PawnTech Trend Report 2021

9

PawnTech Trend Report 2021 How to keep the lights on and knowing the trends of the Pawn Industry

Transcript of PawnTech Trend Report 2021

PawnTech Trend Report2021 How to keep the lights on and knowing the trends of the Pawn Industry

2

Trend Report | 2021 June

3888.407.6287 bravostoresystems.com 888.407.6287 bravostoresystems.com

Inside the Report 04 Hello from Tally Mack, CEO

06 The Impact of the Pawn Industry

08 How Pawn Differs from Other Financial Institutions

09 The Pawn Community

10 Pawn Industry & Demography

12 Confiscation & Redemption Percentages

13 Impact of COVID-19

14 Mobile Trends

16 Top 6 Industry Trends

Methodology & Sources

Information and analysis presented in this report is produced using proprietary data from Bravo Store Systems,

unless otherwise cited. To protect the anonymity of Bravo customers, data is presented in the form of averages

across all Bravo customer locations.

Information presented represents data from January 1, 2020 to June 1, 2021, unless otherwise noted.

T R E N D S 2021 JUNE

54

Message from the CEO from Tally Mack

There were challenging moments during the Covid-19 pandemic when it seemed that everything had been turned upside down, leaving everyone with questions about when, if ever, the pawnbroking world would return to previous conditions.

Like most businesses, Bravo weathered the pandemic byleaning into our core purpose and focusing on serving our customers.As we navigated through unprecedented business conditions together with the roughly 1,300+ pawnshops that are supported through our platform, it reminded us of something that we've always known: Pawn doesn't quit.

Tally Mack, Chief Executive

Hello

As the industry leader in developing first-to-market software solutions and services to niche industries, we believe we are in a unique position to advocate for underserved and underrepresented markets through providing this critical insight. Some of the findings are unsurprising. For example, changes that were already afoot—like the shift towards mobile—were accelerated over the past year.

In our first PawnTech Report, we hope to spark an insightful dialogue about the critical nature of the non-recourse, secured, safety-net credit supplied by pawnshops millions of times each year. This data may also help clear up confusion about pawnshops as compared with other alternative lenders and help the public understand that no other creditor offers the same type of transaction provided by pawnbrokers. "

The purpose of this report is to share key industry data with the people who help shape our landscape (such as stakeholders, media and lawmakers) and to provide business operators with PawnTech trends that can help inform decisions about technology investments.

""

Trend Report | 2021 June

We know that in order to recover, it is necessary to take a deep dive into what the latest industry data is telling us.

888.407.6287 bravostoresystems.com 888.407.6287 bravostoresystems.com

6

Trend Report | 2021 June

7888.407.6287 bravostoresystems.com 888.407.6287 bravostoresystems.com

The Impact of the Pawn IndustryPawnbroking is the oldest source of credit. A pawn is a collateral loan. Pawnbrokers lend money on items of value ranging from gold and diamond jewelry to musical instruments, televisions, electronics, tools and equipment, firearms and more.

The amount of the loan is based on the value of the collateral. Pawn loans are typically small-dollar safety net loans. The interest charged, as well as the term, can vary from one state to the next. During the pawn transaction, customers receive a written explanation, called a pawn ticket, that explains the details, including the interest amount, how long the customer has to pay back the loan and more.

No other creditor offers the same type of transaction as do pawnbrokers.

A study by Vanderbilt University noted that Consumers seem to avoid making big financial mistakes when using pawnshops. Something about the

use of personal items (and particularly sentimental personal items) as collateral

may distinguish these loans from credit cards, payday loans, and the like in

terms of borrowers’ repayment and default behavior.

The 16% of Americans who are underbanked have some sort of bank account, but they also rely on alternative financial services.

According to the latest findings of the FDIC, 22% of American adults (63 million) are either

unbanked or underbanked.

22%U.S. adults unbanked

underbanked

The almost 6% of Americans who are unbanked have no bank account whatsoever and must rely on alternative financial products and services—such as payday loans, check cashing services, money orders and pawn shop loans—to take care of their finances.

5.4%U.S. adults

unbanked with no bank

whatsoever

16%

U.S. adults underbanked

"

"

8

Trend Report | 2021 June

9888.407.6287 bravostoresystems.com 888.407.6287 bravostoresystems.com

What are Non-Recourse Loans The distinction between recourse loans

and non-recourse loans comes into play if you cannot repay the money you’ve borrowed. According to the IRS,“recourse debt holds the borrower personally liable and allows lenders to collect what is owed for the debt even after they’ve taken collateral (home, credit cards). Recourse lenders have the right to garnish your wages, levy your accounts and impact your credit score. By contrast, a non-recourse debt (loan) does not allow the lender to pursue anything other than the collateral.”

Therefore, the primary difference oan favors the lender, while a non-recourse loan benefits the borrower. Payday loans are recourse loans, just like title loans and paycheck advances.

That means that if a borrower can’t repay a payday loan, it can hurt their credit, overdraw their bank account, incite calls from debt collectors and even cause wages to be garnished.

Additionally, payday lenders frequently allow borrowers to roll over their debt. This gives the customer more time to pay back the loan, but it also adds interest and fees, which increases their debt. This can happen over and over again, creating a cycle of debt that is difficult to break.

73k

approximate number of pawnshops in the U.S.10k

The Pawn CommunitySize of the Pawn Industry

How Pawn Differs from Other Financial InstitutionsPawnbrokers serve customers at every income level, but some rely on pawn loans because they do not have access to traditional banking products.

Most customers, as reflected on page 12, redeem their loans and simply pick up the item from the

pawnshop once they've repaid what they owe. Pawn loans are non-recourse, meaning if the customer does not

redeem their loan, it has no impact on their credit score. Rather, the item is forfeited to the pawnbroker, who then sells it in their shop— usually at a deeply discounted price

when compared to retail value.

*Multiplied approximate number of pawnshops in the U.S. and average number of employees across all Bravo customer locations.

estimated number of employees in the pawn industry*

10

Trend Report | 2021 June

Pawn Industry & Demography

Loans by Gender

MALE

Loans by Age Group

18-24$155.61

25-34$196.64

35-44$227.60

45-54$283.98

55-64$283.72

65+$244.46

Average loan amount

Average loan amount

FEMALE$288.20 $253.02

Rings

Chains

Watches

Bracelets

Miscellaneous Jewelry

Electronics

Firearms & Knives

Tools

Musical Instruments

Necklaces Top 10 Loan Categories

Loans by Loan Type

New Loan

Average loan amount

$187.01

888.407.6287 bravostoresystems.com 11888.407.6287 bravostoresystems.com

12

Trend Report | 2021 June

888.407.6287 bravostoresystems.com

13888.407.6287 bravostoresystems.com

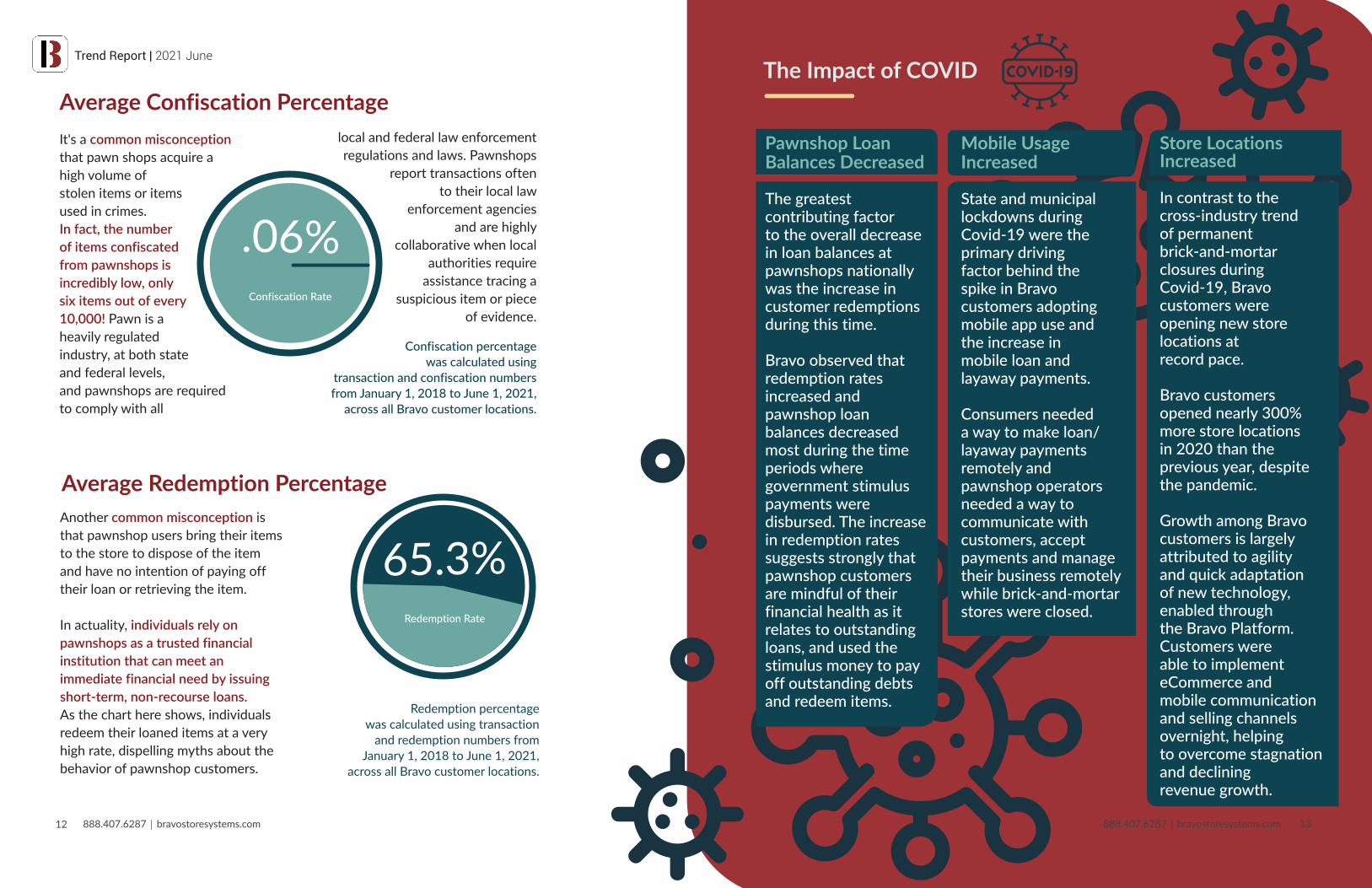

The Impact of COVID Average Confiscation Percentage

Average Redemption Percentage

It's a common misconception that pawn shops acquire a high volume of stolen items or items used in crimes. In fact, the number of items confiscated from pawnshops is incredibly low, only six items out of every 10,000! Pawn is a heavily regulated industry, at both state and federal levels, and pawnshops are required to comply with all

local and federal law enforcement regulations and laws. Pawnshops

report transactions often to their local law

enforcement agencies and are highly

collaborative when local authorities require

assistance tracing a suspicious item or piece

of evidence.

Confiscation percentage was calculated using

transaction and confiscation numbers from January 1, 2018 to June 1, 2021,

across all Bravo customer locations.

Another common misconception is that pawnshop users bring their items to the store to dispose of the item and have no intention of paying off their loan or retrieving the item.

In actuality, individuals rely on pawnshops as a trusted financial institution that can meet an immediate financial need by issuing short-term, non-recourse loans. As the chart here shows, individuals redeem their loaned items at a very high rate, dispelling myths about the behavior of pawnshop customers.

Redemption percentage was calculated using transaction

and redemption numbers from January 1, 2018 to June 1, 2021,

across all Bravo customer locations.

Pawnshop Loan Balances Decreased

The greatest contributing factor to the overall decrease in loan balances at pawnshops nationally was the increase in customer redemptions during this time.

Bravo observed that redemption rates increased and pawnshop loan balances decreased most during the time periods where government stimulus payments were disbursed. The increase in redemption rates suggests strongly that pawnshop customers are mindful of their financial health as it relates to outstanding loans, and used the stimulus money to pay off outstanding debts and redeem items.

Mobile Usage Increased

State and municipal lockdowns during Covid-19 were the primary driving factor behind the spike in Bravo customers adopting mobile app use and the increase in mobile loan and layaway payments.

Consumers needed a way to make loan/layaway payments remotely and pawnshop operators needed a way to communicate with customers, accept payments and manage their business remotely while brick-and-mortar stores were closed.

Store Locations Increased

In contrast to the cross-industry trend of permanent brick-and-mortar closures during Covid-19, Bravo customers were opening new store locations at record pace.

Bravo customers opened nearly 300% more store locations in 2020 than the previous year, despite the pandemic.

Growth among Bravo customers is largely attributed to agility and quick adaptation of new technology, enabled through the Bravo Platform. Customers were able to implement eCommerce and mobile communication and selling channels overnight, helping to overcome stagnation and decliningrevenue growth.

14

Trend Report | 2021 June

15888.407.6287 bravostoresystems.com 888.407.6287 bravostoresystems.com

Consumer Adoption and Usage of MobilePawn App

Percentage of Loan Payments Made Through MobilePawn App

Percentage of Layaway Payments Made Through MobilePawn App

14%

12%

10%

8%

6%

4%

2%

0%January 2018 January 2019 January 2020 January 2021

14%

12%

10%

8%

6%

4%

2%

0%January 2018 January 2019 January 2020 January 2021

Bravo Customer Adoption & Usage of MobilePawn App

# of Bravo Customers Using Mobile Pawn

January 2018 January 2019 January 2020 January 2021

800

700

600

500

400

300

200

100

0

16-20k110kconsumer downloads of MobilePawn

payments made through MobilePawn each month

Consumers with MobilePawn are

200x more likely to redeem than forfeit

16

Trend Report | 2021 June

888.407.6287 bravostoresystems.com

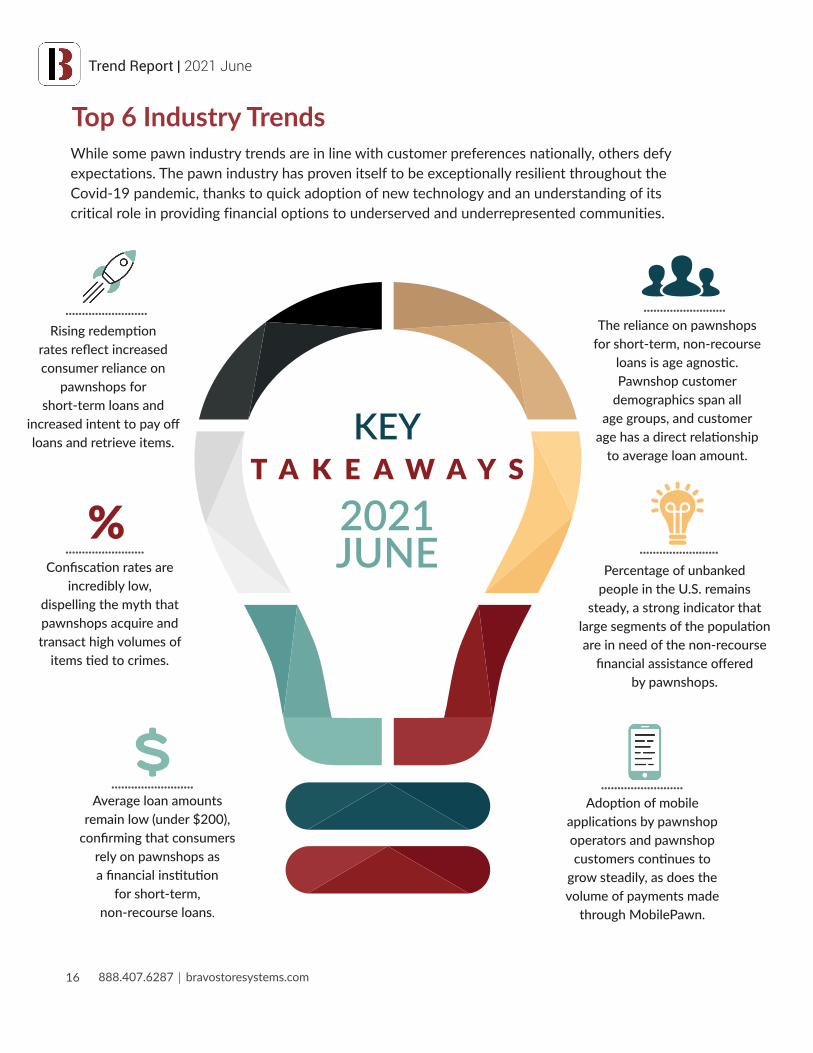

Top 6 Industry TrendsWhile some pawn industry trends are in line with customer preferences nationally, others defy expectations. The pawn industry has proven itself to be exceptionally resilient throughout the Covid-19 pandemic, thanks to quick adoption of new technology and an understanding of its critical role in providing financial options to underserved and underrepresented communities.

KEYT A K E A W A Y S

2021 JUNE

Adoption of mobile applications by pawnshop operators and pawnshop customers continues to

grow steadily, as does the volume of payments made

through MobilePawn.

Rising redemption rates reflect increased consumer reliance on

pawnshops for short-term loans and

increased intent to pay off loans and retrieve items.

Confiscation rates are incredibly low,

dispelling the myth that pawnshops acquire and transact high volumes of

items tied to crimes.

Average loan amounts remain low (under $200),

confirming that consumers rely on pawnshops as a financial institution

for short-term, non-recourse loans.

The reliance on pawnshops for short-term, non-recourse

loans is age agnostic. Pawnshop customer

demographics span all age groups, and customer

age has a direct relationship to average loan amount.

Percentage of unbanked people in the U.S. remains

steady, a strong indicator that large segments of the population are in need of the non-recourse

financial assistance offered by pawnshops.

%