NORDIC RETAIL MARKET ANALYSIS -...

50

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Transcript of NORDIC RETAIL MARKET ANALYSIS -...

NORDIC RETAILMARKET ANALYSISAUGUST 2016

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

TABLE OF CONTENTS2

Foreword 3

Acknowledgements 3

Executive Summary 4

1.0 Introduction 5

2.0 Retail Environment 6

2.1 History of the Region 6 2.2 Consumer Socio-Demographics 8 2.2.1ConsumerSocio-DemographicProfile,Denmark 9 2.2.2ConsumerSocio-DemographicProfile,Finland 9 2.2.3ConsumerSocio-DemographicProfile,Norway 10 2.2.4ConsumerSocio-DemographicProfile,Sweden 10 2.3 Economic Fundamentals 11 2.4 Economic Prospects 12 2.4.1EconomicProspects,Denmark 12 2.4.2EconomicProspects,Finland 13 2.4.3EconomicProspects,Norway 13 2.4.4EconomicProspects,Sweden 14 2.5 Retail Landscape 15 2.5.1RetailerPresence 15 2.5.2RetailFormat 16 2.5.3RentalDynamics 20

3.0 Consumer Preferences and Behaviour 22

3.1 Preferred Shopping Location 23 3.2 Frequency and Duration of Visit 24 3.3 Purpose of Shopping Centre Visit 26 3.4 Factors important when choosing a shopping centre 29 3.5 Travelling to a shopping centre 31 3.6 Interaction with technology during the shopping journey 32

4.0 Retailer Insight 35

4.1 Perception of the Nordic Market 35 4.2 Market Opportunities 37 4.3 Consumer Perceptions 38 4.4 Retailer Strategies 41 4.5 Expansion Plans 44

5.0 Conclusions 45

5.1 Region-Wide Considerations 45 5.1.1Denmark 48 5.1.2Finland 48 5.1.3Norway 49 5.1.4Sweden 49

TABLE OF CONTENTS

NORDIC RETAIL MARKET ANALYSIS AUGUST2016

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Inrecentyears,retailershaveincreasinglybeguntolookattheNordicsas

anattractivemarketforexpansion,ledbythecapitalcitiesofStockholm,

CopenhagenandOsloand,toaslightlylesserextent,Helsinki,fuelledbythe

region’seconomicgrowthprospects,ahighlevelofaffluenceandanexpanding

population.

InternationalretailerpresenceintheNordicsiscurrentlylowcomparedwithother

Europeancountriesand,despitemanystrongdomesticbrands,thereisahealthy

appetitefromconsumersfortheintroductionofnewmainstreamfashion-oriented

andluxuryretailersfromaroundtheworld.

Retailerexpansionintheregionis,however,dependantontheavailabilityof

suitablespaceanddevelopershaverespondedtothisgrowingdemandwitha

numberofhighqualitynewdevelopmentsemergingoverthepastfewyears,most

recentlyexemplifiedbyUnibail-Rodamco’sonemillionsqft‘MallofScandinavia’,

whichopeneditsdoorsinNovember2015.

DespitetheclearappealoftheNordicsasawhole,itisimportanttorecognise,

however,thattheregioncomprisesfourverydistinctindividualretailmarkets

–Denmark,Finland,NorwayandSweden–eachwiththeirownunique

characteristicsandstructures–theacknowledgementandunderstandingof

whicharecrucialtoasuccessfulretailerstrategy.

Thisreportseekstohighlightthekeyconsiderationsforretailerswhoarelooking

toexpandtoanyofthefourmajorretailmarketsintheNordicregionwithregard

totheirindividualeconomic,socio-politicalandculturalcharacteristicstoenable

themtoidentifywheretheopportunitiesareforexpansionandensurethattheir

brandstrategyistailoredtotheuniqueneedsanddesiresofDanish,Finnish,

NorwegianandSwedishconsumers,ratherthanauniversal‘Nordicconsumer’.

FOREWORD

Jean LambertICSC,VicePresident, Research

Sarah ColeICSC,Managerof InternationalResearch

AcknowledgementsThisreportwaspreparedbyCBRELimitedandwasreviewedandeditedbyICSCResearch.SpecialthankstoBrenna

O’Roarty(RHLStrategicSolutions)andSandraGreisman(TheRetailHeadquartersAB)fortheirsupportandadvice.

InternationalCouncilofShoppingCenters

29QueenAnne'sGate

LondonSW1H9BU

UnitedKingdom

+442079763100

www.icsc.org/europe

3

FOREWORD

FOREWORD

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

4 2.0 RETAIL ENVIRONMENT

Key findings of the study are:• Thecountriesareallsmall,open,export-led,mixed

economies.However,thecompositionoftheunderlying

exportmarketsvariessignificantly,resultingindivergent

economicperformanceandprospects.

• Theregionisaffluentandwealthiswidelydistributed

acrossthepopulations,withtheNorwegiansbeing

themostaffluentandtheFinnstheleast.Focusingon

comparativewealthwithintheregion,however,might

mistakenlyleadtoFinlandbeingdiscountedgiven

itsspendingpotentialsignificantlyexceedstheEU

average.

• Theretaillandscapeisdominatedbyshoppingcentres

inFinland,NorwayandSweden,inpartduetotheharsh

winterclimatethatfavoursenclosedretailformats.This

ismirroredinshoppingbehaviour,withupto40%of

consumersvisitingshoppingcentresatleastoncea

week,inNorway,SwedenandFinland,whilethisfallsto

alittleover20%inDenmark.(InDenmark,high-street

retailingpredominates.)

• Retailersmustbecognisantofthedifferentconsumer

attitudes,currencies,regulationsandcompetitorswithin

eachmarket.Forexample,Sundaytradinghoursvary

acrossthemarketsandwhileconsumerist,Swedesare

priceconsciouswhileNorwegiansfavourlocallysourced

products.

• Theyoungest(16-24)andoldest(55-65)agecohorts

havethestrongestpreferenceforshoppingcentresin

Denmark,NorwayandSweden.InFinland,the25-34

yearsoldsaremoreengaged.

• Inadditiontovisitingstores,whichremainstheprincipal

reasonforvisitingshoppingcentres,consumersalso

identifyshoppingcentresassocialspaces,witha

strongpropensitytomeetfriendswhentheyvisit.This

isparticularlystrongamongsttheyoungerageprofile.

Althoughthissupportsfoodandbeverage(F&B)

servicesinshoppingcentres,thelevelofengagement

isloweracrossallNordicmarketscomparedwithother

Europeancountries.Yet,consumersalsoindicated

thatincreasingtheF&Bofferwouldencouragethemto

frequentshoppingcentresmoreoften.

• Thepenetrationofinternationalretailersislowrelative

tootherEuropeanmarkets.Tosomeextentthisisdue

tostrongdomesticbrandsinkeysegments(e.g.,fast-

fashion)butalsoasaresultofalackofunderstanding

oftheopportunitiesineachmarket.Theconsumer

opportunityinthesemoreaffluentmarketsanda

shifttowardscity-ratherthancountry-ledexpansion

strategies,isincreasingcross-borderretaileractivityin

theregion.Suchretailersarefocusedoneithercapital

ormajorcitiesandincomparisontodomesticbrands,

arehesitanttoexpandtowhatmightbeconsidered

moresecondarycities/locations.

• TheperceptionoftheNordicmarketsdiffersamongst

retailers,andthisismanifestinbusinessstrategies.

RetailersfromwithintheNordicsregionvieweach

countryasadiscretemarketandtailorstrategies

accordingly,withstorenetworksmanagedatanational

level.Incontrast,internationalretailershaveatendency

toconsidertheregionasonehomogeneousmarketand

manageitaccordingly.

TheNordicregionisoftenreferredtoasasingle,homogeneousretaileconomy.Althoughtheysharesomesocio-political

andculturalsimilarities,Denmark,Finland,NorwayandSwedeneachhaveadistinctretailmarketplace.Thisisevident

ineconomicstructureandcycles,legalframeworks,theretailhierarchyandconsumerbehaviour.Understandingthese

differencesisessentialtoidentifyingtheopportunitiesineachcountry,requiringthedevelopmentofassetmanagementand

retailerstrategiestailoredtoeachmarket.

NORDIC RETAIL MARKET ANALYSIS AUGUST2016

4

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

TheNordicregioncomprisesDenmark,Finland,NorwayandSwedenandeach

countrypossessesadistinctretaillandscape.Asharedhistoryandintra-regional

tradingagreements,withsomecommonalityoflanguageinthecountriesmaking

upScandinavia,haveoftenresultedinthemisconceptionthatretailstrategiesin

oneNordiccountrycanbereadilyappliedtoothermarketsintheregion.While

Nordiccountrieshavesomepoliticalandsocio-economicsimilarities,witheach

beingasmall,mixedandexport-ledeconomy,thecountrieshavedistinctsocio-

politicalculturesandeconomiccycles.Thisaimofthisresearchistoclearly

distinguishtheretaileconomieshousedwithintheNordicregion,toidentifythe

roleofshoppingcentreswithintheretailhierarchyandhighlightdifferencesin

consumerbehaviour,andtoconsiderifandhowthesedifferencesimpactretailer

businessstrategiesacrosstheregion.

ThisreportsetsouttheretailopportunityintheNordicsandconsidershowit

differsacrossandbetweencountrieswithintheregion.First,thesocio-economic

contextisconsidered,examiningtheconsumerprofilewithintheregionand

evaluatingopportunitiesagainstprevailingeconomicprospectsandtheretailreal

estatelandscape.Second,theroleofshoppingcentreswithintheretailhierarchy

isassessedforeachmarketfromtheconsumerperspective.Theanalysis

evaluatescentreattributesthatarekeytoattractingandretainingcustomers.

Third,theresearchconsiderstheimplementationofretailerstrategiesacrossthe

regionandhowtheydifferacrossthemarketsandbetweendomesticandcross-

borderretailers.Finally,theretailopportunityofeachmarket

issummarised.

Theresearchfindingsarebaseduponadesktopanalysisof

existingliteratureanddatainordertoevaluatethecurrent

retailenvironment.Aquestionnairewasundertakenwitha

representativesampleofconsumersineachcountrytofurther

buildonthisknowledgebase,andspecificallytoidentify

consumerbehaviourandpreferencesinregardtoshopping

centres.Inordertogainamoredetailedunderstandingof

retailerstrategiesintheregionandhowtheymightdifferacross

countries,structuredinterviewswereundertakenwithretailers.

Abroadrangeofretailersexperiencedintheregionwere

interviewed,includingthosewithestablishedretailbrands,

fascias,retailersthathadenteredandlaterwithdrawnfromone

ofmoreofthemarkets,andretailersthatareintheprocess

ofenteringatleastoneoftheretailmarketswithintheregion.

While Nordic countries have some political and socio-economic similarities, with each being a small, mixed and export-led economy, the countries have distinct socio-political cultures and economic cycles

5

1.0 INTRODUCTION

1.0 INTRODUCTION

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

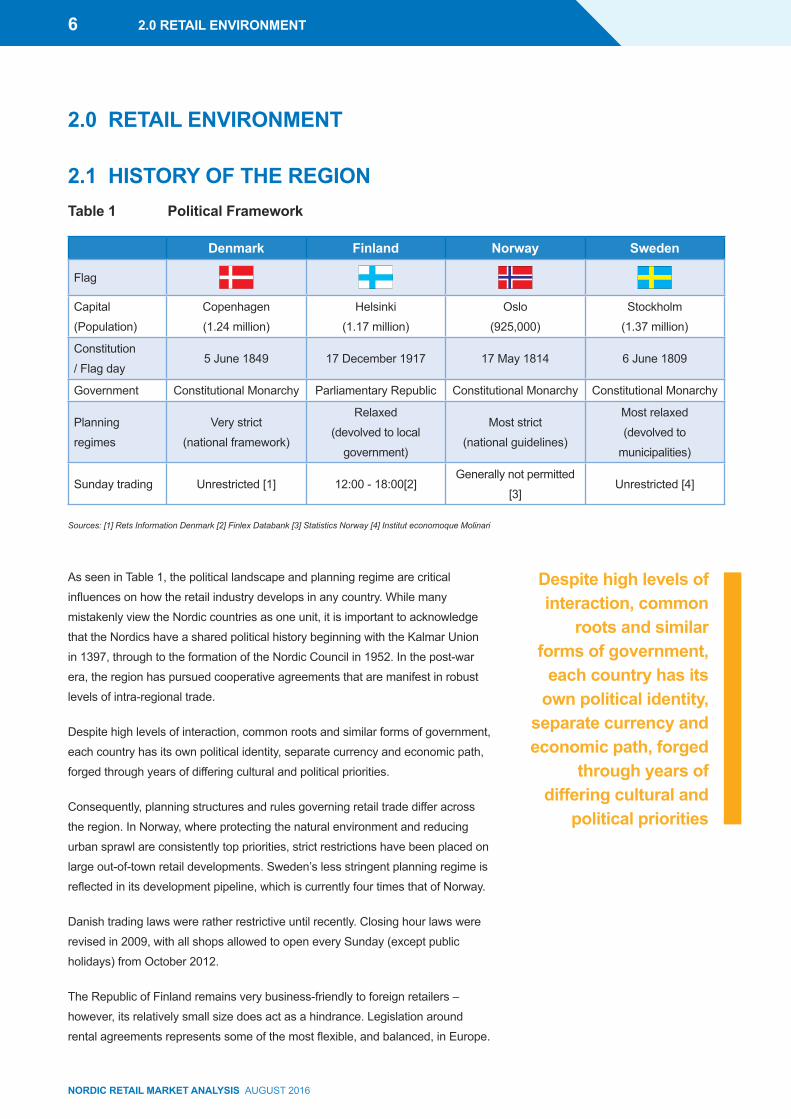

AsseeninTable1,thepoliticallandscapeandplanningregimearecritical

influencesonhowtheretailindustrydevelopsinanycountry.Whilemany

mistakenlyviewtheNordiccountriesasoneunit,itisimportanttoacknowledge

thattheNordicshaveasharedpoliticalhistorybeginningwiththeKalmarUnion

in1397,throughtotheformationoftheNordicCouncilin1952.Inthepost-war

era,theregionhaspursuedcooperativeagreementsthataremanifestinrobust

levelsofintra-regionaltrade.

Despitehighlevelsofinteraction,commonrootsandsimilarformsofgovernment,

eachcountryhasitsownpoliticalidentity,separatecurrencyandeconomicpath,

forgedthroughyearsofdifferingculturalandpoliticalpriorities.

Consequently,planningstructuresandrulesgoverningretailtradedifferacross

theregion.InNorway,whereprotectingthenaturalenvironmentandreducing

urbansprawlareconsistentlytoppriorities,strictrestrictionshavebeenplacedon

largeout-of-townretaildevelopments.Sweden’slessstringentplanningregimeis

reflectedinitsdevelopmentpipeline,whichiscurrentlyfourtimesthatofNorway.

Danishtradinglawswereratherrestrictiveuntilrecently.Closinghourlawswere

revisedin2009,withallshopsallowedtoopeneverySunday(exceptpublic

holidays)fromOctober2012.

TheRepublicofFinlandremainsverybusiness-friendlytoforeignretailers–

however,itsrelativelysmallsizedoesactasahindrance.Legislationaround

rentalagreementsrepresentssomeofthemostflexible,andbalanced,inEurope.

Sources: [1] Rets Information Denmark [2] Finlex Databank [3] Statistics Norway [4] Institut economoque Molinari

Denmark Finland Norway Sweden

Flag

Capital

(Population)

Copenhagen

(1.24million)

Helsinki

(1.17million)

Oslo

(925,000)

Stockholm

(1.37million)

Constitution

/Flagday5June1849 17December1917 17May1814 6June1809

Government ConstitutionalMonarchy ParliamentaryRepublic ConstitutionalMonarchy ConstitutionalMonarchy

Planning

regimes

Verystrict

(nationalframework)

Relaxed

(devolvedtolocal

government)

Moststrict

(nationalguidelines)

Mostrelaxed

(devolvedto

municipalities)

Sundaytrading Unrestricted[1] 12:00-18:00[2]Generallynotpermitted

[3]Unrestricted[4]

Table 1 Political Framework

Despite high levels of interaction, common

roots and similar forms of government,

each country has its own political identity,

separate currency and economic path, forged

through years of differing cultural and

political priorities

6

2.1 HISTORY OF THE REGION

2.0 RETAIL ENVIRONMENT

2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Forinstance,leasescanbeterminatedifagreedbetweentheparties.Tenantsare

responsibleonlyforinternalrepairsandareoftencompensatedforimprovements.

SundaytradinginFinlandwasintroducedin1994,withmoreliberalisedtrading

hoursacrosstheweekintroducedin2009.

Norway,despitebeingoutsideoftheEuropeanUnion,remainsconnectedto

itsinternalmarketplacethroughtheEuropeanFreeTradeAssociation(EFTA).

Presently,storesareprohibitedfromlateeveningSaturdaytradingandare

generallynotallowedtoopenmostSundaysunlesstheymeetverystrictcriteria

–e.g.smallerthan100squaremetres(sqm),locatedintransporthubsorinhigh-

traffickedtouristareas,etc.RecentproposalstorelaxSundaytradinglawswere

metwithobjectionsfromlabourunionsaswellasretailersandconsumers.

Largelyduetoitsmixedeconomyandpoliticalstability,Swedenisoften

consideredaparticularlysuccessfulpost-industrialisedsociety.Unlikeinother

NordicandlargeEuropeancountries,tradinglawsarelargelyrelaxedand

unregulated,havingbeenliberalisedintheearly1970s.Retailersarefreetoopen

everydayoftheweek,withnorestrictionsonSundaytrading.However,labour

costsareoneofthehighestinEurope,withworkerspaidmorethanthestandard

wageonSundays.Thesewagesarethereforeprohibitivelyhighforsome.While

planninglawsremainregulated,planningislargelydecentralisedandrelatively

laxcomparedtoDenmarkandNorway.

72.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

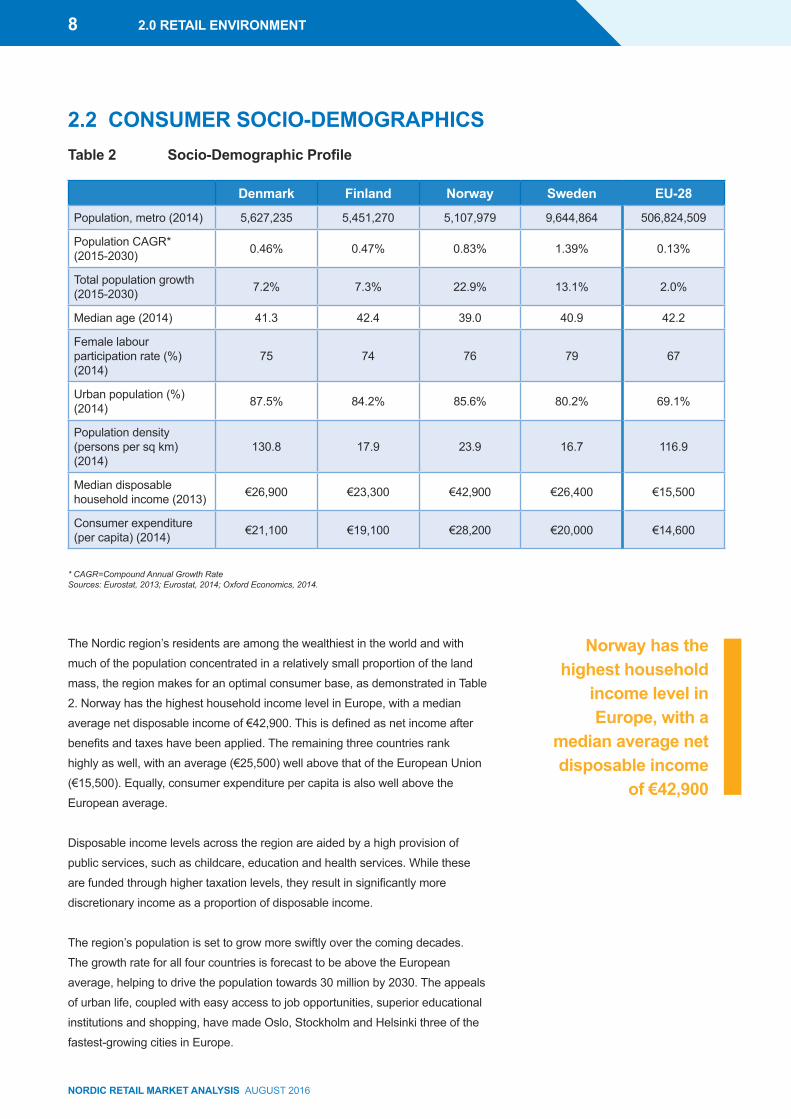

TheNordicregion’sresidentsareamongthewealthiestintheworldandwith

muchofthepopulationconcentratedinarelativelysmallproportionoftheland

mass,theregionmakesforanoptimalconsumerbase,asdemonstratedinTable

2.NorwayhasthehighesthouseholdincomelevelinEurope,withamedian

averagenetdisposableincomeof€42,900.Thisisdefinedasnetincomeafter

benefitsandtaxeshavebeenapplied.Theremainingthreecountriesrank

highlyaswell,withanaverage(€25,500)wellabovethatoftheEuropeanUnion

(€15,500).Equally,consumerexpenditurepercapitaisalsowellabovethe

Europeanaverage.

Disposableincomelevelsacrosstheregionareaidedbyahighprovisionof

publicservices,suchaschildcare,educationandhealthservices.Whilethese

arefundedthroughhighertaxationlevels,theyresultinsignificantlymore

discretionaryincomeasaproportionofdisposableincome.

Theregion’spopulationissettogrowmoreswiftlyoverthecomingdecades.

ThegrowthrateforallfourcountriesisforecasttobeabovetheEuropean

average,helpingtodrivethepopulationtowards30millionby2030.Theappeals

ofurbanlife,coupledwitheasyaccesstojobopportunities,superioreducational

institutionsandshopping,havemadeOslo,StockholmandHelsinkithreeofthe

fastest-growingcitiesinEurope.

Denmark Finland Norway Sweden EU-28

Population,metro(2014) 5,627,235 5,451,270 5,107,979 9,644,864 506,824,509

PopulationCAGR*(2015-2030) 0.46% 0.47% 0.83% 1.39% 0.13%

Totalpopulationgrowth(2015-2030) 7.2% 7.3% 22.9% 13.1% 2.0%

Medianage(2014) 41.3 42.4 39.0 40.9 42.2

Femalelabourparticipationrate(%)(2014)

75 74 76 79 67

Urbanpopulation(%)(2014) 87.5% 84.2% 85.6% 80.2% 69.1%

Populationdensity(personspersqkm)(2014)

130.8 17.9 23.9 16.7 116.9

Mediandisposablehouseholdincome(2013) €26,900 €23,300 €42,900 €26,400 €15,500

Consumerexpenditure(percapita)(2014) €21,100 €19,100 €28,200 €20,000 €14,600

Table 2 Socio-Demographic Profile

* CAGR=Compound Annual Growth RateSources: Eurostat, 2013; Eurostat, 2014; Oxford Economics, 2014.

Norway has the highest household

income level in Europe, with a

median average net disposable income

of €42,900

8

2.2 CONSUMER SOCIO-DEMOGRAPHICS

2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.2.1 CONSUMER SOCIO-DEMOGRAPHIC PROFILE, DENMARK

Denmark,atjustover5.6million,isthesecond-largest

countryintheregion.Withabirthrateandimmigration

levelslowerthanotherScandinaviancountries,Denmark’s

populationisnotexpectedtogrowassignificantlyoverthe

comingdecadesasNorwayandSweden.By2030,the

populationisforecasttobe6.1million,thelowestgrowth

leveloftheregionat7.6%.

At89.5%,Denmark’shighpopulationdensity,coupled

withitssmallsize,hasledtothehighesturbanisationrate

bothwithintheNordicbeltandthewiderEuropeanregion.

Copenhagen,AarhusandOdense,thethreelargestcities,

accountformorethan30%ofDenmark’stotalpopulation.

OECDfiguresrankDenmarkashavingthehighest

incomeequalityofanyEUmembercountry.This,

coupledwithamedianhouseholdincomeof€26,900,

hashelpedDenmarkachieveconsumerexpenditure

levelssome44%abovetheEUaverage,althoughwell

abovetheEUpublicspending.Danishconsumersspend

markedlymoreoneducationalservicesasapercentage

ofoverallhouseholdexpenditure.Conversely,household

spendingonfurnishingsandhouseholdgoodsisthe

lowestintheregion.

2.2.2 CONSUMER SOCIO-DEMOGRAPHIC PROFILE, FINLAND

Finland’spopulationreached5.5millionin2014.

Traditionally,Finlandhasexperiencedlowlevelsof

populationgrowth,duetorelativelylowbirthratesand

minimalinwardmigration.Atanationallevel,thesetrends

aresettocontinuewithpopulationgrowthrateforecasts

beingbelowotherNordiccountriesoverthecoming

decades.However,urbanisationtrendsareresultingin

strongpopulationgrowthforitslargestcities.

Thethreelargestmetropolitanregions,Helsinki,Tampere

andTurku,arehometonearly40%ofFinland’spopulation.

TheHelsinkiMetropolitanArea(HMA)comprisesa

conurbationofthreecitiesandaccountsfor25%of

Finland’stotalpopulation,with1.4millionresidents.

Overall,nearly85%ofFinland’spopulationliveinurban

areas,ahigherratethantheUnitedKingdom,theUnited

StatesandFrance.

RelativetootherNordiccountries,Finland’saverage

householdincomeislow.However,comparedwith

otherEuropeancountriesitremainsnoteworthy.Incomes

inFinlandaremorethan10%higherthantheeconomic

powerhousesofFrance,GermanyandtheUnited

Kingdom.Lowlevelsofincomeinequalityhave

contributedtoFinland’shighlevelsofdisposableincome

andconsumerexpenditure.Thisisamajordrawfor

retailersenteringthemarket.

TheFinnishconsumerspendsproportionallymorethan

otherNordicconsumerswithrespecttofood,alcoholic

beveragesandrestaurants.Interestingly,expenditureon

cateringservicesinparticularis20%higherforFinnish

householdsrelativetotheDanishand75%higherthan

Norwegianhouseholds,highlightingthehighertendency

ofFinnishhouseholdstoeatout.

92.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.2.4 CONSUMER SOCIO-DEMOGRAPHIC PROFILE, SWEDEN

2.2.3 CONSUMER SOCIO-DEMOGRAPHIC PROFILE, NORWAY

NorwayisthesmallestNordiccountry,withapopulation

of5.1million.Ofthis,nearly30%or1.5millionlivewithin

theOsloregionand44%livewithinthethreelargestcities:

Oslo,BergenandTrondheim.Populationgrowthhasbeen

robustinrecentyears,drivenbylargeinwardflowsof

migrantsandasubsequentincreaseinfertilityrates.This

hasresultedinNorwayhavinganunexpectedlyyouthful

population,withamedianageof39years,significantly

belowneighbouringcountries.Projectionssuggestthis

issettocontinue,withthepopulationforecasttoreach

6millionwithinthenexttenyearsandnearly8million

by2050.

InternalmigrationalsoplaysapowerfulroleinNorway,

withmajorcities’populationshavingexpandedsignificantly

inrecentyears.Indeed,Norwayhasthehighesturban

populationgrowthrateintheNordicsandoneofthehighest

inEurope.Asthepopulationcontinuestoconcentratein

afewcorecities,networkplanningacrosssuchalarge

countrybecomessignificantlyeasier.

WhilealltheNordiccountriesranksignificantlyhigherthan

theEUandWesternaveragesformostincomefactors,

Norwayregularlytakesthetoppositionintheregionand

therestoftheworldwithrespecttoaveragehousehold

income,disposableincomeandconsumerexpenditure.

Indeed,consumerexpenditurepercapitainNorwayis

€28,200,nearlytwicetheEU-28average.

Asaresultofhighdisposableincomelevels,theNorwegian

consumerhasanincreasedpropensitytospendonluxury

andhigh-endgoods.Therelationshipbetweenprice

andqualityremainsimportanttoNorwegians,withmost

optingtospendonqualitygoodsoverdiscountbrands.

Expenditureonoutdoorapparelandsportinggoodsis

markedlyhigherthanotherNordiccountries,highlighting

Norwegiansgenerallovefornature,theenvironment

andoutdooractivities.Additionally,asapercentage

ofconsumerexpenditure,Norwegianhouseholds

spend20%moreoverallonclothingthantheir

Nordicneighbours.

Sweden,withapopulationof9.6million,isthelargest

countryintheNordicregion.Forecastsplacethe

populationinexcessof10millionby2020andjustunder

11millionby2030.ThevastmajorityofSweden’scurrent

populationisconcentratedwithinthesouthernandeastern

regions.Theseregions,particularlytheareasalongthe

southwesterncoast,areprojectedtoseethehighest

populationgrowthrates.

Swedenis,forthemostpart,ethnicallyhomogeneous;

however,itskeycitiesarehighlydiverse,andhistorically

verywealthybyEuropeanstandards.Thishasresulted

inhighlevelsofimmigrationandinternalmigration,

particularlytocorecities.Notably,Stockholmisexpected

toseea17%increaseinitspopulationby2020–

comparedwithLondon(+9.0%)andParis(+3.5%).

Presently,thethreemetropolitanareas,Stockholm,Malmö

andGothenburg,accountfor40%ofSweden’spopulation.

Despitehavingoneofthehighestnetsavings-to-

disposableincomeratiosinEurope(11.5%),Sweden

alsohashighlevelsofhouseholdexpenditureand

overalldisposableincome.Swedishconsumersare

generallyconsideredtrend-conscious,earlyadopters

anddemandingbuyerswhovalueandembracenew

internationalretailbrands.

10 2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.0 RETAIL ENVIRONMENT

TheNordicregionismadeupofsmall,economicallyopencountries,withlarge

export-drivenmarkets.Highlevelsoffiscalresponsibilityhavehelpedtheregion

remainfinanciallystableandsolvent.Whiletheeurozoneasawholeisstill

feelingtheilleffectsoftheGlobalFinancialCrisis(GFC),therelativeeconomic

performanceoftheNordicregionhasbeenstrong,withGDPforbothNorwayand

Swedensurpassingtheirpre-recessionmarketpeaksasearlyas2013,before

anyotherEuropeancountries.

Whiletherearenumeroussimilarities,includinghighfemaleparticipationrates

inthelabourmarket,highlevelsofproductivityandgeneralfiscalstability,the

countriesarequitedistinct,asdemonstratedinTable3.Denmark’seconomy

remainslessvolatileduetoitsfocusonfast-movingconsumergoods,while

Norway’sfortunehashistoricallybeenfuelledbytheNorthSeaoilindustry.

Despiteyearsofrobustgrowthandstrongeconomicfundamentals,countries

withintheregionarecurrentlyexperiencingdivergenteconomiccycles.

TheNorwegianeconomyhascomeunderpressurefromfallingoilprices,while

inFinland,thedeclineinfortunesforitstechnologysector,resultantweak

domesticdemandandeconomicsanctionsbetweentheEUandRussia,akey

tradingpartner,havenegativelyimpacteditsgrowthtrajectory.Incontrast,the

DanisheconomicrecoveryissolidifyingandSweden’seconomyhasoutpaced

allgrowthexpectations.EconomicforecastsfortheregionareabovetheEU

average,althoughnear-termeconomicprospectsdiffersignificantly.

Source: Oxford Economics, 2014

Denmark Finland Norway Sweden Eurozone

2014GrossDomesticProduct(GDP)growth(%)

1.1% -0.04% 2.2% 2.4% 0.9%

2015/2016GDPforecast(%)

1.7%/2.0% -0.03%/0.9% 1.1%/0.8% 2.4%/2.7% 1.7%/1.9%

Unemployment(%)(Nov2015)

4.8% 10.0% 4.2% 8.0% 11.1%

ConsumerPriceIndex(%)–latest

0.7% -0.2% 2.6% -0.4% 0.2%

Industrialoutput(y-on-y%change)

-3.2% -5.1% 5.1% 3.3% 1.6%

Retailsalesvolumegrowth(Q1’10-Q1’15)

0.0% 4.1% 10.7% 15.1% -0.1%

Privateconsumptiongrowth2014(%)

0.7% -0.1% 2.0% 2.5% 1.0%

Interestrate(%) -0.75% 0.05% 1.0% -0.35% 0.05%

Table 3 Key Economic Variables

While there are numerous similarities, including high female participation rates in the labour market, high levels of productivity and general fiscal stability, the countries are quite distinct

2.3 ECONOMIC FUNDAMENTALS

112.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Source: Oxford Economics, 2014

2.4.1 ECONOMIC PROSPECTS, DENMARK

Geopoliticaltensionsandeconomicuncertaintywithinthe

eurozonehavenotbeenenoughtodampenDenmark’s

economicprospects.(SeeTable4.)Althoughthemarket

recoveredin2009,thehousingcrashinpreceding

yearsdraggedontheeconomy,togetherwithausterity

measuresrequiredtorestorebudgetaryimbalances.

Consumerconfidencedeteriorated,stiflingspendinginthis

consumeristeconomy.Asaresult,Denmarkexperienced

threeyearsofeconomicstagnationbeforerecoveringto

growthof1.1%in2014.Over2015,theDanisheconomic

recoveryhasslowlyaccelerated,supportedbyarecovery

inhousepriceswhichhasbeenacatalystforreleasing

pent-upconsumerspending.GDPgrowthof1.7%and

2.4%isforecastfor2015and2016respectively.

Expectationsofhighereconomicgrowtharelargelydue

totherecoveryofexportmarkets,lowinterestratesand

increasedconsumption.Improvingeconomicconditions

bodewellforretailsales,whichsuffereduntilthehousing

marketbegantorecoverthisyear.Retailtrade,having

peakedin2007,sawsteadydeclinesforsixyearsbefore

bottomingoutover2013.Retailsalesexpandedby1.2%in

2014,makingitthefirstfullyearofgrowthforthismeasure

since2007.Consumerconfidencehasreachedarecord-

highduring2015andbymid-yearthiswastranslatinginto

strongerretailsalesgrowth.

Draggeddownbyfallingfoodpricesandthesignificant

dropinglobaloilprices,inflationremainslow,standingat

0.5%inJune2015.However,lowinflationhasresulted

inrealwagegrowthaswellasanincreaseindisposable

income,up1.9%year-on-year.

2015f-2019f Denmark Finland Norway Sweden

Totalconsumerspending

growth7.4% 6.2% 8.0% 12.1%

Retailsalesgrowth 12.2% 13.0% 7.6% 19.2%

Proportionof

onlineretailsales

(2014/2019)

11.8%/16.3% 9.8%/11.2% 8.3%/10.3% 8.0%/10.5%

Table 4 Consumption and Retail Sales Prospects

Expectations of higher economic growth are largely due to the recovery of export markets, low interest rates and increased consumption

12

2.4 ECONOMIC PROSPECTS

2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

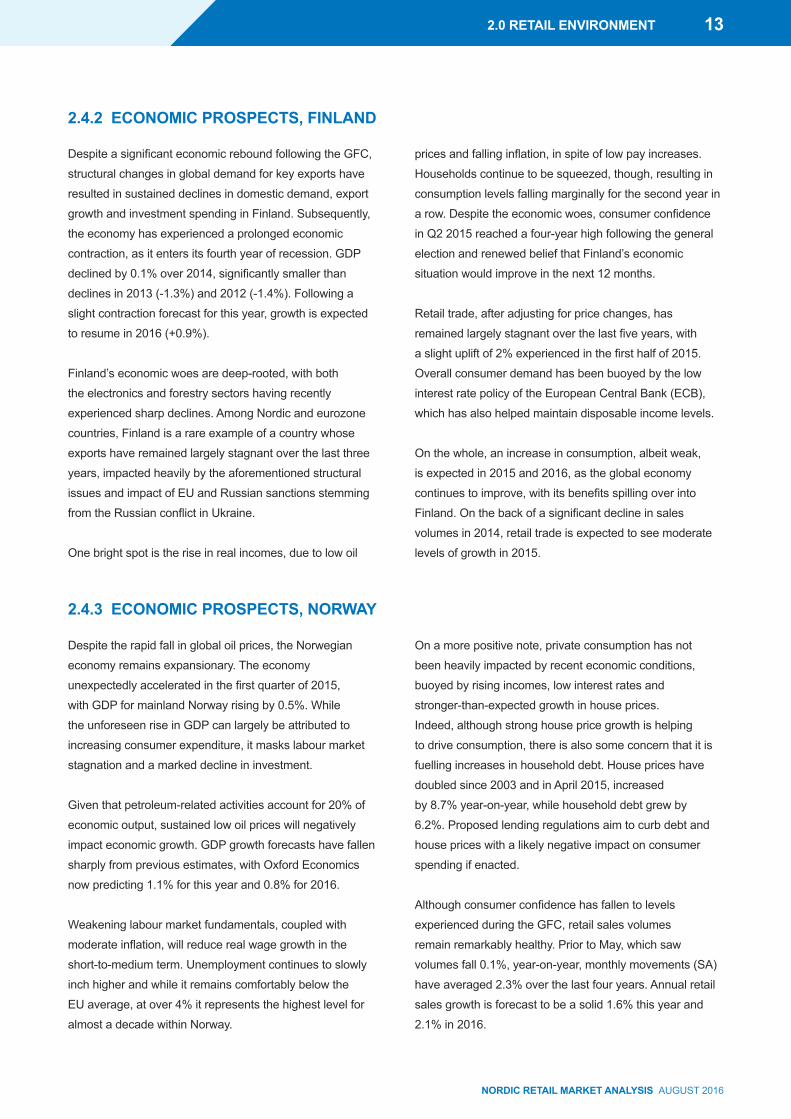

2.4.2 ECONOMIC PROSPECTS, FINLAND

DespiteasignificanteconomicreboundfollowingtheGFC,

structuralchangesinglobaldemandforkeyexportshave

resultedinsustaineddeclinesindomesticdemand,export

growthandinvestmentspendinginFinland.Subsequently,

theeconomyhasexperiencedaprolongedeconomic

contraction,asitentersitsfourthyearofrecession.GDP

declinedby0.1%over2014,significantlysmallerthan

declinesin2013(-1.3%)and2012(-1.4%).Followinga

slightcontractionforecastforthisyear,growthisexpected

toresumein2016(+0.9%).

Finland’seconomicwoesaredeep-rooted,withboth

theelectronicsandforestrysectorshavingrecently

experiencedsharpdeclines.AmongNordicandeurozone

countries,Finlandisarareexampleofacountrywhose

exportshaveremainedlargelystagnantoverthelastthree

years,impactedheavilybytheaforementionedstructural

issuesandimpactofEUandRussiansanctionsstemming

fromtheRussianconflictinUkraine.

Onebrightspotistheriseinrealincomes,duetolowoil

pricesandfallinginflation,inspiteoflowpayincreases.

Householdscontinuetobesqueezed,though,resultingin

consumptionlevelsfallingmarginallyforthesecondyearin

arow.Despitetheeconomicwoes,consumerconfidence

inQ22015reachedafour-yearhighfollowingthegeneral

electionandrenewedbeliefthatFinland’seconomic

situationwouldimproveinthenext12months.

Retailtrade,afteradjustingforpricechanges,has

remainedlargelystagnantoverthelastfiveyears,with

aslightupliftof2%experiencedinthefirsthalfof2015.

Overallconsumerdemandhasbeenbuoyedbythelow

interestratepolicyoftheEuropeanCentralBank(ECB),

whichhasalsohelpedmaintaindisposableincomelevels.

Onthewhole,anincreaseinconsumption,albeitweak,

isexpectedin2015and2016,astheglobaleconomy

continuestoimprove,withitsbenefitsspillingoverinto

Finland.Onthebackofasignificantdeclineinsales

volumesin2014,retailtradeisexpectedtoseemoderate

levelsofgrowthin2015.

2.4.3 ECONOMIC PROSPECTS, NORWAY

Despitetherapidfallinglobaloilprices,theNorwegian

economyremainsexpansionary.Theeconomy

unexpectedlyacceleratedinthefirstquarterof2015,

withGDPformainlandNorwayrisingby0.5%.While

theunforeseenriseinGDPcanlargelybeattributedto

increasingconsumerexpenditure,itmaskslabourmarket

stagnationandamarkeddeclineininvestment.

Giventhatpetroleum-relatedactivitiesaccountfor20%of

economicoutput,sustainedlowoilpriceswillnegatively

impacteconomicgrowth.GDPgrowthforecastshavefallen

sharplyfrompreviousestimates,withOxfordEconomics

nowpredicting1.1%forthisyearand0.8%for2016.

Weakeninglabourmarketfundamentals,coupledwith

moderateinflation,willreducerealwagegrowthinthe

short-to-mediumterm.Unemploymentcontinuestoslowly

inchhigherandwhileitremainscomfortablybelowthe

EUaverage,atover4%itrepresentsthehighestlevelfor

almostadecadewithinNorway.

Onamorepositivenote,privateconsumptionhasnot

beenheavilyimpactedbyrecenteconomicconditions,

buoyedbyrisingincomes,lowinterestratesand

stronger-than-expectedgrowthinhouseprices.

Indeed,althoughstronghousepricegrowthishelping

todriveconsumption,thereisalsosomeconcernthatitis

fuellingincreasesinhouseholddebt.Housepriceshave

doubledsince2003andinApril2015,increased

by8.7%year-on-year,whilehouseholddebtgrewby

6.2%.Proposedlendingregulationsaimtocurbdebtand

housepriceswithalikelynegativeimpactonconsumer

spendingifenacted.

Althoughconsumerconfidencehasfallentolevels

experiencedduringtheGFC,retailsalesvolumes

remainremarkablyhealthy.PriortoMay,whichsaw

volumesfall0.1%,year-on-year,monthlymovements(SA)

haveaveraged2.3%overthelastfouryears.Annualretail

salesgrowthisforecasttobeasolid1.6%thisyearand

2.1%in2016.

132.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.4.4 ECONOMIC PROSPECTS, SWEDEN

Sweden’seconomygrewbyaremarkable2.3%in2014,

thestrongestlevelofgrowthachievedwithinWestern

Europe.Growthisexpectedtoremainrobustoverthenext

twoyears,withforecastsestimatinganexpansionof2%

in2015andafurther2.8%in2016.

Sweden’spositiveeconomicclimatecanlargelybe

attributedtohouseholdspendinginrecentyears,with

theexportgrowthover2015restoringbalancetothis

mixedeconomy.Supportedbysolidemploymentgrowth,

substantialincreasesinrealwagesandariseindisposable

income,privateconsumptionhasrisensignificantly.Retail

salesvolumesgrewnearly4%year-on-yearin2014.

Indeed,Swedenhasenjoyedthestrongestlevelsofretail

salesgrowthintheNordicsoverthelastfiveyearsandis

oneofthebestperformersinWesternEurope.Retailsales

volumesareforecasttoexpandbymorethan4%in2015,

thestrongestsince2007.

Despiteimprovingeconomicfundamentals,deflationary

fearscontinuetolinger,withSweden’sconsumerprice

indexperpetuallyfallingbelowtheRiksbank’s2%target

rateforthelastthreeyears.Therecentfallinoilpriceshas

placedfurtherdownwardpressureoninflationandfollowing

currencyappreciationaftertheECBratecut,theRiksbank

wasforcedtorespond.Thecentralbankintroduced

negativeinterestratesforthefirsttime,aswellas

asmallquantitativeeasingprogramme.Bothhave

hadapositiveimpactonhouseholdconsumptionand

subsequently,retailtrade.

SimilarlytoNorway,Swedenhasseensignificantincreases

inhouseprices,whichinturnaresupportingincreased

householdconsumptionanddebt.Long-termsupply

shortageshavedrivenpricesup11%inthe12months

toMay.

Overall,Sweden’seconomicfutureappearslargely

positive.Thegovernmentpredictsitwillmanage

tobalancethebudgetby2018,whilesimultaneously

loweringunemploymentandbringinginflationinline

withthehistoricallong-termaverageof2%.

2.0 RETAIL ENVIRONMENT14 2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.0 RETAIL ENVIRONMENT

Denmark Finland Norway Sweden

PrimeHighStreetrents

(€/sqm)2,015 1,750 2,230 1,690

Prime Shopping Centre

rents(€/sqm)1,070 1,050 1,240 1,030

Rentalgrowthforecast

(CAGR,*fiveyears)1.8% 3.9% 4.6% 6.9%

Shoppingcentredensity

(sqmper1,000persons)261.7 353.5 606.3 288.8

Shoppingcentresover

30,000sqm(count)16 20 41 52

Largestshoppingcentre

(turnover,€millions)Field’s(€370m) Itis(€368m) Sandvika(€402m) Nordby(€490m)

CBREGlobalRetailer

RepresentationRank

(outof61countries)

43 55 49 38

* Compound Annual Growth RateSource: CBRE, 2015

2.5.1 RETAILER PRESENCE

Highdistributioncosts,aswellastheperceptionofthe

marketsbeingtoosmallanddisparate,havetraditionally

beenconsideredthemainobstaclestomarketentryinthe

Nordicregion.Despitesubstantialmarketopportunity,the

Nordicshaslongbeenalow-priorityregionforinternational

retailers.However,thankstopositiveeconomic

fundamentalsandashiftfromcountrytocity-ledretailer

expansionstrategies,thistrendhasbeguntoshift.More

well-knownbrandshavebeguntakingspaceintheregion,

primarilyinmajorcities.

Mostinternationalretailerschoosetoenterthemarket

throughfranchises,departmentstoreconcessionsor

partneredformats.Notonlydoesthismodelreducerisk

associatedwithportfolioexpansion,butitalsoreduces

capitalrequiredbyutilisingestablishedfranchisee

distributionnetworks.Despitereducingrisks,manynew

marketentrantsfailtofullyconquertheregionandexit

shortlyafterentry.Anumberofbrandswithinternational

presencehaveenteredandwithdrawnfromtheNordic

markets;GAME,OnOffandtheExpertGroupalldeparting

soonafterexpandingintheregion.Tosomeextentthis

hasbeendrivenbytheverycompetitiveretailcategories

theseretailersarefocusedon,ratherthananinnate

incompatibilitywiththeNordics’retaillandscape.

Thelackofinternationalbrandshasalloweddomestic

retailerstodominateeveryaspectofthelocalmarket.

Thefast-fashionmarketisparticularlycompetitiveandthe

strongvalueformoneyofferedbydomesticchainsresults

intheopportunityforcrossborderretailersinthissegment

beingverynarrow.WithH&M,Lindex,Cubus,KappAhlas

wellasotherlargedomesticbrands,thereislimitedspace

forwell-knowninternationalbrandslikeUniqlo,Topshop

andGAP.

Table 5 Retail Real Estate Profile

Well-known brands have begun taking space in the region,

primarily in major cities

2.5 RETAIL LANDSCAPE

152.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

TheNordicretaillandscapeisdominatedbyshoppingcentres.Indeed,

Norway,SwedenandFinlandhavethehighestdensityofshoppingcentresin

WesternEurope–rankingfirst,thirdandfourth,respectively.Therearesome

800shoppingcentresacrosstheregion,providingthemainformofretailin

smallertownsandcomplementinghighstreetsinmajorcities.Whiletherearea

significantnumberofcentres,theytendtobequitesmall.Notably,theaverage

UnitedKingdomcentreisnearly36%largerthantheaverageNordicshopping

centre.Theaverageschemesizeislessthan20,000sqm.

Shoppingcentreformatsdifferacrosstheregion,

withsmallercentresinNorwayandDenmarkand

relativelylargeronesinSwedenandFinland.TheF&B

provisionhastraditionallybeenlowinNorway,relative

totheothermarkets.Conversely,groceryanchorsare

abundantacrosstheregion,withmostschemeshaving

atleastoneoperator.

Despitethepredominanceofshoppingcentres,

theregionisoneofthemostmatureomni-channel

retailingmarkets.Onlineretailtradein2014amounted

toapproximately€15bn.Whilesmallinabsolute

termsrelativetolargerEuropeanmarketsliketheUK

(€43bn),Germany(€25bn)andFrance(€22bn),ona

percapitabasisthefourNordicmarketsrankhigher

thanallotherEuropeancountries,excepttheU.K.

Notably,Norwegianseachspend€627onlineonaverage,nearlytwicethatof

Germans(€344)andFrench(€361).Onlineretailsalescurrentlyaccountforan

estimated9%ofallretailtradeandareforecasttogrowat10%perannum.This

representsasignificantopportunityfornewinternationalomni-channelretailers

topre-testthemarket.

Whileshoppingcentredensityandhighlevelsofonlinespendrepresentseveral

commonthemesacrosstheregion,theNordicretailenvironmentremainshighly

diversifiedwithnotabledifferencesacrossmarkets.

(i) DenmarkInspiteofitssize,DenmarkisoneofthemostmatureretailmarketsinEurope.

Totalretailstockamountstoapproximately12.4millionsqm,ofwhichshopping

centres’accountfor1.5millionsqm,or12%.WhilestillabovetheEuropean

average,Denmarkhasthelowestprovisionofshoppingcentrespaceofallthe

Nordicmarkets,asseeninTable5.Thisisprimarilyduetoastrongtraditionof

highstreetretailingandstrictplanningrulesonout-of-townspace.Danishcentres

areonaveragethesmallestintheregion.Thereiscurrentlyonlyonescheme

withmorethan100,000sqmGLAinDenmark,theRosengårdcentretinOdense.

Shoppingcentredevelopmentcontinuestofocusonrefurbishmentand

2.5.2 RETAIL FORMAT

Despite the predominance of

shopping centres, the region is one of the most mature omni-

channel retailing markets

16 2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

reconfigurationofexistingschemes.Betterconfiguredspaceandimproving

economicconditionshavenotbeenenoughtoreducetheoverallvacancyrate,

whichremainsstubbornlyhighat6.3%.Thisissignificantlyabovethemarket

lowof1.9%experiencedin2007.

Generatingnearly25%ofretailturnover,Copenhagen,andthewiderCapital

Region,remainsthefocusfornewmarketentrants.Denmark’sthreeregional

cities(Aalborg,AarhusandOdense)arealsoimportantretailcentres,servingas

secondaryexpansionpointsforretailers.

Danishbrands,alongwiththeirSwedishcounterparts,representthelargest

shareofcross-borderbrandsintheregion.FromBestseller,ownerofVeroModa,

SelectedandJack&Jones,toICCompany,ownerofByMaleneBirger,Peak

PerformanceandSaintTropez,Danishstyleandfashioncanbefoundacross

thevaluespectrum.

WhileDanishbrandscontinuetoexpandoutsideofthehomemarket,

internationalretailersarecontinuingtoenterandexpandwithinthemarket.

Typically,thesecondmarketforexpansionafterSweden,Denmark’sCapital

Regionoffersanarrayofinternationalbrands,numberingonlyslightlyfewerthan

Stockholm.RecentmarketentrantsincludeTod’s,ValentinoandIsabelMarant.

172.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.0 RETAIL ENVIRONMENT

(ii) FinlandFinlandhasthesmallestretailmarketofthefourNordiccountriesstudied.Its

strategiclocationhasestablisheditasagatewaybetweentheEUandRussia

andtheBalticSearegion.Despitethisposition,Finland,andspecificallyHelsinki,

remainsthelastcountry/cityinternationalbrandstypicallyenterwhenexpanding

intheNordics.Thistrendhasshiftedslightlyhowever,withMarks&Spencer

notablyopeningitsfirstNordicstoreinFinlandbeforeexpandingintothelarger

SwedishandNorwegianmarkets.

Overallinternationalretailerpresencehastraditionallybeenlow,withmostretail

centresdominatedbywell-knowndomesticbrands.However,theentryofforeign

brandshasslowlyincreased,primarilybyretailersalreadywellestablishedwithin

the EU.

ThetotalretailstockinFinlandis7millionsqm,withshoppingcentresaccounting

for1.97millionsqmor30%ofspace.Ingeneral,shoppingcentresandretail

warehousesaremorecommonthanhighstreets,aresultofFinland’surban

structure,lowpopulationdensityandregionalplanningregimes.Withmorethan

athirdofthepopulationwithina90-minutedrive,theHMAisthemostimportant

retailcentreinthecountryandaccountsfornearly50%ofallretailspace.

Whiletheshoppingcentrepipelinecurrentlystandsat90,000sqm,themajority

remainsintheplanningstagewithlimitedspaceunderconstruction.

DevelopersremainhesitanttobreakgroundonnewschemesinFinland’s

currenteconomicclimate.

(iii) Norway Despitethecountry’ssubstantialwealthanddemandforqualityproducts,

internationalretailerpenetrationhasremainedlow.CBREestimatesthatof

theleading334internationalretailers,only16%arelocatedinNorway.Thisis

primarilyduetoNorway’ssmallmarketsize,dispersedpopulationanditsnon-EU

status.TypicallyinternationalbrandswillexpandintheNorwegianmarketonly

aftertheyhaveestablishedtheirbrandsinSwedenandDenmark.OutsideofOslo

andseveraltiertwocities,includingBergen,TrondheimandStavangerthereare

fewareasabletoattractforeignretailers.

Inthelasttwoyearsanumberofpremiumretailershaveopenedflagships,

includingSandro,BurberryandtheKooples.LikeinotherNordicmarkets,

manyretailershavechosenthefranchise/partnerroutetomarket.

Norwayhasawell-developedretailmarket,largelycentredonout-of-town

shoppingdestinations.AtnearlythreetimestheEuropeanaverage,Norwayhas

thelargestprovisionofshoppingcentresofanyEuropeancountry.Shopping

centrestockissettoexpandslightly,with70,000sqmofspace

underconstruction.

Refurbishmentofexistingshoppingcentrespaceratherthannewdevelopmentis

theongoingtrend.Thisispartlyduetotown-centrefirstretailplanningregulations,

Finland has the smallest retail market

of the four Nordic countries studied

18 2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

2.0 RETAIL ENVIRONMENT

whichaimtostrengthenurbanandsuburbanareas,avoidurbansprawland

improvepublictransportoptionsforresidentswithoutaccesstocars.However,a

numberofnewschemeshaveopenedinthepasttwoyears,followingarelatively

quietperiod.ThishasimpactedtheoveralldesirabilityofNorwegianshopping

centres,withonlythelargest,redeveloped,regionalschemesabletoattract

internationalbrands.

OnlineretailsalesinNorwayhaveincreasedbyanestimated16%perannum

since2013.NorwayleadsScandinavianotonlyincurrentonlineretailsalesper

capita,butalsoinpredictedgrowthoftheindustry.

(iv) Sweden OftheNordicretailmarkets,Swedenisthelargestandmost

influentialintheregion.Asaresultofitsgeographicalsize

andurbandensityinthesouth,itisfrequentlythefirsttarget

destinationforinternationalretailersenteringtheNordic

region.TheopennessoftheSwedishpeople,coupledwith

thestrongeconomicfundamentals,easesmarketentryand

aidsfurtherregionalexpansion.

Swedishretailersrepresentalargeshareofcross-border

retailbrandsandincludeH&MGroup,IKEA,LindexandGina

Tricot.WhileContinentalEuropehashistoricallybeenthe

mainexporterofcross-borderbrands,U.S.andU.K.brands

haveincreasinglytakenaninterestintheregion.Superdry,

HollisterandRiverIslandallrepresentrecententrantstothe

Swedishmarket.

Swedishshoppingcentresarecurrentlyundergoinga

structuralshift,withnewandredevelopedschemesbeginning

toattractretailerswhopreviouslypreferredhighstreetlocations.Forexample,

DunkinDonuts,MichaelKorsandtheDisneyStorewillallbeopeningstoresin

theMallofScandinaviaoutsideofStockholm.

LiketherestoftheNordicregion,Swedenhasawell-developedshoppingcentre

market.Ofits18millionsqmofretailstock,2.8millionsqmrepresentshopping

centrespace.Theshoppingcentrepipelineremainsstrong,with340,000sqmof

spaceunderconstructionacrossnewandexistingschemes.

Despitethepullofout-of-townshoppingcentres,mostSwedishcitieshavea

particularlystrongcitycentreretailoffer.Sweden’smajorcitiescontinuetobe

theprimaryfocusforinternationalretailers.Stockholmremainsthepremierretail

marketforSwedenandthewiderNordicregion,withnumeroushighstreets,

departmentstoresaswellasseveralstrong-performinginner-cityshopping

centreslikeGallerianandMOODStockholm.Aswellasbeingthelargestretail

marketintheregion,StockholmsitsatSweden’sgeographicalcentreandas

such,frequentlyservesasahubforregionaldistributionnetworks.

192.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

(i) DenmarkAfterfiveconsecutiveyearsofstagnation,primehighstreetrentshaverisen

slightlyinrecentquarters,currentlystandingat€2,015/sqm(DKK15,000/sqm).

Primeshoppingcentrerentsarepresently€1,070/sqm(DKK8,000/sqm).

Despitestagnation,primerentsinCopenhagenwere,untilrecently,thehighest

intheregionduetoconsistentlystrongdemandoutpacingsupply.Sustained

demandforprimehighstreetspaceisexpectedtodriverentsevenhigher.

Moreover,limitedspaceonkeythoroughfareshasresultedinspilloverto

secondarystreetsandprimeshoppingcentres.

(ii) FinlandPrimerentshaveremainedlargelystableoverthelastfouryears,currently

standingat€1,750/sqm,thethirdhighestoftheNordiccapitals.Occupieractivity

continuestobecentredoncorehighstreetsandprimeregionalshoppingcentres.

Tier2citieshavebeguntoexperienceincreaseddemand,particularlyTurku,

TampereandOulu.

Tradingpatternshaveshiftedoverthelast10years,withagreaterconcentration

ofactivityinlargerschemes.Larger,moremodernschemeshavecaptured

significantmarketsharefromsmallerschemesandtowncentres,leadingto

decreasedrevenueandhighervacancyratesinoutdatedcentres.

Continuousdeclinesinretailsaleshavecontributedtotherecentspikeinvacant

units,particularlyinsecondarylocations.Nevertheless,primerentsareexpected

tocomeunderslightupwardpressureoverthenext12-24monthsasprime

supplyfalls.

2.5.3 RENTAL DYNAMICS

Occupier activity continues to be centred on core high streets and

prime regional shopping centres

Sustained demand for prime high street

space is expected to drive rents

even higher

20 2.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Norway has experienced steady rental growth over the last three years, with prime high street rents increasing 5.1% per annum on average

Strong levels of both domestic and international occupier demand have dramatically reduced supply levels along key high streets and quality shopping centres

(iii) Norway

Norwayhasexperiencedsteadyrentalgrowthoverthelastthreeyears,with

primehighstreetrentsincreasing5.1%perannumonaverageandcurrently

standingat€2,230/sqm(NOK18,000/sqm),thehighestintheregion.Prime

shoppingcentrerentsare€1,240/sqm(NOK10,000/sqm).

Strongeconomicfundamentalshaveaidedtheretailsector,helpingtodrive

internationaldemand.Coffeeretailers,inparticularAmerican-basedDunkin

DonutsandStarbucksaswellasSweden’sEspressoHouse,allhaveplansfor

furtherexpansioninthemarket.

Demandforprimespacealongkeyhighstreetshashelpedsustainrentalgrowth

andsuppressvacancyrates.However,growthinthenext12to24monthsshould

bemoremodest,increasingataround3%perannum.

(iv) SwedenPrimehighstreetrentsaregenerallystableinSwedenandcurrentlystandat

€1,690/sqm(SEK14,000/sqm),themostaffordablecapitalintheregion.Partly

duetothestructureoftheretailmarket,primeshoppingcentrerentscontinueto

climb,currentlystandingat€1,030/sqm(SEK8,500/sqm).Withtheopeningof

EmporiaoutsideMalmoandMallofScandinaviaoutsideStockholm,destination

shoppingcentresinout-of-town/suburbanlocationshavebeguntore-establish

themselvesaskeycompetitorsofcitycentres.

Stronglevelsofbothdomesticandinternationaloccupierdemandhave

dramaticallyreducedsupplylevelsalongkeyhighstreetsandqualityshopping

centres.Secondarystreetsandcommunityshoppingcentrescontinueto

experiencelowlevelsofdemand,withvacantunitsstillhardtolet.

Robustdemandfromretailerswillhelpdrivefuturerentalgrowth.CBREforecasts

thatSweden,andparticularlyStockholm,willseethehighestlevelsofgrowthin

theregionoverthecomingfiveyears,atanannualaverageof7%perannum.

212.0 RETAIL ENVIRONMENT

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

TheNordicregionismadeupofsmall,economically

opencountries,withlargeexport-drivenmarkets.

Highlevelsoffiscalresponsibilityhavehelpedtheregion

remainfinanciallystableandsolvent.Whiletheeurozone

asawholeisstillfeelingtheilleffectsoftheGlobal

FinancialCrisis(GFC),therelativeeconomicperformance

oftheNordicregionhasbeenstrong,withGDPforboth

NorwayandSwedensurpassingtheirpre-recessionmarket

peaksasearlyas2013,beforeanyother

European countries.

Whiletherearenumeroussimilarities,includinghigh

femaleparticipationratesinthelabourmarket,highlevels

ofproductivityandgeneralfiscalstability,thecountries

arequitedistinct,asdemonstratedinTable3.Denmark’s

economyremainslessvolatileduetoitsfocusonfast-

movingconsumergoods,whileNorway’sfortunehas

historicallybeenfuelledbytheNorthSeaoilindustry.

Despiteyearsofrobustgrowthandstrongeconomic

fundamentals,countrieswithintheregionarecurrently

experiencingdivergenteconomiccycles.

TheNorwegianeconomyhascomeunderpressurefrom

fallingoilprices,whileinFinland,thedeclineinfortunes

foritstechnologysector,resultantweakdomesticdemand

andeconomicsanctionsbetweentheEUandRussia,a

keytradingpartner,havenegativelyimpacteditsgrowth

trajectory.Incontrast,theDanisheconomicrecoveryis

solidifyingandSweden’seconomyhasoutpacedallgrowth

expectations.Economicforecastsfortheregionareabove

theEUaverage,althoughnear-termeconomicprospects

differsignificantly.

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

22 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

‘Traditional’shoppingcentresarethepreferredshopping

locationacrossallfourretailmarkets,particularlyinNorway

where60%ofrespondentsprefertoshopineitherasmall

orlargeshoppingcentre.Ofthosewhoprefertoshopin

‘traditional’centres,thelargemajorityinDenmark,Norway

andSwedenfavourlargeshoppingcentresoversmall

ones,althoughinFinlandthereisnoclearsizepreference.

Thispreferenceforlargecentresisparticularlyapparentin

the16-24agegroup–atrendthatispresentacrossallfour

nations.Conversely,smallshoppingcentresareshownto

bemorepopularamongthe55-65agebracket.

NorwayandDenmarkhaveahighcorrelationinregard

toconsumers’preferredshoppinglocation,albeitaslightly

higherproportionofshoppersinthelatterprefertoshop

onthehighstreet.Indeed,inDenmark,almostathirdof

shoppersfavourthehighstreet–thehighestpercentage

ofallfourNordiccountries.Bycontrast,thehighstreet

isthepreferredshoppinglocationforonly10%of

Finnishrespondents.

Overall,Finlandhasthemostdistinctandvariedshopper

locationprofile.Despite‘traditional’shoppingcentresbeing

themostfavouredformatby43%ofrespondents,

overaquarterofshoppersprefertoshopinretailparks–

thisbeingsignificantlyhigherthaninanyoftheother

Nordiccountries.

Furthermore,bydistinction,Finlandhasthehighest

proportionofonlineshoppersat19%(comparedwith

11%,11%and6%inDenmark,NorwayandSweden

respectively),risingto29%inthe35-44agecategory.

InNorwayandSweden,however,the16-24and25-34

agegroupsareshowntofavouronlineshoppingthemost,

withthelatteragecohortalsobeingthelargestonline

shoppersinDenmark.Thesurveyrevealsthat,acrossall

fourcountries,thepercentageofpeoplewhoprefertoshop

onlineishigheramongstmalesthanfemalesandthistrend

isparticularlymarkedinDenmarkandFinland.

Only3%ofrespondentsinDenmark,FinlandandNorway

prefertoshopinfactoryoutletcentres,however,thisrises

to11%inSweden,ledbythe35-44agebracketbutwith

arelativelyevensplitbetweenmalesandfemales.Despite

thepropositionoffactoryoutletcentresbeingdiscounting

andvalue,thereisnocleardistinctioninpreferenceforthis

shoppingformatbyincomelevel.

Source: ICSC Nordic Consumer Survey, 2015.

Figure 1: Where do consumers prefer to shop?

3.1 PREFERRED SHOPPING LOCATION

233.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

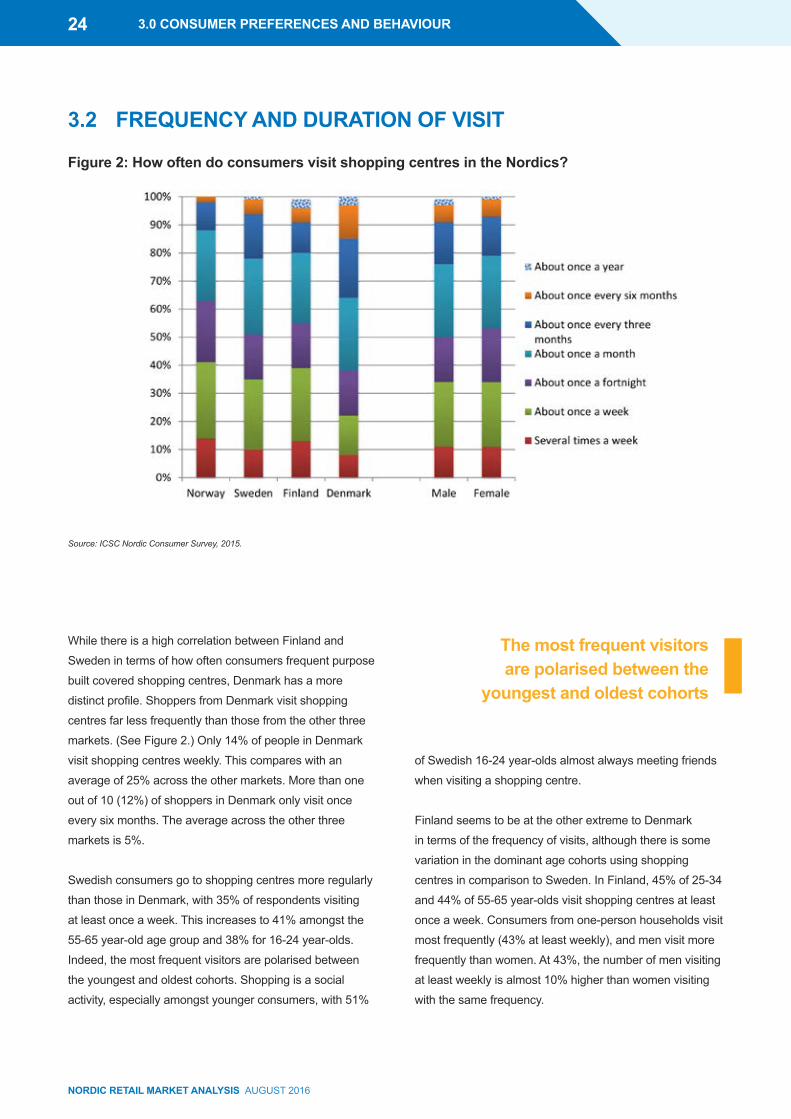

WhilethereisahighcorrelationbetweenFinlandand

Swedenintermsofhowoftenconsumersfrequentpurpose

builtcoveredshoppingcentres,Denmarkhasamore

distinctprofile.ShoppersfromDenmarkvisitshopping

centresfarlessfrequentlythanthosefromtheotherthree

markets.(SeeFigure2.)Only14%ofpeopleinDenmark

visitshoppingcentresweekly.Thiscompareswithan

averageof25%acrosstheothermarkets.Morethanone

outof10(12%)ofshoppersinDenmarkonlyvisitonce

everysixmonths.Theaverageacrosstheotherthree

marketsis5%.

Swedishconsumersgotoshoppingcentresmoreregularly

thanthoseinDenmark,with35%ofrespondentsvisiting

atleastonceaweek.Thisincreasesto41%amongstthe

55-65year-oldagegroupand38%for16-24year-olds.

Indeed,themostfrequentvisitorsarepolarisedbetween

theyoungestandoldestcohorts.Shoppingisasocial

activity,especiallyamongstyoungerconsumers,with51%

ofSwedish16-24year-oldsalmostalwaysmeetingfriends

whenvisitingashoppingcentre.

FinlandseemstobeattheotherextremetoDenmark

intermsofthefrequencyofvisits,althoughthereissome

variationinthedominantagecohortsusingshopping

centresincomparisontoSweden.InFinland,45%of25-34

and44%of55-65year-oldsvisitshoppingcentresatleast

onceaweek.Consumersfromone-personhouseholdsvisit

mostfrequently(43%atleastweekly),andmenvisitmore

frequentlythanwomen.At43%,thenumberofmenvisiting

atleastweeklyisalmost10%higherthanwomenvisiting

withthesamefrequency.

Source: ICSC Nordic Consumer Survey, 2015.

Figure 2: How often do consumers visit shopping centres in the Nordics?

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

3.2 FREQUENCY AND DURATION OF VISIT

The most frequent visitors are polarised between the

youngest and oldest cohorts

24 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Inregardtodurationofvisit,10%ofDanishconsumers

spendovertwohourswhentheyvisitashoppingcentre

whileonly4%ofpeoplebetween16and24spendless

than30minutes,asshowninFigure3.Thiscontrastswith

25%of55-65year-oldsspendinglessthan30minutes.

Youngerconsumerstendtodwelllongerinthecentre,

beingmoreengagedontheirvisits,typicallybyfoodand

leisureoffers.

Thereisanapparentdisparitybetweenhouseholdsizeand

durationofvisitinDenmark.Insingle-personhouseholds,

21%ofpeoplespendlessthan30minutespervisit.

Equally,thedurationofvisitsbyconsumersintheage

cohort55-65yearsislow.Giventhehighdivorceratein

Denmark,whichisapproaching50%ofmarriages,and

profileofemptynesters,itislikelythatthereisastrong

overlapbetweenrespondentsinsingle-personhouseholds

andthoseinthe55-65agecohort.Incontrast,only9%of

householdsinexcessofthreepersonsvisitforlessthan

30minutes.

Norwegians,alongwithFinns,arelesslikelytospend

anextendedamountoftimeinacentre.Only3%spend

overtwohoursinashoppingcentre,comparedwith11%

inSweden.Ahighpercentageacrossallagegroupsin

Norwayspendslessthananhouronvisits,with62%ofall

consumersreportingatripdurationoflessthananhour.

Thisfallsmodestlyforeventheyoungestagecohorts,at

55%.Maleshoppersareevenlesslikelytolinger,with73%

spendinglessthananhourpervisit.InNorway,itisthe

higher-incomegroupthattendstovisitthemostfrequently,

with46%visitingonceaweekonaverage.

SimilarlytoconsumersinNorway,only3%ofconsumers

inFinlandspendtwohoursormoreinacentre.However,

thedurationofvisitismorevariablebyagecohortin

Finland.While72%ofpeoplefromFinlandbetweenthe

agesof55and65spendlessthananhourinashopping

centrepervisit,thisfallsto47%for16-24year-olds.

AlthoughFinnishmaleshaveahigherfrequencyofvisit

tofemales,thedurationoftheirvisitsisshorterwith

14%moremalesspendinglessthananhourinacentre

comparedwithfemales.

Swedishconsumersalsostaylonger,with11%ofpeople

spendingmorethantwohoursonavisit.Thisisalmost

fourtimestheequivalentpercentageforFinland.However,

at53%,morethanhalfofconsumersinthe55-65year-old

agecohortspendlessthananhouronsite.Swedish

malesarealsomorepronetoshortvisits,with44%of

malesspendinglessthananhourcomparedwith32%

offemales.

Source: ICSC Nordic Consumer Survey, 2015.

Figure 3: What is the duration of visits to shopping centres in the Nordics?

3.0 CONSUMER PREFERENCES AND BEHAVIOUR 253.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Inallmarkets,goingtoshopsistheprincipalpurpose

ofvisitingshoppingcentres.Althoughthisisperhaps

unsurprising,itisanimportantremindertoownersas

assetstrategiesfocusoncreatinganappropriatebalance

ofstores,facilitiesandservicesthatenticeconsumers.

AsFigure4shows,forallfourmarkets,shoppingwasthe

mostfrequentlycitedreasontovisit.However,inSweden

asignificantlylowernumberofpeoplesaidthiswasthe

case,withonly55%ofrespondentsclaimingshopping

asthemainreasontovisit.PeopleinNorwayscorethe

highestwhenitcomestocitingshoppingasthereason

fortheirvisit,with70%statingthattheydothisalmost

everytimetheyvisit.

InDenmarkfemalesaregenerallymoresociable,with

22%offemalesalmostalwaysmeetingfriendswhenthey

visitacentreincomparisonto11%ofmen.Thesocial

aspectofshoppingisevenmoreprevalentwithinthe

youngeragecohortof16-24year-olds,with37%almost

alwaysmeetingfriends.

Generally,thereislowengagementwithF&Bwhile

shoppingacrosstheNordics.Whileanaverageof27%

ofpeoplehavesomethingtoeatanddrinkwhenvisiting

ashoppingcentre,thisislowerthantherestofEurope

(excludingtheNordics)wheretheaverageisaround

40%(Source:JLLFoodserviceConsulting).However,

theprovisionofF&Binshoppingcentresisundergoing

somewhatofatransformation.Untilrecently,F&B

averaged10%to12%ofGLAinEurope.Thishas

increasedtoapproximately15%forallcentres,with

newdestinationcentrestypicallypositioningthemselves

with17%-20%ofspacededicatedtoF&B(Source:JLL

FoodserviceConsulting).

However,certainmarketsandshoppingcentreswithinthe

Nordicshaveintroducedexcitingandinnovativedining

conceptsthathaveprovedhighlysuccessfulandthathave

beenadoptedelsewhereinEurope.Destinationcentres

inparticularhaveusedhigh-qualityF&Btodrivefootfall

andcreateapointofdifference.Forexample,Moodin

Stockholmcitycentreoffersarangeofupscalebarand

Source: ICSC Nordic Consumer Survey, 2015.

Figure 4: What do people almost always do when they visit shopping centres?

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

3.3 PURPOSE OF SHOPPING CENTRE VISIT

In all markets, going to shops is the principal purpose of visiting shopping centres

26 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

restaurantoperators,andtherangeandqualityofF&Bis

animportantelementofthecustomerdrawingpowerof

thenewlyopenedMallofScandinavia.Thisisnowbeing

mirroredacrosstheregionasschemesseektoincorporate

moreleisureintotheiroffer,whichisbeingmetwithmuch

success.ThisshifttowardsagreaterproportionofF&Bis

particularlyimportantasonlineretailfurtherpenetratesthe

Nordicregion.Aswellasbeingasectorthatisnotdirectly

impactedbyonlineretail,F&Bcreatesasenseofplacefor

shoppingcentres,attractingandengagingcustomers.

ThereisalsoacleardivideinDenmarkbetweenpeople

fromdifferenthouseholdsizeswhenitcomestoeating

anddrinking,partlyexplainingdifferencesindurationof

shopping.Householdsofthreeormorepersonstendmore

toregularlyuseF&Bservices(36%)thansingle-person

households(23%).Largerhouseholdsarealsomorelikely

tointeractwhenshoppingwithalmost25%socialising,

almosttwicethelevelforallotherhouseholdsizes.

InSwedenandDenmark,perhapsreflectingtheirhigher

propensitytomeetfriendswhenshopping,45%of16-24

year-oldsalmostalwaysuseF&Bserviceswhentheyvisit

acentre.Anunexpectedfindingwasthatthisyounger

agegrouppreferreddiningataseated,asopposed

tofastfood,restaurant,with39%and17%indicating

theywouldregularlyusetheserespectiveF&Boptions.

Equally,youngershoppersindicateahigheruseofseated

restaurantsthantheolderagecohortof55-65year-olds,

again39%versus17%.

Reflectingthegreatersociabilityofyoungerconsumers

withinshoppingcentreenvironments,itisclearthat

youngeragegroupsaremorelikelytoengagewithother

leisureoperators.Astheyvisitcentresmostoften,spend

thegreatestamountoftimeandeatanddrinkmost

regularly,youngershoppersremainakeyconsumer

groupforshoppingcentres.

InNorway,asinDenmark,itistheyoungerpeoplethat

aremoreengagedbytheF&Boffer,with52%ofall16-24

year-oldsindicatingtheyalmostalwayseatordrinkwhen

visitingacentre.Overall,though,only18%viewcoffee

shopsasanimportantfactor,thelowestofallfourmarkets.

Again,thisagecohortisalsothemostlikelytomeetfriends

whentheygotoashoppingcentre.Norwegiansarethe

leastlikelytoshowanyinterestinenjoyingleisurefacilities,

with42%sayingtheyneverusethemand68%sayingthey

hardlyeverorneverusethem.

ThereisslightlylessengagementinFinland,withonly

28%indicatingtheyalmostalwayspartakeofF&Bwhen

theyvisit.ThegoodnewsinFinlandisthat16-24year-

oldsaremostengagedwithF&B,withalmosthalf(48%)

3.0 CONSUMER PREFERENCES AND BEHAVIOUR 273.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

Source: ICSC Nordic Consumer Survey, 2015.

Shoppingcentresareapreferredretailformatforcomparison

(non-food)shopping,withover20%ofconsumersinNorway,

SwedenandFinlandspendinghalftheirnon-foodbudgetin

theseenvironments,asshowninFigure5.Theoneanomaly

seemstobeDenmark,where20%ofpeoplespendless

than5%inashoppingcentre,reflectingthelower

dominanceofthisretailformatasapercentageof

totalstock.

Figure 5: How much of their non-food shopping do consumers do in a shopping centre?

indicatingtheyalmostalwaysuseF&Bservices.

Thehighestlevelsofengagementwerewithseated

restaurantsandcoffeeshops.

Interestingly,thoseonalowerincomearemorelikelyto

almostalwayseatinashoppingcentre,withascoreof15%

higherthanthosefromahigherincomebracketinFinland.

Incontrasttoothermarkets,therangeandqualityofF&B

hasbeenslowertotakerootinFinland.Nevertheless,

overhalfofthoseinthe16-24year-oldagecohort(52%)

viewthepresenceofcoffeeshopsasveryimportantin

determiningwhichshoppingcentretovisit,contrasting

withapproximatelyaquarterof55-65year-olds(26%).

Intermsofotherreasonstovisitthecentre,11%ofFinns

almostalwaysuseaservice,suchasahairdresser,bank

ordentist,while81%almostalwaysvisitshops.The

respondentsalsoscoredtheseareasmorehighlythan

consumersinothercountriesintermsoftheirpreferences

fordifferentelementsofshoppingcentres.

28 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

ConsumersinDenmarkwithinthehigherincome

groupinghavehigherexpectationsoftheirshopping

centresthanthoseinotherincomegroups.Whenasked

toaddressfactorsthatwereextremelyorveryimportant

tothem,thelocation,mix,rangeofretailers,parking

facilities,presenceoflocalretailersallscoredhigherthan

forthoseonlowtomiddleincomes.Theareawherethe

reversewastruewasprovisionofpublictransport.

Theyoungeragecohorthasafargreaterpreference

toshopinlargeshoppingcentres(43%)thanon

highstreets(13%).Incontrast,theolderagegroups

demonstratedamuchhigherpreferenceforhigh

streetdestinations.

Seventy-eightpercentofSwedishrespondents

indicatedtherangeandchoiceofretailersisextremely

orveryimportanttothemindecidingwheretovisit.This

wassignificantlyhigherthantheaverageof64%across

theotherthreemarkets.ConsumersinSwedenarealso

themostpassionateaboutseeinginternationalretailers,

with30%seeingthisasadeterminingfactoroftheir

chosenshoppinglocation.Theabilitytocollectproducts

orderedonlinewasveryorextremelyimportantto22%

ofrespondents.

Similarly,accesstopublictransportisidentifiedasa

decision-influencingfactorby46%ofSwedishconsumers,

moreimportantthaninNorwayandDenmark,whereonly

35%ofshoppersindicateditsprovisionwouldimpactupon

theirchoiceofshoppingdestination.

DespitethecurrentlowengagementwithF&Binexisting

centresinFinland,41%ofconsumersindicatedthatthey

aremorelikelytoselectacentreifitoffersgood-quality

restaurants,while41%indicatetheprovisionofcoffee

shopsasadecisivefactor.Indeed,surveyrespondents

identifiedextendingtheF&Bofferofbothlower-andhigher-

costoptionsasafactorthatwouldincreasethefrequency

ofshoppingvisits.ThissuggeststhatthecurrentF&Boffer

isnotrespondingtoconsumerdemand.

Convenience,locationandpricingweremoreimportant

totheyoungeragecohortinSweden.Accesstopublic

transportshowedthewidestvariation,with16-24year-olds

judgingthistobeatleast17%moreimportantthanany

oftheotheragesegments.Good-qualityrestaurantsalso

scoredrelativelyhighly.Thisisagainastrongmessage

thatafocusonF&Bisessential.Theyoungergeneration

isengagingwiththefoodonoffer,displayingmoreinterest

intheseatedrestaurantthaninfastfood.Asaresult,the

Source: ICSC Nordic Consumer Survey, 2015.

Figure 6: What elements do consumers find very or extremely important when choosing which centre to visit?

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

3.4 FACTORS IMPORTANT WHEN CHOOSING A SHOPPING CENTRE

293.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

Withtheexceptionofmoremid-pricedbrands

inSwedenandFinland,andmoreF&BinFinland,

consumersacrosstheregiondidnotidentifyveryclearly

anyelementsthatcouldbeincreasedorimprovedthat

wouldencouragethemtofrequentshoppingcentresmore

often,asshowninFigure7.ConsumersinNorwayand

Denmarkareparticularlydifficulttoenticefurther,scoring

lowerthanaverageoneverymetricwhenaskedwhatthey

wouldliketoseemoreofwhenvisitingshoppingcentres,

anddisplayingnotrendastowantinglower-price,mid-price

orhigher-priceproducts.Equally,Danishconsumersare

unlikelytobeenticedbyeitherbetterqualityormorevalue-

orientedF&Bofferings,althoughtheirresponsessuggest

aslightlyhigherappetiteforluxurybrands.Thismaybe

becausethereisahighdegreeofsatisfactionalreadywith

theshoppingcentreoffer.

Source: ICSC Nordic Consumer Survey, 2015.

Figure 7: What would encourage consumers to visit more often? (Mean score where 1 = No difference and 10= Much more likely)

presenceofrestaurantsandcoffeeshops,alongwiththe

abilitytocollectgoodsthathavebeenpurchasedonline,

aremoreimportanttotheselectionofshoppingcentres

foryoungeragecohorts.

InNorway,whenaskedforthefactorsthatinfluencetheir

decisionastowheretoshop,over40%of45-65year-olds

indicateapreferenceforlocalretailers.Thisissignificantly

higherthanforotheragegroups.Incontrast,younger

shoppersdemonstratethatthepresenceofinternational

retailersstronglyinfluencestheirchoiceofashopping

centre.Lessthanhalf(49%)ofallconsumersinNorway

considerpricinganimportantfactor.Thisisthelowest

scoreacrossthecountriesandissome25%lowerthanfor

Finland.Theconvenienceofthecentrelocation

againscoreslowerforNorwegiansthanforany

othermarket.

Asforreasonsjudgedasextremelyorveryimportantto

thechoiceofshoppingcentre,Finnishconsumerssee

themixandrangeofretailersasbeingfarlessimportant

thanacrosstheothercountries.Only60%seethisaskey

inFinlandcomparedwith78%inSweden.Offargreater

importanceisthelocationoftheshoppingcentre,with78%

ofFinnishconsumersseeingthisascritical.Pricingisalso

adeterminingfactorwith74%indicatingitasbeingatleast

veryimportant.Thisis13%higherthananyoftheother

Nordicmarkets.

30 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Norwegianrespondentstypicallyliveclosertoshopping

centres,evidencedbythefactthattwiceasmany(8%)

travelbyfoottothecentreincomparisonwiththeother

countries(4%).(SeeFigure8.)Furthermore,39%travelled

forlessthan10minutestothecentretheyfrequentmost.

RespondentsinNorwayarealsothehighestusersofbuses

whentravellingtoacentre,with14%ofpeopleusingthis

modeoftransport.

Only20%ofSwedishconsumersspendlessthan

10minutesontheirwaytotheircentre,comparedwith

39%ofNorwegians.Intermsofdistancetotheshopping

centre,Swedishconsumerstravelledforlongerthanthose

intheothercountries.While58%travelledtothecentre

nearesttotheirhome,38%hadatleastmorethanone

centrenearertowheretheylivedthantheonethey

preferredtovisit.

Source: ICSC Nordic Consumer Survey, 2015.

Figure 8: What mode of transport do consumers use to travel to shopping centres?

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

3.5 TRAVELLING TO A SHOPPING CENTRE

Norwegian respondents typically live closer to shopping centres, evidenced by the fact that twice

as many (8%) travel by foot to the centre in comparison

with the other countries (4%)

In terms of distance to the shopping centre, Swedish

consumers travelled for longer than those in the other countries

313.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Shoppersacrossallmarketsmakeactiveuseoftheir

deviceswhileinshoppingcentres,asseeninFigure9.

Checkingbasiccentreinformationisthemostfrequent

useofsmartphonetechnology,anditisalsocommonfor

shopperstoundertakepricecomparisonorgainfurther

productinformationonlinewhileinstore.Transactingonline

wastheleastcommonreasontouseasmartphonewhile

shoppinginstore.Althoughonly12%ofNorwegiansmake

anonlinepurchaseinstore,thisissignificantlyhigherthan

forconsumersinallothermarkets.

Source: ICSC Nordic Consumer Survey, 2015.

Therehasbeenmuchconcerninthepastdecadeabout

thefutureofshoppingcentresandothertraditionalforms

ofbricks-and-mortarretailduetothegrowthofonlineretail

sales.However,ithasbecomeclearoverthepastfew

yearsthatonlineandofflinechannelsareinter-dependent

andthatshoppersusethesechannelsinterchangeably

withinashoppingjourney.Consequently,manyretailers

haveinvestedheavilyinaseamlesslyintegratedomni-

channeloffer.

Itisnowcommonforpeopletousetechnologywhile

shoppinginstorestochecksizes,comparepricesand

purchasefromanextendedproductrangeunavailable

inthestore.Thistendencyofconsumers,andincreasingly

retailers,tousetechnologysimultaneouslywhileshopping

orsellingvariesacrosscountriesandageprofilesindegree

andpurposeofuse.

Figure 9: How do consumers use their smartphones when in a shopping centre?

3.6 INTERACTION WITH TECHNOLOGY DURING THE SHOPPING JOURNEY

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

It has become clear over the past few years that online and offline

channels are inter-dependent and that shoppers use these

channels interchangeably within a shopping journey

32 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

Figure 10: When making a purchase online, how do consumers receive the product?

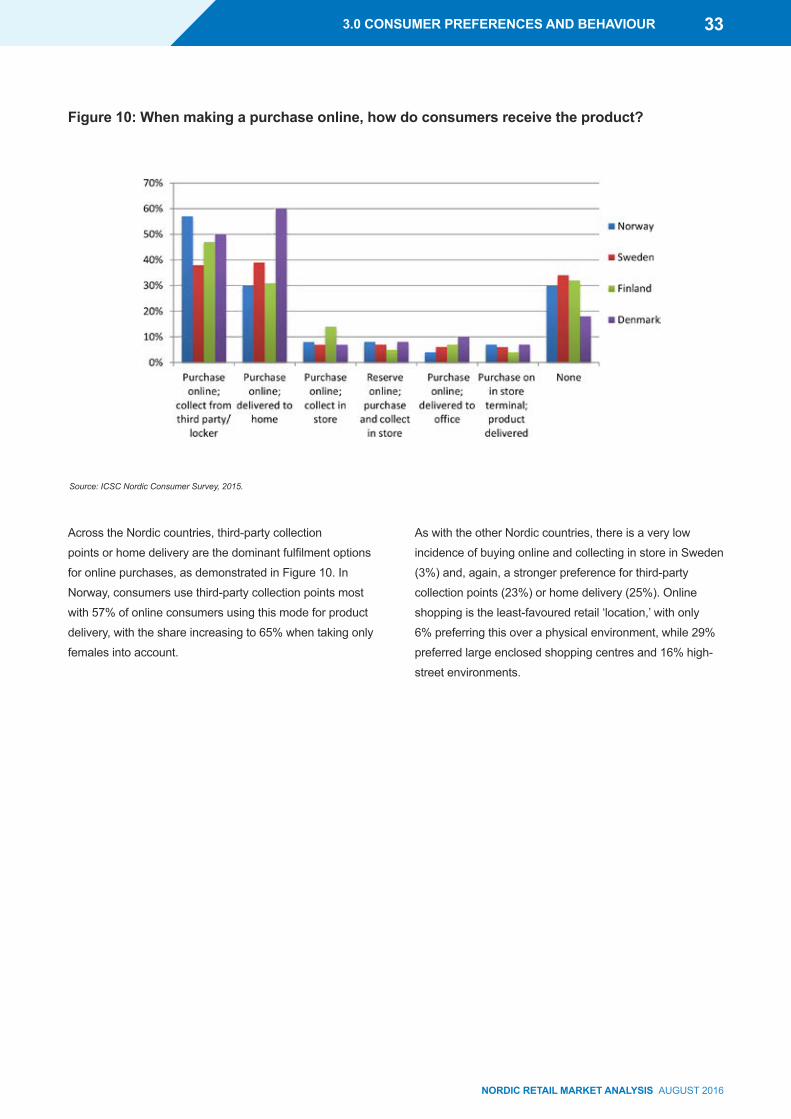

AcrosstheNordiccountries,third-partycollection

pointsorhomedeliveryarethedominantfulfilmentoptions

foronlinepurchases,asdemonstratedinFigure10.In

Norway,consumersusethird-partycollectionpointsmost

with57%ofonlineconsumersusingthismodeforproduct

delivery,withtheshareincreasingto65%whentakingonly

femalesintoaccount.

AswiththeotherNordiccountries,thereisaverylow

incidenceofbuyingonlineandcollectinginstoreinSweden

(3%)and,again,astrongerpreferenceforthird-party

collectionpoints(23%)orhomedelivery(25%).Online

shoppingistheleast-favouredretail‘location,’withonly

6%preferringthisoveraphysicalenvironment,while29%

preferredlargeenclosedshoppingcentresand16%high-

streetenvironments.

Source: ICSC Nordic Consumer Survey, 2015.

3.0 CONSUMER PREFERENCES AND BEHAVIOUR 333.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

3.0 CONSUMER PREFERENCES AND BEHAVIOUR

Figure 11: How much of your shopping do you believe will be done online in 3 years’ time?

DenmarkisamongthetopfourmarketsinEuropeinterms

ofonlinespendingpercapita(source:EcommerceEurope).

Thisisreflectedinsurveydatasuggestingthatjustover

70%ofDanishconsumerswillundertakealittleorsome

oftheirshoppingonlinewithinthenextthreeyears.

(SeeFigure11.)Almostathirdof25-34year-oldsin

Denmarkexpecttocarryoutmostoftheirnon-food

shoppingtransactionsonlinewithinthenextthreeyears.

OnlineshoppingisalsointegratedintoSwedishconsumer

behaviour,with87%havingmadeanonlinepurchaseor

reservedonlineinthepast12months.Theanalysisalso

indicatesthattwo-thirdsofSwedishconsumersexpect

toundertakesomeoralittleoftheirshoppingonline

inthenextfewyears,with18%foreseeingbuying

mostoftheirnon-foodshoppingonlinewithin

threeyears.

NorwayranksamongthetopfourmarketsinEuropewhen

itcomestoonlineretailspending(source:Ecommerce

Europe).However,inrelativecontrasttotheotherNordic

markets,acomparativelylow12%ofpeopleexpectmostof

theirnon-foodshoppingtobedoneonlineinthenextthree

years.FinnishandNorwegianconsumersarealsotheleast

confidentthatanyoftheirshoppingwouldbedoneonlinein

thenextfewyears.

Source: ICSC Nordic Consumer Survey, 2015.

34 3.0 CONSUMER PREFERENCES AND BEHAVIOUR

NORDIC RETAIL MARKET ANALYSIS AUGUST 2016

4.0 RETAILER INSIGHT

4.1 PERCEPTION OF THE NORDIC MARKET

4.0 RETAILER INSIGHT

InordertounderstandtheperceptionoftheNordicregion,interviewswere

conductedwithdomesticandinternationalretailersthatareeitheractive,

experienced,ornewlyenteringtheregion.Theseinterviewstookplaceinthelast

year.Theretailersinterviewedcamefrommanydifferentproductcategoriesand

pricepoints.Whilstsomewerestalwartsoftheregionwithhundredsofstores

acrossallfourmarkets,otherswerelookingtoenterwiththeirfirstlocations.

WhatbecameclearfromtheoutsetwasthatNordicretailersperceivethe

market(s)differentlyfromtheirnon-Nordiccounterparts.Thesedifferencesin

perceptionwereapparentinhowithasaffectedthedevelopmentofeachretailer’s

respectivebusinessintheregion.

Formanyoftheinternationalbrandsthatwerelookingtoexpandwithinthe

Nordics,themovemarkedtheculminationofawiderEuropeanexpansion

strategythatwasprecededbyanexpansionwithinthelargermarketstothe

south.Astherelativepopulationsizeoftheregionislessthanmanyother

Europeancountries,thetendencyamongstretailersfromoutsidetheregionwas

toviewtheNordicmarket‘asone’.Thisviewwaslargelyre-enforcedbyinternal

structures.Whereaninternationalbrandwaseitherseekingtoentertheregion

orhadenteredintomorethanonecountry,thesameindividualorteamwould

beresponsibleforallmarkets.Inthemajorityofinterviewsofthistype,entrants

plannedtomanagetheirbusinesseseitherfromtheirhomemarketorfrom

anotherEuropeanlocation.Thisexternalmanagementoftheregionmayreinforce

thenotionamongstnewentrantsthattheregionislargelyhomogeneouswith

fewsignificantdifferences.Theroleofe-commercewasalsoanimportantfactor

whenbusinessesfromoutsidetheregionwereplanningtoenter.Theregionis

seenasagood‘fit’forane-commerceledbusiness,aspeoplearetechsavvybut

morelikelytobegeographicallyisolatedfromaphysicalstore.Asaresult,many

internationalentrantslooktocoverthedisparateareasoftheregionthroughan

onlineonlystrategy.

Inthecaseofthemoreaspirationalretailersthatweinterviewed,brandswere

morelikelytorefersimplytothecitiesinwhichtheytradeoraretargetingfor

expansion.Inthisstrategy,brandsdonotdifferentiatebetweentheindividual

marketswithinaNordicregion.RatherthanDenmarkandSwedencompared

Nordic counterparts. These differences in perception were apparent in how it has affected the development of each retailer’s respective business in the region