OPEC Oil Market Outlook - International Energy Forum (IEF) · OPEC Oil Market Outlook Prepared by...

26

8 th IEA-IEF-OPEC Symposium on Energy Outlooks IEF Secretariat, Riyadh 14th February 2018 OPEC Oil Market Outlook Prepared by OPEC Secretariat

Transcript of OPEC Oil Market Outlook - International Energy Forum (IEF) · OPEC Oil Market Outlook Prepared by...

8th IEA-IEF-OPECSymposiumonEnergyOutlooksIEFSecretariat,Riyadh14thFebruary2018

OPECOilMarketOutlook

Prepared by OPEC Secretariat

2©2018OrganizationofthePetroleumExportingCountries

Disclaimer

2

“The data, analysis and any other information ('Content') contained in this presentation is for informational purposes and isintended solely for the use of the person(s) to whom it is addressed and may be legally privileged and/or confidential. Anyunauthorized use, disclosure or copying of this Presentation or any parts of it or its attachment(s) by any unintended recipientis strictly prohibited. If you have received this Presentation in error, please immediately return or destroy it. The Content ofthis Presentation is not intended as a substitute for advice from your business, finance, investment consultant or otherprofessional. Whilst reasonable efforts have been made to ensure the accuracy of the Content of this Presentation, the OPECSecretariat makes no warranties or representations as to its accuracy, currency or comprehensiveness and assumes noliability or responsibility for any error or omission and/or for any loss arising in connection with or attributable to any actionor decision taken as a result of using or relying on the Content of this Presentation. Nothing in this Presentation shall beconstrued as interpreting or modifying any legal obligations under any agreement, treaty, law or other texts; or expressingany legal opinions or having probative legal value in any proceedings. This Presentation may contain references tomaterial(s) from third parties whose copyright must be acknowledged by obtaining necessary authorization from thecopyright owner(s). The OPEC Secretariat will not be liable or responsible for any unauthorized use of third party material(s).The views expressed in this Presentation are those of the OPEC Secretariat and do not necessarily reflect the views ofindividual OPEC Member Countries. The material contained in this Presentation may not be used and/or reproduced for anypurposes without prior written permission from the OPEC Secretariat”.

© 2018 Organization of the Petroleum Exporting Countries

Outline

3

● Short-term Market Outlook– Review of the oil market 2014-2016– Declaration of Cooperation– Projection for the oil market in 2018– Supply/demand balance in 2018– Concluding remarks

● Medium to Long-term Market Outlook– Key assumptions– Energy outlook– Oil outlook– Key takeaways

© 2018 Organization of the Petroleum Exporting Countries

World oil supply growth outpaced oil demand growth during 2014-2016, y-o-y change, mb/d

From2014to2016,worldsupplygrewby5.5mb/d,whilewordoildemandincreasedby4.1mb/d.

0.92

-0.16

0.18

2.29

1.90

1.20

0.11

1.53

1.30

0.97

0.11

-0.71

-2 -1 0 1 2 3 4 5

World demand

OPEC crude

OPEC NGLs

Non-OPEC production 3.1 mb/d

2014 2015 2016

2.0mb/d

0.4 mb/d

4.1 mb/d

5.5mb/d

Source:OPECSecretariat. 4

© 2018 Organization of the Petroleum Exporting Countries

Rise in OECD commercial inventories, mb

2,562

2,706

2,989 2,985

2,888

2,500

2,600

2,700

2,800

2,900

3,000

3,100

2013 2014 2015 2016 2017

427mb

OECDcommercialinventoriesattheendoftheyear

8 mb

386 mb

109 mb

0

100

200

300

400

500

Oct

14

Dec

14Fe

b 15

Apr 1

5Ju

n 15

Aug

15O

ct 1

5De

c 15

Feb

16Ap

r 16

Jun

16Au

g 16

Oct

16

Dec

16Fe

b 17

Apr 1

7Ju

n 17

Aug

17O

ct 1

7De

c 17

Difference to 5-year average

Source:OPECSecretariat.

5

© 2018 Organization of the Petroleum Exporting Countries

OPEC landmark decisions in 2016

Algiers Accord

• 170th(Extraordinary)MeetingoftheConference–28September2016;Algiers

Vienna Decision• 171stMeetingoftheConference–30November2016;Vienna

• Adjustmentof1.2mb/dfromOPEC-11countries

Joint Declaration of Cooperation

• OPECandnon-OPECMinisterialMeeting–10December2016;Vienna

• Adjustmentof0.6mb/dfrom11non-OPECparticipatingcountries

6

© 2018 Organization of the Petroleum Exporting Countries

Drop in OECD commercial oil stock since Declaration of Cooperation by component and region

7Sources:Euroilstock,IEA,METI,OPECSecretariatandUSEIA.

221100

119

8

339

109

0100200300

Jan 17 Dec 17

Crude Products Total

By component-231mb

23574

17

16

87

19

339

109

0100200300

Jan 17 Dec 17

Americas Asia Pacific Europe OECD Total

By region-231 mb

129%

0%

20%

40%

60%

80%

100%

120%

140%

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

Percentage conformity

Yearly average 107%

© 2018 Organization of the Petroleum Exporting Countries Sources:CFTC,CMEGroup,IntercontinentalExchangeandOPECSecretariat.

Crude oil prices improvedDriven by a sizeable stocks draw as well as signs of bullish market sentiment

8

40

50

60

70

80

1FM 6FM 11FM 16FM

US$/b ICEBrentforwardcurve

Current

Ayearago

6monthsago

45.84

67.62

253545556575

Jan-16

Mar-16

May-16

Jul-1

6

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-1

7

Sep-17

Nov-17

Jan-18

US$/b ICEBrent

921 1,074

-600-300

0300600900

1,2001,500

Jan-16

Mar-16

May-16

Jul-1

6

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-1

7

Sep-17

Nov-17

Jan-18

‘000contracts Combinednetlongpositions(ICEBrent&NYMEXWTI)

Long

Short

Net

1.84

14.16

0

5

10

15

Jan-16

Mar-16

May-16

Jul-1

6

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-1

7

Sep-17

Nov-17

Jan-18

Ratio Ratiototallong/short

© 2018 Organization of the Petroleum Exporting Countries

PerformanceoftheworldeconomyGDPchangefromthepreviousyear,%

9

Note:*2018=Forecast.Sources:OPECSecretariat,IMF,Markit andHaver Analytics.

2.9

6.57.2

1.81.9

4.9

1.62.2

2.72.4

3.8

2.5

6.96.5

1.91.0

4.8

1.82.5

2.32.5

3.8

-5.0 -2.0 1.0 4.0 7.0 10.0

OPEC

ChinaIndia

RussiaBrazil

Non-OECD

JapanEuro-zone

USOECD

World

2017 2018*

GDPgrowthinselectedcountries

© 2018 Organization of the Petroleum Exporting Countries

Oil demand growth remains healthy in 2017-2018,while non-OPEC supply recovers during the same period

1.60 1.59

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2014 2015 2016 2017 2018*

Non-OECD OECD World

WorldoildemandgrowthY-o-ychange,mb/d

Note:*2018=Forecast.

Source:OPECSecretariat. 10

0.86

1.40

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015 2016 2017 2018*

US Canada Othernon-OPEC Total

Non-OPECsupplygrowthY-o-ychange,mb/d

© 2018 Organization of the Petroleum Exporting Countries

Medium- and Long-term outlook

11

●–––––

● Medium- and Long-term Market Outlook– Key assumptions– Energy outlook– Oil outlook– Key takeaways

©2018OrganizationofthePetroleumExportingCountries

Theworldisexperiencinganeraofdemographicchange

● Global population to increase by 1.8 billion, reaching almost 9.2 billion in 2040

● India to become the most populated country in the early 2020s and population in China peaks in 2028

● Population growth in OECDsupported by migration

● Population growth will decelerate

Population by region (millions)

12

0.0

0.4

0.8

1.2

1.6

2.0

0

2,000

4,000

6,000

8,000

10,000

2015 2020 2025 2030 2035 2040

%millionNon-OECD OECDOECDannualgrowth Non-OECDannualgrowth

©2018OrganizationofthePetroleumExportingCountries

Economicgrowthinthelong-term

● Long-term global GDP growth estimated at an average rate of 3.5% p.a.

● Long-term economic growth will be driven by Developing Countries, with growth in the OECD constrained by weaker demographics

● The size of the global economy in 2040 is estimated to be 126% that of 2016

● The Reference Case assumes an evolutionary development of technology and energy policy in the long-term

Long-term real GDP growth rates (%, 2011 PPP)

13

©2018OrganizationofthePetroleumExportingCountries

Globalprimaryenergydemandwillincreaseby35%

14

World primary energy demand by fuel type

+35%

● Energy demand increases by 96 mboed and oil remains dominant

● Gas contributes most to future demand growth and coal peaks

● Renewables record the fastestgrowth rate (6.8%)

©2018OrganizationofthePetroleumExportingCountries

Energydemandwillbedrivenbynon-OECDcountries

15

● Energy demand increases by 96 mboed and oil remains dominant

● Gas contributes most to future demand growth and coal peaks

● Renewables record the fastest growth rate (6.8%)

● Growth is concentrated in non-OECD countries

● India & China are the two largest contributors to demand growth

Growth in primary energy demand by region & Fuel, 2015–2040

©2018OrganizationofthePetroleumExportingCountries

Oildemandinthelong-term

● In long term, global oil demandwill increase by 15.8 mb/d, reaching 111.1 mb/d by 2040

● The transportation sector will remain the main consumer of oil

● Strong growth is also foreseen in the petrochemicals sector

● Demand growth decelerates over the long-term

World oil demand by sector

16

©2018OrganizationofthePetroleumExportingCountries

Total liquids supply, 2016-2040

17

● Non-OPEC liquids supply peaks at close to 64 mb/d in 2025-2030

● In the long-term, non-OPEC liquids modestly decline to 60.4 mb/d by 2040

● US tight oil is the most important contributor to non-OPEC supply, but peaks after 2025

● Demand for OPEC crude risessteadily after 2025 to reach 41.4 mb/d by 2040

Liquidssupplyinthelong-term

©2018OrganizationofthePetroleumExportingCountries

ThemajorityofnewrefiningcapacityexpansionlocatedinDevelopingcountries

● Total capacity additions until 2040 estimated at 19.6 mb/d

● The majority of new refining capacity expansion located in Developing countries, driven by rising oil demand

● Expansion led by Asia-Pacific and the Middle East accounting for almost 70% of the total

Crude distillation capacity additions,2017–2040

18

©2018OrganizationofthePetroleumExportingCountries

Keytakeaways

● During 2014 – 2016 global oil supply outpaced world oil demand growth, leading to excess supply in the market and a strong deterioration in oil prices.

● The Declaration of Cooperation was a necessary response to the growing market imbalance. ● Assuming OPEC and non-OPEC continue at full conformity in the coming months, the

market rebalancing is expected by the end of the year.● In the long-term, energy demand increases by 35% between 2015 and 2040● Global oil demand will increase by 15.8 mb/d, reaching 111.1 mb/d by 2040● US tight oil is the most important contributor to non-OPEC supply, but peaks after 2025,

raising the need for more OPEC crude● Refining capacity expansion takes place predominantly in developing countries, led by Asia-

Pacific and the Middle East

19

www.opec.org

Thankyou

8th IEA-IEF-OPECSymposiumonEnergyOutlooksIEFSecretariat,Riyadh14thFebruary2018

AcomprehensiveinteractiveversionoftheWOOisavailableatwww.opec.org

20

© 2018 Organization of the Petroleum Exporting Countries

Market balance expected by the end of 2018

Note:*1Q18-4Q18=Forecast.

Source:OPECSecretariat.

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18*

2Q18*

3Q18*

4Q18*

mb

5-yearaverage

ExceptedOECDstocklevels353

40

-31

-200

-100

0

100

200

300

400

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18*

2Q18*

3Q18*

4Q18*

mbDifferencetofive-yearaverage

OPEC-12andnon-OPECparticipantsproduceat fullconformity

21

©2018OrganizationofthePetroleumExportingCountries

OildemandintheEconomicGrowthsensitivities

● Two alternative sensitivities: Higher GDP growth (HG) and Lower GDP growth (LG)

● Demand in 2040:– Reference Case: 111.1 mb/d– HG: 113.8 mb/d– LG: 107.5 mb/d

● Overall uncertainty from GDP growth is in the range of 6 mb/d in 2040

Long-term oil demand (mb/d)

22

©2018OrganizationofthePetroleumExportingCountries

OildemandinthepenetrationofEVsSensitivityCase

● Sensitivity Case: Penetration of EVs is higher than in the reference case

● Annual EV sales reach 80 million by 2040

● Oil demand in 2040 is reduced by 2.5 mb/d compared to the Reference Case, to total 108.6 mb/d

● Global oil demand plateaus around this level in the second half of the 2030s

Long-term oil demand (mb/d) in the reference Case and the Sensitivity Case

23

©2018OrganizationofthePetroleumExportingCountries

OildemandintheefficiencyimprovementsSensitivityCase

● Accelerated Efficiency (AE) Case assumes more aggressive efficiency improvements

● Overall demand reduction in the AE case is 3.2 mb/d by 2040, reaching 107.9 mb/d

● Two-thirds of the demand reduction takes place in DCs

Long-term oil demand (mb/d)

24

©2018OrganizationofthePetroleumExportingCountries

LiquidssupplyintheUpside/DownsideSensitivities

● Based on the Upside Sensitivity, demand for OPEC crude would be curbed in the medium-term; reaching 36.8 mb/d by 2040

● By contrast, in a Downside Sensitivity Case, demand for OPEC crude stays relatively flat at 33 mb/d until mid-2020s; then rises to 45 mb/d by 2040

Supply sensitivities: impact on demand for OPEC crude

25

© 2018 Organization of the Petroleum Exporting Countries

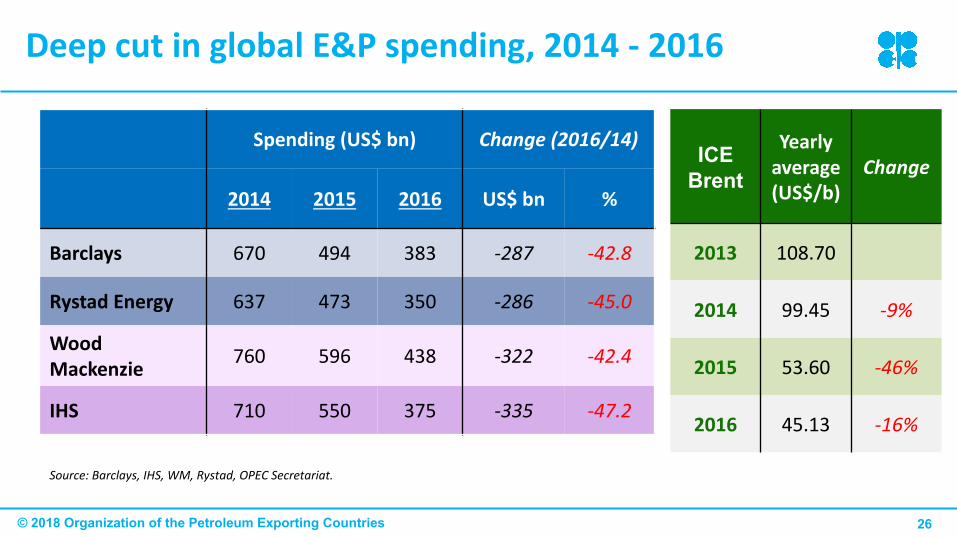

DeepcutinglobalE&Pspending,2014- 2016

Spending (US$bn) Change(2016/14)

2014 2015 2016 US$bn %

Barclays 670 494 383 -287 -42.8

RystadEnergy 637 473 350 -286 -45.0

WoodMackenzie 760 596 438 -322 -42.4

IHS 710 550 375 -335 -47.2

ICEBrent

Yearlyaverage(US$/b)

Change

2013 108.70

2014 99.45 -9%

2015 53.60 -46%

2016 45.13 -16%

Source:Barclays,IHS,WM,Rystad,OPECSecretariat.

26