Oshkosh Corporation Investor Handout September 2011 Mission

21

Oshkosh Corporation Investor Handout September 2011 Mission Driven: To Move the World at Work

Transcript of Oshkosh Corporation Investor Handout September 2011 Mission

Oshkosh Corporation

Investor Handout

September 2011

Mission Driven:

To Move the World at Work

INVESTOR HANDOUT SEPTEMBER 2011

Forward Looking Statements

2

This presentation contains statements that the Company believes to be “forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including, without limitation, statements

regarding the Company’s future financial position, business strategy, targets, projected sales, costs, earnings, capital expenditures,

debt levels and cash flows, and plans and objectives of management for future operations, are forward-looking statements. When used

in this press release, words such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “should,” “project” or “plan” or the

negative thereof or variations thereon or similar terminology are generally intended to identify forward-looking statements. These

forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties, assumptions and other

factors, some of which are beyond the Company’s control, which could cause actual results to differ materially from those expressed or

implied by such forward-looking statements. These factors include the expected level and timing of DoD procurement of products and

services and funding thereof; risks related to reductions in government expenditures in light of U.S. defense budget pressures and an

uncertain DoD tactical wheeled vehicle strategy; the cyclical nature of the Company’s access equipment, commercial and fire &

emergency markets, especially during periods of global economic weakness, tight credit markets and lower municipal spending; the

Company’s ability to produce vehicles under the FMTV contract at targeted margins; the duration of the ongoing global economic

weakness, which could lead to additional impairment charges related to many of the Company’s intangible assets and/or a slower

recovery in the Company’s cyclical businesses than equity market expectations; the impact on revenues and margins of the decrease

in M-ATV production rates; the potential for the U.S. government to competitively bid the Company’s Army and Marine Corps contracts;

risks related to work stoppages and other labor matters, especially in light of the pending contract expiration for union employees at the

Company’s Oshkosh defense facilities; the consequences of financial leverage, which could limit the Company’s ability to pursue

various opportunities; increasing commodity and other raw material costs, particularly in a sustained economic recovery; the ability to

pass on to customers price increases to offset higher input costs; risks related to costs and charges as a result of facilities consolidation

and alignment, including that anticipated cost savings may not be achieved; risks related to the collectability of receivables, particularly

for those businesses with exposure to construction markets; the cost of any warranty campaigns related to the Company’s products;

risks related to production delays arising from supplier quality or production issues; risks associated with international operations and

sales, including foreign currency fluctuations and compliance with the Foreign Corrupt Practices Act; the potential for disruptions or

cost overruns in the Company’s global enterprise resource planning system implementation; the potential for increased costs relating to

compliance with changes in laws and regulations; and risks related to disruptions in the Company’s distribution networks. Additional

information concerning these and other factors is contained in the Company’s filings with the Securities and Exchange Commission,

including the Form 8-K filed July 28, 2011. The Company disclaims any obligation to update such forward-looking statements.

All operating results included in this presentation reflect results from continuing operations only.

Forward looking statements speak as of July 28, 2011.

Oshkosh Corporation Moves the World at Work

3 INVESTOR HANDOUT SEPTEMBER 2011

DEFENSE FIRE & EMERGENCY COMMERCIAL ACCESS EQUIPMENT

A Portfolio of Leaders

4 INVESTOR HANDOUT SEPTEMBER 2011

GLOBAL RANK

NORTH AMERICA(1) RANK Access Equipment #1

Fire Apparatus #1

Airport Products #1

Heavy Defense Trucks #1 (Army & Marines)

Concrete Mixers / Batch Plants #1

Refuse Collection Vehicles #1

Medium Defense Trucks #1 (Army & Marines)

(1) The leading supplier of heavy, medium and MRAP vehicles

for the U.S. Armed Forces

INVESTOR HANDOUT SEPTEMBER 2011

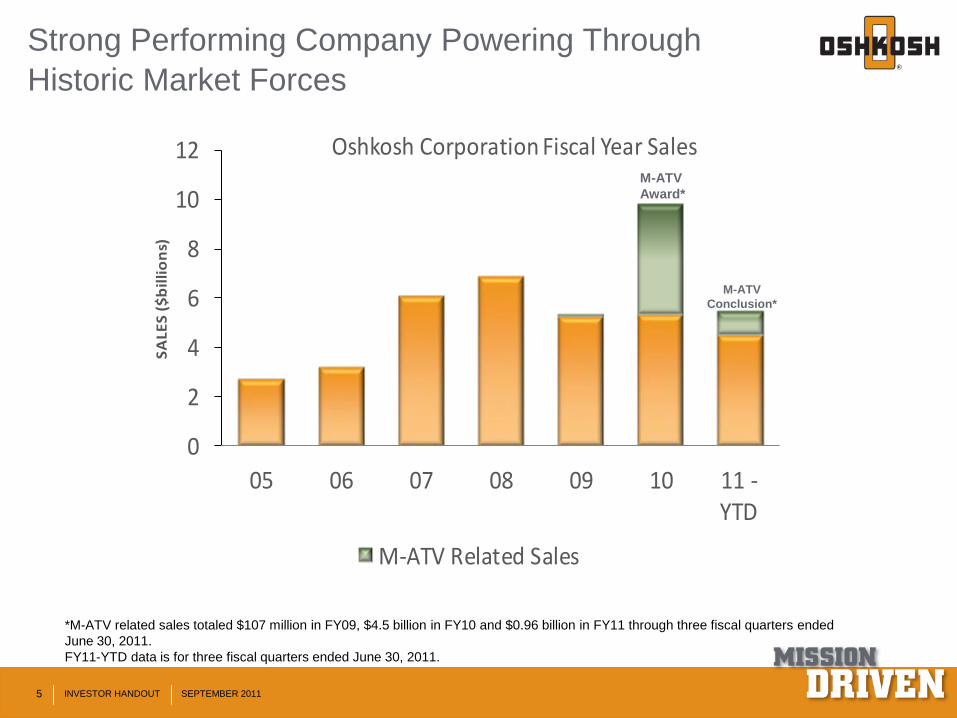

Strong Performing Company Powering Through

Historic Market Forces

5

0

2

4

6

8

10

12

05 06 07 08 09 10 11 -YTD

SA

LES

($

bil

lio

ns)

Oshkosh Corporation Fiscal Year Sales

M-ATV Related Sales

*M-ATV related sales totaled $107 million in FY09, $4.5 billion in FY10 and $0.96 billion in FY11 through three fiscal quarters ended

June 30, 2011.

FY11-YTD data is for three fiscal quarters ended June 30, 2011.

M-ATV

Award*

M-ATV

Conclusion*

INVESTOR HANDOUT SEPTEMBER 2011

Significant pressure on defense spending

Later cycle non-defense businesses

down 40-95%

– Municipal spending expected to decline further

in FY12 (fire apparatus and refuse collection)

– Concrete mixer demand expected to

remain weak

– Access equipment replacement demand

improving in near term; need construction

spending increase for longer term growth

Strong and improved balance sheet in

uncertain operating environment

– Expect modest use of cash in FY12

– Asset sales/dispositions don’t add

fair value at this time

Historic Market Forces Causing Transition Period…

With Significant Earnings Leverage in a Recovery

6

INVESTOR HANDOUT SEPTEMBER 2011

Implementing MOVE

Focusing on the most impactful

initiatives under current economic

conditions

– Reducing costs aggressively

– Seeking organic growth

– Focusing on optimizing cash flow

– Preserving balance sheet strength

Preparing for eventual market recovery

Improved cost structure

Expect significant earnings leverage

Executing Our Prudent Strategy

7

INVESTOR HANDOUT SEPTEMBER 2011

Mission Driven: To Move the World at Work

8

To From

A U.S. focused

manufacturer,

anchored in

Defense

A globally balanced

and integrated

industrial company

Consistent mission

“Oshkosh Corporation partners with customers to

deliver superior solutions that safely and

efficiently move people and materials at work

around the globe and around the clock.”

Primary Objectives

Execute a strong global

growth strategy to drive

superior shareholder value

in any market conditions

Optimize operations and

performance during transition

period

Leverage mission driven

culture to support and

enhance new strategic

direction

8

INVESTOR HANDOUT SEPTEMBER 2011 9

Capture full upside of economic recovery and market

growth with strong focus on execution and conquest sales

Continue to lead in innovation over the product life cycle

Drive international growth in targeted geographies

Optimize our cost and capital structure to provide value for

customers and shareholders

arket recovery

and growth

ptimize cost and

capital structure

alue

innovation

merging market

expansion

Mission Driven Culture

M

O

V

E

MOVE Strategy

INVESTOR HANDOUT SEPTEMBER 2011

- Market Recovery and Growth

Major non-defense markets have significant

upside potential

10

OS

K O

pe

ratin

g In

co

me

($ m

illio

ns)

0

100

200

300

400

500

600

Prior Peak * Most Recent TTM **

Attractive recovery opportunities in non-defense markets

Access F&E Commercial

* Prior Peak Operating Income: Access $363M – FY08, F&E $96M – FY07, Commercial $76M – FY07.

** Most Recent TTM data is for four fiscal quarters ended June 30, 2011: Access $38M, F&E $22M, Commercial $9M.

Approaching $500M

opportunity in recovery

M

INVESTOR HANDOUT SEPTEMBER 2011

- Optimize Cost and Capital Structure

Targeting cost reduction to drive mid

single digit margins at cycle bottom

– Dedicated teams focused on process

and product cost reduction

Facilities rationalization

– Manufacturing footprint reduced by ~20%

since FY07

– Evaluating further opportunities

Standardize and commonize with

Oshkosh Operating System (OOS)

– Drive improved inventory turns with OOS

Debt reduction remains top priority

11

* Q311 data represents total debt thru three fiscal quarters ended June 30, 2011.

O

INVESTOR HANDOUT SEPTEMBER 2011

- Value Innovation

Increased focus on delivering value-enhancing

solutions

– Expect significant near term Defense opportunities

Drive share gains and margin expansion

Proven history of industry-leading innovations

– TAK-4®- independent suspension - the platinum

standard

– Pierce Ultimate Configuration (PUC™)

• ~20% of fire truck orders

– Dash Cab Forward (CF)

• Expected to become 30% of fire truck sales

– CNG-powered vehicles

• Moving to 15-20% of RCV sales

– M-ATV

• The standard for high mobility IED protection

12

V

INVESTOR HANDOUT SEPTEMBER 2011

- Emerging Market Expansion

Targeting high growth regions for organic

growth, including BRICs

– Attractive markets with low product penetration rates

• Work-at-height equipment

• Fire & emergency apparatus

• Infrastructure expansion

International non-BRIC also strong potential

Global opportunities for

defense

– M-ATV variants

– Canadian TAPV & MSVS

– Medium and heavy trucks

– Remanufacturing/aftermarket

13

E

INVESTOR HANDOUT SEPTEMBER 2011

OSK: Investment Highlights

14

Top Tier Asset Base and Solid Reputation Market leading brands

Strong distribution network

Industry leading innovator

Experienced management team

Strong Balance Sheet and Improved Financial Profile ~$2 billion debt reduction since FY08

Facility rationalizations improving cost structure

Additional cost structure improvements identified

Significant Upside Potential with MOVE Market recovery (non-defense)

– Strong access equipment growth in near term

Optimize cost and capital structure

Value innovation

Emerging market expansion

INVESTOR HANDOUT SEPTEMBER 2011

For information contact:

Patrick Davidson

Vice President, Investor Relations

920 966-5939

Tina Schmiedel

Director, Investor Relations

920 233-9235

15

INVESTOR HANDOUT SEPTEMBER 2011

Appendix: Consolidated Results

Sales impacted by:

– Lower M-ATV related volume

+ FMTV volume

+ Traditional access equipment

business

Margins impacted by:

– Lower M-ATV revenues

– Higher FMTV volume and ramp-

up expenses

$25 million debt reduction

Net Sales $2,022.9 $2,439.0

% Change (17.1)% 100.8%

Operating Income $126.0 $340.5

% Change (63.0)% 764.7%

% Margin 6.2% 14.0%

Earnings Per Share $0.75 $2.31

% Change (67.5)% 925.0%

(Dollars in millions, except per share amounts)

Comments

2011 2010

Third Quarter

INVESTOR HANDOUT SEPTEMBER 2011

Appendix: Defense

Net Sales $1,107.0 $1,700.7

% Change (34.9)% 180.9%

Operating Income $112.5 $304.1

% Margin 10.2% 17.9%

Comments

2011 2010

Third Quarter (Dollars in millions)

■ Sales impacted by:

Significantly lower M-ATV

volume compared to

prior year

FMTV production ramp-up

■ Margins impacted by:

Adverse product mix

FMTV ramp-up costs

■ Backlog up 9% vs. prior

year to $4.86 billion

INVESTOR HANDOUT SEPTEMBER 2011

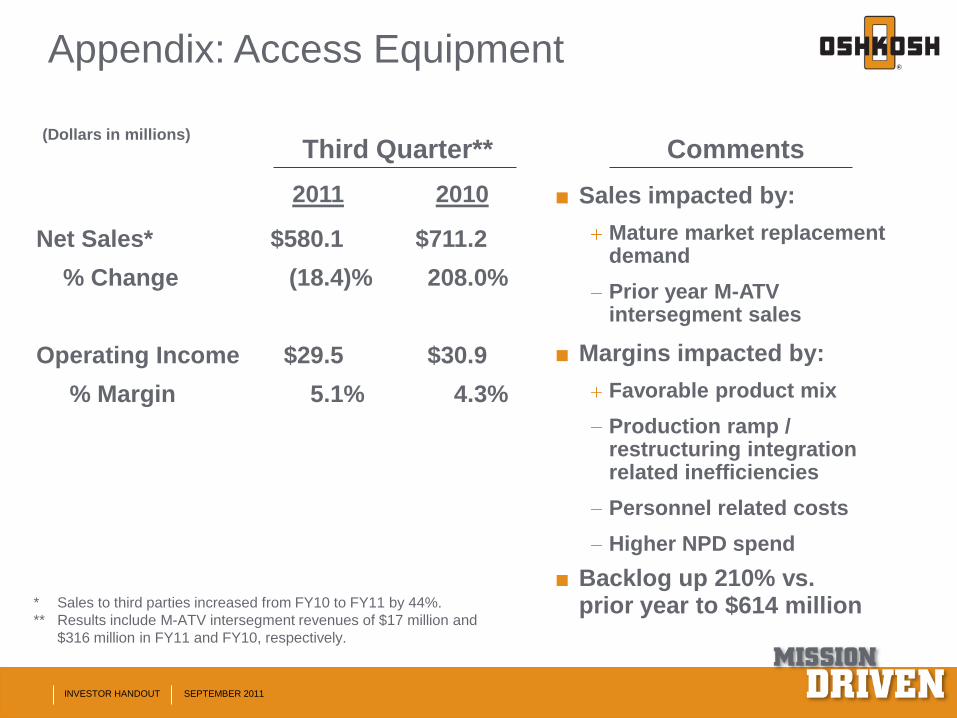

Appendix: Access Equipment

Net Sales* $580.1 $711.2

% Change (18.4)% 208.0%

Operating Income $29.5 $30.9

% Margin 5.1% 4.3%

Comments

■ Sales impacted by:

Mature market replacement demand

Prior year M-ATV intersegment sales

■ Margins impacted by:

Favorable product mix

Production ramp / restructuring integration related inefficiencies

Personnel related costs

Higher NPD spend

■ Backlog up 210% vs. prior year to $614 million

2011 2010

Third Quarter** (Dollars in millions)

* Sales to third parties increased from FY10 to FY11 by 44%.

** Results include M-ATV intersegment revenues of $17 million and

$316 million in FY11 and FY10, respectively.

INVESTOR HANDOUT SEPTEMBER 2011

Appendix: Fire & Emergency

Net Sales $216.0 $222.0

% Change (2.7)% (17.4)%

Operating Income $4.4 $18.3

% Margin 2.0% 8.2%

Comments

■ Sales impacted by:

Lower municipal

spending activity

Timing of airport products

deliveries

■ Margins impacted by:

Production inefficiencies

Restructuring-related costs

Adverse product mix

■ Backlog down 1% vs. prior

year to $458 million

2011 2010

Third Quarter

(Dollars in millions)

INVESTOR HANDOUT SEPTEMBER 2011

Appendix: Commercial

Net Sales $158.5 $158.3

% Change 0.1% 14.4%

Operating Income $3.7 $7.0

% Margin 2.4% 4.4%

Comments

2011 2010

Third Quarter

(Dollars in millions)

■ Sales impacted by:

Higher sales of mechanic

trucks and telescoping

cranes

Improved aftermarket

parts sales

– Lower RCV and

intersegment sales

■ Margins impacted by:

Higher production costs

not offset by pricing

■ Backlog up 55% vs. prior

year to $126 million

INVESTOR HANDOUT SEPTEMBER 2011

Appendix: Commonly Used Acronyms

ARFF Aircraft Rescue and Firefighting M-ATV MRAP All-Terrain Vehicle

AWP Aerial Work Platform MRAP Mine Resistant Ambush Protected

CNG Compressed Natural Gas MSVS Medium Support Vehicle System (Canada)

DoD Department of Defense MTT Medium Tactical Truck

EAME Europe, Africa & Middle East NPD New Product Development

EMD Engineering & Manufacturing Development OI Operating Income

FHTV Family of Heavy Tactical Vehicles PLS Palletized Load System

FMS Foreign Military Sales PUC Pierce Ultimate Configuration

FMTV Family of Medium Tactical Vehicles RCV Refuse Collection Vehicle

HEMTT Heavy Expanded Mobility Tactical Truck RFP Request for Proposal

HET Heavy Equipment Transporter ROW Rest of World

HEWATT HEMTT-Based Water Tender TACOM Tank-automotive and Armaments Command

HMMWV High Mobility Multi-Purpose Wheeled Vehicle TAPV Tactical Armor Protected Vehicle (Canada)

JLTV Joint Light Tactical Vehicle TFFT Tactical Fire Fighting Truck

JPO Joint Program Office TPV Tactical Protector Vehicle

JROC Joint Requirements Oversight Council TWV Tactical Wheeled Vehicle

JUONS Joint Urgent Operational Needs Statement UCA Undefinitized Contract Action

LVSR Logistic Vehicle System Replacement UIK Underbody Improvement Kit (for M-ATV)