Philippine real estate investment project terms for ADMC

27

-

Upload

linkededge -

Category

Business

-

view

1.039 -

download

2

Transcript of Philippine real estate investment project terms for ADMC

30.5 hectares (+): 20.54 hectares, plus an additional 10 hectares

Property Location• This is a 30(+) hectares project centered on a single title 20.54 hectares

– ADMC has the first mortgage on the Property constituting a mortgage subscription receivable (“MSR”) equity to ADMC

– Property value: $54 million (appraisal and exhibits)• http://admc24-7city.com/files/C/roundpeak_property_report_doc-_march_26_2010.pdf• http://admc24-7city.com/files/C/roundpeak_appraisal_exhibits_vitale_valuations_061208.pdf

– MSR value $38 million

• On solid ground and bedrock (not reclaimed land) • ATO height limit of 81.4 m, i.e., 22 to 26 floors, plus 2 below ground• 1.2 km frontage along the Coastal Highway overlooking the Manila Bay• 4 km from the airport and 6 km from the new Las Vegas PAGCOR City, f• 5 km from the Mall of Asia• Property at the start of the C-6 six lane new highway into Cavite and • Property at the start of the 4 lane Alabang Zapote Hwy. • Terminus for planned LRT3 elevated rail from Makati City, through the

airport, is planned to abut the commercial area of the Project construction• 10 minutes drive to the American Embassy on Roxas Blvd.• 15 minutes drive to the center of Makati City, Fort Bonifacio, Global City

Single title property as collateral 20.54 hectares

Security for first stage infrastructure fundingThis is the initial phase financing of a preconstruction development of a “live-

work-play” BPO call center and HR Training campus, for which ADMC is looking for subscribers to a $13.5 million private placement security:

• First mortgage: security with HSBC as Trustee (see mortgage certification)– Supplemental Mortgage Trust Indenture (“SMTI”)– Mortgage participation certificates (“MPC”)

• Collateral: $54 million, 20.54 hectares prime property • Loan to value: “LTV” 25% • Nominal interest prepaid the first year• Title guarantee: Fidelity Title AA rated • Principal guarantee: Malayan Insurance S&P BBB rated, callable end 3 yrs

– Owned by Yuchengco Group of Companies in the Philippines http://ygc.com/, affiliates presented in the following link: http://www.malayan.com/links.html

• Exit: Plan A / Plan B repayment scenarios • ROI: the greater of $4 million per year of funds usage or

– 2.5% of the overall net project profits – which is potentially much greater than the $4 million ROI per year use of funds– when the project construction is completed or before.

“Live-work-play” BPO call center and HR Training city campus projectThe project is designed as an integrated project, 30(+) hectares masterplanned to include• 4 condo towers, 4 serviced apartments (each 50,000 sm) and hotels, 2 medical towers to

support the complex and surrounding area, medical tourism / wellness, 2 marina towers (20,000 sm each), retail and entertainment podium malls (35 hectares) and 4 office towers (50,000 sm each), 11 BPO call center and training towers (16,000 sm to 24,000 sm) and commercial spaces. Total 2.85 million sm.

• Office towers: leasing includes BPO call centers, R&D and Human Resources• HR sourcing and training

– BPO call center workers nationwide in a JV with BPAP to support their vision for the expanding high end market, where trained personnel is a critical key to the growth of high quality BPO call center leasing, includes www.assessmentanalytics.com, www.OmniTouchInternational.com, www.icmi.com

– Hospitality, entertainment, medical, engineering for local and international placement.

• Designated market: Both the self sustaining integrated campus concept as well as support for the surrounding most densely populated area of Metro Manila / Cavite Philippines

• Parallel marketing strategies include both– Leasing minimum of 30,000 sm of BPO call center / office over space will generate a construction of

7 times space and 5 times cash flows for raw space leases (not including utilities)– However, each component of the total is a standalone. – Together, the sum of each standalone marketing component is much greater than the parts.

• Marketing: US, Europe, Philippines and ADMC marketing offices– Cuervo Far East (Cushman & Wakefield), CBRE, Colliers, Jones Lang LaSalle

Sustainable, renewable, Low carbon, Platinum LEEDs “green” ProjectA key factor to the marketing to US and European tenants for the BPO call centers for

the office towers and light manufacturing and R&D outsourcing for the commercial space is the “green” aspect to the Project, including green specialists

• Design engineering:– Ove Arup & Partners HK Ltd– Meinhardt Philippines Inc.

• Construction:– Leighton Contractors (Asia)– Beijing Construction Engineering Group (“BCEG”)

• Quantity surveyor: Davis Langdon Shea• Waste management and recycling:

– Aliron International

• Low carbon footprint: – To reduce the carbon from cement usage, contractors will mix the cement 50/50 with fly

ash for a lighter more fluid non cracking cement, then add polymers to increase hardness by 8x and reduce drying time to 12 hours, thus accelerating speed of construction and reducing concrete required by 30%, cement /carbon by 70%.

• Many other construction innovations and alternative energy technologies– See ADMC 24-7 City Project Overview Pg 5&6

• All utilities will be owned by Singapore REIT with usage charged to tenants.

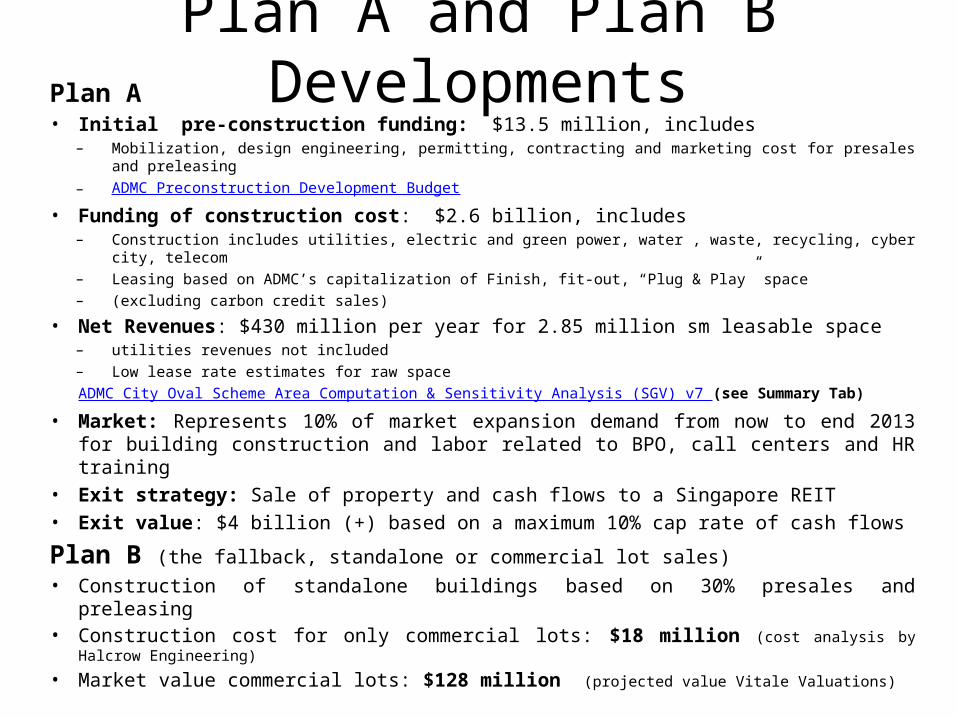

Plan A and Plan B DevelopmentsPlan A • Initial pre-construction funding: $13.5 million, includes

– Mobilization, design engineering, permitting, contracting and marketing cost for presales and preleasing– ADMC Preconstruction Development Budget

• Funding of construction cost: $2.6 billion, includes– Construction includes utilities, electric and green power, water , waste, recycling, cyber city, telecom– Leasing based on ADMC’s capitalization of Finish, fit-out, “Plug & Play” space – (excluding carbon credit sales)

• Net Revenues: $430 million per year for 2.85 million sm leasable space– utilities revenues not included– Low lease rate estimates for raw space

ADMC City Oval Scheme Area Computation & Sensitivity Analysis (SGV) v7 (see Summary Tab)

• Market: Represents 10% of market expansion demand from now to end 2013 for building construction and labor related to BPO, call centers and HR training

• Exit strategy: Sale of property and cash flows to a Singapore REIT• Exit value: $4 billion (+) based on a maximum 10% cap rate of cash flows

Plan B (the fallback, standalone or commercial lot sales)• Construction of standalone buildings based on 30% presales and preleasing• Construction cost for only commercial lots: $18 million (cost analysis by Halcrow Engineering)

• Market value commercial lots: $128 million (projected value Vitale Valuations)

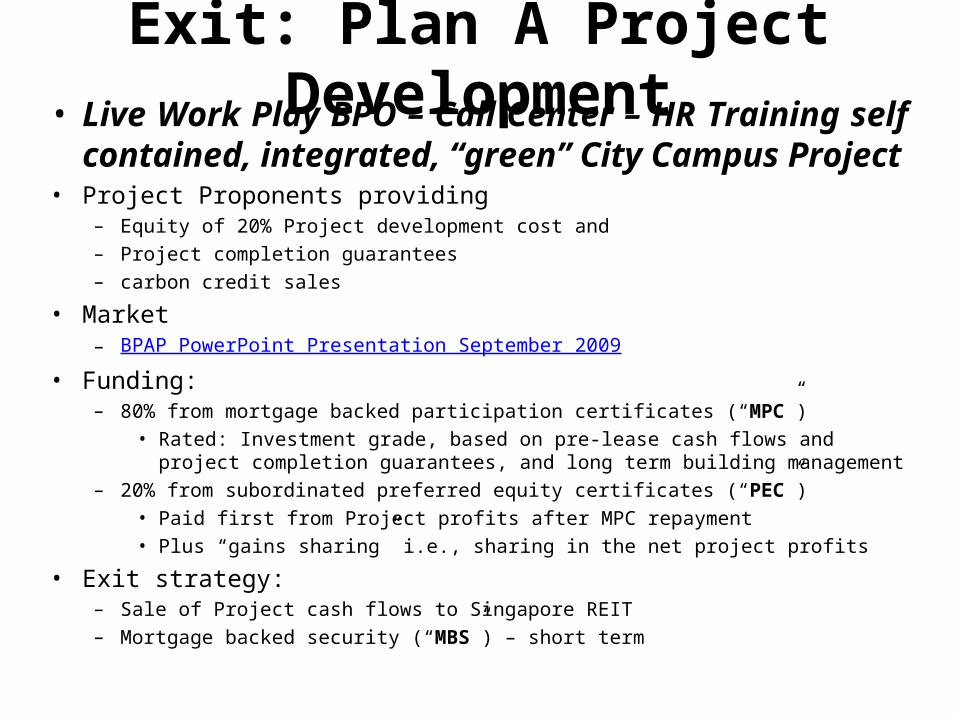

Exit: Plan A Project Development• Live Work Play BPO – Call Center – HR Training self

contained, integrated, “green” City Campus Project• Project Proponents providing

– Equity of 20% Project development cost and – Project completion guarantees– carbon credit sales

• Market– BPAP PowerPoint Presentation September 2009

• Funding:– 80% from mortgage backed participation certificates (“MPC”)

• Rated: Investment grade, based on pre-lease cash flows and project completion guarantees, and long term building management

– 20% from subordinated preferred equity certificates (“PEC”)• Paid first from Project profits after MPC repayment• Plus “gains sharing” i.e., sharing in the net project profits

• Exit strategy: – Sale of Project cash flows to Singapore REIT– Mortgage backed security (“MBS”) – short term

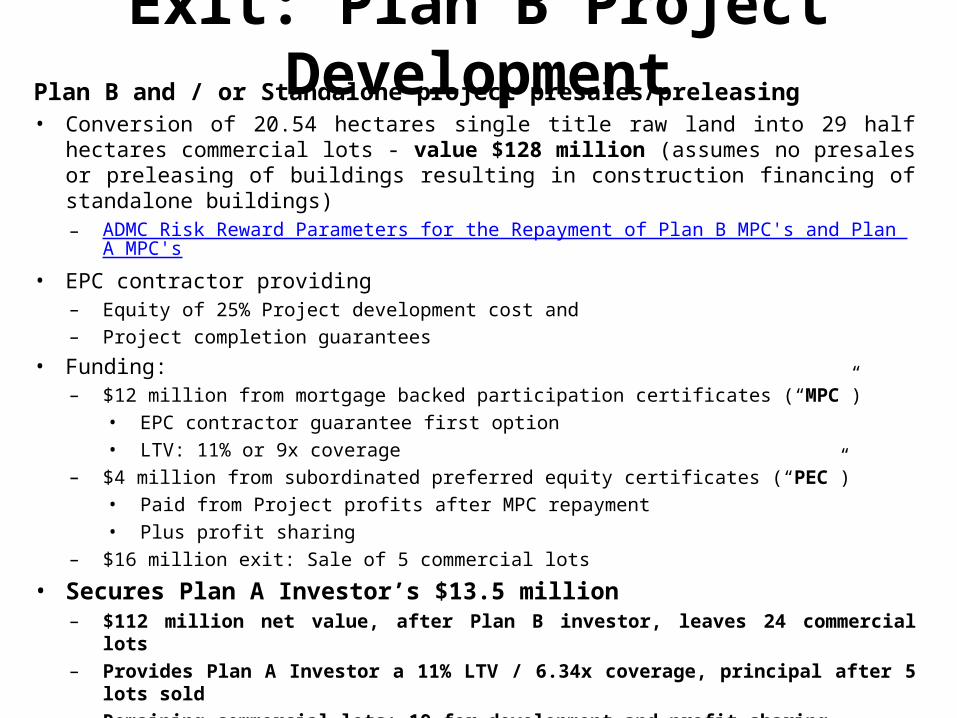

Exit: Plan B Project DevelopmentPlan B and / or Standalone project presales/preleasing• Conversion of 20.54 hectares single title raw land into 29 half hectares commercial lots

- value $128 million (assumes no presales or preleasing of buildings resulting in construction financing of standalone buildings)– ADMC Risk Reward Parameters for the Repayment of Plan B MPC's and Plan A MPC's

• EPC contractor providing– Equity of 25% Project development cost and – Project completion guarantees

• Funding: – $12 million from mortgage backed participation certificates (“MPC”)

• EPC contractor guarantee first option• LTV: 11% or 9x coverage

– $4 million from subordinated preferred equity certificates (“PEC”)• Paid from Project profits after MPC repayment• Plus profit sharing

– $16 million exit: Sale of 5 commercial lots

• Secures Plan A Investor’s $13.5 million – $112 million net value, after Plan B investor, leaves 24 commercial lots– Provides Plan A Investor a 11% LTV / 6.34x coverage, principal after 5 lots sold– Remaining commercial lots: 19 for development and profit sharing

Subscription Receivable

Mortgage Subscription Receivable• SR secured by mortgage trust indenture (“MTI”)• Registration: at time of annotation of MTI on the

property title at the Land Registry• Value MSR: 70% appraised value• Appraised value: $54 million• MSR value = ADMC shares value = $38 million

Subscription to ADMC Preference shares

Preference shares AgreementLandowner ADMC

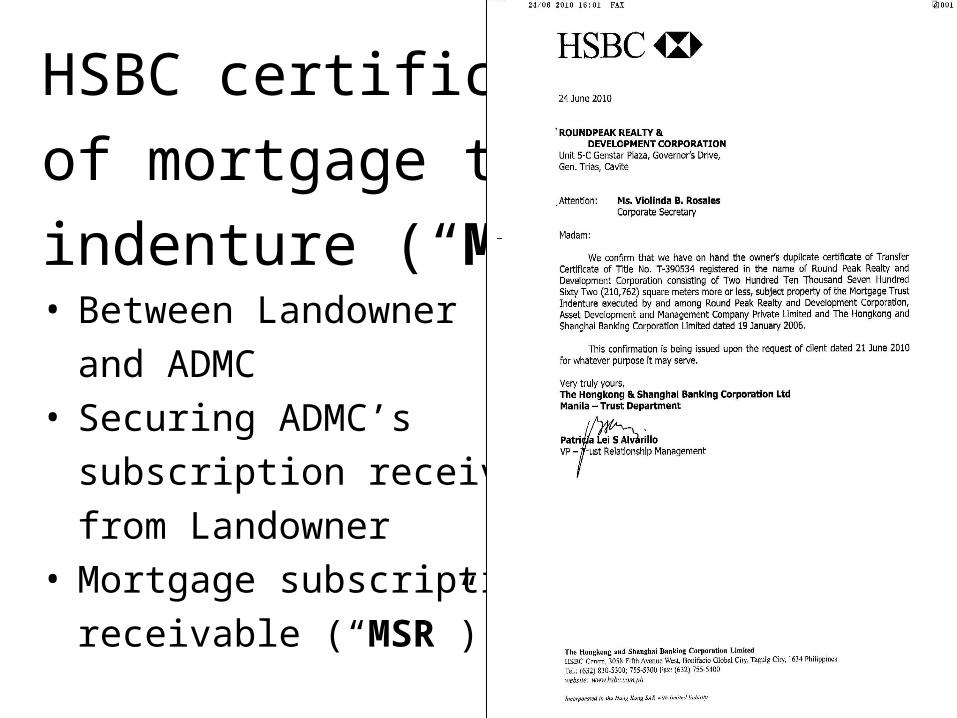

HSBC certificationof mortgage trustindenture (“MTI”)• Between Landowner

and ADMC• Securing ADMC’s

subscription receivablefrom Landowner

• Mortgage subscriptionreceivable (“MSR”)

Consortium: Project Proponents• ADMC and Landowner

– Supplemental Joint property development agreement (“SJPDA”)

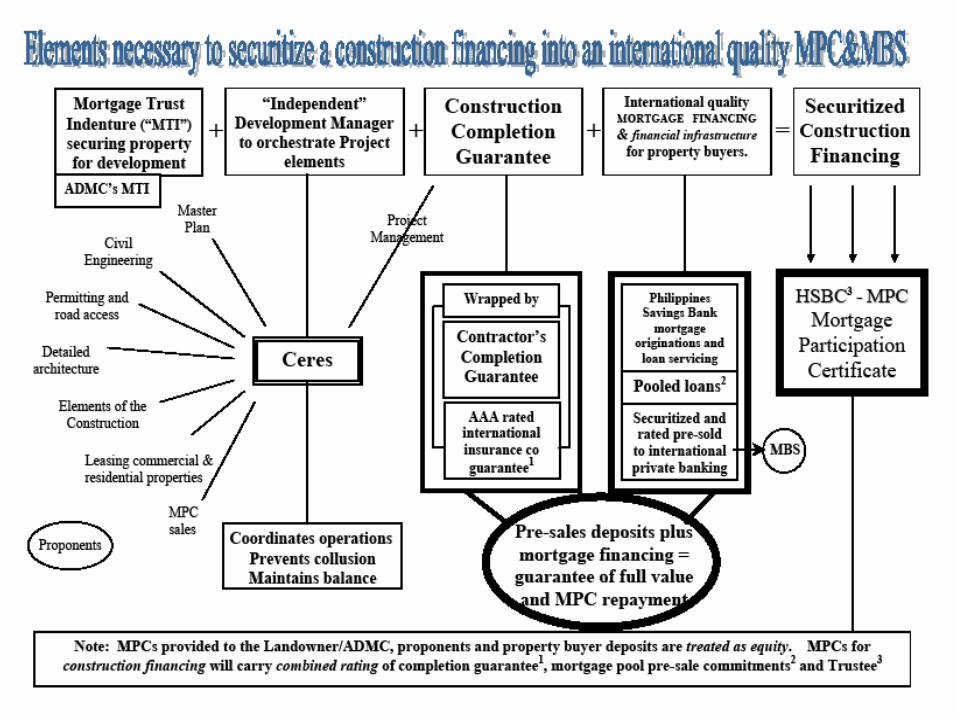

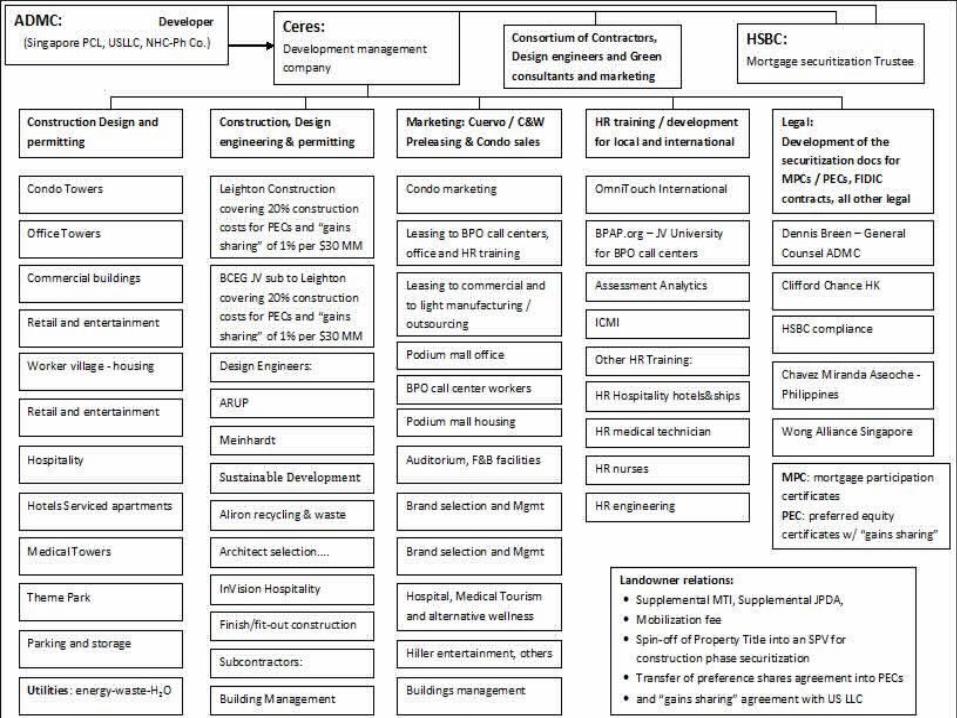

• Development Management Company - Ceres:– Builder of cities: http://admc24-7city.com/files/D/101104_ceres_profile_for_email.pdf – orchestrates entire project from concept, to master plan, to selection of design

engineering team, to negotiation of “open book” contract with EPC contractor, to pre-lease marketing, to MPC marketing, to construction oversight, to eventual sale of Project

• EPC Contractor – Leighton Construction

• The biggest international contractor in the Philippines, Asia and the Middle East• http://www.leightonasia.com/v4/default.asp?lid=1&sec=Locations&subsec=Philippines

– Beijing Construction Engineering Group (“BCEG”)• Owned by the Chinese government – The biggest contractor of China• http://www.bcegc.com/Default.aspx?tabid=635 – http://www.bbbc.com.cn/bceg.php

• Provide Guarantees– Design completion, fixed price “open book” EPC Contract for Plan A– Construction completion for Plan A and Plan B– Equity from payment in PEC for Plan A and Plan B

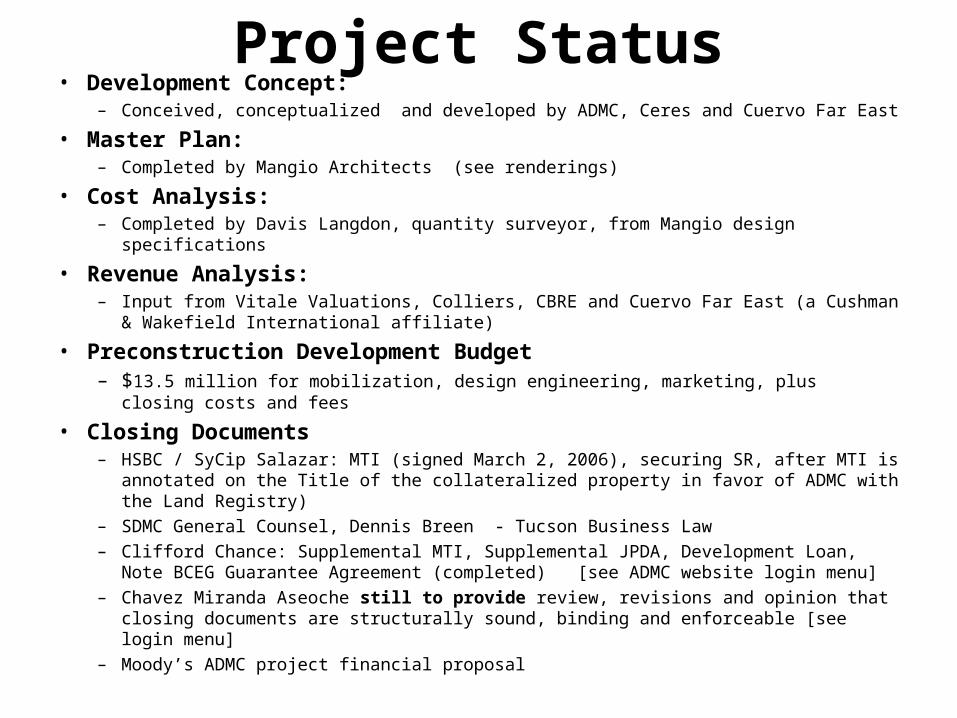

Project Status• Development Concept:

– Conceived, conceptualized and developed by ADMC, Ceres and Cuervo Far East

• Master Plan: – Completed by Mangio Architects (see renderings)

• Cost Analysis: – Completed by Davis Langdon, quantity surveyor, from Mangio design specifications

• Revenue Analysis: – Input from Vitale Valuations, Colliers, CBRE and Cuervo Far East (a Cushman &

Wakefield International affiliate)

• Preconstruction Development Budget– $13.5 million for mobilization, design engineering, marketing, plus closing costs and fees

• Closing Documents– HSBC / SyCip Salazar: MTI (signed March 2, 2006), securing SR, after MTI is annotated on

the Title of the collateralized property in favor of ADMC with the Land Registry)– SDMC General Counsel, Dennis Breen - Tucson Business Law– Clifford Chance: Supplemental MTI, Supplemental JPDA, Development Loan, Note BCEG

Guarantee Agreement (completed) [see ADMC website login menu]– Chavez Miranda Aseoche still to provide review, revisions and opinion that closing

documents are structurally sound, binding and enforceable [see login menu]– Moody’s ADMC project financial proposal

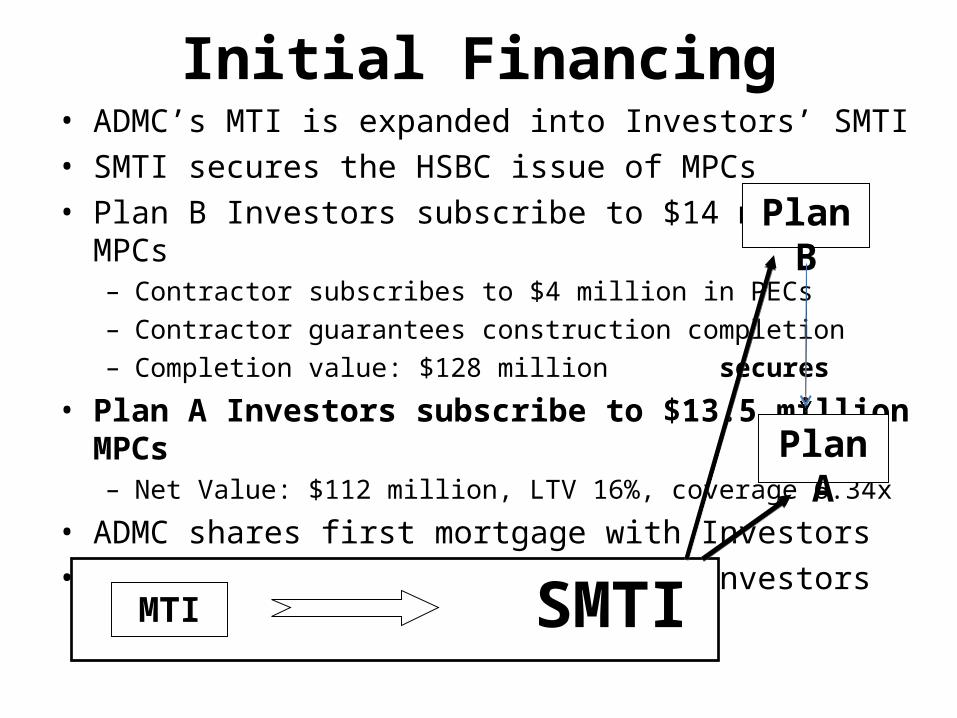

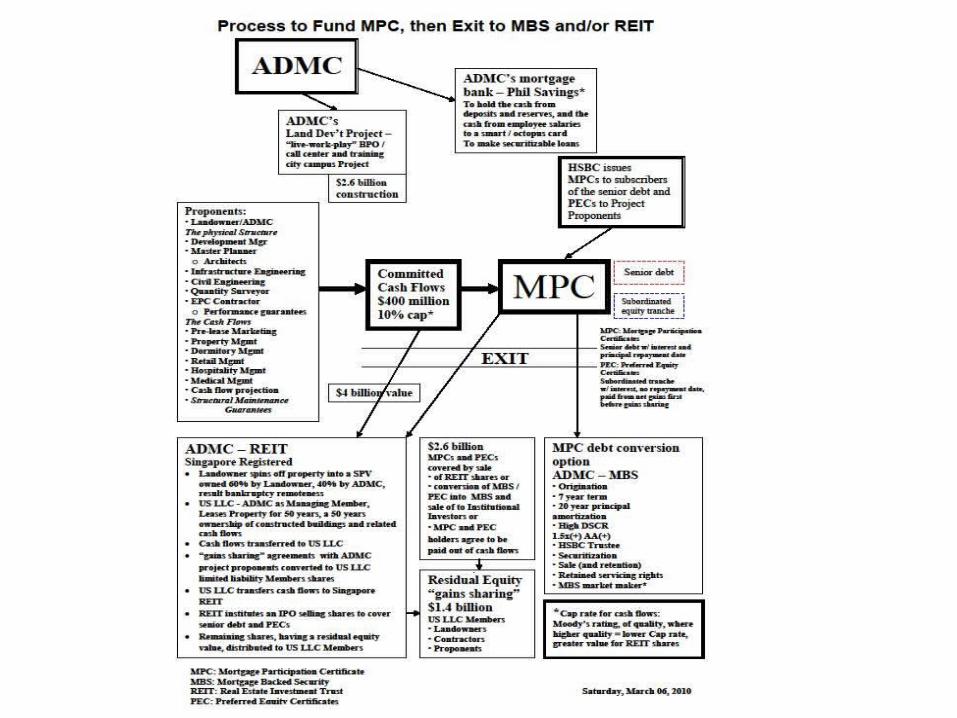

Initial Financing• ADMC’s MTI is expanded into Investors’ SMTI• SMTI secures the HSBC issue of MPCs• Plan B Investors subscribe to $14 million MPCs

– Contractor subscribes to $4 million in PECs– Contractor guarantees construction completion– Completion value: $128 million secures

• Plan A Investors subscribe to $13.5 million MPCs– Net Value: $112 million, LTV 16%, coverage 6.34x

• ADMC shares first mortgage with Investors• ADMC subordinates its rights to Investors

SMTIMTI

Plan B

Plan A

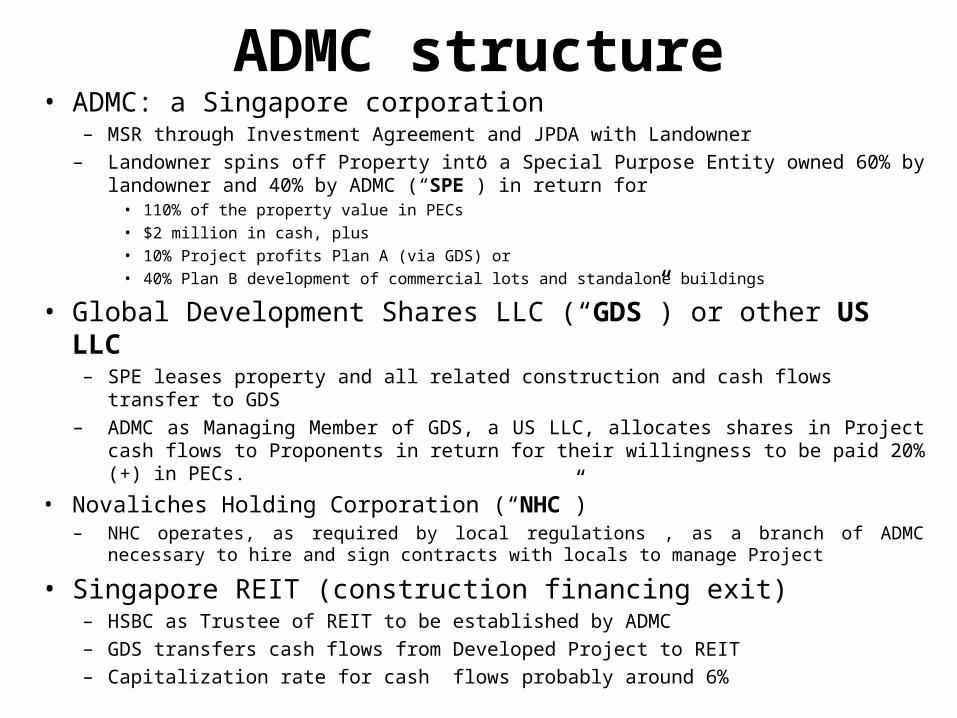

ADMC structure• ADMC: a Singapore corporation

– MSR through Investment Agreement and JPDA with Landowner– Landowner spins off Property into a Special Purpose Entity owned 60% by landowner

and 40% by ADMC (“SPE”) in return for • 110% of the property value in PECs• $2 million in cash, plus • 10% Project profits Plan A (via GDS) or • 40% Plan B development of commercial lots and standalone buildings

• Global Development Shares LLC (“GDS”) or other US LLC– SPE leases property and all related construction and cash flows transfer to GDS– ADMC as Managing Member of GDS, a US LLC, allocates shares in Project cash flows to

Proponents in return for their willingness to be paid 20% (+) in PECs.

• Novaliches Holding Corporation (“NHC”)– NHC operates, as required by local regulations , as a branch of ADMC necessary to hire and

sign contracts with locals to manage Project

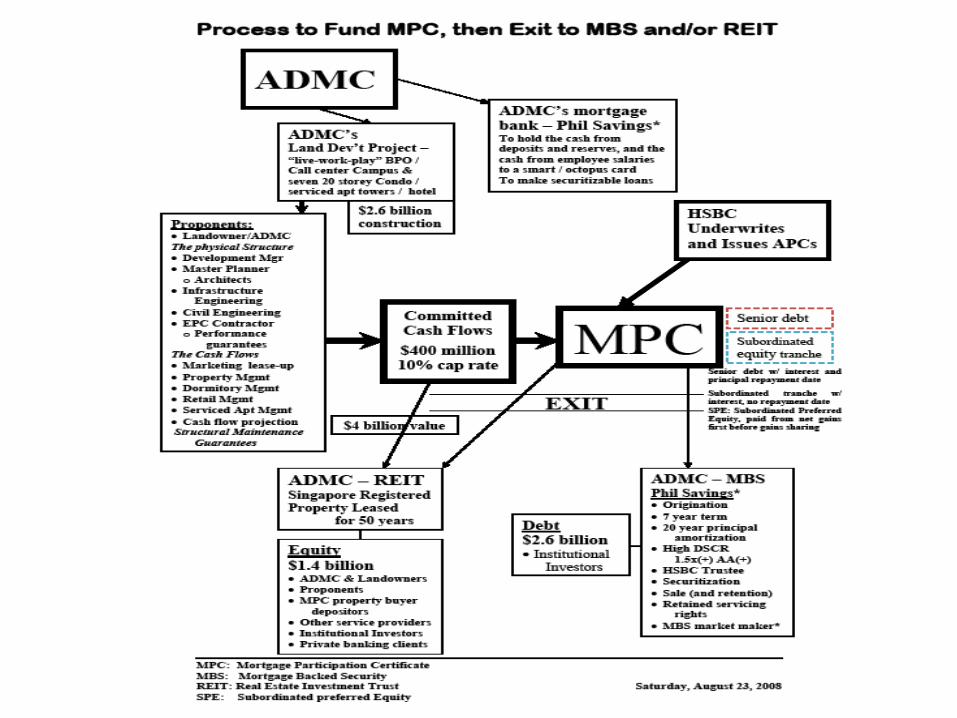

• Singapore REIT (construction financing exit)– HSBC as Trustee of REIT to be established by ADMC– GDS transfers cash flows from Developed Project to REIT– Capitalization rate for cash flows probably around 6%

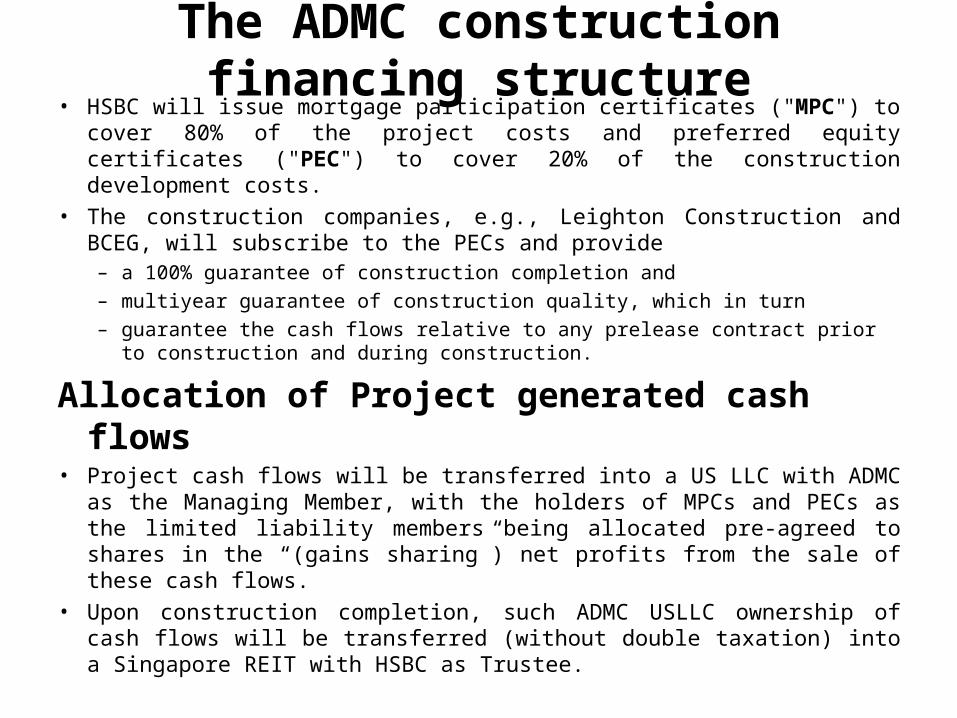

The ADMC construction financing structure• HSBC will issue mortgage participation certificates ("MPC") to cover 80%

of the project costs and preferred equity certificates ("PEC") to cover 20% of the construction development costs.

• The construction companies, e.g., Leighton Construction and BCEG, will subscribe to the PECs and provide – a 100% guarantee of construction completion and – multiyear guarantee of construction quality, which in turn – guarantee the cash flows relative to any prelease contract prior to

construction and during construction.

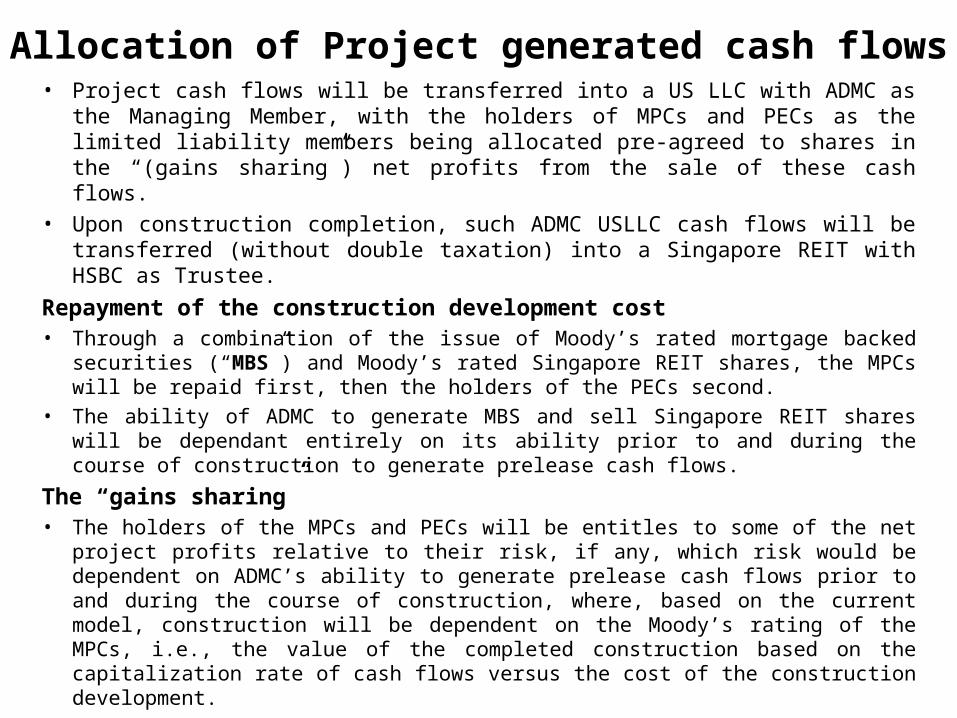

Allocation of Project generated cash flows• Project cash flows will be transferred into a US LLC with ADMC as the

Managing Member, with the holders of MPCs and PECs as the limited liability members being allocated pre-agreed to shares in the “(gains sharing”) net profits from the sale of these cash flows.

• Upon construction completion, such ADMC USLLC ownership of cash flows will be transferred (without double taxation) into a Singapore REIT with HSBC as Trustee.

Allocation of Project generated cash flows• Project cash flows will be transferred into a US LLC with ADMC as the Managing

Member, with the holders of MPCs and PECs as the limited liability members being allocated pre-agreed to shares in the “(gains sharing”) net profits from the sale of these cash flows.

• Upon construction completion, such ADMC USLLC cash flows will be transferred (without double taxation) into a Singapore REIT with HSBC as Trustee.

Repayment of the construction development cost• Through a combination of the issue of Moody’s rated mortgage backed securities

(“MBS”) and Moody’s rated Singapore REIT shares, the MPCs will be repaid first, then the holders of the PECs second.

• The ability of ADMC to generate MBS and sell Singapore REIT shares will be dependant entirely on its ability prior to and during the course of construction to generate prelease cash flows.

The “gains sharing” • The holders of the MPCs and PECs will be entitles to some of the net project profits

relative to their risk, if any, which risk would be dependent on ADMC’s ability to generate prelease cash flows prior to and during the course of construction, where, based on the current model, construction will be dependent on the Moody’s rating of the MPCs, i.e., the value of the completed construction based on the capitalization rate of cash flows versus the cost of the construction development.

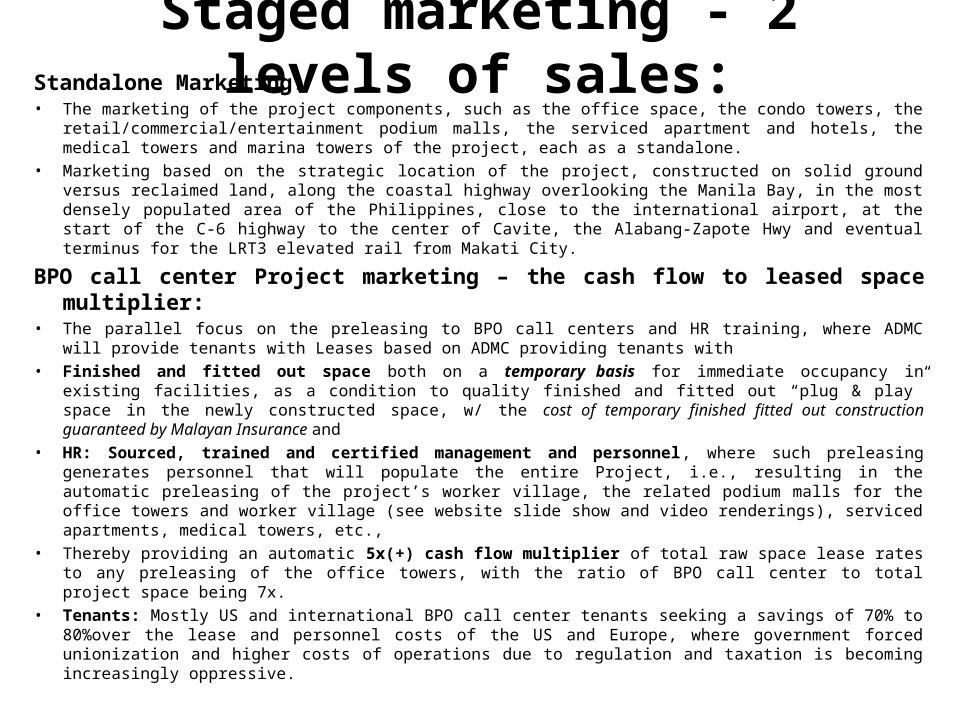

Staged marketing - 2 levels of sales:Standalone Marketing:• The marketing of the project components, such as the office space, the condo towers, the

retail/commercial/entertainment podium malls, the serviced apartment and hotels, the medical towers and marina towers of the project, each as a standalone.

• Marketing based on the strategic location of the project, constructed on solid ground versus reclaimed land, along the coastal highway overlooking the Manila Bay, in the most densely populated area of the Philippines, close to the international airport, at the start of the C-6 highway to the center of Cavite, the Alabang-Zapote Hwy and eventual terminus for the LRT3 elevated rail from Makati City.

BPO call center Project marketing – the cash flow to leased space multiplier:• The parallel focus on the preleasing to BPO call centers and HR training, where ADMC will provide

tenants with Leases based on ADMC providing tenants with• Finished and fitted out space both on a temporary basis for immediate occupancy in existing facilities, as

a condition to quality finished and fitted out “plug & play” space in the newly constructed space, w/ the cost of temporary finished fitted out construction guaranteed by Malayan Insurance and

• HR: Sourced, trained and certified management and personnel, where such preleasing generates personnel that will populate the entire Project, i.e., resulting in the automatic preleasing of the project’s worker village, the related podium malls for the office towers and worker village (see website slide show and video renderings), serviced apartments, medical towers, etc.,

• Thereby providing an automatic 5x(+) cash flow multiplier of total raw space lease rates to any preleasing of the office towers, with the ratio of BPO call center to total project space being 7x.

• Tenants: Mostly US and international BPO call center tenants seeking a savings of 70% to 80%over the lease and personnel costs of the US and Europe, where government forced unionization and higher costs of operations due to regulation and taxation is becoming increasingly oppressive.

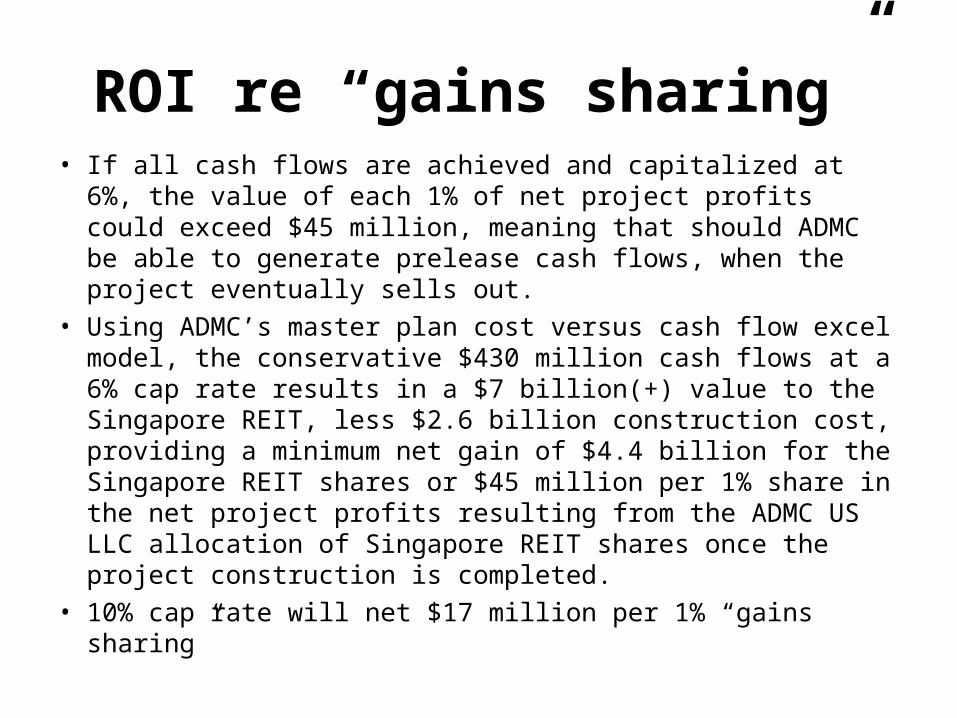

ROI re “gains sharing”• If all cash flows are achieved and capitalized at 6%, the value

of each 1% of net project profits could exceed $45 million, meaning that should ADMC be able to generate prelease cash flows, when the project eventually sells out.

• Using ADMC’s master plan cost versus cash flow excel model, the conservative $430 million cash flows at a 6% cap rate results in a $7 billion(+) value to the Singapore REIT, less $2.6 billion construction cost, providing a minimum net gain of $4.4 billion for the Singapore REIT shares or $45 million per 1% share in the net project profits resulting from the ADMC US LLC allocation of Singapore REIT shares once the project construction is completed.

• 10% cap rate will net $17 million per 1% “gains sharing”

Note: Current ADMC equity - $38 million; March 26, 2010 appraisal - $54 million; HSBC security - $13.5 million

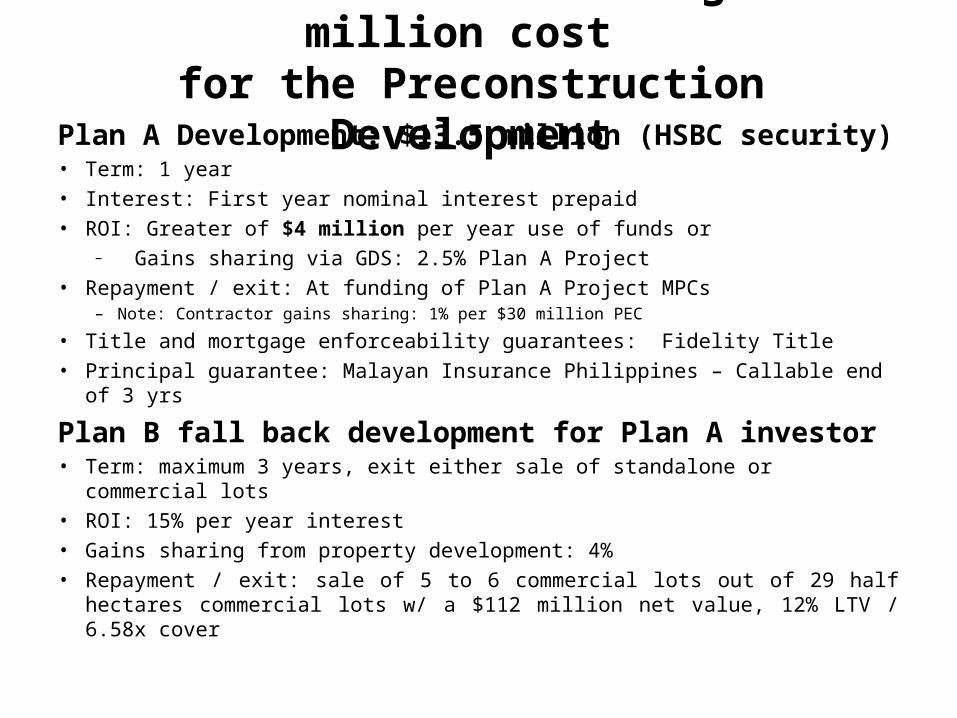

Return to Investor Funding $13.5 million cost for the Preconstruction Development

Plan A Development: $13.5 million (HSBC security)• Term: 1 year• Interest: First year nominal interest prepaid• ROI: Greater of $4 million per year use of funds or

– Gains sharing via GDS: 2.5% Plan A Project• Repayment / exit: At funding of Plan A Project MPCs

– Note: Contractor gains sharing: 1% per $30 million PEC

• Title and mortgage enforceability guarantees: Fidelity Title• Principal guarantee: Malayan Insurance Philippines – Callable end of 3 yrs

Plan B fall back development for Plan A investor• Term: maximum 3 years, exit either sale of standalone or commercial lots• ROI: 15% per year interest• Gains sharing from property development: 4%• Repayment / exit: sale of 5 to 6 commercial lots out of 29 half hectares

commercial lots w/ a $112 million net value, 12% LTV / 6.58x cover

ADMC websiteBPO call center office towers and buildings(see website Project renderings and video)

http://admc24-7city.com Username: (provided)Password: ADMC