NVQ Level 3 in Payroll Administration Completing Year End Procedures … · NVQ Level 3 in Payroll...

28

NVQ Level 3 in Payroll Administration Completing Year End Procedures (CYE) 2003 Standards Friday 7 December 2007 (afternoon) Time allowed – 3 hours plus 15 minutes’ reading time Please complete the following information in BLOCK CAPITALS: Student member number Desk number Venue code Date Venue name Important: This exam paper is in two sections. You should try to complete every task in both sections. We recommend that you use the 15 minutes’ reading time to study the exam paper fully and carefully so that you understand what to do for each task. However, you may begin to write your answers within the reading time, if you wish. We strongly recommend that you use a pen rather than a pencil. You may not use programmable calculators or dictionaries in the exam. Do NOT open this paper until instructed to do so by the Supervisor. SA7570 CYE Exam

Transcript of NVQ Level 3 in Payroll Administration Completing Year End Procedures … · NVQ Level 3 in Payroll...

NVQ Level 3 in Payroll AdministrationCompleting Year End Procedures (CYE)2003 Standards

Friday 7 December 2007 (afternoon)

Time allowed – 3 hours plus 15 minutes’ reading time

Please complete the following information in BLOCK CAPITALS:

Student member number Desk number

Venue code Date

Venue name

Important:

This exam paper is in two sections. You should try to complete every task in both sections.

We recommend that you use the 15 minutes’ reading time to study the exam paper fullyand carefully so that you understand what to do for each task. However, you may begin towrite your answers within the reading time, if you wish.

We strongly recommend that you use a pen rather than a pencil.

You may not use programmable calculators or dictionaries in the exam.

Do NOT open this paper until instructed to do so by the Supervisor.

SA7570 CYE

Exam

GLOSSARY OF TERMS

AVC Additional Voluntary Contribution

COMP Contracted Out Money Purchase

ET Earnings Threshold (for National Insurance Contributions)

GAYE Give As You Earn

HMRC Her Majesty’s Revenue & Customs

LEL Lower Earnings Limit

NI National Insurance

NIC National Insurance Contribution

PAYE Pay As You Earn

SAP Statutory Adoption Pay

SMP Statutory Maternity Pay

SPP Statutory Paternity Pay

SSP Statutory Sick Pay

UEL Upper Earnings Limit

2

This exam paper is in TWO sections.

You must show competence in BOTH sections. So, try to complete EVERY task in BOTH sections.

Section 1 contains 3 tasks and Section 2 contains 10 tasks.

You should spend about 130 minutes on Section 1, and about 50 minutes on Section 2.

There is blank space for your workings on pages 21 and 22, but you should include all essentialcalculations in your answers.

Both Sections 1 and 2 are based on the business described below.

Introduction:

• You are a Payroll Officer for Fictitious Ltd.

• The company pension scheme is a COMP.

• Fictitious Ltd is a large company for the purposes of recovery of statutory payments.

• It is not permitted to recover any Statutory Sick Pay it has paid out.

• The company is permitted to recover only 92% of any Statutory Adoption, Maternity and Paternity Pay it

has paid out.

Note:This page is perforated. You may remove it for easy reference.

3

Section 1 – Operational tasks

You should spend about 130 minutes on this section.

Complete all three tasks.

Data

The data below is an extract from the final payroll records for the tax year 2006/07.

Note:This page is perforated. You may remove it for easy reference.

4

Sue Tamimi Richard House Kim BaudainsSpare column

for workings

Final Tax Code 508L K194 127L Wk1

Date of starting 17 Apr 1997 11 Sept 2006 15 Jan 1985

Date of leaving 9 Feb 2007

National Insurance number PS497021B LT628851A MK913764B

Gross pay for year including

SAP, SMP, SPP, SSP and

previous employment

35,176.82 67,786.67 41,285.71

Pay from previous employment Nil 26,586.67 Nil

Pension scheme contributions 2,814.15 3,296.00 Nil

AVC contributions 3,000.00 Nil Nil

GAYE for year 300.00 Nil 3,420.00

Tax deducted for year including

tax from previous employment5,016.06 20,323.60 7,850.92

Tax in previous employment Nil 8,132.62 Nil

Earnings at the LEL (where

earnings reach or exceed the

LEL)

4,368 2,548 4,004

Earnings between the LEL and

the ET667 392 616

Earnings between the ET and

the UEL28,505 16,625 24,615

Employee NIC in the year 2,262.23 1,772.85 2,828.23

Employer NIC in the year 2,972.30 4,727.11 4,693.21

Student loan deductions Nil 3,033 2,480

SSP paid in the year 1,443.03 Nil 798.57

SMP paid in the year 5,761.58 Nil Nil

SAP paid in the year Nil Nil 2,830.10

SPP paid in the year Nil 217.70 Nil

Task 1.1

Using the information given on page 4 prepare the end of year returns form P14 for each employeefor the tax year 2006/07. Use the P14 forms on pages 6, 7 and 8.

5

6

FICTITIOUS LIMITEDHOLMES TOWERFULCHESTERHANTS FU2 6GA

2007

BASINGSTOKE

B18 150

F

615002R

PS 49 70 21 B

TAMIMI

SUE

7

FICTITIOUS LIMITEDHOLMES TOWERFULCHESTERHANTS FU2 6GA

M

615002R

LT 62 88 51 A

HOUSE

RICHARD

2007

BASINGSTOKE

B18 150

8

F

615002R

MK 91 37 64 B

BAUDAINS

KIM

FICTITIOUS LIMITEDHOLMES TOWERFULCHESTERHANTS FU2 6GA

2007

BASINGSTOKE

B18 150

9

Task 1.2

Using the information given on page 4 and your interpretation of this on the P14s on pages 6, 7 and 8,complete the details in the summary section of the extract of Form P35 for the tax year 2006/07. Usethe form P35 on page 10.

Note 1

Boxes to Enter 'R' beside any minus amounts.

Note 2

Boxes and If you are not required to

complete the 'Part 1 Summary ofemployees and directors' sectionyou should begin by entering therespective NICs and Income Taxtotals for all employees for whomyou have completed a form P11 (or equivalent record).

Note 3

Box Whole pounds only.Do not enter pence in shaded area.

Note 4

Boxes to Do not enter the totals paid.

Only enter the amounts you areentitled to recover. You will find thisin your P30BC Payslip Booklet oryour own equivalent paymentrecord.

Note 5

Box 22 If box 21 is a minus

figure then add

box 21 to box 11

Note 6

See your Contractor’s Annual Return,form CIS36, box F.

Note 7

Box If a Tax-free Incentive payment was credited

to your PAYE payment record for this year, for having sent any previousyear's returns electronically, enter theamount. If the Incentive was repaiddirectly to you by cheque, leave thisbox blank.

26

1812

10

63

61

• If you are sending your form P35 and all of your forms P14 on paper you musta) list each employee or director for whom you have completed a form P11 Deductions Working Sheet

(or equivalent record). If you have more than ten entries, please prepare P35(CS) Continuation Sheetsb) ensure that all forms P14 are enclosed with this return.

• If some or all of your forms P14 are not enclosed with this return because they are being sent by Internet, Electronic Data Interchange (EDI) or magnetic media, there is no need to complete the 'Part 1 Summary of employees and directors' section of this return. Instead you must begin by completing boxes 3 and 6 of the 'Part 2 Summary of payments for the year' section below.

£

Fill in boxes 28 and 29 only if you are a limited companythat has had CIS deductions made from payments received for work in the construction industry.

If any of the boxes do not applyto you, please leave them blank.

If you make a mistake andrecord the wrong entry,• draw a line through the entry

so that it can still be read, and• record the correct figure

alongside.

CIS deductions suffered Total of col E on form CIS132

Revised amount now payable

Employee’s namePut an asterisk (*) by the name if the person is a director

Income Tax deducted or refunded in this employment. Write 'R' beside an amount to show a net refund.

National Insurance contributions (NICs)Enter the total NICs from column 1d on form P11. Write 'R' beside any minus amounts.

NICs and Tax paid already

Deductions made from subcontractors see Note 6

Amount payable for the year 22 + 23

Tax-free Incentive payment received during the year see Note 7

see Note 5

Totals from P35(CS)Continuation Sheets

Total NICs shown above after deducting amounts marked 'R'

£

Page 2Page 3

Advance received from HM Revenue & Customs

to refund tax

Totals from P35(CS)Continuation Sheets

Total Tax shown aboveafter deducting amounts

marked 'R'

see Note 4

Statutory Maternity Pay(SMP) recovered

Statutory Paternity Pay(SPP) recovered

NIC compensation on SPP

Statutory Adoption Pay(SAP) recovered

NIC compensation on SAP

Funding received fromHM Revenue & Customs to pay SSP/SMP/SPP/SAP

Statutory Sick Pay (SSP) recovered

Please now fill in page 4

Total StudentLoan deductions

see Note 3

NIC compensation on SMP

Part 1 Summary of employees and directors

Part 2 Summary of payments for the year

Guidance notes – Some useful hints are given below. For step-by-step guidance refer to the ‘Help’ section on Page 1.

Income TaxNICs

Combined amounts

9 + 10

Total NICs and Tax 3 + 8

Total Tax 6 + 7

Total NICs 1 + 2 Total Tax 4 + 5

Statutory payments recovered

19 minus 20

11 minus 21

27 minus 28

3

1 £4

£6

£7

£8

£9

£11

£10

£12

£13

£14

£15

£16

£17

£18

£20

£19

£21

£22

£29

£25

£24

£23

£28

Total of boxes 12 to 18

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£

£2 £5

see Note 2 see Note 2

£26

NOW PAYABLE 24 minus 25 and 26 £27 Do not include a payment with this form. If a payment is due, please make itimmediately. See page 1 for notes on how to pay.

�

ntns3

Combined amounts

£9

£11

£10

1256 30

850

2016 30 2106.30

SUE TAMIMIRICHARD HOUSEKIM BAUDAINS

41,722 27

Data

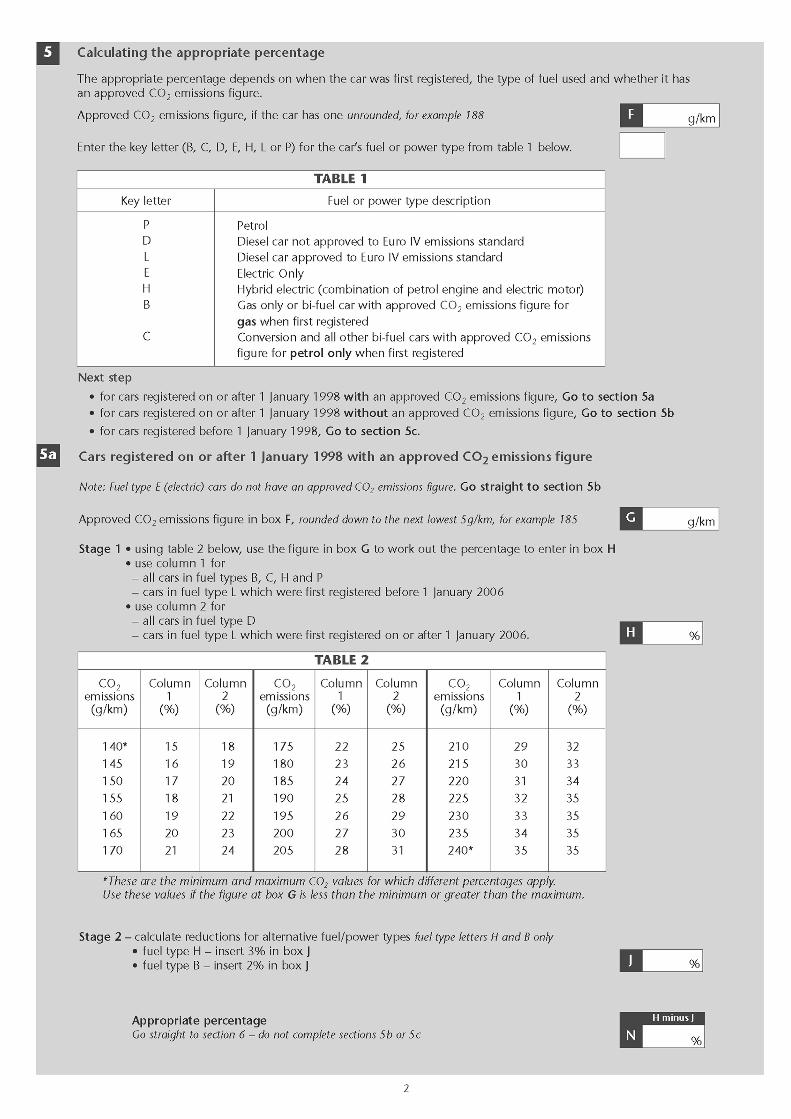

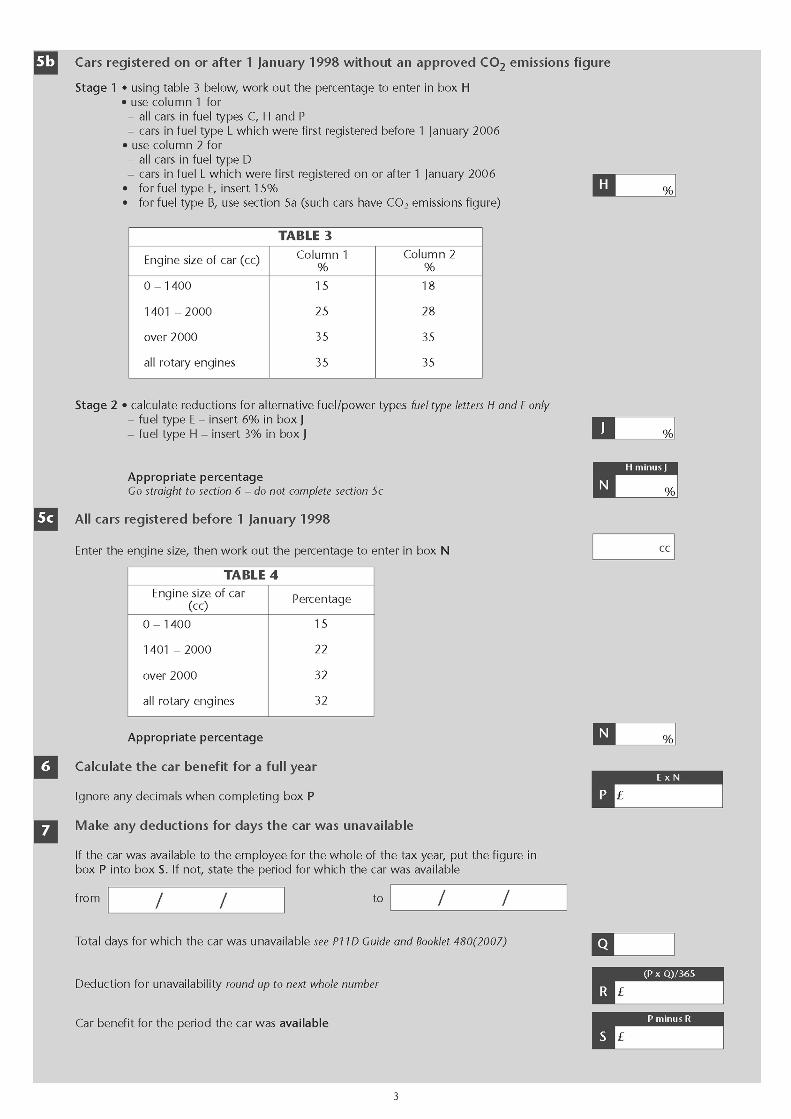

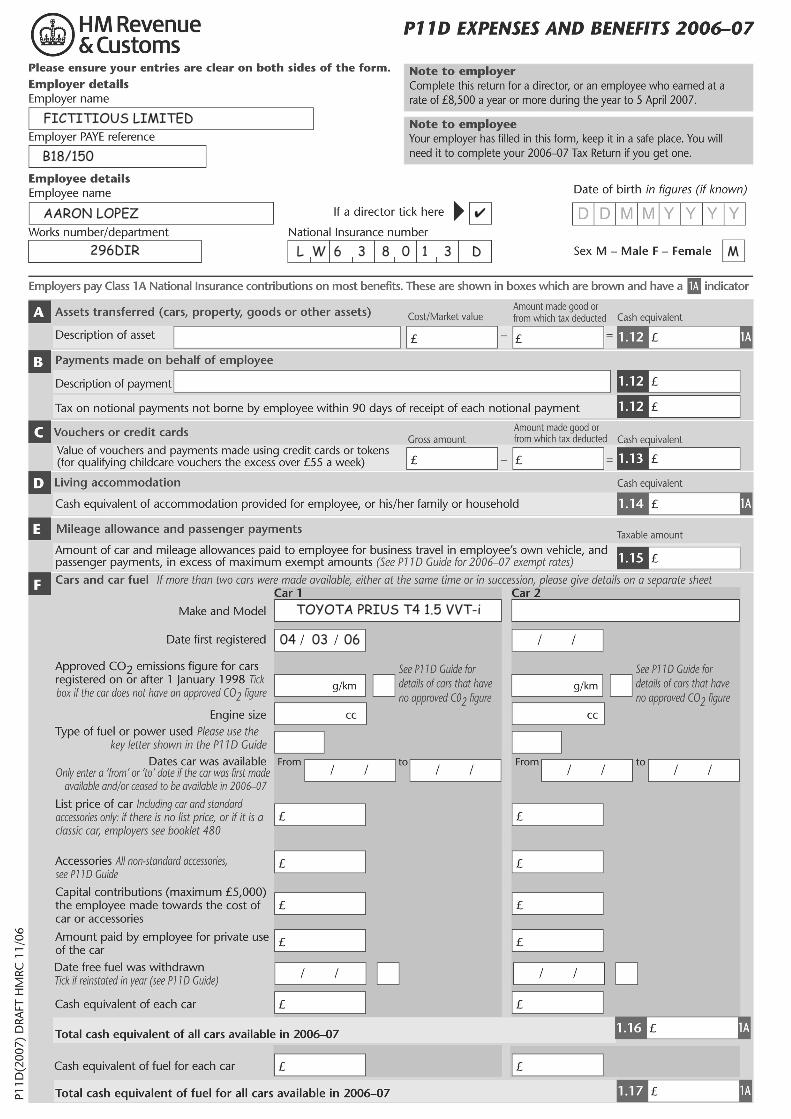

Aaron Lopez, a company director, has enjoyed the following benefits in kind, which you now need to take

into consideration for the year end P11D reporting process.

1. For the whole tax year Aaron had a company car which was also available for private use. The

details are as follows;

• The car is a Toyota Prius T4 1.5 VVT – i.

• The petrol engine of 1,497 cc is backed up with an emission free self charging electric motor.

• It cost £22,355 when new and first registered and supplied to him on 4 March 2006.

• The CO2 rating of the car is 104 g/km.

• No fuel is provided by the company.

• Aaron pays £100 a month towards the private use of the car.

2. Aaron received £4,680 in qualifying Childcare Vouchers towards the cost of childcare arrangements.

3. The company has loaned Aaron £27,000, interest free, repayable over 5 years at £450 a month. At

6 April 2006 the balance of the loan was £5,850.

Note:This page is perforated. You may remove it for easy reference.

11

Task 1.3

(a) Calculate the benefit in kind values of the relevant items on page 11 using the P11D workingsheets on pages 13 to 18.

(b) Complete the P11D on pages 19–20.

12

FICTITIOUS LIMITED AARON LOPEZ

296DIRB18/150

TOYOTA

04 03 2006

PRIUS T4 1.5 VVT-i

L W 6 3 8 0 1 3 D

�

FICTITIOUS LIMITED AARON LOPEZ

296DIRB18/150 L W 6 3 8 0 1 3 D

FICTITIOUS LIMITED

AARON LOPEZ

296DIR

B18/150

L W 6 3 8 0 1 3 D M

�

TOYOTA PRIUS T4 1.5 VVT-i

04 03 06

Note:You may use this page for your workings.

21

Note:You may use this page for your workings.

22

Section 2 – Short answer questions

You should spend about 50 minutes on this section.

Write in the space provided, tick the appropriate box OR circle the correct answer. Do not give youranswer in any other way.

Answer all the questions on pages 23 to 27.

Task 2.1

Payroll year end is governed by strict deadlines for each stage of the process.

(a) By which one of the following dates must P14s be received by HMRC?

19 April 6 May 19 May 31 May

(b) By which one of the following dates must P60s be received by employees?

30 April 31 May 30 June 31 July

(c) Assuming the company has over 250 employees and pays its PAYE electronically, by whichone of the following dates must the final payment of PAYE be received by HMRC?

19 April 22 April 30 April 6 May

Task 2.2

Each year employees are issued with a P60.

(a) Would you issue a P60 to an employee who left the company on 3 April?

Yes No

(b) What would be the position if the employee left on 7 April?

(c) What action would you take if an employee claimed to have lost their P60 and wanted a newone?

23

Task 2.3

The company pays for a number of social events during the year. The main event was the summer dance

costing £132.50 for each person who attended. A second event in the Autumn cost a further £27.50 with a

Christmas dance following at a cost of £92.70 for each person who attended.

(a) Outline the benefit in kind rules relating to the above events.

(b) On the basis of your description above, which one of the following is the benefit value to bereported on the P11D?

£27.50 £92.70 £120.20 £132.50

(c) What would be the position if the company also gave a gift to each employee for Christmas?

Task 2.4

(a) By which one of the following dates must the annual benefit in kind returns, P11D, bereceived by HMRC?

6 April 31 May 30 June 6 July

(b) Describe how the company calculates its Class 1A NIC liability at year end.

(c) When must the company account for its Class 1A NIC liability if it is paying electronically?

19 May 22 June 22 July 19 August

24

Task 2.5

The company is required to consider the benefit in kind report, P9D, when completing the year end process.

(a) Under what particular circumstances will you use form P9D instead of a P11D?

(b) Which form would you use for the company directors?

Neither P9D P11D Depends on earnings

Task 2.6

(a) How can an organisation avoid reporting certain benefits, in particular expenses, onemployee P11Ds?

(b) List TWO specific benefits that would qualify under (a) above.

1.

2.

25

Task 2.7

(a) List THREE circumstances where travel costs from home to permanent workplace that arereimbursed by the employer would be allowable for tax purposes?

1.

2.

3.

(b) List TWO of the four types of vehicle which carry an HMRC Approved Mileage AllowancePayment value.

1.

2.

Task 2.8

(a) Give ONE situation where travel is not strictly for work reasons but would still be allowable ifpaid by the employer.

(b) Give TWO special considerations that are available for travel by registered disabledemployees.

26

Task 2.9

“Services Supplied” is a particular benefit covered on the P11D at Section K.

The company is a combined legal and accounting services supplier and provides a range of beneficial

services to its employees.

In respect of each one of the following services determine if a benefit in kind report is required andexplain your answer in each case.

(a) Printing work Benefit in kind report: Yes No

Reason:

(b) House conveyance Benefit in kind report: Yes No

Reason:

(c) Tax returns Benefit in kind report: Yes No

Reason:

(d) Computer repair work Benefit in kind report: Yes No

Reason:

Task 2.10

A company marketing roadshow has three employees travelling round major clients in a company-purchased

luxury caravan. After it finishes, one of the employees buys the caravan from the company. It cost £18,750 to

buy and fit out and at the end of the various events its market value is calculated as £10,500. The employee

purchases it for £8,500 and the company pays £287.50 to transport it to her home.

(a) Describe the tax rules for determining the value of the caravan as purchased by theemployee.

(b) What value will be entered on the P11D in this case?

Nil £2,287.50 £10,250.00 £10,537.50

27

NVQ/SVQ qualification codes

Payroll Administration Level 3 (2003 standards) – 100/2939/4 G75M23

Unit number (CYE) – Y/101/8093

© Association of Accounting Technicians (AAT) 12.07

140 Aldersgate Street, London EC1A 4HY, UK

t: 0845 863 0800 (UK) +44 (0)20 7397 3000 (non-UK)

e: [email protected] w: aat.org.uk

527570