Orient Paper Update 4-4-2013

3

CMP – Rs7.35 NSE Code: ORIENTPPR BSE Code: 502420 Equity Capital: Rs204.87mn Face Value: Re 1 Market Capitalization: Rs1.52-bn 2week Avg Trd. Volume (NSE & BSE) –1.03-mn shares 04 Apr 2013 Orient Paper & Industries Ltd (OPIL) recently got re-listed post demerger of Cement Busi- ness, which is set to be listed later in May-June’13. However, valuation of OPIL with the re- sidual business of Electrical Appliances along with paper has been marred by undue negativ- ism stems from the ailing paper unit at Amlai, MP. Based on limited financial information, estimated valuation of the Company leaves lot of up side p otential. Electrical Appliance Business: Expansion underway To achieve long term growth, the management has introduced new products like Lighting Products, Geysers etc. to its extant portfolio comprising mainly of Fans. The Fan Brand “Orient” is endorsed by top sport luminary MS Dhoni. Further, the management has plans to promote the new products to penetrate across breadth of the country. Owing to such promo- tional activities, the historical profitability (~ at par with Bajaj Electricals, V Guard etc in FY11 ) has taken a hit temporarily, is set to reverse in FY14-15e. Paper Business: Input bottleneck issues addressed, heading towards turnaround The paper unit has been incurring loss due to couple of operational issues like water avail- ability during summer and rising energy cost . The management has tried to address the input-side issues by implementing two key projects, 1) a water reservoir to ensure water availability during peak summer and 2) a 55MW Captive Power Unit to reduce operating cost. The plant is undergoing stabilization process, hence, appropriate cost saving is not yet visible. The Amlai unit is expected to be turning around in FY14-15e. Quoted investments protects downside The Company, belonging to KK Birla stable, has other investments, mainly in group company HIL (ex- Hyderabad Ind) and Century Textiles (a BK Birla stable firm), besides investments in liquid MFs. The value of all these holdings (all are at decent level, having low downside) is pegged at Rs1104mn after applying 30% discount to the ruling price. Market ignores the value of idle land at closed Unit-I paper mill at Brajarajnagar Orient Paper & Industries Ltd Deep discount to fundamentals The main attraction of the story remains the 865 acre prime l anded property at Brajarajnagar, (proximity to the local railway station) in the industry dominated Jharsuguda District of West- ern Odisha. The land is vacant since 1999, as the oldest industry of the State, set up in 1936 was closed do wn by the management due to operational ground. Brajarajnagar is a munici- pal town, having population of over 100,000 (2001 census: ~77,000) is quite close to Jhar- suguda town (~23km). Brajrajnagar has in its vicinity numerous open-cast and under-ground coal mines of Ib Valley Coalfield and Orient Colliery Are a belonging to govern ment owned Mahanadi Coalfields Limited, a subsidiary of Coal India Ltd. Prominent industry groups have operations nearby (Vedant Power, Bhushan Steel etc). The area is well connected through railway networks. The current ruling price of land at Brajarajnagar could be pegged at more than Rs10mn /acre. The landed value is expected to be monetized at appropriate time, de- pending on industrial expansion in the area. Given land aggregation is a tough issue in the present context, disposal of the land parcel to industrial groups/ realty developers could only happen, if at all, with significant premium. As promoters holding the land parcel since pre- independence era is in n o hurry to dispose the same Since, cash accrual could happen over longer time horizon, 50% discount to NAV is justified for valuation purpose. Recommendation First-cut estimation yields immense value primarily emanating from land value and electrical appliance business. The stre et has expressed too much pessimism over its ailing paper business. The Company has debt of ~Rs1.8-bn (post spin off), as per management sources (~47% of old debt), which can be brought down significantly, should the management li qui- date the quoted investments worth ~Rs1.6-bn. The s tock holds deep upside potential from the ruling level. However, the investment theme is apt for investors having high-risk appetite with long term investment perspective.

Transcript of Orient Paper Update 4-4-2013

7/28/2019 Orient Paper Update 4-4-2013

http://slidepdf.com/reader/full/orient-paper-update-4-4-2013 1/3

7/28/2019 Orient Paper Update 4-4-2013

http://slidepdf.com/reader/full/orient-paper-update-4-4-2013 2/3

2

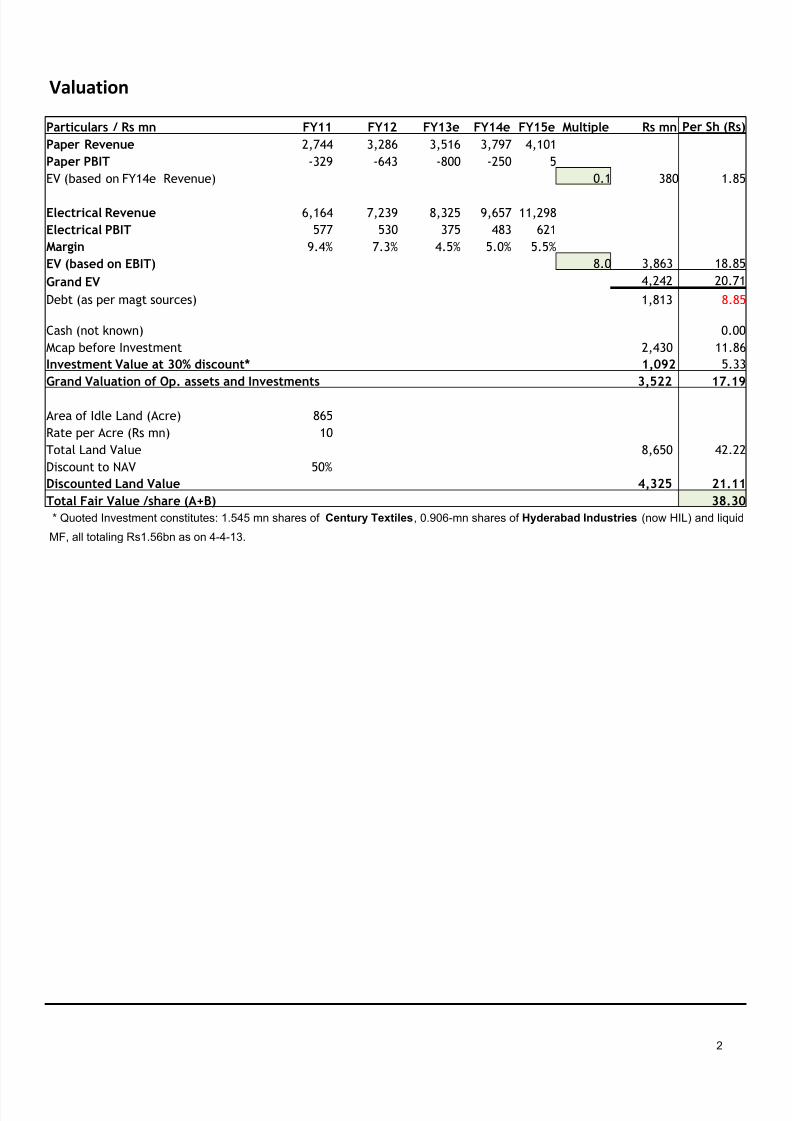

* Quoted Investment constitutes: 1.545 mn shares of Century Textiles, 0.906-mn shares of Hyderabad Industries (now HIL) and liquid

MF, all totaling Rs1.56bn as on 4-4-13.

Particulars / Rs mn FY11 FY12 FY13e FY14e FY15e Multiple Rs mn Per Sh (Rs)

Paper Revenue 2,744 3,286 3,516 3,797 4,101

Paper PBIT -329 -643 -800 -250 5

EV (based on FY14e Revenue) 0.1 380 1.85

Electrical Revenue 6,164 7,239 8,325 9,657 11,298

Electrical PBIT 577 530 375 483 621

Margin 9.4% 7.3% 4.5% 5.0% 5.5%

EV (based on EBIT) 8.0 3,863 18.85

Grand EV 4,242 20.71

Debt (as per magt sources) 1,813 8.85

Cash (not known) 0.00

Mcap before Investment 2,430 11.86

Investment Value at 30% discount* 1,092 5.33

Grand Valuation of Op. assets and Investments 3,522 17.19

Area of Idle Land (Acre) 865

Rate per Acre (Rs mn) 10

Total Land Value 8,650 42.22

Discount to NAV 50%

Discounted Land Value 4,325 21.11

Total Fair Value /share (A+B) 38.30

Valuation

7/28/2019 Orient Paper Update 4-4-2013

http://slidepdf.com/reader/full/orient-paper-update-4-4-2013 3/3

3

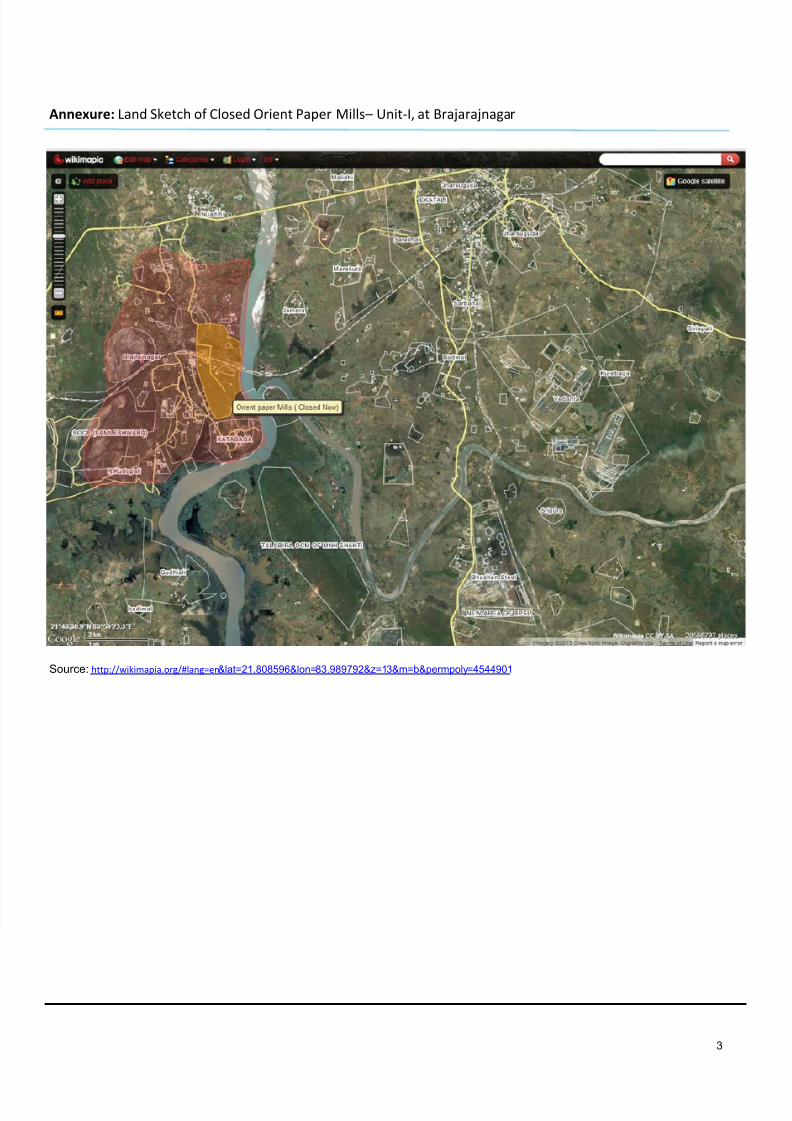

Annexure: Land Sketch of Closed Orient Paper Mills – Unit-I, at Brajarajnagar

Source: http://wikimapia.org/#lang=en&lat=21.808596&lon=83.989792&z=13&m=b&permpoly=4544901