Operations and Technical Update -...

219

OPERATIONS AND TECHNICAL UPDATE Wednesday, February 22, 2017

Transcript of Operations and Technical Update -...

OPERATIONS AND TECHNICAL UPDATEWednesday, February 22, 2017

Certain information contained or incorporated by reference in this presentation, including any information as to our strategy, projects, plans, or future financial or operating performance, constitutes "forward-looking statements". All statements, other than statements of historical fact, are forward-looking statements. The words "believe", "expect", "anticipate", "contemplate", "target", "plan", "objective" "aspiration", "aim", "intend", "project", "goal", "continue", "budget", "estimate", "potential", "may", "will", "can", "should", "could", "would", and similar expressions identify forward-looking statements. In particular, this presentation contains forward-looking statements including, without limitation, with respect to: (i) Barrick's forward-looking production guidance; (ii) estimates of future cost of sales per ounce for gold and per pound for copper, all-in-sustaining costs per ounce/pound, cash costs per ounce, and C1 cash costs per pound; (iii) cash flow forecasts; (iv) projected capital, operating, and exploration expenditures; (v) targeted debt and cost reductions; (vi) mine life and production rates; (vii) potential mineralization and metal or mineral recoveries; (viii) Barrick's Best-in-Class program (including potential improvements to financial and operating performance that may result from certain Best-in-Class initiatives); (ix) potential improvements to financial and operating performance and mine life at Barrick’s Cortez, Goldstrike, Pueblo Viejo, Veladero, Lagunas Norte, Turquoise Ridge and Hemlo mines; (x) potential developments at Barrick’s Goldrush, Alturas and Pascua Lama projects, including the Lama starter project and the potential for phased-in development of the Pascua-Lama project; (xi) the potential to identify new reserves and resources; (xii) our pipeline of high confidence projects at or near existing operations; (xiii) the benefits of integrating the Cortez and Goldstrike operations; (xiv) the potential impact and benefits of Barrick's digital transformation; (xv) asset sales, joint ventures, and partnerships; (xvi) expectations regarding future price assumptions, financial performance, and other outlook or guidance; and (xvii) the estimated timing and conclusions of technical reports and other studies.

Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company as at the date of this press release in light of management's experience and perception of current conditions and expected developments, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements, and undue reliance should not be placed on such statements and information. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold, copper, or certain other commodities (such as silver, diesel fuel, natural gas, and electricity); the speculative nature of mineral exploration and development; changes in mineral production performance, exploitation, and exploration successes; risks associated with the fact that certain Best-in-Class and other initiatives are still in the early stages of evaluation, and additional engineering and other analysis is required to fully assess their impact; risks associated with the implementation of Barrick's digital transformation initiative, and the ability of the projects under this initiative to meet the Company's capital allocation objectives; diminishing quantities or grades of reserves; increased costs, delays, suspensions, and technical challenges associated with the construction of capital projects; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges, and disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with environmental and health and safety laws and regulations; timing of receipt of, or failure to comply with, necessary permits and approvals; uncertainty whether some or all of the Best-in-Class initiatives and targeted investments and projects will meet the Company's capital allocation objectives; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; adverse changes in our credit ratings; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations, and/or changes in the administration of laws, policies, and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States , and other jurisdictions in which the Company does or may carry on business in the future; damage to the Company’s reputation due to the actual or perceived occurrence of any number of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings with community groups, whether true or not; the possibility that future exploration results will not be consistent with the Company’s expectations; risks that exploration data may be incomplete and considerable additional work may be required to complete further evaluation, including but not limited to drilling, engineering and socio-economic studies and investment; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation; contests over title to properties, particularly title to undeveloped properties, or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; risks associated with working with partners in jointly controlled assets; our ability to successfully integrate acquisitions or complete divestitures; employee relations; increased costs and risks related to the potential impact of climate change; and availability and increased costs associated with mining inputs and labor. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks).

Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this presentation are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a more detailed discussion of some of the factors underlying forward- looking statements and the risks that may affect Barrick's ability to achieve the expectations set forth in the forward-looking statements contained in this presentation.

The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

GLOSSARY OF KEY ACRONYMS

AC Autoclave LOM Life of Mine

AISC All-in Sustaining Costs M&I Measured and Indicated

ANFO Ammonium Nitrate, Fuel Oil MTBF Mean Time Between Failure

ARS Argentine Peso MTO Mine Traffic Optimization

Au Gold NEPA The National Environmental Policy Act

BCRA Banco Central de Republica Argentina NPV Net Present Value

BiC Best-in-Class NZ North Zone

CAGR Compound Annual Growth Rate OEE Overall Equipment Efficiency

CCTV Closed-circuit Television OP Open Pit

CDP Carbon Disclosure Project OPEX Operational Expenditure

CiC Carbon-in-Column PFS Pre-feasibility Study

CIL Carbon In Leach PMR Proyecto Mineral Refractario

CIP Carbon In Pulp POX Pressure Oxidation

CSR Corporate Social Responsibility PV Pueblo Viejo

DJSI Dow Jones Sustainability Indices QQ1 Quisqueya 1

DR The Dominican Republic ROD Record of Decision

Cu Copper ROIC Return on Invested Capital

DSO Direct Shipping Ore SAG Semi-Autogenous Grinding

EBITDA Earnings Before Interest, Tax, Depreciation and Amortization SIC Short Interval Control

EIA Environmental Impact Assessment SME Society for Mining, Metallurgy, and Exploration

EIS Environmental Impact Statement SZ South Zone

FCF Free Cash Flow TCM Total Carbonaceous Matter

FDI Foreign Direct Investment TPA Tonne Per Annum

FS Feasibility Study TPD Tonne Per Day

FT Feet TPOH Tonne Per Operating Hour

FWP Footwall Pond TR Turquoise Ridge

FX Forex TRIFR Total Recordable Injury Frequency Rate

GHG Greenhouse Gas TRJV Turquoise Ridge Joint Venture

GM General Manager TSR Total Shareholder Return

G/T Grams Per Tonne UAV Unmanned Aerial Vehicle

HCCUEP Horse Canyon/Cortez Unified Exploration Plan UG Underground

HFO Heavy Fuel Oil VRS Value Realization Support

KCGM Kalgoorlie Consolidated Gold Mines WTPOH Wet Ton Per Operating Hour

KPI Key Performance Indicator YE Year-End

LHD Load, Haul, Dump Machine YOY Year Over Year

LNG Liquefied Natural Gas

Operations and Technical Update | 1

OperationsandTechnicalUpdate

RichardWilliamsChiefOperatingOfficer

Operations and Technical Update | 2

Operations&TechnicalUpdateAgenda

Operations,Exploration,InnovationandOptionality2:00– 2:45

Welcome & Opening Remarks Richard Williams

Value Creation through Exploration Rob Krcmarov

Digital Transformation & Innovation Michelle Ash

Long Term Portfolio Optionality Matt Gili

OperatingMineandGrowthProjectUpdates2:45– 4:00

Nevada Overview, Goldstrike: TCM, Future Growth Bill MacNevin

Cortez: Digitization, Deep South, Goldrush Curtis Cadwell

Turquoise Ridge: TR Shaft/UG Expansion Henri Gonin

Pueblo Viejo: Best-in-Class, Tailing Expansion Greg Walker

Veladero: Digitization, Environmental Monitoring Jorge Palmes

Lagunas Norte: Refractory Mine Life Extension Jim Whittaker

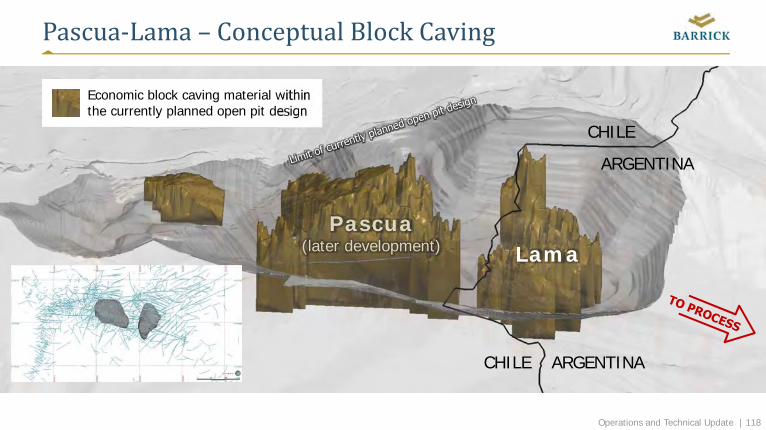

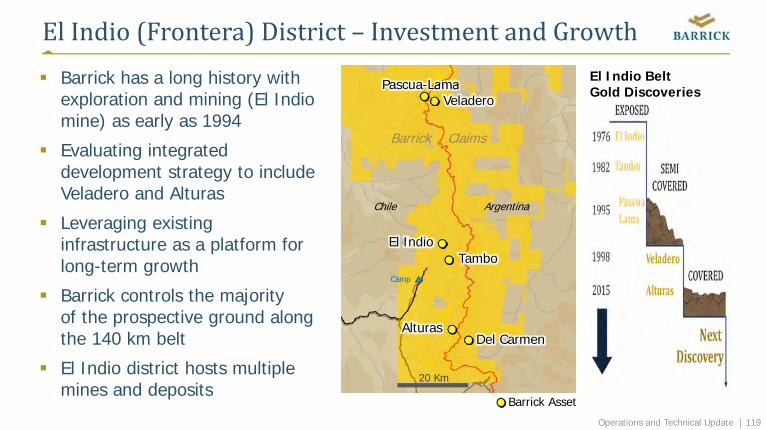

Lama & Frontera District Development George Bee

Reserves and Resources Rick Sims

SustainabilityandClosing4:00– 5:00

Sustainability Peter Sinclair

Closing Remarks and Q&A Kelvin Dushnisky

February 22nd 2017, 2:00pm – 5:00pm | Cisco Technology Innovation Center, Toronto, ON

Operations and Technical Update | 3

OurVision

OurVisionisthegenerationofwealththroughresponsiblemining–wealthforourowners,ourpeople,andthecountriesandcommunitieswithwhichwepartner.Weaimtobetheleadingminingcompanyfocusedongold,growingourcashflowpersharebydevelopingandoperatinghighqualityassetsthroughdisciplinedallocationofhumanandfinancialcapitalandoperationalexcellence.

Operations and Technical Update | 4

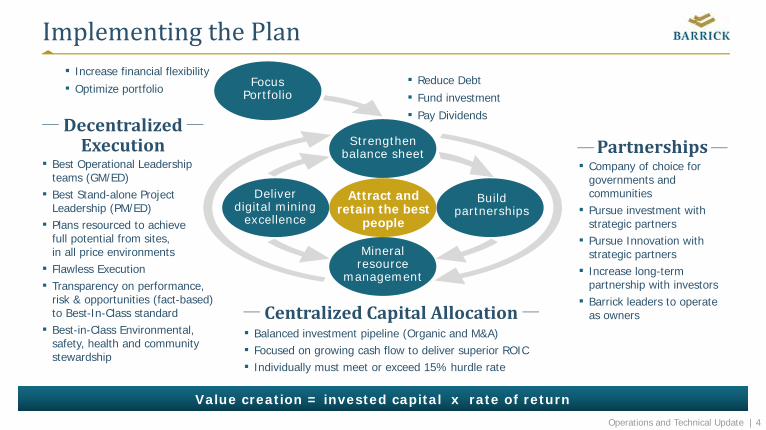

ImplementingthePlan

▪ Company of choice for governments and communities

▪ Pursue investment with strategic partners

▪ Pursue Innovation with strategic partners

▪ Increase long-term partnership with investors

▪ Barrick leaders to operate as owners

▪ Best Operational Leadership teams (GM/ED)

▪ Best Stand-alone Project Leadership (PM/ED)

▪ Plans resourced to achieve full potential from sites, in all price environments

▪ Flawless Execution▪ Transparency on performance,

risk & opportunities (fact-based) to Best-In-Class standard

▪ Best-in-Class Environmental, safety, health and community stewardship

▪ Increase financial flexibility▪ Optimize portfolio

▪ Reduce Debt ▪ Fund investment▪ Pay Dividends

Value creation = invested capital x rate of return

▪ Balanced investment pipeline (Organic and M&A)▪ Focused on growing cash flow to deliver superior ROIC ▪ Individually must meet or exceed 15% hurdle rate

CentralizedCapitalAllocation

PartnershipsDecentralizedExecution

Deliverdigital mining

excellence

Attract andretain the best

people

Buildpartnerships

Mineralresource

management

Strengthenbalance sheet

FocusPortfolio

Operations and Technical Update | 5

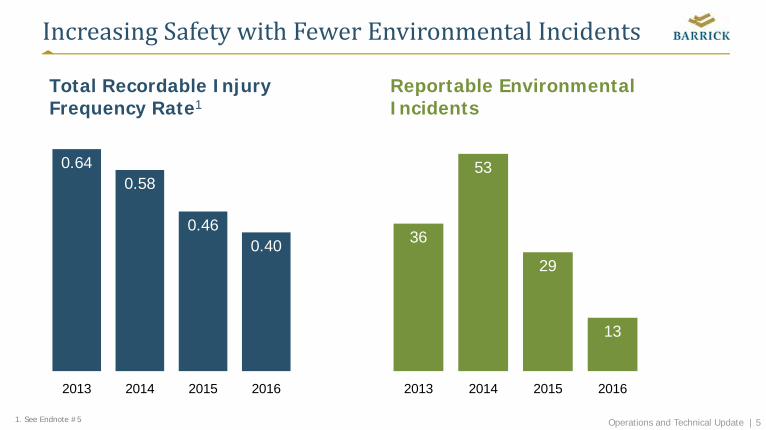

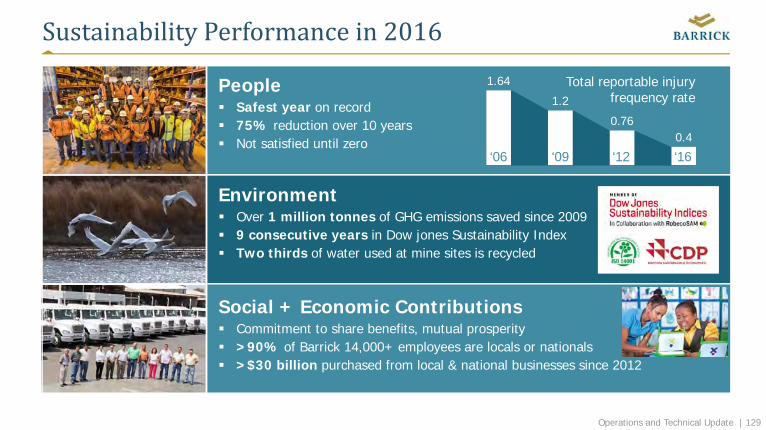

IncreasingSafetywithFewerEnvironmentalIncidents

36

53

29

13

2013 2014 2015 2016

Reportable Environmental Incidents

0.640.58

0.460.40

2013 2014 2015 2016

Total Recordable Injury Frequency Rate1

1. See Endnote #5

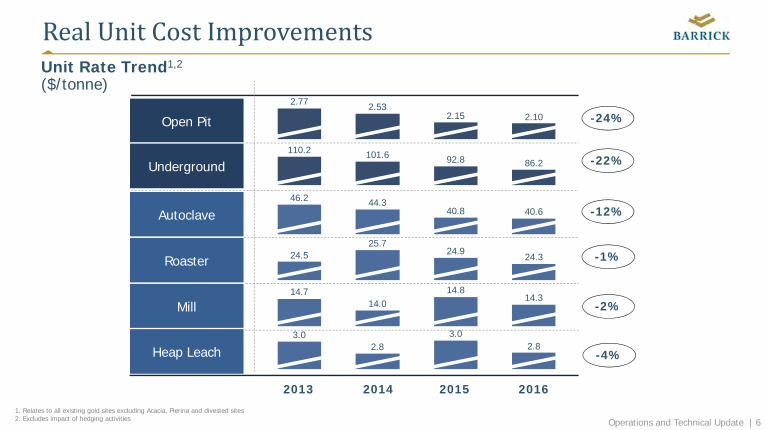

Operations and Technical Update | 61. Relates to all existing gold sites excluding Acacia, Pierina and divested sites2. Excludes impact of hedging activities

Unit Rate Trend1,2

($/tonne)

RealUnitCostImprovements

-24%

-22%

-12%

-1%

-2%

-4%

2.772.15 2.10

2.53

86.2101.6110.2

92.8

40.640.844.346.2

25.724.924.5 24.3

14.314.814.7

14.0

3.02.8

3.02.8

Open Pit

Underground

Autoclave

Roaster

Mill

Heap Leach

2014 2015 20162013

Operations and Technical Update | 7

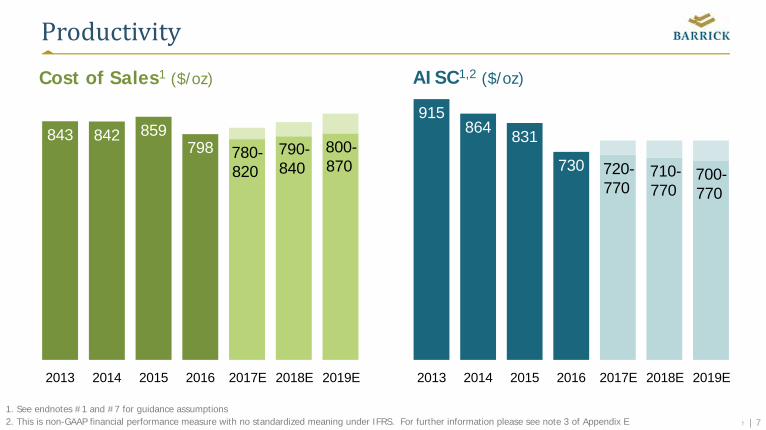

Productivity

843 842 859798

2013 2014 2015 2016 2017E 2018E 2019E

Cost of Sales1 ($/oz)

915864 831

730

2013 2014 2015 2016 2017E 2018E 2019E

AISC1,2 ($/oz)

720-770

710-770

700-770

780-820

790-840

800-870

1. See endnotes #1 and #7 for guidance assumptions2. This is non-GAAP financial performance measure with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations and Technical Update | 8

ValueCreationThroughExploration

RobKrcmarovExecutiveVicePresidentExplorationandGrowth

Operations and Technical Update | 9

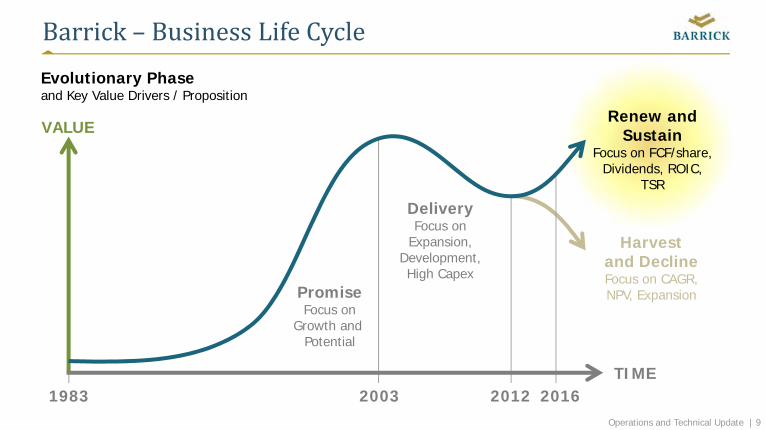

Barrick– BusinessLifeCycle

Renew and Sustain

Focus on FCF/share, Dividends, ROIC,

TSR

Harvest and DeclineFocus on CAGR, NPV, Expansion

DeliveryFocus on

Expansion, Development, High Capex

PromiseFocus on

Growth and Potential

VALUE

TIME1983 20162003 2012

Evolutionary Phase and Key Value Drivers / Proposition

Operations and Technical Update | 10

Barrick– ExplorationStrategy

Superior portfolio of long life production assets

Deep project pipeline– Some of the largest undeveloped

projects on the planet

A track record of generating organic value from exploration

Partnerships

Exploration Drilling in Nevada

Operations and Technical Update | 11

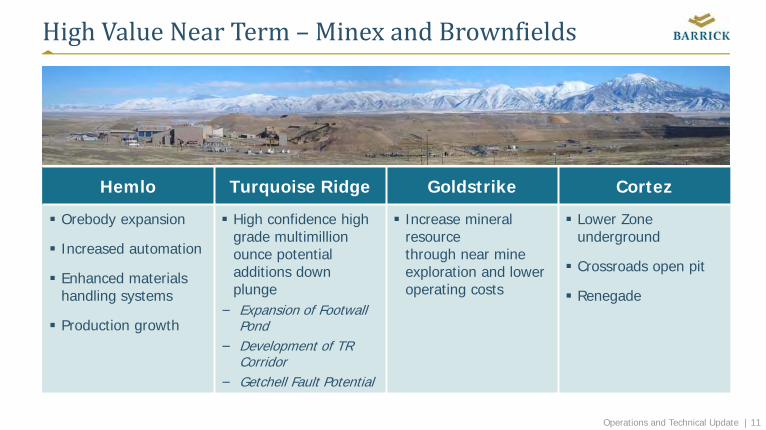

HighValueNearTerm– MinexandBrownfields

Hemlo Turquoise Ridge Goldstrike Cortez

Orebody expansion

Increased automation

Enhanced materials handling systems

Production growth

High confidence high grade multimillion ounce potential additions down plunge

− Expansion of Footwall Pond

− Development of TR Corridor

− Getchell Fault Potential

Increase mineral resource through near mine exploration and lower operating costs

Lower Zone underground

Crossroads open pit

Renegade

Operations and Technical Update | 12

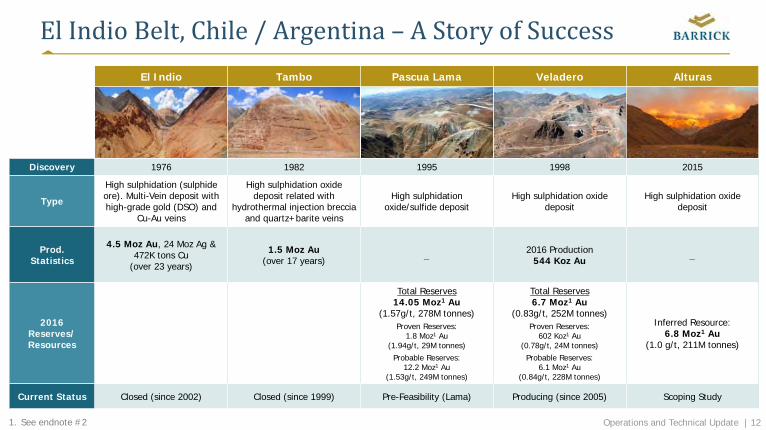

ElIndioBelt,Chile/Argentina– AStoryofSuccessEl Indio Tambo Pascua Lama Veladero Alturas

Discovery 1976 1982 1995 1998 2015

Type

High sulphidation (sulphide ore). Multi-Vein deposit with high-grade gold (DSO) and

Cu-Au veins

High sulphidation oxidedeposit related with

hydrothermal injection breccia and quartz+barite veins

High sulphidationoxide/sulfide deposit

High sulphidation oxide deposit

High sulphidation oxide deposit

Prod.Statistics

4.5 Moz Au, 24 Moz Ag & 472K tons Cu

(over 23 years)

1.5 Moz Au(over 17 years) _ 2016 Production

544 Koz Au _

2016 Reserves/Resources

Total Reserves14.05 Moz1 Au

(1.57g/t, 278M tonnes)Proven Reserves:

1.8 Moz1 Au (1.94g/t, 29M tonnes)

Probable Reserves:12.2 Moz1 Au

(1.53g/t, 249M tonnes)

Total Reserves6.7 Moz1 Au

(0.83g/t, 252M tonnes)Proven Reserves:

602 Koz1 Au (0.78g/t, 24M tonnes)

Probable Reserves:6.1 Moz1 Au

(0.84g/t, 228M tonnes)

Inferred Resource:6.8 Moz1 Au

(1.0 g/t, 211M tonnes)

Current Status Closed (since 2002) Closed (since 1999) Pre-Feasibility (Lama) Producing (since 2005) Scoping Study

1. See endnote #2

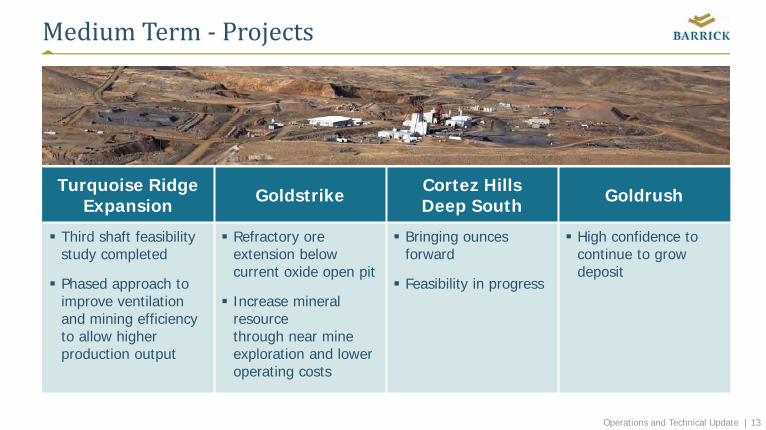

Operations and Technical Update | 13

MediumTerm‐ Projects

Turquoise Ridge Expansion Goldstrike Cortez Hills

Deep South Goldrush

Third shaft feasibility study completed

Phased approach to improve ventilation and mining efficiency to allow higher production output

Refractory ore extension below current oxide open pit

Increase mineral resource through near mine exploration and lower operating costs

Bringing ounces forward

Feasibility in progress

High confidence to continue to grow deposit

Operations and Technical Update | 14

Alturas

Goldrush

Pueblo Viejo

Veladero

Donlin Gold

Cortez

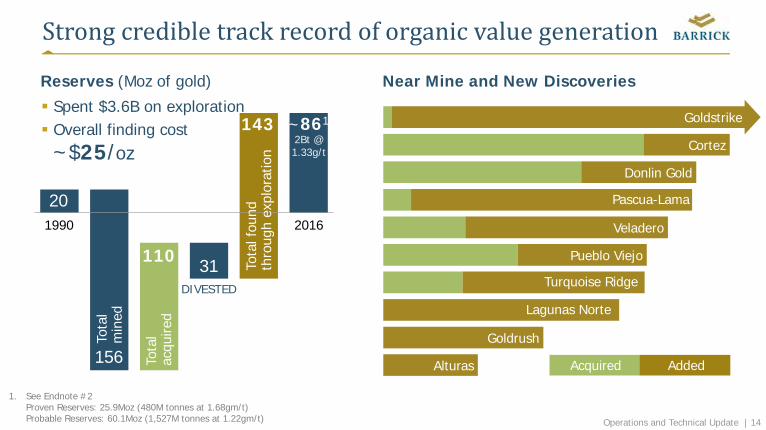

Strongcredibletrackrecordoforganicvaluegeneration

Spent $3.6B on exploration Overall finding cost ~$25/oz

1990

DIVESTED

Tota

lac

quire

d

Tota

lm

ined

1. See Endnote #2Proven Reserves: 25.9Moz (480M tonnes at 1.68gm/t)Probable Reserves: 60.1Moz (1,527M tonnes at 1.22gm/t)

Reserves (Moz of gold) Near Mine and New Discoveries

110

156

20

31

143

Tota

l fou

ndth

roug

h ex

plor

atio

n

~861

2Bt @1.33g/t

Turquoise Ridge

Acquired Added

Lagunas Norte

Goldstrike

2016

Pascua-Lama

Operations and Technical Update | 15

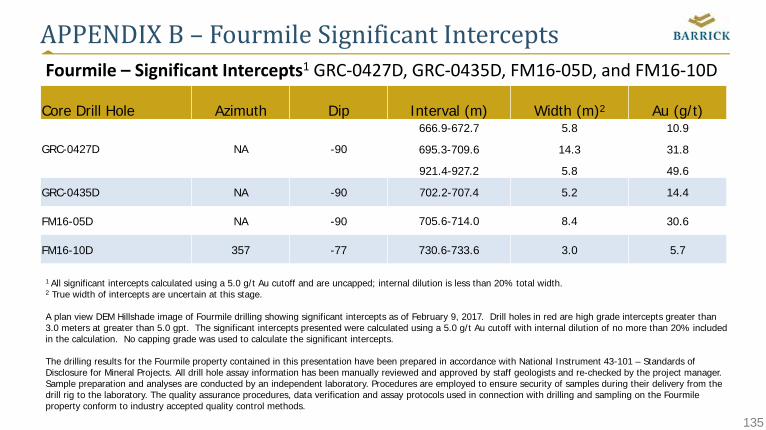

Fourmile

High grade, high value targets with small footprint

Three holes with intercepts more than double the average grade of the Goldrush resource1

– 14.3m @ 31.8 g/t– 5.8m @ 49.6 g/t– 8.4m @ 30.6 g/t

Strike length of high grade Fourmile mineralization extended 500m in 2016

1. See end note #2 and #4 and Appendix B for additional details including assay results for the significant intercepts.

Mill Canyon StockPre-mineral Intrusive Rock

5.2m @ 14.4 g/t

3.0m @ 5.7 g/t

5.8m @ 10.9 g/t 14.3m @ 31.8 g/t 5.8m @ 49.6 g/t

8.4m @ 30.6 g/t

LegendDrillhole with >3m @ 5g/tDrillholeResource Footprint

Operations and Technical Update | 16

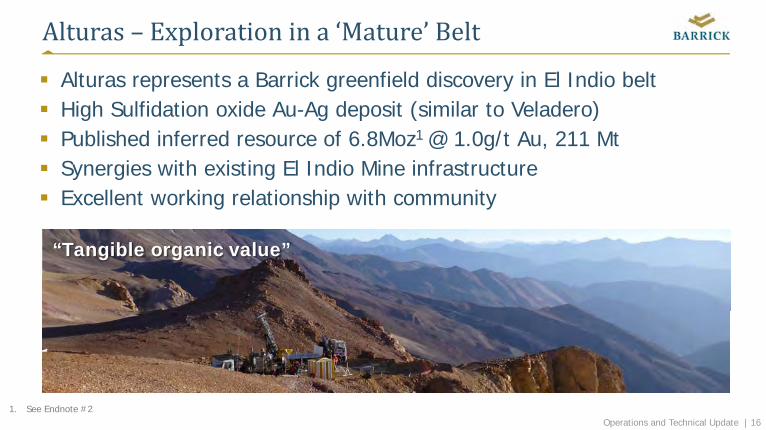

Alturas– Explorationina‘Mature’Belt

Alturas represents a Barrick greenfield discovery in El Indio belt High Sulfidation oxide Au-Ag deposit (similar to Veladero) Published inferred resource of 6.8Moz1 @ 1.0g/t Au, 211 Mt Synergies with existing El Indio Mine infrastructure Excellent working relationship with community

“Tangible organic value”

1. See Endnote #2

Operations and Technical Update | 17

2km

�Drill Fences-plannedDrill Fences-completedPre-2016 DrillingShallow pits

Mafic DykesDioriteMetasedimentsVolcanics

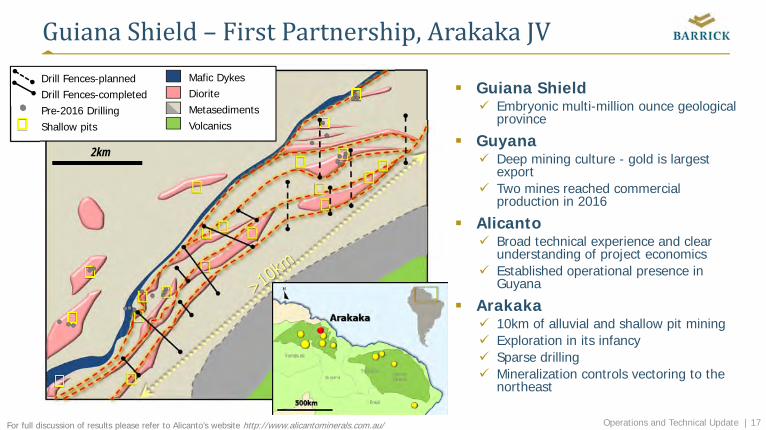

GuianaShield– FirstPartnership,Arakaka JV

Guiana Shield Embryonic multi-million ounce geological

province

Guyana Deep mining culture - gold is largest

export Two mines reached commercial

production in 2016

Alicanto Broad technical experience and clear

understanding of project economics Established operational presence in

Guyana

Arakaka 10km of alluvial and shallow pit mining Exploration in its infancy Sparse drilling Mineralization controls vectoring to the

northeast

For full discussion of results please refer to Alicanto’s website http://www.alicantominerals.com.au/

Operations and Technical Update | 18

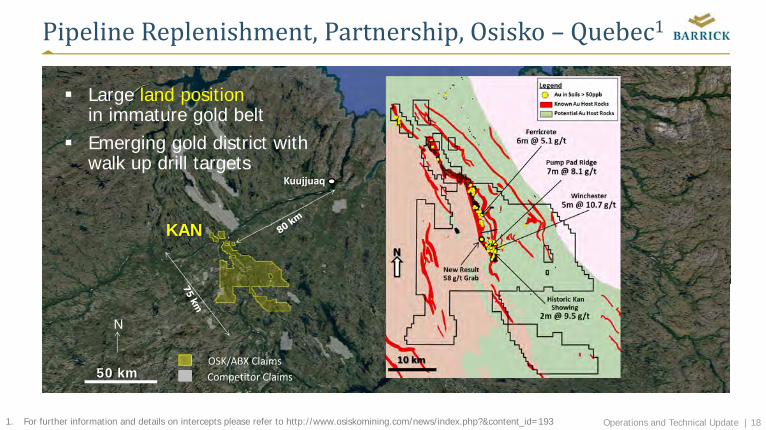

PipelineReplenishment,Partnership,Osisko – Quebec1

KAN

N

Kuujjuaq

50 km Competitor ClaimsOSK/ABX Claims

1. For further information and details on intercepts please refer to http://www.osiskomining.com/news/index.php?&content_id=193

Large land positionin immature gold belt

Emerging gold district with walk up drill targets

Operations and Technical Update | 19

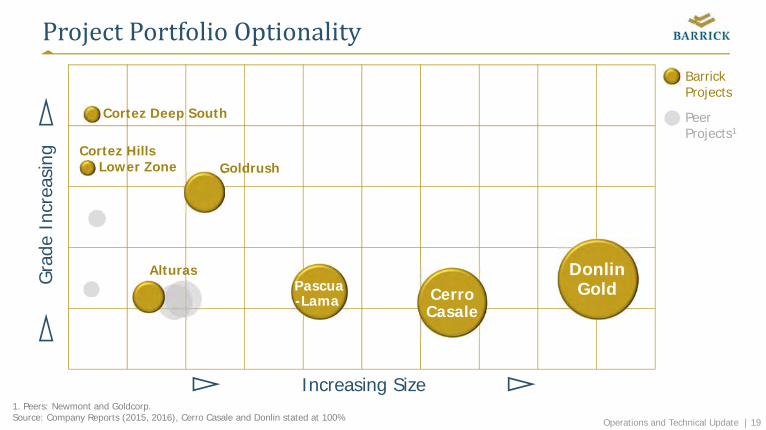

ProjectPortfolioOptionality

1. Peers: Newmont and Goldcorp.Source: Company Reports (2015, 2016), Cerro Casale and Donlin stated at 100%

Gra

de I

ncre

asin

g

Increasing Size

Barrick Projects

PeerProjects1

Goldrush

Cortez Deep South

Pascua-Lama Cerro

Casale

DonlinGold

Alturas

Cortez HillsLower Zone

Operations and Technical Update | 20

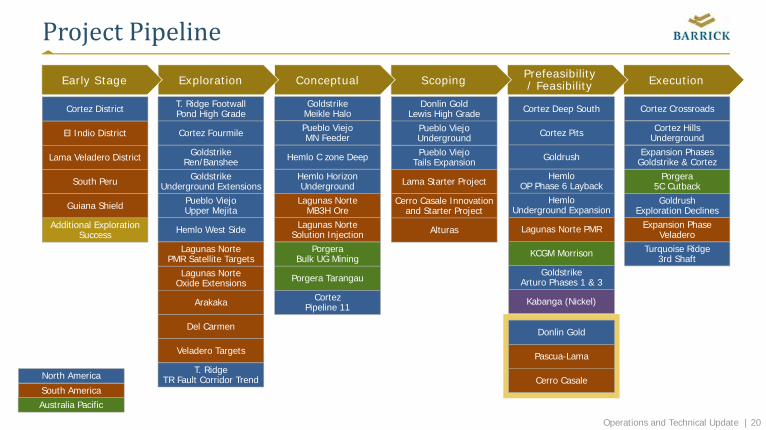

ProjectPipeline

Pascua-Lama

Donlin Gold

Cerro Casale

Kabanga (Nickel)

ExecutionPrefeasibility/ FeasibilityScopingConceptualExplorationEarly Stage

North America

South AmericaAustralia Pacific

Porgera5C Cutback

Cortez Crossroads

Cortez HillsUnderground

Turquoise Ridge3rd Shaft

Goldrush Exploration Declines

Expansion PhasesGoldstrike & Cortez

Expansion PhaseVeladero

Cortez District

El Indio District

Lama Veladero District

South Peru

Guiana Shield

Additional Exploration Success

Donlin GoldLewis High Grade

Pueblo Viejo UndergroundPueblo Viejo

Tails Expansion

Lama Starter Project

Alturas

Cerro Casale Innovationand Starter Project

Pueblo ViejoUpper Mejita

Lagunas NorteOxide Extensions

Hemlo West Side

T. Ridge Footwall Pond High Grade

Lagunas NortePMR Satellite Targets

Cortez Fourmile

Arakaka

Del Carmen

GoldstrikeUnderground Extensions

GoldstrikeRen/Banshee

Veladero Targets

T. Ridge TR Fault Corridor Trend

GoldstrikeMeikle Halo

Lagunas NorteMB3H Ore

Pueblo ViejoMN Feeder

Hemlo C zone Deep

PorgeraBulk UG Mining

Porgera Tarangau

CortezPipeline 11

Hemlo Horizon Underground

Lagunas NorteSolution Injection

GoldstrikeArturo Phases 1 & 3

Cortez Deep South

Cortez Pits

Goldrush

HemloOP Phase 6 Layback

KCGM Morrison

Lagunas Norte PMR

HemloUnderground Expansion

Operations and Technical Update | 21

DigitalTransformation&Innovation

MichelleAshChiefInnovationOfficer

Operations and Technical Update | 22

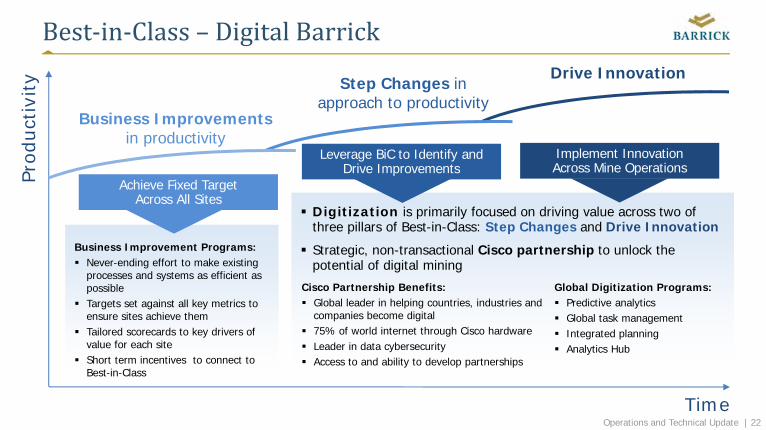

Best‐in‐Class– DigitalBarrickPr

oduc

tivity

Time

Leverage BiC to Identify and Drive Improvements

Achieve Fixed Target Across All Sites

Implement Innovation Across Mine Operations

Drive InnovationStep Changes in

approach to productivityBusiness Improvements

in productivity

Digitization is primarily focused on driving value across two of three pillars of Best-in-Class: Step Changes and Drive Innovation

Strategic, non-transactional Cisco partnership to unlock the potential of digital mining

Global Digitization Programs: Predictive analytics Global task management Integrated planning Analytics Hub

Cisco Partnership Benefits: Global leader in helping countries, industries and

companies become digital 75% of world internet through Cisco hardware Leader in data cybersecurity Access to and ability to develop partnerships

Business Improvement Programs: Never-ending effort to make existing

processes and systems as efficient as possible

Targets set against all key metrics to ensure sites achieve them

Tailored scorecards to key drivers of value for each site

Short term incentives to connect to Best-in-Class

Operations and Technical Update | 23

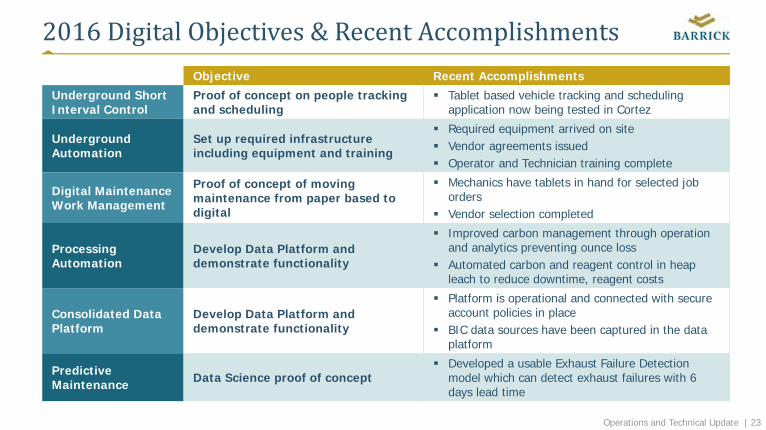

2016DigitalObjectives&RecentAccomplishmentsObjective Recent Accomplishments

Underground Short Interval Control

Proof of concept on people tracking and scheduling

Tablet based vehicle tracking and scheduling application now being tested in Cortez

Underground Automation

Set up required infrastructure including equipment and training

Required equipment arrived on site Vendor agreements issued Operator and Technician training complete

Digital Maintenance Work Management

Proof of concept of moving maintenance from paper based to digital

Mechanics have tablets in hand for selected job orders

Vendor selection completed

Processing Automation

Develop Data Platform and demonstrate functionality

Improved carbon management through operation and analytics preventing ounce loss

Automated carbon and reagent control in heap leach to reduce downtime, reagent costs

Consolidated Data Platform

Develop Data Platform and demonstrate functionality

Platform is operational and connected with secure account policies in place

BIC data sources have been captured in the data platform

Predictive Maintenance Data Science proof of concept

Developed a usable Exhaust Failure Detection model which can detect exhaust failures with 6 days lead time

Operations and Technical Update | 24

Codemine – Elko,Nevada

The Codemine has been established in Elko to design code to integrate several applications

Pioneering digital products

Completed proof of concepts for initial digital projects (e.g. short interval control)

Developing customized digital solutions with computer developers and programmers working with operators

Agile approach minimizes upfront capital and execution risk

Operations and Technical Update | 25

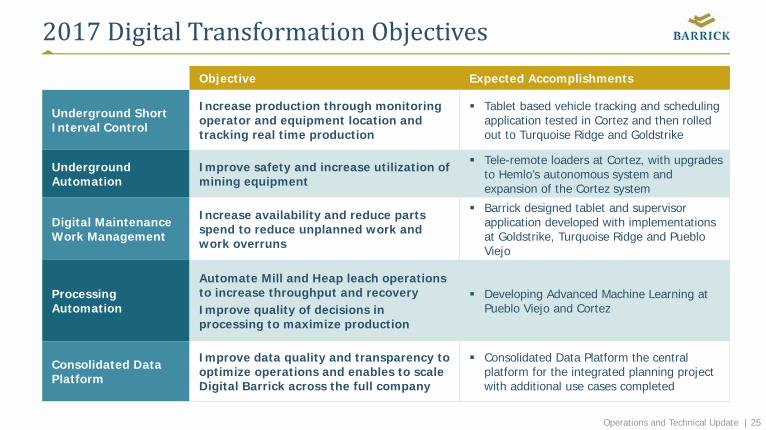

2017DigitalTransformationObjectivesObjective Expected Accomplishments

Underground Short Interval Control

Increase production through monitoring operator and equipment location and tracking real time production

Tablet based vehicle tracking and scheduling application tested in Cortez and then rolled out to Turquoise Ridge and Goldstrike

Underground Automation

Improve safety and increase utilization of mining equipment

Tele-remote loaders at Cortez, with upgrades to Hemlo’s autonomous system and expansion of the Cortez system

Digital Maintenance Work Management

Increase availability and reduce parts spend to reduce unplanned work and work overruns

Barrick designed tablet and supervisor application developed with implementations at Goldstrike, Turquoise Ridge and Pueblo Viejo

Processing Automation

Automate Mill and Heap leach operations to increase throughput and recovery Improve quality of decisions in processing to maximize production

Developing Advanced Machine Learning at Pueblo Viejo and Cortez

Consolidated Data Platform

Improve data quality and transparency to optimize operations and enables to scale Digital Barrick across the full company

Consolidated Data Platform the central platform for the integrated planning project with additional use cases completed

Operations and Technical Update | 26

InnovationFocusNew Barrick competencies will permit deep strategies that transform mining

Best miner

Best Partner

Best Platform

Extraction Reimagined

Prosperous Partnerships

Absolute Integration

Mineral Cartography

Operations and Technical Update | 27

EmergingInnovationFocusAreas

MineralCartography

Ourgoalistolocateand

describeeverygolddepositintheworld

AbsoluteIntegration

Weplantoconnectevery

assetandactivityinourecosysteminanintelligentandtransparent

system

ProsperousPartnerships

Weaimtocreatesustainableprosperity

throughworkingpartnerships

withcompanies,communitiesandgovernments

ExtractionReimagined

Weplantobeabletoextractanydeep,

complex,low‐gradegold

depositintheworld,safelyand

profitably

NewBusinesses

Weaimtoexploreandcreate

alternativesourcesofrevenuethatleverageourunique

competencies

$

Operations and Technical Update | 28

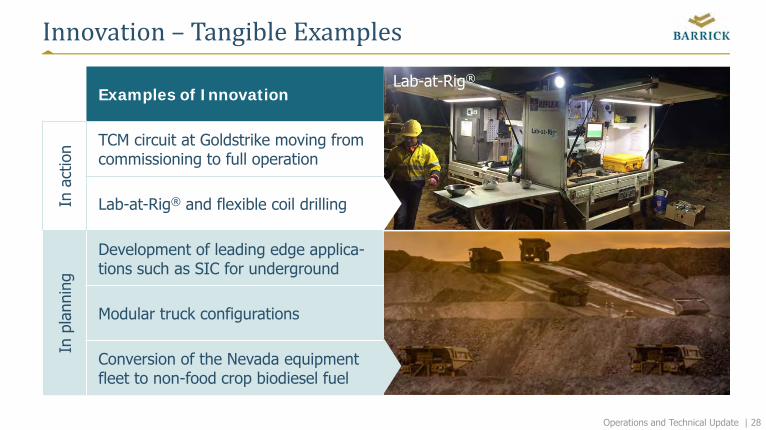

Innovation– TangibleExamples

Examples of Innovation

In a

ctio

n TCM circuit at Goldstrike moving from commissioning to full operation

Lab-at-Rig® and flexible coil drilling

In p

lann

ing

Development of leading edge applica-tions such as SIC for underground

Modular truck configurations

Conversion of the Nevada equipment fleet to non-food crop biodiesel fuel

Lab-at-Rig®

Operations and Technical Update | 29

Barrick’s DigitalandInnovationJourneyDesired Achievements Aspirational Target

MineralCartography

Develop predictive and cognitive algorithms to better define targets and orebodies

Increase in speed and accuracy for orebody definition

Development of a non-intrusive method to visualize gold deposits

Significant cost reduction in exploration and resource definition

ExtractionReimagined

Development of fully autonomous mining and processing system

Everyone on surface and at low elevation Reduction in AISC and closure costs

Development of processing techniques for low grade and refractory ores Significant increase in resource and reserves

World class trades productivity and asset reliability Significant increase in OEE

ProsperousPartnerships

Conversion to electricity and/or renewable forms of energy

Most of our power from renewables; all UG operations are emission free

Wealth creation through a number of significant partnerships Fully trusted by our partners

AbsoluteIntegration

Fully integrated operational and data systems

Real time response to changes in the plan to optimize value

Full transparency of data and operational performance through Operating Centers Robust reduction in operational risk

Operations and Technical Update | 30

Long‐termPortfolioOptionality

MattGiliChiefTechnicalOfficer

Operations and Technical Update | 31

Growth Plan: Long term upside opportunities

Strategic Plan: Life of mine plan with key growth projects

FromIdentifyingourFullPotential…

Full Potential: Optimized strategic planning for growth

Life of Mine Plan: Most probable scenario for future production and development

Business Plan Annual Cycle

Reserve Plan: Annual production planCollaborative effort

between

Operations (Mines, Sites and Project Teams)

Finance

Technical Office

Exploration

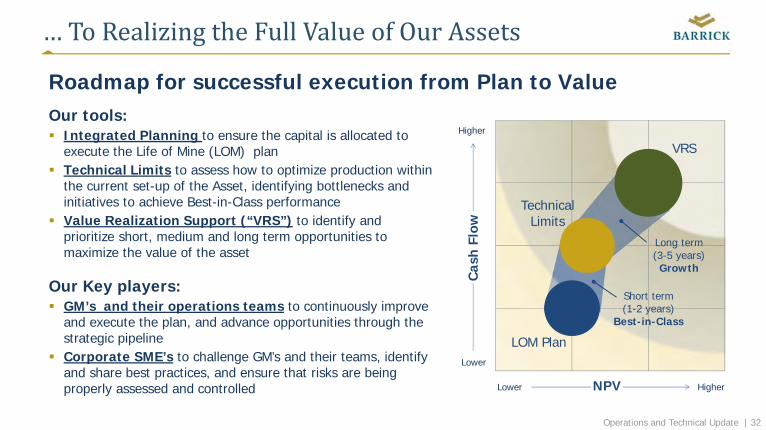

Operations and Technical Update | 32

Technical Limits

LOM Plan

VRS

Cas

h Fl

ow

NPV

Short term(1-2 years)

Best-in-Class

Long term(3-5 years)Growth

…ToRealizingtheFullValueofOurAssets

Roadmap for successful execution from Plan to Value Our tools: Integrated Planning to ensure the capital is allocated to

execute the Life of Mine (LOM) plan Technical Limits to assess how to optimize production within

the current set-up of the Asset, identifying bottlenecks and initiatives to achieve Best-in-Class performance

Value Realization Support (“VRS”) to identify and prioritize short, medium and long term opportunities to maximize the value of the asset

Our Key players: GM’s and their operations teams to continuously improve

and execute the plan, and advance opportunities through the strategic pipeline

Corporate SME’s to challenge GM’s and their teams, identify and share best practices, and ensure that risks are being properly assessed and controlled Higher

Higher

Lower

Lower

Operations and Technical Update | 33

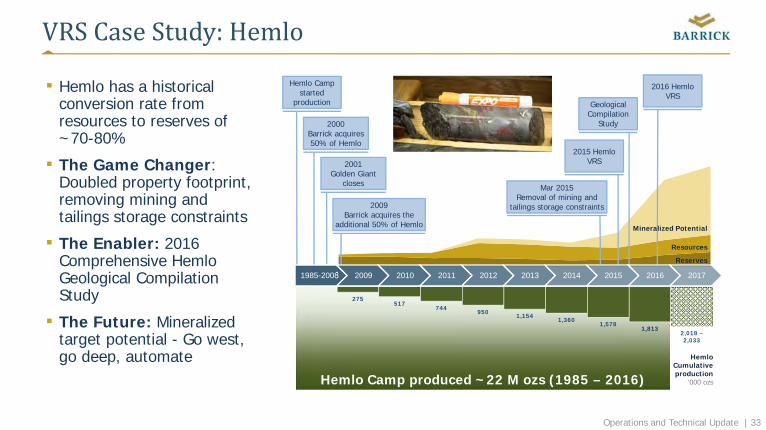

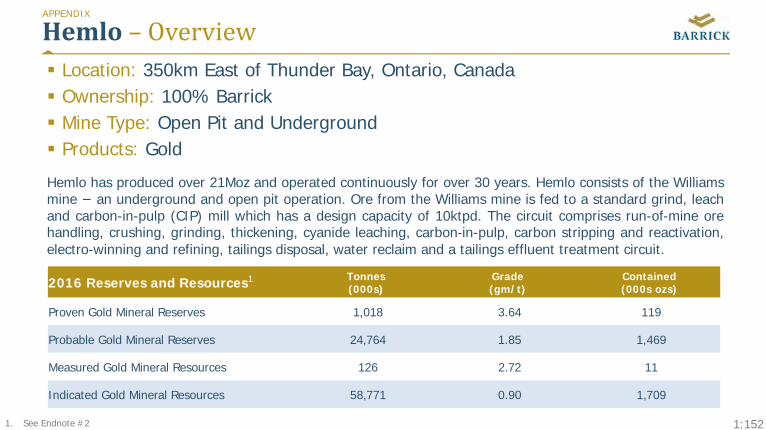

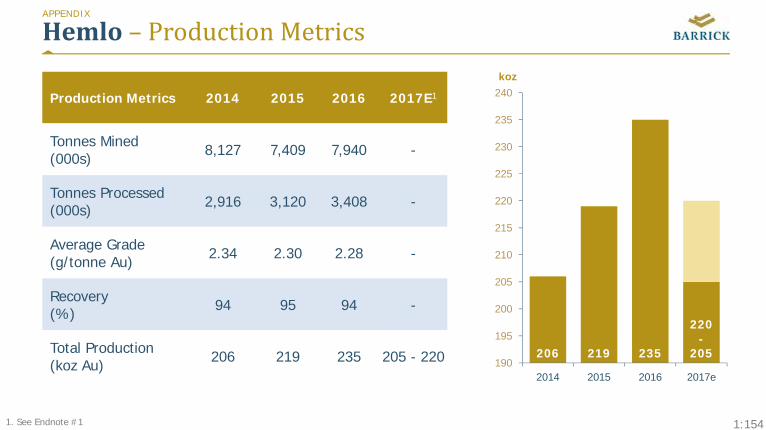

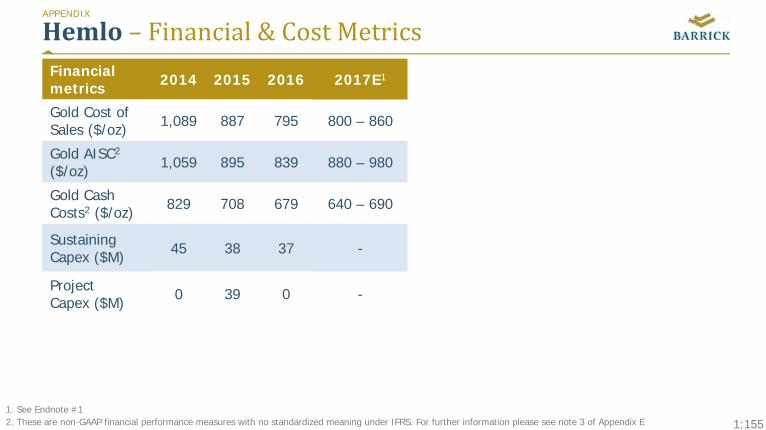

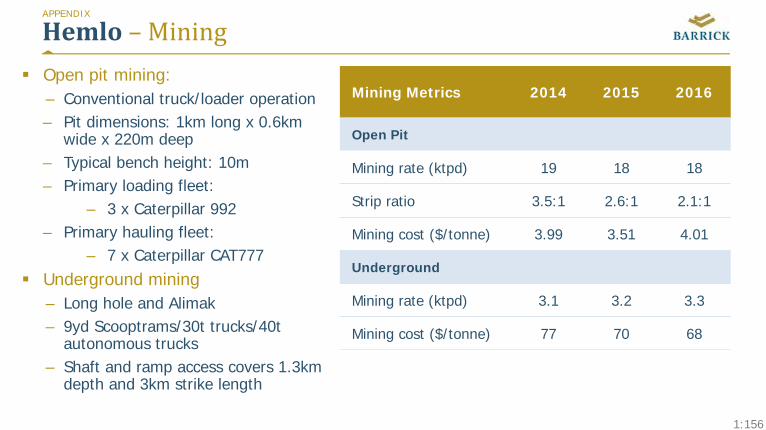

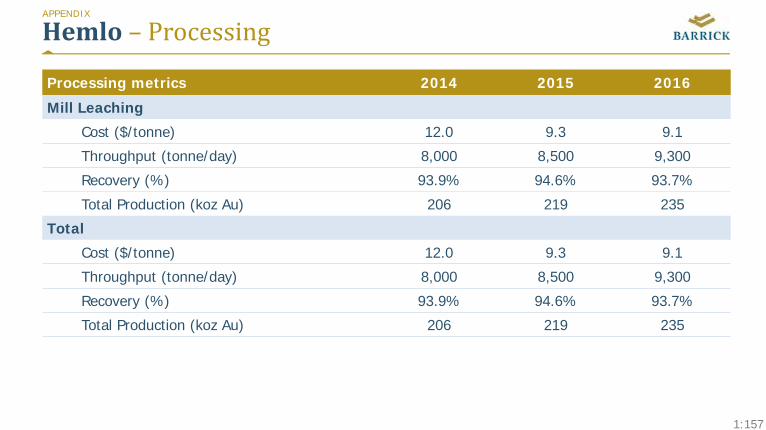

Hemlo Camp produced ~22 M ozs (1985 – 2016)

VRSCaseStudy:Hemlo

▪ Hemlo has a historical conversion rate from resources to reserves of ~70-80%

▪ The Game Changer: Doubled property footprint, removing mining and tailings storage constraints

▪ The Enabler: 2016 Comprehensive HemloGeological Compilation Study

▪ The Future: Mineralized target potential - Go west, go deep, automate

275517

744950

1,1541,360

1,5781,813

2,025

Mar 2015Removal of mining and

tailings storage constraints

2015 HemloVRS

2016 HemloVRS

Hemlo Camp started

production Geological Compilation

Study

2009Barrick acquires the

additional 50% of Hemlo

2000Barrick acquires 50% of Hemlo

1985-2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

HemloCumulative production

‘000 ozs

Mineralized Potential

Resources

Reserves

2001Golden Giant

closes

2,018 –2,033

Operations and Technical Update | 34

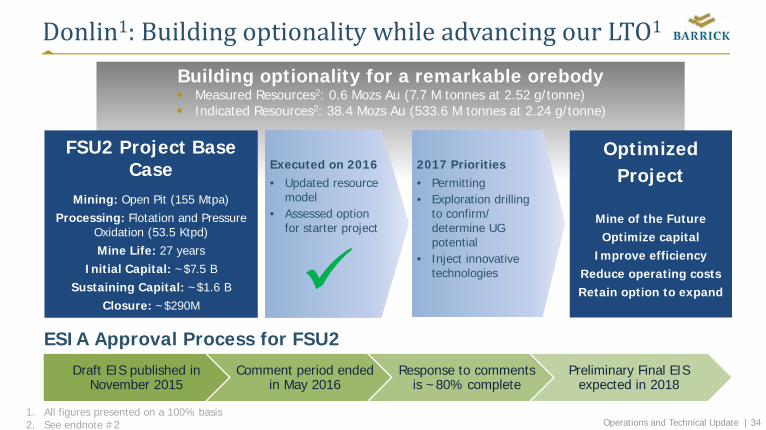

Donlin1:BuildingoptionalitywhileadvancingourLTO1

Building optionality for a remarkable orebody Measured Resources2: 0.6 Mozs Au (7.7 M tonnes at 2.52 g/tonne) Indicated Resources2: 38.4 Mozs Au (533.6 M tonnes at 2.24 g/tonne)

ESIA Approval Process for FSU2

FSU2 Project Base Case

Mining: Open Pit (155 Mtpa)Processing: Flotation and Pressure

Oxidation (53.5 Ktpd) Mine Life: 27 years

Initial Capital: ~$7.5 BSustaining Capital: ~$1.6 B

Closure: ~$290M

Draft EIS published in November 2015

Comment period ended in May 2016

Response to comments is ~80% complete

Preliminary Final EIS expected in 2018

Optimized Project

Mine of the FutureOptimize capital

Improve efficiencyReduce operating costsRetain option to expand

Executed on 2016• Updated resource

model• Assessed option

for starter project

2017 Priorities• Permitting• Exploration drilling

to confirm/determine UG potential

• Inject innovative technologies

1. All figures presented on a 100% basis2. See endnote #2

Operations and Technical Update | 35

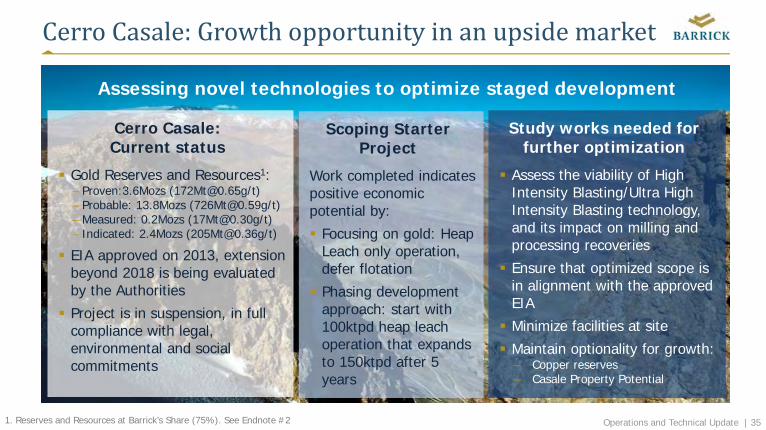

CerroCasale:Growthopportunityinanupsidemarket

Cerro Casale: Current status

Gold Reserves and Resources1:– Proven:3.6Mozs ([email protected]/t)– Probable: 13.8Mozs ([email protected]/t)– Measured: 0.2Mozs ([email protected]/t)– Indicated: 2.4Mozs ([email protected]/t)

EIA approved on 2013, extension beyond 2018 is being evaluated by the Authorities

Project is in suspension, in full compliance with legal, environmental and social commitments

Scoping Starter Project

Work completed indicates positive economic potential by:

Focusing on gold: Heap Leach only operation, defer flotation

Phasing development approach: start with 100ktpd heap leach operation that expands to 150ktpd after 5 years

Study works needed for further optimization

Assess the viability of High Intensity Blasting/Ultra High Intensity Blasting technology, and its impact on milling and processing recoveries

Ensure that optimized scope is in alignment with the approved EIA

Minimize facilities at site

Maintain optionality for growth:– Copper reserves– Casale Property Potential

Assessing novel technologies to optimize staged development

1. Reserves and Resources at Barrick’s Share (75%). See Endnote #2

Operations and Technical Update | 36

BarrickNevada– SecuringtheFuture

BillMacNevinBarrickNevadaCEO

Operations and Technical Update | 37

UnifyingNevadaAssets

Enabler of Change

First Step – What? Vision – How? Drive – Why?WeareunitingourCortezandGoldstrike operationsinNevada,combiningassets,infrastructureandexpertise…

…buildingonourcombinedstrengthsbyunitingtheseoperationsunderonesitebasedleadershipstructure…

…inordertocreatenewopportunitiesandgrowthebusinessforourpeople,communitiesandownersbydrivingimprovementsinefficiencyandproductivity

Operations and Technical Update | 38

BarrickNevadaValueCapture Targeting lower AISC/oz through combined efficiency and productivity improvements

– Focus talent and resources from whole business on opportunities of greatest value

Integrated collaboration and joint metal planning to optimize ore processing– Improve consistency of ore feed improving throughput in the Roaster

Integrated Leadership Team to share and adopt best practices– Prioritizing equipment and people to improve free cash flow

Deliver improved free cash flow through integrated processing operations– Deploy an integrated planning operating system to identify risk and opportunity in our plans

Expedite Digital Transformation through integrated digital operations management center– Barrick Nevada Operations Support Center to include dispatch for open pit and underground

mines, process control rooms, remote operations work stations to increase the capabilities of our people

Operations and Technical Update | 39

Goldstrike– FocusedonOperationalExcellence

Operations and Technical Update | 40

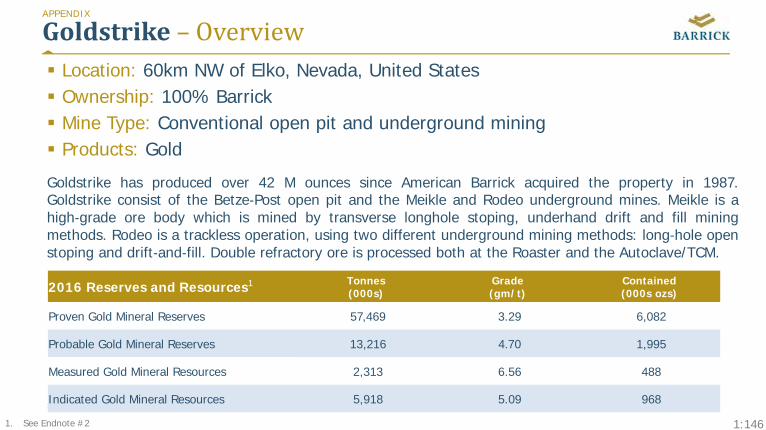

Goldstrike– Today

Vision – A core operation and processing option of choice focused on improvement, operational excellence and growth to ensure a sustainable, profitable production profile Conventional open pit and underground mining consisting of the Betze-Post open pit

and the Meikle and Rodeo underground mines Meikle and Rodeo are mined by transverse longhole stoping and underhand drift and

fill mining methods Double refractory ore is processed both at the Roaster and the Autoclave/TCM 30 Years of Operations, both open pit and underground, moving 3.5 billion tonnes and

producing 42M ounces – still going strong

Highlights of 2016:– Commenced commercial production at Arturo– Autoclave/TCM technology performing in line with expectations– Lowered water table to access high margin ounces in the underground– Delivered additional free cash flow through focus on operational excellence

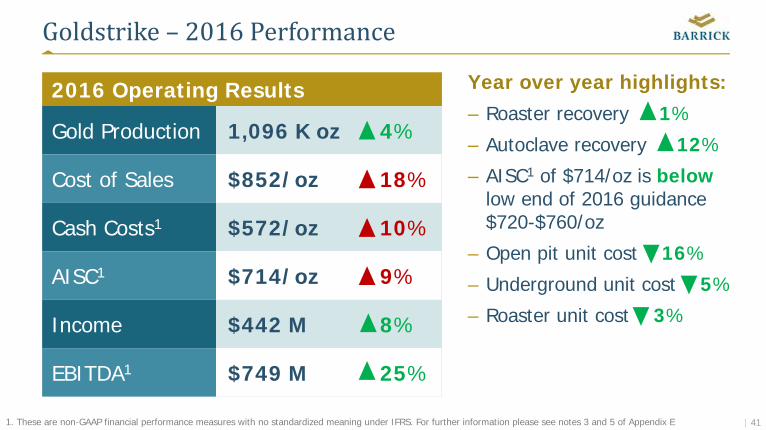

Operations and Technical Update | 41

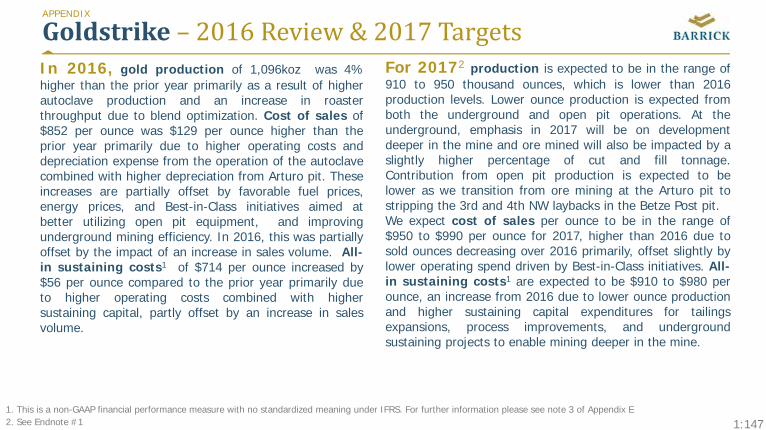

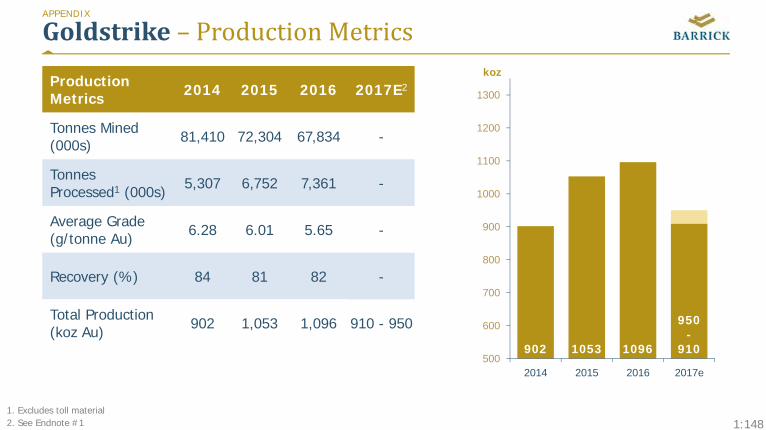

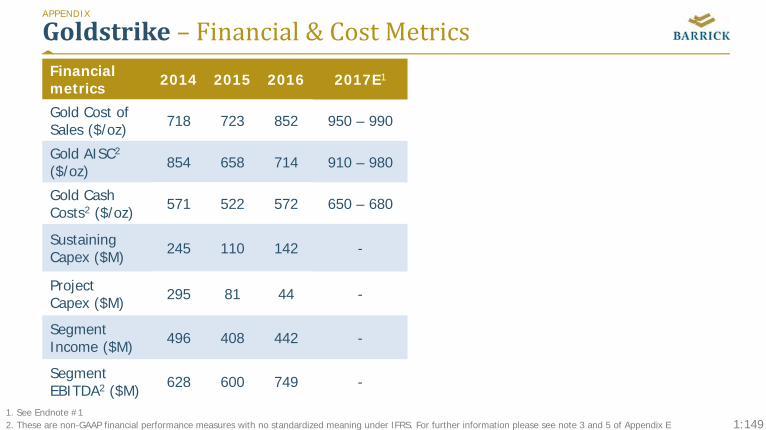

Goldstrike – 2016Performance

Year over year highlights:– Roaster recovery 1%

– Autoclave recovery 12%

– AISC1 of $714/oz is belowlow end of 2016 guidance $720-$760/oz

– Open pit unit cost 16%

– Underground unit cost 5%

– Roaster unit cost 3%

2016 Operating Results

Gold Production 1,096 K oz 4%

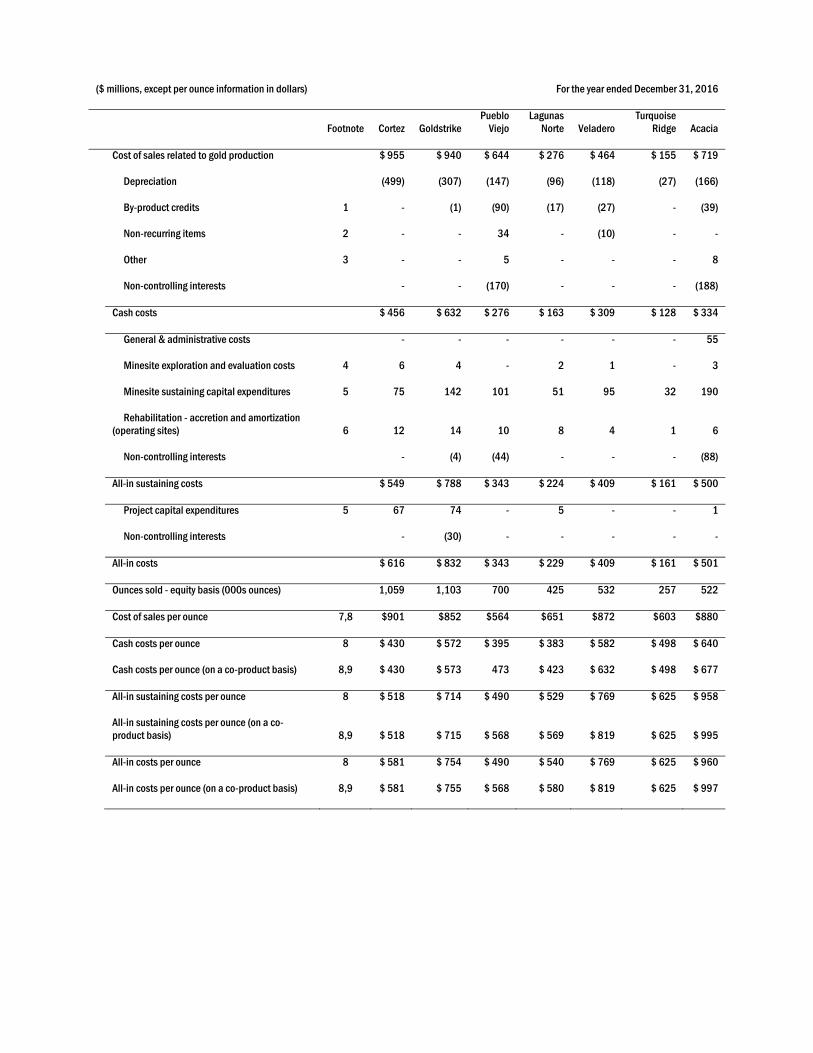

Cost of Sales $852/oz 18%

Cash Costs1 $572/oz 10%

AISC1 $714/oz 9%

Income $442 M 8%

EBITDA1 $749 M 25%

1. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see notes 3 and 5 of Appendix E

Operations and Technical Update | 42

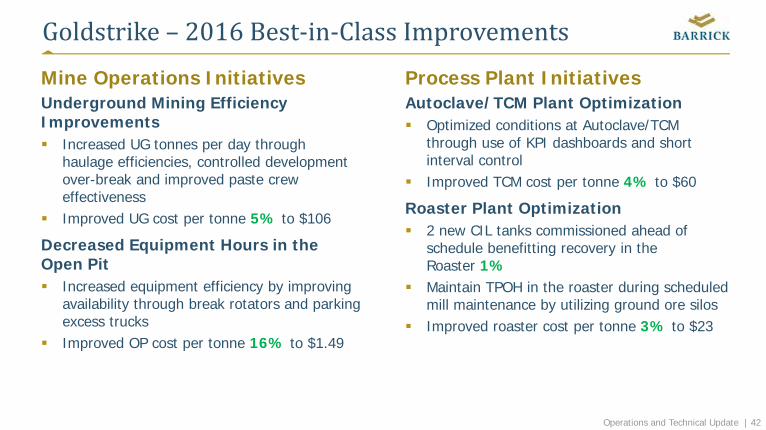

Goldstrike– 2016Best‐in‐ClassImprovementsMine Operations InitiativesUnderground Mining Efficiency Improvements Increased UG tonnes per day through

haulage efficiencies, controlled development over-break and improved paste crew effectiveness

Improved UG cost per tonne 5% to $106

Decreased Equipment Hours in the Open Pit Increased equipment efficiency by improving

availability through break rotators and parking excess trucks

Improved OP cost per tonne 16% to $1.49

Process Plant InitiativesAutoclave/TCM Plant Optimization Optimized conditions at Autoclave/TCM

through use of KPI dashboards and short interval control

Improved TCM cost per tonne 4% to $60

Roaster Plant Optimization 2 new CIL tanks commissioned ahead of

schedule benefitting recovery in the Roaster 1%

Maintain TPOH in the roaster during scheduled mill maintenance by utilizing ground ore silos

Improved roaster cost per tonne 3% to $23

Operations and Technical Update | 43

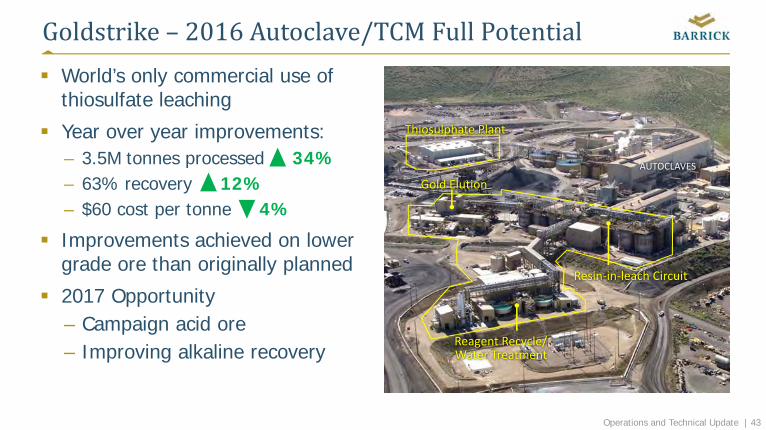

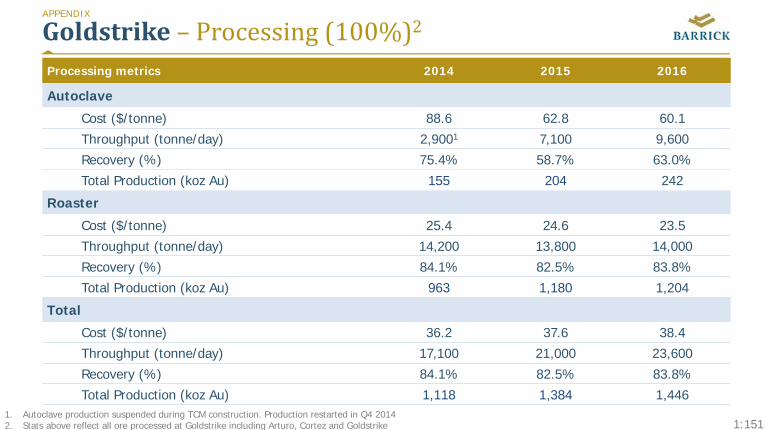

Goldstrike– 2016Autoclave/TCMFullPotential World’s only commercial use of

thiosulfate leaching

Year over year improvements:– 3.5M tonnes processed 34%– 63% recovery 12%– $60 cost per tonne 4%

Improvements achieved on lower grade ore than originally planned

2017 Opportunity– Campaign acid ore– Improving alkaline recovery

Resin‐in‐leach Circuit

Reagent Recycle/Water Treatment

Thiosulphate Plant

AUTOCLAVES

Gold Elution

Operations and Technical Update | 44

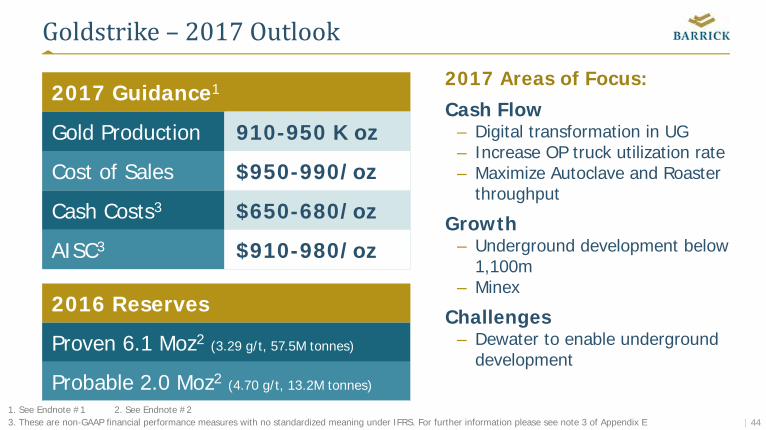

Goldstrike – 2017Outlook

2017 Guidance1

Gold Production 910-950 K oz

Cost of Sales $950-990/oz

Cash Costs3 $650-680/oz

AISC3 $910-980/oz

2017 Areas of Focus:

Cash Flow– Digital transformation in UG – Increase OP truck utilization rate– Maximize Autoclave and Roaster

throughput

Growth– Underground development below

1,100m– Minex

Challenges– Dewater to enable underground

development

2016 Reserves

Proven 6.1 Moz2 (3.29 g/t, 57.5M tonnes)

Probable 2.0 Moz2 (4.70 g/t, 13.2M tonnes)

1. See Endnote #1 2. See Endnote #23. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations and Technical Update | 45

Goldstrike – 2017Best‐in‐ClassInitiatives Open Pit

– Improve maintenance efficiencies by increasing component life

– Increase truck OEE by focusing on utilization

Underground– Digitization enabling short interval control

and automated jumbo trails– Improve planning effectiveness

Process – Improve Autoclave recovery – Improve throughput and water treatment

metrics to lower $/tonne in the Autoclave– Blend for margin in the Roaster to increase

throughput

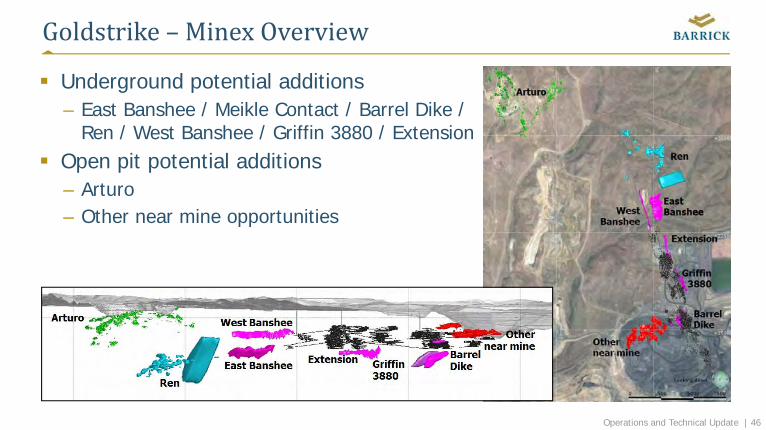

Operations and Technical Update | 46

Goldstrike– MinexOverview

Underground potential additions– East Banshee / Meikle Contact / Barrel Dike /

Ren / West Banshee / Griffin 3880 / Extension Open pit potential additions

– Arturo– Other near mine opportunities

Operations and Technical Update | 47

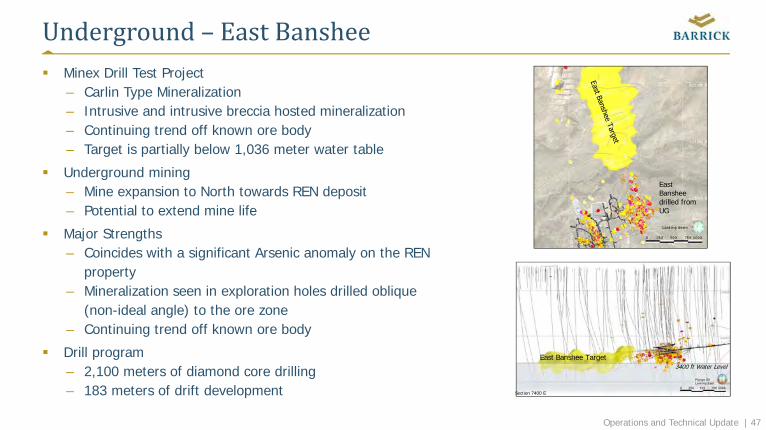

Underground– EastBanshee Minex Drill Test Project

– Carlin Type Mineralization– Intrusive and intrusive breccia hosted mineralization– Continuing trend off known ore body– Target is partially below 1,036 meter water table

Underground mining– Mine expansion to North towards REN deposit – Potential to extend mine life

Major Strengths– Coincides with a significant Arsenic anomaly on the REN

property– Mineralization seen in exploration holes drilled oblique

(non-ideal angle) to the ore zone– Continuing trend off known ore body

Drill program– 2,100 meters of diamond core drilling – 183 meters of drift development

East Banshee drilled from UG

3400 ft Water Level

Section 7400 E

East Banshee Target

Operations and Technical Update | 48

OpenPit‐ Arturo:Phases1,2,&3withGoldGradeShells

Additional Phases of Arturo utilizing existing mine equipment

Mining and process facilities are permitted

Under evaluation– Leach pad feasibility– Economics– Recoveries– Mining costs– In-pit backfill (backfilling not

permitted)

Mining will expose new geology and potential deep UG exploration targets

Phase 1Exploration Target

Phase 2: Mining completed Feb 2017

Phase 3Exploration Target

Operations and Technical Update | 49

Goldstrike– FutureGrowthOptionality

Upside: Increase mineral resource through near mine exploration and lower operating costs

Open Pit – Arturo I & III

Open Pit – 5NW layback

Underground – Minex, lower mining cost to reduce cutoff grades

Autoclave – reach full potential byincreasing throughput, maximizingbenefit of acid and alkaline ores

Roaster – blend for margin to maximize FCF

Near mine exploration

Operations Technical Update Day | 50

Cortez– OrganicandTechnicalGrowth

CurtisCadwellGeneralManagerOperationsBarrick Nevada

Operations Technical Update Day | 51

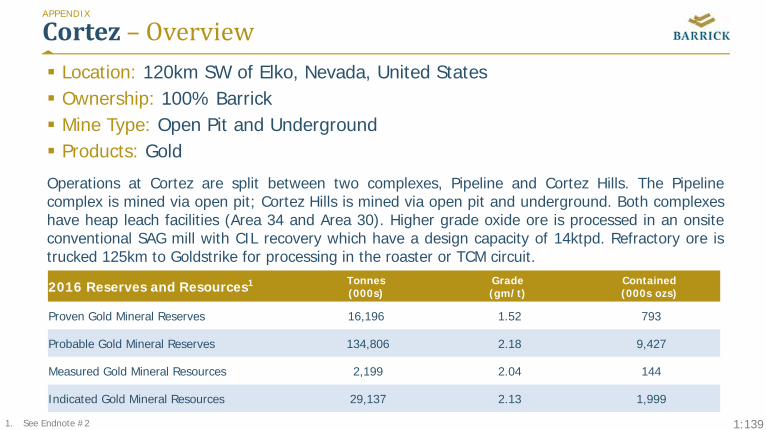

Cortez– Today

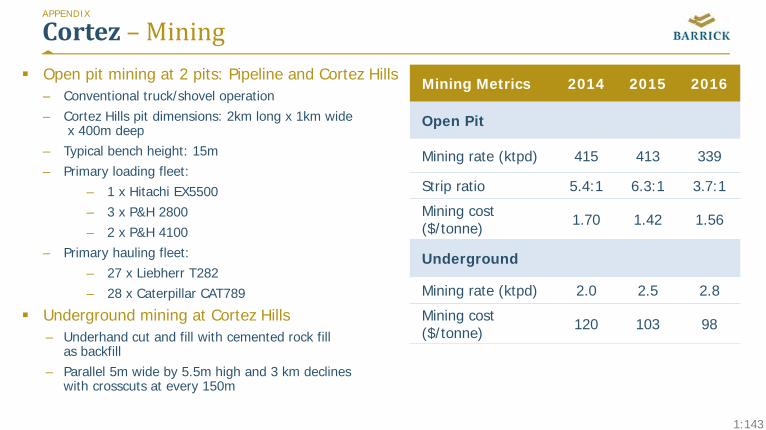

Vision is to be a multi-mine operation, focused on increasing cash flow through relentless pursuit of operational excellence while generating sustainable growth Open pit and underground mining consisting of Pipeline open pit and Cortez

Hills open pit and underground Oxide ore is processed using heap leach and Oxide SAG+CIL, refractory ore

trucked to Goldstrike Roaster or TCM circuit Achievements in 2016:

– 43% reduction in reportable safety incidents from 2015 to lowest reporting rate on record for Cortez

– Commenced Digitization projects with focus on automation, process control, and maintenance data

– Commenced development of the Range Front Declines to increase Cortez Hills UG production

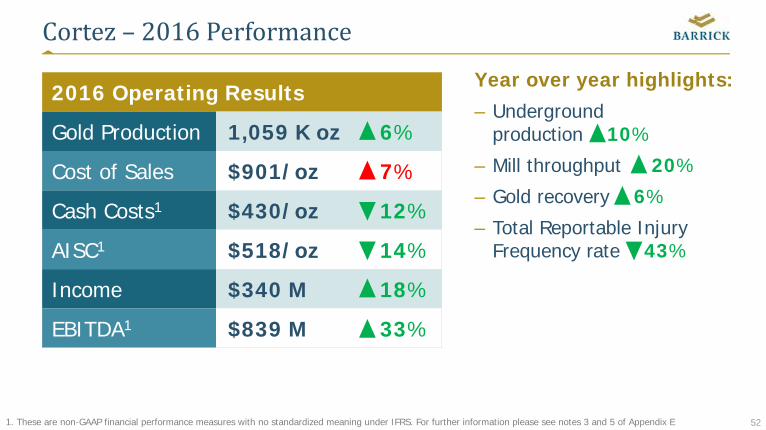

Operations Technical Update Day | 52

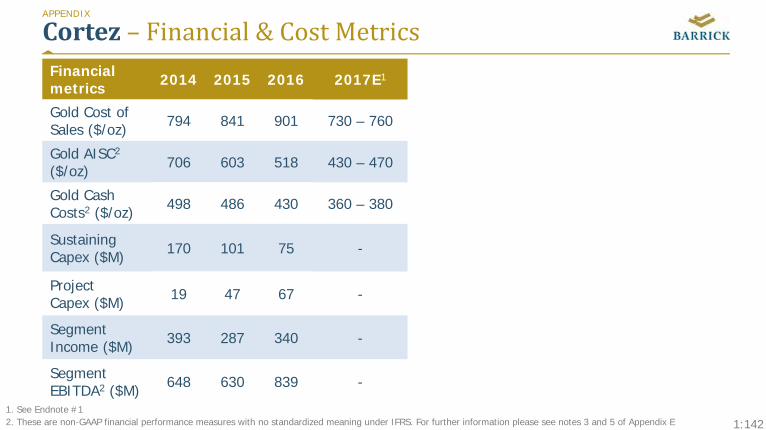

Cortez– 2016Performance

Year over year highlights:– Underground

production 10%

– Mill throughput 20%

– Gold recovery 6%

– Total Reportable Injury Frequency rate 43%

2016 Operating Results

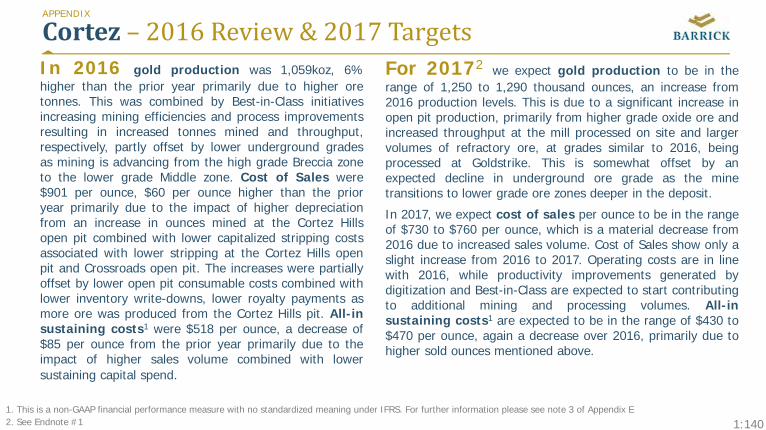

Gold Production 1,059 K oz 6%

Cost of Sales $901/oz 7%

Cash Costs1 $430/oz 12%

AISC1 $518/oz 14%

Income $340 M 18%

EBITDA1 $839 M 33%

1. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see notes 3 and 5 of Appendix E

Operations Technical Update Day | 53

Cortez– 2016Best‐in‐ClassInitiatives Open pit productivity initiatives

– Introduced operator scorecards– Adopted short interval control process

and focused on right loading of trucks– Digital work management and predictive

maintenance improving truck availability

Step change in underground production– Move to bulk mining increased efficiencies

and lowered mining cost per tonne– Completed 10 benches– Completed first long hole stope

UG operating performance

Operations Technical Update Day | 54

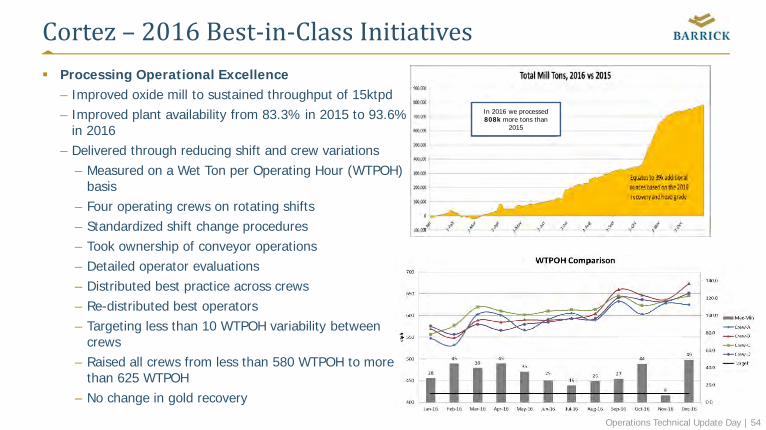

Cortez– 2016Best‐in‐ClassInitiatives Processing Operational Excellence

– Improved oxide mill to sustained throughput of 15ktpd– Improved plant availability from 83.3% in 2015 to 93.6%

in 2016– Delivered through reducing shift and crew variations

– Measured on a Wet Ton per Operating Hour (WTPOH) basis

– Four operating crews on rotating shifts– Standardized shift change procedures– Took ownership of conveyor operations– Detailed operator evaluations– Distributed best practice across crews– Re-distributed best operators– Targeting less than 10 WTPOH variability between

crews– Raised all crews from less than 580 WTPOH to more

than 625 WTPOH– No change in gold recovery

In 2016 we processed 808k more tons than

2015

Operations Technical Update Day | 55

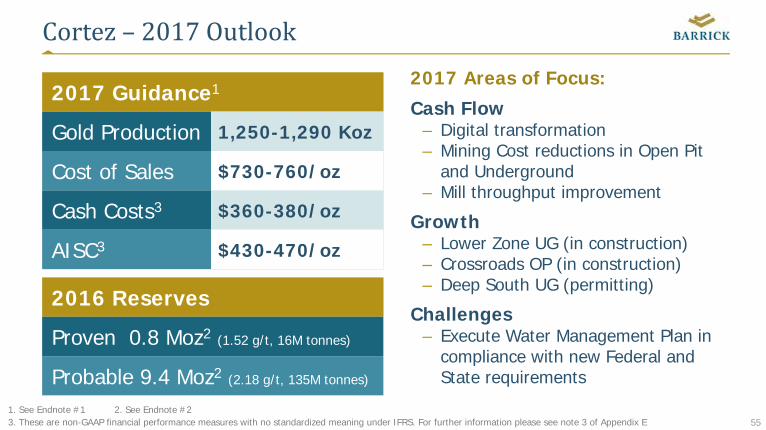

Cortez– 2017Outlook2017 Areas of Focus:

Cash Flow– Digital transformation– Mining Cost reductions in Open Pit

and Underground– Mill throughput improvement

Growth– Lower Zone UG (in construction)– Crossroads OP (in construction)– Deep South UG (permitting)

Challenges– Execute Water Management Plan in

compliance with new Federal and State requirements

2017 Guidance1

Gold Production 1,250-1,290 Koz

Cost of Sales $730-760/oz

Cash Costs3 $360-380/oz

AISC3 $430-470/oz

2016 Reserves

Proven 0.8 Moz2 (1.52 g/t, 16M tonnes)

Probable 9.4 Moz2 (2.18 g/t, 135M tonnes)

1. See Endnote #1 2. See Endnote #23. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations Technical Update Day | 56

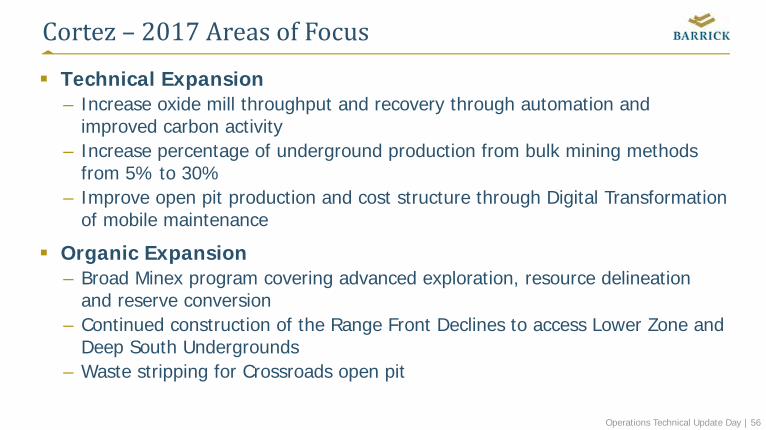

Cortez– 2017AreasofFocus

Technical Expansion– Increase oxide mill throughput and recovery through automation and

improved carbon activity– Increase percentage of underground production from bulk mining methods

from 5% to 30%– Improve open pit production and cost structure through Digital Transformation

of mobile maintenance

Organic Expansion– Broad Minex program covering advanced exploration, resource delineation

and reserve conversion– Continued construction of the Range Front Declines to access Lower Zone and

Deep South Undergrounds– Waste stripping for Crossroads open pit

Operations Technical Update Day | 57

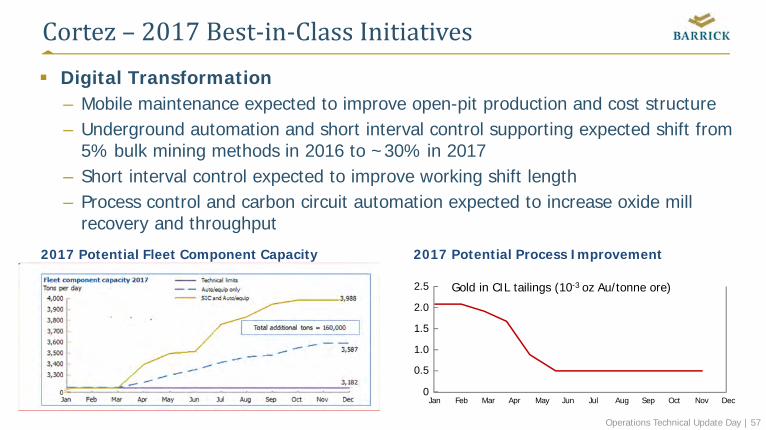

Cortez– 2017Best‐in‐ClassInitiatives Digital Transformation

– Mobile maintenance expected to improve open-pit production and cost structure– Underground automation and short interval control supporting expected shift from

5% bulk mining methods in 2016 to ~30% in 2017– Short interval control expected to improve working shift length– Process control and carbon circuit automation expected to increase oxide mill

recovery and throughput

2017 Potential Fleet Component Capacity 2017 Potential Process Improvement

2.5

2.0

1.5

1.0

0.5

0Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Gold in CIL tailings (10-3 oz Au/tonne ore)

Operations Technical Update Day | 58

Cortez– GrowthPlan:MinexObjective: Replace mined reserves

(annually) Fill LOM production gap Incremental + new discovery

ounces

Maintain Project Pipeline: Targets ranging from

– target delineation– drill test– advanced exploration– resource delineation– reserve conversion

Operations Technical Update Day | 59

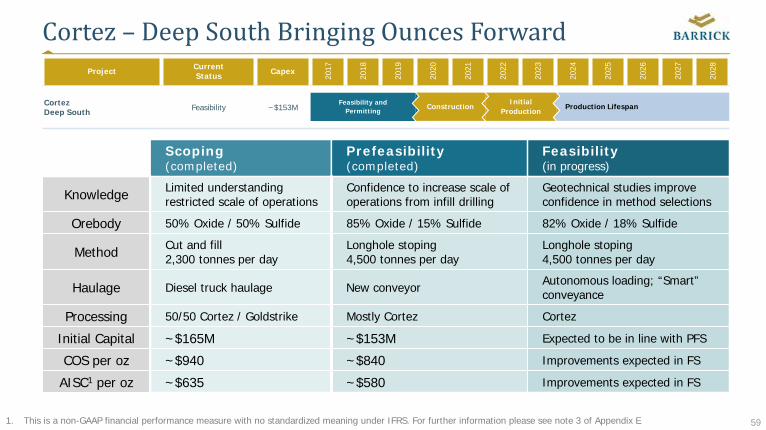

Project Current Status Capex

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

Cortez Deep South Feasibility ~$153M

Scoping (completed)

Prefeasibility (completed)

Feasibility (in progress)

Knowledge Limited understandingrestricted scale of operations

Confidence to increase scale of operations from infill drilling

Geotechnical studies improve confidence in method selections

Orebody 50% Oxide / 50% Sulfide 85% Oxide / 15% Sulfide 82% Oxide / 18% Sulfide

Method Cut and fill2,300 tonnes per day

Longhole stoping4,500 tonnes per day

Longhole stoping4,500 tonnes per day

Haulage Diesel truck haulage New conveyor Autonomous loading; “Smart” conveyance

Processing 50/50 Cortez / Goldstrike Mostly Cortez Cortez

Initial Capital ~$165M ~$153M Expected to be in line with PFS

COS per oz ~$940 ~$840 Improvements expected in FS

AISC1 per oz ~$635 ~$580 Improvements expected in FS

Cortez– DeepSouthBringingOuncesForward

Production LifespanConstructionFeasibility andPermitting

InitialProduction

1. This is a non-GAAP financial performance measure with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations Technical Update Day | 60

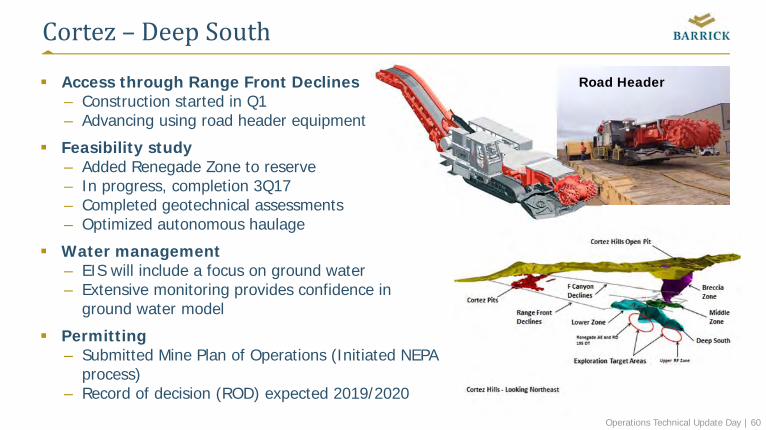

Cortez– DeepSouth

Access through Range Front Declines– Construction started in Q1– Advancing using road header equipment

Feasibility study – Added Renegade Zone to reserve– In progress, completion 3Q17– Completed geotechnical assessments– Optimized autonomous haulage

Water management– EIS will include a focus on ground water – Extensive monitoring provides confidence in

ground water model

Permitting– Submitted Mine Plan of Operations (Initiated NEPA

process)– Record of decision (ROD) expected 2019/2020

Road Header

Operations Technical Update Day | 61

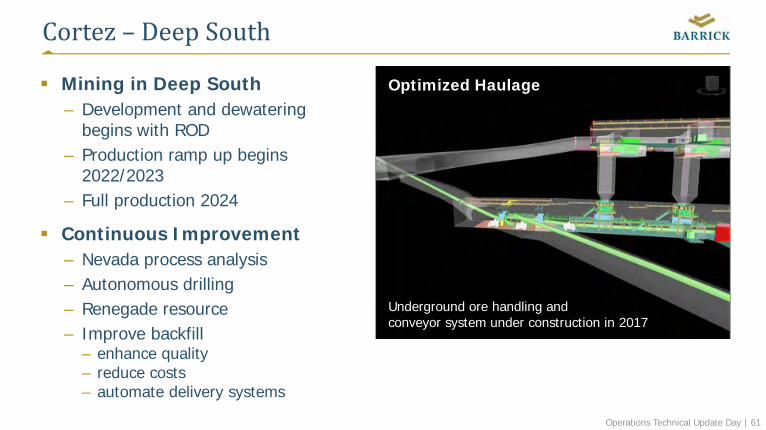

Cortez– DeepSouth

Mining in Deep South – Development and dewatering

begins with ROD– Production ramp up begins

2022/2023 – Full production 2024

Continuous Improvement– Nevada process analysis– Autonomous drilling– Renegade resource– Improve backfill

– enhance quality– reduce costs– automate delivery systems

Optimized Haulage

Underground ore handling and conveyor system under construction in 2017

Operations Technical Update Day | 62

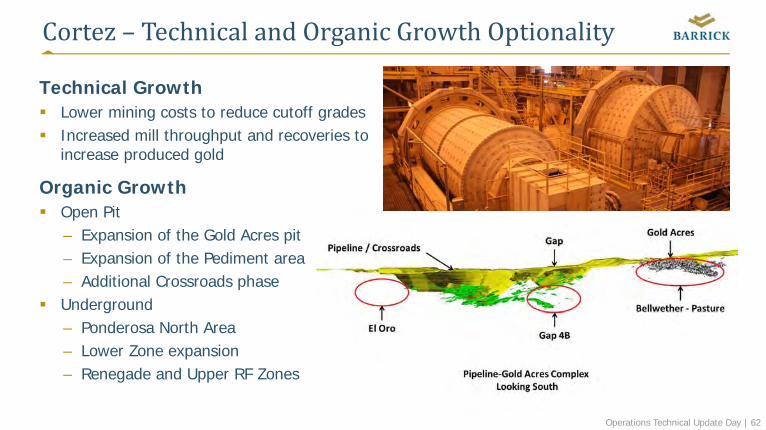

Cortez– TechnicalandOrganicGrowthOptionality

Technical Growth Lower mining costs to reduce cutoff grades Increased mill throughput and recoveries to

increase produced gold

Organic Growth Open Pit

– Expansion of the Gold Acres pit– Expansion of the Pediment area– Additional Crossroads phase

Underground– Ponderosa North Area– Lower Zone expansion– Renegade and Upper RF Zones

Operations Technical Update Day | 63

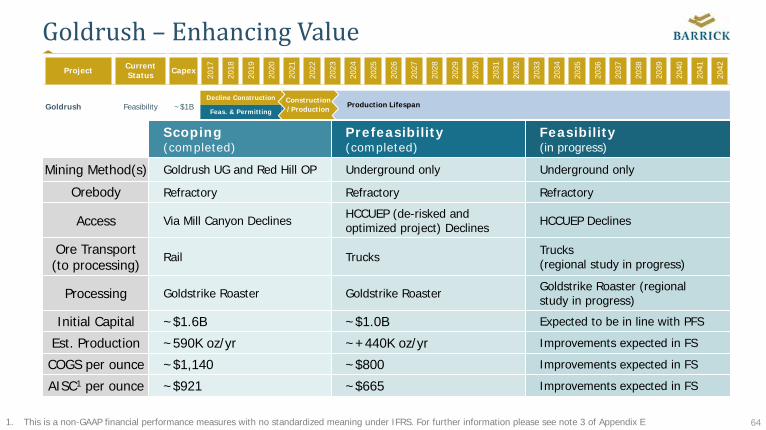

Goldrush– EnhancingValue

Operations Technical Update Day | 64

Project Current Status Capex

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

Goldrush Feasibility ~$1B

Goldrush– EnhancingValue

Scoping (completed)

Prefeasibility(completed)

Feasibility (in progress)

Mining Method(s) Goldrush UG and Red Hill OP Underground only Underground only

Orebody Refractory Refractory Refractory

Access Via Mill Canyon Declines HCCUEP (de-risked and optimized project) Declines HCCUEP Declines

Ore Transport (to processing)

Rail Trucks Trucks (regional study in progress)

Processing Goldstrike Roaster Goldstrike Roaster Goldstrike Roaster (regional study in progress)

Initial Capital ~$1.6B ~$1.0B Expected to be in line with PFS

Est. Production ~590K oz/yr ~+440K oz/yr Improvements expected in FS

COGS per ounce ~$1,140 ~$800 Improvements expected in FS

AISC1 per ounce ~$921 ~$665 Improvements expected in FS

Production LifespanDecline Construction

Feas. & Permitting

Construction/Production

1. This is a non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations Technical Update Day | 65

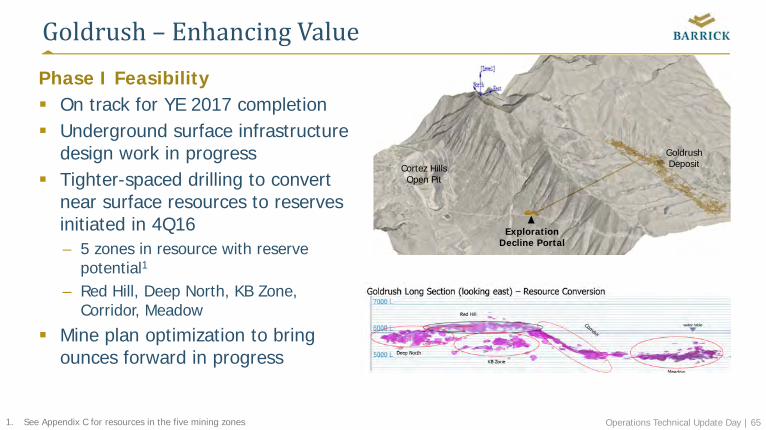

Goldrush– EnhancingValuePhase I Feasibility On track for YE 2017 completion Underground surface infrastructure

design work in progress Tighter-spaced drilling to convert

near surface resources to reserves initiated in 4Q16– 5 zones in resource with reserve

potential1

– Red Hill, Deep North, KB Zone, Corridor, Meadow

Mine plan optimization to bring ounces forward in progress

ExplorationDecline Portal

Cortez HillsOpen Pit

GoldrushDeposit

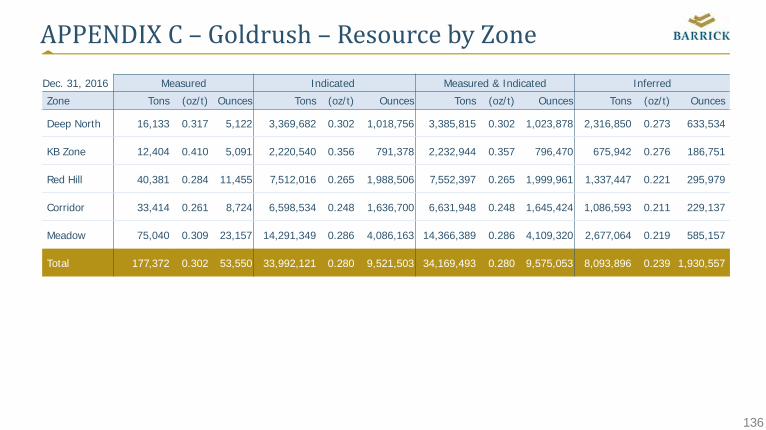

1. See Appendix C for resources in the five mining zones

Operations Technical Update Day | 66

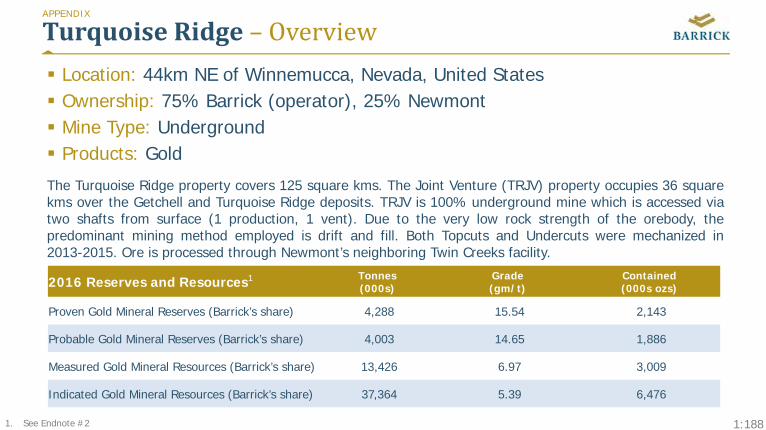

TurquoiseRidge– BuildingonSuccess

HenriGoninGeneralManagerTurquoiseRidge, Nevada

Operations Technical Update Day | 67

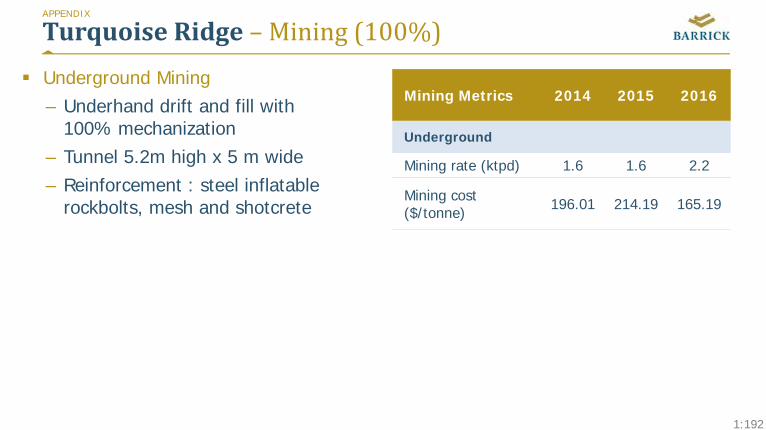

TurquoiseRidge– Today

Our vision is to responsibly grow our mine into a core asset for our stakeholders and our people, delivering maximized value through the agile application of innovative technologies, methodologies and systems

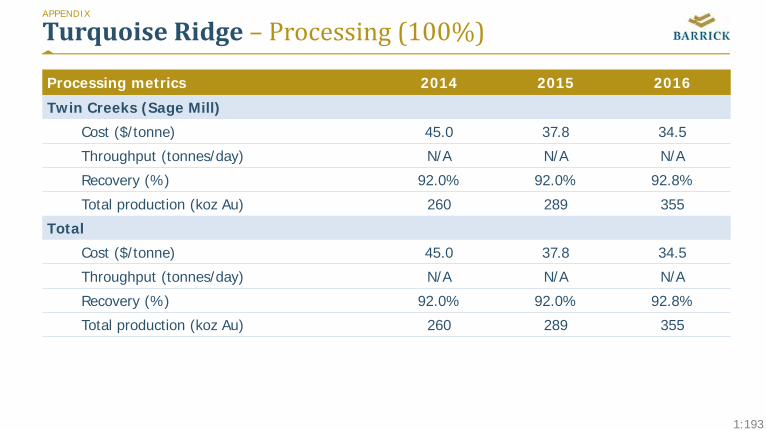

75% owned joint venture, underground mine using drift and fill mining method. Ore is processed through Newmont’s neighboring Twin Creeks facility.

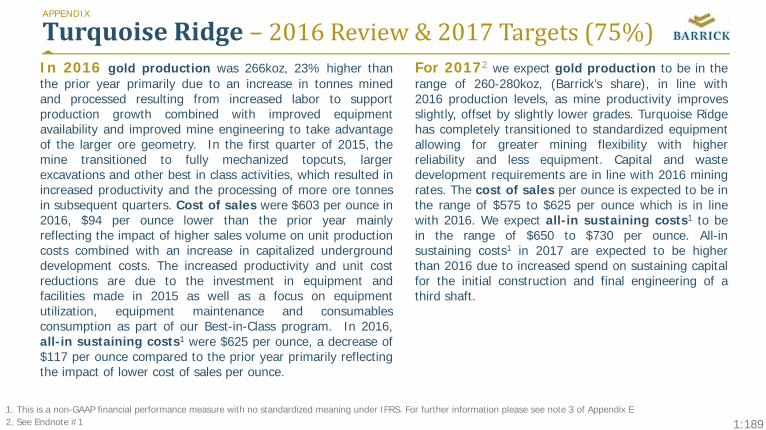

Achievements in 2016:– 2016 marks the doubling of production in five years at Turquoise Ridge– Winner of Nevada Mining Assoc. Safety Award for large underground mine– Record low mining cost– Record low AISC

Operations Technical Update Day | 68

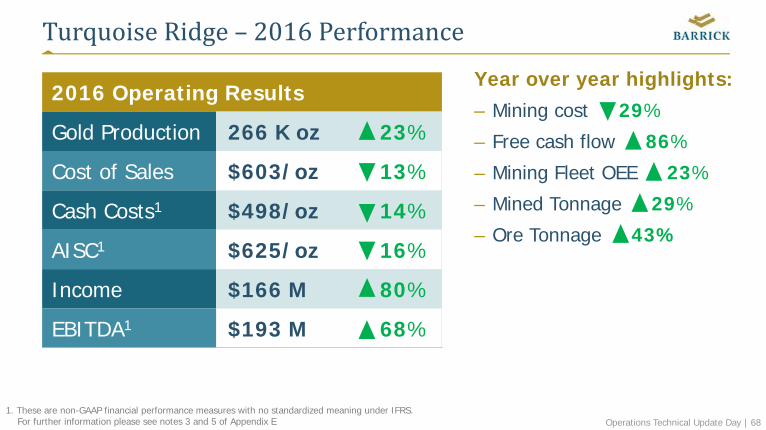

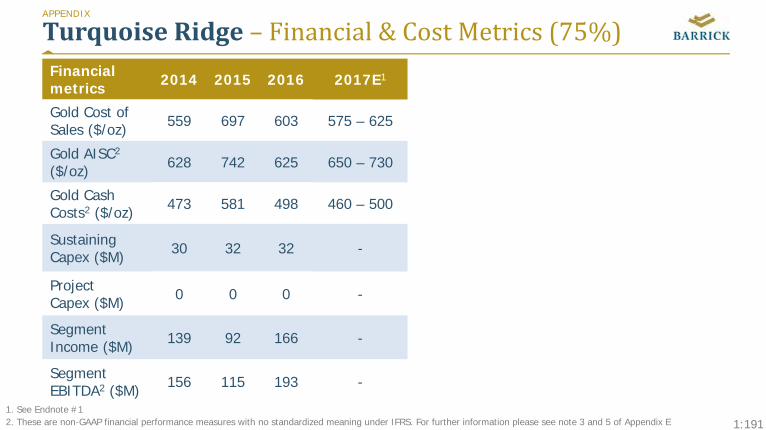

TurquoiseRidge– 2016Performance

Year over year highlights:– Mining cost 29%

– Free cash flow 86%

– Mining Fleet OEE 23%

– Mined Tonnage 29%

– Ore Tonnage 43%

2016 Operating Results

Gold Production 266 K oz 23%

Cost of Sales $603/oz 13%

Cash Costs1 $498/oz 14%

AISC1 $625/oz 16%

Income $166 M 80%

EBITDA1 $193 M 68%

1. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see notes 3 and 5 of Appendix E

Operations Technical Update Day | 69

Old FWD-2721Level Design

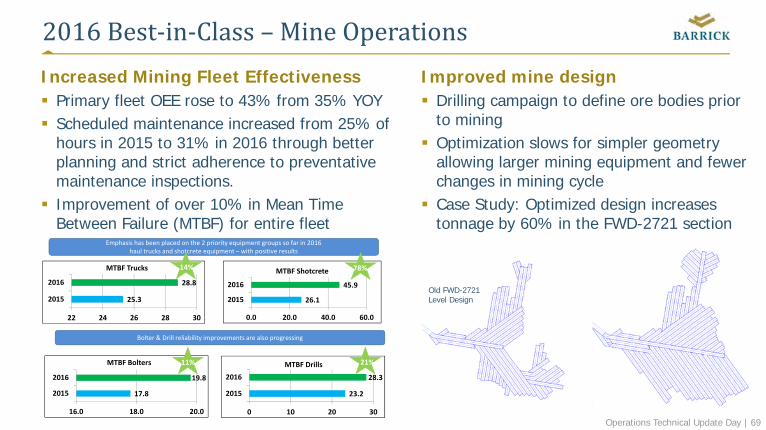

2016Best‐in‐Class– MineOperationsIncreased Mining Fleet Effectiveness Primary fleet OEE rose to 43% from 35% YOY Scheduled maintenance increased from 25% of

hours in 2015 to 31% in 2016 through better planning and strict adherence to preventative maintenance inspections.

Improvement of over 10% in Mean Time Between Failure (MTBF) for entire fleet

Improved mine design Drilling campaign to define ore bodies prior

to mining Optimization slows for simpler geometry

allowing larger mining equipment and fewer changes in mining cycle

Case Study: Optimized design increases tonnage by 60% in the FWD-2721 section

17.8

19.8

16.0 18.0 20.0

2015

2016

MTBF Bolters

23.2

28.3

0 10 20 30

2015

2016MTBF Drills

26.1

45.9

0.0 20.0 40.0 60.0

2015

2016

MTBF Shotcrete

25.3

28.8

22 24 26 28 30

2015

2016

MTBF Trucks

Bolter & Drill reliability improvements are also progressing

Emphasis has been placed on the 2 priority equipment groups so far in 2016haul trucks and shotcrete equipment – with positive results

78%

21%

14%

11%

Operations Technical Update Day | 70

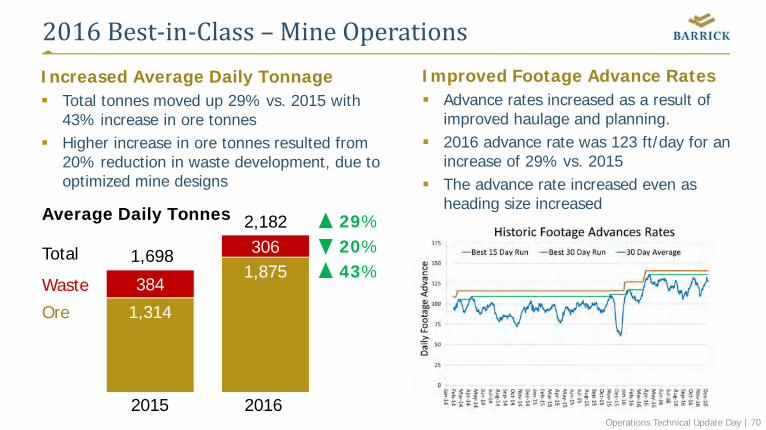

2016Best‐in‐Class– MineOperationsIncreased Average Daily Tonnage Total tonnes moved up 29% vs. 2015 with

43% increase in ore tonnes Higher increase in ore tonnes resulted from

20% reduction in waste development, due to optimized mine designs

Improved Footage Advance Rates Advance rates increased as a result of

improved haulage and planning. 2016 advance rate was 123 ft/day for an

increase of 29% vs. 2015 The advance rate increased even as

heading size increased

1,314

1,875384

3061,698

2,182

2015 2016

29%20%43%

Total

Waste

Ore

Average Daily Tonnes

Operations Technical Update Day | 71

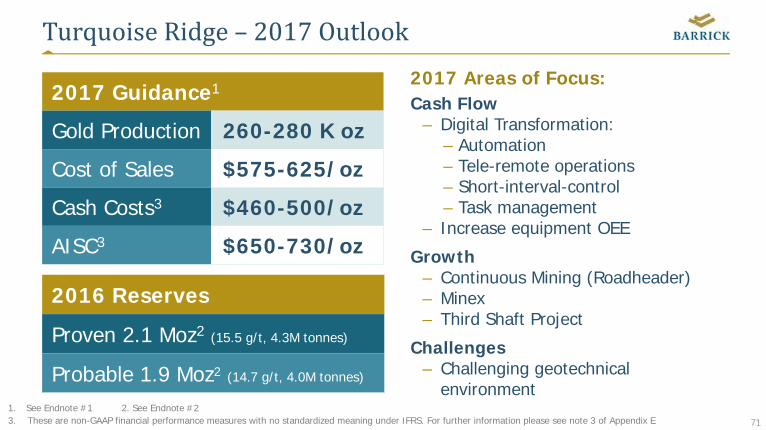

TurquoiseRidge– 2017Outlook2017 Areas of Focus:Cash Flow

– Digital Transformation: – Automation– Tele-remote operations– Short-interval-control– Task management

– Increase equipment OEE

Growth– Continuous Mining (Roadheader)– Minex– Third Shaft Project

Challenges– Challenging geotechnical

environment

2017 Guidance1

Gold Production 260-280 K oz

Cost of Sales $575-625/oz

Cash Costs3 $460-500/oz

AISC3 $650-730/oz

2016 Reserves

Proven 2.1 Moz2 (15.5 g/t, 4.3M tonnes)

Probable 1.9 Moz2 (14.7 g/t, 4.0M tonnes)

1. See Endnote #1 2. See Endnote #2 3. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations Technical Update Day | 72

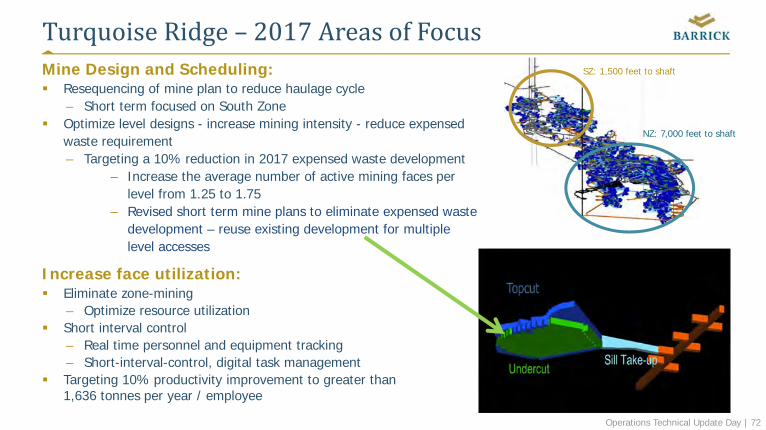

TurquoiseRidge– 2017AreasofFocusMine Design and Scheduling: Resequencing of mine plan to reduce haulage cycle

– Short term focused on South Zone Optimize level designs - increase mining intensity - reduce expensed

waste requirement– Targeting a 10% reduction in 2017 expensed waste development

– Increase the average number of active mining faces per level from 1.25 to 1.75

– Revised short term mine plans to eliminate expensed waste development – reuse existing development for multiple level accesses

Increase face utilization: Eliminate zone-mining

– Optimize resource utilization Short interval control

– Real time personnel and equipment tracking– Short-interval-control, digital task management

Targeting 10% productivity improvement to greater than 1,636 tonnes per year / employee

SZ: 1,500 feet to shaft

NZ: 7,000 feet to shaft

Operations Technical Update Day | 73

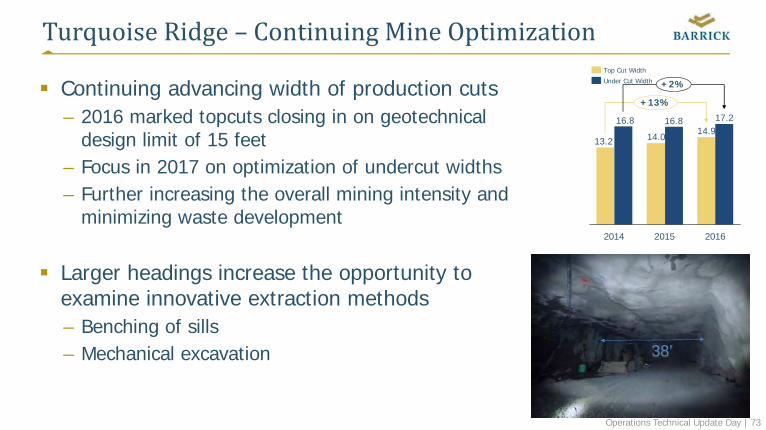

TurquoiseRidge– ContinuingMineOptimization

Continuing advancing width of production cuts– 2016 marked topcuts closing in on geotechnical

design limit of 15 feet– Focus in 2017 on optimization of undercut widths– Further increasing the overall mining intensity and

minimizing waste development

Larger headings increase the opportunity to examine innovative extraction methods– Benching of sills– Mechanical excavation

14.914.013.2

17.216.816.8

2014

+13%

2016

+2%

2015

Under Cut Width

Top Cut Width

38’

Operations Technical Update Day | 74

TurquoiseRidge– 20171stStageofContinuousMining

Commission a road header in ore production during the 4th Quarter– Initial component of a transition to

continuous mining operations– Reduction in ground support

costs of $10-20/tonne expected– Ventilation and electrical upgrades

in progress – Complete mining system and

support design in progress

Operations Technical Update Day | 75

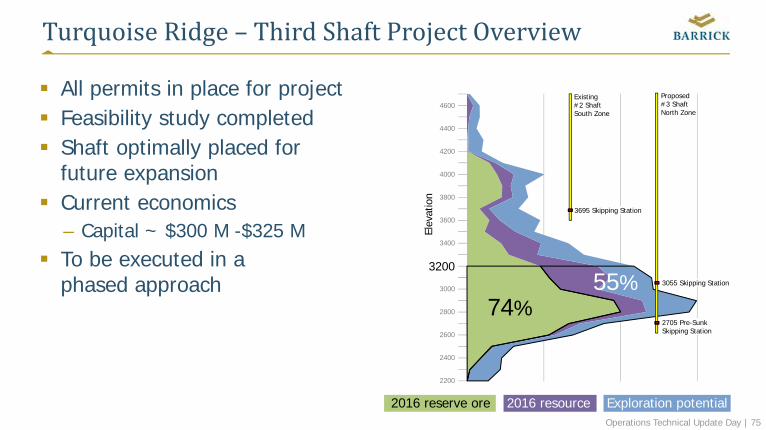

TurquoiseRidge– ThirdShaftProjectOverview

All permits in place for project Feasibility study completed Shaft optimally placed for

future expansion Current economics

– Capital ~ $300 M -$325 M To be executed in a

phased approach

2016 reserve ore 2016 resource Exploration potential

4600

4400

4200

4000

3800

3600

3400

3200

3000

2800

2600

2400

2200

74%55% 3055 Skipping Station

2705 Pre-Sunk Skipping Station

3695 Skipping Station

Existing#2 ShaftSouth Zone

Proposed #3 ShaftNorth Zone

Elev

atio

n

Operations Technical Update Day | 76

ShaftProjectScheduleandProjectedSpend

Preconstruction2017-2018• Site preparation and

utilities• Dewatering wells• Further mine optimization

studies

• ~$40 M

Shaft Sink2018-2022• Shaft sinking by

contractor• Underground capital

development by TRJV• ~$110 M

Shaft equipping2019-2021• Shaft Utilities• Hoist and headframe• ~$110 M

Surface facilities2020-2021• Mine offices and

change buildings• Final utilities• Surface ore handling

facilities• ~$30 M

Project Current Status Capex

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

Turquoise Ridge shaft

Feasibility complete,

optimisationongoing

$300M-$325M

Convert to Production Production Lifespan

Construct as Ventilation

Operations Technical Update Day | 77

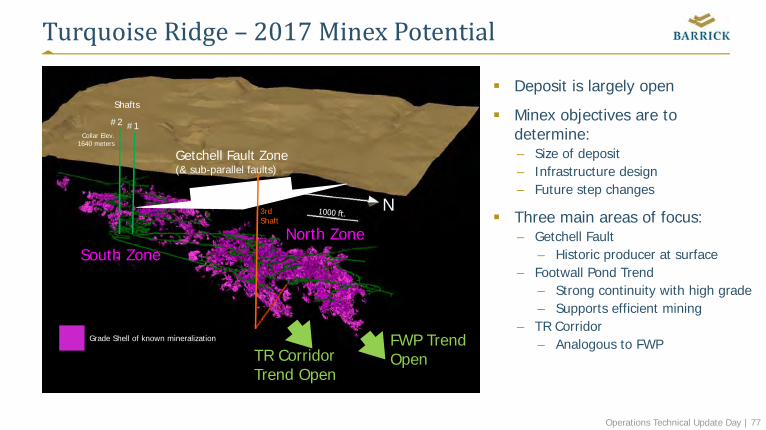

TurquoiseRidge– 2017Minex Potential

FWP TrendOpenTR Corridor

Trend Open

3rdShaft

N

Grade Shell of known mineralization

Shafts

#1#2

North ZoneSouth Zone

Collar Elev.1640 meters

Getchell Fault Zone(& sub-parallel faults)

Deposit is largely open

Minex objectives are to determine:– Size of deposit– Infrastructure design– Future step changes

Three main areas of focus: – Getchell Fault

– Historic producer at surface– Footwall Pond Trend

– Strong continuity with high grade – Supports efficient mining

– TR Corridor – Analogous to FWP

Operations Technical Update Day | 78

TurquoiseRidge‐ FutureGrowthPotentialNear Term Mine Exploration

– Expansion of the FWP– Development of the TR Corridor– Determine the potential for the Getchell Fault

Current Operations– Optimization of costs and cut off grades– Prove road header as primary mining machine

Life of Mine Third shaft

– Increase throughput– Decrease operating costs

Innovation– Examine new mining methods– Design the mine for success

Operations Technical Update Day | 79

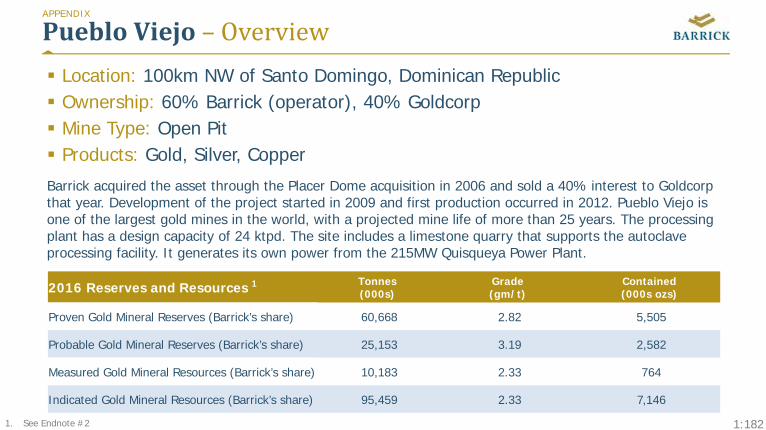

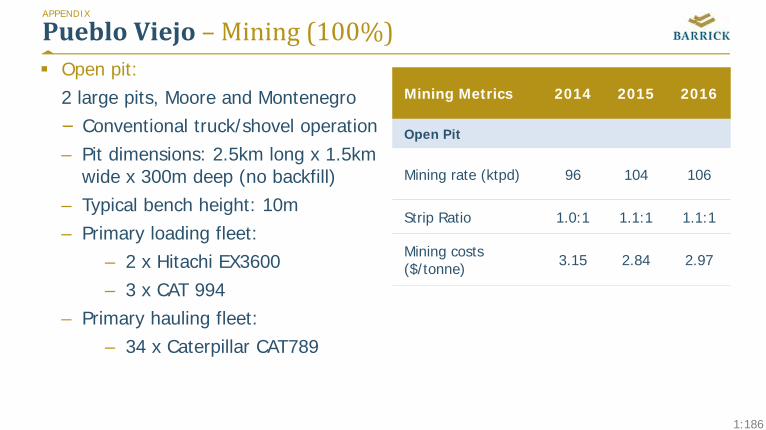

PuebloViejo– ImprovedPerformanceandGrowth

GregWalkerExecutiveGeneralManagerPuebloViejo,DominicanRepublic

Operations Technical Update Day | 80

PuebloViejo– Today

Vision is to grow and mature our business, focusing on developing our people and systems while growing our returns to stakeholders in a responsible way Open pit mining at two large pits, Moore and Montenegro and a satellite

pit, Monte Oculto Norte Conventional truck and shovel operation, the processing is via autoclave,

carbon in leach (CIL) and Copper Precipitation Achievements in 2016:

– Winner of Barrick’s “Most Improved Safety Performance”– Gained contract to close the Dominion Republic government’s old Mejita

tailings dam– Implemented business improvement program and employee development

center

Operations Technical Update Day | 81

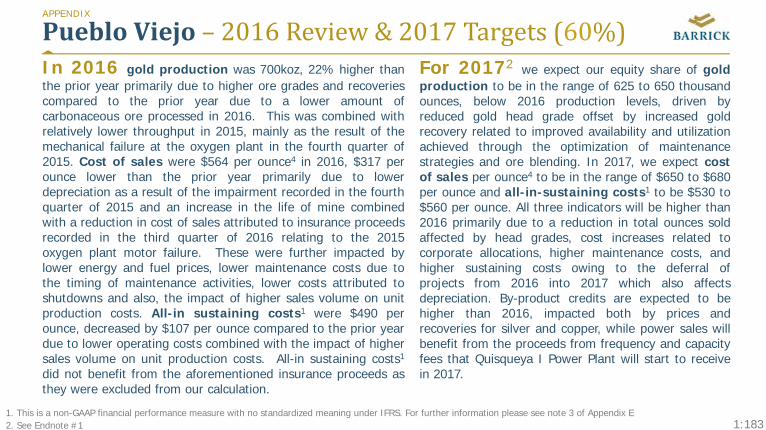

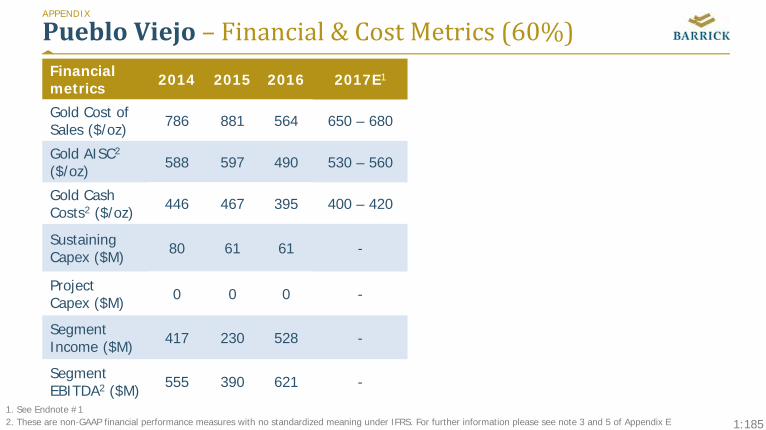

PuebloViejo– 2016Performance

Year over year highlights:– Gold recovery 4%

– Silver recovery 30%

– Autoclave OEE 7%

– Truck OEE 4%

– Shovel OEE 2%

– Total Reportable Injury Frequency rate2 25%

2016 Operating Results (60%)

Gold Production 700 K oz 22%

Cost of Sales $564/oz 36%

Cash Costs1 $395/oz 15%

AISC1 $490/oz 18%

Silver Production 3,385 K oz 36%

Income $528 M 130%

EBITDA1 $621 M 59%

1. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see notes 3 and 5 of Appendix E 2. See endnote #5

Operations Technical Update Day | 82

PuebloViejo– 2016Best‐in‐ClassImprovements

Mine Operations InitiativesOre Re-Binning Optimization Changed sulfur cut-off to increase gold grade

in mill feed ~14k oz Au

Improve Pre-split to Steepen Walls Reduce stripping and advance high grade ore

~9k oz Au

Mine Plan Sequence Optimization Change design to reduce stripping and

advance high grade ore ~23k oz Au

Reduce Drilling & Blasting Costs Increased hole diameter to reduce meters

drilled requirement and increase drilling meter efficiency

Process Plant InitiativesExtend Time Between Shutdowns More durable walls to improve AC performance

and reduce maintenance time and costs, in addition increasing throughput by ~100k tonnes

Anti-scalant in CIL Feed Line and Installation of Redundant CIL Feed Line An anti-scalant prevents scale formation and

the redundant feed line reduces descaling impact in production resulting in an additional ~25k tonnes processed due to a reduction in downtime.

Improved Grinding Circuit Availability Extended time between shutdowns and

improved efficiency to increase grinding circuit availability from 88% to 91%

Operations Technical Update Day | 83

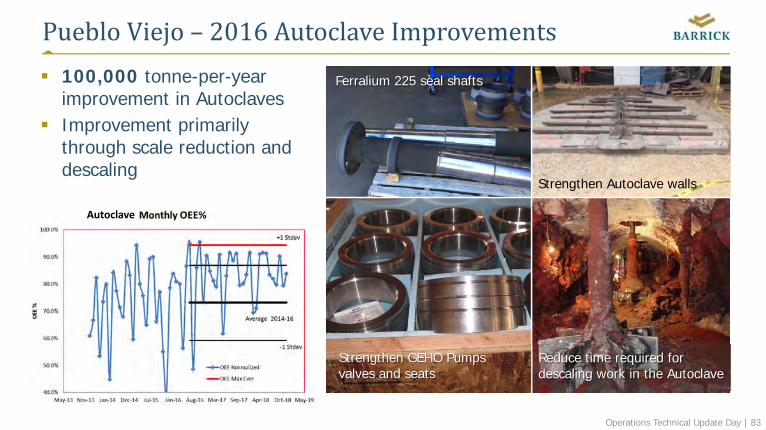

PuebloViejo– 2016AutoclaveImprovements 100,000 tonne-per-year

improvement in Autoclaves Improvement primarily

through scale reduction and descaling

Strengthen Autoclave walls

Ferralium 225 seal shafts

Strengthen GEHO Pumps valves and seats

Reduce time required for descaling work in the Autoclave

KPI improvement metrics to come

Autoclave

Operations Technical Update Day | 84

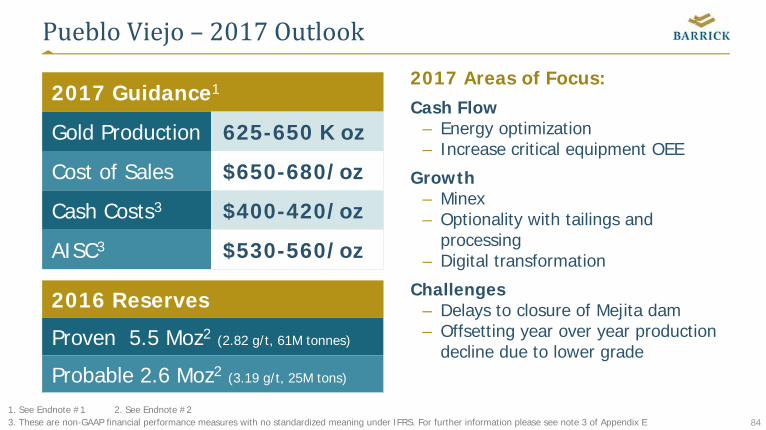

PuebloViejo– 2017Outlook2017 Areas of Focus:Cash Flow

– Energy optimization– Increase critical equipment OEE

Growth– Minex– Optionality with tailings and

processing– Digital transformation

Challenges– Delays to closure of Mejita dam– Offsetting year over year production

decline due to lower grade

2017 Guidance1

Gold Production 625-650 K oz

Cost of Sales $650-680/oz

Cash Costs3 $400-420/oz

AISC3 $530-560/oz

2016 Reserves

Proven 5.5 Moz2 (2.82 g/t, 61M tonnes)

Probable 2.6 Moz2 (3.19 g/t, 25M tons)

1. See Endnote #1 2. See Endnote #23. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations Technical Update Day | 85

PuebloViejo– 2017AreasofFocusEnergy Expansion and Optimization: Sell excess 80M watt capacity from Quisqueya 1 (QQ1)

power plant to the grid– Grid connection at San Pedro– New Bonao sub-station connection

Increased demand in the DR power market enhances project benefits

Convert QQ1 Power Plant from HFO to LNG or Bio Fuel Convert lime kilns from diesel to natural gas or Bio Fuel

AISC and free cash flow improvements: Develop supervision and workforce to reduce

contractors and optimize labor costs Improved maintenance materials and reliability

Critical Overall Equipment Effectiveness: Further autoclave and grinding optimization Increase truck and shovel availability from 81% to 85%

Quisqueya 1 Power Plant

Pueblo Viejo lime kilns

Operations Technical Update Day | 86

PuebloViejo– GrowthPlan:Minex

2017 Minex Targets:1. Monte Negro Feeder

2. PV Underground high grade pods testing (1, 2 & 3)

3. Upper Mejita

4. low sulphur ore near surface

1 2

3

1.2.

3.

Operations Technical Update Day | 87

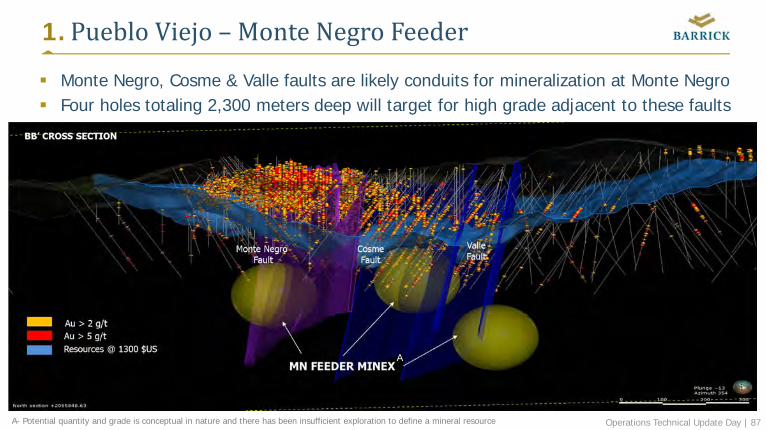

1.PuebloViejo– MonteNegroFeeder

Monte Negro, Cosme & Valle faults are likely conduits for mineralization at Monte Negro Four holes totaling 2,300 meters deep will target for high grade adjacent to these faults

A- Potential quantity and grade is conceptual in nature and there has been insufficient exploration to define a mineral resource

A

Operations Technical Update Day | 88

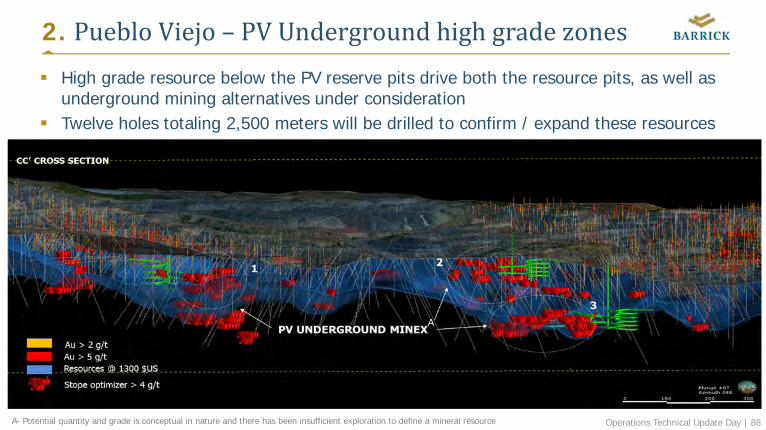

2. PuebloViejo– PVUndergroundhighgradezones High grade resource below the PV reserve pits drive both the resource pits, as well as

underground mining alternatives under consideration Twelve holes totaling 2,500 meters will be drilled to confirm / expand these resources

A

A- Potential quantity and grade is conceptual in nature and there has been insufficient exploration to define a mineral resource

Operations Technical Update Day | 89

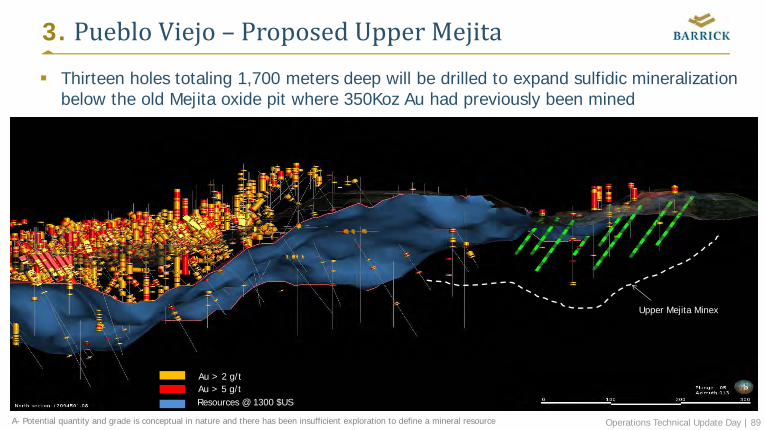

Upper Mejita Minex

3. PuebloViejo– ProposedUpperMejita Thirteen holes totaling 1,700 meters deep will be drilled to expand sulfidic mineralization

below the old Mejita oxide pit where 350Koz Au had previously been mined

Au > 2 g/tAu > 5 g/tResources @ 1300 $US

A- Potential quantity and grade is conceptual in nature and there has been insufficient exploration to define a mineral resource

Operations Technical Update Day | 90

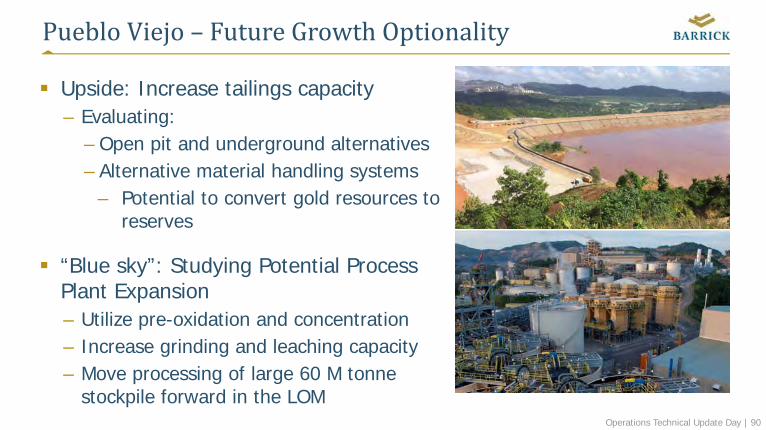

PuebloViejo– FutureGrowthOptionality

Upside: Increase tailings capacity– Evaluating:

– Open pit and underground alternatives– Alternative material handling systems

– Potential to convert gold resources to reserves

“Blue sky”: Studying Potential Process Plant Expansion– Utilize pre-oxidation and concentration– Increase grinding and leaching capacity– Move processing of large 60 M tonne

stockpile forward in the LOM

Operations Technical Update Day | 91

PuebloViejo– ImprovedPerformanceandGrowth

Continue to focus on operational excellence

Leverage off the digital initiatives generated at Cortez

Maximize benefit available through improved energy management

Target additional high grade ore and explore underground potential

Unlock the low grade mineral inventory

Operations and Technical Update | 92

Veladero– InvestinginFutureGrowth

JorgePalmesExecutiveGeneralManagerVeladero,Argentina

Operations and Technical Update | 93

Veladero – Today

Vision – Responsible leaders, trusted partners, safety champions

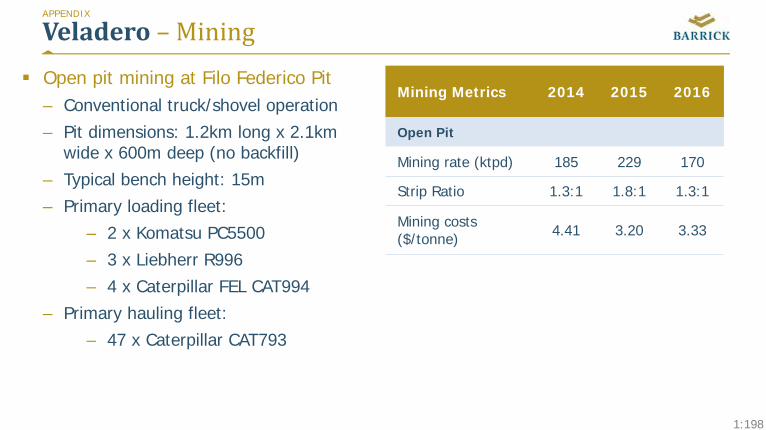

Conventional open pit valley heap leach using the Merrill Crowe process for gold and silver recovery

Achievements in 2016:– Appointed new executive team with significant

in-country experience to unlock value– Strong safety record (TRIFR1 0.28)– Rapid recovery in operating performance

following weather challenges and mine suspension

1. See endnote #5

Operations and Technical Update | 94

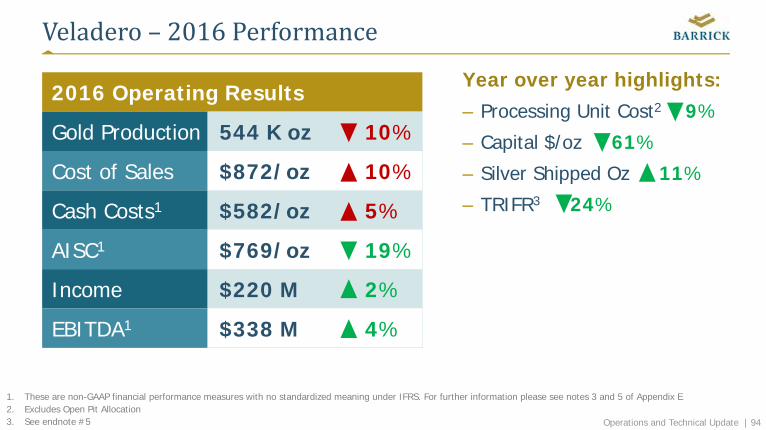

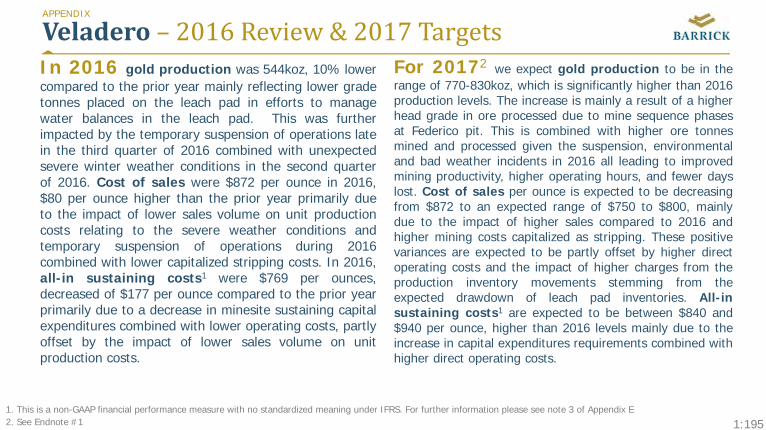

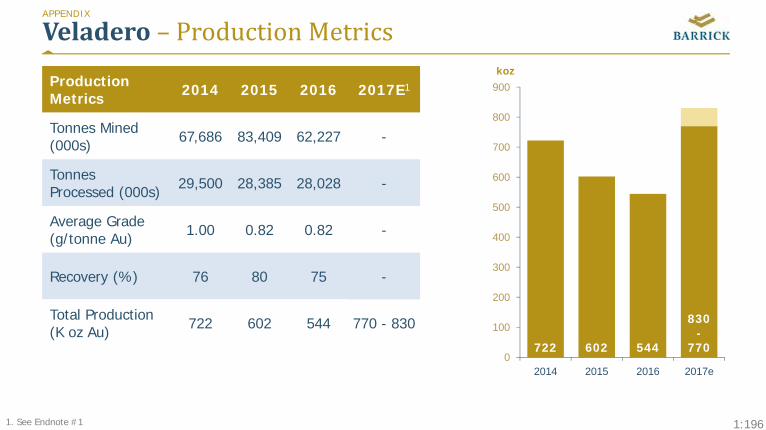

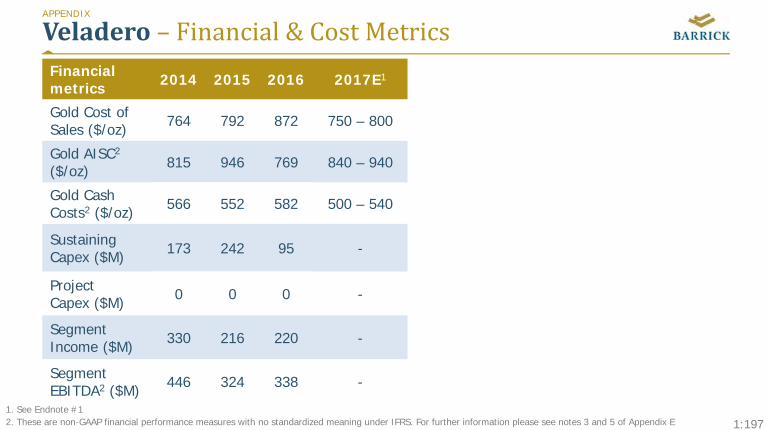

Veladero– 2016Performance

2016 Operating Results

Gold Production 544 K oz 10%

Cost of Sales $872/oz 10%

Cash Costs1 $582/oz 5%

AISC1 $769/oz 19%

Income $220 M 2%

EBITDA1 $338 M 4%

Year over year highlights:– Processing Unit Cost2 9%

– Capital $/oz 61%

– Silver Shipped Oz 11%

– TRIFR3 24%

1. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see notes 3 and 5 of Appendix E 2. Excludes Open Pit Allocation3. See endnote #5

Operations and Technical Update | 95

Veladero– NewBusinessConfidence

1. Mid-December 2015 AR$/US$ 9.8 to currently $AR/$US 15.7

EconomicMeasures

Elimination of Export Duties Removing Currency Controls Business friendlytax reform

Impact on Business

Improved FCF Increasing reserves

Lower operating cost Improved CF and

increasing reserves

Lowering tax burden Increasing FCF

What has Changed

Export duties repealed for most products including doré

FX Deregulation Elimination of most de-

facto restrictions Allowing peso to float

Repealed: Tax on dividends (10%) Personal Asset Tax Minimum Presumed Income

Tax

Impact on Economy

Incentivizing economic development, production and increasing exports

>50%1 depreciation ARS Inflow of US$ Increased BCRA reserves

Increase competitiveness Incentivize investment and

economic development Argentina FDI interest

Operations and Technical Update | 96

Veladero– 2016Best‐in‐ClassInitiatives

Operations Initiatives Enhanced water management

system - Construction and improvement of water diversion system and construction of ponds to manage record snow fall and melt

Reduced blasting costs by optimizing ANFO mix - 10% savings in blasting costs

Decreased hauling cycle time by increasing road width – 15%reduction of cycle time on major routes

Operations and Technical Update | 97

Veladero– 2016Best‐in‐ClassInitiatives

Operations Initiatives Reduced Maintenance Repair

Operation spend through supplier optimization - $10 M in operating cost savings

Improved maintenance practices - 66% reduction of complete engine failures

Implementation of Drone technology – Unmanned Aerial Vehicles for site monitoring and rapid data acquisition

Operations and Technical Update | 98

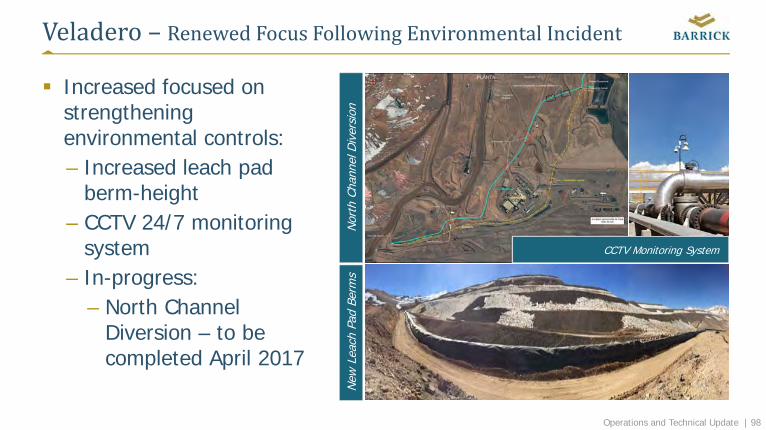

Veladero – RenewedFocusFollowingEnvironmentalIncident

Increased focused on strengthening environmental controls:– Increased leach pad

berm-height – CCTV 24/7 monitoring

system– In-progress:

– North Channel Diversion – to be completed April 2017

New

Lea

ch P

ad B

erm

sN

orth

Cha

nnel

Div

ersi

on

CCTV Monitoring System

Operations and Technical Update | 99

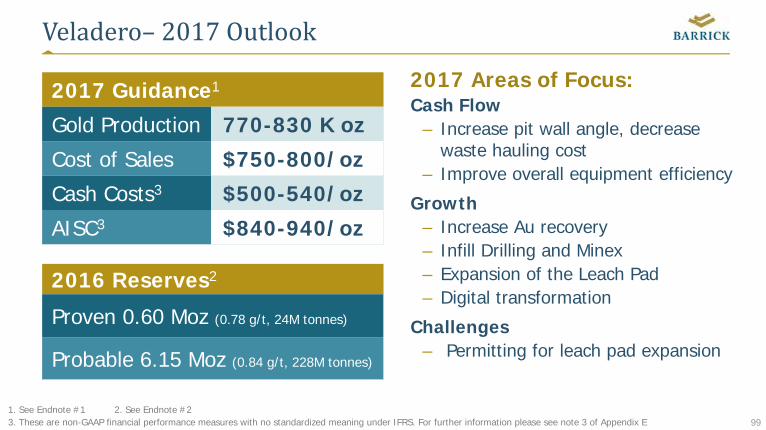

Veladero– 2017Outlook

2017 Areas of Focus:Cash Flow

– Increase pit wall angle, decrease waste hauling cost

– Improve overall equipment efficiency

Growth– Increase Au recovery– Infill Drilling and Minex– Expansion of the Leach Pad– Digital transformation

Challenges– Permitting for leach pad expansion

2017 Guidance1

Gold Production 770-830 K oz

Cost of Sales $750-800/oz

Cash Costs3 $500-540/oz

AISC3 $840-940/oz

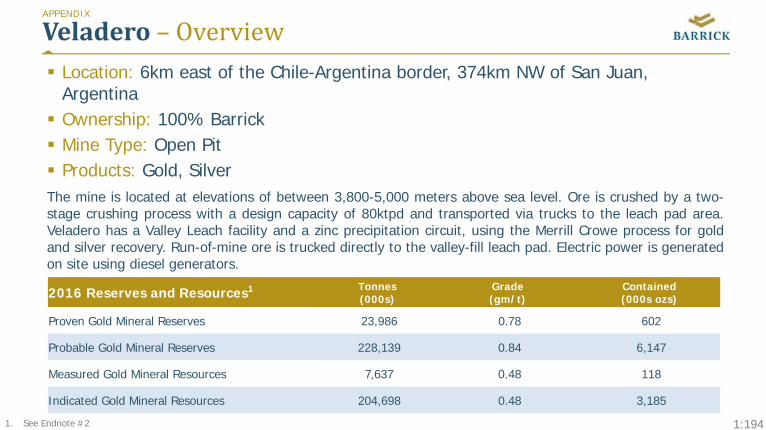

2016 Reserves2

Proven 0.60 Moz (0.78 g/t, 24M tonnes)

Probable 6.15 Moz (0.84 g/t, 228M tonnes)

1. See Endnote #1 2. See Endnote #23. These are non-GAAP financial performance measures with no standardized meaning under IFRS. For further information please see note 3 of Appendix E

Operations and Technical Update | 100

Veladero– 2017AreasofFocusIncrease pit wall angle: Increase angle 4% to 54o

Improve overall equipment efficiency: Implement comprehensive portfolio of initiatives

Increase Au recovery: Increase recovery by 3% through operational

improvements

Reduce external spend: Continue spend reduction effort (e.g. explosives,

logistics, service contracts)

Digital initiative example: UAV drone technology for maintenance Integrated Remote Operations Centre

Environmental Focus: Enhanced site water management

Operations and Technical Update | 101

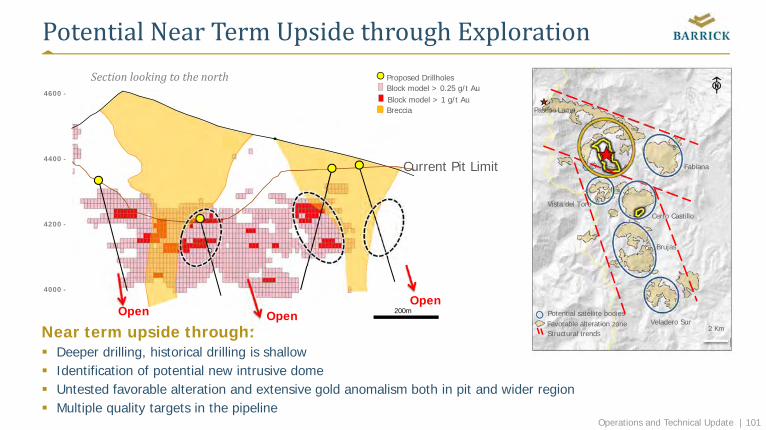

PotentialNearTermUpsidethroughExploration

Near term upside through: Deeper drilling, historical drilling is shallow Identification of potential new intrusive dome Untested favorable alteration and extensive gold anomalism both in pit and wider region Multiple quality targets in the pipeline

2 KmFavorable alteration zonePotential satellite bodies

Structural trends

Pascua Lama

Vista del Toro

Brujas

Cerro Castillo

Veladero Sur

Fabiana

4000 -

200m

4200 -

SectionlookingtothenorthBlock model > 0.25 g/t AuProposed Drillholes

Breccia

4600 -

4400 -Current Pit Limit

Block model > 1 g/t Au

OpenOpen Open

Operations and Technical Update | 102

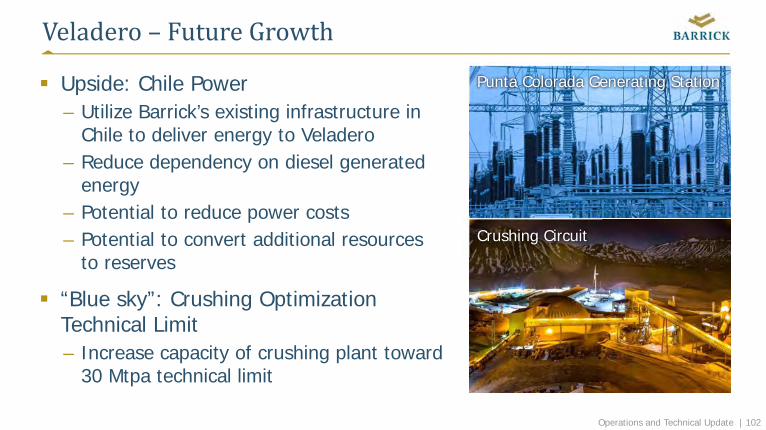

Veladero– FutureGrowth

Upside: Chile Power– Utilize Barrick’s existing infrastructure in

Chile to deliver energy to Veladero– Reduce dependency on diesel generated

energy– Potential to reduce power costs – Potential to convert additional resources

to reserves

“Blue sky”: Crushing Optimization Technical Limit– Increase capacity of crushing plant toward

30 Mtpa technical limit

Punta Colorada Generating Station

Crushing Circuit

Operations and Technical Update | 103

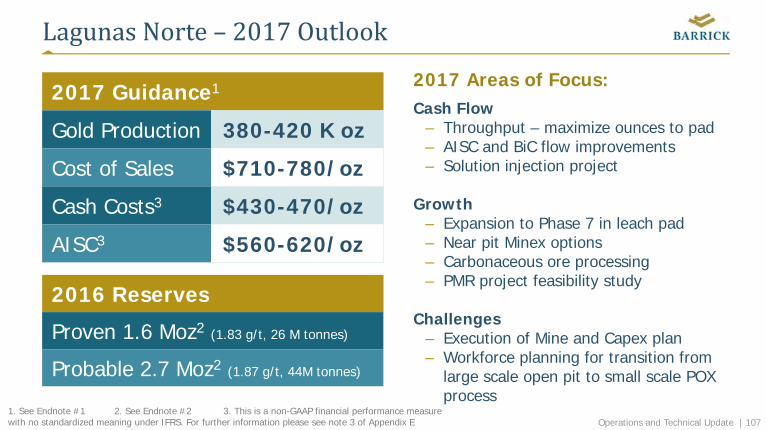

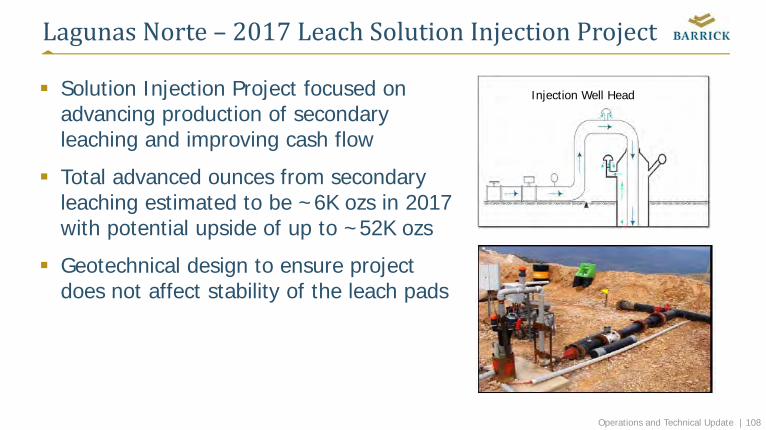

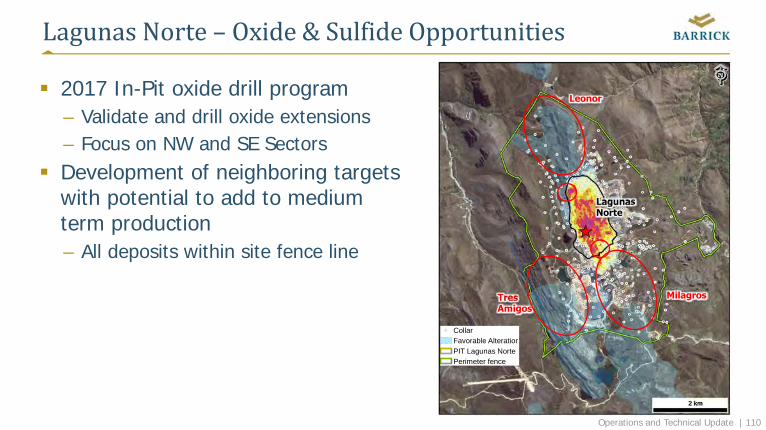

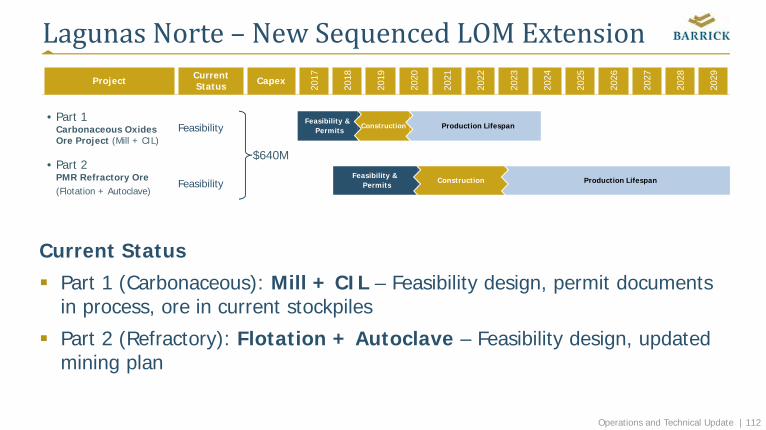

LagunasNorte– PreparingfortheFuture

JimWhittakerGeneralManagerLagunasNorte,Peru

Operations and Technical Update | 104

LagunasNorte– Today

Vision: We are a company dedicated to the sociably responsible extraction and production of gold, being a key influence for development in the region, reaching for the highest standards of safety and environmental protection, maintaining the efficiency and continuous improvement of our processes, with a commitment to the development of our employees Conventional open‐pit, crush, valley‐fill heap leach operation, two‐stage

conventional crushing circuit, heap leach, Merrill Crowe or Carbon-in-column (CIC) precipitation plants

Achievements in 2016:– Safety incident frequency has decreased for the first time in 5 years– On target production and under target AISC– Successful negotiation of unionized labor contracts– Prioritized resource portfolio to extend current mine life– Refractory ore PMR expansion project Feasibility Study phase 1 completed

Operations and Technical Update | 105

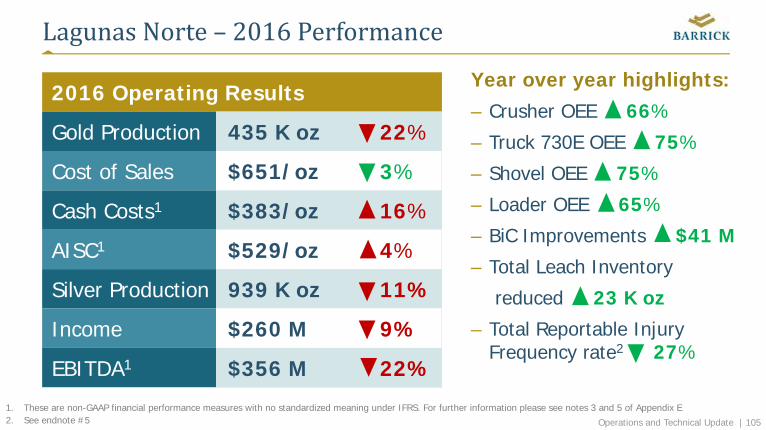

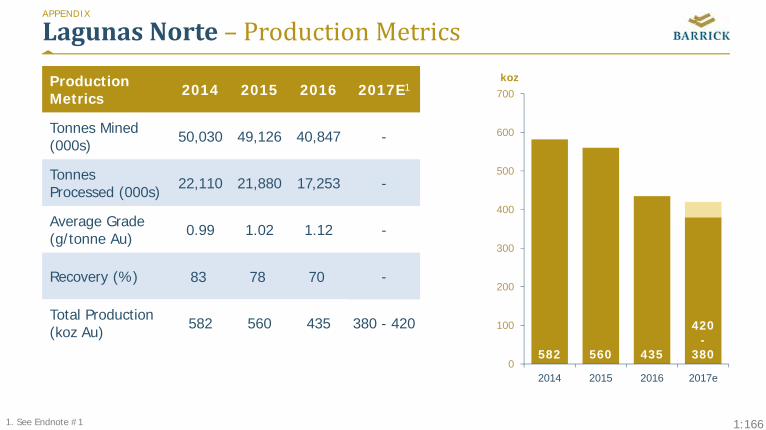

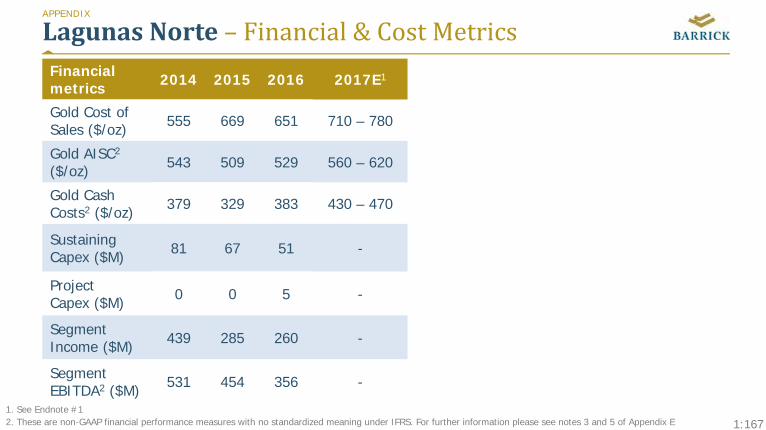

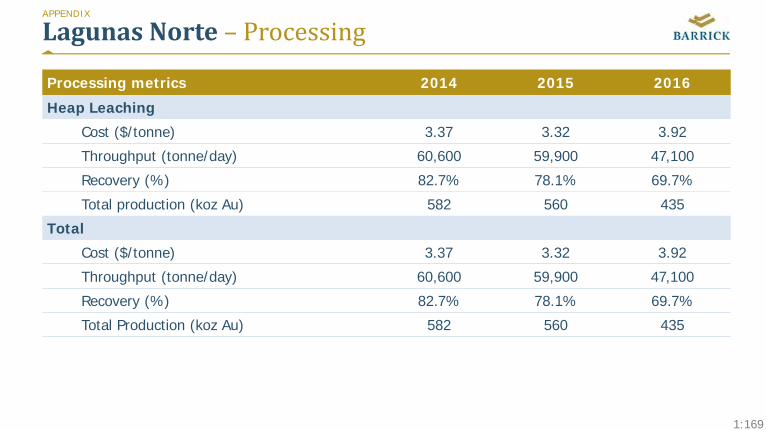

LagunasNorte– 2016Performance

Year over year highlights:– Crusher OEE 66%

– Truck 730E OEE 75%

– Shovel OEE 75%

– Loader OEE 65%

– BiC Improvements $41 M

– Total Leach Inventory

reduced 23 K oz

– Total Reportable Injury Frequency rate2 27%

2016 Operating Results

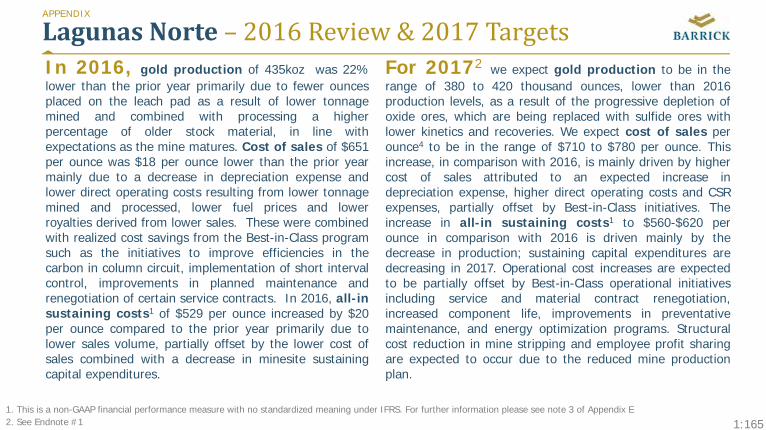

Gold Production 435 K oz 22%

Cost of Sales $651/oz 3%

Cash Costs1 $383/oz 16%

AISC1 $529/oz 4%

Silver Production 939 K oz 11%

Income $260 M 9%

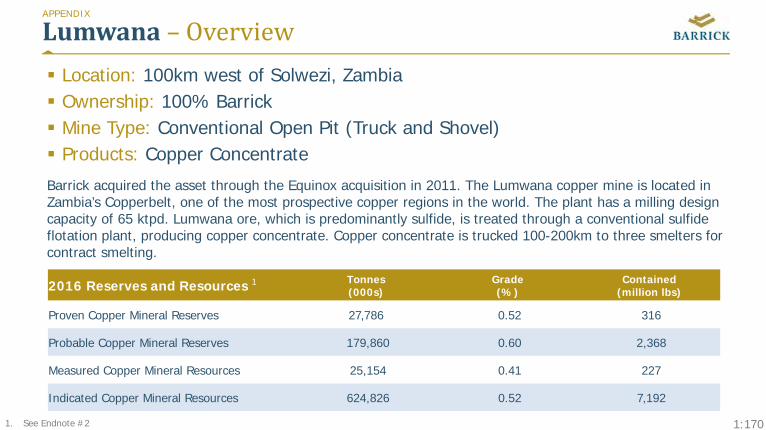

EBITDA1 $356 M 22%