Rating Snowstorms Based on Travel Impacts Ernie Ostuno National Weather Service, GRR.

Upload

mandy-hancockCategory

view

220download

1description

©Texas Institute 2011

Impact of Nuclear Power Projects on Credit Ratings and

Creditor Recoveries Following Default of Investor Owned

Utilities Sponsoring Nuclear Projects

Assessing credit rating impact of nuclear power projects and recoveries by

creditors following default for United States investor owned utilities operating

nuclear power projects from 1960 to present

A Research Study by

September 1st, 2011

www.TexasInstitute.org

1

Table of Contents Introduction .................................................................................................................................................. 3

Acknowledgements ....................................................................................................................................... 3

Executive Summary ....................................................................................................................................... 3

Methodology ................................................................................................................................................. 4

Analysis of Credit Rating Impact of Nuclear Plant Development ................................................................. 6

Significance and Definition ....................................................................................................................... 6

Conclusion ................................................................................................................................................. 6

Technical Summary and Charts ................................................................................................................. 6

Default Events of Nuclear Power Sponsors .................................................................................................. 8

Significance and Definition ....................................................................................................................... 8

Conclusion ................................................................................................................................................. 9

Technical Summary and Charts ................................................................................................................. 9

Rating Transition Rates for Nuclear Power Investor Owned Utilities ......................................................... 12

Significance and Definition ..................................................................................................................... 12

Conclusion ............................................................................................................................................... 12

Technical Summary and Charts ............................................................................................................... 13

Historical Default Rates for Investor Owned Utilities ................................................................................. 14

Significance and Definition ..................................................................................................................... 14

Conclusion ............................................................................................................................................... 14

Technical Summary and Charts ............................................................................................................... 14

Rating Dynamics of Nuclear Power Defaulters ........................................................................................... 17

Significance and Definition ..................................................................................................................... 17

Conclusion ............................................................................................................................................... 17

Technical Summary and Charts ............................................................................................................... 17

Default Experience for Preferred Stock ...................................................................................................... 18

Significance and Definition ..................................................................................................................... 18

Conclusion ............................................................................................................................................... 18

Technical Summary and Charts ............................................................................................................... 18

Risk of Loss to Creditors .............................................................................................................................. 19

Significance and Definition ..................................................................................................................... 19

2

Conclusion ............................................................................................................................................... 19

Technical Summary and Discussion ........................................................................................................ 19

Value-Weighted Ultimate Recovery Rates.................................................................................................. 20

Significance and Definition ..................................................................................................................... 20

Conclusion ............................................................................................................................................... 20

Technical Summary and Charts ............................................................................................................... 20

Creditor Loss Using 30 Days Post Default Trading Price ............................................................................. 22

Significance and Definition ..................................................................................................................... 22

Conclusion ............................................................................................................................................... 22

Technical Summary and Charts ............................................................................................................... 22

Discussion Regarding Risk of Loss to Creditors ........................................................................................... 24

Condensed Information Regarding Specific Default Events of US Utilities with Nuclear Operations ........ 25

1) El Paso Electric Company, January 8, 1992 ......................................................................................... 25

2) Energy Future Holdings Corp., August 17, 2010 ................................................................................. 26

3) Pacific Gas & Electric Company, April 6, 2001 .................................................................................... 26

4) Public Service Company of New Hampshire, January 28, 1988.......................................................... 27

5) Southern California Edison Company, January 16, 2001 .................................................................... 27

6) Yankee Companies, Incorporated, June 30, 1987 .............................................................................. 28

Summary of Findings................................................................................................................................... 28

Appendices .................................................................................................................................................. 30

Table 1 Precedent Rating Actions for Utilities Attempted to Build Reactors .......................................... 30

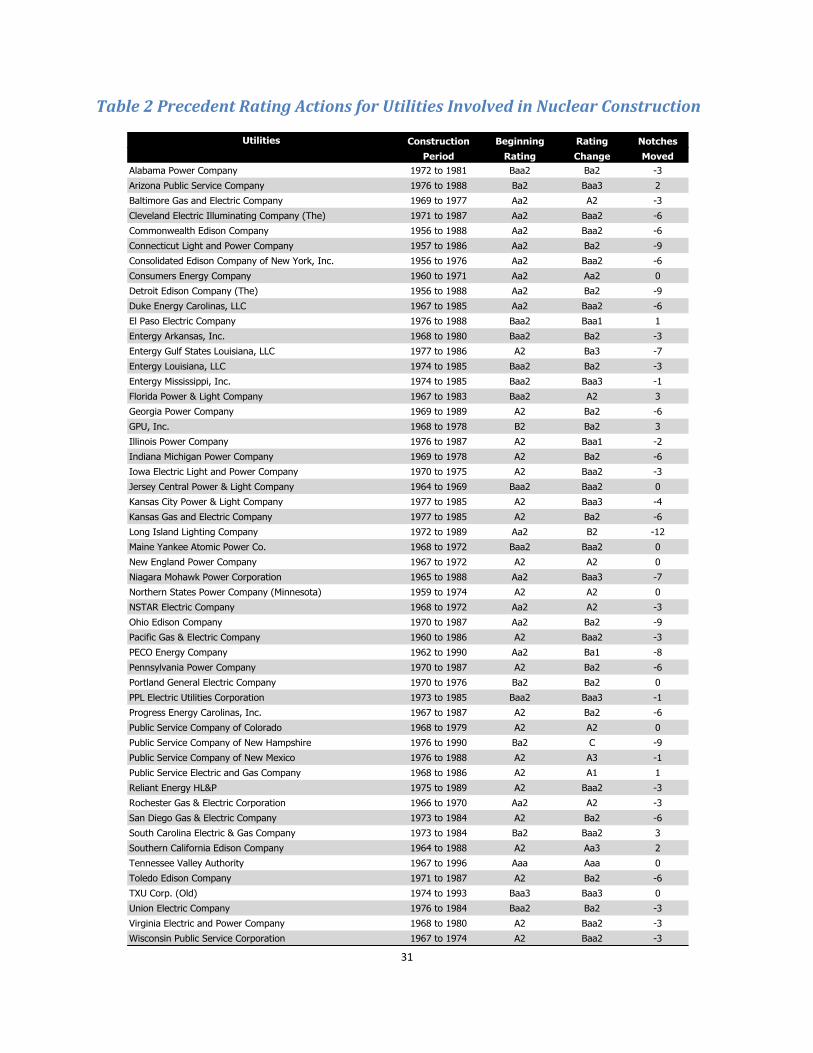

Table 2 Precedent Rating Actions for Utilities Involved in Nuclear Construction ................................... 31

Table 3 Utilities Received Their Lowest Rating While Building Nuclear Plants ....................................... 32

Table 4 Rating Criteria of Agencies and Banks ....................................................................................... 33

Table 5 Moody's Rating Methodology for Electric Utilities ..................................................................... 34

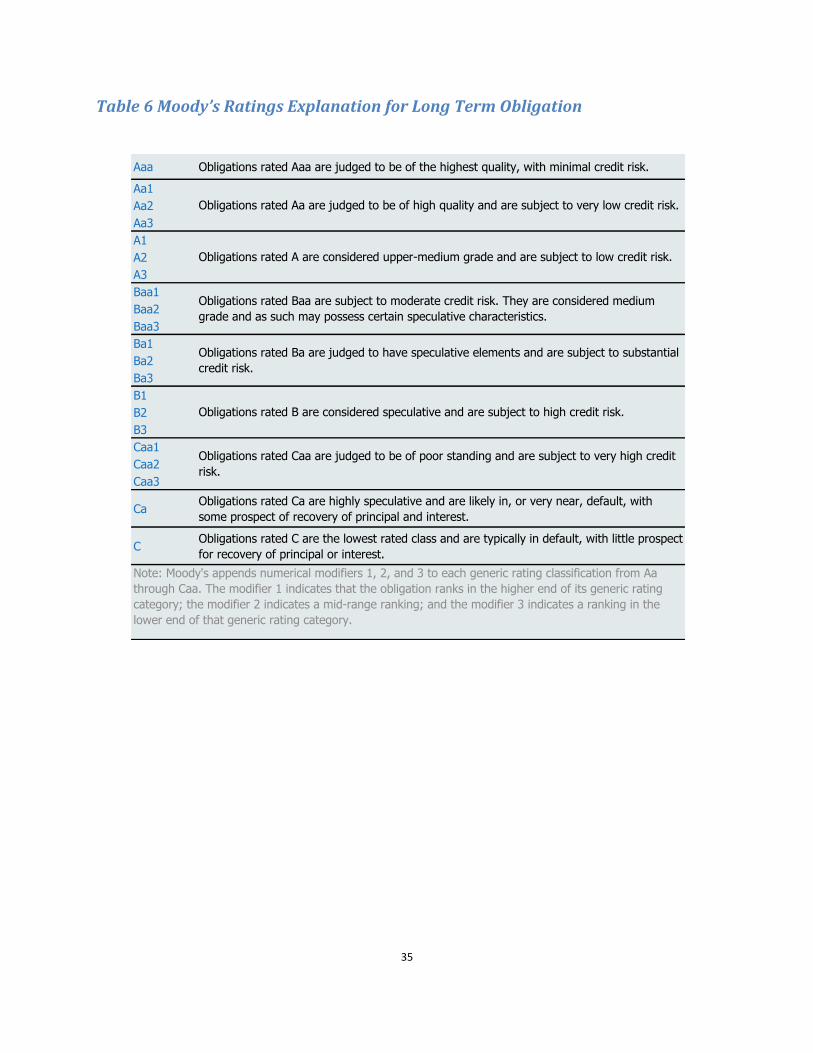

Table 6 Moody’s Ratings Explanation for Long Term Obligation............................................................ 35

Table 7 The Average Cumulative Default Rates for Moody's Credit Ratings in 2007 by % ..................... 36

Definition of Terms ..................................................................................................................................... 37

References .................................................................................................................................................. 38

3

Introduction Recent controversy regarding the credit scores assigned by the Office of Management and Budget to

certain proposed nuclear power projects under the Loan Guarantee program of the Department of

Energy under Title XVII of the Energy Policy Act of 2005 (Title XVII) led us to review the literature

regarding credit risks associated with the announcement, construction, and operation of nuclear power

plants in the United States. We found recent white papers issued by the Nuclear Energy Institute (NEI),

the Congressional Budget Office and the Union of Concerned Scientists, but did not find any significant

academic literature on the subject1. Further, the white papers did not appear to be based upon an

analysis of the experience of investor owned utilities that announced construction of nuclear power

plants in the United States from 1960 to present, but rather seemed to be based upon statistical

information regarding the utility industry as a whole. We felt that we could add to the discussion

underway by providing an analysis based on the credit impact of nuclear plant development on investor

owned utilities in the United States during the period from 1960 to present as represented by a

database provided by Moody’s Investors Service.

Acknowledgements The Texas Institute in partnership with The University of Texas at Dallas would like to thank our

reviewers for their comments: Peter Bradford, Adjunct Professor at Vermont Law School; Mark Cooper,

Director of Research at Consumers Federation of America; and Kenneth Marks, Executive Vice President

at Coalition for Green Capital. A special thanks as well to our authors Monty Humble, Managing Director

of The Texas Institute and Yan Zhang as well as our research team of Dr. Feng Zhao, University of Texas

at Dallas and Jeremy Vickers Program Director of The Texas Institute.

Executive Summary In summary, based upon our examination of the Moody’s database for investor owned utilities that

announced plans to construct nuclear power projects, we found that:

The announcement of an intention to construct a new nuclear facility did not, by itself, result in

credit rating impact or increase risk of default for investor owned utilities operating in the

United States.

Commencement of construction of a new nuclear plant by an investor owned utility operating in

the United States carried an almost 70% probability that the utility would experience a rating

downgrade of uncertain magnitude.

1 Nuclear Energy Institute, Credit Subsidy Costs for New Nuclear Power Projects Receiving Department of Energy (DOE) Loan

Guarantees: An Analysis of DOE’s Methodology and Major Assumptions, NEI White Paper (Washington, D.C.: NEI, September

2010), available at www.nei.org/filefolder/CreditSubsidyCostWhitePaper.pdf. Congressional Budget Office, Federal Loan

Guarantees for the Construction of Nuclear Power Plants (August 2011); and David Schlissel, Michael Mullett, and Robert

Alvarez, Nuclear Loan Guarantees: Another Taxpayer Bailout Ahead? (Cambridge, Mass.: Union of Concerned Scientists

Publications, March 2009).

4

Three (5.8%) of 52 investor owned utilities operating nuclear plants in the United States

defaulted soon after completion of construction as a result of disallowance of construction costs

as imprudently incurred by their state regulators.

Senior secured creditors of defaulting investor owned utilities that operated nuclear facilities in

the United States recovered an average of 83.9% of the amounts owed, considering only the

three nuclear plant operators that defaulted soon after completion of construction.

Based upon the three defaults, the indicated expected cumulative loss to a creditor from a

portfolio of 20 year maturity senior bonds of nuclear plant sponsors would be $1.15 per $1000

in credit extended (using value of principal to calculate percentages, assuming the creditor held

to ultimate resolution of the default, and including only the three described defaults).

Three other utilities that operated nuclear facilities defaulted many years after completion of

construction of the nuclear plants as a result of events unrelated to nuclear plant ownership and

operations.

Senior secured creditors of the six defaulting investor owned utilities that operated nuclear

facilities in the United States recovered a substantial portion of the amounts owed, depending

upon the specific factors taken into account, up to 97.8% (using value of principal to calculate

percentages, assuming the creditor held to ultimate resolution of the default, and including

strategic defaults).

Based upon the six defaults, the indicated expected cumulative loss to a creditor from a

portfolio of 20 year maturity senior bonds of nuclear plant sponsors would be $0.221 per $1000

in credit extended (again, using value of principal to calculate percentages, assuming the

creditor held to ultimate resolution of the default, and including all six defaults).

Based upon these findings, an investor would have been well advised to avoid owning debt of

investor owned utilities during the period immediately following completion of a nuclear power

project.

Methodology Based on historical data supplied by Moody’s Investor Service and additional research from other

sources, we reviewed default events, default rates, and recovery rates for all U.S. investor owned

utilities that were nuclear plant sponsors from 1960 to the present time. We identified all changes in

credit ratings assigned to investor owned nuclear plant sponsors to determine whether there was a

correlation between nuclear plant announcements, construction or operation and rating changes.

Further, we analyzed each of the default events of investor owned nuclear plant sponsors and provide a

brief description of the default event. We studied all default and other negative credit rating events

affecting investor owned nuclear plant sponsors, and examined whether those negative events had

been forecast by Moody’s ratings.

We excluded from our analysis rating events and defaults by federal, state and local government owned

utilities and electric cooperative owned utilities. In the case of government owned utilities, the single

5

default by the Washington Public Power Supply System, although financially significant, was not

statistically significant2. In the case of electric cooperatives, there does not appear to be a publicly

available source that provides sufficiently detailed information regarding total credit extended or credit

losses to permit meaningful analysis, despite that fact that it appears from GAO reports3 that this class

of borrower produced the largest creditor losses of any nuclear plant sponsor class, based upon changes

in balances owed to the United States’ Rural Utilities Service by electric cooperatives during the 1990s.

We also excluded from our analysis debt that had not been assigned a public rating by Moody’s, a factor

that could have had a significant impact on the percentage calculations with respect to probability of

default and recovery because of the large amount of privately placed debt of Energy Future Holdings.

However, we were not able to obtain comparable information regarding privately placed debt with

respect to other nuclear plant sponsors and thus were not able to make meaningful calculations using

the information regarding privately placed debt with respect to Energy Future Holdings alone.

Finally, the significant changes in the structure of the United States wholesale and retail power markets

since the enactment of the Energy Policy Act of 1992, and the adoption of Federal Energy Regulatory

Commission Order 888, and individual state restructuring of electric markets may have implications for

the credit risk associated with nuclear plant development in the future, particularly for entities seeking

to build new reactors in deregulated markets, but we are not aware of any nuclear plants constructed in

the past in the United States that commenced operation in a deregulated power market and thus could

not assess possible ratings impacts, default risks or potential creditor losses in markets where nuclear

power plants would be exposed to wholesale power market competition.

Under the regulatory regime in effect when the previous generation of nuclear plant construction was

undertaken, investor owned utilities were monopolies that controlled generation, transmission,

distribution, and customer services within defined, legally protected, service areas. As a consequence of

dedicating their property to public service, the utilities were required to provide reliable service to all

customers, but were entitled to a rate of return on property prudently acquired that was used or useful

in providing the public service. This rate of return, plus a captive customer base, virtually assured that a

utility would earn enough to repay its creditors, unless it incurred costs imprudently or acquired

unnecessary property. Three of the defaults by owners of nuclear plants that are discussed below

resulted from determinations by regulators that nuclear plant costs had not been prudently incurred.

The remaining three, more recent, defaults all occurred in unregulated markets where utilities are no

longer granted monopolies for generation assets. The absence of regulated monopoly status would be a

significant change in the conditions surrounding a nuclear plant, and we would hesitate to apply our

findings discussed herein to such a changed environment without further research. We believe that our

research continues to be applicable to traditionally regulated utility markets.

2 in at least one case, a municipal utility was relieved of its obligations with respect to a nuclear power plant through an

agreement with the investor owned utility sponsor of the plant during the investor owned utility’s bankruptcy proceedings.

3 Federal Electricity Activities: The Federal Government’s Net Cost and Potential for Future Losses (GAO/Al&ID-97-110,

September 19,1997).

6

Analysis of Credit Rating Impact of Nuclear Plant Development

Significance and Definition A credit rating is a formal opinion given by a rating agency of the potential default risk faced by investing

in a particular issue of debt securities. Moody's is one of the three general purpose nationally

recognized statistical rating organizations in the U.S. (See Table 7 for Moody's definition of rating scale).

The rating process begins when a rating agency receives a formal request from an entity planning to

issue a bond. The request for a rating is made because without one, it would be difficult for the entity to

market a bond issue to the public. Once a credit rating is assigned, the rating agency monitors the credit

quality of the issuer and can reassign a different credit rating to the bond. An "upgrade" occurs when

there is an improvement in the credit quality of an issue; a "downgrade" occurs then there is

deterioration in the credit quality of an issue. A downgrade of an issue or issuer may increase the credit

spread and result in a decline in the market price of the issuer's bonds.

Conclusion From a credit perspective, the risks of building new nuclear plants are notable, entailing significantly

higher operating risk, with very high capital costs, and vulnerability to potential shifts in energy policy.

Historically, 69% nuclear power project sponsoring utilities suffered rating downgrades while building

these facilities and 52% of the nuclear power sponsors received their lowest rating during the

construction period.

Technical Summary and Charts As shown in Exhibit 1, 69% of investor-owned utilities suffered rating downgrades while constructing

nuclear power plants. Of 52 utilities that completed nuclear plants (operating and shutdown, but not

including test sites) during their construction period, seven utilities received rating upgrades, nine

utilities were unchanged and the other 36 suffered downgrades.

Exhibit 1: Rating migrations for IOUs while constructing nuclear power plants

The issuers on average fell 3 credit rating notches and the issuer with the greatest rating change, Long

Island Lighting Company, fell 12 notches, from Aa2 in 1972 to B2 in 1984. All of these ratings were

evaluated on Moody’s assigned issuer rating, which is the issuer’s senior long term debt rating using the

update algorithm.

Upgraded No change Downgraded

7 9 36

13% 17% 69%

7

We define a utility’s nuclear plant construction period as from the date a construction permit was issued

to the date of commercial operation. We examined the data from 1960 to February 2011 and discovered

that half (52%) of the nuclear power sponsors received their lowest rating during their nuclear plant

construction period. The average length of time needed to build a nuclear power facility is 104.6

months, which is approximately 17% of the time period reviewed.

Exhibit 3: Half of IOUs received their lowest rating during nuclear plant construction period

There were 46 utilities that eventually canceled at least one of their planned nuclear reactors. Eight of

those utilities canceled their only planned reactor. That is, these 8 utilities merely announced plans to

build nuclear plants but did not receive a construction license to begin any nuclear plant construction.

The credit rating trend for these 8 utilities is normal, although the small sample size prevents statistically

meaningful conclusions.

Exhibit 4: Rating trends for utilities which announced nuclear power plant construction

0

2

4

6

8

10

12

Exhibit 2: Rating changes during last nuclear building cycle

Average Construction length 105 Months Lowest Rating Received 27

Data scope from 1960 to 2011 615 Months Total Utilities 52

17% 52%

8

Historical data suggests that nuclear power announcements did not necessarily bring negative rating

impact on sponsors, but the actual construction activities did increase ratings pressure on sponsors.

This is consistent with the hypothesis that very large capital expenditures required for nuclear power

plant construction combined with the uncertainty associated with the last nuclear plant construction

cycle would materially increase the sponsor’s operating risk in the view of rating agencies (See rating

criteria for rating agencies and banks in Table 5 of Appendix).

A further specific examination on Moody's rating methodology of regulated electric utilities and

unregulated electric utilities (Table 6 of Appendix) clearly illustrates that although nuclear power

construction may enjoy some political and regulatory support, the issuer's rating would be seriously

affected by a number of other factors, especially the financial metrics. The multi-billion size of the

investments and sizeable sunk costs could undoubtedly introduce material financial distress for almost

any issuer. These impacts could overcome regulatory support in the form of rate of return regulation

and service area monopolies, as well as tax incentives and other financial support available as a result of

the job creation and tax base expansion likely to result from new nuclear plant construction.

Default Events of Nuclear Power Sponsors

Significance and Definition Here we use the same definition for default as Moody’s Default Risk Service and its other risk

management products. Moody's definition of default includes three types of credit events:

A missed or delayed disbursement of interest and/or principal, including delayed payments

made within a grace period

Bankruptcy, administration, legal receivership, or other legal blocks (perhaps by regulators) to

the timely payment of interest and/or principal

A distressed exchange occurs where: (i) The issuer offers debt holders a new security or

package of securities that amount to a diminished financial obligation (such as preferred or

common stock, or debt with a lower coupon or par amount, lower seniority, or longer maturity);

or (ii) the exchange had the apparent purpose of helping the borrower avoid default.

Upgrade No change Downgrade

Completed 7 9 36

13% 17% 69%

Canceled 2 3 3

25% 38% 38%

9

Conclusion Six investor owned utilities that sponsored nuclear power projects have defaulted on debt rated by

Moody’s4 since 1960. None of the defaulting utilities was liquated, and two of these defaults can be

characterized as strategic defaults. We define a strategic default as one initiated by a borrower that is

capable of servicing its indebtedness as it comes due, but chooses to default in order to address other

liabilities. In these cases, because the debtor defaults when it still has substantial resources, the likely

outcome is payment in full for the senior creditors once the other liability issues have been resolved.

Technical Summary and Charts Based upon a review of available sources, no investor owned utilities that announced plans to build a

nuclear reactor, but abandoned the plans prior to commencement of construction experienced a

default. Further, it does not appear that any investor owned utility that commenced construction of a

nuclear reactor experienced a default prior to completion of construction of the nuclear reactor, despite

substantial construction delays and cost overruns for a number of nuclear projects.

The absence of defaults during plant construction and the three defaults that occurred shortly following

plant completion merits some discussion. As stated in the introduction, at the time that nuclear plant

construction was commenced in the United States, utilities were permitted monopolies in their service

areas, but their rates were regulated. The utilities were generally allowed to charge their customers an

amount that was expected to provide for their cost of providing service plus a return on the assets that

were used or useful in providing service to customers, limited by a requirement that the costs be

prudently incurred. Assets under construction were not permitted to earn a rate of return until they

were placed in service. Instead, utilities funded debt service on assets under construction by borrowing

additional amounts, so that no utilities defaulted during construction since they continued to borrow to

pay debt service. When construction was completed, nuclear plant owners sought to increase their

charges to customers to recover a return on the nuclear plant investments. In a number of cases, the

utility regulators concluded that nuclear plant construction costs had not been prudently incurred and

denied the utilities permission to recover the imprudently incurred costs. The three utilities that

defaulted shortly after completion of nuclear plants lacked other resources (either shareholder equity or

revenues from other sources) from which to pay debt service on the disallowed costs and defaulted as a

result.

There were six investor owned utilities that experienced defaults during the period of nuclear plant

ownership. The three most recent of those defaults, however, occurred for reasons that appear to be

substantially unrelated to their nuclear plant ownership. In particular, both Pacific Gas & Electric

Company (PG&E) and Southern California Edison defaulted in 2001 as a result of the disastrous effects of

a California law deregulating the wholesale electricity industry. The law was viewed in hindsight as

4 As stated above, we limit our analysis to debt covered by the Moody’s database. That would exclude most privately placed

debt, as well as most high yield debt because many high yield (or junk) debt issues do not seek a credit rating from Moody’s.

We are aware of at least one bankruptcy by an issuer of unrated bonds related to the Seabrook nuclear project, as well as one

case where Public Service New Hampshire while in bankruptcy assumed the power purchase obligations of a municipal utility.

10

having been flawed, and the implementation scheme was subject to manipulation by power marketing

companies who earned substantial profits at the expense of the utilities. The last case involved Energy

Future Holdings, which has vigorously denied that its voluntary exchange of debt instruments with its

creditors constituted a default at all. We treat it as a default because Moody’s has classified it as a

default. However the event is classified, its cause is the leveraged buyout of Texas Utilities in 2007, and

the significant decline in natural gas prices in the Energy Future Holdings service area since mid-2008,

not nuclear plant operations, which have continued in the same manner since Comanche Peak came on

line in the early 1990s.

Exhibit 5: Default events for nuclear power sponsors

The 52 utilities that undertook nuclear projects issued a total of $239 billion in senior secured debt and

$286 billion in senior unsecured debt during the study period. Not all of this debt was outstanding at

any one time, but all of it could potentially have been the subject of a default by the issuer of the debt.

For the same reason that we include all defaults that occurred in the period from 1960 to 2011, we

include the principal amount of all debt issued by investor owned utilities that owned nuclear plants

during the relevant period in our calculations.

Exhibit 6: Senior debt issued by nuclear power sponsors from 1960 to 2011

Nuclear Power SponsorsDefault

TimeDefault Type Resolution Type

1 El Paso Electric Company 1/8/1992 Chapter 11 Emerged from Chapter 11

2 Energy Future Holdings Corp. 8/17/2010 Distressed exchange

3 Pacific Gas & Electric Company 4/6/2001 Chapter 11 Reorganization plan confirmed

4Public Service Company of New

Hampshire1/28/1988 Chapter 11 Emerged from Chapter 11

5 Southern California Edison Company 1/16/2001Missed principal and

interest paymentsCreditors paid in full

6Yankee Companies, Incorporated,

The6/30/1987

Missed interest

payment

Decade Sr. Secured Sr. UnSecuredTotal

(in $million)

1960's 304 91 $395

1970's 2,499 - $2,499

1980's 49,608 15,351 $64,959

1990's 86,616 62,449 $149,065

2000's 90,206 191,966 $282,172

2010's 9,851 15,986 $25,837

Total (in $million) $239,084 $285,843

11

The six utilities that experienced a default constituted 11.5% of all nuclear plant sponsors, and their

$14.8 billion in senior debt, both secured and unsecured, outstanding at the time of default constituted

2.82% of all senior debt issued by investor owned utilities that sponsored nuclear plants in the United

States. If we exclude the three defaults by nuclear plant sponsors that do not appear to be related to

nuclear plants, 5.8% of all issuers, and 0.32% of all senior debt issued by investor owned utilities that

sponsored nuclear plants in the United States experienced a default.

Exhibit 7: Default amount of nuclear power defaulters

Compared to the observation on the larger class of global corporate issuers5, bankruptcy played a

significant role for nuclear power sponsors, accounting for 50% of initial defaults. El Paso Electric, PG&E

and Public Service Company of New Hampshire filed Chapter 11 and emerged from bankruptcy.

Southern California Edison and The Yankee Companies repaid their creditors in full following defaults,

but did not file bankruptcy. None of the defaulting utilities was liquidated, reflecting the traditional

monopoly status accorded to electric utilities and the essential nature of providing electric service to the

public, both of which made continued operation of the enterprise assets, rather than liquidation, the

preferred outcome of bankruptcy cases.

Exhibit 8: Default type of nuclear power sponsors

5 " Corporate Default and Recovery Rates, 1920-2007", February 2008

Default NumberDefaulted Senior Debt

(in $million)

Nuclear Power Defaulters 6 $14,783

11.5% 2.82%

Default due to

Nuclear Operations3 $1,700

5.8% 0.32%

12

Rating Transition Rates for Nuclear Power Investor Owned Utilities

Significance and Definition Consider a simple rating system with two rating classes A and B, and a default category Default. The

transition matrix for this rating system is a table listing the probabilities that a borrower rated A at the

start of a period has rating A, B or Default at the end of the period.

Exhibit 9: Structure of a transition matrix

Rating at end of period

A B Default

Rating at start of period

A Probability of Staying in A Probability of Migrating to B Probability of Default from A

B Probability of Migrating to A Probability of Staying in B Probability of Default from B

Rating agencies use a cohort approach to estimate transition probabilities through historical transition

frequencies. We also apply the cohort approach here to create a benchmark to evaluate the nuclear

power sponsors' performance.

Conclusion Although the rating system of nuclear power investor owned utilities is extremely stable, the inadequate

forecast for the two strategic defaults raises doubts with respect to the predictive power of Moody's

ratings.

0%

10%

20%

30%

40%

50%

60%

Global Corporate Issuers1970-2007

Nuclear Power Sponsors1960-2011

Distressed Exchange Bankruptcy Payment Default

13

Technical Summary and Charts The following table illustrates one year rating transition rates for all investor owned utilities during 1960

to present.

Since our data in the study period only has 52 issuers and has very limited C ratings samples, our

discussion is mainly focused on A and B classes. The one year rating transition matrix reflects two

findings:

First, the rating system of nuclear power investor owned utilities is extremely stable: their on-diagonal

entries are the highest, ranges from 72% to over 98%, and their ratings withdrawal rates are the lowest.

It illustrates that, compared to the larger class of regulated utilities6 or even to the largest class of all

nonfinancial corporations7, a relatively higher percentage of nuclear power sponsors remained at their

original rating and a lower percentage of nuclear power sponsors experienced a rating withdrawal.

Exhibit 10: Comparison of rating system for Nuclear IOUs, Regulated utilities and all corporations

Second, default frequencies for the best two rating classes are zero. This is consistent with their high

rating classes, since the default event for an Aaa or Aa class in a one year horizon is very rare. Due to the

two 2001 strategic defaults (PG&E and SCE), however, the A class default rate, 0.18% (compared to

0.003% to 0.037% for A rated category in Table 9), is abnormally high. Because most of nuclear power

sponsors are A rated or Baa rated, the result raises questions regarding the efficacy of Moody's rating

6 According to Moody’s, "Regulated electric and gas companies are a diverse universe in terms of business model (ranging from

vertically integrated to unbundled generation, transmission and/or distribution entities) and regulatory environment (ranging

from stable and predictable regulatory regimes to those that are less developed or undergoing significant change). " Our study

included regulated electric and gas utilities and excluded regulated electric and gas networks (companies primarily engaged in

the transmission and/or distribution of electricity and/or natural gas that do not serve retail customers). Municipal utilities and

electric cooperatives were also excluded.

7 " Corporate Default and Recovery Rates, 1920-2010" February 2011

1 Year Rating Transition Rates, 1960-2010

Aaa Aa A Baa Ba B Caa Ca-C Default WR

Aaa 98.04% 0.00% 1.96% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Aa 0.00% 90.67% 9.00% 0.33% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

A 0.09% 0.98% 92.64% 5.41% 0.35% 0.00% 0.18% 0.00% 0.00% 0.35%

Baa 0.00% 0.18% 3.78% 91.61% 3.87% 0.00% 0.09% 0.00% 0.00% 0.46%

Ba 0.00% 0.00% 0.29% 13.91% 82.03% 2.32% 0.58% 0.00% 0.00% 0.87%

B 0.00% 0.00% 0.00% 0.00% 20.45% 72.73% 2.27% 0.00% 2.27% 2.27%

Caa 0.00% 0.00% 0.00% 0.00% 33.33% 0.00% 44.44% 11.11% 11.11% 0.00%

Ca-C 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 50.00% 50.00%

Nuclear Power IOUs Regulated Utilities Nonfinancial Corporations

On-diagonal 72.7% to 98.0% 60.5% to 89.7% 74.2% to 86.6%

WR rate 0.4% to 2.2% 2.4% to 5.2% 4.7% to 10.7%

Rating Stablility Very Stable Stable Normal

14

system. The effect lasts for a long time. From exhibit 11, we can observe that the A class’s average

cumulative default rate is much higher than the lower class Baa’s average cumulative default rate. For

example, at a 20 year horizon, the average cumulative default rates for A rated utility is 1.95% verse

0.87% for Baa rated.

Exhibit 11: Average cumulative default rates for A-rated verse Baa-rated class

Historical Default Rates for Investor Owned Utilities

Significance and Definition In this section we compared our result with the default rates of all regulated utilities in Moody's

research report.

Conclusion Comparing our result to Moody's recent research report8, both the default rates of A rated nuclear

power investor owned utilities and Baa rated nuclear power investor owned utilities are lower than that

of all regulated utilities. No investor owned utilities experienced a default during the construction

period for a nuclear power project, although several experienced defaults immediately following

construction as a result of disallowance of cost recovery by regulators based upon the regulators’

findings that construction costs had been imprudently incurred .

Technical Summary and Charts Exhibit 12: Comparison for default rates between nuclear power IOUs and all regulated utilities

8 " Default, Recovery, and Credit Loss Rates for Regulated Utilities, 1983-2008", May 2009

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

A-rated IOUs has higher default rates than Baa-rated class

A rated IOUs Baa rated IOUs

15

When we remove the limitation of specific rating category, and then examine all nuclear power issuers

during the study period, the cumulative default rates of Nuclear Power sponsors appear to be much

lower than that of all regulated utilities.

Exhibit 13: Cumulative default rates for all rated issuers

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Default Rates for A-rated Nuclear power IOUs are low relative to A-rated Regulated Utilities

Nuclear Power IOUs Regulated Utilities

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Default Rates for Baa-rated Nuclear power IOUs are low relative to Baa-rated Regulated Utilities

Nuclear Power IOUs Regulated Utilities

16

If we exclude Energy Future Holdings, Southern California Edison and PG&E, each of which can be

argued to have defaulted for reasons completely unrelated to ownership of a nuclear facility, the

cumulative default rates come back to normal. The 20 year default rate of Baa rated utilities that own

nuclear projects is below 1.00%, this result is significantly lower than the comparable assumption of

Appendix C in Moody’s regulated utilities report.

Exhibit 14: Assume Energy Future Holdings, SCE and PG&E not default

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Default Rates for All-rated Nuclear power IOUs are low relative to All-rated Regulated Utilities

Nuclear Power IOUs Regulated Utilities

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

1.00%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Default due to nuclear plant operations

A rated IOUs Baa rated IOUs

17

Rating Dynamics of Nuclear Power Defaulters

Significance and Definition We examined the characteristic of rating dynamics for all nuclear power defaulters.

Conclusion As illustrated in the following exhibit 15, nuclear power sponsors appear to default at relatively high

rating levels.

Technical Summary and Charts Exhibit 15: Rating changes prior default

At Default 1 month 6 months 1 year 2 years 3 years Default Date

El Paso Electric Company Ca B2 B1 Ba3 Ba3 Baa1 1/8/1992

Energy Future Holdings Corp. Caa2 Caa2 Caa2 Caa1 B3 8/17/2010

Pacific Gas & Electric Company Caa2 Caa2 A2 A2 A2 A2 4/6/2001

Public Service Company of New Hampshire C C Caa2 Caa2 Caa2 Caa2 1/28/1988

Southern California Edison Company Baa3 A2 A2 A2 A2 A2 1/16/2001

Yankee Companies, Incorporated, The Caa2 Caa2 B2 6/30/1987

Time Prior to DefaultDefaulter

3 years 2 years 1 year 6 months 1 month At Default

Rating Dynamics of Nuclear Power Defaulters

InvestmentGrade

Near Default

YankeeEnergy Future

Hampshire

El Paso

PG&E

SCE

18

Within 6 months prior to default, only two of these six defaulters (Energy Future Holdings Corp. and

Public Service Company of New Hampshire) had been downgraded to C grade; Pacific Gas & Electric

Company and Southern California Edison Company were even in an investment grade category, A2.

The high likelihood of unexpected strategic default definitely increases default risk of sponsors, and

probably would suggest that rating agencies should consider exogenous event risk (e.g., changes in

regulatory scheme) on investor-owned utilities in the future.

Default Experience for Preferred Stock

Significance and Definition Just as issuers may miss interest or principal payments on loans or bonds, they may also miss dividend

payments on preferred stock as well. Although preferred stock ranks below debt in a firm’s capital

structure, it usually has a number of debt-like characteristics. A dividend omission is also a significant

negative credit event.

Conclusion Historical statistics show that sponsors usually would receive a rating downgrade followed within a very

short period by a dividend omission of preferred stock. The extent of downgrade was about 1 to 2

notches.

Technical Summary and Charts Exhibit 16: Impairments for nuclear power sponsors

Based on Moody’s research report9, 45% dividend omissions of preferred stock (50 out of 110 dividend

omissions from 1983 to 2007) were followed by bond defaults. Within the scope of our study, El Paso

Electric Company and Public Service Company of New Hampshire are two of these five dividend

omissions (40%) followed by bond defaults.

9 " Corporate Default and Recovery Rates, 1920-2007", February 2008

Default_IssuerDividend

Omission

Distressed

ExchangeChapter 11

Missed

Payments

1 El Paso Electric Company √ √

2 Energy Future Holdings Corp. √

3 Entergy Gulf States Louisiana, LLC √

4 Entergy Louisiana, LLC √

5 Long Island Lighting Company √

6 Pacific Gas & Electric Company √ √

7 Public Service Company of New Hampshire √ √

8 Southern California Edison Company √

9 Yankee Companies, Incorporated, The √

Impairment Type

19

Exhibit 17: Rating changes followed by dividend omission

Historical statistics show that sponsors usually would receive a rating downgrade followed within a very

short period by a dividend omission of preferred stock. The extent of downgrade was about 1 to 2

notches.

Risk of Loss to Creditors

Significance and Definition An objective of this study is to describe the characteristics of nuclear power bond defaults in the U.S.

The most important attribute is the amount lost if an issuer defaults. For management of utilities and

investors in nuclear power sponsors, improved understanding of losses enables them to make better

decisions, to allocate capital more efficiently, and to obtain more accurate estimates of valuations of

existing debt. For government agencies, the benefit is a more informed decision about perspective

credit subsidy costs.

Conclusion While the rating impact of nuclear plant construction is significant for both investor owned utility

managers and investors, the risk of loss of principal is the ultimate concern for creditors.

Technical Summary and Discussion An often used methodology for measuring loss to creditors given default assumes that the creditor exits

the defaulted investment within 30 days following the default event. This is consistent with the

behavior of many investors in debt securities, and may be valuable information to those investors. We

analyzed the consequences of defaults using this method, but we also attempted to assess the ultimate

recovery for the creditor if the creditor held the debt instrument through the resolution of any

subsequent reorganization of the debtor, which is more likely to model the behavior of a guarantor such

as the United States government under the Title XVII loan guarantee program currently available to

sponsors of the construction of a limited number of new nuclear facilities.

Dividend Omission DownGrade Within Rating Changes Notches

El Paso Electric Company Y 2 weeks B1 to B2 -1

Entergy Gulf States Louisiana, LLC Y immediately Ba3 to B1 -1

Entergy Louisiana, LLC Y 1 week Ba1 to Ba3 -2

Long Island Lighting Company N

Public Service Company of New Hampshire Y 3 days B3 to Caa2 -2

20

Value-Weighted Ultimate Recovery Rates

Significance and Definition “Ultimate recoveries" refer to the recovery values that creditors actually receive at the resolution of a

default, usually at the time of emergence from Chapter 11 bankruptcy proceedings.

Conclusion The aggregate ultimate recovery rate for all six nuclear power defaulters are similar to all regulated

utilities, however, the ultimate recovery rate for the three utilities that defaulted due to nuclear plant

ownership is much lower.

Technical Summary and Charts Based upon the three cases where investor owned nuclear plant operators have experienced a default

attributable to disallowance of construction costs, the experience of creditors of nuclear plant operating

investor owned utilities is significantly worse than the experience of all bankrupt regulated utilities, with

creditors recovering only about 83.9% of the amounts owed. Based upon the six cases where investor

owned nuclear plant operators have experienced some form of default, the ultimate recovery rate by

creditors has been reasonably consistent with the experience of creditors of all bankrupt regulated

utilities, 98.5% for all defaulting regulated utilities versus 97.8% for those that operated nuclear plants.

However, there is certainly room for debate whether the three defaults not directly related to nuclear

plant operations should be excluded from the analysis, since defaults always arise from events that were

likely unexpected, at least by the creditor, at the time that the credit was extended. It may be most

reasonable to use the limited three default universe as a guide to decision making by utilities

considering nuclear plant ownership, since those three defaults seem to be attributable to nuclear plant

ownership, but to use the six default universe as a guide for potential guarantors because the guarantor

must also consider default risks beyond those related to nuclear plant ownership.

Exhibit 18: Ultimate recovery rate for nuclear power sponsors

21

Nuclear Power SponsorsDefault

TimeDefault Type

Ultimate

Recovery

El Paso Electric Company 1/8/1992 Chapter 11 98.33%

Energy Future Holdings Corp. 8/17/2010 Distressed exchange N/A

Pacific Gas & Electric Company 4/6/2001 Chapter 11 100%

Public Service Company of New

Hampshire1/28/1988 Chapter 11 77.41%

Southern California Edison

Company1/16/2001

Missed principal and

interest payments100%

Yankee Companies, Incorporated,

The6/30/1987 Missed interest payment N/A

Average for all defaulted IOUs 97.8%

Average for defaults due to nuclear operations 83.9%

98.5% 97.8%

83.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Regulated Utilities1983-2009

Nuclear Power1960-2010

Defaults due to Nuclear Operations

Ultimate recovery

22

Creditor Loss Using 30 Days Post Default Trading Price

Significance and Definition The data available in Moody’s DRD allows us to analyze bond losses for all nuclear power sponsors

during the period of 1960 to 2010. LGD (loss given default) is defined as the 30 day post default trading

price, expressed as a percentage of par value.

Conclusion Only the two strategic defaulters (PGE and SCE) have recovery rates comparable with the class of

regulated utilities. Creditors of the remaining defaulters suffered much greater losses following the

default.

Technical Summary and Charts The definition of LGD applied to the unique set of nuclear power utilities defaults yields a loss given

default of 29.7%. In other words, based on past experience, an investor who sells its holdings of bonds

issued by a defaulting nuclear plant owner should expect to recover, on average, 70.3% of the default

amount for nuclear power bonds, specifically, 75.1% for senior secured bonds and 59.0% for senior

unsecured bonds. If we use value weighted recovery rate instead of issuer weighted recovery rate, a

more accurate estimate is 82.5% for senior secured bonds and 62.8% for senior unsecured bonds.

Exhibit 19: Comparison between nuclear power sponsors and all Moody's corporate issuers

In comparison with the larger class of Moody’s corporate issuers, we have two observations. First, the

recovery rate of nuclear power utilities is significantly higher than that of the broad class. Second, due to

the huge debt amount of nuclear power utilities, the difference between value weighted recovery rate

and issuer weighed recovery rate is also significant.

The difference between value weighted recovery rate and issuer weighted of nuclear power sponsors is

greater than that of all corporate issuers. That is because the defaulted amount is unevenly distributed

among all six defaulters. From the following exhibit 20, the two 2001 strategic defaults (PG&E and SCE)

involved defaults with respect to senior securities totaling $11.6 billion, which is two-thirds of all

defaulted debts. A strategic default is the decision by a borrower to default (i.e. stop making fixed

payments) on a debt despite having the financial ability to make the payments. Not surprisingly, the

creditors affected by these defaults had very high recovery rates, since the defaulting debtors had the

ability to repay their creditors.

Exhibit 20: Defaulted amount and type of defaulted debt

Corporate Issuers Nuclear Power Corporate Issuers Nuclear Power

1983-2010 1960-2010 1983-2010 1960-2010

Sr.Secured Bond 50.8% 75.1% 49.1% 82.5%

Sr.UnSecured Bond 36.7% 59.0% 37.4% 62.8%

Lien Position

Issuer-Weighted Value-Weighted

23

Exhibit 21: Recovery rates if we assume PG&E and SCE do not default

Above exhibit 21 shows that if we assume PE&G and SCE had not defaulted in 2001, as well as Energy

Future Holdings Corp. had not defaulted in 2010, nuclear power utilities still outperform the largest class

of all corporate issuers in the senior secured bonds. But how did they perform against the comparable

class of regulated utilities?

Exhibit 22: Comparison for nuclear power sponsors without strategic bankruptcies

Actually nuclear plant ownership does not necessarily guarantee more "senior security" to the issuer.

Only the two strategic defaulters have comparable performance of recovery rate against the bigger class

of regulated utilities. Other nuclear power “normal” defaulters suffered much bigger losses than their

peer companies. The above table shows that nuclear power defaulters without the 2 strategic defaults

only recovered 68.0% of Senior Secured Bonds and 43.9% of Senior Unsecured Bonds, which is much

lower than regulated utilities did.

$million

Company NameDefaulted

Amount

Senior

Secured

Senior

Unsecured

Senior

Secured

Senior

Unsecured

El Paso Electric Company $665.64 62.05% 56.27%

Energy Future Holdings Corp. $3,593.86 61.80% 62.18%

Pacific Gas & Electric Company $5,910.29 83.59% 61.33% 83.52% 60.87%

Public Service Company of New

Hampshire$1,420.88 70.79% 36.76% 79.01% 33.91%

Southern California Edison Company $5,709.40 86.73% 73.07% 87.35% 73.23%

Yankee Companies, Incorporated,

The$45.00 85.00% 85.00%

Issuer-Weighted Value-Weighted

Corporate Issuers Defaults due to Corporate Issuers Defaults due to

1983-2010 Nuclear Operations 1983-2010 Nuclear Operations

Sr.Secured Bond 50.8% 68.0% 49.1% 71.7%

Sr.UnSecured Bond 36.7% 36.8% 37.4% 33.9%

Lien Position

Issuer-Weighted Value-Weighted

Corporate Issuers Regulated Utilities Nuclear Power Nuclear Power W/O

1983-2010 1983-2009 1960-2010 Strategic Bankruptcy

Sr.Secured Bond 50.8% 83.7% 75.1% 68.0%

Sr.UnSecured Bond 36.7% 67.8% 59.0% 43.9%

Lien Position

Issuer-Weighted

24

Discussion Regarding Risk of Loss to Creditors The risk of loss to a creditor advancing funds to a sponsor of a proposed nuclear facility is a union of two

probabilities—first that the debt will default, and second that there will be a loss arising from that

default. As discussed above, the universe of defaulting nuclear plant sponsors is small and half of the

sponsors in that universe can be said to have defaulted for reasons unrelated to the fact that they were

sponsors of nuclear plants. That said, those defaults did occur, and illustrate real risks that face

creditors who advance funds to utilities, so we believe that the better side of the argument is that there

are six nuclear plant sponsoring utilities who have defaulted in the 51 year study period, roughly 11% of

the total. We also believe that since a sponsor default typically affects all of the debt issued by a

sponsor, it is appropriate to calculate the percentage risk to a creditor that the creditor’s portfolio of

debt instruments will be affected by a default using an average weighted by the dollar amounts of

defaulted debt.

Over our 51 year study period, the risk of default in any single year would be calculated to be around

0.17% or 0.0017. For a 20 year debt instrument, the cumulative risk would be around 1.00%. Now,

having concluded that we should include all six defaulting utilities in our calculation of risk of default, we

also conclude that we should include all six in our calculation of risk of loss, given default. Also, we

choose to use the ultimate recovery method for determining risk of loss, rather than 30 days post

default trading price methodology because we are more interested in assessing the question from the

perspective of a guarantor who guarantees payment, not one that indemnifies against risk of market

loss. Using that method, we derive a probability of loss given default of (1-0.978), or 2.2%.

83.7%

75.1%

68.0%67.8%

59.0%

43.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Regulated Utilities

1983-2009

Nuclear Power

1960-2010

Nuclear Power W/O

Strategic Bankruptcy

Sr.Secured Bond

Sr.UnSecured Bond

25

The product of these two probabilities is 0.000221, or 0.0221%, yielding an expected cumulative loss to

the creditor from a portfolio of 20 year maturity bonds issued by nuclear plant sponsors of $0.221 per

$1,000 in credit extended.

If we limit our analysis to those cases that clearly arise from nuclear plant ownership (i.e., we exclude

PG&E, SCE and Energy Future Holdings from the analysis), the expected portfolio loss rate is higher. The

one year probability of default on a principal weighted basis falls to 0.1%, and the 20 year probability of

default on a principal weighted basis falls to 0.71%. However, the risk of loss to senior secured creditors

given default rises to 16.1%, and the product of the two probabilities is thus increased to 0.114%, or a

cumulative loss expectation to the holder of a portfolio of 20 year maturity bonds issued by nuclear

plant sponsors of $1.15 per $1,000 invested.

We have not attempted to adjust this loss expectation to reflect the present value of losses based upon

the likelihood that loan losses will occur at particular points in the life of the loan. We do not believe

that the available data would support an attempt to refine the analysis to this level.

Condensed Information Regarding Specific Default Events of US Utilities

with Nuclear Operations

1) El Paso Electric Company, January 8, 1992

Created in 1901, El Paso Electric generates and provides electricity to approximately 250,000 customers

in El Paso and the Rio Grande Valley in Texas and in southern New Mexico. The company faced a

liquidity crisis directly related to its heavy investment in the Palo Verde Nuclear Generating Station in

Arizona. Development costs exceeded estimates considerably due to the unfamiliarity of management

with this type of project and changes in government regulations, primarily in reaction to the incident at

the Three Mile Island nuclear plant. Subject to regulations on rates enacted by the Public Utility

Commission of Texas (PUCT), the company was not allowed to include the total costs of its investment in

Palo Verde in determining its rates. Given the $550 million plus of debt obligations due at the end of

1991, El Paso was forced to restructure its debt. As a part of its restructuring plan, the company

requested a $131 million increase in rates in July 1991 from the PUCT. Although the Commission

subsequently ordered a $52 million increase, the increase was insufficient for El Paso Electric to meet its

obligations, and the company filed for bankruptcy protection.

Time Event_Description

9/19/1991 Annouced that it will not pay preferred stock dividends due 10/1/91

10/1/1991 Dividend omission

1/8/1992 Filed for Chapter 11 bankruptcy protection

9/8/1992 Filed reorganization plan

11/18/1992 Reorganization plan approved by bankruptcy court

2/12/1996 Emerged from bankruptcy

26

2) Energy Future Holdings Corp., August 17, 2010

On August 17, 2010, Energy Future Holdings Corp. successfully completed a debt restructuring of its

10.875% Senior Notes due 2017 and its 11.25% / 12.00% Senior PIK Toggle Notes due 2017. EFH

exchanged in aggregate principal amount approximately $1.428B of the 10.875% Senior Notes and

$2.166B of the 11.25% / 12.00% Senior PIK Toggle Notes for $2.18B of new 10.00% Senior Secured Notes

due 2020 issued by Energy Future Intermediate Holding Company, LLC and $499.7mm in cash. The

completion of the exchange effectively allowed EFH to reduce its overall net debt by approximately

$1.0B and to extend a portion of its maturities. Given the company’s very weak financial profile,

untenable capital structure, questionable long-term business plan, material operating headwinds, and a

loss of approximately 30% for investors who participated in the exchange, Moody’s views the

transaction as a distressed exchange, which is tantamount to default. Energy Future Holdings Corp.

generates, transmits, and distributes electricity in the greater north Texas region. EFH has two primary

operating subsidiaries: Oncor Electric Delivery Company, LLC and Texas Competitive Electric Holdings

Company, LLC.

3) Pacific Gas & Electric Company, April 6, 2001

On April 6, 2001, Pacific Gas & Electric Company filed for Chapter 11 following the company's inability to

reach consensus with government officials and regulators concerning the recovery of approximately $9

billion of under-collections related to the wholesale power market. In 1996, California was the first state

to deregulate its wholesale electricity market, while continuing to regulate retail electric rates. Under

the deregulation program (now widely considered to have been poorly designed), the state’s investor-

owned utilities sold most of their power generating plants, and then had to buy back that power at spot

market prices. Wholesale prices of electricity spiked and rolling blackouts occurred throughout the

state of California. Pacific Gas & Electric Company, headquartered in San Francisco, California, is the

state’s largest utility and is engaged principally in the business of providing electricity and natural gas

distribution.

Time Event_Description

8/17/2010 Distressed Exchange completed

Time Event_Description

1/17/2001 Missed payment on commercial paper

2/1/2001 Missed payment on commercial paper

3/16/2001 Announced that it would defer PG&E Capital Is quarterly distribution

payment on its 7.9% Cumulative Quarterly Income Preferred

Securities due on April 2, 20014/6/2001 Chapter 11

1/12/2004 Reorganization plan confirmed

27

4) Public Service Company of New Hampshire, January 28, 1988

Public Service Company of New Hampshire was the first major utility to file for bankruptcy protection

since the 1930s. It provided electric service to more than 400,000 homes and businesses, and was

headquartered in Manchester, NH. It had invested about $3 billion in the Seabrook Station nuclear

power generating facility. According to New Hampshire law, the investment in this facility could not be

included in the rate base until the plant was functional, which led to PSNH’s debt servicing problems.

PSNH emerged from bankruptcy on May 16, 1991, and was acquired by Northeast Utilities about a year

afterwards.

5) Southern California Edison Company, January 16, 2001

On January 16, 2001, Southern California Edison Company failed to honor interest and principal

payments on its public debts. In 1996, California was the first state to deregulate its electricity market.

Under deregulation, the state’s investor-owned utilities sold most of their power generating plants, and

Time Event_Description

4/19/1984 Dividend omission

10/15/1987 Interest default on 17.5% Debentures due 10/15/04

11/15/1987 Interest default on 15% Debentures due 11/15/03

1/28/1988 Chapter 11

2/1/1988 Interest default on 14.375% Debentures due 2/1/91

2/15/1988 Interest default on Deferred Interest Third Mortgage, Series A due

2/15/963/1/1988 Interest default on 9% First Mortgage, Series S due 3/1/04

3/15/1988 Interest default on 12% General and Refunding Mortgage, Series B

due 9/15/994/1/1988 Interest default on 6.125% First Mortgage, Series N due 10/1/96

and 15.75% Debentures due 10/1/884/15/1988 Interest default on 9.125% First Mortgage, Series V due 10/15/06

5/1/1988 Interest default on 7.125% First Mortgage, Series P due 11/1/98

and 9% First Mortgage, Series Q due 11/1/006/1/1988 Interest default anticipated on 6.25% First Mortgage, Series O due

6/1/97 and 17% General and Refunding Mortgage, Series D due

12/1/906/15/1988 Interest default anticipated on 7.625% First Mortgage, Series R due

6/15/02 and 18% General Refunding Mortgage, Series E due7/1/1988 Interest default anticipated on 4.625% First Mortgage, Series M due

7/1/927/15/1988 Interest default anticipated on 14.5% General and Refunding Series

C due 1/15/004/20/1990 Reorganization plan confirmed

Time Event_Description

1/16/2001 Missed principal and interest payments on maturing senior

notes; Failed to make interest payment on its senior notes

due 2006 and 2010 as well as its first mortgage notes due1/18/2001 Missed payment on maturing commercial paper and announced that

it would defer dividend payment on preferred stock6/1/2001 Missed interest paymen on its senior notes due 2001

2/8/2002 Creditors Paid in Full

3/1/2002 Credit Facility offer complete; creditors paid in full

28

then had to buy back that power at market prices. Wholesale prices of electricity spiked and rolling

blackouts occurred throughout the state of California. The company suffered from escalating financial

stress, which resulted from its inability to recover high market-priced wholesale power costs against the

legislatively frozen electric retail rates. Southern California Edison, headquartered in Rosemead,

California, is California’s second largest utility and serves southern California.

6) Yankee Companies, Incorporated, June 30, 1987

On June 30, 1987, Yankee Companies, Inc. missed interest payments on Senior Secured Bonds. The

Yankee Companies included Connecticut Yankee Atomic Power Company, Maine Yankee Atomic Power

Company, Massachusetts Yankee Atomic Power Company, Vermont Yankee Atomic Operating Company,

and Yankee Atomic Electric Company. The nuclear generating plants previously operated by these

companies are all decommissioned or in the process of being decommissioned.

Summary of Findings In summary, based upon our examination of the Moody’s database for investor owned utilities that

announced plans to construct nuclear power projects, we found that:

The announcement of an intention to construct a new nuclear facility did not, by itself, result in

credit rating impact or increase risk of default for investor owned utilities operating in the

United States.

Commencement of construction of a new nuclear plant by an investor owned utility operating in

the United States carried an almost 70% probability that the utility would experience a rating

downgrade of uncertain magnitude.

Commencement of operation of a nuclear facility arguably resulted in defaults by three (5.8%)

of 52 investor owned utilities operating in the United States, and an additional three utilities

that operated nuclear facilities also ultimately defaulted as a result of unrelated events.

Senior secured creditors of defaulting investor owned utilities that operated nuclear facilities in

the United States recovered a substantial portion of the amounts owed, depending upon the

specific factors taken into account, of up to 97.8% (using value of principal to calculate

percentages, assuming the creditor held to ultimate resolution of the default, and including

strategic defaults).

The indicated expected cumulative loss to a creditor from a portfolio of 20 year maturity senior

bonds of nuclear plant sponsors would be $0.221 per $1000 in credit extended (again, using

Time Event_Description

6/30/1987 Interest default

10/1/1987 Debt exchange offer

2/8/1988 Debt exchange for Yankee Gas, wholly owned subsidiary of the

Yankee Companies, Inc

29

value of principal to calculate percentages, assuming the creditor held to ultimate resolution of

the default, and including strategic defaults).

Based upon these findings, an investor would have been well advised to avoid owning debt of

investor owned utilities during the construction period for a nuclear power project. However,

owning debt of an investor owned utility following the conclusion of the rate case that

determined the costs allowable for ratemaking and commencement of operation of the nuclear

plant carried a relatively low risk of loss.

-- Monty Humble and Yan Zhang

30

Appendices

Table 1 Precedent Rating Actions for Utilities Attempted to Build Reactors This table examined Moody's rating actions for utilities who canceled their nuclear power plan. Table 3

examined Moody's rating actions for utilities who completed their nuclear power plant. Table 4

examined whether the utility received its lowest rating during the construction period.

Utilities Year Canceled Beginning Rating Notches

of Order Date Rating Change Moved

Delmarva Power & Light Company 1971 1975 A2 Baa2 -3

Duke Energy Ohio, Inc. 1969 1984 Aa2 Ba2 -9

New York State Electric and Gas Corporation 1967 1980 A2 Ba2 -6

Northern Indiana Public Service Company 1967 1981 A2 A2 0

Potomac Electric Power Company 1972 1977 Baa2 Baa2 0

Public Service Company of Indiana 1974 1985 A2 A2 0

Public Service Company of Oklahoma 1973 1982 A2 A1 1

Puget Sound Energy, Inc. (Old) 1973 1983 Ba2 Baa3 2

31

Table 2 Precedent Rating Actions for Utilities Involved in Nuclear Construction

Utilities Construction Beginning Rating Notches

Period Rating Change Moved

Alabama Power Company 1972 to 1981 Baa2 Ba2 -3

Arizona Public Service Company 1976 to 1988 Ba2 Baa3 2

Baltimore Gas and Electric Company 1969 to 1977 Aa2 A2 -3

Cleveland Electric Illuminating Company (The) 1971 to 1987 Aa2 Baa2 -6

Commonwealth Edison Company 1956 to 1988 Aa2 Baa2 -6

Connecticut Light and Power Company 1957 to 1986 Aa2 Ba2 -9

Consolidated Edison Company of New York, Inc. 1956 to 1976 Aa2 Baa2 -6

Consumers Energy Company 1960 to 1971 Aa2 Aa2 0

Detroit Edison Company (The) 1956 to 1988 Aa2 Ba2 -9

Duke Energy Carolinas, LLC 1967 to 1985 Aa2 Baa2 -6

El Paso Electric Company 1976 to 1988 Baa2 Baa1 1

Entergy Arkansas, Inc. 1968 to 1980 Baa2 Ba2 -3

Entergy Gulf States Louisiana, LLC 1977 to 1986 A2 Ba3 -7

Entergy Louisiana, LLC 1974 to 1985 Baa2 Ba2 -3

Entergy Mississippi, Inc. 1974 to 1985 Baa2 Baa3 -1

Florida Power & Light Company 1967 to 1983 Baa2 A2 3

Georgia Power Company 1969 to 1989 A2 Ba2 -6

GPU, Inc. 1968 to 1978 B2 Ba2 3

Illinois Power Company 1976 to 1987 A2 Baa1 -2

Indiana Michigan Power Company 1969 to 1978 A2 Ba2 -6

Iowa Electric Light and Power Company 1970 to 1975 A2 Baa2 -3

Jersey Central Power & Light Company 1964 to 1969 Baa2 Baa2 0

Kansas City Power & Light Company 1977 to 1985 A2 Baa3 -4

Kansas Gas and Electric Company 1977 to 1985 A2 Ba2 -6

Long Island Lighting Company 1972 to 1989 Aa2 B2 -12

Maine Yankee Atomic Power Co. 1968 to 1972 Baa2 Baa2 0

New England Power Company 1967 to 1972 A2 A2 0

Niagara Mohawk Power Corporation 1965 to 1988 Aa2 Baa3 -7

Northern States Power Company (Minnesota) 1959 to 1974 A2 A2 0

NSTAR Electric Company 1968 to 1972 Aa2 A2 -3

Ohio Edison Company 1970 to 1987 Aa2 Ba2 -9

Pacific Gas & Electric Company 1960 to 1986 A2 Baa2 -3

PECO Energy Company 1962 to 1990 Aa2 Ba1 -8

Pennsylvania Power Company 1970 to 1987 A2 Ba2 -6

Portland General Electric Company 1970 to 1976 Ba2 Ba2 0

PPL Electric Utilities Corporation 1973 to 1985 Baa2 Baa3 -1

Progress Energy Carolinas, Inc. 1967 to 1987 A2 Ba2 -6

Public Service Company of Colorado 1968 to 1979 A2 A2 0

Public Service Company of New Hampshire 1976 to 1990 Ba2 C -9

Public Service Company of New Mexico 1976 to 1988 A2 A3 -1

Public Service Electric and Gas Company 1968 to 1986 A2 A1 1

Reliant Energy HL&P 1975 to 1989 A2 Baa2 -3

Rochester Gas & Electric Corporation 1966 to 1970 Aa2 A2 -3

San Diego Gas & Electric Company 1973 to 1984 A2 Ba2 -6

South Carolina Electric & Gas Company 1973 to 1984 Ba2 Baa2 3

Southern California Edison Company 1964 to 1988 A2 Aa3 2

Tennessee Valley Authority 1967 to 1996 Aaa Aaa 0

Toledo Edison Company 1971 to 1987 A2 Ba2 -6

TXU Corp. (Old) 1974 to 1993 Baa3 Baa3 0

Union Electric Company 1976 to 1984 Baa2 Ba2 -3

Virginia Electric and Power Company 1968 to 1980 A2 Baa2 -3

Wisconsin Public Service Corporation 1967 to 1974 A2 Baa2 -3

32

Table 3 Utilities Received Their Lowest Rating While Building Nuclear Plants

Utilities Construction Lowest Reactors

Period Rating

Alabama Power Company 1972 to 1981 TRUE Farley

Arizona Public Service Company 1976 to 1988 TRUE Palo Verde

Baltimore Gas and Electric Company 1969 to 1977 Calvert Cliffs

Cleveland Electric Illuminating Company (The) 1971 to 1987 Beaver Valley / Davis-Besse /

PerryCommonwealth Edison Company 1956 to 1988

Braidwood / Byron / Dresden /

LaSalle / Quad Cities / Zion

Connecticut Light and Power Company 1957 to 1986 Millstone / Conn. Yankee /

Yankee Rowe

Consolidated Edison Company of New York, Inc. 1956 to 1976 TRUE Indian Point

Consumers Energy Company 1960 to 1971 Palisades / Big Rock

Detroit Edison Company (The) 1956 to 1988 TRUE Fermi

Duke Energy Carolinas, LLC 1967 to 1985 TRUE Catawba / McGuire / Oconee

El Paso Electric Company 1976 to 1988 Palo Verde

Entergy Arkansas, Inc. 1968 to 1980 Arkansas

Entergy Gulf States Louisiana, LLC 1977 to 1986 River Bend

Entergy Louisiana, LLC 1974 to 1985 Waterford

Entergy Mississippi, Inc. 1974 to 1985 Grand Gulf

Florida Power & Light Company 1967 to 1983 TRUECrystal River / St. Lucie / Turkey

Point

Georgia Power Company 1969 to 1989 TRUE Hatch / Vogtle

GPU, Inc. 1968 to 1978 TRUE Three Mile Island

Illinois Power Company 1976 to 1987 Clinton

Indiana Michigan Power Company 1969 to 1978 TRUE Cook

Iowa Electric Light and Power Company 1970 to 1975 Duane Arnold

Jersey Central Power & Light Company 1964 to 1969 Oyster Creek

Kansas City Power & Light Company 1977 to 1985 TRUE Wolf Creek

Kansas Gas and Electric Company 1977 to 1985 TRUE Wolf Creek

Long Island Lighting Company 1972 to 1989 TRUE Shoreham

Maine Yankee Atomic Power Co. 1968 to 1972 TRUE Maine Yankee

New England Power Company 1967 to 1972 Vermont Yankee

Niagara Mohawk Power Corporation 1965 to 1988 FitzPatrick / Nine Mile

Northern States Power Company (Minnesota) 1959 to 1974 Monticello / Prairie Island /

Pathfinder

NSTAR Electric Company 1968 to 1972 Pilgrim

Ohio Edison Company 1970 to 1987 TRUE Beaver Valley / Perry

Pacific Gas & Electric Company 1960 to 1986 Diablo Canyon / Humboldt Bay

PECO Energy Company 1962 to 1990 TRUE Limerick / Peach Bottom

Pennsylvania Power Company 1970 to 1987 TRUE Beaver Valley / Perry

Portland General Electric Company 1970 to 1976 TRUE Trojan

PPL Electric Utilities Corporation 1973 to 1985 TRUE Susquehanna

Progress Energy Carolinas, Inc. 1967 to 1987 TRUEBrunswick / H. B. Robinson /

Shearon Harris

Public Service Company of Colorado 1968 to 1979 Fort St. Vrain

Public Service Company of New Hampshire 1976 to 1990 TRUE Seabrook

Public Service Company of New Mexico 1976 to 1988 Palo Verde

Public Service Electric and Gas Company 1968 to 1986 Hope Creek / Salem

Reliant Energy HL&P 1975 to 1989 TRUE South Texas Project

Rochester Gas & Electric Corporation 1966 to 1970 Ginna