PERSPECTIVES AND COOPERATIVE BANKS

118

FINANCIAL INCLUSION IN SPAIN: A COMPARATIVE STUDY AMONG BANKS, SAVINGS BANKS AND COOPERATIVE BANKS PERSPECTIVES 65 October 2012

Transcript of PERSPECTIVES AND COOPERATIVE BANKS

FINANCIAL INCLUSION IN SPAIN:A COMPARATIVE STUDYAMONG BANKS, SAVINGS BANKSAND COOPERATIVE BANKS

PER

SPEC

TIV

ES65October 2012

FINANCIAL INCLUSION IN SPAIN:A COMPARATIVE STUDYAMONG BANKS, SAVINGS BANKSAND COOPERATIVE BANKS

Beatriz Fernández OlitPhD Student of the Universidad Nacional de Educación a [email protected]

The views expressed in this Perspectives are the responsibility of theauthor and are not to be regarded as representing the views of ESBGMembers. The findings, interpretations and conclusions expressed in thispaper do not necessarily reflect the views of WSBI (World Savings BanksInstitute) or ESBG (European Savings Banks Group). Neither WSBI norESBG guarantee the accuracy of the data included in this work. The materialin this publication is copyrighted.

TABLE OF CONTENTS

Introduction 7

1. Financial exclusion: definition, causes, consequences,and situation in europe and spain 9

2. Market responses to promote financial exclusion:a review of the types of commercial banking entitiesin Spain 27

3. Geographical financial exclusion in Spain:analysis of significative differences 33

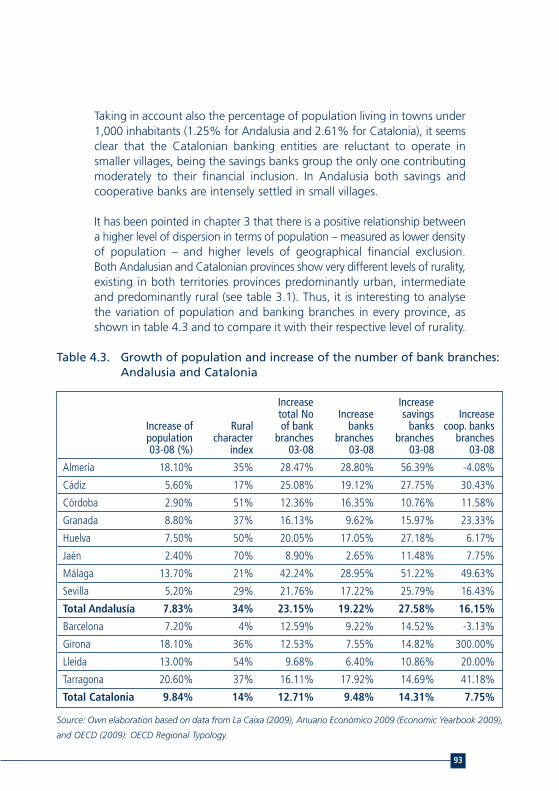

4. Types of banking entities and financial inclusion:a comparative analysis in Catalonia and Andalusia 89

5. Conclusions 109

References 115

5

6

7

Financial inclusion, as well as financial education and prevention of over-indebtedness, are recognized as issues of great importance that have notbeen sufficiently studied both in Europe and Spain1. There is a lack ofregulation at European level regarding the right of all citizens to haveaccess to basic financial services and to guarantee the use of a basicpaying account. This is a cause for concern for the EuropeanCommission, as these are risk factors for social exclusion. In fact, amongthe developed economies, it is in countries like the United Kingdom andthe United States where the financial exclusion has been more deeplystudied, as response to critical changes in their banking systems duringthe 80’s that affected socially-oriented banking models.

It is important to revise and study the situation of financial exclusion inEurope at a moment of important transformation of the national bankingsystems, and especially in Spain, where the restructuring process is veryimportant. It involves reviewing the few previous studies about this issuein Spain, determining the ongoing levels and features of financialexclusion, and establishing a base of measure for its future evolution.In addition, it is also relevant to analyse the role and expectations inthis process of the different kinds of retail commercial banks in Spain,and particularly of the socially-oriented models such as savings banks andcooperative banks, as their foundational principles address financialinclusion of disadvantaged people and rural areas.

INTRODUCTION

1 See European Commission, 2007; CNMV and Banco de España, 2008; and websiteshttp://ec.europa.eu/internal_market/finservices-retail/inclusion_en.htm (visited 07/30/09)http://ec.europa.eu/employment_social/spsi/financial_exclusion_en.htm (visited 07/30/09)http://www.bde.es (visited 07/30/09).

8

2 Inspired in Sinclair, 2001.

9

1.1. Definition of financial exclusion and related issues

The concept of ‘financial exclusion’ can be understood in different ways,depending on the level of access to financial services being analysed,and the kind of those financial services (transactions, credit, savings, etc.).But financial exclusion is usually related to social exclusion, and thisexplains the focus on basic financial services. To clarify better this concept,several definitions are being revised:

n Gardener et al (2005) propose two different definitions of financialexclusion. A broad definition2, describes it as ‘the inability of access tobasic financial services in an appropriate way. It emerges as a result ofproblems regarding access, conditions, prices, marketing and saleschannels, or by self-exclusion as response to several negative experiencesor feelings’. This first definition gathers supply-side (characteristics offinancial product) and demand-side (needs and previous experience ofuser) grounds for financial exclusion. A more direct definition describesthe financial exclusion as ‘the inability (sometimes induced) that somesocial groups face to access to the financial system’. This seconddefinition makes reference to the most vulnerable groups of society,this means mainly to lowest income groups; and it relates financialexclusion directly, as a booster, to other kinds of social exclusion.

n Carbó and López del Paso (2005) define financial exclusion as ‘thesituation that some disadvantaged individuals or groups face asconsequence of their geographical location, their economic or socialcondition, and their inability or difficulty to acquire or contract financialproducts and services, including difficulties to access to the differentfinancial intermediaries and markets’.

1. FINANCIAL EXCLUSION:DEFINITION, CAUSES,CONSEQUENCES,AND SITUATIONIN EUROPE AND SPAIN

3 Gardener et al, 2005; Carbó and López del Paso, 2005; European Commission, 2008.

10

This definition revises the main determinants of financial excludedpopulation: geographical location makes reference to rural population,sometimes living far from a bank branch, and also to population livingin socially excluded urban neighbourhoods; economic condition refersto families of lower incomes; and social condition refers to ethnicminorities or migrants, for example.

n The European Commission (2008) proposes the following definition:‘Financial exclusion refers to a process whereby people encounterdifficulties accessing and/or using financial services and products in themainstream market that are appropriate to their needs and enablethem to lead a normal social life in the society to which they belong’.This definition includes two additional factors: the reference tomainstream markets, this is, to normalized financial services notincluding specific social products, such as microcredit, or informal lendersas usurers; and the assumption that mainstream financial services arenecessary to be completely integrated in the society, at least in Europe.It refers then, to basic financial services as a bank account to pay watersupply or a flat rent by standing order. The discussion about whatshould be understood as ‘normal’ in a certain society will dependfinally on the country we consider, even inside Europe.

1.1.1. Financial exclusion and social exclusion

Financial exclusion can be basically defined as ‘the difficulty of access tobasic financial services, experimented by certain social groups’. The previousreview of other definitions has shown that it is a concept strongly relatedto social exclusion3. There are bidirectional flows of influence betweenthese two concepts, but clearer effect is made in the sense that financialexclusion may accelerate the social exclusion process: in our currentsocieties, the access to a basic financial service such as a paymentsaccount determines the social normalization of people, as it may beessential, for example, to have access to water or electricity supply. That iswhy, apart from credit or savings exclusion, the lack of access totransaction services is the most important factor to hinder the socialnormalization of a person.

4 Delgado and Rodríguez, 2006.5 EU10: Cyprus, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovenia

and Slovakia. 6 EU15: Germany, Austria, Belgium, Denmark, Finland, France, Greece, Holland, Ireland,

Italy, Luxembourg, Portugal, Spain, Sweden and the United Kingdom. 7 Gardener et al, 2005.

11

We can identify several groups that face a special risk in terms of financialexclusion, classified by their socioeconomic features4:

n By their working situation: unemployed and households wherenobody has a job;

n By age: elder retired people, and young people under 25 years old; n By physical or psychical condition: people with chronic disease or with

disabilities; n By origin or ethnic group: recent migrants and ethnic minorities; n By personal status: mono-parental families, housewives; n By educational level: people with low educational level; n By economic and financial background: families with low incomes,

families receiving social aid and allowance, over-indebtedness people,families with non-payment records; people ‘used to cash’.

n By geographical area: population of depressed or rural areas.

Nevertheless, risk groups may be different, depending on the nationalcontext: in the EU105 rural population and people over 65 years old sufferhigh rates of financial exclusion. In the EU156 countries, these are not riskfactors, however being under 25 years old is.

1.1.2. Causes of financial exclusion

Most of the authors coincide regarding the origins or causes of financialexclusion, and classify them as coming from the supply side(inappropriate features of services and products), or as coming from thedemand side (depending on the needs or previous experience of users).They comprise the following7:

n Exclusion from the access to financial services of several groups thatdo not fit in a certain profit-risk profile.

n Exclusion via prices, as they are too high for some people or groups. n Commercial exclusion, as strategies and channels of commercialization

of financial services are not adequate for certain people (ex: on-linebanking for elderly people).

12

n Exclusion via conditions, as these are inappropriate or difficult tounderstand by certain people or groups.

n Self-exclusion, when a person refuses to use financial services due tolack of self-confidence to use them, lack of trust on the bankingsystem, or ethic or religious reasons.

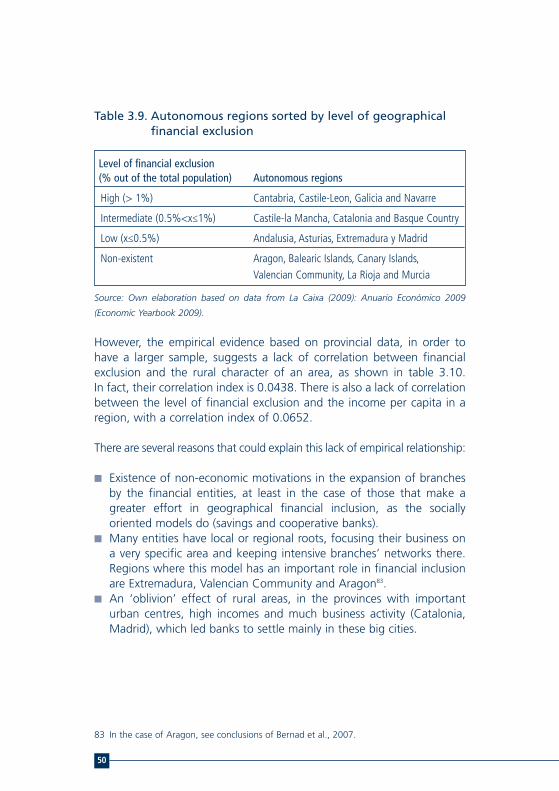

Some examples regarding causes of financial exclusion are shown intable 1.1

The mere possibility of access to financial services is not enough tovalue the situation of financial inclusion of a person. The ability of certaingroups and individuals to understand and use financial services shouldalso be considered.

Table 1.1. Causes and examples of financial exclusion

ORIGIN CAUSE EXAMPLE

Supply side - Exclusion from the access Systems of credit risk rating that to financial services penalize automatically the inhabitants

of certain villages or neighbourhoods,using zip codes as a filter.

- Exclusion via prices High commission costs applied to currentor transaction accounts, higher whenaverage balance are lower.

- Commercial exclusion Marketing and sales, including productswith lower costs, via the Internet, notsuitable for people not used to newTechnologies or with not access to them.

Demand side - Exclusion via conditions The language used to define conditionsfor products and services is too technicaland it is not understandable by peoplewith lower educational levels.

- Self-exclusion Muslims that refuse the services ofmainstream Banks due to the use ofinterest rates/Migrants with negativebanking experiences in their originalcountries (very common in Latin-Americanpopulation).

Source: Own elaboration based on Gardener et al (2005).

8 European Commission, 2008.

13

It implies necessarily the assessment of their level of financial culture andtheir effective ability to use fluently the mainstream products andservices. In many cases, this will be linked to social factors: illiteracy, notspeaking or not having a good understanding of the local language,disability, etc.

1.1.3. Typologies and consequences of financial exclusion

There are three main types of financial exclusion:

(i) Exclusion based on transaction services: This is the most common threshold to decide if a person is facingfinancial exclusion or not. It is measured as the possibility of access toa basic bank account with transactions facilities, in order to dopayments or to receive any kind of income or earning. The access tobasic domestic facilities depends on the access to this kind of bankingservices. The use of credit and debit cards can also reduce the levelof vulnerability of a person to losses or thefts: since it reduces thenecessity to use cash.

There are three levels, considering exclusion of transaction services8:‘unbanked’ (people not disposing this kind of services); ‘marginally banked’(people having a bank account with basic transaction facilities, butnot online services or use of cards; and people having access to thiskind of services, but not using them due to lack of self-confidence ortraining); and ‘completely banked’ (people accessing to a wide rangeof transactions and payment services addressing their needs).

(ii) Exclusion based in credit: This is the secondly most analysed typology of financial exclusion, andit is narrowly related to the analysis criteria that banking entities use todecide if a person is able to comply with the refund duties of a credit.This risk rating, that comprises wealth and guarantees evaluation, isnot a factor of exclusion itself. But it is when some subjective orgeneric filters are used regarding certain social groups, obviating theindividual analysis: for example, when the assignment of higher ratesof credit risk to migrant people, ethnic minorities, or people living inspecific neighbourhoods, leads the bank to refuse the individual studyof credit risk profile, or to increase the credit conditions.

9 European Commission, 2008 10 Banco de España (National Bank of Spain) 2009: Annual Report, 2008, pp. 48.11 European Commission, 2008.

14

As not all kinds of credit services are related to basic needs, creditexclusion is defined as9:

• The lack of access to credit that can stigmatize a person, blockingits access to essential goods and services. It reduces the self-confidence and not allows reaching a minimum standard of life,coming close to the social exclusion.

• The lack of access to credit that leads to a higher budgetaryunbalance in the medium or long time, or even to over-indebtnessdue to use of other non formal lending sources.

Credit barriers depend strongly on the economic circumstances of asociety or country at a given time. In fact, this has been a phenomenonbroadly studied in under-developed economies, and microcredit hasemerged as an inclusive tool that has helped to ‘democratize’ thelending in the poorest countries. But it is the moment to reflect onthe role that western banking entities played during the last decade,when families (this is the case of many families in Spain) got over-indebted10 in response to the low interest rates. Did they useappropriate risk analysis standards in 2005? Were they the same as thestandards used in the second half of 2007, when credit markets beganto tighten due to the international liquidity crisis? The subprimemortgages in the United States, were they an example of financialinclusion? Or were they a new way to broaden the operative marginof financial entities lending to new segments of clients with unclearguarantees of repayment credit? All those factors compound acomplex system that requires a deeper analysis going beyond from theaims of this paper. But it must be highlighted that an essentialcondition when talking of financial inclusion is that banking servicesmust meet the needs and characteristics of the user. This should beunderstood as well in an ‘excess’ as in a ‘defect’ way. Over-indebtnessand default in credit repayments can build an undesirable ‘financialbackground’ promoting financial exclusion of certain people in abanking environment with open information flows11.

12 European Commission, 2008; Carbó et al, 2005.13 World Bank, 2005.

15

(iii)Exclusion based in savings:Lack of savings is commonly defined as a consequence of socialproblems, and not so often as a consequence of banking barrier.Causes of lack of savings are12: low or inexistent incomes, having thehabit of managing funds in cash, distrust of banking entities dueto prejudice or previous negative experiences, and high costs ofbanking services.

The relationship between lack of savings and the increase of socialexclusion is not often analysed. But future expectations regardingsocial public welfare in the European countries attracts attention tothe increasing importance of private retirement savings in the future.This means that in the next decades, savings placed in complementarypension funds may suppose the avoiding of situations of poverty andsocial exclusion among elderly population.

Financial exclusion from the mainstream retail banking sector canbring to several situations13: the excluded person turns to socialbanking resources (microcredit, etc.); the excluded person turns toinformal sector, especially when searching for credit (usurers, family);or the excluded person is left to a complete lost of financial support.Usually, in the European case, none of these situations solves theproblem of meeting transaction needs, and this fact increases the riskof social exclusion.

1.2. Financial exclusion in Europe and in Spain

1.2.1. The studies about Europe

Financial exclusion has been studied in Europe by different authors.One of the most important references of financial exclusion, socialexclusion and their relationship is the Rowntree Report (1999), whichanalysed and assessed the situation in the United Kingdom: a 7% ofBritish families were financially excluded at that time, and expectationsfor ten years later supposed an increase of this ratio up to 20%.

16

14 Gardener et al, 2005.15 Cit in Gardener et al, 2005, pp.14. 16 Those incorporated to the European Union until 1995. 17 Delgado y Rodríguez, 2006.

The rise of poverty in the United Kingdom has been highlighted as oneof the boosters of financial exclusion14, linked to an increase of inequityin the incomes redistribution, and to the falling of the real income ofpoorest sectors of British society during the decades of the 80’s and 90’s,while the average income of the country kept growing. In addition,there are other factors involved, as the value maximization, a systemused by financial entities to assess clients in base to their possibility ofgenerating a minimum profit margin in the use of financial services. It isused as a threshold to accept or not a certain group or individual asclients. Following Boyce (2000)15, the profit-risk assessment of clients inthe banking industry has become a system to increase the turnover andwealth of shareholders, at the expenses of poorest and underprivilegedpeople. Regarding excluded population, some groups have beenidentified as those with a higher risk (unemployed people, pensioners,certain ethnic groups – Pakistani and Bengali origin – single-parentfamilies, etc.). And it has been demonstrated that financial inclusiontends to be geographically concentrated: a 50% of financially excludedBritish population live in the 50 less privileged districts.

There are comparative studies regarding the financial exclusion levels ofthe European Union. It is appropriate to analyse separately the countriesbelonging to the EU1516 and the countries associated later (in 2004:EU25; in 2007: EU27). Most of the countries incorporated in 2004 andafter are ex-socialist countries, which have a very different financialtradition and less banking maturity in comparison with ‘western’countries. The recent integration processes in the EU of the easterncountries have involved a pronounced process of financial liberalisation17.Delgado and Rodríguez (2006) have studied, based on data provided bythe World Bank, the levels of credit given to the private sector in relationto the GDP for the countries belonging to the EU15 and EU25. It hasbeen understood as a relative indicator of the level of development of thefinancial system in every country. As conclusion, the countries integratedinto the European Union in 2004 (as Poland, Hungary, Estonia, etc.) showa lower grade of sophistication of their financial systems, but also lessinclination to indebtedness.

18 Delgado and Rodríguez, 2006.19 Delgado and Rodríguez, 2006; Carbó and López del Paso, 2005.20 European Commission, 2008; Carbó and López del Paso, 2005.21 Carbó and López del Paso, 200522 Based in data of Eurobarometer 60.2 (end 2003) and Eurobarometer 2003.5, and revised

with the most recently available information.23 Countries integrated into the EU in 2004.

17

In the field of financial exclusion, those same authors analyse the levelof banking coverage in every country, assuming as a premise that inEurope branches are the main physical channel to supply bankingservices. Spain is the country with the highest coverage of branches per100,000 inhabitants (95.8), followed at a long distance by Austria (53.4).Countries belonging to the EU10 have the lowest rates, such as Slovenia(2.2) or Lithuania (3.4)18. It has been estimated that 10% of the Europeanpopulation does not have even a transactions account, includingthe EU15, and in countries near the Spanish context, such as Italy,Greece, Portugal or Ireland, these rates range between 15% and 20%19.The countries with better rates are Denmark (0.9%), Holland (1.1%) andSweden (2%). The savings banks industry stands out as being the mostimportant agent in the reduction of this rate. The countries wherethis model is strongly established have lower rates of financial exclusion,(e.g. Spain)20.

In Europe, financially excluded population is characterised by some riskfactors as being a woman, being young or old, having a low educationallevel and being long-term unemployed. Regarding the European case, itis again determined that the discrimination that banking entities havemade to give service preferentially to those groups with better profit-riskprofiles, searching for a maximization of benefit, has promoted thefinancial walkout of other groups21. This reinforces the important role ofsocially oriented banking entities stemming the rise of financial exclusion.

Finally, the most recent study developed at the European level has beenpublished by the European Commission (2008)22 and also divides theanalysis into EU15 and EU1023 groups. Spain is considered in the firstgroup, which have more developed banking systems. The average levelsof lack of use of financial products for both groups of countries areshown by the table 1.2 on the next page.

18

Table 1.2. Percentage of European population not using basicfinancial products

Source: Own elaboration based on data from European Commission (2008): Financial Services

Provision and Prevention of Financial Exclusion.

In the case of the EU15 group of countries, the general levels of financialexclusion have been estimated as shown in table 1.3.

Table 1.3. Levels of financial exclusion in the countries belongingto EU15

Source: Own elaboration based on data from European Commission (2008): Financial Services

Provision and Prevention of Financial Exclusion.

Percentage of populationnot using those products

EU15 EU10

Bank account with transaction facilities 18% 53%

Any other kind of bank account 10% 47%

Percentage of population GDP per capita Indexfinancially excluded (%) EU25 average=100

Austria 3 122

Belgium 1 119

Denmark 1 122

Finland 6 115

France 2 111

Germany 3 109

Greece 28 82

Holland 1 120

Ireland 12 139

Italy 16 105

Luxemburg <1 223

Portugal 17 73

Spain 8 98

Sweden 2 116

United Kingdom 6 119

24 Delgado and Rodríguez, 2006. 25 Bernad et al, 2007.

19

The empirical analysis based in the Eurobarometer data confirmed thesocioeconomic characterization defined by the previous studies to pointout the groups with highest risk of financial exclusion in Europe:

n Women, especially housewives or single parents.n Young people (particularly in EU15 countries), and elderly people

(particularly in EU10 countries). n Single parent families and individuals living alone, especially in the

case of young and elderly people. n People with low educational levels, except in the case of young

students, also a risk group. n People living in rural areas (not relevant for EU15 countries) n People with lack of financial culture and perception that ‘banking

products are not made for them’.

It has been proved statistically that unemployment is the mostmeaningful circumstance pushing to be at risk of financial exclusion.Other important factors – but not so consistent regarding statisticalcontrast – are being a migrant or being over-indebted. There are alsoevidences of the geographical concentration of financial exclusion in themost deprived areas.

1.2.2. Public initiatives tackling financial exclusion

It has been highlighted that the processes homogenising pricingconditions and trans-boundary consolidation of financial entities into theEuropean Union, may be boosting difficulties in the access to financialservices in certain countries24. In this sense, keeping the institutional localdiversity regarding banking entities is important in order to promotefinancial inclusion, as it has been demonstrated with the example ofsaving banks and similar entities.

In the Spanish case, it has been also recommended to keep the partly publiccharacter of some financial entities, as the saving banks25. This structureof property has been pointed as one of the reasons to promote financialinclusion by these entities, as it provides them with a social orientation.

26 European Commission, 2008. 27 European Commission, 2008.

20

These socially oriented financial entities have often also supported publicinitiatives regarding the financial inclusion of communities with fewerresources. An example of it would be the agreement of post bankingoffices with the public authorities to provide banking services to the ruralpopulation in the United Kingdom.

There are several recommendations for the public sector to promotefinancial inclusion26:

(i) To promote the public debate, and also the public and privateresearch, homogenising analysis criteria and indicators at theEuropean level.

(ii) To promote from public authorities, the removal of barriers of accessto the financial services: assuring the consumers protection and trustin the banking entities, including in their financial strength;guaranteeing transparency and competitiveness among financialentities; tackling the over-indebtness of families; and promoting thefinancial education. In this sense, the development of regulation toguarantee a minimum of banking services to all citizens can also beconsidered.

(iii) To encourage the policies and practices of corporate socialresponsibility of banking entities, including initiatives of self-regulation into the sector related to financial exclusion. To control andsupervise, as well, the transparency of the information made publicby the banking sector about this matter, establishing objectiveindicators to assess practices in the filed of financial inclusion.

In fact, there already are in Europe some examples of public regulation toguarantee the financial inclusion of citizens, assuring the right to open anaccount available for banking transactions27.

n In Norway this right is enjoyed by every person owning anidentification number issued by the government.

n In France, the banks are required to offer alternative paying means tothose people with a risk profile not adequate to access to debit/creditcards or chequebook. In addition, the postal bank guaranties theopening of a banking account with no costs, to everybody that hadbeen previously refused as client by three other banks.

n In Belgium, every banking entity offering current accounts are requiredto offer access to basic transaction services to any citizen, when theyare not used for professional use.

Regarding self-regulation by the banking sector, the British BankersAssociation requires the disclosure by their associates of informationabout the supply of services to the most vulnerable social groups, andabout the amount of credit given to low income people and other sociallyexcluded groups28.

Additionally, the National Strategy Reports on Social Protection and SocialInclusion of every member state of the EU29, are reviewed biannually anddeal with financial inclusion issues, including prevention and correction ofover-indebtness. These are recognized as matters of concern in terms ofsocial policies. The Spanish report30 does not study in depth the issue offinancial inclusion, apart from the mention to the need of establishingstructures of access to microcredit as tool for self-employment, and somebroad aspects regarding the financial sustainability of pension funds system.

1.2.3. Financial exclusion in Spain

The few studies about the Spanish situation point at a medium-low levelof financial exclusion (8%), despite the wide network of bank branches,and coincide in pointing out that the main risk factors are: age under 25;being unemployed or a housewife; being in the lowest half of thepopulation in terms of incomes; and having scarce knowledge aboutbanking and financial markets31.

The analysis of empirical data about ownership of accounts or depositswith transaction facilities, showed in table 1.4 on the next page, allowdrawing similar conclusions: low levels of incomes and wealth are the keyfactors for not having an account, followed by being unemployed orinactive. Age is a minor risk factor, and only affects in the case of youngpeople, because retired people or people over 65, show higher rates ofuse of transaction accounts than the average households32.

21

28 Gardener et al., 200529 The National Strategy Reports 2008-2010 can be found at http://ec.europa.eu/

employment_social/spsi/financial_exclusion_en.htm. No up-to-date Reports have beenfound on date 12/08/2012.

30 National Strategy Report on Social Protection and Social Inclusion 2008-2010 – Spain. 31 European Commission, 2008; Carbó and López del Paso, 2002, Nieri, 2007. 32 Banco de España: Encuesta Financiera de las Familias 2005 (Survey of Household Finances),

2007.

Other studies suggest that the deregulation process of the Spanishbanking system during the last years, and the elimination of barriers,could affect the bank branches network and eliminate the less profitableones, due to the harder requirements of a more competitive market33.Thus, branches located in areas with low incomes or low population level,mainly rural areas, are the most vulnerable to disappear under marketcriteria. In fact, these studies show less availability of banking services intowns with the lowest incomes, and also point that savings banks are themain entities that contribute to guarantee banking activity in such areas.The maximization of the banking coverage by the savings banks sector,in order to promote financial inclusion, is the reason for the expansionprocess in Spain during the last decade, contrary to the European trendof closing bank branches.

However, the effects of the economic and financial crisis of the recentyears become evident in the slowing down of the annual growth of thenumber of bank branches. Between the years 2008 and 2009, thisgrowth rate was almost three times lower than the average annualgrowth during the five previous years (table 1.5). Regarding autonomousregions, there was an annual increase in the number of branches in allregions during the period 2003 and 2008.

22

33 Bernad et al, 2007; Carbó and López del Paso, 2005.

Rate of use of accounts and depositswith transactions facilities

All families 97,8%

Lowest incomes percentile (<20) 94,6% Highest income percentile (>90) 99,4%

Head of family’s age < 45 years 97,4% Head of family’s age > 65 years 98,3%

Working situation: inactive/ 95,9% Working situation: retired 98,6%unemployed, not retired

Net wealth percentile < 25 95,4% Net wealth percentile > 75 99,1%

Table 1.4. Definition of Spanish families owning accounts and depositswith transaction facilities

Source: Own elaboration based on data from Bank of Spain (2007): Encuesta Financiera de las Familias 2005

(Financial Survey of Households, 2005).

However, between 2008 and 2009, the expansion of branches has beenslower in almost all regions, except in the Basque Country and Navarre,and it has been drastically reduced in some regions such as Galicia andthe Canary Islands. Only Catalonia has shown a decrease in the numberof bank branches, but this trend is supposed to go on in the followingyears and in other regions.

23

Averageannual

No. of Bank No. of Bank No. of Bank No. of Bank growthbranches branches branches branches in period

Total per region 2009 2008 2003 2008-2009 2003-2008

Total Andalusia 7,010 6,911 5,612 1.43% 4.63%

Total Aragon 1,796 1,787 1,636 0.50% 1.85%

Total Asturias 966 956 868 1.05% 2.03%

Total Balearic Islands 1,254 1,241 1,080 1.05% 2.98%

Total Canary Islands 1,463 1,440 1,080 1.60% 6.67%

Total Cantabria 503 495 449 1.62% 2.05%

Total Castile and Leon 3,162 3,143 2,827 0.60% 2.24%

Total Castile-La Mancha 2,020 1,978 1,736 2.12% 2.79%

Total Catalonia 8,098 8,103 7,189 -0.06% 2.54%

Total Valencian Community 5,061 4,963 4,058 1.97% 4.46%

Total Extremadura 1,197 1,193 1,142 0.34% 0.89%

Total Galicia 2,512 2,507 2,337 0.20% 1.45%

Total Madrid 6,024 5,886 4,749 2.34% 4.79%

Total Murcia 1,353 1,326 1,081 2.04% 4.53%

Total Navarre 717 706 672 1.56% 1.01%

Total Basque Country 1,988 1,923 1,700 3.38% 2.62%

Total La Rioja 496 484 423 2.48% 2.88%

Total Ceuta 25 25 20 0.00% 5.00%

Total Melilla 21 21 17 0.00% 4.71%

Total Spain 45,666 45,088 38,676 1.28% 3.32%

Table 1.5. Average annual growth of the number of bank branches,by provinces

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009 (Economic Yearbook 2009)

1.2.4. Financial education to avoid financial exclusion

It is also important to highlight that Spanish banking sector has detecteda serious gap of knowledge of the Spanish society regarding a financialmarket and financial products growing in complexity. It has been seen asone of the main factors contributing to aggravate the consequences ofthe financial crisis for many families. The improvement of financialeducation levels is now a target for the Spanish banking industry, and itis closely linked to avoiding over-indebtness and financial exclusion offamilies and individuals. Some of the most remarkable initiatives are34:

n Bank of Spain (BE) and the National Commission of the Spanish StockMarket (Comisión Nacional del Mercado de Valores - CNMV): FinancialEducation Plan 2008-2012, published in May 200835. That documentis based on the 2002 and 2005 results of the Financial Survey ofHouseholds (Encuesta Financiera de las Familias) developed by the BE.It highlights that families with a lower level of incomes and those withlower educational level, show the worst over-indebtness ratio,measured in terms of disposable income.

n Spanish Network of Financial Education (Red Española de EducaciónFinanciera)36, created in December 2008 by the Spanish Confederationof Saving Banks (Confederación Española de Cajas de Ahorros - CECA).

1.3. The global financial crisis and its effects in termsof financial exclusion

The financial crisis during the second semester of 2007 in the United Statesrapidly transmitted to the European economies. It has strongly affectedto the growth of the GDP during the last five years. The Spanish economyhas specially suffered from the deceleration of GDP growth, from risesof even 4% in the pre-crisis years, to a rate of growth of 0.7% in 2011and even negative growth between the middle of 2008 and the middleof 201037.

24

34 It is also relevant to highlight that other large Spanish banks have developed their ownfinancial education projects as bancaparatodos.com (BBVA) and finanzasparamortales.com(Cantabria University and Santander Group).

35 See www.bde.es36 See www.rededucacionfinanciera.es/home.htm37 Banco de España, 2012.

The main causes for this situation have been found in the imbalancesgenerated in the Spanish economy between 1999 and 2006, due to anintensive allocation of financial and productive resources in the propertyand building sectors, as well as to an excessive over-indebtness of bothfamilies and, specially, industry. Many banking entities had an excessiverisk exposure due to this fact. The crisis has been very severe in theproperty and building sectors, with very high rates of unemployment,bankruptcy of companies and non-repayment of liabilities and credits,and this has sharply affected the Spanish banking sector, meaning theliquidation, breakdown and disappearance of some entities, mainly savingsbanks. Other entities, again mainly savings banks, have merged followingthe directives of the Spanish central bank regarding recapitalizing offinancial entities to strengthen their balances. Some of them have evenbeen intervened by the central bank. As a consequence, the number ofcredit cooperatives has been reduced from 85 to 76 between the years2007 and 2011, and the number of savings banks has been reduced from46 to 35 during the same period, with the additional circumstance, in thiscase, that many saving banks have transferred their banking activity tonew banks38 created under the national central bank recommendations.

From 2008 there has been also a restriction in the credit flows of bankingmarkets. In the case of Spain, it has lead to a very drastic reduction ofthe credit to families, which fell down from growth rates of 20% duringthe pre-crisis years to an average growth rate of 5% in 2008, and toa decreasing rate of near -3% at the end of 201139. This contraction ofthe volume of credit, linked to the low profitability of the financialintermediation due to the low interest rates generally kept during thecrisis period to control the imbalances of local economies, incite the bankingsector to search for the deals with best profit-risk profiles. In fact, during2010 and 2011, conditions of credit granting have hardened becausethe transfer to clients of the growing difficulties of the banking sectorfunding40.

25

38 These banks have a separated legal structure from their related saving banks, but beingthese their main owners. Formally, these banks are S.A. ‘sociedades anónimas’, a legalfigure similar to PLC (in UK) and to Inc. (in the US).

39 Banco de España (2009 and 2012): Annual reports of 2008 and 2011. 40 Banco de España, 2012.

This contraction of credit has helped to avoid a greater over-indebtnessof Spanish families, but it has not mitigated their previous leverage dueto the lack of growth in terms of income41. Additionally, the continuousrising of unemployment rate in Spain and the expected generation oflarger pockets of poverty and exclusion constitute an environmentpropitious to the increase of financial exclusion.

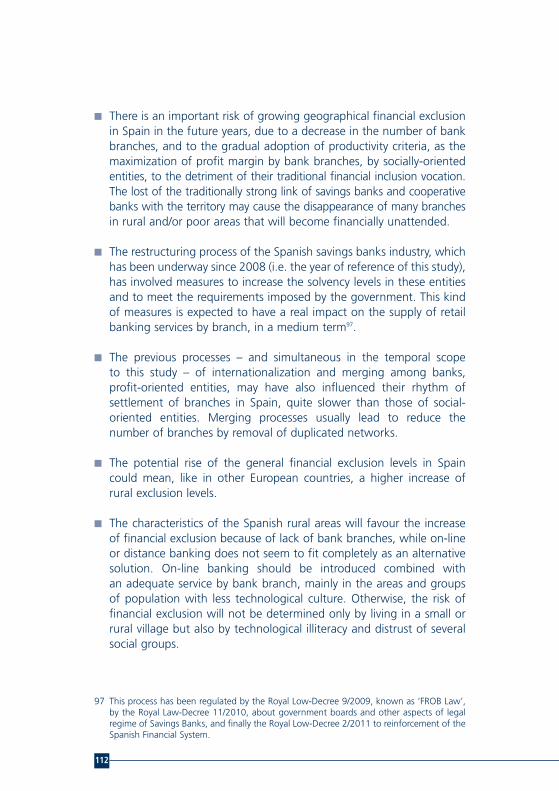

One of the kinds of financial exclusion potentially affected is thegeographical exclusion due to the reduction of the number of bankbranches, especially in those areas where branches are less profitable.This is the case of socioeconomically most deprived neighbourhoods orvillages, and of areas with low density of population. Paradoxically,the dynamism of the building sector has been also highlighted as anindicator to attract the set up of bank branches in a certain territory42.Thus, regions that are suffering also a greater intensity of the crisis effectsdue to an economy based mainly in this activity can be facing also ahigher risk of being financially left.

26

41 Banco de España, 2012. 42 Carbó and López del Paso, 2002.

43 As an adaptation of the classification proposed by the European Commission, 2008, pp 61.

27

The Spanish banking system is composed of three types of entities (banks,savings banks and cooperative banks), each of them with different originand legal form. Savings banks and cooperative banks were both createdwith the aim of promoting financial inclusion. The main objective ofsavings banks was the provision of financial services to all groups ofpopulation, especially to poor and disadvantaged people, unattended bybanks. Cooperative banks were founded to promote the financialinclusion of rural areas. Therefore, the Spanish banking entities can beclassified into profit oriented entities (banks) and socially-orientedentities (savings banks and cooperative banks), as shown in figure 2.143.

Figure 2.1. Financial services providers in Spain

Source: Own elaboration with data from the European Commission (2008): “Financial services

provision and prevention of financial exclusion”.

2. MARKET RESPONSESTO PROMOTE FINANCIALEXCLUSION: A REVIEW OFTHE TYPES OF COMMERCIALBANKING ENTITIES IN SPAIN

Financial servicesproviders

Commercial

Not for profit

Profit oriented: Banks

Socially oriented:Savings Banks andCooperative Banks

ICO, Bank of Spain

44 Palomo Zurdo, 2004.45 Gardener et al, 2005; Aalbers, 2003. 46 De la Cuesta, M.; Muñoz, M.J.; Fernández, M.A., 2006.47 Muñoz et al., 2005.

28

Thus, the different main purposes of the Spanish banking entities can becategorized as follows44:

n Banks: Maximization of value for shareholdersn Savings banks: Maximization of value for society through the action in

the community (obra social) n Cooperative banks: Maximization of services to meet the financial

needs of their members.

There are several kinds of responses to the financial exclusion in Europe,among them, the following45:

n Voluntary roles of banks (Spain, France, Germany and Belgium)n Government acting as mediator between banks and excluded people

(United Kingdom, and tentatively France)n Government acting as regulator (France, Portugal and Sweden)

2.1. Corporate Social Responsibility (CSR) applied tothe financial sector

Applying the concept of CSR to the financial system involves theintroduction of social and environmental issues, besides the financialones, in the policies, processes and products developed by the differentinstitutions that compose it46. Transparency is a key factor, not onlyfrom the point of view of the internal management or the governmentof financial institutions, but also in their relationship with all the otherplayers operating in the financial system, including families and individuals.

Several aspects have been defined as relevant in the management ofsocial risks of a banking entity, implementing criteria of corporate socialresponsibility and integrating sustainability in its operations47:

(i) Integration of ethical criteria in the assessment and granting of credits,in the investment policies and in the raising of savings and assets formanagement: e.g. proceedings to avoid the money laundering.

(ii) Decisions of the entity in order to offer services just to clients takingin account the social and environmental impact of their projects:e.g. giving credit only to sustainable projects when financing buildingactivities.

(iii) Respect of the human rights in those underdeveloped countrieswhere the institution is operating, and not contributing to a majorover-indebtness of these countries.

(iv) Engagement with the community in which it operates. This meansgiving facilities for the access to credit and financial services toregions, sectors or groups of population with risk of social andfinancial exclusion (due to geographical, age or technologicalknowledge, for example), and contributing with donations andpatronage activities into the community (community involvement).

Thus, for retail banking entities, assuring the access to basic financialservices of individuals, families and small companies, independently oftheir level of income, wealth or residence place, means internalising CSRcriteria in the business core.

2.2. Financial inclusion: a differentiating element in thecorporate social responsibility of banking entities

The access to credit through the banking system is the main source offinancial resources for families and SMEs48, which are necessary to face upto their investments and needs of consumption. The access to transactionservices is needed to access to some basic facilities and to social integration.Guaranteeing this access to basic financial services is also defined as asocial responsibility in order to keep the dynamism of a local economy,and talking in terms of banking industry, it means the integration of socialresponsibility into its business model.

The analysis of the integration of financial inclusion into the policies ofthe different kind of banking entities in Spain offers the followingprofiles:

n Banks: They are commercial financial services providers, profit-oriented and whose capital belongs to private shareholders. In Spainthere is no duty or regulations that force banks to supply peoplewithout resources or certain geographical areas.

29

48 Small and medium-sized enterprises.

Their strategies for territorial expansion are decided in base to themarket and to profitability criteria. The empirical research has foundevidences of a very low contribution of banks to the financial inclusionin Spain: they do not operate in almost the 50% of the towns withlower income. And a regional analysis of the region of Aragon,determined that the bank sector reduced its number of branchesbetween 1996 and 2004, meanwhile savings banks and cooperativebanks enlarged theirs49.

Regarding CSR policies of Spanish banks, they did not use to considerfinancial inclusion generally into their main objectives, at least duringthe pre-crisis period. An analysis of main Spanish banks CSR policies in2008 finds very few related strategies referring to financial inclusion,and mainly in developing countries (microcredit)50. But the analysis ofCSR policies in 2011 shows a different panorama: most of the CSRreports make mention to financial inclusion in Spain, to financialeducation and to providing of services adapted to people in risk ofsocial exclusion. All of them make reference to the financing of SMEsin an economic juncture of credit restrictions.

n Savings banks: Their origins go back to the 19th century and areprecisely based in motivations of financial inclusion of the broad socialgroups with fewer resources, with an aim of social progress of Spain51.The model was imported from other European countries, replicatingthe most successful experiences.

As not for profit organizations, they have less competitive pressure togenerate profits and give them out to shareholders. In addition, theirfoundational objectives make them to take in account social criteriafor the establishment of new branches. There are several evidences ofthe contribution of Spanish savings banks to financial inclusion: interms of proximity and suitable conditions and prices of bankingservices52; and in terms of facilitating basic transaction accounts andaccess to mortgages to a great part of the Spanish population,providing suitable remittance services to migrants, and developingmicrocredit in Spain53.

30

49 Bernad et al., 2007.50 Analysis based on the 2008 and 2011 CSR reports of Banco Santander, BBVA, Banco

Popular and Banco Sabadell. 51 Quintás, 2004.52 Carbó et al.,2002; Gardener et al.,2005; Riera, 2005. 53 European Commission, 2002 ; Garderner et al., 2005.

Additionally it has been stated that already in 1998, for 13% ofSpanish towns, standing for a 3.5% of total population, saving bankswere the only kind of entity supplying banking services54. A moredetailed study of same authors55 determined that saving banks havefinancially rescued villages of an average population of two thousandpeople, tending to grow and become urban units, and with higherrates of women unemployment regarding national average.

n Cooperative banks: they keep their traditional link to social economy(their market) and to rural areas. Several authors confirm this issue,highlighting their effect in the financial inclusion of people living inrural areas and with very basic needs56. Also it has been empiricallystated that cooperative banks, jointly with savings banks industry,are the main contributors to financial inclusion in Spain, particularly intowns with low income average levels, attended in a 98% exclusivelyby both kind of entities57.

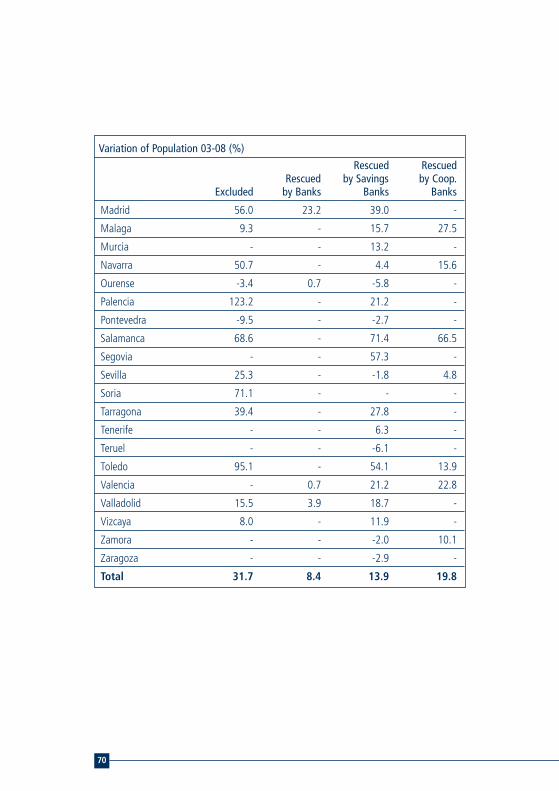

2.3. Banking models and effects of financial crisis

When analysing the effects of the current financial crisis in terms ofreduction of bank branches in Spain, we can see a different evolution forevery kind of banking entities, as shown in table 2.1.

Table 2.1. Annual growth of bank branches by kind of bankingentity. Comparison between 08-09 and 03-08

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009

(Economic Yearbook 2009).

31

54 Carbó et al., 2002.55 Carbó y López del Paso (2002).56 Bernad et al, 2007; European Commission, 2002.57 Bernad et al, 2007.

Savings Cooperative Banks Banks Banks

Average annual growthof branches 03-08 2.09% 4.20% 3.17%

Annual growth of branches 08-09 0.05% 0.32% 0.58%

It can be considered that the year 2008 was the first whole economicperiod lived in Spain into the crisis scenario. That year there was a sharpcontraction of the growth rhythm of setting up of branches for allthe typologies of banking entities, regarding the average annual growthof the previous years. In fact, during the year 2008 there was a low growthof the number of banking branches. Banks have slowed the most therhythm of branches expansion (that during the previous years was alreadythe slowest one), and cooperative banks have experienced a softerdeceleration. Savings banks, that previously had been leaders in terms ofsetting up of branches in Spain, have showed during 2009 a reduction ofthat tendency, with a rhythm of growth of branches ten times lower thatthe annual average of the five previous years. It must be highlightedthat during the second half of 2008 began the merging processes amongsaving banks.

32

58 See Carbó and López del Paso, 2002, and Carbó et al (2002).59 LA CAIXA (2009). Anuario Económico de España, 2009. 60 The analysis developed by Carbó and López del Paso (2002), just analyses the role of

savings banks, as this is the kind of banking entity with a more important effect in termsof financial inclusion of small villages in Spain. The actual work pretends, as well as toverify that this role remains the same and to define the tendency followed during the yearsbetween both analysis (2002-2008), to determine potential differences among the villagesfinancially rescued by every kind of banking entity.

61 The analysis of socioeconomic characteristics of excluded and rescued villages, follows andreviews the methodology proposed by Carbó and López del Paso (2002). It assumes thehypothesis that savings banks are the kind of entities making a larger effort in the financialinclusion of small villages, but enlarges the analysis also to the performance of banks andcooperative banks, to determine if there are socioeconomic differences among the villagesrescued by every kind of entity.

62 Carbó and López del Paso, 2002, and Carbó et al (2002).

33

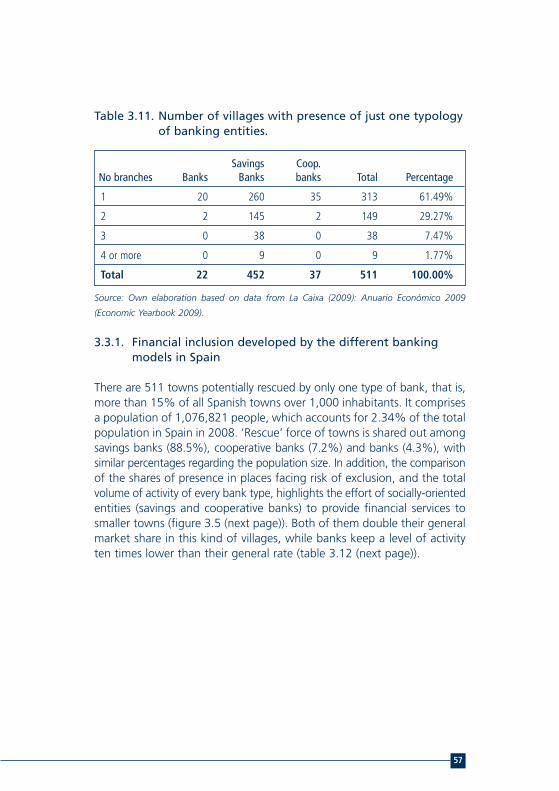

This chapter contains an empirical analysis regarding the financialexclusion of Spanish villages and it is based on the previous research outputof the Financial System Department of the Foundation for Economicand Social Research of the Spanish Confederation of Savings Banks58.The analysis takes as time reference the year 2008 and uses the statisticaldata provided by the Economic Yearbook 2009 published by La Caixa59.It determines the number and social features of the Spanish villages withpopulation over 1,000 inhabitants, that are financially excluded, what meansthat they do not have any bank branch. At the same time it analyses the‘financial rescue’ of villages by the different types of banks (savings banks,cooperative banks, or banks)60, determining their relative importanceregarding this issue61.

3.1. Territorial financial exclusion, size of villages andrural areas: relation between concepts

Preceding studies62 conclude that saving banks are the banking entitieswith clearer vocation of service to small villages and those contributing ina major way to their financial inclusion.

3. GEOGRAPHICAL FINANCIALEXCLUSION IN SPAIN:ANALYSIS OF SIGNIFICATIVEDIFFERENCES

64 Carbó and López del Paso, 2002. 65 OCDE (2009): “OECD Regional Typology”. Dirección de Gobierno público y Desarrollo

Territorial, 4 de Marzo de 2009.66 These units are called ‘municipios’ in the Spanish case. 67 Exceptionally, for Japan and Korea this limit is 500 inhabitants per square kilometre,

due to their high national densities of population.

34

Geographic and demographic factors, as the density of population, maydefine the provision – or not- of financial services through bank branchin a region. As it is described in chapters 1 and 2, different authors agreethat commercial banks that use productivity criteria to choose whichpotential market to attend, give priority to the best profit-risk profiles63.In terms of geographical expansion of these entities through branches,it means a tendency to set up branches in higher income areas, with highindustrial and commercial activity, and enough population, that is apotential market that can guarantee their productivity’s objectives64.Then, areas that do not fit in this profile – poor neighbourhoods,small villages, rural areas – may face a serious risk of financial exclusion,as they do not seem interesting enough in terms of profit to be attendedby bank branches.

This study defines the geographical or territorial financial exclusion asthe absence of financial services offered by, at least, one bank branch ina village or territory. Physical presence of bank branches is important tosolve problems of financial exclusion based on supply factors (provision ofservices adapted to local population), and on demand factors (financialself-exclusion, low knowledge about products and services, etc.). Staff ofbranches make easier the understanding of financial terms and languageto the potential users, and also can explain how certain financial productsand services work. Personal relationship with the staff of a branch givessome people the necessary trust to use financial services.

It is important also to state if villages of minor size belong necessaryto rural areas, in order to delimit the concept of territorial financialexclusion. The Organisation for Economic Co-operation and Development(OECD) defines both the concepts of urban and rural areas65.Following these definitions, the main factor to define a local area as ruralor urban is its density of population: local units (regional division atthe lowest geographic level66) are classified as rural if their density ofpopulation is lower than 150 inhabitants per square kilometre67. Thus, itmust be considered both the number of inhabitants and also theextension of the territory.

68 For the Spanish case, this regional level is divided in provinces (provincias), andautonomous regions (comunidades autónomas). Autonomous regions are integrated byone or several provinces.

69 BOE (2007): “LEY 45/2007, de 13 de diciembre, para el desarrollo sostenible del mediorural”. Boletín Oficial del Estado.

35

In terms of delimitation for this study, a local analysis of the density ofpopulation would be too detailed. Thus, it is used the next level in thegeographical scale, the regional level68, and under the standards ofthe OECD the classification of the Spanish regions remains as follows:

n Predominantly urban (PU), when less than a 15% of total populationlives in rural local units.

n Intermediate (IN), when the average of population living in rural localunits keeps between 15% and 50%.

n Predominantly rural (PR), when more than a 50% of population isliving in local rural units.

There is an additional criterion, the absolute size of urban centres locatedin a regional territory:

n A region initially classified as predominantly rural (PR) is consideredintermediate (IN) if holds an urban centre of more than 200,000inhabitants, representing at less the 25% of the total regional population.

n A region initially classified as intermediate (IN) is considered predominantlyurban (PU) if holds an urban centre of more than 500,000 inhabitants,representing at less the 25% of the total regional population.

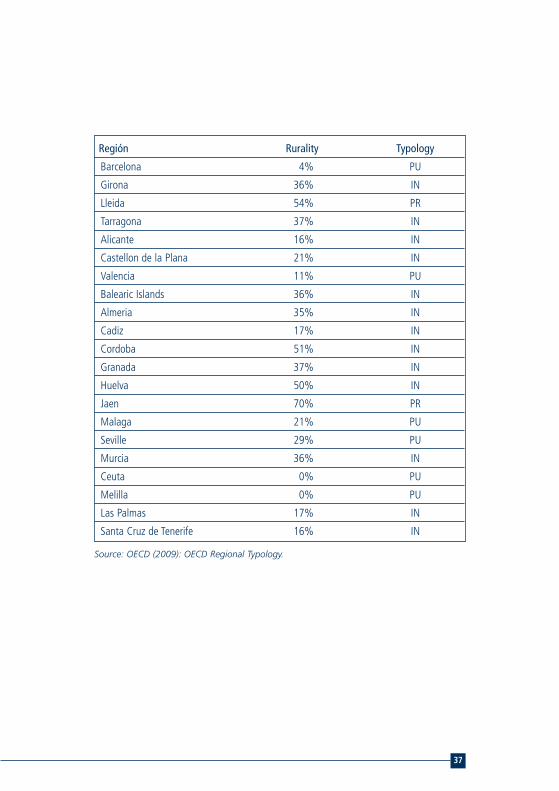

The classification of the Spanish regions (provinces) in terms of ruralcharacter is shown in table 3.1 and in figure 3.1 on the next page.

The Spanish regulation of the rural medium69 gives also references for thedefinition of rural areas:

n The rural medium is the geographic territory formed by the aggregationof towns (municipios) or smaller local units, recognized by the competentauthorities, with a population of less than 30,000 inhabitants and adensity of population of less than 100 inhabitants per square kilometre.

n Rural towns (municipio) of small size hold a resident population of lessthan 5,000 inhabitants and are integrated in the rural area.

Table 3.1. Spanish regions and rural typology

36

Región Rurality Typology

A Coruña 30% IN

Lugo 73% PR

Orense 56% PR

Pontevedra 21% IN

Asturias 26% IN

Cantabria 25% IN

Alava 16% IN

Guipúzcoa 7% PU

Vizcaya 6% PU

Navarra 45% IN

La Rioja 31% IN

Huesca 74% PR

Teruel 100% PR

Zaragoza 26% PU

Madrid 4% PU

Avila 63% PR

Burgos 33% IN

Leon 46% IN

Palencia 51% PR

Salamanca 43% IN

Segovia 61% PR

Soria 100% PR

Valladolid 31% IN

Zamora 59% PR

Albacete 100% PR

Ciudad Real 77% PR

Cuenca 100% PR

Guadalajara 44% IN

Toledo 65% PR

Badajoz 88% PR

Caceres 91% PR

Source: OECD (2009): OECD Regional Typology.

37

Región Rurality Typology

Barcelona 4% PU

Girona 36% IN

Lleida 54% PR

Tarragona 37% IN

Alicante 16% IN

Castellon de la Plana 21% IN

Valencia 11% PU

Balearic Islands 36% IN

Almeria 35% IN

Cadiz 17% IN

Cordoba 51% IN

Granada 37% IN

Huelva 50% IN

Jaen 70% PR

Malaga 21% PU

Seville 29% PU

Murcia 36% IN

Ceuta 0% PU

Melilla 0% PU

Las Palmas 17% IN

Santa Cruz de Tenerife 16% IN

Figure 3.1. Spanish regions and rural typology

Source: OECD (2009): “OECD Regional Typology”.

Thus, the analysis developed in chapters 3 and 4 will be based on thefollowing parameters:

n Towns with less than 1,000 inhabitants are generally considered asrural areas.

n Towns with less than 5,000 inhabitants are considered small villages,but not necessarily rural areas, except those cases which are located inregions classified as PR.

n The chapter 4 focuses on two regions (autonomous communities)with very different socioeconomic features: Andalusia and Catalonia.Both of them have provinces classified as predominantly rural (PR),predominantly urban (PU) and intermediate (IN), this last categorybeing the most common. But following the table 3.2, we find thatthe density of population of Andalusia is quite lower than is the casein Catalonia.

38

n Predominantly ruraln Intermediaten Predominantly urban

Table 3.2. Density of population of Andalusia and Catalonia

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009

(Economic Yearbook 2009).

To assign an average score on the scale of the OECD to everyautonomous community, some estimations have been calculated asshowed in table 3.3 (Estimation of average ‘rurality’ of Andalusia andCatalonia). Their correspondence with the general classification of theOECD is Andalusia being an intermediate region and Catalonia being apredominantly urban region.

Table 3.3. Estimation of average ‘rurality’ of Andalusiaand Catalonia

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009

(Economic Yearbook 2009), and OECD (2009): OECD Regional Typology.

39

Population Extension (km²) Density of population

Andalusia 8,202,220 87,591 93.64

Catalonia 7,364,078 32,091 229.47

Rurality Population Rural population

Almeria 35% 667,635 233,672

Cadiz 17% 1,220,467 207,479

Cordoba 51% 798,822 407,399

Granada 37% 901,220 333,451

Huelva 50% 507,915 253,958

Jaen 70% 667,438 467,207

Malaga 21% 1,563,261 328,285

Seville 29% 1,875,462 543,884

Total 8,202,220 2,775,335

Average rurality Andalusia 33.84%

Barcelona 4% 5,416,447 216,658

Girona 35% 731,864 256,152

Lleida 54% 426,872 230,511

Tarragona 37% 788,895 291,891

Total 7,364,078 995,212

Average rurality Catalonia 13.51%

70 European Commission, 2008.71 European Commission, 2008; Carbó and López del Paso, 2002.

40

3.1.1. Financial exclusion and rural areas

Rural financial exclusion, clearly linked to the concept of territorialfinancial exclusion, is seen as a minor problem for EU-15 countries70.As table 3.4 (Average of European population financially excluded,by geographical areas of residence) shows: In the countries with a lowmedium level of national financial exclusion (between 3% and 8%),the exclusion in rural areas accounts only for 4% on average. This is thegroup to which Spain belongs. However, countries with a high mediumlevel of financial exclusion (between 12% and 28%), such as Ireland,Italy or Greece, rural financial exclusion is estimated to be up to 20%.Looking to the EU-10 countries, financial exclusion rises to 43% in ruralareas – meanwhile in large cities it is 25% – and it constitutes really amatter of concern.

In fact, some authors have highlighted that, in the richer countries,the relationship of financial exclusion with low incomes and deprivedsocial and familiar environments71, raises the discussion about theconcentration of financially excluded population in larger cities, wherewider pounds of poverty are located.

Countries with low-medium level of

EU15 Countries* EU10 Countries** financial exclusion***

Rural area or village 7 43 4

Small or middle sized town 7 30 5

Large town 6 25 5

Table 3.4. Average of European population financially excluded,by geographical areas of residence

* EU15: Germany, Austria, Belgium, Denmark, Finland, France, Greece, the Netherlands, Ireland, Italy, Luxembourg,

Portugal, Spain, Sweden and the United Kingdom.

** EU10: Cyprus, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovenia and Slovakia.

*** Spain belongs to the group of countries with low-medium level of financial exclusion, as it has been

established by the abovementioned study.

Source: Own elaboration based on data from European Commission (2008): Financial Services Provision and

Prevention of Financial Exclusion.

Nevertheless, there are some important factors related to the financialexclusion that we can easily find as features of Spanish rural areas:

n Low industrial and commercial activity.n Unemployment and low incomes.n High rate of people out of the labour market (housewives, retired

people, etc.).n High rate of elderly population.n Lower level of education, including financial education.n Higher frequency of cash economic transactions. n Increasing immigrant population.

There are also other factors leading to a preferential setting up of bankbranches in urban areas, with detriment to rural ones72:

n Higher financial culture in urban centres, with larger average amounts,diversity and number of transactions per user.

n Lower dispersion levels of resident population in urban centres, whatmeans higher volumes of activity per branch and, subsequently, higherprofit margin.

n Variation of population, increasing in urban centres and descending inmany rural areas.

n Economically deprived regions, with high unemployment levels andlow incomes per capita, profile in which many rural areas in Spain fit.

n Production and commercialization of goods and services, moredynamic in urban than in rural areas.

n Access to the Internet and generally to telecommunications facilities,as mobiles phones, which constitute new channels to provide bankingservices, and whose use is limited among elder population, andsubsequently, among rural population.

Thus, all these factors are analysed in this chapter from a double perspective:the size of population of villages and towns (not determinant, but aninitial indicator of their rural or urban character); and the classification aspredominantly rural (PR), intermediate (IN) or predominantly urban (PU) oftheir region of reference (autonomous community or province). The resultscontained in chapter 4 also gather this double perspective in the rural orurban classification of villages and the consequences in terms of financialservices, for two regions: Andalusia and Catalonia.

41

72 Carbó et al., 2002

3.1.2. Bank branches and their relevance tackling financialexclusion

The wide expansion of bank branches in Spain has been very importantto satisfy the needs and expectations of users of financial services.Other models, such as phone or postal banking, have had a very limiteddevelopment due to the general and traditional distrust of Spanishpopulation to long-distance sales services. The users of banking servicesin Spain give great importance to the personalised attention at a bankbranch and even to the personal relationship with the commercial staff,in the process of selection and hiring of financial services. Additionally,recommendations of the branch staff are highly valued – and followed-by the clients with less financial culture, as they feel ‘lost’ in the selectionof financial products.

On-line banking does not seem to solve the lack of financial servicesthrough branches in Spanish rural areas, due to some specific negativefactors:

n Low level of financial culture, which makes the intermediation andassessment role of the bank staff very relevant for the buying financialservices.

n Widespread difficulties using on-line banking and technologies, andthose specific of rural areas in Spain: limited fixed phone lines in areaswith low population density; higher cost of mobile communicationsand internet connection than costs in other European countries, old-aged population in rural areas with very low culture of use of newtechnologies.

The analysis of the consequences of the deregulation process of theSpanish financial system in the 70’s and 80’s concluded that in 1998the 40.1% of Spanish villages did not have any bank branch in theirterritory73. The average size of those villages was 2,500 inhabitants, andthe total population financially excluded for living in these villages wasabout 3.2% of total Spanish population. It was also stated that savingsbanks were the entities with the largest impact on financial inclusion ofsmall and rural villages, as they developed a significant part of theirbusiness in those areas. These conclusions have been supported bysubsequent studies74.

42

73 Carbó et al., 2002.74 Carbó and López del Paso, 2002 and 2005.

In the past, the Spanish banking system, and in particular the savingsbanks industry, made great efforts to cover the maximum number ofvillages through bank branches75. Meanwhile, the cooperative bankssector is the one most actively engaged with supplying retail financialservices to rural areas76.

To compensate the lack of bank branches in rural areas, some alternativemeans have been introduced: on-line banking, buses acting as travellingbranches, commercial agents, or periodical visits of staff from the mainbranch to financially unattended villages in the same region. There is notmuch information available about those alternative ways to attend torural population, and for this reason it is difficult to value exactly theirsuccess in terms of geographical financial inclusion. But, consideringthat the Spanish rural population is not given to use distance or on-linebanking and that travelling bank branches offer only a temporary service,it seems important to analyse the magnitude and causes of the lack ofphysical and permanent bank branches in Spanish villages.

The current process of restructuring of the banking sector in Spain,including changes in the savings banks industry, might have seriousconsequences for the financial exclusion level in this country, due toprice-factors and geographical access- factors. The potential rise of therates of exclusion could affect harshly the Spanish rural areas. Therefore,it is important to study the situation of the geographical financialexclusion in the initial phase of this process, and to analyse the role of thedifferent Spanish banking models in approaching exclusion.

3.2. Geographical financial coverage in the differentregions of Spain

The number of bank branches in Spain has risen between 1999 and 2008in a slightly higher rate than the population did, as it is shown in table3.5 on the next page. Therefore, geographical coverage per branch of theSpanish Banking System has not been negatively affected, at least in aquantitative sense, in comparison with previous studies on the rate offinancial exclusion77.

43

75 Delgado and Rodríguez, 2006.76 European Commission, 2008.77 Carbó et al., 2002.

Table 3.5. Increase of bank branches and rise of populationin Spain, 1999-2008

Source: Own elaboration based on data from Banco de España (2009): Boletín Estadístico

2009, and Instituto Nacional de Estadística (National Institute of Statistics).

Bank branches established in small centres of population have to work inless relevant markets in terms of number of potential clients, and thus,they assume a comparative disadvantage of getting the same profitmargin as those branches operating in larger markets. However, thepresence in smaller villages shows that banks make an additional effortto supply their services, taking into account not only the economic profit,but also the social profit stemming from generating financial inclusion.Table 3.6 shows a comparison of the relative effort made by the differentkind of retail banks to include financially small villages in Spain78.

To determine the average number of people attended per bank branch inSpain, the outcomes have also been segmented in two series. The firstone comprises towns with 1,000 inhabitants or more, which represents96.7% of total Spanish population, and the second one, covers townswith less than 1,000 inhabitants, that is 3.3% of total population.

44

78 As it has been stated in Chapter 2, in Spain there are three different models of retailbanking institutions: Banks (whose corporate status is usually a public limited company),savings banks and cooperative banks.

1999 2008 Increase

Bank branches 38,986 45,662 17%

Total population 40,202,160 46,157,822 15%

Banks Savings banks Cooperative banksNo. No. No.

branches % branches % branches %

Towns with 1,000 inhabitants or more 15,457 99.16% 23,729 94.81% 4,485 87.46%

Towns with less than 1,000 inhabitants 131 0.84% 1,298 5.19% 643 12.54%

Table 3.6. Activity rates of the different kind of retail banks in towns aboveand under 1,000 inhabitants

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009 (Economic Yearbook 2009).

These data have also been also disclosed by region, as shown in table 3.779.

45

79 The database used in this analysis, La Caixa: Anuario Económico de España (EconomicYearbook of Spain), 2009, offers only detailed data about the number of banks establishedin every town, when villages have above one thousand inhabitants. The coverage ofsmaller towns by banking services can be analysed using aggregated data by region,provided by the same source.

Towns with 1,000 inhabitants or more

Savings Coop Total No. People/Population Banks Banks Banks branches branch

Total Spain 44,648,478 15,457 23,729 4,485 43,671 1022.38

Andalusía 8,099,599 1,976 3,783 1,108 6,867 1179.50

Aragon 1,169,772 407 716 283 1,406 831.99

Asturias 1,071,046 450 375 127 952 1125.05

Balearic Island 1,069,228 562 655 30 1,247 857.44

Canary Islands 2,075,253 590 725 148 1,463 1418.49

Cantabria 567,259 217 258 19 494 1148.30

Castile-León 2,059,488 914 1,347 331 2,592 794.56

Cast-La Mancha 1,867,646 485 958 328 1,771 1054.57

Catalonia 7,171,750 2,352 5,466 140 7,958 901.20

Valenc. Com, 4,936,275 1,732 2,385 793 4,910 1005.35

Extremadura 1,000,714 396 558 154 1,108 903.17

Galicia 2,771,939 1,237 1,214 46 2,497 1110.11

Madrid 6,251,210 2,625 3,265 119 6,009 1040.31

Murcia 1,424,549 371 711 269 1,351 1054.44

Navarre 564,916 226 258 158 642 879.93

Basque Country 2,111,334 772 817 371 1,960 1077.21

La Rioja 287,663 125 216 57 398 722.77

Ceuta 77,389 9 14 2 25 3095.56

Melilla 71,448 11 8 2 21 3402.29

Table 3.7. Average number of people attended per bank branch,sorted by town’s size and region

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009 (Economic Yearbook 2009).

The average people attended per bank branch in Spain in 2008 was1,010.77. In the case of larger towns (1,000 inhabitants or more)this number rose to 1,022.38, but for smaller villages it decreased to756.56 people per branch. This shows that the average size of thepotential market of a Spanish bank branch is around 1,000 inhabitants.In other words, towns with more than 1,000 people should be interestingenough, in terms of profit, to be established at least one retail bankbranch in them.

46

Towns with less than 1,000 inhabitants

Savings Coop Total No. People/Population Banks Banks Banks branches branch

Total Spain 1,509,344 131 1,298 643 1,995 756.56

Andalusía 102,621 1 102 40 143 717.63

Aragon 157,146 11 203 176 390 402.94

Asturias 9,092 1 5 8 14 649.43

Balearic Island 3,616 2 5 0 7 516.57

Canary Islands 715 0 0 0 0 -

Cantabria 14,879 5 4 0 9 1653.22

Castile-León 497,842 55 375 140 570 873.41

Cast-La Mancha 175,454 6 115 128 249 704.63

Catalonia 192,328 18 122 0 140 1373.77

Valencian Commun. 93,326 2 65 84 151 618.05

Extremadura 97,030 20 66 3 89 1090.22

Galicia 12,230 0 15 0 15 815.33

Madrid 20,428 1 14 0 15 1361.87

Murcia 1,560 0 2 0 2 780.00

Navarre 55,461 4 40 31 75 739.48

Basque Country 45,778 1 27 0 28 1634.93

La Rioja 29,838 0 96 2 98 304.47

Ceuta 0 0 0 0 0 -

Melilla 0 0 0 0 0 -

Table 3.7. Average number of people attended per bank branch,sorted by town’s size and region

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009 (Economic Yearbook 2009).

In absolute terms, the number of savings banks branches doubles thenumber of those belonging to cooperative banks in towns with less than1,000 inhabitants. But cooperative banks make a relatively greater effort,taking into account their total number of branches: The 12.5% of thebranches of cooperative banks are located in the smaller villages, wherethe potential market size per branch is a 25% lower than in larger towns.For savings banks this percentage is 5.2%. Banks prefer targeting thelargest towns, which are believed to have higher profit-margins perbranch, and have just a 0.8% of branches located in the villages under1,000 inhabitants.

With regard to regional results, there is a wide variation in the averagenumber of people attended per branch in towns with at least 1,000inhabitants (1,010.77). Some regions such as the Canary Islands orAndalusia exceed this average, and the North- African cities of Ceutaand Melilla, even triple it. Worst results are found in outlying provinces,which means either that financial entities need there a larger potentialmarket to attend per branch to get the same profit rates as in otherregions, or that banks relegate the setting up of branches in those areasin favour of investing in richer and more developed provinces.

In the case of towns with less than 1,000 people, the worst attendedregions are Cantabria, Extremadura, Catalonia, Madrid and the BasqueCountry, with very saturated branches in their smaller villages. This findingconfirms the paradoxical conclusions of Carbó et al. (2002), which statethat rural areas of provinces in which there are important financialcentres, such as Madrid or Bilbao, are poorly covered by bank branches.This ‘oblivion effect’ of small villages could be explained by thecomparatively enormous attractiveness of nearby urban areas, in terms ofprofit potential.

The regions with better coverage by bank branches in villages over1,000 inhabitants are Aragon, Balearic Islands and Castile-Leon, findingthe best ratios in predominantly rural provinces as Huesca, Soria, Palenciaand Segovia. In the case of villages under 1,000 inhabitants, the bestratios are found also in Aragon and Balearic Islands, but not in Castile-Leon,where the smallest villages are quite worse attended than the nationalaverage. On the opposite side is Asturias, where the smallest villages showbetter coverage ratios than those with more than 1,000 inhabitants.

47

3.2.1. Geographical financial exclusion in the different regionsof Spain.

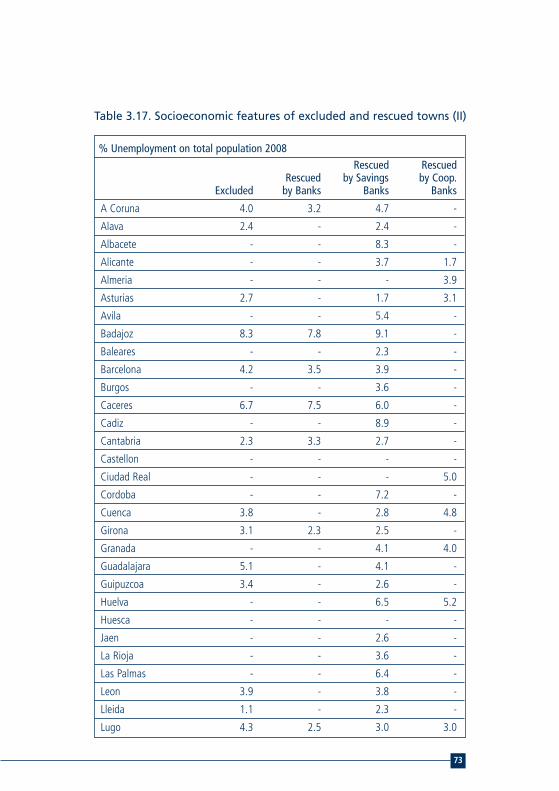

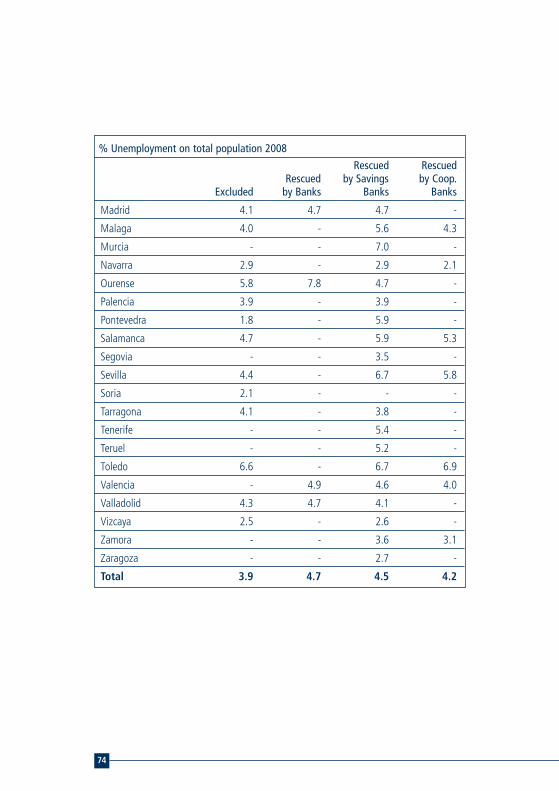

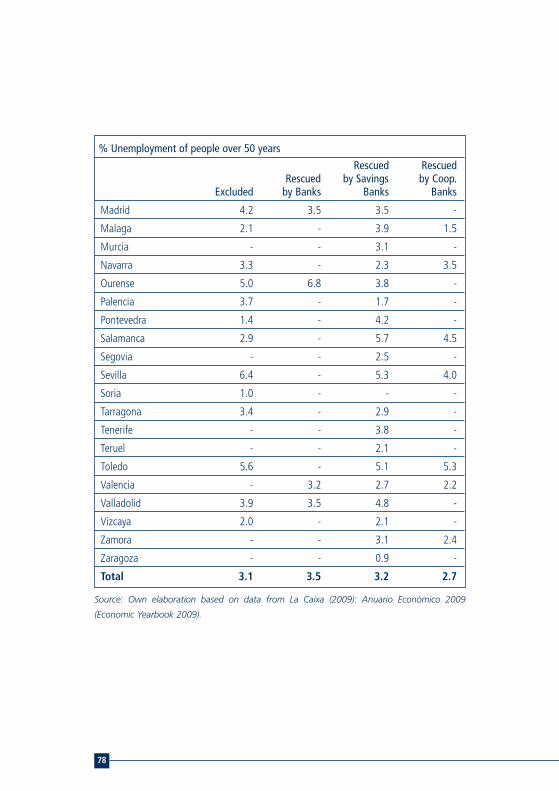

Considering an average of 1,010.77 inhabitants per bank branch in Spain,this amount could be used as a threshold to analyse how many towns,whose population exceeds it, do not have any branch at their disposal,and what the reasons are. The chosen database, aforementioned, allowshaving the information of towns over 1,000 inhabitants broken down toa municipal, provincial and regional level80. The rates of geographicalfinancial exclusion by region are shown in table 3.8.

Table 3.8. Rates of geographical financial exclusion by regions

Source: Own elaboration based on data from La Caixa (2009): Anuario Económico 2009

(Economic Yearbook 2009).

48

80 The territory of Spain is divided in three levels: local units or towns (municipios), provinces(provincias), and autonomous regions (comunidades autónomas). Autonomous regions areintegrated by one or several provinces.

Absence of bank branchesNo. towns % of total

over 1,000 in. Population population

Andalusia 3 4,997 0.06%

Aragon 0 0 0.00%

Asturias 2 4,477 0.41%

Balearic Islands 0 0 0.00%