board design template 2010 - Cavewire · 400 800 R 1200 1600 NIPPER BOARD R 2000

www.woodmac.com

Delivering commercial insight

Perspectives on US Energy Outlook,

Cocktail Party Issues and Impacts on

E&C Players

October 4, 2011

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 2

2 US Refining and Gasoline Outlook

1 World Oil Outlook

3 US Natural Gas Outlook

4 US NGL Outlook

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 3

Source: Wood Mackenzie

Canada

US

Mexico

North Sea

Brazil

Russia

Thailand

Argentina

Indonesia

Australia

Ghana

Kazakhstan

Egypt

Yemen

Total Non-OPEC

Supply *

2010: 50.48 m b/d

2020: 56.06 m b/d

+5.58 m b/d

*including unconventionals

and Indonesia

Note: Countries included where change is greater than 100,000 b/d

0.10<0.25

m b/d

0.25<0.50

m b/d

0.50< m

b/d

Unconventionals

Oil supply, outside OPEC increases markedly

China

Oman

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 4

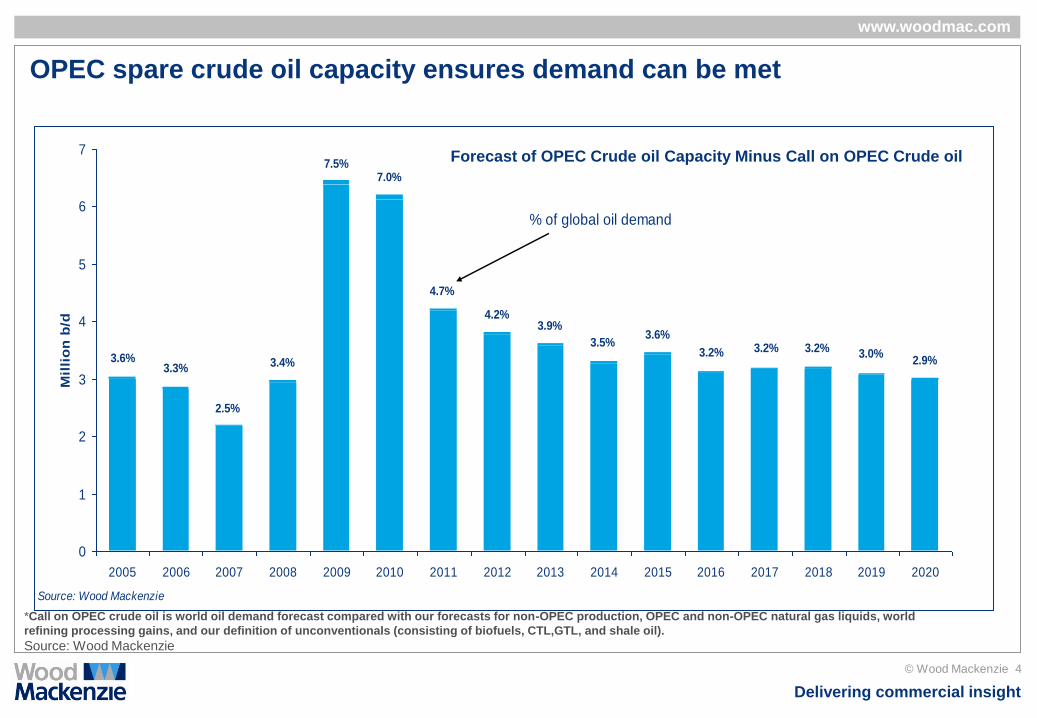

3.6%3.5%

3.9%4.2%

4.7%

7.0%7.5%

3.4%

2.5%

3.3%3.6% 2.9%

3.2% 3.2% 3.2% 3.0%

0

1

2

3

4

5

6

7

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mil

lio

n b

/d

Source: Wood Mackenzie

% of global oil demand

OPEC spare crude oil capacity ensures demand can be met

*Call on OPEC crude oil is world oil demand forecast compared with our forecasts for non-OPEC production, OPEC and non-OPEC natural gas liquids, world

refining processing gains, and our definition of unconventionals (consisting of biofuels, CTL,GTL, and shale oil).

Source: Wood Mackenzie

Forecast of OPEC Crude oil Capacity Minus Call on OPEC Crude oil

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 5

World oil demand forecast shows strong growth

Source: History-IEA, EIA; Forecast-Wood Mackenzie

Demand by Region Demand by Major Sectors

North America

Europe

Advanced Asia

China

India

Other Asia

Middle East

Latin America

Africa

FSU

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

105

1980 1990 2000 2010 2020

Millio

n b

/d

-

10

20

30

40

50

60

1980 1985 1990 1995 2000 2005 2010 2015 2020

millio

n b

/d

Transport Petrochemical Feedstock

Industry & Pow er Generation Residential/Commercial

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 6

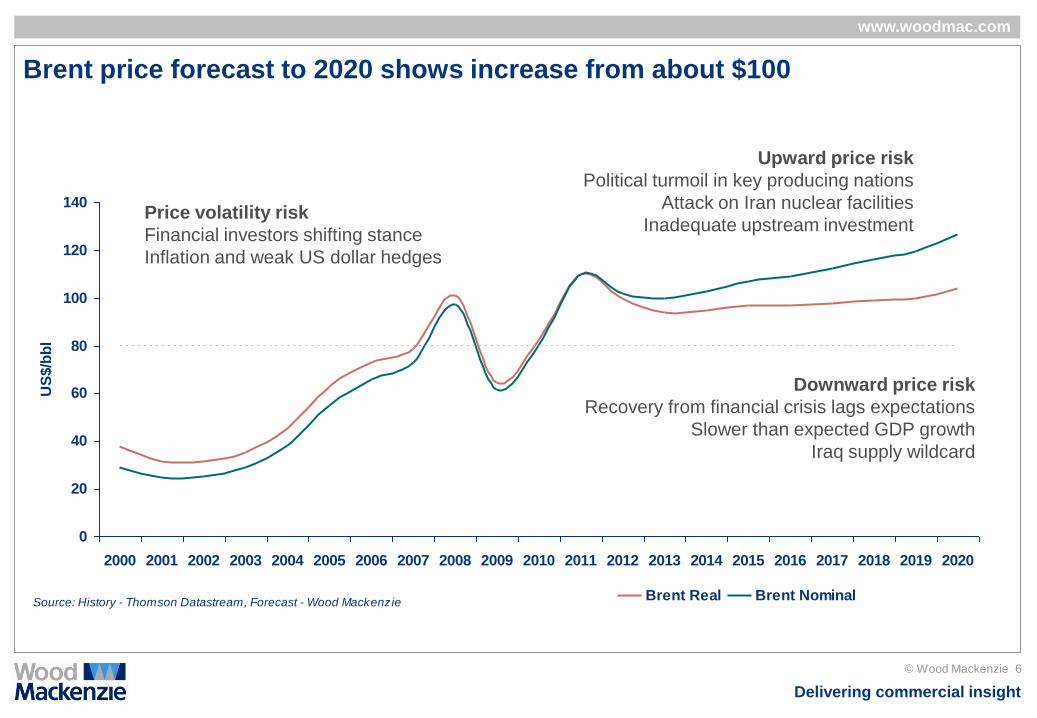

0

20

40

60

80

100

120

140

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

US

$/b

bl

Brent Real Brent NominalSource: History - Thomson Datastream, Forecast - Wood Mackenzie

Brent price forecast to 2020 shows increase from about $100

Price volatility risk

Financial investors shifting stance

Inflation and weak US dollar hedges

Upward price risk

Political turmoil in key producing nations

Attack on Iran nuclear facilities

Inadequate upstream investment

Downward price risk

Recovery from financial crisis lags expectations

Slower than expected GDP growth

Iraq supply wildcard

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 7

COCKTAIL PARTY ISSUE #1: What’s up with WTI?

Cushing constraints dislocate WTI from global oil markets

Brent – WTI spread has multiple drivers

• Rising North America light crude production (WTI ↓)

• US refineries re-positioning (WTI ↓)

• Strong Asian oil demand growth (Brent ↑)

• Libya production off-line (Brent ↑)

Widening spread helps inland refiners

• Buy crude on a WTI basis

• Product import competition (from USGC) indexed off Brent

Brent – WTI Price Spread

-5

0

5

10

15

20

25

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

$/bbl

Source: Platts, Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 8

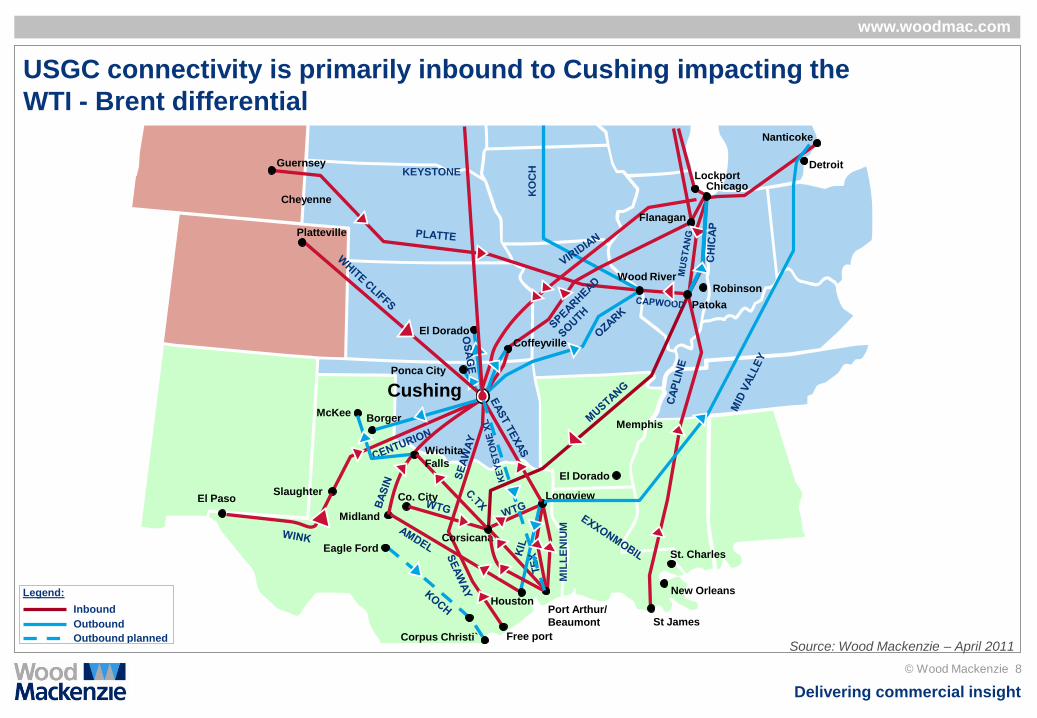

USGC connectivity is primarily inbound to Cushing impacting the

WTI - Brent differential

Cheyenne

El Dorado

Lockport

Guernsey Detroit

Nanticoke

Houston Port Arthur/

Beaumont

Free port

El Paso Slaughter

Midland

McKee

Ponca City

Chicago

Memphis

Wood River

KO

CH

MIL

LE

NIU

M

Coffeyville

Longview

Robinson

Cushing

Corpus Christi`

Co. City

Platteville

Borger

Wichita

Falls

Corsicana

New Orleans

St James

Patoka

St. Charles Eagle Ford

Flanagan

El Dorado

KEYSTONE

Legend:

Inbound

Outbound

Outbound planned Source: Wood Mackenzie – April 2011

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 9

Cushing storage utilizations influence the price dynamics of Brent –

WTI differentials

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jan

-04

Ju

l-04

Jan

-05

Ju

l-05

Jan

-06

Ju

l-06

Jan

-07

Ju

l-07

Jan

-08

Ju

l-08

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

Jan

-11

1000' bbls

0%

20%

40%

60%

80%

100%

(Utiliz. %)

Capacity Stock Utilization

Cushing – Stock & Shell Capacity (2004-2010)

-5

-4

-3

-2

-1

0

1

2

3

4

5

Jan

-04

Ju

l-04

Jan

-05

Ju

l-05

Jan

-06

Ju

l-06

Jan

-07

Ju

l-07

Jan

-08

Ju

l-08

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

Jan

-11

WTI $/bbl

0%

20%

40%

60%

80%

100%

(Utiliz. %)

Brent-WTI Utilization

Recent differentials suggest other factors

are governing the dynamics of WTI

Brent – WTI diff vs. Storage utilization (2004-2010)

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 10

2 US Refining and Gasoline Outlook

1 World Oil Outlook

3 US Natural Gas Outlook

4 US NGL Outlook

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 11

Global capacity additions are concentrated in emerging Asia and the Middle

East, with closures in the developed world

Source: Wood Mackenzie Product Markets Service

-400

-350

-300

-250

-200

-150

-100

-50

0

2009 2010 2011 2012 2013 2014 2015

Greater Europe N. America Asia Pacific

kb/d

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

Asia

Pacif ic

Middle

East

North

America

Latin

America

Greater

Europe

FSU Sub-

Saharan

Africa

Additi

onal C

DU

Capacity

, kbd .

by end 2010 2011-17

Refinery Capacity

Additions Refinery Closures and Capacity

Reductions

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 12

0

2

4

6

8

10

12

2011 2012 2013 2014 2015 2016 2017

Cu

mu

lati

ve

ch

an

ge

, M

bd

Non-refinery supply

Refinery expansions

New refineries

Demand

On a cumulative basis demand just outpaces capacity growth

Excludes capacity creep and utilisation rate changes

Global Demand and Capacity to Supply

Source: Wood Mackenzie Product Markets Service

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 13

North American Oil Product Demand shows decreased Gasoline

and Naphtha Demand

Million barrels per day 2005 2010 2011 2015 2020 2025 2030

United States

LPG (excl C2) 1.37 1.26 1.25 1.21 1.16 1.16 1.15

Naphtha 0.40 0.27 0.26 0.22 0.19 0.19 0.18

Gasoline 9.16 9.03 9.03 9.11 8.79 8.27 7.75

Jet/Other Kero 1.75 1.44 1.44 1.50 1.56 1.60 1.63

Gas/Diesel Oil 4.12 3.79 3.90 4.16 4.20 4.23 4.22

Fuel Oil 0.92 0.55 0.53 0.39 0.37 0.35 0.33

Other 3.09 2.80 2.92 3.14 3.23 3.23 3.20

US-50 Total 20.80 19.15 19.32 19.73 19.51 19.03 18.46

Sources: EIA & IEA (history), WM (forecast)

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 14

0

1

2

3

4

5

6

7

8

9

10

20

00

20

05

20

10

20

15

20

20

20

25

$/bbl

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Percent

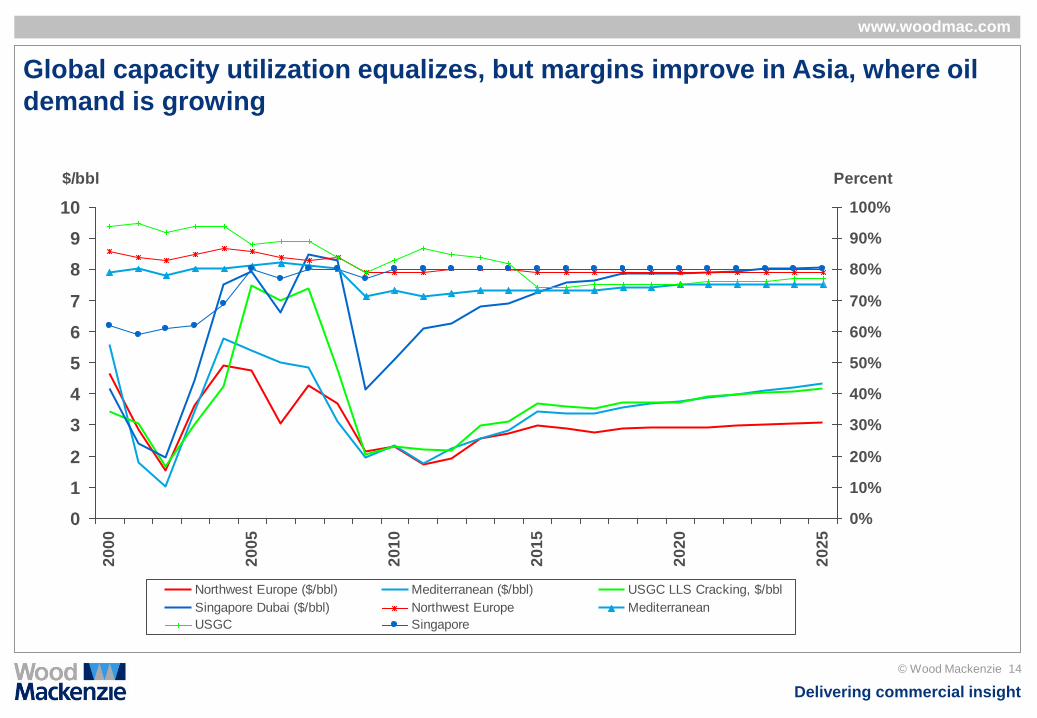

Northwest Europe ($/bbl) Mediterranean ($/bbl) USGC LLS Cracking, $/bbl

Singapore Dubai ($/bbl) Northwest Europe Mediterranean

USGC Singapore

Global capacity utilization equalizes, but margins improve in Asia, where oil

demand is growing

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 15

CP ISSUE #2: What is happening on USEC refining?

USEC continues to suffer from global competition

Current key trade (kbd)

Gasoline Trade

Source: Wood Mackenzie Analysis

-1500

-1000

-500

0

500

1000

1500

-1500

-1000

-500

0

500

1000

1500

-1500

-1000

-500

0

500

1000

1500

-1500

-1000

-500

0

500

1000

1500

Asia

FSU

2000 2005 2009 2015 2020

New net trade 2015 (kbd)

Europe

North

America

-1500

-1000

-500

0

500

1000

1500

-1500

-1000

-500

0

500

1000

1500

Africa

Gasoline flows from

Europe to North

America are forecast to

continue

Europe continues to

export to Africa and

the Middle East

Growing

surplus of

gasoline in

FSU as

refiners

invest in

improving

octane

levels

-1500

-1000

-500

0

500

1000

1500

Middle

East

Latin America Asian exports to the

Middle East decline

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 16

Opportunity may be for USEC players to play a larger role in supplying

diesel/gasoil to Europe

Current key trade (kbd)

Diesel/Gasoil Trade

Source: Wood Mackenzie Analysis

-1200

-800

-400

0

400

800

1200

-1200

-800

-400

0

400

800

1200

-1200

-800

-400

0

400

800

1200

-1200

-800

-400

0

400

800

1200

Asia

FSU

2000 2005 2009 2015 2020

New net trade 2015 (kbd)

Europe

-1200

-800

-400

0

400

800

1200

-1200

-800

-400

0

400

800

1200

Middle

East

North

America

US exports of diesel to

Europe should increase

Russia continues

to export

diesel/gasoil to

Europe

Middle East

diesel/gasoil exports to

Asia fall later in the

forecast period

-1200

-800

-400

0

400

800

1200

Africa Latin America

European imports

from Middle East

should increase

US exports of diesel to

Latin America should

decline

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 17

AsiaAsia

Run cut losers are in the Atlantic Basin

USGC utilisations manage to stay fairly constant

65

70

75

80

85

90%

2006 2007 20082010 2015

USGC Utilisation

65

70

75

80

85

90

%

2006 2007 20082010 2015

65

70

75

80

85

90%

2006 2007 20082010 2015

US East Coast Utilisation

Europe Utilisation

Source: Wood Mackenzie Product Markets Service

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 18 © Wood Mackenzie 18

CP ISSUE #3: Why are these utilizations so low?

Improved vehicle efficiency is a restraint on gasoline demand

0

10

20

30

40

2000

2005

2010

2015

2020

mile

s p

er

ga

llon

Average Fleet Average Light Vehicles Revised Cafe Standard

Average light vehicle efficiency is below

CAFÉ standards which measure vehicles in optimum

driving conditions not typical driving conditions

Existing vehicle stock means the average fleet

efficiency takes longer to improve

By 2025 CAFÉ standards are

proposed to move towards 54 mpg

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 19

Compliance with RFS and LCFS regulation substitutes with Ethanol

The Californian LCFS Carbon Intensity Requirements vs

Two Gasoline Ethanol Blends Forecast Compliance With the US RFS

CARBOB + 10%

Brazilian Ethanol CARBOB + 20%

Brazilian Ethanol

CARBOB - California Reformulated Gasoline Blendstock for Oxygenate Blending

80

82

84

86

88

90

92

94

96

98

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Carb

on

in

ten

sit

y, g

CO

2e/M

J

0

500

1,000

1,500

2,000

2,500

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

kb

/d

Ethanol Biodiesel Renewable Fuel Standard

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 20

2 US Refining and Gasoline Outlook

1 World Oil Outlook

3 US Natural Gas Outlook

4 US NGL Outlook

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 21

Natural gas supply anticipated to grow (Bcfd, dry)

Supply overall

increases by 27 Bcfd in

the US 2010-2030.

The largest increases

are in the Gulf Coast

and the Northeast.

0

20

40

60

80

100

120

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

bcfd

Rockies San Juan Gulf Coast Gulf of Mexico MidContinent

Permian Fort Worth Northeast West Coast Alaska

WCSB East Coast Arctic

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 22

Shale gas reserves are key to growth

Gulf of Mexico

Atl

an

tic O

cean

Pacific

Ocean

Gulf CoastPermian

Rockies

Northeast

UNITED STATES OF AMERICA

CANADA

Almond TGS

Baxter Shale

Mancos TGS

Honaker Trail TGS

Columbia TGS

Wyodak CBM

Big George CBM

Lance Pinedale TGS

Mesaverde CBM

Mesaverde Piceance TGS

Niobrara TGS

Gothic Shale

Fruitland CBM

Vermejo CBM

Pierre Shale

Barnett-Woodford Shale

Mesaverde-San Juan

Granite Wash TGS

AnadarkoWoodfordShale

Cherokee CBM

Arkoma Woodford

Caney Shale

Fayetteville Shale

Barnett Shale

Austin Chalk TGS

Eagle Ford Shale

Wilcox TGS

Lower Vicksburg Shale

LoboWilcoxTGS

New Albany Shale

Marcellus Shale

BereaOriskany

Huron Shale

Chatanooga Shale

Pennsylvanian CBM

Floyd Shale

Selma ChalkCotton ValleyTGS

Haynesville Shale

Deep Bossier Shale

Travis Peak TGS

Horn RiverShale

Montney TGS

Mannville CBM

HorseshoeCanyon CBM

Utica Shale

West Coast

WCSB

Antrim Shale

Hovensweep

Palo Duro Shale

Deep Haley TGS

MEXICO

Mid-ContinentWasatch TGS

0 400 800200

km

Source: Wood Mackenzie

Horn River

Woodford

Fayetteville

Haynesville

Marcellus

Barnett

Monteney

Eagle Ford

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 23

0

5

10

15

20

25

30

35

40

45

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

bc

fd

Barnett Fayetteville Woodford

Haynesville Marcellus Eagle Ford

Horn River Montney & Duverney

CP ISSUE #4: Will we be allowed to get to it?

The supply mix depends on shales, and hydraulic fracturing

Close to 50% of supply longer term will be affected by regulations on hydraulic fracturing.

Still, strong growth potential - 28.5 Bcfd in the known shale plays by 2025!

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 24

Power is still the largest and a growing use of natural gas in the US

Initially, rapid growth, but a longer term slowing

Coal retirements, a

resumption of

economic growth

drive 1.5 Bcfd growth

annually through

2020

Post 2020,

efficiencies and

renewables reduce

growth to < 1 Bcfd

yearly.

US Power Demand for Gas

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

TW

h

0

5

10

15

20

25

30

35

40

bcfd

Nuclear Hydro Coal Gas Renew ables Other Gas demand

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 25

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 7 8 9 10 11

bcfd

20

10

$/m

mb

tu

2011 2020

Eagle Ford

Marcellus

Fayetteville

BarnettHaynesville

Pinedale

tight gas

Eagle Ford

Marcellus

Barnett

HaynesvillePinedale tight

gas

FayettevilleLower Bossier

tight gasCotton Valley tight

gas

Lower Bossier

tight gas

Cotton Valley

tight gas

New-drill cost curves indicate higher long-term Henry Hub price requirement,

but well below recent years

US new drill gas supply stack*

Source: Wood Mackenzie (North America Gas Service)

*Assumes development breakeven economics (not

including land lease costs) at a 10% real IRR

adjusted to a Henry Hub- equivalent price

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 26

2 US Refining and Gasoline Outlook

1 World Oil Outlook

3 US Natural Gas Outlook

4 US NGL Outlook

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 27

Middle East continues to dominate the LPG production – while the US

supply remains steady

0

500

1000

1500

2000

2500

3000

3500

4000

2000 2005 2010 2015 2020

(Th

ou

sa

nd

bb

l/d

)

US FSU Europe Asia Africa Latin America Middle East

Regional NGL Production 2000 -2020

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 28

Given the infrastructure of regional demand, the USGC is the hub for

Propane and Butane for Chemical use

US North West

Europe Middle East Asia

Ethane Propane Butane Naphtha Gasoil Other

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 29

LPG petchem demand expected to increase in the Middle East while

other regions’ demand profile remains nearly unchanged

Industry Petchem Feedstock Residential Commercial Agriculture Road Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2020

US

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2020

Europe

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2020

Asia

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2020

Middle East

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 30

CP ISSUE #5: Why is everybody’s talking about Ethane?

With all these shales NGL content (“richness”) is a key driver

High oil-gas price differential

has increased the

attractiveness of liquids-rich

shale gas plays…

• Increased focus on “wetter”

shale plays in 2010/11

• Shifting upstream strategies

and capital allocation across

independents

Source: Wood Mackenzie Unconventional Gas Service

0

5

10

15

20

25

30

35

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

bcfd

Barnett Eagle Ford Montney Marcellus Fayetteville Woodford

Haynesville Horn River

Wet

Lean

US Shale Gas Production by Play

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 31

North America’s “Liquids Fairway” unveils an “ethane supply” story

Aux

Sable

Liquids

“Fairway

”

Sarnia

Mont

Belvieu

Conway

Source: Wood Mackenzie

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2007

2010

2015

2020

Th

ou

san

d B

bl/

day

Ethane Propane Butane

US NGL Production (2007-2020)

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 32

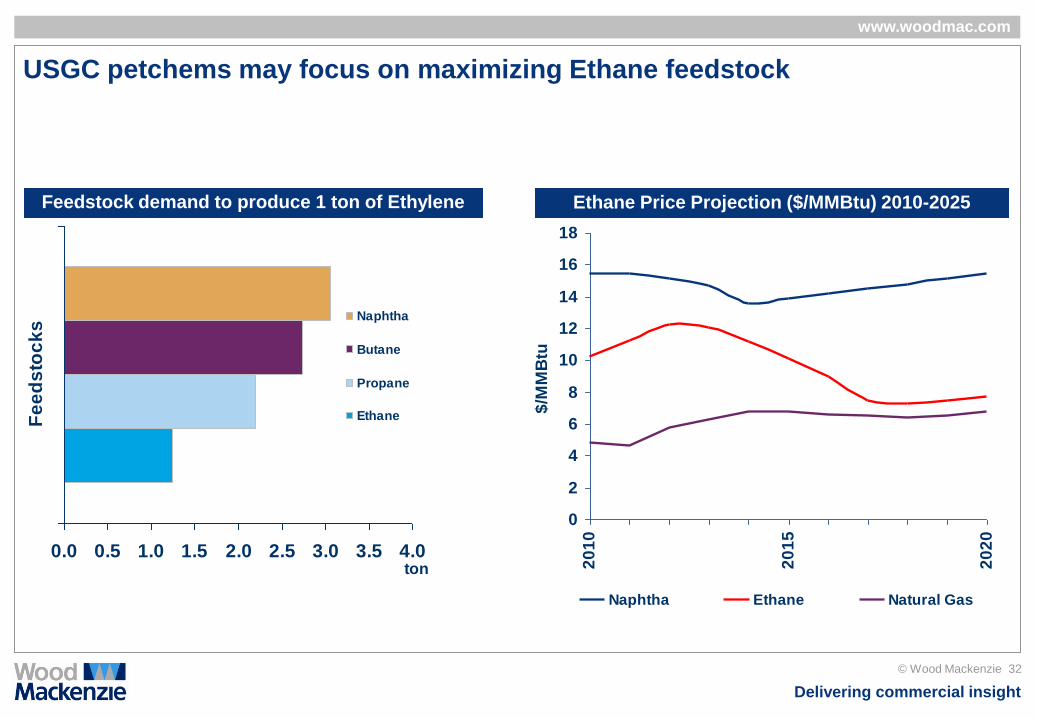

USGC petchems may focus on maximizing Ethane feedstock

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

Fe

ed

sto

ck

s

ton

Naphtha

Butane

Propane

Ethane

Feedstock demand to produce 1 ton of Ethylene

0

2

4

6

8

10

12

14

16

18

20

10

20

15

20

20

$/M

MB

tu

Naphtha Ethane Natural Gas

Ethane Price Projection ($/MMBtu) 2010-2025

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 33

In summary, how do the broader trends in the energy industry

impact the E&C business?

Oil supply is stable and more

from non-OPEC sources

Gasoline demand declining

• Overall demand

• CAFÉ

• RFS/LCFS

Natural gas volumes increased

with (wet) shale plays

NGL supply stable, but ethane

will grow significantly

E&C Impact Macro-Fundamentals

Mega projects in the upstream

remain in the mix (Brazil

deepwater and Canada)

Infrastructure plays become the

more important in future

Refining projects to be smaller

more geared to regulatory

compliance vs. profitability

Gas fired power plants win the

day

Ethylene units may already have

too many announced

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 34

THANKS

Any Questions?

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 35

Wood Mackenzie

Kintore House

74-77 Queen Street

Edinburgh EH2 4NS

Global Contact Details

Europe +44 (0)131 243 4400

Americas +1 713 470 1600

Asia Pacific +65 6518 0800

Email [email protected]

Global Offices

Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States

Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry

for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better

business decisions. For more information visit: www.woodmac.com