Nordea Bank, Financial Forecast Update, July 22, 2013.

26

Financial forecasts Global Macro & Strategy, 22 July 2013

-

Upload

glenn-viklund -

Category

Documents

-

view

214 -

download

0

Transcript of Nordea Bank, Financial Forecast Update, July 22, 2013.

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 1/26

Financial forecasts

Global Macro & Strategy, 22 July 2013

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 2/26

Overview Major forecast changes

Major trends

Central banks Fed lower market rates or slower tapering

ECB low rates for an extended period

Riksbank the rate cut window is closingNorges Bank on hold until Q4 2014

Nationalbanken sidelined

Market rates USD rates sell-off looks excessive

EUR rates yields to fall in the near term

Foreign exchange USD stronger on Fed tapering

GBP Carney may not be a game-changer

JPY caught between Abenomics and Fed tapering

CHF floored but no one’s counting

SEK long term it is way above its averageNOK fair value model points to 7.90

Commodities Oil political risk premium supports oil price

Metals lower price path on market surplus

Tables

2

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 3/26

Overview: major forecast changes

• We have made no major forecast changes this time around.

3

Anders Svendsen

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 4/26

Overview: major trends

• Fixed income short term: the extreme sell-off in rates, triggered by the Fed opening the door

for tapering later on this year, looks hyperbolic and a rebound lower, especially in shorter EUR

rates, seems reasonable to us.

• Fixed income longer term: as market expectations of an eventually tighter Fed policy stance

build and the Euro-area recession comes to an end, we expect market rates to move higher.

• FX: the USD is forecast to appreciate significantly versus the EUR in the longer run as the US

economy is likely to grow more briskly than the Euro area.

• Oil short term: oil prices have rebounded from mid-April lows but the market has lacked

fundamental catalysts as seasonal weakness and negative economic surprises from especially

China continue to weigh on demand expectations.

• Oil longer term: the oil balance is tighter in H2 13 as demand growth resumes momentum.

OPEC’s effective spare capacity may decline from Q1 levels this year, but should be able tobuild slightly next year.

4

Johnny Bo Jakobsen

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 5/26

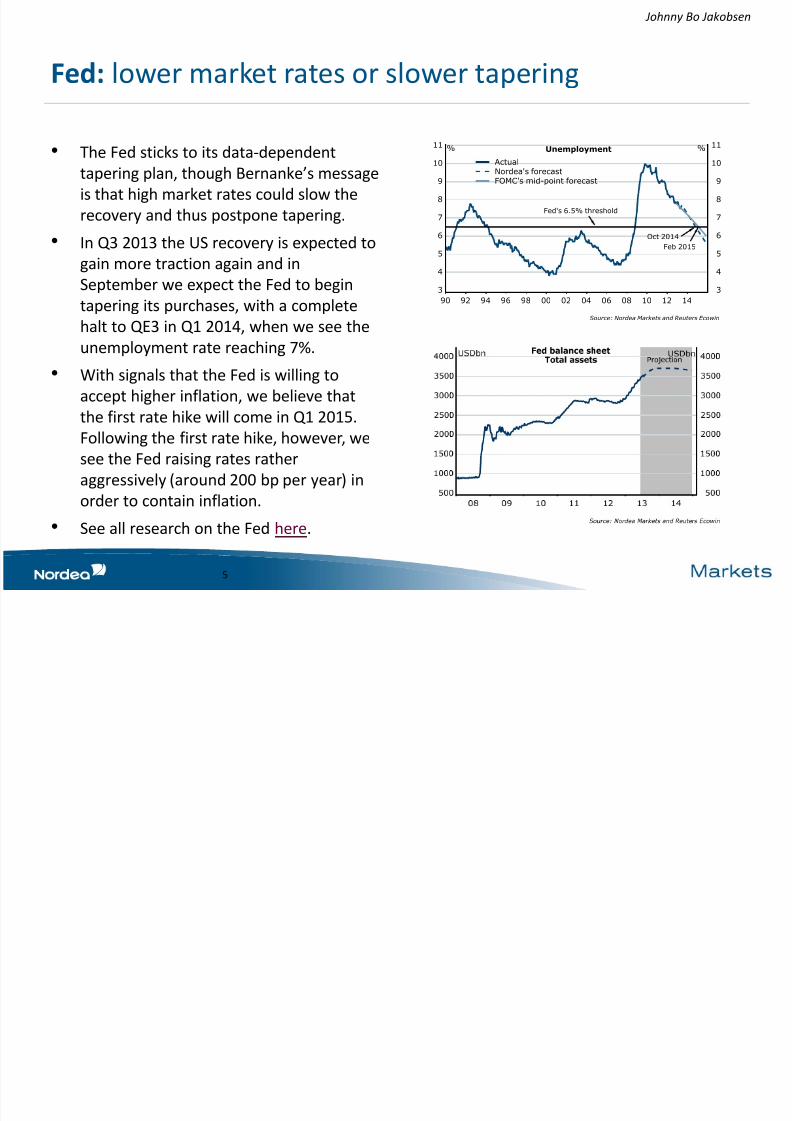

Fed: lower market rates or slower tapering

• The Fed sticks to its data-dependent

tapering plan, though Bernanke’s message

is that high market rates could slow the

recovery and thus postpone tapering.

• In Q3 2013 the US recovery is expected to

gain more traction again and in

September we expect the Fed to begin

tapering its purchases, with a completehalt to QE3 in Q1 2014, when we see the

unemployment rate reaching 7%.

• With signals that the Fed is willing to

accept higher inflation, we believe that

the first rate hike will come in Q1 2015.Following the first rate hike, however, we

see the Fed raising rates rather

aggressively (around 200 bp per year) in

order to contain inflation.

• See all research on the Fed here.

5

Johnny Bo Jakobsen

Source: Nordea Markets and Reuters Ecowin

90 92 94 96 98 00 02 04 06 08 10 12 14

3

4

5

6

7

8

9

10

11

3

4

5

6

7

8

9

10

11 %%

ActualNordea's forecastFOMC's mid-point forecast

Unemployment

Fed's 6.5% threshold

Oct 2014

Feb 2015

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 6/26

ECB: low rates for an extended period

• No more rate cuts in our baseline

scenario.

– We still expect recovery in the second half

of the year.

– Forward guidance used to talk down

implied rate path. Extended period means

longer than markets priced in at the time.

–

7 out of 23 opted against a cut at the Julymeeting according to Der Spiegel sources.

• Significant risk of one more refi rate cut

during the coming months and even a

deposit rate cut.

– Maybe as little as one month of badnumbers is enough to prompt a cut.

• We expect the first rate hike in the

beginning of 2015.

•

See all research on the ECB here.

6

Anders Svendsen

Source: Nordea Markets and Reuters Ecowin

09 10 11 12 130.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0%%

Euribor 3m

ECBs deposit rate

Main refi-rate

Marginal lending facility

Eonia O/N

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 7/26

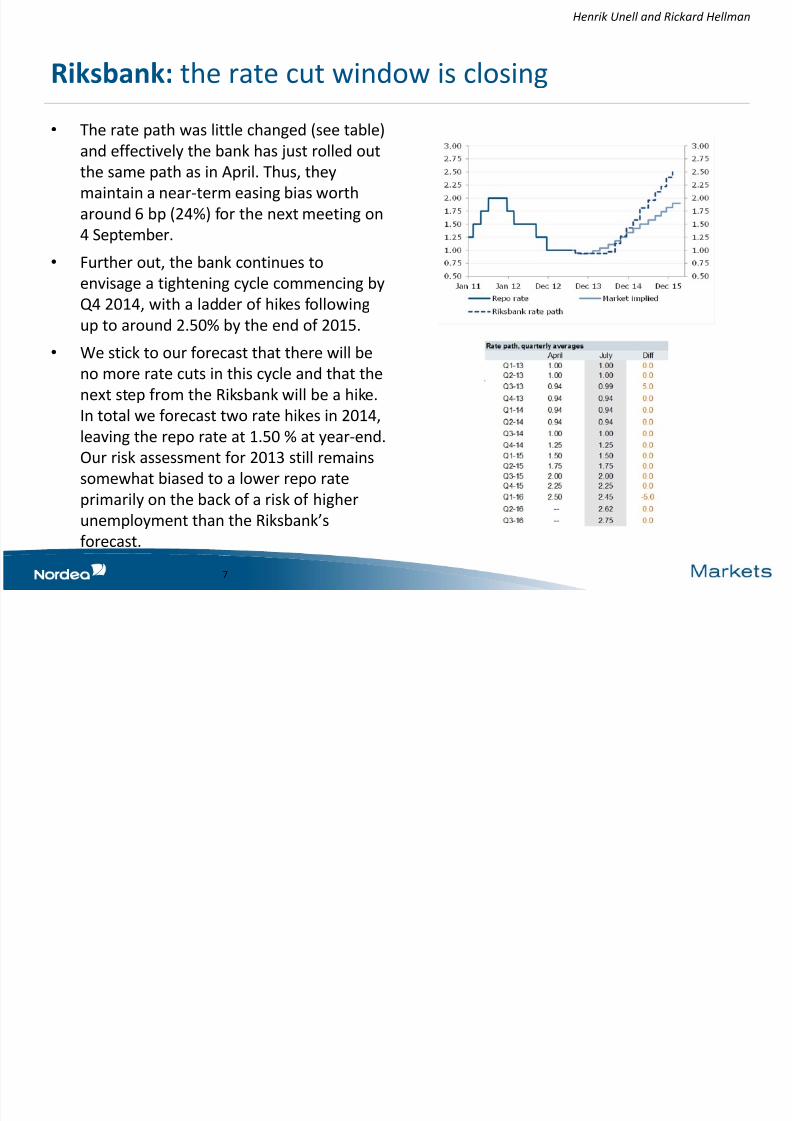

Riksbank: the rate cut window is closing

7

Henrik Unell and Rickard Hellman

• The rate path was little changed (see table)

and effectively the bank has just rolled out

the same path as in April. Thus, they

maintain a near-term easing bias worth

around 6 bp (24%) for the next meeting on4 September.

• Further out, the bank continues to

envisage a tightening cycle commencing by

Q4 2014, with a ladder of hikes followingup to around 2.50% by the end of 2015.

• We stick to our forecast that there will be

no more rate cuts in this cycle and that the

next step from the Riksbank will be a hike.

In total we forecast two rate hikes in 2014,leaving the repo rate at 1.50 % at year-end.

Our risk assessment for 2013 still remains

somewhat biased to a lower repo rate

primarily on the back of a risk of higher

unemployment than the Riksbank’sforecast.

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 8/26

Norges Bank: on hold until Q4 2014

• We expect unchanged policy rates until

December 2014 when we expect the first

rate hike.

• Norges Bank signalled in the last MPR a

50% probability of a rate cut at the next

meeting in September. If the NOK remains

much weaker than Norges Bank’s forecast,

we would need some very weak keyfigures to justify a rate cut in September.

So far key figures have been neutral

compared to Norges Bank’s view.

• A rate hike will not be on the table for a

long time as we expect inflation to staywell below Norges Bank’s target, growth

to show a more moderate pace and

unemployment slightly higher.

8

Katrine Godding Boye

1.68 1.681.75

1.94

2.15

1.68 1.681.76

2.00

2.30

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15

3m NIBOR Norges Bank deposit Market implied Central bank forecast

Norw ay Spot 3M 31Dec13 30Jun14 31Dec14

Leading rate 1.50 1.50 1.50 1.50 1.75

3M 1.70 1.70 1.70 1.70 1.95

2Y 1.96 1.96 2.14 2.31 2.84

5Y 2.60 2.34 2.84 3.00 3.41

10Y 3.31 2.98 3.54 3.64 3.88

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 9/26

Nationalbanken: sidelined

• Since January the Danish central bank has

not intervened in the FX market.

•

Over the last months the DKK has beenvery stable against the EUR.

• Assuming an unchanged ECB policy rate,

we expect the central bank’s lending rate

to be unchanged over the remainder of

the year.

• In 2014 the central bank will likely resume

the gradual normalisation of monetary

policy, taking the lending rate to the ECB

level as we head towards the end of 2014.

9

Jan Størup Nielsen

Source: Nordea Markets and Reuters Ecowin

08 09 10 11 12 13

-60

-50

-40

-30

-20

-100

10

20

30

40

50

607.425

7.430

7.435

7.440

7.445

7.450

7.455

7.460

7.465 DKK bn per monthCentral parity

Central bank intervention>>

EUR/DKK

<<EUR/DKK

Denmark Spot 3M 31Dec13 30Jun14 31Dec14

Leading rate 0.20 0.20 0.20 0.35 0.50

3M 0.26 0.30 0.35 0.45 0.552Y 0.70 0.60 0.65 1.00 1.50

5Y 1.27 1.00 1.40 1.75 2.20

10Y 2.05 1.75 2.35 2.55 2.85

30Y 2.50 2.35 2.95 3.10 3.35

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 10/26

USD rates: sell-off looks excessive

• The extreme sell-off in rates, triggered by

the Fed opening the door for tapering

later on this year, was most likely

reinforced by the elimination of massive

long positions and MBS convexity hedging.

• Considering the huge upward move seen,

a more notable rebound lower looks likely,

especially now that the uptrend in placesince early May has been broken.

• Volatility will remain high due to high

uncertainty.

• We expect yields to continue to rise

gradually in the medium term and also

short yields to start increasing, as the

economic recovery gains traction and

expectations of Fed rate hikes build.

10

Jan von Gerich

0

1

2

3

45

6

7

8

9

10

0

1

2

3

45

6

7

8

9

10

Jan-90 Jun-95 Dec-00 Jun-06 Nov-11

Germany US

10-year government

benchmark yields

% %

Source: Nordea Markets and Reuters Ecowin

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 11/26

EUR rates: yields to fall in the near term

• The move higher in EUR rates was driven to a

notable extent by US events – a further

correction lower looms.

• Especially the short end of the curve has fallenback, as the ECB introduced forward guidance

and made it clear it remains tilted towards

further easing measures.

•Political risks increased in several Euro-zonecountries, acting as a reminder that the euro

crisis is far from over.

• Interest rates remain historically very low, and

it is not hard to picture rates rising from current

levels in the medium term.

• Euro-zone debt problems and only a very slow

recovery mean that rates will rise only very

gradually.

11

Jan von Gerich

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-09 May-10 Sep-11 Feb-13

1-year EUR swap 1 year forward

% %

Source: Nordea Markets and Bloomberg

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-11 Jul-11 Feb-12 Aug-12 Mar-13

Germany US

10-year government

benchmark yields

% %

Source: Nordea Markets and Reuters Ecowin

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 12/26

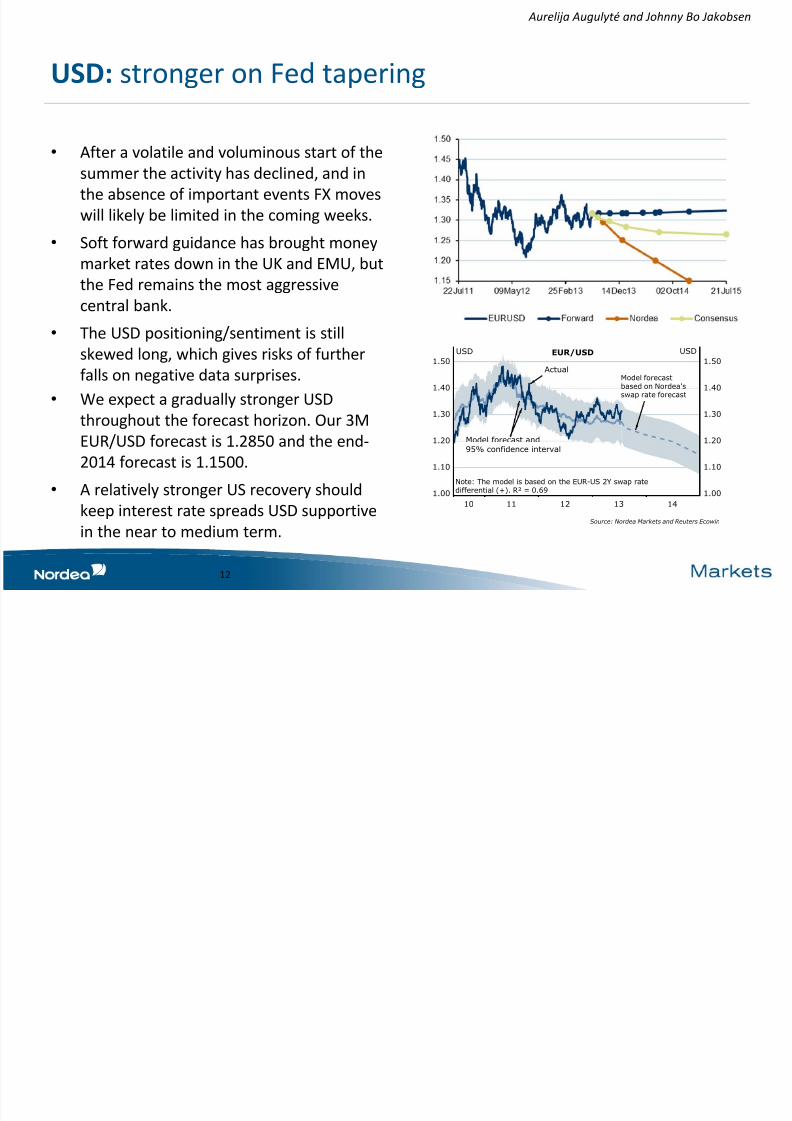

USD: stronger on Fed tapering

• After a volatile and voluminous start of the

summer the activity has declined, and in

the absence of important events FX moves

will likely be limited in the coming weeks.

• Soft forward guidance has brought money

market rates down in the UK and EMU, but

the Fed remains the most aggressive

central bank.• The USD positioning/sentiment is still

skewed long, which gives risks of further

falls on negative data surprises.

• We expect a gradually stronger USD

throughout the forecast horizon. Our 3MEUR/USD forecast is 1.2850 and the end-

2014 forecast is 1.1500.

• A relatively stronger US recovery should

keep interest rate spreads USD supportivein the near to medium term.

12

Aurelija Augulyté and Johnny Bo Jakobsen

Source: Nordea Markets and Reuters Ecowin

10 11 12 13 14

1.00

1.10

1.20

1.30

1.40

1.50

1.00

1.10

1.20

1.30

1.40

1.50

USD EUR/USD USD

Note: The model is based on the EUR-US 2Y swap ratedifferential (+). R² = 0.69

Model forecast and95% confidence interval

Model forecastbased on Nordea'sswap rate forecast

Actual

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 13/26

GBP: Carney may not be a game-changer

• EUR/GBP has breached the important

0.8600 range level and risks are now for

further upside in the short term.

• The net short positioning is still very high

and we do see risks of disappointment

later in August.

• Risks of forward guidance as a way to ease

monetary policy further (rather than moreQE) are weighing on the GBP. We are not

so sure that forward guidance will imply

more easing given recent strong data.

• Looking further ahead, we expect Fed

tapering and eventual QE exit to gradually

weaken the GBP versus the USD. A

relatively faster-growing UK economy

versus the Euro area will keep interest

rate spreads in support of the GBP versus

the EUR but not against the USD.

13

Aurelija Augulyté and Anders Svendsen

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 14/26

JPY: caught between Abenomics and Fed tapering

• We expect a range-bound USD/JPY and

EUR/JPY in the short term with risks of

more weakness.

• US Treasury yields have been a key driver

recently, and we expect them to move

lower in the coming months.

• The JPY could weaken versus the USD and

the EUR in the longer term as monetarypolicy will remain more aggressive.

Abenomics will only be called a success

when structural reforms aimed at lifting

potential growth are introduced.

• We maintain our JPY forecast on the

longer term, that is, end-2013 = 100, Jun-

14 = 105 and Dec-14 = 110.

14

Aurelija Augulyté and Amy Zhuang

0

50

100

150

200

250

300

350

400

65

70

75

80

85

90

95

100

105

110

115

2008 2009 2010 2012 2013 2014

USDJPY USD vs JPY 10Y IRS

USDJPY 10y IRS diff

Source:Nordea, Bloomberg

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 15/26

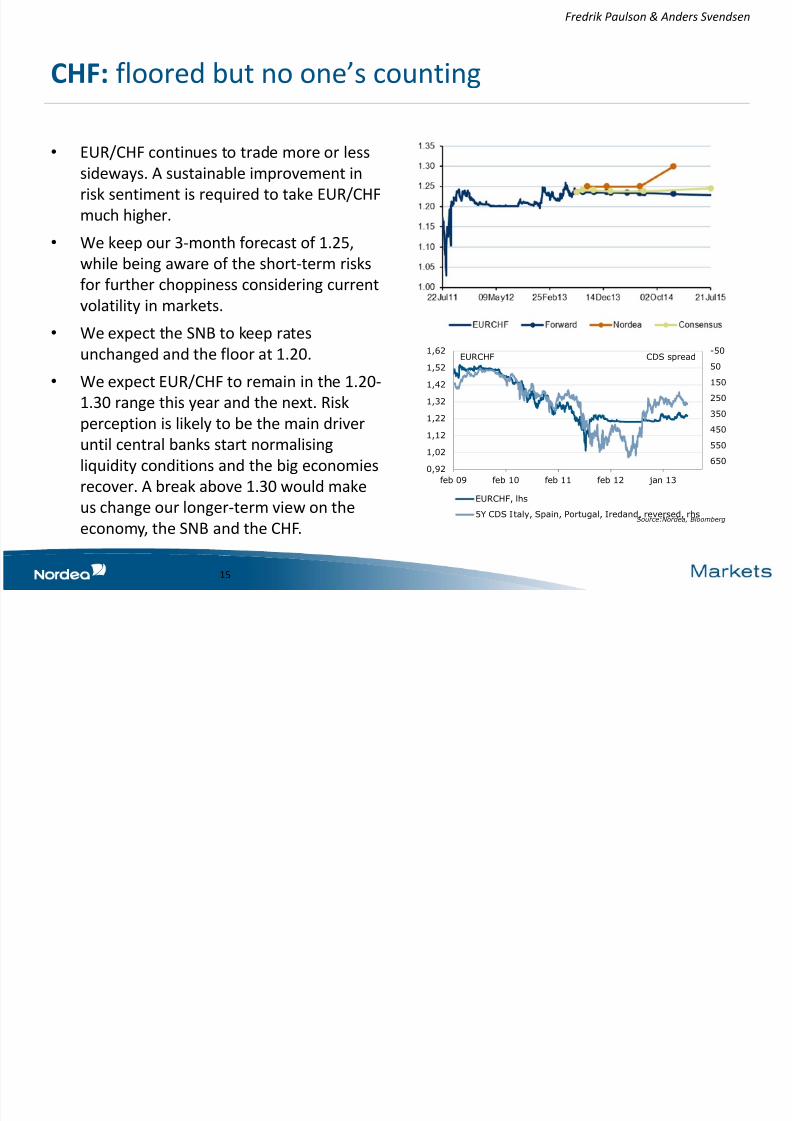

CHF: floored but no one’s counting

• EUR/CHF continues to trade more or less

sideways. A sustainable improvement in

risk sentiment is required to take EUR/CHF

much higher.

• We keep our 3-month forecast of 1.25,

while being aware of the short-term risks

for further choppiness considering current

volatility in markets.• We expect the SNB to keep rates

unchanged and the floor at 1.20.

• We expect EUR/CHF to remain in the 1.20-

1.30 range this year and the next. Risk

perception is likely to be the main driver

until central banks start normalising

liquidity conditions and the big economies

recover. A break above 1.30 would make

us change our longer-term view on the

economy, the SNB and the CHF.

15

Fredrik Paulson & Anders Svendsen

-50

50

150

250

350

450

550

6500,92

1,02

1,12

1,22

1,32

1,42

1,52

1,62

feb 09 feb 10 feb 11 feb 12 jan 13

EURCHF, lhs

5Y CDS Italy, Spain, Portugal, Iredand, reversed, rhs

EURCHF CDS spread

Source:Nordea, Bloomberg

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 16/26

SEK: long term it is way above its average

• Our view on the economy is that Swedish

growth will gradually improve in the

second half of 2013. Our leading GDP

indicator points to a scenario where GDPgrowth should be 2.0-2.5% y/y in Q4.

• Nordea’s forecast, due to the Riksbank

focus on household/financial stability, is

an unchanged repo rate for the rest of 2013 and an increase in the first half of

2014.

• No safe haven traces in SEK movements

lately. Works better as a global risk on/risk

off barometer. Having a neutral view onstock market volatility we still maintain

our argument for a stronger SEK ahead.

Present rate spreads indicate a good entry

point to buy the SEK. The long-term

EUR/SEK average is way below today’sspot rate.

16

Henrik Unell and Rickard Hellman

S E K

ö v e r v ä r d e r a d

- >

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 17/26

NOK: fair value model points to 7.90

• Higher US rates destroy the carry trade

including the NOK.

•

Dovish Norges Bank the main trigger forthe EUR/NOK rally.

• We don’t see much more upside potential

for long end US rates short term.

• We don’t see Norges Bank cutting rates.

– Especially not with this weak NOK.

• Our fair value model points to 7.90.

– We expect implied volatility to come down

once liquidity improves which will bring

down the estimate as well.• The long-term forecast is based on our

forecast for interest rate differentials, oil

prices and historical average implied

volatility.

17

Ole Håkon Eek-Nielsen

7.057.10

7.157.207.257.307.357.407.457.507.557.607.657.707.757.80

7.857.907.958.008.058.108.158.20

May12 Jul12 Sep12 Nov12 Jan13 Mar13 May13Cut/hike Meeting Neutral EURNOK EURNOK

7.2

7.4

7.6

7.8

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6

9.8

10.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

7.2

7.4

7.6

7.8

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6

9.8

10.0

+/- 1 stdev ECB deposi t = 0 EURNOK Oi l trend, Imp Vol, Sov CDS & IR di f

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 18/26

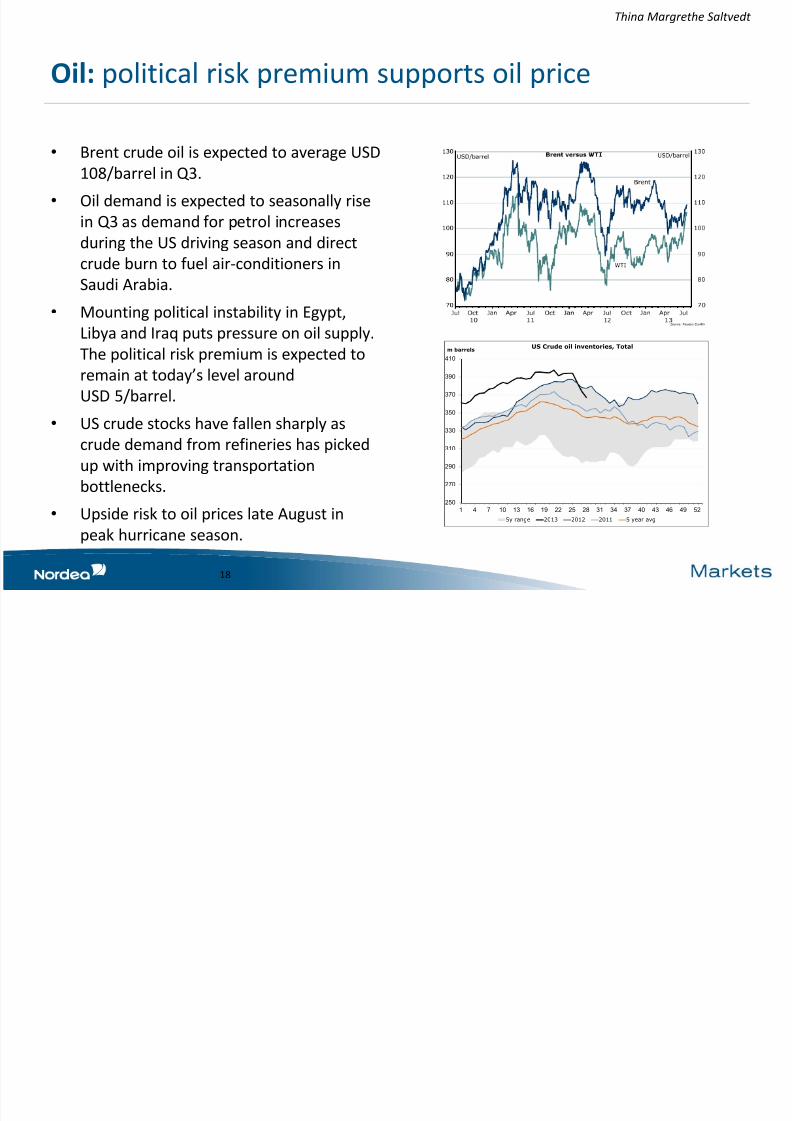

Oil: political risk premium supports oil price

18

Thina Margrethe Saltvedt

• Brent crude oil is expected to average USD

108/barrel in Q3.

•

Oil demand is expected to seasonally risein Q3 as demand for petrol increases

during the US driving season and direct

crude burn to fuel air-conditioners in

Saudi Arabia.

• Mounting political instability in Egypt,Libya and Iraq puts pressure on oil supply.

The political risk premium is expected to

remain at today’s level around

USD 5/barrel.

• US crude stocks have fallen sharply as

crude demand from refineries has picked

up with improving transportation

bottlenecks.

•

Upside risk to oil prices late August inpeak hurricane season.

250

270

290

310

330

350

370

390

410

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

m barrelsUS Crude oil inventories, Total

5y range 2013 2012 2011 5 year avg

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 19/26

Metals: lower price path on market surplus

19

Bjørnar Tonhaugen

• We lower our forecast across the base

metals complex partly on mark-to-market

and partly on a weaker outlook for China.

• We see upside from current levels for

prices of the four base metals covered

compared to cash costs and long-term

incentive prices, but upside is limited.

• Chinese demand has remained fairlystrong, but not enough to prevent global

inventory accumulation across most

metals. Risks to supply capacity

expansions are on the downside amid

weak prices, but markets remain well-supplied over the forecast horizon.

• The price path has been lowered as supply

has caught up with sluggish global

demand. Market balances will likely be

tighter in 2014, except for copper.Source: Nordea Markets and Reuters Ecowin

04 05 06 07 08 09 10 11 12 13 14

10

15

20

25

30

35

40

45

50

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Nickel, rhs

Zinc

('000) USD/tonne

Forecast

('000) USD/tonne

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 20/26

Tables

20

Fi i l f t

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 21/26

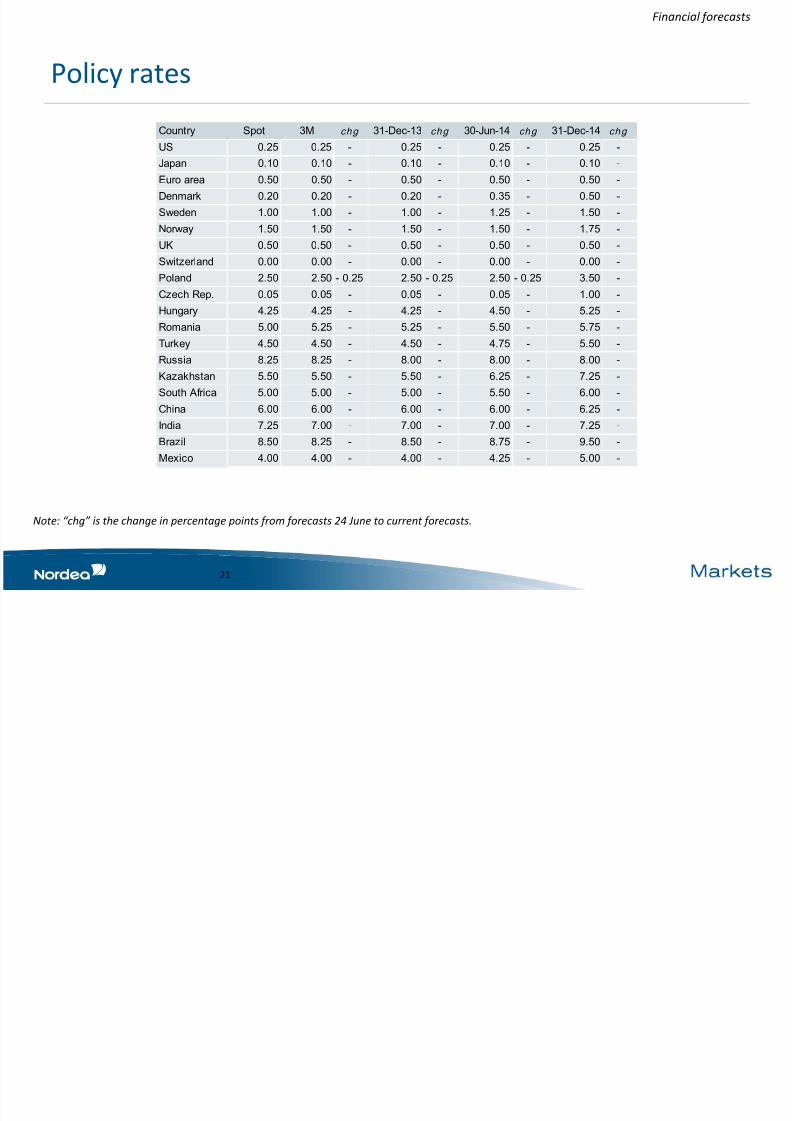

Policy rates

21

Financial forecasts

Note: “chg” is the change in percentage points from forecasts 24 June to current forecasts.

Country Spot 3M chg 31-Dec-13 chg 30-Jun-14 chg 31-Dec-14 chg

US 0.25 0.25 - 0.25 - 0.25 - 0.25 -

Japan 0.10 0.10 - 0.10 - 0.10 - 0.10 -

Euro area 0.50 0.50 - 0.50 - 0.50 - 0.50 -

Denmark 0.20 0.20 - 0.20 - 0.35 - 0.50 -

Sweden 1.00 1.00 - 1.00 - 1.25 - 1.50 -

Norway 1.50 1.50 - 1.50 - 1.50 - 1.75 -

UK 0.50 0.50 - 0.50 - 0.50 - 0.50 -

Switzerland 0.00 0.00 - 0.00 - 0.00 - 0.00 -

Poland 2.50 2.50 0.25- 2.50 0.25- 2.50 0.25- 3.50 -

Czech Rep. 0.05 0.05 - 0.05 - 0.05 - 1.00 -

Hungary 4.25 4.25 - 4.25 - 4.50 - 5.25 - Romania 5.00 5.25 - 5.25 - 5.50 - 5.75 -

Turkey 4.50 4.50 - 4.50 - 4.75 - 5.50 -

Russia 8.25 8.25 - 8.00 - 8.00 - 8.00 -

Kazakhstan 5.50 5.50 - 5.50 - 6.25 - 7.25 -

South Africa 5.00 5.00 - 5.00 - 5.50 - 6.00 -

China 6.00 6.00 - 6.00 - 6.00 - 6.25 -

India 7.25 7.00 - 7.00 - 7.00 - 7.25 -

Brazil 8.50 8.25 - 8.50 - 8.75 - 9.50 -

Mexico 4.00 4.00 - 4.00 - 4.25 - 5.00 -

Fi i l f t

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 22/26

Fixed income forecasts

22

Financial forecasts

Note: “chg” is the change in percentage points from forecasts 24 June to current forecasts.

Govies Govies

US Spot 3M ch g 31-Dec-13 chg 30-Jun-14 ch g 31-Dec-14 ch g Germany Spot 3M chg 31-Dec-13 chg 30-Jun-14 chg 31-Dec-14 chg

Leading rate 0.25 0.25 - 0.25 - 0.25 - 0.25 - Leading rate 0.50 0.50 - 0.50 - 0.50 - 0.50 -

3M 0.26 0.30 - 0.35 - 0.35 - 0.60 - 3M 0.22 0.20 - 0.20 - 0.30 - 0.40 -

2Y 0.30 0.30 - 0.65 - 1.20 - 2.10 - 2Y 0.08 0.00 - 0.15 - 0.50 - 1.10 -

5Y 1.28 1.00 - 1.45 - 2.00 - 2.75 - 5Y 0.50 0.35 - 0.90 - 1.25 - 1.80 -

10Y 2.47 2.10 - 2.65 - 2.80 - 3.25 - 10Y 1.51 1.30 - 1.90 - 2.10 - 2.40 -

30Y 3.54 3.30 - 3.65 - 3.75 - 4.00 - 30Y 2.37 2.25 - 2.65 - 2.80 - 3.00 -

5Y-2Y 0.98 0.70 - 0.80 - 0.80 - 0.65 - 5Y-2Y 0.42 0.35 - 0.75 - 0.75 - 0.70 -

10Y-2Y 2.17 1.80 - 2.00 - 1.60 - 1.15 - 10Y-2Y 1.44 1.30 - 1.75 - 1.60 - 1.30 -

30Y-10Y 1.08 1.20 1.00 - 0.95 - 0.75 - 30Y-10Y 0.85 0.95 - 0.75 - 0.70 - 0.60 -

Swap rate Swap rate

US Spot 3M ch g 31-Dec-13 chg 30-Jun-14 ch g 31-Dec-14 ch g EUR Spot 3M chg 31-Dec-13 chg 30-Jun-14 chg 31-Dec-14 chg

2Y 0.47 0.50 - 0.90 - 1.50 - 2.50 - 2Y 0.50 0.35 - 0.45 - 0.80 - 1.30 -

5Y 1.45 1.20 - 1.70 - 2.30 - 3.15 - 5Y 1.05 0.75 - 1.20 - 1.55 - 2.00 -

10Y 2.66 2.30 - 2.75 - 2.95 - 3.50 - 10Y 1.85 1.55 - 2.15 - 2.35 - 2.65 -

30Y 3.51 3.20 - 3.50 - 3.70 - 4.10 - 30Y 2.43 2.25 - 2.90 - 3.05 - 3.30 -

5Y-2Y 0.99 0.70 - 0.80 - 0.80 - 0.65 - 5Y-2Y 0.55 0.40 - 0.75 - 0.75 - 0.70 -

10Y-2Y 2.20 1.80 - 1.85 - 1.45 - 1.00 - 10Y-2Y 1.35 1.20 - 1.70 - 1.55 - 1.35 -

30Y-10Y 0.85 0.90 - 0.75 - 0.75 - 0.60 - 30Y-10Y 0.58 0.70 - 0.75 - 0.70 - 0.65 -

Financial forecasts

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 23/26

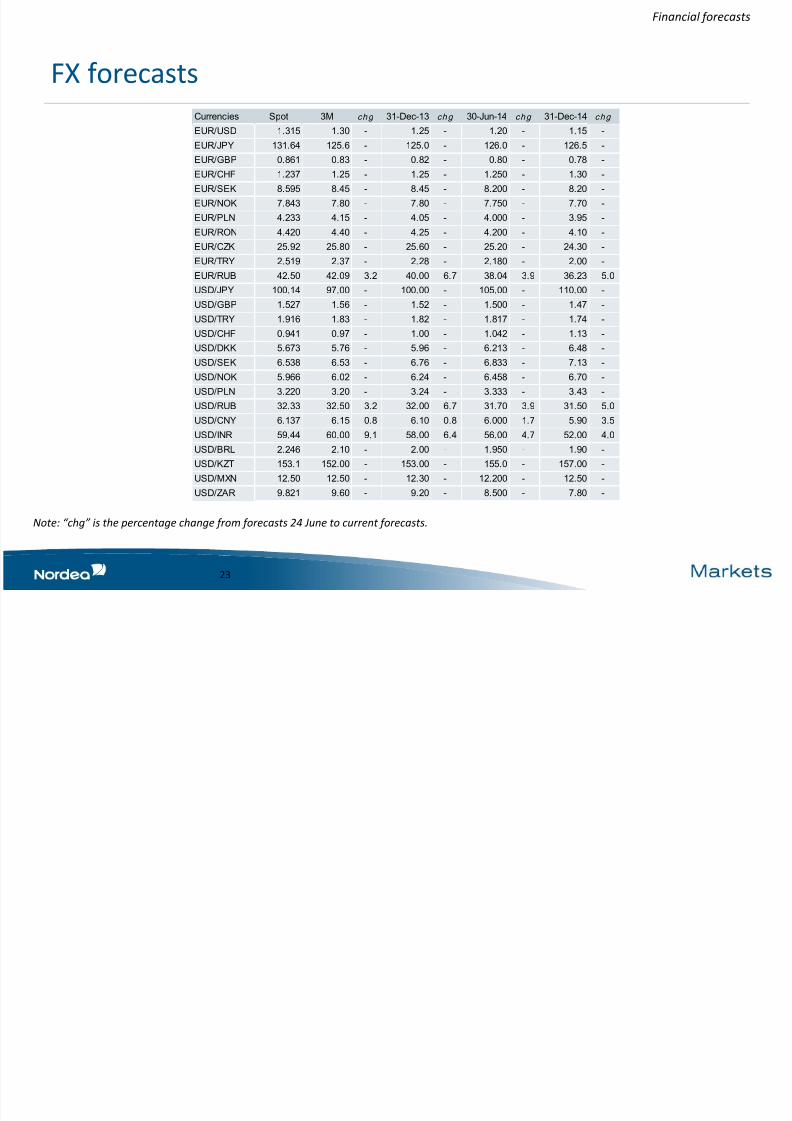

FX forecasts

23

Financial forecasts

Note: “chg” is the percentage change from forecasts 24 June to current forecasts.

Currencies Spot 3M chg 31-Dec-13 chg 30-Jun-14 chg 31-Dec-14 chg

EUR/USD 1.315 1.30 - 1.25 - 1.20 - 1.15 -

EUR/JPY 131.64 125.6 - 125.0 - 126.0 - 126.5 -

EUR/GBP 0.861 0.83 - 0.82 - 0.80 - 0.78 -

EUR/CHF 1.237 1.25 - 1.25 - 1.250 - 1.30 -

EUR/SEK 8.595 8.45 - 8.45 - 8.200 - 8.20 -

EUR/NOK 7.843 7.80 - 7.80 - 7.750 - 7.70 -

EUR/PLN 4.233 4.15 - 4.05 - 4.000 - 3.95 -

EUR/RON 4.420 4.40 - 4.25 - 4.200 - 4.10 -

EUR/CZK 25.92 25.80 - 25.60 - 25.20 - 24.30 -

EUR/TRY 2.519 2.37 - 2.28 - 2.180 - 2.00 -

EUR/RUB 42.50 42.09 3.2 40.00 6.7 38.04 3.9 36.23 5.0

USD/JPY 100.14 97.00 - 100.00 - 105.00 - 110.00 -

USD/GBP 1.527 1.56 - 1.52 - 1.500 - 1.47 -

USD/TRY 1.916 1.83 - 1.82 - 1.817 - 1.74 -

USD/CHF 0.941 0.97 - 1.00 - 1.042 - 1.13 -

USD/DKK 5.673 5.76 - 5.96 - 6.213 - 6.48 -

USD/SEK 6.538 6.53 - 6.76 - 6.833 - 7.13 -

USD/NOK 5.966 6.02 - 6.24 - 6.458 - 6.70 -

USD/PLN 3.220 3.20 - 3.24 - 3.333 - 3.43 -

USD/RUB 32.33 32.50 3.2 32.00 6.7 31.70 3.9 31.50 5.0

USD/CNY 6.137 6.15 0.8 6.10 0.8 6.000 1.7 5.90 3.5

USD/INR 59.44 60.00 9.1 58.00 6.4 56.00 4.7 52.00 4.0

USD/BRL 2.246 2.10 - 2.00 - 1.950 - 1.90 -

USD/KZT 153.1 152.00 - 153.00 - 155.0 - 157.00 -

USD/MXN 12.50 12.50 - 12.30 - 12.200 - 12.50 -

USD/ZAR 9.821 9.60 - 9.20 - 8.500 - 7.80 -

Financial forecasts

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 24/26

Commodities

24

Financial forecasts

Note: “chg” is the percentage change from forecasts 24 June to current forecasts. Commodity forecasts are average prices over periods.

Metals Spot 2013 chg 2014 chg

Aluminum 1,773 1,973 - 2,275 -

Copper 6,920 7,343 - 7,500 -

Gold 1,318 1,500 - 1,400 -

Nickel 13,980 15,149 - 16,000 -

Silver 20.0 26.0 - 24.0 -

Zinc 1,834 1,894 - 2,200 -

Oil New chg

Spot 110

6/30/2013 104 -

9/30/2013 108 -

12/31/2013 110 -

3/31/2014 111 -

6/30/2014 110 -

9/30/2014 112 -

12/31/2014 112 -

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 25/26

Global Research

Global MacroHelge Pedersen, Global Chief Economist*

Focus: Global & Denmark

+45 3333 3126 / +45 2269 7912

Johnny Bo Jakobsen, Chief Analyst

Focus: North America

[email protected] +45 3333 6178 / +45 6122 4550

Anders Svendsen, Chief Analyst

Focus: Europe

+45 3333 3951 / +45 6122 4549

Dr. Holger Sandte, Chief Analyst

Focus: Europe

[email protected] +45 3333 1191 / +45 6122 3076

Amy Zhuang, CFA, Senior Analyst

Focus: Asia

+45 3333 5607 / +45 6122 2287

Piotr Bujak, Chief Economist*

Focus: Poland

+48 2252 13651 / +48 693 333 127

25

Dmitry Savchenko, CFA, Chief Economist*

Focus: Russia

+7 495 7773477, ext. 4194

Tõnu Palm, Chief Economist*

Focus: Estonia

+372 6283345

Andris Strazds, Chief Economist*

Focus: Latvia

+371 6700 5252

Annika Lindblad, Analyst*

Focus: Czech Republic, Hungary & Turkey

[email protected] +358 9 165 59940 / +358 50 34 88545

Zygimantas Mauricas, Chief Economist*

Focus: Lithuania

+370 5265 7198

Heidi Østergaard, Assistant Analyst

Focus: Data mining, support

[email protected] +45 3333 6102

Henrik L. Rasmussen, Assistant Analyst

Focus: Data mining, support

+45 3333 4007

Global StrategyJan von Gerich, Chief Analyst

Focus: Fixed Income Strategy (Euro)

+358 9 165 59937 / +358 500 405 182

Christian Börjesson, Chief Analyst

Focus: Fixed Income Strategy (US)

[email protected] +46 8614 7884 / +46 7611 80622

Fredrik Floric, Chief Analyst

Focus: Fixed Income Strategy (Scandi)

+46 8614 8215 / +46 70 235 1078

Aurelija Augulyte, CFA, Senior Analyst

Focus: FX Strategy

[email protected] +45 3333 6437 / +45 6122 3247

Fredrik L. Paulsson, Analyst

Focus: FX Strategy

+45 3333 6437 / +45 6122 3247

Bjørnar Tonhaugen, Senior Analyst

Focus: Commodities (Energy and metals)

[email protected] +47 2248 7959 / +47 4666 2509

Thina M. Saltvedt, Chief Analyst*

Focus: Oil and global commodities

+47 2248 7993

Emil Kuch Jørgensen, Assistant Analyst

Focus: Data mining, support [email protected]

+45 3333 1502

Global ResearchSteen V. Grøndahl

Senior Director & Head of Global Research

+45 33331453 / +45 6122 2388

* Reports to local manager

7/28/2019 Nordea Bank, Financial Forecast Update, July 22, 2013.

http://slidepdf.com/reader/full/nordea-bank-financial-forecast-update-july-22-2013 26/26

Thank you!

Global Research, Nordea Markets

Nordea Markets is the name of the Markets departments of Nordea Bank

Norge ASA, Nordea Bank AB (publ), Nordea Bank Finland Plc and Nordea

Bank Danmark A/S.

The information provided herein is intended for background information

only and for the sole use of the intended recipient. The views and other

information provided herein are the current views of Nordea Markets as of

the date of this document and are subject to change without notice. This

notice is not an exhaustive description of the described product or the risksrelated to it, and it should not be relied on as such, nor is it a substitute for

the judgement of the recipient.

The information provided herein is not intended to constitute and does not

constitute investment advice nor is the information intended as an offer or

solicitation for the purchase or sale of any financial instrument. Theinformation contained herein has no regard to the specific investment

objectives, the financial situation or particular needs of any particular

recipient. Relevant and specific professional advice should always be

obtained before making any investment or credit decision. It is important to

note that past performance is not indicative of future results.

Nordea Markets is not and does not purport to be an adviser as to legal,

taxation, accounting or regulatory matters in any jurisdiction.

This document may not be reproduced, distributed or published for any

purpose without the prior written consent from Nordea Markets.