Perak Transit Berhad SUBSCRIBE -...

17

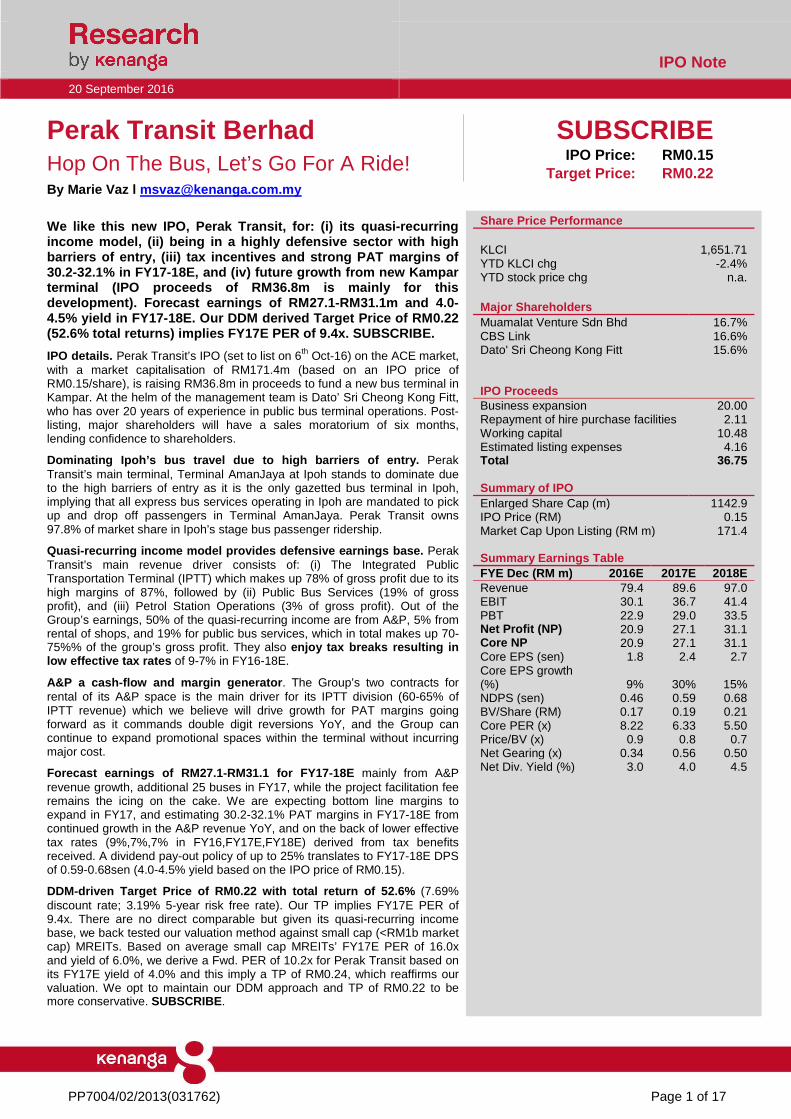

IPO Note 20 September 2016 PP7004/02/2013(031762) Page 1 of 17 Perak Transit Berhad SUBSCRIBE Hop On The Bus, Let’s Go For A Ride! IPO Price: RM0.15 Target Price: RM0.22 By Marie Vaz l [email protected] We like this new IPO, Perak Transit, for: (i) its quasi-recurring income model, (ii) being in a highly defensive sector with high barriers of entry, (iii) tax incentives and strong PAT margins of 30.2-32.1% in FY17-18E, and (iv) future growth from new Kampar terminal (IPO proceeds of RM36.8m is mainly for this development). Forecast earnings of RM27.1-RM31.1m and 4.0- 4.5% yield in FY17-18E. Our DDM derived Target Price of RM0.22 (52.6% total returns) implies FY17E PER of 9.4x. SUBSCRIBE. IPO details. Perak Transit’s IPO (set to list on 6 th Oct-16) on the ACE market, with a market capitalisation of RM171.4m (based on an IPO price of RM0.15/share), is raising RM36.8m in proceeds to fund a new bus terminal in Kampar. At the helm of the management team is Dato’ Sri Cheong Kong Fitt, who has over 20 years of experience in public bus terminal operations. Post- listing, major shareholders will have a sales moratorium of six months, lending confidence to shareholders. Dominating Ipoh’s bus travel due to high barriers of entry. Perak Transit’s main terminal, Terminal AmanJaya at Ipoh stands to dominate due to the high barriers of entry as it is the only gazetted bus terminal in Ipoh, implying that all express bus services operating in Ipoh are mandated to pick up and drop off passengers in Terminal AmanJaya. Perak Transit owns 97.8% of market share in Ipoh’s stage bus passenger ridership. Quasi-recurring income model provides defensive earnings base. Perak Transit’s main revenue driver consists of: (i) The Integrated Public Transportation Terminal (IPTT) which makes up 78% of gross profit due to its high margins of 87%, followed by (ii) Public Bus Services (19% of gross profit), and (iii) Petrol Station Operations (3% of gross profit). Out of the Group’s earnings, 50% of the quasi-recurring income are from A&P, 5% from rental of shops, and 19% for public bus services, which in total makes up 70- 75%% of the group’s gross profit. They also enjoy tax breaks resulting in low effective tax rates of 9-7% in FY16-18E. A&P a cash-flow and margin generator. The Group’s two contracts for rental of its A&P space is the main driver for its IPTT division (60-65% of IPTT revenue) which we believe will drive growth for PAT margins going forward as it commands double digit reversions YoY, and the Group can continue to expand promotional spaces within the terminal without incurring major cost. Forecast earnings of RM27.1-RM31.1 for FY17-18E mainly from A&P revenue growth, additional 25 buses in FY17, while the project facilitation fee remains the icing on the cake. We are expecting bottom line margins to expand in FY17, and estimating 30.2-32.1% PAT margins in FY17-18E from continued growth in the A&P revenue YoY, and on the back of lower effective tax rates (9%,7%,7% in FY16,FY17E,FY18E) derived from tax benefits received. A dividend pay-out policy of up to 25% translates to FY17-18E DPS of 0.59-0.68sen (4.0-4.5% yield based on the IPO price of RM0.15). DDM-driven Target Price of RM0.22 with total return of 52.6% (7.69% discount rate; 3.19% 5-year risk free rate). Our TP implies FY17E PER of 9.4x. There are no direct comparable but given its quasi-recurring income base, we back tested our valuation method against small cap (<RM1b market cap) MREITs. Based on average small cap MREITs’ FY17E PER of 16.0x and yield of 6.0%, we derive a Fwd. PER of 10.2x for Perak Transit based on its FY17E yield of 4.0% and this imply a TP of RM0.24, which reaffirms our valuation. We opt to maintain our DDM approach and TP of RM0.22 to be more conservative. SUBSCRIBE. Share Price Performance KLCI 1,651.71 YTD KLCI chg -2.4% YTD stock price chg n.a. Major Shareholders Muamalat Venture Sdn Bhd 16.7% CBS Link 16.6% Dato' Sri Cheong Kong Fitt 15.6% IPO Proceeds Business expansion 20.00 Repayment of hire purchase facilities 2.11 Working capital 10.48 Estimated listing expenses 4.16 Total 36.75 Summary of IPO Enlarged Share Cap (m) 1142.9 IPO Price (RM) 0.15 Market Cap Upon Listing (RM m) 171.4 Summary Earnings Table FYE Dec (RM m) 2016E 2017E 2018E Revenue 79.4 89.6 97.0 EBIT 30.1 36.7 41.4 PBT 22.9 29.0 33.5 Net Profit (NP) 20.9 27.1 31.1 Core NP 20.9 27.1 31.1 Core EPS (sen) 1.8 2.4 2.7 Core EPS growth (%) 9% 30% 15% NDPS (sen) 0.46 0.59 0.68 BV/Share (RM) 0.17 0.19 0.21 Core PER (x) 8.22 6.33 5.50 Price/BV (x) 0.9 0.8 0.7 Net Gearing (x) 0.34 0.56 0.50 Net Div. Yield (%) 3.0 4.0 4.5

Transcript of Perak Transit Berhad SUBSCRIBE -...

IPO Note

20 September 2016

PP7004/02/2013(031762) Page 1 of 17

Perak Transit Berhad SUBSCRIBE Hop On The Bus, Let’s Go For A Ride! IPO Price: RM0.15

Target Price: RM0.22 By Marie Vaz l [email protected]

We like this new IPO, Perak Transit, for: (i) its q uasi-recurring income model, (ii) being in a highly defensive sect or with high barriers of entry, (iii) tax incentives and strong PAT margins of 30.2-32.1% in FY17-18E, and (iv) future growth from new Kampar terminal (IPO proceeds of RM36.8m is mainly for thi s development). Forecast earnings of RM27.1-RM31.1m a nd 4.0-4.5% yield in FY17-18E. Our DDM derived Target Pric e of RM0.22 (52.6% total returns) implies FY17E PER of 9.4x. SU BSCRIBE.

IPO details. Perak Transit’s IPO (set to list on 6th Oct-16) on the ACE market, with a market capitalisation of RM171.4m (based on an IPO price of RM0.15/share), is raising RM36.8m in proceeds to fund a new bus terminal in Kampar. At the helm of the management team is Dato’ Sri Cheong Kong Fitt, who has over 20 years of experience in public bus terminal operations. Post-listing, major shareholders will have a sales moratorium of six months, lending confidence to shareholders.

Dominating Ipoh’s bus travel due to high barriers o f entry. Perak Transit’s main terminal, Terminal AmanJaya at Ipoh stands to dominate due to the high barriers of entry as it is the only gazetted bus terminal in Ipoh, implying that all express bus services operating in Ipoh are mandated to pick up and drop off passengers in Terminal AmanJaya. Perak Transit owns 97.8% of market share in Ipoh’s stage bus passenger ridership.

Quasi-recurring income model provides defensive ear nings base. Perak Transit’s main revenue driver consists of: (i) The Integrated Public Transportation Terminal (IPTT) which makes up 78% of gross profit due to its high margins of 87%, followed by (ii) Public Bus Services (19% of gross profit), and (iii) Petrol Station Operations (3% of gross profit). Out of the Group’s earnings, 50% of the quasi-recurring income are from A&P, 5% from rental of shops, and 19% for public bus services, which in total makes up 70-75%% of the group’s gross profit. They also enjoy tax breaks resulting in low effective tax rates of 9-7% in FY16-18E.

A&P a cash-flow and margin generator . The Group’s two contracts for rental of its A&P space is the main driver for its IPTT division (60-65% of IPTT revenue) which we believe will drive growth for PAT margins going forward as it commands double digit reversions YoY, and the Group can continue to expand promotional spaces within the terminal without incurring major cost.

Forecast earnings of RM27.1-RM31.1 for FY17-18E mainly from A&P revenue growth, additional 25 buses in FY17, while the project facilitation fee remains the icing on the cake. We are expecting bottom line margins to expand in FY17, and estimating 30.2-32.1% PAT margins in FY17-18E from continued growth in the A&P revenue YoY, and on the back of lower effective tax rates (9%,7%,7% in FY16,FY17E,FY18E) derived from tax benefits received. A dividend pay-out policy of up to 25% translates to FY17-18E DPS of 0.59-0.68sen (4.0-4.5% yield based on the IPO price of RM0.15).

DDM-driven Target Price of RM0.22 with total return of 52.6% (7.69% discount rate; 3.19% 5-year risk free rate). Our TP implies FY17E PER of 9.4x. There are no direct comparable but given its quasi-recurring income base, we back tested our valuation method against small cap (<RM1b market cap) MREITs. Based on average small cap MREITs’ FY17E PER of 16.0x and yield of 6.0%, we derive a Fwd. PER of 10.2x for Perak Transit based on its FY17E yield of 4.0% and this imply a TP of RM0.24, which reaffirms our valuation. We opt to maintain our DDM approach and TP of RM0.22 to be more conservative. SUBSCRIBE .

Share Price Performance

KLCI 1,651.71 YTD KLCI chg -2.4% YTD stock price chg n.a.

Major Shareholders Muamalat Venture Sdn Bhd 16.7% CBS Link 16.6% Dato' Sri Cheong Kong Fitt 15.6% IPO Proceeds Business expansion 20.00 Repayment of hire purchase facilities 2.11 Working capital 10.48 Estimated listing expenses 4.16 Total 36.75

Summary of IPO Enlarged Share Cap (m) 1142.9 IPO Price (RM) 0.15 Market Cap Upon Listing (RM m) 171.4

Summary Earnings Table FYE Dec (RM m) 2016E 2017E 2018E Revenue 79.4 89.6 97.0 EBIT 30.1 36.7 41.4 PBT 22.9 29.0 33.5 Net Profit (NP) 20.9 27.1 31.1 Core NP 20.9 27.1 31.1 Core EPS (sen) 1.8 2.4 2.7 Core EPS growth (%) 9% 30% 15% NDPS (sen) 0.46 0.59 0.68 BV/Share (RM) 0.17 0.19 0.21 Core PER (x) 8.22 6.33 5.50 Price/BV (x) 0.9 0.8 0.7 Net Gearing (x) 0.34 0.56 0.50 Net Div. Yield (%) 3.0 4.0 4.5

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 2 of 17

BACKGROUND & BUSINESS

Perak Transit was incorporated in Malaysia on 5th September 2008 as a private limited company and was later converted to a public company on 26th March 2010. The group is principally involved in: (i) the operations and ownership of Terminal AmanJaya integrated public transportation terminal, (ii) provision of public bus services, and (iii) petrol sales business with the operations of several petrol stations in Ipoh, Lahat and Kuala Kangsar, Perak. In 2015, its subsidiary, CKS Bumi signed a Retail Trading Agreement with Petron Malaysia for the operations of a Petron petrol station located at Lubok Merbau, Kuala Kangsar. The operations of the petrol station commenced in August 2015.

Further in 2015, the group received a Letter of Intent from SPAD on the appointment of The Combined Bus as bus network operator for Ipoh under the SBST Programme for a period of eight years commencing on 1st June 2016. The Combined Bus network is a consolidation of public bus services in Perak such as General Omnibus, Ipoh Omnibus, Kinta Omnibus and CKS Bumi which makes up 97.8% of bus services in Ipoh. Prior to the Consortium Arrangement in 2009 and the LOI in 2015 by SPAD, public bus services in Ipoh were operated by these public bus services operators, and Reliance Omnibus, individually. Post the Consortium Arrangement, The Combined Bus network will act as the manager for these consolidated bus operations. The creation of the consortium was to improve the standard of public bus services in Ipoh and surrounding areas to achieve greater economies of scale through more centralised management of bus operations, pooling of bus drives and operational resources, whilst reducing duplication and competition of bus routes.

Terminal AmanJaya has been in operations for almost four years now with operations commencing on 25th Sept 2012. Terminal AmanJaya is a three-storey building complex that has bus platforms (17 departure bays on the ground floor and five arrival bays on the first floor) on which an entrance fee on express busses is imposed. It also has 40 bus holding bays, ticketing counters, retail and office space, promotional spaces, a budget hotel, lobby and basement car park. The gross building area is 208,802sf with 49,291sf of gross leasable space. Construction cost for the building was RM160m, which includes RM25m land cost. As of 2014, Terminal AmanJaya was formally noted as the only gazetted express bus terminal in Ipoh by SPAD, qualifying that all express bus services operating in Ipoh are mandated to pick up and drop off passengers at Terminal AmanJaya only.

Experienced management team. At the helm of the company is Dato’ Sri Cheong Kong Fitt who has over 20 years of experience in public bus terminal operations. In 2006, Dato’ Sri Cheong Kong Fitt with his business partners aimed to combine public bus services in Ipoh Stesen Bas, Jalan Kidd with the aim to upgrade the standards of the service and up to 2009 merged bus operations in Ipoh, General Omnibus, Ipoh Omnibus and Kinta Omnibus, owing to his knowledge of managing terminal and bus operations. Dato’ Sri Cheong Kong Fitt is supported by key management personnel such as Dato’ Cheong Peak Sooi, Executive Director, which will be in charge of the construction of Terminal Kampar due to his long standing experience in the construction sector (over 10 years).

Terminal AmanJaya and Bus Departure Bays during pea k hours

Source: Company, Kenanga Research

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 3 of 17

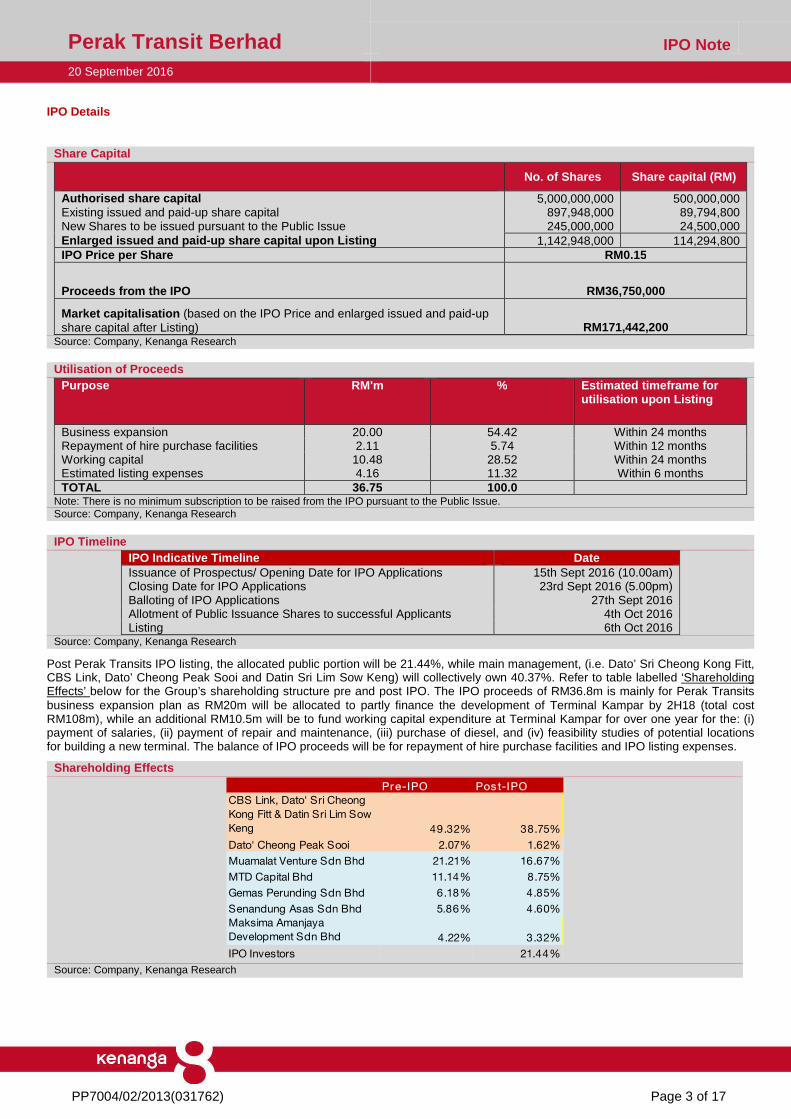

IPO Details

Share Capital

No. of Shares Share capital (RM)

Authorised share capital 5,000,000,000 500,000,000 Existing issued and paid-up share capital 897,948,000 89,794,800 New Shares to be issued pursuant to the Public Issue 245,000,000 24,500,000 Enlarged issued and paid -up share capital upon Listing 1,142,948,000 114,294,800 IPO Price per Share RM0.15

Proceeds from the IPO RM36,750,000

Market capitalisation (based on the IPO Price and enlarged issued and paid-up share capital after Listing) RM171,442,200

Source: Company, Kenanga Research

Utilisation of Proceeds Purpose RM'm % Estimated timeframe for

utilisation upon Listing

Business expansion 20.00 54.42 Within 24 months Repayment of hire purchase facilities 2.11 5.74 Within 12 months Working capital 10.48 28.52 Within 24 months Estimated listing expenses 4.16 11.32 Within 6 months TOTAL 36.75 100.0

Note: There is no minimum subscription to be raised from the IPO pursuant to the Public Issue. Source: Company, Kenanga Research

IPO Timeline

IPO Indicative Timeline Date Issuance of Prospectus/ Opening Date for IPO Applications 15th Sept 2016 (10.00am) Closing Date for IPO Applications 23rd Sept 2016 (5.00pm) Balloting of IPO Applications 27th Sept 2016 Allotment of Public Issuance Shares to successful Applicants 4th Oct 2016 Listing 6th Oct 2016

Source: Company, Kenanga Research

Post Perak Transits IPO listing, the allocated public portion will be 21.44%, while main management, (i.e. Dato’ Sri Cheong Kong Fitt, CBS Link, Dato’ Cheong Peak Sooi and Datin Sri Lim Sow Keng) will collectively own 40.37%. Refer to table labelled ‘Shareholding Effects’ below for the Group’s shareholding structure pre and post IPO. The IPO proceeds of RM36.8m is mainly for Perak Transits business expansion plan as RM20m will be allocated to partly finance the development of Terminal Kampar by 2H18 (total cost RM108m), while an additional RM10.5m will be to fund working capital expenditure at Terminal Kampar for over one year for the: (i) payment of salaries, (ii) payment of repair and maintenance, (iii) purchase of diesel, and (iv) feasibility studies of potential locations for building a new terminal. The balance of IPO proceeds will be for repayment of hire purchase facilities and IPO listing expenses.

Shareholding Effects

Source: Company, Kenanga Research

Pre-IPO Pos t-IPO

CBS Link, Dato' Sri Cheong

Kong Fitt & Datin Sri Lim Sow

Keng 49.32% 38.75%

Dato' Cheong Peak Sooi 2.07% 1.62%

Muamalat Venture Sdn Bhd 21.21% 16.67%

MTD Capital Bhd 11.14% 8.75%

Gemas Perunding Sdn Bhd 6.18% 4.85%

Senandung Asas Sdn Bhd 5.86% 4.60%

Maksima Amanjaya

Development Sdn Bhd 4.22% 3.32%

IPO Investors 21.44%

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 4 of 17

Long lock -in period by major shareholders lends confidence to shareholders . The moratorium applies to the promoters’ entire shareholding for a six-month period from the date of admission into the ACE Market. Besides the promoters, Muamalat Venture, MTD Capital, Gemas Perunding, Senandung Asas and Maksima Amanjaya Development have voluntarily furnished an undertaking letter that they would not sell, transfer, or assign their shareholdings for the first six-month moratorium (refer to table below). Additionally, there is no offer for sale of units on the part of the promoters or major shareholders post the moratorium period which we view positively as it signifies that major shareholders will be committed in the long run.

Moratorium Details

Promoters/Shareholders Held under Moratorium for the first 6 months upon L isting

No. of Shares ('000) %(i)

CBS Link 190,000 16.62 Dato' Sri Cheong Kong Fitt 178,263 15.60 Datin Sri Lim Sow Keng 74,658 6.53 Dato' Cheong Peak Sooi 18,551 1.62 Muamalat Venture (ii) 190,476 16.67 MTD Capital 100,000 8.75 Gemas Perunding 55,481 4.85 Senandung Asas 52,593 4.60 Maksima Amanjaya Development 37,926 3.32

Total 897,948 78.56 Notes:

(i) Based on our enlarged issued and paid-up share capital of 1,142,948,000 Shares after the IPO

(ii) Muamalat Venture is a corporation undertaking private equity activity and registered with the SC pursuant to the SC Guidelines on the Registration of Venture Capital and Private Equity Corporations and Management Corporations. As such, the moratorium imposed on Muamalat Venture on the sale, transfer or assignment of our Shares will be for a period of 6 months from the Listing.

Source: Company, Kenanga Research

INVESTMENT MERIT

Dominating Ipoh’s bus travel due to high barriers o f entry. Perak Transits main terminal, Terminal AmanJaya at Ipoh stands to dominate due to the high barriers of entry as it is the only gazetted bus terminal in Ipoh. In FY14, Terminal AmanJaya was noted by SPAD as the only gazetted bus terminal in Ipoh, implying that all express bus services operating in Ipoh are mandated to pick up and drop off passengers in Terminal AmanJaya. Perak Transit owns 97.8% of market share in Ipoh’s stage bus passenger ridership which is expected to be at least maintained at this level going forward. Given the performance of Terminal AmanJaya which has proven to the state government that they have the capabilities to manage such terminals, we believe Perak Transit will stand in good stead to qualify for other terminals (i.e. Terminal Kampar) and enjoy ease of approvals for bus permits.

Filling the demand gap for reliable transportation. Demand for travel and good connectivity in Malaysia has been a long standing necessity due to the lack of timely and reliable ground public transport service. As such, over the years, the government and SPAD have been ramping up initiatives to address the issue of enhancing urban connectivity and rural and inter-city connectivity as part of the National Land Public Transport Master Plan. As part of its initiatives, SPAD developed myBAS in 2015, whereby the Federal Government will invest RM100m in key cities including Kangar, Seremban, Ipoh, and Kuala Terengganu to improve accessibility where stage buses still remain the backbone of public transportation. Perak Transit is continuously working closely with SPAD to enhance connectivity in Ipoh through bus travel, and is the sole operator of myBAS’s in Ipoh, owning 42 busses for myBAS operations. The myBas model will allow Perak Transit to work on a cost per vehicle-km model with SPAD, while SPAD will manage the cost of operations, including drivers cost. This would allow Perak Transit to be able to scale up quickly to meet consumer demand for busses without worrying about the cost of operations, whilst generating revenue for services rendered.

MyBas

Source: SPAD Website, Kenanga Research

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 5 of 17

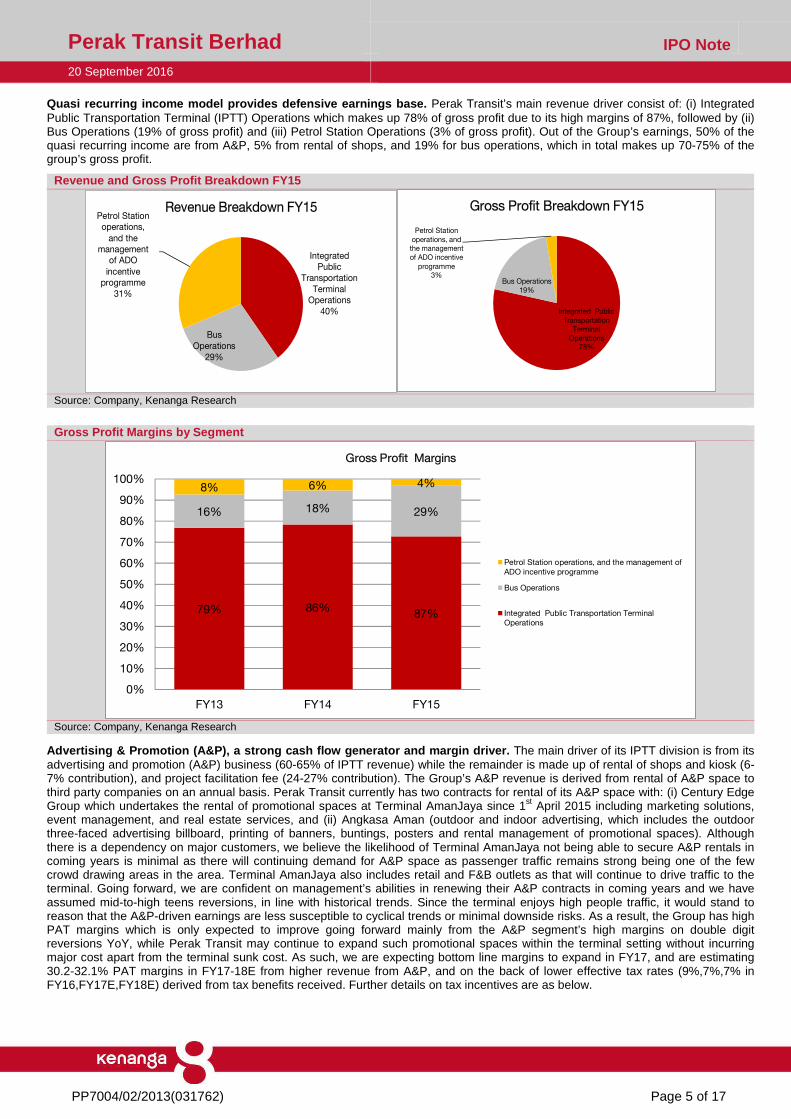

Quasi recurring income model provides defensive earnings base . Perak Transit’s main revenue driver consist of: (i) Integrated Public Transportation Terminal (IPTT) Operations which makes up 78% of gross profit due to its high margins of 87%, followed by (ii) Bus Operations (19% of gross profit) and (iii) Petrol Station Operations (3% of gross profit). Out of the Group’s earnings, 50% of the quasi recurring income are from A&P, 5% from rental of shops, and 19% for bus operations, which in total makes up 70-75% of the group’s gross profit.

Revenue and Gross Profit Breakdown FY15

Source: Company, Kenanga Research

Gross Profit Margins by Segment

Source: Company, Kenanga Research

Advertising & Promotion (A&P), a strong cash flow gen erator and margin driver. The main driver of its IPTT division is from its advertising and promotion (A&P) business (60-65% of IPTT revenue) while the remainder is made up of rental of shops and kiosk (6-7% contribution), and project facilitation fee (24-27% contribution). The Group’s A&P revenue is derived from rental of A&P space to third party companies on an annual basis. Perak Transit currently has two contracts for rental of its A&P space with: (i) Century Edge Group which undertakes the rental of promotional spaces at Terminal AmanJaya since 1st April 2015 including marketing solutions, event management, and real estate services, and (ii) Angkasa Aman (outdoor and indoor advertising, which includes the outdoor three-faced advertising billboard, printing of banners, buntings, posters and rental management of promotional spaces). Although there is a dependency on major customers, we believe the likelihood of Terminal AmanJaya not being able to secure A&P rentals in coming years is minimal as there will continuing demand for A&P space as passenger traffic remains strong being one of the few crowd drawing areas in the area. Terminal AmanJaya also includes retail and F&B outlets as that will continue to drive traffic to the terminal. Going forward, we are confident on management’s abilities in renewing their A&P contracts in coming years and we have assumed mid-to-high teens reversions, in line with historical trends. Since the terminal enjoys high people traffic, it would stand to reason that the A&P-driven earnings are less susceptible to cyclical trends or minimal downside risks. As a result, the Group has high PAT margins which is only expected to improve going forward mainly from the A&P segment’s high margins on double digit reversions YoY, while Perak Transit may continue to expand such promotional spaces within the terminal setting without incurring major cost apart from the terminal sunk cost. As such, we are expecting bottom line margins to expand in FY17, and are estimating 30.2-32.1% PAT margins in FY17-18E from higher revenue from A&P, and on the back of lower effective tax rates (9%,7%,7% in FY16,FY17E,FY18E) derived from tax benefits received. Further details on tax incentives are as below.

Integrated

Public

Transportation

Terminal

Operations

40%

Bus

Operations

29%

Petrol Station

operations,

and the

management

of ADO

incentive

programme

31%

Revenue Breakdown FY15

Integrated Public

Transportation

Terminal

Operations

78%

Bus Operations

19%

Petrol Station

operations, and the management

of ADO incentive

programme 3%

Gross Profit Breakdown FY15

79% 86%87%

16% 18% 29%

8% 6% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15

Gross Profit Margins

Petrol Station operations, and the management of

ADO incentive programme

Bus Operations

Integrated Public Transportation Terminal

Operations

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 6 of 17

Gross Profit margins vs. PAT margins

Source: Company, Kenanga Research

Control of market share for Public Bus Service. The bus operations make up 19% of gross profit which is mainly derived from provision of public stage bus and express bus services, as well as rental of spaces on buses for advertisements. We expect contributions from this segment to be stable going forward as Perak Transit owns 97.8% of market share in Ipoh’s stage bus passenger ridership operating 146 buses currently, of which 119 are public stage buses and 27 are express buses. We expect the demand for stage buses within Ipoh to be resilient as the state and SPAD will continue to increase routes and buses in tandem with demand, with Perak Transit being the main beneficiary due to the Group’s strong track record with the state government. The routes are approved by SPAD which contain fare stage with separate fare, timetable and schedule of fares for each stage. Additionally the minimum number of trips and frequency per day will be determined by SPAD. This is part of the Consortium arrangement under The Combined Bus whereby it pays for all the expenses for the operations and maintenance of the buses, but is entitled to all the revenue and profits from the business. As for express buses, Perak Transit operates five express bus routes while the fares are set out by SPAD.

- Lastly, the Group’s petrol station operations consist of four petrol stations based on a ‘dealer-owned dealer-operated model’ whereby Perak Transit erects a service station and convenience store to supply motor fuels, lubricating oils and other petroleum products at the station. However, this segment does not contribute significantly to earnings due to is low margins, resulting in <5% contribution to gross profits.

A&P at Terminal AmanJaya

Source: Company, Kenanga Research

0%

10%

20%

30%

40%

50%

60%

Gross Profit vs. PAT margins

Gross

Profit

Margins

PAT

Margins

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 7 of 17

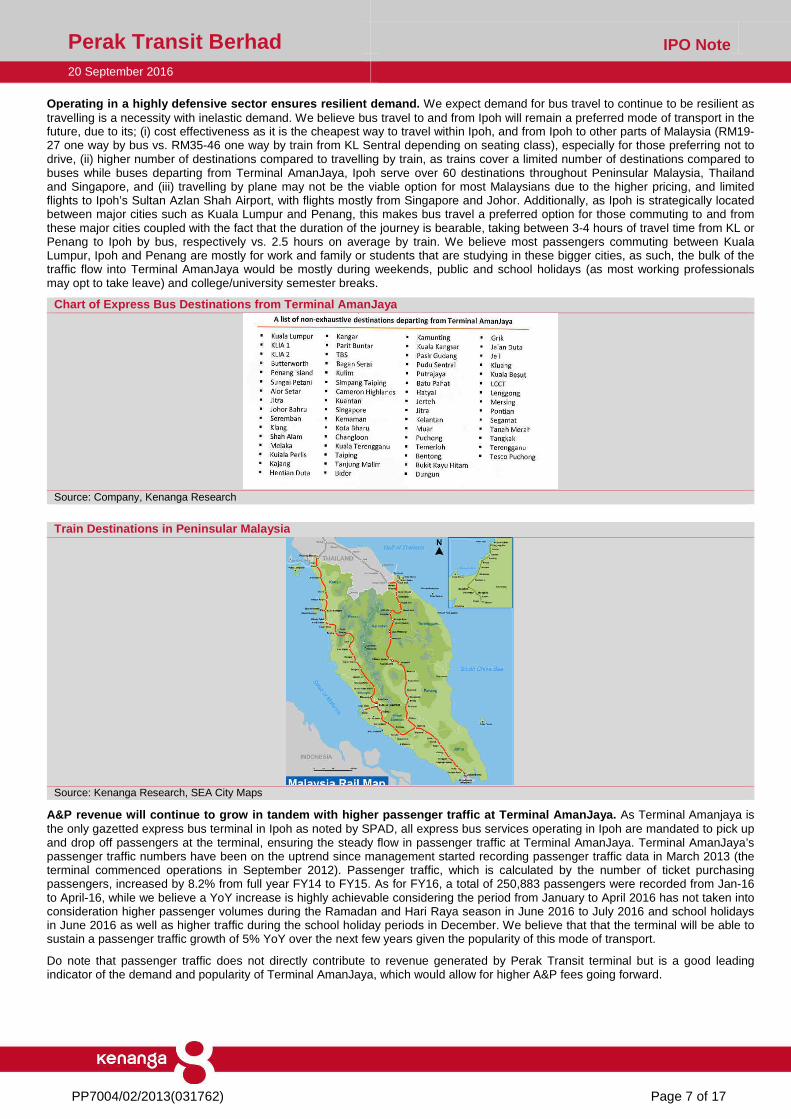

Operating in a highly defensive sector ensures resi lient demand. We expect demand for bus travel to continue to be resilient as travelling is a necessity with inelastic demand. We believe bus travel to and from Ipoh will remain a preferred mode of transport in the future, due to its; (i) cost effectiveness as it is the cheapest way to travel within Ipoh, and from Ipoh to other parts of Malaysia (RM19-27 one way by bus vs. RM35-46 one way by train from KL Sentral depending on seating class), especially for those preferring not to drive, (ii) higher number of destinations compared to travelling by train, as trains cover a limited number of destinations compared to buses while buses departing from Terminal AmanJaya, Ipoh serve over 60 destinations throughout Peninsular Malaysia, Thailand and Singapore, and (iii) travelling by plane may not be the viable option for most Malaysians due to the higher pricing, and limited flights to Ipoh’s Sultan Azlan Shah Airport, with flights mostly from Singapore and Johor. Additionally, as Ipoh is strategically located between major cities such as Kuala Lumpur and Penang, this makes bus travel a preferred option for those commuting to and from these major cities coupled with the fact that the duration of the journey is bearable, taking between 3-4 hours of travel time from KL or Penang to Ipoh by bus, respectively vs. 2.5 hours on average by train. We believe most passengers commuting between Kuala Lumpur, Ipoh and Penang are mostly for work and family or students that are studying in these bigger cities, as such, the bulk of the traffic flow into Terminal AmanJaya would be mostly during weekends, public and school holidays (as most working professionals may opt to take leave) and college/university semester breaks.

Chart of Express Bus Destinations from Terminal Aman Jaya

Source: Company, Kenanga Research

Train Destinations in Peninsular Malaysia

Source: Kenanga Research, SEA City Maps

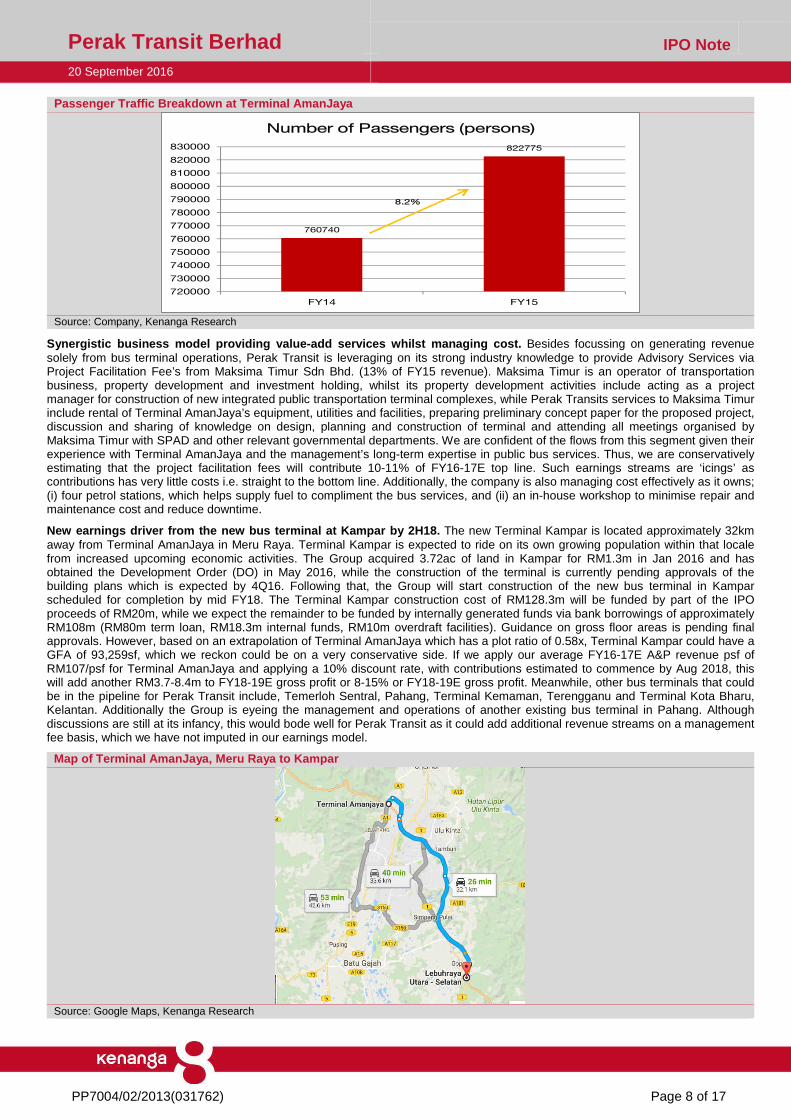

A&P revenue will continue to grow in tandem with hi gher passenger traffic at Terminal AmanJaya. As Terminal Amanjaya is the only gazetted express bus terminal in Ipoh as noted by SPAD, all express bus services operating in Ipoh are mandated to pick up and drop off passengers at the terminal, ensuring the steady flow in passenger traffic at Terminal AmanJaya. Terminal AmanJaya’s passenger traffic numbers have been on the uptrend since management started recording passenger traffic data in March 2013 (the terminal commenced operations in September 2012). Passenger traffic, which is calculated by the number of ticket purchasing passengers, increased by 8.2% from full year FY14 to FY15. As for FY16, a total of 250,883 passengers were recorded from Jan-16 to April-16, while we believe a YoY increase is highly achievable considering the period from January to April 2016 has not taken into consideration higher passenger volumes during the Ramadan and Hari Raya season in June 2016 to July 2016 and school holidays in June 2016 as well as higher traffic during the school holiday periods in December. We believe that that the terminal will be able to sustain a passenger traffic growth of 5% YoY over the next few years given the popularity of this mode of transport.

Do note that passenger traffic does not directly contribute to revenue generated by Perak Transit terminal but is a good leading indicator of the demand and popularity of Terminal AmanJaya, which would allow for higher A&P fees going forward.

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 8 of 17

Passenger Traffic Breakdown at Terminal AmanJaya

Source: Company, Kenanga Research

Synergistic business model providing value-add serv ices whilst managing cost. Besides focussing on generating revenue solely from bus terminal operations, Perak Transit is leveraging on its strong industry knowledge to provide Advisory Services via Project Facilitation Fee’s from Maksima Timur Sdn Bhd. (13% of FY15 revenue). Maksima Timur is an operator of transportation business, property development and investment holding, whilst its property development activities include acting as a project manager for construction of new integrated public transportation terminal complexes, while Perak Transits services to Maksima Timur include rental of Terminal AmanJaya’s equipment, utilities and facilities, preparing preliminary concept paper for the proposed project, discussion and sharing of knowledge on design, planning and construction of terminal and attending all meetings organised by Maksima Timur with SPAD and other relevant governmental departments. We are confident of the flows from this segment given their experience with Terminal AmanJaya and the management’s long-term expertise in public bus services. Thus, we are conservatively estimating that the project facilitation fees will contribute 10-11% of FY16-17E top line. Such earnings streams are ‘icings’ as contributions has very little costs i.e. straight to the bottom line. Additionally, the company is also managing cost effectively as it owns; (i) four petrol stations, which helps supply fuel to compliment the bus services, and (ii) an in-house workshop to minimise repair and maintenance cost and reduce downtime.

New earnings driver from the new bus terminal at Ka mpar by 2H18. The new Terminal Kampar is located approximately 32km away from Terminal AmanJaya in Meru Raya. Terminal Kampar is expected to ride on its own growing population within that locale from increased upcoming economic activities. The Group acquired 3.72ac of land in Kampar for RM1.3m in Jan 2016 and has obtained the Development Order (DO) in May 2016, while the construction of the terminal is currently pending approvals of the building plans which is expected by 4Q16. Following that, the Group will start construction of the new bus terminal in Kampar scheduled for completion by mid FY18. The Terminal Kampar construction cost of RM128.3m will be funded by part of the IPO proceeds of RM20m, while we expect the remainder to be funded by internally generated funds via bank borrowings of approximately RM108m (RM80m term loan, RM18.3m internal funds, RM10m overdraft facilities). Guidance on gross floor areas is pending final approvals. However, based on an extrapolation of Terminal AmanJaya which has a plot ratio of 0.58x, Terminal Kampar could have a GFA of 93,259sf, which we reckon could be on a very conservative side. If we apply our average FY16-17E A&P revenue psf of RM107/psf for Terminal AmanJaya and applying a 10% discount rate, with contributions estimated to commence by Aug 2018, this will add another RM3.7-8.4m to FY18-19E gross profit or 8-15% or FY18-19E gross profit. Meanwhile, other bus terminals that could be in the pipeline for Perak Transit include, Temerloh Sentral, Pahang, Terminal Kemaman, Terengganu and Terminal Kota Bharu, Kelantan. Additionally the Group is eyeing the management and operations of another existing bus terminal in Pahang. Although discussions are still at its infancy, this would bode well for Perak Transit as it could add additional revenue streams on a management fee basis, which we have not imputed in our earnings model.

Map of Terminal AmanJaya, Meru Raya to Kampar

Source: Google Maps, Kenanga Research

760740

822775

720000

730000

740000

750000

760000

770000

780000

790000

800000

810000

820000

830000

FY14 FY15

Number of Passengers (persons)

8.2%

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 9 of 17

Details of the Business Expansion plan a.k.a Termina l Kampar Descr iption Amount (RM'm) A. Construction cost (1) Site clearance, site improvement, earth works, piling works and main building works - from lower ground floor to the 8th floor (comprising building platforms, bus loading/ unloading bays, hotel facilities such as lobby and events hall, cinema and entertainment outlets, car parks, sports and fitness club and dental specialist centre)

89.64

(2) External works(comprising road and drainage, external water reticulation, primary soil drainage, mechanical and electrical infrastructure and landscaping works), design and construction contingency expenses and preliminaries (i.e. construction site overheads)

13.96

B. Other costs (1) Professional fees (e.g. architects, civil and structural engineers, mechanical and electrical engineers, landscape architects and town planning) and project management fees

19.10

(2) Statutory contribution and planning fees payable to authorities (i.e. Tenaga Nasional Berhad, Indah Water Konsortium, and Lembaga Air Perak)

1.63

(3) Marketing and promotions (to market and promote the Terminal Kampar to potential tenants and to the public)

4.00

Total cost 128.33

Source: Company, Kenanga Research

IPO Proceeds to be used for the business expansion pl an a.k.a Terminal Kampar Description RM'm Professional fees (1) 11.50 Construction works (2) 8.50 Total 20.00 (1) Part payment for total estimated professional fees of RM19.1m, which includes Architects, Civil & Structural Engineers, Mechanical & Electrical Engineers and Project Management fees. This includes: (i) First progressive payment of approximately RM1.9m payable to appoint the professionals and initiate the construction project; (ii) Fees payable to architects and relevant professionals for services rendered to prepare and submit the architectural plans and the relevant documents to the respective authorities for approval; and (iii) Fees to respective professionals to perform periodical supervision and inspection work, attending site meetings and notification to the relevant authorities on the progress of the work. (2) Construction works consists of: (i) The cost of piling works for the whole integrated public transportation terminal which is estimated to be RM5.2m; and (ii) The estimated RM3.3m, being part payment of the total construction cost of the main building works of approximately RM89.64m.

Source: Company, Kenanga Research

Expect sustainable demand from Kampar, leveraging on its growing education hub. Kampar town has been identified as a suitable location for the next terminal due to its ever growing population driven by increased economic activities from: (i) higher learning institutions such as TAR College, Universiti Tunku Abdul Rahman (UTAR), Westlake International School (WIS), while upcoming institutions include UCSI University and Metropolitan College, (ii) new townships and development plans (ex: Taman Bandar Baru), (iii) various hypermarkets to cater to the increasing demand (i.e. Tesco, Giant, Econsave), and (iv) its strategic location close to the North-South Expressway.

Tax breaks allow for low effective tax rates. Due to the nature of business which requires large sums of capex invested for projects that serve national interest, Perak Transit is a beneficiary of Approved Service Project Status (ASPS) tax whereby Perak Transit is able to claim up to 60% of capex invested from FY12-17 (5-year period). Historically, the company has received a total tax incentive of RM49.4m for FY13-15 and has a remaining RM88m to go which can be progressively utilised over a longer period. The Group is going to apply for the ASPS tax incentive for the new Terminal Kampar and we are confident they will be successful as it is a national interest project; which we have yet to impute. For now, we expect the effective tax rate in FY16,17-18E to be 9%,7%-7%.

Benefiting from Government incentives. Besides tax savings, the company also receives government grants, and during the construction of Terminal AmanJaya, it received a one-time government grant of RM9.98m (which is amortised over a 50 year period) from the Public Private Partnership Unit of the Prime Ministers Department in 2012. Perak Transit also receives funding from Interim Stage Bus Support Fund (ISBSF) is financial assistance provided by SPAD to improve the quality of bus services that has totalled RM9.54m from FY13-16 which translates to c.RM2m revenue p.a. which we have accounted for in our estimates. Other initiatives by SPAD include Stage Bus Service Transformation (SBST) programme whereby The Combined Bus being the network operator will be paid cost per vehicle-km for 16 stage bus routes in Ipoh, to expand bus route coverage by shifting away from the fare-box revenue model, to the gross cost service delivery model. This is expected to translate to an additional RM1.9-3.8m in total in FY16-17E; which we have accounted for in our estimates. Additionally, Perak Transit receives sales tax exemption of CKD bus and air conditioning equipment of RM2.44m from MoF for the purchase of CKD buses and air conditioning equipment during FY13-15 and GST exemption of RM0.57m from MoF for the purchase of CKD buses and air conditioning equipment during FY15-FY16, which provides cost savings on cost purchases, depreciation and operating expenses of bus services.

Capex assumptions of RM38-80m in FY16-17E . All in, we are expecting the Group to allocate RM140m for CAPEX over FY16-18E, which are mainly for the development of Terminal Kampar (total cost RM128m) of which RM20m will be raised via the IPO, including an additional RM12m for the acquisition of 25 new express busses which we expect by FY17. As such, we are expecting the group to allocate capex of RM38-80m in FY16-17E, while the remainder of RM22m in FY18E which will be funded via borrowings and internally generated funds.

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 10 of 17

Expect FY16, 17-18E net gearing of 0.3 4, 0.56-0.50x…The Group’s net gearing is expected to rise over the next one to two years due to progressive draw down on its borrowing facilities for the construction of the new Terminal Kampar which is set to be completed by mid-2018. We believe its net gearing will normalise closer to 0.30x by FY21 post construction of Terminal Kampar assuming no further major capex plans. However, it appears that the Group has expansion plans for Terminal AmanJaya, and possible development of other terminals post Terminal Kampar, which we have yet to build into our estimates.

…which we are comfortable given a healthy interest coverage ratio of 4.2, 4.8-5.2x in FY16, 17-18E. Despite high capital commitments for the construction of its terminals, Perak Transit has maintained extremely healthy interest coverage ratios of >3.0x since FY14 while we are expecting FY16, 17-18E interest coverage ratio of 4.2, 4.8-5.2x which is more than comfortable given their strong cash-flow income streams. Note that the group has very healthy receivables day coverage of 21-58 days over FY14-16E.

Interest Coverage Ratio

Source: Kenanga Research

Listing to increase credibility and funding options . The public listing is a positive as it would increase the Group’s credibility, especially in securing new deals from other government agencies and Project Facilitation Fee’s deals. Listed companies are more transparent when it comes to information disclosure and would have been vetted through by the Securities Commission during the listing process. Secondly, public listing will also mean more funding options in the future which is handy given that terminal developments requires high capex. As Perak Transits business model of Terminal management is capital intensive, especially during the construction phase of new terminal, the Group will require added avenues for funding such as rights issuances, bond issuances, etc. At this juncture, Perak Transit is set on expanding Terminal Kampar and buying new buses, while longer term and not so concrete plans include adoption of new A&P platforms to increase A&P space at Terminal AmanJaya and further expansions of Terminal AmanJaya’s built-up area.

OUTLOOK

Terminal AmanJaya a commercial and lifestyle hub. The Group plans to evolve Terminal AmanJaya into a commercial and lifestyle hub by increasing retail operations on 136,721sf of undeveloped land at Terminal AmanJaya, currently. The expanded section of the terminal will increase gross building area (GBA) by 166,443sf (+80% of the existing GBA), while increments of GLA is yet to be finalised. However, this certainly bodes well in terms of additional A&P space revenue which is the Group’s main earnings driver, as well as increments to rental of GLA. Plans for the extension of Terminal AmanJaya is likely by FY19, post the completion of Terminal Kampar.

Expecting additional revenue streams from the rental of A&P space after adopting new A&P platforms. Perak Transit is continuously expanding efforts to increase A&P space, and plans to adopt new platforms for A&P such as digital platforms with digital signage in infrastructure, as well as media capabilities that can leverage on consumers mobile, social and online technologies. This would directly increase A&P space, accreting directly to the Groups revenue and is part of the longer term initiatives.

RISK

Non approval of business licences. The Group will not be able to carry out its core operations to serve as a terminal as its Terminal License for its terminal operations by SPAD has yet to be granted considering that SPAD has yet to finalise its internal regulatory framework for the issuance of any bus terminal license in Peninsular Malaysia. SPAD has confirmed that pending the finalisation of the internal framework, there will not be any penalties for terminals operating without such a license. We believe the likelihood of Terminal AmanJaya obtaining a terminal license is just about “in the bag” considering these factors; (i) Terminal AmanJaya has already commenced operations with relevant business licenses and obtained a certificate of fitness (CF) for the premises, (ii) SPAD and the state government has noted the commencement of terminal operations on Sept 2012, (iii) SPAD’s circular stated that all express busses entering and exiting Ipoh must drop off and pick up passengers at Terminal AmanJaya, unless special permission is given, and (iv) the terminal has been gazetted by the Mayor of Ipoh City as the terminal for public service vehicles (busses and taxis) from 31st July 2012. In June 2016, SPAD commenced the registration process for the licencing of all terminals, and on 1 July 2016, The Combined Bus submitted its formal application for the Terminal Licence.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

FY13 FY14A FY15A FY16E FY17E FY18E

Interest coverage ratioX

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 11 of 17

Non-renewal of bus route permits. Not being able to renew bus route permits or revocation may pose an impact on earnings. The management will do their best to achieve timely approvals of such permits and have to date not encountered difficulty in renewing vehicle permits, bus route permits and business licences in the past. Although there is a possibility that there may be delays, modifications or impositions of further conditions for the renewal of such licences, we do not expect it to have a significant adverse impact on the Group’s earnings due to managements competencies in ensuring these conditions are met, whilst renewal or expiry of vehicle permits are specific to the affected license only, and thus shall not affect the validity of other vehicle permits.

Dependency on major customers and other risks. We believe the likelihood of Terminal AmanJaya not being able to secure A&P rental in coming years is minimal due to sustained demand for A&P space as passenger traffic remains strong. Terminal AmanJaya also includes retail and F&B outlets that will continue to drive traffic to the terminal. In terms of risk of tenancy renewals, the bulk of the Group’s tenancies are mainly for 2-year periods meaning Terminal AmanJaya will see a fairly significant rate of expirations each year, with 27%, 47% and 25% expiring in FY16,17-18. That said, rental revenue from tenants make up <5% of top line which is not overly significant. Another risk is the volatility in earnings from Project Facilitation Fees. The Group’s project facilitation fees are usually on an ad-hoc basis upon client request and therefore, are susceptible to volatility YoY depending on market conditions.

FINANCIALS

Expecting earnings of RM27.1-RM31.1m for FY17-18E mainly from A&P revenue growth, as well as public bus services from the additional 25 buses set to contribute to revenue by FY17, while the icing on the cake would be the project facilitation fee which we estimate at 11.3-9.5% of FY17-18E top line. Additionally, we are expecting bottom line margins to expand in FY17 and are estimating 30.2-32.1% PAT margins in FY17-18E from continued growth in the A&P revenue YoY, and on the back of lower effective tax rates (9%,7-7% in FY16,17-18E) derived from tax benefits received.

A dividend pay-out policy of up to 25%. Management will implement a dividend policy to pay out up to 25% of PATAMI, which we view positively to provide confidence to shareholders. Of course, the policy is subject to profit levels, cash and indebtedness. We believe a 25% pay-out is highly achievable as the bulk of its profits is made up of the strong cash-flow nature from A&P revenue and believe pay-out could be higher post its major CAPEX obligations like the new Terminal Kampar. Based on the pay-out, this translates to FY17-18E DPS of 0.59-0.68 sen (4.0-4.5% yield based on the IPO price of RM0.15).

VALUATIONS

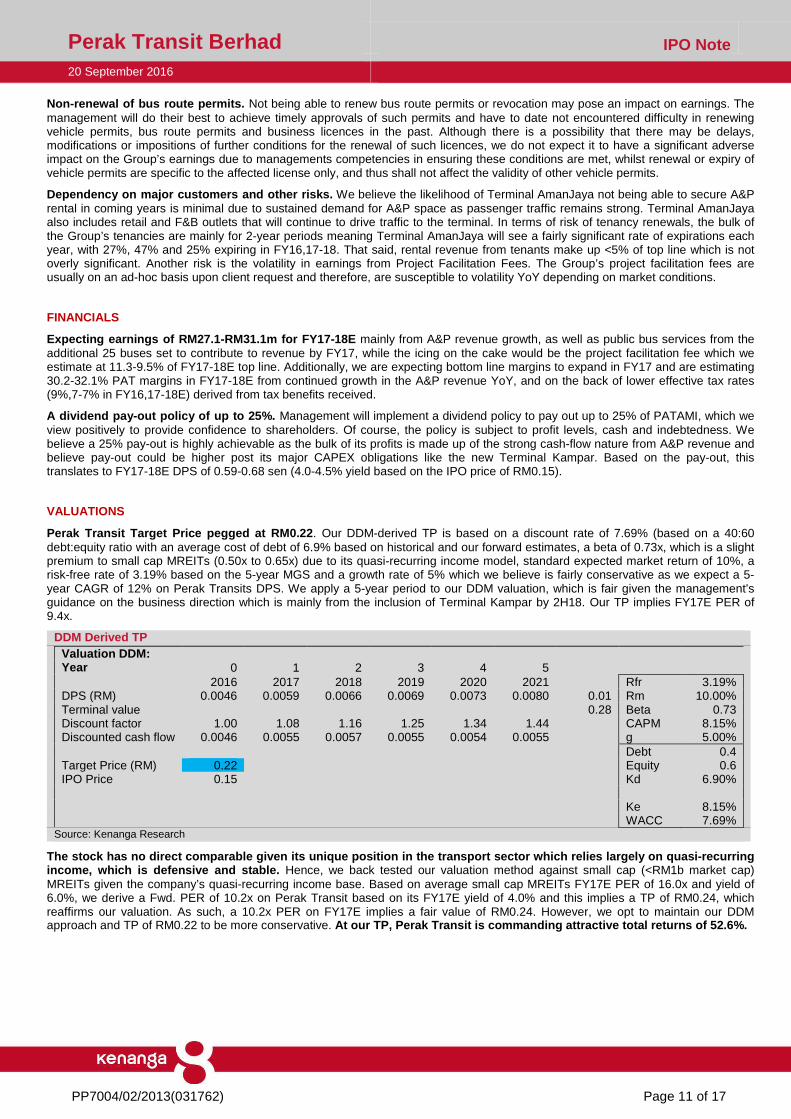

Perak Transit Target Price pegged at RM0.22 . Our DDM-derived TP is based on a discount rate of 7.69% (based on a 40:60 debt:equity ratio with an average cost of debt of 6.9% based on historical and our forward estimates, a beta of 0.73x, which is a slight premium to small cap MREITs (0.50x to 0.65x) due to its quasi-recurring income model, standard expected market return of 10%, a risk-free rate of 3.19% based on the 5-year MGS and a growth rate of 5% which we believe is fairly conservative as we expect a 5-year CAGR of 12% on Perak Transits DPS. We apply a 5-year period to our DDM valuation, which is fair given the management’s guidance on the business direction which is mainly from the inclusion of Terminal Kampar by 2H18. Our TP implies FY17E PER of 9.4x.

DDM Derived TP Valuation DDM: Year 0 1 2 3 4 5 2016 2017 2018 2019 2020 2021 Rfr 3.19% DPS (RM) 0.0046 0.0059 0.0066 0.0069 0.0073 0.0080 0.01 Rm 10.00% Terminal value 0.28 Beta 0.73 Discount factor 1.00 1.08 1.16 1.25 1.34 1.44 CAPM 8.15% Discounted cash flow 0.0046 0.0055 0.0057 0.0055 0.0054 0.0055 g 5.00% Debt 0.4 Target Price (RM) 0.22 Equity 0.6 IPO Price 0.15 Kd 6.90%

Ke 8.15% WACC 7.69%

Source: Kenanga Research

The stock has no direct comparable given its unique position in the transport sector which relies larg ely on quasi-recurring income, which is defensive and stable. Hence, we back tested our valuation method against small cap (<RM1b market cap) MREITs given the company’s quasi-recurring income base. Based on average small cap MREITs FY17E PER of 16.0x and yield of 6.0%, we derive a Fwd. PER of 10.2x on Perak Transit based on its FY17E yield of 4.0% and this implies a TP of RM0.24, which reaffirms our valuation. As such, a 10.2x PER on FY17E implies a fair value of RM0.24. However, we opt to maintain our DDM approach and TP of RM0.22 to be more conservative. At our TP, Perak Transit is commanding attractive tot al returns of 52.6%.

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 12 of 17

APPENDIX

Shareholding Effects Promoters and

substantial shareholders Nationality /

Place of incorporation

Before IPO After IPO (1)

Direct Indirect Direct Indirect

No. of Shares ('000)

%(2) No. of Shares ('000)

%(2) No. of Shares ('000)

%(5) No. of Shares ('000)

%(5)

CBS Link Malaysia 190,000 21.16 - - 190,000 16.62 - -

Dato' Sri Cheong Kong Fitt Malaysian 178,263 19.85 264,658 (3) 29.47 (3) 178,263 15.60 264,658 (3) 23.16 (3)

Dato' Cheong Peak Sooi Malaysian 18,551 2.07 - - 18,551 1.62 - -

Datin Sri Lim Sow Keng Malaysian 74,658 8.31 368,263 (4) 41.01 (4) 74,658 6.53 368,263 (4) 32.22 (4)

Gemas Perunding Malaysia 55,481 6.18 - - 55,481 4.85 - -

Muamalat Venture Malaysia 190,476 21.21 - - 190,476 16.67 - -

MTD Capital Malaysia 100,000 11.14 - - 100,000 8.75 - -

Senandung Asas Malaysia 52,593 5.86 - - 52,593 4.60 - -

Notes: (1) Assuming after the Proposed Public Issue. (2) Computed based on our enlarged issued and paid-up share capital of 897,948,000 Shares after the New Share Issuance as stated in Section 1.6.1 herein and before our IPO. (3) Deemed interested pursuant to his interest held in CBS Link via CKS Maju pursuant to Section 6A of the Act and the direct interest of his spouse, Datin Sri Lim Sow Keng. (4) Deemed interested pursuant to her interest held in CBS Link via CKS Maju pursuant to Section 6A of the Act and the direct interest of her spouse, Dato' Sri Cheong Kong Fitt. (5) Computed based on our enlarged issued and paid up share capital of 1,142,948,000 Shares after our IPO.

Source: Company, Kenanga Research

Perak Transit subsidiaries and their respective prin cipal activities Company name Date/ Place of incorporation Issued and

paid-up share

capital (RM)

Effective equity

interest (%)

Year commenced operations

Principal activities

CKS Bumi 2 July 2008 / Malaysia 500,000 69.99 2008 Bus operator, operator of petrol station and providing management services

CKS Labur 5 March 2008 / Malaysia 250,000 100.00 2008 Operator of petrol station

IpohLink 23 July 2008 / Malaysia 300,000 100.00 2008 Providing management services for bus operations

Star Kensington 7 September 2006 / Malaysia 350,000 95.71 2006 Operator of petrol station

Syarikat Sumber Manusia

11 September 2009 / Malaysia

100,000

100.00

2009 Providing services of human resource management

The Combined Bus

2 August 2006 / Malaysia

55,600,003 99.89 2006 Operators of bus terminal, petrol station and public transportation

Terminal Urus 25 April 2012 / Malaysia 100,000 100.00 2012 Bus Terminal Management

Source: Company, Kenanga Research

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 13 of 17

Key Milestones and Achievement Year Key milestones and achievement 2006 • Incorporation of The Combined Bus 2008 • Incorporation of Perak Transit 2009 • The Combined Bus initiated the Consortium Arrangement with General Omnibus, Ipoh Omnibus and Kinta Omnibus, and

consolidated the bus services operations of General Omnibus, Ipoh Omnibus and Kinta Omnibus under The Combined Bus. • The Combined Bus submitted an application to the Ipoh City Council to seek for planning approvals to construct an express bus

terminal in Meru Raya, Ipoh. 2010 • The Combined Bus received approval for the abovementioned application and commenced construction of integrated public

transportation terminal. • Consortium Arrangement was formalized between The Combined Bus, General Omnibus, Ipoh Omnibus and Kinta Omnibus. • Completed the acquisitions of IpohLink and Syarikat Sumber Manusia to provide management services for public bus services

operations and to provide human resource management, respectively. • Acquired The Combined Bus.

2011 • The Consortium Agreement was noted by LPKP. • Signed a Supply and License Agreement with Boustead Petroleum Marketing Sdn Bhd to operate a BHP petrol station at Terminal

AmanJaya 2012 • Terminal AmanJaya was gazetted by the Mayor of Ipoh City as the station for public service vehicles (bus and taxi services) with

effect from 31 July 2012. • Acquired CKS Bumi which held 50 stage bus permits and 50 express bus permits and CKS Bumi was noted by SPAD to join as a

member of the Consortium Arrangement. • Qualified for the SPAD’s ISBSF, a fund established by the Government of Malaysia to improve the quality of bus services. • Applied and received approval for Approved Service Project Status for The Combined Bus. • Received an approval-in-principle from Public Private Partnership Unit of the Prime Minister Department, a Government grant for

infrastructure cost of the integrated public transportation terminal. • Completed the acquisitions of CKS Bumi, CKS Labur and Star Kensington, wherein the services is expanded to include petrol

stations operations. • Completed the construction of Terminal AmanJaya and commenced operations of Terminal AmanJaya, including the operations of

BHP petrol station located within the terminal compound. 2014 • Terminal AmanJaya’s status as the only gazetted express bus terminal in Ipoh, Perak is recognized by SPAD in the SPAD Circular.

The release of this SPAD Circular is to centralize express bus operations in Terminal AmanJaya, and provide improved public transportation services to passengers in the form of comfort, safety, access to improve travel information and notification, as well as enhanced public transportation network.

• Completed the acquisition of Terminal Urus to provide bus terminal management services. 2015 • Signed a Retail Trading Agreement with Petron Malaysia for the operations of a Petron petrol station located at Lubok Merbau,

Kuala Kangsar and commenced operations in August 2015. • Received Letter of Intent from SPAD on the appointment of The Combined Bus as network operator for Ipoh under the SBST

Programme for a period of 8 years. 2016 • The Combined Bus entered into a conditional sale and purchase agreement for the purchase of 2 parcels of land measuring

approximately 3.72 acres which are situated in Mukim of Kampar, Daerah Kampar, Perak. • The Combined Bus then entered into a conditional agreement with SPAD pursuant to the appointment as a bus network operator

for Ipoh under the SBST Programme, following the receipt of the Letter of Intent from SPAD in 2015. The Group has commenced the bus operations of six (6) routes under SBST Programme since 1 June 2016.

Source: Company

Profile of Key Management Personnel Name Position Background

Dato' Sri Cheong Kong Fitt Managing Director

• Diploma in Business from the School of Marketing, Ipoh in 1986

• Currently persuing Masters of Art in International Business in York St John University, England

• 20 years of working experience in public bus terminal operations

• Began career as supervisor in Choong Sam Tin Mine (1980)

• Joined Swee Keong Construction Pte Ltd in 1985 as a supervisor tasked with logistics planning

• Joined The Combined Bus Services (Partnership), operator of Stesen Bas Jalan Kidd as supervisor in 1992 where he was responsible for managing the public bus terminal operations.

• In 2006 to 2009, was instrumental in leading the bus services operations of General Omnibus, Ipoh Omnibus, and Kinta Omnibus

• Founded Perak Transit in 2008, and commeced operations at Terminal AmanJaya in 2012

Dato' Cheong Peak Sooi Executive Director

• Holds Certificate in Business Management from MDIS Business School, Singapore in 1988

• Commenced career as site manager for G&C Civil Engineering Pte Ltd in Singapore, responsible for overseeing the Company's daily construction work up to 2000.

• In 2001, took position as filed service representative in a multinational company in Singapore (Amerton Pte Ltd) liasing with clients, preparing proposals for clients, supervising and monitoring the installation of piping, quality checks and handover.

• Joined Star Kensington in 2008 as a director responsible for petrol station operations, and subsequently resigned in 2011.

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 14 of 17

• Appointed as director of The Combined Bus in 2011 responsible for monitring the construction and day-to-day operations of Terminal AmanJaya.

Loh Kwang Yean Chief Financial Officer

• Graduated with a Bachelor of Accounting with honours from University Utara Malaysia in 1999.

• Became a member of the Malaysian Institute of Accountants. • Began his career as an Audit Assistant with Deloitte KassimChan in 1999. • In 2000, was promoted to Audit Senior II and Audit Senior I in 2001.

• In 2002, joined P.I.E. Industrial Berhad as a Project Officer in the Corporate Finance department.

• In 2004, joined Dufu Technology Corp. Berhad as a Group Accountant.

• In 2008, was promoted to Finance Manager and also headed the due diligence team in a cross-border acquisition of a manufacturing plant in China which has a holding company in Hong Kong, Futron Techonology Limited.

• Founded Northern Bridge Advisory Sdn Bhd, an independent advisory company. • Joined LNG Resources Berhad as an Executive Director. • Joined Perak Transit as Chief Financial Officer. • Resigned as Director in Northern Bridge Advisory Sdn Bhd on 1st October 2015.

Jennifer Chin Yi Teng

Administration and Finance Manager

• Graduated with a Bachelor of Science (Hons) in Applied Accounting from Oxford Brookes University, United Kingdom, in 2011.

• Currently pursuing professional qualification with the Association of Chartered Certified Accountants.

• Began her career as an Account Executive with Kin Kun Group Sdn Bhd. • Joined Perak Transit as an Account Executive • In 2014, was promoted to Administration and Finance Manager.

Nur Liana Binti Ahmad Tarmizi Terminal Manager

• Obtained Bachelor of Civil Engineering with honours from University Tenaga Nasional, Malaysia in 2012.

• Obtained a Master Degree in Management from University of Bath, United Kingdom in 2014. • Began her career as a manager with Impian Atah Enterprise in 2012. • Joined Perak Transit as terminal manager in March 2015.

Chen Lee Keen Bus Operations Administrator

• Graduated with a Sijil Pelajaran Malaysia from SMJK Ave Maria Convent, Ipoh, Perak in 1982.

• Has around 24 years working experiences in the public transportation industry.

• Started her career in 1984 with Homegym Pte.Ltd.

• In 1986, started working as a shipping executive with CDF Chimie Pte.Ltd, a Singapore company based in Petaling Jaya.

• In 1991, joined Ipoh Omnibus as a chief clerk and was in-charge of daily bus operations.

• In 1998, was promoted as personal assistant of the Director.

Source: Company

Profile of Directors Name Position Background Tan Sri Dato' Chang Ko Youn

Independent Non-Executive Chairman

• Graduated with a Bachelor of Laws (Honours) from the University of Hull, England in 1981 • In 1982, was called to the English Bar as a Barrister-At-Law of Lincoln's Inn, London and

Malayan Bar in 1983. • Began his career as a lawyer in Ipoh in 1983 until 1995 where he was attached to Chang Ko

Youn & Co. • In 1987, was appointed as Councillor of the Kuala Kangsar District Council until 1995. • Assumed the political position of Perak Gerakan Youth Chairman until 1996, and current

position of Committee Member of Perak State. • In 1987 was elected as the Chairman of Sungai Siput Division until 2008. • In 1996, assumed 3 political positions as the National Youth Chairman, Vice-Chairman of

Perak State and Committee Member of Central Committee until the years 1999, 2002 and 2013 respectively.

• In 1995, held the position as Member of Perak State Executive Council until 2008. • Held 2 important political positions in 1999, as Deputy Secretary-General of the Central

Committee and Head of its Legal Bureau until the years 2005 and 2008. • In 2002 until 2005, he assumed the position of Secretary of the Perak Parti Gerakan. • In 2005, assumed 2 political positions as Vice-President of Parti Gerakan National Committee

and Chairman of the Perak State until 2008 and 2013 respectively. • Held onto his current position of Chairman of Beruas Division since 2008. • Was appointed as the Advisor of the Chief Acting President of the Parti Gerakan for a few

months, and been appointed to current position as its National Advisor. • Since 2014, has resumed his legal practice at Toh Theam Hock & Co in Ipoh and appointed

as the Chairman of Yayasan Penjaja Dan Peniaga Kecil 1 Malaysia (YPPKM).

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 15 of 17

Dato' Wan Asmadi Bin Wan Ahmad

Non-Independent Non-Executive Director

• Graduated with a Bachelor degree in Business Administration with a major in Accounting from Temple University, Philadelphia, USA in 1989.

• Graduated with a Masters of Business Administration specializing in Finance from the same university.

• Began career as an assistant for tax and audit works with Pricewaterhouse Tax Service (M) Sdn Bhd in 1989.

• In 1990, entered the oil and gas industry, and joined Mobil Oil (M) Sdn Bhd as a Financial Executive.

• In 1991, joined Petronas Carigali Sdn Bhd as the Unit Head of Budget and Management Accounting of the Peninsular Malaysia Operations.

• In 1996, entered the investment banking industry and joined Maybank Investment Bank Berhad as a Deputy Manager of the Corporate Finance Department.

• In 2002, joined Affin Investment Bank Berhad as an Assistant General Manager. • Joined Malaysian International Merchant Bankers Berhad from 2002 to 2004 as a General

Manager. • In 2004, returned to Maybank Investment Bank Berhad as the head of the newly setup

Equities Market Division. • Was promoted to become the Director of Dealing in Maybank Securities Sdn Bhd • Was assigned to set-up and head the Islamic Capital Market, a division independent from the

conventional Debt Market Division. • Appointed as the Chief Operating Officer of Anfaal Capital in 2009. • Assumed his current position as Managing Principal, Director and Co-Founder of DWA

Advisory Sdn Bhd. • Founded DWA Private Equity Sdn Bhd and been serving as the non-Executive Chairman. • Currently a member of the Market Participants Committee of Bursa Malaysia.

Mohd Annas Bin Md Isa Non-Independent Non-Executive Director

• Graduated with a Bachelor of Finance (Honours) from University Teknologi MARA, Malaysia, in 2000.

• Began his career as a dealer representative with OSK Securities Berhad in 2000. • Joined Aseambankers Malaysia Berhad as a Senior Executive. • In 2006, joined Kenanga Investment Bank Berhad. • In 2009, joined AmInvestment Bank Berhad as a Manager in the Equity Capital Market

division. • In 2013, joined Bank Muamalat Malaysia Berhad as the Head of Equity Capital Market/

Private Equity in Investment Banking division. • Has more than 15 years of experience in various capacities in the equity capital market

division and investment banking. Ng Wai Luen Independent

Non-Executive Director

• Graduated with a Bachelor of Business (Accounting) with distinction from RMIT University, Australia in 1992.

• In 1994, completed the Certified Public Accountant Australia examinations. • Completed Malaysia Institute of Certified Public Accountant examinations. • Is a member of CPA Australia, MICPA and a Chartered Accountant registered with the

Malaysian Institute of Accountant. • Began his career with KPMG Malaysia in 1993. • Joined OKA Corporation Berhad as Finance Manager. • Was appointed as joint company secretary. • In 2002, was promoted to General Manager and Chief Financial Officer. • Was appointed as head of the risk management committee from 2003 to 2011. • Was appointed as head of the strategic business management team, member of a

remunerations committee and member of the Employee Share Option Scheme from 2004 to 2011.

• In 2012, joined Starken AAC Sdn Bhd and G-Cast Concrete Sdn Bhd, direct and indirect subsidiaries of Chin Hin Group Berhad as an executive director.

Source: Company

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 16 of 17

Income Statement Financial Data & Ratios

FY Dec (RM m) 2013A 2014A 2015A 2016F 2017F 2018F FY Dec (RM m) 2013A 2014A 2015A 2016F 2017F 2018F Revenue 64.4 77.6 74.1 79.4 89.6 97.0 Growth (%)

EBITDA 14.3 25.6 33.5 36.9 43.8 50.8 Revenue n.a. 20.5 (4.5) 7.1 12.9 8.2

Depreciation -5.2 -5.8 -6.7 -6.8 -7.2 -9.4 EBITDA n.a. 79.2 30.8 10.3 20.3 15.6

EBIT 9.1 19.8 26.7 30.1 36.7 41.4 Operating Income n.a. 118.1 34.8 12.7 21.7 12.9

Interest Income 0.0 0.0 0.0 0.0 0.0 0.0 Pre-tax Income n.a. 211.3 44.7 19.1 26.4 15.6

Interest Expense -4.8 -6.5 -7.5 -7.2 -7.7 -7.9 Net Income n.a. 87.0 42.3 8.8 29.8 15.0

Others 0.9 0.9 1.8 1.8 2.0 2.2 Exceptionals/FV 0.0 0.0 0.0 0.0 0.0 0.0 PBT 4.3 13.3 19.3 22.9 29.0 33.5 Profitability (%) Taxation 2.9 0.2 -0.1 -2.1 -1.9 -2.3 EBITDA Margin 22.2 33.0 45.1 46.5 49.5 52.9

Minority Interest 0.0 0.0 0.1 0.0 0.0 0.0 Operating Margin 14.1 25.5 36.0 37.9 40.9 42.7

Net Profit 7.2 13.5 19.2 20.9 27.1 31.1 PBT Margin 6.6 17.2 26.0 28.9 32.3 34.5

Net Margin 11.2 17.4 25.9 26.3 30.2 32.1

E. Tax Rate 68.7 1.3 (0.3) (9.0) (6.5) (7.0)

Balance Sheet ROE 9.9 16.5 16.5 17.7 12.8 13.0

FY Dec (RM m) 2013A 2014A 2015A 2016F 2017F 2018F ROA 3.5 6.0 7.5 7.1 7.6 7.7

Fixed Assets 174 210 226 257 329 350 Intangibles 3 2 2 2 2 2 Other FA 7 6 7 7 7 7 DuPont Analysis Inventories 1 1 1 1 1 1 Net margin (%) 11.2 17.4 25.9 26.3 30.2 32.1

Receivables 3 5 12 13 14 16 Assets Turnover (x) 31.4 34.5 29.0 27.2 25.3 24.1

Other CA 2 1 7 7 7 7 Leverage Factor (x) 2.8 2.7 2.4 1.8 1.7 1.7

Cash 13 20 12 29 31 30 ROE (%) 9.9 16.5 17.7 12.8 13.0 13.5

Total Assets 203 244 267 316 392 412 Leverage Payables 4 2 3 3 3 3 Debt/Asset (x) 0.40 0.42 0.45 0.31 0.39 0.36

ST Borrowings 12 3 21 25 25 25 Debt/Equity (x) 1.12 1.12 0.95 0.49 0.70 0.62

Other ST Liability 4 3 8 7 7 7 N Debt/(Cash) 68.3 81.5 108.0 67.9 121.8 119.9

LT Borrowings 62 94 97 72 128 125 N Debt/Eqty (x) 0.94 0.90 0.85 0.34 0.56 0.50

Other LT Liability 16 14 12 10 10 10 Minority Int. 0 0 1 1 1 1 Valuations Net Assets 73 90 126 199 219 243 Core EPS (sen) 0.6 1.2 1.7 1.8 2.4 2.7

NDPS (sen) 0.0 0.0 0.0 0.46 0.59 0.68

Share Cap 50 50 71 114 114 114 BV/share (RM) 0.06 0.08 0.11 0.17 0.19 0.21

Reserves 6 39 56 85 105 128 Core PER (x) 23.78 12.72 8.93 8.22 6.33 5.50

Shareholders’ Equity

73 90 126 199 219 243 N. Div. Yield (%) 0.0 0.0 0.0 3.0 4.0 4.5

PBV (x) 2.3 1.9 1.4 0.9 0.8 0.7

Cashflow Statement EV/EBITDA (x) 16.2 9.7 8.3 6.5 9.7 8.3

FY Dec (RM m) 2013A 2014A 2015A 2016F 2017F 2018F Operating CF 10 21 30 33 41 48

Investing CF -45 -9 -29 -40 -80 -30

Financing CF 43 4 -9 24 41 -18

Net Change in Cash 8 16 -8 17 1 -1

Free Cash Flow -35 12 1 -5 -39 18

Source: Kenanga Research

Perak Transit Berhad IPO Note 20 September 2016

PP7004/02/2013(031762) Page 17 of 17

Stock Ratings are defined as follows: Stock Recommendations OUTPERFORM : A particular stock’s Expected Total Return is MORE than 10% (an approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%). MARKET PERFORM : A particular stock’s Expected Total Return is WITHIN the range of 3% to 10%. UNDERPERFORM : A particular stock’s Expected Total Return is LESS than 3% (an approximation to the 12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate). Sector Recommendations*** OVERWEIGHT : A particular sector’s Expected Total Return is MORE than 10% (an approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%). NEUTRAL : A particular sector’s Expected Total Return is WITHIN the range of 3% to 10%. UNDERWEIGHT : A particular sector’s Expected Total Return is LESS than 3% (an approximation to the

12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate). ***Sector recommendations are defined based on market capitalisation weighted average expected total return for stocks under our coverage.

This document has been prepared for general circulation based on information obtained from sources believed to be reliable but we do not make any representations as to its accuracy or completeness. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may read this document. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees. Kenanga Investment Bank Berhad accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. Kenanga Investment Bank Berhad and its associates, their directors, and/or employees may have positions in, and may effect transactions in securities mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealings with respect to these companies.

Published and printed by: KENANGA INVESTMENT BANK BERHAD (15678-H) 8th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia Chan Ken Yew Telephone: (603) 2166 6822 Facsimile: (603) 2166 6823 Website: www.kenanga.com.my Head of Research