NEW YORK WORKERS’ COMPENSATION OCTOBER 1, …2017-8-18 · NEW YORK WORKERS’ COMPENSATION...

88

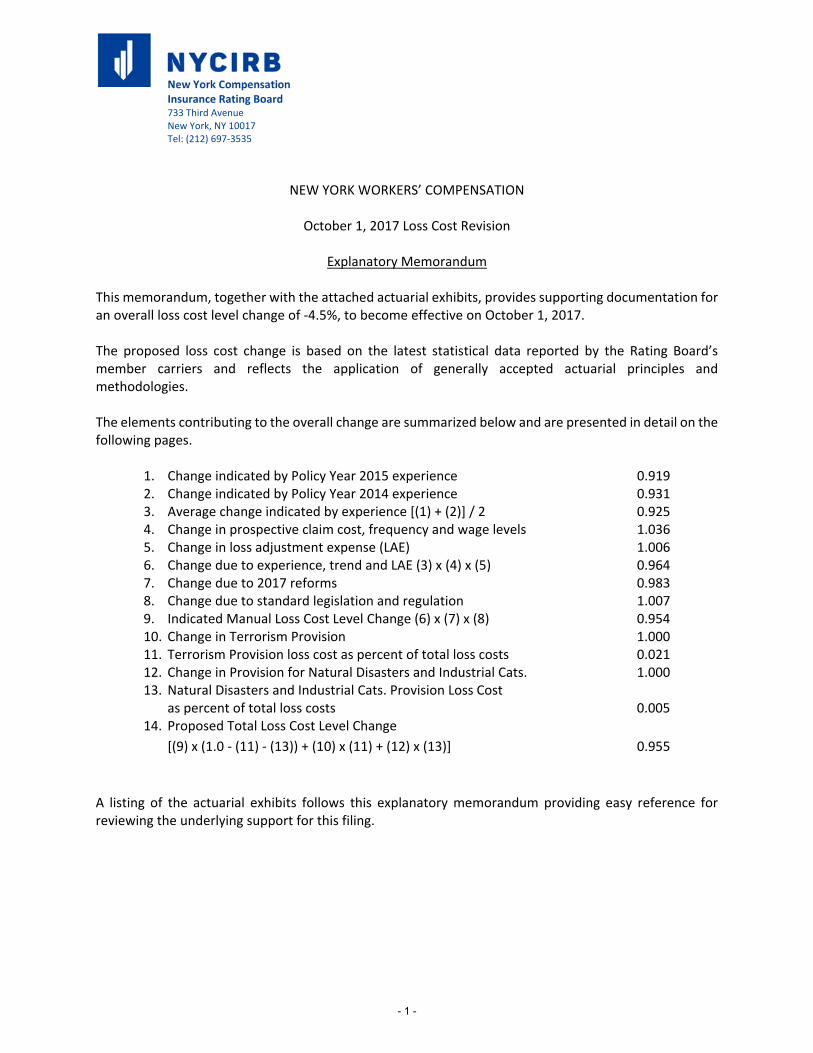

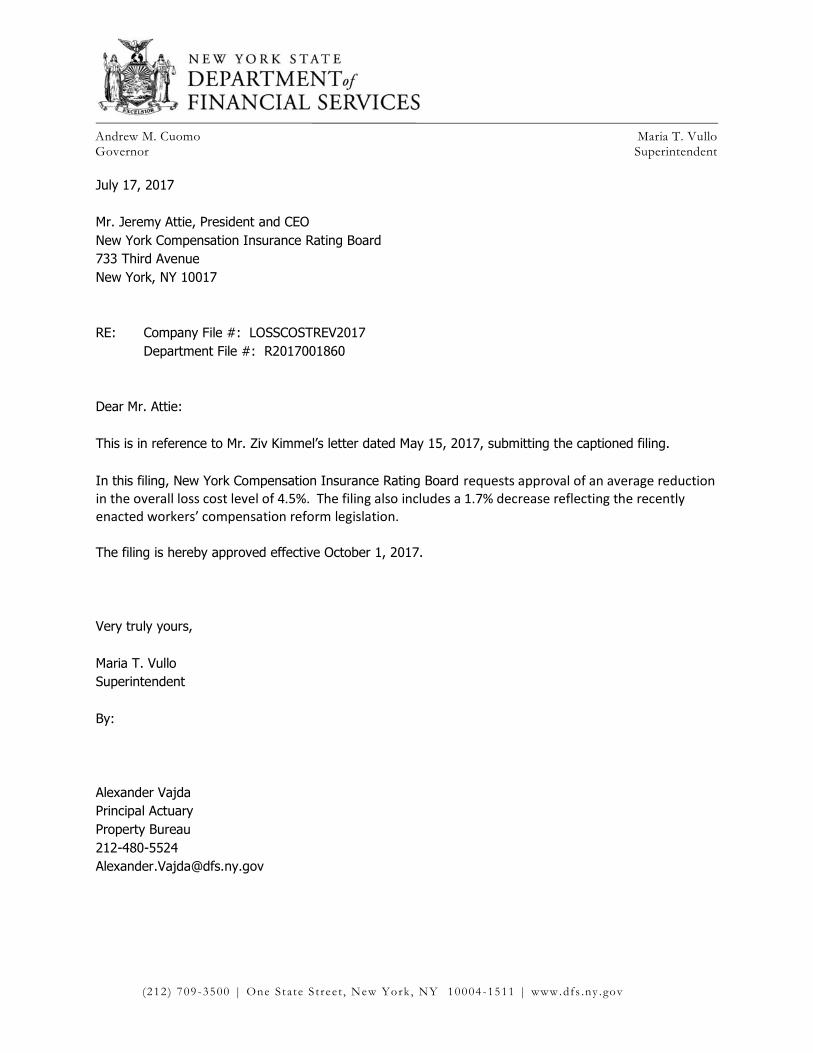

NEW YORK WORKERS’ COMPENSATION OCTOBER 1, 2017 LOSS COST FILING • Actuarial Committee Recommended Loss Cost Level Change: -4.5% • Proposed Loss Cost Level Change: -4.5% • Approved Loss Cost Level Change: -4.5% The Rating Board submitted the 2017 General Loss Cost Revision to the New York State Department of Financial Services on May 15, 2017 requesting an average change of -4.5% in the loss cost level to become effective on October 1, 2017. The loss cost revision reflects the experience of the two most recent policy years, as well as projected trends, benefit level changes, and changes in loss adjustment expenses. In addition, the proposed change reflects the impact of certain components of the 2017 workers’ compensation reform. The filing proposed no changes to the terrorism and catastrophe loss cost provisions. The filing was approved on July 17, 2017. The attached actuarial exhibits provide specific information on all components of the approved 2017 loss cost revision. Included also is the detailed Filing Memorandum that accompanied the Rating Board’s filing submission. The Department of Financial Services’ approval letter is also attached and can be found following the actuarial exhibits.

Transcript of NEW YORK WORKERS’ COMPENSATION OCTOBER 1, …2017-8-18 · NEW YORK WORKERS’ COMPENSATION...

NEW YORK WORKERS’ COMPENSATION OCTOBER 1, 2017 LOSS COST FILING

• Actuarial Committee Recommended Loss Cost Level Change: -4.5%

• Proposed Loss Cost Level Change: -4.5%

• Approved Loss Cost Level Change: -4.5%

The Rating Board submitted the 2017 General Loss Cost Revision to the New York State Department of Financial Services on May 15, 2017 requesting an average change of -4.5% in the loss cost level to become effective on October 1, 2017.

The loss cost revision reflects the experience of the two most recent policy years, as well

as projected trends, benefit level changes, and changes in loss adjustment expenses. In addition, the proposed change reflects the impact of certain components of the 2017 workers’ compensation reform. The filing proposed no changes to the terrorism and catastrophe loss cost provisions.

The filing was approved on July 17, 2017.

The attached actuarial exhibits provide specific information on all components of the approved 2017 loss cost revision. Included also is the detailed Filing Memorandum that accompanied the Rating Board’s filing submission.

The Department of Financial Services’ approval letter is also attached and can be found following the actuarial exhibits.

New York Compensation Insurance Rating Board 733 Third Avenue New York, NY 10017 Tel: (212) 697‐3535

NEW YORK WORKERS’ COMPENSATION

October 1, 2017 Loss Cost Revision

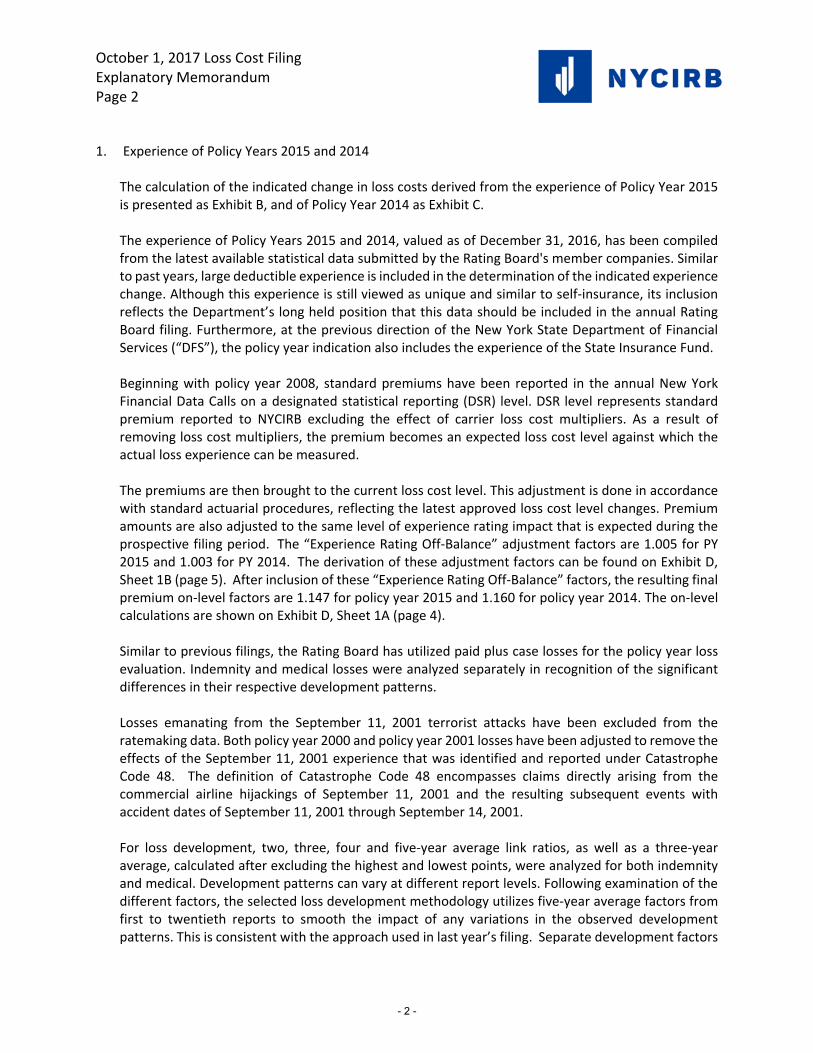

Explanatory Memorandum This memorandum, together with the attached actuarial exhibits, provides supporting documentation for an overall loss cost level change of ‐4.5%, to become effective on October 1, 2017. The proposed loss cost change is based on the latest statistical data reported by the Rating Board’s member carriers and reflects the application of generally accepted actuarial principles and methodologies. The elements contributing to the overall change are summarized below and are presented in detail on the following pages.

1. Change indicated by Policy Year 2015 experience 0.919 2. Change indicated by Policy Year 2014 experience 0.931 3. Average change indicated by experience [(1) + (2)] / 2 0.925 4. Change in prospective claim cost, frequency and wage levels 1.036 5. Change in loss adjustment expense (LAE) 1.006 6. Change due to experience, trend and LAE (3) x (4) x (5) 0.964 7. Change due to 2017 reforms 0.983 8. Change due to standard legislation and regulation 1.007 9. Indicated Manual Loss Cost Level Change (6) x (7) x (8) 0.954 10. Change in Terrorism Provision 1.000 11. Terrorism Provision loss cost as percent of total loss costs 0.021 12. Change in Provision for Natural Disasters and Industrial Cats. 1.000 13. Natural Disasters and Industrial Cats. Provision Loss Cost

as percent of total loss costs 0.005 14. Proposed Total Loss Cost Level Change

[(9) x (1.0 ‐ (11) ‐ (13)) + (10) x (11) + (12) x (13)] 0.955

A listing of the actuarial exhibits follows this explanatory memorandum providing easy reference for reviewing the underlying support for this filing.

- 1 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 2 1. Experience of Policy Years 2015 and 2014

The calculation of the indicated change in loss costs derived from the experience of Policy Year 2015 is presented as Exhibit B, and of Policy Year 2014 as Exhibit C.

The experience of Policy Years 2015 and 2014, valued as of December 31, 2016, has been compiled from the latest available statistical data submitted by the Rating Board's member companies. Similar to past years, large deductible experience is included in the determination of the indicated experience change. Although this experience is still viewed as unique and similar to self‐insurance, its inclusion reflects the Department’s long held position that this data should be included in the annual Rating Board filing. Furthermore, at the previous direction of the New York State Department of Financial Services (“DFS”), the policy year indication also includes the experience of the State Insurance Fund.

Beginning with policy year 2008, standard premiums have been reported in the annual New York Financial Data Calls on a designated statistical reporting (DSR) level. DSR level represents standard premium reported to NYCIRB excluding the effect of carrier loss cost multipliers. As a result of removing loss cost multipliers, the premium becomes an expected loss cost level against which the actual loss experience can be measured.

The premiums are then brought to the current loss cost level. This adjustment is done in accordance with standard actuarial procedures, reflecting the latest approved loss cost level changes. Premium amounts are also adjusted to the same level of experience rating impact that is expected during the prospective filing period. The “Experience Rating Off‐Balance” adjustment factors are 1.005 for PY 2015 and 1.003 for PY 2014. The derivation of these adjustment factors can be found on Exhibit D, Sheet 1B (page 5). After inclusion of these “Experience Rating Off‐Balance” factors, the resulting final premium on‐level factors are 1.147 for policy year 2015 and 1.160 for policy year 2014. The on‐level calculations are shown on Exhibit D, Sheet 1A (page 4).

Similar to previous filings, the Rating Board has utilized paid plus case losses for the policy year loss evaluation. Indemnity and medical losses were analyzed separately in recognition of the significant differences in their respective development patterns.

Losses emanating from the September 11, 2001 terrorist attacks have been excluded from the ratemaking data. Both policy year 2000 and policy year 2001 losses have been adjusted to remove the effects of the September 11, 2001 experience that was identified and reported under Catastrophe Code 48. The definition of Catastrophe Code 48 encompasses claims directly arising from the commercial airline hijackings of September 11, 2001 and the resulting subsequent events with accident dates of September 11, 2001 through September 14, 2001.

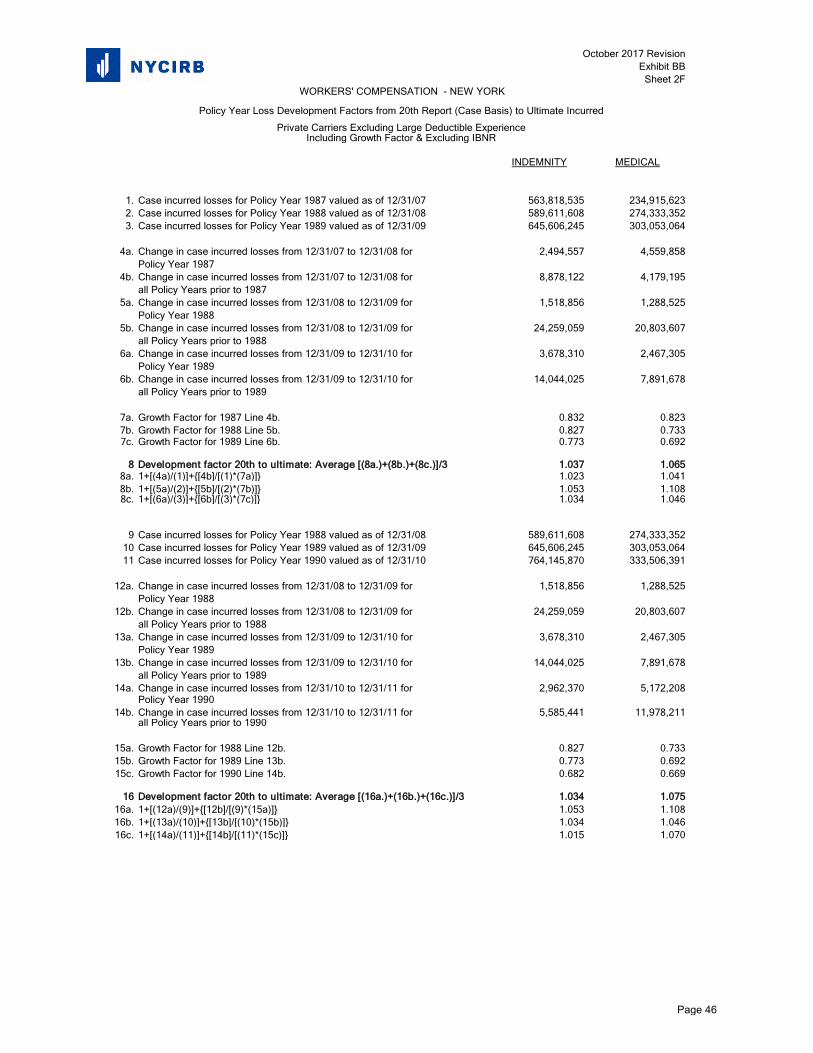

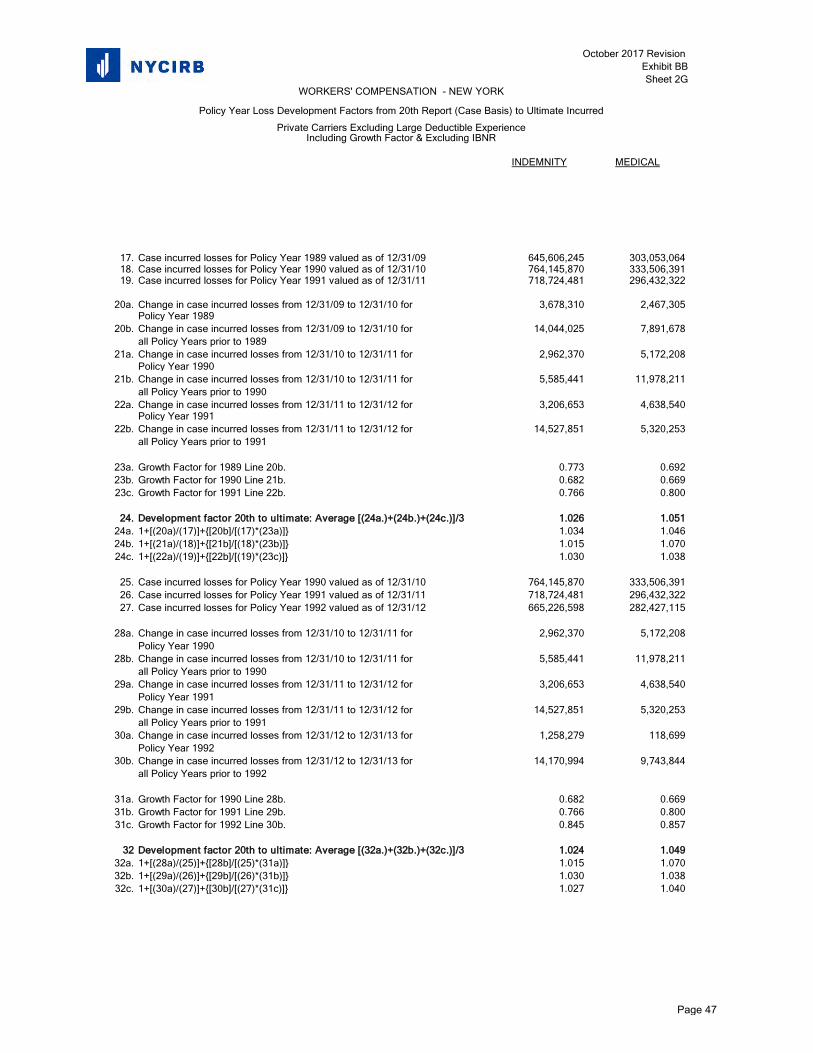

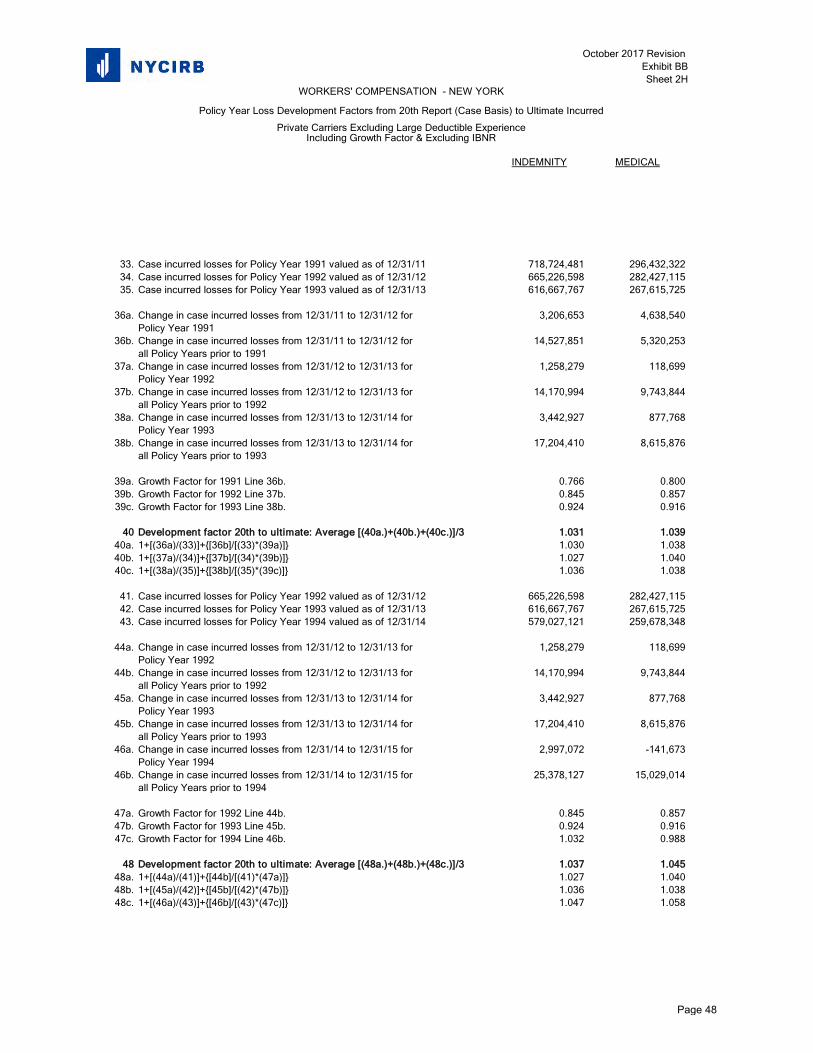

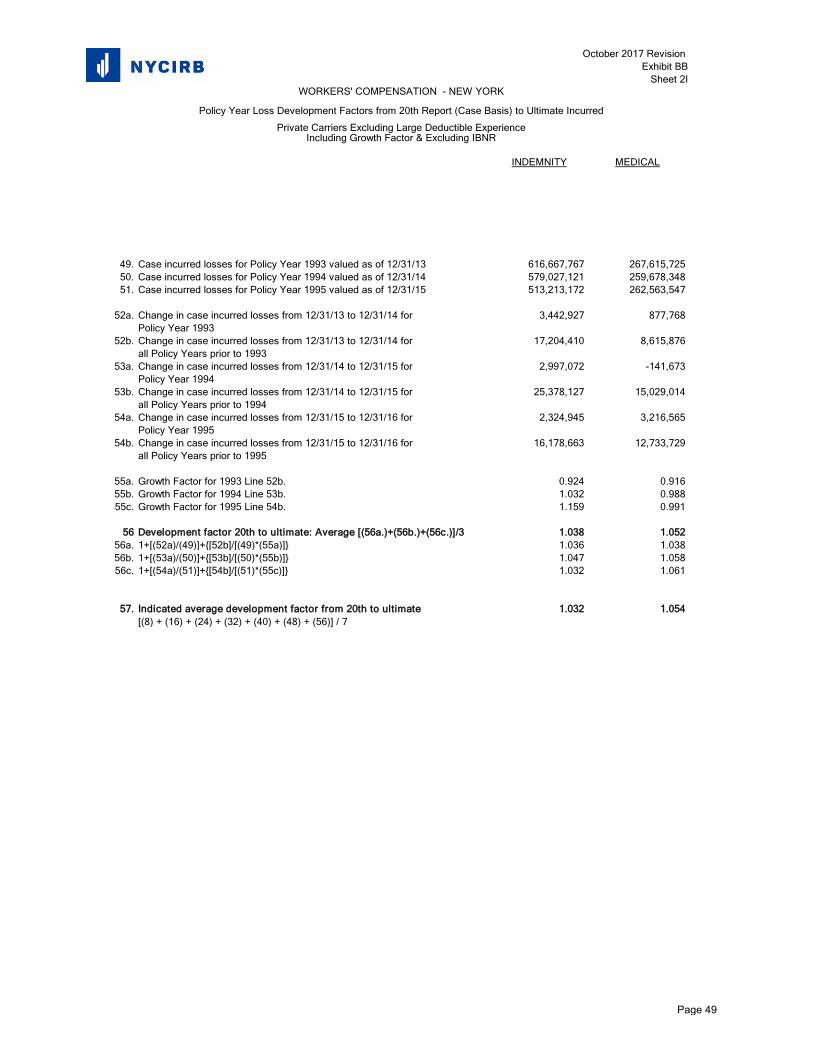

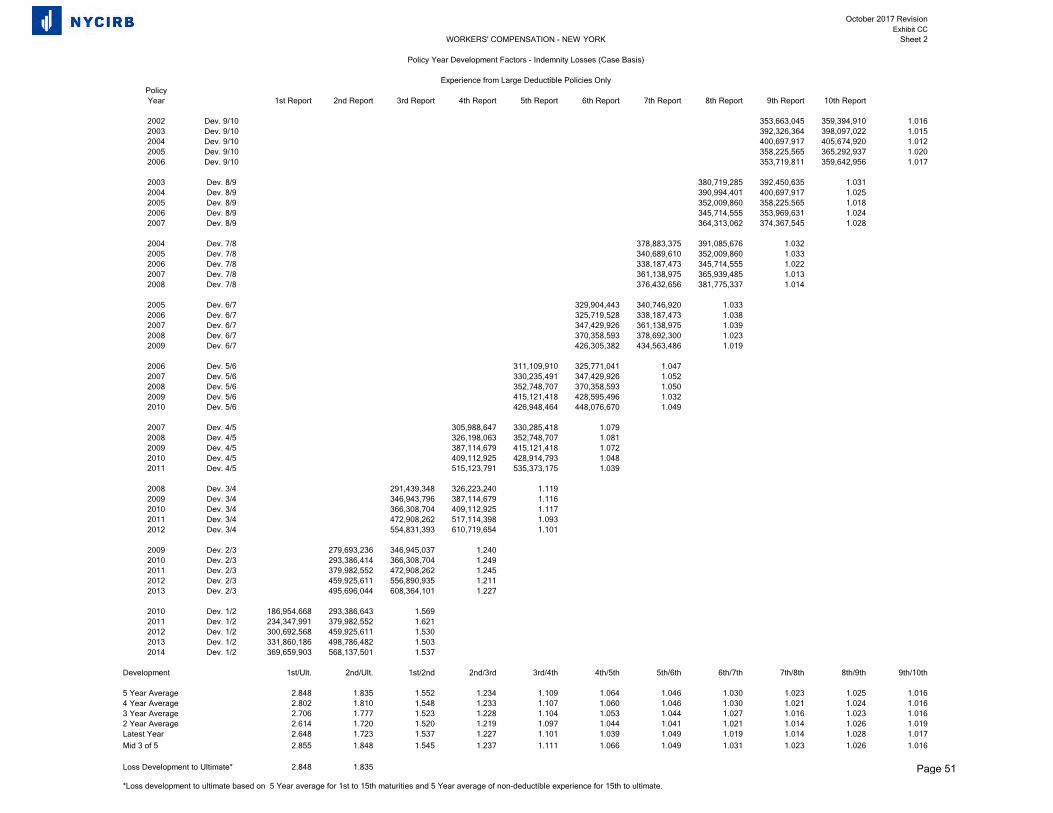

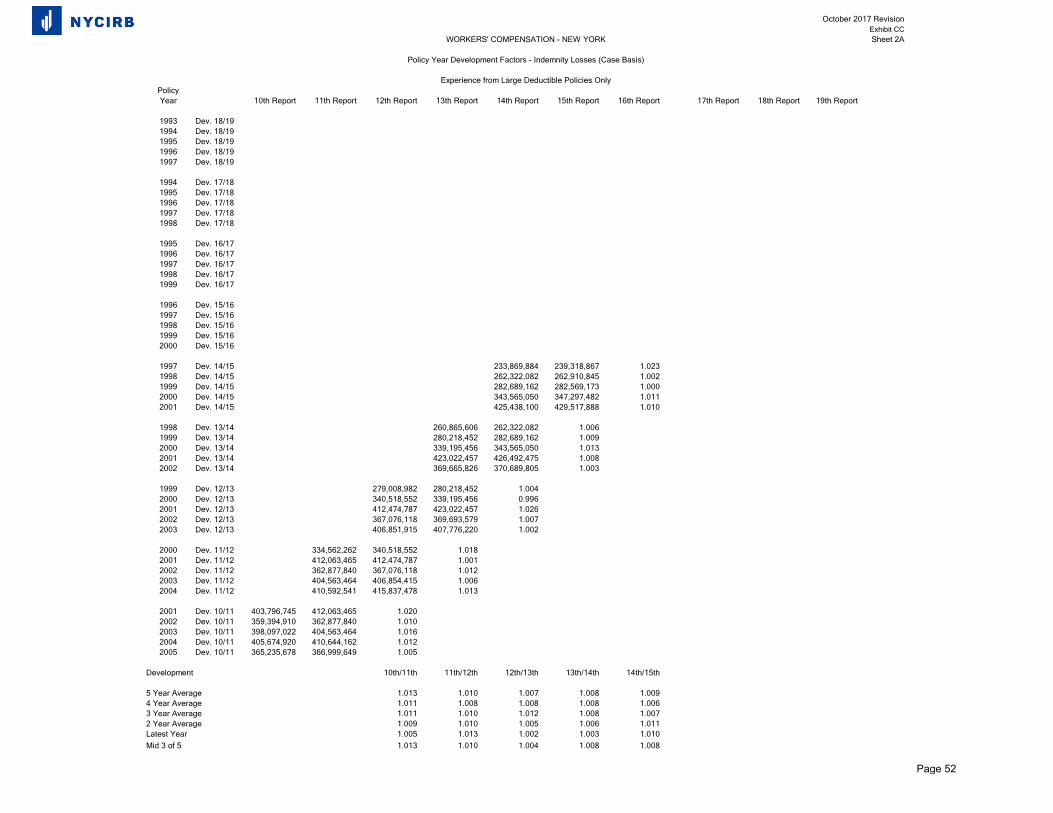

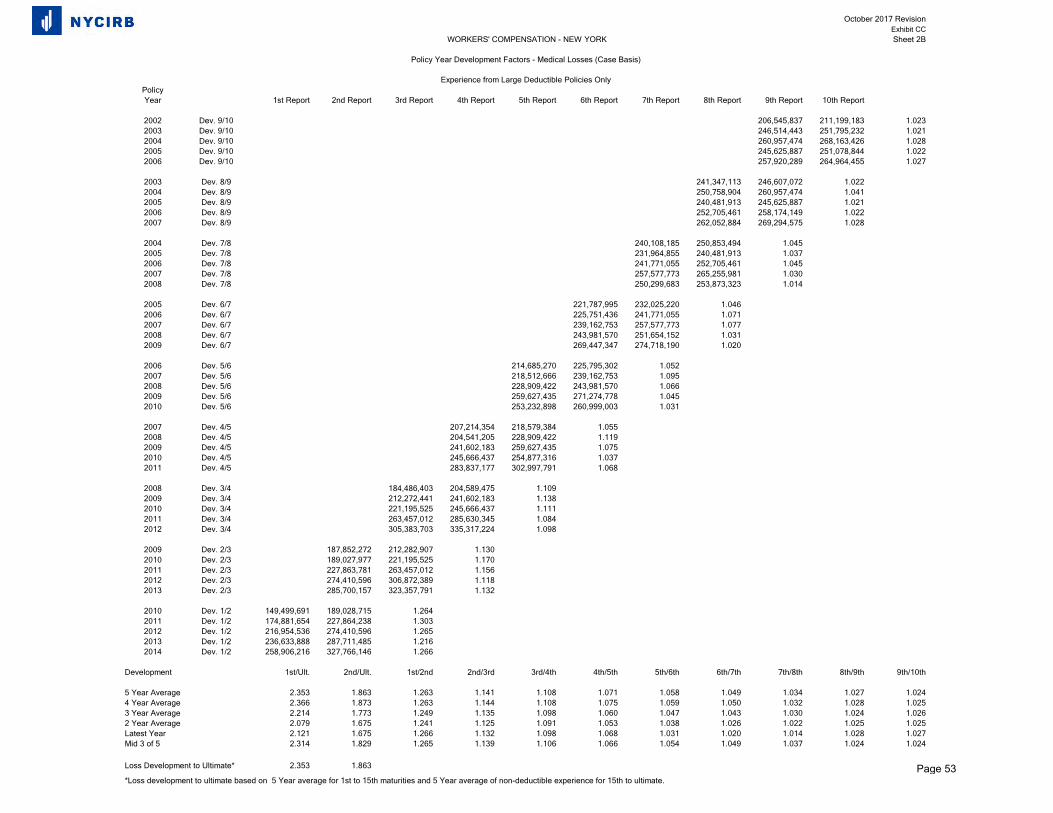

For loss development, two, three, four and five‐year average link ratios, as well as a three‐year average, calculated after excluding the highest and lowest points, were analyzed for both indemnity and medical. Development patterns can vary at different report levels. Following examination of the different factors, the selected loss development methodology utilizes five‐year average factors from first to twentieth reports to smooth the impact of any variations in the observed development patterns. This is consistent with the approach used in last year’s filing. Separate development factors

- 2 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 3

were derived for the non‐large deductible experience, the large deductible experience, and the State Insurance Fund using the same methodology, except for the 11th to 12th report development ratio for the State Insurance Fund, where the middle three of five factors were used.

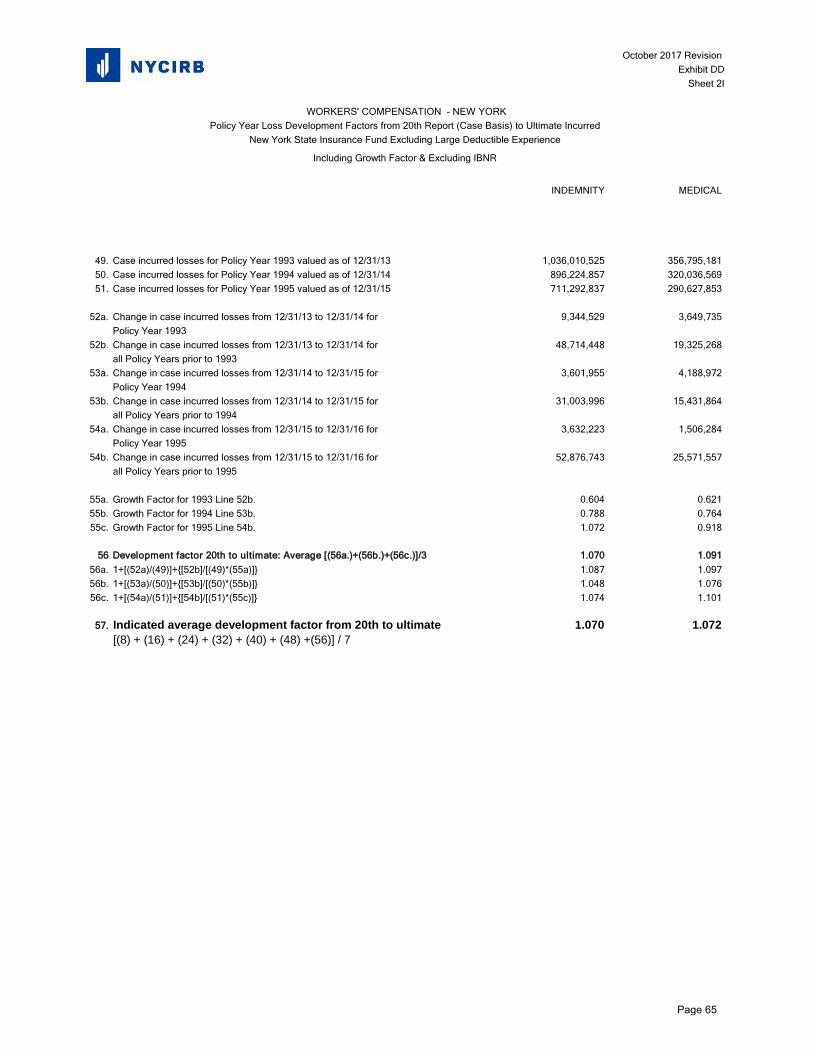

The procedure used to calculate the loss development factor from 20th to ultimate (the tail factor) is similar to the procedure used in last year’s filing, utilizing paid plus case losses and applying a growth factor. The growth factor is used to adjust the experience of prior years used in the tail calculation to the level of the base development year at 19th report. The adjustment is needed to reflect trend and benefit level changes in the historical experience. Information from Policy Years 1987 through 1995 was included in the tail factor calculation. This approach is consistent with the methodology used by NCCI. An improvement, included in this year’s filing, is the utilization of seven reports of data at seven successive valuations. The final tail factor is determined by averaging these seven factors. This enhancement to the tail methodology should improve long term tail factor stability. Last year, a six‐year average was used.

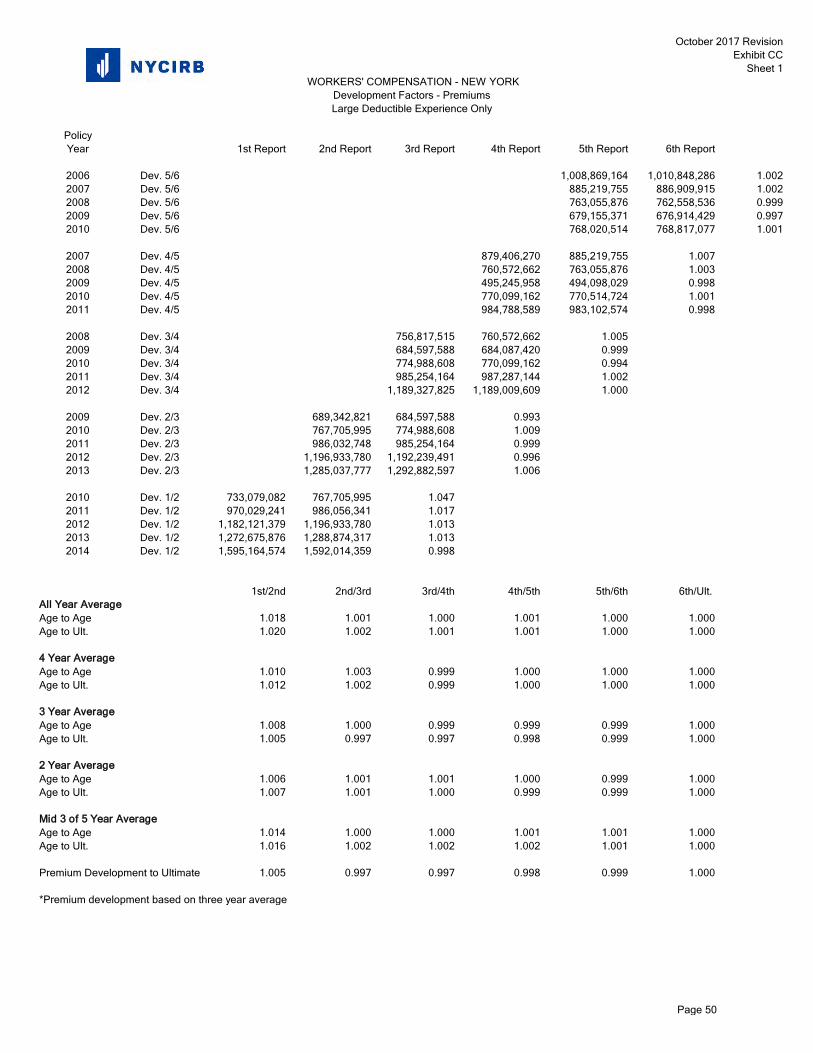

Premium development factors for both non‐large deductible and large deductible private carriers, as well as the State Insurance Fund, are based on three‐year averages.

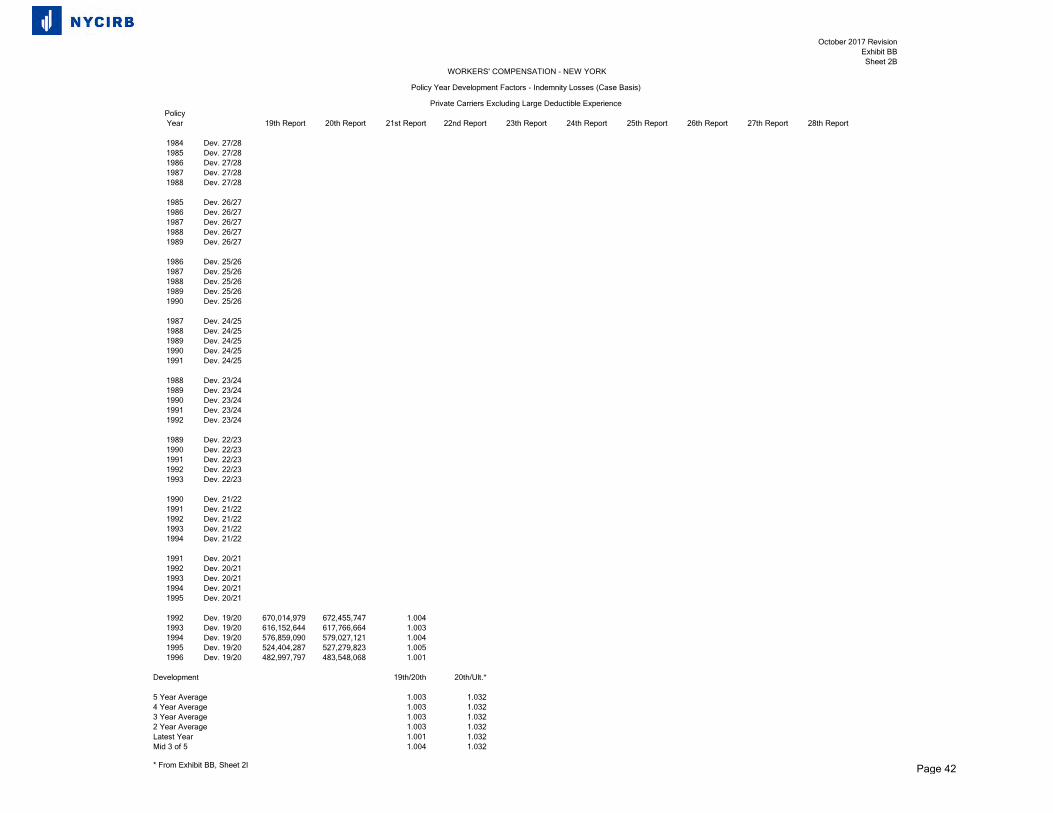

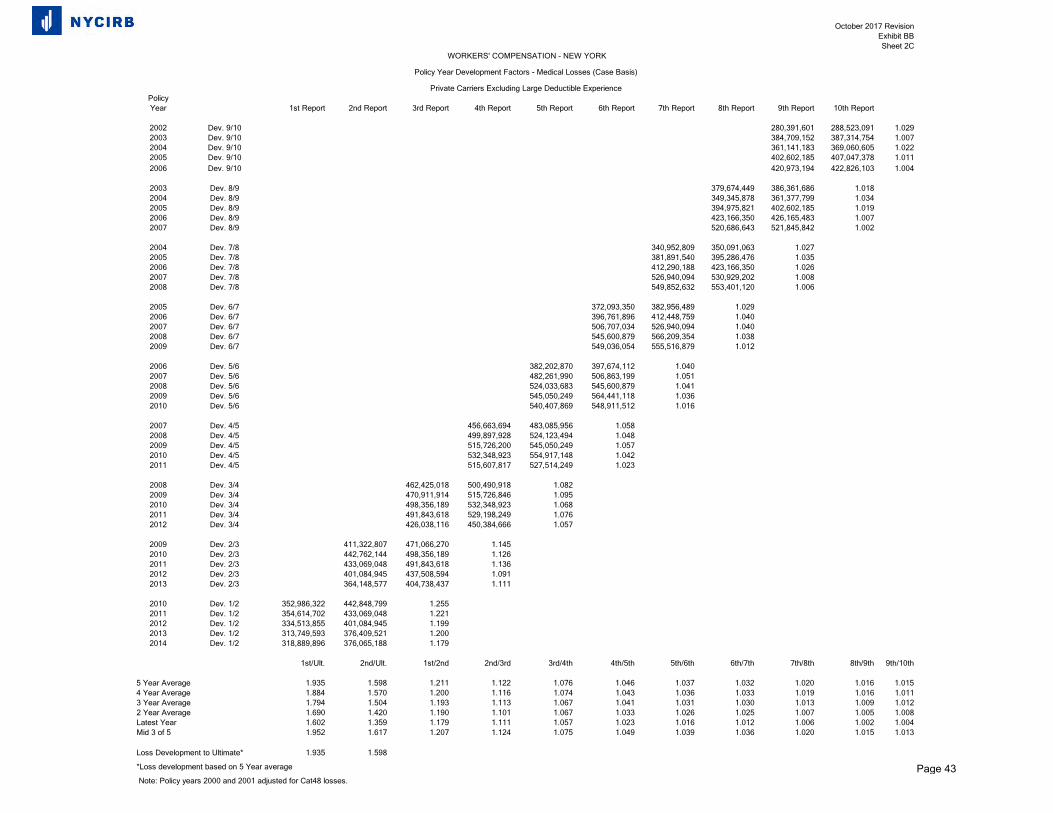

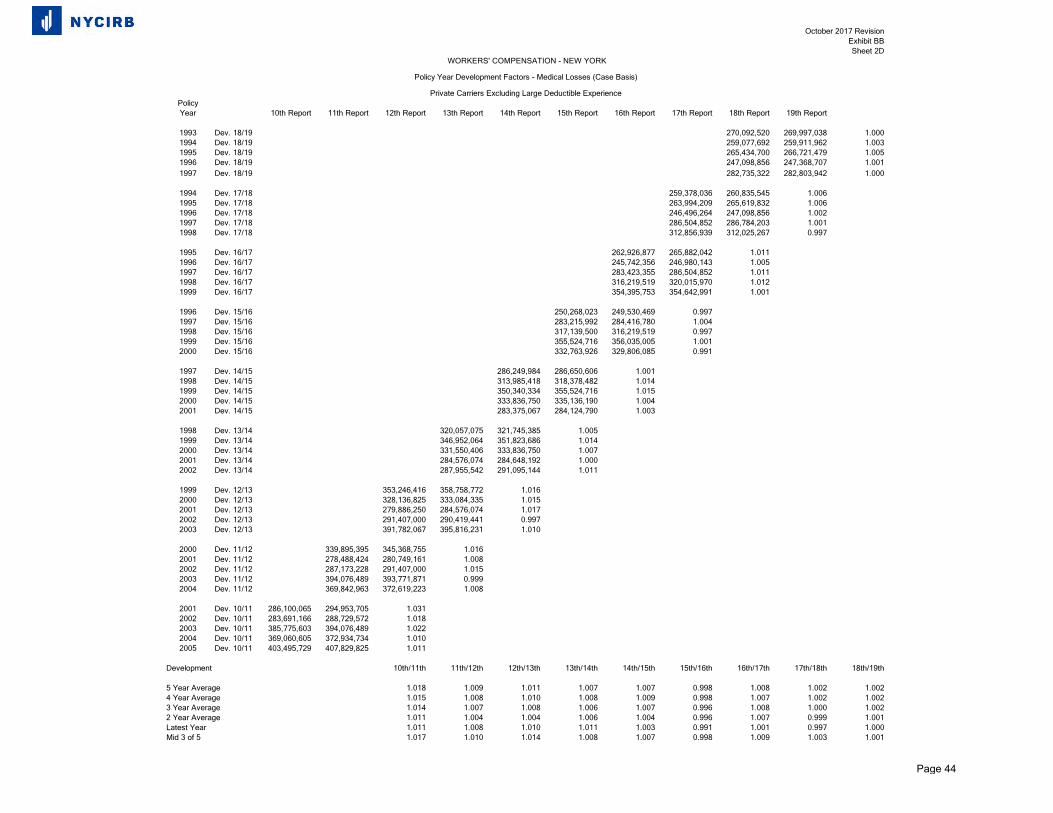

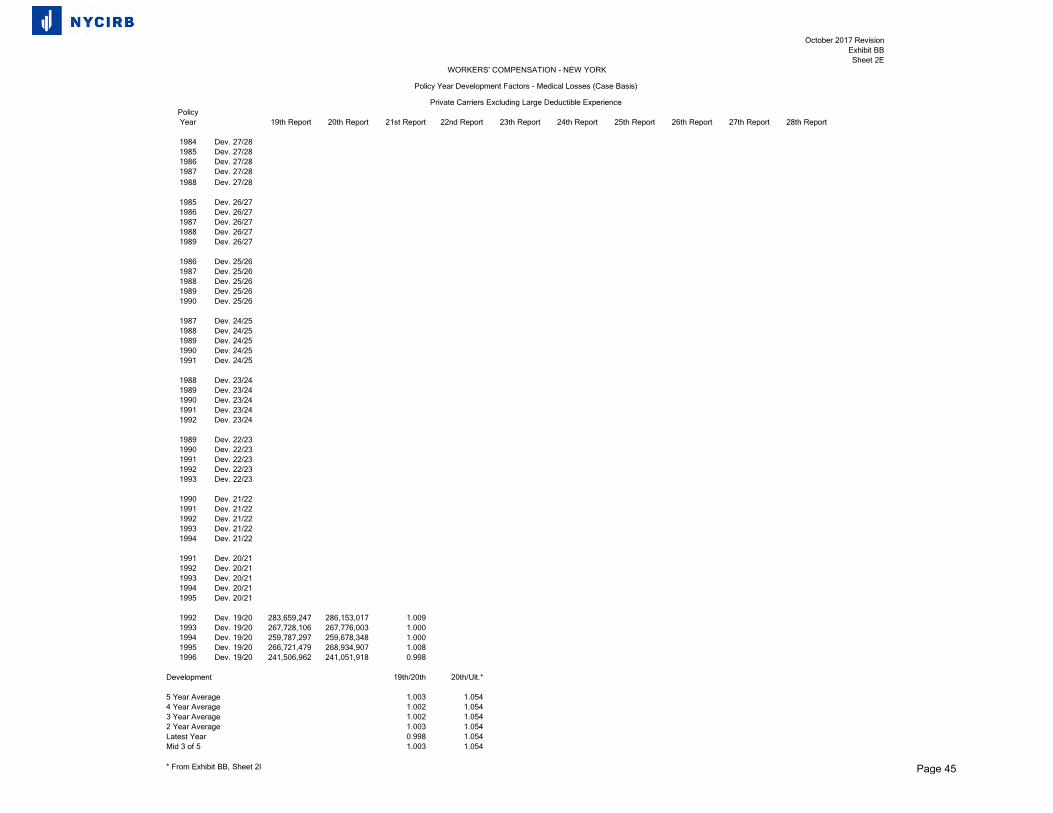

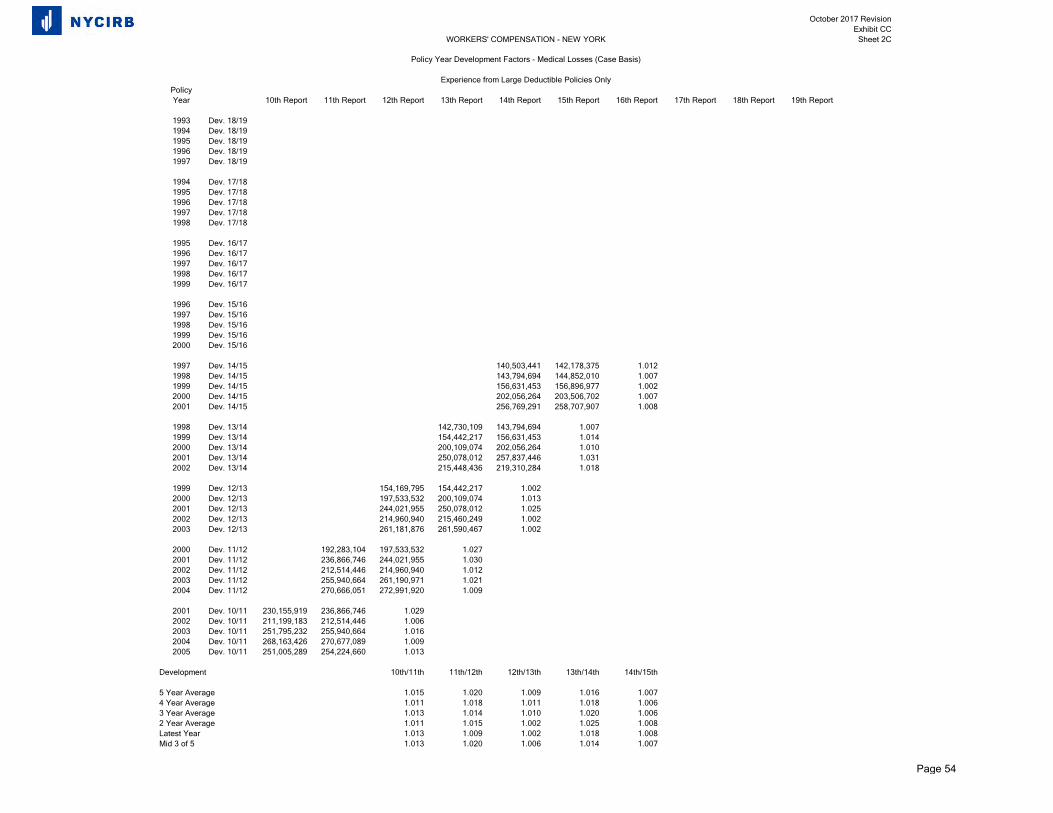

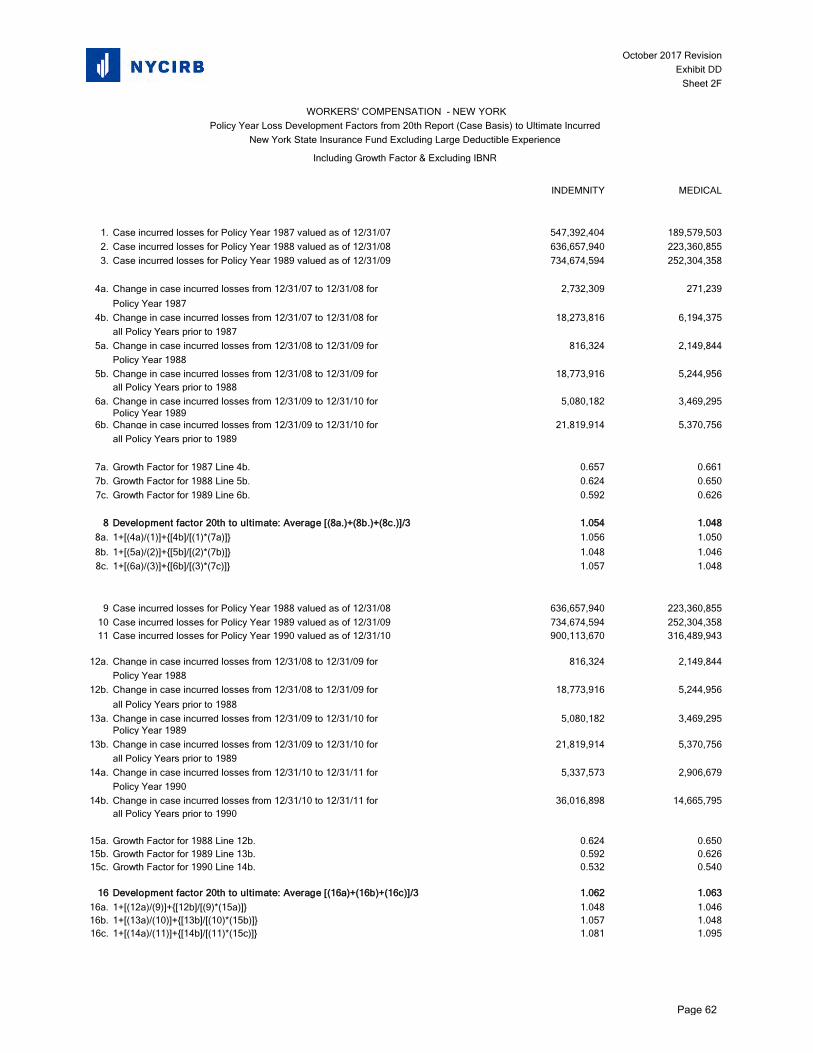

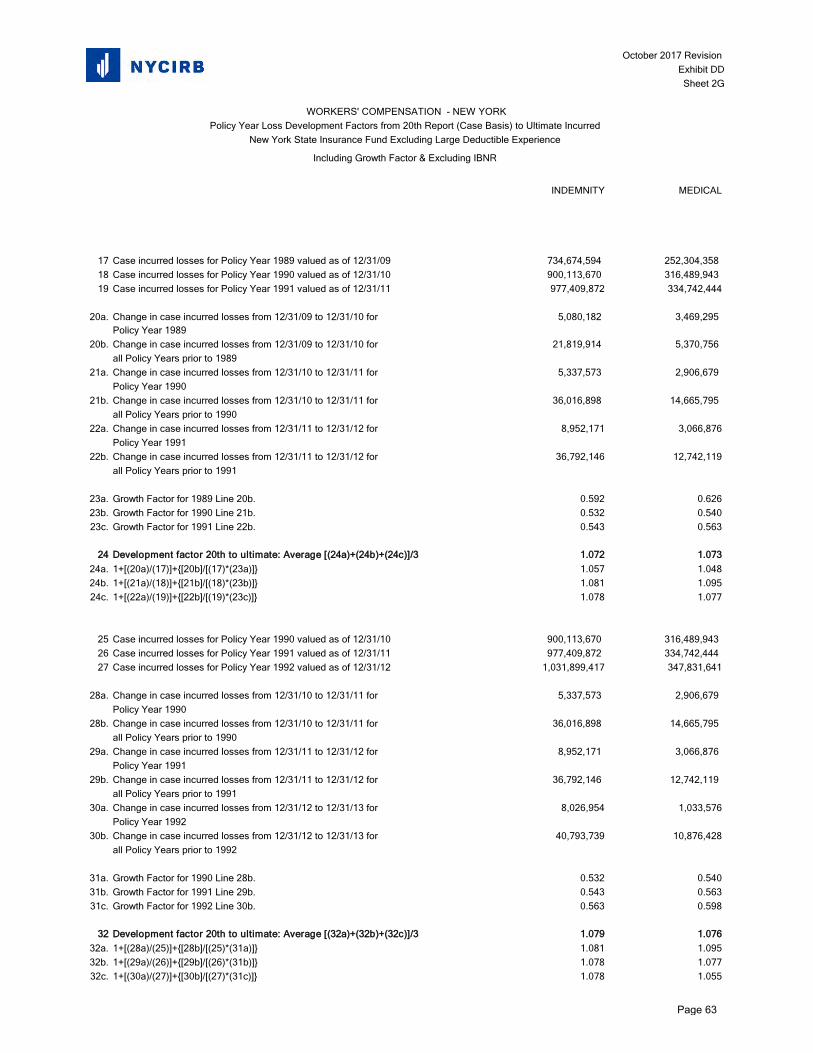

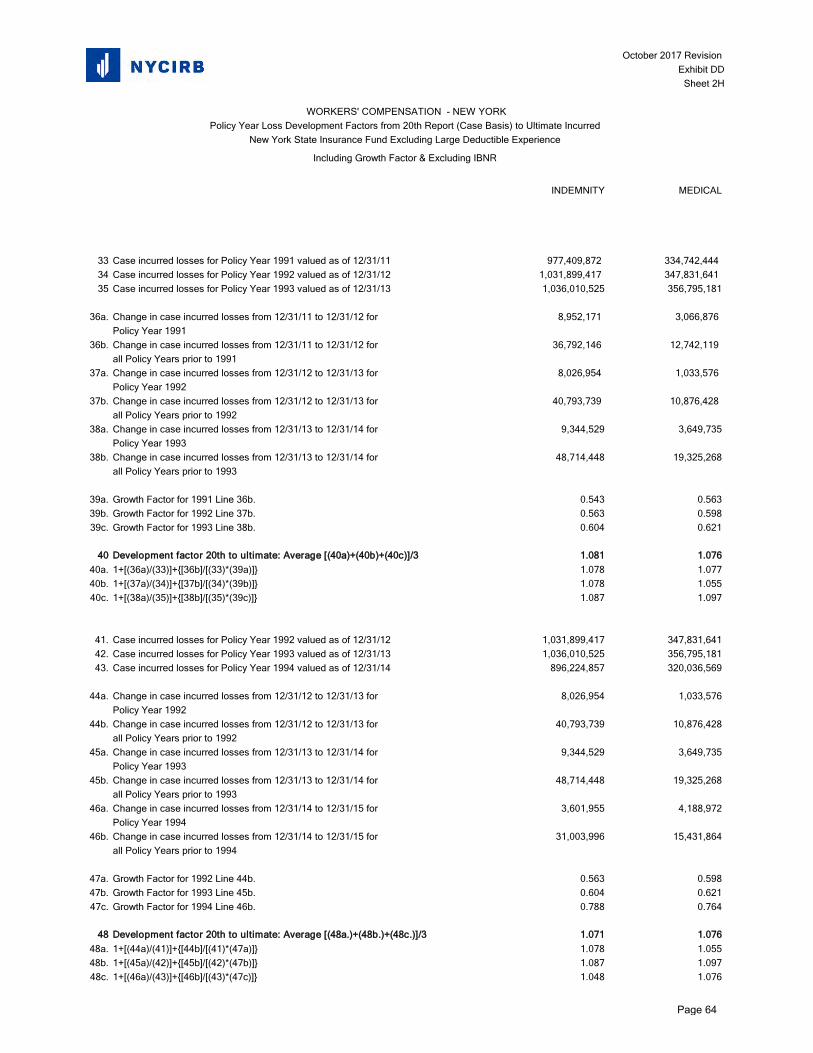

The private carrier non‐large deductible development data can be found on Exhibits BB, Sheets 1 through 2I (pages 35‐45). For large deductible development, exhibits labeled as Exhibit CC, Sheets 1‐2C (pages 46‐50) are provided.

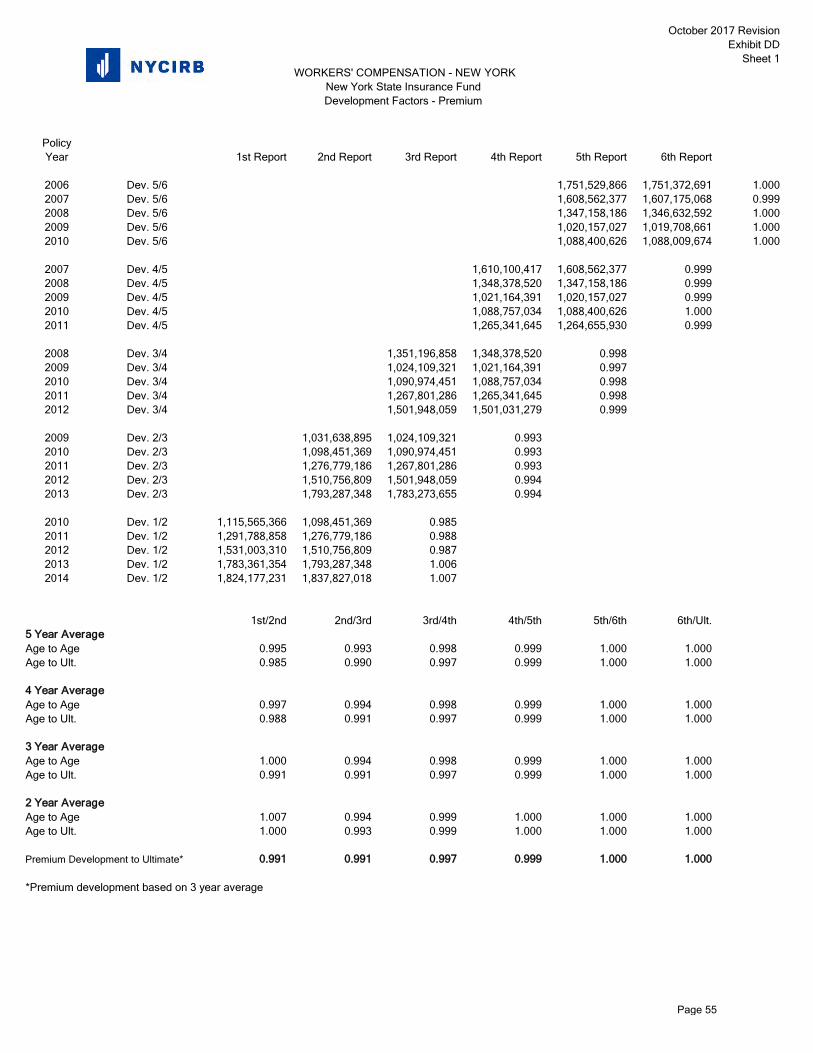

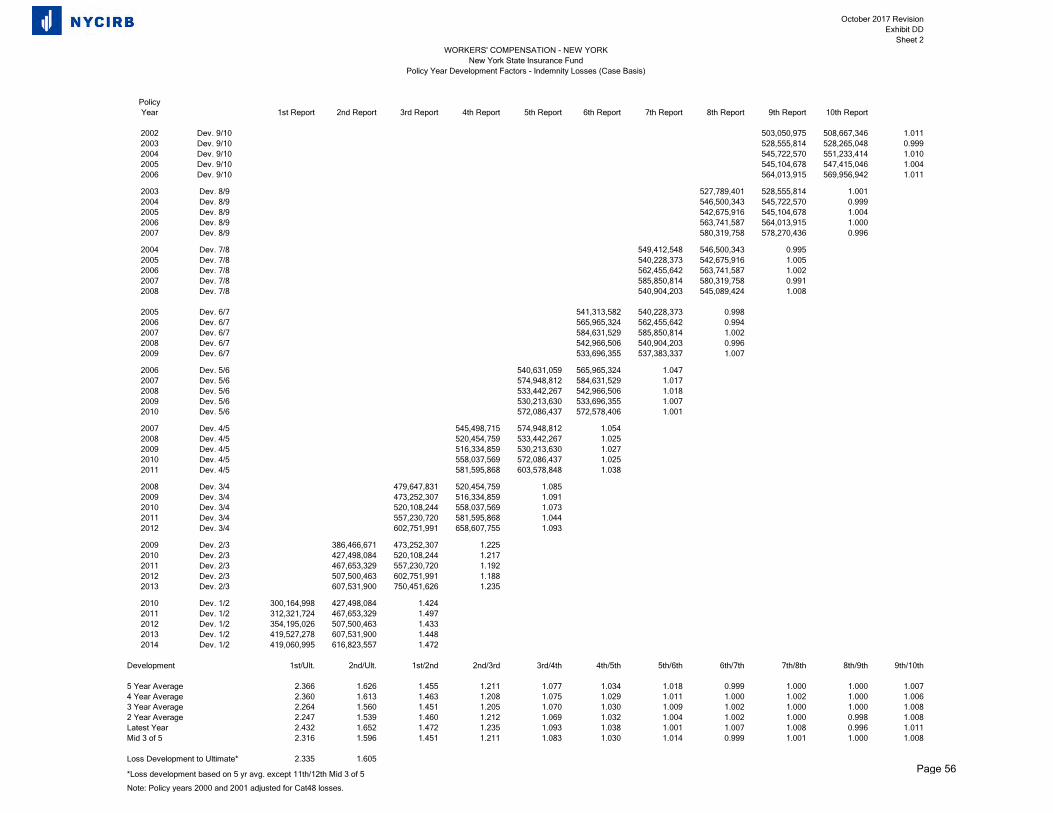

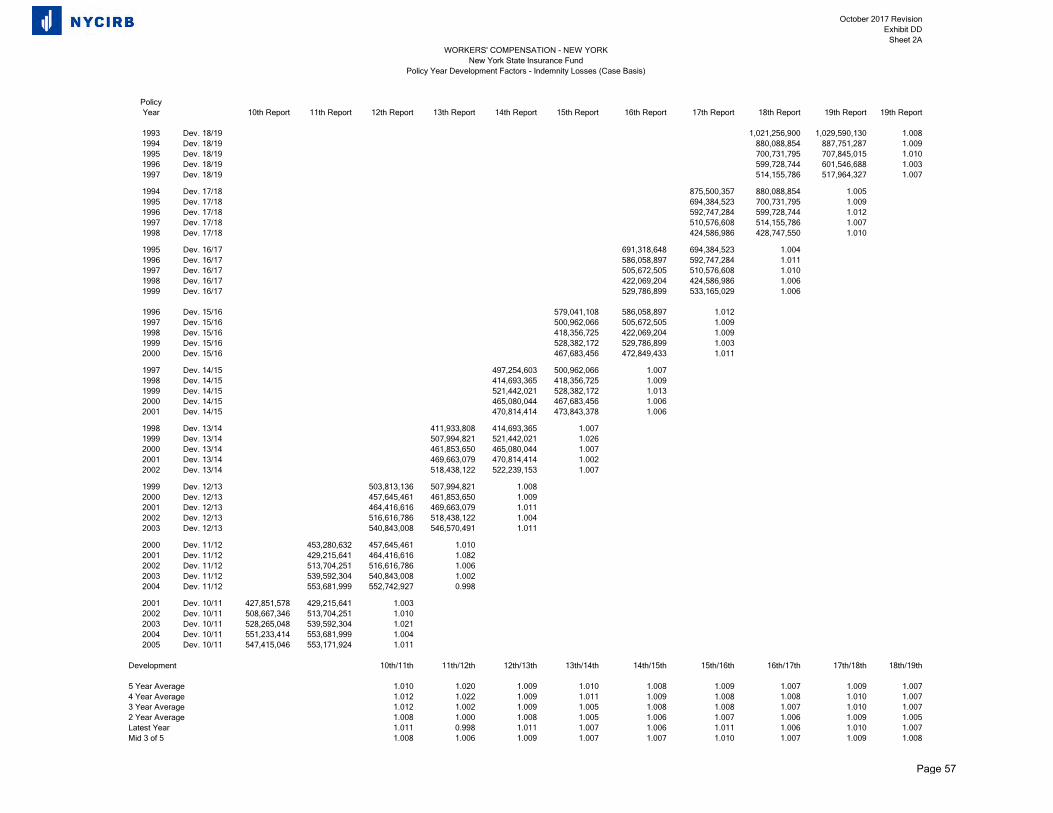

Exhibit DD, Sheets 1‐2I (pages 51‐61) contains the experience of the State Insurance Fund. These pages include premium development factors for the policy year, and separate indemnity and medical loss development factors. Because of the large volume of State Insurance Fund data, it is appropriate that projections of ultimate losses reflect this experience’s own development patterns. This is consistent with the approach utilized in past filings. Policy year losses for the private carrier non‐large deductible experience, State Insurance Fund experience, and the large deductible experience are separately adjusted to an ultimate settlement basis, as described above.

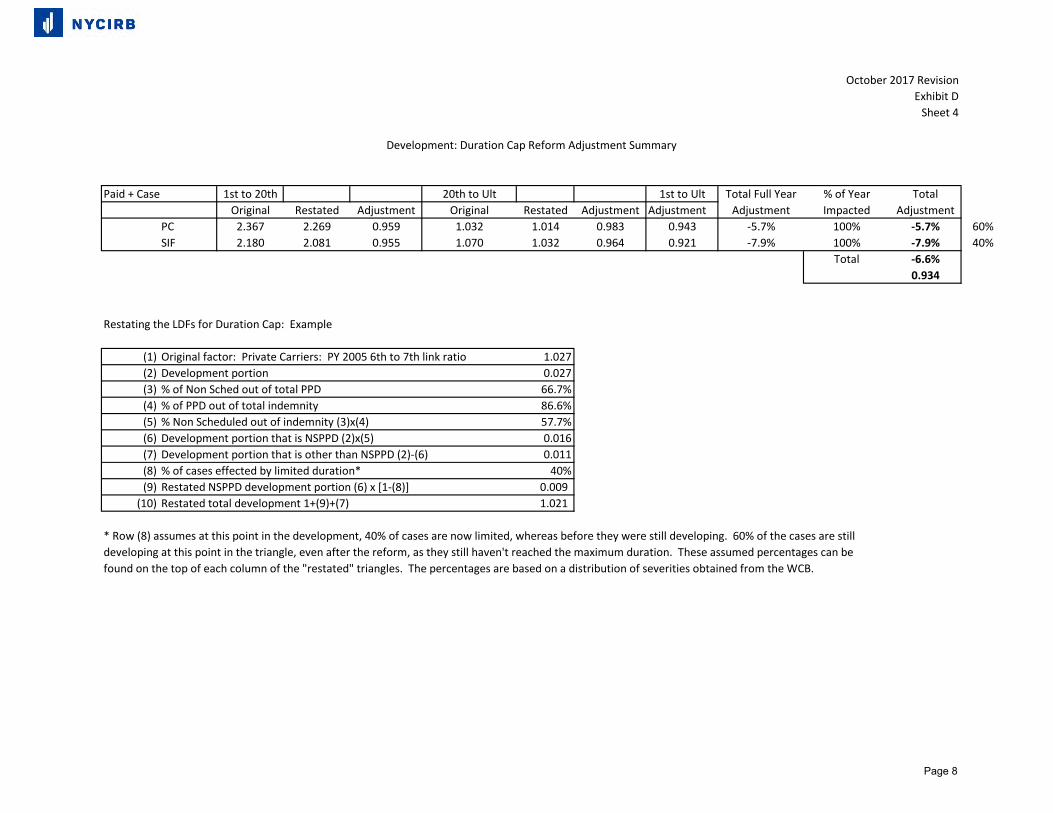

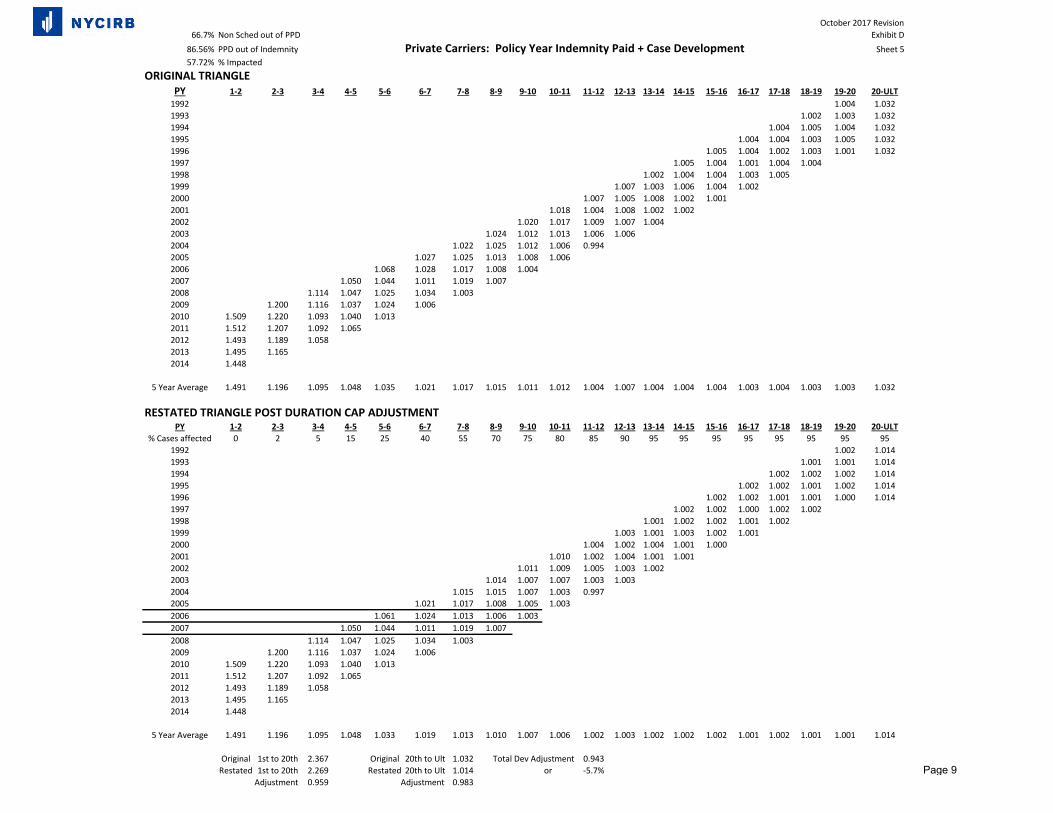

Losses are then adjusted to reflect the current benefit level. All losses in the experience period of policy years 2014 and 2015 have occurred subsequent to the 2007 reforms. The three major components of the 2007 reform are the increase in maximum weekly benefits, the elimination of the Special Disability Fund (“SDF”) and the introduction of capped benefit durations for claimants with Non‐Scheduled Permanent Partial Disability Benefits (“NS‐PPD”). In theory, losses that have occurred after the reform would not need to be adjusted for the full impact of the reform, as they are already at the post‐reform level. However, because experience from pre‐reform years is used to derive loss development factors, using the LDFs as reported may not result in appropriate post‐reform ultimate losses. Therefore, some adjustments are warranted. The adjustment due to the implementation of duration caps is derived by restating any pre‐reform link ratio from the reported development triangle to post‐reform level. Then, the adjustment factor

- 3 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 4

is the ratio of the resulting ultimate development factor after the restatement to the ultimate factor based on the reported values. The restatement of each link ratio assumes that a portion of the development that is reflected in the link ratio is attributable to the unwinding of discount on life annuities on NS‐PPD injuries, while the remainder is due to other injuries. Based on Unit Statistical Data, it was determined that, for the pre‐reform years, permanent partial indemnity costs account for 86.56% of total indemnity costs. It was also determined, based on data obtained from the New York State Workers’ Compensation Board (“WCB”) that 66.7% out of all permanent partial injuries were, in fact, NS‐PPD. Therefore, 57.7% (=.667 x .8656) out of total indemnity are attributable to NS‐PPD, which is the portion of the development factor that needs to be adjusted. The remaining 42.3% of indemnity costs are not adjusted. The full details of the calculation are presented on Exhibit D, Sheet 4 (page 8) and the restated LDF triangle is shown on Exhibit D, Sheet 5 (page 9) for private carriers and Exhibit D, Sheet 6 (page 10) for the State Insurance Fund. The overall adjustment factor resulting from this procedure is 0.934.

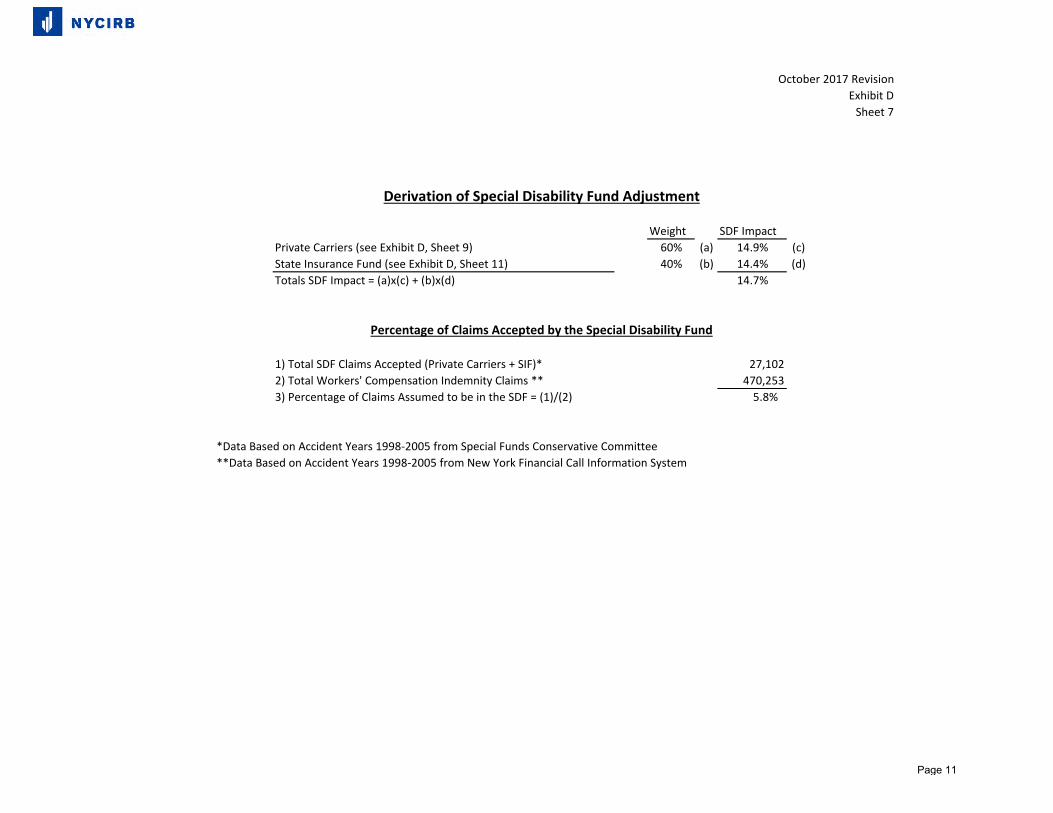

With respect to the closing of the SDF, until three years ago, indemnity losses were adjusted upward by the full estimated impact of the reform (17.8%). This is because most of the loss development factors are from pre‐reform years, and are therefore suppressed, as they reflect the subrogation from the SDF. As part of the 2013 filing, a new approach was taken to determine the impact of the SDF that needs to be applied to the reported losses. Based on information that was obtained from the Special Funds Conservation Committee with respect to the rate at which claims were accepted into the SDF, it was first determined that, on average, 5.8% of indemnity claims were affected by the SDF elimination. This percentage is multiplied by the percentage of cases accepted by the SDF at each development age, to determine the percentage out of all claims that were accepted by the SDF at each development age. The next step in the calculation is to restate each pre‐reform link ratio in the loss development triangle using the following formula:

LRS = LRO x SDF% x AF + LRO x (1‐ SDF%) Where LRS = the Restated link ratio, LRO = Original Link Ratio SDF% = percentage of cases accepted to the SDF at a given development age AF = Adjustment Factor.

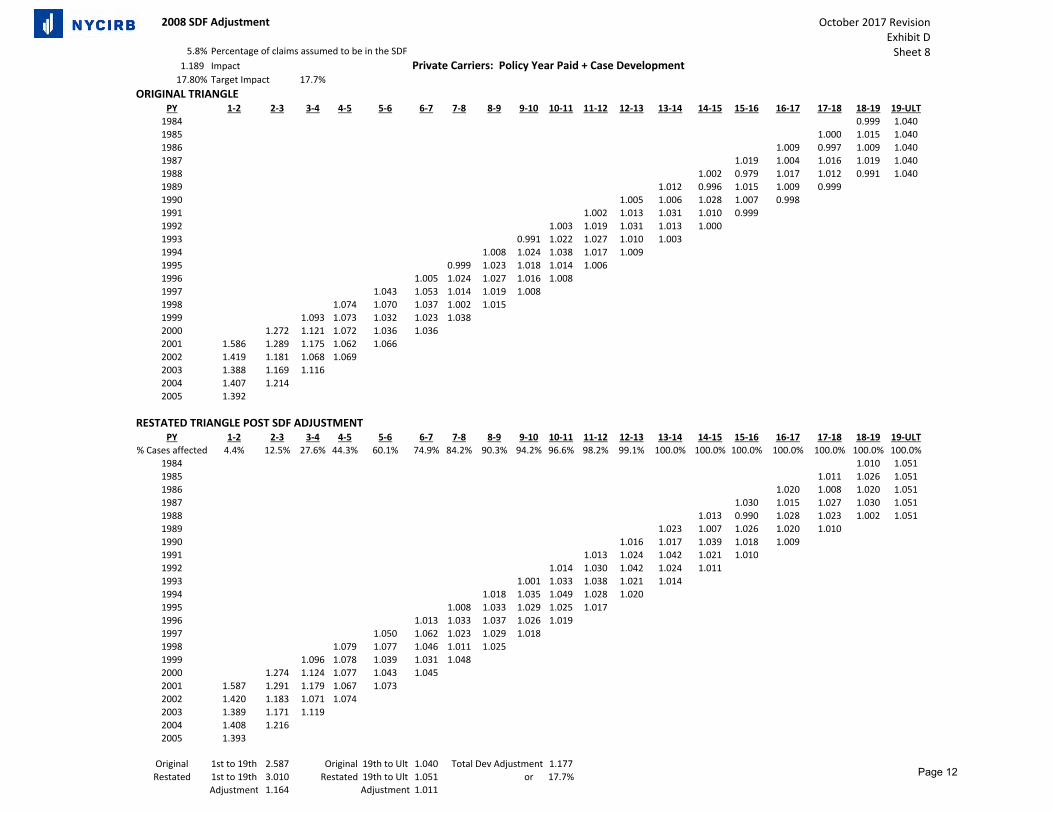

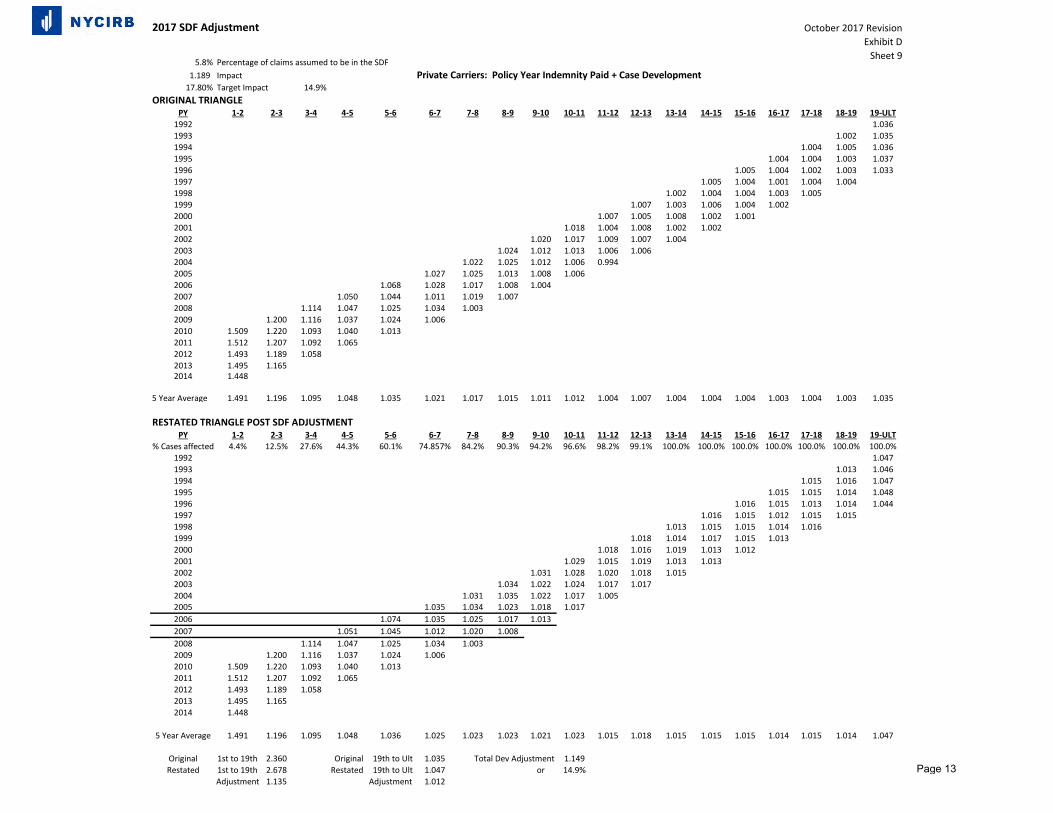

The adjustment factor was determined separately for the private carriers and the State Insurance Fund by restating the latest available loss development triangle which consisted entirely of pre‐reform years (that was used as part of the 2008 Loss Cost Filing) in the same way as described above, such that the restated LDF to ultimate is 17.8% higher than the original LDF to ultimate. (This was the originally estimated impact of the reform on indemnity benefits). The 2008 triangles, which include

- 4 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 5

the derivation of the adjustment factors, are shown on Exhibit D, Sheet 8 (page 12) for private carriers and Exhibit D, Sheet 10 (page 14) for the State Insurance Fund. Then, the impact of the SDF that is used in this filing is determined as the ratio of the ultimate LDF in the restated triangle to the ultimate LDF in the original triangle. These impacts were 14.9% in the Private Carrier analysis and 14.4% in the SIF analysis. A weighted average using 60%/40% weights resulted in the overall impact 14.7%, as is shown in Exhibit D, Sheet 7 (page 11). This impact is used in the loss on‐level factors, which may be found in Exhibit D, Sheet 2 (page 6).

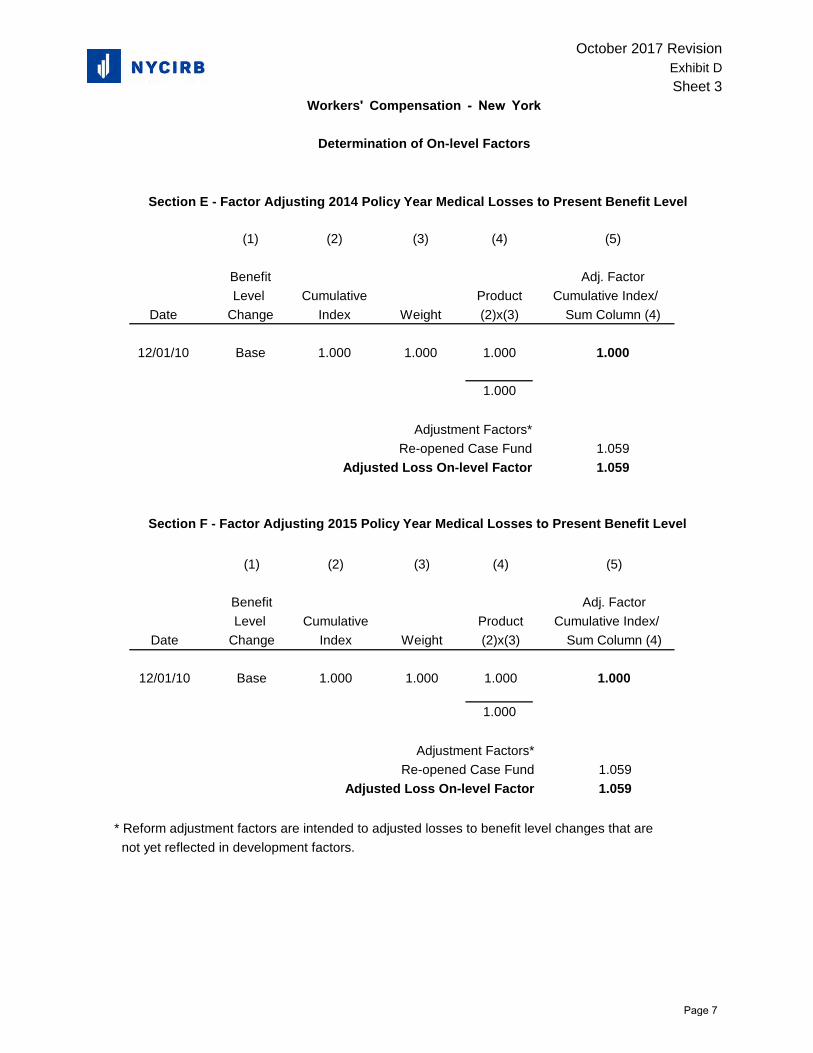

An additional adjustment is needed to account for the January 1, 2014 closing of the Re‐Opened Case Fund (25‐A). The adjustment involved using the same approach that is used to determine the SDF adjustment. It was estimated that the total impact of the Re‐Opened Case Fund elimination was 6.3%. The adjustment accounts for the fact that carriers have been paying and reserving for re‐opened claims over the last 3 calendar years, since the fund has been closed. This has been reflected on Exhibit D, Sheet 14 (page 18). After re‐stating the loss development triangles, it was determined that the appropriate factors that need to be used in this year’s revision are 5.9% for medical, and 5.7% for indemnity. The derivation of these factors can be found on Exhibit D, Sheet 12 (page 16) The loss on‐level calculations are presented on Exhibit D, Sheets 2 and 3 (pages 6‐7). The standard loss on‐level calculation is shown, followed by the reform adjustments described above, resulting in an overall factor to bring the losses to the current benefit level. The final indemnity loss on‐level factors are 1.145 for PY 2014 and 1.137 for PY 2015. For medical, the factors are 1.059 for both PY 2014 and PY 2015. Loss cost indications are calculated separately for the non‐large deductible and large deductible experience and are then weighted based on their respective net earned premiums to arrive at a decrease of 8.1% in loss cost level based upon Policy Year 2015 experience (Exhibit B) and 6.9% based on Policy Year 2014 experience (Exhibit C).

2. Average Experience Change

With equal weights given to the 8.1% decrease indicated by the Policy Year 2015 experience and the 6.9% decrease indicated by the Policy Year 2014 experience, the average effect of experience is a decrease of 7.5%.

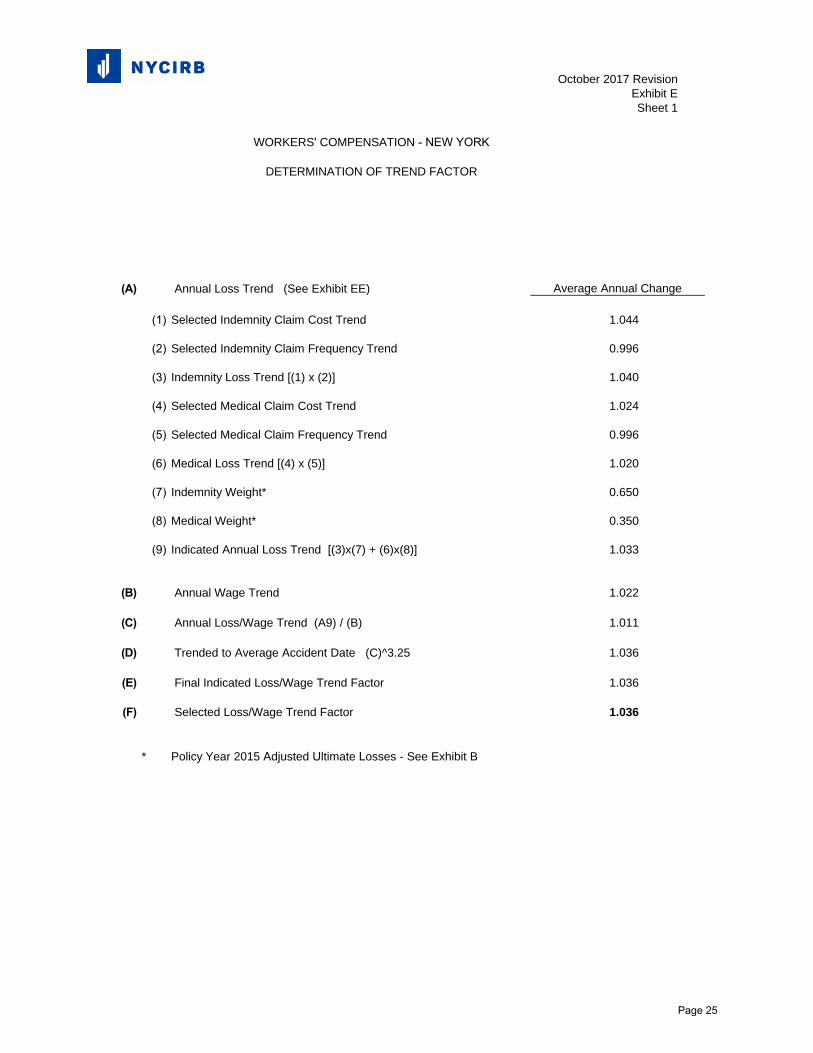

3. Trend Factor Analysis

The presentation of the loss portion of the trend factor is similar to previous years in that indicated trends are expressed in terms of average annual changes in claim costs and claim frequencies. This year’s methodology, which is the same as filed last year, bases the indicated frequency and severities directly on the combined financial data of all private carriers (excluding large deductible experience) and the State Insurance Fund. All data has been adjusted to current levels, i.e., the premiums underlying the frequency calculation are adjusted to the current loss cost level and losses are adjusted to an estimated ultimate settlement

- 5 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 6

basis, as well as to the current benefit level in the same manner as previously described. Premium amounts are also adjusted to a consistent “experience rating off‐balance.” This refers to the overall impact of the experience rating, which may differ from year to year. This adjustment, which was introduced with last year’s filing, ensures that the overall trend results measures pure changes in claim frequency, which may be misrepresented if this adjustment is not made. Claim counts have also been adjusted to ultimate values.

It should be noted that the claim counts reported in the financial data include only lost‐time claims, i.e., medical‐only claim counts are not part of the analysis under this methodology. This produces amore material trend since, while medical‐only cases represent over 60% of the total claims, theyrepresent less than 4% of the losses. The inclusion of medical‐only claims in a frequency and severityanalysis can have a misleading effect on the final trend. The exclusion of medical‐only claims resultsin a greater focus on medical costs on lost‐time claims, which are a major cost driver in the workers’compensation system.

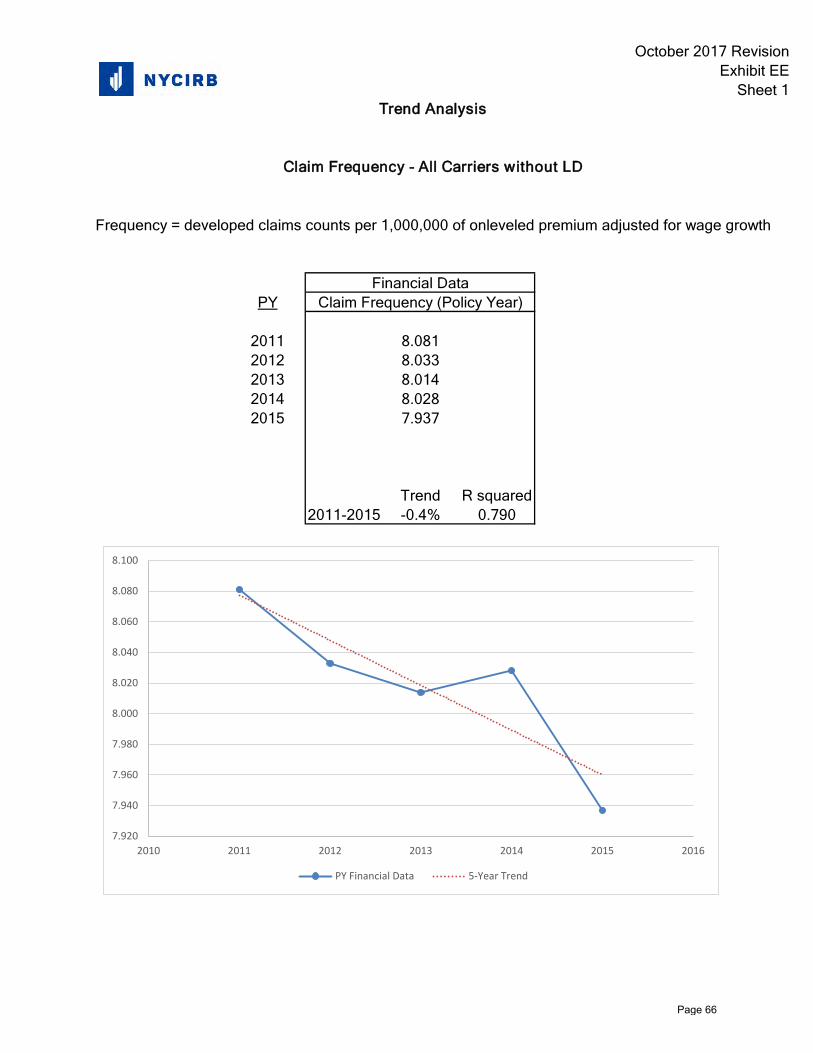

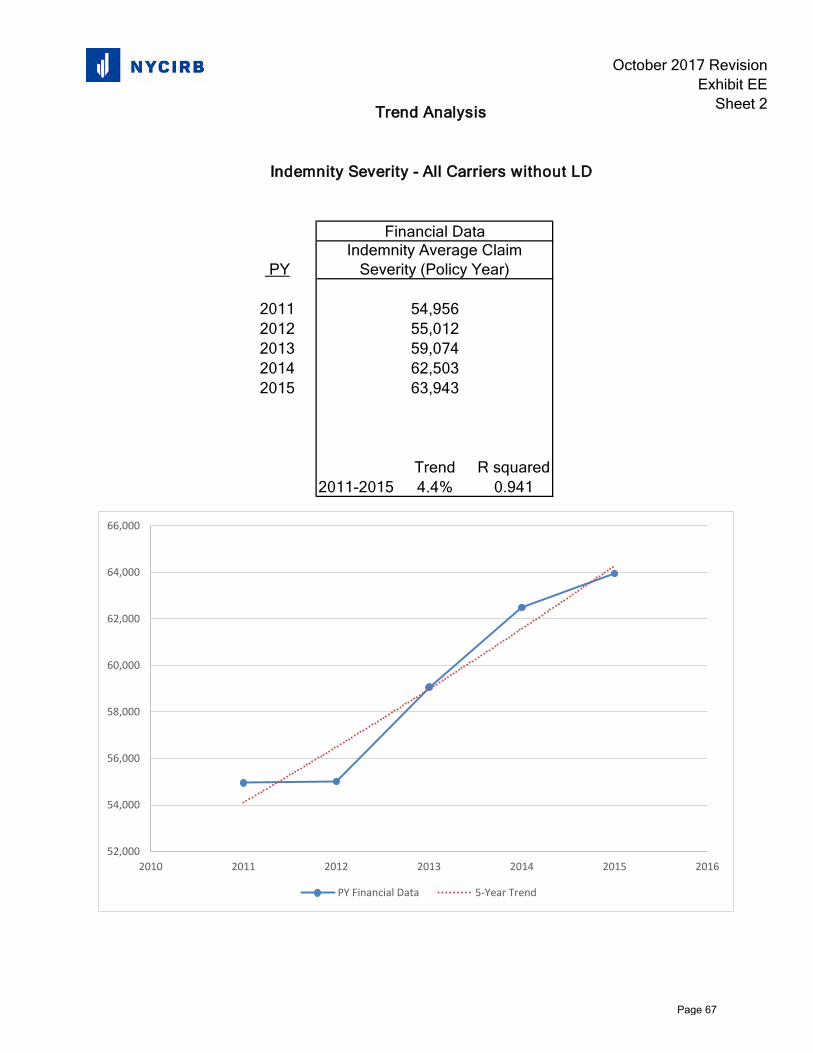

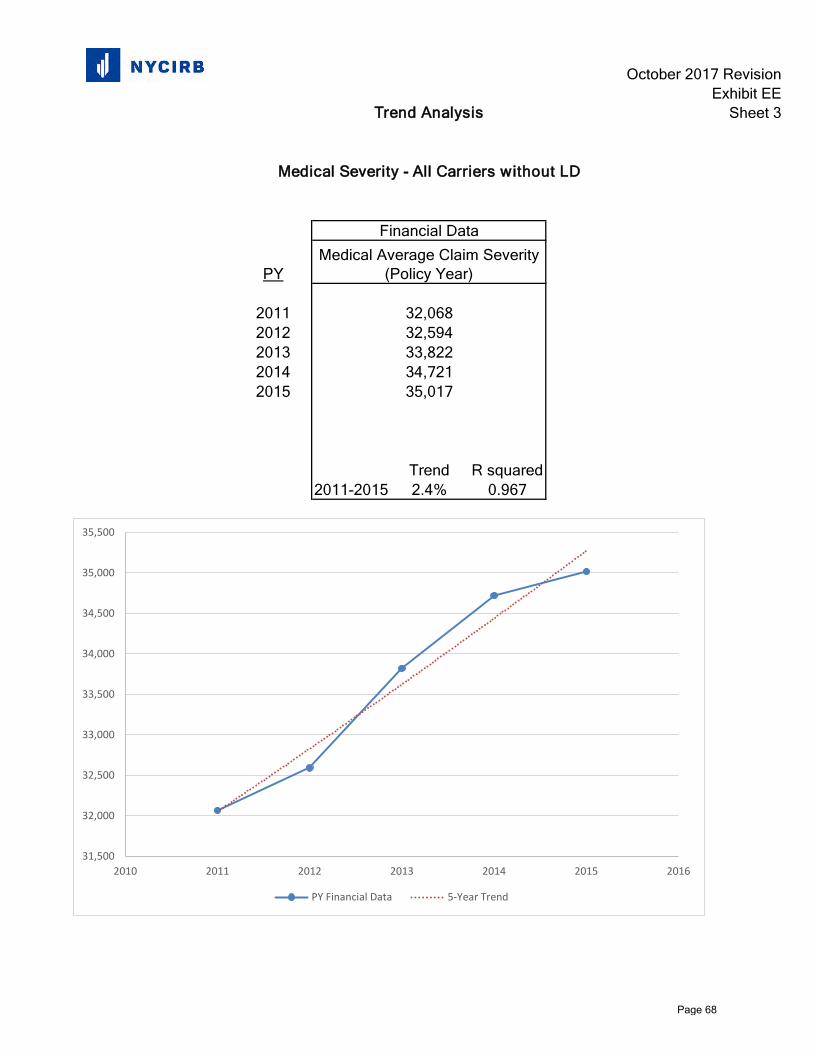

Exhibit EE, Sheets 1‐3 (pages 62‐64) show the derivation of the indicated claim frequency trend and the claim cost trend for both indemnity and medical losses. Since 2011, claim frequency in New York experienced a slight decrease each year except 2014, resulting in a small negative five‐year frequency trend. Claim costs continue to increase though at a lower rate than was observed last year. In this revision, consistent with the approach used in the past several filings, a five‐year exponential trend analysis was performed to derive the indicated trends. For claim frequency, the analysis resulted in an annual trend of ‐0.4%. For indemnity severity, the regression resulted in an annual trend of 4.4%. For medical severity, the five‐year exponential regression produced the indicated annual trend of 2.4%.

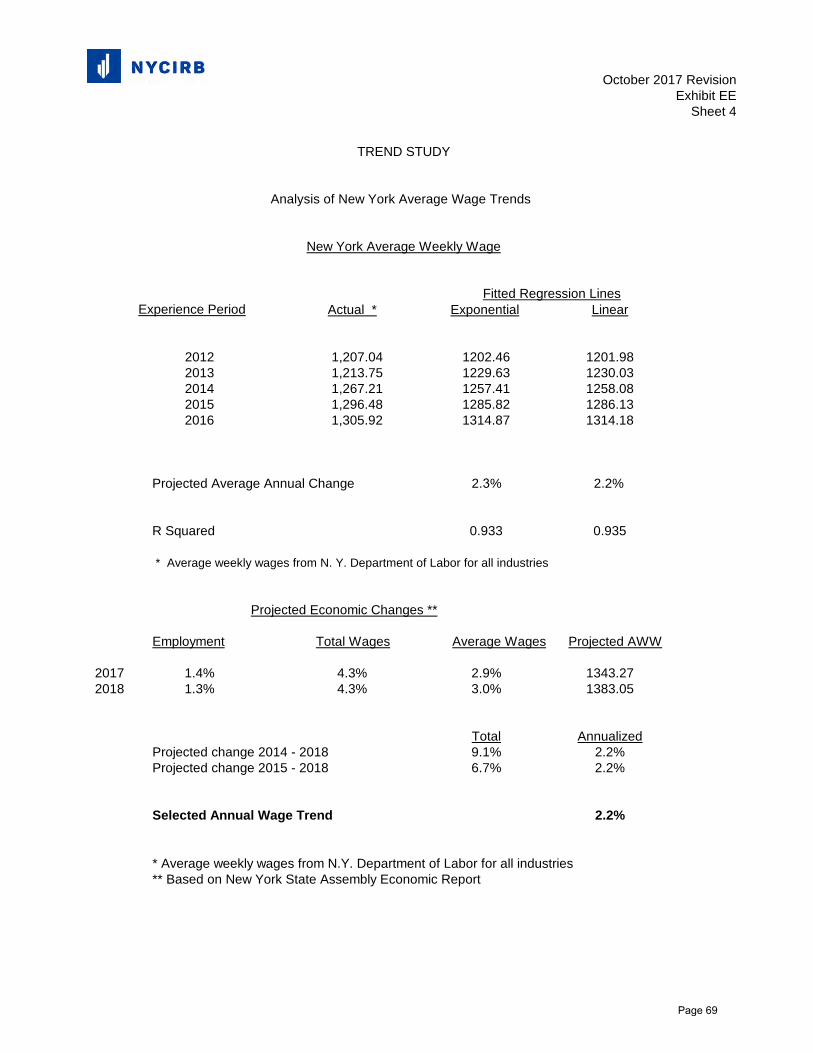

A wage trend analysis procedure, using both an exponential and linear regression of the latest five years of wage data from the New York State Department of Labor (DOL), was examined as part of the wage trend analysis as per the methodology used in previous years. The average weekly wages are derived directly from DOL statistics for all industries. The top section of Exhibit EE, Sheet 4 (page 65), shows the calculation of the wage trend factor produced by this methodology. However, the indicated annual wage trend of 2.3%, which is based on historical wage changes, may differ from the actual wage change during the trend period, i.e., from the experience period through the prospective policy period. Per the New York State Assembly’s 2017 Economic Report, average wage growth is expected to be 2.9% in 2017 and 3.0% in 2018. Using these projections, the average annual expected wage growth from the experience period to the prospective filing period is 2.2%.

As can be seen on Exhibit E, Sheet 1 (page 25), combining the frequency, severity and wage trends results in a combined annual trend of 1.011 or +1.1%. This overall annual trend factor represents an increase from the annual trend factor in last year’s filing. This is driven by the increase in the frequency trend and the decrease in wage trend. After projecting over the full trend period, the total proposed trend factor is 1.036, or +3.6%.

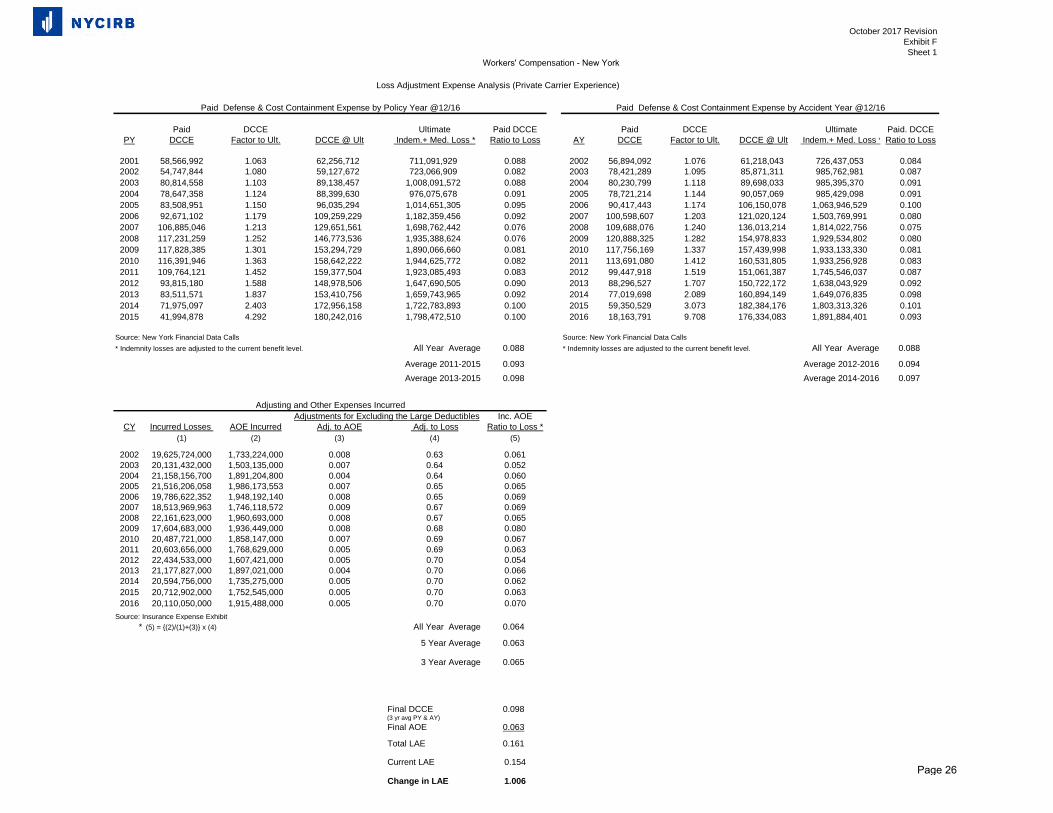

4. Loss Adjustment Expense

The indicated change in loss adjustment expense can be found on Exhibit F (page 26).

- 6 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 7

In this filing, similar to last year, loss adjustment expense has been determined based on paid policy year and accident year Financial Call data for Defense and Cost Containment Expense (DCCE), and on Insurance Expense Exhibit data for Adjusting and Other Expense (AOE). The utilization of Financial Call data for determining DCCE provides a stable base for measuring these expenses and is the most current data available. Ratios of paid DCCE to paid loss is an accurate measure of these costs since any variability over time in reserves for either loss or DCCE does not enter the calculation of this factor. AOE continues to be based on Insurance Expense Exhibit data since it is the only data available with which to calculate this expense. For both DCCE and AOE, the effects of the 2007 reforms on losses have been taken into account implicitly in the development factors. The historical underlying policy year and accident year indemnity losses were brought to the post‐reform benefit level through adjustment to the loss development factors, which are reported at pre‐reform levels. For AOE, ratios of indemnity to total loss were estimated for each calendar period. Similar to last year’s filing, an average of the latest three years of policy year and accident year ratios was used to determine the final DCCE provision. The use of the latest three years is considered to be responsive to the latest trends in DCCE ratios observed in both the policy year and accident year experience. For AOE, the five‐year average continues to be used for this element of loss adjustment expense. The proposed 1.161 factor for LAE represents an increase of 0.6% in this provision of the loss cost.

5. Legislative and Regulatory Changes ‐ 2017 Workers’ Compensation Reform

Part NNN of the Revenue Bill as part of the enacted 2017 New York State Budget Legislation (S.2009C/A3009C) included several workers’ compensation reforms that have cost impact on the overall loss cost level in the system. Specifically, the following reform provisions were examined by the Rating Board and were determined to have a cost impact included as part of this filing:

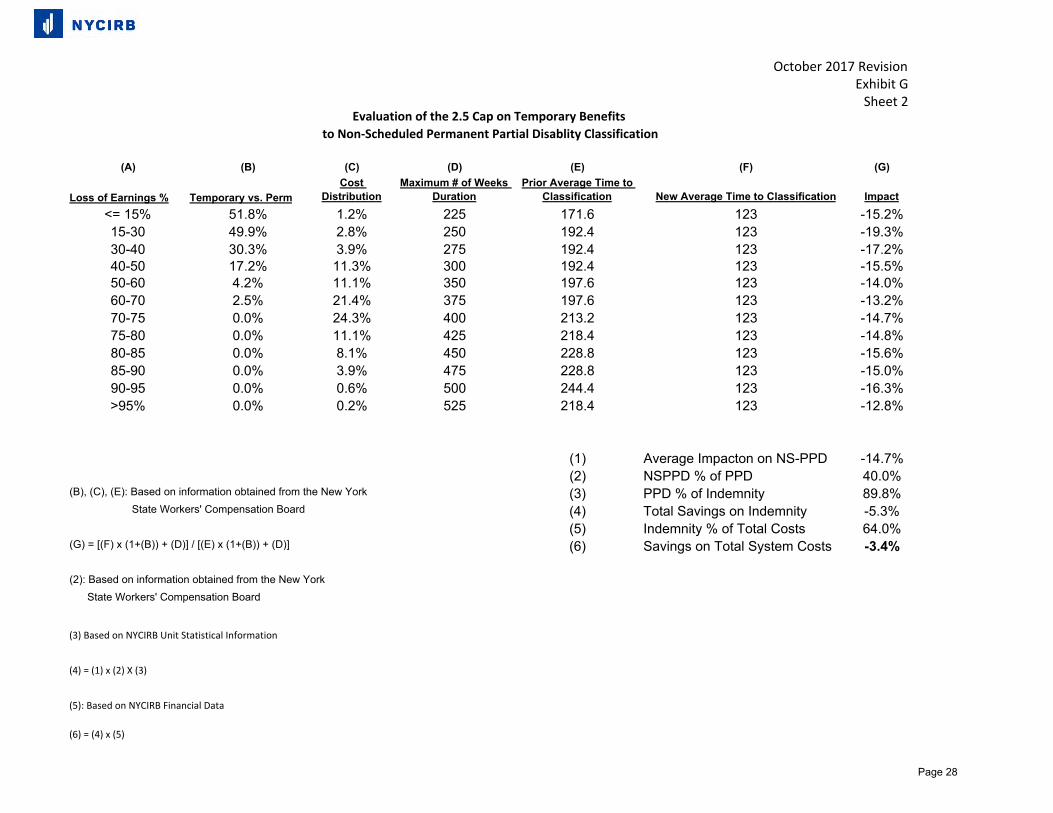

a. The law provides that for accidents occurring on or after the effective date of the law (April 10, 2017), temporary indemnity payments in excess of 130 weeks will be credited against the durational cap on NS‐PPD claims. To estimate the cost impact of the cap of 130 weeks on temporary benefits until NS‐PPD classification, the Rating Board has obtained information from the WCB with respect to the current average time to classification. The information received was by loss of earning capacity (“LOEC”) category in line with the duration caps as per Section 15 (3) (w) of the Workers’ Compensation Law. Information regarding the percentage of claims in each category was also received. Based on that information, the estimated cost savings for each loss of earning capacity category was calculated as the total number of weeks under the new law to the total number of weeks under the old law. Although the cap on temporary benefits to classification is 130 weeks, it was determined that, because some claims would take less than 130 weeks to reach maximum medical improvement (“MMI”) and be classified, the average time to classification would be 123 weeks. The expected savings for each LOEC category is determined as the ratio of the total number of weeks on the claim including the average number of temporary benefits after to the reform, to the total number of weeks per claim including the average number of temporary weeks prior to the reform. It was also estimated that, based on information

- 7 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 8

obtained from the WCB, for certain LOEC categories the average weekly benefits are different than the weekly benefits during the permanency period. Those differences were taken into account when calculating the cost impact by giving more weight to the temporary benefits when determining the total number of weeks. Based on this calculation, which is presented on Exhibit G, Sheet 2 (page 28), it was determined the expected cost impact on NS‐PPD claims is a savings of 14.7%.

Indemnity costs of NS‐PPD claims represent 40% of total permanent partial (“PP”) indemnity costs, and PP indemnity costs represent 89.8% of total indemnity costs. Therefore, it is estimated that the total impact on indemnity costs is ‐5.3% (= ‐14.7% x 40% x 89.8%). Indemnity costs represent 64% of overall system costs, and therefore, the overall system cost impact of this section of the reform is a 3.4% savings (= ‐5.3% x 64%), not including the impact of the possibility that some claimants will be able to extend the time of temporary benefits beyond 130 weeks (see below).

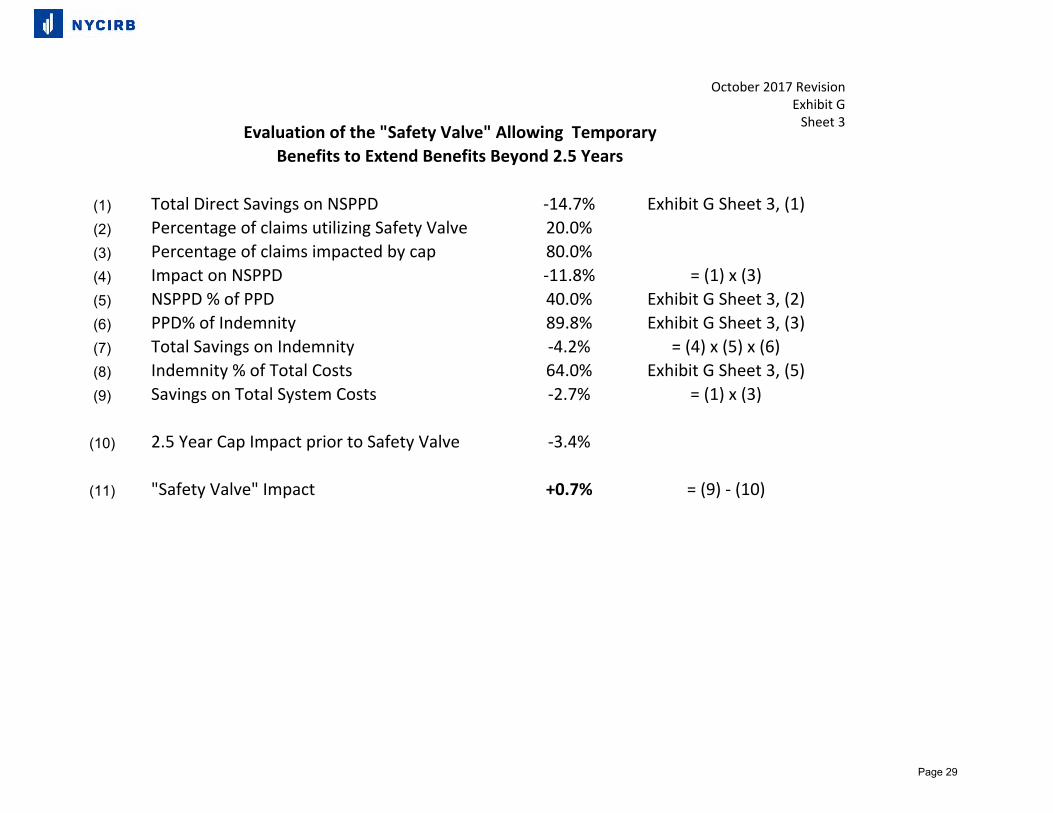

b. The law also provides that, based on medical evidence, the WCB may determine that MMI has

not been reached within 130 weeks, in which case the credit described above will not apply. The impact of this provision, referred to as the “safety valve”, was determined by estimating that 20% of claimants will be able to extend the time of temporary benefits beyond 130 weeks. Therefore, 20% of the estimated impact of the 130‐week cap would not be achieved, and the impact on NS‐PPD after accounting for the “safety valve” would be ‐11.8% (= ‐14.7% x 80%) and the overall system cost impact would be ‐2.7% following the same calculation as presented above. The impact of the “safety valve”, as presented on Exhibit G, Sheet 3 (page 29), is therefore +0.7% (=‐2.7%‐(‐3.4%)).

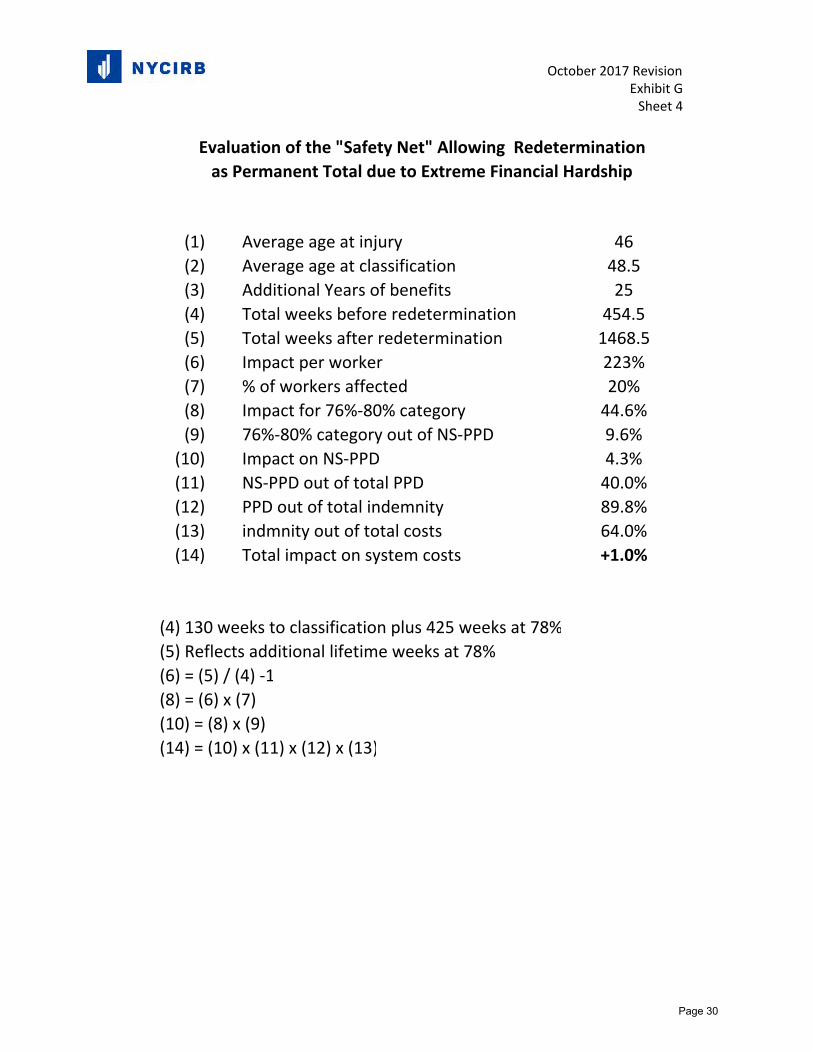

c. The reform reduces the eligibility criteria threshold to apply for an extreme hardship

redetermination from an 81% LOEC to a 76% LOEC. The impact of the extending the “safety net” to claimants with LOEC of 76% to 80% was determined by assuming the additional benefits obtained by such claimants would be, on average, 25 years. This assumption was derived by considering the average age of injury and examining life expectancy tables, since redetermination due to extreme financial hardship would entitle the claimant to lifetime benefits. For an individual claimant, the impact of redetermination would be an increase in benefits of 223%. It is expected, however, that of the total population of claimants in the 76% to 80% LOEC category, a certain percentage will settle, which would preclude them from applying for redetermination, and a certain percentage would pass away prior to becoming eligible to apply for redetermination. Of the remaining population, given the criteria established by the WCB for granting applications of extreme financial hardship, it is assumed that about a third would be found eligible and would get the benefit. After considering this information, and taking into account that those receiving such benefits would be relatively low wage earners, an assumption was made that 20% of the total population in this category would be receiving this benefit. Therefore, the impact of this change on the costs of claims in the 76% to 80% LOEC category is 44.6% (= 223% x 20%). Since claims in this category represent 9.6% of all NS‐PPD claims, this will have a 4.3% increase in costs of NS‐PPD claims (= 44.6% x 9.6%). Finally, the overall impact of this provision is derived in the same manner as described above, resulting in an overall system cost increase of +1.0%. These calculations are shown in Exhibit G, Sheet 4 (page30).

- 8 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 9

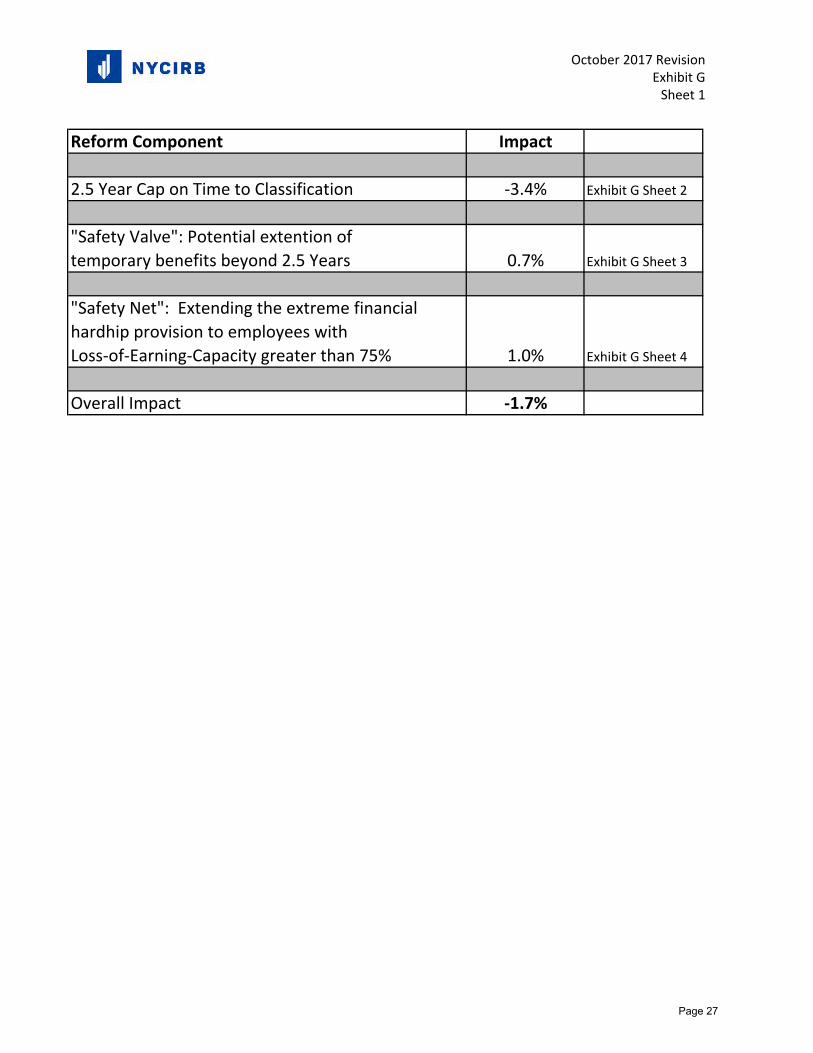

d. The combined impact of the above described components, i.e. the 2.5 year cap on temporary

benefits as part of an NS‐PPD claim, the safety valve, allowing claimants to extend temporary benefits beyond 2.5 years in certain circumstances, and the extension of the extreme hardship safety net provision to claimants with LOEC between 76% and 80%, is ‐1.7%. The derivation of the combined impact is shown in Exhibit G, Sheet 1 (page 27).

Other noteworthy components of the reform, are as follows: e. Subpart A of the reform eliminates the requirement that claimants demonstrate ongoing

attachment to the labor market to collect indemnity on NS‐PPD claims. Based on information obtained from the WCB, it was determined that this statutory change will have a negligible (i.e. less than 0.1%) impact on overall system costs. Any additional costs incurred due to this provision will be reflected in future loss experience.

f. Subpart I of the reform provides that certain emergency first responders (paid police officers and

firefighters, EMTs, paramedics, certified emergency medical providers, and emergency dispatchers) who encounter extraordinary stress in a work‐related emergency and file a mental injury claim, will no longer need to overcome the defense that the stress was not greater than that which usually occurs in the normal work environment. This provision is expected to have a negligible impact on overall system costs. However, certain classifications, which include employees described in this provision, may experience a cost increase. Such increases will be reflected in future loss experience for those classifications.

g. Subpart B directs the WCB to consult with representatives of labor, business, medical providers, insurance carriers, and self‐insured employers and issue revised permanency guidelines concerning medical evaluation of impairment and the determination of permanency. The revised guidelines must reflect modern medicine, be issued for public comment by September 1, 2017 and be adopted by January 1, 2018. Since the guidelines have not yet been published, the Rating Board has not determined the cost impact of this provision, and such cost impact is not reflected in the requested loss cost filing.

h. Subpart C directs the WCB to establish a prescription drug formulary by December 31, 2017. Since the formulary has not yet been published, the Rating Board has not determined the cost impact of this provision, and such cost impact is not reflected in the requested loss cost filing.

i. Section 4 of Subpart F directs the Rating Board to make a filing with the DFS requiring that the final premiums charged (i) on workers’ compensation policies with an effective date between April 10, 2017 and September 30, 2017, and (ii) on the unexpired portion of workers’ compensation policies in force after April 10, 2017 with an effective date on or after October 1, 2016, reflects the cost impact of the 2017 reform, and that differences between premiums charged and the final premium on such policies are to be settled by on or before December 31, 2018. Pursuant to this law, the Rating Board respectfully requests that the cost savings of 1.7%, as calculated above, be credited accordingly.

- 9 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 10 6. Legislative and Regulatory Changes – Standard Update due to Increase in Maximum Weekly Benefits

In accordance with the 2007 legislation, the maximum weekly benefit for injured workers increased to 2/3 of the statewide average weekly wage effective July 1, 2010, indexed annually on July 1 of each subsequent year to the statewide average weekly wage published by the New York Department of Labor. The determination of the loss cost impact resulting from the statutory benefit changes that raise the minimum or maximum weekly benefit continues to be based on a universally accepted actuarial methodology developed by Barney Fratello in a paper entitled “The Workmen’s Compensation Injury Table and Standard Wage Distribution Table – Their Development and Use in Workers Compensation Insurance Ratemaking”, published by the Casualty Actuarial Society. This publication, or portions thereof, has been used for over fifty years by actuaries in all jurisdictions to price the effects of changes in the maximum weekly benefit that are either proposed or enacted by their respective state legislatures. The incorporation of a state’s current statutory maximum weekly benefit, the new maximum weekly benefit, the state’s average weekly wage and the 2010 ‘Standard Actuarial Wage Distribution Table’ enable an actuary to produce an accurate estimate of the benefit cost when changes to the maximum are proposed or enacted. The actual methodology used by the Rating Board to calculate the effects of changes in the maximum weekly benefit is a Limit Factor Analysis, as set forth in Mr. Fratello’s actuarial paper. For a better understanding of the method, the following should be especially noted:

While the methodology refers to average benefits and wage levels, these are expressed in terms of ratios for use with the Wage Distribution Table and are not intended to be actual values.

The methodology only measures changes in the minimum and maximum benefits, or percentage that these benefits bear to an employee’s wages, and nothing more. It assumes that the current administrative functions within the workers’ compensation system and the level of disability or impairment of the injured workers that determines these benefits are at the current level.

The methodology also reflects potential increases in utilization of the system as a result of the increase in benefits. In other states, when large benefit changes were enacted, it was often seen that more claimants applied for the more generous benefits, which resulted in higher actual effects than the actuarial estimates were able to predict.

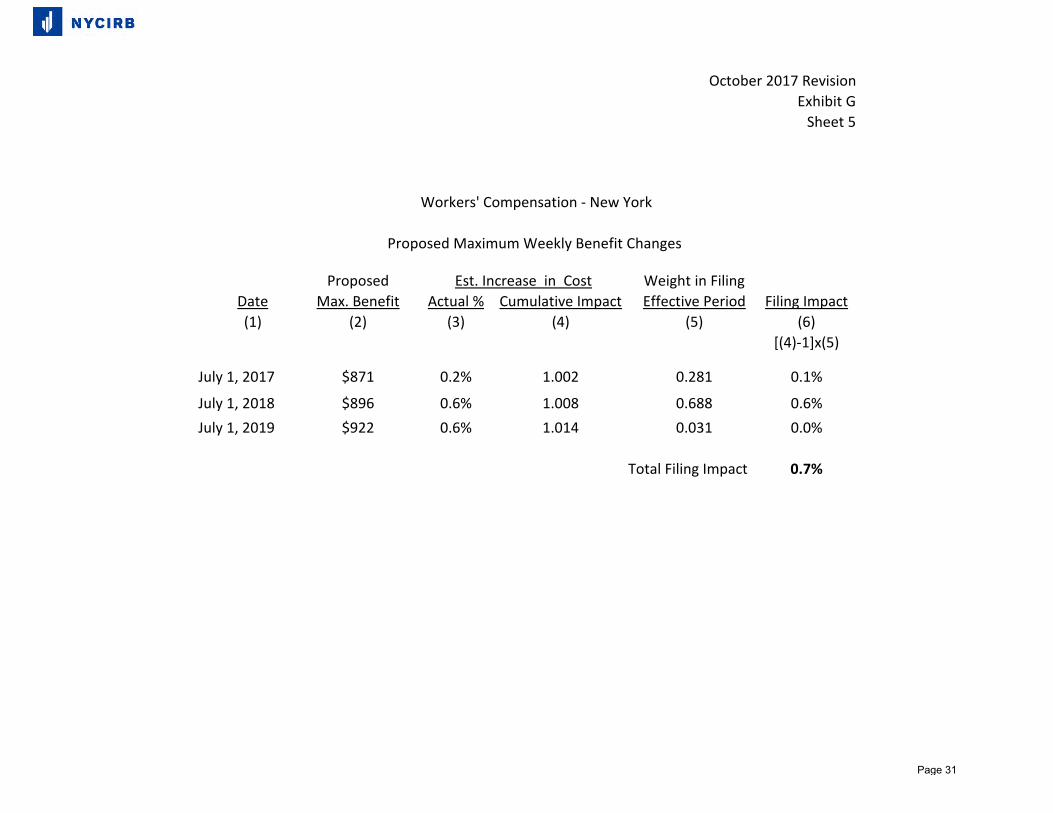

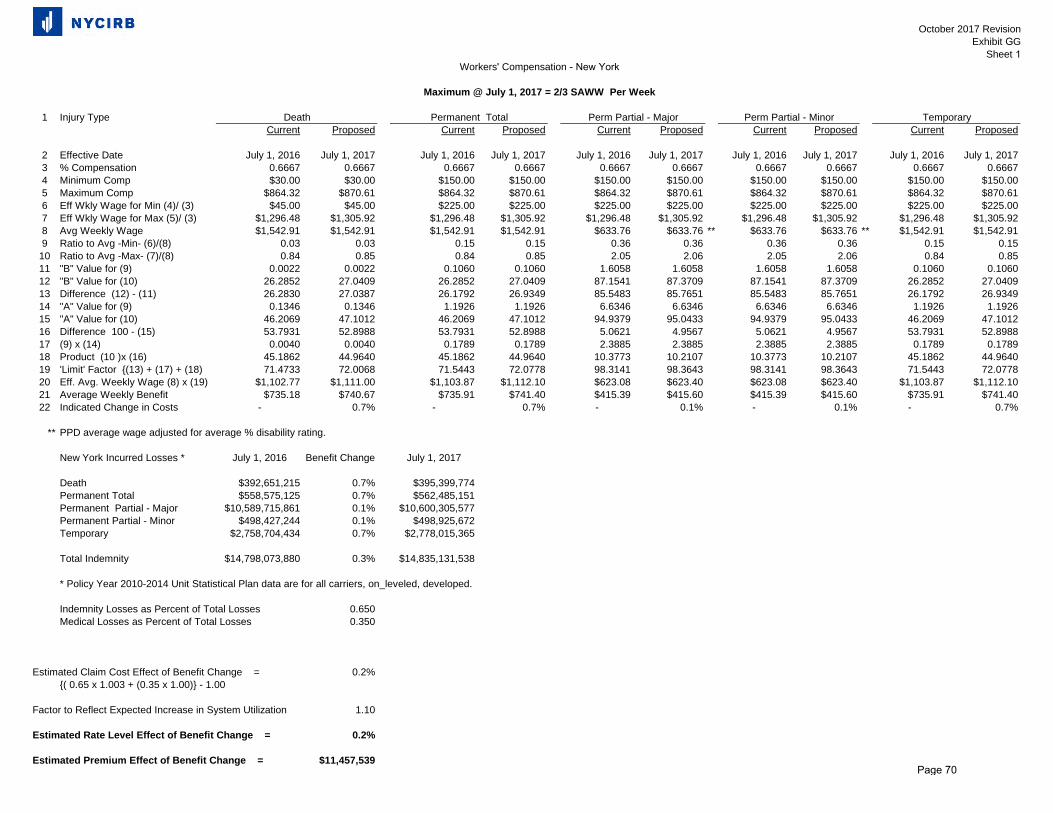

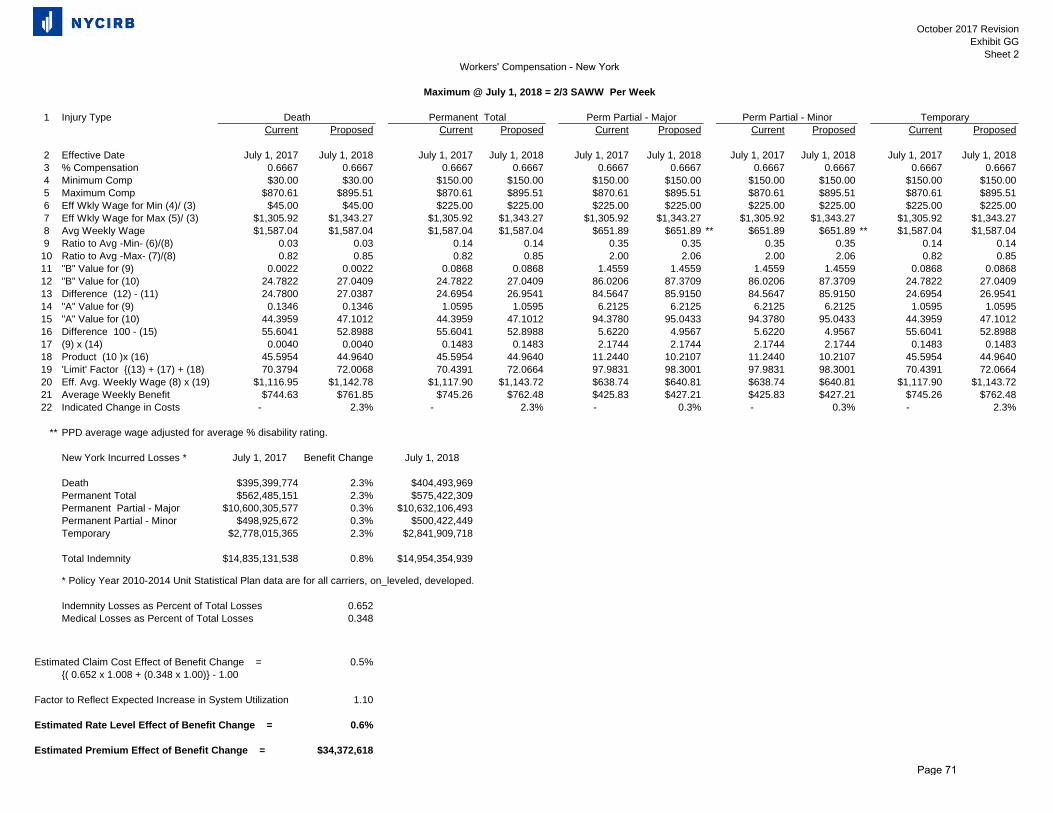

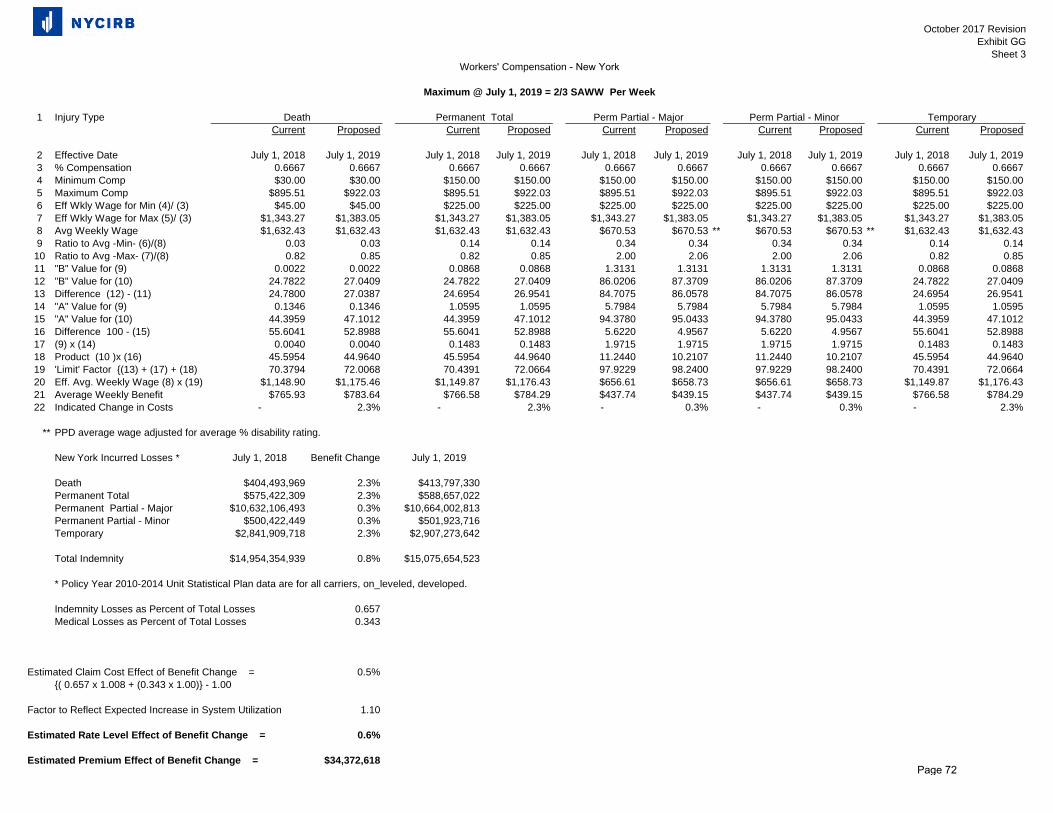

The determination of the overall impact in New York of increasing the maximum weekly benefits as of July 1, 2017, and then on July 1, 2018 and July 1, 2019, can be found on Exhibit GG. Exhibits GG, Sheets 1 through 3 (pages 66‐68) display the calculation of the 2017, 2018 and 2019 benefit changes, respectively. Note that it was assumed that the average weekly wage will increase by 2.9% in 2017 and 3.0% in 2018. The methodology is performed separately for each injury type [death, permanent total, permanent partial and temporary] to recognize any variation in the maximum, as a percent of wage, that is provided for by statute. Recognition has also been given to the lower wage levels of PPD

- 10 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 11

claimants and the manner of determining benefits that is used by the WCB for PPD cases. This is consistent with last year’s calculation. Once the indicated changes are determined by injury type, these changes are applied to a distribution of incurred losses by injury type to obtain the estimated change in total indemnity costs. A five‐year distribution of losses by injury type has been used to provide stability to this part of the analysis. The resultant indicated indemnity change is then weighted with the distribution of indemnity and medical losses based on 2015 policy year financial data to obtain an overall change. The Rating Board analysis then includes a utilization factor of 1.10 that contemplates the additional utilization of the workers’ compensation system as a result of the significantly higher benefit level. This adjustment is consistent with the utilization factor used in last year’s analysis. The increases in the maximum weekly benefit, as summarized in Exhibit G, Sheet 5 (page 31) is expected to result in a 0.7% increase in total workers’ compensation claim costs.

7. Catastrophe Provisions

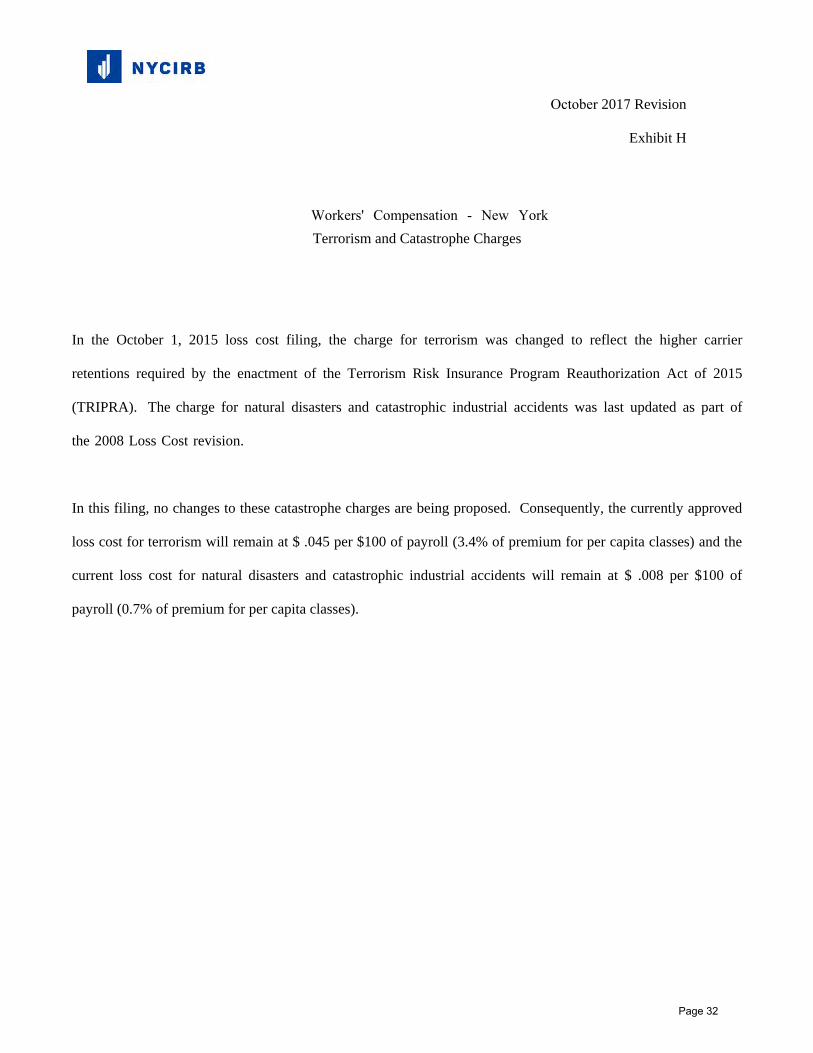

In January 2015, the Terrorism Risk Insurance Program Reauthorization Act of 2015 (TRIPRA) extended the federal backstop for terrorism through December 31, 2020. The Rating Board has retained a catastrophe modeler (AIR Worldwide) to evaluate the proper level of terrorism loss costs in New York. The report issued by AIR indicated terrorism loss costs that vary by year, based on increased carrier retention levels as required by TRIPRA. Based on the information in the report, and following a payroll limitation adjustment, a loss cost of $0.045 (per $100 of payroll) was filed and approved as part of 2015’s loss cost filing. In this year’s filing, despite an increase in the carrier retention levels in 2018, no change is proposed in the terrorism loss cost provision. This is explained on Exhibit H (page 32). Also, note that no change in the loss cost provision for natural disasters and catastrophic industrial accidents is being proposed.

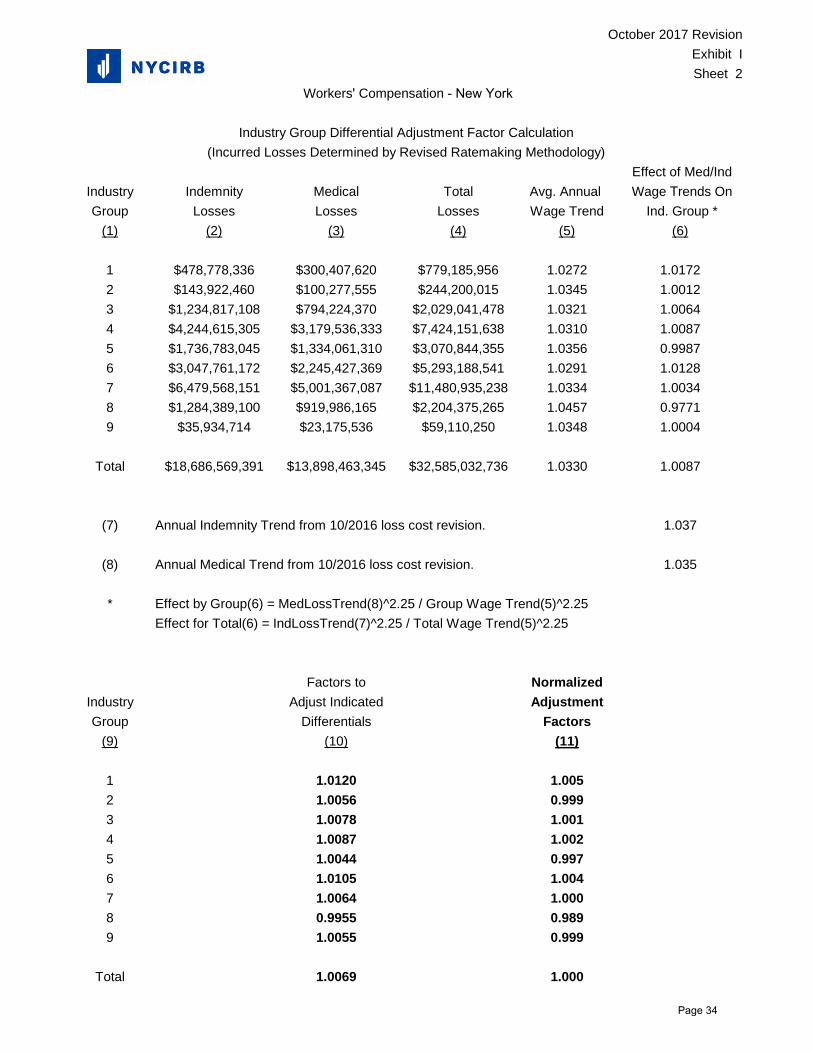

8. Industry Group Differentials

Industry group differentials are used to more equitably distribute the overall loss cost level change to individual employer classifications. Nine industry groups are used in this analysis and are listed below:

Food and Beverage Manufacturing Stores and Dealers‐Wholesale/Retail Chemical Manufacturing Professional and Office All Other Manufacturing Services Contracting Miscellaneous Maritime, Admiralty and Federal

- 11 -

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 12

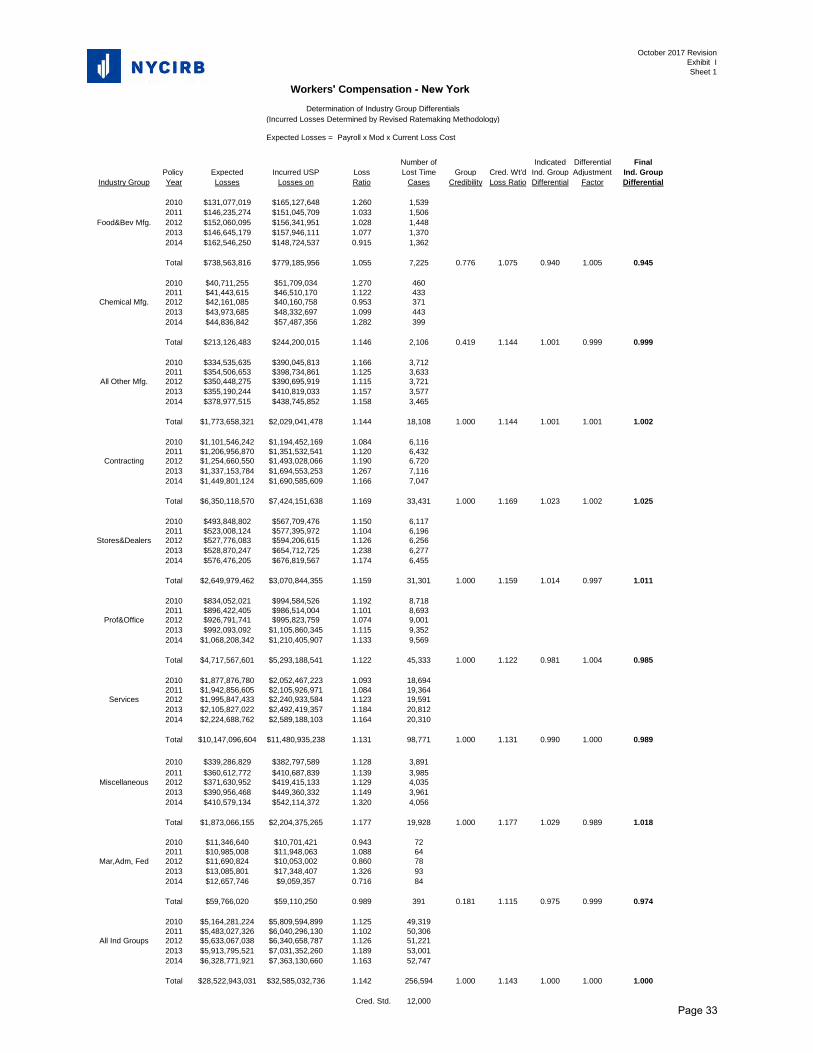

The industry group methodology entails a compilation of the latest five years of Unit Statistical Plan data into the nine industry groups, and utilizes loss cost ratios as the basis for calculating a differential for each group relative to the statewide average (Exhibit I, Sheet 1 on page 33). In years prior to the 2012 filing, three years had been used. The change to five years was introduced in 2012 to further stabilize the industry group differentials from year to year. The underlying base is standard premium at current loss cost level and includes payroll development. This year, the methodology to bring premiums to current level is revised to use an “extension of exposures” procedure, which multiplies the reported payroll for each class on a policy by the current class loss cost, and then multiplying by the experience rating modification factor for the policy. This procedure adds precision to the prior methodology, which required premium level adjustments to reported premiums by industry group, removal of expenses, etc. Incurred losses have been developed to ultimate and are at the October 1, 2017 benefit level to be consistent with the classification pure premiums. The development of losses to ultimate and application of trend and excess factors was done in accordance with the revised methodology approved by DFS in 2015. Credibility for each industry group is based on the five‐year total number of lost‐time claims, with an industry standard of 12,000 lost‐time claims as the standard for full credibility. The credibility standard is intended to enable each industry group differential to be more representative of the actual experience of the respective industry groups.

Partial credibility for each group is determined by the formula (N/T)^1/2, where N is the five‐year total of lost‐time claims for the industry group and T is 12,000 lost‐time claims. The complement of credibility is the loss ratio for all groups combined. Indicated differentials are calculated by relating each credibility‐weighted industry group’s loss ratio to the overall total loss ratio. As in past revisions, an additional refinement to the indicated differential is included which recognizes different wage trends by industry group on Exhibit I, Sheet 2 (page 34). The final differentials will be applied as part of the process which calculates loss costs from class pure premiums. The use of relativities by industry group provides a more refined and equitable distribution of the overall loss cost level to each class. To ensure overall balance, after the differentials are applied in the determination of class loss costs, a test of loss costs will become the final step in the process.

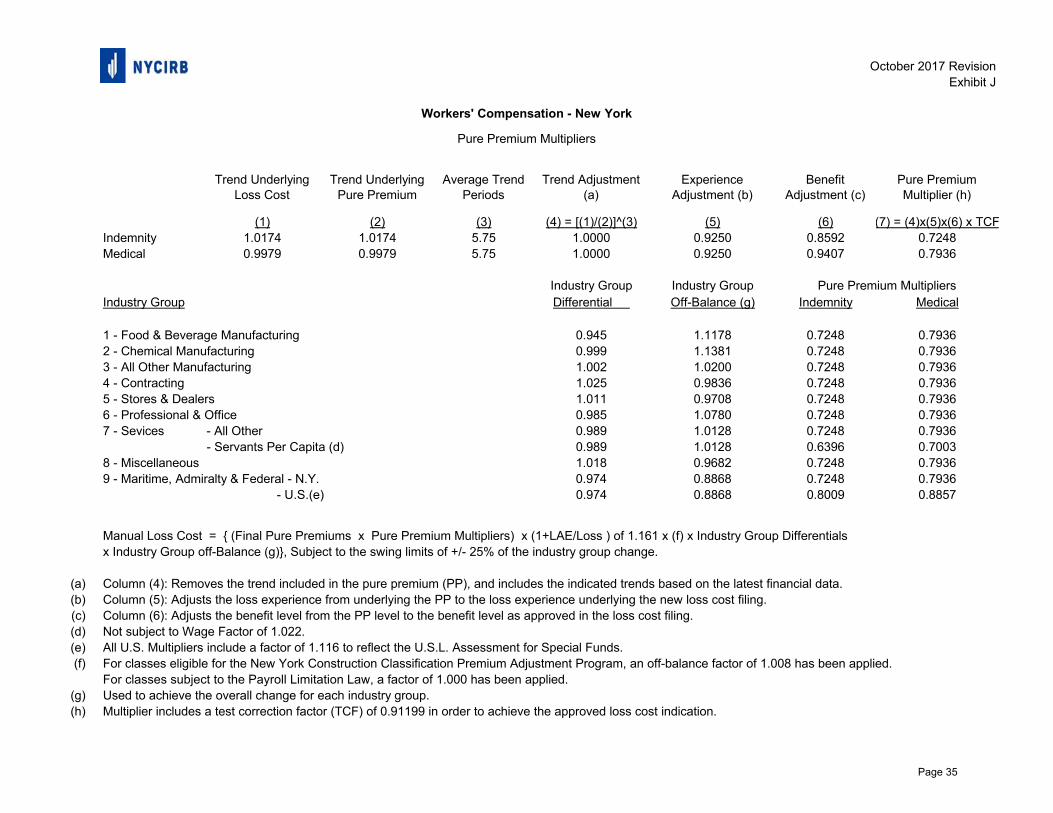

9. Classification Pure Premiums

Classification pure premiums are based on the experience of all carriers for the five policy years 2010 ‐ 2014, excluding the experience of self‐rated risks. In addition, losses over $500,000 per claim are excluded from the pure premium development. Consistent with past revisions, five years of experience are used to determine the proposed pure premiums for all classes, irrespective of credibility. The classification experience was calculated in accordance with the revised methodology approved by DFS in 2015.

Complete details with respect to the classification experience are contained in a separate document that will be provided to DFS separately.

- 12 -

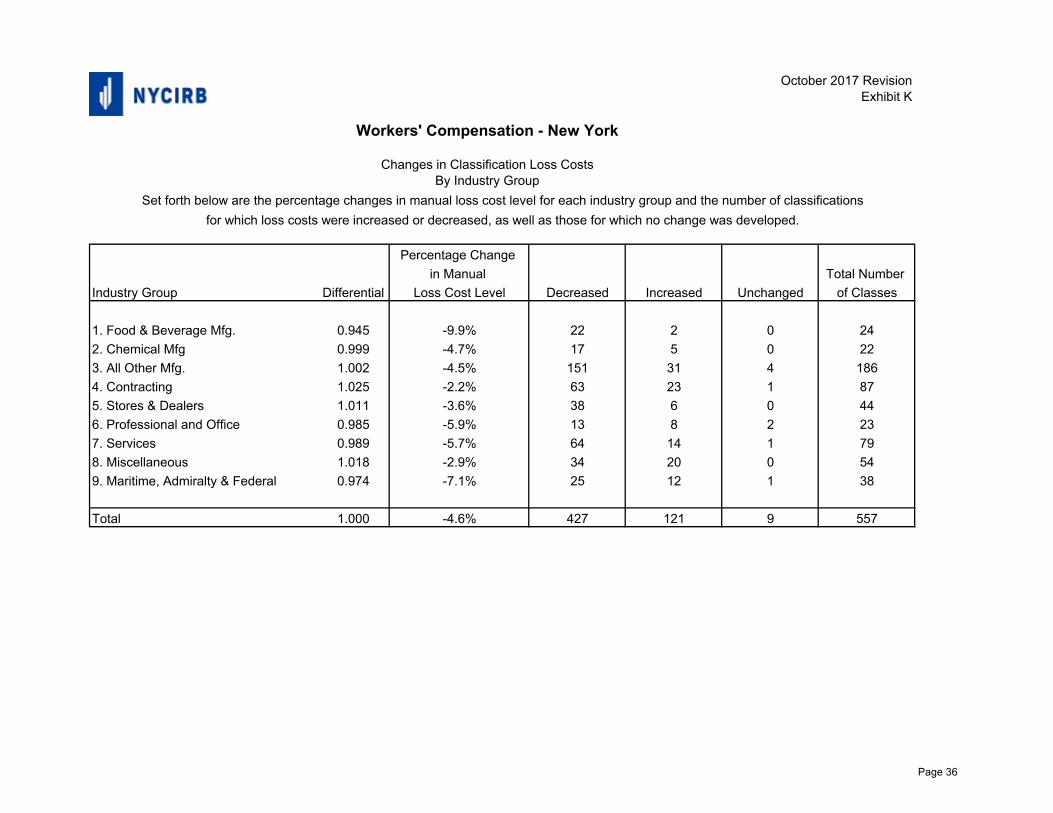

October 1, 2017 Loss Cost Filing Explanatory Memorandum Page 13 10. Changes in Loss Cost by Classification and Industry Group

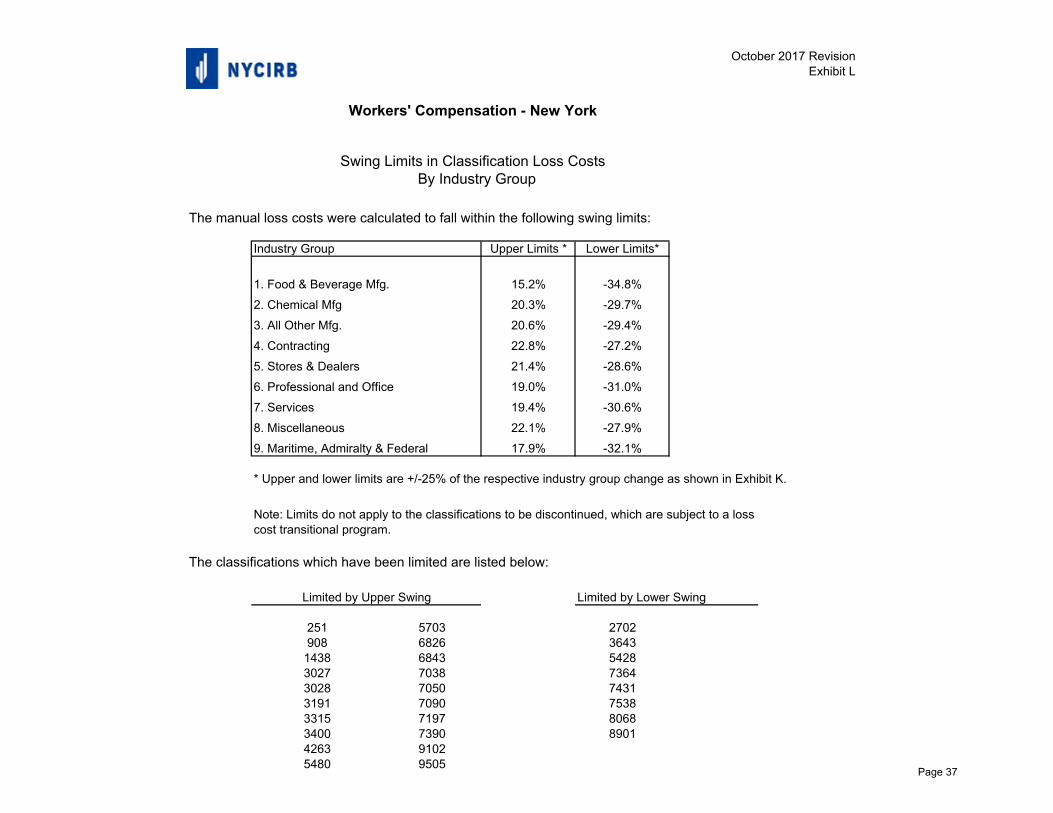

A table showing the percentage change in loss cost level for each classification and industry group and the number of classifications for which loss costs are to be increased or decreased, as well as those to which no change will be applicable, will be provided upon approval. Loss cost changes for each classification will be limited to +/‐ 25% from the calculated industry group change to minimize the swings in loss cost level by class while still maintaining a proper relativity structure.

11. Total Change

The above analyses result in an indicated manual loss cost level change of ‐4.6%. When combined with no change in the loss cost provisions for terrorism, natural disasters, and catastrophic industrial accidents, an overall change of ‐4.5% is proposed.

12. Effective Date

It is proposed that the filed loss costs and related rating values, after approval by DFS, become effective on October 1, 2017 for new and renewal business. As indicated in item 5‐i above, it is proposed that an outstanding change of ‐1.7% will be applied to policies with effective dates between April 10, 2017 and September 30, 2017, and on the unexpired portion as of April 10, 2017, of policies effective between October 1, 2016 and April 9, 2017.

- 13 -

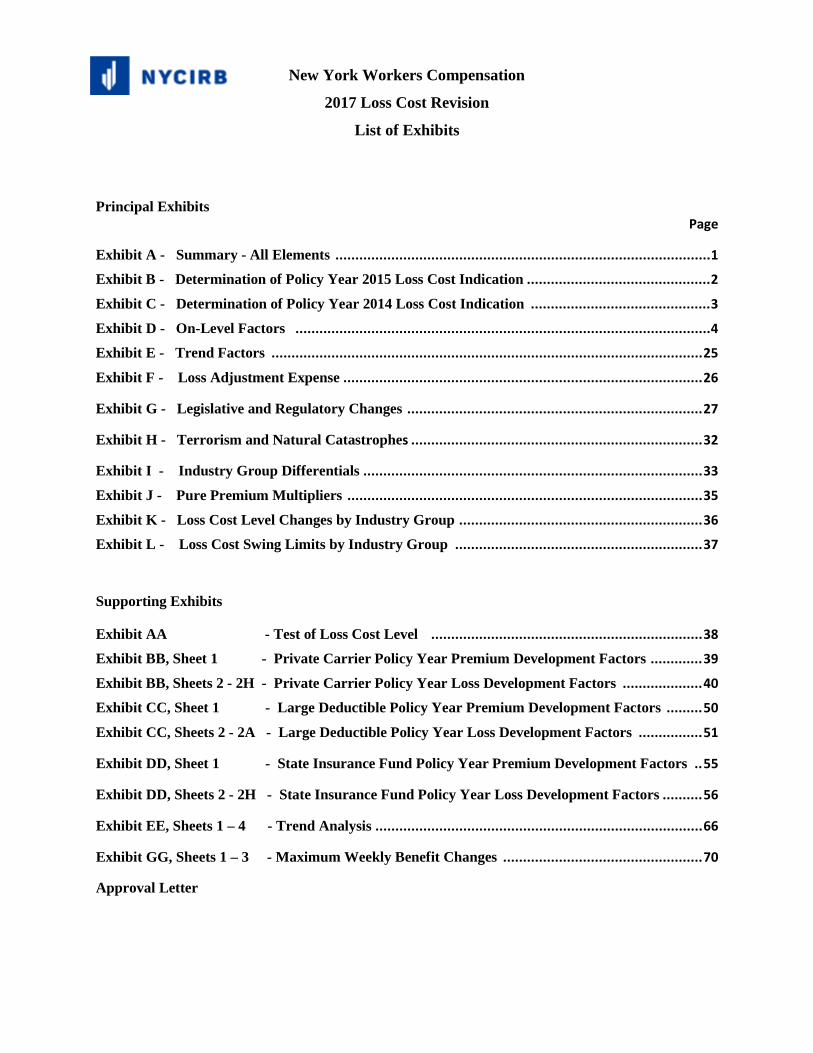

New York Workers Compensation

2017 Loss Cost Revision

List of Exhibits

Principal Exhibits

Page

Exhibit A - Summary - All Elements .............................................................................................. 1

Exhibit B - Determination of Policy Year 2015 Loss Cost Indication .............................................. 2

Exhibit C - Determination of Policy Year 2014 Loss Cost Indication ............................................. 3

Exhibit D - On-Level Factors ........................................................................................................ 4

Exhibit E - Trend Factors ............................................................................................................ 25

Exhibit F - Loss Adjustment Expense .......................................................................................... 26

Exhibit G - Legislative and Regulatory Changes .......................................................................... 27

Exhibit H - Terrorism and Natural Catastrophes ......................................................................... 32

Exhibit I - Industry Group Differentials ..................................................................................... 33

Exhibit J - Pure Premium Multipliers ......................................................................................... 35

Exhibit K - Loss Cost Level Changes by Industry Group ............................................................. 36

Exhibit L - Loss Cost Swing Limits by Industry Group .............................................................. 37

Supporting Exhibits

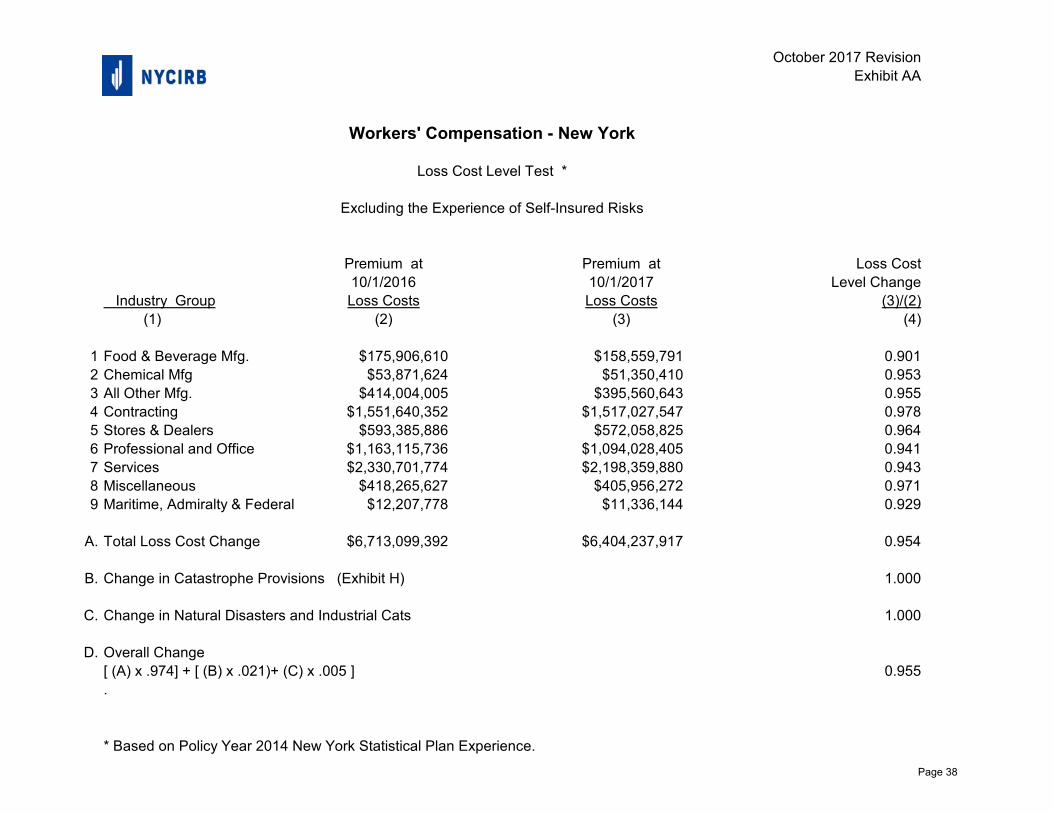

Exhibit AA - Test of Loss Cost Level .................................................................... 38

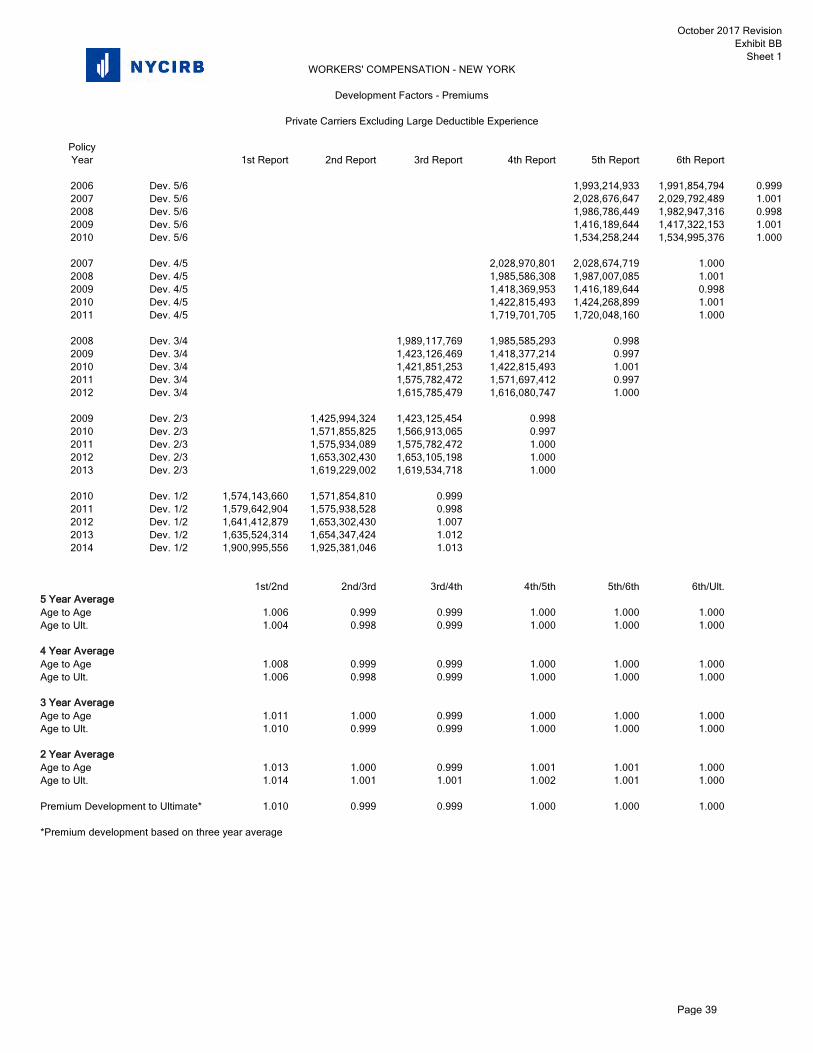

Exhibit BB, Sheet 1 - Private Carrier Policy Year Premium Development Factors ............. 39

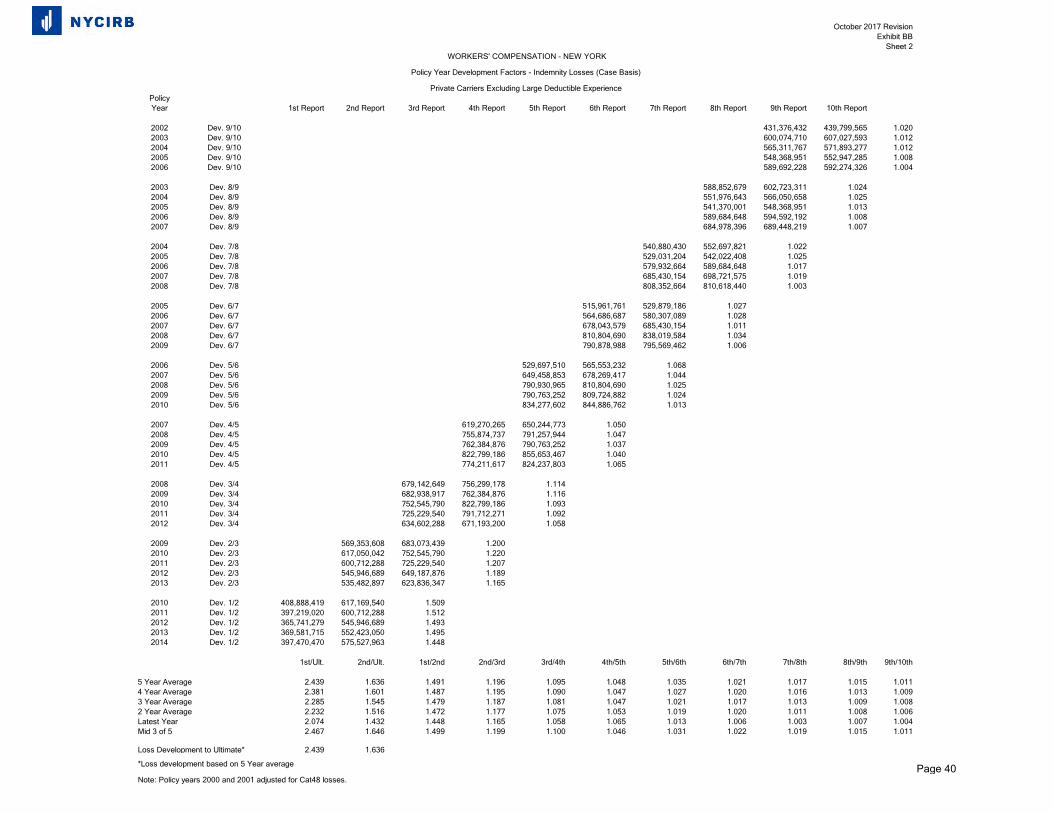

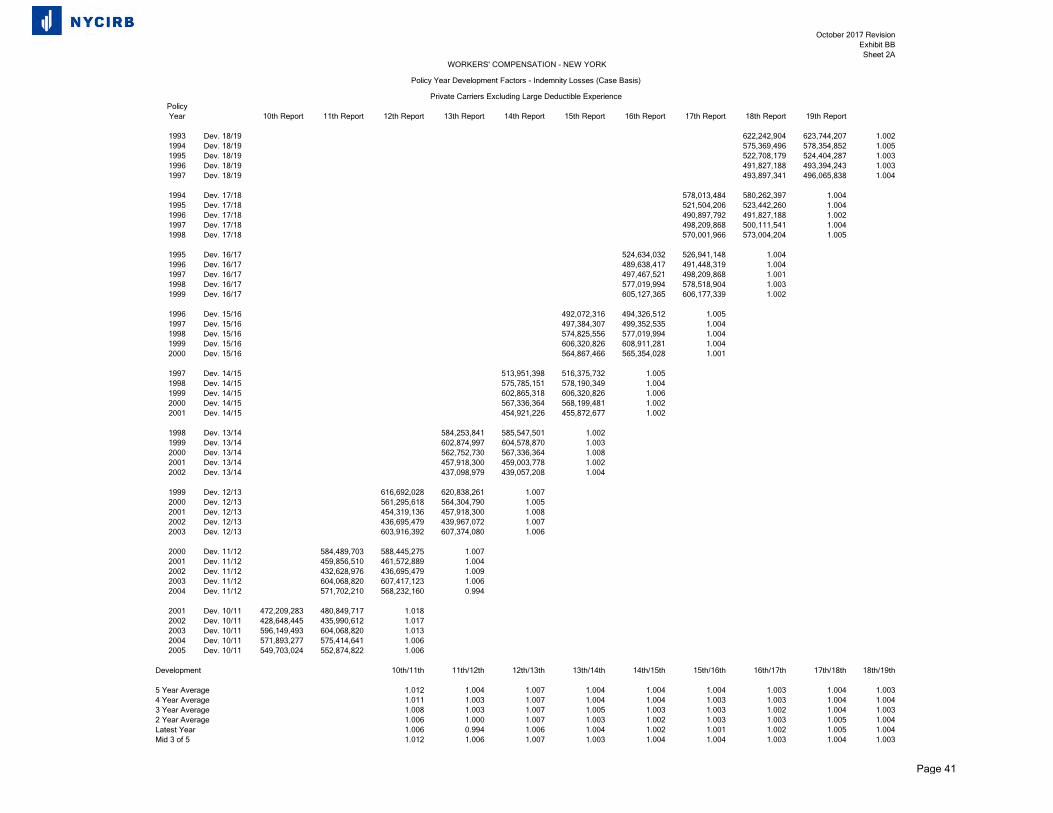

Exhibit BB, Sheets 2 - 2H - Private Carrier Policy Year Loss Development Factors .................... 40

Exhibit CC, Sheet 1 - Large Deductible Policy Year Premium Development Factors ......... 50

Exhibit CC, Sheets 2 - 2A - Large Deductible Policy Year Loss Development Factors ................ 51

Exhibit DD, Sheet 1 - State Insurance Fund Policy Year Premium Development Factors .. 55

Exhibit DD, Sheets 2 - 2H - State Insurance Fund Policy Year Loss Development Factors .......... 56

Exhibit EE, Sheets 1 – 4 - Trend Analysis .................................................................................. 66

Exhibit GG, Sheets 1 – 3 - Maximum Weekly Benefit Changes .................................................. 70

Approval Letter

October 2017 RevisionExhibit A

2 Policy Years

0.919

0.931

0.925

1.036

1.006

0.964

1. Loss Cost Change Indicated by Policy Year 2015 Experience (Exhibit B)

2. Loss Cost Change Indicated by Policy Year 2014 Experience (Exhibit C)

3. Average Loss Cost Change Indicated by Experience [(1)+(2)] / 2

4. Projected Change in Loss Costs (Exhibit E)

5. Change in Loss Adjustment Expenses (Exhibit F)

6. Indicated Change in Loss Costs Based on Experience[(3) x (4) x (5)]

7. 2017 NY WC Reform Impacts (Exhibit G, Sheet 1 - 4) 0.983

8. 1.007

9 0.954

Legislative Changes (Exhibit G, Sheet 5)

Indicated Total Loss Cost Change[(6) x (7) x (8)]

1.000

0.021

1.000

0.005

0.955

10. Change in Terrorism Provision (Exhibit H)

11. Terrorism Provision Loss Cost as Percent of Total Loss Costs

12. Change in Provision for Natural Disasters and Industrial Cats. (Exhibit H)

13. Natural Disasters and Industrial Cats. Provision Loss Cost as Percent of Total Loss Costs

14. Total Proposed Premium Level Change[(9) x (1.0 - (11) - (13)) + (10) x (11) + (12) x (13)]

WORKERS' COMPENSATION - NEW YORK

GENERAL LOSS COST REVISION - OCTOBER 1, 2017

SUMMARY - ALL ELEMENTS

Page 1

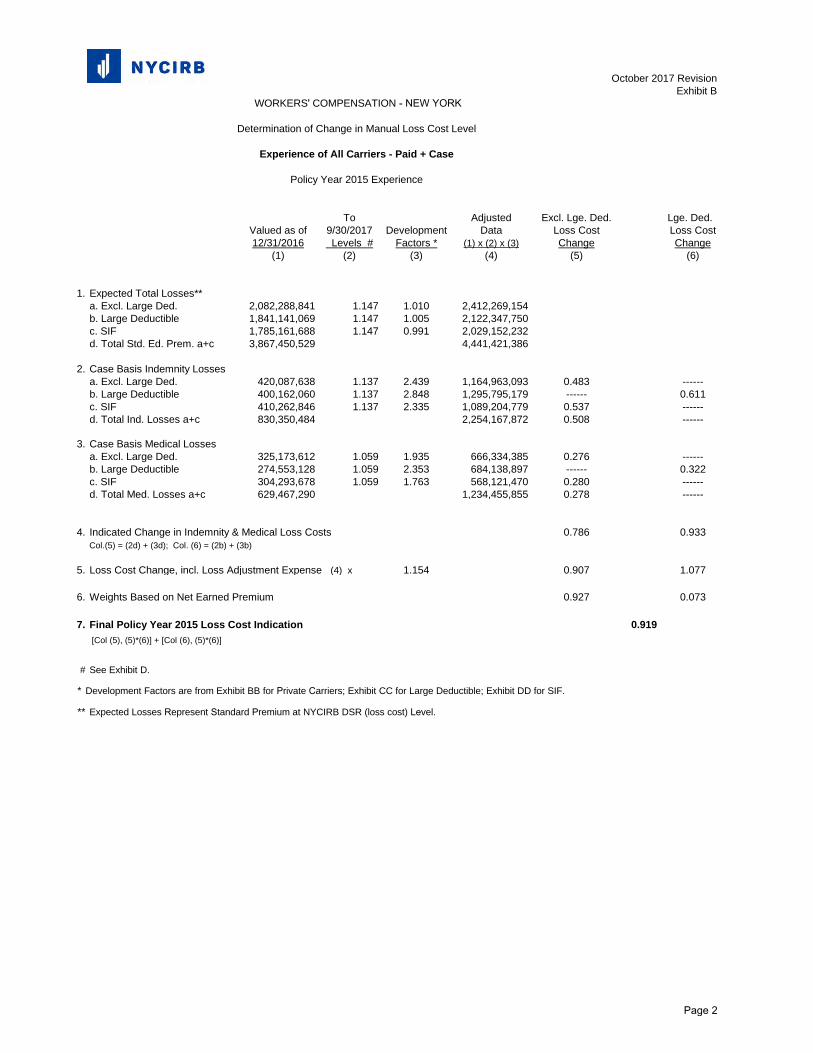

October 2017 RevisionExhibit B

To Adjusted Excl. Lge. Ded. Lge. Ded.Valued as of 9/30/2017 Development Data Loss Cost Loss Cost12/31/2016 Levels # Factors * (1) x (2) x (3) Change Change

(1) (2) (3) (4) (5) (6)

1. Expected Total Losses**a. Excl. Large Ded. 2,082,288,841 1.147 1.010 2,412,269,154b. Large Deductible 1,841,141,069 1.147 1.005 2,122,347,750c. SIF 1,785,161,688 1.147 0.991 2,029,152,232d. Total Std. Ed. Prem. a+c 3,867,450,529 4,441,421,386

2. Case Basis Indemnity Lossesa. Excl. Large Ded. 420,087,638 1.137 2.439 1,164,963,093 0.483 ------b. Large Deductible 400,162,060 1.137 2.848 1,295,795,179 ------ 0.611c. SIF 410,262,846 1.137 2.335 1,089,204,779 0.537 ------d. Total Ind. Losses a+c 830,350,484 2,254,167,872 0.508 ------

3. Case Basis Medical Lossesa. Excl. Large Ded. 325,173,612 1.059 1.935 666,334,385 0.276 ------b. Large Deductible 274,553,128 1.059 2.353 684,138,897 ------ 0.322c. SIF 304,293,678 1.059 1.763 568,121,470 0.280 ------d. Total Med. Losses a+c 629,467,290 1,234,455,855 0.278 ------

4. Indicated Change in Indemnity & Medical Loss Costs 0.786 0.933Col.(5) = (2d) + (3d); Col. (6) = (2b) + (3b)

5. Loss Cost Change, incl. Loss Adjustment Expense (4) x 1.154 0.907 1.077

6. Weights Based on Net Earned Premium 0.927 0.073

7. Final Policy Year 2015 Loss Cost Indication 0.919 [Col (5), (5)*(6)] + [Col (6), (5)*(6)]

# See Exhibit D.

* Development Factors are from Exhibit BB for Private Carriers; Exhibit CC for Large Deductible; Exhibit DD for SIF.

** Expected Losses Represent Standard Premium at NYCIRB DSR (loss cost) Level.

WORKERS' COMPENSATION - NEW YORK

Determination of Change in Manual Loss Cost Level

Experience of All Carriers - Paid + Case

Policy Year 2015 Experience

Page 2

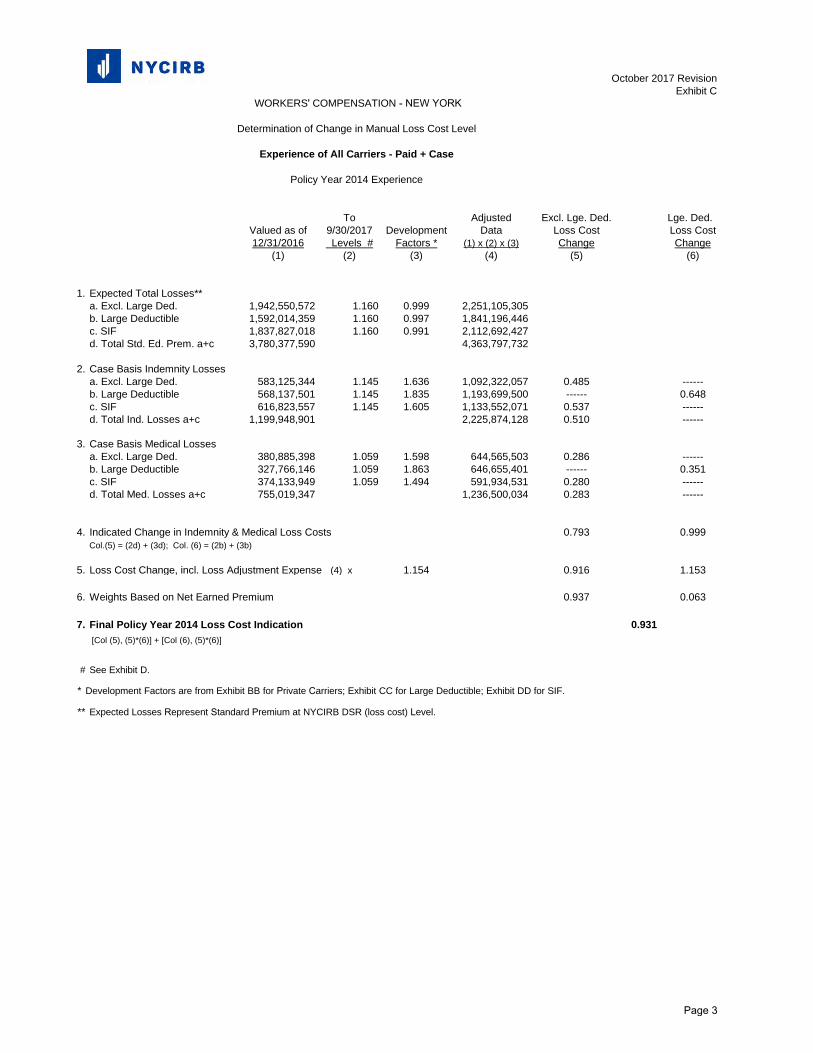

October 2017 RevisionExhibit C

To Adjusted Excl. Lge. Ded. Lge. Ded.Valued as of 9/30/2017 Development Data Loss Cost Loss Cost12/31/2016 Levels # Factors * (1) x (2) x (3) Change Change

(1) (2) (3) (4) (5) (6)

1. Expected Total Losses**a. Excl. Large Ded. 1,942,550,572 1.160 0.999 2,251,105,305b. Large Deductible 1,592,014,359 1.160 0.997 1,841,196,446c. SIF 1,837,827,018 1.160 0.991 2,112,692,427d. Total Std. Ed. Prem. a+c 3,780,377,590 4,363,797,732

2. Case Basis Indemnity Lossesa. Excl. Large Ded. 583,125,344 1.145 1.636 1,092,322,057 0.485 ------b. Large Deductible 568,137,501 1.145 1.835 1,193,699,500 ------ 0.648c. SIF 616,823,557 1.145 1.605 1,133,552,071 0.537 ------d. Total Ind. Losses a+c 1,199,948,901 2,225,874,128 0.510 ------

3. Case Basis Medical Lossesa. Excl. Large Ded. 380,885,398 1.059 1.598 644,565,503 0.286 ------b. Large Deductible 327,766,146 1.059 1.863 646,655,401 ------ 0.351c. SIF 374,133,949 1.059 1.494 591,934,531 0.280 ------d. Total Med. Losses a+c 755,019,347 1,236,500,034 0.283 ------

4. Indicated Change in Indemnity & Medical Loss Costs 0.793 0.999Col.(5) = (2d) + (3d); Col. (6) = (2b) + (3b)

5. Loss Cost Change, incl. Loss Adjustment Expense (4) x 1.154 0.916 1.153

6. Weights Based on Net Earned Premium 0.937 0.063

7. Final Policy Year 2014 Loss Cost Indication 0.931 [Col (5), (5)*(6)] + [Col (6), (5)*(6)]

# See Exhibit D.

* Development Factors are from Exhibit BB for Private Carriers; Exhibit CC for Large Deductible; Exhibit DD for SIF.

** Expected Losses Represent Standard Premium at NYCIRB DSR (loss cost) Level.

WORKERS' COMPENSATION - NEW YORK

Determination of Change in Manual Loss Cost Level

Experience of All Carriers - Paid + Case

Policy Year 2014 Experience

Page 3

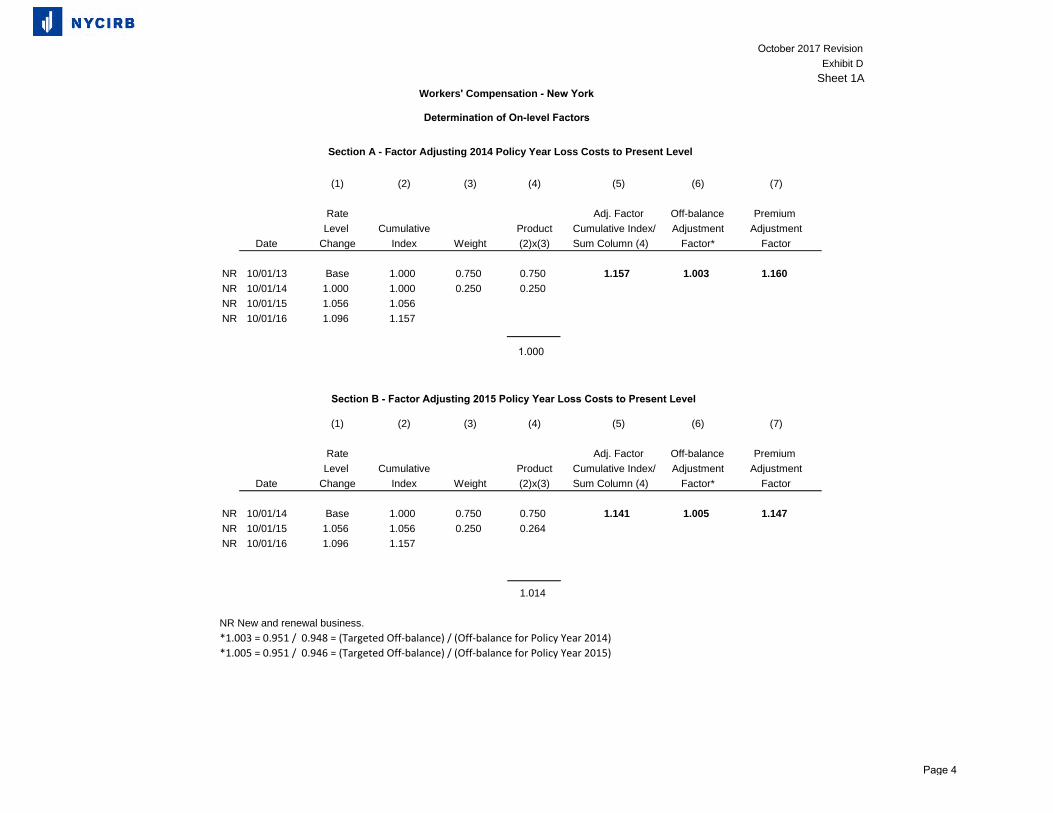

October 2017 RevisionExhibit D

Sheet 1A

(1) (2) (3) (4) (5) (6) (7)

Rate Adj. Factor Off-balance Premium Level Cumulative Product Cumulative Index/ Adjustment Adjustment

Date Change Index Weight (2)x(3) Sum Column (4) Factor* Factor

NR 10/01/13 Base 1.000 0.750 0.750 1.157 1.003 1.160NR 10/01/14 1.000 1.000 0.250 0.250NR 10/01/15 1.056 1.056 0.000NR 10/01/16 1.096 1.157

(1) (2) (3) (4) (5) (6) (7)

Rate Adj. Factor Off-balance Premium Level Cumulative Product Cumulative Index/ Adjustment Adjustment

Date Change Index Weight (2)x(3) Sum Column (4) Factor* Factor

NR 10/01/14 Base 1.000 0.750 0.750 1.141 1.005 1.147NR 10/01/15 1.056 1.056 0.250 0.264NR 10/01/16 1.096 1.157 0.000 0.000

1.014

NR New and renewal business.*1.003 = 0.951 / 0.948 = (Targeted Off-balance) / (Off-balance for Policy Year 2014)*1.005 = 0.951 / 0.946 = (Targeted Off-balance) / (Off-balance for Policy Year 2015)

Workers' Compensation - New York

Section A - Factor Adjusting 2014 Policy Year Loss Costs to Present Level

Determination of On-level Factors

Section B - Factor Adjusting 2015 Policy Year Loss Costs to Present Level

1.000

Page 4

October 2017 Revision

Exhibit D

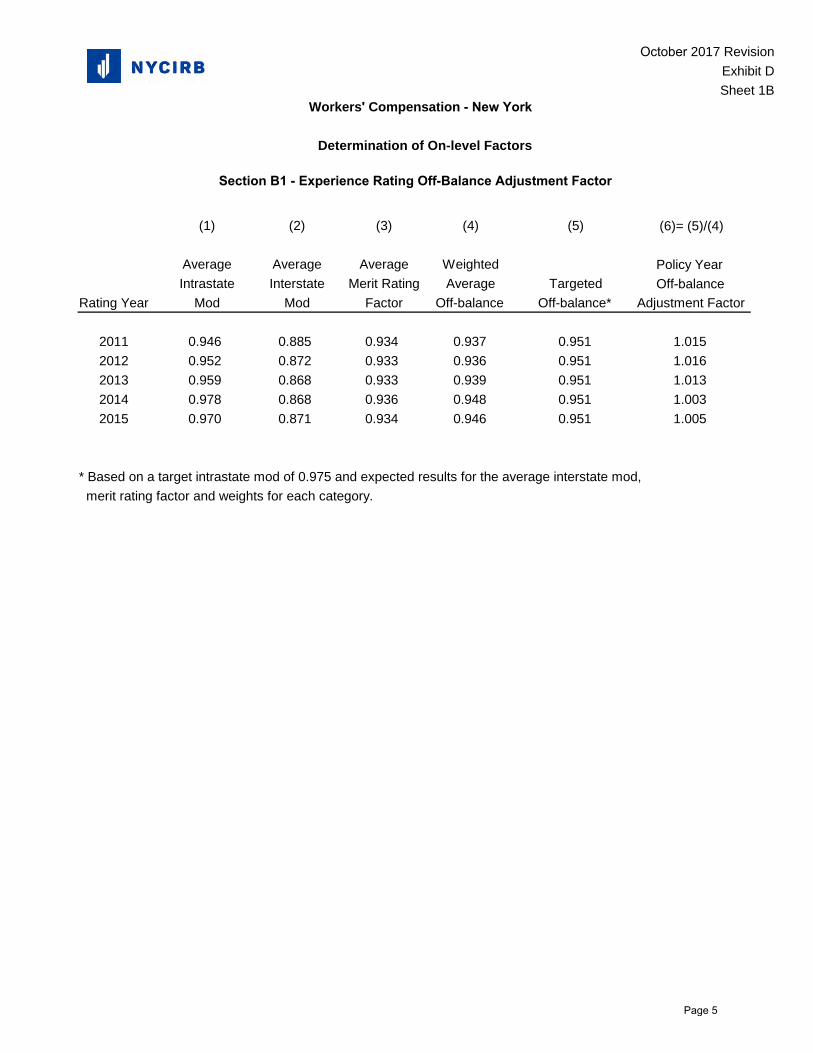

Sheet 1B

(1) (2) (3) (4) (5)

Average Average Average WeightedIntrastate Interstate Merit Rating Average Targeted

(6)= (5)/(4)

Policy Year Off-balance

Rating Year Mod Mod Factor Off-balance Off-balance* Adjustment Factor

2011 0.946 0.885 0.934 0.937 0.951 1.0152012 0.952 0.872 0.933 0.936 0.951 1.0162013 0.959 0.868 0.933 0.939 0.951 1.0132014 0.978 0.868 0.936 0.948 0.951 1.0032015 0.970 0.871 0.934 0.946 0.951 1.005

* Based on a target intrastate mod of 0.975 and expected results for the average interstate mod,merit rating factor and weights for each category.

Workers' Compensation - New York

Determination of On-level Factors

Section B1 - Experience Rating Off-Balance Adjustment Factor

Page 5

October 2017 RevisionExhibit DSheet 2

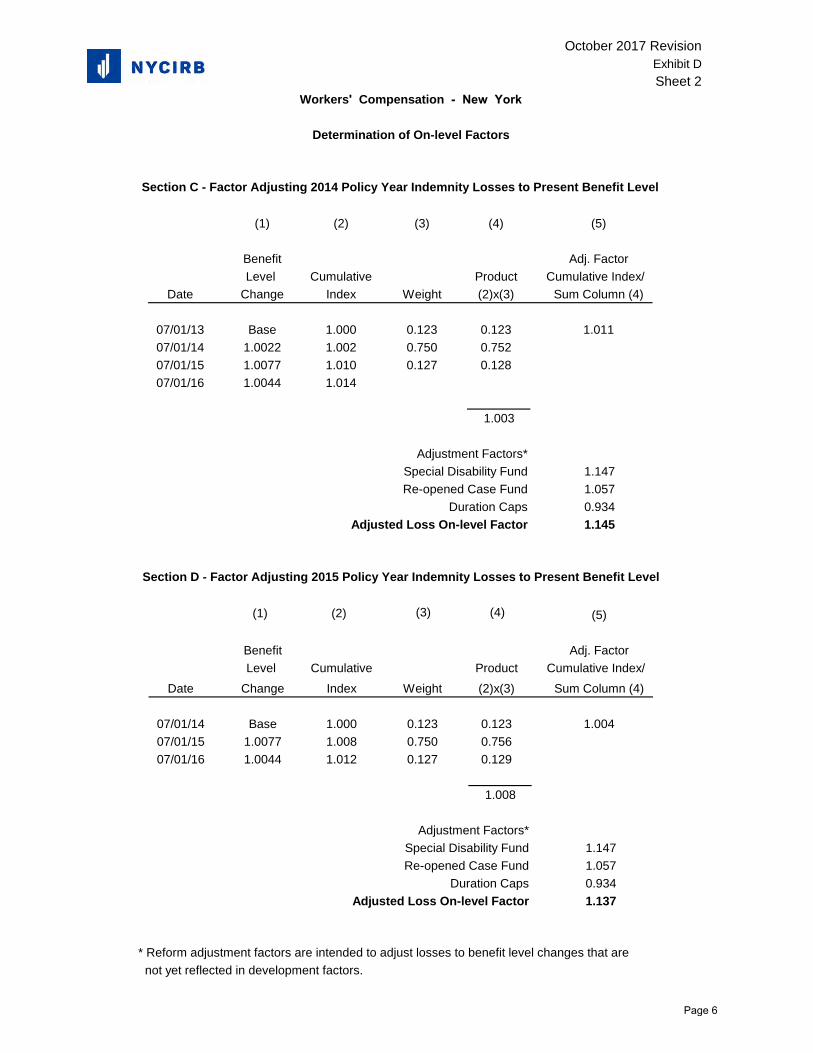

Workers' Compensation - New York

Determination of On-level Factors

Section C - Factor Adjusting 2014 Policy Year Indemnity Losses to Present Benefit Level

(1) (2) (3) (4) (5)

Benefit Adj. FactorLevel Cumulative Product Cumulative Index/

Date Change Index Weight (2)x(3) Sum Column (4)

07/01/13 Base 1.000 0.123 0.123 1.01107/01/14 1.0022 1.002 0.750 0.75207/01/15 1.0077 1.010 0.127 0.12807/01/16 1.0044 1.014 0.000 0.000

1.003

Adjustment Factors*Special Disability Fund 1.147Re-opened Case Fund 1.057

Duration Caps 0.934Adjusted Loss On-level Factor 1.145

Section D - Factor Adjusting 2015 Policy Year Indemnity Losses to Present Benefit Level

(1) (2) (3) (4) (5)

Benefit Adj. FactorLevel Cumulative Product Cumulative Index/

Date Change Index Weight (2)x(3) Sum Column (4)

07/01/14 Base 1.000 0.123 0.123 1.00407/01/15 1.0077 1.008 0.750 0.75607/01/16 1.0044 1.012 0.127 0.129

1.008

Adjustment Factors*Special Disability Fund 1.147Re-opened Case Fund 1.057

Duration Caps 0.934Adjusted Loss On-level Factor 1.137

* Reform adjustment factors are intended to adjust losses to benefit level changes that arenot yet reflected in development factors.

Page 6

October 2017 RevisionExhibit DSheet 3

Workers' Compensation - New York

Determination of On-level Factors

Section E - Factor Adjusting 2014 Policy Year Medical Losses to Present Benefit Level

(1) (2) (3) (4) (5)

Benefit Adj. FactorLevel Cumulative Product Cumulative Index/

Date Change Index Weight (2)x(3) Sum Column (4)

12/01/10 Base 1.000 1.000 1.000 1.000

1.000

Adjustment Factors*Re-opened Case Fund 1.059

Adjusted Loss On-level Factor 1.059

Section F - Factor Adjusting 2015 Policy Year Medical Losses to Present Benefit Level

(1) (2) (3) (4) (5)

Benefit Adj. FactorLevel Cumulative Product Cumulative Index/

Date Change Index Weight (2)x(3) Sum Column (4)

12/01/10 Base 1.000 1.000 1.000 1.000

1.000

Adjustment Factors*Re-opened Case Fund 1.059

Adjusted Loss On-level Factor 1.059

* Reform adjustment factors are intended to adjusted losses to benefit level changes that arenot yet reflected in development factors.

Page 7

October 2017 Revision

Exhibit D

Sheet 4

Paid + Case 1st to 20th 20th to Ult 1st to Ult Total Full Year % of Year Total

Original Restated Adjustment Original Restated Adjustment Adjustment Adjustment Impacted Adjustment

PY 08 PC 2.367 2.269 0.959 1.032 1.014 0.983 0.943 -5.7% 100% -5.7% 60%

SIF 2.180 2.081 0.955 1.070 1.032 0.964 0.921 -7.9% 100% -7.9% 40%

Total -6.6%

0.934

Restating the LDFs for Duration Cap: Example

(1) Original factor: Private Carriers: PY 2005 6th to 7th link ratio 1.027

(2) Development portion 0.027

(3) % of Non Sched out of total PPD 66.7%

(4) % of PPD out of total indemnity 86.6%

(5) % Non Scheduled out of indemnity (3)x(4) 57.7%

(6) Development portion that is NSPPD (2)x(5) 0.016

(7) Development portion that is other than NSPPD (2)-(6) 0.011

(8) % of cases effected by limited duration* 40%

(9) Restated NSPPD development portion (6) x [1-(8)] 0.009

(10) Restated total development 1+(9)+(7) 1.021

* Row (8) assumes at this point in the development, 40% of cases are now limited, whereas before they were still developing. 60% of the cases are still

developing at this point in the triangle, even after the reform, as they still haven't reached the maximum duration. These assumed percentages can be

found on the top of each column of the "restated" triangles. The percentages are based on a distribution of severities obtained from the WCB.

Development: Duration Cap Reform Adjustment Summary

Page 8

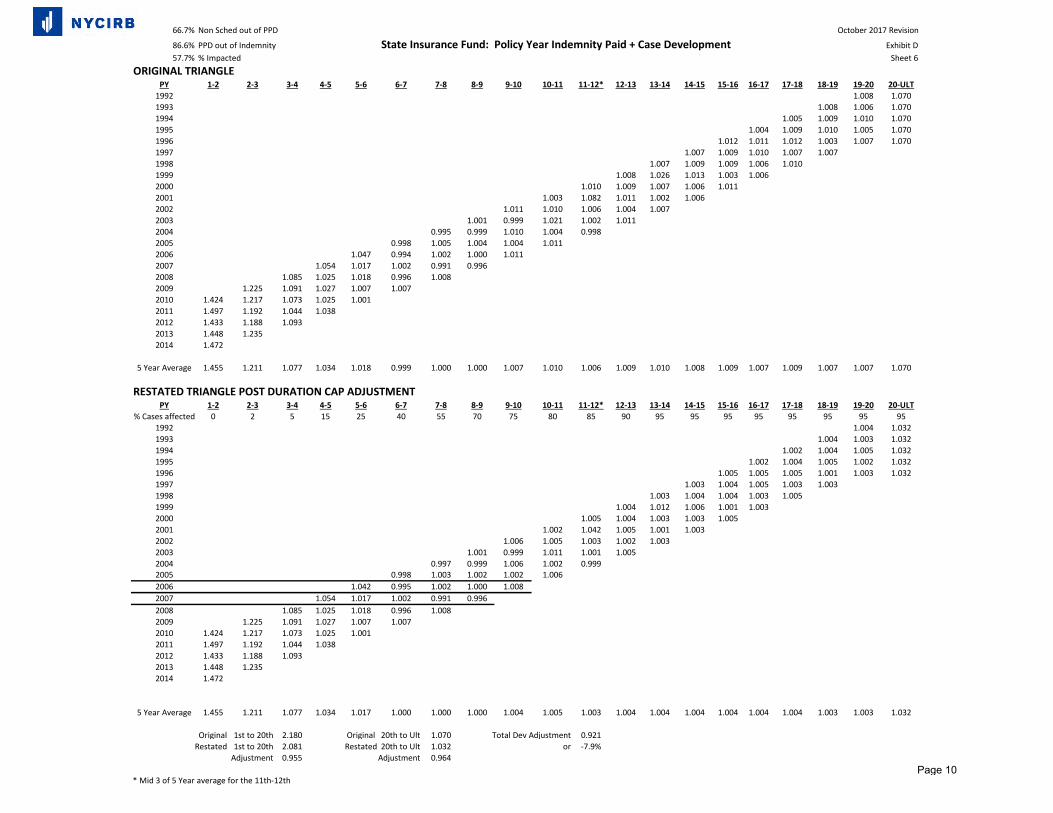

October 2017 Revision66.7% Non Sched out of PPD Exhibit D

86.56% PPD out of Indemnity Private Carriers: Policy Year Indemnity Paid + Case Development Sheet 557.72% % Impacted

ORIGINAL TRIANGLEPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-20 20-ULT

1992 1.004 1.0321993 1.002 1.003 1.0321994 1.004 1.005 1.004 1.0321995 1.004 1.004 1.003 1.005 1.0321996 1.005 1.004 1.002 1.003 1.001 1.0321997 1.005 1.004 1.001 1.004 1.0041998 1.002 1.004 1.004 1.003 1.0051999 1.007 1.003 1.006 1.004 1.0022000 1.007 1.005 1.008 1.002 1.0012001 1.018 1.004 1.008 1.002 1.0022002 1.020 1.017 1.009 1.007 1.0042003 1.024 1.012 1.013 1.006 1.0062004 1.022 1.025 1.012 1.006 0.9942005 1.027 1.025 1.013 1.008 1.0062006 1.068 1.028 1.017 1.008 1.0042007 1.050 1.044 1.011 1.019 1.0072008 1.114 1.047 1.025 1.034 1.0032009 1.200 1.116 1.037 1.024 1.0062010 1.509 1.220 1.093 1.040 1.0132011 1.512 1.207 1.092 1.0652012 1.493 1.189 1.0582013 1.495 1.1652014 1.448

5 Year Average 1.491 1.196 1.095 1.048 1.035 1.021 1.017 1.015 1.011 1.012 1.004 1.007 1.004 1.004 1.004 1.003 1.004 1.003 1.003 1.032

RESTATED TRIANGLE POST DURATION CAP ADJUSTMENTPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-20 20-ULT

% Cases affected 0 2 5 15 25 40 55 70 75 80 85 90 95 95 95 95 95 95 95 951992 1.002 1.0141993 1.001 1.001 1.0141994 1.002 1.002 1.002 1.0141995 1.002 1.002 1.001 1.002 1.0141996 1.002 1.002 1.001 1.001 1.000 1.0141997 1.002 1.002 1.000 1.002 1.0021998 1.001 1.002 1.002 1.001 1.0021999 1.003 1.001 1.003 1.002 1.0012000 1.004 1.002 1.004 1.001 1.0002001 1.010 1.002 1.004 1.001 1.0012002 1.011 1.009 1.005 1.003 1.0022003 1.014 1.007 1.007 1.003 1.0032004 1.015 1.015 1.007 1.003 0.9972005 1.021 1.017 1.008 1.005 1.0032006 1.061 1.024 1.013 1.006 1.0032007 1.050 1.044 1.011 1.019 1.0072008 1.114 1.047 1.025 1.034 1.0032009 1.200 1.116 1.037 1.024 1.0062010 1.509 1.220 1.093 1.040 1.0132011 1.512 1.207 1.092 1.0652012 1.493 1.189 1.0582013 1.495 1.1652014 1.448

5 Year Average 1.491 1.196 1.095 1.048 1.033 1.019 1.013 1.010 1.007 1.006 1.002 1.003 1.002 1.002 1.002 1.001 1.002 1.001 1.001 1.014

Original 1st to 20th 2.367 Original 20th to Ult 1.032 Total Dev Adjustment 0.943Restated 1st to 20th 2.269 Restated 20th to Ult 1.014 or -5.7%

Adjustment 0.959 Adjustment 0.983Page 9

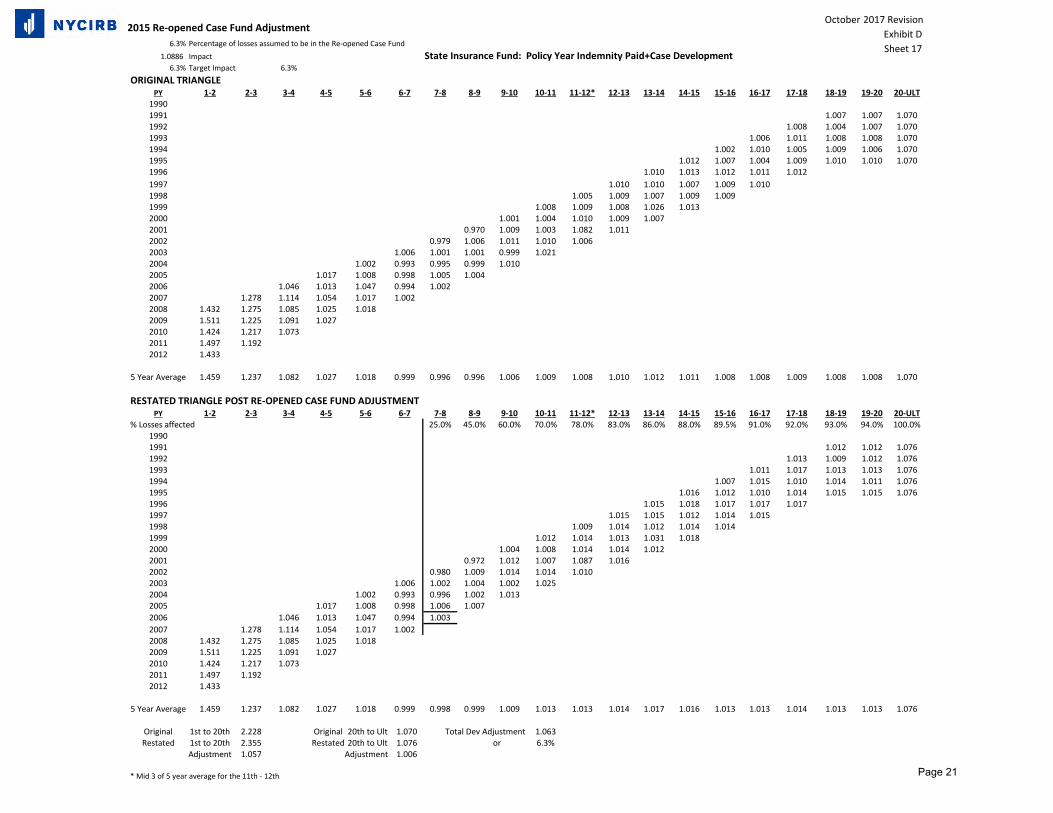

66.7% Non Sched out of PPD October 2017 Revision

86.6% PPD out of Indemnity State Insurance Fund: Policy Year Indemnity Paid + Case Development Exhibit D57.7% % Impacted Sheet 6

ORIGINAL TRIANGLEPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12* 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-20 20-ULT

1992 1.008 1.0701993 1.008 1.006 1.0701994 1.005 1.009 1.010 1.0701995 1.004 1.009 1.010 1.005 1.0701996 1.012 1.011 1.012 1.003 1.007 1.0701997 1.007 1.009 1.010 1.007 1.0071998 1.007 1.009 1.009 1.006 1.0101999 1.008 1.026 1.013 1.003 1.0062000 1.010 1.009 1.007 1.006 1.0112001 1.003 1.082 1.011 1.002 1.0062002 1.011 1.010 1.006 1.004 1.0072003 1.001 0.999 1.021 1.002 1.0112004 0.995 0.999 1.010 1.004 0.9982005 0.998 1.005 1.004 1.004 1.0112006 1.047 0.994 1.002 1.000 1.0112007 1.054 1.017 1.002 0.991 0.9962008 1.085 1.025 1.018 0.996 1.0082009 1.225 1.091 1.027 1.007 1.0072010 1.424 1.217 1.073 1.025 1.0012011 1.497 1.192 1.044 1.0382012 1.433 1.188 1.0932013 1.448 1.2352014 1.472

5 Year Average 1.455 1.211 1.077 1.034 1.018 0.999 1.000 1.000 1.007 1.010 1.006 1.009 1.010 1.008 1.009 1.007 1.009 1.007 1.007 1.070

RESTATED TRIANGLE POST DURATION CAP ADJUSTMENTPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12* 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-20 20-ULT

% Cases affected 0 2 5 15 25 40 55 70 75 80 85 90 95 95 95 95 95 95 95 951992 1.004 1.0321993 1.004 1.003 1.0321994 1.002 1.004 1.005 1.0321995 1.002 1.004 1.005 1.002 1.0321996 1.005 1.005 1.005 1.001 1.003 1.0321997 1.003 1.004 1.005 1.003 1.0031998 1.003 1.004 1.004 1.003 1.0051999 1.004 1.012 1.006 1.001 1.0032000 1.005 1.004 1.003 1.003 1.0052001 1.002 1.042 1.005 1.001 1.0032002 1.006 1.005 1.003 1.002 1.0032003 1.001 0.999 1.011 1.001 1.0052004 0.997 0.999 1.006 1.002 0.9992005 0.998 1.003 1.002 1.002 1.0062006 1.042 0.995 1.002 1.000 1.0082007 1.054 1.017 1.002 0.991 0.9962008 1.085 1.025 1.018 0.996 1.0082009 1.225 1.091 1.027 1.007 1.0072010 1.424 1.217 1.073 1.025 1.0012011 1.497 1.192 1.044 1.0382012 1.433 1.188 1.0932013 1.448 1.2352014 1.472

5 Year Average 1.455 1.211 1.077 1.034 1.017 1.000 1.000 1.000 1.004 1.005 1.003 1.004 1.004 1.004 1.004 1.004 1.004 1.003 1.003 1.032

Original 1st to 20th 2.180 Original 20th to Ult 1.070 Total Dev Adjustment 0.921Restated 1st to 20th 2.081 Restated 20th to Ult 1.032 or -7.9%

Adjustment 0.955 Adjustment 0.964

* Mid 3 of 5 Year average for the 11th-12thPage 10

October 2017 RevisionExhibit D

Sheet 7

Weight SDF ImpactPrivate Carriers (see Exhibit D, Sheet 9) 60% (a) 14.9% (c)State Insurance Fund (see Exhibit D, Sheet 11) 40% (b) 14.4% (d)Totals SDF Impact = (a)x(c) + (b)x(d) 14.7%

27,102470,253

1) Total SDF Claims Accepted (Private Carriers + SIF)*2) Total Workers' Compensation Indemnity Claims **3) Percentage of Claims Assumed to be in the SDF = (1)/(2) 5.8%

*Data Based on Accident Years 1998-2005 from Special Funds Conservative Committee**Data Based on Accident Years 1998-2005 from New York Financial Call Information System

Derivation of Special Disability Fund Adjustment

Percentage of Claims Accepted by the Special Disability Fund

Page 11

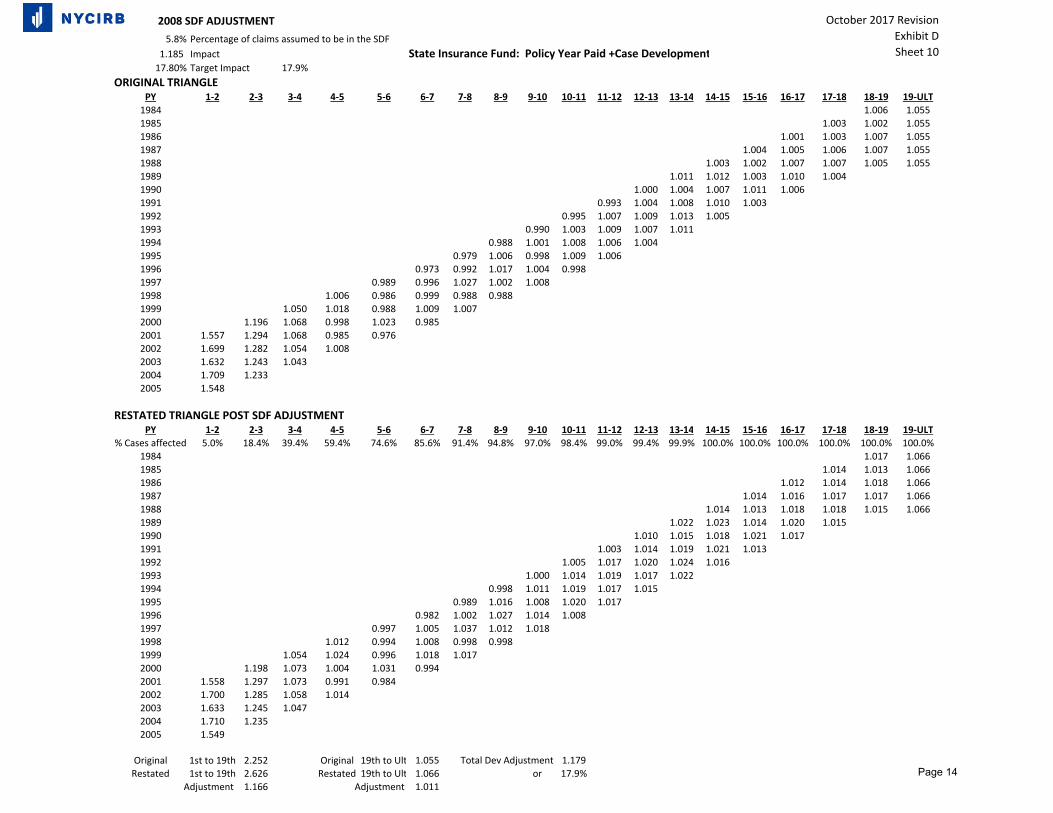

2008 SDF Adjustment October 2017 RevisionExhibit DSheet 85.8% Percentage of claims assumed to be in the SDF

1.189 Impact Private Carriers: Policy Year Paid + Case Development17.80% Target Impact 17.7%

ORIGINAL TRIANGLEPY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐ULT1984 0.999 1.0401985 1.000 1.015 1.0401986 1.009 0.997 1.009 1.0401987 1.019 1.004 1.016 1.019 1.0401988 1.002 0.979 1.017 1.012 0.991 1.0401989 1.012 0.996 1.015 1.009 0.9991990 1.005 1.006 1.028 1.007 0.9981991 1.002 1.013 1.031 1.010 0.9991992 1.003 1.019 1.031 1.013 1.0001993 0.991 1.022 1.027 1.010 1.0031994 1.008 1.024 1.038 1.017 1.0091995 0.999 1.023 1.018 1.014 1.0061996 1.005 1.024 1.027 1.016 1.0081997 1.043 1.053 1.014 1.019 1.0081998 1.074 1.070 1.037 1.002 1.0151999 1.093 1.073 1.032 1.023 1.0382000 1.272 1.121 1.072 1.036 1.0362001 1.586 1.289 1.175 1.062 1.0662002 1.419 1.181 1.068 1.0692003 1.388 1.169 1.1162004 1.407 1.2142005 1.392

RESTATED TRIANGLE POST SDF ADJUSTMENTPY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐ULT

% Cases affected 4.4% 12.5% 27.6% 44.3% 60.1% 74.9% 84.2% 90.3% 94.2% 96.6% 98.2% 99.1% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%1984 1.010 1.0511985 1.011 1.026 1.0511986 1.020 1.008 1.020 1.0511987 1.030 1.015 1.027 1.030 1.0511988 1.013 0.990 1.028 1.023 1.002 1.0511989 1.023 1.007 1.026 1.020 1.0101990 1.016 1.017 1.039 1.018 1.0091991 1.013 1.024 1.042 1.021 1.0101992 1.014 1.030 1.042 1.024 1.0111993 1.001 1.033 1.038 1.021 1.0141994 1.018 1.035 1.049 1.028 1.0201995 1.008 1.033 1.029 1.025 1.0171996 1.013 1.033 1.037 1.026 1.0191997 1.050 1.062 1.023 1.029 1.0181998 1.079 1.077 1.046 1.011 1.0251999 1.096 1.078 1.039 1.031 1.0482000 1.274 1.124 1.077 1.043 1.0452001 1.587 1.291 1.179 1.067 1.0732002 1.420 1.183 1.071 1.0742003 1.389 1.171 1.1192004 1.408 1.2162005 1.393

Original 1st to 19th 2.587 Original 19th to Ult 1.040 Total Dev Adjustment 1.177Restated 1st to 19th 3.010 Restated 19th to Ult 1.051 or 17.7%

Adjustment 1.164 Adjustment 1.011

Page 12

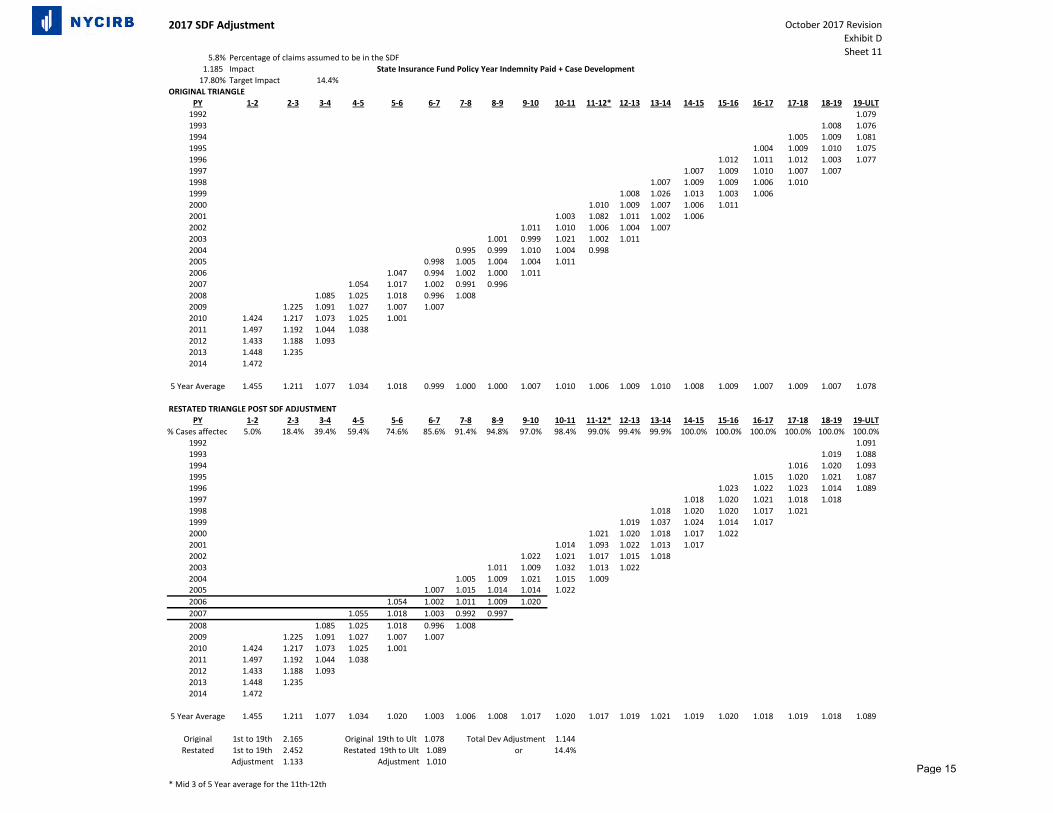

2017 SDF Adjustment October 2017 Revision

Exhibit DSheet 9

5.8% Percentage of claims assumed to be in the SDF1.189 Impact Private Carriers: Policy Year Indemnity Paid + Case Development Exhibit D

17.80% Target Impact 14.9% Sheet 9ORIGINAL TRIANGLE

PY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-ULT1992 1.0361993 1.002 1.0351994 1.004 1.005 1.0361995 1.004 1.004 1.003 1.0371996 1.005 1.004 1.002 1.003 1.0331997 1.005 1.004 1.001 1.004 1.0041998 1.002 1.004 1.004 1.003 1.0051999 1.007 1.003 1.006 1.004 1.0022000 1.007 1.005 1.008 1.002 1.0012001 1.018 1.004 1.008 1.002 1.0022002 1.020 1.017 1.009 1.007 1.0042003 1.024 1.012 1.013 1.006 1.0062004 1.022 1.025 1.012 1.006 0.9942005 1.027 1.025 1.013 1.008 1.0062006 1.068 1.028 1.017 1.008 1.0042007 1.050 1.044 1.011 1.019 1.0072008 1.114 1.047 1.025 1.034 1.0032009 1.200 1.116 1.037 1.024 1.0062010 1.509 1.220 1.093 1.040 1.0132011 1.512 1.207 1.092 1.0652012 1.493 1.189 1.0582013 1.495 1.1652014 1.448

5 Year Average 1.491 1.196 1.095 1.048 1.035 1.021 1.017 1.015 1.011 1.012 1.004 1.007 1.004 1.004 1.004 1.003 1.004 1.003 1.035

RESTATED TRIANGLE POST SDF ADJUSTMENTPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-ULT

% Cases affected 4.4% 12.5% 27.6% 44.3% 60.1% 74.857% 84.2% 90.3% 94.2% 96.6% 98.2% 99.1% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%1992 1.0471993 1.013 1.0461994 1.015 1.016 1.0471995 1.015 1.015 1.014 1.0481996 1.016 1.015 1.013 1.014 1.0441997 1.016 1.015 1.012 1.015 1.0151998 1.013 1.015 1.015 1.014 1.0161999 1.018 1.014 1.017 1.015 1.0132000 1.018 1.016 1.019 1.013 1.0122001 1.029 1.015 1.019 1.013 1.0132002 1.031 1.028 1.020 1.018 1.0152003 1.034 1.022 1.024 1.017 1.0172004 1.031 1.035 1.022 1.017 1.0052005 1.035 1.034 1.023 1.018 1.0172006 1.074 1.035 1.025 1.017 1.0132007 1.051 1.045 1.012 1.020 1.0082008 1.114 1.047 1.025 1.034 1.0032009 1.200 1.116 1.037 1.024 1.0062010 1.509 1.220 1.093 1.040 1.0132011 1.512 1.207 1.092 1.0652012 1.493 1.189 1.0582013 1.495 1.1652014 1.448

5 Year Average 1.491 1.196 1.095 1.048 1.036 1.025 1.023 1.023 1.021 1.023 1.015 1.018 1.015 1.015 1.015 1.014 1.015 1.014 1.047

Original 1st to 19th 2.360 Original 19th to Ult 1.035 Total Dev Adjustment 1.149Restated 1st to 19th 2.678 Restated 19th to Ult 1.047 or 14.9%

Adjustment 1.135 Adjustment 1.012Page 13

2008 SDF ADJUSTMENT October 2017 Revision

Exhibit D

Sheet 105.8% Percentage of claims assumed to be in the SDF

1.185 Impact State Insurance Fund: Policy Year Paid +Case Development17.80% Target Impact 17.9%

ORIGINAL TRIANGLEPY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐ULT1984 1.006 1.0551985 1.003 1.002 1.0551986 1.001 1.003 1.007 1.0551987 1.004 1.005 1.006 1.007 1.0551988 1.003 1.002 1.007 1.007 1.005 1.0551989 1.011 1.012 1.003 1.010 1.0041990 1.000 1.004 1.007 1.011 1.0061991 0.993 1.004 1.008 1.010 1.0031992 0.995 1.007 1.009 1.013 1.0051993 0.990 1.003 1.009 1.007 1.0111994 0.988 1.001 1.008 1.006 1.0041995 0.979 1.006 0.998 1.009 1.0061996 0.973 0.992 1.017 1.004 0.9981997 0.989 0.996 1.027 1.002 1.0081998 1.006 0.986 0.999 0.988 0.9881999 1.050 1.018 0.988 1.009 1.0072000 1.196 1.068 0.998 1.023 0.9852001 1.557 1.294 1.068 0.985 0.9762002 1.699 1.282 1.054 1.0082003 1.632 1.243 1.0432004 1.709 1.2332005 1.548

RESTATED TRIANGLE POST SDF ADJUSTMENTPY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐ULT

% Cases affected 5.0% 18.4% 39.4% 59.4% 74.6% 85.6% 91.4% 94.8% 97.0% 98.4% 99.0% 99.4% 99.9% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%1984 1.017 1.0661985 1.014 1.013 1.0661986 1.012 1.014 1.018 1.0661987 1.014 1.016 1.017 1.017 1.0661988 1.014 1.013 1.018 1.018 1.015 1.0661989 1.022 1.023 1.014 1.020 1.0151990 1.010 1.015 1.018 1.021 1.0171991 1.003 1.014 1.019 1.021 1.0131992 1.005 1.017 1.020 1.024 1.0161993 1.000 1.014 1.019 1.017 1.0221994 0.998 1.011 1.019 1.017 1.0151995 0.989 1.016 1.008 1.020 1.0171996 0.982 1.002 1.027 1.014 1.0081997 0.997 1.005 1.037 1.012 1.0181998 1.012 0.994 1.008 0.998 0.9981999 1.054 1.024 0.996 1.018 1.0172000 1.198 1.073 1.004 1.031 0.9942001 1.558 1.297 1.073 0.991 0.9842002 1.700 1.285 1.058 1.0142003 1.633 1.245 1.0472004 1.710 1.2352005 1.549

Original 1st to 19th 2.252 Original 19th to Ult 1.055 Total Dev Adjustment 1.179Restated 1st to 19th 2.626 Restated 19th to Ult 1.066 or 17.9%

Adjustment 1.166 Adjustment 1.011Page 14

2017 SDF Adjustment

5.8% Percentage of claims assumed to be in the SDF1.185 Impact State Insurance Fund Policy Year Indemnity Paid + Case Development

17.80% Target Impact 14.4%

October 2017 Revision

Exhibit DSheet 11

2017 Revision Exhibit DSheet 11

ORIGINAL TRIANGLEPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12* 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-ULT

1992 1.0791993 1.008 1.0761994 1.005 1.009 1.0811995 1.004 1.009 1.010 1.0751996 1.012 1.011 1.012 1.003 1.0771997 1.007 1.009 1.010 1.007 1.0071998 1.007 1.009 1.009 1.006 1.0101999 1.008 1.026 1.013 1.003 1.0062000 1.010 1.009 1.007 1.006 1.0112001 1.003 1.082 1.011 1.002 1.0062002 1.011 1.010 1.006 1.004 1.0072003 1.001 0.999 1.021 1.002 1.0112004 0.995 0.999 1.010 1.004 0.9982005 0.998 1.005 1.004 1.004 1.0112006 1.047 0.994 1.002 1.000 1.0112007 1.054 1.017 1.002 0.991 0.9962008 1.085 1.025 1.018 0.996 1.0082009 1.225 1.091 1.027 1.007 1.0072010 1.424 1.217 1.073 1.025 1.0012011 1.497 1.192 1.044 1.0382012 1.433 1.188 1.0932013 1.448 1.2352014 1.472

5 Year Average 1.455 1.211 1.077 1.034 1.018 0.999 1.000 1.000 1.007 1.010 1.006 1.009 1.010 1.008 1.009 1.007 1.009 1.007 1.078

RESTATED TRIANGLE POST SDF ADJUSTMENTPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12* 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-ULT

% Cases affected 5.0% 18.4% 39.4% 59.4% 74.6% 85.6% 91.4% 94.8% 97.0% 98.4% 99.0% 99.4% 99.9% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%1992 1.0911993 1.019 1.0881994 1.016 1.020 1.0931995 1.015 1.020 1.021 1.0871996 1.023 1.022 1.023 1.014 1.0891997 1.018 1.020 1.021 1.018 1.0181998 1.018 1.020 1.020 1.017 1.0211999 1.019 1.037 1.024 1.014 1.0172000 1.021 1.020 1.018 1.017 1.0222001 1.014 1.093 1.022 1.013 1.0172002 1.022 1.021 1.017 1.015 1.0182003 1.011 1.009 1.032 1.013 1.0222004 1.005 1.009 1.021 1.015 1.0092005 1.007 1.015 1.014 1.014 1.0222006 1.054 1.002 1.011 1.009 1.0202007 1.055 1.018 1.003 0.992 0.9972008 1.085 1.025 1.018 0.996 1.0082009 1.225 1.091 1.027 1.007 1.0072010 1.424 1.217 1.073 1.025 1.0012011 1.497 1.192 1.044 1.0382012 1.433 1.188 1.0932013 1.448 1.2352014 1.472

5 Year Average 1.455 1.211 1.077 1.034 1.020 1.003 1.006 1.008 1.017 1.020 1.017 1.019 1.021 1.019 1.020 1.018 1.019 1.018 1.089

Original 1st to 19th 2.165 Total Dev Adjustment 1.144Restated 1st to 19th 2.452 or 14.4%

Adjustment 1.133

Original 19th to Ult 1.078

Restated 19th to Ult 1.089

Adjustment 1.010

* Mid 3 of 5 Year average for the 11th‐12th

Page 15

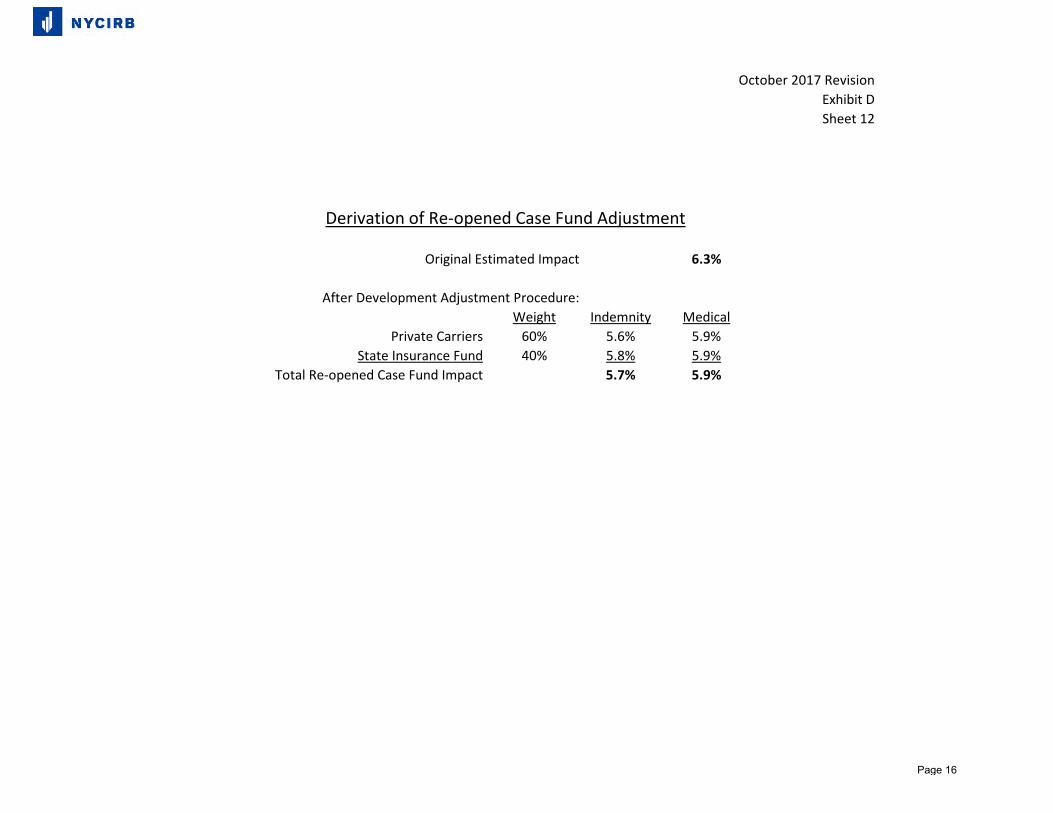

October 2017 Revision

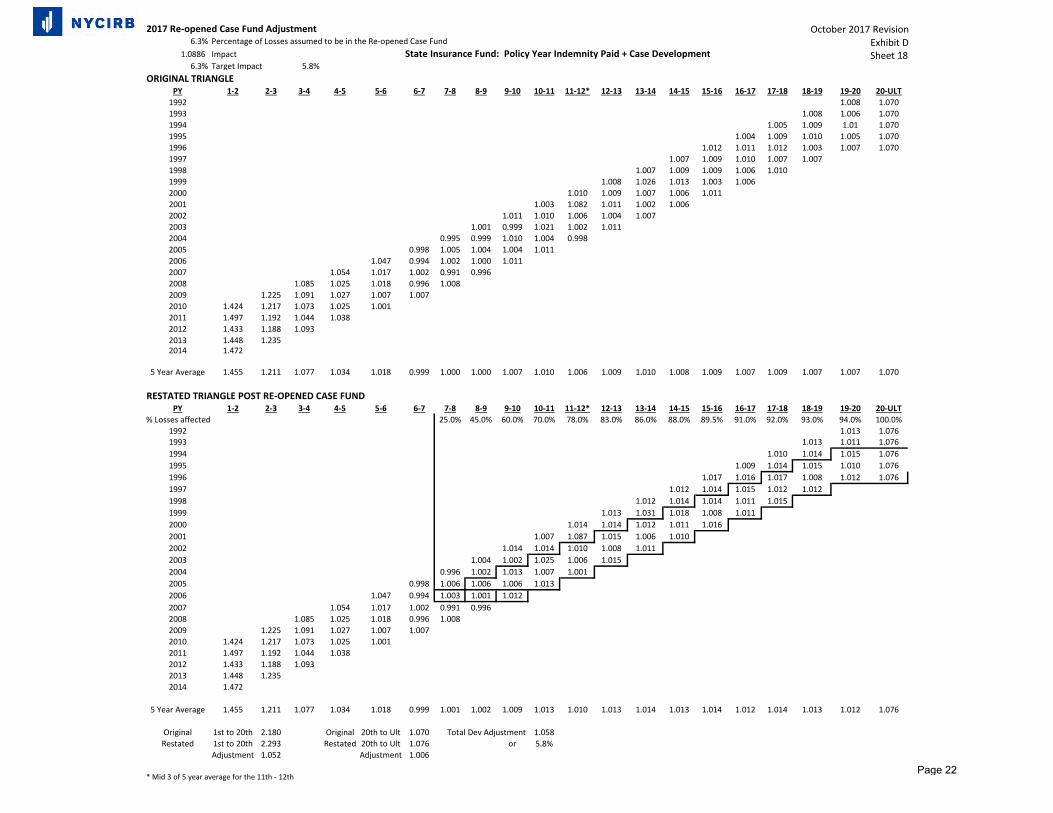

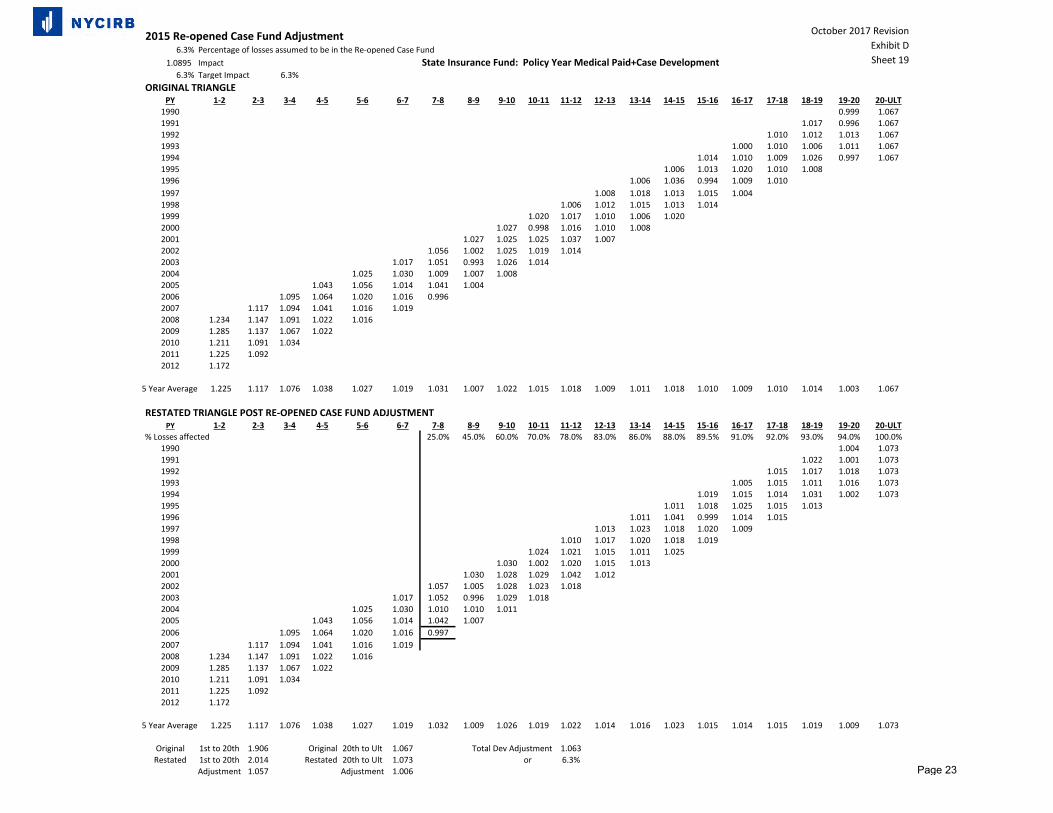

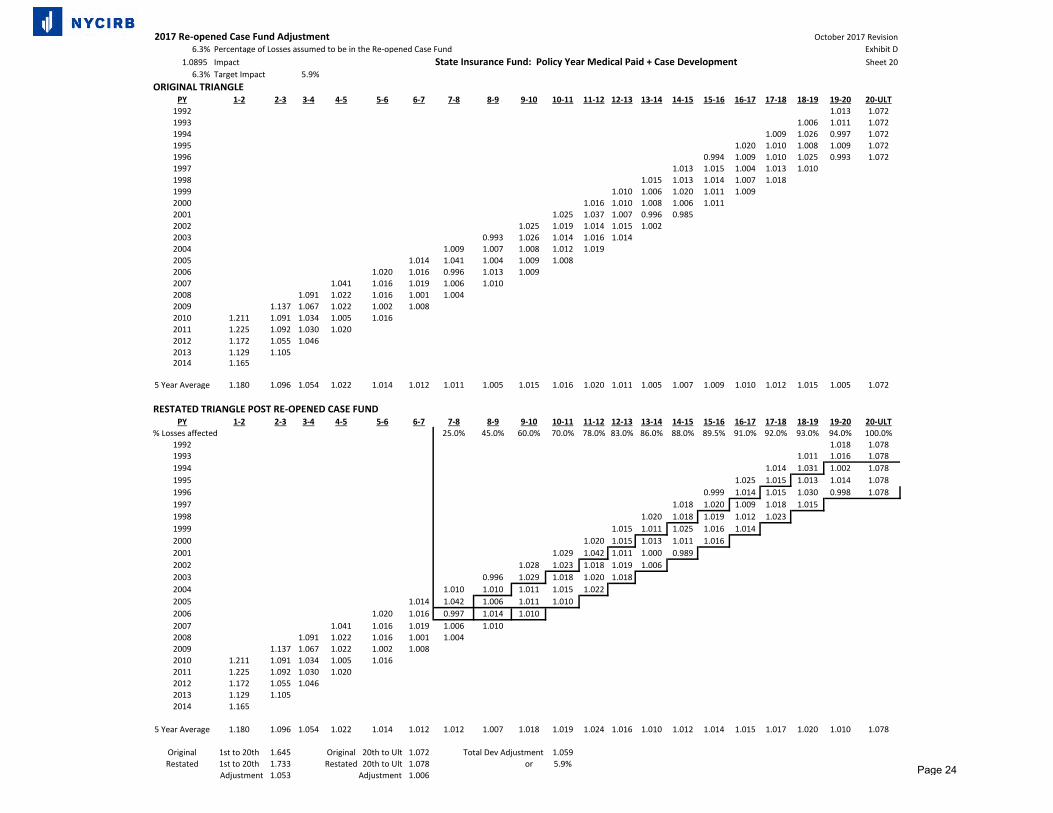

Exhibit DSheet 12

Original Estimated Impact 6.3%

After Development Adjustment Procedure:Weight Indemnity Medical

Private Carriers 60% 5.6% 5.9%State Insurance Fund 40% 5.8% 5.9%

Total Re-opened Case Fund Impact 5.7% 5.9%

Derivation of Re-opened Case Fund Adjustment

Page 16

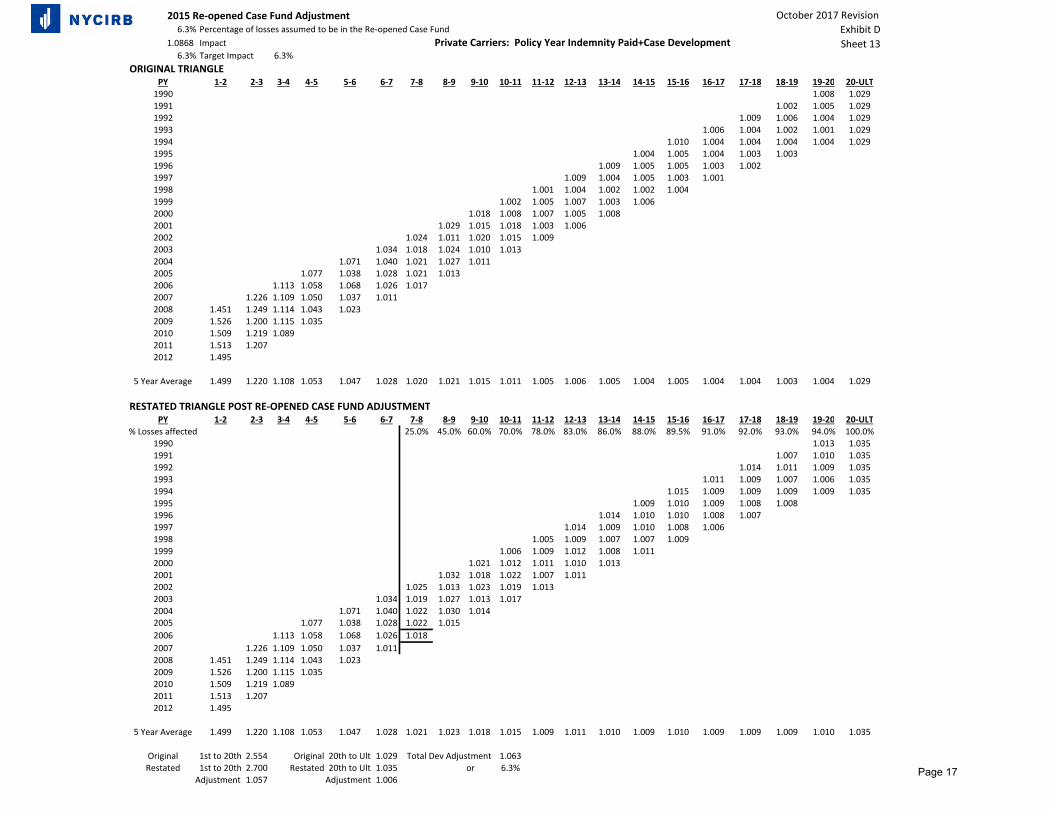

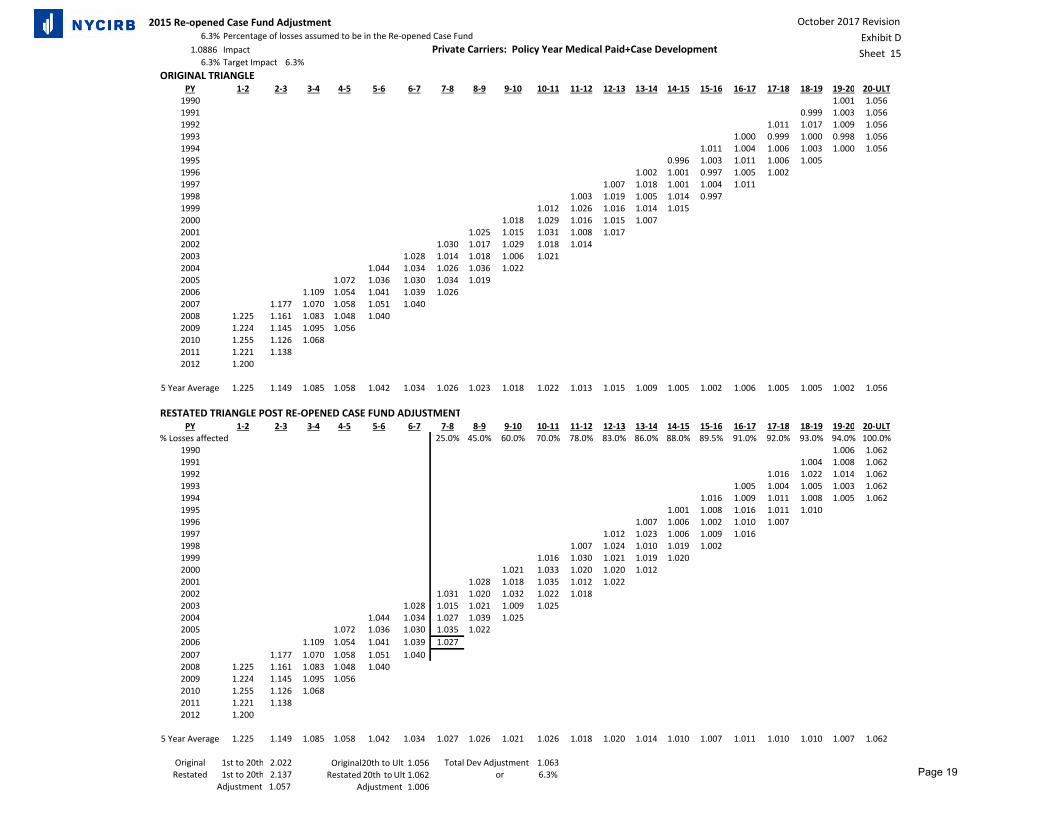

2015 Re‐opened Case Fund Adjustment October 2017 RevisionExhibit DSheet 13

6.3% Percentage of losses assumed to be in the Re‐opened Case Fund1.0868 Impact Private Carriers: Policy Year Indemnity Paid+Case Development

6.3% Target Impact 6.3%ORIGINAL TRIANGLE

PY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐20 20‐ULT1990 1.008 1.0291991 1.002 1.005 1.0291992 1.009 1.006 1.004 1.0291993 1.006 1.004 1.002 1.001 1.0291994 1.010 1.004 1.004 1.004 1.004 1.0291995 1.004 1.005 1.004 1.003 1.0031996 1.009 1.005 1.005 1.003 1.0021997 1.009 1.004 1.005 1.003 1.0011998 1.001 1.004 1.002 1.002 1.0041999 1.002 1.005 1.007 1.003 1.0062000 1.018 1.008 1.007 1.005 1.0082001 1.029 1.015 1.018 1.003 1.0062002 1.024 1.011 1.020 1.015 1.0092003 1.034 1.018 1.024 1.010 1.0132004 1.071 1.040 1.021 1.027 1.0112005 1.077 1.038 1.028 1.021 1.0132006 1.113 1.058 1.068 1.026 1.0172007 1.226 1.109 1.050 1.037 1.0112008 1.451 1.249 1.114 1.043 1.0232009 1.526 1.200 1.115 1.0352010 1.509 1.219 1.0892011 1.513 1.2072012 1.495

5 Year Average 1.499 1.220 1.108 1.053 1.047 1.028 1.020 1.021 1.015 1.011 1.005 1.006 1.005 1.004 1.005 1.004 1.004 1.003 1.004 1.029

RESTATED TRIANGLE POST RE‐OPENED CASE FUND ADJUSTMENTPY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐20 20‐ULT

% Losses affected 25.0% 45.0% 60.0% 70.0% 78.0% 83.0% 86.0% 88.0% 89.5% 91.0% 92.0% 93.0% 94.0% 100.0%1990 1.013 1.0351991 1.007 1.010 1.0351992 1.014 1.011 1.009 1.0351993 1.011 1.009 1.007 1.006 1.0351994 1.015 1.009 1.009 1.009 1.009 1.0351995 1.009 1.010 1.009 1.008 1.0081996 1.014 1.010 1.010 1.008 1.0071997 1.014 1.009 1.010 1.008 1.0061998 1.005 1.009 1.007 1.007 1.0091999 1.006 1.009 1.012 1.008 1.0112000 1.021 1.012 1.011 1.010 1.0132001 1.032 1.018 1.022 1.007 1.0112002 1.025 1.013 1.023 1.019 1.0132003 1.034 1.019 1.027 1.013 1.0172004 1.071 1.040 1.022 1.030 1.0142005 1.077 1.038 1.028 1.022 1.0152006 1.113 1.058 1.068 1.026 1.0182007 1.226 1.109 1.050 1.037 1.0112008 1.451 1.249 1.114 1.043 1.0232009 1.526 1.200 1.115 1.0352010 1.509 1.219 1.0892011 1.513 1.2072012 1.495

5 Year Average 1.499 1.220 1.108 1.053 1.047 1.028 1.021 1.023 1.018 1.015 1.009 1.011 1.010 1.009 1.010 1.009 1.009 1.009 1.010 1.035

Original 1st to 20th 2.554 Original 20th to Ult 1.029 Total Dev Adjustment 1.063Restated 1st to 20th 2.700 Restated 20th to Ult 1.035 or 6.3%

Adjustment 1.057 Adjustment 1.006Page 17

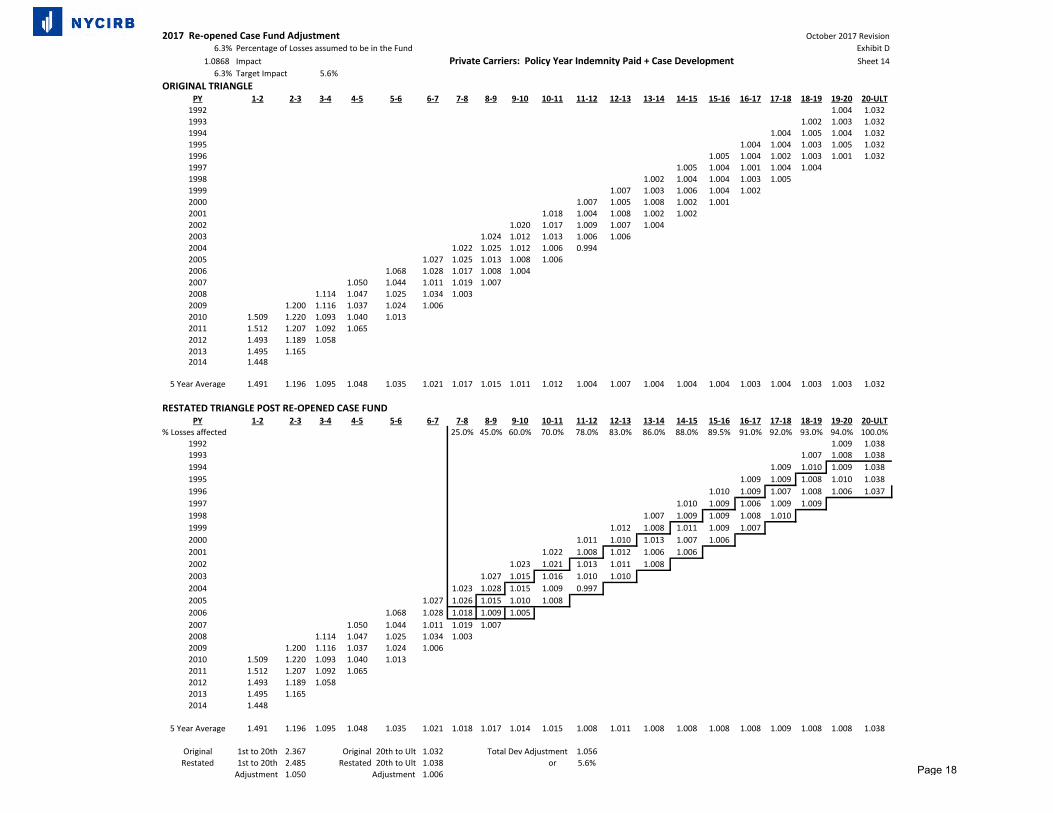

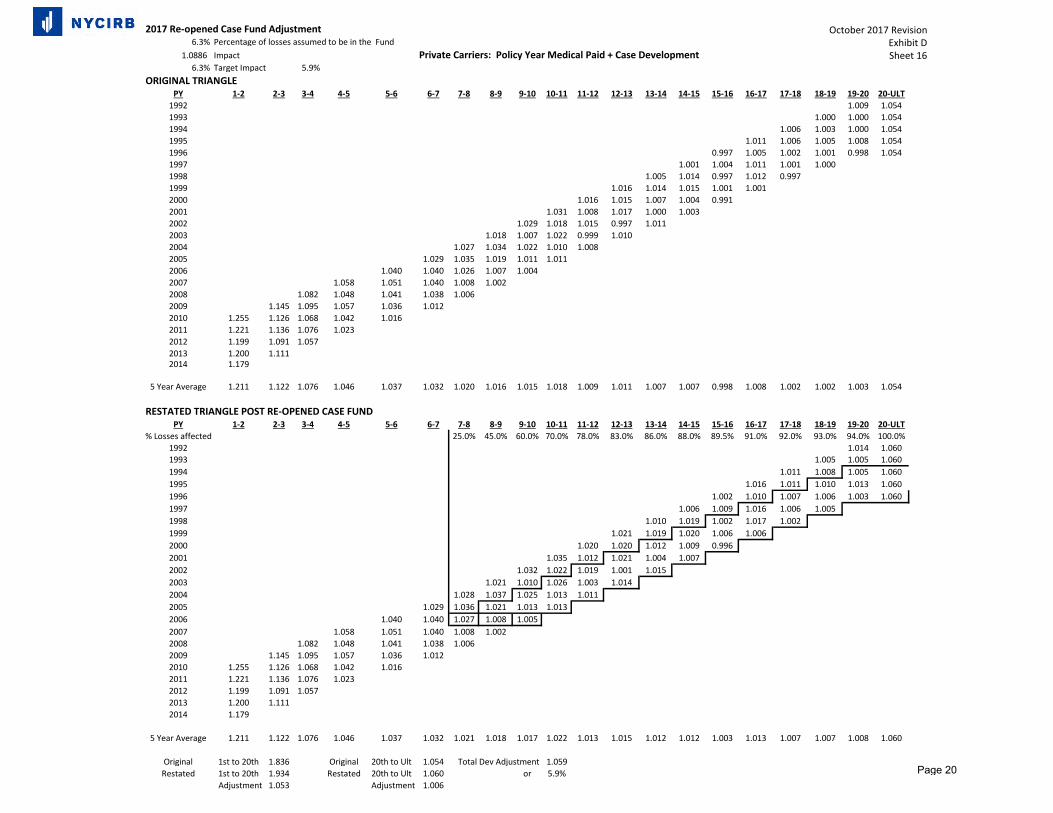

2017 Re-opened Case Fund Adjustment October 2017 Revision6.3% Percentage of Losses assumed to be in the Fund Exhibit D

1.0868 Impact Private Carriers: Policy Year Indemnity Paid + Case Development Sheet 146.3% Target Impact 5.6%

ORIGINAL TRIANGLEPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-20 20-ULT

1992 1.004 1.0321993 1.002 1.003 1.0321994 1.004 1.005 1.004 1.0321995 1.004 1.004 1.003 1.005 1.0321996 1.005 1.004 1.002 1.003 1.001 1.0321997 1.005 1.004 1.001 1.004 1.0041998 1.002 1.004 1.004 1.003 1.0051999 1.007 1.003 1.006 1.004 1.0022000 1.007 1.005 1.008 1.002 1.0012001 1.018 1.004 1.008 1.002 1.0022002 1.020 1.017 1.009 1.007 1.0042003 1.024 1.012 1.013 1.006 1.0062004 1.022 1.025 1.012 1.006 0.9942005 1.027 1.025 1.013 1.008 1.0062006 1.068 1.028 1.017 1.008 1.0042007 1.050 1.044 1.011 1.019 1.0072008 1.114 1.047 1.025 1.034 1.0032009 1.200 1.116 1.037 1.024 1.0062010 1.509 1.220 1.093 1.040 1.0132011 1.512 1.207 1.092 1.0652012 1.493 1.189 1.0582013 1.495 1.1652014 1.448

5 Year Average 1.491 1.196 1.095 1.048 1.035 1.021 1.017 1.015 1.011 1.012 1.004 1.007 1.004 1.004 1.004 1.003 1.004 1.003 1.003 1.032

RESTATED TRIANGLE POST RE-OPENED CASE FUNDPY 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 15-16 16-17 17-18 18-19 19-20 20-ULT

% Losses affected 25.0% 45.0% 60.0% 70.0% 78.0% 83.0% 86.0% 88.0% 89.5% 91.0% 92.0% 93.0% 94.0% 100.0%1992 1.009 1.0381993 1.007 1.008 1.0381994 1.009 1.010 1.009 1.0381995 1.009 1.009 1.008 1.010 1.0381996 1.010 1.009 1.007 1.008 1.006 1.0371997 1.010 1.009 1.006 1.009 1.0091998 1.007 1.009 1.009 1.008 1.0101999 1.012 1.008 1.011 1.009 1.0072000 1.011 1.010 1.013 1.007 1.0062001 1.022 1.008 1.012 1.006 1.0062002 1.023 1.021 1.013 1.011 1.0082003 1.027 1.015 1.016 1.010 1.0102004 1.023 1.028 1.015 1.009 0.9972005 1.027 1.026 1.015 1.010 1.0082006 1.068 1.028 1.018 1.009 1.0052007 1.050 1.044 1.011 1.019 1.0072008 1.114 1.047 1.025 1.034 1.0032009 1.200 1.116 1.037 1.024 1.0062010 1.509 1.220 1.093 1.040 1.0132011 1.512 1.207 1.092 1.0652012 1.493 1.189 1.0582013 1.495 1.1652014 1.448

5 Year Average 1.491 1.196 1.095 1.048 1.035 1.021 1.018 1.017 1.014 1.015 1.008 1.011 1.008 1.008 1.008 1.008 1.009 1.008 1.008 1.038

Original 1st to 20th 2.367 Original 20th to Ult 1.032 Total Dev Adjustment 1.056Restated 1st to 20th 2.485 Restated 20th to Ult 1.038 or 5.6%

Adjustment 1.050 Adjustment 1.006 Page 18

2015 Re‐opened Case Fund Adjustment October 2017 Revision Exhibit D

Sheet 15

6.3% Percentage of losses assumed to be in the Re‐opened Case Fund1.0886 Impact Private Carriers: Policy Year Medical Paid+Case Development

6.3% Target Impact 6.3%ORIGINAL TRIANGLE

PY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐20 20‐ULT1990 1.001 1.0561991 0.999 1.003 1.0561992 1.011 1.017 1.009 1.0561993 1.000 0.999 1.000 0.998 1.0561994 1.011 1.004 1.006 1.003 1.000 1.0561995 0.996 1.003 1.011 1.006 1.0051996 1.002 1.001 0.997 1.005 1.0021997 1.007 1.018 1.001 1.004 1.0111998 1.003 1.019 1.005 1.014 0.9971999 1.012 1.026 1.016 1.014 1.0152000 1.018 1.029 1.016 1.015 1.0072001 1.025 1.015 1.031 1.008 1.0172002 1.030 1.017 1.029 1.018 1.0142003 1.028 1.014 1.018 1.006 1.0212004 1.044 1.034 1.026 1.036 1.0222005 1.072 1.036 1.030 1.034 1.0192006 1.109 1.054 1.041 1.039 1.0262007 1.177 1.070 1.058 1.051 1.0402008 1.225 1.161 1.083 1.048 1.0402009 1.224 1.145 1.095 1.0562010 1.255 1.126 1.0682011 1.221 1.1382012 1.200

5 Year Average 1.225 1.149 1.085 1.058 1.042 1.034 1.026 1.023 1.018 1.022 1.013 1.015 1.009 1.005 1.002 1.006 1.005 1.005 1.002 1.056

RESTATED TRIANGLE POST RE‐OPENED CASE FUND ADJUSTMENTPY 1‐2 2‐3 3‐4 4‐5 5‐6 6‐7 7‐8 8‐9 9‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17 17‐18 18‐19 19‐20 20‐ULT

% Losses affected 25.0% 45.0% 60.0% 70.0% 78.0% 83.0% 86.0% 88.0% 89.5% 91.0% 92.0% 93.0% 94.0% 100.0%1990 1.006 1.0621991 1.004 1.008 1.0621992 1.016 1.022 1.014 1.0621993 1.005 1.004 1.005 1.003 1.0621994 1.016 1.009 1.011 1.008 1.005 1.0621995 1.001 1.008 1.016 1.011 1.0101996 1.007 1.006 1.002 1.010 1.0071997 1.012 1.023 1.006 1.009 1.0161998 1.007 1.024 1.010 1.019 1.0021999 1.016 1.030 1.021 1.019 1.0202000 1.021 1.033 1.020 1.020 1.0122001 1.028 1.018 1.035 1.012 1.0222002 1.031 1.020 1.032 1.022 1.0182003 1.028 1.015 1.021 1.009 1.0252004 1.044 1.034 1.027 1.039 1.0252005 1.072 1.036 1.030 1.035 1.0222006 1.109 1.054 1.041 1.039 1.0272007 1.177 1.070 1.058 1.051 1.0402008 1.225 1.161 1.083 1.048 1.0402009 1.224 1.145 1.095 1.0562010 1.255 1.126 1.0682011 1.221 1.1382012 1.200

5 Year Average 1.225 1.149 1.085 1.058 1.042 1.034 1.027 1.026 1.021 1.026 1.018 1.020 1.014 1.010 1.007 1.011 1.010 1.010 1.007 1.062

Original 1st to 20th 2.022 Total Dev Adjustment 1.063Restated 1st to 20th 2.137 or 6.3%

Adjustment 1.057

Original20th to Ult 1.056 Restated 20th to Ult 1.062

Adjustment 1.006Page 19