PAYROLL LAW - PSF Presentations · presentation slides: ... •Payroll law compliance is more...

68

Presented by Pamela Shull PAYROLL LAW

Transcript of PAYROLL LAW - PSF Presentations · presentation slides: ... •Payroll law compliance is more...

Presented by

Pamela Shull

PAYROLL LAW

Today’s Presentation Slides

• You can download copies of today’s presentation slides:

www.psfpresentations.com

Click on “services”

Under the Payroll Classes section click on your state.

Take a picture of this slide with your cell phone

True or False? WB-1

•Payroll law compliance is more about how

•you interpret the law than the actual “Math”

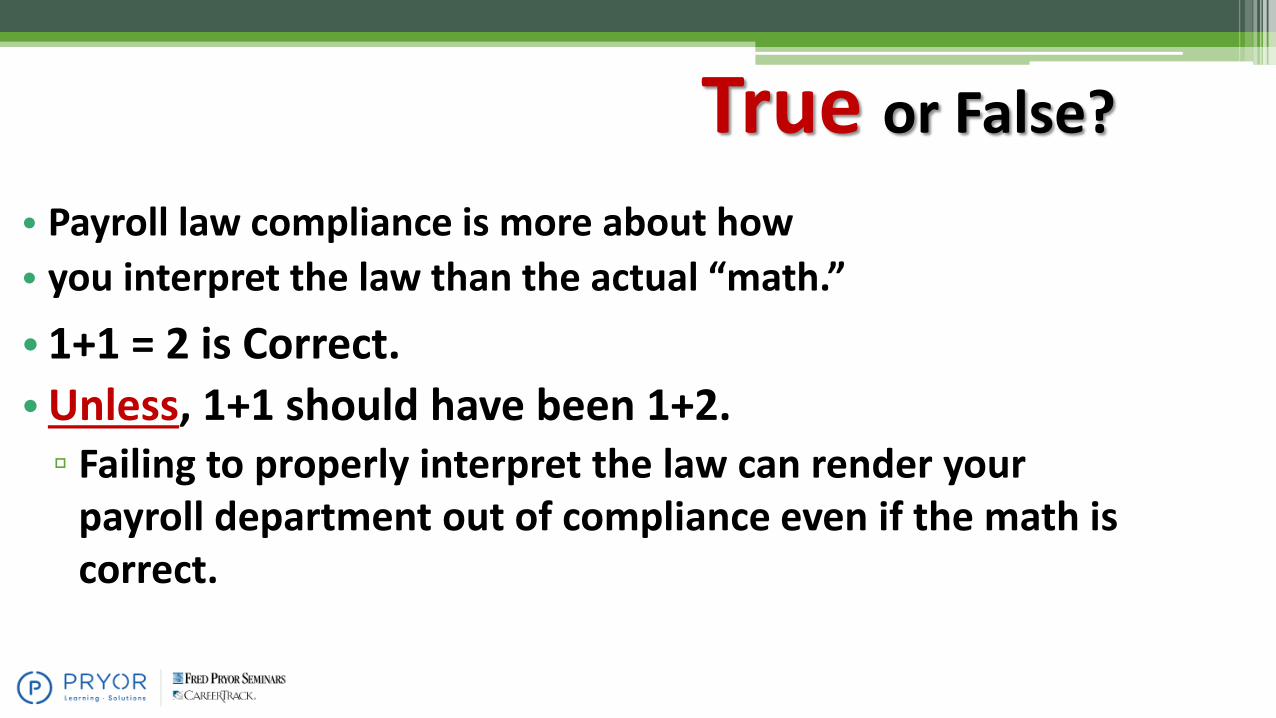

True or False?

• Payroll law compliance is more about how

• you interpret the law than the actual “math.”

• 1+1 = 2 is Correct.

•Unless, 1+1 should have been 1+2.▫ Failing to properly interpret the law can render your

payroll department out of compliance even if the math is correct.

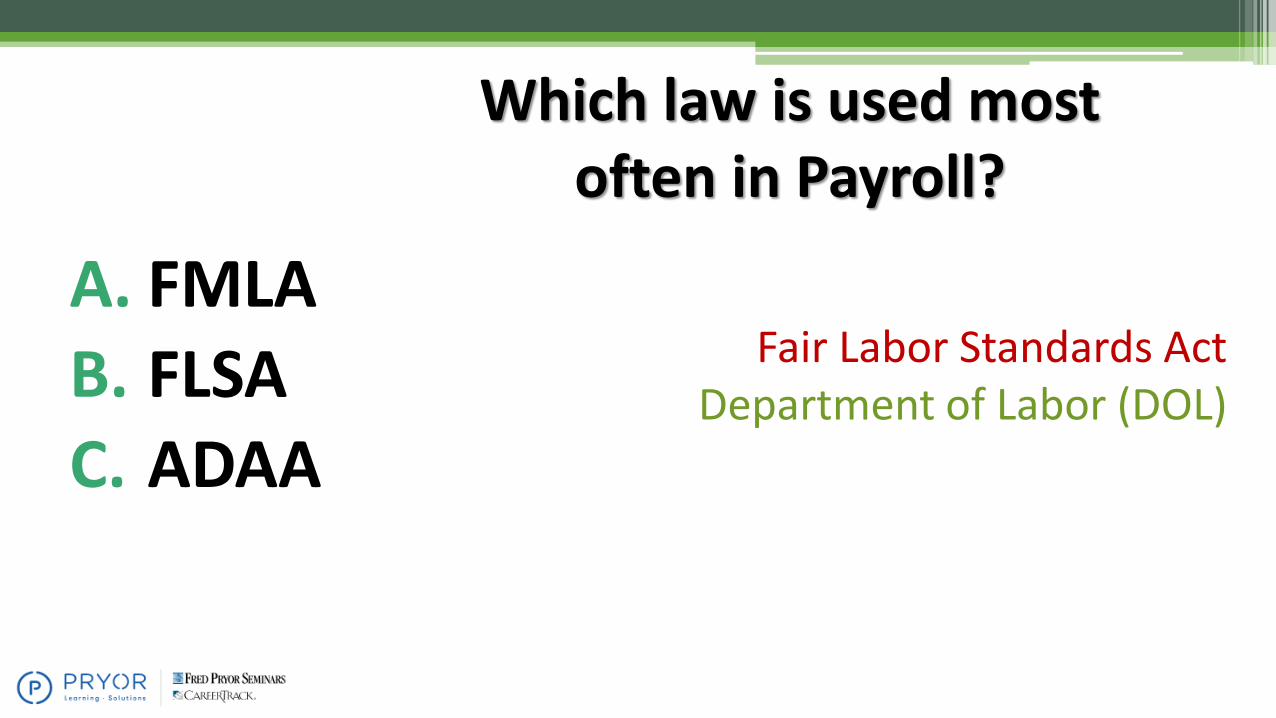

Which law is used most often in Payroll?

A. FMLA

B. FLSA

C. ADAA

Fair Labor Standards ActDepartment of Labor (DOL)

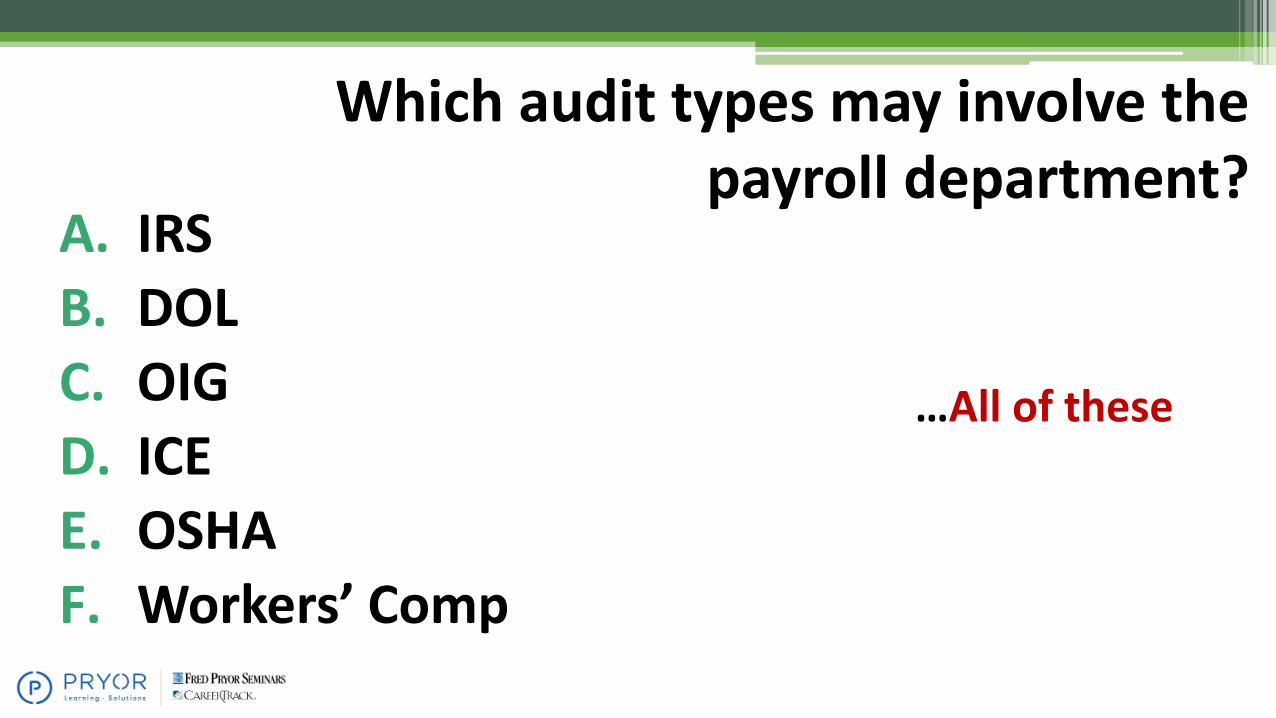

Which audit types may involve the payroll department?

A. IRS

B. DOL

C. OIG

D. ICE

E. OSHA

F. Workers’ Comp

…All of these

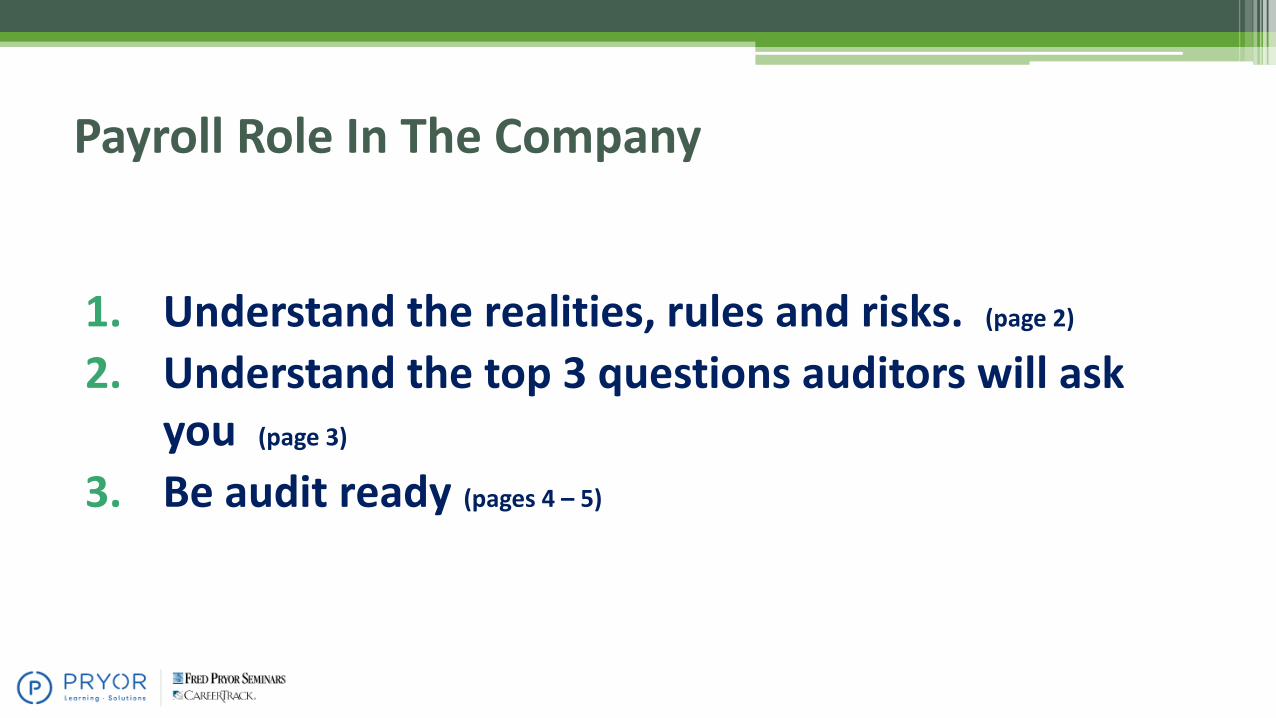

Payroll Role In The Company

1. Understand the realities, rules and risks. (page 2)

2. Understand the top 3 questions auditors will ask you (page 3)

3. Be audit ready (pages 4 – 5)

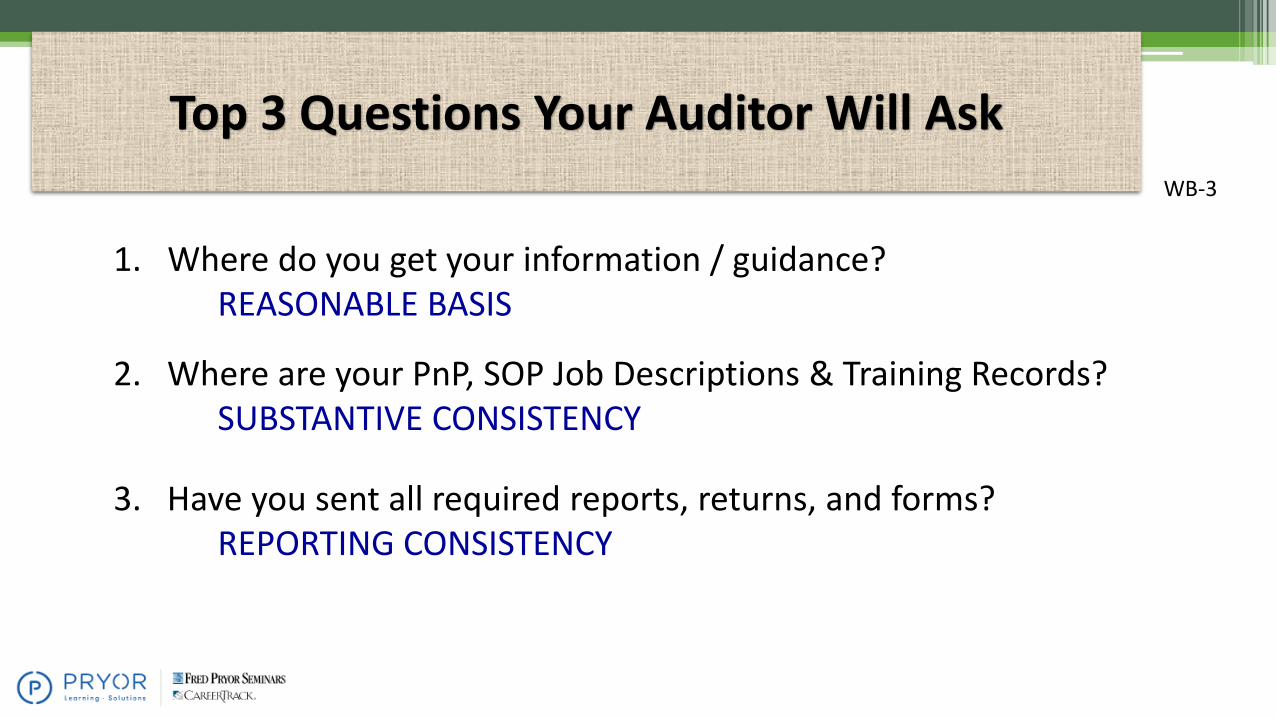

Top 3 Questions Your Auditor Will Ask

1. Where do you get your information / guidance? REASONABLE BASIS

2. Where are your PnP, SOP Job Descriptions & Training Records?SUBSTANTIVE CONSISTENCY

3. Have you sent all required reports, returns, and forms?REPORTING CONSISTENCY

WB-3

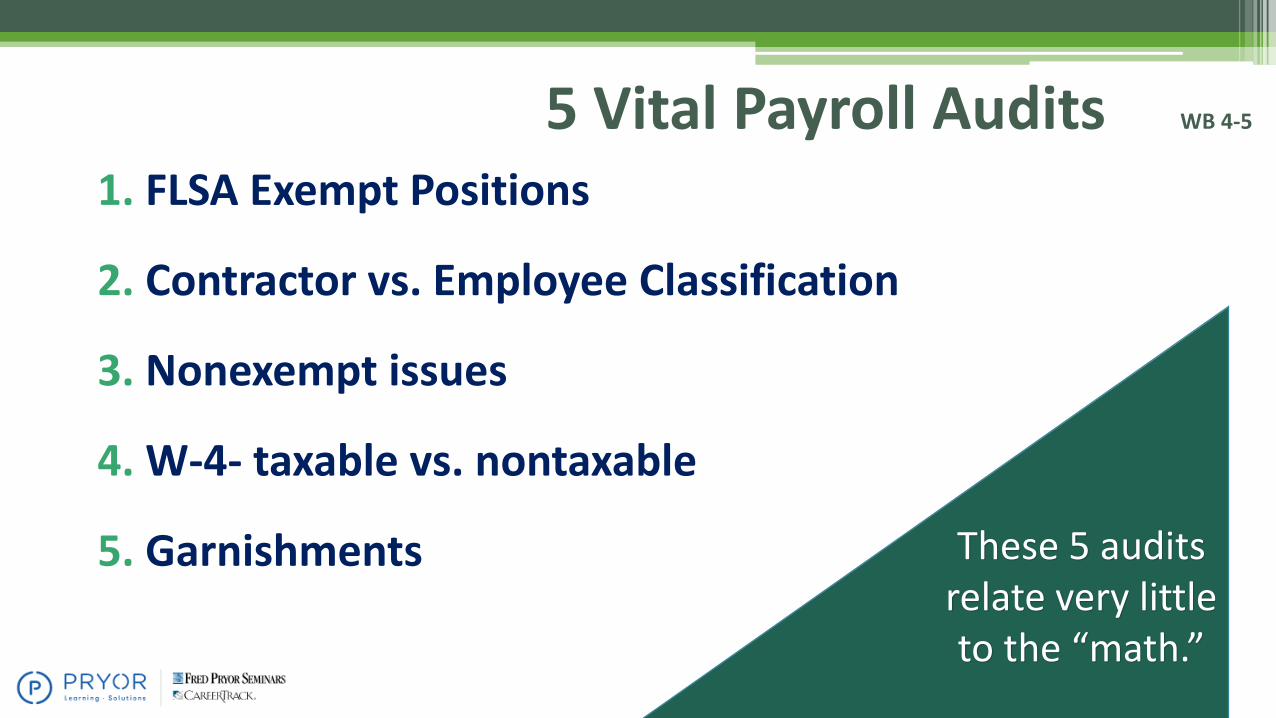

5 Vital Payroll Audits WB 4-5

1. FLSA Exempt Positions

2. Contractor vs. Employee Classification

3. Nonexempt issues

4. W-4- taxable vs. nontaxable

5. Garnishments These 5 audits relate very little to the “math.”

•Company Tools▫ Employee Handbook – what the law says

– Ultimate Employer

▫ Payroll Policies and Procedure Manual –how the law works – Helpdesk for Payroll

▫ Job Descriptions – overtime or not? Contractor or employee? – Ultimate Employer

Audit Tools

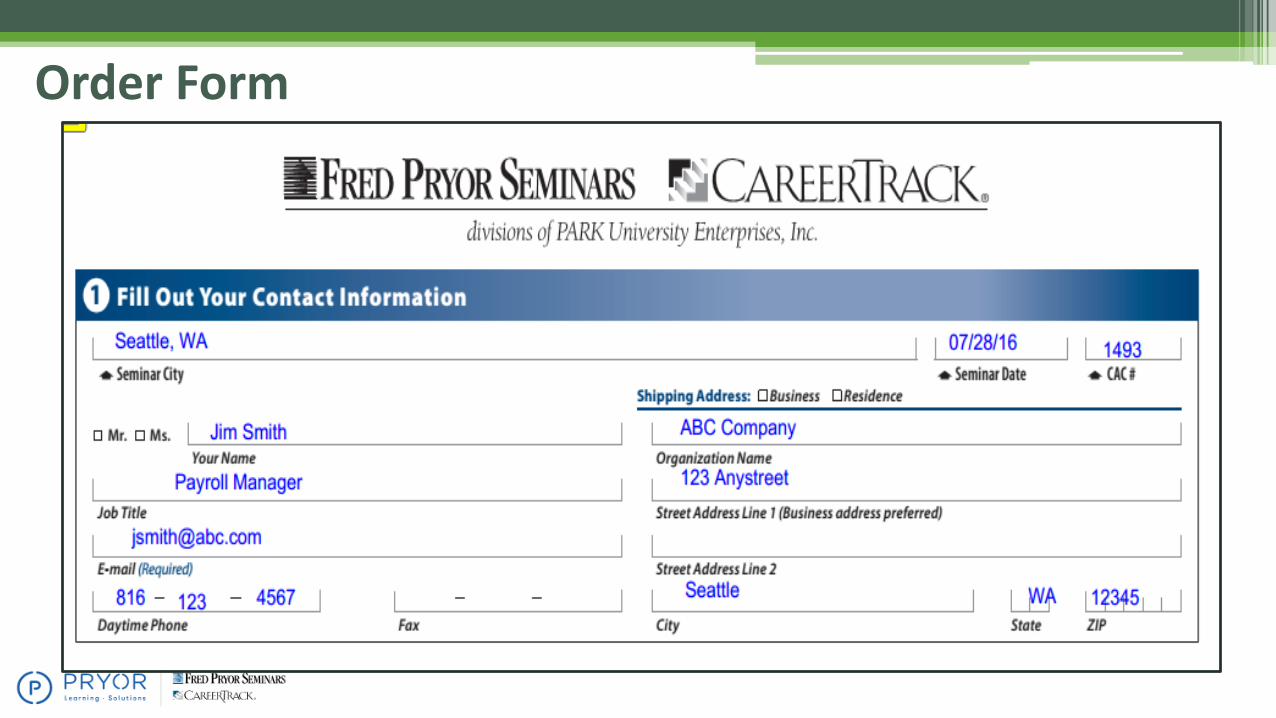

Order Form

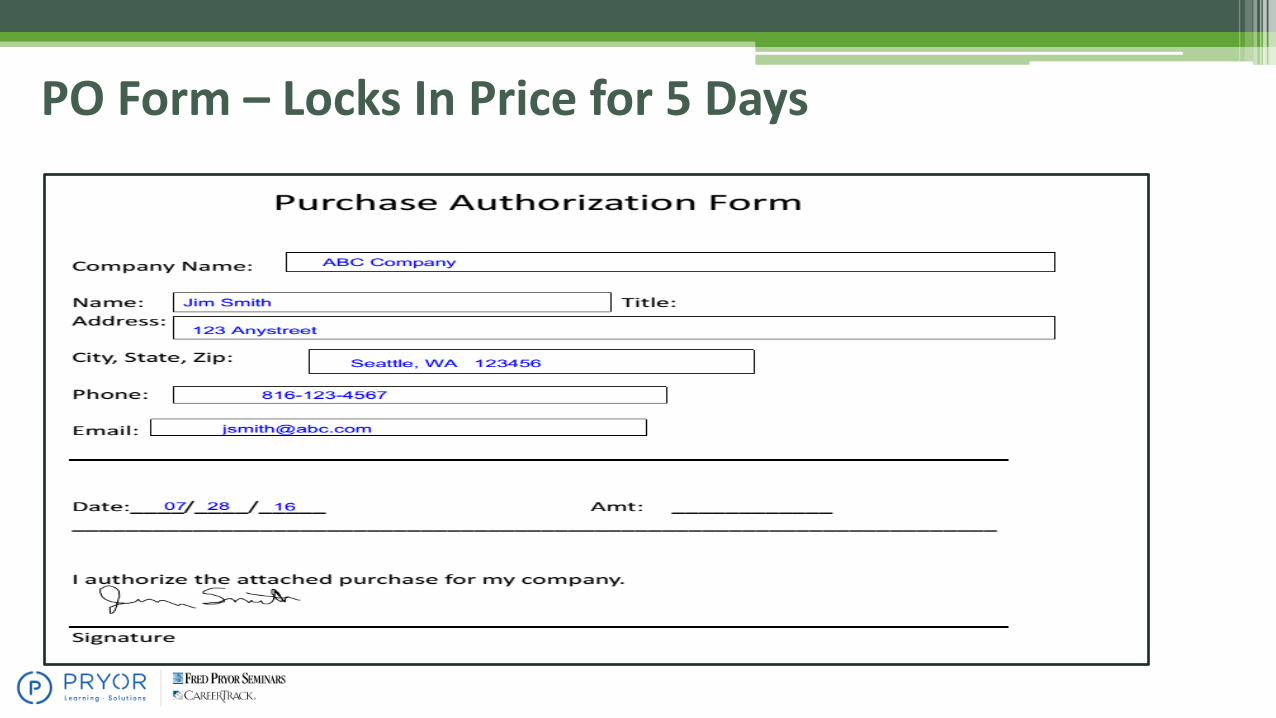

PO Form – Locks In Price for 5 Days

Module 2

Pages 6 - 18

Exempt Employees

• Exempt employees▫ Guaranteed weekly salary▫ Hours do not apply to them▫ Paid a salary “to get the job done”▫ Overtime is not a factor

• Nonexempt employees▫ May be salaried or hourly▫ Gets paid for every hour worked▫ Paid overtime if physically works over 40 in a workweek

Exempt vs. Nonexempt WB 6

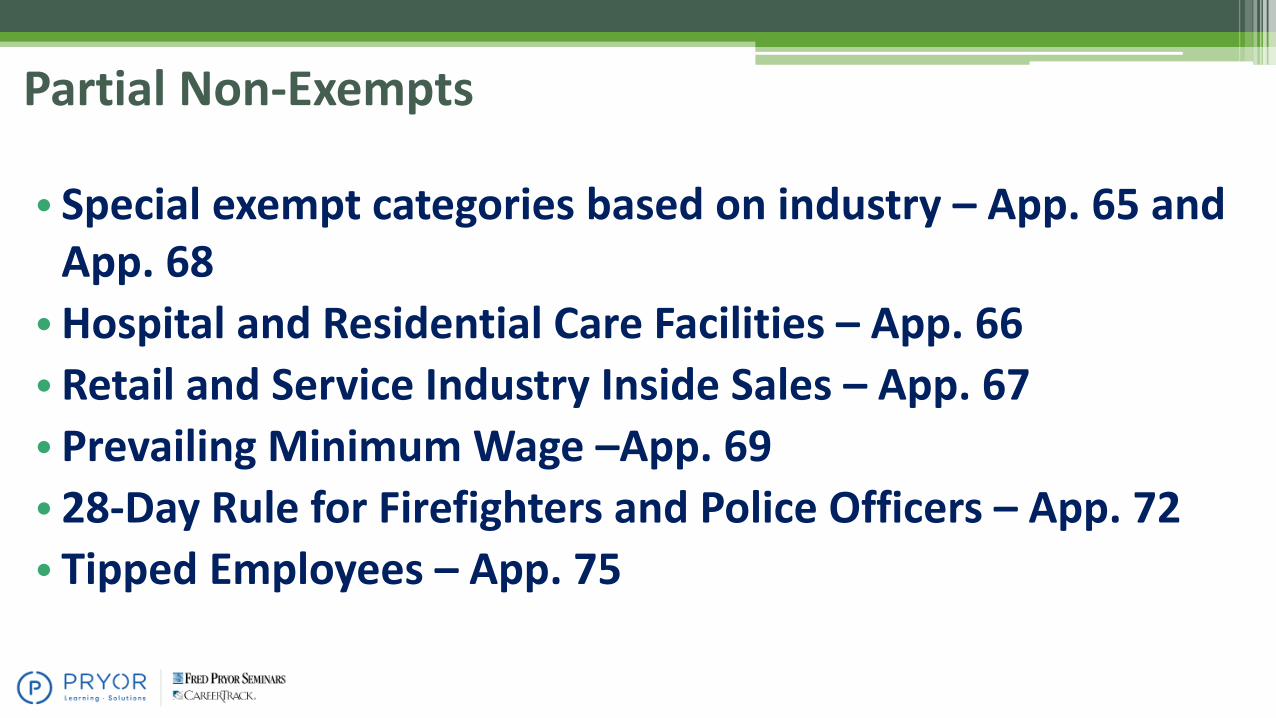

• Special exempt categories based on industry – App. 65 and App. 68

•Hospital and Residential Care Facilities – App. 66

•Retail and Service Industry Inside Sales – App. 67

• Prevailing Minimum Wage –App. 69

• 28-Day Rule for Firefighters and Police Officers – App. 72

• Tipped Employees – App. 75

Partial Non-Exempts

Exempt Classifications WB-6

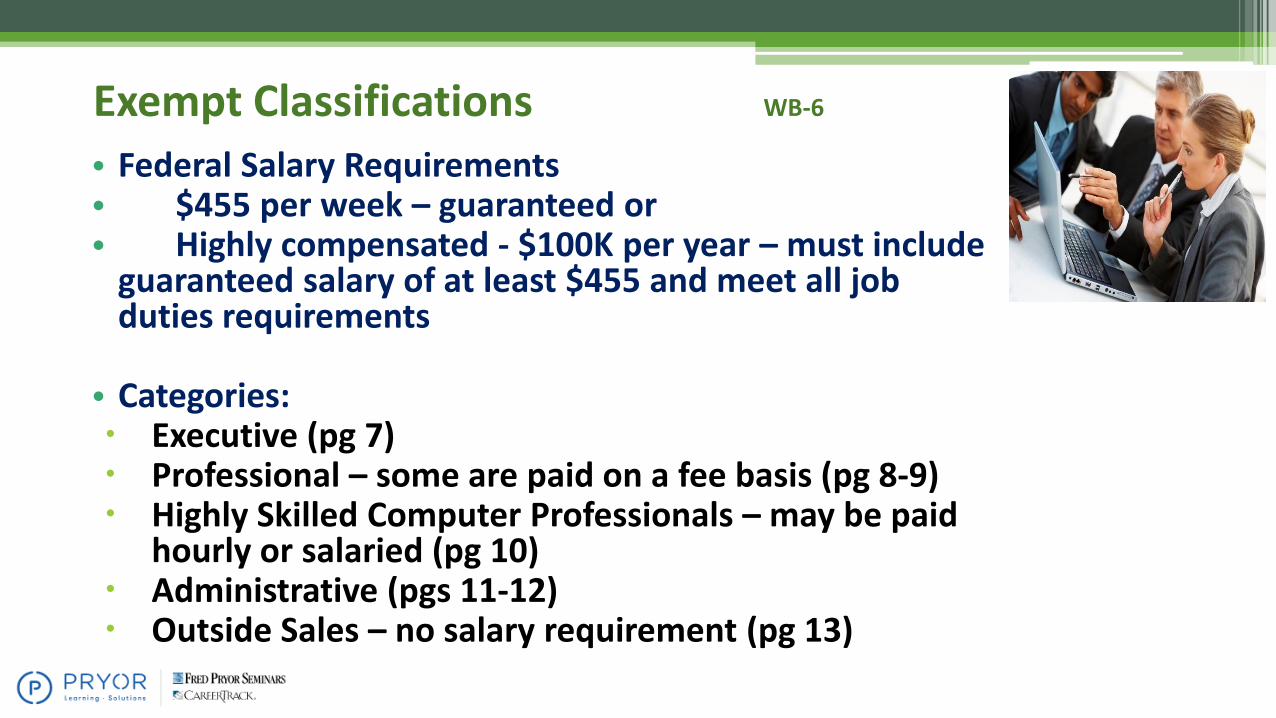

• Federal Salary Requirements• $455 per week – guaranteed or• Highly compensated - $100K per year – must include

guaranteed salary of at least $455 and meet all job duties requirements

• Categories: Executive (pg 7) Professional – some are paid on a fee basis (pg 8-9) Highly Skilled Computer Professionals – may be paid

hourly or salaried (pg 10) Administrative (pgs 11-12) Outside Sales – no salary requirement (pg 13)

Executive Exempt Requirements

• Run a recognized portion of the company

• Ability to hire, terminate, change policy, set budgets, make decisions, etc.

• Supervise 2 or more full-time persons or the equivalent of

WB-7

Professional Exempt Requirements WB-8- 9

• Learned Professional (WB 8)

• Advanced knowledge in a recognized professional field

• Impart knowledge

• Use discretionary judgment

• Creative-Artistic Professional (WB 9)

• Use of creative and artistic abilities

• Cannot be told how to create the work

Highly Skilled in a Computer-Related OccupationWB-10

• Federal Pay Option• Salary (at least $455 per week) or• Hourly rate of $27.63 an hour

• Computer programmers, designers of computers and system analysts

• Does not include: computer operators, repairpersons, technicians, data entry or help desks

Administrative Exempt Requirements WB 11-12

• Office or non-manual work pertaining to general business operations. Work of substantial importance with higher learning or experience.

• Limited powers of responsibility, authority and influence.

• Must report directly to another exempt employee

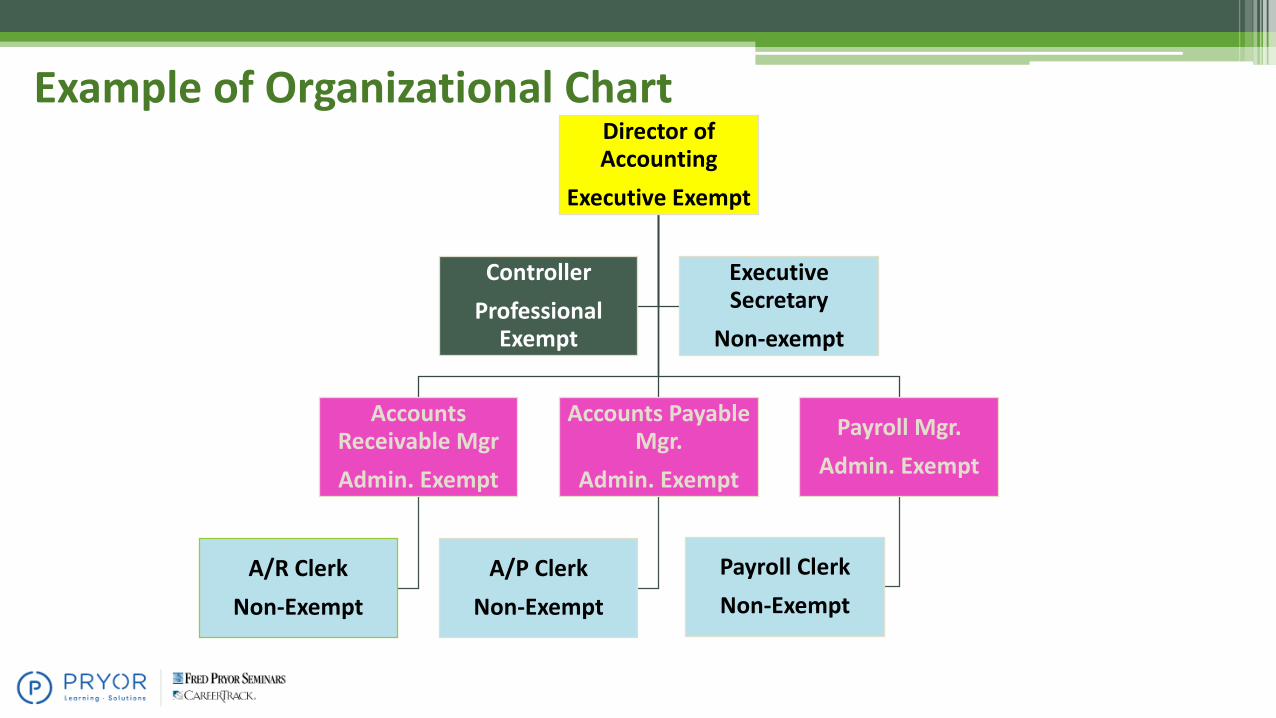

Example of Organizational ChartDirector of Accounting

Executive Exempt

Accounts Receivable Mgr

Admin. Exempt

A/R Clerk

Non-Exempt

Accounts Payable Mgr.

Admin. Exempt

A/P Clerk

Non-Exempt

Payroll Mgr.

Admin. Exempt

Payroll Clerk

Non-Exempt

Controller

Professional Exempt

Executive Secretary

Non-exempt

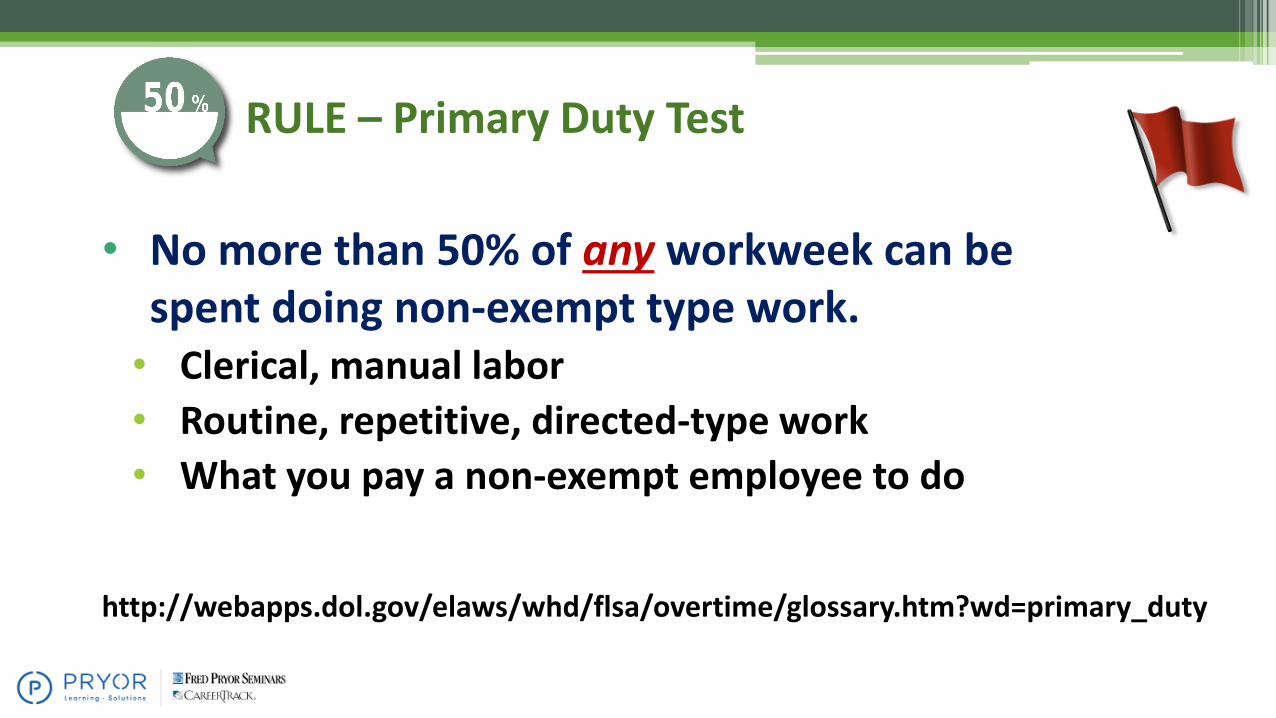

RULE – Primary Duty Test

• No more than 50% of any workweek can be spent doing non-exempt type work.• Clerical, manual labor

• Routine, repetitive, directed-type work

• What you pay a non-exempt employee to do

http://webapps.dol.gov/elaws/whd/flsa/overtime/glossary.htm?wd=primary_duty

Exempt Employee Pay Requirement WB 14-16

An exempt employee must receive the same amount of pay per workweek regardless of the number of hours they work or the quality of their work

• (§29 CFR 541.118 and .602)

Module 3

Pages 19 - 38

Contractors vs. Employees

25

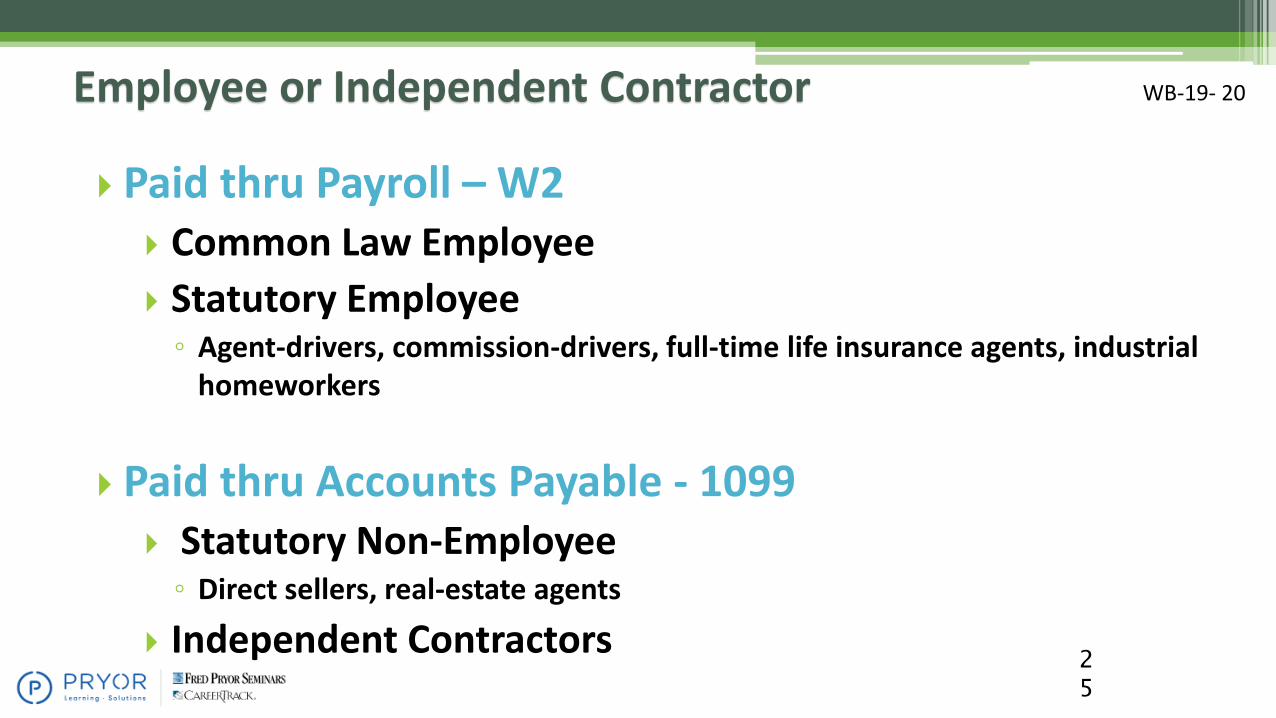

Employee or Independent Contractor

Paid thru Payroll – W2 Common Law Employee

Statutory Employee◦ Agent-drivers, commission-drivers, full-time life insurance agents, industrial

homeworkers

Paid thru Accounts Payable - 1099 Statutory Non-Employee◦ Direct sellers, real-estate agents

Independent Contractors

WB-19- 20

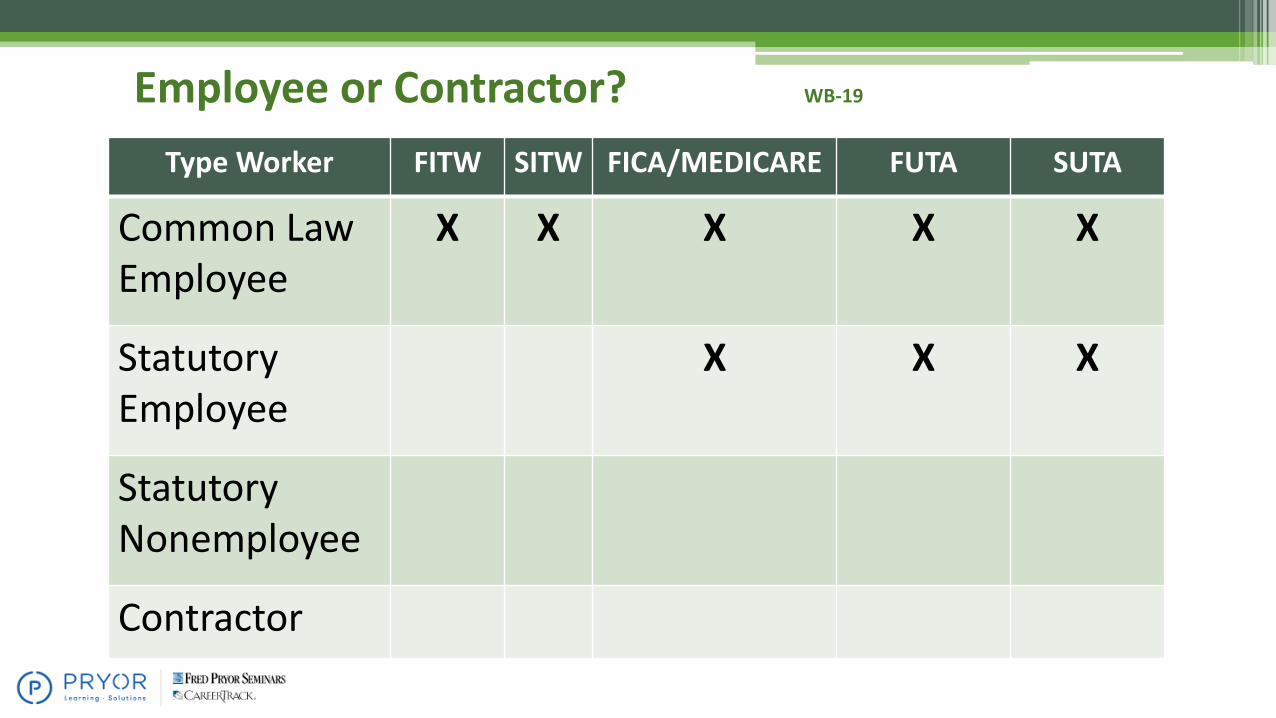

Employee or Contractor? WB-19

Type Worker FITW SITW FICA/MEDICARE FUTA SUTA

Common Law Employee

X X X X X

Statutory Employee

X X X

Statutory Nonemployee

Contractor

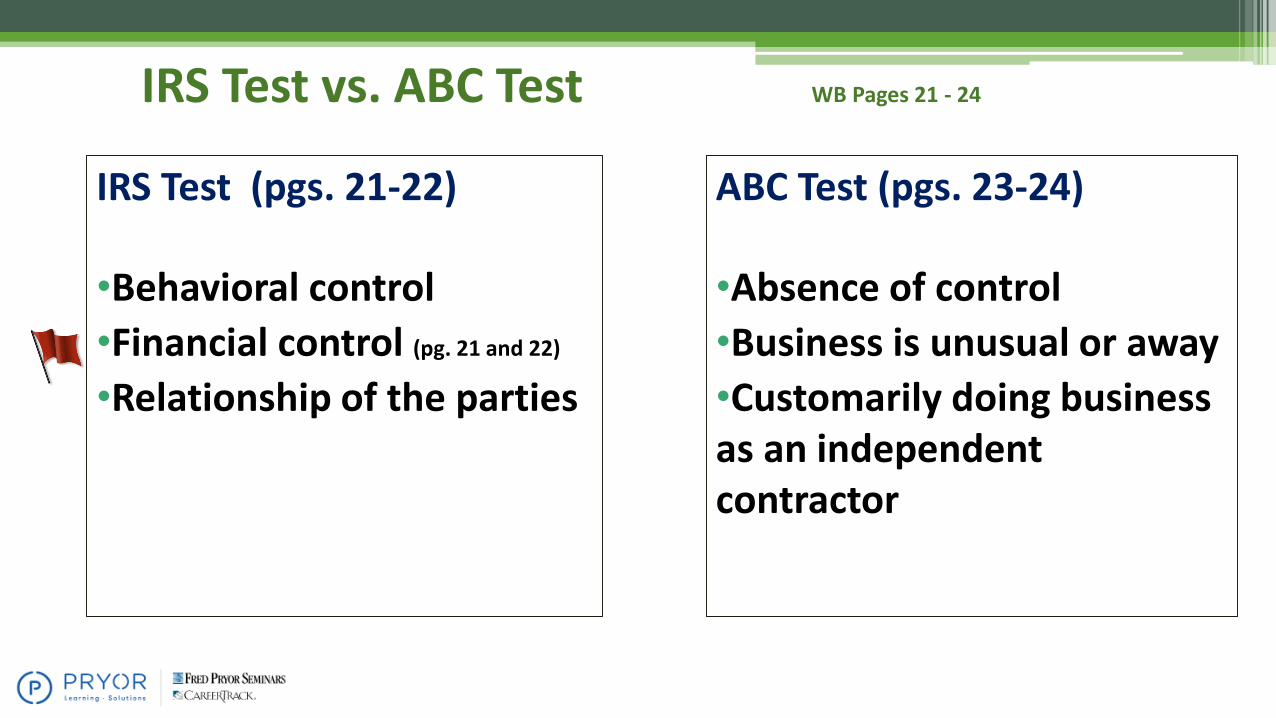

IRS Test (pgs. 21-22)

•Behavioral control

•Financial control (pg. 21 and 22)

•Relationship of the parties

ABC Test (pgs. 23-24)

•Absence of control

•Business is unusual or away

•Customarily doing business as an independent contractor

IRS Test vs. ABC Test WB Pages 21 - 24

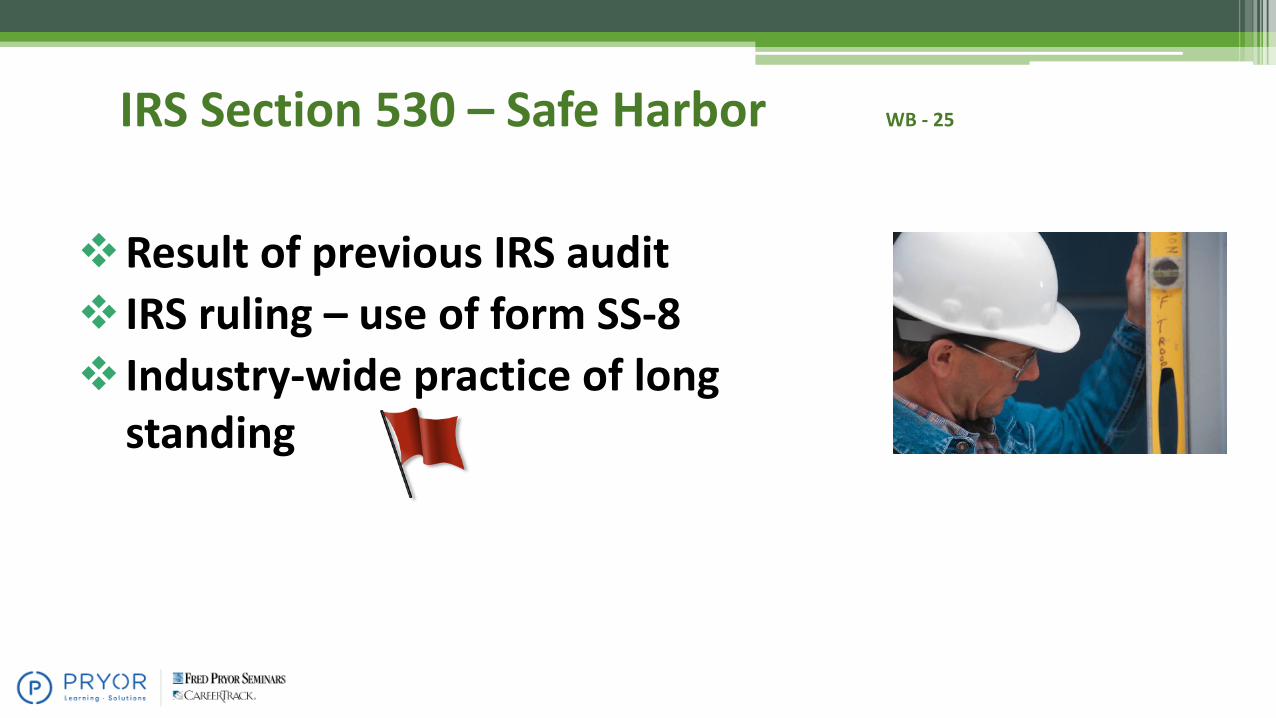

IRS Section 530 – Safe Harbor WB - 25

❖Result of previous IRS audit

❖ IRS ruling – use of form SS-8

❖ Industry-wide practice of long standing

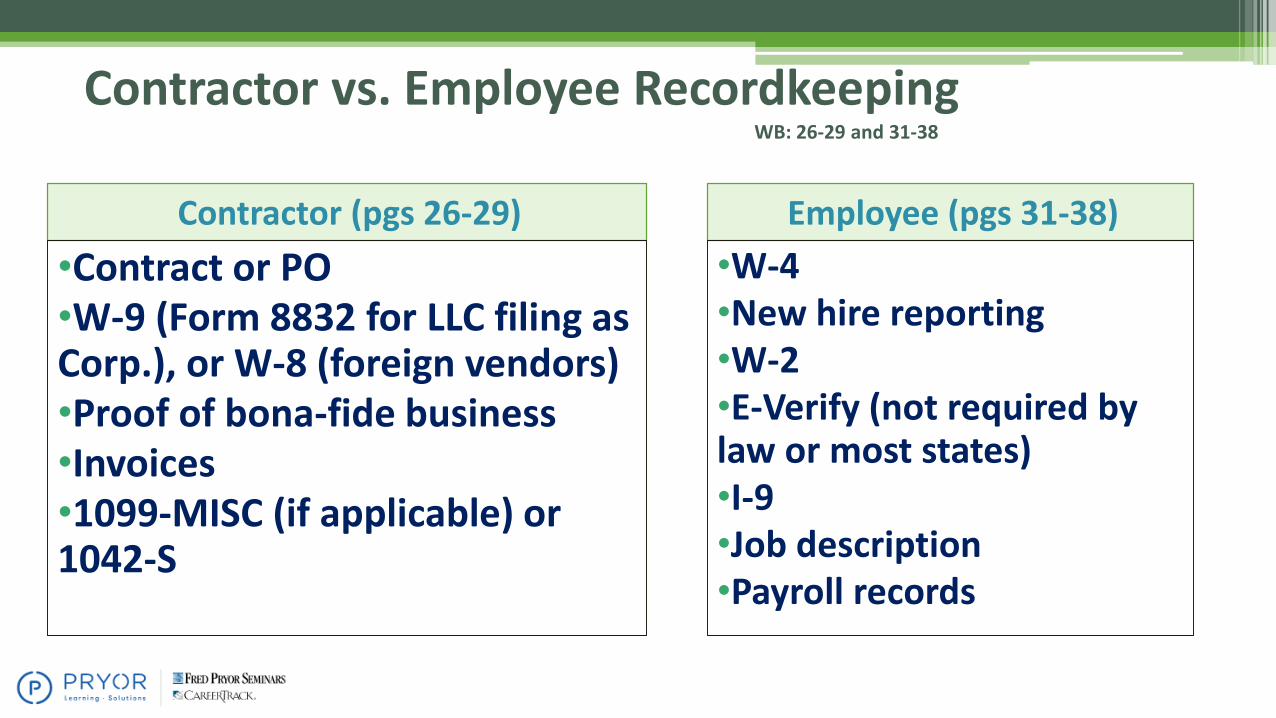

Contractor vs. Employee RecordkeepingWB: 26-29 and 31-38

Contractor (pgs 26-29)

•Contract or PO•W-9 (Form 8832 for LLC filing as Corp.), or W-8 (foreign vendors)•Proof of bona-fide business•Invoices•1099-MISC (if applicable) or 1042-S

Employee (pgs 31-38)

•W-4•New hire reporting•W-2•E-Verify (not required by law or most states)•I-9•Job description•Payroll records

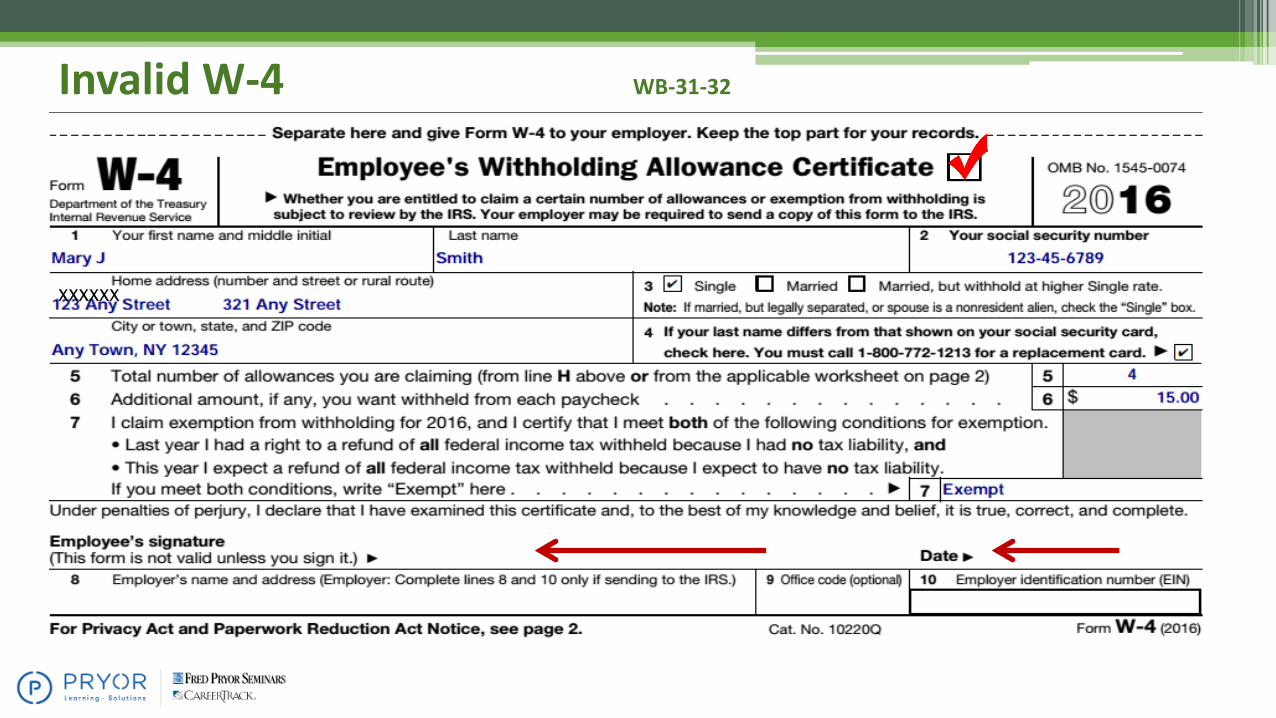

Invalid W-4 WB-31-32

xxxxxx

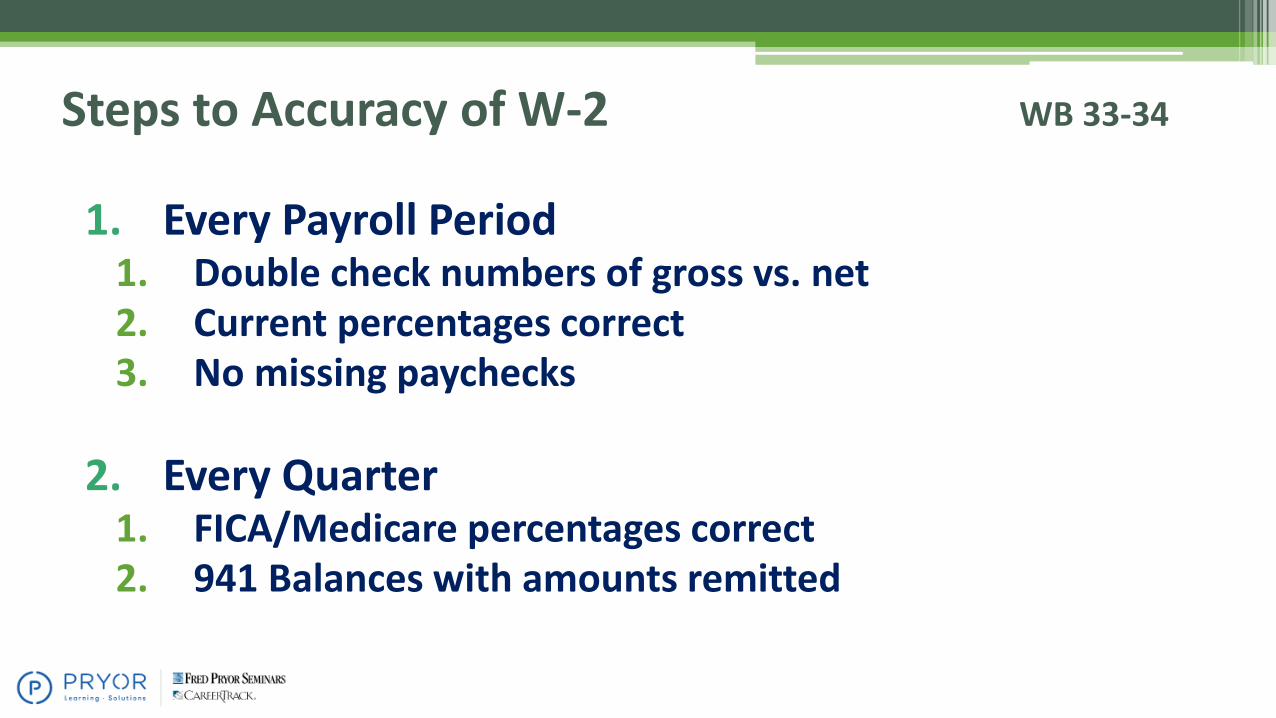

1. Every Payroll Period1. Double check numbers of gross vs. net2. Current percentages correct3. No missing paychecks

2. Every Quarter1. FICA/Medicare percentages correct2. 941 Balances with amounts remitted

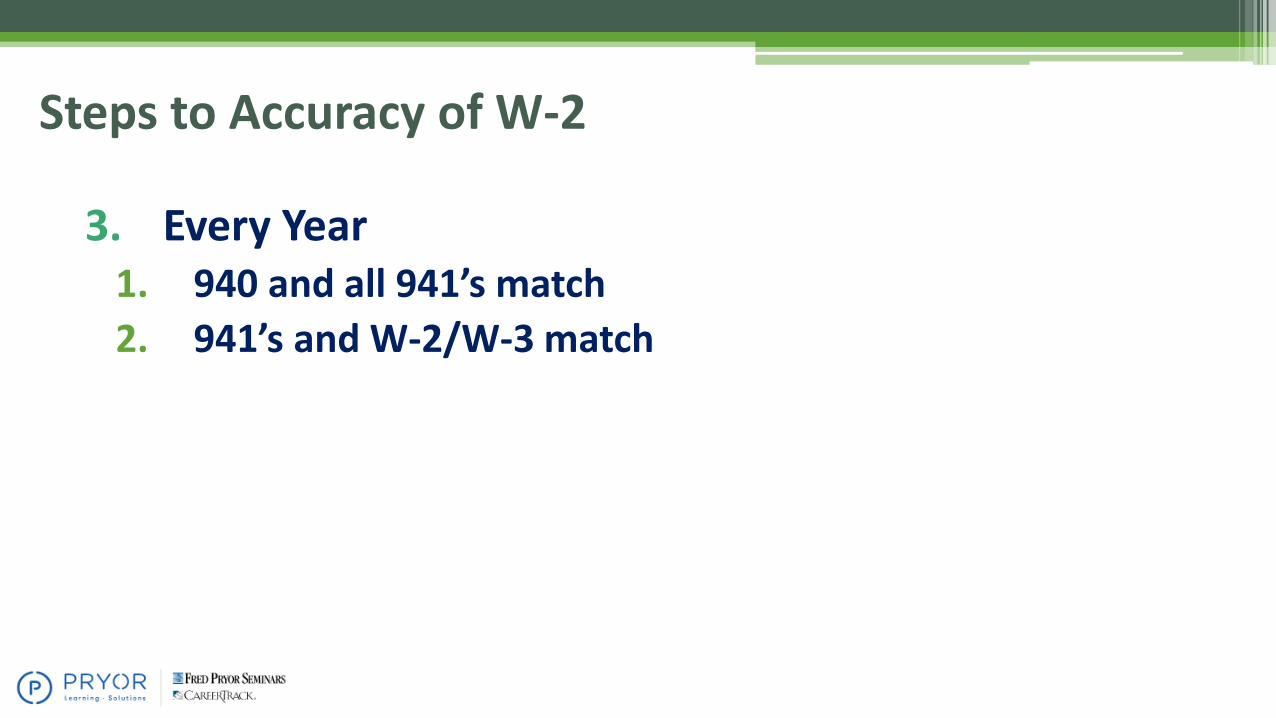

Steps to Accuracy of W-2 WB 33-34

3. Every Year1. 940 and all 941’s match

2. 941’s and W-2/W-3 match

Steps to Accuracy of W-2

SSN Matching/I-9 – E-Verify WB-35-38

• Social Security Number verification is suggested for all new hires after they are hired and before they are scheduled to work

▫ www.ssa.gov – Business Services On-Line tab

▫ www.uscis.gov – E-verify tab

Module 4

Pages 39-47

Payroll and the Nonexempt Employee

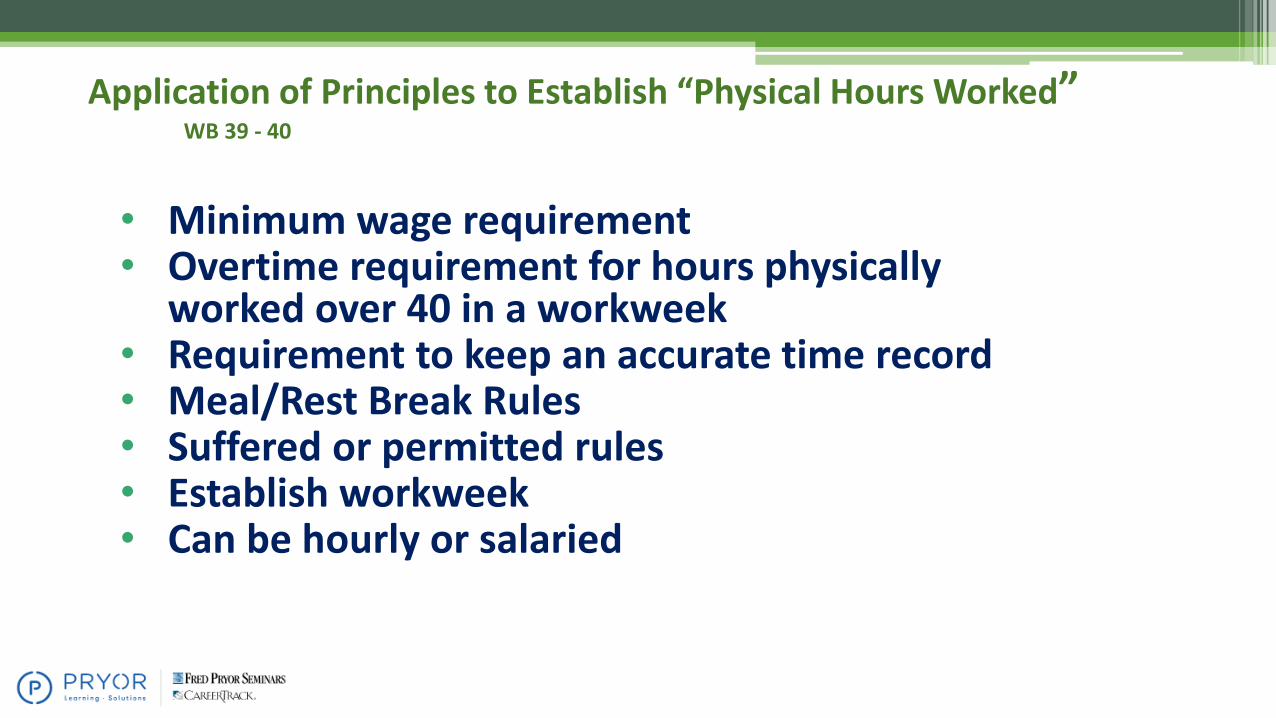

Application of Principles to Establish “Physical Hours Worked”WB 39 - 40

• Minimum wage requirement• Overtime requirement for hours physically

worked over 40 in a workweek• Requirement to keep an accurate time record• Meal/Rest Break Rules• Suffered or permitted rules• Establish workweek• Can be hourly or salaried

Salaried Non-Exempt – Purple Squirrel

Can be paid fixed or fluctuating◦Pay fixed when: employee’s schedule is a fixed schedule and rarely has overtime◦Pay fluctuating when: employee’s schedule will always fluctuate and almost always has overtime – but you never know how much

Must keep a time record

WB-41

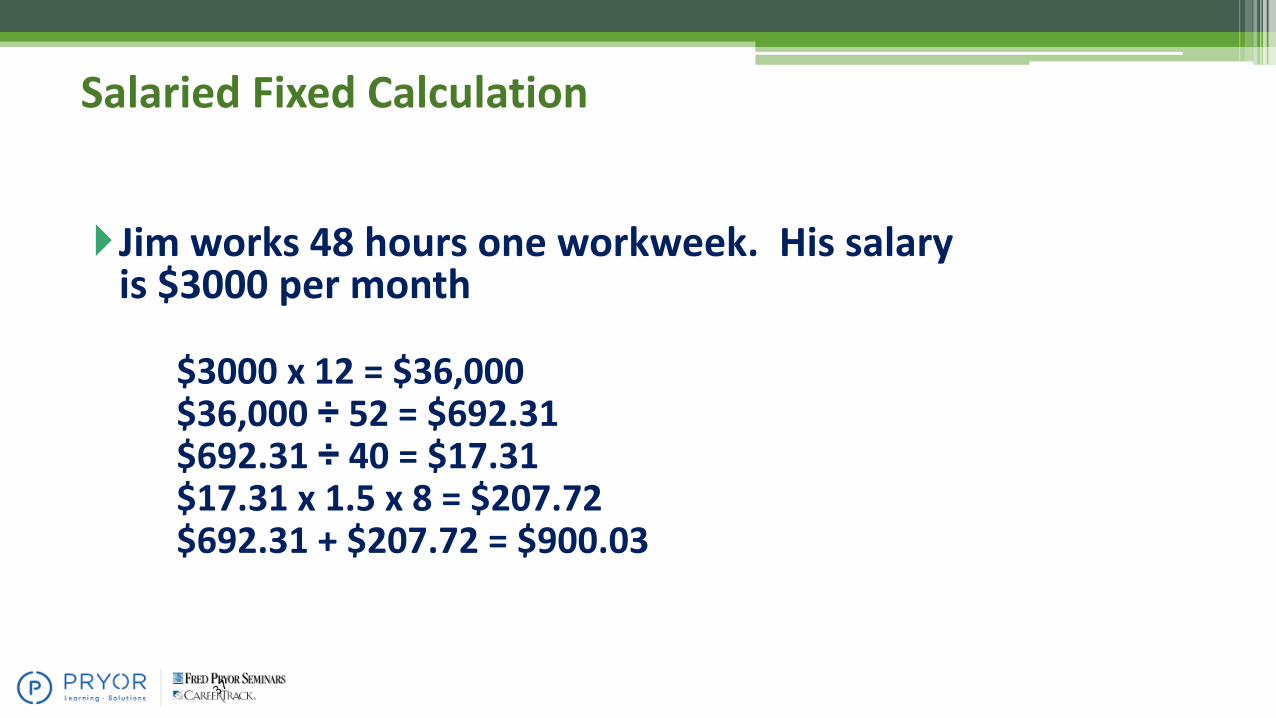

Salaried Fixed Calculation

Jim works 48 hours one workweek. His salary is $3000 per month

$3000 x 12 = $36,000$36,000 ÷ 52 = $692.31$692.31 ÷ 40 = $17.31$17.31 x 1.5 x 8 = $207.72$692.31 + $207.72 = $900.03

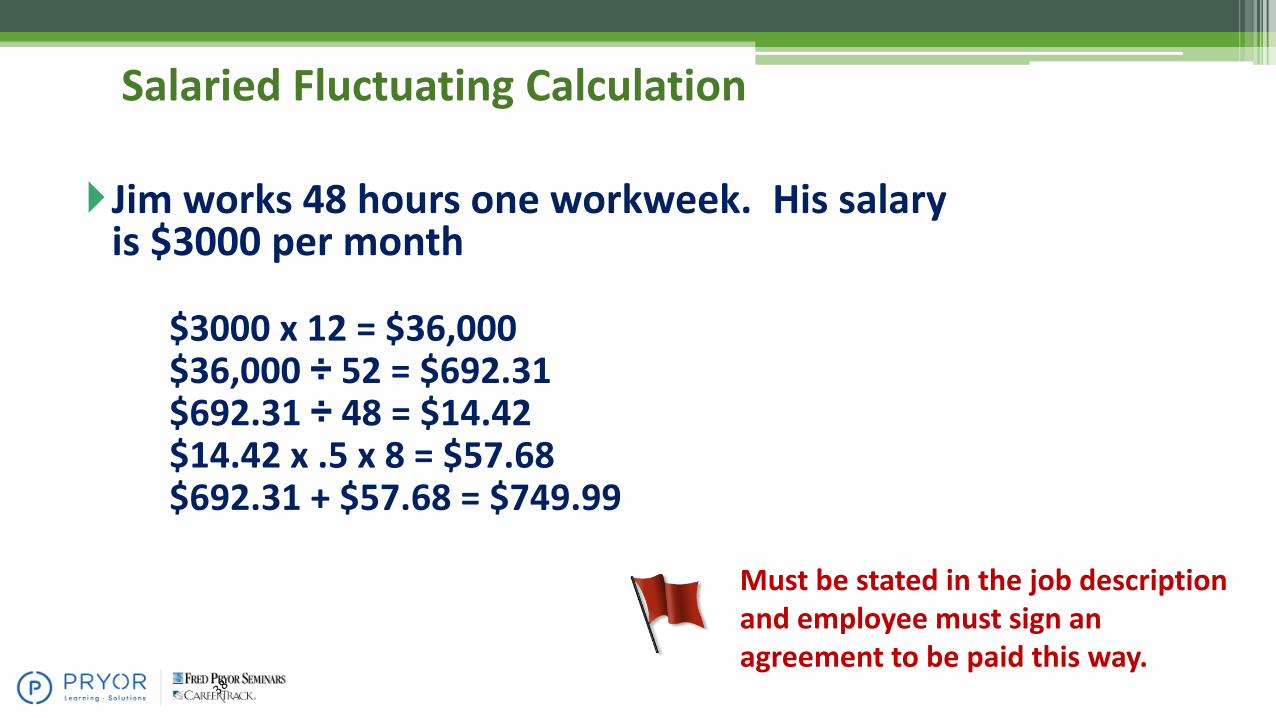

Salaried Fluctuating Calculation

Jim works 48 hours one workweek. His salary is $3000 per month

$3000 x 12 = $36,000$36,000 ÷ 52 = $692.31$692.31 ÷ 48 = $14.42$14.42 x .5 x 8 = $57.68$692.31 + $57.68 = $749.99

Must be stated in the job description and employee must sign an agreement to be paid this way.

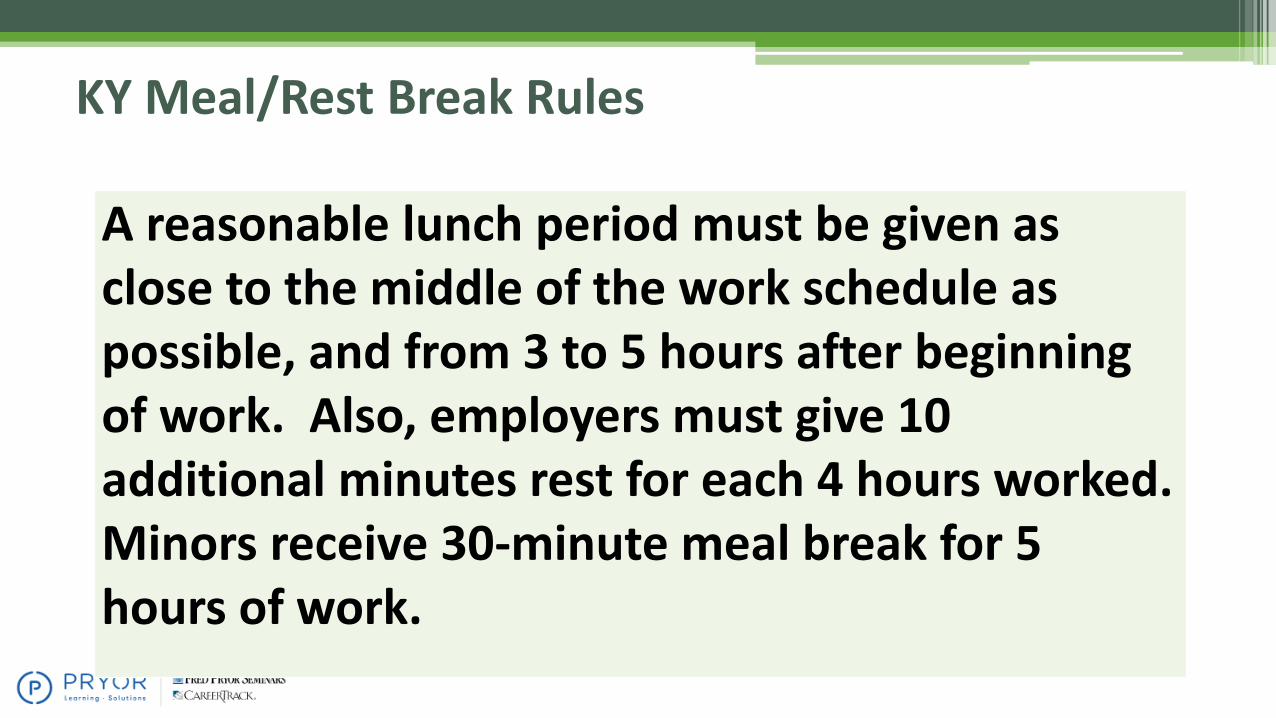

A reasonable lunch period must be given as close to the middle of the work schedule as possible, and from 3 to 5 hours after beginning of work. Also, employers must give 10 additional minutes rest for each 4 hours worked. Minors receive 30-minute meal break for 5 hours of work.

KY Meal/Rest Break Rules

Federal Meal/Rest Break Rules

• If the employee is offered a meal break –they must have 30 minutes uninterrupted as unpaid. If they get interrupted during the 30 minutes, they must be paid for the whole 30 minutes.

• If the employee is offered a rest break –all rest breaks of 20 minutes or less must be paid rest breaks

WB 42

Lectures, Meetings and Training Programs WB 42

•Not counted as working time (must meet all four requirements)1. Attendance is outside the employee’s regular working hours

2. Attendance is voluntary

3. The course, lecture or meeting is not directly related to the employee’s current job.

4. The employee does not perform any productive work during such attendance.

Comp Time for Non-Exempt Employees

• Private entities – not allowed in California▫ Same week it’s worked, or▫ Same pay period at time and a half

• Public entities▫ Up to 240 hours for non-emergency personnel▫ Up to 480 hours for emergency personnel▫ Must be banked at time and a half▫ No “use it or lose it” policy allowed

WB 43

Military Pay Page 46

• Supplemental Military Pay▫Compensation paid to employees while on military duty that represents the difference between employee’s regular pay and the pay provided by the state or federal government.

▫Temporary assignment – FITW, FICA, Medicare and unemployment taxes▫Indefinite assignment - 1099-MISC (over $600)

Module 5

Pages 48-57

Special Payroll Considerations and Hot Tips for Maintaining Compliance

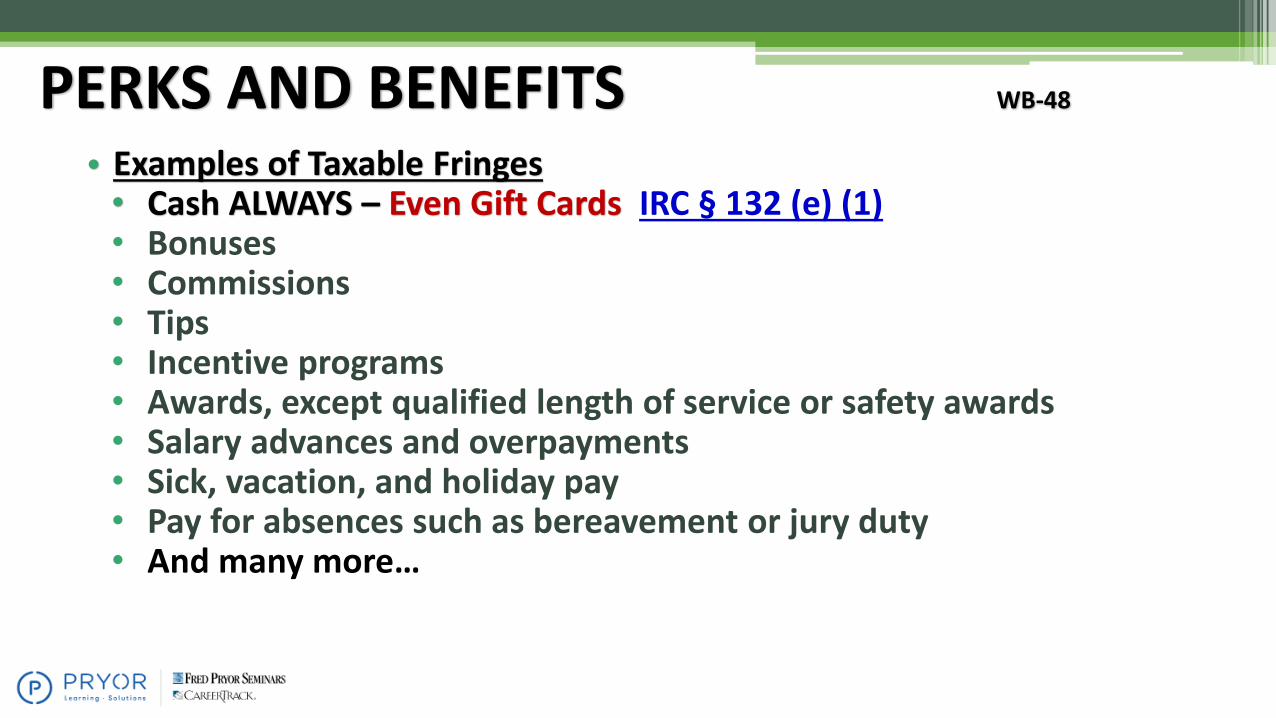

PERKS AND BENEFITS WB-48

• Examples of Taxable Fringes• Cash ALWAYS – Even Gift Cards IRC § 132 (e) (1)• Bonuses• Commissions• Tips• Incentive programs• Awards, except qualified length of service or safety awards• Salary advances and overpayments• Sick, vacation, and holiday pay• Pay for absences such as bereavement or jury duty• And many more…

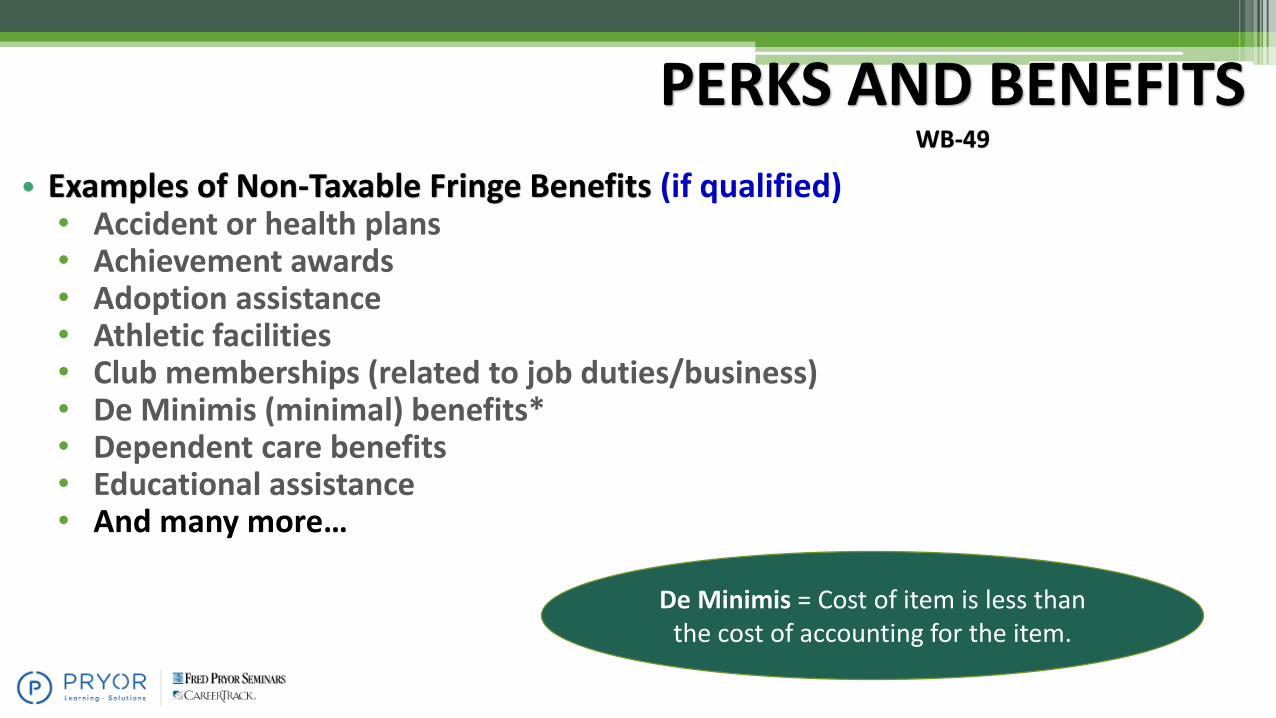

PERKS AND BENEFITSWB-49

• Examples of Non-Taxable Fringe Benefits (if qualified)• Accident or health plans• Achievement awards• Adoption assistance• Athletic facilities• Club memberships (related to job duties/business)• De Minimis (minimal) benefits*• Dependent care benefits• Educational assistance• And many more…

De Minimis = Cost of item is less than the cost of accounting for the item.

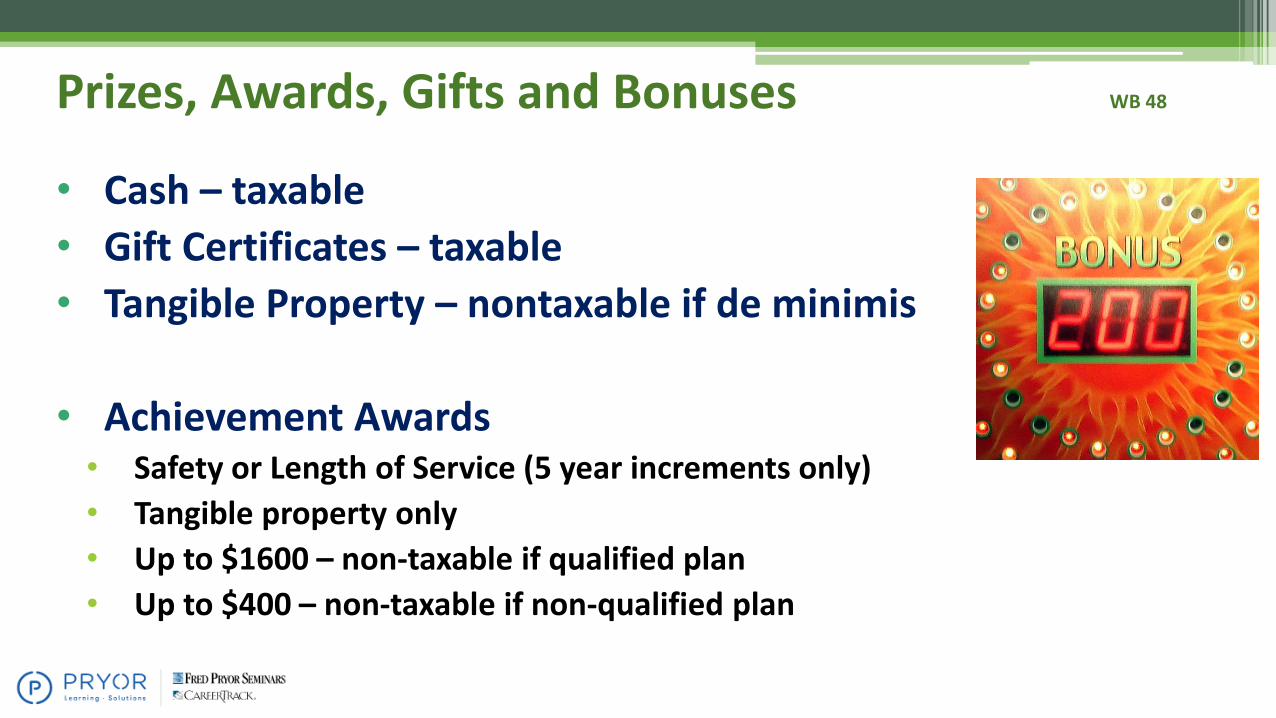

Prizes, Awards, Gifts and Bonuses WB 48

• Cash – taxable

• Gift Certificates – taxable

• Tangible Property – nontaxable if de minimis

• Achievement Awards• Safety or Length of Service (5 year increments only)

• Tangible property only

• Up to $1600 – non-taxable if qualified plan

• Up to $400 – non-taxable if non-qualified plan

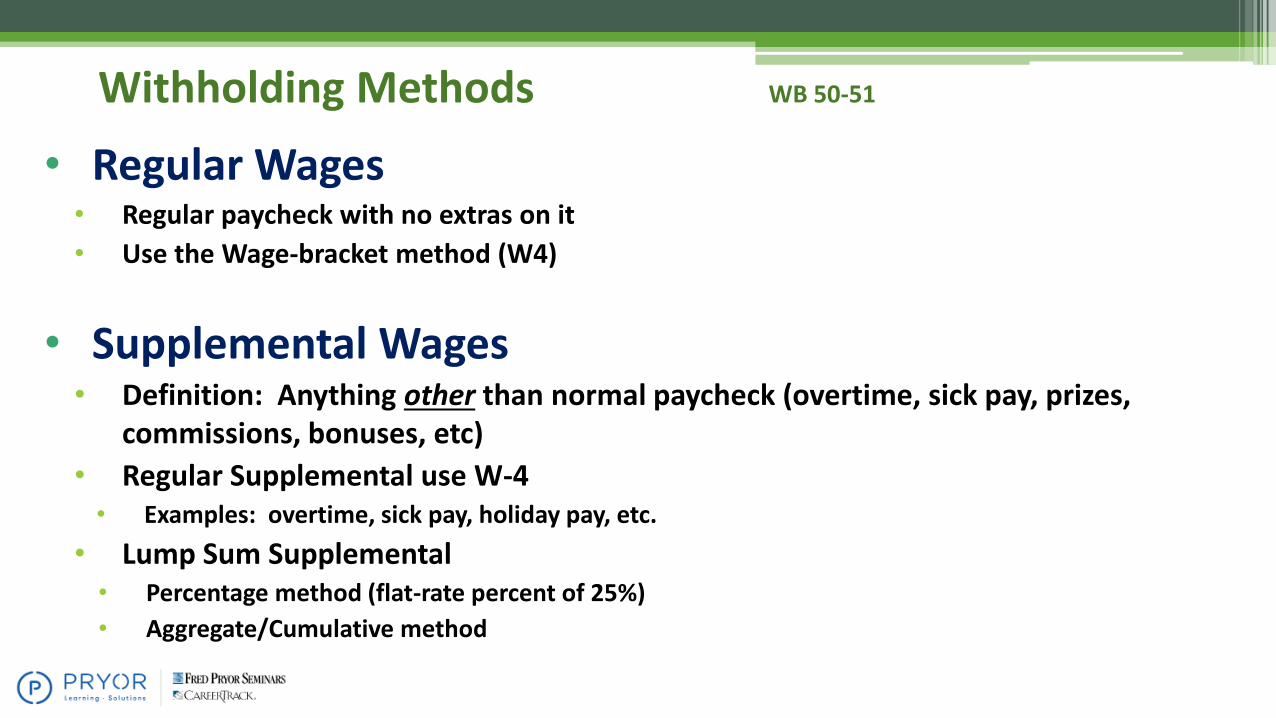

Withholding Methods WB 50-51

• Regular Wages• Regular paycheck with no extras on it

• Use the Wage-bracket method (W4)

• Supplemental Wages• Definition: Anything other than normal paycheck (overtime, sick pay, prizes,

commissions, bonuses, etc)

• Regular Supplemental use W-4• Examples: overtime, sick pay, holiday pay, etc.

• Lump Sum Supplemental• Percentage method (flat-rate percent of 25%)

• Aggregate/Cumulative method

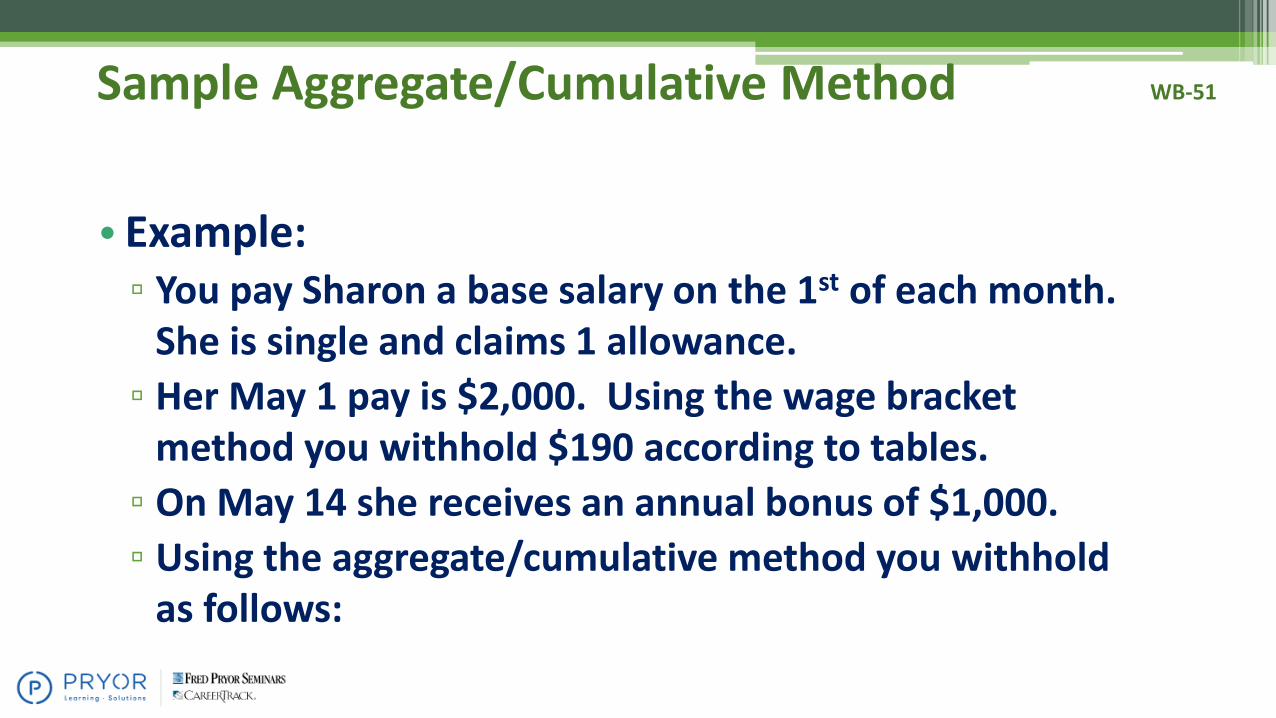

Sample Aggregate/Cumulative Method WB-51

• Example:▫ You pay Sharon a base salary on the 1st of each month.

She is single and claims 1 allowance.

▫ Her May 1 pay is $2,000. Using the wage bracket method you withhold $190 according to tables.

▫ On May 14 she receives an annual bonus of $1,000.

▫ Using the aggregate/cumulative method you withhold as follows:

Sample Aggregate/Cumulative Method WB-51

• Example: (continued)1. Add the bonus amount to the amount of wages from

the most recent base salary pay date ($2,000 + $1,000 = $3,000)

2. Determine the amount of withholding on the combined $3,000 using the wage bracket tables ($340.00)

3. Subtract the amount withheld from wages on the most recent base salary pay date ($340 - $190 = $150)

4. Withhold $150 from bonus payment

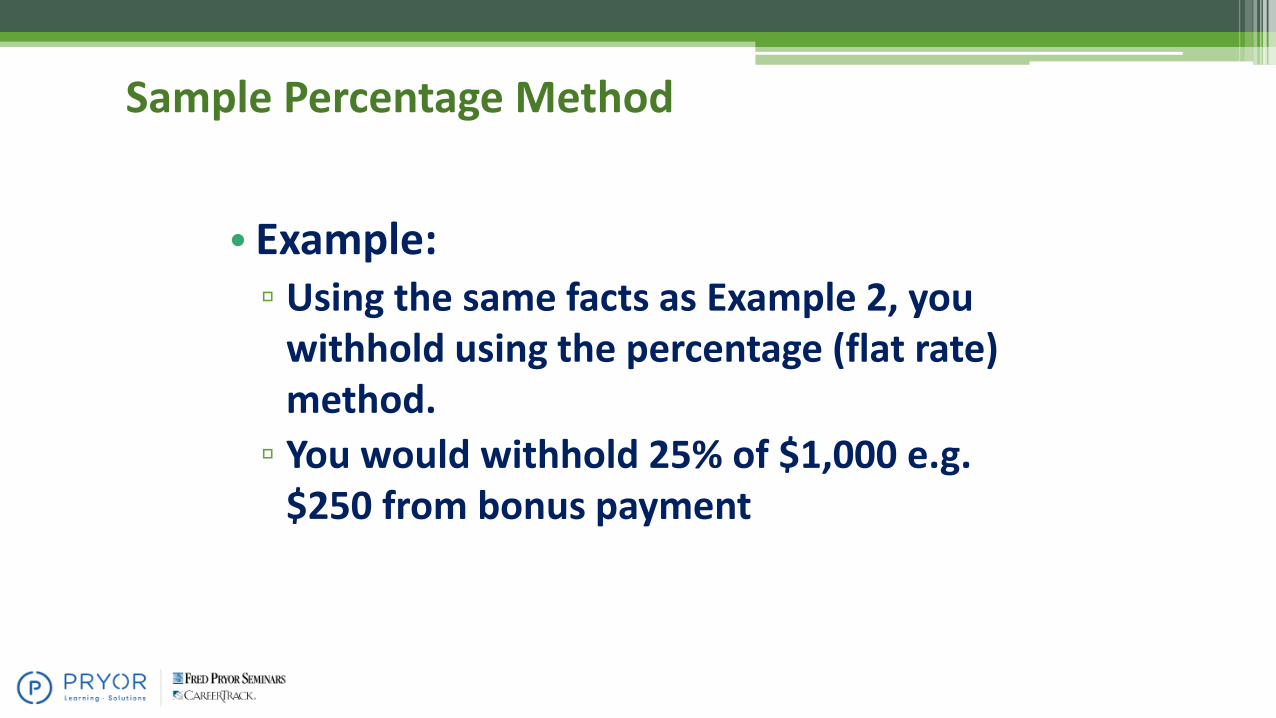

Sample Percentage Method

• Example:▫ Using the same facts as Example 2, you

withhold using the percentage (flat rate) method.

▫ You would withhold 25% of $1,000 e.g. $250 from bonus payment

Gross Up Example

•Net pay is $500

• Federal flat rate 25%

• State flat rate 4.25% (example only)

• FICA and Medicare 6.2% + 1.45% = 7.65%

• 100 – 25 – 4.25 – 7.65 = 63.10%

• $500 / 63.10% = $792.39

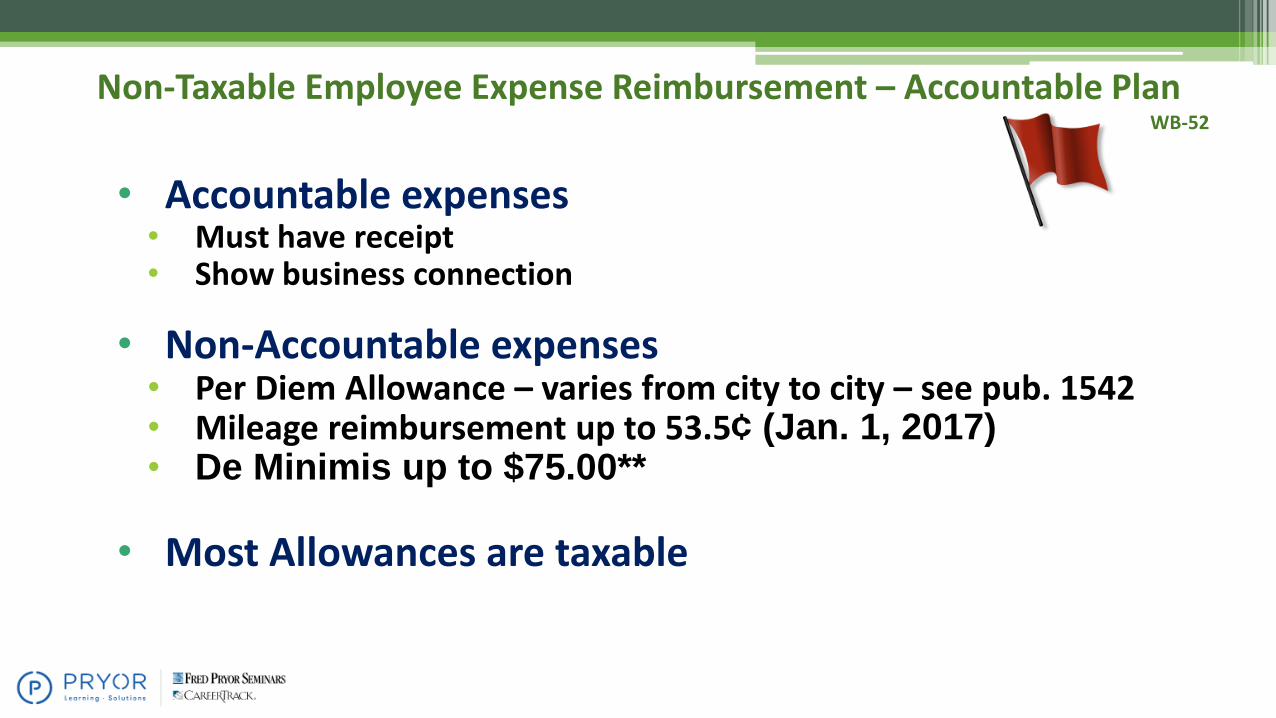

Non-Taxable Employee Expense Reimbursement – Accountable PlanWB-52

• Accountable expenses• Must have receipt• Show business connection

• Non-Accountable expenses• Per Diem Allowance – varies from city to city – see pub. 1542• Mileage reimbursement up to 53.5¢ (Jan. 1, 2017) • De Minimis up to $75.00**

• Most Allowances are taxable

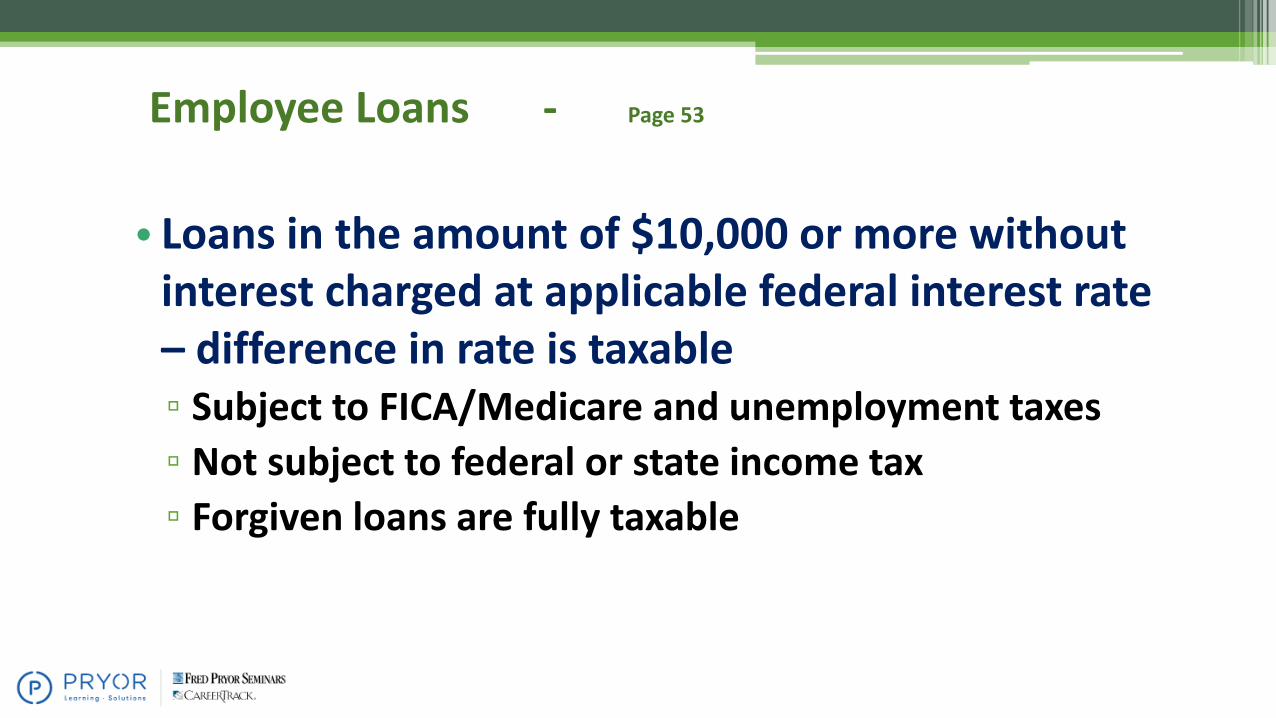

Employee Loans - Page 53

• Loans in the amount of $10,000 or more without interest charged at applicable federal interest rate – difference in rate is taxable▫ Subject to FICA/Medicare and unemployment taxes

▫ Not subject to federal or state income tax

▫ Forgiven loans are fully taxable

Pages 54 - 56

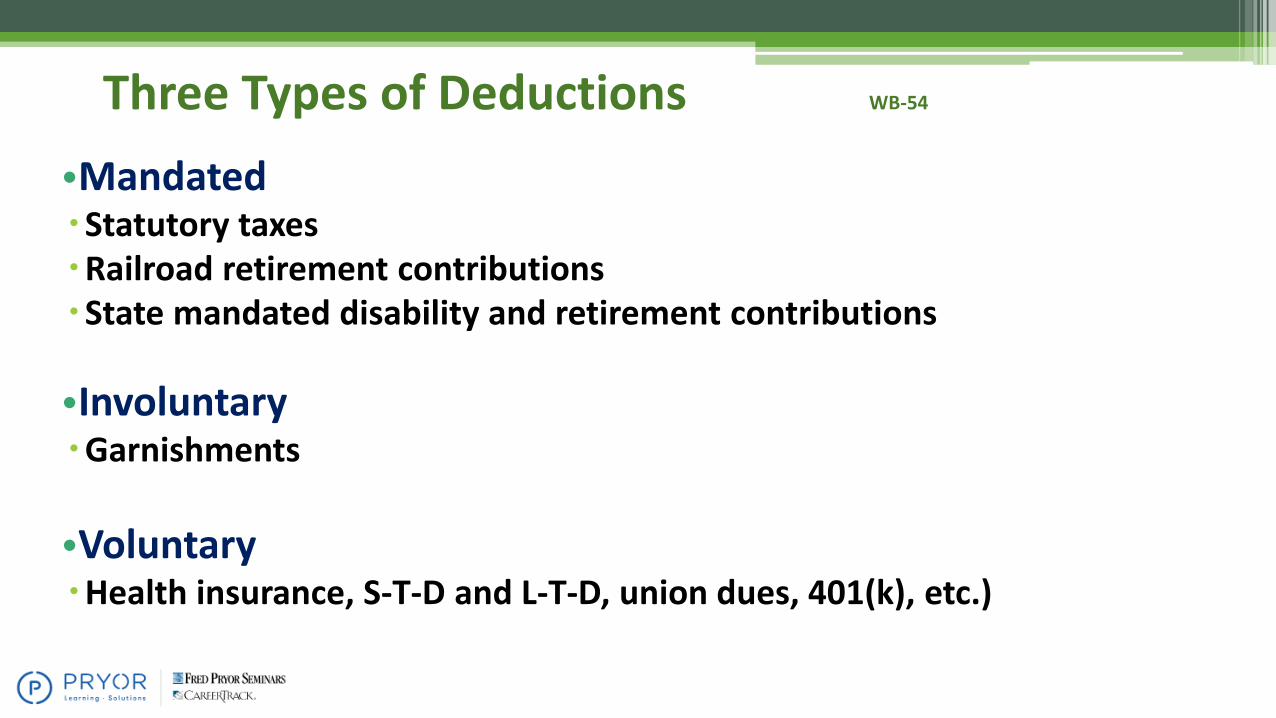

Three Types of Deductions WB-54

•MandatedStatutory taxesRailroad retirement contributionsState mandated disability and retirement contributions

•InvoluntaryGarnishments

•VoluntaryHealth insurance, S-T-D and L-T-D, union dues, 401(k), etc.)

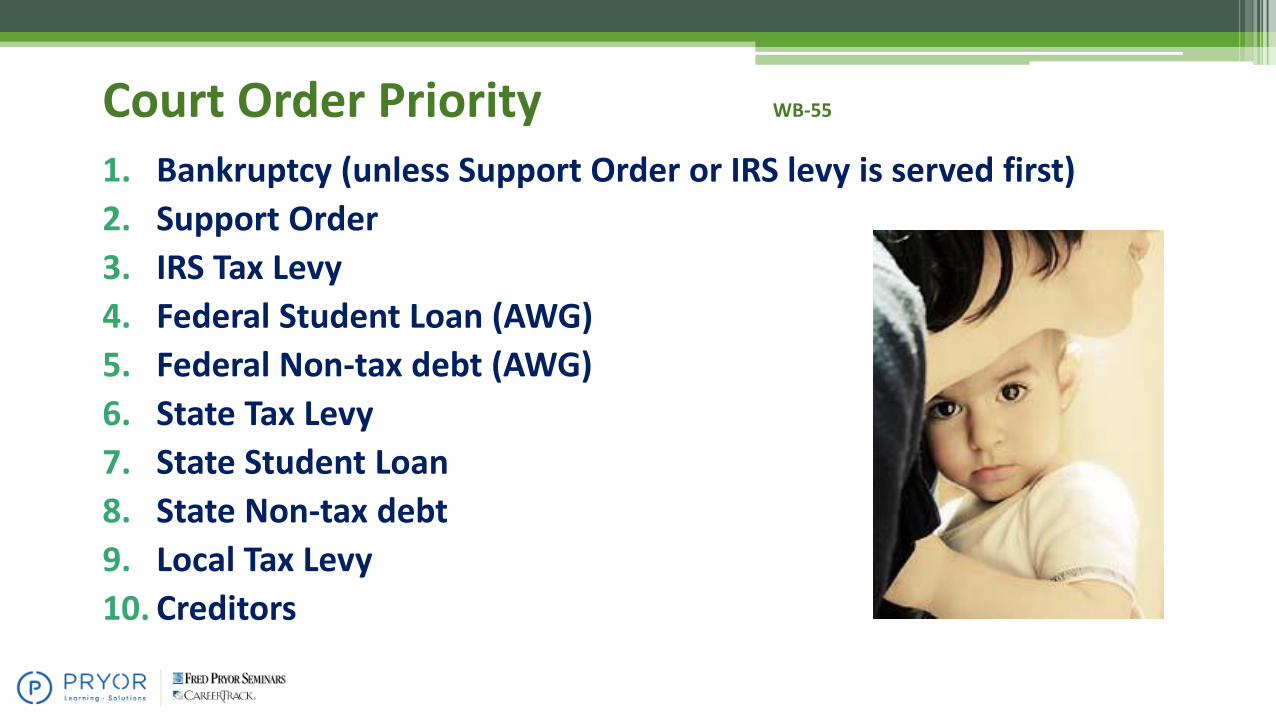

Court Order Priority WB-55

1. Bankruptcy (unless Support Order or IRS levy is served first)

2. Support Order

3. IRS Tax Levy

4. Federal Student Loan (AWG)

5. Federal Non-tax debt (AWG)

6. State Tax Levy

7. State Student Loan

8. State Non-tax debt

9. Local Tax Levy

10. Creditors

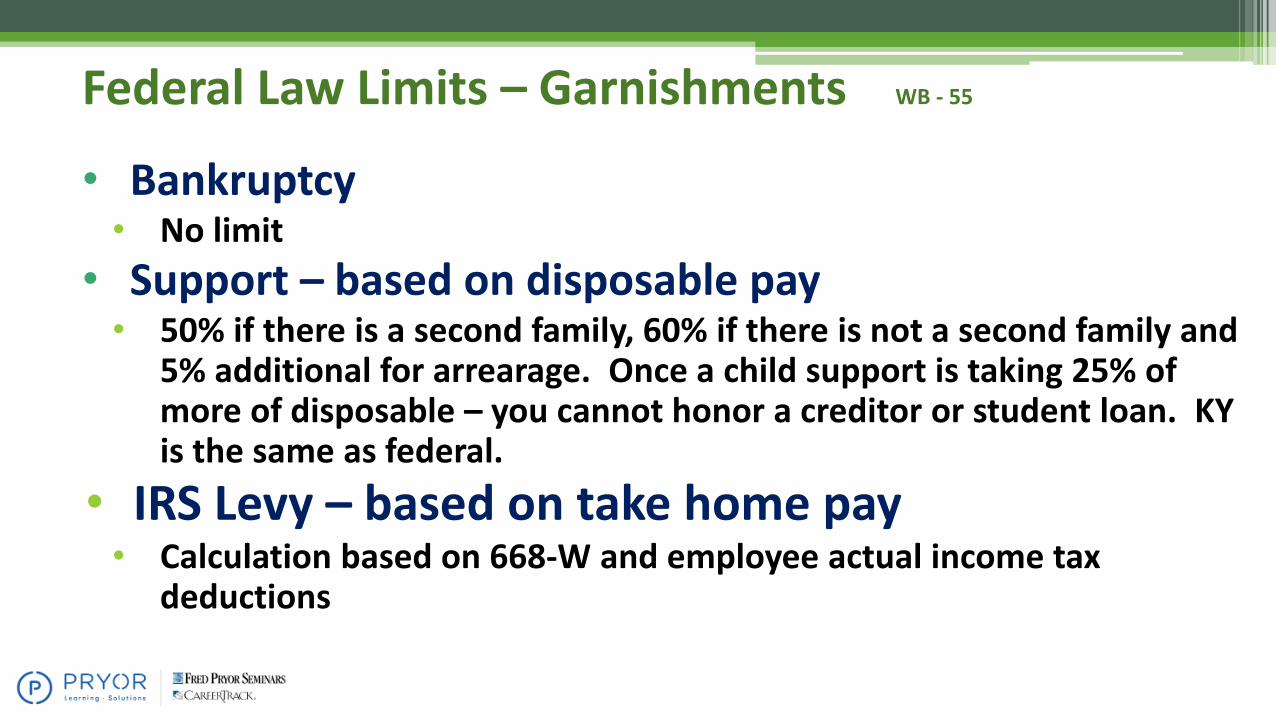

Federal Law Limits – Garnishments WB - 55

• Bankruptcy• No limit

• Support – based on disposable pay• 50% if there is a second family, 60% if there is not a second family and

5% additional for arrearage. Once a child support is taking 25% of more of disposable – you cannot honor a creditor or student loan. KY is the same as federal.

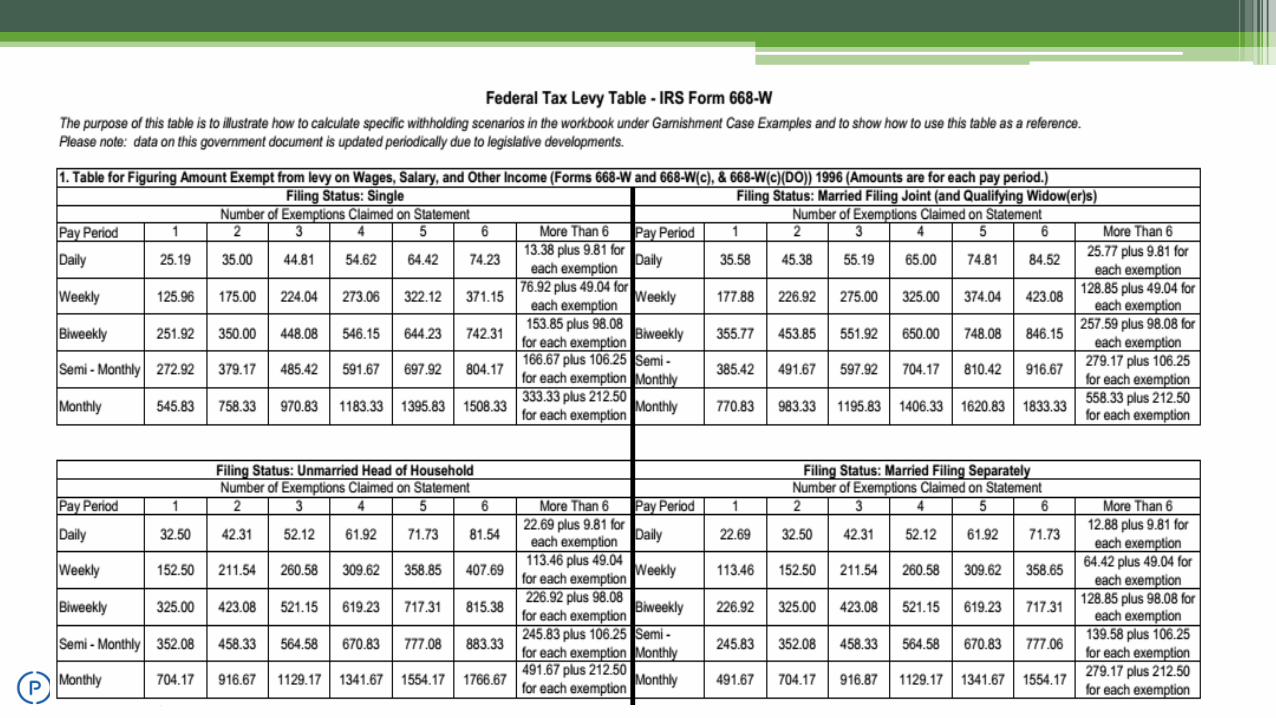

• IRS Levy – based on take home pay• Calculation based on 668-W and employee actual income tax

deductions

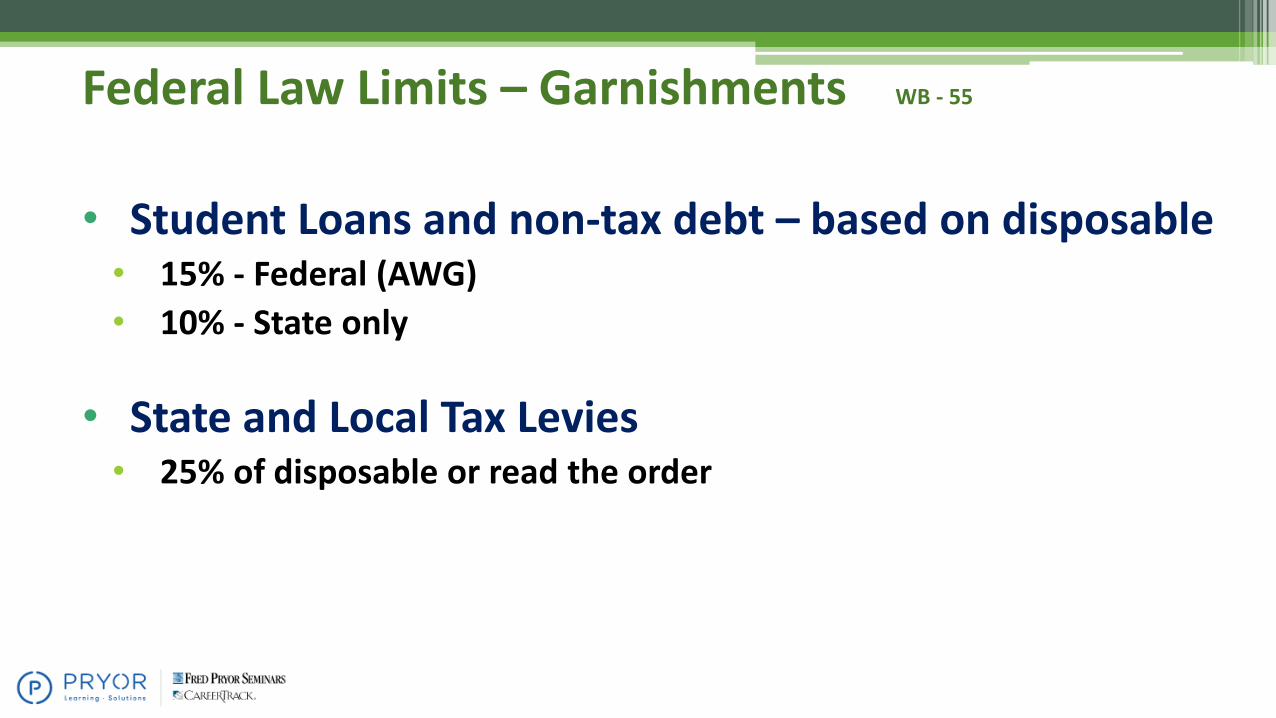

• Student Loans and non-tax debt – based on disposable• 15% - Federal (AWG)

• 10% - State only

• State and Local Tax Levies• 25% of disposable or read the order

Federal Law Limits – Garnishments WB - 55

•Creditor▫ 25% of disposable or 30 times federal minimum wage from

disposable (as of 7/24/09 = $217.50 per week) KY is the same as federal.

Federal Law Limits – Garnishments

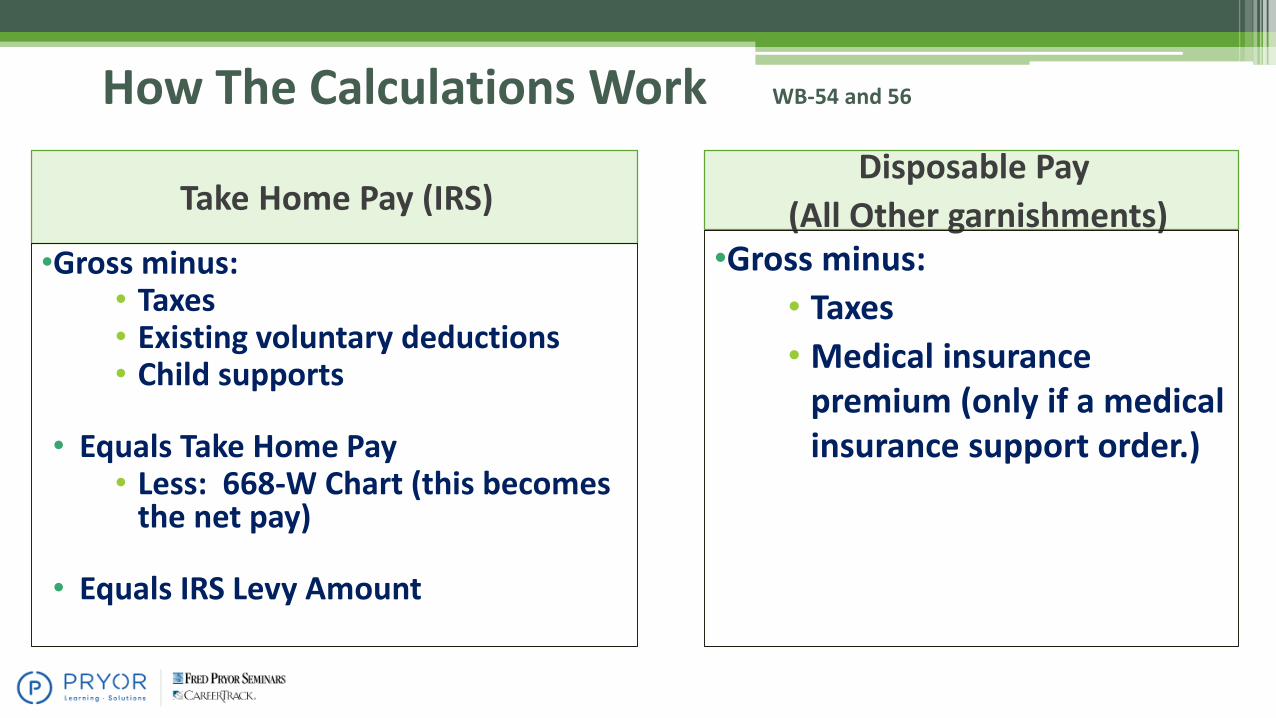

How The Calculations Work WB-54 and 56

Take Home Pay (IRS)

•Gross minus:• Taxes• Existing voluntary deductions• Child supports

• Equals Take Home Pay• Less: 668-W Chart (this becomes

the net pay)

• Equals IRS Levy Amount

Disposable Pay

(All Other garnishments)•Gross minus:

• Taxes

• Medical insurance premium (only if a medical insurance support order.)

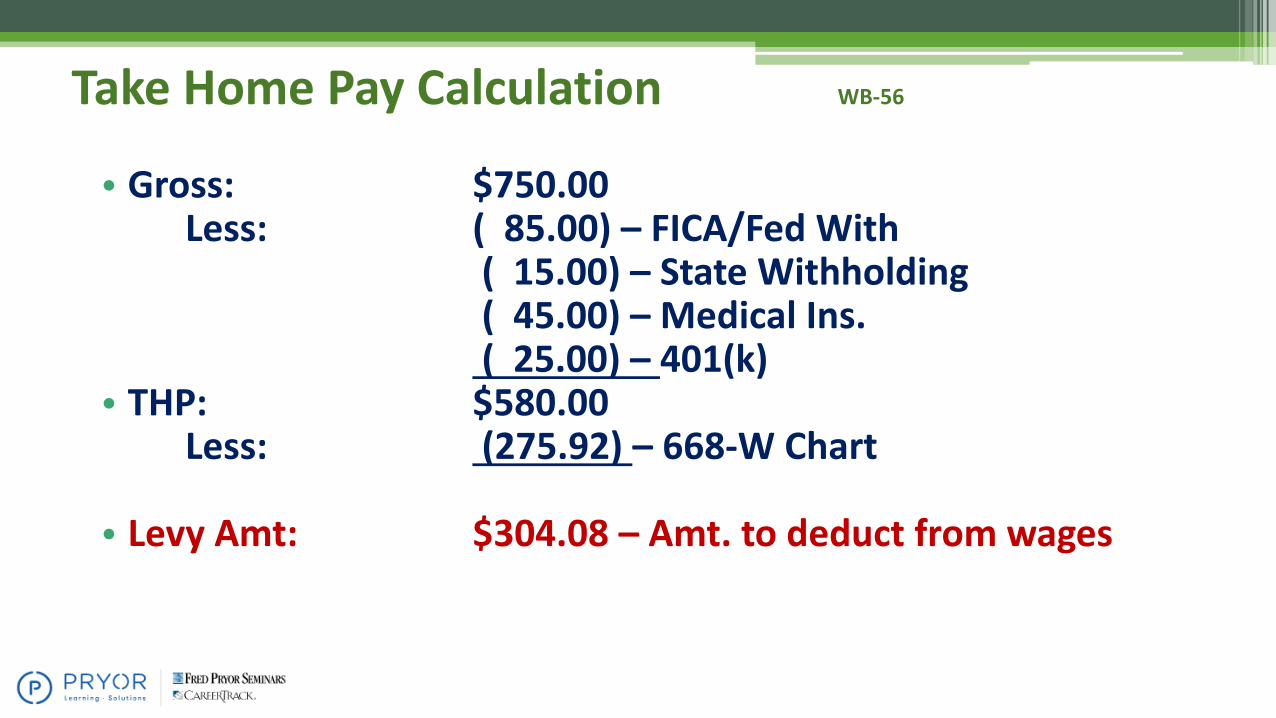

Take Home Pay Calculation WB-56

• Gross: $750.00Less: ( 85.00) – FICA/Fed With

( 15.00) – State Withholding( 45.00) – Medical Ins.( 25.00) – 401(k)

• THP: $580.00Less: (275.92) – 668-W Chart

• Levy Amt: $304.08 – Amt. to deduct from wages

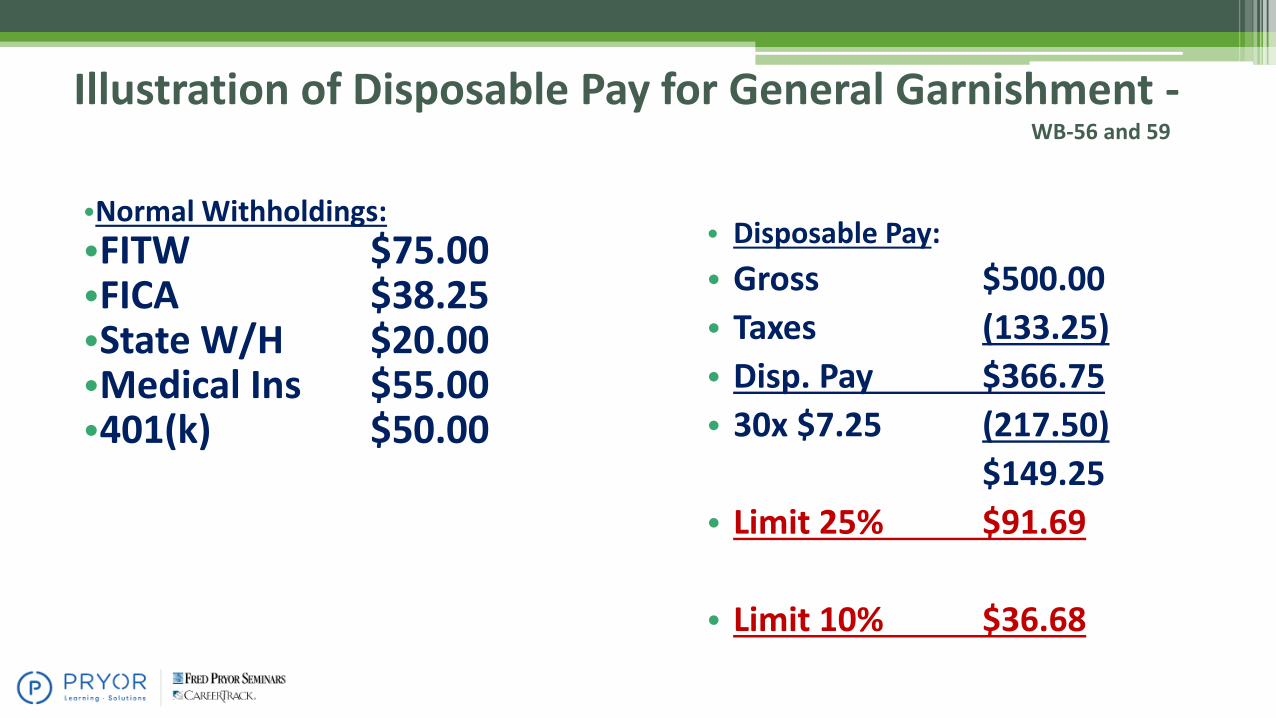

• Disposable Pay:

• Gross $500.00

• Taxes (133.25)

• Disp. Pay $366.75

• 30x $7.25 (217.50)

$149.25

• Limit 25% $91.69

• Limit 10% $36.68

Illustration of Disposable Pay for General Garnishment -WB-56 and 59

•Normal Withholdings:

•FITW $75.00•FICA $38.25•State W/H $20.00•Medical Ins $55.00•401(k) $50.00

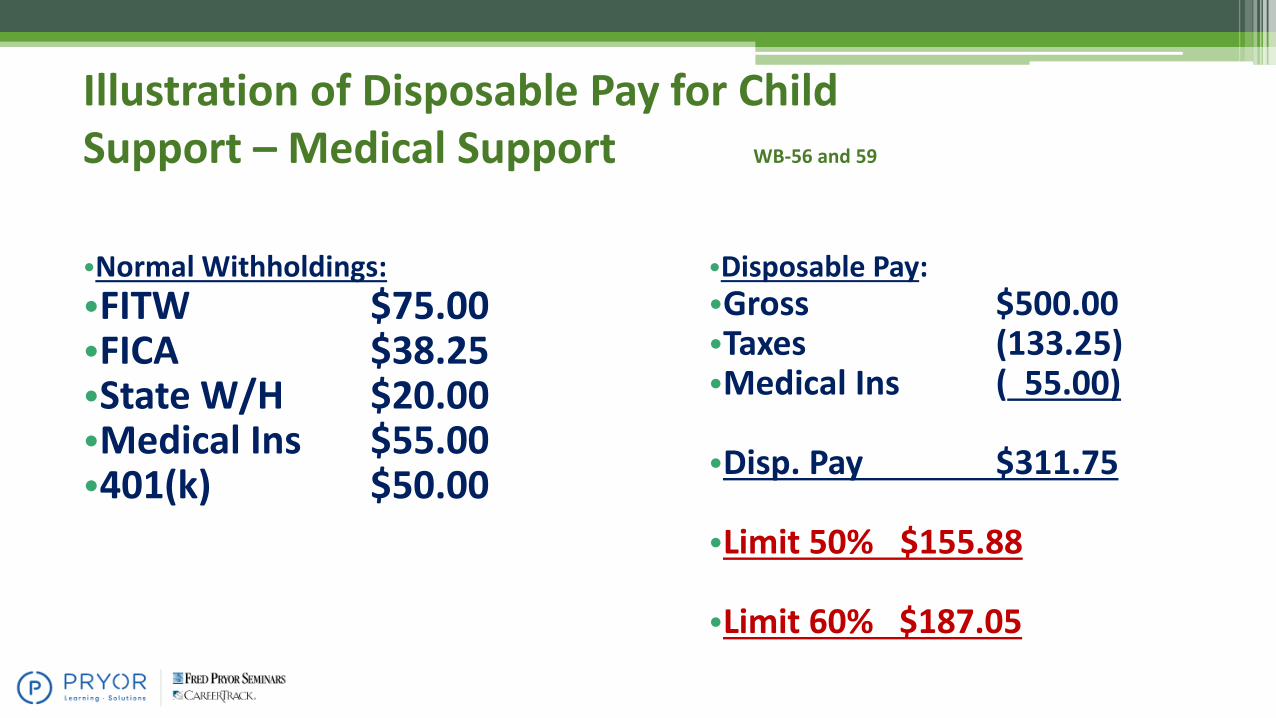

Illustration of Disposable Pay for Child Support – Medical Support WB-56 and 59

•Normal Withholdings:

•FITW $75.00•FICA $38.25•State W/H $20.00•Medical Ins $55.00•401(k) $50.00

•Disposable Pay:•Gross $500.00•Taxes (133.25)•Medical Ins ( 55.00)

•Disp. Pay $311.75

•Limit 50% $155.88

•Limit 60% $187.05

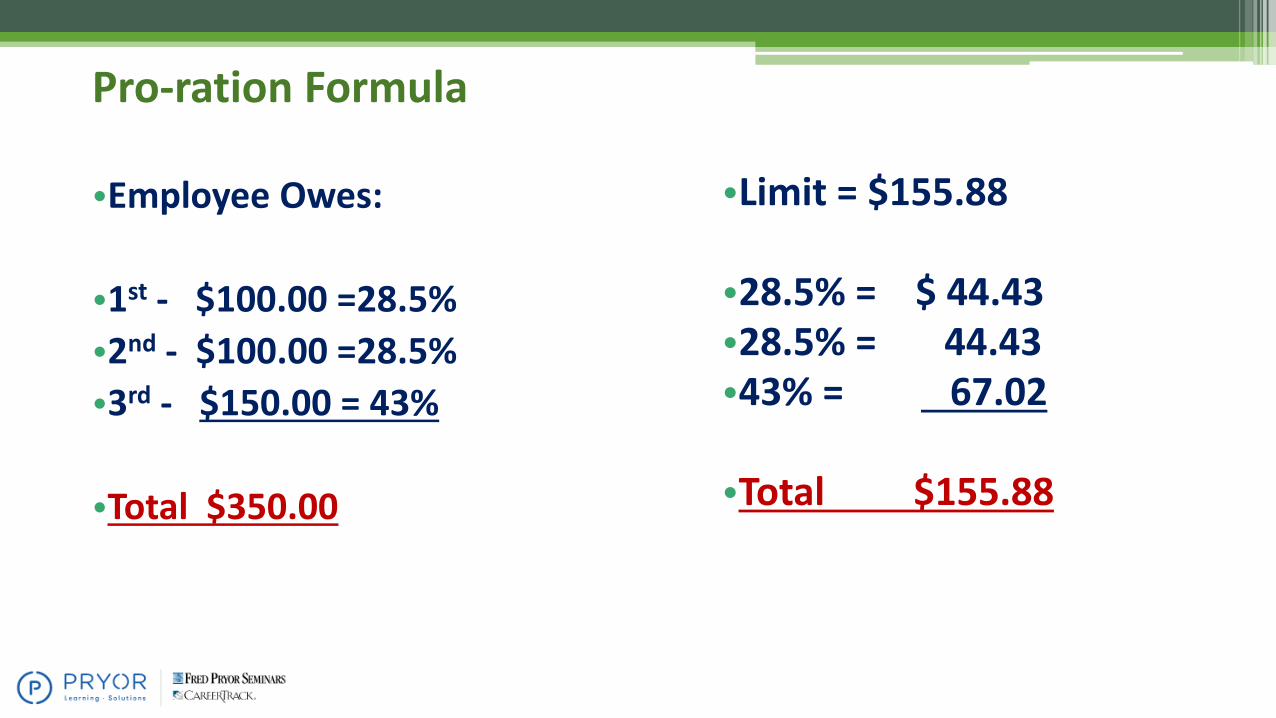

•Employee Owes:

•1st - $100.00 =28.5%

•2nd - $100.00 =28.5%

•3rd - $150.00 = 43%

•Total $350.00

•Limit = $155.88

•28.5% = $ 44.43•28.5% = 44.43•43% = 67.02

•Total $155.88

Pro-ration Formula

•Employee Owes:

•1st - $100.00 =28.5%

•2nd - $100.00 =28.5%

•3rd - $150.00 = 43%

•Total $350.00

•Limit = $171.46

•28.5% = $ 48.87•28.5% = 48.87•43% = 73.72

•Total $171.46

Pro-ration Formula – with arrearage

Seminar Disclaimer

This seminar is from an auditor’s point of view. It is possible your

company attorney may disagree with our interpretation. That is

okay. It does not mean we are right or that we have given you

wrong information. You may have an exception to the rule that

your attorney knows about.

IRS CIRCULAR 230

Any tax advice included in this written or electronic communication was not intended or written to be used, and it

cannot be used by the taxpayer, for the purpose of avoiding any penalties that may be imposed on the taxpayer by any

governmental taxing authority or agency.