New Cobra Rules (April 24 2009)

37

May 21, 2009 May 21, 2009 The Job Show The Job Show The American Recovery And The American Recovery And Reinvestment Act Of 2009 Reinvestment Act Of 2009 The COBRA Premium Subsidy The COBRA Premium Subsidy Presented by: Presented by: John P. McMorrow, Esq. John P. McMorrow, Esq.

-

Upload

mvrotary -

Category

Entertainment & Humor

-

view

684 -

download

3

Transcript of New Cobra Rules (April 24 2009)

May 21, 2009May 21, 2009

The Job ShowThe Job Show

The American Recovery And The American Recovery And Reinvestment Act Of 2009Reinvestment Act Of 2009

The COBRA Premium SubsidyThe COBRA Premium Subsidy

Presented by:Presented by:

John P. McMorrow, Esq.John P. McMorrow, Esq.

WHAT DOES THE ACT PROVIDE? The American Recovery and Reinvestment Act of 2009 (the

“Act”) effective February 17, 2009 provides a federal government subsidy of COBRA premiums for up to 9 months for individuals who are COBRA qualified beneficiaries because of a covered employee’s involuntary termination of employment (for other than gross misconduct).

The Joint Committee of Taxation estimates:

– The COBRA continuation subsidy cost - $14.302 billion and $9.154 billion in the 2009 and 2010.

– Approximately 7 million people will benefit from the credit for some portion of 2009.

If the economy doesn't snap back quickly enough, the continuation subsidy may be extended.

2

WHAT IS THE COBRA PREMIUM ASSISTANCE SUBSIDY?

An “assistance eligible individual” (AEI) pays 35% of the COBRA premium otherwise chargeable to the AEI for up to 9 months.

The federal government subsidizes 65% of the COBRA premium otherwise chargeable to the AEI for up to 9 months.

The premium assistance subsidy is not taxable to the AEI (subject to a recapture rule for high income individuals) and does not count as income in determining the AEI’s eligibility for federal or state assistance programs, such as food stamps.

3

WHAT TYPES OF HEALTH PLANS ARE ELIGIBLE FOR PREMIUM ASSISTANCE?

The subsidy applies to the premium cost of group health plan coverage under both the federal COBRA law and any state “mini-COBRA” laws (i.e., M.G.L. Chapter 176 Section 9 applicable to employers with 2-19 employees).

See next slide.

4

WHAT TYPES OF HEALTH PLANS ARE ELIGIBLE FOR PREMIUM ASSISTANCE?

Health benefits eligible for premium assistance.

– Medical plans (including high deductible health plans), dental plans, vision plans, health reimbursement arrangements (HRAs), any other group health plans subject to COBRA.

Health benefits not eligible for premium assistance.

– Health FSAs.– Non-ERISA health savings accounts (HSAs).

5

HOW IS THE SUBSIDY PROVIDED?

An AEI pays 35% of the COBRA premium otherwise payable but for the new law. The government subsidizes 65% of the COBRA premium.

The Reimbursement Mechanism. If the applicable COBRA premium is $1,020 (102% x $1,000), the AEI pays 35% of $1,020. The employer “advances” the 65% subsidy, then recoups the “advanced” amount as a credit against its liability for payroll taxes. (This may result in a direct payment to an employer whose payroll tax liability is less than the credit). The “payroll tax liability” is defined as federal income tax withholdings on wages and FICA taxes (both the employer and employee share). Does not include federal unemployment (FUTA) taxes.

For insured coverage, the employer’s payment to the carrier doesn’t change.

6

WHO CLAIMS THE PREMIUM ASSISTANCE SUBSIDY REIMBURSEMENT?

The employer, if the plan is subject to the Federal COBRA continuation provisions contained in the Code, ERISA, Public Health Service Act, or civil service provisions of the U.S. Code.

The insurer, if the plan is fully insured and subject to the Massachusetts mini-COBRA rules.

The plan, if the plan is a multiemployer group health plan (such as a Taft-Hartley plan).

7

WHAT DOES THE EMPLOYER HAVE TO DO TO CLAIM THE PAYROLL TAX CREDIT?

To claim the payroll tax credit an employer must file a Form 941 ("Employer's Quarterly Federal Tax Return”) for the quarter during which the subsidy is provided (or for a later quarter in the same year). The employer can file Form 941X ("Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund") for that quarter.

The revised 2009 Form 941 includes:

– Line 12a - COBRA premium assistance payments.– Line 12b - Number of individuals provided assistance.

If the amount of the COBRA premium subsidy entered on Form 941 exceeds the employer's tax liabilities for the quarter, it can choose to have the excess either refunded or applied to the next quarter (but if the employer chooses to have the excess refunded, IRS will not send a notice before making the refund).

Employers may only report the premium assistance payments that they made for the AEIs who have paid their 35% share of the COBRA premium.

8

WHAT OTHER INFORMATION RELATING TO THE COBRA SUBSIDY MUST BE SUBMITTED WITH THE FORM 941 BESIDES

THE ENTRIES ON LINES 12A AND 12B?

None! However, Employers must retain supporting documentation for the credit claimed including:

– Information on the receipt, including dates and amounts, of the assistance eligible individuals’ 35% share of the premium

– Proof of timely payment of the full premium to the insurer (or proof of the premium amount and the coverage provided, in the case of a self-funded plan).

– Attestation of the former employee's involuntary termination and proof of an AEI's eligibility for, and election of, COBRA during the relevant period.

– A record of the SSN’s of all covered employees, the amount of the subsidy reimbursed with respect to each covered employee, and whether the subsidy was for 1 individual or 2 or more individuals.

– Other documents necessary to verify the correct amount of reimbursement. 9

DOES THE SUBSIDY CHANGE UNDER A COBRA PREMIUM COST SHARING ARRANGEMENT?

Examples: Three Companies With Monthly COBRA Premiums Of $300

COBRA Premium Cost-Sharing / The Premium Assistance Subsidy

Company A Company B Company C

COBRA Premium Cost Sharing

Qualified beneficiary pays $300 $100 $0

Company pays $0 $200 $300

The Premium Assistance Subsidy

AEI pays a reduced COBRA premium

$300 x 35% = $105 $100 x 35% = $35 $0 x 35% = $0

Employer claims a credit against its payroll tax liability

$300 x 65% = $195 $100 x 65% = $65 $0 x 65% = $0

10

WHO IS AN ASSISTANCE ELIGIBLE INDIVIDUAL?

An AEI includes any COBRA qualified beneficiary:

1. Who elects COBRA continuation coverage during the original COBRA election period or during the special election period provided by the Act,

2. Who is eligible for COBRA continuation coverage by virtue of a covered employee’s involuntary termination from employment (other than for gross misconduct), and

3. The involuntary termination resulting in COBRA continuation coverage must occur during the period from September 1, 2008, through December 31, 2009.

To be an AEI an individual must be eligible for COBRA coverage, i.e., must actually have coverage under the group health plan at the time of the involuntary termination.

11

WHAT IS AN INVOLUNTARY TERMINATION? Termination for Termination of employment for cause

(except in cases of gross misconduct) is an involuntary termination for the purposes of qualifying for the COBRA premium assistance subsidy.

IRS has issued comprehensive guidance (Notice 2009-27).

Employer initiated action that causes a material negative change in the employment relationship is required for there to be an involuntary termination

Facts and circumstances test.

12

WHAT IS AN INVOLUNTARY TERMINATION?Involuntary Termination Not Involuntary Termination

Employer does not renew employee’s contract, if employee is willing to sign a new contract.

Death.

Employer ends employment while employee is absent due to illness or disability.

Absence due to illness or disability.

Resignation or retirement, if employee knows that the employer will terminate his or her employment.

Resignation or Retirement except when in lieu of termination/layoff.

.

Resignation due to employer-initiated reduction in hours if it’s a material negative change in the employment relationship.

Reduction in hours except where employee resigns or where hours are reduced to zero.

Layoff with right to recall, furlough or other suspension of employment.

Work stoppage as a result of strike initiated by employees or union.

Resignation due to a material change in employment geographic location.

Voluntary acceptance of severance programs (buy-out) if additional terminations are likely after the buy-out election period ends

WHO IS AN ASSISTANCE ELIGIBLE INDIVIDUAL?

1. Individuals who are currently covered by COBRA by reason of an involuntary termination on or after September 1, 2008.

2. Individuals who were previously eligible for COBRA continuation coverage by reason of an involuntary termination on or after September 1, 2008 but did not elect COBRA.

3. Individuals who were previously eligible for COBRA coverage by reason of an involuntary termination on or after September 1, 2008, elected COBRA, but are no longer covered as of February 17, 2009 (because, for example, the individual did not pay the required premium).

4. Other individuals who are eligible for COBRA coverage by reason of an involuntary termination on and after September 1, 2008 and on or before December 31, 2009.

14

WHO IS AN ASSISTANCE ELIGIBLE INDIVIDUAL?

An AEI includes a covered employee OR a covered employee’s covered spouse or dependent who became a qualified beneficiary because of a covered employee’s involuntary termination from employment.

A qualified beneficiary may independently elect COBRA receive the premium assistance subsidy. Thus, for example, the subsidy for an assistance-eligible individual could continue even after the covered employee’s death.

An AEI does NOT include a same-sex spouse or a domestic partner. Such an individual is not a “qualified beneficiary” for purposes of federal COBRA even if offered continuation coverage overage.

If a plan determines that an individual is not eligible for the premium assistance subsidy, the individual may appeal the decision by filing the form available at www.dol.gov/COBRA. The DOL (or Dept. of Health and Human Services to mini-COBRA coverage laws) will handle the appeal within 15 days.

15

WHEN DOES THE PREMIUM ASSISTANCE SUBSIDY BEGIN?

No one is eligible for the premium assistance subsidy before February 17, 2009.

The premium assistance subsidy applies to periods of COBRA continuation coverage beginning after February 17, 2009.

A “period of coverage” is the monthly (or shorter) period for which COBRA premiums are charged.

For group health plans using calendar months as the period of coverage, the premium assistance subsidy applies to COBRA coverage beginning March 1, 2009.

16

HOW LONG WILL THE SUBSIDY BE PAID? The premium assistance subsidy ends (and the full COBRA premium may then

be charged) as of the earlier of:

– The date the AEI becomes eligible for coverage (not actually covered) under another group health care plan (other than plans providing only dental, vision, counseling, or referral services, a health care flexible spending plan, or a health reimbursement arrangement) or Medicare coverage.

– The date that is 9 months after the first day of the first month to which the subsidy applies (beginning no earlier than March 1, 2009) (e.g., if the subsidy is available beginning March 1, 2009, it would last through November 30, 2009, and expire December 1, 2009).

– The end of the maximum COBRA continuation coverage period (including permissible early terminations, such as for failure to pay a required premium).

COBRA duration unaffected by subsidy. If an AEI elects COBRA during the special election period for federal COBRA coverage, the end of the maximum federal COBRA coverage period is the date that would have applied if the AEI had elected federal COBRA coverage when first entitled to do so. 17

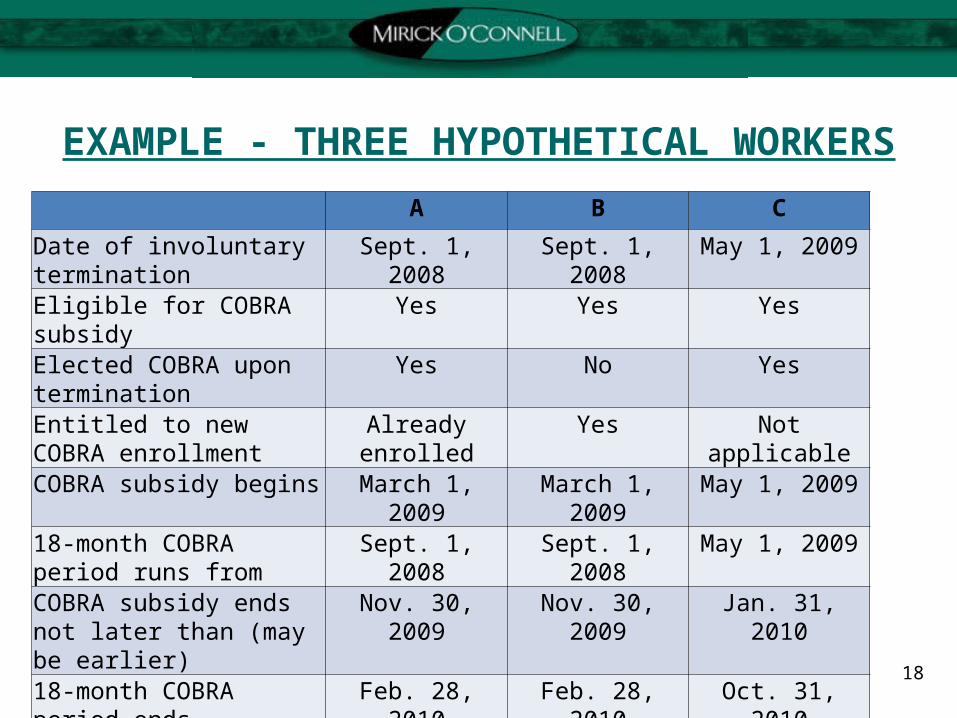

EXAMPLE - THREE HYPOTHETICAL WORKERS

A B C

Date of involuntary termination

Sept. 1, 2008 Sept. 1, 2008 May 1, 2009

Eligible for COBRA subsidy Yes Yes Yes

Elected COBRA upon termination

Yes No Yes

Entitled to new COBRA enrollment

Already enrolled Yes Not applicable

COBRA subsidy begins March 1, 2009 March 1, 2009 May 1, 2009

18-month COBRA period runs from

Sept. 1, 2008 Sept. 1, 2008 May 1, 2009

COBRA subsidy ends not later than (may be earlier)

Nov. 30, 2009 Nov. 30, 2009 Jan. 31, 2010

18-month COBRA period ends

Feb. 28, 2010 Feb. 28, 2010 Oct. 31, 2010

18

DISQUALIFYING COVERAGE The premium assistance subsidy does not apply to any

month that begins after the date that a COBRA qualified beneficiary becomes eligible for coverage under another “group health plan” or Medicare.

The term “group health plan” does not include a plan that provides only one or more of the following benefits:

– Dental care, vision care, counseling or referral services,

– Health FSA or an HRA under Code section 106(c), or– An on-site medical clinic that consists primarily of first-

aid services, prevention, wellness and/or similar care.19

DOES AN AEI HAVE TO NOTIFY THE PLAN OF DISQUALIFYING COVERAGE?

Yes. Once the AEI is eligible for group health coverage or Medicare, the AEI is required to provide timely written notice to the plan providing COBRA coverage.

Failure to provide timely notice results in 110% penalty imposed on the AEI for premium reduction provided “after termination of eligibility” (subject to reasonable cause exception).

20

ARE THERE INCOME RESTRICTIONS ON ELIGIBILITY FOR PREMIUM ASSISTANCE?

Premium assistance recaptured for “high-income individuals”

– A single taxpayer with modified adjusted gross income less than $125,000 (single) or $250,000 (couples) is eligible for the full premium assistance subsidy.

– Prorated subsidy for “high-income individuals” earning $125,000 to $149,999 (single) or $250,000 to $289,999 (couples).

A “high-income individual” is required to repay the subsidy as an additional tax on his or her tax return for the year in which the subsidy was received.

An employer is required to “pay” the subsidy even if the employer knows the AEI is a high-income individual.

21

MAY A “HIGH-INCOME INDIVIDUAL” WAIVE THE SUBSIDY?

Yes. To avoid the recapture tax high-income individuals may permanently waive their right to the subsidy.

Can the waiver occur by not returning the application form for the subsidy?

Individuals who waive their right to the subsidy cannot claim the right in a subsequent year (e.g., 2010) if their income level qualifies. So, individuals who do not qualify in 2009 (due to income level) may want to pay the taxes associated with the recapture rather than waive the right to premium assistance.

22

WHAT DOES A PLAN ADMINISTRATOR NEED TO DO?

Take the steps required to provide the COBRA premium assistance subsidy to AEIs beginning March 1, 2009.

Failure to update and distribute notices as required potentially subjects employers to daily COBRA penalties (ERISA $110 per day and Internal Revenue Code excise tax of $100 per day).

Transition rule (Remedy if AEI pays more than 35%).

– For AEIs who pay 100% of their COBRA premiums during the first two COBRA coverage periods on and after February 17, 2009.

– The employer may either:• Reimburse the AEI for 65% of the premiums paid, or• Credit such amount against future provided that the credit is used up

within 180 days.

23

WHAT ARE THE NEW NOTICE REQUIREMENTS? New subsidy notice. Provide notice to all individuals who become eligible

for COBRA between September 1, 2008 and December 31, 2009, even if the individual is not an AEI (because an event other than involuntary job loss triggered his or her right to COBRA coverage). DOL March 20 Guidance: Employers do not have to provide this notice to individuals who are not AEIs and who did not elect COBRA coverage when they first had the chance to do so.

– The notice must be provided by April 18, 2009, if the individual became eligible for COBRA between September 1, 2008 and February 16, 2009.

New notice re second chance to elect COBRA. AEIs who do NOT have COBRA coverage as of February 17, 2009 must be given a second chance to elect COBRA . – The notice and election form must be provided by April 18, 2009.– COBRA coverage under the second-chance election is not retroactive to

the date of job loss.– This COBRA election does not apply to Mass mini-COBRA. 24

SUBSIDY NOTICE DEADLINES FOR INDIVIDUALS BECOMING COBRA-ELIGIBLE FOR ANY REASON FROM SEPTEMBER 1, 2008 THROUGH DECEMBER 31, 2009

25

Subsidy notice deadlines for individuals becoming COBRA-eligible for any reason from September 1, 2008, through December 31, 2009

Individual first eligible to elect COBRA Subsidy notice due by

Between Sept. 1, 2008 and Feb. 16, 2009

Assistance-eligible individuals

with COBRA on February 17, 2009 April 18, 2009

without COBRA on February 17, 2009 (did not elect COBRA when first eligible or elected COBRA but dropped it before February 17, 2009)

April 18, 2009

Individuals ineligible for assistance

whose 44-day COBRA election notice distribution period HAS NOT ended

End of applicable 44-day COBRA election notice distribution period

whose 44-day COBRA election notice distribution period HAS ended

DOL March 20 Guidance:With COBRA - April 18, 2009Without COBRA - No notice due

Between February 17, 2009 and December 31, 2009End of applicable 44-day COBRA election notice distribution period

WHAT ARE THE CONTENT REQUIREMENTS FOR THE NEW SUBSIDY NOTICE?

The notice regarding the premium assistance subsidy must include the following information:

A description of the right to the subsidy and any conditions for receiving it.

The forms necessary to establish subsidy eligibility.

A description of the second, special COBRA election period.

A description of the individual’s duty – and the penalty for failure – to inform the plan once eligibility for the subsidy is lost due to eligibility for Medicare or other group health plan coverage.

The plan administrator’s name, address and telephone number, as well as those of any other person with information relevant to the subsidy.

If the employer chooses to permit it, a description of the individual’s right to choose a lower cost COBRA coverage option.

26

THE SECOND CHANCE TO ELECT COBRA (UNDER FEDERAL LAW)

Example re employer cash flow:

– 10/1/2008: Individual is involuntarily terminated, does not elect COBRA.

– 2/17/2009: No federal COBRA coverage. – 4/15/2009: Employer sends notice of special election right.

6/10/2009: Individual elects COBRA.– 3/1/2009: Coverage and subsidy effective date.– The 18-month period of COBRA coverage begins on

10/1/2008.– The 9-month period of subsidy eligibility on 3/1/2009.

The 9-month subsidy period runs concurrently with any months in which the employer subsidizes all or part of an individual’s COBRA premium.

27

THE SECOND CHANCE TO ELECT COBRA (UNDER FEDERAL LAW)

For these AEIs with the second chance to elect COBRA, the gap between the date of the covered employee’s involuntary job loss and the first day of the first COBRA coverage period beginning after February 17, 2009 (March 1, 2009) is disregarded when determining if applying HIPAA’s 63-day significant break in coverage rules for the purposes of applying pre-existing condition exclusions.

HIPAA certificates will have to be revised and reissued to those who exercise their second chance COBRA election right.

No second election for plans only subject to state “mini-COBRA” laws.

28

WHAT COBRA COVERAGE CAN BE ELECTED?

Generally, COBRA coverage is the same coverage that the qualified beneficiary had immediately before the qualifying event.

Switching Benefit Options: An employer may (but is not required) to allow AEIs to elect an alternative coverage option that is different from the COBRA coverage originally offered to the AEI.

29

WHAT REQUIREMENTS APPLY TO ALTERNATIVE COBRA COVERAGE?

The COBRA premium cost of the alternative coverage option must be the same or less than the COBRA premium cost for the coverage in which the AEI was enrolled when the COBRA qualifying event occurred.

The alternative coverage option must be coverage that is available to active employees.

The alternative coverage option cannot be limited to: (1) dental, vision, counseling or referral services (singly or in any combination); (2) a health care flexible spending account or (3) an on-site facility primarily providing first aid, prevention, or wellness care.

If an employer decides to offer an alternative coverage option, the employer must provide notice and the AEI has 90 days to elect from notice of the plan enrollment option.

30

THE DOL HAS ISSUED 4 MODEL NOTICES

The model notices do not provide any new or significantly revised interpretations of the assistance payment rules.

The model notices and accompanying DOL questions and answers:

– Require that qualified beneficiaries declare themselves eligible for the 65% assistance payment.

– Contemplate a pen-and-paper process for electing COBRA and the 65% assistance payment.

– Fail to indicate that employers or COBRA administrators are free to use any other forms of their choosing.

– Fail to recognize that employers or COBRA administrators can use electronic or telephonic processes to enroll in COBRA, claim eligibility for the 65% assistance payment, or notify an employer that a qualified beneficiary is no longer eligible for the assistance payment.

31

THE MODEL GENERAL NOTICE (FULL VERSION)

Send to individuals who have a COBRA qualifying at any time from September 1, 2008 through December 31, 2009 AND who either have not yet been provided an election notice or who were provided an election notice on or after February 17, 2009 that did not include the additional information required by ARRA. (The DOL altered its guidance the weekend of March 20th).

The notice contains explanatory material about COBRA and the new premium assistance subsidy and:

– A form to elect COBRA.– A form to switch COBRA coverage benefit options (if this option is made

available by the employer).– A form that the individual may use to request treatment by the employer

as an AEI. – A form that may be used by an individual who becomes ineligible for the

new COBRA premium subsidy by virtue of becoming eligible for other certain group health plan coverage or Medicare. 32

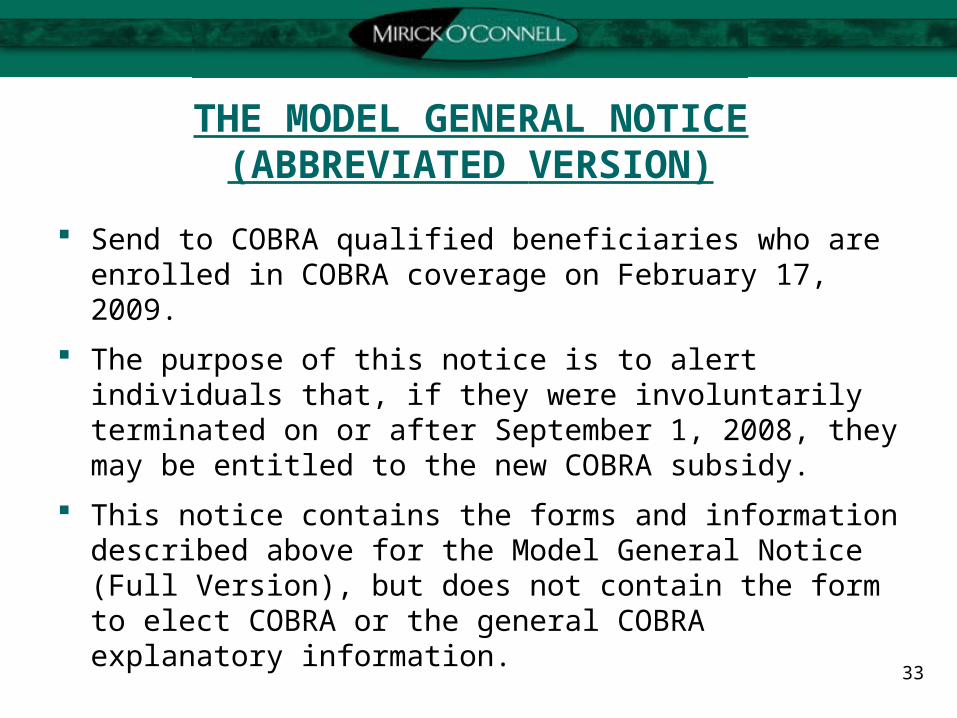

THE MODEL GENERAL NOTICE(ABBREVIATED VERSION)

Send to COBRA qualified beneficiaries who are enrolled in COBRA coverage on February 17, 2009.

The purpose of this notice is to alert individuals that, if they were involuntarily terminated on or after September 1, 2008, they may be entitled to the new COBRA subsidy.

This notice contains the forms and information described above for the Model General Notice (Full Version), but does not contain the form to elect COBRA or the general COBRA explanatory information.

33

THE MODEL NOTICE IN CONNECTION WITH EXTENDED ELECTION PERIODS

Send to AEIs, individuals who had a COBRA qualifying event during the period September 1, 2008 through February 16, 2009 and who could be eligible for the new COBRA premium subsidy but who are NOT enrolled in COBRA coverage on February 17, 2009.

This notice contains largely the same information as that provided in the first general notice except that the COBRA election form and some of the explanatory information are specifically oriented to the individuals described above.

34

THE MODEL ALTERNATIVE NOTICE

For use by employers subject to state continuation coverage provisions rather than the federal COBRA rules.

The notice is primarily a generic document that employers may use to notify employees of their mini-COBRA rights; no state-specific information is provided. The notice does, however, contain the forms described in conjunction with the first general notice above.

The issuer of the group health plan subject to state coverage must provide the notice to qualified beneficiaries on how to apply for the subsidy within the time frame required by state law.

State continuation coverage programs are not required to offer an additional election period to enroll in continuation coverage to eligible individuals involuntarily terminated during the period September 1, 2008 to February 16, 2009, although states may take action to offer this second election period.

35

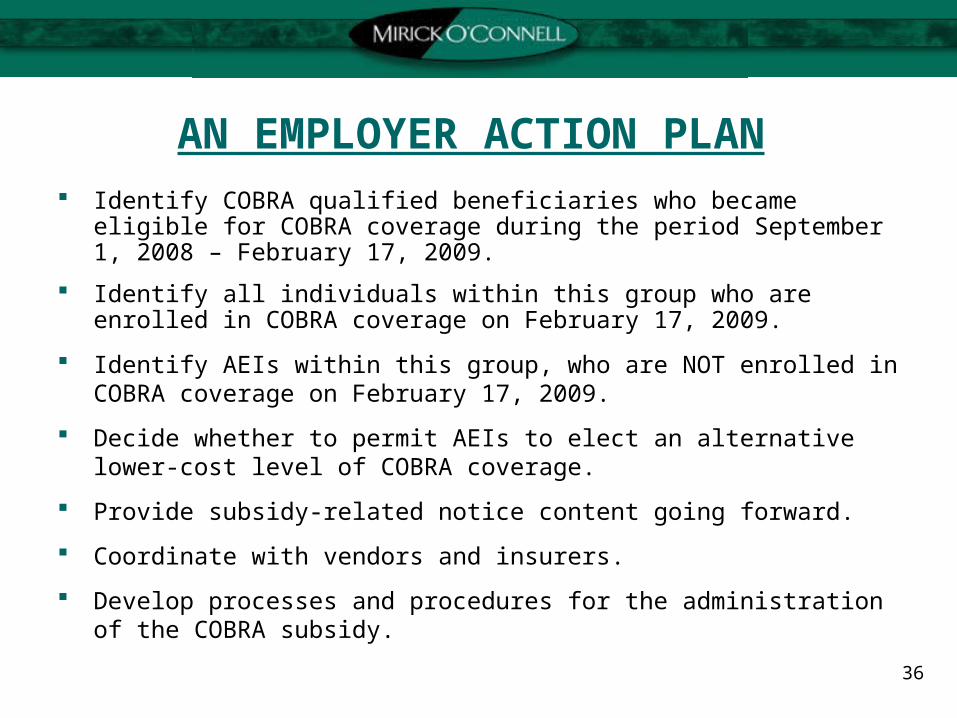

AN EMPLOYER ACTION PLAN Identify COBRA qualified beneficiaries who became eligible for COBRA

coverage during the period September 1, 2008 – February 17, 2009.

Identify all individuals within this group who are enrolled in COBRA coverage on February 17, 2009.

Identify AEIs within this group, who are NOT enrolled in COBRA coverage on February 17, 2009.

Decide whether to permit AEIs to elect an alternative lower-cost level of COBRA coverage.

Provide subsidy-related notice content going forward.

Coordinate with vendors and insurers.

Develop processes and procedures for the administration of the COBRA subsidy.

36