Particle Learning for Sequential Bayesian Computation · 2017-10-23 · Particle learning provides...

44

BAYESIAN STATISTICS 9, pp. 317–360. J. M. Bernardo, M. J. Bayarri, J. O. Berger, A. P. Dawid, D. Heckerman, A. F. M. Smith and M. West (Eds.) c Oxford University Press, 2011 Particle Learning for Sequential Bayesian Computation Hedibert F. Lopes The University of Chicago, USA [email protected] Carlos M. Carvalho The University of Chicago, USA [email protected] Michael S. Johannes Columbia University, USA [email protected] Nicholas G. Polson The University of Chicago, USA [email protected] Summary Particle learning provides a simulation-based approach to sequential Bayesian computation. To sample from a posterior distribution of interest we use an essential state vector together with a predictive distribution and propaga- tion rule to build a resampling-sampling framework. Predictive inference and sequential Bayes factors are a direct by-product. Our approach provides a simple yet powerful framework for the construction of sequential posterior sampling strategies for a variety of commonly used models. Keywords and Phrases: Particle learning; Bayesian; Dynamic factor models; Essential state vector; Mixture models; Sequential inference; Conditional dynamic linear models; Nonparametric; Dirichlet. Hedibert F. Lopes is Associate Professor of Econometrics and Statistics, The University of Chicago Booth School of Business. Carlos M. Carvalho is Assistant Professor of Econo- metrics and Statistics, University of Chicago Booth School of Business and Donald D. Harrington Fellow at The University of Texas, Austin. Michael S. Johannes is Roger F. Murray Associate Professor of Finance, Graduate School of Business, Columbia University. Nicholas G. Polson is Professor of Econometrics and Statistics, The University of Chicago Booth School of Business. We would like to thank Mike West, Raquel Prado and Peter M¨ uller for insightful comments that greatly improved the article. We also thank Seung-Min Yae for research assistance with some of the examples. Part of this research was conducted while the first two authors were visiting the Statistical and Applied Mathematical Sciences Institute for the 2008-09 Program on Sequential Monte Carlo Methods. Carvalho would like to acknowledge the support of the Donald D. Harrington Fellowship Program and the IROM Department at The University of Texas at Austin.

Transcript of Particle Learning for Sequential Bayesian Computation · 2017-10-23 · Particle learning provides...

BAYESIAN STATISTICS 9, pp. 317–360.J. M. Bernardo, M. J. Bayarri, J. O. Berger, A. P. Dawid,D. Heckerman, A. F. M. Smith and M. West (Eds.)c Oxford University Press, 2011

Particle Learning for SequentialBayesian Computation

Hedibert F. Lopes

The University of Chicago, [email protected]

Carlos M. Carvalho

The University of Chicago, [email protected]

Michael S. Johannes

Columbia University, [email protected]

Nicholas G. Polson

The University of Chicago, [email protected]

Summary

Particle learning provides a simulation-based approach to sequential Bayesiancomputation. To sample from a posterior distribution of interest we use anessential state vector together with a predictive distribution and propaga-tion rule to build a resampling-sampling framework. Predictive inference andsequential Bayes factors are a direct by-product. Our approach provides asimple yet powerful framework for the construction of sequential posteriorsampling strategies for a variety of commonly used models.

Keywords and Phrases: Particle learning; Bayesian; Dynamic factor

models; Essential state vector; Mixture models; Sequential

inference; Conditional dynamic linear models; Nonparametric;

Dirichlet.

Hedibert F. Lopes is Associate Professor of Econometrics and Statistics, The Universityof Chicago Booth School of Business. Carlos M. Carvalho is Assistant Professor of Econo-metrics and Statistics, University of Chicago Booth School of Business and Donald D.Harrington Fellow at The University of Texas, Austin. Michael S. Johannes is Roger F.Murray Associate Professor of Finance, Graduate School of Business, Columbia University.Nicholas G. Polson is Professor of Econometrics and Statistics, The University of ChicagoBooth School of Business. We would like to thank Mike West, Raquel Prado and PeterMuller for insightful comments that greatly improved the article. We also thank Seung-MinYae for research assistance with some of the examples. Part of this research was conductedwhile the first two authors were visiting the Statistical and Applied Mathematical SciencesInstitute for the 2008-09 Program on Sequential Monte Carlo Methods. Carvalho wouldlike to acknowledge the support of the Donald D. Harrington Fellowship Program and theIROM Department at The University of Texas at Austin.

318 H. F. Lopes, C. M. Carvalho, M. S. Johannes and N. G. Polson

1. THE PL FRAMEWORK

Sequential Bayesian computation requires the calculation of a set of posterior distri-butions p(θ | yt), for t = 1, . . . , T , where yt = (y1, . . . , yt). The inability to directlycompute the marginal p(yt) =

Rp(yt | θ)p(θ)dθ implies that accessing the desired

posterior distributions requires simulation schemes. This paper presents a sequen-tial simulation strategy to calculate both p(θ | yt) and p(yt) based on a resample-sampling framework called Particle Learning (PL). PL is a direct extension of theresample-sampling scheme introduced by Pitt and Shephard (1999) in the fixed-parameter, time series context.

Our new look at Bayes’s theorem delivers a sequential, on-line inference strategyfor effective posterior simulation strategies in a variety of commonly used models.These strategies are intuitive and easy to implement. In addition, when contrastedto MCMC methods PL delivers more for less as it provides

(i) posterior samples in a direct approximations of marginal likelihoods;

(ii) parallel environment, an important feature as more multi-processor computa-tional power becomes available.

Central to PL is the creation of an essential state vector Zt to be tracked sequen-tially. We assume that this vector is conditionally sufficient for the parameter ofinterest; so that p(θ |Zt) is either available in closed-form or can easily be sampledfrom.

Given samples Z(i)t , i = 1, . . . , N ∼ p(Zt | yt), or simply Z(i)

t by omitting Nfrom the notation, then a simple mixture approximation to the set of posteriors (ormoments thereof) is given by

pN (θ | yt) =1N

NX

i=1

p(θ |Z(i)t ).

This follows from the Rao-Blackwellised identity,

p(θ | yt) = E p(θ |Zt) =

Zp(θ |Zt) p(Zt | yt) dZt.

If we require samples, we draw θ(i) ∼ p(θ |Z(i)t ). See West (1992,1993) for an early

approach to approximating posterior distributions via mixtures.

The task of sequential Bayesian computation is then equivalent to a filteringproblem for the essential state vector, drawing Z(i)

t ∼ p(Zt | yt) sequentially fromthe set of posteriors. To this end, PL exploits the following sequential decompositionof Bayes’ rule

p(Zt+1 | yt+1) =

Zp(Zt+1 |Zt, yt+1) dP(Zt | yt+1)

∝Z

p(Zt+1 |Zt, yt+1)| z propagate

p(yt+1 |Zt)| z resample

dP(Zt | yt).

Particle Learning 319

The distribution dP(Zt | yt+1) ∝ p(yt+1 |Zt)dP(Zt | yt), where P(Zt | yt) denotes thedistribution of the current state vector. In particle form this would be representedby N−1 PN

i=1 δZ

(i)t

, where δ is the Dirac measure.

The intuition is as follows. Given P(Zt | yt) we find the smoothed distributionP(Zt | yt+1) via resampling and then propagate forward using p(Zt+1 |Zt, yt+1) tofind the new Zt+1. Making an analogy to dynamic linear models this is exactly theKalman filtering logic in reverse, first proposed by Pitt and Shephard (1999). Froma sampling perspective, this leads to a very simple algorithm for updating particlesZ(i)

t to Z(i)t+1 in 2 steps:

(i) Resample: with replacement from a multinomial with weights proportional to

the predictive distribution p(yt+1 |Z(i)t ) to obtain Zζ(i)

t ;

(ii) Propagate: with Z(i)t+1 ∼ p(Zt+1 |Zζ(i)

t , yt+1) to obtain Z(i)t+1.

The ingredients of particle learning are the essential state vector Zt, a predictiveprobability rule p(yt+1 |Z(i)

t ) for resampling ζ(i) and a propagation rule to update

particles Zζ(i)t to Z(i)

t+1. We summarize the algorithm as follows:

Particle Learning (PL)

Step 1. (Resample) Generate an index ζ ∼ Multinomial(ω, N) where

ω(i) =p(yt+1 |Z(i)

t )PN

i=1 p(yt+1 |Z(i)t )

;

Step 2. (Propagate)

Z(ζ(i))t+1 ∼ p(Zt+1 |Z(ζ(i))

t , yt+1);

Step 3. (Learn)

pN (θ | yt+1) =1N

NX

i=1

p(θ |Zt+1).

Example 1 (Constructing Zt for the i.i.d. model). As a first illustration of the

derivation of the essential state vector and the implementation of PL, consider the following

simple i.i.d. model

yt | λt ∼ N(µ, τ2λt)

λt ∼ IG(ν/2, ν/2)

for t = 1, . . . , T and known ν and prior µ | τ2 ∼ N(m0, C0τ2) and τ2 ∼ IG(a0, b0).

Here the essential state vector is Zt = (λt+1, at, bt, mt, Ct) where (at, bt) index the

sufficient statistics for the updating of τ2, while (mt, Ct) index the sufficient statistics

for the updating of µ. Set m0 = 0 and C0 = 1. The sequence of variables λt+1 are

320 H. F. Lopes, C. M. Carvalho, M. S. Johannes and N. G. Polson

i.i.d. and so can be propagated directly from p(λt+1), whilst the conditional sufficient

statistics (at+1, bt+1) are deterministically calculated based on previous values (at, bt) and

parameters (µt+1, λt+1). Here µt+1 simply denotes draws for the parameter µ at time t+1.

Given the particle set (Z0, µ, τ2)(i), PL cycles through the following steps:

Step 1. Resample (Zt, µ, τ2)(i) from (Zt, µ, τ2

)(i) with weights

w(i)t+1 ∝ p(yt+1 |Z(i)

n ) = fN (yt+1; m(i)t , τ2(i)

(C(i)t + λ(i)

t+1)), i = 1, . . . , N ;

Step 2. Propagate a(i)t+1 = a(i)

t + 0.5 and b(i)t+1 = b(i)t + 0.5y2t+1/(1 + λ(i)

t+1), and sample

τ2(i)from IG(a(i)

t+1, b(i)t+1), for i = 1, . . . , N ;

Step 3. Propagate C(i)t+1 = 1/(1/C(i)

t + 1/λ(i)t+1) and (C(i)

t+1)−1m(i)

t+1 = (C(i)t )

−1m(i)t +

yt+1/λ(i)t+1, and sample µ(i)

t+1 from N(m(i)t+1, C(i)

t+1), for i = 1, . . . , N ;

Step 4. Sample λ(i)t+2 from p(λt+2) and let Z(i)

t+1 = (λt+2, at+1, bt+1, mt+1, Ct+1)(i)

, for

i = 1, . . . , N .

!

!!

!

!

!

!!!! !

!!!

!!

!

!

!

!!

!

!

!

!

!!

!

!

! !

!! !

!

!

!

!!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!!

!

!

!

!

!!

!

!

!!

!

!!

! !

!

!!

!

!

!

!!!

!

!!

!! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!!! !!

!

! ! !

!!

!

!

!

!!

!

! !

!

!!

!

!

! !!

!

!!

! !!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!!

!

!

!

!

! ! ! !!

!

!

!

! !

!

!

!

!

!

!

!

!!

!

!!

!!

!!

!

!

!!!

!

!!

!

!

!!

!!

!

!

!!

!! !

!

!

!!

!!

!

! !

!

!!

!

!

!

!

!!!

!! !!

!

!!!

!

!!

!

!

!!

!

! !!!!

!!

! !!

!

!

!!

!!

!!

!! !

!

!

!

!

!!

!

!

! !

!

!!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!! ! !

!

!

!

!

!

!!

!

!!

!

!

!!

!!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!!!

!

!

!

!

!

!! !!

!

!!

!!

!

!

! !!

!

!

! !

!

!!

!

!

!

!!

!

!

!!!!

!!

!

!

!

!!

!!

!

!!

!

!

!

!

!

!!

!!!!

!!

!

!

!

!

!

!

!!

!!!

!

!

!

!

!!

!

!

!

!!

!!

!

!

!

!! !

!

!

!

!

!

!

!

! !

!

!

! !

! !

!!!

!!

!

!

!

!!

!

!!!

!

!

!

!

!!

!

!!! !

!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!!

! !

!!

!!

!

!!

!

!

!!

!

!

!

!

!

!

!!

!!

!!

!

!

!!

!!!!! !

!

!!!

!

!

!

!

!

!

!

!

!

!

!

!

!!!! !

!

!

!

!

!!!!

!!!! !!

!

!!

!

!

!

!!

!

!

! !

! !

!

!!!

!!

! !!

!!

! !!!

!!!

!

!

!

!!

!

!

!!!

!!

! !!

!

!

!

!

!

!!!

!!!

!!!

! !

!!

!

!

!!

!

!

!

! !! !

! !!

!

!

!

!

!

!!!

!!!

!!

!

!

!

!

! !

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!!

!

!

!!

! !!!!

!

!

!

!!!

!

!

!

!

!

!

!

!

!

!!!

!!!!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

! !!!!

!!

!!

!

!!!

!

!!

!!

!

!!

!

!

!!

!

!!!!! !

!

!

!

!

!

!

!

!!

!

!!

!!

!!! !

!!

!

!

!

!

!

!!

!

!

!

!

!

!

!!

!

!

!

!

!

!!

!

!

!!

!

!!

!

!

!

!

!

!

!

!!

!

!

!!

!!

!

!

!

!!

!! !!

!

! !

!

!

!

!

!

!

!!

!

!

!

!!!

!

!

!!

!!

!!

!!

!

!!

!

!! !

!

!

!

!

!!!

!

!!

!

!!

!

!!

!

! !

!

!! !

!

!

!

!

!

!!

!!

!

!!

!

!!

!!

!

!

!

!!!!

!! !

!

!!

!! !!!!

!!!!

!

!

!

!

!

!

!!

!!

!!!

!

!

!

!!

!

!

!

!

!

!

!

!!!!

!

! !!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!!

!!

!!! !

!! !

!!

!

! !!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!

!!! !

!!

!

!

!!

!

!

!

!!

!

!

!

!

! !!

! !

!!!

!! !

!!

!

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

! !!

!

!

!

!

!

!

!

!!!

!

! !

!

!

!!

!

!

!!

!!

!

!

!

! !

!!

!

!!!!

!

!

!

!

! !

! !

!

!

!

!!

!

!

!!

!

!

!!

!

!

!

!

!

!

! !

!

!

!

!

!

!

!

!

! !!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!!

!

! !!

!! !

!

!!!

!

!!

!

!!

!

!

!!

!

!

!

!!

!

!

!

!

!!! !

!

!

!

!

!

!!

!

!

!!

!!!

!!

!!

!!

!!

!

!

!

!

!

!

!!

!

!

!!

!

!!

!!!

!

!

!

!

!!

!

!!

!

!

!

!

!!

!

!!

!

!!

!

!!

! !

!

!

!

!!

!!

!

!

!

!

!

!

!!!

!

!

!!

!

!

!

!!

!

! !

!!

!

!

!

!

!

!!

! !

!

!

!!

!

! !!

!

! !

!!

!

!

!!

!

!

!

! !!

!

!

!!

!!

!

!

!!

!

!

!

!!!

!!!

!

!!

!!

!

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!!

!

!

!

!

!

! !!!

!

!!!!!

!!!

!

!!!

!

!

!

!! !!

!

!

!

!

!!!

!

!

!

!

!

!

!

!

!

!!

! !

!

!

!

!

!

!!! !!!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!

!!

! !!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!

!!!!

!

!!

!!

!! !

!

!

! !

! !! !

!

!

! !

!

!

!

!

!

!!

!

! !

!

!!

!!!!

!

!

! !!

!

!

!!

!

!

!

!

!

!

!

!

! !!

!

!!

!

!

!

!!

!!

!

!!!

!

!

!

!!

!

!

!

!!

!

!!

!!

!

!

! !

!

!

!!!

!!

!

!!

!

!!

! !!

!

!

!!

!

!

!

!!

!!

!!

!

!

!

! !!

!!!

!

!!

!!

!

!! !!!

!!

!

!

!! !!

!

!

!

!

!

!

!

!!

!

!!

!

!!

!!!!

!

!

!

!

!! !!

!

!

!

!

! !

!

!

! !!

!

!

!

!

!

!

!

!!!

!!

!

!

!!

!!

!

!

!

!

!

!!

!

!!

!!

!

!

!!

!!

!

!

!!

!!

!

!

!

! !!

!

! !

!

!

!!

!

!!

!

!!!

!!

!!

!!

!

!

!

!

!

!

!

!

!

! !!

!

!! !!

!!

!

!

!

!!

!

!

!

!!!

!!!

!

!

!

!

!

!!

!

!

!!

!

!

!

!!

!!

!!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!!

! !

! !

!!

!!

!

! !

!!! !

!

!!

!

!!

!!

!! !!

!

!

!

!

!

!

!

!

!

!!! !

!

!

!

!

!!

!!

!!

!

!

! ! !!!

!

!

!!

!

!!

!

!!

!

!!!

!

!

!!

!

!!!

!

!!

!

!

!!!!!

!

!

!

!

! !!!

!!

!

!

!

!

!!

!

!

! !!!

!!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!

!!!

!!!!

!

!

!

!!

!

!

!!

!

!

!

!

!!

!!

!!

!

!!!

!!

!

!

!!

!

! !!

!

!!

!

!

!

!

!

!

!!! !

! !

!

!

!

!

!

!

!

!

!

!!!!

!!

!

!

!

! !!!

! !

!

!

!

!!

!!

!

!!

!

!

!

!

! !

!! !!!!!

!! !

!

!!

!!

!!

!!

!

!!

!

!

!!

!

!

!

!

!!

!

!!

!

!

!

!!

!!

!!

!

!!

!

!!

!

!

!

!

!

!

!

!

!!

!!

! !

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!!

!

!!!

!

!

!

!

!

!!

!

!!

!

!

!

!!

!

!

!

!!

!!

!

!

!

!!

!

!!

!

!

!! !!!

!!!

!!

!!! !

!

!!

!

!!

!

!

! !

!

!

!!

!!

! !!

!!

!!

!!!

!

!!

!!!!!

! !!

!!! !

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!!!

!

!!

!

!

!

!

!

!!

!

!

!

!

! !

!

!!

!

!!!!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

! !!!

!!

!

!

!!

!!

!

!!

!

!!! !

!!

!!!

!

!!

!

!!

!

!

!!!

!

!! !

!!

!!

!

!

!

!! ! !! !

!!

!!!

!!

!

!!

!!

!

!

! !

!

!

!

!

!

!

!!

! !!

!!!! !

!

!

!!

!

!

!!!!

!! !!

! !

!

!

!

!! !

!!!

! !

!!!!

!!

!

!

!

!

!!

!!

!

!

!

!

!!

! !

!

!

!

!

!!!

!

!

!!

!

!

!

!

!

!!

!!

!

!

! !

!! !

!

!

!

!

!!

!

!

!!

!

!!!

! !

!!

!!

!!!!

!

!

!!

!

!!

!

!

!!

!!

!

!!

!

!!!

!

!!

!

!!

!!

! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!!!

!!

!

!!

!

!!!

!

!!!

!

!

!

!! !!

!

!

!!! !

!!

!!!!

! !!

!!

!

!!

!!!

!

!

!

!!

! !!

!

!!

!!!

!

!

!

!

! !

!

!!!

!

!

!!

!

!

!

!

! !!!!

!

!

!!

!!

!

! !

!

!

!

!

!

!!

!! !

!

!

!

!

!!

!!

!

!!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!!! !!

!

!

!

!

!

!!

!!

!! ! !

! !

!

!! !

!!

!!

!!

!

!

!

!!

!

!

!

!

!!!

!

!

!

!

!!!

!

!

!

!

!

!!

!

!

!!!

! !!

!

!

!

!

!

!!

!

!!

!!

!

!

!

!!

!

! !!

!

!

!

!!!

!

!

!!

! ! !

!

!

!

!

!

!

!!

!!

!

!

! !!

!

!!

!!

!

!

!

!

!!

!!

!

! !

!

!

!! !

!!

!

!!!

!

!

!!

!! ! !!

!

!

!

!!!!

!!!!

!!

!

!

! !!

!

!

!

!

!

!

!!

!!!

!

!

!!

!

!

!!!

!!

!

!!

!!

!

!

!

! !

!

!!

!

!

! !

!

!

!

!!

!

!

!!

!

!

!

!

!

!!

!! !!!

!

!!

!

!

!

!

!

! !!

!

!!

!!!

!!

!

!!

!!!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!!

!!

!

!

!!

!

! !

!

!

!

!!

!

!!

!!

!!

!!!

!

!!

!!

!

!

!!

!

!!!

!!!!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!!

!

!

!! !

!!

!

!

!!

!

!!!

!

!!

!

!!

!!!

!!

!!! !

!

! !!! !!!

!

!

!!

!

!

!!

!!

!!

!! !!

!

!

!!

!!

!

!

!

!

!

!!!

!!

!

!

!!

!

!

!

!

!

! !!! !

!!

!

!! !!

!!

!!

!

!

!

!

!!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!

!

!

!!

!

!!!

!

!

!!

!

!

!!

!

!

!!

!

!

!!

!

!!

!!

!

!

!

!

!

!

!

!!!

!

!!

!

!

!

!

!! !! !! !

!

!

!

!

!

!

!

!

! !

!

!

! !

!!

! !!

!!

!

!

!!

!

!

! !

!

!

!

!

!! !

!!! !!

!

!!

! !

!

!

!

!! !!

!

! !!

!!

!

!!

!!

!! !

!

!

!

!

!!

!

!

!

! !

!

!

!

!

! !!

!

!!!

!

!

!

!

!

!

!

!! !

!

!

!

!

!

!

!

!!

! !

!

!

!!

!

!!

!!!

!! !

!!

!

!!

!

!!!

!

!

!

!

!!

!

!

!!

! !

!

!!

!

! !

!

!

! !!

!

!!!

!

!

!

!

!!

!!

!

!

!

!

!!

! !

!!

!

!

!

!!

!

!!

!!!

!!

!

!

!!

!

!

!

!!

!

! !

!

!!

!!

!

!

!!

!!

!

!

!

!

!

!

!

!

! !

!!!!

! !

!!

!

!

!

!!

!!!

!

!

!!

!

!

! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!!

!

!

!

!

!!

!!

!!!

!!

!!

!

!

! !

!

!

!

!

!

!

! !! !

! !

!!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!!

!!

! !!!

!!!

!

!

!

!!

!!

!!

!!

!!

!

!

!!

!!

!

!!

!

!!

! !

!

!!

!

!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!!!

!

!!

!

!

!

!

!

!

! !

!

!!!

!!!

!!

!

! !

!

!!

!!

!! !

!!!!

!

!

!

!

!

!

!!

!!

!

!

!! !

!!!!

!!

!!

!

!!

!

!

!!

!! !

!

! !!

!!

!

!!

!

!

!

!

!

!!

!

!

!!

!

!

!!

!

!

!

!! !

!

!!

!!!

!

!

!

!

!

!! !

!!!

!

!

!!

! !

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

!

!!

!!

!

!

!!

!

!

! !

!

!

!

!

!!!!!

!

!!

!! !

!

!

!!!

!

!

!! !

!!

!

!

!!

!

! !!

!!

!!

!!

!!

!

!

! !!

!

!

!

!

!

! !

!

!

!

!! !!

!

!

!!!

!!

!

! !

!!!

!!!

!!

!

!!!

!

!!

!!

!

!

!

!!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!!

!

!

!

!

!

!!

!!!!!

!

!

!

!!

!

!

! !

!

!

!

!

!

!!

!!!

!

!

! !!!!

!!

!!

!!

!!

!!

!

!!!!

!

!!

!

!

! !

!

!

!!

!

!

!!!!

!

!!

!

!

! !

!

!!

!

!! !

!

!

!

!

!

!!!

!!

!

!

!

! !!!

!

!!!

!

! !!

!

!!! !

! !!

!!!

!

!!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!!

!

!!

!

!

!

!

!

!

!

!!

!

!!

!

!!!

!!

!

!

!

!!!

!

!!

!

!

! !!

!

!!

!

!

!

!

!

!

!

!

!

!!

!

!

!!! !

!!

! !!

!

!! !

!

!!!!

!

!

!!

!!

!

!

!!

!

!

!

!

!

!! !

!

!

!

!

!

!!

!!

!

!

!!

!! !

!

! !!!

!!

!

! !!

!!!

!

!

!

!

!!

!!

!

!!!

!

!

!

!

!

!

!

!

! ! !!

! !

!!

!!

!!

!

!

!

!!!

!

!

!

!

!

!

!! !

!!

!

! ! !

!!

!

!

!

!!

!

!!

! !

!!

!!

!!

!!

! !

!

!

!!

!

!!!

!! !

!!

!

!!!

!

!

!

!

!

!

!

!

! !

!

!

!!!

!

!

!

!

!!!

!! !

!

!

!!! !

!

!

!! !!

!

! !!

!

!

!!

!

!

!

!!

!

!!

!!!

!

!!

!

!

! !

!

!

!

!

!

!

!

!!

!!

!!

!!

!! !

!

! !!

!!

!!!

!

!

!

!

!

! !

! !

!!!

!

!

!!!! !

!

!!!!! !

!

!!

!

!

!

!!

!

!

!!!

!

!

! ! !!

!

!

!!

!!

!!

!

!!

!!

!!

!

!!

!

!

!!

!

!!

!

! !

!!!

!

!

!

!!

!

!

!!

!

!!

!

!

!

!

!

!

! !!

!

!!

!

!

!

!! !

!

!

!

!

!!

!!!

! !!

!

!

!

!!!

!!

!!!

!!

!!

!!

!

!

!!

!!!

!

!

!!

!

!

!

!

!!

!!

!!

!!! !

! !

!

!

!

!

!

!

!!!

!

!

!!

! !

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!!!

!

!

!

!

!

!

!

! !!!!!

!

!

!

!

!

!!

!!

!!

!!

!

!

!!

!

!

!

!

!

!!

!

!

!

! !!

!

!

!

!

!!

!

! !!

!

!

!

!

!!

!!

!

!

!

!

!!!

!

!

!!

!!

!!

!!

!

!!

!

!

!

!

!!

!!

!!

! !

!!!!

!!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!!

! !!!

!

!! !

!

!

!

! !! !

!

!!

!

! !

!!!

!

!

!

!

!!

!

!

!

!

! !!!

!

! !!!

!

!!

!

!

!!

!

!

!!

!!

!

!!!

!

!! !

!

!!!

!

!

!

!!!

!

!

!!

!

!

!

!

!

!

!

!!!

!

!

!

!

! !

!

!!

!!

!

!

!

!

!!

!

!!

!

!

!

!

!! !

!!

!!!

!!! !

!!!

!

! !

!!

!

!

!

!!

!

!

!

!

!

!

!

! !

!

!

!!!!

!! !

!

! !

!

!

!!

!

!

!

!

!!

!! !

!!

!!

!

!

!

!!

!

!

!

!

!!

!!

!

!!

! !

!

!!

!!

!

! !!

!

!

!! !

!

!

!!

!

!

!

!

!

!

!

!

!

! !

!

!!!

! !!

! !!

!!

! !

!!

!

!!

!

!

!!

! !!

!

!!

!

!

!!

!!!! !

!

!

!!

!!

!

!

!

!

!

!! !

!!

!!

!

!! !

!

!

!!!

!!

!

!!!

!

!

!

!

!

!

!!!

!

!

!

!

!

!

!

! !!

!

! !

!

!!

!!

!

!

! !!!

!

!!

!

!

!!

!!

! !!

!

!

!

!

!

!!!

!

! !

!

!

!

!

!

!

! !

!

!!!

!

!!

!

!

!!

!!

!!

!

!

!!

!!

!

! !

!!

! !

!!

!

!

!

!

!!

!!

−0.5 0.0 0.5 1.0

0.00

0.05

0.10

0.15

0.20

0.25

GIBBS

µµ

!!2

!!

!

!!

!

!

!

!

!

!

!!!

!

!!!

!

!

!!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

! !

!

!! !! !

!

!

!!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

! !!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

! !!

!

!

!

!!

!!

!

!

!

!

! !

!!

!

!

!

!

!!

!!

!

!

!

!

!!

!

!

!

!

!

!

!!

!

!

!

! !

!

!! !!

!

!!

!

!

!

!

!

!

!

! !

!

!

! !!

!

!

!

!

!

! !

!

!

!

! !!

!

! !

!

!

! !

!

!!

!!

!

!

! !!

!!

!

!

!

!

!

!!

!

!!

!!! !

!

!

!

!

!!

!!

!

!

! !!

!

!

!

!

!

!

!!

!

!

!

!!

!!

!

!!

!

!

!!

!!

!

!!!

!

!

!

!

!

!!

!

!

!

! !

!

!

!

! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!!

!

!

!

!!

! !

!

!

!

!

!! !

!!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!!

!

!!

!

! !

!!

!

! !

! !!

!

!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!

!

!!!

!

!

!

!

!

!

!

!

!!!

!

!

!

!

!

!!

!!

!

!

!!!

!

!

!

!

!

!

!

!

!

!

! !!

!!!

!

!

!

! !

!

!!

!

!!

!

!

!

!

!

!

!!

!

! !!

!!

!

!

!

!

!!!

!

!

!

!

!

!

!!

!!!

!!!

!

! !!

!!

!!

!

!

!

!!!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!!

!

!

!

!

!

!

!!

!

!

!

!

!

!!!

!

!

!

!!

!

!

!!

!! !

!

!

!

!

!

!

! !!

!

!

!

!!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!!!

!

!

!

!

!

!

!

!!

!

!! !

!

!

!

!

!!

!!

!

!!

!! !

! !!

!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!!!

!

!

!

!

!

!

!

!!

!

!

!

!!

!

!!!

!

!

!

!

!

!

!

!

! !

!

!

!

!

!!

!!!

!

!

!!

!

!

!

!!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!!

!!

!

! !

!!!

!

! !

!

!

! !!

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!!!

!! !

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!!

!

!

!!

!

! !!

!!!

!

!

!

!

!

! !

!

!!

!

!

!!!

!

! !!

!

!

!

!

!

! !

!

!

!

!

!

!

!!

!!!

!

! !

!

!

!

!

!!

!

!

!

!

! !!

! !!

!

!!!

!

!

! !!

!

!

!

!

!

!

!

!

!

!

!

!!!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

!!!!

!

!

!

!

!!

!

!

!!!!!

!

!

! !

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!!

!

!

!!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

! !

!

!

!!

!

!!

!

!

!

!

!!

!

!

!

!

!

!

!

! !

!!

!

!!!

!

!!

!

!!

!

!

!

!

!!!

!

!!

!!

!

!

!

!

!

!!

!!!

!

!!!!

!

!! !

!!

!

!

!

!

!

!

!

!

!!

!!

!!

!!

!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!!!

!

!!!

!

!

! !!!

!

! !

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!!

!

!! !

!

!

!

!

!

!

!

!!

!

!

!

!

!!!!

!! !

!

!

!

!

!

!

!

!

!!!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!!

!

! !

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!!

!

!

!!!

!!

!

!

!

!

!

!

!

!

! !

!

!!

!!!

!

!

!

!

!!

!

!

!

!!!

!!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!!

!

!! !

!

!

!

!

! !

!

!

!

!

!!

!

!

! !!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

! !

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

! !

!!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!

!

!

!

! !

!

!!

!

!

! !!

!

!

!

!

!!

!

!

!!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

! !!

! !

!

!!

!

!

!

!

!

!

!

!

!

!!!

!

!

!

!

!

!!

!

!

!

!

!!

!

!!!

!

!!

!

!

!

!

!

!

!!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!!!

!

!

!

!!!

!

!

!

! !

!

!

!

!

!!!

!

!!

!!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!! !

!

!!

!!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!!

! !!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

! !!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!!!!

! !

!

!

!

!

!

!

!

!

!!

!

!

!

!!

!

!

!!!

!!!!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!!

!

!

!

!

! !

! !

!!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!! !

!

!!

!

!!!

!

!

!

!!

!

!!!

!

!

!

!

!!

!

!!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!!!!

!!

!

!

!

!

!!!

!

!

!

!!

!!

!!

!!

!

!

!

! !

!

!

!!

!

!!

!

!!!

!

!

!

!

!

!

!

!

! !

!! !

!

!

!

!

!!

!

!

!

!

!

!

! !

!

!

!

!!

!

!

!

!!

!

!

!

!

!

!!

!

!

! !

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

! !

!

!

!

!!

!

!

!

!

! !! !

!!

!

! !!!

!

!

!!

!

!

!! !

!!

!

!

!

!

!

!

!!

!

!

!!!

!

!

!! !

!

!!

!

!

!

!

!

!!

!

!! !

!!

!!

!

!!

!

!

!

!

!!

!

!

!!

!

!!

!

!

!

!

!

!

!

!

!

!!!

!

!!

!

!

!

!!

!

!

! !

!!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!!

!

!

!

!

!!

!

!

!

!

!! !

!!

!

!!

!

!

!

!!

!

!!

!

!

! !

!

!

!

!

!

!

!

!

! !

!

!

!

!

!

!

!!!

!

!

!

!

!

!

! !

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!

!

!

!! !

!!

!

!

!

!

!

!

!

!!

!

!!

!

!!

!

! !!!

!

!

!

! !

!!!

!!

!!

!!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!! !

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

! !

!!

!

!

!!

!

!

!

!!

!

! !!

!

!!

!!

!!

!!

!!!!

!

!

!

!!!

!

!

!

!

! !

!!!!

!

!

!

!

!

! !

!

!!

!

!

!

! !

!

!!

!

!!

!!

!

!! !!

!

!!

!

!

!

!

!

!

!

!

!

!!

!!

!! !

!

!!

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!

!

! !

!

!

! !

!

!

!

!

!

!!

! !!!!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!!! ! !

! !

!

!

!

! !!

!!

!

!

!

!

!

!

!

! !

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!

!

!

!!!!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!!

! !

!

!

!

!!

!

!!

!

!

!!

!

!

!

!!

!

!

!!

!!!

!!!

!

!!

!

!!

!!

!!

!

!!

!

!

!

! !

!

!

!

!

! !

!!

! !

!

!!

!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!

!!!

!

!!

!!!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!!!!

!!!

!

!!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!!

!

!

!

!

!!

!

!

!!

!!!!

!

!

!

!!

!

!!

!

!

!

!! !

!

!!

!

!

!

!!

!!

!

!

!

!

!!!

!!!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!

!! !

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!!

!!!

!

!!

!

!

!

!

!

!

!

!!!!

!

!

!

!

!!!!

!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!

!!!

!!

!

!

!

!

!

!

!!

!!!

!

!

!

!

!

!

!

!! !

!

!

!

!

!

!!!

!!

!

!!!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!!

!

!

!

!

!

!

!!!

!

!

!

!

!!

!

!

!!

!

!!

!

!!

!! !!

!

!!

!

!!

!

!

!

!

!

!

!! !

!!

!!

!

!!!

!

!!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!

!

!!

!!

!

!

!

!

!!

!

!

!! !

!!

!

!

!!

!

!!

!

!

!!

!!

! !!

!

!!

!

!

!

!

!

!!

!

!

!

!!

!

!

! !

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!

!!

!

!!

!

!!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!! !

!

!!

!

!

!

! !

!

!

!

!

!! !

!

!

!!

!!

!!

!

!

!

!

!

!!

!!

!!!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!!

!!

!

!

!

!

!

!!

!

!

!

! !

!

!

!

! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!!!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!!! ! !

!!!

!

!

!

! !!

!!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!!

!

!!

!

!

!

!

! !

!

!

!

!!

!!

!

!

!

!!

!

!

! !

!

!

!

! ! !

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!!!

!

!

!

!

!!

!! !!

! !!!

!

!

!

!

!

!!

!!

!

!

!

!!!!

!

!

! !!!

!

!

!!

!

!

!

!!! !

!

!!!

!

!

!!

!!!

!

!

!

!

!

!

!

!

!

!! !!

!!

!

!

!

!

!

!

!! !

!!

!

!!

!

!!

!

!!

!

!

!

!

!!!

!

!

!

!

!

!

!

!!!

!

!

!

!

!

!!

!

!

!!

!!

!

! !

!

!

!!

!

!

!!!

!!!

!

!!

!

!

!

!

!

!

!

!

!!

!

!

!

!!

!

!

!

!!

!

!! !

!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!

! !

!!

!

!!

!

!

!

! !!

!

!

!

!

!

!

!

!!

!!

!!

!

!

!

!

! !! !!

!!

!

!

!!

!

!

!

!!

!

!

!

!!

!!

!

!!!

!!

!

!

!

!!

!

!

!

!!

!

! !

!! !

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

! !

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

! !!

!

!!

!

!

!

!

!! !

!

!

!!

!

!!

!

!

! !!

!

!

!

!!

!!

!

!

!

!

!

!

!!

!

!

! !

!

!

!!

!

!

!

!!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

! !!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!!

!

! !

!

!!!

!

!

!

!

!

!

!

!

!!

!

!!

!

!

!!

!

!

!

!

!

!!

!

!!

!

!

!

!!!

!

!!

!

!

!

!

!

!

!!

!

!!

!

!!

!

!

!

!

!

!!

!

!

!

!

!

!

!!

!

!

!!!

!!!

!

!!

!

!!

!

!

!

!

!

! !

!

!

!!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!!

!!

!!

!!

!

! !

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!!

! !

!

!

!

!!

!

!!!

!!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!!

!

!!

!

!!

!

!!

!

!

!

!!!

!

!

!

!

!

!!

!

!!

!

!

!

!!

!

!

!

!! !

!

!!

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!!!!!

!

!!

!

!

!!

!

!

!

!

!!!

!!

!!!

!

!

!!!

!

!!

!

!!

!

!

!

!

!!

!

!

!

! !!

!

!

!

!

!

! !! !!!

!

!

!

!! !

!

! !

! !

!

! !

!!

!

!

!

!

!

!

! !

!!

!! !

!

!!

!

!

!

!

!

!!

! !

!!

!

!

! !!

!

!

!

!

!!

!!

!

!

!

!

!

!

!! !!

!

!!

!

!

!

!

!

!

!

! !

!

!

!

!!

!

!!!

!

!

!

!!

!

!!

!

!!

!

!

!

!!

!

!

!

!

! !

!

!!

!

!

!

!!!

!

!

!

!

!

!

!!

!

!

!!

!

!!

!

! !

!

!!

!

!! !!

!

!

!!

!

!

!

!

!

!!

!

!!

!

!

!

!!

!

!

!!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!!

! !

!

!

! !!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!!!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!!

!

!

!

!!

!

!!

!

!!

!

!

!

!!

!!

!

!

!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!!

!

!!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!! !!

!

!

!!

!!

!

!

!

!

!

!

! !!

!!!

!!

!

!

!

!

!

!

!

!

!!!

!

!

!

!

!

!!

!

!!

!

!

!

!!

!

!

!!

!

!!

!!!

!

!

!

!

!

!

! !

!

!

!!

!!

!

!

!

!

! !

!!

!

! !

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

! !

!

!

!!

!!

!!

!

!!

!

!

!

!

!

!

!

!

!

!!! !

!!!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

! !

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

! !

!

!!

!

!

!

!

!

!

!! !

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!!!

!

! !

!

!

!!

!

!

!

!!!

!!

!

!

! !

!

!

!

!

!!!

!

!

!

!

!!!

!

!!!!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

! !!

!

!

!

!

!!

!!! !

!!

!

!

!!!

!! !

!

!!

!

!

!

!!

!!

!

!

!!

!

!

!

!

!

!!

!

!! !

!!!

!

!

!

!

!

!!

!

!

!

!!

!!!

!

!

!!

!

!!

!!

!

!

!!

!

!

!!!

!

!

! !

!

!

! !

!

!!

!!!

!!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!

!!

!

!

!

!

!!

!!!

!!

!

!

!

!

!

! !

!!

!

!

!

!

!

!

!!

!

!

!

! !

!

!!

!

!!

!

!

!

!

!

!

!!

!

!

!

!!

!

!!!

!

! !

!

!

!!

!

!

!

!

!

!

−0.5 0.0 0.5 1.0

0.00

0.05

0.10

0.15

0.20

0.25

PL

µµ

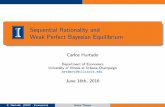

!!2

Figure 1: i.i.d. model. Gibbs versus Particle Learning. Data y =(−15,−10, 0, 1, 2), number of degrees of freedom ν = 1, and hyperparameters

a0 = 5, b0 = 0.05, m0 = 0 and C0 = 1. For the Gibbs sampler, the initial

value for τ2is V (y) = 58.3 and 5000 draws after 10000 as burn-in. PL is based

on 10000 particles. The contours represent the true posterior distribution.

In step 2 fN (y; µ, σ2) denotes the density of N(µ, σ2

) evaluated at y. The posterior

for µ and τ2could be approximated via a standard Gibbs sampler since the full conditionals

are

µ |λ, τ2, y ∼ N(g1(y, λ)/s(λ); τ2/s(λ))

τ2 |λ, y ∼ IG(a0 + T/2, b0 + 0.5g2(y, λ))

λt | τ2, yt ∼ IG

„ν + 1

2,ν + (yt − µ)

2/τ2

2

«t = 1, . . . , T.

where s(λ) = 1 +PT

t=1 λ−1t , g1(y, λ) =

PTt=1 yt/λt, and g2(y, λ) =

PTt=1 y2

t /(1 + λt).

Figure 1 provides an illustration of both PL to the Gibbs sampler.

Particle Learning 321

1.1. Constructing the Essential State Vector

At first sight, PL seems to be a rather simple paradigm. The real power, however,lies in the flexibility one has in defining the essential state vector. This may include:state variables, auxiliary variables, subset of parameters, sufficient statistics, modelspecification, among others. The dimensionality of Zt can also be included in theparticle set and increase with the sample size as, for example, in the non-parametricmixture of Dirichlet process discussed later.

In sum, the use of an essential state vector Zt is an integral part of our approach,and its definition will become clear in the following sections. The propagation rulecan involve either stochastic or deterministic updates and in many ways it is amodeling tool by itself. For example, in complicated settings (variable selection,treed models) the propagation rule p(Zt+1 | Zt, yt+1) suggests many different waysof searching the model space. It is our hope that with the dissemination of theideas associated with PL there will be more cases where the use of Zt leads to newmodeling insights. The following represent examples of the form of Zt in the modelsthat will be addressed later in the chapter:

(i) Mixture Regression Models: Auxiliary state variable λt and conditional suffi-cient statistics st for parameter inference;

(ii) State Space Models: In conditionally Gaussian dynamic linear models Zt