should not be construed as a representation that such currency could have been, or could be, converted into Indian Rupees, at any particular rate or at all. Unless otherwise stated, we have in this Draft Red Herring Prospectus used a conversion rate of Rs.40.44 for one U.S. Dollar as of July 31, 2007. (Source: Reserve Bank of India as of July 31, 2007 available at http://www.rbi.org.in/scripts/ReferenceRateArchive.aspx).

x

FORWARD LOOKING STATEMENTS The Draft Red Herring Prospectus contains certain “forward looking statements”. These forward looking statements can generally be identified by words or phrases such as “will”, “aim”, “will likely result”, “believe”, “expect”, “will continue”, “anticipate”, “estimate”, “intend”, “plan”, “contemplate”, “seek to”, “future”, “objective”, “goal”, “project”, “should”, “will pursue” and similar expressions or variations of such expressions. Similarly, statements that describe our objectives, strategies, plans or goals are also forward looking statements. All forward looking statements are subject to risks, uncertainties and assumptions about us that could cause our actual results to differ materially from those contemplated by the relevant forward looking statement. Important factors that could cause actual results to differ materially from our expectations include, among others: • Our ability to raise finances to fund our planned capital expenditures; • Our ability to successfully implement our strategy and plan to complete the construction of the Pipavav

Shipyard as per schedule; • Our lack of an operating history or prior experience in ship building, ship repair or the Offshore

Business; • Our reliance on third party contractors and strategic partners; • Changes in the availability and price of our raw materials; • Our dependence on a limited number of customers and loss of business from significant customers; • Changes in the interest rates and the exchange rates; • Changes in laws and regulations that apply to shipbuilding industries; • Increasing competition in and the conditions of the Indian and global ship building industry; • Increase in labor costs; • Labor unrest or other difficulties; and • General economic and business conditions in India and other countries. For a further discussion of factors that could cause our actual results to differ, see the sections “Risk Factors”, “Our Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” beginning on pages [●], [●] and [●], respectively, of the Draft Red Herring Prospectus. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated. Forward looking statements speak only as of the date of the Draft Red Herring Prospectus. None of the Company, its Directors, its officers, any Underwriter, or any of their respective affiliates or associates has any obligation to update or otherwise revise any statement reflecting circumstances arising after the date hereof or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to fruition. In accordance with SEBI requirements, the Company, the BRLMs and the CBRLMs will ensure that investors in India are informed of material developments until the commencement of listing and trading.

xi

SECTION II: RISK FACTORS

RISK FACTORS An investment in the Equity Shares involves a high degree of risk. You should carefully consider all the information in the Draft Red Herring Prospectus, including the risks described below before making an investment decision. If any of the risks described below actually occur, our business, prospects, financial condition and results of operations could be seriously harmed, the trading price of our Equity Shares could decline, and you may lose all or part of your investment.

Unless specified or quantified in the relevant risk factors below, we are not in a position to quantify the financial or other implication of any of the risks described in this section.

Any potential investor in, and purchaser of, our Equity Shares should pay particular attention to the fact that we are governed in India by a legal and regulatory environment which in some material respects may be different from that which prevails in the United States and other countries. In addition, the risks set out in the Draft Red Herring Prospectus may not be exhaustive and additional risks and uncertainties not presently known to us, or which we currently deem to be immaterial, may arise or may become material in the future. This section has been numbered solely for convenience only and the order in which the risks appear does not reflect the prioritization of any risk.

Risks Relating to Our Company and Its Business

1. There are certain legal proceedings and regulatory actions against our Directors, our Promoters and certain Promoter Group companies. There are outstanding legal proceedings against our Directors, our Promoters and Promoter Group companies. These proceedings are pending at different levels of adjudication before various courts, tribunals, enquiry officers and appellate tribunals. An adverse outcome in any of these litigations could have a material adverse effect on the Directors and Promoters, as well as on our business, prospects, financial condition and results of operations and that of the Promoter Group companies. For further details on these proceedings, see the section “Outstanding Litigation and Material Developments” beginning on page [●] of this Draft Red Herring Prospectus. Proceedings/Regulatory Actions involving the Directors There are criminal proceedings pending against certain of our Directors. There are certain other regulatory actions, including in relation to securities laws, involving certain Directors of our Company in their capacity as directors of other companies, including in relation to the suspension of trading of the equity shares of Horizon Infrastructure Limited by the NSE. Please see the section “Outstanding Litigation and Material Developments” beginning on page [●] of the Draft Red Herring Prospectus. Proceedings involving the Promoters Please see the section “Outstanding Litigation and Material Developments” beginning on page [●] of the Draft Red Herring Prospectus. Proceedings involving the members of the Promoter Group Please see the section “Outstanding Litigation and Material Developments” beginning on page [●] of the Draft Red Herring Prospectus. 2. We may be unable to raise finances to fund our planned capital expenditure.

The proceeds received in connection with the Issue will cover only a part of our planned capital expenditure. We will require additional debt and equity funding to fund future expansion (including the

xii

development of the second dry dock), operational needs and debt service payments. The amount of such additional required funding will depend on whether the shipyard construction project is completed within budget, the timing of completion of the construction of the Pipavav Shipyard and commencement of our revenue generating operations, any further investments we may make, and the amount of cash flow from our operations in the future. If delays and cost overruns are significant, the additional funding we would require could be substantial. Additional debt funding may not be available as and when required and, if incurred, would result in increased debt service obligations and could result in additional operating and financing covenants, or liens on our assets, that would restrict our operations. The sale of additional equity securities could result in additional dilution to our shareholders.

Our ability to obtain required funding on acceptable terms is subject to a number of uncertainties, including:

• Limitations on our ability to incur additional debt, including as a result of prospective lenders’ evaluations of our creditworthiness and pursuant to restrictions on incurrence of debt in our existing and anticipated credit arrangements;

• Investors’ and lenders’ perception of, and demand for, debt and equity securities of shipbuilding companies and companies engaged in the Offshore Business, as well as the offerings of competing financing and investment opportunities in India by our competitors;

• Conditions in the Indian and international capital markets in which we may seek to raise funds;

• Our future results of operations, financial condition and cash flows; and

• Economic, political and other conditions in India and internationally.

Without required funding, we may not be able to:

• complete the development of the Pipavav Shipyard;

• commence or continue our operations;

• hire, train and retain employees;

• obtain or complete any vessel construction orders or orders for our Offshore Business products;

• market our products; or

• respond to competitive pressures or unanticipated funding requirements.

We cannot assure you that necessary financing will be available in amounts or on terms acceptable to us, or at all. If we fail to raise additional funds in such amounts and at such times as we may need, we may be forced to reduce our capital expenditures and construction to a level that can be supported by our currently available funding sources and delay the construction of the Pipavav Shipyard, which may result in our inability to meet drawing conditions under our current loan facilities or default and exercise of remedies by the lenders under our loan facilities. In that event, we may be unable to complete our projects under construction and could suffer a partial or complete loss of our investments in our projects.

3. We may not be able to execute our plan to complete the construction of the Pipavav Shipyard as scheduled or at all.

A key part of our strategy is dependent upon the timely completion of the Pipavav Shipyard, which is expected to be completed in October 2008. However, we cannot assure you that the construction of the

xiii

Pipavav Shipyard will be completed as scheduled, or that it will become operational or operate as efficiently as planned. The construction and timely completion of Pipavav Shipyard will be subject to engineering, construction and other commercial risks, including:

• the availability of financing on acceptable terms;

• reliance on third parties to construct and complete, among other things, the fabrication, block building and dry dock facilities as well as the facilities required for the Offshore Business;

• reliance on arrangements with certain strategic partners for technical assistance and other operational needs;

• reliance on Punj Lloyd Limited (“Punj Lloyd”) to facilitate our entry into the Offshore Business;

• construction and development delays or defects;

• engineering design and technological changes;

• mobilizing the required resources, including housing and training a large workforce;

• failure to obtain necessary governmental and other approvals;

• changes in market conditions;

• disputes with and defaults by contractors and subcontractors;

• environmental, health and safety issues, including site accidents;

• infrastructure and transport delays;

• actions of our competitors;

• accidents, natural disasters and weather-related delays;

• time and cost overruns and unanticipated expenses; and

• regulatory changes.

We intend to undertake concurrent construction of our fabrication, assembly and dry docks facilities simultaneously with the construction of vessels for our customers. Accordingly, any delay in the construction of any of these facilities will delay the manufacturing and delivery of vessels to customers. As of the date of the Draft Red Herring Prospectus, we had aggregate orders of approximately US$1,063.12 million (Rs.42,992.6 million) for the construction of 26 Panamax bulk carriers (including options for four ships which have been exercised) for delivery from 2009 to May 2012. We would not be able to meet these orders if the Pipavav Shipyard is not completed as planned. Any delay in the completion and delivery of the vessels under our shipbuilding contracts will result in our being liable to pay our customers damages, liquidated or otherwise. If the delay continues beyond the time stipulated in the contracts, our customers may terminate their vessel construction contracts. In addition, the timely completion of the Pipavav Shipyard would also be essential for us to start bidding for contracts for our Offshore Business products. Accordingly, any delay in the construction of the Pipavav Shipyard would have an adverse impact on our reputation and could have a material adverse effect on our business, financial condition, results of operation and prospects.

xiv

4. We rely heavily on third-party contractors and their sub-contractors for the timely completion of our shipyard. Any default by our contractors or suppliers could materially and adversely affect our ability to execute our shipbuilding and Offshore Business orders and contracts.

We rely upon third-party contractors for the construction of the proposed facilities at the Pipavav Shipyard. We also expect to sub-contract certain portions of our vessel construction and Offshore Business fabrication projects. Although we may sub-contract work, in accordance with the terms of the contracts with our customers, we will be responsible for the deliverables by such sub-contractors. Accordingly, any acts or omissions by our sub-contractors could expose us to liability including for delays, sub-standard workmanship, injury and damage and those arising from termination of these construction contracts. Our contractors and sub-contractors may face difficulties and competition in finding qualified construction labor or materials and sub-components at acceptable cost and consequently use sub-standard or defective materials and sub-components or the employment of under-qualified or less skilled workers.

We also intend to use third-party providers for the supply of most of our raw materials. Transportation strikes by members of various truckers’ unions have had in the past, and could have in the future, an adverse effect on our receipt of raw materials and equipment and our ability to deliver our products in a timely manner. In addition, transportation costs have been steadily increasing. Continuing increases in transportation costs may have an adverse effect on our business and results of operations. Our reliance on third-party contractors, sub-contractors and other third party providers may subject us to construction delays which are beyond our control. Any such delay may lead to cost overruns. Furthermore, any default on part of our sub-contractors and providers may expose us to liability.

We have placed bulk orders for the supply of parts for the ships to be built by us with a limited number of suppliers. Any failure on the part of one or more of our suppliers to make timely delivery in accordance with our specifications would expose us to the risk of default under our shipbuilding contracts, which could give rise to liquidated damages, other liability and cost overruns and harm our reputation. Any of the foregoing may have a material adverse effect on our business, results of operations and financial condition.

5. We have no track record or prior experience in shipbuilding or repair activities, or in the Offshore Business.

We have no prior experience in shipbuilding or repair activities or in the Offshore Business. We will face managerial, technical and logistical challenges while implementing our construction projects, and in the absence of prior experience, we may not be able to efficiently handle such challenges. Any failure on our part to effectively meet the challenges posed by technical and other processes involved in our shipbuilding or repair activities and the Offshore Business could cause disruptions to our business and could be detrimental to our long-term business outlook. Additionally, in view of the factors stated above, we may not be able to meet our vessel construction schedules and may face delays in the delivery of vessels to our customers. Similar delays could occur in relation to the Offshore Business. We may also face difficulties qualifying as an approved supplier which could require us to discount in order to win business, thereby adversely affecting our results of operations. Any of the foregoing may have a material adverse effect on our business, prospects, results of operations and financial condition.

6. We have no operating history; it is difficult to estimate our future performance.

We have no operating history from which you can evaluate our business, future prospects and viability and you should not evaluate our prospects and viability based on the performance of our Promoters and Promoter Group Companies, existing shareholders or strategic partners. Furthermore, we have not commenced commercial operations and, in accordance with Indian GAAP, we do not record revenue and do not maintain a Profit & Loss Account. As a result, our future revenue and profitability are difficult to estimate and could fluctuate significantly and, as a result, the price of our Equity Shares may be volatile. While we intend to complete the construction of the Pipavav Shipyard in October 2008, our prospects must be considered in light of the risks and uncertainties related to completion of our shipyard facilities and our ability to successfully commence and maintain our shipbuilding and repair business and the Offshore

xv

Business. Many of the factors which will affect the foregoing are beyond our control. For example, our business and results of operations may be adversely affected by:

• economic downturns or stagnant economies in India and global markets;

• a decrease in demand for our vessels in the Indian and global markets;

• fluctuations in global freight rates;

• a decrease in the demand for offshore platforms, rigs, jackets, vessels for offshore exploration and production by the oil and gas sector;

• reduction in the price of oil and gas in the global market;

• fluctuations in the price and availability of key raw materials, including steel;

• an increase in interest rates at which we can raise debt financing or increases in our existing floating interest rate liabilities;

• adverse fluctuations in the exchange rate of the rupee versus major international currencies, including the U.S. dollar;

• strikes or work stoppages by our employees;

• competition from global and Indian shipbuilders and providers of facilities to the offshore oil and gas sector and increased shipbuilding capacity;

• changes in government policies affecting the shipbuilding industry and/or the upstream oil and gas business in India; and

• accidents, natural disasters or outbreaks of diseases.

Unfavorable changes in any of the above factors may significantly and adversely affect our business and results of operations, which may vary significantly from the expectations of shareholders, market analysts and the investing public.

7. Our construction costs may exceed our budgeted amounts.

The anticipated costs of construction of our facilities are based on budgets, estimates and numerous assumptions. The cost of construction of certain facilities expected at the Pipavav Shipyard was initially appraised by the Industrial Development Bank of India Limited ("IDBI") in July 2006. However, following such appraisal, we decided to include additional facilities in our construction plan which resulted in a significant increase in our capital expenditure plans compared to the project costs appraised by IDBI. Our current estimates of project costs and allocation of such costs, as set forth in section “Objects of the Issue,” beginning on page [●] of the Draft Red Herring Prospectus, are higher than the IDBI appraised cost by Rs. 7,925.9 million, and this incremental amount is based on management estimates as well as estimates obtained from third party contractors, and has not been appraised by any bank, financial institution or other independent organization. The actual costs of construction of our facilities may exceed such budgeted amounts due to a variety of factors such as construction delays, adverse changes in raw material costs, interest rates, labor costs, foreign exchange rates, regulatory and environmental factors, weather conditions and our financing needs. Our financial condition, results of operations and liquidity would be materially and adversely affected if our project or construction costs materially exceed such budgeted amounts.

xvi

8. Cyclical trends in the shipbuilding, offshore business and related industries may adversely affect our businesses, profitability and financial condition.

The demand for ships and offshore facilities will be dependent upon many factors, including the financial condition of companies in the shipping, shipbuilding, offshore oil and gas and petrochemical industries, including companies that purchase marine ships and require marine repair and conversion services. Companies in these industries are subject to significant fluctuations in their revenue and profitability due to a variety of factors, including general economic conditions and factors affecting each of these industries individually. Due to the cyclical nature of these industries, we may also get excess orders which we cannot service when there is a boom and may have fewer orders and excess production capacity when there is a downturn in a particular industry.

We expect that freight rates will affect our shipbuilding business. The demand for ships based on freight rates is cyclical in nature and can be difficult to predict. When freight rates are on the rise, ship owners generally place orders for new ships. This generates additional capacity and eventually results in over-capacity. This over-capacity then exerts a downward pressure on freight rates which in turn reduces demand for new ships and causes fleets to shrink. The cycle begins again when shrinking fleets create a capacity shortage, which once again leads to an increase in freight rates and results in an increase in orders for new ships. We may be unable to accurately predict these cycles and this may have an adverse effect on our business. For example, we may incur substantial costs to increase our shipbuilding capacity in anticipation of a rise in freight rates and resultant demand for new ships and, if demand for new ships does not increase or if we are unable to secure sufficient orders for our enhanced shipbuilding capacity, we will be subject to significant operational costs and our revenues could be inadequate to meet our operational needs. Conversely, if we do not expand our capacity sufficiently to meet increased demand, we may be unable to take advantage of market growth. Any of the foregoing could have a material adverse effect on our business, financial condition and results of operations.

Oil prices generally affect the Offshore Business directly, and the shipbuilding industry indirectly. An increase in oil prices often leads to considerable growth in deepwater and sub-sea activity and demand for ships as oil companies increase their oil exploration and production activities. Conversely, when oil and gas prices fall, upstream oil and gas sector companies reduce their offshore exploration and production investments, and also often results in a decrease in demand for ships. We expect to manufacture some vessels that are used in the oil exploration industry. Declining oil or gas prices or declining demand for oil or gas can depress offshore exploration, development and production activities and result in decline in the demand for the products of our Offshore Business by our offshore oil and gas customers, which would have a material adverse effect on our business, prospects, financial condition and results of operations. In addition, significant increases in the price of oil and gas could result in lower worldwide consumption and thus, a decline in demand for crude oil tankers and gas carriers, which could also materially and adversely affect our business, prospects, financial condition and results of operations.

9. Our substantial indebtedness and the conditions and restrictions imposed by our financing and other agreements could adversely affect our ability to conduct our business, financial condition and operations.

We had outstanding long-term indebtedness in the aggregate principal amount of Rs. 3,661.51 million as of November 30, 2007. For information regarding loans taken by us, see the sections “Financial Indebtedness” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” beginning on pages [●] and [●] of this Draft Red Herring Prospectus, respectively. We expect to incur additional substantial indebtedness in the future. Our outstanding term loans of Rs. 1,832.82 million from Housing and Urban Development Corporation Limited (“HUDCO”) were rescheduled in May 2006 and are currently payable in 37 quarterly instalments commencing in February 2008. Our outstanding term loans of Rs. 481.25 million from Infrastructure Leasing & Financial Services Limited (“IL&FS”) were rescheduled in June 2006 and are currently payable in 29 quarterly instalments commencing March 2008. Under our loan agreements with our lenders, revenues of the Pipavav Shipyard have to be routed through a separate account called a “Trust and Retention Account” (“TRA Account”). Monies in the TRA Account can be disbursed to the lenders on default by us under the loans. The documents pertaining to the Pipavav

xvii