Passive Insights - DeutscheAM Insights... · db X-trackers ETF Team Winchester House ... asset...

48

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 1 Passive Insights March 2017 Marketing Material. Confidential. For non- individual Professional Clients (MiFID Directive 2004/39/EC Annex II) only. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA). For institutional investors only. Further distribution of this material is strictly prohibited. Sector Rotation: a multi-factor perspective Deutsche Bank AG Deutsche Asset Management db X-trackers ETF Team Winchester House 1 Great Winchester Street London EC2N 2DB United Kingdom [email protected] etf.deutscheam.com Authors Vincent Denoiseux [email protected] Pierre Debru [email protected] Verity Worsfold [email protected] Bhavesh Warlyani [email protected] Vivek Dinni [email protected] Tanuj Dora [email protected] Roopal Pareek [email protected] Contents 1. Executive Summary 1 2. Sectors: ideal building blocks for portfolios 2 3. Factor Identification and Statistical Testing 5 4. The sector assessment framework: Monthly insights on sector investing 31 “Buy low and sell high. It's pretty simple. The problem is knowing what's low and what's high.” Jim Rogers This marketing document has been produced for information purposes only by a Structuring function of Deutsche AM and contains opinions developed by the Passive Asset Management team. This does not constitute investment advice or independent research. This paper is intended for professional investors only who understand the strategies and views introduced in this paper and can form an independent view of them. Please refer to the risk factors and disclaimers at the end of this document. Executive Summary Historically, asset allocation within global equity portfolios has primarily been built around country allocations. As a consequence of the increasing convergence of global economies, there is mounting evidence that a portfolio would benefit from an industry-based approach (Baca, Sean P., Brian L. Garbe, and Richard A. Weiss. 2000). Markets are traditionally understood to evolve through cycles, and sectors demonstrate different behaviours through these cycles. Professional investors have utilized this behaviour to build sector rotation strategies, which entail taking a short, medium or long term view on the prospects of specific industry sectors, such as financials, industrials, energy etc.. The proliferation of sector-based exchange-traded funds (ETFs) has made accessing specific sector exposures very straight forward. In this paper, we examine the efficiency of different investment styles to approach the investment theme of sector rotation. We find that: Sectors have two very interesting features: on one hand, each sector represents a diversified set of equities, on the other each demonstrates differentiated behaviour across market cycles, compared to other sectors. Our research shows five bases for sector rotation strategies that have delivered historically high probabilities of outperformance: the

Transcript of Passive Insights - DeutscheAM Insights... · db X-trackers ETF Team Winchester House ... asset...

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 1

Passive Insights March 2017 Marketing Material. Confidential. For non-

individual Professional Clients (MiFID

Directive 2004/39/EC Annex II) only. For

Qualified Investors (Art. 10 Para. 3 of the

Swiss Federal Collective Investment

Schemes Act (CISA). For institutional

investors only. Further distribution of this

material is strictly prohibited.

Sector Rotation: a multi-factor perspective

Deutsche Bank AG Deutsche Asset Management db X-trackers ETF Team Winchester House 1 Great Winchester Street London EC2N 2DB United Kingdom [email protected] etf.deutscheam.com Authors Vincent Denoiseux [email protected]

Pierre Debru [email protected]

Verity Worsfold [email protected]

Bhavesh Warlyani [email protected] Vivek Dinni [email protected] Tanuj Dora [email protected] Roopal Pareek [email protected]

Contents 1. Executive Summary 1 2. Sectors: ideal building blocks for

portfolios 2 3. Factor Identification and

Statistical Testing 5 4. The sector assessment

framework: Monthly insights on sector investing 31

“Buy low and sell high. It's pretty simple. The problem is knowing what's low and what's high.”

Jim Rogers

This marketing document has been produced for information purposes only

by a Structuring function of Deutsche AM and contains opinions developed

by the Passive Asset Management team. This does not constitute investment

advice or independent research. This paper is intended for professional

investors only who understand the strategies and views introduced in this

paper and can form an independent view of them. Please refer to the risk

factors and disclaimers at the end of this document.

Executive Summary

Historically, asset allocation within global equity portfolios has primarily been

built around country allocations. As a consequence of the increasing

convergence of global economies, there is mounting evidence that a portfolio

would benefit from an industry-based approach (Baca, Sean P., Brian L.

Garbe, and Richard A. Weiss. 2000).

Markets are traditionally understood to evolve through cycles, and sectors

demonstrate different behaviours through these cycles. Professional

investors have utilized this behaviour to build sector rotation strategies, which

entail taking a short, medium or long term view on the prospects of specific

industry sectors, such as financials, industrials, energy etc.. The proliferation

of sector-based exchange-traded funds (ETFs) has made accessing specific

sector exposures very straight forward.

In this paper, we examine the efficiency of different investment styles to

approach the investment theme of sector rotation. We find that:

Sectors have two very interesting features: on one hand, each sector

represents a diversified set of equities, on the other each

demonstrates differentiated behaviour across market cycles,

compared to other sectors.

Our research shows five bases for sector rotation strategies that

have delivered historically high probabilities of outperformance: the

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 2

Sectors represent well-diversified sets of equities and as such reduce company specific risk

macro economy, valuation, fundamentals, momentum and

sentiment.

By examining factors such as valuations or momentum, investors in

Sector may take advantage of different performance patterns to add

value in different market environments.

With this publication we also take the opportunity to introduce our monthly

Sector Assessment Framework which aims to gather, filter and combine all

the data required to assess and implement each of the five investment

strategies mentioned above (Macro Economy, Valuation, Fundamental,

Momentum and Sentiment).

------------

Sectors: ideal building blocks for portfolios

Sectors (or ‘industries’) are defined by classifying companies within a given

investment universe (e.g. a regional index, local equity exchange, etc.) into a

limited number of groups with common characteristics - typically in terms of

their business model.

Each company is unique for example each demonstrates distinct business

strategies and client base. Nonetheless by combining firms according to their

main business purposes, sectors essentially provide useful groupings of

companies. From an investor’s point of view this offers two unique features:

Each sector is well diversified across firms (see Figure 1) and to that

extent it significantly mitigates company specific risk.

Each sector delivers a performance that relates to a particular

business activity. According to Figure 2-5sectors tend to exhibit very

different performance characteristics.

Sectors offer strong diversification

Taking the example of the Global Industry Classification Standard (“GICS”)

as applied to the MSCI World, Figure 1 shows that the least diversified sector

is still composed of 44 different stocks.. This inherent diversification of each

sector reduces the need to analyse individual stocks and may free time and

resources for an investor with economic / business model views as opposed

to a time-consuming deep dive into each company’s financial statements.

Figure 1: # of stocks in the MSCI World sectors

Source: Bloomberg LP, MSCI, Deutsche AM Calculations. Data as of December 2016. For illustrative purpose only. Past performance is not indicative of future performance.

0

100

200

300

400

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 3

Sectors offer a high level of diversification. Sectors exhibit identifiable and varying behaviours across business cycles.

More importantly, this high level of diversification (sometimes referred to as

(low) intra-correlation) within each sector comes with a high level of

diversification between the sectors themselves (sometimes referred to as

(low) cross-index correlation). Figure 2 shows the correlations of excess

returns of the 10 historical GICS World sectors. Such low correlations

demonstrate that sectors can offer both diversified and targeted exposures.

Figure 2: Correlation between the excess returns of sector indices

Ma

teria

ls

Cons. S

tap.

Fin

ancia

ls

IT

Healthcare

Industr

ials

Energ

y

Te

lecom

Utilit

ies

Cons. Stap. -17%

Financials 3% -36%

IT -35% -43% -24%

Healthcare -30% 59% -35% -31%

Industrials 30% -12% 6% -10% -22%

Energy 30% -6% -12% -33% -7% -15%

Telecom -16% 15% -19% -4% 6% -24% -17%

Utilities -1% 57% -31% -41% 36% -14% 13% 19%

Cons. Discr -10% -1% -9% 12% -13% 24% -39% -7% -18%

Source: Bloomberg , MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016 using MSCI World sectors. Correlations are calculated on the basis of daily returns. Past performance is not indicative of future performance.

Furthermore, as illustrated by Baca, Sean P., Brian L. Garbe, and Richard A.

Weiss 2000), the relative importance of geographical and economic

influences on stock returns has shifted in favour of sectors. The factor

contribution of sector in global equity performance is as high as 30%,making

them prime candidates to be used in strategic and tactical allocation.

Direct exposure to economic cycles

Figure 3 shows historical performances of the 10 MSCI World sectors . We

make three observations

There is rotation in annual sector performances: every year, the best

and worst performing sector has varied significantly. E.g. whilst

Financials was the worst performer in 2008, it was the third best in

2009.

Sector rotation has materialized with a large level of cross-sectional

dispersion. The magnitude of the differences in annual performances

are very large. E.g. there was 30% difference between the best and

worst performing sectors in 2015.

Some sectors demonstrated similar behaviour. E.g. Healthcare and

Utilities performed relatively well in 2008 and 2014 when MSCI World

performance was poor, but underperformed in 2009-10 during market

recovery.

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 4

Sectors can be split in specific families depending on those behaviours: Cyclical/Defensive.

It is common practice to group sectors in two main families: cyclical and

defensive, with cyclical sectors performing better in ‘risk on’ environments

and defensive sectors performing better in ‘risk off’ environments.

Figure 3: Annual Performance of MSCI World Sectors

Source: Bloomberg . Deutsche AM Calculations. Data from December 2007 to December 2061. For illustrative purposes only. Past performance is not indicative of future performance.

Whilst the cyclical and defensive sectors show differing performances

through different market trends, we also observe similar groupings based on

their respective risk. Some sectors indeed exhibit more or less volatility and

cyclical sectors (as defined by the GICS classification) tend to have higher

volatility as highlighted by the clustering in Figure 4.

Figure 4: Volatility of returns

Defensive Sectors

Cyclical Sectors

Source: Bloomberg , MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016. Volatility is calculated on the basis of daily returns. Past performance is not indicative of future performance.

Similarly to volatility, looking at the Beta versus their benchmark, Figure 5

exhibits an even stronger clustering than Figure 4 with four cyclical sectors

showing an above 100% beta and four defensive sectors a below 100% beta.

10% 15% 20% 25%

Cons. Stap.

Healthcare

Utilities

MSCI World

Cons. Discr

Industrials

Telecom

Materials

Financials

IT

Energy

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 5

We investigate in the below factor based approaches to sector rotation that would benefits from the diversification and cyclical behaviour of sectors.

Of course this distinction may sound a bit arbitrary as demonstrated by the

positionning of Energy in Figure 4 and Figure 5. Despite being classified a

defensive sector, it displays high volatility and high beta. However, it is still

an interesting and useful framework to assess sector performance.

Figure 5: Sectors Beta of returns

Defensive Sectors

Cyclical Sectors

Source: Bloomberg , MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016. Volatility is calculated on the basis of daily returns. Past performance is not indicative of future performance.

All of the above illustrations illustrates why sectors are a very efficient tool to

develop dynamic investment strategies.

Factor Identification and Statistical Testing

Five factors utilized for Sector rotation

The first section illustrates several interesting features of equity sectors:

Sectors represent large groupings of stocks and as such

demonstrate low levels of idiosyncratic risk.

The behaviour of certain sectors during specific macro-economic

conditions can be associated with the broad sector’s business model

characteristics. As such, getting insights on future macro-economic

conditions may represent a source of outperformance.

We can generally classify sectors as being either cyclical or

defensive, representing its likelihood to outperform (resp.

underperform) during different part of the cycle and vice versa.

Sectors demonstrate a high level of cross-sectional dispersion which

in concrete terms means that a sector rotation strategy may yield

strong positive or negative performance depending on the quality of

the investment signals.

In this section we investigate five different investment styles – increasingly

referred to as ‘factors’ – that can be utilised to implement sector rotation.

0% 20% 40% 60% 80% 100% 120% 140%

Cons. Stap.

Utilities

Healthcare

Telecom

Cons. Discr

MSCI World

Industrials

Materials

Energy

IT

Financials

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 6

We assess the predictive power of different factor descriptors across 5 factors.

At the heart of a sector rotation strategy is the process of selecting the

appropriate sector to invest at a given time. In the below, we investigate five

factor-based approaches:

Momentum: identification of the recent absolute and relative

performances of each sector.

Valuation: identification of relative cheapness/richness of each

sector based on recognized valuation approaches (e.g. Price to

Earning Ratio).

Sentiment: positioning according to the overall change in Analyst

Forecasts for each sector as illustrated by upward and downward

revisions.

Fundamental: identification of the particular strengths of each

sector as measured by the growth in fundamental metrics (e.g.

Earning Growth).

Macro-Economic: identification of the current macro-economic

environment, based on assumed relationships between Sectors

and the Business Cycle.

A deep dive into the predictive power of each factor

For each factor approach, the predictive power of different factor descriptors,

(’sub-factors’) is tested and evaluated.

Figure 6: A comprehensive suite of recognized factors

Source: Deutsche AM. Illustrative Only

The framework for this study is a solid

dataset and comprehensive

statisitical analyses

Based on the suite of sub-factors shown in Figure 6 we develop a Sector

Assessment Framework that will compile relevant data points in a concise

format to help investors form an assessment of current market opportunities

looking at sectors from 5 different angles.

To develop this framework, we followed a three step process:

Compilation of datasets: using recognized data sources such as

Bloomberg, Datastream, IBES Aggregates.

Comprehensive Statistical Analysis: Each sub-factor is tested to

evaluate its ‘predictive power’. In what follows, we define the success

of a particular sub-factor as per its ability to correctly predict the

performance of a particular sector either on an absolute basis or

compared to its benchmark. We use ‘hit ratios’ to do this, i.e. the

proportion of correctly forecasted market evolutions (either relative or

absolute).

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 7

Momentum is a pervasive equity

factor.

Investment Strategies: For each sub-factor that demonstrates a

sufficiently high hit ratio, a sector picking strategy is tested across the

available historical dataset.

For the sub-factors where data is sector specific (i.e. everything but Macro-

Economic data), an important consideration when running the statistical

analysis is to decide whether to assess the factor on its current value, against

its history, or the relative positioning of against other sectors.

This could for example be expressed as the decision to go long a sector

based on a) it being cheap in absolute terms, b) it being cheap compared to

its own historical averags, or c) a comparison of its valuation metrics to others

to identify relative cheapness. We respectively call these comparison,

‘Absolute’, ‘Historical’ and ‘Cross-sectional’ assessments, and we test all

three where possible when it makes statistical and fundamental sense.

With reference to macroeconomic factors, the sub-factors are common to all

sectors and as such the objective will be to assess if each sub-factor is more

favourable for defensive or cyclical sectors.

We focus on 3 distinct geographical universes:

Developed market equities using the sectors of the MSCI World

Emerging market equities using the sectors of the MSCI Emerging

Market

European equities using the sectors of the Europe STOXX 600

Momentum, a straightforward and resilient approach

In their seminal research papers, Jegadeesh, N., 1990 and Jegadeesh, N.,

and S. Titman, 1993 highlighted the pervasiveness of momentum as a

contributor to the performance of equities.

In their paper “Momentum of Sector ETFs”, Denoiseux, V. and DEBRU, P.

2014, studied such momentum at sector level The analysis showed:

Momentum-driven global sector rotation strategies exhibit a higher

risk adjusted return compared to global market cap weighted stock

indices, on the basis of simulated results.

A momentum-driven emerging market sector rotation portfolio would

have demonstrated, on a simulated basis, a higher Sharpe Ratio

than the MSCI Emerging Market Index

The first step is to run a hit ratio analysis. We start with the absolute value

assessment - as usually implemented in the literature - i.e. the signal used is

the 11 Month Momentum 1 month removed:

𝑀𝑜𝑚𝑒𝑛𝑡𝑢𝑚 𝑆𝑐𝑜𝑟𝑒 =𝑃𝑡−1𝑚

𝑃𝑡−12𝑚

− 1

For each sector, at the end of each month, the momentum score and the

performance over the next 3 months are calculated. The hit ratio is then the

ratio between the number of month end historical observations where the

performance of the sector over the next 3 months is in line with expectations,

divided by the total number of observations. A high Momentum Score is

expected to signal a sector with a good tailwind and therefore likely to

translate into positive performance. Similarly, a low Momentum Score is

expected to translate into a negative performance.

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 8

Figure 7 illustrates the hit ratio. In this graph each data point represents a

historical observation with the Momentum Score at the time of observation on

thex-axis, and the performance of the sector over the following 3 months on

the y-axis. Each data point in a green zone is considered to be a positive

result, while each data point in the red zone is considered to be negative.

The hit ratio is the ratio of dots in the green zone to the total number of dots.

Overall a hit ratio above 50% indicates a positive relationship between the

factor and the resulting relative performance.

Figure 7: Momentum Absolute Hit Ratio Calculation

Source: Bloomberg LP, MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016. 10 MSCI World Sectors are used for this analysis. Past performance is not indicative of future performance.

Looking at the results sector-by-sector over the past 15 years, Momentum

exhibits very strong hit ratios across the board for MSCI World Sectors.

Figure 9 shows that all sectors exhibit high fifties to low sixties hit ratios

highlighting good predictive power.

Figure 8: Momentum absolute hit ratios for MSCI World sectors

Source: Bloomberg LP, MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016. 10 MSCI World Sectors are used for this analysis. Past performance is not indicative of future performance.

Looking at the same for European Sectors (Europe STOXX 600) and

Emerging Market Sectors (MSCI Emerging Markets), it is clear that

-50%-40%-30%-20%-10%

0%10%20%30%40%50%

-50% -30% -10% 10% 30% 50%

Forw

ard

3M

Pe

rfo

rman

ce

Momentum Score

53%63% 57% 62% 66% 62% 57% 57% 57% 60% 59%

0%

20%

40%

60%

80%

100%

Mo

men

tum

Hit

Rat

io

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 9

Absolute Momentum exhibits very

strong hit ratios across the board for

MSCI World Sectors.

Absolute Momentum also exhibits

strong and consistent predictive

power over the short to medium term

for Emerging Market and european

equities.

Momentum exhibits strong and consistent predictive power over the short to

medium term.

Figure 9: Momentum absolute hit ratios for Europe (left) and EM (right)

Source: Bloomberg LP, MSCI, STOXX, Deutsche AM Calculations. Data from December 2000 to November 2016 for MSCI EM and July 2000 to November 2016 for Europe STOXX 600 Sectors (except Consumer Services and Consumer Goods where the data starts in September 2004). MSCI EM Sectors are used for EM Sectors and Europe STOXX 600 Sectors are used for Europe. Past performance is not indicative of future performance.

We also run hit-ratio analysis on a cross sectional basis- instead of looking

at the sign of the Momentum Score, the analysis looks at the strength of the

Momentum Score, for each sector compared to the score of all the other

sectors at a given point in time. The underlying assumption being that the

sectors with the strongest Momentum Score will exhibit higher performance

than the sectors with the lowest Momentum Score over the next 3 months.

Each month, sectors are ranked according to their Momentum Scores, and

the average performance over the next 3 months of the 3 highest ranked

sectors and the 3 lowest ranked sectors is calculated. An occurrence where

the high Momentum Score sectors outperform the low Momentum Score

sectors is considered as a positive result. The Hit ratio is then calculated by

dividing the number of positive observations by the total number of

observations.

Figure 10 shows the average cross sectional hit ratio of the 10 sectors in each

of the 3 universes considered. We observe that momentum also exhibits

strong predictive power from a cross sectional perspective

51

% 66

%5

9%

55

% 64

%6

0%

49

% 58

%6

3%

61

%5

9%

0%

20%

40%

60%

80%

100%

Bas

ic M

ater

ials

Co

nsu

mer

Go

od

s

Fin

anci

als

Tech

no

logy

Hea

lth

care

Ind

ust

rial

s

Oil&

Gas

Tele

com

Uti

litie

s

Co

nsu

mer

Ser

vice

s

STO

XX

Eu

rop

e 6

00…

Mo

men

tum

Hit

Rat

io

54

%5

9%

50

%4

9%

54

%5

0%

52

%5

5%

54

%5

4%

53

%

0%

20%

40%

60%

80%

100%

Mat

eria

ls

Co

nsu

mer

Sta

ple

s

Fin

anci

als IT

Hea

lth

care

Ind

ust

rial

s

Ener

gy

Tele

com

mu

nic

atio

ns

Uti

litie

s

Co

nsu

mer

Dis

cre

tio

nn

ary

MSC

I EM

Sec

tors

Mo

men

tum

Hit

Rat

io

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 10

Momentum also exhibits strong

predictive power from a cross

sectional perspective.

Figure 10: Momentum Cross Sectional hit ratios

Source: Bloomberg LP, STOXX, MSCI, Deutsche AM Calculations. Data from December 2000 to November 2016 for MSCI EM and July 2000 to November 2016 for Europe STOXX 600 Sectors (except Consumer Services and Consumer Goods where the data starts in September 2004). Past performance is not indicative of future performance.

Having assessed the strength of momentum as a predictive signal for future

sector performance, we put together a straightforward potential investment

strategy using this signal to allocate capital. To this end, we define a potential

strategy that invests on a quarterly basis an equal amount in the 3 sectors

demonstrating the 3 highest Momentum (Figure 11).

Figure 11: Momentum driven potential investment strategy

Illustrative Only

Due to the relatively large available timespan for the price time series, we

were able to test the potential strategy on each the 3 universes (US, EM and

Europe) over periods of more than 15 years. As illustrated in Figure 12,

overall each of the 3 strategies yielded a positive excess return over the entire

observation period.

Since the hit ratios and potential strategy performance for momentum were

sufficiently high to be considered significant, we consider this factor relevant

as a possible approach to sector investing.

57% 62% 60%

0%

20%

40%

60%

80%

100%

Mo

men

tum

Hit

Rat

io

Portfolio Rebalancing

Quarterly

Portfolio Construction

Equal Weight Basket of 3 Sectors with highest Momentum Score

Momentum Score and Ranking

Rank the sectors by Momentum Score

Investment Universe

Sector Indices In MSCI World (resp MSCI EM and EuroSTOXX 600)

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 11

From a backtesting perspective,

Momentum also exhibits strong

results across investment universes.

Overall Momentum proved

successful across all our statistical

tests.

Value is a very pervasive equity factor

and we analyse it through the prism

of six sub-factors.

Figure 12: Momentum Strategies on the 3 universes

Momentum Strategy MSCI World

Annual growth 5.46% 5.13%

Annualized volatility 17.1% 16.8%

Sharpe Ratio 0.2 0.2

Max. drawdown -56.4% -57.8%

Momentum Strategy MSCI EM

Annual growth 12.43% 9.53%

Annualized volatility 18.8% 20.1%

Sharpe Ratio 0.6 0.4

Max. drawdown -63.5% -65.2%

Momentum Strategy Europe STOXX 600

Annual growth 5.31% 3.29%

Annualized volatility 21.2% 20.4%

Sharpe Ratio 0.2 0.1

Max. drawdown -56.8% -58.7% Source: Bloomberg LP, STOXX, MSCI, Deutsche AM Calculations. Data from July 2001 to November 2016 for World and Europe and December 2001 to November 2016 for Europe. The performance data is shown for illustrative purpose only and is based on the retrospective simulation of the strategies. The performance has been calculated on the basis of historical performances of each sector index net total return in USD (EUR for Europe). The performance is calculated gross of any replication costs but net of 20bps transaction costs excluding any applicable tax. Risk arising from assets being traded in foreign currencies is not hedged here. Past performance is not indicative of future performance.

Valuation and sentiment: Does buying cheap work in practice?

Value strategies i.e. buying cheap equities are one of the most famous and

most popular investment philosophies among the investment community.

Academic research, including by Fama E.F, French K.R. 1992 posits that

‘cheap’ equities - based on market prices relative to accounting values -

outperform ‘expensive’ equities over the long-term.

50

100

150

200

250

Jul 01 Jul 03 Jul 05 Jul 07 Jul 09 Jul 11 Jul 13 Jul 15

Momentum Strategy MSCI World Index

0100200300400500600700

Dec 01 Dec 03 Dec 05 Dec 07 Dec 09 Dec 11 Dec 13 Dec 15Momentum Strategy MSCI Emerging Markets

50

100

150

200

250

Jul 01 Jul 03 Jul 05 Jul 07 Jul 09 Jul 11 Jul 13 Jul 15Momentum Strategy STOXX Europe 600 Index

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 12

Cross-Sectional hit ratios for

valuation sub-factors are uneven,

with Dividend and P/E exhibiting

relatively strong results, while other

sub-factors show weaker results than

may have been expected

Following a few years of poor performance and limited interest, value stocks

and value strategies saw a large pick up of interest in the last quarter of 2016.

In fact, Value Factor ETFs worlwide raised over 10.7bn EUR in the last 3

months of 2016. In this section, we assess valuation indicators as predictors

of future performance for sectors.

For the sake of completeness we also bring the Sentiment factor into this

analysis framework, even if is not a value sub-factor sensu stricto.

We consider the 6 following sub-factors with data sourced from Thomson

Financial DataStream - I/B/E/S Global Aggregates:

Price to Earnings ratio - weighted average price/earnings per share

ratio based on 12-month-forward Earnings per share (P/E)

Price to Book ratio - weighted average price/book value per share

ratio based on 12-month-forward Book Value per share (P/B)

Price to Cash Flows ratio -. Weighted average price/CPS ratio based

on 12-month-forward Cash Flow per share (P/CF)

Price to EBIT raio - Weighted average price/EBIT per share ratio

based on 12-month-forward EBIT per share (P/EBIT)

Dividend Yield - Weighted average dividend yield based on the

indicated annual dividend

Sentiment - the 12-month-forward pro-rata number of Earning Per

shares estimates up since last month for all companies within the

sectors minus the numbers of estimates down divided by the total

number of estimates.

We begin by performing a hit ratio assessment for each sub-factor, on a cross

sectional basis. As we did for momentum, we rank sectors according to the

absolute value of the sub-factors and then compare the performance of the 3

highest and the 3 lowest ranked sectors over the next 12 months.

Commonly accepted expectations are for the lowest ranked sector according

to P/E, P/B, P/EBIT, P/CF and the highest ranked according to Dividend Yield

and Sentiment to exhibit the highest performance in the future

Figure 13: Valuations Cross Sectional hit ratios

Source: Bloomberg LP I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. See Annex for a detailed description of the data used. Past performance is not indicative of future performance.

56

%

39

%

43

%

36

%

57

%

56

%

53

%

42

%

38

%

41

% 52

%

67

%

44

%

37

% 41

%

41

%

54

%

56

%

0%

20%

40%

60%

80%

100%

Val

uat

ion

s H

it R

atio

MSCI World Sectors MSCI EM Sectors STOXX Europe 600 Sectors

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 13

We introduce a different type of hit

ratio: the Historical hit ratio. The

objective is to assess for each sector

whether it is currently cheap or

expensive compared to its own

history.

Figure 13 shows the average Cross Sectional hit ratios across all the sectors

for all universes and all sub-factors. Results for valuations of sub-factors are

uneven with Dividend and P/E exhibiting relatively strong results while the

other sub-factors exhibited weaker results than expected. This is partly due

to the fact that some sectors are structurally cheaper than others. For

example, the long term average value of the P/E of MSCI World Utilities is 14

compared to 22 for MSCI World IT,meaning that a direct comparison is likely

to generate many wrong signals.

On the other hand, the Cross Sectional hit ratios for Sentiment yield the

strongest results. In general, the “Sentiment Index”, defined as the ratio of the

number of investment advisers who are bearish divided by the total number

of advisors, has been considered as a contrarian signal (or no signal at all)

(see Solt, Michael E., and Meir Statman. 1988) but here we are considering

stock level expectation of changes in earnings per share which is a very

different measure and may explain this new result.

In an attempt to improve the results of the cross sectional hit ratio for

valuation, we introduce a different type of hit ratio: the Historical hit ratio. The

objective being to assess for each sector if it is currently low or high compared

to its own history.

As shown in Figure 14, the sentiment score for a given sector tends to

oscillate around a long term average. Our objective here is to assess how far

from this average the sector currently stands, and in which direction.

Figure 14: Illustration of Historical Sentiment Score

Source: For illustrative purpose only

Mathematically, we do this by calculating a 5Y historical Z-Score as defined

below.

𝐻𝑖𝑠𝑡𝑜𝑟𝑖𝑐𝑎𝑙 𝑍𝑆𝑐𝑜𝑟𝑒 = 𝐶𝑢𝑟𝑟𝑒𝑛𝑡 𝑉𝑎𝑙𝑢𝑒 − 5𝑌 𝐴𝑣𝑒𝑟𝑎𝑔𝑒(𝑉𝑎𝑙𝑢𝑒)

5𝑌 𝑆𝑡𝑎𝑛𝑑𝑎𝑟𝑑 𝐷𝑒𝑣 (𝑉𝑎𝑙𝑢𝑒)

-25

-20

-15

-10

-5

0

5

10

15

Dec 07 Dec 08 Dec 09 Dec 10 Dec 11 Dec 12 Dec 13 Dec 14

Score

Sentiment Average

Short Term deviationfrom long term average

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 14

We define the hit ratio as for the absolute hit ratio - i.e for each sector at the

end of each month, the Z Score is compared to the performance over the next

12 months.

As previously, the hit ratio is calculated as the ratio between the number of

month-end historical observations where the performance of the sector over

the following 12 months is in line with expectations, and the total number of

observations. Taking the example of P/E, a high historical Z-Score is

expected to signal a sector which is expensive and therefore to translate into

a negative future performance. Similarly a low Z-Score is expected to

translate into a positive future performance.

Overall a hit ratio above 50% indicates a significant relationship between the

factor and the resulting performance.

Figure 15: Historical hit ratio calculations for Sentiment

Source: Illustrative Only

Looking at the results sector-by-sector over the past 15 years for MSCI World

sectors, Sentiment exhibits relatively good historical hit ratios across sub-

factors. Figure 16 shows that most sectors exhibit high fifties to low sixties hit

ratios.

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-300% -200% -100% 0% 100% 200% 300%

Forw

ard

12

M P

erf

orm

ance

Historical ZScore Sentiment

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 15

Sentiment exhibits relatively good

historical hit ratios across sub-factors.

P/B performed relatively poorly on a

Cross Sectional basis, however

showa much stronger results for

Historical hit ratios- with 8 sectors out

of 10 showing hit ratios above 50%,

and as high as 70% for Developed

Equities.

Figure 16: Sentiment Historical Hit Ratios on MSCI World Sectors

Source: Bloomberg LP, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. Data from December 1995 to November 2016. Past performance is not indicative of future performance.

For P/B which performed relatively poorly on a Cross Sectional basis, the

results are a lot stronger on a Historical hit ratio basis - with 8 sectors out of

10 showing hit ratios above 50%, with some as high as 70% for Developed

Equities.

This is also true for European and Emerging Market equity universes.

Figure 17: P/B Historical hit ratios forMSCI World sectors

Source: Bloomberg LP, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. Data from January 2004 to November 2016. Past performance is not indicative of future performance.

Figure 18: P/B Historical hit ratios for Europe (left) and EM (right)

Source: Bloomberg LP, I/B/E/S Global Aggregates,STOXX , MSCI, Deutsche AM Calculations. Data from January 2004 to November 2016. For Europe Consumer Services and Consumer Goods Sector data is from October 2004 to November 2016. Past performance is not indicative of future performance.

56% 48%67%

57%42%

58%47%

60% 62% 55% 55%

0%20%40%60%80%

100%

Sen

tiem

ent

Hit

Rat

io

72%

43% 50%60% 52% 55%

70%56% 56%

48%56%

0%20%40%60%80%

100%

P/B

PS

Hit

Rat

io

61

%5

2%

47

%4

5%

50

% 58

%5

6% 62

% 68

%5

0%

55

%

0%

20%

40%

60%

80%

100%

Bas

ic M

ater

ials

Co

nsu

mer

Go

od

s

Fin

anci

als

Tech

no

logy

Hea

lth

care

Ind

ust

rial

s

Oil&

Gas

Tele

com

Uti

litie

s

Co

nsu

mer

Ser

vice

s

STO

XX

Eu

rop

e 6

00…

P/B

PS

Hit

Rat

io

44

% 52

% 64

%6

2%

56

%6

0%

44

%7

9%

65

%5

5%

56

%

0%

20%

40%

60%

80%

100%

Mat

eria

ls

Co

nsu

mer

Sta

ple

s

Fin

anci

als IT

Hea

lth

care

Ind

ust

rial

s

Ener

gy

Tele

com

mu

nic

atio

ns

Uti

litie

s

Co

nsu

mer

…

MSC

I EM

Sec

tors

P/B

PS

Hit

Rat

io

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 16

Taking an aggregated view of all universes and sub-factors, the Historical hit

ratios exhibit stronger and more consistent results on the 5 Valuation sub-

factors than cross sectional hit ratios.

Figure 19: Valuation and Sentiment Historical hit ratios

Source: Bloomberg LP, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. See Annex for a detailed description of the data used. Past performance is not indicative of future performance.

Having established a reliable signal, we now turn to constructing a

straightforward potential investment strategy using this signal to allocate

capital. To this end, we define two strategies:

A Valuation-based strategy

A Sentiment-based strategy

The Valuation based strategy uses cross-sectional scores equal weighting

the score of the 5 following sub-factors: P/E, P/BPS, P/CF, P/EBIT and Div

Yield. The strategy invests in an equally weighted basket of the 3 cheapest

sectors.

Figure 20: Valuation based potential investment strategy

The potential strategy relies on the predictive power of the 5 sub-factors but

also on robustness coming from using multiple different signals. As illustrated

in Figure 21, the strategy outperforms the benchmark over the long term in

the 3 sector universes we test. This outperformance comes with slightly

60

%

56

%

53

%

56

%

60

%

55

%

58

%

52

% 58

%

58

%

51

%

54

%

47

%

50

%

53

%

55

%

52

%

49

%

0%

20%

40%

60%

80%

100%

Val

uat

ion

s H

it R

atio

MSCI World Sectors MSCI EM Sectors STOXX Europe 600 Sectors

Portfolio Rebalancing

Quarterly

Portfolio Construction

Equal Weight Basket of 3 Sectors with Lowest Valuation Score

Valuation Score and Ranking

Rank the sectors by the equal weight of the 5 sub factor cross sectional Z Score

Investment Universe

Sector Indices In MSCI World (resp MSCI EM and EuroSTOXX 600)

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 17

The strategy outperforms the

benchmark over the long term in the

3 sector universes. This

outperformance comes with slightly

increased volatility, in line with the

academic comprehension of value as

a very cyclical factor.

increased volatility, in line with the academic comprehension of value as a

cyclical factor.

Figure 21: Valuation based potential investment strategy on the 3 universes

Valuation Strategy MSCI World

Annual growth 5.29% 3.46%

Annualized volatility 17.3% 16.8%

Sharpe Ratio 0.2 0.1

Max. drawdown -59.4% -57.8%

Valuation Strategy MSCI EM

Annual growth 10.89% 8.72%

Annualized volatility 20.9% 20.1%

Sharpe Ratio 0.4 0.3

Max. drawdown -62.6% -65.2%

Valuation Strategy Europe STOXX 600

Annual growth 7.19% 6.79%

Annualized volatility 21.2% 19.5%

Sharpe Ratio 0.3 0.3

Max. drawdown -56.3% -58.7% Source: Bloomberg LP, I/B/E/S Global Aggregates, STOXX, MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016 for World, December 2000 to November 2016 for EM and December 2002 to November 2016 for Europe. For Europe Consumer Services and Consumer Goods Sector data is from October 2004 to November 2016. So effectively the Europe Strategy runs on 8 sectors in the first 2 years. The performance data is shown for illustrative purpose only and is based on the retrospective simulation of the strategies. The performance has been calculated on the basis of historical performances of each sector index net total return in USD (EUR for Europe). The performance is calculated gross of any replication costs but net of 20bps transaction costs excluding any applicable tax. Risk arising from assets being traded in foreign currencies is not hedged here. Past performance is not indicative of future performance.

50

100

150

200

250

Jul 00 Jul 02 Jul 04 Jul 06 Jul 08 Jul 10 Jul 12 Jul 14 Jul 16Cross Sectional Valuation Strategy MSCI World Index

0100200300400500600700800

Dec 00 Dec 02 Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14

Cross Sectional Valuation Strategy MSCI Emerging Market

50

100

150

200

250

300

350

Dec 02 Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14Cross Sectional Valuation Strategy STOXX Europe 600 Index

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 18

The strategy also exhibits

performance patterns similar to single

stock based value strategies a very

difficult period post financial crisis and

a recent pick up in performance.

If we consider the performance of this strategy over shorter horizons (such

as 2Y rolling, seeFigure 22), we observe that the strategy goes through

periods of out- performance and under-performance. It also exhibits

performance patterns similar to single stock based value strategies, showing

negative performance post the 2008 financial crisis and a recent pick up in

performance.

Figure 22: 2 year rolling performance for the Valuation based potential

investment strategy on MSCI World

Source: Bloomberg LP, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016 for World. The performance data is shown for illustrative purpose only and is based on the retrospective simulation of the strategies. The performance has been calculated on the basis of historical performances of each sector index net total return in USD (EUR for Europe). The performance is calculated gross of any replication costs but net of 20bps transaction costs excluding any applicable tax. Risk arising from assets being traded in foreign currencies is not hedged here. Past performance is not indicative of future performance.

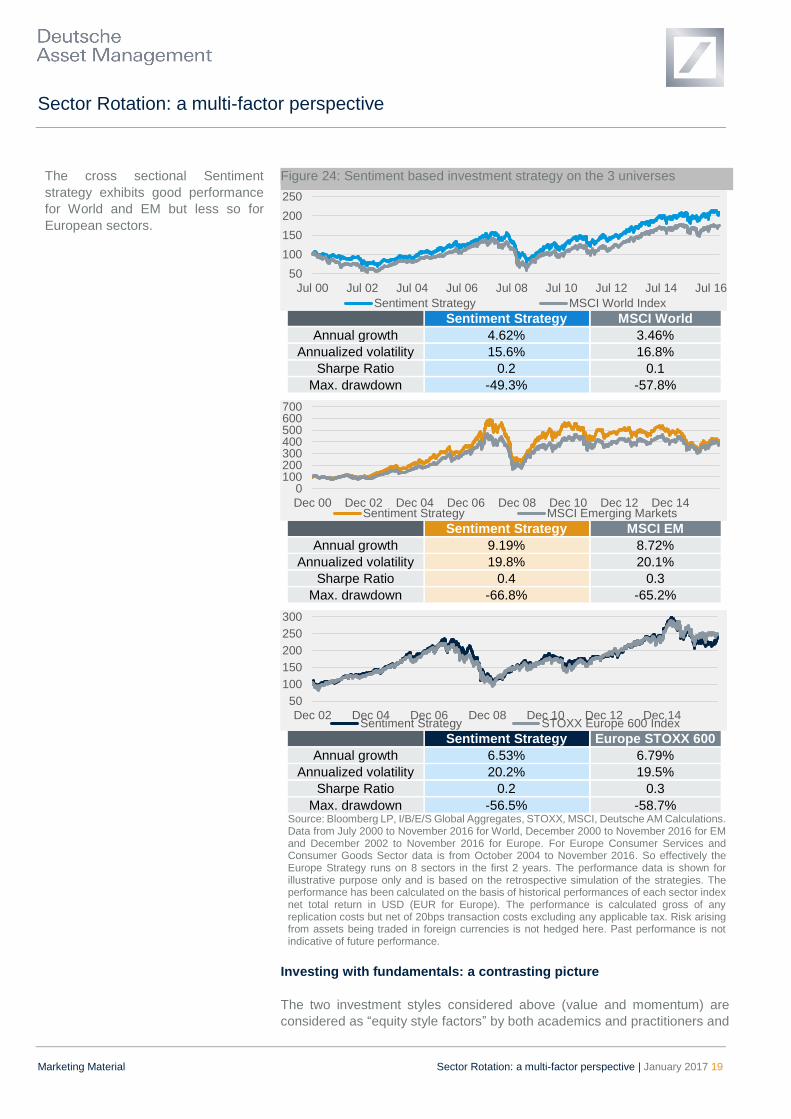

The Sentiment based potential strategy uses cross sectional Sentiment

scores. The strategy invests in an equally weighted basket of the 3 sectors

with the highest sentiment score.

Figure 23: Sentiment based potential investment strategy

Source: For illustrative Purpose Only

The strategy exhibits good performance for World and EM but less so for

European sectors.

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jul 02 Jul 04 Jul 06 Jul 08 Jul 10 Jul 12 Jul 14 Jul 16

Portfolio Rebalancing

Quarterly

Portfolio Construction

Equal Weight Basket of 3 Sectors with highest Sentiment Score

Valuation Score and Ranking

Rank the sectors by the Sentiment cross sectional Z Score

Investment Universe

Sector Indices In MSCI World (resp MSCI EM and EuroSTOXX 600)

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 19

The cross sectional Sentiment

strategy exhibits good performance

for World and EM but less so for

European sectors.

Figure 24: Sentiment based investment strategy on the 3 universes

Sentiment Strategy MSCI World

Annual growth 4.62% 3.46%

Annualized volatility 15.6% 16.8%

Sharpe Ratio 0.2 0.1

Max. drawdown -49.3% -57.8%

Sentiment Strategy MSCI EM

Annual growth 9.19% 8.72%

Annualized volatility 19.8% 20.1%

Sharpe Ratio 0.4 0.3

Max. drawdown -66.8% -65.2%

Sentiment Strategy Europe STOXX 600

Annual growth 6.53% 6.79%

Annualized volatility 20.2% 19.5%

Sharpe Ratio 0.2 0.3

Max. drawdown -56.5% -58.7% Source: Bloomberg LP, I/B/E/S Global Aggregates, STOXX, MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016 for World, December 2000 to November 2016 for EM and December 2002 to November 2016 for Europe. For Europe Consumer Services and Consumer Goods Sector data is from October 2004 to November 2016. So effectively the Europe Strategy runs on 8 sectors in the first 2 years. The performance data is shown for illustrative purpose only and is based on the retrospective simulation of the strategies. The performance has been calculated on the basis of historical performances of each sector index net total return in USD (EUR for Europe). The performance is calculated gross of any replication costs but net of 20bps transaction costs excluding any applicable tax. Risk arising from assets being traded in foreign currencies is not hedged here. Past performance is not indicative of future performance.

Investing with fundamentals: a contrasting picture

The two investment styles considered above (value and momentum) are

considered as “equity style factors” by both academics and practitioners and

50

100

150

200

250

Jul 00 Jul 02 Jul 04 Jul 06 Jul 08 Jul 10 Jul 12 Jul 14 Jul 16

Sentiment Strategy MSCI World Index

0100200300400500600700

Dec 00 Dec 02 Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14Sentiment Strategy MSCI Emerging Markets

50

100

150

200

250

300

Dec 02 Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14Sentiment Strategy STOXX Europe 600 Index

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 20

Fundamental Factors offer a

contrasting picture looking at

statistical results.

Cross Sectional hit ratios results are

quite poor

there is broad consensus on their expected long term outperformance against

traditional market cap strategies.

This, however, is not the case for the sub-factors we consider below. Growth

can be used as a factor to explain the performance of stocks but it has not

demonstrated that it carries an expectation of outperformance over the long

term at stock level. We now assess whether these fundamental economic

sub-factors are also good predictors of the sectors future performance.

We begin by conductinga hit ratio assessment on a cross sectional basis. As

with momentum and valuation, we rank sectors according to the level of the

different sub-factors listed below, and compare the performance of the 3

highest and the 3 lowest ranked sectors over the next 12 months.

Growth in Book Value per Share - Weighted 12-month-forward

growth in Book Value per Share (BPS Growth)

Growth in Earnings per Share - Weighted 12-month-forward growth

in Earnings per Share (EPS Growth)

Growth in Sales - Weighted 12-month-forward growth in Sales (Sales

Growth)

Growth in Cash Flows - Weighted 12-month-forward growth in Cash

Flows (Cash Flows Growth)

A commonly accepted expectation would be for the highest ranked sectors

(those exhibiting the highest growth) to realise the best performance in the

future.

Cross Sectional hit ratios (Figure 25) show only 2 of the 12 universe/sub-

factor pairs with hit ratios above 50%. Valuations could be explained by the

long term tendency for some sectors to have a higher growth rate than

others. Again to account for this, we move to Historical hit ratios.

Figure 25: Fundamental Cross Sectional Hit Ratios

Source: Bloomberg LP, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. See Annex for a detailed description of the data used. Past performance is not indicative of future performance.

The results of this last analysis are the least expected. We find that this

fundamental data may exhibit strong Historical hit ratios - but only when

looking at the expectations on a contrarian basis, i.e. by inversing

expectations. In other words, the hit ratios are calculated on the basis that

high growth is a signal of future under performance - a kind of ‘overbought’

signal.

56%

34%44%

35%

60%50% 48%

37%44%29%

36% 35%

0%

20%

40%

60%

80%

100%

Fun

dam

enta

l H

it R

atio

MSCI World Sectors MSCI EM Sectors STOXX Europe 600 Sectors

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 21

Fundamental data exhibits strong

contrarian Historical hit ratios -by

inversing expectations

As an example, using EPS Growth for MSCI World sectors, on a contrarian

basis, 9 out of 10 historical hit ratios are above 50%

Figure 26: EPS Growth Historical Hit Ratios

Source: Bloomberg LP, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. Data from December 1995 to November 2016. Past performance is not indicative of future performance.

Still on a contrarian basis, we find very strong results for fundamental data.

On average across all universes and across all sub-factors, all hit ratios are

above 50%.

Figure 27: Fundamental Historical Hit Ratios

Source: Bloomberg LP, STOXX, I/B/E/S Global Aggregates, MSCI, Deutsche AM Calculations. See Annex for a detailed description of the data used. Past performance is not indicative of future performance.

Using Contrarian Fundamental signals, we construct an investment strategy

to test the viability of the signals. The idea is to buy the 3 sectors showing the

lowest growth across the 4 sub factors on a quarterly basis.

Figure 28: Fundamental potential Investment Strategy

Source: For illustrative purpose only

58% 64%49%

63% 63%51% 51% 51% 43%

55% 55%

0%20%40%60%80%

100%

EPS

Gro

wth

Hit

Rat

io

61

%

67

%

58

%

55

%

56

%

54

%

50

%

57

%

51

%

54

%

61

%

56

%

0%20%40%60%80%

100%

Fun

dam

enta

ls H

it

Rat

io

MSCI World Universe MSCI EM Sectors STOXX Europe 600 Sectors

Portfolio Rebalancing

Quarterly

Portfolio Construction

Equal Weight Basket of 3 Sectors with Lowest Fundamental Score

Fundamental Score and Ranking

Rank the sectors by the equal weight of the Historical ZScore of the 4 sub factors

Investment Universe

Sector Indices In MSCI World (resp MSCI EM and EuroSTOXX 600)

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 22

On a contrarian basis, results for

Fundamental factors are excellent for

EM and Europe and fine for

developed equities.

The results in Figure 29 are excellent for EM and Europe with outperformance

of 3.94% and 2.99% per annum respectively and are quite good for World.

Max drawdowns are also down across the board compared to the benchmark.

Figure 29: Fundamental Strategies on the 3 universes

Fundamental Strategy MSCI World

Annual growth 4.36% 4.02%

Annualized volatility 16.8% 16.9%

Sharpe Ratio 0.2 0.1

Max. drawdown -56.8% -57.8%

Fundamental Strategy MSCI EM

Annual growth 12.66% 8.72%

Annualized volatility 18.4% 20.1%

Sharpe Ratio 0.6 0.3

Max. drawdown -49.9% -65.2%

Fundamental Strategy Europe STOXX 600

Annual growth 6.17% 3.18%

Annualized volatility 22.1% 20.7%

Sharpe Ratio 0.2 0.1

Max. drawdown -48.6% -58.7% Source: Bloomberg LP, I/B/E/S Global Aggregates, STOXX, MSCI, Deutsche AM Calculations. Data from July 2000 to November 2016 for World, December 2000 to November 2016 for EM and December 2002 to November 2016 for Europe. For Europe Consumer Services and Consumer Goods Sector data is from October 2004 to November 2016. So effectively the Europe Strategy runs on 8 sectors in the first 2 years. The performance data is shown for illustrative purpose only and is based on the retrospective simulation of the strategies. The performance has been calculated on the basis of historical performances of each sector index net total return in USD (EUR for Europe). The performance is calculated gross of any replication costs but net of 20bps transaction costs excluding any applicable tax. Risk arising from assets being traded in foreign currencies is not hedged here. Past performance is not indicative of future performance.

50

100

150

200

250

Jan 01 Jan 03 Jan 05 Jan 07 Jan 09 Jan 11 Jan 13 Jan 15

Fundamental Strategy MSCI World Index

0100200300400500600700800900

Dec 00 Dec 02 Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14Fundamental Strategy MSCI Emerging Markets

50

100

150

200

250

Mar 06 Mar 08 Mar 10 Mar 12 Mar 14 Mar 16Fundamental Strategy STOXX Europe 600 Index

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 23

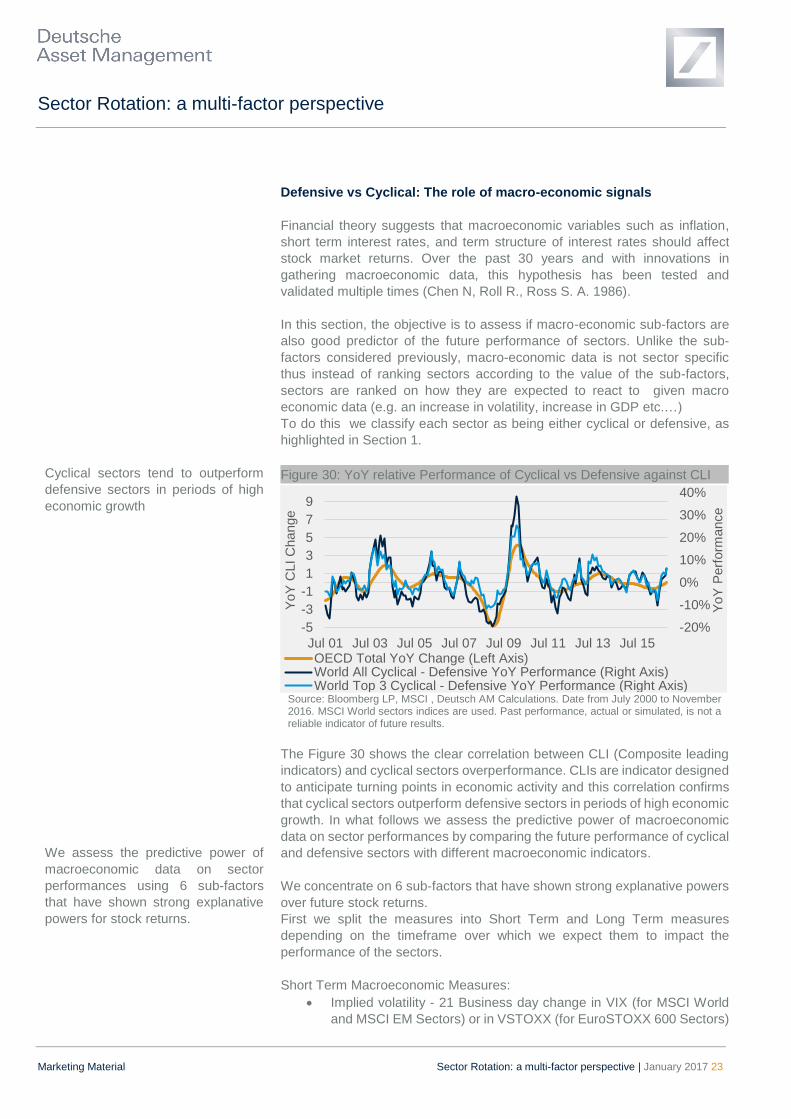

Cyclical sectors tend to outperform

defensive sectors in periods of high

economic growth

We assess the predictive power of

macroeconomic data on sector

performances using 6 sub-factors

that have shown strong explanative

powers for stock returns.

Defensive vs Cyclical: The role of macro-economic signals

Financial theory suggests that macroeconomic variables such as inflation,

short term interest rates, and term structure of interest rates should affect

stock market returns. Over the past 30 years and with innovations in

gathering macroeconomic data, this hypothesis has been tested and

validated multiple times (Chen N, Roll R., Ross S. A. 1986).

In this section, the objective is to assess if macro-economic sub-factors are

also good predictor of the future performance of sectors. Unlike the sub-

factors considered previously, macro-economic data is not sector specific

thus instead of ranking sectors according to the value of the sub-factors,

sectors are ranked on how they are expected to react to given macro

economic data (e.g. an increase in volatility, increase in GDP etc.…)

To do this we classify each sector as being either cyclical or defensive, as

highlighted in Section 1.

Figure 30: YoY relative Performance of Cyclical vs Defensive against CLI

Source: Bloomberg LP, MSCI , Deutsch AM Calculations. Date from July 2000 to November 2016. MSCI World sectors indices are used. Past performance, actual or simulated, is not a reliable indicator of future results.

The Figure 30 shows the clear correlation between CLI (Composite leading

indicators) and cyclical sectors overperformance. CLIs are indicator designed

to anticipate turning points in economic activity and this correlation confirms

that cyclical sectors outperform defensive sectors in periods of high economic

growth. In what follows we assess the predictive power of macroeconomic

data on sector performances by comparing the future performance of cyclical

and defensive sectors with different macroeconomic indicators.

We concentrate on 6 sub-factors that have shown strong explanative powers

over future stock returns.

First we split the measures into Short Term and Long Term measures

depending on the timeframe over which we expect them to impact the

performance of the sectors.

Short Term Macroeconomic Measures:

Implied volatility - 21 Business day change in VIX (for MSCI World

and MSCI EM Sectors) or in VSTOXX (for EuroSTOXX 600 Sectors)

-20%

-10%

0%

10%

20%

30%

40%

-5

-3

-1

1

3

5

7

9

Jul 01 Jul 03 Jul 05 Jul 07 Jul 09 Jul 11 Jul 13 Jul 15

YoY

Perf

orm

ance

YoY

CLI C

hange

OECD Total YoY Change (Left Axis)World All Cyclical - Defensive YoY Performance (Right Axis)World Top 3 Cyclical - Defensive YoY Performance (Right Axis)

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 24

Credit Default Swap levels - 21 Business day change in an Equal

Weight Basket of 125 CDS defined as the Markit CDX North America

Investment Grade Index (for MSCI World and MSCI EM Sectors) and

in an Equal Weight Basket of 125 CDS defined as the Markit iTraxx

Europe Investment Grade Index (for EuroSTOXX 600 Sectors)

Term Structure - 21 Business day change in the difference between

the 10Y and 2Y government bond rate in USD (for MSCI World and

MSCI EM Sectors) and in EUR (for EuroSTOXX 600 Sectors)

Long Term Macroeconomic Sub-Factors:

GDP - the US Gross Domestic Product Seasonality Adjusted Quarter

on Quarter Change published by the Bureau of Economic Analysis

(for MSCI World and MSCI EM Sectors) and Euro Area Gross

Domestic Product Chained 2010 Prices QoQ published by Eurostat

(for EuroSTOXX 600 Sectors)

Inflation - the monthly change in US CPI urban consumer non

Seasonability adjusted (for MSCI World and MSCI EM Sectors) and

the Euro Area Harmonized index of consumer prices (for

EuroSTOXX 600 Sectors)

Leading Short Term Interest Rates -. changes in Fed Funds Target

Rate (for MSCI World and MSCI EM Sectors) and the short term

EUR rate (for EuroSTOXX 600 Sectors)

Considering the Short Term Macroeconomic Sub-Factors first, we calculate

a Historical Hit Ratio as defined previously. For each sub-factor, we calculate

the historical Z Score over the last 5 years (1Y for CDS due to a lack of

historical data). For each sector at the end of each month, the Z Score is

compared to the performance over the next 1 month (12 months for Term

Structure). Our expectation is that for cyclical sectors, a strong positive

change in VIX would be a negative signal (similarly for CDS and Term

Structure) and a positive signal for defensive sectors. Z scores between -0.5

and 0.5 are not considered in order to remove from the dataset low

significance macroeconomic events i.e. where the measure is not considered

to move enough.

The hit ratio is the ratio between the number of month-end historical

observations where the performance of the actual sector over the following 1

month (12 months for Term Structure) is in line with expectations, and the

total number of observations.

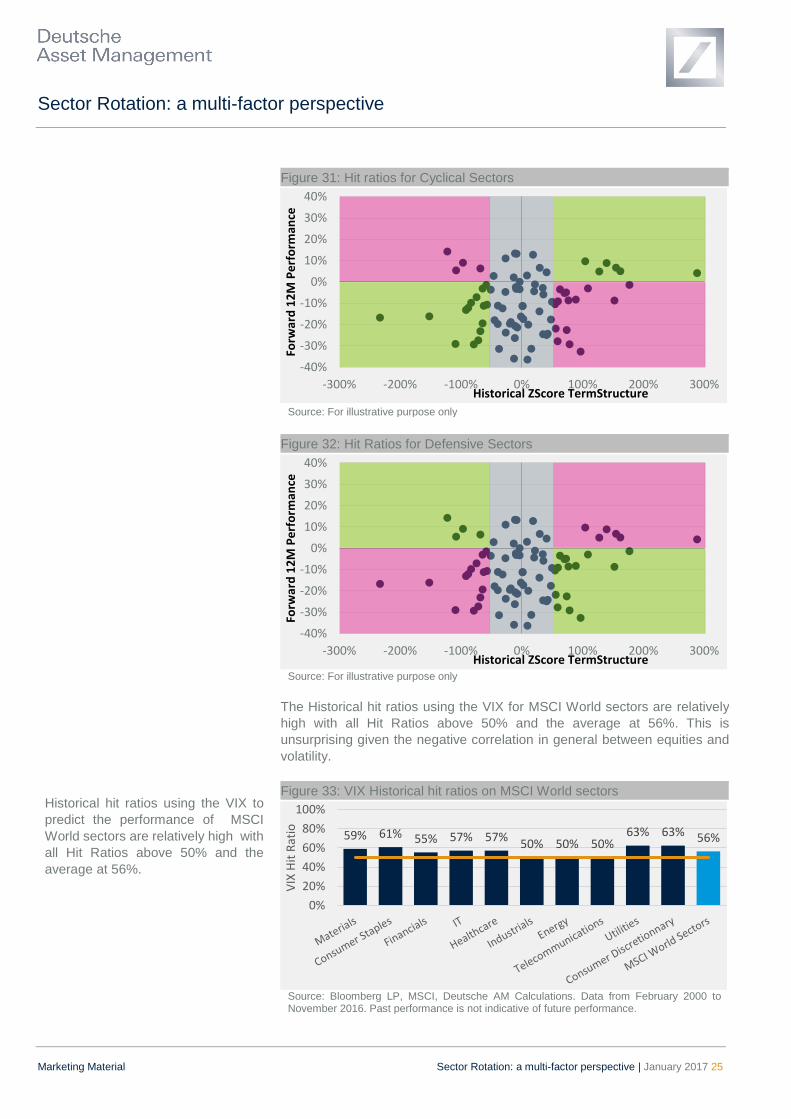

Figure 31 illustrates the hit ratio.

We consider that a hit ratio above 50% indicates a significant relationship

between the factor and the resulting relative performance.

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 25

Historical hit ratios using the VIX to

predict the performance of MSCI

World sectors are relatively high with

all Hit Ratios above 50% and the

average at 56%.

Figure 31: Hit ratios for Cyclical Sectors

Source: For illustrative purpose only

Figure 32: Hit Ratios for Defensive Sectors

Source: For illustrative purpose only

The Historical hit ratios using the VIX for MSCI World sectors are relatively

high with all Hit Ratios above 50% and the average at 56%. This is

unsurprising given the negative correlation in general between equities and

volatility.

Figure 33: VIX Historical hit ratios on MSCI World sectors

Source: Bloomberg LP, MSCI, Deutsche AM Calculations. Data from February 2000 to November 2016. Past performance is not indicative of future performance.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-300% -200% -100% 0% 100% 200% 300%

Forw

ard

12

M P

erf

orm

ance

Historical ZScore TermStructure

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-300% -200% -100% 0% 100% 200% 300%

Forw

ard

12

M P

erf

orm

ance

Historical ZScore TermStructure

59% 61% 55% 57% 57%50% 50% 50%

63% 63% 56%

0%

20%

40%

60%

80%

100%

VIX

Hit

Rat

io

Sector Rotation: a multi-factor perspective

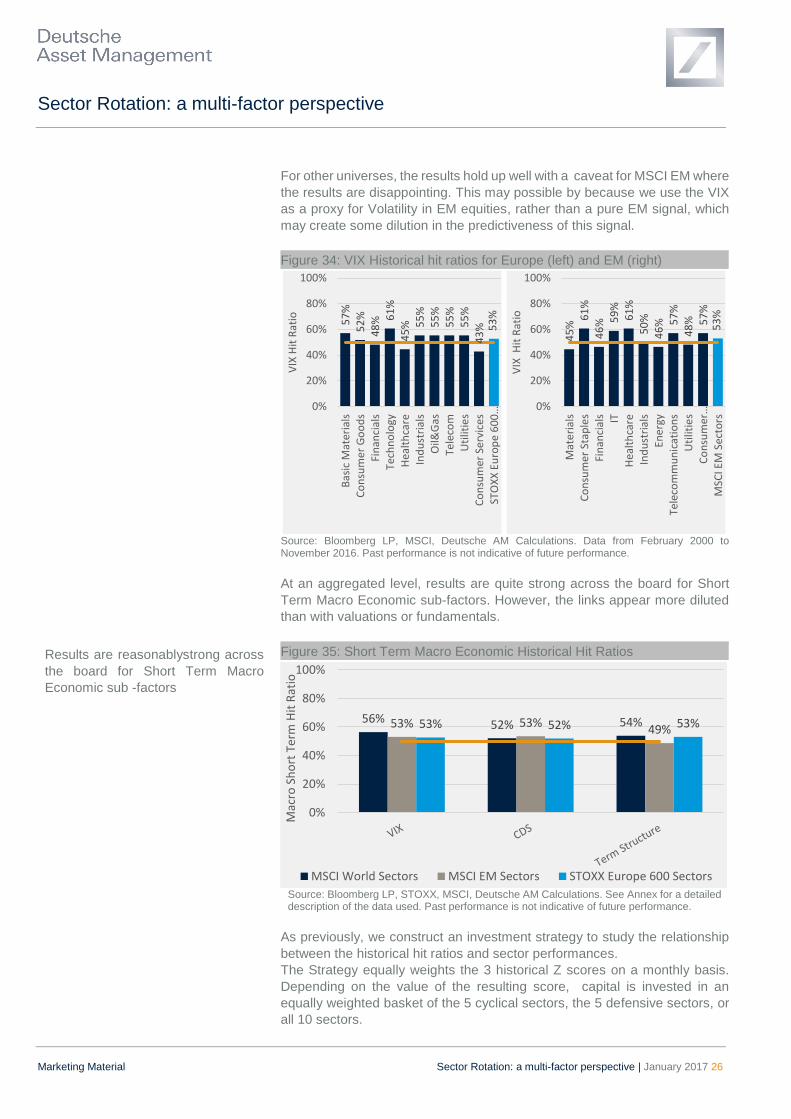

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 26

Results are reasonablystrong across

the board for Short Term Macro

Economic sub -factors

For other universes, the results hold up well with a caveat for MSCI EM where

the results are disappointing. This may possible by because we use the VIX

as a proxy for Volatility in EM equities, rather than a pure EM signal, which

may create some dilution in the predictiveness of this signal.

Figure 34: VIX Historical hit ratios for Europe (left) and EM (right)

Source: Bloomberg LP, MSCI, Deutsche AM Calculations. Data from February 2000 to November 2016. Past performance is not indicative of future performance.

At an aggregated level, results are quite strong across the board for Short

Term Macro Economic sub-factors. However, the links appear more diluted

than with valuations or fundamentals.

Figure 35: Short Term Macro Economic Historical Hit Ratios

Source: Bloomberg LP, STOXX, MSCI, Deutsche AM Calculations. See Annex for a detailed description of the data used. Past performance is not indicative of future performance.

As previously, we construct an investment strategy to study the relationship

between the historical hit ratios and sector performances.

The Strategy equally weights the 3 historical Z scores on a monthly basis.

Depending on the value of the resulting score, capital is invested in an

equally weighted basket of the 5 cyclical sectors, the 5 defensive sectors, or

all 10 sectors.

57

%5

2%

48

% 61

%4

5% 5

5%

55

%5

5%

55

%4

3% 5

3%

0%

20%

40%

60%

80%

100%

Bas

ic M

ater

ials

Co

nsu

mer

Go

od

sFi

nan

cial

sTe

chn

olo

gyH

ealt

hca

reIn

du

stri

als

Oil&

Gas

Tele

com

Uti

litie

sC

on

sum

er S

ervi

ces

STO

XX

Eu

rop

e 6

00

…

VIX

Hit

Rat

io

45

%6

1%

46

% 59

%6

1%

50

%4

6% 5

7%

48

% 57

%5

3%

0%

20%

40%

60%

80%

100%

Mat

eri

als

Co

nsu

mer

Sta

ple

sFi

nan

cial

s ITH

ealt

hca

reIn

du

stri

als

Ener

gyTe

leco

mm

un

icat

ion

sU

tilit

ies

Co

nsu

mer

…M

SCI E

M S

ecto

rs

VIX

Hit

Rat

io

56% 52% 54%53% 53%49%53% 52% 53%

0%

20%

40%

60%

80%

100%

Mac

ro S

ho

rt T

erm

Hit

Rat

io

MSCI World Sectors MSCI EM Sectors STOXX Europe 600 Sectors

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 27

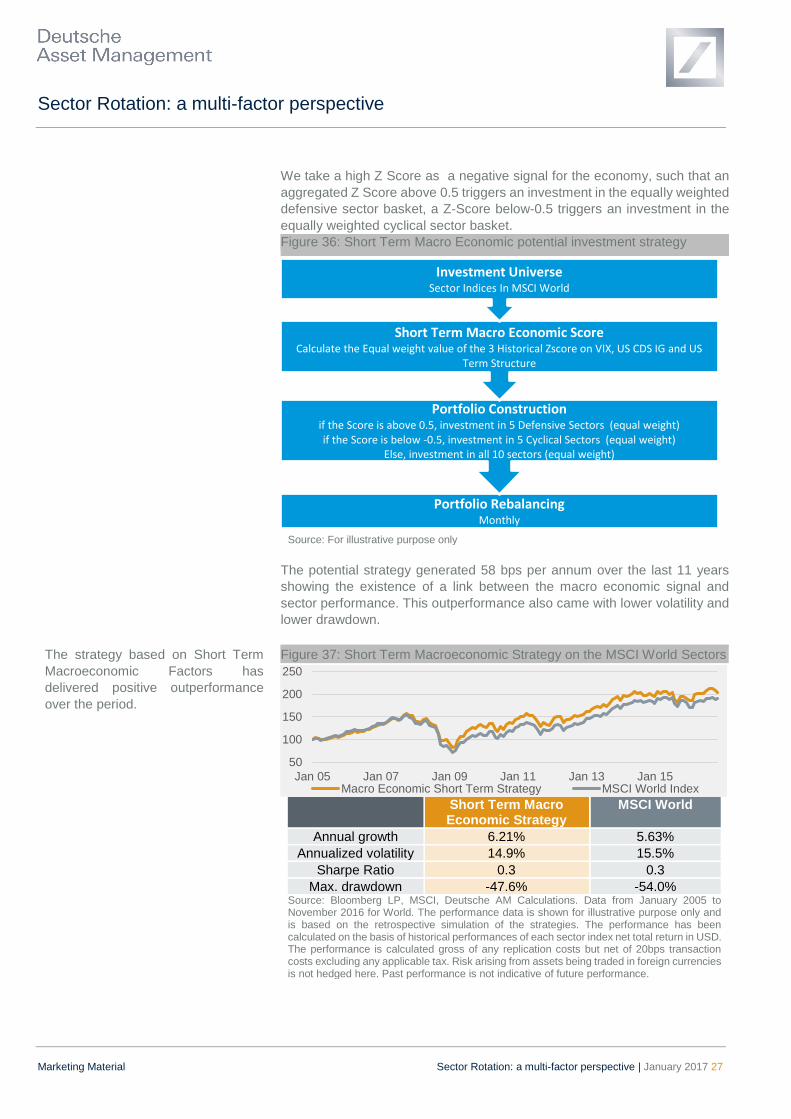

The strategy based on Short Term

Macroeconomic Factors has

delivered positive outperformance

over the period.

We take a high Z Score as a negative signal for the economy, such that an

aggregated Z Score above 0.5 triggers an investment in the equally weighted

defensive sector basket, a Z-Score below-0.5 triggers an investment in the

equally weighted cyclical sector basket.

Figure 36: Short Term Macro Economic potential investment strategy

Source: For illustrative purpose only

The potential strategy generated 58 bps per annum over the last 11 years

showing the existence of a link between the macro economic signal and

sector performance. This outperformance also came with lower volatility and

lower drawdown.

Figure 37: Short Term Macroeconomic Strategy on the MSCI World Sectors

Short Term Macro

Economic Strategy MSCI World

Annual growth 6.21% 5.63%

Annualized volatility 14.9% 15.5%

Sharpe Ratio 0.3 0.3

Max. drawdown -47.6% -54.0% Source: Bloomberg LP, MSCI, Deutsche AM Calculations. Data from January 2005 to November 2016 for World. The performance data is shown for illustrative purpose only and is based on the retrospective simulation of the strategies. The performance has been calculated on the basis of historical performances of each sector index net total return in USD. The performance is calculated gross of any replication costs but net of 20bps transaction costs excluding any applicable tax. Risk arising from assets being traded in foreign currencies is not hedged here. Past performance is not indicative of future performance.

Portfolio RebalancingMonthly

Portfolio Constructionif the Score is above 0.5, investment in 5 Defensive Sectors (equal weight)if the Score is below -0.5, investment in 5 Cyclical Sectors (equal weight)

Else, investment in all 10 sectors (equal weight)

Short Term Macro Economic ScoreCalculate the Equal weight value of the 3 Historical Zscore on VIX, US CDS IG and US

Term Structure

Investment UniverseSector Indices In MSCI World

50

100

150

200

250

Jan 05 Jan 07 Jan 09 Jan 11 Jan 13 Jan 15Macro Economic Short Term Strategy MSCI World Index

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 28

For the Long Term Macroeconomic Sub-Factors, we calculate an absolute

Hit Ratio for GDP and Leading Short Term Interest Rates. For Inflation, we

use a 5 year Historical Hit Ratio (with a 0.5/-0.5 threshold) similar to the one

used for the VIX and Term Structures.

For each sector, at the end of each month, the Score (absolute or historical)

is compared to the performance of the sector over the next 18 months. The

Hit ratio is again the ratio between the number of month-end historical

observations where the performance of the sector over the next 18 months is

in line with expectations, divided by the total number of observations.

For Cyclical Sectors, intuitively, positive GDP changes are positive signals for

future performance.

As illustrated in Figure 38, interest rate hike are detrimental to the

performance of defensive sectors. Figure 38 shows the average excess

return duration – defined as the price return of the sector minus the price

return of the universe, divided by the change in the 5y swap rate - for MSCI

World sectors. The average is taken over periods which experienced EUR

rate hikes, from July 2000 to December 2016.

Figure 38 : Average excess return duration of MSCI World sectors

‘Excess return duration’ is calculated as the price return of the sector minus the price return of the MSCI World over the period, divided by the change in the EUR 5y swap rate over the period. The bar chart shows the average excess return duration over the 14 periods of interest rate increases from Jul 2000 – Dec 2016. Source: Bloomberg, Deutsche Bank Asset Management Calculations. Data: July 2000 to December 2016. Past performance, actual or simulated, is not a reliable indicator of future results..

Inflation is a slightly different animal. One might expect that cyclical stocks

and inflation would be positively related. However, multiples empirical studies

(Jaffe and Mandelker (1976), Fama and Schwert (1977), Schwert (1981), and

Boudoukh and Richardson (1993)) suggest that the relationship is in fact

negative.

In what follows, for Cyclical Sectors an increase in inflation is considered to

be a negative signal.

-6

-4

-2

0

2

4

6

8

Ave

rag

e

Exce

ss R

etu

rn D

ura

tio

n*

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 29

Results for interest rates and Inflation

are quite strong. However the results

on GDP are average.

Figure 39: Long Term Macro Economic hit ratios

Source: Bloomberg LP, STOXX, MSCI, Deutsche AM Calculations. See Annex for a detailed description of the data used. Past performance is not indicative of future performance.

Results for inflation are quite strong. However the results using GDP or short

term interest rates are pretty average.

Finally, we create 3 investment strategies (one per measure) using 5Y

Historical Z Scores . Depending on this score the portfolio invests in defensive

only, cyclical only, or all sectors. For GDP and short term interest rate,

positive signals translate into investment in cyclical sectors. For inflation on

the other hand, such signal translates into investment in defensive sectors.

Figure 40: GDP based potential investment strategy

Source: For illustrative purpose only

The performance of the GDP based potential investment strategy for MSCI

World sectors is quite strong generating 53bps per annum of outperformance

over MSCI World over the last 15 years.

52% 51%60%

43%50% 54%

39%47%

53%

0%

20%

40%

60%

80%

100%

Mac

ro L

on

g Te

rm H

it R

atio

MSCI World Sectors MSCI EM Sectors STOXX Europe 600 Sectors

Portfolio RebalancingQuaterly

Portfolio Constructionif the Score is above 0.5, investment in 5 Cyclical Sectors (equal weight)

if the Score is below -0.5, investment in 5 Defensive Sectors (equal weight)Else, investment in all 10 sectors (equal weight)

Inflation ScoreHistorical Z-Score of GDP QoQ

Investment UniverseSector Indices In MSCI World

Sector Rotation: a multi-factor perspective

Marketing Material Sector Rotation: a multi-factor perspective | January 2017 30

The performance of the GDP based

investment strategy for MSCI World

sectors is strong

The performance of the Short Term

Interest Rate strategy is very strong

Figure 41: GDP Strategy on the MSCI World Sectors

GDP Strategy MSCI World

Annual growth 5.54% 5.01%

Annualized volatility 16.0% 16.3%

Sharpe Ratio 0.2 0.2