Operations Management I For Confederation of Indian Industry (CII) R M Harindranath MBA MCA (Ph D)...

35

Operations Management I For Confederation of Indian Industry (CII) R M Harindranath MBA MCA (Ph D) MCT

-

Upload

hope-robinson -

Category

Documents

-

view

219 -

download

5

Transcript of Operations Management I For Confederation of Indian Industry (CII) R M Harindranath MBA MCA (Ph D)...

Operations Management I For Confederation of Indian Industry

(CII)

R M Harindranath MBA MCA (Ph D) MCT

Development Of OMScientific Management by Frederick Taylor• Major Landmark in Operations management • Scientific laws governs how much a worker can

produce per day• Taylor introduced formalized time-study and work-

study concepts.Moving Assembly Line by Henry Ford• Because of Assembly line the worker can reduce from

12.5 hours to 93 minutes• Moving Assembly line coupled with the concept of

scientific management gives labor specialization

Computers & MRP• 1970 – Application of Materials management

planning to product control• MRP program helps to manage to production

schedules & Inventory.JIT/TQC/AUTOMATION• JIT strives to eliminate sources of manufacturing

waste by producing the right part in the right place at the right time

• (TQC) which seeks to eliminate causes of production defects

• CIM,FMS & FOF

Development Of OM

Operations Management• Operations management (OM) involves all

activities involved in the production of goods and/or services.

• Inputs Transformation Outputs

Goal of Operations Activities

To produce the right product/service at the right time, in the right quantity, with the highest quality, at the lowest cost, and with the shortest delivery time.

Operating Decisions

System Design

Product and service designLong-range capacity

Process selection

Layout

Work system design

Location

Total quality management

System Operation

Quality managementQuality control

Short-term capacity (waiting line management)

Production planning

Inventory management

Scheduling

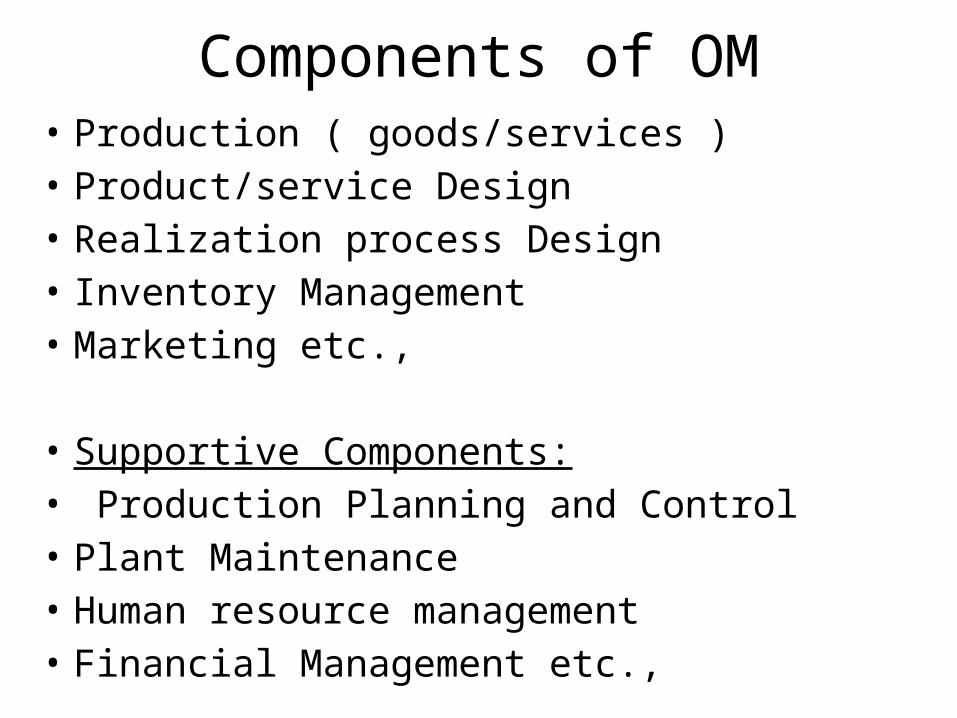

Components of OM• Production ( goods/services )• Product/service Design• Realization process Design• Inventory Management• Marketing etc.,

• Supportive Components:• Production Planning and Control• Plant Maintenance• Human resource management• Financial Management etc.,

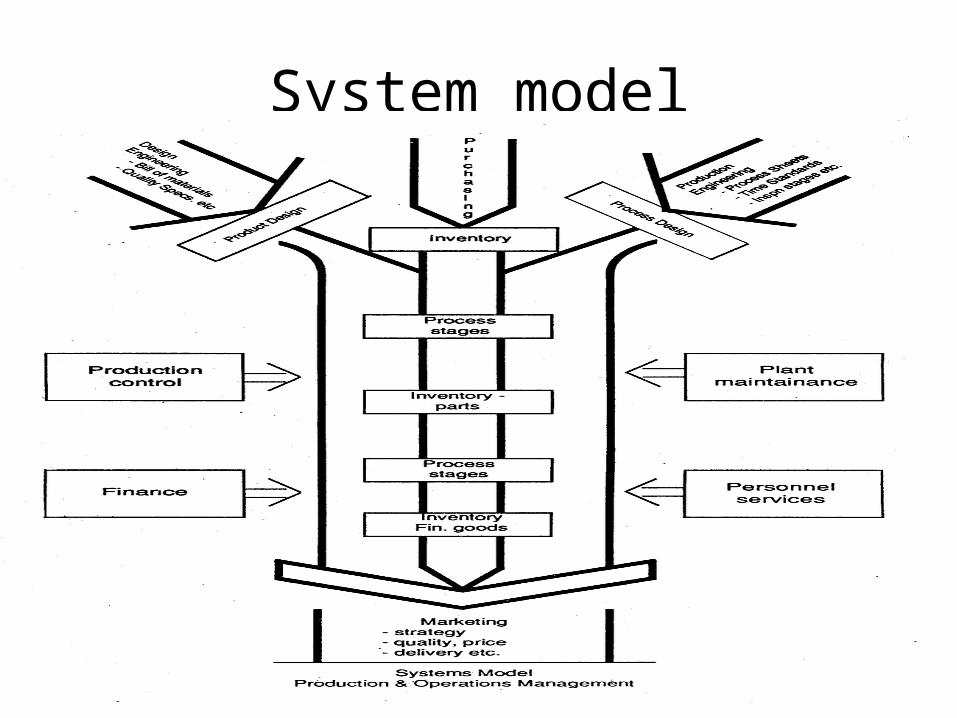

System model

Why study OM

• Production and Operations lie at the heart of business activity.

• They use human and material resources to create the products that either make an organization healthy and competitive

• The underlying theory of OM is common to both goods and services production.

• e.g., these are applicable to the management of hospital or airline operations as it is to the manufacture of automobiles.

• Operations are one of the most strategically vital areas of managerial concern

Chapter IIConcept of costing, Finance and Accountancy in OM• Cost Used for forecasting, planning and budgeting,

cost control, decision making and reporting• Cost can be direct or Indirect and Fixed or Variable• Direct costs belong to a product or service where

indirect don’t• Fixed costs cannot be during the accounting period• Variable cost directly relates to volume

CostingFull Costing• Allocates both fixed and variable costs to products

and allocates cost in various waysMarginal Costing• Allocate variable costs to products and so product

contribution (= revenue – variable costs) is the target

Activity-based CostingCost are allocated on the basis of activity & business

drivers

How much to cost• 1. Pricing decisions• 2. Formulating overall strategies• 3. Product and service-emphasis decisions

Product Costing Systems• Product Costing Systems accumulate, track and

assign the costs of production to the goods and services produced

• Three different costing systems: job costing, process costing, and operations costing

Job costing: • Assign cost for each job• Work well when individual products/services are

customized

• Process costing• Assigns costs to processes and then to products equally

by process• Works well when products are homogeneous and are

produced on a continuous basis

• Operations Costing• Hybrid of job & Process costing• Used by Cos that produce products in large batches• Each batch is treated like job costing, and each product is

treated like process costing. •

Product Costing Systems

Basic Job-order Costing for Manufacturing and Service Companies

• Measuring and tracking direct material• Usually an easy task • Determine how much material was used for each

job and then apply the correct cost.•

Spoilage

• Normal – results from the regular operation of the production process.

• Abnormal – results from improper handling, poorly trained craftspeople, and/or equipment that is in poor condition.

• Service companies usually have very little direct material.

Measuring and Tracking Direct Labor

• Usually an easy task • Measure the amount of hours used in the production

process for each job and apply the wage rate.• Fringe Benefits• Must be included in the wage rate• Usually run 30 to 35 percent of actual base wage rate • Overtime Premium• The cost of the overtime premium should be

included in manufacturing overhead.

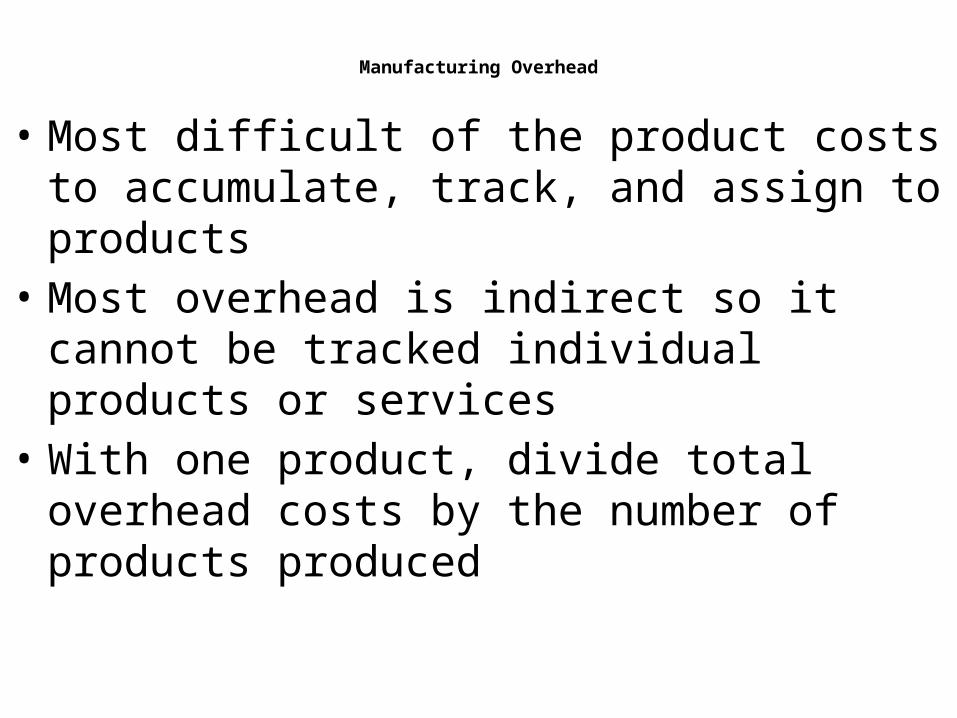

Manufacturing Overhead

• Most difficult of the product costs to accumulate, track, and assign to products

• Most overhead is indirect so it cannot be tracked individual products or services

• With one product, divide total overhead costs by the number of products produced

The Role of Cost Pools and Cost Drivers

• 1. Cost drivers are activities that cause overhead costs to be incurred.

Examples are direct labor hours and machine hours.• 2. Cost pools are used to accumulate similar costs as

they are incurred.• 3. Finally, cost drivers are used to allocate the cost pools

to products. • Departmental Overhead Rates• Useful as products become more diverse and plants

become more heavily automated• Each department has a separate cost pool

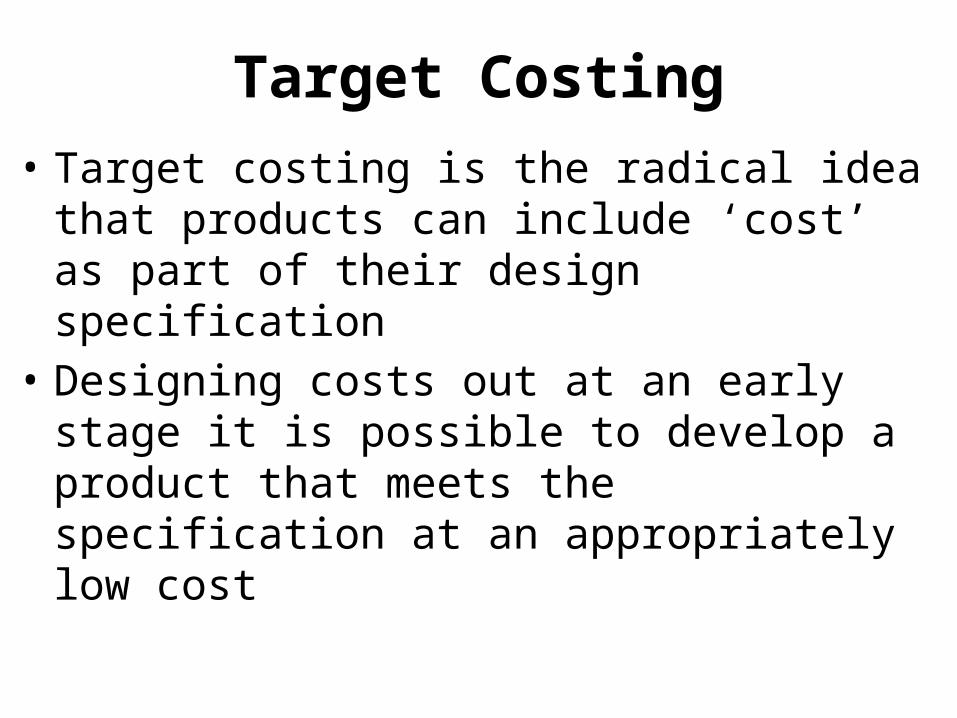

Target Costing• Target costing is the radical idea that products can

include ‘cost’ as part of their design specification• Designing costs out at an early stage it is possible

to develop a product that meets the specification at an appropriately low cost

Financial Concepts

• Financial management deals with the management of finances of a business enterprise,

• Investments deals with financial markets and security pricing

• Financial institutions deals with financial firms (such as banks).

• Managers who work in all three areas rely on the same basic knowledge of finance

Finance

• Finance is based on economic principles. • Finance uses accounting information as input to

decision-making. • Finance is international in perspective. • Finance is constantly changing. • Finance is the study of how to invest and raise

money productively.

Financial Analysis

• Financial Analysis is a tool that involves evaluating the financial condition and operating performance of a business enterprise. Financial analysis requires an evaluation of the firm, the firm's industry, and the economy.

• Financial analysis may be used to determine the credit-worthiness

Types of Accounts1.Financial accounts – also called as statutory

Accounts• Follow set of rules & conventions• What went during the financial year• Mainly used by the people outside the business2.Management Accounts• Not strictly required by law• Often predict the future as well as the past

Chapter III Job Design

Job Design• Identifies the content of the job, where is to be

performed & competencies required by the personThree basic school of thought: 1. Socio-technical Approach designed by Eric Trist et al

Social ConstraintsTechnological Constraints

Set of all

feasible social job designs

Set of feasible solutions for a joint optimum

Set of all feasible technical job designs

Advantages & Disadvantages Socio-technical Approach

S. No. For Management For Labor

1. Simplifies training Low education and skill requirements

2. High productivity Minimum responsibilities

3. Low wage costs Little mental efforts needed

S. No. For Management For Labor

1. Difficult to motivate quality work Monotonous work

2. Worker dissatisfaction, possibly resulting in absenteeism, high turnover and disruptive tactics

Limited opportunities for advancement

3. Little control over work Little opportunity for self-fulfillment

Disadvantages

Behavioral Approaches to Job Design

• Job enlargement = giving a worker a larger portion of the total task, by horizontal loading

• Job rotation = workers periodically exchange jobs• Job enrichment = increasing responsibility for

planning and coordination tasks, by vertical loading

Benefits of sound job designBenefits to Organization Benefits for staff members

- Highly skilled workforce

- Flexible and responsive workforce

- Increased productivity and efficiency

- Improved quality delivery

- A reduction in Occupational, Health & Safety(OHS) problems

- Reduction of unnecessary levels of supervision, checking and control

- Greater organizational effectiveness

- Increased customer service standards

- Improved efficiency by reducing costs associated with waste/delays/ accidents

- Positions are appropriately developed/ described

- Better work focus

Increased job satisfaction

Increased skills and training

More opportunity to participate in decision-making and planning

A safer workplace

More career opportunities

Improved quality of working life

Greater clarity of work role and purpose

Shared understanding of work expectation between staff member and supervisor

Key Characteristics of a well designed job

Factors in a job to make it meaningful & satisfying• Variety• Personal responsibility for the position• Autonomy to the level possible• Task Identity• Constructive feedback• Participation in decision-making• Provision of recognition and support• A conducive working environment

Who designed the job• Nominated supervisor of the position is

responsible for designing the job• Staff in the functional/ organizational unit may

also play an important part in assisting with this process

• For redesigning, the affected employees need to be consulted

• Both the incumbent & supervisor should be provided to contribute to the design

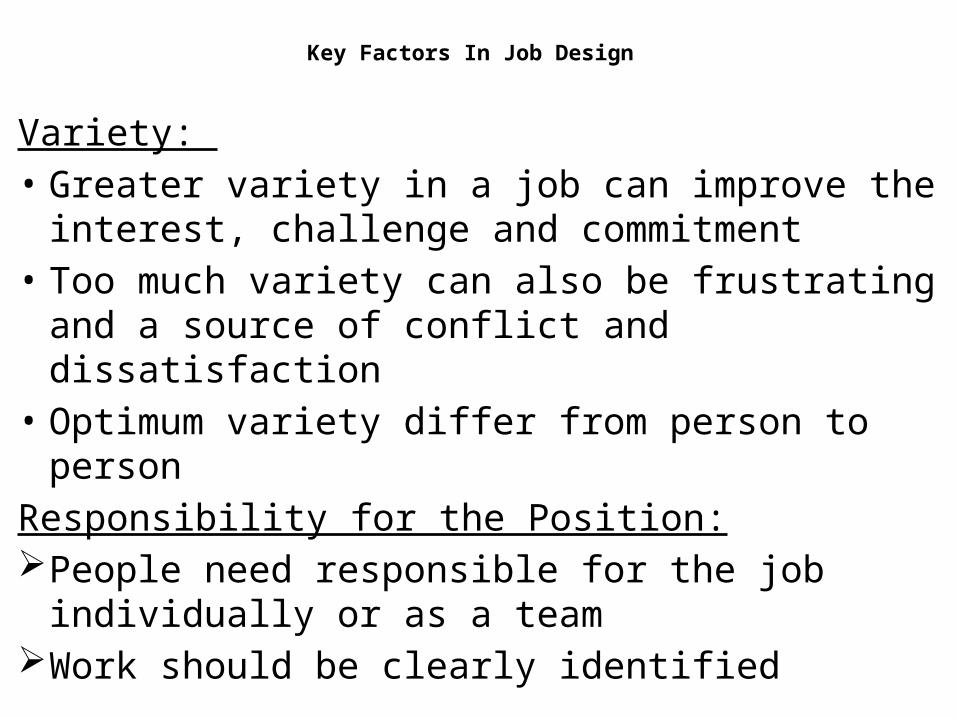

Key Factors In Job Design

Variety: • Greater variety in a job can improve the interest,

challenge and commitment• Too much variety can also be frustrating and a

source of conflict and dissatisfaction• Optimum variety differ from person to personResponsibility for the Position:People need responsible for the job individually or

as a teamWork should be clearly identified

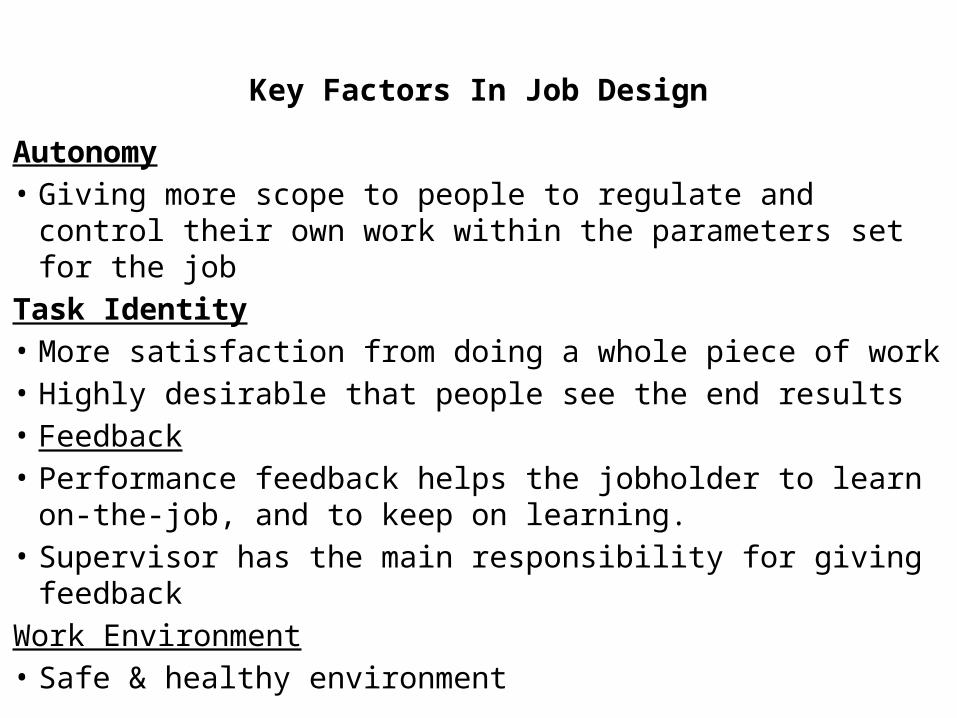

Autonomy• Giving more scope to people to regulate and control their

own work within the parameters set for the jobTask Identity• More satisfaction from doing a whole piece of work• Highly desirable that people see the end results• Feedback• Performance feedback helps the jobholder to learn on-the-

job, and to keep on learning.• Supervisor has the main responsibility for giving feedbackWork Environment• Safe & healthy environment

Key Factors In Job Design

Ergonomics is the science of fitting jobs to people

Ergonomic design is the application of this body of knowledge to the design of the workplace

Good ergonomic design makes the most efficient use of worker capabilities

Ergonomics

Thank you