Not-for-Profit Organizations Exposed Presented by: Donna Cassidy Executive Underwriter.

34

Not-for-Profit Organizations Exposed Presented by: Donna Cassidy Executive Underwriter

-

Upload

jasmin-bryan -

Category

Documents

-

view

215 -

download

0

Transcript of Not-for-Profit Organizations Exposed Presented by: Donna Cassidy Executive Underwriter.

Not-for-Profit Organizations Exposed

Presented by:

Donna Cassidy

Executive Underwriter

Agenda

• Section I: Vulnerabilities– Employment Practices Liability– Directors and Officers Liability– Fiduciary Liability– Crime

• Section II:Product Solutions

Not-for-Profit Organizations At Risk

Not-for-Profit Organization’s dealings with donors, employees, volunteers, customers or recipients of services, suppliers, vendors, other not-for-profit organizations, government agencies and creditors all pose risks to the Organization and it’s Directors and Officers

and Are currently operating without a safety net when it comes to management liability and professional liability exposures.

Vulnerability: EPL

An employee could sue for wrongful dismissal, or discrimination.

A client, customer or vendor could sue for discrimination or sexual harassment.

• In many ways the risks are no different than that of a Public or Private Company

• Unique in the respect that NFP organizations rely on people to bring the mission statement to life, but ofter serving that mission takes priority over serving the employees.

Unique to NFP’s: Employment Practices Liability

Employment Practices Liability• Wrongful dismissal• Employment Discrimination• Employment Harassment• Negligent Evaluation• Wrongful Discipline• Wrongful deprivation of a career

opportunity• Failure to promote

Third Party Liability

• Clients, Customers or Vendors

• Discrimination or Sexual Harassment

Employment Practices Liability

Employment Practices Liability

• Coverage gaps exist with GL, Umbrella and D&O policies.

• Breach of employment contract not covered under the traditional liability policy.

• Exclusions in GL and Umbrella policies for intentional acts and employment-related matters.

Vulnerability: D&O

The Risk: A donor, recipient of services or other NFP organization sues for misrepresentation, breach of duty or error.

Allegations can threaten the personal assets of D&O’s. Personal liability of directors can be the same for NFP’s as public companies.

Indemnification is not a certainty.

Unique to NFP’s

• Every dollar is to go to the mission.

• Training courses, manuals, corporate governance, and outside legal advice is curtailed as the Organization focuses on spending every dollar on its mission.

Duties of Directors and Officers

Not just an issue for public company executives. In many ways the duties are the same…

• Duty to Manage the Organization

• Duty of Care/Diligence

• Business Judgment Rule

Who can sue?

• Donors• Employees• Volunteers• Customers• Recipients of Services• Suppliers• Vendors• Other Not-for-Profit Organizations• Government Agencies• Members• Creditors

D&O

• Standard components involved in defending yourself in a civil suit:

• Pleadings • Factual Investigations• Motions and Cross-Examinations on Affidavits• Discovery• Experts• Legal Research and Analysis• Mediation and/or Arbitration• Pre trial conference• Trial• Appeals

Where can claims come from?• Breach of Fiduciary duty

• Mismanagement of assets

• Negligent supervision

• Conflict of interest

• Misrepresentation

D&O Loss Scenario

• An author sued a business association over misappropriation of materials as association did not receive proper permission to use materials in its journals. Defence costs: $495K.

• Agricultural association of cattle changed the standards for Grade A animals, causing some members herds to quality as top grade. They sued for economic damages and injunctive relief. Defence and settlement: $2.1M.

Vulnerability: Fiduciary LiabilityThe Risk: A retiree or employee could sue

the organization and its plan fiduciaries for a breach in its fiduciary duty.

Fiduciary Liability

• Administrative Errors & Omissions for Pension Plans and Health and Welfare Plans including Government Plans

• Liability coverage for Organization sponsored Pension Plans and Health and Welfare Plans

Fiduciary Loss Scenario

Administrative Error • An employee at a charity died in a car accident. The primary

beneficiary of his group life insurance, claimed the life insurance benefit paid to her under the benefit plan should have been five times her deceased husband’s salary, not the two times his salary granted. The association denied the claim. She sued alleging that her husband had requested the amount be changed from two times to five times just weeks prior to his death. The charity denied that any change had been requested.

• After the charity investigated the widow’s claim, it learned that indeed her spouse had requested a change in his benefits, but that the request had not been properly processed. The association settled the claim for more than $250,000 after spending over $25,000 in defence costs.

Vulnerable to Crime

My employees would never steal from me or the mission that they are entrusted to execute.

No organization is immune to the potential losses of an embezzlement scheme.

Unique to NFP’s

• Assets have been “entrusted” to the not-for-profit organization

• Every dollar is to deliver on the mission statement, there is no surplus

Crime Loss Scenario

• A trade association’s HR manager set up a phony consulting firm and billed the organization for consulting services that were never provided. The theft was detected upon annual audit. The manager has stolen more than $500,000.

• The payroll clerk for a NFP organization added several relatives to the payroll. This continued for three years. The clerk stole more than $300,000.

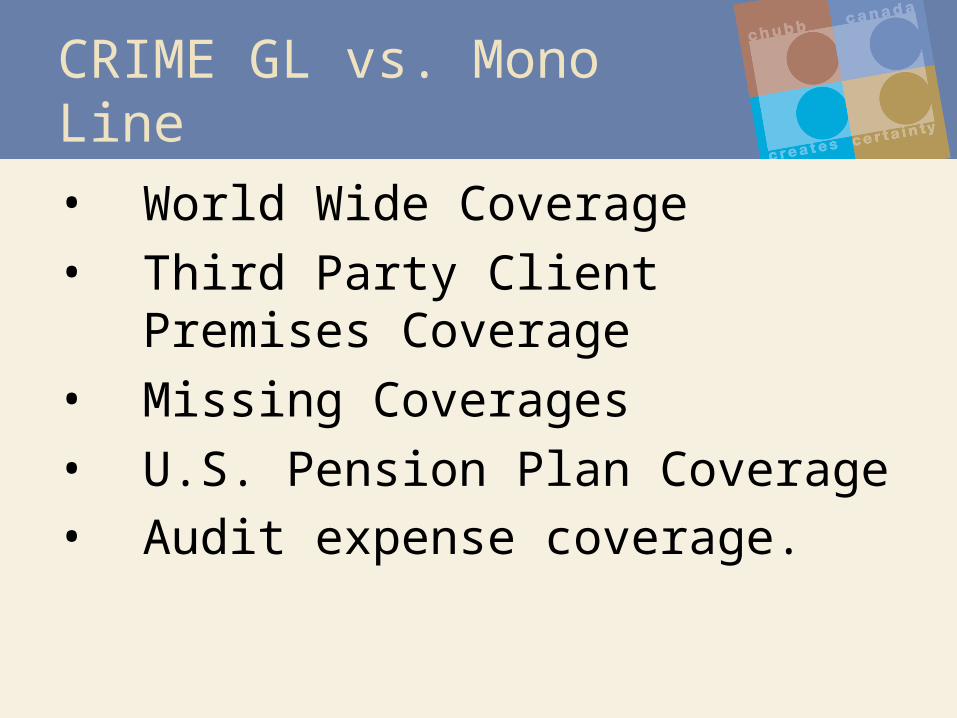

CRIME GL vs. Mono Line

• World Wide Coverage

• Third Party Client Premises Coverage

• Missing Coverages

• U.S. Pension Plan Coverage• Audit expense coverage.

Section II: Product Solutions

Product Solutions

• Not for Profit Organization Liability Policy – D&O, EPL, ODL (and F/L if Enhancement

End’t), +

• Enhancement Endorsement

• Stand-Alone Executive Protection Policy with Crime and Kidnap/ Ransom and Extortion Coverage Sections

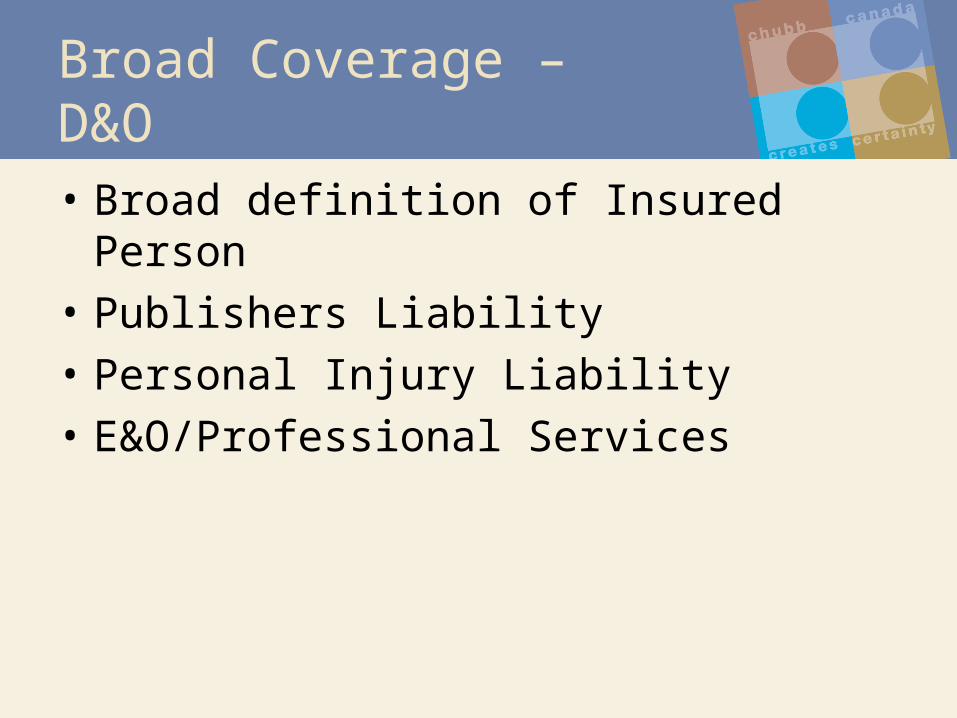

Broad Coverage – D&O

• Broad definition of Insured Person

• Publishers Liability

• Personal Injury Liability

• E&O/Professional Services

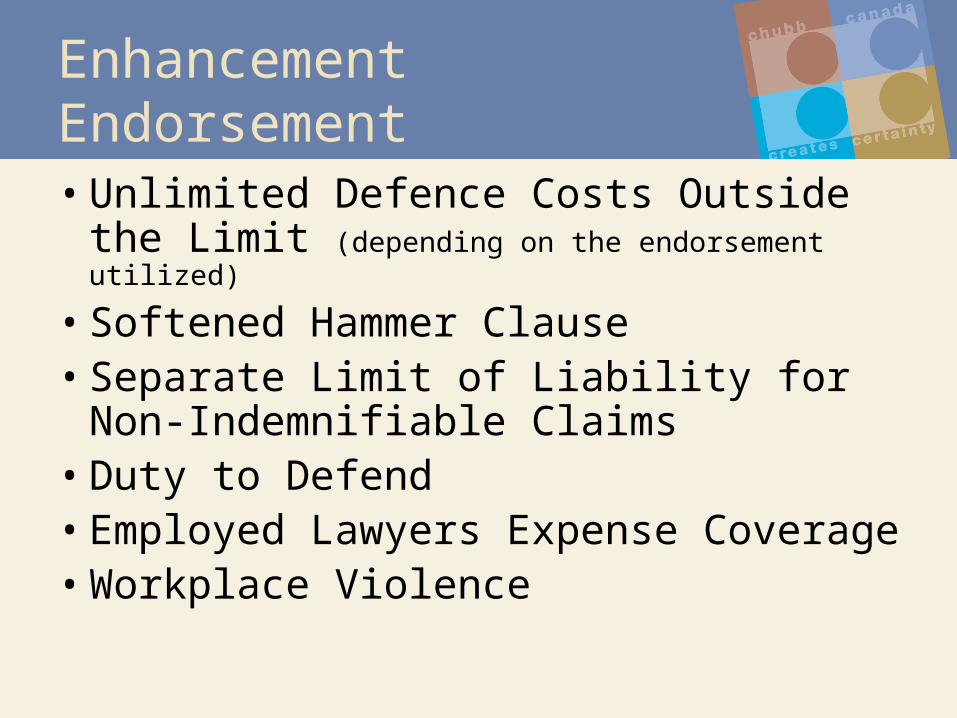

Enhancement Endorsement• Unlimited Defence Costs Outside the

Limit (depending on the endorsement utilized)

• Softened Hammer Clause• Separate Limit of Liability for Non-

Indemnifiable Claims• Duty to Defend• Employed Lawyers Expense Coverage• Workplace Violence

Overview of Bill 168 (Workplace Violence)

According to Bill 168,the Occupational Health and Safety Amendment Act (Violence and Harassment in the Workplace):

“workplace harassment” means engaging in a course of vexatious comment or conduct against a worker in a workplace that is known or ought reasonably to be known to be unwelcome

Overview of Bill 168 (Workplace Violence) • All employers are required to prepare

policies with respect to workplace violence and workplace harassment and to review these policies no less than once per year

• Workplace violence risk assessments

• Protecting workers from domestic violence

• Disclosure of persons with a history of violence

• Right to refuse work where health or safety is in danger

What Does this mean For Your Business?

• Employers are required to update policies, develop programs and conduct risk assessments with respect to workplace violence and harassment

Enhancement Endorsement• Fiduciary Liability Coverage• Worldwide Blanket Not-for-Profit Outside

Directorship Coverage• Third Party Discrimination and Sexual

Harassment Coverage• Broadened I vs I Exclusion• Pollution Defence Coverage• Defence Coverage for Bill C-45 and

Manslaughter Claims

Bill C-45 (Amendment to the Criminal Code)

Bill C-45 (Section 217.1 in the Criminal Code):

• Created rules for establishing criminal liability to organizations for the acts of their representatives.

• Establishes a legal duty for all persons "directing the work of others" to take reasonable steps to ensure the safety of workers and the public.

• Sets out the factors that courts must consider when sentencing an organization.

• Provides optional conditions of probation that a court may impose on an organization.

Enhancement Endorsement• Coverage for Punitive and Exemplary Damages

(where insurable by law)

• Broad Definition of Insured Person• Pre-Determined Allocation for Defence Costs• Spousal Coverage• Non-Cancelable by Chubb except for non-

payment of premium• Broad Severability• Non-rescindable Side A

Why Chubb?

• Commitment to the D&O market. In Canada for 30 years.

• Product offering is best-in-class• Choice and Flexibility with limits and

coverages including manuscripting• Claims Handling in Canada with a well

deserved reputation for fair and prompt service to our customers

• Financial Strength

Email Submissions or Questions to:

General questions and enquiries:1-416-359-3222 ext. 4339

Product Information and Applications:www.chubbinsurance.com

Contacting Chubb