European Banking Trend Radar 2021 - deloitte.com

30

European Banking Trend Radar 2021 Edition 1: The Client Perspective

Transcript of European Banking Trend Radar 2021 - deloitte.com

European Banking Trend Radar 2021Edition 1: The Client Perspective

Investing in Germany | A guide for Chinese businesses

02

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

03

Executive summary 04

Why systematically monitoring trends in banking matters 06

A structured process to identify, categorize, and monitor trends 08

Six banking trend dimensions 10

The banking trend radar 12

The way forward 26

End notes 27

Contacts 28

Investing in Germany | A guide for Chinese businesses

04

• This study develops a methodology to screen and assess trends that shape the future of the European banking land-scape.

• We have split our trends into six dimen-sions. This edition covers the first of these, the client perspective.

• Our systematic process evaluates trends along two measures: The size of the impact that they will have in the future and the time it takes to adopt them. Depending on where they fall on the matrix, we assign one of three priority levels to each trend: act, prepare, or watch.

• In the ‘act’ category, cross-generational experience is most pressing. It is char-acterized by high impact and two to four years until adoption. Therefore, taking action is imperative as the trend is already well advanced.

• In the ‘prepare’ category, hyper-personali-zation ranks as the most significant trend and adoption is expected within the next four to six years. The trend is fairly advanced and justifies preparation.

• In the ‘watch’ category, crowdbanking is the most relevant trend. Mainstream adoption will take place within the next four to six years, but its impact in the foreseeable future is rather low. Thus, at this point in time it would be sufficient to observe the trend.

Executive summary

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

05

Investing in Germany | A guide for Chinese businesses

06

Why systematically monitoring trends in banking matters

Fig. 1 – Global Economic Policy Uncertainty Index (January 2006 – May 2021)

Source: Economic Policy Uncertainty, www.policyuncertainty.com.

02006

Financial CrisisSep. 2007

Euro CrisisApr. 2010

2021

50

100

150

200

250

300

350

400

450

500

Brexit ReferendumJun. 2016

1st Wave COVID-19Mar. 2020 2nd Wave

COVID-19Nov. 2020

Trade ConflictsMay 2018

In a world that is constantly changing, mar-ket participants need to cope with uncer-tain future developments. The dynamics of change force companies to adapt rapidly in several dimensions, such as technological advancements, changes in culture and soci-ety, climate challenges, economic develop-ments, and many others.

In the wake of the COVID-19 crisis, uncer-tainty increased even further. Unsurpris-ingly, the levels measured by the Global

Economic Policy Uncertainty Index (based on sentiments expressed in newspaper articles) peaked in spring 2020 when the pandemic hit Europe (see figure 1). Since then, insecurity about economic, social, and public developments has remained high. The recent crisis brought unprece-dented challenges for companies – and banking is no exception. COVID-19 reshaped the banking industry in several ways: it affected the competitive landscape, the role of branches, and growth in some

traditional product areas. At the same time, the pandemic accelerated innovation and digitization in almost every sphere of bank-ing and capital markets.1 Thus, it is essential for companies to adapt to potential trends and changes at an increasing pace.

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

07

However, many of these forces have already been moving the financial industry since the last decade. In fact, the European banking sector has been subject to massive structural change in the wake of the global financial crisis. Regulations became more and more stringent, while the macro- financial environment was extraordinarily challenging and new competitors entered the market.2 In addition, the increasingly digital operational environment and changing values led to new customer expectations. This has put traditional banking business models to the test, and it is not expected that this transformation will slow down, let alone stop, any time soon. However, banks frequently struggle to adapt quickly and successfully to new developments since it is almost impossible to predict how the numerous and often interdependent trends and drivers will affect the market. Some benefit the banks, others disrupt business. The challenge of anticipating future developments and their impact on the market highlights the impor-tance of systematically monitoring trends in banking.

To respond to such uncertainty, banks must start by identifying all relevant trends in the market. At the same time, it is also necessary to continuously review

and update the trends already collected. However, it is not enough to list trends and drivers, they must also be evaluated and analyzed.

To do so systematically and in an ongoing fashion, it is vital to establish a structured trend monitoring system that is based on a well-defined process. We have developed a framework that helps banks navigate uncertainty and supports them in defining future-proof business models.

Banks must identify, update and analyze trends to respond to uncertainty.

Investing in Germany | A guide for Chinese businesses

08

A structured process to identify, categorize, and monitor trends

Trend research is challenging since there is typically a plethora of trends and innova-tions to be monitored. Therefore, keeping track of the market and identifying those trends that are likely to have the highest impact on banking are complex tasks. We provide a structured approach to this exercise based on a specific trend tool. By developing a systematic process to detect trends, recognize patterns, and evaluate them, we aim to monitor the development of banking trends in both the short and the long run. To do so, our approach follows a three-step procedure.

1. Trend screening First, we created a comprehensive data-base containing a variety of existing and emerging trends on the European banking market. In doing so, we screened a large amount of data from external3 and internal sources, selected all relevant information, and identified numerous banking trends. A group of experts then pre-selected the most relevant trends, which can be catego-rized into three levels:

• The first layer is micro-trends, which are specific innovations or projects that already exist today and provide use cases for a macro-trend. Overall, we collected about 600 micro-trends that are relevant to the European banking industry.4

• Macro-trends describe the underly-ing core aspect that is common to the respective micro-trends. Therefore, every micro-trend is assigned to one or more macro-trends. Focusing only on the most important items, we ended up with 45 macro-trends, which we included in our banking trend radar (see figure 4).

• The last layer consists of mega-trends. It describes overarching and long-lasting phenomena that lead to extensive struc-tural change. In order to categorize the considerable number of banking trends, we clustered the mega-trend level and derived six main dimensions. These categories aim to capture the key trend drivers in the banking market. We provide a more detailed description of the six dimensions in the next section.

2. Trend assessment In the second step, we set up a survey and asked banking experts to assess the 45 pre-selected trends at the macro-level with respect to two aspects: their potential influ-ence and expected time until mainstream adoption.

Influence describes the size of the impact that the trend is likely to have on the European banking market. Time of main-stream adoption refers to the point in time at which most market participants in the industry are likely to have applied the trend in one way or another.

3. Trend radar The third step is to derive an interactive trend radar from our evaluation results. Depending on the expert assessment of influence and time until mainstream adop-tion, each trend is assigned to one of three categories within the radar: watch, prepare, or act. ‘Act’ consists of all trends that have a high or very high influence where main-stream adoption is expected within the next five years. ‘Prepare’ includes trends that are not part of the ‘act’ category, have a rather high to very high influence, and with mainstream adoption expected within seven years. The ‘watch’ category contains all remaining trends with a low to very high influence and mainstream adoption taking more than ten years.

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

09

Fig. 2 – Framework for ranking trends in the radar

0–2

Very

hi

ghH

igh

Rath

er

high

Rath

er

low

Low

Very

low

2–4 4–6 6–8 8–10 10+

Mainstream adoption (in years)

Act

Prepare

Watch

Out of scope

Influe

nce

Source: Trend One.

Investing in Germany | A guide for Chinese businesses

10

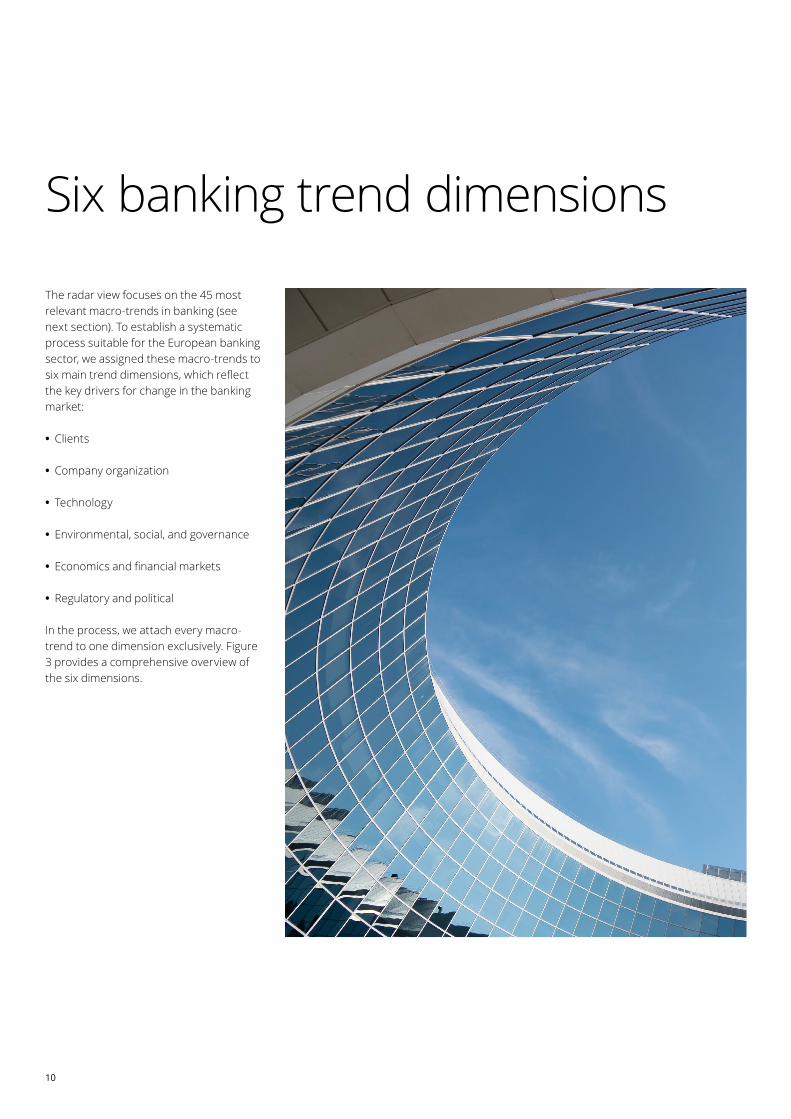

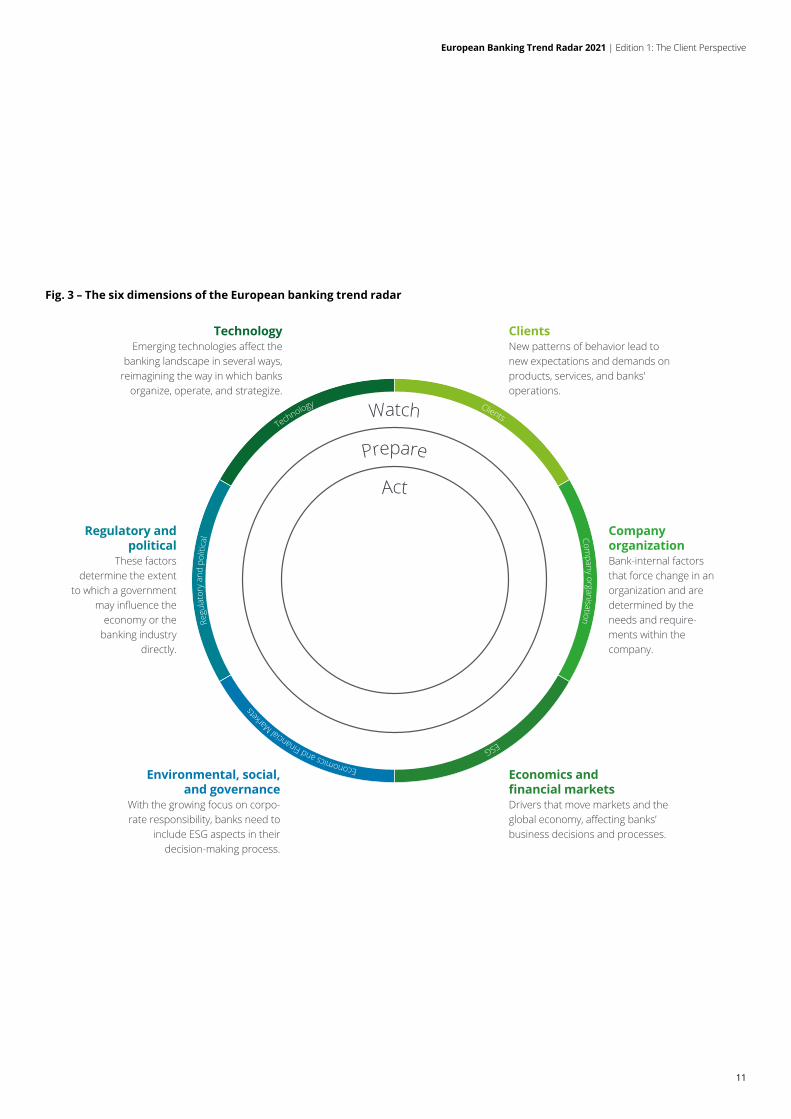

Six banking trend dimensions

The radar view focuses on the 45 most relevant macro-trends in banking (see next section). To establish a systematic process suitable for the European banking sector, we assigned these macro-trends to six main trend dimensions, which reflect the key drivers for change in the banking market:

• Clients

• Company organization

• Technology

• Environmental, social, and governance

• Economics and financial markets

• Regulatory and political

In the process, we attach every macro- trend to one dimension exclusively. Figure 3 provides a comprehensive overview of the six dimensions.

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

11

Six banking trend dimensions

Fig. 3 – The six dimensions of the European banking trend radar

ClientsNew patterns of behavior lead to new expectations and demands on products, services, and banks' operations.

Regulatory and political

These factors determine the extent

to which a government may influence the

economy or the banking industry

directly.

TechnologyEmerging technologies affect the

banking landscape in several ways, reimagining the way in which banks

organize, operate, and strategize.

Company organizationBank-internal factors that force change in an organization and are determined by the needs and require-ments within the company.

Economics and financial marketsDrivers that move markets and the global economy, affecting banks’ business decisions and processes.

Environmental, social, and governance

With the growing focus on corpo-rate responsibility, banks need to

include ESG aspects in their decision-making process.

ESG

Economics and Financial M

ark

ets

Regu

lato

ry a

nd P

oliti

cal Com

pany Organisation

ClientsTechnology

ESG

Economics and Financial M

ark

ets

Regu

lato

ry a

nd p

oliti

cal Com

pany organisation

ClientsTechnology Watch

Prepare

Act

Investing in Germany | A guide for Chinese businesses

12

The banking trend radar

The six trend dimensions also define the structure of our trend radar, as illus-trated in figure 4. All 45 macro-trends are located according to the result of the expert assessment: (1) the closer to the center a macro-trend is on the radar, the more mature it is; and (2) the larger the trend bubble, the higher its impact on the banking industry. As the radar is evolving constantly, it may be adjusted from edition to edition.

In this edition, we take a closer look at a first set of macro-trends on the radar, i.e. we focus on one trend dimension to illus-trate the results. The remaining dimensions will be covered in future editions. We chose the client perspective as our first dimen-sion because this highly relevant area is currently facing extraordinary disruptions. In particular, the client dimension is pri-marily driven by changing customer needs, which have been heavily influenced by the recent crisis.

The client perspective Banks increasingly face new client behav-iors and expectations. This first trend dimension is certainly one of the key drivers for change in banking and covers different aspects of relevant mega-trends. A multitude of reasons leads to this con-clusion. First of all, factors such as chang-ing social values and an expectation that companies will offer true added value lead to new patterns of behavior. Second, social diversity and distinct individual needs are increasingly acknowledged and therefore banks should factor them in. Furthermore,

higher affinity with digital and technological aspects shapes consumer preferences for everyday banking activities. Lastly, global developments and economic events such as the COVID-19 pandemic may also push clients to adapt their behavior.

As a result, customers place new expecta-tions and demands on banking products, services, and banks' operations, and at an accelerating speed. New standards are emerging for financial services compa-nies since customer centricity is a major competitive differentiator. Banks should therefore ensure that they provide the best seamless experience to their customers. This raises the question: What can banks do to react to changing client preferences and know which trends to watch and when to act?

In the following, we discuss the potential impact of nine central client-related trends. The resulting banking trend radar is illus-trated in figure 4.

Customers place new expectations and demands on banking products, services, and banks' operations.

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

13

Fig. 4 – Banking trend radar with focus on client trends

ESG

Economics and Financial M

ark

ets

Regu

lato

ry a

nd p

oliti

cal Com

pany organisation

ClientsTechnology

Watch

Prepare

Act

Client Empowerment

Cross-GenerationalExperience

The TransparencyParadigm-Shift Data

Awareness

Playful Banking

Age of Crowdbanking

Hyper-Personalized Banking

Social Channel Banking

Future of Loans

Note: Figure 4 illustrates a static view of the interactive banking trend radar.

Investing in Germany | A guide for Chinese businesses

14

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

15

Cross-generational experience

What is it about? We begin with the most pressing trend, which is to provide distinct experiences to different generations. The trend is driven primarily by the divergence in customer expectations in various age groups. Millen-nials and Generation Z have grown up in an environment shaped by the advancement of the information age. Technically savvy, they are able to communicate with phys-ically distant people and quickly gather information from all types of sources. This has also changed their values, their views, and the way they want to be treated – including with respect to their finances. Overall, they demand high-quality products and services that meet their specific per-sonal needs.5,6

Simultaneously, Baby Boomers account for an increasing market share in the banking sector due to demographic changes. Less drawn to digital innovation, this generation has different customer requirements. New challenges for banks arise as a one-size-fits-all approach will not accommodate the growing generational gap. As a result, finan-cial institutions tailor their offerings to each generation separately. They either develop distinct products for each generation or design a single product in a way that it appeals to customers across generations.7

What is happening in the market? A number of banks have already imple-mented specific marketing strategies to address this trend. Targeting different generations on corresponding channels with tailored campaigns is key to success-fully creating a brand that appeals to more than one group. Further, there are banks that have adapted their product portfolios. Financial platforms with innovative features have been developed to target younger generations. Other examples can be found in the credit card space, where banks often follow multi-product strategies offering different types of credit cards to different age groups. Recent innovations are mostly driven by US companies; by contrast, European financial institutions are slower to respond to the trend. It is also important to note that digital innovations typically target younger generations, while older generations’ interests are often ignored despite higher financial means. This leads to unused potential.8

As mainstream adoption is expected within the next two to four years and the impact is high, cross-generational experience falls into the ‘act’ category and is our most imperative trend in the client dimension. It is therefore essential for banks to ramp up customization with respect to serving different generations.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

Investing in Germany | A guide for Chinese businesses

16

Data awareness

What is it about? Our second most important trend takes longer to adopt and revolves around data. The advancement of digitization has led to an enormous stream of data generated every day. Typically, users who provide data input quickly lose control of it: They often do not know which data was collected, stored, shared, or analyzed. On the other hand, awareness of these issues is growing rapidly, as are concerns about data mis-use. Therefore, customers desire to regain control over the personal information they provide. Banks are particularly affected by this trend as they deal with highly sensi-tive financial data. Two key components contribute to help customers successfully manage their data in a self-sufficient and responsible way. First, banks must estab-lish technical infrastructure that offers clients control over their data. The second component is data literacy: Customers need expertise and knowledge on the topic to make informed decisions. Several examples demonstrate the significant impact this trend has had on the financial sector over recent years and will have in the future.

What is happening in the market? The examples that we observe in the mar-ket include banks in Europe that have run advertising campaigns to inform consum-ers about data security matters and raise awareness. Other companies, specializing on digital innovation in the payment space, have developed credit cards for one-time use and cryptocurrencies that can verify transactions while hiding details. Thus, only necessary data is transmitted, which helps to prevent fraud. Tech companies also apply cryptocurrency and blockchain technology to create markets where users can sell their data directly via newly devel-oped apps.9

Banks can play a vital role in these develop-ments. As specialists for payment services and storage, they need to embrace cyber and data security technology to transfer traditional business into the digital age.

The trend is characterized by a high influ-ence and mainstream adoption within the next four to six years. Even though it is slightly less imminent than cross- generational experience, the expert assessment underlines that market partic-ipants should act immediately to consider these developments.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

17

Client empowerment

What is it about? Client empowerment is a trend toward let-ting customers conduct banking business independently and autonomously. Suc-cessful client empowerment heavily relies on transferring knowledge to customers in a way that guarantees understanding, since banks must ensure that customers are able to make informed and responsible decisions. This is key for financial services providers as faulty decisions can result in particularly grave consequences.

The purpose of client empowerment is two-fold. Firstly, it can enhance user experience by providing a sense of control. For certain customer groups, this increases engage-ment and motivation. Secondly, integrating clients into the value chain inherently reduces costs as consumers take on employees’ tasks. To do so effectively, client empowerment requires adopting the latest technology to facilitate the transition.

What is happening in the market? Due to the advancement of the trend, measures are already being undertaken to promote client empowerment. Banks are shifting from a product-centric view to a need-based customer strategy.10 The new need-based paradigm fosters client empowerment as it is more straightfor-ward to inform customers about how to meet their needs instead of teaching them about products. To do so effectively, companies have opened learning centers where customers can train their financial knowledge. These brick-and-mortar stores are equipped with innovative technology to offer an efficient and enjoyable learning experience. Alternatively, physical locations are not always necessary: Companies are developing learning software and mobile apps to transfer knowledge to clients and reduce costs.11

Similar to the previous trend, our expert assessment predicts a high influence with a four- to six-year time horizon for main-stream adoption. Consequently, client empowerment is an equally urgent matter.

Watch

Prepare

Act

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Investing in Germany | A guide for Chinese businesses

18

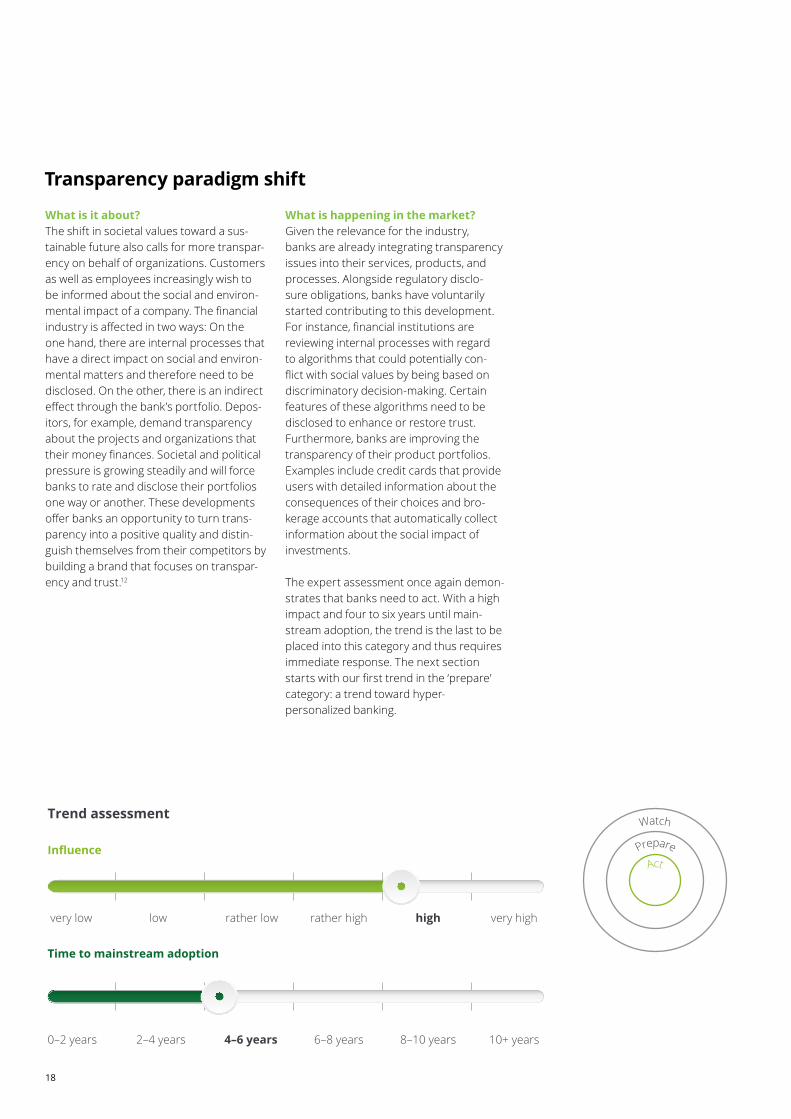

Transparency paradigm shift

What is it about? The shift in societal values toward a sus-tainable future also calls for more transpar-ency on behalf of organizations. Customers as well as employees increasingly wish to be informed about the social and environ-mental impact of a company. The financial industry is affected in two ways: On the one hand, there are internal processes that have a direct impact on social and environ-mental matters and therefore need to be disclosed. On the other, there is an indirect effect through the bank’s portfolio. Depos-itors, for example, demand transparency about the projects and organizations that their money finances. Societal and political pressure is growing steadily and will force banks to rate and disclose their portfolios one way or another. These developments offer banks an opportunity to turn trans-parency into a positive quality and distin-guish themselves from their competitors by building a brand that focuses on transpar-ency and trust.12

What is happening in the market? Given the relevance for the industry, banks are already integrating transparency issues into their services, products, and processes. Alongside regulatory disclo-sure obligations, banks have voluntarily started contributing to this development. For instance, financial institutions are reviewing internal processes with regard to algorithms that could potentially con-flict with social values by being based on discriminatory decision-making. Certain features of these algorithms need to be disclosed to enhance or restore trust. Furthermore, banks are improving the transparency of their product portfolios. Examples include credit cards that provide users with detailed information about the consequences of their choices and bro-kerage accounts that automatically collect information about the social impact of investments.

The expert assessment once again demon-strates that banks need to act. With a high impact and four to six years until main-stream adoption, the trend is the last to be placed into this category and thus requires immediate response. The next section starts with our first trend in the ‘prepare’ category: a trend toward hyper- personalized banking.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

19

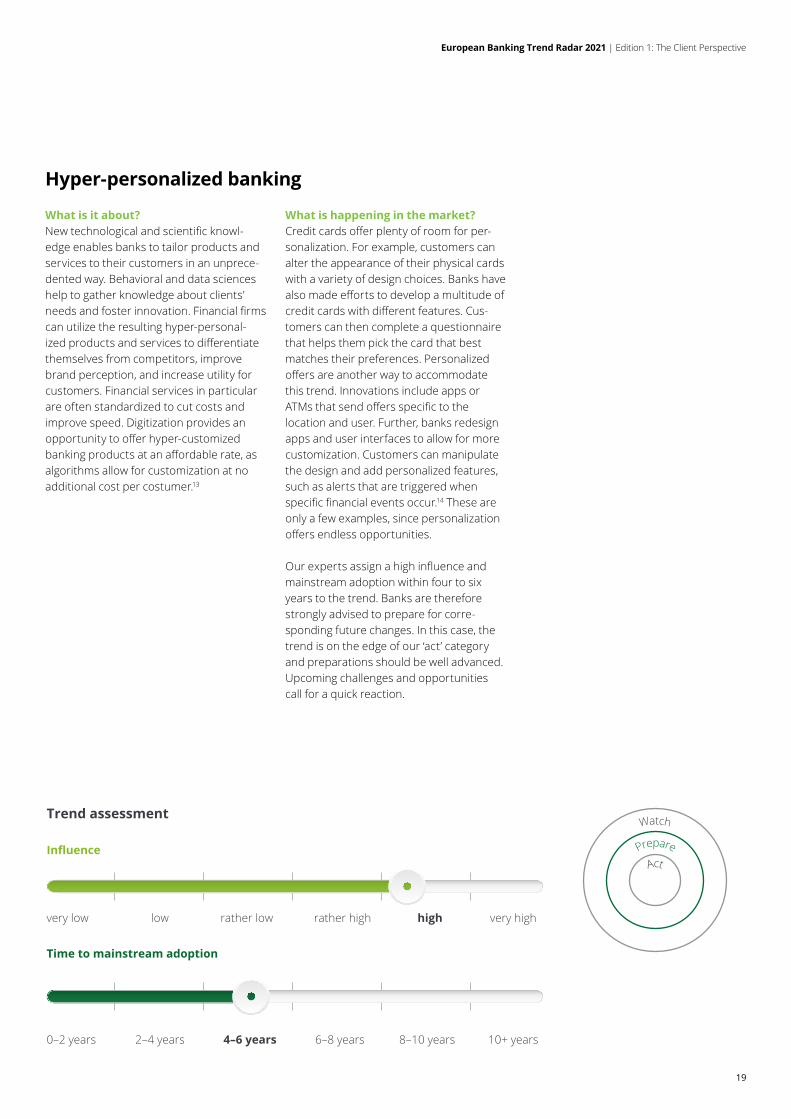

Hyper-personalized banking

What is it about? New technological and scientific knowl-edge enables banks to tailor products and services to their customers in an unprece-dented way. Behavioral and data sciences help to gather knowledge about clients’ needs and foster innovation. Financial firms can utilize the resulting hyper-personal-ized products and services to differentiate themselves from competitors, improve brand perception, and increase utility for customers. Financial services in particular are often standardized to cut costs and improve speed. Digitization provides an opportunity to offer hyper-customized banking products at an affordable rate, as algorithms allow for customization at no additional cost per costumer.13

What is happening in the market? Credit cards offer plenty of room for per-sonalization. For example, customers can alter the appearance of their physical cards with a variety of design choices. Banks have also made efforts to develop a multitude of credit cards with different features. Cus-tomers can then complete a questionnaire that helps them pick the card that best matches their preferences. Personalized offers are another way to accommodate this trend. Innovations include apps or ATMs that send offers specific to the location and user. Further, banks redesign apps and user interfaces to allow for more customization. Customers can manipulate the design and add personalized features, such as alerts that are triggered when specific financial events occur.14 These are only a few examples, since personalization offers endless opportunities.

Our experts assign a high influence and mainstream adoption within four to six years to the trend. Banks are therefore strongly advised to prepare for corre-sponding future changes. In this case, the trend is on the edge of our ‘act’ category and preparations should be well advanced. Upcoming challenges and opportunities call for a quick reaction.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

Investing in Germany | A guide for Chinese businesses

20

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

21

Social channel banking

What is it about? Social media are now an integral part of modern marketing strategies across all industries – and banks should prepare for this highly relevant trend. Younger gener-ations frequently refrain from consuming traditional media and can more easily be targeted via online channels. For banks, this is particularly challenging, as financial topics are not usually in line with younger people’s interests and can be considered conservative.

Influencer marketing is steadily replacing traditional advertising, making it a tool for banks to appeal to a younger target group. Financial institutions could consider reaching out to influencers to help banks enhance their social media strategies. Influencers are content providers who have generated extensive reach on social media platforms. They often shape user opinions by publicly sharing their own views and engaging with their followers. On the one hand, banks can cooperate with influenc-ers for traditional marketing purposes. On the other, they can profit from provid-ing influencers with innovative products and financial tools. The latest trends also include virtual influencers, where an ani-mated character stands in for the human influencer.

What is happening in the market? A great number of use cases and oppor-tunities for banks emerge from this trend. Compared to the EU, US companies are taking more chances here, as the vari-ety and reach of social media channels that cover financial topics are more pro-nounced. German banks, for instance, actively maintain social media channels, but they lack an innovative approach. By contrast, efforts to integrate blockchain technology into the world of influencing are being undertaken in the US and Asia. Innovations include digital currencies that facilitate interactions and payments between influencers and their audience.15

For this trend, our expert assessment results in an influence that is rather high and mainstream adoption of four to six years, which emphasizes that banks need to prepare.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

Investing in Germany | A guide for Chinese businesses

22

Future of loans

What is it about? Innovation in the market for loans is a constant process. Given the rather strong industry impact of this trend, banks increasingly need to address changing consumer behavior and technological dis-ruption. Novel features have emerged from digitization, e.g. repayment mechanisms that depend on various data inputs. Fur-thermore, there is a tendency to automate steps in the loan lifecycle and at the same time increase individualization. Digital tech-nologies allow this efficiently. Lastly, the growing popularity of products that feature social and community-related aspects has spilled over to the credit market. Innovative loan products take these developments into account.16

What is happening in the market? As this trend draws heavily on digital inno-vation, recent applications often rely on artificial intelligence and machine learning. Among other things, new technologies allow banks and fintech companies to collect non-traditional data, such as GPS or call history. The data can be analyzed with novel algorithms to optimize credit risk assessments for personal loans. In B2B markets, AI algorithms evaluate real-time data from machines to determine short-term funding requirements.17 Moreover, banks have introduced pay-per-use loans, which are characterized by flexible repay-ment rates that depend on the machine’s data input, such as utilization. There are also innovative loan products that do not depend on data analytics. Recent examples include platforms to save and lend money in social groups or attempts to provide resi-dents in rural areas of developing countries with loans via existing instant messaging apps.18 Due to their prevalence and con-venience, instant messaging apps may also become relevant for the European credit market. Strategic partnerships with tech companies are key to successfully taking advantage of opportunities that the trend gives rise to.

The expert assessment is close to the preceding trend and therefore banks are strongly recommended to start prepara-tions. This is the final trend to fall into this category and we continue with the remain-ing two trends that we have placed in the ‘watch’ category.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

23

Age of crowdbanking

What is it about? Crowdfunding describes a form of investing where a large number of people individu-ally invest a small sum to fund a company or project. Therefore, projects can profit from collective intelligence as an entire group of people is involved. Benefits arise when investors come from diverse back-grounds and contribute expertise from various fields. Digital platforms provide a tool for matching investors with projects and foster communication between all par-ticipants. Banks can play an important role in this process. They can cooperate with fintech companies to develop and provide these platforms and collect fees for the service. Financing is direct and customers take on the risks. Further, financing is not restricted to equity but may also include debt, intermediate, or social forms.

What is happening in the market? Innovations include platforms that enable founders to accept cryptocurrencies as a form of payment. Other platforms focus on social aspects and assign investors to certain groups, such as “family and friends” or “friends of friends”. Furthermore, banks support or develop social crowdfunding platforms that mostly feature non-profit projects as part of their marketing strategy. In addition, crowdfunding is constantly expanding its scope. Recently, more plat-forms have specialized in political cam-paigning. This gives smaller interest groups who face difficulties with generating suf-ficient attention an opportunity to collect funds and increase their reach.

Even though crowdfunding has been around for several years and continues to evolve, the direct impact on the banking industry is rather small compared to other client-related trends. The expert assess-ment therefore results in a recommenda-tion to watch the trend.

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Watch

Prepare

Act

Investing in Germany | A guide for Chinese businesses

24

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

25

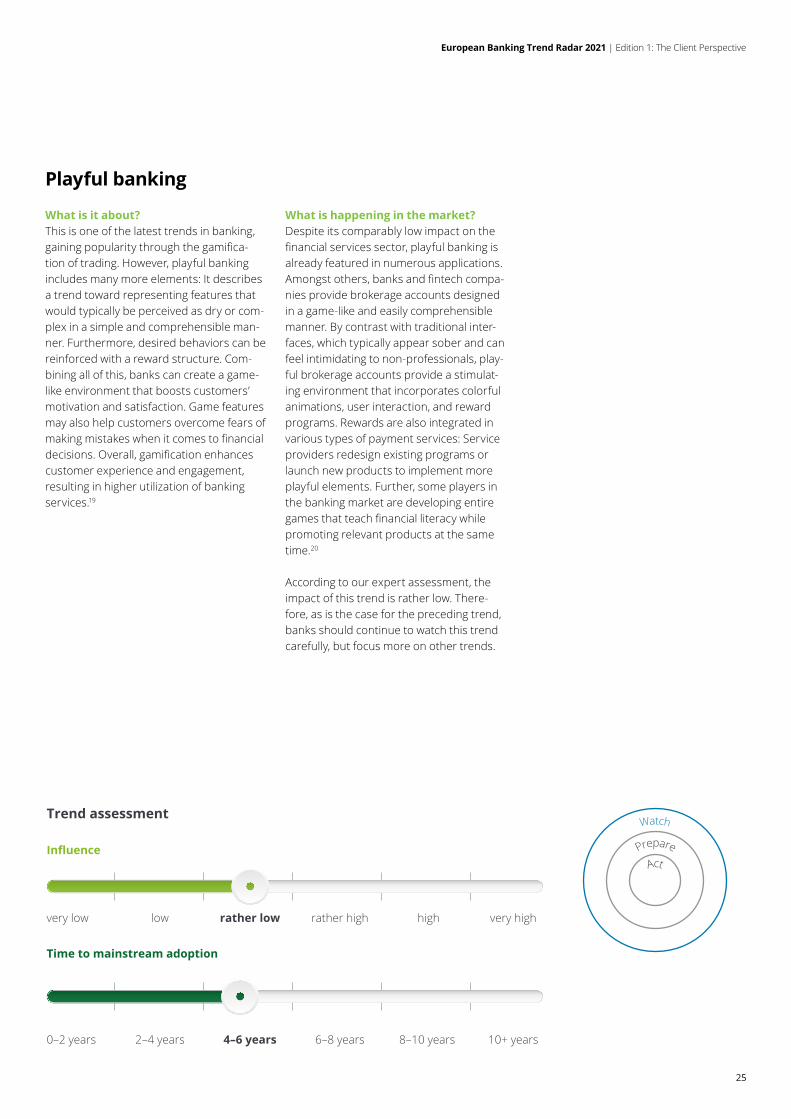

Playful banking

What is it about? This is one of the latest trends in banking, gaining popularity through the gamifica-tion of trading. However, playful banking includes many more elements: It describes a trend toward representing features that would typically be perceived as dry or com-plex in a simple and comprehensible man-ner. Furthermore, desired behaviors can be reinforced with a reward structure. Com-bining all of this, banks can create a game-like environment that boosts customers’ motivation and satisfaction. Game features may also help customers overcome fears of making mistakes when it comes to financial decisions. Overall, gamification enhances customer experience and engagement, resulting in higher utilization of banking services.19

What is happening in the market? Despite its comparably low impact on the financial services sector, playful banking is already featured in numerous applications. Amongst others, banks and fintech compa-nies provide brokerage accounts designed in a game-like and easily comprehensible manner. By contrast with traditional inter-faces, which typically appear sober and can feel intimidating to non-professionals, play-ful brokerage accounts provide a stimulat-ing environment that incorporates colorful animations, user interaction, and reward programs. Rewards are also integrated in various types of payment services: Service providers redesign existing programs or launch new products to implement more playful elements. Further, some players in the banking market are developing entire games that teach financial literacy while promoting relevant products at the same time.20

According to our expert assessment, the impact of this trend is rather low. There-fore, as is the case for the preceding trend, banks should continue to watch this trend carefully, but focus more on other trends.

Watch

Prepare

Act

very low low rather low rather high high very high

0–2 years 2–4 years 4–6 years 6–8 years 8–10 years 10+ years

Trend assessment

Influence

Time to mainstream adoption

Investing in Germany | A guide for Chinese businesses

26

The way forward

The unprecedented situation since spring 2020 has once again highlighted the dynamics of change. It is important for banks to respond to new trends and driv-ers that are transforming the market. This inspired us to set up a systematic process for trend monitoring and evaluation in banking to help market participants to navigate uncertainty.

In this edition, we focused on the first of six trend dimensions: The client perspective. We will take a closer look at the other five dimensions of the banking trend radar in upcoming editions:

• Company organization

• Economics and financial markets

• Environmental, social, and governance

• Regulatory and political

• Technology

It is important for banks to respond to new trends and drivers that are transforming the market.

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

27

End notes01. Deloitte, 2021 banking and capital markets outlook: Strengthening resilience, accelerating

transformation, December 2020. https://www2.deloitte.com/global/en/insights/industry/financial-services/financial-services-industry-outlooks/banking-industry-outlook.html

02. Bank for International Settlement, Structural changes in banking after the crisis, CGFS Papers No. 60, January 2018.

03. TrendOne04. For the sake of clarity, the large number of micro-trends is not directly integrated in the radar view.05. The Deloitte Global 2021 Millennial and Gen Z Survey. Deloitte 2021. https://www2.deloitte.com/

content/dam/Deloitte/global/Documents/2021-deloitte-global-millennial-survey-report.pdf06. Banking for Millennials - What do they want from banks? Deloitte 2019. https://www2.deloitte.com/

lu/en/pages/banking-and-securities/articles/banking-for-millenials.html07. Source: Deloitte Analysis, Trend One Database.08. Source: Deloitte Analysis, Trend One Database.09. Source: Trend One.10. Deloitte Perspectives: Re-envisioning the customer banking experience, https://www2.deloitte.

com/uk/en/pages/financial-services/articles/re-envisioning-the-customer-banking-experience.html11. Source: Deloitte Analysis, Trend One Database.12. See for example: Deloitte Perspectives, Transparency builds trust, https://www2.deloitte.com/

au/en/pages/financial-services/articles/transparency-builds-trust.html or Deloitte 2020: ESG risk disclosures for banks - The path to transparency: https://ukfinancialservicesinsights.deloitte.com/post/102guay/esg-risk-disclosures-for-banks-the-path-to-transparency

13. The future of retail banking - The hyper-personalisation imperative. Deloitte 2020. https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/financial-services/deloitte-uk-hp-the-future-of-retail-banking.pdf

14. Source: Deloitte Analysis, Trend One Database.15. Source: Deloitte Analysis, Trend One Database.16. The Future of Credit - A European perspective. Deloitte and Mastercard 2019. https://www2.

deloitte.com/uk/en/pages/financial-services/articles/the-future-of-consumer-credit-in-europe.html17. Deloitte 2020: The multiplier effect: The imperative for coordinated technology deployment in

financial services, https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Financial-Services/gx-fsi-wef-summary.pdf

18. Source: Trend One.19. Gamification in Private Banking & Wealth Management - Strengthening Client Experience and

Proximity. Deloitte2020. https://www2.deloitte.com/ch/en/pages/financial-services/articles/gamification-in-private-banking-and-wealth-management.html

20. Source: Deloitte Analysis, Trend One Database.

Investing in Germany | A guide for Chinese businesses

28

Tilmann BolzeDirectorBanking Operations ConsultingTel: +49 172 2073 [email protected]

Dr. Hans-Martin KrausPartnerFSI TransformationTel: +49 151 5807 [email protected]

Dr. Alexander BörschChief Economist & DirectorResearchTel: +49 89 29036 [email protected]

Anna Elin SeidelAssociate ManagerTrend Research Tel: +49 89 29036 [email protected]

For more information please visit us here: www.deloitte.com/de/banking-trend-radar

Thomas PeekPartnerRisk AdvisoryTel: +49 179 6913 [email protected]

Jörg EngelsPartner & Sektor Lead Banking & Capital MarketsTel: +49 177 8772 [email protected]

Dr. Florian KleinDirector & Head of Foresight Consulting Tel: +49 69 9713 [email protected]

Contacts

European Banking Trend Radar 2021 | Edition 1: The Client Perspective

29

For more information please visit us here: www.deloitte.com/de/banking-trend-radar

Investing in Germany | A guide for Chinese businesses

30

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/de/UeberUns to learn more.

Deloitte provides industry-leading audit and assurance, tax and legal, consulting, financial advisory, and risk advisory services to nearly 90% of the Fortune Global 500® and thousands of private companies. Legal advisory services in Germany are provided by Deloitte Legal. Our professionals deliver measurable and lasting results that help reinforce public trust in capital markets, enable clients to transform and thrive, and lead the way toward a stronger economy, a more equitable society and a sustainable world. Building on its 175-plus year history, Deloitte spans more than 150 countries and territories. Learn how Deloitte’s more than 345,000 people worldwide make an impact that matters at www.deloitte.com/de.

This communication contains general information only, and none of Deloitte GmbH Wirtschaftsprüfungsgesellschaft or Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser.

No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate and independent entities.

Issue 11/2021