November La Voz 2010

32

-

Upload

independent-insurance-agents-of-nm -

Category

Documents

-

view

215 -

download

1

description

The Official e-zine for Independent Agents in New Mexico

Transcript of November La Voz 2010

SM

SM

Now boarding your out-of-stateworkers’ compensation clients...

Give us a look!$500 Southwest Airline Gift Card Drawing• For an out-of-state application submitted, the agent/CSR name will be

placed in the drawing once.• For any out-of-state policy that is bound with premium less than $25,000,

the agent/CSR name will be placed in the drawing twice.

Bind it with us!$100 Southwest Airline Gift Card • Qualify by binding any out-of-state account (can include any new New Mexico

business premium towards the premium goal) with premium of $25,000 to $49,999.

$250 Southwest Airline Gift Card• Qualify by binding any out-of-state account (can include any new New Mexico business

premium towards the premium goal) with premium of $50,000 to $100,000.

$500 Southwest Airline Gift Card • Qualify by binding any out-of-state account (can include any new New Mexico business

premium towards the premium goal) with premium over $100,000.

The preferred workers’ compensation insurance carrier of the Independent Insurance Agents of New Mexico, New Mexico Mutual wants your business! Just submit a completed Accord application, loss runs and emod worksheet to your underwriter and we’ll take it from there.

Ticketing Information

We are now where yourclients need us to be.

From now through March 31, 2011, qualify for Southwest Airlines gift cards by using our new program.

www.NewMexicoMutual.com • 1-800-788-8851

that we can now write your customers with out-of-state exposure.*New Mexico Mutual is proud to announce

All states are eligible for Other States Coverage Program except the “monopolistic states” of North Dakota, Ohio, Washington and Wyoming.

SM

SM

Now boarding your out-of-stateworkers’ compensation clients...

Give us a look!$500 Southwest Airline Gift Card Drawing• For an out-of-state application submitted, the agent/CSR name will be

placed in the drawing once.• For any out-of-state policy that is bound with premium less than $25,000,

the agent/CSR name will be placed in the drawing twice.

Bind it with us!$100 Southwest Airline Gift Card • Qualify by binding any out-of-state account (can include any new New Mexico

business premium towards the premium goal) with premium of $25,000 to $49,999.

$250 Southwest Airline Gift Card• Qualify by binding any out-of-state account (can include any new New Mexico business

premium towards the premium goal) with premium of $50,000 to $100,000.

$500 Southwest Airline Gift Card • Qualify by binding any out-of-state account (can include any new New Mexico business

premium towards the premium goal) with premium over $100,000.

The preferred workers’ compensation insurance carrier of the Independent Insurance Agents of New Mexico, New Mexico Mutual wants your business! Just submit a completed Accord application, loss runs and emod worksheet to your underwriter and we’ll take it from there.

Ticketing Information

We are now where yourclients need us to be.

From now through March 31, 2011, qualify for Southwest Airlines gift cards by using our new program.

www.NewMexicoMutual.com • 1-800-788-8851

that we can now write your customers with out-of-state exposure.*New Mexico Mutual is proud to announce

All states are eligible for Other States Coverage Program except the “monopolistic states” of North Dakota, Ohio, Washington and Wyoming.

Save the Date!Legislative Mixer

La Posada de Santa Fe Hotel, Resort & Spa

Please pencil in Wednesday, January 26th from 5:30 to 7:30 pm.

We will send out more information on this event as the date draws closer.

IIANM Staff

2010-2011 OfficersChairKathy YeagerVice-ChairScott JonesSecretary/TreasurerPJ WolffNational DirectorSam ConleeImmediate Past ChairAlma Franzoy-Capron

Tech Talk 08

Education Edge 28

November's Clickable Calendar 29

Odds n Ends 31

IIANM's Partners Program 32

Features

This publication is intended to provide accurate and authoritative information on the subject mat-ter covered, but is distributed with the under-standing that neither IIANM, nor any contributing author, publisher, contributor or advertiser is rendering legal, accounting or any other profes-sional service and assume no liability whatsoever in connection with its use. Further, the electronic links to our advertisers and/or contributors found in this publication are provided as a courtesy to our readers and do not necessarily indicate an endorsement by IIANM.

News items from members of Independent Insurance Agents of New Mexico and the general insurance industry are encouraged. The advertis-ing deadline is the fifteenth day of the month, pre-ceding publication.

Advertising rates are available upon request.

Please contact Rachel Sheffield at [email protected] for details

Take a Cue from the Movie Industry 06

Negative Insurance Outlook Remains 11

The "Born Salesman" Myth 13

Insurers Have Other Ideas of Cars Value 14

Rebellion With A Cause? 17

Your Web Strategy MUST Change 19

imagine... 22

Should Agents Send Certificates to Insurers? 24

How to Conduct & Measure Advertising & Marketing Campaigns 26

Acuity 18

American Mining Insurance Company 15

Burns & Wilcox 16

Colonial General Insurance Agency, Inc. 10

Infinisource Payroll 27

Litchfield Special Risks, Inc. 23

Market Finders, Inc. 20

Neff Risk Services, Inc. 07

New Mexico Mutual 02

Risk Placement Services, Inc. (RPS) 12

Trustco 25

In Every Issue

Advertiser Index

"The Voice" of Independent Agents since 1934LoVZ

Loa

VZ

President/CEOThom Turbett, CIC

VP Of Membership ServicesLorri Gaffney

Director Of CommunicationsRachel Sheffield

Director Of Insurance ProgramsCarmen Reese Porter, ACSR, CISR

Receptionist / Member Services Associate

Renee Rivera

“La Voz” is the official monthly publication of the

Independent Insurance Agents of NM 1511 University Blvd. NE Albuquerque, NM 87102.

(505) 843-7231. Fax (505) 243-3367. Web site www.iianm.org.

retailers and DVD rental companies are extremely con-

cerned and upset over the possibility that the movie studios

may shorten the timeframe and compete with the current

industry formula. Movie studios are contending that short-

ening the time frame for VOD release will not substantially

threaten their business and reduce movie pirating.

What is the lesson for independent insurance agents? For

nearly 100years, the only distribution channel for movie

studios was movie theaters. And, since theaters had big

screens and great sound systems, they had a monopoly on

the movie experience. However, with the advent of home

entertainment systems, high definition viewing systems

and surround sound technology, the experience is close

to being replicated. Will “date night” still mostly occur at

the movies? Most likely the answer is yes. But the biggest

advantage theaters have right now is the immediacy of new

releases. As that time frame becomes compressed, movie

owners will have to think of other ways to differentiate

themselves from competing channels.

This quandary should sound familiar to independent

agents. Just as technology has enabled the online distri-

bution channel to be a threat to independent insurance

agents, it is also a tool that agents should use to drive

business to their website and ultimately in their front door.

Virtually every way that products and services are delivered

in our economy is being challenged. The answer is not to

try to duck the challenge. Instead, agents should harness it

to capitalize on the channel’s strategic advantages: choice,

customization and advocacy.

Take a Cue from the Movie In-vie Industry

In addition to the usual concerns of soft markets, bat-

tling populist insurance legislation and recruiting talented

employees, over the past decade independent agents have

watched another challenge evolve. Technology, coupled

with massive advertising budgets, has enabled direct writ-

ers to increase market share in personal auto insurance.

Agents are feeling like they are in the crosshairs.

For guidance and empathy, independent agents can look

to a brewing battle between theater owners and studios. A

recent FCC ruling allows movie studios to use technology

that can help prevent video-on-demand (VOD) systems

from being copied. On the surface this may not seem

significant, but copy blocking technology can herald the use

of VOD which will enable people to watch movies on their

home entertainment systems at a lower price – about $20

- $25.

The current business model gives movie theatres an

exclusive timeframe—typically of 120 days—to show new

movies. After that, consumers can purchase movies using

VOD for $5 or they can purchase the movie at a DVD re-

tailer like Wal-Mart. However, studios are now planning to

tap into consumer interest in seeing new movies in a much

shorter time frame—45 days. This option may be especially

attractive for families looking cut down on the expense of

to a family trip to the movie theater, which can run as much

as $45 including snacks. Of course, theater owners, DVD

Movie theaters, facing a distribution channel threat, must evolve. What can agents learn?

by Dave Evans

Page 6 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Page 6 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Page 8 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Recent headlines have underscored the importance of agents having written security plans to protect the

security of their operations and the privacy of their clients’ personal information. Not only could a breach of clients’ personal information devastate an agency’s reputation; it is likely to result in the agency’s having to undertake time consuming and costly actions on behalf of clients whose personal information is compromised.

We are aware of agents being fined in at least two states for not having a written security plan and of a major firm recently having to announce two data breaches, one occurring online and the other when a laptop contain-ing confidential personal information was stolen. Just as a well managed agency takes specific steps to protect against E&O risk, it needs to have a written security plan, incorporate the plan into its procedures, train its employ-ees to implement these procedures consistently, and monitor for compliance.

ACT’s Information Security PlanACT has developed a free prototype security plan to as-sist agents and brokers in formulating and implementing specific procedures, training and monitoring to protect the security of their operations and the privacy of their client information. The plan is the product of ACT’s Agency Security Best Practices Work Group, with assistance from ACT’s Security Issues Work Group and IIABA’s Office of General Counsel. We owe the Massachusetts Associa-tion of Insurance Agents special thanks for making the plan it had developed for its members available to us, which we used as a starting point for our plan.

Before sitting down to develop your agency’s security plan, or to refine your current plan, it is essential for you to be thoroughly familiar with your state’s data breach notification and privacy laws, your insurance laws and regulations, applicable federal laws and regulations, as well as the laws of any states where you hold nonresident licenses or possess personal information on the state’s residents. This will enable you to conform your agency’s plan to these requirements. We used the Massachusetts privacy law as a starting point for the ACT prototype plan, because Massachusetts imposes some of the most specific requirements.

Before providing some specific guidance on how best to use the ACT prototype plan in your agency, it is important to provide you with a brief overview of some of these laws and regulations.

State & Federal Privacy Laws

Agents need to be aware of the general business and insurance specific security and privacy laws, regula-tions and administrative letters that apply to them in their resident states, as well as in states where they hold non-resident licenses or where individuals they insure are resident. For example, the Massachusetts privacy law applies to “all persons that own, license, store or maintain personal information about a resident” of Massachusetts. Similarly, the recent August, 2010 Connecticut Insurance Bulletin applies whenever there is an “unauthorized acqui-sition or transfer of, or access to” the personal information of any Connecticut resident, even if the data is encrypted, and the Insurance Department must be notified within five days from when the “information security incident” is identified.

The federal Gramm-Leach-Bliley Act (GLB Act) requires businesses to proactively implement administrative, technical, and physical safeguards to protect customer non-public personal information. Many states have en-acted laws and regulations to implement the GLB Act for the insurance industry in their state. Overlay onto these requirements the Security Breach Notification laws that have passed in 46 states and the District of Columbia.

We are now starting to see state privacy laws move from the implementation of general safeguards to much more specific requirements. For example, the Nevada law and Massachusetts law (March 1, 2010) specifically require that email containing “personal information” be sent in an encrypted manner. This would include, for example, per-sonal information submitted on commercial applications. The Massachusetts law in addition would require the encryption of personal information contained on laptops and mobile devices because of the higher risk posed that these devices will be lost or stolen.

Implementing Your Agency’s Security ProgramAfter familiarizing yourself with the laws and regulations

ACT’s Releases Prototype Agency Information Security Plan

by Jeff Yates, ACT Executive Director

Page 8 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 9

that apply to you, you are ready to develop or refine your own Information Security Plan using the ACT prototype plan as a starting point. It is important that you either use ACT’s prototype plan as a checklist or customize its terms to fit your particular agency’s operations. The various state and federal laws typically provide that the admin-istrative, technical, electronic and physical safeguards a business incorporates into its security program be appro-priate to the size and complexity of the business and the nature and scope of its activities.

ACT prototype plan also contains a series of “Notes” designed to help agencies in customizing the plan and pointing out the need to consult additional laws that might apply to your agency. A good example is the Note on HIPAA, pointing out that if the agency is a “Business As-sociate” handling “protected health information” (“PHI”), there are additional specific security requirements that the agency would need to add to the prototype plan, along with some resources for the agency to consult.

Consider taking the following implementation steps:

1. Appoint a Data Security Coordinator who will oversee the development and implementation of your agency’s security program.

2. Ascertain all of the types of private client and employee information that your agency retains, every place where it is stored (whether in paper or electronic format), exactly who has access to it and how it is used and transmitted. Be particularly sensitive to the types of private information that are singled out in the privacy and data breach laws that are applicable to you.

3. Decide whether you really need to store or transmit all of this private information that you possess, and if not, don’t keep it. If you do need to possess it, restrict its access to only those employees who need to use it, keep it off PCs, mobile devices and home computers, and encrypt it wherever it is stored (where possible) and when it is transmitted.

4. Have an employee team go through the prototype plan and customize it to your agency’s operations and develop new procedures and workflows as necessary to implement it.

5. Acquire or upgrade your hardware and move to the latest versions of your software so that you incorporate the latest security protections, and then keep your agency current on both hardware and software versions in the future.

6. Thoroughly train all employees on your agency’s new security plan and any accompanying new procedures and workflows, and secure their written commitment that they will abide by the plan. Change your procedures so that new hires are immediately trained on the security plan. Make sure your procedures assure that the access

of terminated employees is cut off immediately from the agency’s systems, as well as from any carrier websites or other third party sites. Ongoing employee training and re-minders about your security requirements and protecting clients’ private information are absolutely key, because security breaches often result from employee error or a lack of sensitivity to protecting this information.

7. Make sure that third party vendors that possess any of your agency’s private information have equivalent security plans and procedures in place, as well as a strong com-mitment to security and protecting this information.

8. Monitor your employees’ adherence to your agency’s security plan and procedures, monitor the traffic over your systems for any unusual activity and consider periodic security audits by an outside security professional.

9. Review and update your security plan, procedures and workflows at least annually.

The Big Picture

One year ago ACT completed its latest report on key trends and “must do” issues the industry must tackle to be properly positioned to succeed in the future.

We identified three critical “must do” issues and the first was to increase industry awareness and collaboration on security & privacy. ACT concluded that the significant progress the industry has made with Real Time and other new workflows is directly dependent on protecting the security and privacy of the client information being used. In addition, agents have unprecedented opportunities with online marketing and servicing using their websites, social media and other Internet tools, but again, protecting the security of these mechanisms and the privacy of client information on them is critical.

ACT is committed to providing independent agencies with information and tools to help them protect the security of their operations and client information. We believe ACT’s new prototype information security plan will be a major resource for agents and brokers and it provides a good example of the kind of industry collaboration on security issues that needs to occur.

Editor’s note:

Please visit www.iiaba.net/act at the “Security & Privacy” quick link for ACT’s free Agency Information Security Plan and other security related resources, including an online version of this article with links to the various laws and regulations mentioned.

This article reflects the views of the author and should not be construed as an official statement by ACT.

Page 8 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Founded in 1985, Colonial General Insurance Agency, Inc. is a wholesale General Agency providing quality insurance products to the Independent Insurance Agent.

Colonial General specializes in both standard and non-standard business. Our Property and Casualty business includes:

♦ Commercial Auto

♦ Commercial Contract

♦ Personal Lines

♦ Professional Liability

With 2,500 active producers under contract, Colonial General operates in eight states throughout the South-West. Our offices are located in Murray, Utah and Scottsdale, Arizona.

Most of all, we pride ourselves in our friendly customer service and our ability to help our producing agents with their many insurance needs.

♦ Preferred BOP ♦ Property ♦ Inland Marine ♦ Professional Liability ♦ Commercial Liability ♦ Workers Compensation

♦ Truckers ♦ Physical Damage ♦ NB Mexican Truckers ♦ Local Radius ♦ Garage ♦ Intermediate Radius

♦ Masterpiece Company ♦ Standard Company ♦ Umbrellas ♦ Stand-alone Liability ♦ Vacant ♦ Seasonal ♦ Dwelling Fire ♦ Homeowners

Commercial Lines/Brokerage Department

Transportation Department

Personal Lines Department

Preferred Commercial Lines Division

Avoid monthly or annual membership fees, use Colonial General for your Preferred Business Owners Policies. We have several markets available to give you the best quote possible. For additional information contact your underwriter.

Please contact our Utah office for all your Transportation needs!

P.O. Box 571770, Murray, Utah 84157 Phone: (801) 562-1188 Wats: (800) 594-8900

Fax: (801) 562-2218 Toll Free Fax: (800) 332-9285

You will never pay a fee to access our companies. No volume or binding contracts.

P.O. Box 14770 Scottsdale, AZ 85267 8475 E. Hartford Drive, Suite #100 Scottsdale, AZ 85255

Phone: (480) 991-7889 Wats: (800) 848-8860 Fax: (480) 948-1394 www.colonialgeneral.com

Colonial General Insurance Agency Colonial General Insurance Agency

Page 8 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Founded in 1985, Colonial General Insurance Agency, Inc. is a wholesale General Agency providing quality insurance products to the Independent Insurance Agent.

Colonial General specializes in both standard and non-standard business. Our Property and Casualty business includes:

♦ Commercial Auto

♦ Commercial Contract

♦ Personal Lines

♦ Professional Liability

With 2,500 active producers under contract, Colonial General operates in eight states throughout the South-West. Our offices are located in Murray, Utah and Scottsdale, Arizona.

Most of all, we pride ourselves in our friendly customer service and our ability to help our producing agents with their many insurance needs.

♦ Preferred BOP ♦ Property ♦ Inland Marine ♦ Professional Liability ♦ Commercial Liability ♦ Workers Compensation

♦ Truckers ♦ Physical Damage ♦ NB Mexican Truckers ♦ Local Radius ♦ Garage ♦ Intermediate Radius

♦ Masterpiece Company ♦ Standard Company ♦ Umbrellas ♦ Stand-alone Liability ♦ Vacant ♦ Seasonal ♦ Dwelling Fire ♦ Homeowners

Commercial Lines/Brokerage Department

Transportation Department

Personal Lines Department

Preferred Commercial Lines Division

Avoid monthly or annual membership fees, use Colonial General for your Preferred Business Owners Policies. We have several markets available to give you the best quote possible. For additional information contact your underwriter.

Please contact our Utah office for all your Transportation needs!

P.O. Box 571770, Murray, Utah 84157 Phone: (801) 562-1188 Wats: (800) 594-8900

Fax: (801) 562-2218 Toll Free Fax: (800) 332-9285

You will never pay a fee to access our companies. No volume or binding contracts.

P.O. Box 14770 Scottsdale, AZ 85267 8475 E. Hartford Drive, Suite #100 Scottsdale, AZ 85255

Phone: (480) 991-7889 Wats: (800) 848-8860 Fax: (480) 948-1394 www.colonialgeneral.com

Colonial General Insurance Agency Colonial General Insurance Agency

Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 11

More rating downgrades are expected than upgrades

for the remainder of 2010, which means the industry forecast remains negative until at least the end of the

year. According to a Standard & Poor’s quarterly insur-ance analysis, agents should not expect any near-term changes in the market.

“We are expecting fewer downgrades in 2010 than what we had in 2009 [though]—and that’s certainly been true year-to date,” says Matthew Carroll, director, financial intu-itions ratings at S&P North American Insurance Practice.

“We expect our highly-rated insurance companies, which are typically A+, AA- ratings, to be able to withstand severe stress to be able to maintain those ratings,” Carroll says.

The outlooks for personal and commercial lines are both negative, says John Iten, director, financial intuitions rat-ings at S&P North American Insurance Practice.

“In the commercial lines sector, the primary driver of the negative outlook is the pricing environment, which has been soft really since 2005,” Iten says.

And because of the soft economy and the rebound in the industry’s statutory capital position, there really isn’t anything on the horizon that’s going to turn that pricing environment around—at least not this year.

“The economy also is putting pressure on rates, to the extent that people and companies are making less and under pressure themselves, [so] they’re going to be more resistant to price increases,” Iten says.

But the industry has seen some stabilization in 2010 in terms of the overall economic environment, and agents see that in their day-to-day interactions with clients as well.

“I’m optimistic that the economy is slowly improving so I’m seeing a trend in my clients that they’re beginning to in-crease sales, beginning to increase payroll,” says Sharon Emek, partner and managing director at CBS Coverage Group in New York City.

An improving economy, though, does not necessar-ily mean a harden-ing market, Emek notes. Nonethe-less, independent agents should view strengthening eco-nomic conditions as a positive sign.

“My clients are do-ing better,” Emek says. “In 2008, I had

companies going out of business. In 2009, I didn’t have anyone go out of business. This year, I’ve even added some on.”

Emek doesn’t think there will be a traditional hard mar-ket again, although different lines of business might turn hard. “You have to plan for the fact that premiums are just never going to skyrocket. You have to manage your agency differently,” she says.

Integrating technology like social media and Real Time into your overall approach is one way to reach custom-ers more efficiently in a soft market. Outsourcing process work to retirees who can telecommute is a new trend that can help agencies stay efficient and save money on staffing. With reports that as much as 50% of the boomer generation may retire over the next 10 years, Emek says this is proactive thinking that can only help agencies in the long-term.

The key for independent agents is to fortify their customer and company relationships now during a more difficult economic period.

“Don’t take advantage of the current situation and be respectful of all of your partners,” says Bill Howard, an independent agent at Clarke & Sampson, Inc. in Alexan-dria, Va. “Firm up those relationships with the insurance company. The respect you show them now will be repaid when the market swings.”

Emek says that customer retention is essential during a soft market and that agents should become very close

to their customers so they will want to stay.

“This is the time to keep your retention at 100% if you can,” she says. “The most important thing you can do as an agent is keep getting the best possible rates and providing the best possible poli-cies to your clients.”

Negative Insurance Outlook Remains

Reaffirm relationships with carriers and customers to weather the downturn.

by Diane Rusignola

Page 10 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

www.RP

Sins.com

/scotts

dale

Page 10 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 13

Let's fact it. Most people put professional sales

people on a par with a child molester, but with-out the respect. If you want to clear a room,

tell people you are an insurance sales person or a financial planner -- watch them run for the door like cockroaches when you turn the light on. If you put an "Amway Sold Here" sign on your front door, even the Jehovah Witnesses won't come up and talk to you. Why? Because of the myths about selling.

Probably no myth is more pervasive than the idea that there are "born" sales people. What a crock. This one goes along with the idea that one is born with "the gift of gab." Granted there are some people who seem to naturally have the attributes we associ-ate with "good selling." However, most of the vision of what constitutes selling is manufactured by media portrayals of sales people, not what they really are.

In my Doubleday dictionary, one of the slang defini-tions of selling is "to deceive; cheat." That seems to be the definition that writers and dramatists have seized upon to portray sales people. You see the loudmouth in a plaid coat fast-talking some rube out of their money; you see the huckster running a shell game; you see the flimflam man conning some innocent out of their life savings -- Meredith Wilson's "Music Man," Prof. Harold Hill, conning the whole town into buying his band instruments -- that's selling in the popular literature.

On the other hand you see the sad Willy Loman in Arthur Miller's Pulitzer Prize winning play, "Death of a Salesman," who makes selling a sad and tragic waste of a life. Or, worse yet, "Glen-Gary Glenn-Ross" -- the stage play/movie that shows selling as a mean spirited, con job carried on by desperate losers in dingy offices managed by sociopathic maniacs.

Either way, the popular view of selling is poor.If Herbert Hoover was right and the busi-ness of America is "business," then sell-ing is the key function driving business. It is an accountant's lie that "nothing happens until somebody sells some-thing." Any true professional in sales can tell you that a great deal must happen before anyone sells anything! Selling is the revenue-generating arm of business, but we staff and treat sales people like the "born sales-person."

There are a number of ways people get into professional selling. First there is the "fast buck" chaser that sees a sales person buying a client lunch or playing golf, driv-ing a new car, dressing well, and says, "That's for me!" Yahoo, another sales person is born!

Or there is the "luck truck driver." A sales person quits and the boss looks around, "Let's make Charley a sales-man -- everyone likes him when he makes his deliveries." Obviously he is a "born sales person." Whoop-de-do --

another sales person is "born."

Believing that sales people are born justifies the Darwinian school of developing sales people. Why else would you put someone in sales and then not continuously train or nurture them? Why? Because they are "born," not made. After all, THEY ARE ONLY THE REVENUE RAISING ARM OF THE BUSINESS!

When I asked one of my clients what they had done before hiring me to work with their sales staff I was told, "We gave them a catalog, a car, and a kick in the a__!"

If you run the Darwinian program don't complain about sales or margins -- you're getting what you paid for.

Selling is a set of skills that can be learned by anyone who really wants to be in sales. In fact, many of the traits that most people associate with selling are not particularly desirable in a sales person. The "good fellow well met" may be looking for acceptance or a social outlet and not a profession. The brash center-of-attention may be looking to satisfy psychological needs that will go against them in selling. The extra-

vert that everyone says, "you should be in sales" is usually looking for attention to them selves, not seeking a profes-sion in selling.

That high-ener-gy dynamo that is out to change the world is ev-ery sales man-ager's dream. The "born" sales person who can "sell ice cubes to Eskimos" is

the fantasy of every sales manager's escapist dream. And, allowing that there may be some people who come out of the womb genetically mutated to be "born sales people," they are few and far between.

I would rather have a group of B+ players, dedicated to the profession of selling, than a group of ego-driven prima-donnas. I will get better long-term performance from the journeymen sales people with dedication and hard work than flash-in-the-pan superstars.

The fact is that you can't wait for that one-in-a-million sales person to ride through your door on the white horse and present him or herself to you. You should be building your sales program on the common clay that is readily available.

The

by Bob Ayrer

MyTh

$

Coal mines: surface and underground

coal truckmen

c

c

We offer Workers’ Compenasation Insurnace for:

quarries

sand and gravel digging

c

c

c

c

other types of mining

mining related risks

WWW.AMERICANMINING.COM

“insurance from people who know mining”

For more information, contact Bryant Brown, V.P. Marketing • 1.800.448.5621, x 249.

3490 Independence Drive • Birmingham, Alabama 35209

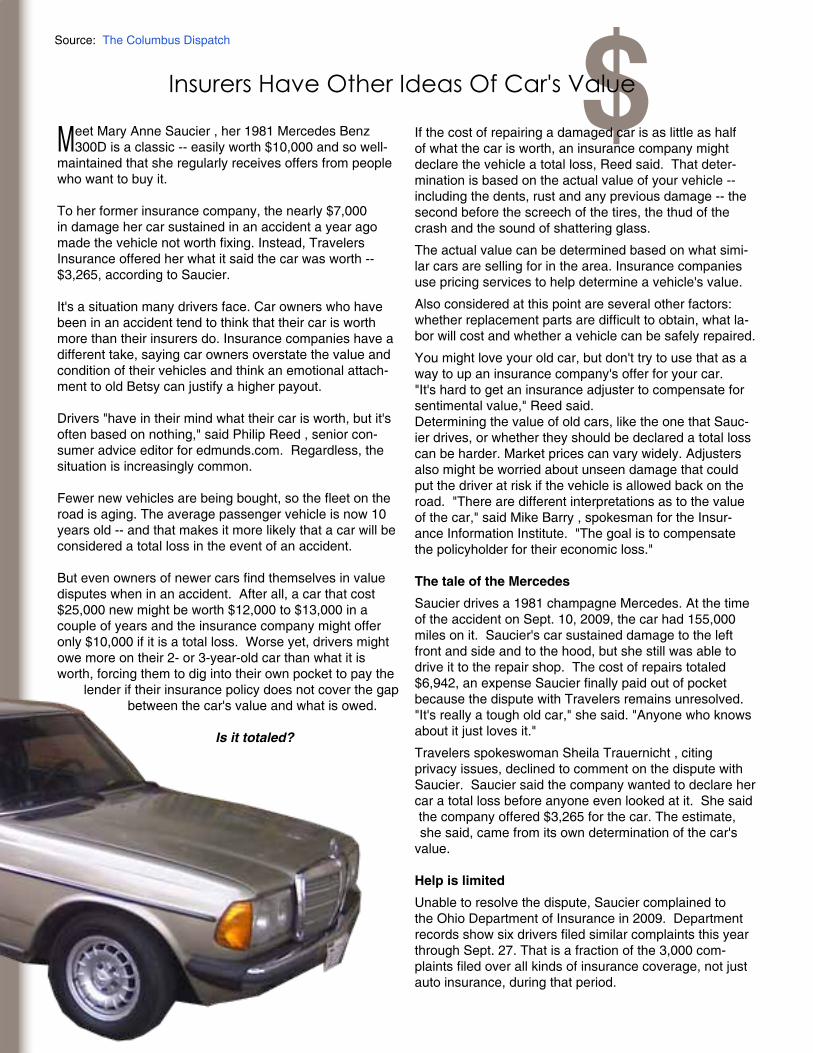

Meet Mary Anne Saucier , her 1981 Mercedes Benz 300D is a classic -- easily worth $10,000 and so well-

maintained that she regularly receives offers from people who want to buy it.

To her former insurance company, the nearly $7,000 in damage her car sustained in an accident a year ago made the vehicle not worth fixing. Instead, Travelers Insurance offered her what it said the car was worth -- $3,265, according to Saucier.

It's a situation many drivers face. Car owners who have been in an accident tend to think that their car is worth more than their insurers do. Insurance companies have a different take, saying car owners overstate the value and condition of their vehicles and think an emotional attach-ment to old Betsy can justify a higher payout.

Drivers "have in their mind what their car is worth, but it's often based on nothing," said Philip Reed , senior con-sumer advice editor for edmunds.com. Regardless, the situation is increasingly common.

Fewer new vehicles are being bought, so the fleet on the road is aging. The average passenger vehicle is now 10 years old -- and that makes it more likely that a car will be considered a total loss in the event of an accident.

But even owners of newer cars find themselves in value disputes when in an accident. After all, a car that cost $25,000 new might be worth $12,000 to $13,000 in a couple of years and the insurance company might offer only $10,000 if it is a total loss. Worse yet, drivers might owe more on their 2- or 3-year-old car than what it is worth, forcing them to dig into their own pocket to pay the

lender if their insurance policy does not cover the gap between the car's value and what is owed.

Is it totaled?

If the cost of repairing a damaged car is as little as half of what the car is worth, an insurance company might declare the vehicle a total loss, Reed said. That deter-mination is based on the actual value of your vehicle -- including the dents, rust and any previous damage -- the second before the screech of the tires, the thud of the crash and the sound of shattering glass.

The actual value can be determined based on what simi-lar cars are selling for in the area. Insurance companies use pricing services to help determine a vehicle's value.

Also considered at this point are several other factors: whether replacement parts are difficult to obtain, what la-bor will cost and whether a vehicle can be safely repaired.

You might love your old car, but don't try to use that as a way to up an insurance company's offer for your car. "It's hard to get an insurance adjuster to compensate for sentimental value," Reed said. Determining the value of old cars, like the one that Sauc-ier drives, or whether they should be declared a total loss can be harder. Market prices can vary widely. Adjusters also might be worried about unseen damage that could put the driver at risk if the vehicle is allowed back on the road. "There are different interpretations as to the value of the car," said Mike Barry , spokesman for the Insur-ance Information Institute. "The goal is to compensate the policyholder for their economic loss."

The tale of the Mercedes

Saucier drives a 1981 champagne Mercedes. At the time of the accident on Sept. 10, 2009, the car had 155,000 miles on it. Saucier's car sustained damage to the left front and side and to the hood, but she still was able to drive it to the repair shop. The cost of repairs totaled $6,942, an expense Saucier finally paid out of pocket because the dispute with Travelers remains unresolved. "It's really a tough old car," she said. "Anyone who knows about it just loves it."

Travelers spokeswoman Sheila Trauernicht , citing privacy issues, declined to comment on the dispute with Saucier. Saucier said the company wanted to declare her car a total loss before anyone even looked at it. She said the company offered $3,265 for the car. The estimate, she said, came from its own determination of the car's

value.

Help is limited Unable to resolve the dispute, Saucier complained to the Ohio Department of Insurance in 2009. Department records show six drivers filed similar complaints this year through Sept. 27. That is a fraction of the 3,000 com-plaints filed over all kinds of insurance coverage, not just auto insurance, during that period.

Insurers Have Other Ideas Of Car's Value

Source: The Columbus Dispatch

Coal mines: surface and underground

coal truckmen

c

c

We offer Workers’ Compenasation Insurnace for:

quarries

sand and gravel digging

c

c

c

c

other types of mining

mining related risks

WWW.AMERICANMINING.COM

“insurance from people who know mining”

For more information, contact Bryant Brown, V.P. Marketing • 1.800.448.5621, x 249.

3490 Independence Drive • Birmingham, Alabama 35209

But the department's authority is limited to making sure insurance companies comply with the law. It can't force an insurance company to increase its offer for a totaled car, for example. Just complaining might bump up an of-fer by a few hundred dollars, Reed said.

If you think you're entitled to more, go to work. Arm yourself with data from pricing guides and classified ads for used cars. Look for examples of similar cars selling for more than you are being offered for yours. Don't forget to take into account factors such as a vehicle's options, mileage, color and the ZIP code where it is being sold.

Saucier had her repaired car appraised at $10,500. She also found a similar car listed for sale at $9,995. Reed said a car's condition is often where drivers stumble. Many people believe their car is in outstanding condition, which could add $1,000 to its value.

Thomas Klepsky , of Cleveland was able to get his insurance company, Columbus-based Motorists Mutual Insurance, to boost its initial offer for his 2005 GMC Envoy from about $13,200 to $16,000, not counting his $500 deductible. But not without a four-month fight. He was able to show in great detail that his vehicle was in outstanding condition and had been carefully maintained and that similar vehicles went for more than the insurance company was offering. Even in the end, he still feels like

he was cheated by about $2,000.

"You have to kind of do this yourself, or you might as well take their initial offer". He said he finally agreed to a settlement after the company told him: "'This is it. Take it or leave it. We're not going to make another offer. We'll let that car rot into the ground.'"

Motorists spokesman Paul Richards declined to comment on Klepsky's case other than confirming the settlement. "What we try to do is reach a point where we are able to make our policyholders whole using as much information as is available to us," he said.

If all else fails

If you and the insurance company can't agree, you might be able to demand an appraisal. Each side picks an ap-praiser who chooses an umpire to evaluate the loss. If you and the company accept the appraisal, the results are binding. Klepsky said he had the option of using arbitra-tion, but he would have had to pay for it and he didn't trust that it would be fair.

Most people would accept what money they can get and move on. "The differential oftentimes ... is not so great as to warrant going down these paths," Barry said.

Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 15

Who has the ability to handle all your specialty insurance needs?

Albuquerque, New Mexico(866) 643-8538 / (505) 822-0018 / fax (505) 822-0092

scottsdale.burnsandwilcox.com

Global Resources. Local Relationships.

Professional Liability

Umbrella & Excess

Employment Practices

Commercial Property

Products Liability

General Liability

Commercial Auto

Personal Lines

is

The

is

TheAnswer

Your Specialty Insurance Professionals

20688 Burns_LaVoz_6.75x9.25.indd 1 1/15/08 3:54:25 PM

www. s c o t t s d a l e . b u r n s a n dw i l c o x . c om

www.s

cottsd

ale.

burn

sand

wilco

x.co

m

Who has the ability to handle all your specialty insurance needs?

Albuquerque, New Mexico(866) 643-8538 / (505) 822-0018 / fax (505) 822-0092

scottsdale.burnsandwilcox.com

Global Resources. Local Relationships.

Professional Liability

Umbrella & Excess

Employment Practices

Commercial Property

Products Liability

General Liability

Commercial Auto

Personal Lines

is

The

is

TheAnswer

Your Specialty Insurance Professionals

20688 Burns_LaVoz_6.75x9.25.indd 1 1/15/08 3:54:25 PM

Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 17

In the almost twenty years I've been consulting, writing, and speaking to insurance agency owners and manag-ers, the only topic that has consistently caused ire is when I discuss holding pro-ducers accountable and/or creating a set of standards by which all producers will abide.

This topic has resulted in hate letters, angry emails,

and an earful of yelling. I have been told I have caused irreparable harm for suggesting producers be held ac-countable. I have been told my articles and comments have caused rebellions, though not armed rebellions, by CSRs. I never dreamed of having such powers of persua-sion.

But let's imagine for a comical moment that I have such power to cause an agencies' staff to openly rebel just because they read an article I wrote. It is safe to say they would not rebel unless they were already unhappy. Why would they be unhappy? I can think of several reasons:

1. They do the work and the producer gets the credit and the pay.

2. The producers have no standards so the CSRs have to fill the gaps to get the job done.

3. Some producers meet the standards but others don't, without repercussion. (Perhaps this sounds better be-cause at least some producers are following rules, but it's not. It causes undue confusion and stress over who's responsible for what. The CSRs are under constant stress because they never know whether they'll be held respon-sible for someone else's mistakes simply because they do not know when it is and when it isn't their responsibility to take care of an issue.)

How does an agency stop a rebellion? A good place to start is with fair compensation. I am often asked about how much an agency should pay its staff. How much is far less important than how fair. And fair is not always paying people the same if the job is not the same.

If a CSR does all the work on a renewal but the producer gets paid for it, where is the fairness? Moreover, where is the common sense? Why pay someone for doing nothing? The issue is not who does more. The issue is who gets paid for doing the work. It does not matter how much of the renewal the producer does versus the CSR.

Whatever mix works best for a particular agency is the right answer for that agency. Good management though dictates that the pay follow the workload.

From a production perspective, how does paying a pro-ducer full price for less work motivate them to produce more business? How does allowing producers to ignore procedures help the agency? Certainly they have far more time, but is it resulting in more growth? Most of the time it doesn't.

How beneficial is it to create an environment in which highly paid people are allowed to be slackers? How motivating is it to work in that environment? How does it generate growth? How does it utilize scarce resources wisely? Of course, by not addressing the issue, peace with those producers is maintained, but peace has a price. I've been in lots of peaceful agencies that are going nowhere fast, incurring significant E&O exposures, and seeing staff churn.

When CSRs get upset about producers not being held accountable, it pays to listen. They almost always have a point. However, they are often not articulating the issue correctly. The problem is the producers are not being managed effectively and that is damaging the agency's profit, growth, and value. Sure, the producers are peace-ful. But is it worth the price at the expense of more profits, more growth, and higher agency values?

Rebellion with a Cause?

by Chris Burand

Page 16 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

trust.acuity.com

Page 16 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 19

Go to your agency's Web site right now. Look at the home page. Put yourself in the mind of a random

person who doesn't know your agency from any other agency. Now look at the page and ask yourself, "What is it they want me to do?"

If you can't immediately answer that question, your Web site needs work.

Most agency Web sites were originally created in the late 90s as a response to the growth of the Internet and search engines. Many people, including myself, said that an agency needs to have a Web site so that they have a presence on the Internet. In response to this, most agencies had a Web site created that was simply an electronic version of their printed agency brochure.

I would argue that even the term "agency Web site" needs to change. In today's hyper-connected world, you need to create a strategy for your "online presence," not just your "agency Web site."

Your online presence will include a combination of multiple Web sites, an agency blog, a Facebook page, a LinkedIn presence for all producers and staff, a Twitter account for customer service, a YouTube channel for agency videos, Google Places for local search, and who knows what else in the next few years.

Along with Duke Williams, I have created the Agency Inter-net Boot Camp as a way to help agencies understand how to create a strategy for their "online presence" and how to start implementing that strategy.

While content is still what gets people to interact with you, it's also your ability to interact with customers and pros-pects via heightened functionality that kicks off the process of engagement—the new success metric. It's not enough for your content to simply be there, flat and uninviting. It has to stand up and practically beg people to interact with it. Your Web site must be more Web app-like than browser-like.

What does this mean for your agency, you ask? Here are a few thoughts:

• Use blog software as the engine: Blog software, such as WordPress, is essentially content management software with SEO, community, and syndication built in. I can think

of very few instances where it would not make sense for an agency to use a tool like WordPress to run their entire Internet presence.

• Get feedback: People are getting used to sites that allow them to offer ratings and reviews. This type of functional-ity is easy to offer and can give social reassurance—if the reviews are good—to visitors considering your agency.

• Beef up your content: In terms of traffic, Google is the number-one search engine, but YouTube is number two. Adding video and audio content has become a must, as visitors expect it and consume it in ways that keep them on your site much longer than sites that feature only static text.

• Integrate Social Media: Adding Facebook "Like" buttons that allow visitors to share your content with their friends is an effective way to allow Facebook visitors to interact with your site. Plugins (e.g. Sociable) make it very easy for people to share, subscribe, and bookmark content found on your Web pages.

Having an agency Web site is just not enough anymore. Creating a comprehensive strategy that integrates all aspects of your online presence will help you become more visible to prospects and to retain clients.

Your Web Strategy Must Changeby Steve Anderson

Page 18 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Page 18 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Taking Advantage of TrustedChoice in your Community and

with your Customers

By Richard McKenny, CIC, National Trusted Choice Board Member

As a New Mexico Trusted Choice member, you are afforded many free options to promote your agency with your community and your customers. We know that your agency is busy and how hard it is to look for new ideas to promote your agency and retain business. By going to the Trust-ed Choice website (www.trustedchoice.com) you will find many ideas and unique tips to promote your agency over the competition.

Below, are just a few ideas that you can easily take from the Trusted Choice website and paste into your agency newsletters, or day to day correspondence to your customers or your local media. Just click on the Trusted Choice website and you will see how easy it is!

General Insurance Topics• 3 Insurance Questions• Business Insurance• Does Volunteering Your Time Mean Volunteering Your Insurance?• Do you need life insurance?• Insuring Significant Others• Is your health insurance right for you?• Life Insurance• Saving Money on Insurance• Travel Insurance• Why you need an umbrella

Commercial Insurance Topics• Discontinued Operations• Insuring the Theft of Customer Information

Homeowners Insurance Topics• Flood Insurance• Home Renovations and Updating Your Insurance

• Homeowners Undervaluation• Is your home fully insured?• Power Surges• Tree Roots and Sewer Lines

Seasonal Insurance Topics• Hurricane/Flood Insurance• Pool Safety• Prepare your home for winter• Protect Christmas Gifts• Spring Safety Checklist• Summer Party Safety• Valentines Day Valuables• Water Safety• Winter Fire Risks

Insurance Topics for Gadgets• Illegal Music Downloads• Is GPS Covered by your Auto Policy?• Mobile Devices - Does Insurance Tag Along?

www.trustedchoice.com

Imagine you have a long time friend and customer…

let’s call her Mary. Imagine you have written insurance for her businesses for more than 20 years. Imagine

Mary calls you and tells you she is starting a new busi-ness and needs to get her BOP/CGL, workers compen-sation, and all the other usual coverages for this new business. Imagine you think you know everything about her and her businesses. Imagine you get some basic information from her and then complete the applications for her. Imagine Mary comes to your office to sign the applications, but because she’s in a hurry to go talk to her banker, she tells you she’s sure everything is fine and she doesn’t read or review the applications, she signs them and leaves. Imagine you didn’t insist that she review the applications. Imagine you send them to the carriers, the policies are issued and all is well. Just imagine…

Imagine six months later Mary calls you and tells you that one of the employees of this new business has severely injured their back and she needs you to contact the work-ers compensation carrier to report the claim. Imagine you ask her where the employee was injured and she tells you it was while he was working in the neighboring state. Imagine your surprise when you hear the words “neigh-boring state”, because remember, you know everything about Mary’s business, except that she had employees working in a neighboring state. Imagine, because you never considered she would do that because she never had before. Imagine, because you didn’t include “all states” coverage on the workers compensation policy. Imagine, the carrier denies the workers compensation claim because coverage is limited only to the home state.

Imagine the claim is a minimum of $500,000. Imagine the next call you make is to your E&O carrier.

The reality is that this story happens. Maybe not exactly like this, but it happens. It may not be a business cus-tomer but it happens with homeowners or personal auto policies or virtually every other type of policy available. Regularly. So what can you do about it? Simple: don’t complete applications for your customers. “But that’s not good customer service.” Actually, it is because having your customer complete the application gives them an op-

portunity to really look at what they do and what they want insured. Who knows this better than themselves? Regard-less of how well you think you know your customer, things change. What was true yesterday, may not be true today.

Does that mean you can’t help them if they have ques-tions? Of course not. That is exactly what customer ser-vice is all about. But the responsibility to provide accurate information belongs to your customer. If the information on the application is not correct and they filled it out, then they are responsible. If the information on the applica-tion is not correct and YOU filled it out, then YOU may be responsible especially if you did not have them review the application. It’s as simple as that.

So imagine your longtime friend and customer Mary calls you and tells you she has a new business. Imagine you send her the insurance applications. Imagine….

This article is intended to be used for general informational purposes only and is not to be relied upon or used for any particular purpose.

Swiss Re shall not be held respon-sible in any way for, and specifically disclaims any liability arising out of or in any way connected to, reliance on or use of any of the information contained or referenced in this article. The information contained or referenced in this article is not intended to constitute and should not be considered legal, ac-

counting or professional advice, nor shall it serve as a substitute for the recipient obtaining such advice. The views expressed in this article do not necessarily represent the views of the Swiss Re Group ("Swiss Re") and/or its subsidiaries and/or management and/or shareholders.

*Richard F. Lund, JD, is an Assistant Vice President of Swiss Re/West-port, underwriting insurance agents errors and omissions coverage. He has also been an insurance agents E&O claims counsel and has presented numerous E&O loss control seminars nationwide, including several for the Missouri Association of Insurance Agents.

imagine...

reality...

By Richard F. Lund, J.D.*

Page 22 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 21

Bringing VIP Service to Surplus Lines Insurance

Superior Customer Service! 24 Hour Quotes

Transportation: Submit quick quotes via our Website and get 24 hr service. All lines of Transportation risks up to 4 units. Let us help you out service your competitors. Visit us today at www.lsrinc.org

Multi Peril: Experience our WEB Rating/Quote System. Establish your own password for Instant Quotes!

Applications and Forms On Line Simplify your work! Find all the forms you need for all of our markets on our web site:

www.lsrinc.org

Policy Changes On Line Save time and energy and make your policy changes efficiently by email! Send to:

For peace of mind you’ll receive emailed confirmations of your change request.

Mobile Underwriters We come to you!

We’ll send an underwriter to work in your office for 2 days at our cost.All we ask is that you keep them busy.

VISIT OUR WEBSITE: www.lsrinc.org

El Paso, TX -Tel. 800-592-1027 Albuquerque, NM- Tel. 888-767-9005 San Antonio, TX- Tel. 888-818-6601 Phoenix, AZ-Tel. 800-592-1027

Page 22 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Page 24 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

An insurer recently sent its agency force a "Good News!" bulletin advising that it was no longer

necessary to send it copies of most certificates of insurance. The bulletin also pointed out that it was the responsibility of the agent to notify the certifi-cate holder of cancellation. What should agencies do when told by a carrier not to send copies of certificates? This question was recently raised (for the nth time) by one of our member agencies:

Question: "One of our companies doesn't want us to send them cop-ies of the certificate of liability insurance. My question is two part:

"1) The certificate of liability form states the 'issuing INSURER will endeavor' to notify the certificate holder of cancellation...how can the agency be held responsible for notification for what is stated clearly the carrier's responsibility?

"2) If the company doesn't want a copy of the certificate, why should the agency start notifying certificate holders?"Should agencies assume the responsibility of what is the carrier's duty? Does the agency have a legal exposure? If yes, then how do you suggest agencies respond?"

Answer:I taught my first E&O class close to 20 years ago. The is-sue of cancellation notice was addressed then and prob-ably had been for years. In general, E&O carriers recom-mend that agents not provide notice of cancellation to insureds, mortgagees, loss payees, certificate holders, or anyone else. Cancellation is the dissolution of a contract.

The parties to the contract are the insured and insurer, not the agent. Ancillary parties either have a contractual right of notice under the policy (e.g., mortgagees and some loss payees) or they don't (most certificate holders, even if ad-ditional insureds). Only a party to a contract can cancel it and that party is the one charged with the responsibility of notice.

I recently participated in a teleconference on this and related issues. An E&O carrier representative and attorney participating in the call advised, regardless of the carrier's

directive, that certificates should be copied to the insurer. You're right...the certificate says that the insurer, not the agent, will endeavor to provide notice of cancellation. Without a copy of

the certificate, that would be impossible and issuance of the certificate would appear to be a sham. In a court hear-ing, how would it look if the plaintiff's attorney accuses the carrier and agency of fraud or misrepresentation for making a claim they clearly had no intention of comply-ing with? (Note: For the ethics of this practice, check out "Certificates of Insurance: Will You 'Endeavor To' Be Ethical.")

In general, since the parties to the contract are insurer and insured, agencies should NOT be sending out can-cellations to anyone. If it's absolutely necessary, then EVERYONE should be getting such notices. Agencies should insist on hold harmless agreements with carriers who do not intend to comply with certificate provisions that they will endeavor to provide notice of cancellation.

We have an article called "Certificates and Court Cases" that outlines a number of situations where agents have been found liable for activities involving certificates of insurance. One such case was brought to my attention recently. In Marlin v. Wetzel County Board of Education, 569 S.E.2d 462 (West Virginia Ct. App., 2002), "[t]he in-surance company asserted that it never received the cer-tificate of insurance or any other document suggesting the insurance policies needed to be amended" to make the Board an additional insured. According to the court, "[The insurer] does not dispute that its agent issued a certificate of insurance listing the Board as an additional insured.

Instead, [the insurer] argues that it had no knowledge of the certificate's existence, and therefore could not modify the actual policy to include coverage for the Board."In addition, most recently (June 2009) in Erie Insurance Group v. National Grange Mutual Ins. Co., the New York Supreme Court found the insurer not responsible in part because it never received a certificate of insurance:A portion of the insurance policy issued by NGM to McClary stated, "Each of the following is added as an Additional Insured . . . [a]ny general contractor, subcon-tractor or owner for whom you are required to add as an

Should Agents Send Certificates to Insurers?

Page 24 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 25

HomeownersCatastropheInsuranceTrust

Your preferred homeowners clients deserve the broadest possible coverage for their homes and personal property. As an active

member of IIANM, you have the original -- the very best such program available to you right now.

The HCIT Difference in Conditions (DIC) policy supplements basic homeowners coverage by providing

protection for catastrophic losses, including FLOOD and EARTHQUAKE.

Just contact:

Trustco, Inc. - HCIT Program Administrator 2063 East 3900 South Ste. 100,Salt Lake City, UT 84124 1-800-644-4334 / Fax: 801-278-9051

Bobbi Phillips / [email protected] Kingdon / [email protected]

www.hcitins.com

additional insured on this policy under a written construc-tion contract or agreement where a certificate of insur-ance showing that person or organization as an additional insured has been issued and received by [NGM] prior to the time of loss." [emphasis added]

One possible reading of the provision is that the con-struction contract or agreement to list someone as an additional insured must be in writing, and a certificate of insurance listing that person or organization must be issued and received by NGM prior to the loss-inducing incident. The provision could also be read as containing two alternate ways of including a person or organization as an additional insured: if a written construction contract so requires, regardless of whether NGM is ever notified; or if any agreement -- oral or written -- so requires and a certificate of insurance listing that person or organization is received by NGM prior to the loss-inducing incident.

Regardless of which interpretation is used, the policy's contractual requirements have not been satisfied so as to include Pine Ridge as an additional insured. The record does not contain a written contract or agreement between McClary and Pine Ridge. Nor did anyone introduce a cer-tificate of insurance listing Pine Ridge as an additional in-sured, let alone proof that such a certificate was sent to or received by NGM. In fact, NGM's employee affirmed that by Bill Wilson

no such certificate was ever received. [emphasis added]

Under the first reading of the policy provision above, plaintiffs cannot prevail because the agreement between Pine Ridge and McClary was not in writing and no per-tinent certificate of insurance was issued or received by NGM. Under the second reading, the first alternative is not met due to the lack of a written contract or agreement and the second alternative is not met due to the lack of the required certificate of insurance. [emphasis added]

Ideally, agents should continue to provide copies of certificates to insurers and insurers should "endeavor to" provide notice of cancellation to certificate holders. The alternative is for insurers to provide agents with an ironclad hold harmless agreement that will defend and indemnify agents for claims or suits involving certificates issued on behalf of parties insured by such carriers.For additional questions and answers about certificates, check out the articles, "Following Up on Certificates of Insurance" and "Certificates of Insurance Q&A."________________________________________"Thank you" to Bill Wilson for this great article. Bill is the Associate VP of Education & Research for the Indepen-dent Insurance Agent & Broker of America and Director if the Big "I" Virtual University.

Page 26 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

client numbers are relatively low, you do not know how successful you have become unless you have a frame of reference.

Once the agency baseline and total insurable population was determined, we began designing a specific combina-tion of internet, media and targeted marketing methods that would sequentially present the agency and its mes-sage to the residents of the local area. We chose a se-quential approach instead of a simultaneous approach in order to measure the activity and results of each method. Measurement of the results is as important a key to suc-cess as making the sale.

A marketing campaign was proposed that included media advertising for name and image recognition, bill boarding to get the agency’s message and motives to the target population, internet presence to permit the computer liter-ate younger people to inquire at their leisure and targeted marketing to chosen local communities consisting of homogeneous and relatively affluent residents. A local advertising agency was solicited on behalf of the client to schedule and budget the entire campaign.

Before the first dollar was spent and the first advertising performed, we knew, as did the agent, the targeted goals of the program, the cost and expected return, the monthly benchmarks that would gauge the agency’s success and the MSL (Minimum Success Level) below which the program would be considered unsuccessful and therefore be terminated. The advertising agency was able to ‘fine tune’ the components of the program to yield the best results based on the sequential presentation and both the activity of each segment.

A marketing campaign is much like a behavior modifica-tion diet to an overweight person. It must be life-changing and continuous or it will eventually fail causing all of the lost weight to be regained (something that many of us Yo-Yo Dieters’ recognize after dozens of years of weight loss and weight gain).

Every agency has its own set of unique strengths and weaknesses. An advertising and marketing program must be tailored to the strengths and away from the weakness-es of the agency and of the agent. Each agency will find

How to Conduct and Measure Advertising and Marketing Campaigns

Reprinted from the PIPELINE by Al DiamondA few years ago Agency Consulting Group, Inc. visited an

agent who boasted about continuous strong advertising and marketing efforts but bemoaned the lack of growth in his agency. Our consultants asked the Agency for the marketing layout and the results. His “continuous strong marketing and advertising efforts” consisted of a full one page ad in the Yellow Pages.

Agency Consulting Group, Inc. began to assist him to cre-ate a true marketing campaign; the campaign was de-signed to spread the advertising over several media types with effective methods to gain a higher visibility among the prospects and to drive more of client to the agency as the preferred insurance professional to handle their asset protection needs.

Whenever Agency Consulting Group, Inc visits an agency, we ask for a record of new business, proposals and prospects over a multi-year period. Two issues are being judged: the effectiveness of the agency’s sales and marketing programs and if agents are even aware of their successes and failures.

The agent only realized that he was having problems when his overall commission income dropped below what he remembered having in the prior year. It was get-ting worse, so he called on Agency Consulting Group to remedy his problem. He immediately assumed that his new business was down and that the cause was market related because of the declining economy in his area. He had no idea of the effect of changing rates, his own reten-tion rate of clients and the secondary effects of changing rates, his own retention rate of clients or the secondary effect of rewriting business to maximize client savings.

But “gut feel” is sometimes intuitive. We measured his retention rate and found it to be over 95% with only five or ten rewrites each month. The agent was right. His marketing method, attracting new residents to the area, was having substantially diminished results. He needed a new way to attract prospects for his products and services through advertising and implementation of a marketing campaign that would yield new prospects and clients for his agency.

We began by identifying the number of total households in his geographic marketing area – his demographic prospect base. Then we determined how many clients he already had insured to determine the agency’s current penetration level. This is critically important. Even if the

Page 26 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 27

a set of advertising and marketing programs that will work to present the agency with more opportunities to grow its customer base. Changing economy (insurance and/or general) will require changing advertising and marketing methods. Only effective record-keeping will permit you to know when you’ve found the right formula for success – and when that formula no longer works and must be refined and revised.

“Begin with the End in Mind” (effectively stolen from Ste-ven Covey). Don’t start any advertising campaign to sim-ply stir up activity. It will drain your pocketbook and leave you hungry. Have a short term (one year) and long term (three to five year) goal that qualifies through the ROAM (Realistic, Objective, Achievable, and Measureable) test.

No, you can’t grow in an unlimited way and get more people as you need them. You are limited by your current staff (how many calls can you take every day?), by your production capabilities (what would you do if you had 50 prospects contact you tomorrow asking for a visit within the next week?) by your markets, (what would you do with hundreds of homeowners asking for insurance if you are on the Coast and are not invited to write homeowners by your current carriers?) and even by your own personal capabilities. Structure your growth path in a comfortable way that “fits” your personality and your organization.Don’t begin a marketing campaign until you know your own statistics and demographics.

Don’t let anyone (including your ad agency) convince you to do multiple advertising methods until you have tested each in a logical sequence to determine how effective each method is alone.

Keep score of the activity related to the programs you implement as well as the results. This means that you must count the responses as well as the sales calls, pro-posals and sales. Keep a budget of costs and results that will be your bible for future marketing efforts.

Finally, once you find the formula that brings you the right number of prospects and clients, keep advertising, extend the marketing efforts and realize that the tide will continue to change. You will find that you must alter your methods to meet the current conditions in order to keep your marketing efforts successful.

You can get started with help from

a new member benefit of IIANM.

Full Name:

First Name for Badge:

Agency / Company:

Address:

City, State, Zip:

Telephone:

Fax:

The pre-licensing classes are designed to be a review for the state licensing examination. We recommend that students be familiar with the study material prior to attending class.

Study materials are NOT included in class prices.

Pre-Licensing Classes

E-Mail:

Method of Payment:

Bill Agency (Members Only)

Check Enclosed (Payable to IIANM)

M/C Visa Disc Amex

Amount: (all prices include tax)

Card No:

Exp. Date:

Signature:

( )

Send in your registration:

Fax in:(505) 243-3367

Mail in:1511 University Blvd. NEAlbuquerque, NM 87102

Give us a call:(505) 843-7231 (800) 621-3978

Go on-line:www.iianm.org or E-mail:

The FINE PRINT: IIANM reserves the right to cancel/reschedule classes. Please call ahead to verify when classes will run. Decisions will be made three days prior to class. Cancellations received after 5 business days, will be assessed a $50.00 cancellation fee. Cancellations received on or after deadline and ‘no shows‘ will forfeit the registration fee altogether. A substitute is always welcome, with no extra fee, but prior notification would be appreciated.

Class Name/Date:

( )

Instructor: Jack Cleary - November 9 - 10 8am - 5pm Instructor: Jack Cleary - December 7 - 8 8am - 5pm

Property & Casualty Review Class (2 days)

Regular Price: $150 Member Price: $120

Life & Health Review Class (1 day)

Regular Price: $115 Member Price: $90

Instructor: Manny Mansour - November 11 8am - 5pm Instructor: Bob Ouellette - December 9 8am - 5pm

Insurance Education Programs in New Mexico are critical to a successful and profitable career in the insurance industry. Every year, we offer exciting opportunities to expand your professional horizons. All of these education programs are designed to help insurance agents thrive in the most competitive of marketplaces.

EducationEDGEIIANM’s

Pre-Licensing Study Materials

To see a list of what is available and to purchase your study materials online, click here.

Page 28 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Click here for a full listing of our education program.

Page 28 Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010

Cla

ssifieds

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

12 13

14 15 16 17 18 19 20

21 22 23

P&CPre-licensing

Class

P&CPre-licensing

Class

L&HPre-licensing

Class

- Click on a class to register online - CE = continuing education hours

4 5 61

24 27

28

25 26

29 30

November's Clickable Calendar

32

Independent Insurance Agents of New Mexico - www.iianm.org - * November 2010 Page 29

11

We’ve re-vamped our Job Bank. Looking to fill a position within your agency? Trying to find a job but don’t know where to look?

Whether you are looking for somewhere new to share your special skills or an employer looking for quality, professional employees, we are there to lend a helping hand.

Click here to take advantage of IIANM’s Career Center.

Do you have an agency you’re trying to sell, or in the market to buy one? Check out our Classifieds!

New Mexico’s Job Bank

8 97 10

Office

Closed Office

Closed

The benefits of increasing sales while lowering E&O exposure have Big “I” members from across the country flocking to purchase the Big I Advantage® Virtual Risk Consultant Powered by Rough Notes (VRC).

And those who have purchased it are glad they did. A recent survey of registered VRC users found that 92% were extremely satisfied and would recommend VRC to other agents.

Starting at $250 a year, the VRC is an easy-to-use agency resource website offering:

Risk Exposure Analysis Tools:Commercial and personal risk exposure analysis information at your fingertips with hundreds of industries, including narrative descriptions, minimum coverages and suggested WC, ISO GL, SIC and NAIC codes.The popular “Coverages Applicable” material, customized questionnaires and E&O coverage checklists are also included.

Reference and Proposal Tools:Reference materials to make sure agency staff understands the product they are selling and help create winning proposals. Included are access to ACORD forms, PF&M and a glossary of insurance terms.

Marketing and Prospecting Tools:Access to articles on various insurance topics that the agency can share with customers, post on their websites or use to create a client newsletter. There are also hundreds of professionally-written building business letters so you can spend more time selling and less time writing.

Gain a competitive advantage by purchasing the exclusive VRC today.Visit www.independentagent.com/VRC to learn more, view a product demo and purchase the tool.

Virtual Risk Consultant a “No-Brainer for Most Agencies”

Decrease E&O exposure and increase sales with this valuable tool.

can u bliev nm is banning txtng while dri-

More Adults are Now Texting

According to a new report from Pew Research Center's Internet & American Life Project, 72% of American adult cell phone users now send and re-ceive text messages, up from 65% last November.

Teens continue to text more than adults with 50 messages a day "on average," in contrast to the "typical 10 text messages sent and received by adults" every day, Pew said. The non-profit organi-zation compared the results of its survey of 2,252 adults with a survey it did previously on the cell phone habits of teens ages 12 to 17.