Payroll Law Canada

56

NAME EVENT NUMBER / DATE 800-556-2998 pryor.com SEMINAR WORKBOOK Payroll Law Canada DISCLAIMER: The principles and suggestions in this workbook and seminar are presented to apply to diverse personal and company situations. These materials and the overall seminar are for general informational and educational purposes only. The materials and seminar, in general, are presented with the understanding that Pryor Learning, Inc. is not engaged in rendering legal advice. Employers with significant legal issues and questions about payroll law in Canada should consult an attorney. ©2020, 2018, 2017, 2015, 2013, 2011 Pryor Learning, Inc. Registered U.S. Patent & Trademark Office and Canadian Trade-Marks office. Except for the inclusion of brief quotations in a review, no part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording or by any information storage and retrieval system, without permission in writing from Pryor Learning, Inc.

Transcript of Payroll Law Canada

N A M E

E V E N T N U M B E R / D A T E

800-556-2998

pryor.com

SEMINAR WORKBOOK

Payroll LawCanada

DISCLAIMER: The principles and suggestions in this workbook and seminar are presented to apply to diverse personal and company situations. These materials and the overall seminar are for general informational and educational purposes only. The materials and seminar, in general, are presented with the understanding that Pryor Learning, Inc. is not engaged in rendering legal advice. Employers with significant legal issues and questions about payroll law in Canada should consult an attorney.

©2020, 2018, 2017, 2015, 2013, 2011 Pryor Learning, Inc. Registered U.S. Patent & Trademark Office and Canadian Trade-Marks office. Except for the inclusion of brief quotations in a review, no part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording or by any information storage and retrieval system, without permission in writing from Pryor Learning, Inc.

©Pryor Learning, Inc. • WYP2004ES-DL ii

Seminar Goals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Prepare to Meet the Challenge Strengthen Your Payroll Compliance Program with Three Steps . . . . . . . . . . . . . . . . . . . . 2 Five Specific “No Math” Audits Every Payroll Department Should Conduct . . . . . . . . . . 5 Employment Labour Standards Complaints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Canadian Payroll Basics Employee/Employer Relationships . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Record Retention Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Filing Forms TD1 and Québec TP1015 .3-V - Who Should File . . . . . . . . . . . . . . . . . . . . . . . 9 Determine Worker Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Contract of Service vs . Contract for Service . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Minimum Wage Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 Hours of Work Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Employment and Labour Standards that Affect Payroll Processing Statutory Holidays . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 Standards for Pregnancy, Maternity and Parental Leaves . . . . . . . . . . . . . . . . . . . . . . . . . 19 Sick, Vacation Leave and Pay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 Termination Pay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Withholdings: Taxable vs. Nontaxable, Garnishments Deductions from Pay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Employment Insurance Premiums . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Federal and Provincial Income Tax Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Employer Share of Statutory Deductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 Special Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 Garnishments Basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Special Payroll Concerns Handling Final Pay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 US Source Income for Canadian Companies Located in the United States . . . . . . . . . . 33

Appendix Vacation Pay Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Deductions from Pay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 Benefits and Allowances Chart . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 Garnishment and Maintenance Orders by Province . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47 How Would You Handle These Situations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 Tax Forms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Table of Contents

©Pryor Learning, Inc. • WYP2004ES-DL 1

Once you have completed the Payroll Law Canada seminar, you will understand fundamental payroll professional’s responsibilities in the modern workplace and your role within that function. You will gain these skills through the seminar presentation and materials.

Performance Objectives

The legal principles and examples and scenarios presented and applied in this seminar will help you:

• Understand the basics of major federal laws and provincial laws regarding tax withholding and reporting

• Comprehend basic labour and employment standards that affect payroll processing

• Undertake payroll document record retention

• Audit-proof your documentation

• Know the steps for special situations that can incur penalties, interest and fines

• Apply critical, need-to-know legal mandates that help you protect your organization

Your Objectives:

Seminar Goals

©Pryor Learning, Inc. • WYP2004ES-DL2

Prepare to Meet the Challenge

Strengthen Your Payroll Compliance Program with Three Steps

Step #1Understand the realities, rules and risks. Tighten compliance and minimize liabilities.

Reality: 99% of the employers in Canada are paying their employees incorrectly.

Rules: Laws exist and most of them are confusing. Laws overlap, however, what Payroll does with the laws may not coincide with what Human Resources does with them. Therefore: confusion.

Risk: Each mistake made costs employers’ money. Understanding taxable vs. nontaxable benefits; when an employee is “on the clock when it’s not that easy to tell”; over or under withholding on a garnishment - All of these mistakes cost the employers penalties, fines, back taxes, back pay, paying an employee’s garnishment for them, paying someone as a contractor when they should have been an employee, etc.

One agency may signal another, and an employer may be subject to multiple audits.

©Pryor Learning, Inc. • WYP2004ES-DL 3

Step #2

Understand the top three questions your auditor will ask in order to establish your “good faith” efforts.

1. Can you show a reasonable basis for your actions?

How do you obtain the guidance which defines your policies and procedures?

Reasonable basis may be proven by:

• Showing reliance on a court ruling, CRA ruling, Provincial ruling, or CRA technical advice

• CRA or other agency previously audited your business and found no issue with the practice in question

• A significant segment of your industry customarily has this practice

• Showing reliance on some other reasonable basis, e.g., your attorney or CPA advised you in writing

2. Can you demonstrate substantive consistency?

Are you able to produce something meaningful and firm that proves your consistent efforts to obey the law? Substantive consistency may be demonstrated through:

• Written employee handbooks

• Standard operating policies and procedures

• Compliant job descriptions

• Training records that show you have consistently made every attempt to train your employees to obey the law

3. Can you prove recordkeeping and reporting consistency?

Have you filed all reports / returns on time and correctly?

Records and Reports may include:

• Filing of ROEs

• T4s

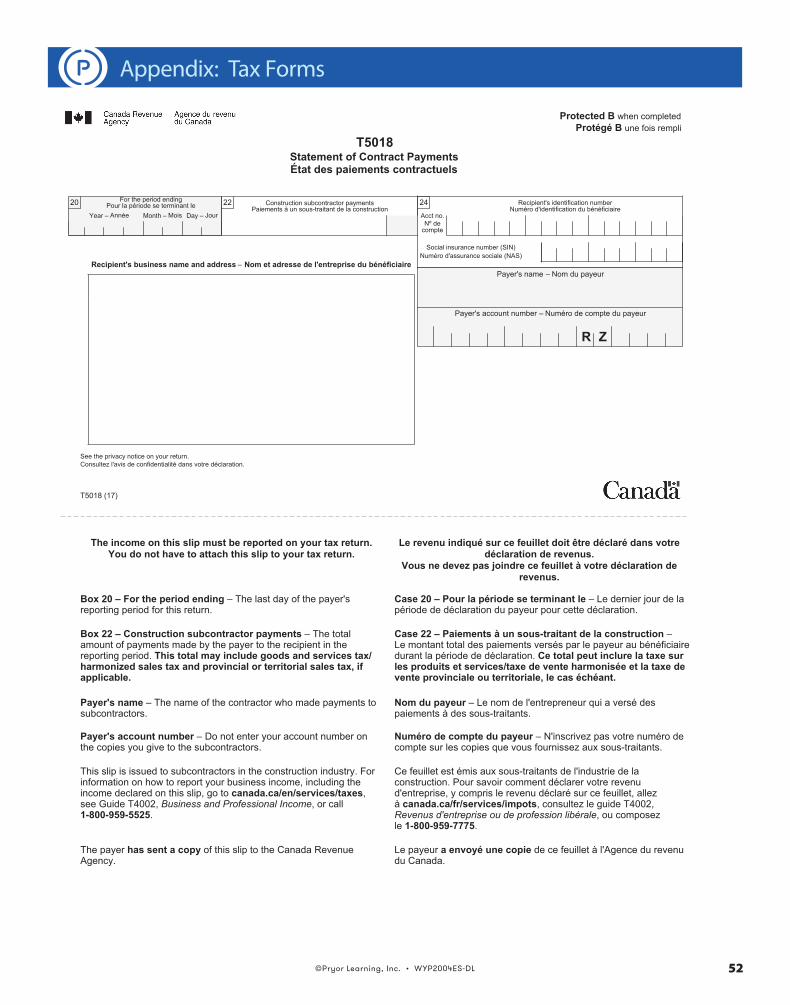

• T4As, T5018, T2200 (where applicable)

• CPP and EI premium remittances

• TD1 (and Provincial equivalent where applicable)

• Garnishment records

Prepare to Meet the Challenge

©Pryor Learning, Inc. • WYP2004ES-DL4

Step #3Internally audit and correct errors before the auditor, inspector, investigator or litigator gets there.

Audit Ready Checklist

1. Reasonable Basis• Professional Resources, Government Resources, Desk References

• Consultant/Attorney advice in writing

2. Payroll Standard Operating Procedures

• Step-by-step guidance for each position

• Follow the rule of three or more sources and reference your reasonable basis

• Must contain update and revision dates, and employee training dates

3. Internal Audit Documentation

• Annual audit documentation for each area

• Must include corrective action plans and outcomes

4. Employee Handbook – Policies/Procedures

• Must reflect federal and/or provincial laws

• Must include specific company policies when law is silent

• Must include documentation of review and updates annually

5. Job Descriptions

• Not optional – review annually

• Must detail essential functions and BFOQs and overtime-exempt qualifiers

• Must be accompanied by interview checklists for non-discrimination compliance

6. Training

• Initial and annual training

• Compliance and incentive

• Show your efforts to educate workers, and obey the law

Prepare to Meet the Challenge

©Pryor Learning, Inc. • WYP2004ES-DL 5

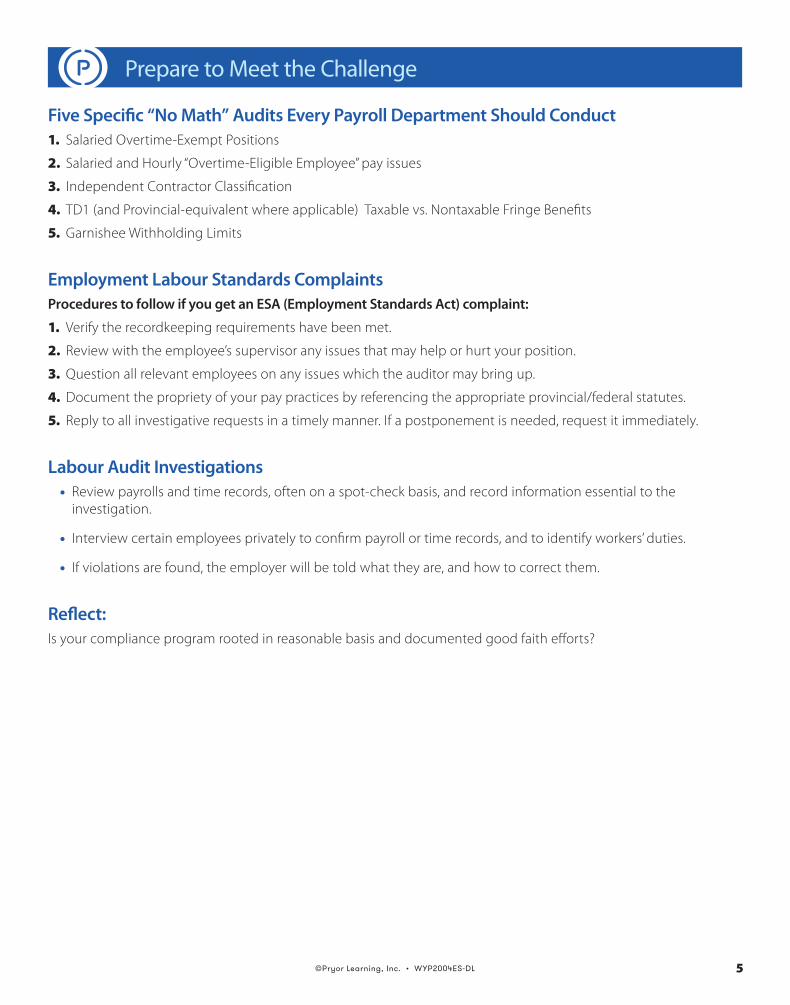

Five Specific “No Math” Audits Every Payroll Department Should Conduct1. Salaried Overtime-Exempt Positions

2. Salaried and Hourly “Overtime-Eligible Employee” pay issues

3. Independent Contractor Classification

4. TD1 (and Provincial-equivalent where applicable) Taxable vs. Nontaxable Fringe Benefits

5. Garnishee Withholding Limits

Employment Labour Standards ComplaintsProcedures to follow if you get an ESA (Employment Standards Act) complaint:

1. Verify the recordkeeping requirements have been met.

2. Review with the employee’s supervisor any issues that may help or hurt your position.

3. Question all relevant employees on any issues which the auditor may bring up.

4. Document the propriety of your pay practices by referencing the appropriate provincial/federal statutes.

5. Reply to all investigative requests in a timely manner. If a postponement is needed, request it immediately.

Labour Audit Investigations• Review payrolls and time records, often on a spot-check basis, and record information essential to the

investigation.

• Interview certain employees privately to confirm payroll or time records, and to identify workers’ duties.

• If violations are found, the employer will be told what they are, and how to correct them.

Reflect:Is your compliance program rooted in reasonable basis and documented good faith efforts?

Prepare to Meet the Challenge

©Pryor Learning, Inc. • WYP2004ES-DL6

What Every Payroll Processor Needs to Know to Get Started

Employer Responsibilities – The Six Payroll Steps

1. Determine your status

2. Opening a payroll account

3. Hiring employees

4. Calculating deductions

5. Remitting deductions

6. Completing and filing information returns

During all of this – you have to keep proper records.

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL 7

Record Retention Requirements

If you deduct Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, or income tax from remuneration or other amounts you pay, you must keep records of:

• the hours worked by each employee and;

• the CPP contributions, EI premiums, or taxes that you withheld.

You also have to keep the following documents:

• Form TD1, Personal Tax Credits Return, which all employees have to complete

• Form TP1015.3, Source Deductions Return, if your employees work in the province of Quebec. This form is available from Revenu Québec.

• Canada Revenue Agency letters of authority that let you reduce the tax deductions for certain employees for a specific year and;

• All information slips issued and all returns filed.

You must keep all these records so that we can verify or review them, on request.

Businesses that use service bureaus, payroll providers, or similar institutions to handle payroll functions are still responsible for keeping records for the time period specified, generally six years.

Payroll records can be kept in either paper or electronic format.

Recommendation: keep electronic copies of your records at your business location.

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL8

Record Retention Requirements

12-Requirements to Recordkeeping:

Your records, whether in paper or electronic format, have to:

• be reliable and complete

• provide correct information needed to assist in fulfilling tax obligations and calculate entitlements

• be supported by source documents to verify the information contained in the records;

• include other documents, such as appointment books, logbooks, income tax and GST/HST returns, scientific research and experimental development (SR&ED) vouchers and records, and certain accountants’ working papers, that assist in determining your obligations and entitlements

• include the general ledger or other books of final entry, in paper or electronic format, containing the summaries of the year-to-year transactions of the corporation

• show the time worked by each employee

• support the CPP contributions, EI premiums, and taxes that you withheld

You also have to keep the following records:

• Form TD1, Personal Tax Credits Return, which all employees have to complete; Form TD1 is used to determine the amount of federal and provincial or territorial tax to be deducted from an individual’s income or other income such as pension income

• If your employees work in the province of Quebec, they also have to complete Form TP1015.3-V, Source Deductions Return (available from Revenu Québec at www.revenu.gouv.qc.ca)

• CRA letters of authority that allow you to reduce the tax deductions for certain employees for a specific year

• all information slips issued and all returns filed; and

• registered pension information

You must keep all these payroll records so that CRA officials can audit or examine them, on request.

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL 9

Filing Forms TD1 and Québec TP1015.3-V – Who Should FileForm TD1

• Used to determine the amount of the employee tax deductions

• Employees must fill out before they receive their first remuneration from the employer

What Employees Need To Know About Their TD1

Who needs to file a TD1?

Individuals who:

• have a new employer or payer;

• want to change amounts from previous claimed;

• want to claim the deduction for living in a prescribed zone; or

• want to increase the amount of tax deducted at source;

• have to complete the federal TD1 and, if more than the basic personal amount is claimed, the provincial or territorial TD1.

Individuals do not have to complete a new TD1 every year unless there is a change to their federal, provincial or territorial personal tax credit amounts. If a change happens, they must complete a new form no later than seven days after the change.

Québec TP1015.3-V

• Used to determine the amount of the employee tax deductions

• Employees must fill out before they receive their first remuneration from the employer

Certification

• Employee signature and date is required

How long do you need to keep your records?

• As a general rule, you must keep all of the records and supporting documents that are required to determine your tax obligations and entitlements for a period of six years from the end of the last tax year to which they relate.

• The six-year retention period under the ITA begins at the end of the tax year to which the records relate.

• The rules are similar for GST/HST under the ETA, as well as for the EIA, the CPP, the EA 2001, and the ATSCA.

• Records and supporting documents concerning long-term acquisitions and disposal of property, the share registry, and other historical information that would have an impact upon sale or liquidation or wind-up of the business must be kept indefinitely .

Note: Copies of these forms are available at www.canada.ca

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL10

The Payroll Department or just the single individual within an organization handling payroll functions has to contend with a mind numbing number of issues, including but not limited to:

Determine Worker Status Canada’s Four-Point Test – Employee or Contractor

1. Control – Who’s running the ship?

• Employer’s right to hire or fire

• Employer determines salary or wage to be paid

• Employer decides time, place and manner in which the work is to be done

2. Ownership of Tools – Who supplies the tools, materials to perform the work?

• CRA (Canada Revenue Agency) says “when workers purchase or rent equipment or large tools that require a major investment and costly maintenance, it usually indicates that they are self-employed individuals, because they may incur losses when replacing or repairing their equipment.”

3. Chance of profit/risk of loss

• Does the worker have a chance of making a profit?

• Does the worker run the risk of incurring losses due to bad debts, damage to equipment or materials, or delays?

• Does the worker cover operating costs?

* If all three questions are true: Worker is a contractor

4. Integration into company

• If company is dependant on the work of the worker for the company to exist: Employee

• If worker provides services for many other companies: Contractor

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL 11

Contract of Service vs. Contract for Services • Contract of service indicates an employee relationship

• Contract for services indicates a business relationship

Determining Worker Status in Québec • Use three-step approach

• Step 1: Ask for intent – purpose worker is being used, contract of service vs. contract for service, etc.

• Step 2: Look to see if employment meets the definition in the Civil Code of Québec of a contract of employment or of a business contract

• Step 3: Confirm that the conditions of the working relationship meet the status that the parties have chosen and that they are consistent with the definitions of the Civil Code of Québec.

To Prove You are Doing It Right • Have written contracts with all contractors

• If contractor is incorporated – this helps prove they are a bona-fide business

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL12

Province General Wage More Employment Standards

Alberta Alberta Employment and Immigration

BC B.C. Ministry of Labour

Manitoba Manitoba Labour

New Brunswick New Brunswick Employment Standards

Newfoundland Labour Relations Agency

NWT

Nova Scotia Environment and Labour

Nunavut

Ontario Ministry of Labour

PEI Community Services, Seniors and Labour

Québec Commission des norms du travail

Saskatchewan Saskatchewan Labour

Yukon

Minimum Wage RulesAnother area payroll professionals must keep up with is the minimum requirement for paying employees. Minimum wage rules for Canada are based on province and territories as listed below:

Child Labour Laws

• Governed by province

• Definitions

• Adolescents – ages 12, 13 or 14 years old

• Young persons – ages 15 through 17

• Most provinces state that persons under 16 years old are required to attend school and may not be employed during normal school hours, unless they are enrolled in an off-campus educations program provided under the School Act.

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL 13

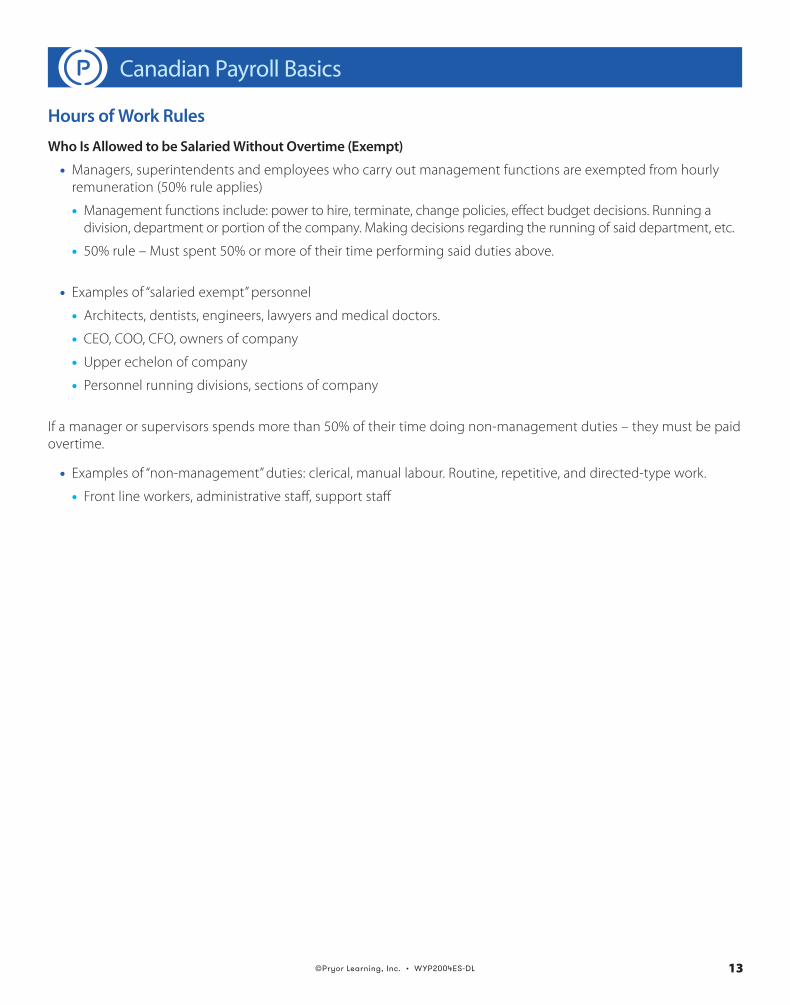

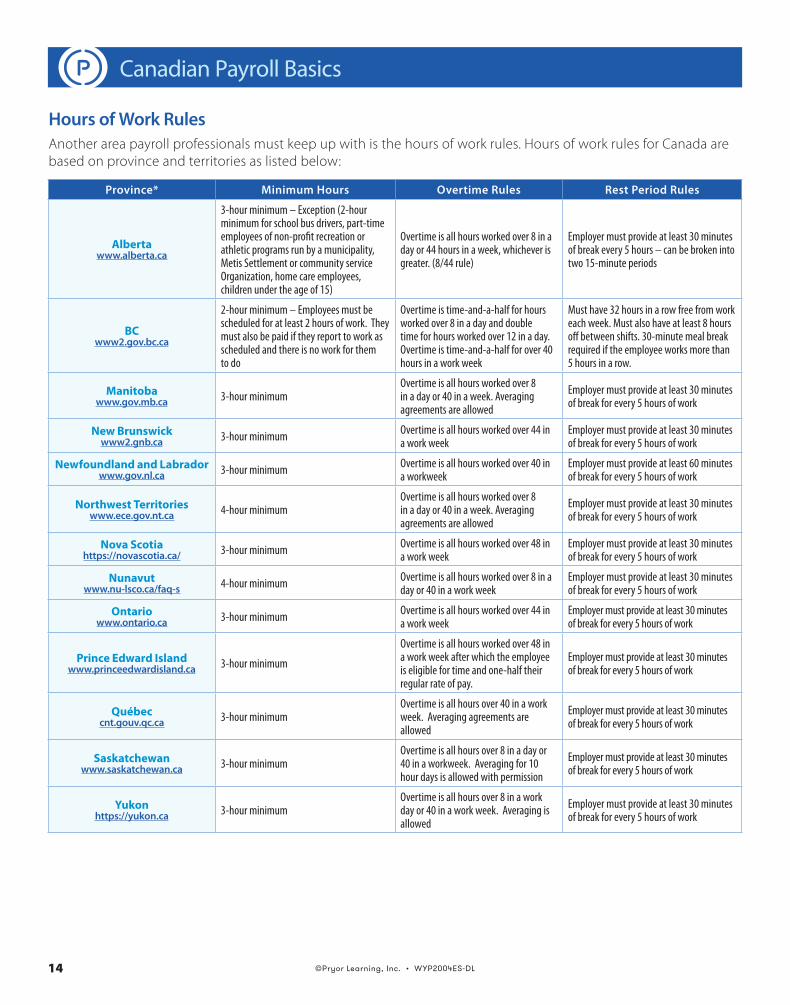

Hours of Work Rules

Who Is Allowed to be Salaried Without Overtime (Exempt)

• Managers, superintendents and employees who carry out management functions are exempted from hourly remuneration (50% rule applies)

• Management functions include: power to hire, terminate, change policies, effect budget decisions. Running a division, department or portion of the company. Making decisions regarding the running of said department, etc.

• 50% rule – Must spent 50% or more of their time performing said duties above.

• Examples of “salaried exempt” personnel

• Architects, dentists, engineers, lawyers and medical doctors.

• CEO, COO, CFO, owners of company

• Upper echelon of company

• Personnel running divisions, sections of company

If a manager or supervisors spends more than 50% of their time doing non-management duties – they must be paid overtime.

• Examples of “non-management” duties: clerical, manual labour. Routine, repetitive, and directed-type work.

• Front line workers, administrative staff, support staff

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL14

Province* Minimum Hours Overtime Rules Rest Period Rules

Albertawww.alberta.ca

3-hour minimum – Exception (2-hour minimum for school bus drivers, part-time employees of non-profit recreation or athletic programs run by a municipality, Metis Settlement or community service Organization, home care employees, children under the age of 15)

Overtime is all hours worked over 8 in a day or 44 hours in a week, whichever is greater. (8/44 rule)

Employer must provide at least 30 minutes of break every 5 hours – can be broken into two 15-minute periods

BCwww2.gov.bc.ca

2-hour minimum – Employees must be scheduled for at least 2 hours of work. They must also be paid if they report to work as scheduled and there is no work for them to do

Overtime is time-and-a-half for hours worked over 8 in a day and double time for hours worked over 12 in a day. Overtime is time-and-a-half for over 40 hours in a work week

Must have 32 hours in a row free from work each week. Must also have at least 8 hours off between shifts. 30-minute meal break required if the employee works more than 5 hours in a row.

Manitobawww.gov.mb.ca 3-hour minimum

Overtime is all hours worked over 8 in a day or 40 in a week. Averaging agreements are allowed

Employer must provide at least 30 minutes of break for every 5 hours of work

New Brunswickwww2.gnb.ca 3-hour minimum Overtime is all hours worked over 44 in

a work weekEmployer must provide at least 30 minutes of break for every 5 hours of work

Newfoundland and Labradorwww.gov.nl.ca 3-hour minimum Overtime is all hours worked over 40 in

a workweekEmployer must provide at least 60 minutes of break for every 5 hours of work

Northwest Territorieswww.ece.gov.nt.ca 4-hour minimum

Overtime is all hours worked over 8 in a day or 40 in a week. Averaging agreements are allowed

Employer must provide at least 30 minutes of break for every 5 hours of work

Nova Scotiahttps://novascotia.ca/ 3-hour minimum Overtime is all hours worked over 48 in

a work weekEmployer must provide at least 30 minutes of break for every 5 hours of work

Nunavutwww.nu-lsco.ca/faq-s 4-hour minimum Overtime is all hours worked over 8 in a

day or 40 in a work weekEmployer must provide at least 30 minutes of break for every 5 hours of work

Ontariowww.ontario.ca 3-hour minimum Overtime is all hours worked over 44 in

a work weekEmployer must provide at least 30 minutes of break for every 5 hours of work

Prince Edward Islandwww.princeedwardisland.ca 3-hour minimum

Overtime is all hours worked over 48 in a work week after which the employee is eligible for time and one-half their regular rate of pay.

Employer must provide at least 30 minutes of break for every 5 hours of work

Québeccnt.gouv.qc.ca 3-hour minimum

Overtime is all hours over 40 in a work week. Averaging agreements are allowed

Employer must provide at least 30 minutes of break for every 5 hours of work

Saskatchewanwww.saskatchewan.ca 3-hour minimum

Overtime is all hours over 8 in a day or 40 in a workweek. Averaging for 10 hour days is allowed with permission

Employer must provide at least 30 minutes of break for every 5 hours of work

Yukonhttps://yukon.ca 3-hour minimum

Overtime is all hours over 8 in a work day or 40 in a work week. Averaging is allowed

Employer must provide at least 30 minutes of break for every 5 hours of work

Hours of Work RulesAnother area payroll professionals must keep up with is the hours of work rules. Hours of work rules for Canada are based on province and territories as listed below:

Canadian Payroll Basics

©Pryor Learning, Inc. • WYP2004ES-DL 15

Canadian Payroll Basics

Province Lieu/Bank Time Allowed Lieu/Bank Time Rules

Alberta Yes1. Agreement with employees2. Banked at time-and-a-half for all hours over 443. Must be taken within 6 months of time worked

British Columbia Yes 1. Agreement with employees

2. Banked at time-and-a-half for all hours over 40

Manitoba Yes1. Agreement with employees2. Banked at time-and-a-half for all hours over 403. Must be taken within 3 months of time worked

New Brunswick No

Newfoundland Yes1. Time and a half for all overtime hours2. Must be paid or time taken within 3 months of the time worked unless

employer and employee have an agreement to extend the time.

Northwest Territories Yes 1. Agreement with employees

2. Banked at time-and-a-half for all hours over 40

Nova Scotia Yes1. Time and a half for all overtime hours2. Must be paid or time taken within 6 months of the time worked unless

employer and employee have an agreement to extend the time.

Nunavut Yes 1. Agreement with employees2. Banked at time-and-a-half for all hours over 40

Ontario Yes1. Agreement with employees2. Banked at time-and-a-half for all hours over 443. Must be taken within 3 months of time worked

Prince Edward Island Yes

1. Time and a half for all overtime hours2. Must be paid or time taken within 3 months of the time worked unless

employer and employee have an agreement to extend the time.

Québec Yes 1. Agreement with employees2. Banked at time-and-a-half for all hours over 40

Saskatchewan Yes 1. Agreement with employees2. Banked at time-and-a-half for all hours over 40

Yukon Yes 1. Agreement with employees2. Banked at time-and-a-half for all hours over 40

Lieu/Bank TimeAnother area payroll professionals must keep up with is the hours of work rules. Hours of work rules for Canada are based on province and territories as listed below:

Training Time – time spent by an employee in training that is required by the employer or by law is counted as work time.

Travel Time – Commuting time is the time it takes an employee to get to work from home and vice-versa. This is NOT counted as work time for the purposes of the ESA. Exceptions to the rule:

• If employee is using the company vehicle for the convenience of the employer

• If employee is transporting other staff or supplies for the convenience of the employer

• If the employee has a usual workplace but is required to travel to another location to perform work

• Traveling between worksites during the workday is considered time worked.

©Pryor Learning, Inc. • WYP2004ES-DL16

Canada Requires Specific Benefits to be Made Available to All EmployeesPayroll departments in Canada must know which benefits affect not only the employee as far as they personally are concerned – but also which benefits affects their pay.

Canadian Statutory Holidays - Mark which ones apply to your company:

Employment and Labour Standards that Affect Payroll Processing

Holiday Federally Regulated Provincially Regulated

New Year’s Day

Islander Day

Family Day

Louis Riel Day

St. Patrick’s Day

Good Friday

Easter Monday

St. George’s Day

Victoria Day

National Patriots Day

National Aboriginal Day

St. Jean Baptiste Day

Discovery Day

Canada Day

Nunavut Day

Civic Holiday

Labour Day

Thanksgiving

Remembrance Day

Christmas Day

Boxing Day

Every year Canada will announce dates of applicable holidays as observed by each province at the beginning of the year. The above chart is subject to change each year.

©Pryor Learning, Inc. • WYP2004ES-DL 17

Province Wages Included in Holiday Pay Holiday Pay Calculation

Alberta Includes all wages, general holiday pay, vacation pay, bonuses. Does not include overtime.

Average day’s pay (5% of employee wages). If irregular schedule – in the last 9 weeks before the holiday, the employee has worked 5 of the same weekdays, then that weekday is considered a regular day of work and the rules for regular days of work apply.

British ColumbiaIncludes all wages, salary, commission, statutory holiday pay an paid vacation. Does not include overtime.

Average day’s pay.

ManitobaAll wages, excluding overtime, vacation and bonus pay. Construction industry has a special standard.

Regular day’s pay or if paid irregular determined by calculating 5% of the gross wages in the 4-week period immediately preceding the holiday.

New Brunswick All regular wages. Does not include overtime or vacation pay.

Regular day’s pay or if paid irregular determined by calculating average based on daily hours over a 20-day period.

Newfoundland All regular wages. Does not include overtime or vacation pay.

Regular day’s pay during the 3 weeks immediately prior to the paid public holiday divided by 15.

Northwest Territories

All regular wages. Does not include overtime or vacation pay. Regular day’s pay.

Nova Scotia All wages, excluding overtime, vacation and bonus pay.

Regular day’s pay or if paid irregular determine average based on daily hours over a 30-day period prior to the holiday.

Nunavut All wages. Does not include commissions, bonuses, overtime or vacation pay.

Regular day’s pay or average of all wages earned in the 28 days immediately before the public holiday.

OntarioAll regular wages including bonuses, commissions. Does not include overtime. May include vacation pay.

All regular wages earned by the employee in the four work weeks before the work week with the public holiday plus all of the vacation pay payable, divided by 20.

Prince Edward Island

All regular wages. Does not include overtime or vacation pay. Regular day’s pay.

Québec All wages including commissions, bonuses. May include overtime and vacation pay.

Regular daily rate or average of all wages earned in the 28 days immediately before the public holiday.

Saskatchewan All wages, including vacation pay. Does not include overtime, bonuses and gratuities.

Average of all wages earned in the 28 days immediately before the public holiday.

Yukon All wages, exclusive of overtime or bonus pay, vacation pay.

Regular daily rate or if paid irregular wages 10% of the wages earned for the hours worked in the 2 calendar weeks immediately prior to the week in which the holiday falls.

Federal All wages. Does not include overtime pay, vacation pay, severance pay or termination pay.

Either regular daily pay or previous 4 weeks divided by 20.

Employment and Labour Standards that Affect Payroll Processing

Wages Included in Statutory Holiday Pay Vary from Province to Province

©Pryor Learning, Inc. • WYP2004ES-DL18

Province Eligibility Vacation Time and Pay

Alberta 1 year of service 1 – 5 years of service – 2 weeks at 4% After 5 years – 3 weeks at 6%

British Columbia After 5 days of employment

1 – 5 years of service – 2 weeks at 4% After 5 years – 3 weeks at 6%

Manitoba 1 year of service 1 – 5 years of service – 2 weeks at 4% After 5 years – 3 weeks at 6%

New Brunswick 1 year of service 1 – 8 years of service – 2 weeks at 4% After 8 years – 3 weeks at 6%

Newfoundland 1 year of service 2 weeks at 4%After 15 years – 3 weeks at 6%

Northwest Territories 1 year of service 1 – 8 years of service – 2 weeks at 4%

After 8 years – 3 weeks at 6%

Nova Scotia 1 year of service 2 weeks at 4%After 8 years – 3 weeks at 6%

Nunavut 1 year of service 2 weeks at 4%After 5 years – 3 weeks at 6%

Ontario 1 year of service 2 weeks at 4%

Prince Edward Island 1 year of service 1 – 8 years of service – 2 weeks at 4%

After 8 years – 3 weeks at 6%

Québec 1 year of service 1 – 5 years of service – 2 weeks at 4% After 5 years – 3 weeks at 6%

Saskatchewan 1 year of service 3 weeks at 6% After 10 years of service – 4 weeks at 8%

Yukon 1 year of service 2 weeks at 4%

Federal 1 year of service 2 weeks at 4%After 5 years – 3 weeks at 6%

Statutory Vacation By Province

Employment and Labour Standards that Affect Payroll Processing

©Pryor Learning, Inc. • WYP2004ES-DL 19

• To qualify employee must complete a certain amount of time with a company (except in BC, New Brunswick and Québec – no minimum requirement).

• Must have worked a minimum of 600 insurable hours in the 52 weeks before you begin your leave.

• Companies may supplement Maternity Leave benefits by making up some of the difference between the employment insurance maternity benefits and the employee’s salary.

• Once leave has started – employee must take it all at one time and cannot split it up.

• Personal Emergency Leave is unpaid, job-protected time off work for up to 10 days per calendar year. Employer can count any part of a day taken off as a full day of personal emergency leave.

• Family Medical Leave is unpaid, job-protected time off work for up to 8 weeks in a 26-week period. The 8-weeks of family medical leave do not have to be taken at the same time.

• Reservist Leave is for employees who are military reservists and who are deployed to an international operation or to an operation within Canada that is or will be providing assistance in dealing with an emergency or its aftermath. This leave is unpaid.

ProvinceMaternity

Leave (in weeks)

Parental Leave

(in weeks)

Adoption Leave

(in weeks)

TotalAllowed

Alberta 16 63 63 78

British Columbia 17 62 62 78

Manitoba 17 35 35 52

New Brunswick 17 35 35 52

Newfoundland and Labrador 17 35 35 52

Northwest Territories 17 37 37 52

Nova Scotia 16 61 61 77

Nunavut 16 36 36 52

Ontario 17 62 62 78

Prince Edward Island 17 35 35 52

Québec 16 52 52 68

Saskatchewan 19 59 59 78

Yukon 17 35 35 52

Federal 17 35 35 52

Standards for Pregnancy, Maternity and Parental Leaves• Pregnancy, Maternity and Parental Leave is subject to each Province human rights code or legislation. However,

they are similar in nature.

Employment and Labour Standards that Affect Payroll Processing

©Pryor Learning, Inc. • WYP2004ES-DL20

• Seniority and benefits must continue during leave time.

• Employer cannot fire an employee for use of these types of leave.

• Canadians who are sick, pregnant, or caring for a newborn or adopted child, as well as those who must care for a family member who is seriously ill with a significant risk of death, may also be assisted by Employment Insurance.

Sick, Vacation Leave and Pay• Sick, Vacation Leave and Pay is part of the flexible benefits an employer can offer their employees.

• Leave for personal reasons – provided for employees with or without pay to deal with family obligations or other personal commitments.

• Sick Leave – enables employees to take time off work when ill.

• Employee may not be dismissed, suspended, laid off or demoted when on sick leave in 6 jurisdictions (federal, Québec, Yukon, Newfoundland, New Brunswick and Saskatchewan).

• May be with or without pay.

• Vacation – enables employees to take time off work for vacation to be taken with spouse and/or family.

• May be taken in shorter periods.

• See appendix for more details.

Employment and Labour Standards that Affect Payroll Processing

©Pryor Learning, Inc. • WYP2004ES-DL 21

Province Termination Notice Termination Pay Requirements

Alberta Depends on length of service 3 days from termination date

British Columbia Depends on length of service If discharge – within 48 hours If employee quits – 6 days of termination

Manitoba Depends on length of service 10 days from termination

New Brunswick Depends on length of service Next regular payday

Newfoundland Depends on length of service Next regular payday

Nova Scotia Depends on length of service Next regular payday

Northwest Territories Depends on length of service Next regular payday

Nunavut Depends on length of service Next regular payday

Ontario Depends on length of service Within 7 days of termination

Prince Edward Island Depends on length of service Next regular payday

Québec Depends on length of service Next regular payday

Saskatchewan Depends on length of service Within 14 days of termination

Yukon Depends on length of service Next regular payday

Federal Depends on length of service Next regular payday

Termination Pay• Termination pay is determined by province. Required notice/pay is determined by length of service and

provincial rules.

• Final termination pay must include all accrued vacation pay regardless of the amount in the accrual. Unlike the vacation time, the vacation pay must be paid out on termination. There is no use it or lose it for the statutory vacation pay (unless employer has permission by the provincial ministry/director of labour).

Employment and Labour Standards that Affect Payroll Processing

©Pryor Learning, Inc. • WYP2004ES-DL22

Deductions from Pay

Canadians are fortunate to have access to a wide range of government programs and support services. To cover this cost, every working Canadian pays a portion of their earnings to the federal and provincial governments in the form of income tax.

Employment Insurance (EI) Deductions • EI benefits are designed to replace a portion of lost wages to qualified employees who are laid off or become ill

for an extended time. Employers and employees contribute to this tax.

Canada Pension Plan (CPP) orQuébec Pension Plan (QPP) • CPP and QPP are retirement plans administered by the government.

Income Tax • Amount required to deduct for both federal and provincial income tax. In Québec the amount is listed

separately. In all other provinces, the sum is a total for both federal and provincial.

Benefits • Some employers offer group health care or dental plans.

Union dues • The fee an employee pays to be a member of a union

Registered Retirement Savings Plan (RRSP) or Employer-Sponsored Pension Fund • Plans employers provide for pension and retirement. This amount is deducted from the employee’s paycheque.

Recordkeeping is an area where payroll professionals must be sure they can prove they are doing what the government regulations require. It is also an area that informs payroll how to properly withhold on various tax and other withholding areas for each employee.

Deduction from Pay

Some employers make deductions from employees’ pay for losses, shortages, damages, etc. Also some employers may make deductions for employee debts that are not for purchases on account.

Rules:

1. These deductions must not take the employee’s gross pay below minimum wage

2. These deductions must be authorized by a clear agreement between the employer and the employee. Deductions are authorized by the employee when there is a written agreement or when the employee has acted in a way that shows that he or she accepts the deduction

3. The authorization cannot have a “blanket statement”

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL 23

Social Insurance Number - Employer Responsibilities

• Correctly identify employees with the help of pieces of identification before finalizing their employment documents. Use the voluntary ROH verification program on Service Canada’s website to help verify SIN information.

• Ensure that employees have a valid SIN. This number is used to administer government benefits under the Income Tax Act the Canada Pension Plan act and the Employment Insurance Act.

• If a new employee does not have a SIN and is eligible to work in Canada instruct the employee to apply for a SIN at a Service Canada office. If the employee’s application and identify document(s) are in order, he or she will receive a SIN in one visit

• You can confirm the SIN of a current or former employee by contacting Service Canada at 1-800-206-7218 (selection option “3”). You will need to provide your business number issued by CRA along with necessary information to verify the identity of your company as well as the employee.

• Store all personal information in a secure area or on an encrypted computer system and ensure that only authorized individuals have access.

• SINS beginning with a “9”

• Issued to temporary workers who are neither Canadian citizens nor permanent residents. These temporary SINs are valid until the expiry date indicated on the immigration document authorizing them to work in Canada.

• Ask to see the employee’s existing immigration document authorizing him or her to work in Canada and verify that it has not expired. If it has expired, take the necessary steps to renew or rehire the employee legally.

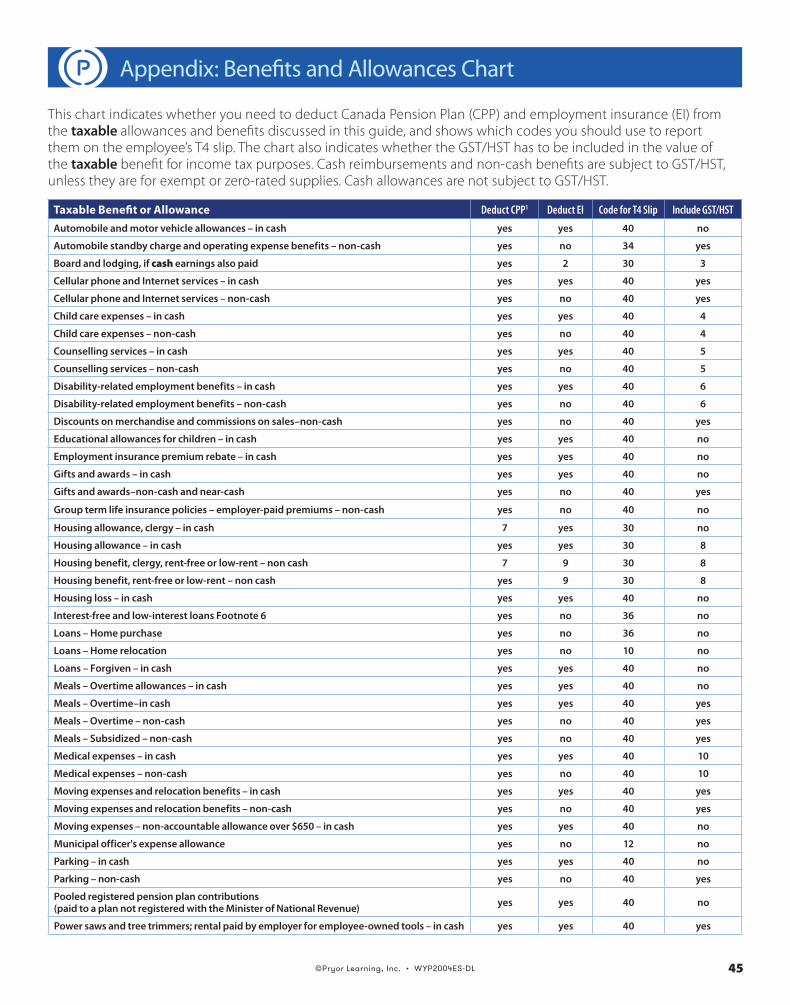

Amounts and Benefits Subject to EI (Employment Insurance) Premiums

• Salary, wages, bonuses, commissions, or other remuneration (including payroll advances or earnings advances), and wages in lieu of termination notice.

• Cash taxable benefits and allowances. See Special Payments Chart in Appendix

• Employer contributions to an employee’s registered retirement savings plan (RRSP) except where employees cannot withdraw amounts from a group RRSP until they retire or cease to be employed.

• Gift, prizes, and awards paid in cash.

• Honorariums, a share of profit, incentive payments, management fees.

• Certain tips and gratuities.

• Remuneration received while on vacation or sick leave.

• Wage-loss benefits that an employee receives from a wage-loss replacement plan

• Salary employer continues to pay to an employee before or after a workers’ compensation board claim is decided.

• Employer must pay 1.4 times the amount of the employee’s premiums. The maximum annual insurable earnings is determined each year.

• Example: EI premiums employer deducted from employees in the month = $195.50. Employer share is 1.4 times = $273.70.

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL24

Employer Share of Statutory Deductions

Amounts and Benefits Subject to CPP or QPP (Canada Pension Plan or Québec Pension Plan) Premiums

• When to deduct:

• Employee is 18 or older, but younger than 70

• Is in pensionable employment during the year; and

• Does not receive a CPP or QPP retirement or disability pension

• Salary, wages, bonuses, commissions, or other remuneration (including payroll advances or earnings advances), and wages in lieu of termination notice

• Cash taxable benefits and allowances (see Special Payments Chart in appendix)

• Employer contributions to an employee’s registered retirement savings plan (RRSP) except where employees cannot withdraw amounts from a group RRSP until they retire or cease to be employed

• Gift, prizes, and awards paid in cash

• Honorariums, a share of profit, incentive payments, management fees

• Certain tips and gratuities

• Remuneration received while on vacation or sick leave

• Benefits derived from security option plans

• Salary employer continues to pay to an employee before or after a workers’ compensation board claim is decided

• Employer must match the amount of the employee’s premiums. The maximum annual insurable earnings is determined each year. Maximum annual pensionable earnings = $48,300. Employee Contribution Rate = 4.95%

• Example: CPP premiums employer deducted from employees in the month = $240.40. Employer share = $240.40

• Québec has their own QPP and QPIP (Québec Parental Insurance Plan) – See www.revenu.gouv.qc.ca for more information

Calculating the Payroll Deductions

• To determine the amount of contributions to deduct, use one of the following tools:

• Payroll Deductions Online Calculator (PDOC) or

• the payroll deduction tables (T4032) or

• computer formulas (T4127)

Income Tax Rates

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL 25

Changes Since the November 22, 2019 releaseThe “What’s New for January 1, 2020” chapter has been updated to provide clarity regarding the Newfoundland and Labrador Temporary Deficit Reduction Levy. The rate and amount for the LCP for Manitoba has been removed in Tables 9.2 and 9.18. A typo has been corrected in Table 9.1 where NB was labeled as MB. The Comma Separated Value (CSV) file “Other rates and amounts” has been updated to include the federal amounts and to remove the Alberta index rate. Factors K4 and K4P has been updated to include commission income.

What’s New for January 1, 2020This guide reflects some income tax changes recently announced which, if enacted as proposed, would be effective January 1, 2020. At the time of publishing, these proposed changes were not law. We recommend that you use the Payroll Deductions Online Calculator (PDOC), the publication T4032 Payroll Deductions Tables, or the publication T4008 Payroll Deductions Supplementary Tables, and the formulas in this guide for withholding, starting with your first payroll in 2020.

Comma-Separated Value (CSV)We now offer the most commonly used rates and amounts from this guide in CSV format. To provide this service we have made the following changes: the claim code tables previously found in Chapter 3 have been moved to Chapter 9; the threshold tables previously found in Chapter 5 have been moved and combined with the threshold tables in Chapter 9; Canada Pension Plan, Quebec Pension Plan, and Employment Insurance tables have been added to Chapter 9; and Chapter 9 has been renamed to Rates and amounts. The CSV files are available at the T4127 Payroll Deductions Formulas website.

Federal ChangesCanada Pension Plan (CPP)For 2020, the maximum pensionable earnings are $58,700, and the basic exemption for the year is $3,500. The contribution rate for employees is 5.25%. The increase in contribution rate is due to the CPP enhancement.

The maximum an employee can contribute for the year is $2,898.00. The employer’s contribution is an amount equal to the total of the employee’s contributions.

For insurance companies that need the year’s maximum pensionable earnings before rounding, the amount for this year is $58,712.35.

Minor revisions have been made to Factor C to calculate CPP in the situation where an employee is transferred by their employer from Quebec to a location outside of Quebec. The Canada Revenue Agency will expect from employers their best efforts to comply with this proposed Regulation during 2020 calendar year. Starting January 1, 2021, employers should be fully compliant with respect to this Regulation.

Quebec Pension Plan (QPP)For 2020, the QPP contribution rate for employees is 5.70%. The maximum an employee can contribute for the year is $3,146.40. The employer’s contribution is an amount equal to the total of the employee’s contributions.

Employment Insurance (EI)For 2020 in Canada (except Quebec), the maximum annual insurable earnings are $54,200 and the EI premium rate is 1.58%, for a maximum annual premium of $856.36. In Quebec, the premium rate is 1.20%, for a maximum annual premium of $650.40.

The Quebec Parental Insurance Plan (QPIP) maximum earnings amount is $387.79 for employees and $543.22 for employers. For 2020, the maximum insurable earnings is $78,500.

Withholdings: Taxable vs . Nontaxable, Garnishments

See publication T4001 - https://www.canada.ca/content/dam/cra-arc/formspubs/pub/t4001/t4001-19e.pdf

©Pryor Learning, Inc. • WYP2004ES-DL26

Special PaymentsThere are several common areas where payroll professionals experience taxable issues that must be addressed at the time of payment. These issues have special rules that are required to be followed in order to know if the income is taxable or not. A payroll professional also needs to know the “definition” of certain words according to the CRA.

Gifts

A gift (either in cash or in kind) from an employer to an employee is a benefit derived during or because of the individual’s employment.

A gift has to be for a special occasion such as Christmas gift, birth of a child, marriage, etc. An employee can receive unlimited number of tangible property gifts with a value up to $500 on a nontaxable basis. Anything over $500 cumulative for the year will be table. Example: Employee receives $650 in tangible property gifts. $150 is taxable.

Cash and near-cash (gift certificates) are taxable. *Special rules apply.

Awards

Must be given for an employment-related accomplishment to be nontaxable.• Outstanding service, employees’ suggestions, or meeting or exceeding safety standards.• It must be recognition of an employee’s overall contribution to the workplace – not recognition of job

performance.• Long-service award: Value up to $500 – tangible property only. Must be for a minimum of 5 years of service.

Is not included in other gift or award benefits.•

RewardsGiven to an employee for performance-related reasons. Example: perfect attendance reward. Taxable.

*Special rules for gift certificates: As long as there is an element of choice regarding the gift card – taxable. Example: You give your employee a $100 gift card to a department store. The employee can use this to choose whatever merchandise or service the store offers.

Example of nontaxable: You give your employee tickets to a hockey game on a specific date at a specific time. There is no element of choice.

Prize Drawings and Social CommitteesTaxable:

• Item given to one employee by an employer via a prize draw.• Item paid for by the employer and given via a draw to an employee of a high-performing team.

Non-Taxable:• Item paid for by a social committee and given via a draw.

• Committee must be entirely funded by the employees.• If funded by employer, taxable.• If funded by both – employer percentage is taxable and employee percentage is nontaxable.

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL 27

There are several common areas where payroll professionals experience taxable issues that must be addressed at the time of payment. These issues have special rules that are required to be followed in order to know if the income is taxable or not. A payroll professional also needs to know the “definition” of certain words according to the CRA.

Automobile AllowancePersonal use of a company vehicle is taxable. Use “stand-by-charge” method of calculation.

Available on CRA website: www.cra.gc.ca/autombenefits-calculator (pub. T4130)

• Per kilometre allowance – nontaxable.

• __________¢ per kilometer.

• Flat rate allowance – taxable.

Cellular Phone Service

• Personal use of a company cell phone is taxable.

Employer has responsibility to determine FMV (fair market value) of personal use. Must justify calculations.

• Exceptions to the rule (all must apply):

• The plan’s cost is reasonable.

• The plan is a basic plan with a fixed cost.

• Our employee’s personal use of the service does not result in charges that are more than the basic plan cost.

Internet Service

• When an employer provides internet service for employee for home use – the fair market value of the service for business use must be calculated. Employee should be taxed on the FMV of personal use.

See Appendix for other taxable/nontaxable benefits.

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL28

Failure to do timely reporting and depositing can result in multiple fines, penalties and interest expenses. The payroll professional needs to know when to remit their taxation withholdings.

Remitter Types and Due DatesRegular Remitter

• If you are a new employer, or your average monthly withholding amount two years ago was less than $25,000

• Remit your deductions so the government receives them on or before the 15th day of the month following the month you made the deductions

Quarterly Remitter

• If you have an average monthly withholding amount of less than $3,000 in either the first or the second preceding calendar year; and

• Have a perfect compliance history

• Remittances are due the 15th day of the month immediately following the end of each quarter. April 15, July 15, October 15 and January 15

Accelerated Remitter

• Threshold 1 – consists of employers who had a total average monthly withholding amount of $15,000 to $49,999.99 prior to 2015 and $25,000 to $99,999.00 as of 2015

• Amounts deducted from remuneration paid in the first 15 days of the month are due by the 25th of the same month. Amounts deducted from the 16th to the end of the month are due by the 10th day of the following month

• Threshold 2 – consists of employers who had a total average monthly withholding amount of $50,000 or more prior to 2015 and $100,000 or more as of 2015

• Amount deducted from remuneration paid any time during the month are due to be received by your Canadian financial institution no later than the third working day after the end of the following periods:

• From the 1st through the 7th day of the month;

• From the 8th through the 14th day of the month;

• From the 15th through the 21st day of the month;

• From the 22nd through the last day of the month.

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL 29

Penalties and InterestFailure to deduct can result in a 10% penalty of the amount of CPP, EI and income tax you failed to deduct. If you fail to deduct the required amount of income tax more than once in a calendar year, a 20% penalty may be applied to the second or later failures if they were made knowingly or under circumstances of gross negligence.

Failure to Remit and Late RemittancesAn assessment penalty of up to 20% of the amount owed when:

• You deducted the amounts, but do not remit them; or• The amounts are received after the due date.

The penalty for remitting late is:• 3% if the amount is one to three days late;• 5% if it is four or five days late; • 7% if it is six or seven days late; and• 10% if it is more than seven days late, or if no amount is remitted.

Interest is compounded daily at the prescribed interest rates. Interest is also applied to unpaid penalties.

How to Avoid a PIER (Pensionable and Insurable Earnings Review)

• Deduct Canada Pension Plan/Quebec Pension Plan (CPP/QPP) contributions, Employment Insurance (EI) premiums, provincial parental insurance plan (PPIP) premiums, and income tax from remuneration or other amounts you pay. See Guide T4001, Employers’ Guide – Payroll Deductions and Remittances for more information.

• Hold these amounts in trust for the Receiver General, except the QPP contributions and PPIP premiums, which are remitted directly to Revenu Québec. You have to keep these amounts separate from the operating funds of your business. Make sure these amounts are not part of an estate in liquidation, assignment, receivership, or bankruptcy.

• Remit these deductions to the Canada Revenue Agency (CRA).

• Report the income and deductions on the T4 information return to the CRA. To do this, complete T4 slips, Statement of Remuneration Paid, and the related T4 Summary, Summary of Remuneration Paid.

• File the T4 Summary, together with the related T4 slips, on or before the last day of February following the calendar year to which the slips apply.

• Give employees their T4 slips on or before the last day of February following the calendar year to which the slips apply.

• Keep records. Keep your paper and electronic records for at least six years after the year to which they relate. If you want to destroy them before the six-year period is over, complete Form T137, Request for Destruction of Records.

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL30

Remember – If you receive a Requirement to Pay notice and you do not comply with the requirements, your organization may be held responsible for the amounts you didn’t remit!

Garnishments Basics

Garnishment of wages is the process by which creditors can withdraw a percentage of an individual’s income in the event that the individual owes an exceptionally large debt and is believed unable or unwilling to pay it off.

Types of Garnishments

• Creditors with or without a court order

• Tax garnishments from CRA (Canada Revenue Agency)

• Child Support Orders

Creditors

• Court ordered

• Percent to withhold governed by federal or provincial law

• Cannot terminate the employee for garnishment – Fine: $1,000 Canadian or face imprisonment with a duration of one year.

• Exception: If wage garnishment has occurred more than once in the history of the employee, employer may discharge the employee at will.

• Non-court ordered

• Only applied when the assignment of wage to a labor union

Tax Garnishments from CRA • Allowed without a court order

• No limit

• Usually last resort when CRA cannot get debtor to pay the taxes

Child Support Orders

See Appendix – Child Support Order Limits by Province

• Court may order be paid in periodic payments, in a lump sum or in a lump sum and periodic payments

• Variation of child support orders

• Includes a determination made in accordance with the applicable table

• Does not include a determination made in accordance with a table

Withholdings: Taxable vs . Nontaxable, Garnishments

©Pryor Learning, Inc. • WYP2004ES-DL 31

What Every Payroll Processor Needs to Know About Special Situations

Once in a while something “out of the ordinary” happens and it affects how we pay an employee. Situations like final paycheques, death of an employee, employee actually works in the United States but it is a Canadian-based company. We need to know what to do in the “special” situations.

Handling Final Pay

• Calculate the employee’s earning and deductions for the year to date, and give the employee his or her T4 slip

• Keep the government copy of the slip and include it with your T4 Summary when you file it by the last day of February of the following year

• Confirm the labour standards of your employee’s province of employment to ensure that you have met their requirements

• If you pay a retiring allowance, report retiring allowances on a T4 slip

• Complete the Record of Employment (ROE)

In the Case of a Death of an Employee

• When an employee dies, you may pay benefits such as a death benefit

• Report all income and deductions as you would when an employee leaves the company

• Address the appropriate slips (T4/T4A) in the name of the beneficiary or “estate of” the deceased person

Special Payroll Concerns

©Pryor Learning, Inc. • WYP2004ES-DL32

Filing ROE (Record of Employment)

When do I have to issue an ROE?

• Each time an employee experiences an interruption of earnings; or

• When Service Canada requests one.

For part-time, on-call, or casual workers:

• You do not have to issue an ROE every time he/she experiences an interruption of earnings of seven days or more. However, you MUST issue one when:

• An employee requests an ROE and an interruption of earnings has occurred;

• An employee is no longer on the employer’s active employment list;

• Service Canada requests an ROE; or

• An employee has not done any work or earned any insurable earnings for 30 days.

When do I issue an ROE?

1. If you issue an ROE on paper

a. You must issue an ROE within 5 calendar days of:

i. The first day of an interruption or earnings; or

ii. The day the employer becomes aware of an interruption of earnings.

2. If you issue ROEs electronically

a. You must issue an ROE within 5 calendar days after the end of the pay period in which an employee’s interruption of earnings occurs; or

b. 15 calendar days after the first day of an interruption of earnings.

Special Payroll Concerns

©Pryor Learning, Inc. • WYP2004ES-DL 33

US Source Income for Canadian Companies Located in the United States

Sometimes a payroll professional needs to know United States laws and regulations in addition to Canadian laws and regulations.

Employment Outside CanadaCPP Contributions

• If you are a Canadian employer and you hire someone to work for you outside Canada, you deduct CPP contributions if:

• The employee usually reports for work at your place of business in Canada; or

• The employee is a Canadian resident and is paid from your place of business in Canada.

• If the employment does not meet either of these conditions, the employment outside Canada is not pensionable. As a result, do not deduct CPP from the employee’s remuneration.

EI Premiums

• You have to deduct EI premiums from employment income an employee earns outside or partly outside Canada if all of these conditions apply:

• You, as the employer, reside in Canada or have a place of business in Canada

• The employee usually resides in Canada

• The employment is not insurance in the country where the employment is performed; and

• The employment is not excluded from insurable employment for any other reason.

Income Tax

• If an employee performs services for you outside Canada, you may have to deduct income tax from that employee’s remuneration.

• Employee may be subject to a foreign tax credit in respect of taxes paid in a foreign jurisdiction.

United States Taxation

• If the employee is a non-resident or resident alien (based on United States Tax Residency regulations) they may be subject to United States IRS regulations for taxation of US Source income.

Special Payroll Concerns

©Pryor Learning, Inc. • WYP2004ES-DL34

Which Payroll Table to Use When

Payroll professionals will, on occasion, have to determine which payroll table applies to employees in special situations:

Your employee is a….Employee reports for work at an establishment of the

employer in Canada

Employee works in Canada but does not report

for work at an establishment of the employer

Employee works in Canada, but employer does not have an establishment in Canada

Resident of Canada

Use the Payroll Deductions Tables for the province or territory where the employee reports for work.

Use the Payroll Deductions Tables for the province or territory where the employer’s establishment is located and from which the employee’s salary is paid.

Use the Payroll Deductions Table for In Canada Beyond the Limits of Any Province or Outside Canada

Deemed resident or sojourner (see Note)

Use the Payroll Deductions Tables for In Canada Beyond the Limits of Any Province or Outside Canada

Use the Payroll Deductions Tables for In Canada Beyond the Limits of Any Province or Outside Canada

Use the Payroll Deductions Tables for In Canada Beyond the Limits of Any Province or Outside Canada

Part-year resident, for the part of the year he/she is resident in Canada (see Note)

Use the Payroll Deductions Tables for the province or territory where the employee reports for work.

Use the Payroll Deductions Tables for the province or territory where the employer’s establishment is located and from which the employee’s salary is paid.

Use the Payroll Deductions Table for In Canada Beyond the Limits of Any Province or Outside Canada

Part-year resident, for the part of the year he/she is non-resident (see Note)

Use the Payroll Deductions Tables for the province or territory where employment duties are performed.

Use the Payroll Deductions Tables for the province or territory where employment duties are performed.

Use the Payroll Deductions Tables for the province or territory where employment duties are performed.

Non-resident, including a commuter (see Note)

Use the Payroll Deductions Tables for the province or territory where employment duties are performed.

Use the Payroll Deductions Tables for the province or territory where employment duties are performed.

Use the Payroll Deductions Tables for the province or territory where employment duties are performed.

Note: for more information, see Interpretation Bulletin IT-221, Determination of an Individual’s Residence Status.

Special Payroll Concerns

©Pryor Learning, Inc. • WYP2004ES-DL 35

Minimum Duration of Annual Vacations

In all jurisdictions, eligible employees are entitled to at least two weeks of annual vacation with pay after each completed year of employment. The exception is Saskatchewan, where employers must provide no less than three weeks of vacation with pay to employees who have completed one year of service.

In 11 jurisdictions, employees are entitled to an additional week of vacation with pay after a specified period of service. In Alberta, British Columbia, Manitoba and Québec, employees are entitled to three weeks of annual vacation with pay after five consecutive years of employment with the same employer. The same applies in the federal jurisdiction after six consecutive years of employment; in the Northwest Territories and Nunavut after six years of employment accumulated over the previous ten years; in New Brunswick and in Nova Scotia after eight years of employment; and lastly, in Newfoundland and Labrador after 15 years of continuous employment. After ten years of employment, employees in Saskatchewan must be granted four weeks of annual vacation with pay. It should be noted that employees in Québec who have at least one year of uninterrupted service, but who do not yet qualify for three weeks of annual leave with pay, can take an additional week of annual leave, without pay, if they so request. This additional leave must be taken in one unbroken period, although it is not necessary to take it immediately before or after an annual leave with pay.

Two provinces, Québec and New Brunswick, afford prorated vacation time to employees who have completed less than one year of service with their employer. In Québec, those employees are entitled to one day of vacation per month of uninterrupted service during the reference year (up to 10 days); in New Brunswick, employees are entitled to at least one day of vacation per month during the vacation pay year in which they worked, to a maximum of two weeks of vacation. Furthermore, employees in New Brunswick who have completed eight consecutive years of service, but who have only worked for part of the vacation pay year, are entitled to one and one-quarter days of vacation per month in which they worked during that period. In contrast, Alberta’s Employment Standards Code allows an employer to reduce an employee’s vacation and vacation pay in proportion to the number of days the employee was absent from work.

Appendix: Vacation Pay Rules

©Pryor Learning, Inc. • WYP2004ES-DL36

To simplify the administration of vacations and vacation pay, especially in larger firms, a number of jurisdictions allow employers to designate a common anniversary date, instead of calculating each individual employee’s length of service. However, this is subject to a number of limitations, to ensure employees’ right to a vacation with pay is not curtailed by such an arrangement. For example, employers in Alberta, Manitoba, Ontario, Saskatchewan and the federal jurisdiction who establish a common anniversary date must provide a prorated vacation with pay to employees with less than one full year of employment on that date. In Manitoba, the Director of Employment Standards may also, under certain circumstances, revoke or impose terms and conditions on the use of a common anniversary date. British Columbia’s Employment Standards Act simply states that “an employer may use a common date for calculating the annual vacation entitlement of all employees (…), so long as this does not result in a reduction of any employee’s rights” with respect to an annual vacation and vacation pay.

Minimum Amount of Vacation Pay

In most Canadian jurisdictions, vacation pay is set at 4% of an employee’s annual wages, except where the employee is entitled to three weeks of vacation, in which case the amount of vacation pay must be equal to at least 6% of annual wages. Vacation pay is calculated differently in Saskatchewan. Vacation pay in that province is defined as 3/52 of an employee’s total wages for the year of employment, or 4/52 when the employee is entitled to four weeks of annual holidays. Moreover, an employee paid monthly in Alberta is entitled to an amount of vacation pay at least equal to his/her wages for normal hours in a work month, divided by 4 1/3 , for each week of vacation. Finally, in Manitoba, an employee is entitled to a vacation allowance consisting of:

• 2% of the wages he/she earned during the year of employment in respect of which he/she is entitled to the annual vacation; and

• 2% of the cash value of board and lodging, or of the allowance in lieu of board and lodging, that the employee received as part of his/her usual remuneration that year in respect of his/her regular working hours (where applicable).

In Québec, special provisions also apply to employees who are absent from work due to sickness or accident or by reason of a maternity leave. Should such an absence result in the reduction of an employee’s annual leave indemnity (i.e., vacation pay), the latter is to be calculated on the basis of average weekly wages earned during the period of work, multiplied by the number of weeks of vacation entitlement. This amount can be prorated for employees who have less than one year of uninterrupted service. An annual leave indemnity calculated in this manner is not to exceed the amount to which an employee would have been entitled were it not for the leave or absence.

Appendix: Vacation Pay Rules

©Pryor Learning, Inc. • WYP2004ES-DL 37

Although the formula used to calculate vacation pay—annual wages times 4% or 6%—is common to most jurisdictions, there is relatively little consistency across Canada as regards the types of earnings (e.g., salary, tips, holiday pay) that are to be considered as “wages”. Indeed, the definition of wages varies in the employment standards legislation of each jurisdiction, both in terms of breadth and precision. For example, Québec’s Act respecting labour standards defines wages as “remuneration in currency and benefits having a pecuniary value due for the work or services performed by an employee”. This is broader, but also much less specific, than definitions used in provinces such as Alberta and Ontario, which explicitly list the types of payments (e.g., tips, expenses, discretionary bonuses) that are not deemed to be wages for vacation pay (and other) purposes. Moreover, special vacation pay provisions sometimes apply to certain categories of employees, particularly in seasonal occupations such as construction and harvesting, or where wages are calculated on a piece work basis.

Timeliness of Payment (Vacation Pay)

Provisions in all jurisdictions stipulate when an employer is required to disburse vacation pay to an employee. However, requirements are far from identical across Canada.

Normally, vacation pay must be paid in a lump sum within a specified period before the vacation begins. For instance, all three territories and the Atlantic Provinces require that an employee receive his/her vacation pay at least one day before beginning a vacation. In Saskatchewan, vacation pay must be paid in the 14-day period preceding the vacation; where an annual vacation is fragmented, a portion of vacation pay must be paid before each period of vacation. Provisions in Manitoba stipulate that vacation pay is to be paid on the “last working day” before the vacation, unless the employer and the employee agree otherwise.

In some jurisdictions, vacation pay may be paid on the regular pay day following the start of a vacation. However, this is normally subject to certain conditions. For example, in the case of Alberta, employees can instead request to receive their vacation pay at least one day before starting a vacation. In the federal jurisdiction, vacation pay may be disbursed on the regular pay day during or immediately following a vacation, but only where it would not be practical to make the payment earlier or where it is an established practice in the industrial establishment. Otherwise, vacation pay must be paid within 14 days before the vacation begins. In British Columbia, an employer must pay an employee his/her vacation pay seven days before the beginning of a vacation, unless both agree (or a collective agreement provides) that payment will be made on the employee’s scheduled pay days.

Appendix: Vacation Pay Rules

©Pryor Learning, Inc. • WYP2004ES-DL38

In Ontario, there are elaborate provisions regarding the payment of vacation pay. Employees covered by the relevant provisions of the Employment Standards Act must normally receive their vacation pay in a lump sum before their vacation begins. There are nevertheless numerous exceptions to this rule. Where an employer pays an employee’s wages by direct deposit, vacation pay may be paid on or before the pay day for the period in which the vacation falls. This also applies if an employee does not take vacation in complete weeks. Moreover, with the employee’s agreement, an amount for vacation pay may be disbursed on each pay day, as soon as it accrues, provided that the amount is indicated separately in a wage statement. An employer and employee may also agree on an alternative date for payment of vacation pay. Ontario’s legislation even specifies that vacation pay must be paid with respect to a vacation that has been cancelled because of a strike or lockout.

Finally, legislation in some jurisdictions, such as Nova Scotia and Saskatchewan, specifies the latest date on which vacation pay must be paid if an employee waives his/her vacation. Any vacation pay owing must be paid out when an employee’s employment is terminated, usually within a set period of time.

Eligibility Requirements

To qualify for a vacation, employees in most jurisdictions must have completed at least one year of continuous employment with their current employer. Ontario’s Employment Standards Act, 2000 expressly states that this includes both active and non-active service (e.g., periods of leave or layoffs that do not constitute a termination of employment).

In some cases, employees whose service with the same employer has been interrupted for a relatively brief period—as is often the case for seasonal or casual employees—may nevertheless be entitled to an annual vacation. In Alberta, any break in employment of less than three months is to be counted as a period of continuous employment when determining whether an employee is entitled to three weeks’ vacation. A provision in Saskatchewan’s Labour Standards Act (not yet proclaimed in force) would include, in the calculation of an employee’s service with an employer, any break in employment of less than 13 weeks. It is worth noting that Yukon’s Employment Standards Act specifies that annual vacation provisions apply “to all employees, including employees who are employed on a part-time, seasonal or temporary basis”.

To be eligible for an annual vacation, employees covered by Newfoundland and Labrador’s Labour Standards Act must also have worked for an employer at least 90% of the normal working hours in a continuous 12-month period. Newfoundland and Labrador is the only province in Canada to have such a requirement.