Overview of the Caribbean Tourism Sector: Managing Tourism Resources Mercedes Silva Sustainable...

27

Overview of the Caribbean Overview of the Caribbean Tourism Sector: Tourism Sector: Managing Tourism Resources Managing Tourism Resources Mercedes Silva Sustainable Tourism Specialist Adaptation to Climate Change in the Caribbean Tourism Sector Workshop Grenada, May 27 th , 2002

-

Upload

wesley-jenkins -

Category

Documents

-

view

219 -

download

1

Transcript of Overview of the Caribbean Tourism Sector: Managing Tourism Resources Mercedes Silva Sustainable...

Overview of the Caribbean Overview of the Caribbean Tourism Sector:Tourism Sector:Managing Tourism ResourcesManaging Tourism Resources

Mercedes SilvaSustainable Tourism Specialist

Adaptation to Climate Change in the CaribbeanTourism Sector WorkshopGrenada, May 27th, 2002

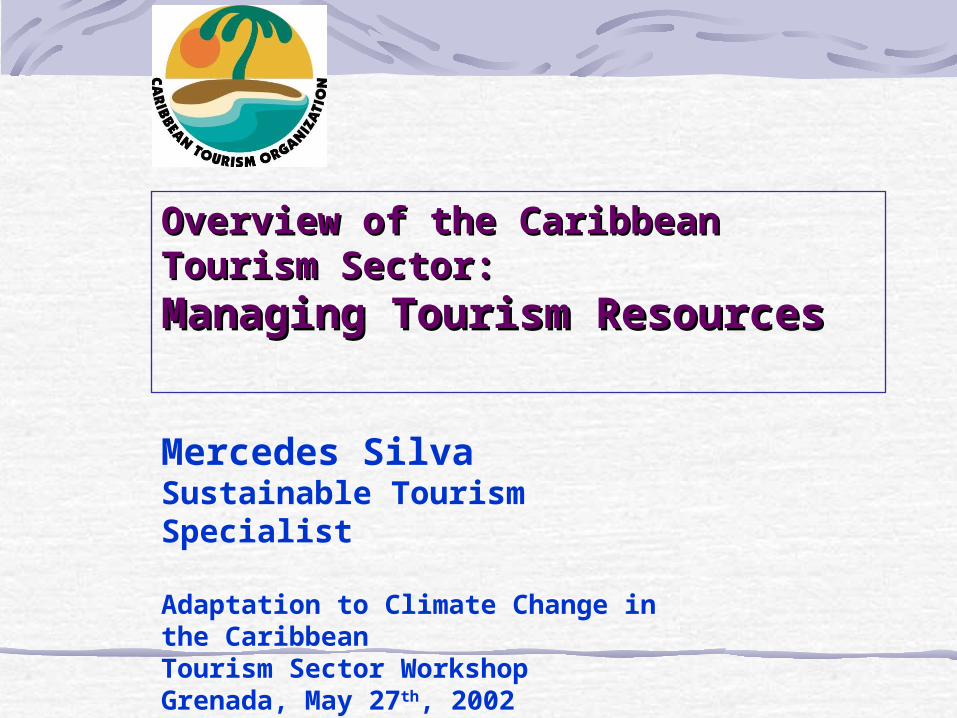

CTO MembershipCTO Membership

Caribbean Map

OECS Countries Dutch West IndiesAnguilla ArubaAntigua & Barbuda* BonaireBritish Virgin Islands CuracaoDominica* SabaGrenada * St EustatiusMontserrat* St MarteenSt Kitts and Nevis*St. Lucia * French West IndiesSt Vincent and the Grenadines* Guadeloupe

Martinique

Other CARICOM Hispanic CaribbeanThe Bahamas CubaBarbados Dominican RepublicBelize Mexico: Cancun / CozumelGuyana VenezuelaJamaicaTrinidad and Tobago US Caribbean

Haiti Puerto Rico Suriname US Virgin Islands

Other Commonwealth Bermuda Cayman IslandsTurks and Caicos Islands * CARICOM

CTO Caribbean Sub-RegionsCTO Caribbean Sub-Regions

Benefits of TourismBenefits of Tourism

Foreign Exchange

Government Revenue

Investment

• Job Creation

• Linkages to Other Sectors

• Socio-Cultural Development

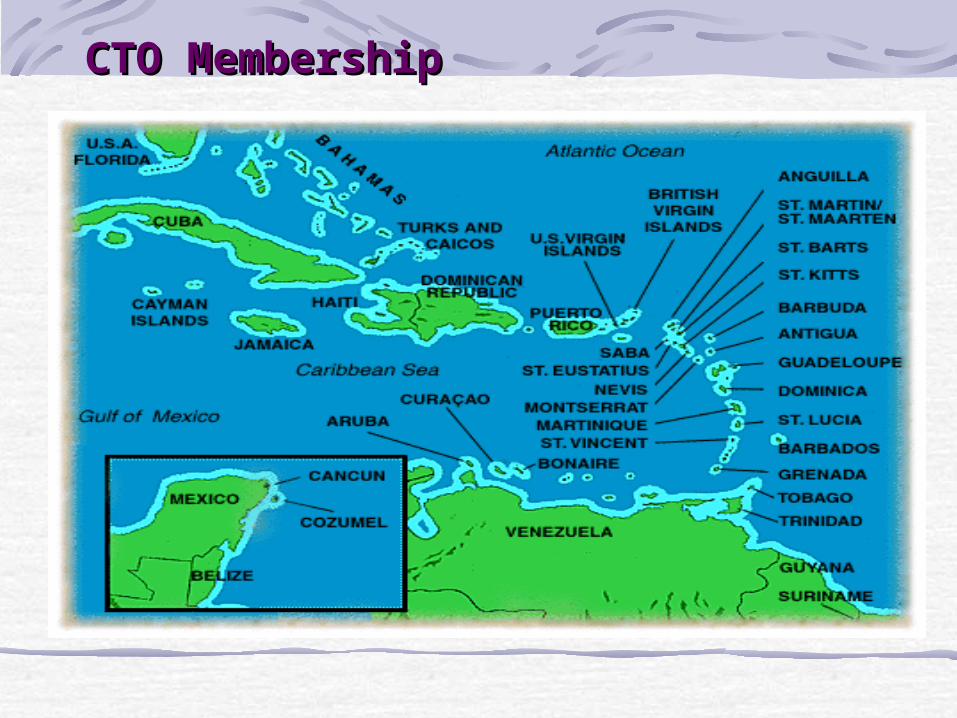

1415

1718

1920

0

2

4

6

8

10

12

14

16

18

20

1995 1996 1997 1998 1999 2000

US$ billion

P

Visitor Expenditure in the Visitor Expenditure in the CaribbeanCaribbean (US$ billion)

Employment in Tourism Employment in Tourism IndustryIndustry

CTO conservatively estimates that more than 900 thousand persons are directly or indirectly employed in the tourism industry (300 thousand in the accommodation sector)

Importance of Tourism to Importance of Tourism to Caribbean EconomiesCaribbean Economies

Visitor Expenditure as a Percentage of GDPAnguilla - 75%Cayman Islands - 60%St. Lucia - 55%Antigua & Barbuda - 49%Aruba - 41%Barbados - 36%St. Kitts & Nevis - 31%Grenada - 28%St. Vincent & G’dines - 28%Jamaica - 25%

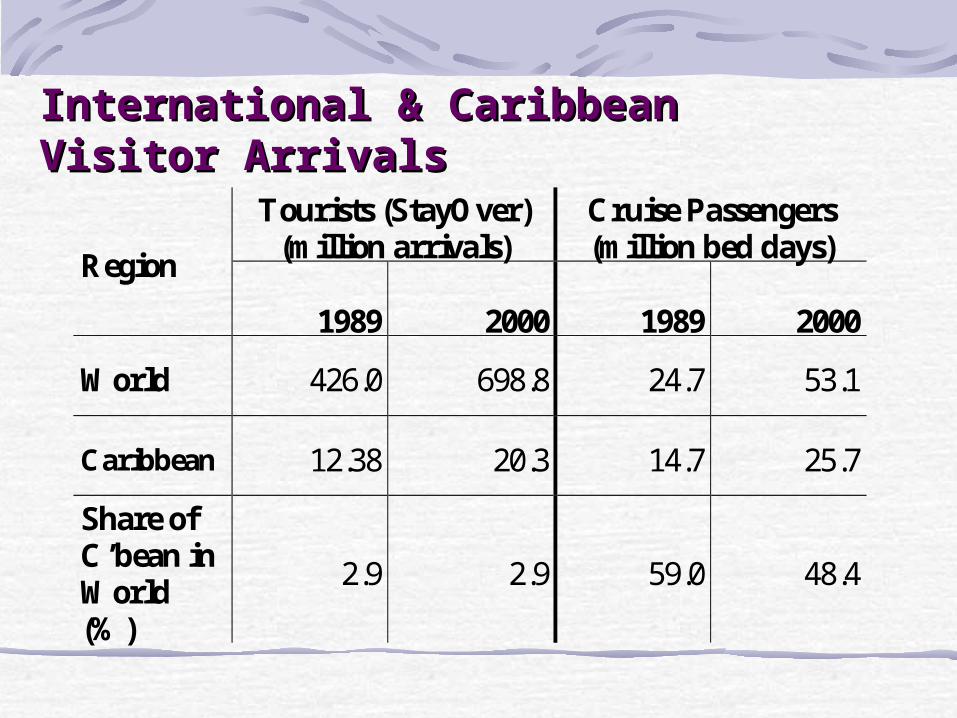

International & Caribbean International & Caribbean Visitor ArrivalsVisitor Arrivals

Tourists (StayOver) (million arrivals)

Cruise Passengers (million bed days)

Region

1989

2000

1989

2000

World 426.0 698.8 24.7 53.1

Caribbean 12.38 20.3 14.7 25.7

Share of C’bean in World (%)

2.9 2.9 59.0 48.4

0

20

40

60

80

100

120

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

YEAR

% GROWTH SINCE 1987

International & Caribbean International & Caribbean Tourist ArrivalsTourist ArrivalsGrowth Performance 1987-2000

CARIBBEAN

WORLD

0

50

100

150

200

250

300

350

1991 1993 1995 1996 1997 1998 1999 2000 2001

YEAR

% GROWTH SINCE 1989

International & Caribbean International & Caribbean Cruise Bed DaysCruise Bed DaysGrowth Performance 1991-2000

CARIBBEAN

WORLD

MEDITERRANEAN

-20

0

20

40

60

80

100

120

140

Year

% G

row

th

All Caribbean

Hisp. Caribbean

Fr. Caribbean

CARICOM

US Caribbean

Dutch Caribbean

Source : Caribbean Tourism Organization

Fr. Caribbean

Hisp. Caribbean

All Caribbean

US. Caribbean

Dutch Caribbean

CARICOM

1990 2000199919981997199619951994199319921991

Growth in Tourist Arrivals to the Caribbean and Growth in Tourist Arrivals to the Caribbean and Selected Sub-regions since 1991Selected Sub-regions since 1991

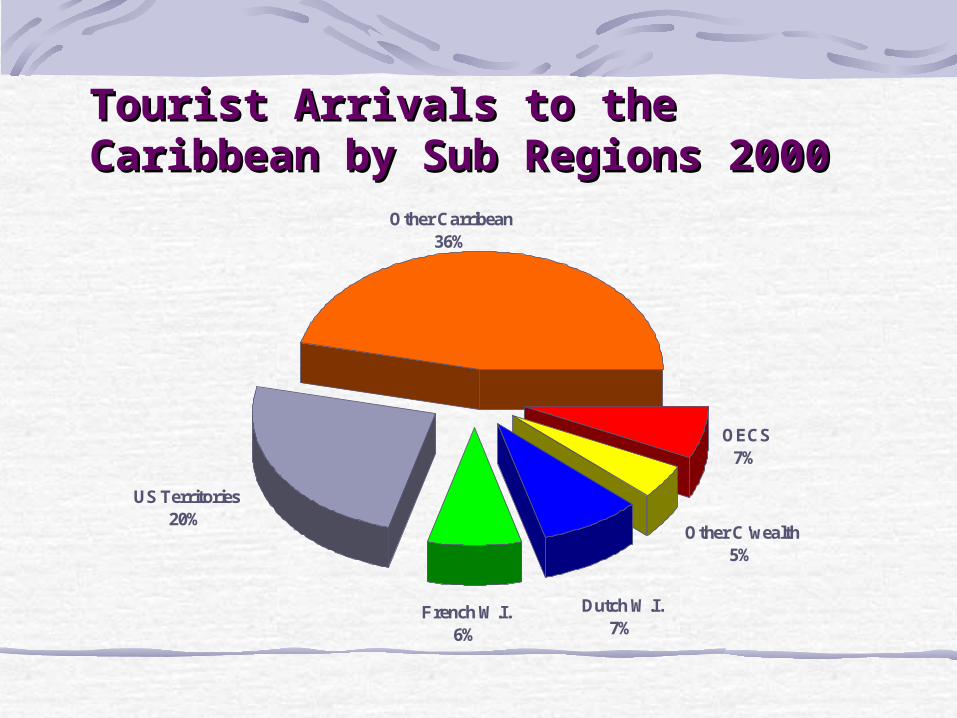

Tourist Arrivals to the Tourist Arrivals to the Caribbean by Sub Regions Caribbean by Sub Regions 20002000 Other Carribean

36%

US Territories20%

Other C'wealth5%

French W.I.6%

OECS7%

Dutch W.I.7%

Other11%

Europe26%

Canada6%

United States50%

Caribbean7%

Tourist Arrivals to the Tourist Arrivals to the Caribbean by Major Markets Caribbean by Major Markets 20002000pp

US Travel to Overseas US Travel to Overseas DestinationsDestinationsComparative Performance 1990 - 2000Comparative Performance 1990 - 2000

-15

-5

5

15

25

35

45

55

65

75

85

95

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Y E A R

All Overseas

Caribbean

Gulf War

Competition

Source USTIA

C A R I C OM

32%

HI SP A NI C

C A R I B B E A N*

57%

DU T C H C A R I B B E A N

4%

U S T E R I T OR I E S

5%

FR E NC H

C A R I B B E A N

1 %

OT HE R C A R I B B E A N

1 %

* Excludes Puerto Rico

C an adian T our is t A r r ivals t o

T he H ispan ic C ar ibbean - 2 0 0 0

p

Cuba

48%Dom

Rep

38%

Cancun

1 4%

Arrivals from Canada to the Arrivals from Canada to the Caribbean by Sub-region 2000pCaribbean by Sub-region 2000p

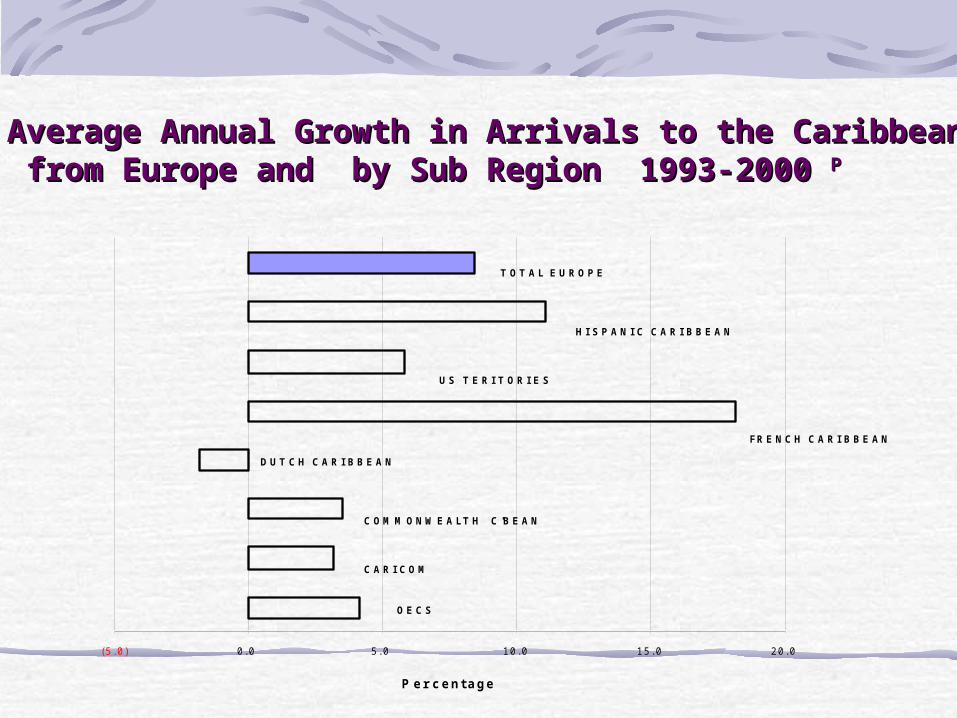

(5. 0) 0. 0 5. 0 10. 0 15. 0 20. 0

P er c entage

OE C S

C A R I C OM

C OM M ONWE A LT H C 'B E A N

FR E NC H C A R I B B E A N

DU T C H C A R I B B E A N

U S T E R I T OR I E S

HI S P A NI C C A R I B B E A N

T OT A L E U R OP E

Average Annual Growth in Arrivals to the CaribbeanAverage Annual Growth in Arrivals to the Caribbean from Europe and by Sub Region 1993-2000 from Europe and by Sub Region 1993-2000 PP

83.8

198.6 209.6 219.4232.6

244.1 251.3

0

50

100

150

200

250

300

Rooms (000)

1980 1995 1996 1997 1998 1999 2000

P

Room Capacity in the Room Capacity in the CaribbeanCaribbean

OECS1%

Other C'wealth

27%

Other52%

US Terr.7%

Dutch6%

French7%

60

61

62

63

64

65

66

67

Rate in %

1993 1994 1995 1996 1997 1998 1999

Occupancy Rates in the Occupancy Rates in the Caribbean Caribbean (percent)(percent)

Challenges to Caribbean Challenges to Caribbean TourismTourism

Diminished economic growth in many of our source marketReduced profitability of airlinesMore countries seriously adopting tourism as a viable development optionIncreased leisure travel options within our major marketsChanging Consumer PatternsChanging distribution systems

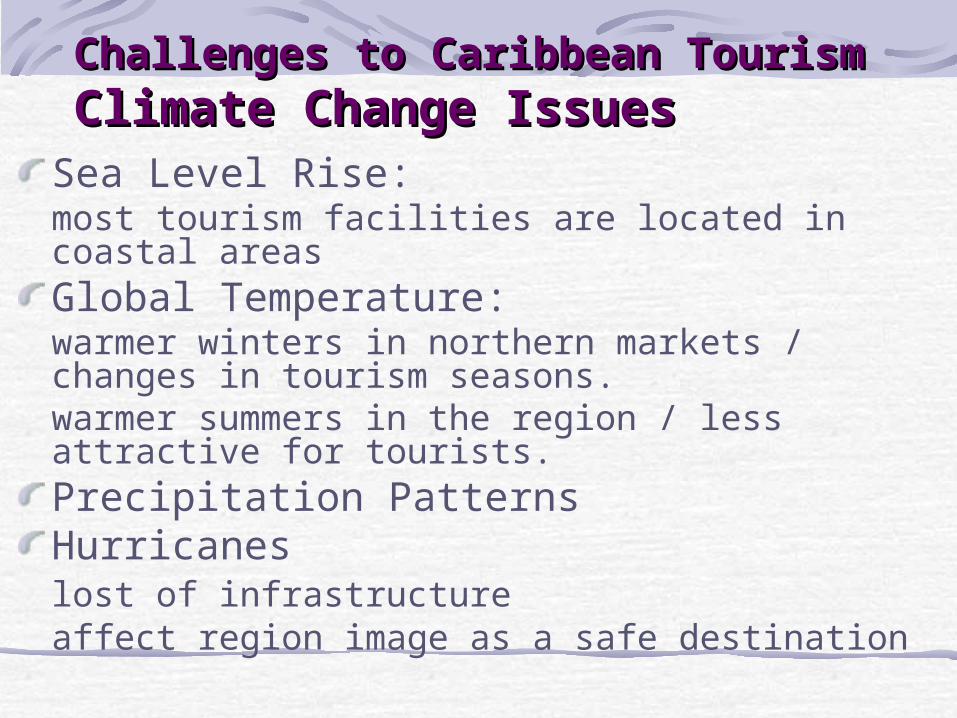

Challenges to Caribbean TourismChallenges to Caribbean TourismClimate Change IssuesClimate Change Issues

Sea Level Rise: most tourism facilities are located in coastal areasGlobal Temperature: warmer winters in northern markets / changes in tourism seasons.warmer summers in the region / less attractive for tourists.Precipitation PatternsHurricaneslost of infrastructureaffect region image as a safe destination

Today’s Changing ConsumerToday’s Changing ConsumerNew Standards of Expectation

less likely to be satisfied with sun, sea & sand alone

more knowledgeable & independent

more environmentally conscious

more security-concerned

more likely to travel in family/groups

Challenges After September 11thChallenges After September 11th

Safety and security the primary concern of travelers both in terms of Air travel and safety at the destination

Shorter booking window, reduced from three months to as much as four weeks

Economic downturn..increased un-employment

Growing Competition - ProductGrowing Competition - Product

higher levels of service outside Caribbean

freer cross-border travel (notably Europe)

huge growth in cruise ship inventory and cruising

destination

better scheduled airlift to other regions

Lack of investment and innovation in product

development in the region

Towards the FutureTowards the Future

The Caribbean is perceived as a safe destination

in comparison to its major competitors in the

middle east and Asia.

Declines in September estimated at 19% are

leveling off and showing positive signals of

recovery.

Preliminary estimates suggest that arrivals to

the region in 2001, declined by 2% compared to

2000

Greater effort in marketing & research

Towards the FutureTowards the FutureSustainable Tourism Sustainable Tourism ApproachApproachEfforts being made towards Sustainable

tourism initiatives inclusive of improved

product & human resource development

Natural Resource Protection

Carrying Capacity Assessments

Environmental and Financial Feasibility

Disaster Mitigation

Research and Education

Projected Growth in World & Projected Growth in World & Caribbean TourismCaribbean Tourism

ave.

annual 1995 2000 2010 %

ch.

Caribbean 14.7 20.3 28.4 4.6

World 567.0 698.8 937.0 3.6

% share 2.6% 2.9% 3.0%

millions

Mercedes SilvaSustainable Tourism Specialistmsilva@caribtourism.comwww.onecaribbean.orgwww.doitcaribbean.com

Adaptation to Climate Change in the CaribbeanTourism Sector WorkshopGrenada, May 27th, 2002