Neural Network Variations for Time Series Forecasting

107

Nova Southeastern University Nova Southeastern University NSUWorks NSUWorks CCE Theses and Dissertations College of Computing and Engineering 2021 Neural Network Variations for Time Series Forecasting Neural Network Variations for Time Series Forecasting David Ason Nova Southeastern University, [email protected] Follow this and additional works at: https://nsuworks.nova.edu/gscis_etd Part of the Computer Sciences Commons Share Feedback About This Item NSUWorks Citation NSUWorks Citation David Ason. 2021. Neural Network Variations for Time Series Forecasting. Doctoral dissertation. Nova Southeastern University. Retrieved from NSUWorks, College of Computing and Engineering. (1150) https://nsuworks.nova.edu/gscis_etd/1150. This Dissertation is brought to you by the College of Computing and Engineering at NSUWorks. It has been accepted for inclusion in CCE Theses and Dissertations by an authorized administrator of NSUWorks. For more information, please contact [email protected].

Transcript of Neural Network Variations for Time Series Forecasting

Nova Southeastern University Nova Southeastern University

NSUWorks NSUWorks

CCE Theses and Dissertations College of Computing and Engineering

2021

Neural Network Variations for Time Series Forecasting Neural Network Variations for Time Series Forecasting

David Ason Nova Southeastern University, [email protected]

Follow this and additional works at: https://nsuworks.nova.edu/gscis_etd

Part of the Computer Sciences Commons

Share Feedback About This Item

NSUWorks Citation NSUWorks Citation David Ason. 2021. Neural Network Variations for Time Series Forecasting. Doctoral dissertation. Nova Southeastern University. Retrieved from NSUWorks, College of Computing and Engineering. (1150) https://nsuworks.nova.edu/gscis_etd/1150.

This Dissertation is brought to you by the College of Computing and Engineering at NSUWorks. It has been accepted for inclusion in CCE Theses and Dissertations by an authorized administrator of NSUWorks. For more information, please contact [email protected].

Neural Network Variations for Time Series Forecasting

by

David Ason

A dissertation submitted in partial fulfillment of the requirements

for the degree of Doctor of Philosophy

in

Computer Science

College of Computing and Engineering

Nova Southeastern University

2021

An Abstract of a Dissertation Submitted to Nova Southeastern University in Partial Fulfillment

of the Requirements for the Degree of Doctor of Philosophy

Neural Network Variations for Time Series Forecasting

by

David Ason

2021

Time series forecasting is an area of research within the discipline of machine learning. The

ARIMA model is a well-known approach to this challenge. However, simple models such as

ARIMA do not take into consideration complex relationships within the data and quite often fail

to produce a satisfactory forecast. Neural networks have been presented in previous works as an

alternative. Neural networks are able to capture non-linear relationships within the data and can

deliver an improved forecast when compared to ARIMA models.

This dissertation takes neural network variations and applies them to a group of time series

datasets found in the literature to look for forecasting improvements and generalizability. Metrics

used to compare the effectiveness of the variations will be taken from the literature and include

the Root Mean Squared Error (RMSE), Directional Accuracy (DA), and Mean Absolute

Percentage Error (MAPE).

A total of 12 datasets were used for this study: 6 series each with a daily and weekly version.

Analysis of the results demonstrates that it is possible to improve performance as gauged by the

metrics in most instances. Neural networks with a feature detection component such as a

convolutional layer or a temporal component such as RNN variations are effective when scored

by the directional accuracy metric. Convolutional layers appear to be especially effective at the

weekly level of granularity in this study. The Stacked Denoising Autoencoder (SDAE)

performed well when judged by the RMSE and MAPE metrics.

The directional accuracy metric was further broken down into a classification problem:

precision, recall, and F1 metrics were used for this evaluation. In addition, the research included

evaluating the models’ ability to predict multiple steps ahead: steps t+1, t+2, and t+3 were

examined. The predictive power of the models generally decreased as timesteps increased. RNN

variations continued to do well at timesteps beyond t+1 for directional accuracy. The predictive

power of the SDAE held up well beyond the t+1 step and dominated the MAPE and RMSE

metrics at steps t+2 and t+3.

Acknowledgements

I would like to start by thanking the faculty and staff at Nova Southeastern University’s

College of Computing and Engineering for giving me the opportunity to pursue a long-held

dream of completing a Doctor of Philosophy degree in Computer Science. The classes that

comprised the core curriculum were engaging and interesting. They helped shape my

understanding of what research would entail. In particular, I would like to express my gratitude

to:

• Dr. Sumitra Mukherjee, my dissertation chair, for his advice, feedback, and the

benefit of his wisdom and experience. My dissertation topic was conceived during his

Artificial Intelligence class, and my work would not have been possible without his

support.

• Dr. Francisco Mitropoulos and Dr. Michael Laszlo for participating on my

dissertation committee and providing excellent instruction in the core classes I took

with them.

Lastly, I would like to thank my family for their support and love as I pursued my

passion. It would not have been possible without them.

iii

Table of Contents List of Figures .............................................................................................................. vii

List of Tables............................................................................................................... viii

Chapter 1 Introduction .....................................................................................................1

Problem Statement .......................................................................................................2

Dissertation Goal .........................................................................................................3

Research Questions ......................................................................................................4

Relevance and Significance .........................................................................................4

The Random Walk Model ........................................................................................4

The ARIMA Model .................................................................................................5

Long Short Term Memory Neural Networks ............................................................7

The Gated Recurrent Unit ........................................................................................9

Ensembling ............................................................................................................ 10

Barriers and Issues ..................................................................................................... 10

Assumptions, Limitations, and Delimitations ............................................................. 11

Definition of Terms ................................................................................................... 12

Summary ................................................................................................................... 12

Chapter 2 Review of the Literature ................................................................................ 14

Introduction ............................................................................................................... 14

iv

The Challenge of Time Series Forecasts .................................................................... 14

A Review of Approaches to Time Series Forecasting ................................................. 15

Time Series Forecasting with Convolutional Neural Networks ............................... 15

Time Series Forecasting with Recurrent Neural Networks ...................................... 18

Time Series Forecasting with Stacked Autoencoders .............................................. 22

Ensembling Multiple Models to Improve Prediction .............................................. 25

Summary ................................................................................................................... 26

Chapter 3 Methodology ................................................................................................. 27

The Datasets .............................................................................................................. 27

Create Baseline Prediction Models............................................................................. 28

Create the SDAE Model ............................................................................................ 29

Create Neural Network Variations ............................................................................. 29

Long Short Term Memory Neural Networks .......................................................... 29

Gated Recurrent Unit Neural Networks .................................................................. 30

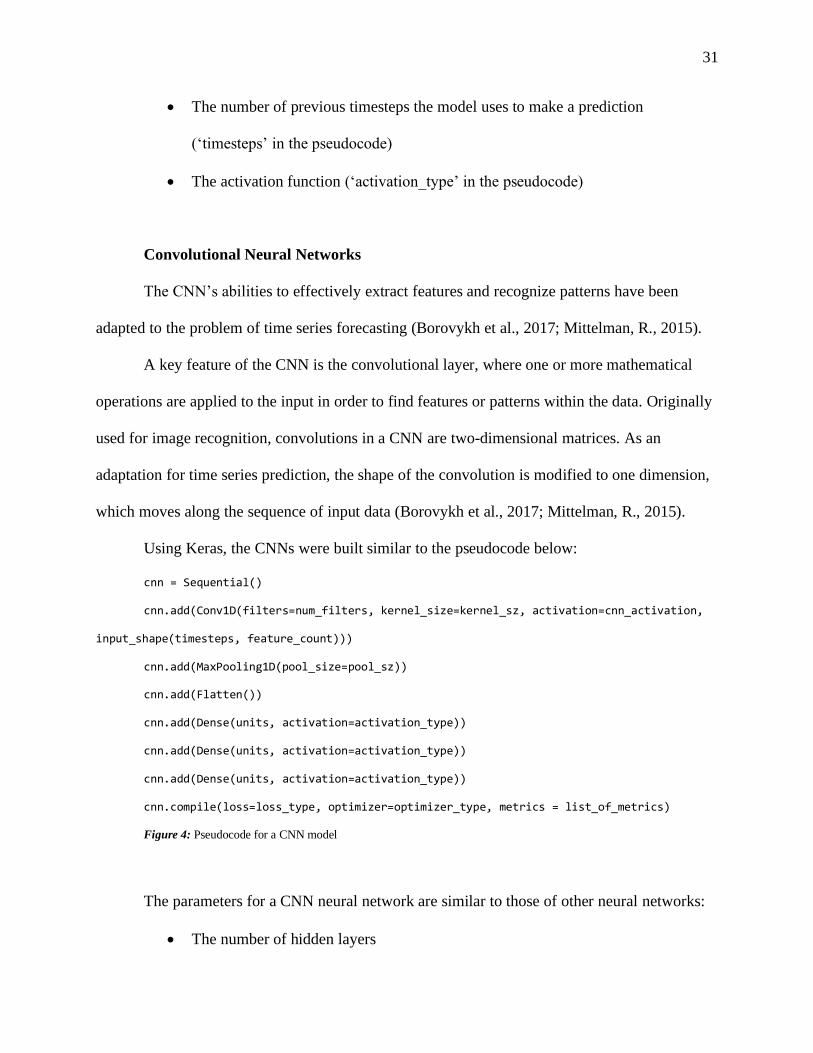

Convolutional Neural Networks ............................................................................. 31

Hybrid Model Variations ....................................................................................... 32

Model Tuning ............................................................................................................ 34

Random Hyperparameter Search ............................................................................ 35

Optimized Hyperparameter Search ......................................................................... 36

Use Ensembling to Improve Model Prediction Results ............................................... 38

v

Compare the Models Using Performance Evaluation Metrics ..................................... 39

Data Analysis......................................................................................................... 40

Format for Presenting Results ................................................................................ 41

Resources .................................................................................................................. 43

Summary ................................................................................................................... 44

Chapter 4 Results ........................................................................................................... 45

Introduction ............................................................................................................... 45

Data Analysis ............................................................................................................ 46

SDAE and baseline comparisons ............................................................................ 47

SDAE and Baselines on Other Datasets ................................................................. 49

Looking for improvement beyond the baselines ..................................................... 51

Ensembling ............................................................................................................ 59

Directional Accuracy ............................................................................................. 64

Directional Accuracy Summary ............................................................................. 73

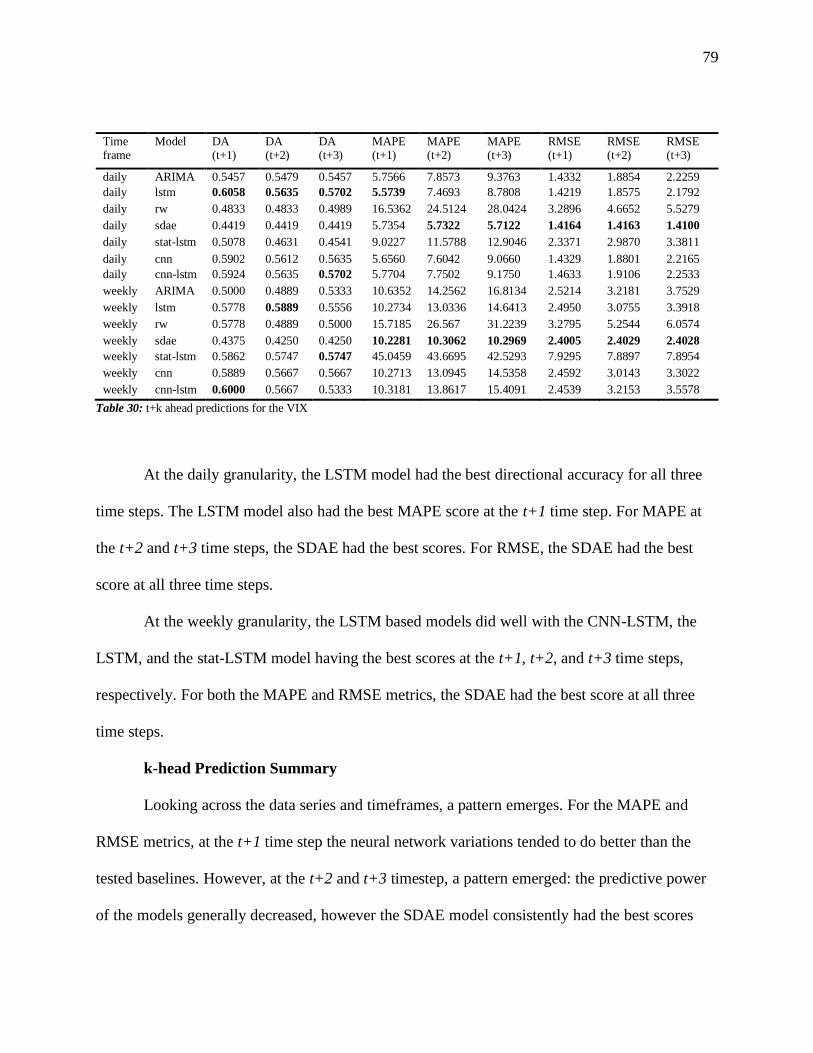

k-ahead Predictions ................................................................................................ 73

k-head Prediction Summary ................................................................................... 79

Findings ..................................................................................................................... 80

Summary of Results ................................................................................................... 82

Chapter 5 Conclusions ................................................................................................... 84

Implications ............................................................................................................... 85

vi

Recommendations for Future Work ........................................................................... 86

Summary ................................................................................................................... 87

References ..................................................................................................................... 89

Appendix A ................................................................................................................... 92

Appendix B – Model Configurations ............................................................................. 93

vii

List of Figures

Figure 1: A GRU cell .................................................................................................................9

Figure 3: Pseudocode for a LSTM model ................................................................................. 29

Figure 4: Pseudocode for a GRU model.................................................................................... 30

Figure 5: Pseudocode for a CNN model ................................................................................... 31

Figure 6: stat-lstm architecture ................................................................................................. 33

Figure 7: cnn-lstm architecture ................................................................................................. 34

Figure 8: The SDAE model (red) compared with the t-1 value (green) and the actual WTI price

(black)....................................................................................................................................... 46

Figure 9: The SDAE model and baselines ................................................................................ 47

Figure 10: Sample LSTM model output on EURUSD .............................................................. 53

Figure 11: CNN model on USDJPY ......................................................................................... 55

Figure 12: Stat-LSTM model on the TNX index ....................................................................... 57

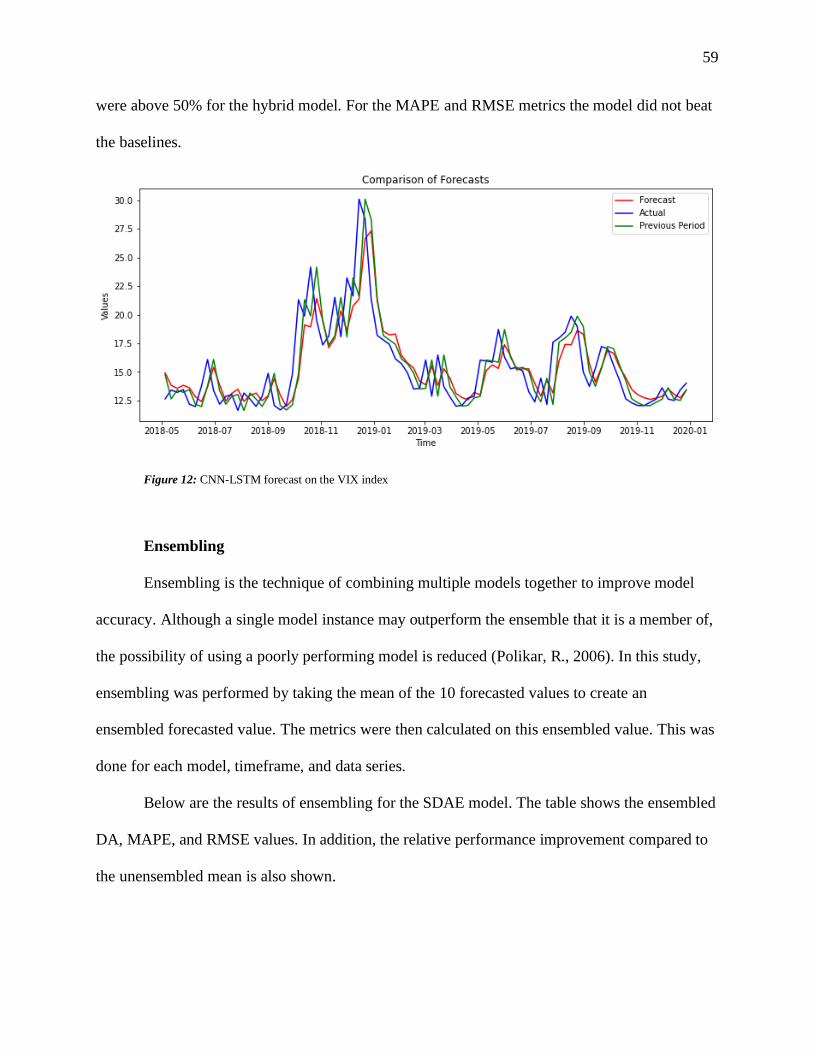

Figure 13: CNN-LSTM forecast on the VIX index ................................................................... 59

Figure 14: t+k ahead predictions ............................................................................................... 74

viii

List of Tables

Table 1: Sample model information .......................................................................................... 41

Table 2: Sample model parameters ........................................................................................... 43

Table 3: SDAE and benchmark comparisons on WTI data........................................................ 48

Table 4: SDAE and benchmarks on weekly data ....................................................................... 49

Table 5: SDAE and benchmark metrics for the daily timeframe................................................ 50

Table 6: LSTM and benchmark metrics for the weekly timeframe ............................................ 51

Table 7: LSTM and baselines for the daily timeframe ............................................................... 52

Table 8: CNN and baselines for the weekly timeframe ............................................................. 54

Table 9: CNN and baselines for the daily timeframe ................................................................. 54

Table 10: stat-lstm hybrid model and baselines on weekly data ................................................. 55

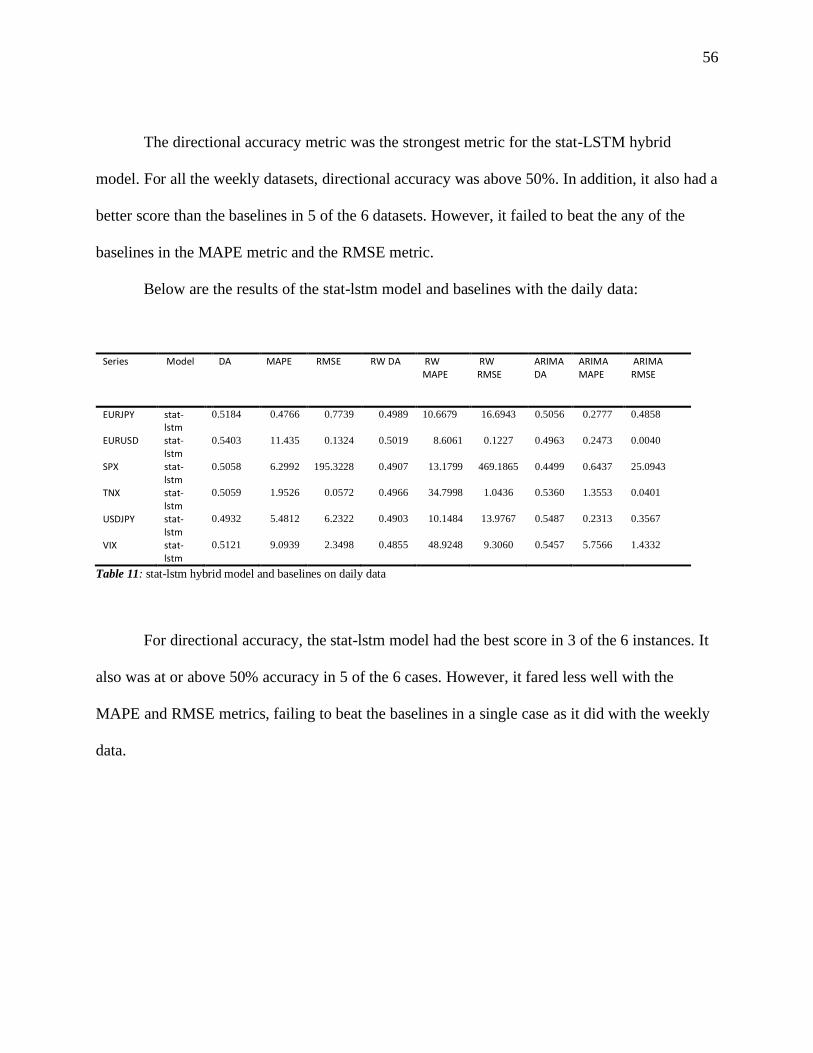

Table 11: stat-lstm hybrid model and baselines on daily data .................................................... 56

Table 12: cnn-lstm hybrid model and baselines on weekly data ................................................ 58

Table 13: cnn-lstm hybrid model and baselines on daily data .................................................... 58

Table 14: SDAE Ensembled values and their relative improvement .......................................... 60

Table 15: LSTM Ensembled values and their relative improvement .......................................... 61

Table 16: cnn ensembled values and their relative improvement ............................................... 62

Table 17: stat-LSTM ensemble results and their relative improvement ..................................... 63

Table 18: cnn-lstm ensemble results and their relative improvement ......................................... 64

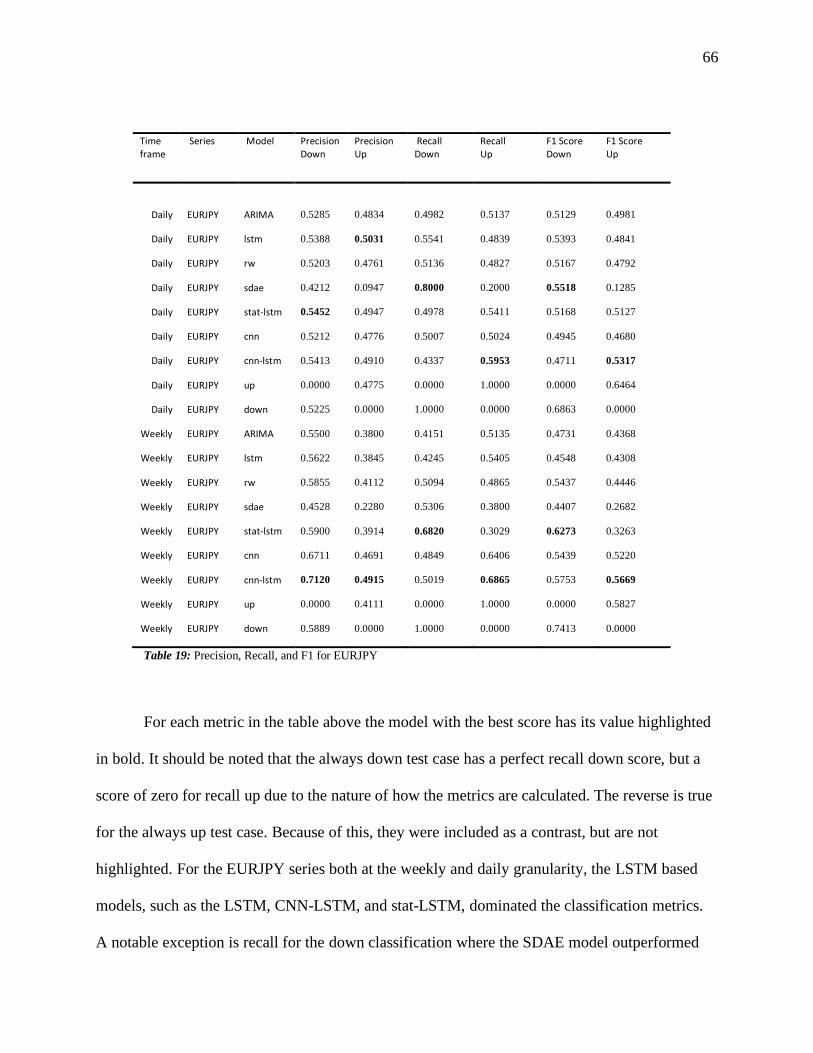

Table 19: Precision, Recall, and F1 for EURJPY ...................................................................... 66

Table 20: Precision, Recall, and F1 for EURUSD ..................................................................... 67

Table 21: Precision, Recall, and F1 on USDJPY ....................................................................... 68

ix

Table 22: Precision, Recall, and F1 for the SPX ....................................................................... 69

Table 23: Precision, Recall, and F1 for the TNX ...................................................................... 71

Table 24: Precision, Recall, and F1 scores for the VIX ............................................................. 72

Table 25: t+k ahead prediction metrics for EURJPY ................................................................. 74

Table 26: t+k ahead predictions for EURUSD .......................................................................... 75

Table 27: t+k ahead predictions for USDJPY............................................................................ 76

Table 28: t+k ahead predictions for the SPX ............................................................................. 77

Table 29: t+k ahead predictions for the TNX ............................................................................ 78

Table 30: t+k ahead predictions for the VIX ............................................................................. 79

Table 31: Best model by category: mean of 10 runs .................................................................. 80

Table 32: Best ensembled model by category ........................................................................... 81

Table 33: CNN Configuration Parameters ................................................................................ 93

Table 34: CNN-LSTM Configuration Parameters ..................................................................... 94

Table 35: LSTM Configuration Settings ................................................................................... 95

Table 36: stat-lstm configuration parameters ............................................................................ 95

1

Chapter 1

Introduction

Forecasting time series data is a subject of interest in multiple fields. However,

forecasting is made difficult by complex relationships and non-linearity in the data (Borovykh,

Bohte, & Oosterlee, 2017). This complexity has led to different approaches to constructing

forecasting models.

Neural network variations such as Convolutional Neural Networks (CNNs), Long Short

Term Memory (LSTMs), and Gated Recurrent Units (GRUs) have been used for time series

forecasts in different domains. Convolutional Neural Networks (CNNs), originally developed to

learn features in an image, have been adapted to forecast time series data (Borovykh et al., 2017;

Mittlelman, 2015). Borovykh et al. (2017), note that there can be correlations between financial

time series. The authors seek to exploit these correlations by using multiple time series as input

to train a CNN (Borovykh et al., 2017). In Mittelman (2015), the author uses a variant CNN,

known as an Undecimated Fully Convolutional Neural Network (UFCNN) to generate forecasts

on three different time series datasets.

GRUs and LSTMs were compared to another neural network model as a way to predict

time series in the work by Chung, Gulcehre, Cho, and Bengio (2014). In their research, the

authors use voice and music data as time series sequences upon which to evaluate the neural

networks. The paper concludes by noting that GRUs show superior performance with some of

the test data, but with other data, the LSTM demonstrates better performance (Chung et al.,

2014). GRUs have also been used to infer missing data to improve time series predictions for

clinical data (Che, Purushotham, Cho, Sontag, and Liu, 2018).

2

Other forecast research seeks to combine neural network variations to improve forecast

accuracy. In Xingjian et al. (2015), the authors combine the convolutional layers of a CNN with

a LSTM to increase the accuracy of short-term weather forecasts. The authors use time series

radar map data to forecast future radar map behavior. The convolutional layer is used to learn

significant spatial features in the data which is then fed into the LSTM network. This

combination of models enables effective short-term weather forecasting, outperforming a LSTM

model and traditional forecast models (Xingjian et al., 2015).

Problem Statement

The Autoregressive Integrated Moving Average (ARIMA) model is a traditional and

popular forecasting tool (Kardakos et al., 2013). However, models such as ARIMA often fail to

make effective forecasts due to the complexity of the relationships in the data (Borovykh et al.,

2017). In Zhao, Li, and Yu (2017), the authors focus on using a neural network variant known as

a Stacked Denoising Autoencoder (SDAE) to predict the price of oil. However, forecasting a

time series such as crude oil or a stock price is challenging because of the nonlinearity, complex

dynamics, and potential non-stationarity of the data (Cao, Li, & Li, 2018; Zhang, Zhang, &

Zhang, 2015). Combinations such as this lead to a complex system whose mechanisms are not

well understood (Alvarez-Ramierz, Soriano, Cisneros, & Suarez, 2003).

In addition to the complex dynamics that make up a financial time series, a time series

itself is related to both data at the current time as well as data from earlier times. Information

from earlier times will be lost if only the present time is considered. Traditional neural networks

(ANNs) can fail to capture this without a mechanism to maintain state. Variant neural networks

such as recurrent neural networks (RNNs) have the ability maintain the state of recent time series

3

movement (Cao, et al., 2018). Because of the inherent complexity in time series data, an accurate

forecast is difficult (Boroyvkh et al., 2017).

Dissertation Goal

The primary goal of this research was to develop and evaluate improved neural network-

based models for time series forecasting. The models were compared to the ARIMA and random

walk models as baselines using benchmark datasets.

The Zhao (2017) dataset consists of WTI price data at the monthly level. Because of this

relatively coarse granularity, only 365 observations are available in this dataset. To facilitate as

accurate an assessment as possible, model variations were tested on datasets found in the

literature beyond the WTI data with more observations. These include the S&P 500 (SPX) broad

market index found in Wiese et al., (2020); an interest rate (TNX) and volatility (VIX) index

found in Borovykh et al., (2017); and the forex currency pairs Euro – Dollar (EURUSD), Dollar

– Japanese Yen (USDJPY), and the Euro – Japanese Yen (EURJPY) found in Mayo, M. (2012).

This study started by comparing the SDAE model against the baselines on the WTI

dataset. The SDAE and baselines were then run on the other time series to look for

generalizability. Next, neural network models such as the CNN, LSTM, and hybrid variants were

developed and evaluated against results produced by the SDAE and baselines.

Comparisons were based on the metrics that are used in Zhao et al. (2017): Root Mean

Squared Error (RMSE), Directional Accuracy (DA), and Mean Absolute Percentage Error

(MAPE). The precision, recall, and F1 scores as defined in Opitz & Burst (2019) were used to

analyze directional accuracy prediction. The goal was to develop models that perform better than

the ARIMA and random walk baselines on the datasets found in the literature.

4

Research Questions

The primary research question for this study is forecast accuracy: is it possible to improve

upon the results from the baselines on the selected datasets? An investigation was done into

neural network variations that included configuration variations such as the network depth,

number of neurons per hidden layer, and activation functions in an effort to improve upon the

forecast. The question posed was then answered with the use of metrics taken from the literature.

Relevance and Significance

Accurate time series predictions are difficult because of the non-linear relationships in the

data as well as noise. Common approaches to time series forecasting such as ARIMA models do

not capture the complex relationships effectively (Borovykh et al., 2017). This study used a

random walk and ARIMA model as baselines and compared them with neural network-based

approaches. The models used in this dissertation are briefly described next.

The Random Walk Model

The random walk model has been used as a baseline in previous studies (Mittlelman,

2015; Zhao et al., 2017). The random walk is described in Hyndman & Athanasopoulos (2018)

as forecasting the current value, 𝑦𝑡, as the value from the previous time, 𝑦𝑡−1, plus a white noise

or random element, 𝜀𝑡 . In equation form:

𝑦𝑡 = 𝑦𝑡−1 + 𝜀𝑡

(Hyndman & Athanasopoulos 2018).

5

The ARIMA Model

The ARIMA model is a simple and popular model for forecasting. Also known as the

Box-Jenkins method, it was originally described in their 1970 textbook, Time Series Analysis:

Forecasting and Control. The ARIMA model is defined in Hyndman & Athanasopoulos (2018)

as:

𝑦𝑡′ = c + 𝜙1𝑦𝑡−1

′ + …. + 𝜙𝑝𝑦𝑡−𝑝′ + 𝜀𝑡 + 𝜃1𝜀𝑡−1+ … + 𝜃𝑞𝜀𝑡−𝑞

In the ARIMA model the output 𝑦𝑡′ is the differenced series at time t, and the right-hand side of

the equation are predictors including lagged values of 𝑦𝑡 and lagged errors. Differencing is the

computation of the differences between sequential observations and can be used to stabilize a

time series’ mean (Hyndman & Athanasopoulos, 2018).

The equation to determine the output is specified in terms of the following:

c, 𝜙, and 𝜃 are parameters of the model to be estimated

𝜀𝑡 is noise or the error term

p is the order of the order of the autoregressive process

q is the order of the moving average

(Hyndman & Athanasopoulos, 2018)

Convolutional Neural Network

Convolutional Neural Networks have grown in popularity as an effective tool for image

recognition after the seminal paper by LeCun, Bottou, Bengio, and Haffner was published in

1998. In this paper, CNNs were introduced for pattern recognition problems such as speech or

handwriting. A CNN passes data through a convolutional layer containing feature maps to

extract features out of the data. The data is then sub-sampled to reduce the sensitivity to specific

6

inputs and is eventually passed into a fully connected layer (LeCun et al., 1998). A fully

connected network is one where each node (or neuron) is connected to all of the nodes in the

next layer.

A convolutional transform is a mathematical operation on the input data that learns to

recognize features within the data. A CNN has layers of convolution operations applied to the

input. The weights for the convolutions are learned through training on input data (Borovykh et

al., 2017).

The CNN’s ability to effectively extract features and recognize patterns have been

adapted to the problem of time series forecasting (Borovykh et al., 2017; Mittelman, 2015). As

part of the adaption to time series forecasting, the shape of the convolutional operations is

modified to one dimension, along the sequence of input data. The convolutions operate on the

input data as a sliding window, moving across the input data and having the product of the

convolution filter and the data calculated. This process allows the model to learn features or

repeating patterns in the data. These abstract features and patterns are used to forecast future

values (Borovykh et al., 2017).

A max-pooling layer is used to make the input less subject to small variations and is a

common feature in many CNN implementations. However, for time series forecasting, this may

not be a desired feature (Mittelman, 2015).

Tunable parameters for the model include the number of convolutional filters, the size of

the filter, the number of layers in the neural network, the number of neurons in each layer, as

well as the activation function. Cross validation training on the input data is used to select or tune

the parameters (Mittelman, 2015).

7

Stacked Denoising Autoencoder

A neural network variant, known as a stacked denoising autoencoder (SDAE), is used as

the central algorithm in Zhao et al.’s 2017 research. The SDAE starts with an autoencoder, a

neural network that maps an input vector to a hidden representation of the input’s features. An

autoencoder is a neural network with one hidden layer where the length of both the input and the

output are of the same size. There are two parts to an autoencoder: encoding to a hidden

representation, and then decoding to an output of the same length as the input. For input vector x

of length d, input x is mapped to a hidden representation y with the following function:

y = 𝑓𝜃

(𝑥) = 𝜙𝑓(𝑊𝑥 + b)

𝑓(𝑥) has as parameters W, a 𝑑′ ∗ 𝑑 weight matrix, b a bias vector, and 𝜙() a non-linear

activation function. The hidden representation is then translated back to vector z, a reconstruction

of input vector x:

z = 𝑔𝜃′

(𝑦) = 𝜙𝑔(𝑊′

y + 𝑏′)

where 𝑊′ is a weight matrix, 𝑏′

is a bias vector and 𝜙() is a non-linear activation

function.

In the variation known as a denoising autoencoder, noise is added to the input, so the

model learns to construct a clean representation of the corrupted input. The algorithm becomes

stacked as denoising autoencoders are layered in the model (Zhao et al., 2017; Vincent,

Larochelle, Lajoie, & Bengio, 2010).

Long Short Term Memory Neural Networks

Recurrent Neural Networks (RNNs) capture a time element in the data by maintaining a

current state within an individual neuron that is dependent upon a previous state. However, it is

8

noted in Chung et al.’s (2014) work that RNNs can be difficult to train using a traditional

backpropagation method because the gradient in the training algorithm can either vanish to zero

or grow without bound and explode (Chung et al., 2014).

The LSTM uses the concept of a memory cell, which uses gates to control the flow of

information to and from the cell (Hochreiter & Schmidhuber, 1997). The LSTM unit sums the

weighted input signals as a traditional neural network, but also applies a memory value c that is

controlled by a modulation function o:

ℎ𝑡𝑗 = 𝑜𝑡

𝑗 tanh (𝑐𝑡

𝑗 )

Where:

ℎ𝑡𝑗is the output of the activation function for an LSTM

𝑐𝑡𝑗 is memory at time t

𝑜𝑡𝑗 is the output gate that modulates the memory content exposure

j represents the j-th LSTM unit

(Chung et al., 2014)

The LSTM neural network architecture was developed by Hochreiter & Schmidhuber in

1997. The LSTM maintains state like an RNN but addresses the issue RNNs have with the

training gradient (Hochreiter & Schmidhuber, 1997). The cell structure characteristic of LSTMs

allows it to effectively model time series data with long time lags. In addition, testing has shown

LSTMs are able to handle noise in the data and can work well with different parameter settings

such as learning rates (Hochreiter & Schmidhuber, 1997).

9

The Gated Recurrent Unit

Gated Recurrent Units, GRUs, are based on RNNs but modify the activation function

with gating units, like the LSTM. GRUs have gating units to control the flow of information

within a cell but do not have separate memory cells. GRUs have been used for language

translation (Cho, Van Merrienboer, Bahdanau, and Bengio 2014a) and sequence prediction

(Chung et al., 2014). The gating mechanism found in GRUs is described in (Cho et al., 2014b).

The architecture of a GRU is influenced by the design of an LSTM but is simpler and

streamlined. The GRU architecture is as follows (Cho et al., 2014b):

Figure 1: A GRU cell

Where the activation of the jth hidden unit is computed as a function of the states above:

𝑟𝑗 = 𝜎 ([𝑊𝑟𝑥 ]𝑗 + [𝑈𝑟ℎ(𝑡−1) ]𝑗)

Where 𝜎 is a logistic sigmoid function.

[. ]𝑗is the jth element of a vector

x is the input and ℎ(𝑡−1) is the previous hidden state

𝑊𝑟 and 𝑈𝑟 are weight matrices which are learned through training

The update gate 𝑧𝑗is computed by:

𝑧𝑗 = 𝜎 ([𝑊𝑧𝑥 ]𝑗 + [𝑈𝑧ℎ(𝑡−1) ]𝑗)

(Cho et al., 2014b)

10

Ensembling

Ensembling is a technique used to improve model performance by creating a blended

prediction from multiple models. In Zhao et al.’s 2017 research on oil price forecasting, the

authors use an ensemble variation known as bagging. The final ensemble prediction is an

average of the individual models’ predictions (Breiman, L., 1996). By creating a composite

prediction with multiple models, it is possible to reduce overfitting (Goodfellow, Bengio, &

Courville, 2016). This study used ensembling as a method to look for further performance

improvement. Results with and without ensembling are presented in Chapter 4.

Barriers and Issues

Neural networks can require large datasets to obtain reliable results (Borovykh et al.,

2017). The Zhao dataset is relatively modest in size at 365 observations, each with 200 features.

The results obtained by the neural networks proposed for this study may be influenced by the

limited size of the dataset. When the number of features in a dataset, p, approaches the number of

rows, n, there is risk in overfitting the data when training a model (James et al., 2013).

Overfitting can happen if the features are perfectly correlated to the response variable or

if there is no correlation to the response variable. A good way to guard against this is to use a

hold out or test set for model validation (James et al., 2013). However, even when a test set is

used, certain metrics such as 𝑅2 will increase as the number of features in a model increases, so

care is warranted when judging the fitness of a particular model with a large number of features

in comparison to the number of observations (James et al., 2013).

The possibility exists that there still may be a coincidental correlation between the model

and the data. In Bao et al. (2017), the authors express concern over the success of models trained

on financial data being due to a coincidental correlation with data, rather than the power of the

11

model itself. To reduce the likelihood of this being the case, and to prove the robustness of their

results, the authors test their model on 6 different financial series (Bao et al., 2017). In order to

mitigate the risk of overfitting to a dataset that is limited in size, this study also used 6 different

time series and focused on two levels of granularity: the daily and weekly levels for a total of 12

datasets to be analyzed.

Another issue is hardware capacity. The limitation of the hardware capabilities selected

for this study imposes an upper bound on the size of the models that can be trained for the study.

Dean et al. (2012) notes that models can grow so large as to not fit in a single computer’s

memory. To help mitigate this risk, in addition to the local hardware used, models were also

trained using Google’s Collaboratory.

Assumptions, Limitations, and Delimitations

Development environment: Python was selected as the programming language since it is

a common language used for neural network development. The Keras library was also selected

for similar reasons: it is a popular choice for specifying neural network architectures.

Resources: the resources used for this project include a laptop and workstation. The

laptop has a 4 core Intel i7 processor, 16GB of RAM, and an nVidia GeForce GTX 960M

graphics card. The workstation has an 8 core AMD FX 8530 processor, 16GB of RAM, and an

nVidia GeForce GTX 650 graphics card. To facilitate the research, Google’s Collaboratory was

also used to train models.

12

Definition of Terms

ANN: Artificial Neural Network

ARIMA: Auto regressive integrated moving average, a method for time series

forecasting.

Back-propagation: an algorithm that works to minimize the error of a model through

repeated iterations of training. This is a time consuming and resource intensive process.

Ensembling: combining the output of more than one model to improve prediction

accuracy.

CNN: Convolutional Neural Network.

Epoch: during model training, an iteration where the entire training set is presented to the

model one time.

GPU: Graphics Processing Unit.

GRU: Gated Recurrent Unit, a variant RNN.

LSTM: Long Short-Term Neural Network, a variant RNN.

RNN: Recurrent Neural Network.

SDAE: Stacked Denoising Autoencoder, a neural network variation.

WTI: West Texas Intermediate, a tradable crude oil commodity

Summary

Time series forecasts are made difficult due to nonlinearity and complex relationships in

the data. Several neural network variations have been applied to the challenge of time series

forecasting. Convolutional Neural Networks, developed for image recognition, have been

successfully applied to time series data (Borovykh et al., 2017; Mittlelman, 2015). Recurrent

13

neural network variations such as LTSMs and GRUs have memory cells and provide a temporal

factor in model training (Chung et al., 2014).

This study’s goal was to improve upon the forecast model baselines, ARIMA and random

walk, by examining neural network variations across different datasets. Methods of evaluating

the quality of model prediction includes metrics used in Zhao et al.’s (2017) work as well as

metrics to evaluate directional accuracy as a classification problem.

14

Chapter 2

Review of the Literature

Introduction

The purpose of this literature review is to expand upon the motivation for the proposed

research. The literature review is divided into three main parts. The first section will discuss the

challenge of time series forecasting. The second section reviews different approaches to time

series forecasting, concluding with a third section on ensembling as a way to improve model

accuracy.

The Challenge of Time Series Forecasts

Accuracy with time series forecasts is made difficult by the non-linearity of the data. In

addition, there is quite often a significant amount of noise in the data that further contributes to

the difficulty, making temporal relationships within the data hard to discern (Borovykh et al.,

2017). A good model will need to be robust and resistant to the noise in the data. With financial

data, the difficulty is increased because conditions change over time, limiting the utility of long

periods of data. (Borovykh et al., 2017).

Financial markets are highly unpredictable because of their characteristic high volatility.

The influences on the financial markets can be classified into two broad categories: macro and

micro variables. Macro variables include things like economic policy and the gross national

product (Zhou et al., 2016). Financial series such as the price of oil have been shown to be

correlated with the gross domestic product growth rate (Mostafa & El-Masry, 2016). By contrast,

micro variables are things like events, rumors, and the irrationality of investors (Zhou et al.,

15

2016). These influences combine to create non-linear behavior in the financial markets (Zhou et

al., 2016). Some financial series will alternate between periods of high and low volatility

(Morana, 2001). This volatility can add to the difficulty of an effective price forecast (Mostafa &

El-Masry, 2016). Time series models such as ARIMA often fail to capture the complexity of

financial markets (Zhou et al., 2016).

There is also a debate on whether financial markets are themselves predictable. The idea

of the Efficient Market hypothesis was first proposed in Malkiel & Fama (1970), stating that

current prices reflect all known information and so it is impossible to get an edge with a

forecasting technique (Nelson et al., 2017). However subsequent work has shown that there is

reason to question this hypothesis (Lo & MacKinlay, 2011; Nelson et al., 2017).

A Review of Approaches to Time Series Forecasting

Given the complexity of creating an accurate time series forecast, different variations of

neural networks have been proposed to improve forecast reliability. This section reviews neural

network variations and provides an overview of how they are used to address time series.

Time Series Forecasting with Convolutional Neural Networks

CNNs, originally developed for image recognition, have been adapted to time series

forecasting. A defining feature of the CNN is the convolutional layer, which consists of

mathematical operations that are applied to the input along a sliding window. This allows the

model to learn significant features or patterns within the input data. These patterns can then be

used to forecast future values (Borovykh et al., 2017).

16

In Borovykh et al. (2017), the authors use the concept of a dilated convolution to capture

long term dependencies. A dilated convolution has a dilation factor, d, where the model applies

the convolutional transform to every dth element in the input. This approach to convolutions

allows the model to learn dependencies farther apart than would otherwise be the case. Multiple

dilated convolutions are stacked in layers, with the dilation factors increasing according to a

power of 2. Part of the transformations include the wavelet transforms which seek to match a

function’s changes to a periodic wavelet function (Borovykh et al., 2017).

The structure of the neural network layer is common to other CNNs where, rather than

the neurons being fully connected between layers; neurons are instead locally connected to

regions within the input. This allows the CNN to learn features within the input. The

convolutions, wavelet transforms, and locally connected neural network combine to create the

WaveNet architecture used in the research (Borovykh et al., 2017).

The authors use multiple correlated time series as features for the input data with the aim

of leveraging the correlations to generate a better forecast. The model will then use the history of

the time series to be predicted as well as the related time series to learn relationships and features

within the data. This strategy is adopted to reduce noise within the data and improve the

robustness of the forecast. The data used for the research is the S&P 500 data, the volatility

index, as well a 10-year interest rate index (Borovykh et al., 2017). To test the performance of

the model, the authors attempt to forecast the day head value of the S&P 500. In addition, the

model architecture is tested on a combination of several Forex exchange rates to exploit the

patterns between currency pairs (Borovykh, et al., 2017). The authors divide the data into a

training period of 750 days and a test period of 250 days. The test data is used for the day ahead

17

predictions. The range of the data is from 01-01-2005 to 12-31-2016 and is split into nine periods

where the test data does not overlap with the training data (Borovykh et al., 2017).

Results of the CNN model plus the WaveNet transform compare favorably to the LSTM

architecture used as a baseline. Training time for the CNN model was faster than the LSTM

baseline (Borovykh et al., 2017).

When used for image processing, CNNs typically use a pooling layer between

convolutional layers to reduce the size of the input to the neural network. For time series, the

pooling layer can cause a loss of information and impact forecasting (Mittleman, R., 2015). In

Mittleman (2015), the author proposes an undecimated fully convolutional network (UFCNN)

where the input and output of the model have the same dimensions. Wavelet transforms are also

used in this research as part of a deconvolutional stage to match the input and output dimensions.

The UFCNN is based on a Fully Convolutional Network (FCN). The FCN uses max-

pooling layers characteristic of CNNs as a downsampling operation. The convolutions plus max-

pooling operations are used so that features within the data are learned, but the dimensions of the

input are preserved in the output of with upsampling operations that pad the data with zeros

(Mittleman, R., 2015). The UFCNN in Mittleman (2015) takes a different approach to

upsampling and downsampling. Instead of padding the data, the UFCNN takes inspiration from

wavelet transforms which are used so that filters at the different levels have corresponding

upsampling operations (Mittleman, R., 2015).

The UFCNN in Mittleman (2015) was tested on music datasets and high frequency

trading data. The music data includes the MUSE and NOTTINGHAM datasets consisting of an

88-dimension vector where each dimension is a musical note. The UFCNN was trained to

18

forecast the vector at the next timestep. To judge the effectiveness of the new model on the

music dataset, the mean squared error metric is used. When the Middleman (2015) UFCNN was

compared to an FCN, the UFCNN demonstrated better performance. When compared to the

RNN and LSTM baselines, the UFCNN outperformed both (Mittleman, R., 2015)

The high frequency trading data was obtained from the Circulum Vite site which

sponsors machine learning competitions on financial data. The financial data includes price and

volume plus other information sampled at two to three times per second, over a period of one

year. The data was partitioned into approximately eight months of training data, two months of

validation data, and two months of test data (Mittleman, R., 2015). The UFCNN algorithm was

trained as a classifier to predict at each time step whether the best action was to buy, sell or do

nothing. To judge the effectiveness of the model, the metrics of profit per time step and

classification accuracy are used. Other models used in the comparison include an RNN, a

random approach, and the Viterbi algorithm which sees the entire dataset and is used as a best

case upper bound for performance. The UFCNN outperformed both the random model and RNN

in both the profit per time step, and classification accuracy metrics (Mittleman, R., 2015).

Time Series Forecasting with Recurrent Neural Networks

RNNs are neural networks that maintain state and so are candidate architectures for

sequence and time series prediction. However, when trained, they suffer from issues with the

training gradient. A variation on RNNs, LSTMs, also maintain state, but do not suffer from

training gradient problems (Hochreiter & Schmidhuber, 1997).

In Nelson, Pereira, & Oliveira (2017), the LSTM is used to forecast a set of stocks from

the Brazilian market. The model in the study was designed as a classification model to predict an

19

up or down movement in a stock’s price. The data collected was from 2008 to 2015 at 15-minute

intervals. The difference of the logarithm function between timesteps was used as a transform to

stabilize the data series. In addition, 175 technical indicators were generated as features from the

price and volume of the stocks (Nelson et al., 2017).

The model in the study was trained on 10 months of data prior to a target day. The

previous week to the target day was used as an out of sample test set. The trained model was then

used to predict price movement for the following trading day. Each day a new model would be

trained for use on the following day. Metrics included for model evaluation were accuracy,

precision, recall, and the F1 score. The LSTM model was compared to a multi-layer perceptron,

the random forest, and a random model. The results of the study were very favorable to the

LSTM as a tool for time series forecasting (Nelson et al., 2017).

Another variation on the RNN is the Gated Recurrent Unit or GRU which has been

applied to the challenge of time series prediction. In Che et al. (2018), the authors use a GRU to

forecast mortality rates from healthcare data that contains missing values. The premise of the

study is that the patterns of missing data are itself information of a sort that can be leveraged as a

feature for the model. The authors create a new feature by looking at the missing data and

associating it with categorical values of other features including mortality and diagnosis. A

Pearson correlation was used to establish the statistical soundness of the association. It was

observed during the study that features with a low rate of missing values tended to have a high or

negative correlation with the labels of interest. The patterns of the missing data are then used as a

feature, rather than trying to impute the missing data prior to model construction. (Che et al.,

2018).

20

The model created in the study uses two features created with the missing data patterns: a

mask and time interval. The mask is a vector that denotes whether or not a feature is missing at a

given timestamp t. The mask is 1 if a feature is present, else it is 0. The time interval records the

number of timesteps since the last observation of a given feature. This allows the model to be

trained to recognize long term patterns as well as patterns within the missing data to make a

forecast (Che et al., 2018).

The authors name their model configuration GRU-D. This model is compared to other

models including support vector machines, random forests, and other GRU variations with

imputed values for missing data. GRU-D, by leveraging patterns in the missing data as a novel

feature, outperforms the other models. The authors note that their model is limited in that if there

is no pattern in the missing information, this will have a negative impact on model performance

(Che et al., 2018).

Convolutional Neural Networks and LSTMs have been combined as a way to improve

forecast accuracy. In Xingjian, Chen, Wang, & Yeung (2015), the authors seek to use a hybrid

CNN-LSTM model, known as ConvLSTM, as a way to predict short term weather events such as

rainfall intensity over a local region in a 0 to 6 hour time window. Predictions are made with past

radar map images, arranged in a series of timesteps, as a primary input. Each radar map is

represented as a matrix of M rows and N columns. Each pixel within this map is considered a

measurement. The radar images are arranged in a temporal order. This input then is used to

predict radar map images one or more timesteps into the future (Xingjian et al., 2015).

To gauge the effectiveness of their approach, Xingjian et al. (2015) compare their

ConvLSTM model against a Fully Connected LSTM (FC-LSTM) model on two datasets: a

21

synthetic dataset known as the Moving-MNIST dataset, and radar echo image data. With the

radar data, the ConvLSTM model is also compared to a conventional forecasting method known

as Real-time Optical flow by Variational methods for Echoes of Radar, or ROVER (Xingjian et

al., 2015). The FC-LSTM used in the authors’ research is based on an architecture used in

Srivastava, Mansimov, & Salakhudinov (2015) to predict video sequences. This study uses an

LSTM as an encoder to learn the representation of video sequences and then an LSTM decoder

to predict future sequences (Srivastava et al., 2015).

The Moving-MNIST dataset consists of 64 x 64 frames that contain a handwritten digit

that is moving around inside the frame. There are 10 frames for the input and 10 as output

(Xingjian et al., 2015). The radar echo dataset used in the research is a sample of radar data

collected in Hong Kong from 2011 to 2013. The radar data is sampled at the rate of once every 6

minutes. Because the authors are trying to predict rain patterns, they select the top 97 rainy days

during this period as their dataset. The radar images are cropped to the central 330 x 330 region

and converted to gray scale. The data is then further filtered so it becomes a 100 x 100 image

(Xingjian et al., 2015).

The ConvLSTM architecture consists of convolutional operations and LSTM nodes that

are stacked into one or more layers. The ConvLSTMs themselves may also be stacked. There are

two main parts to the structure: an encoding network and a forecasting network. The encoding

network learns a representation of the input and the forecasting network provides the prediction

(Xingjian et al., 2015).

When compared to the FC-LSTM, the proposed ConvLSTM outperforms the model

using a cross-entropy metric on the Moving-MNIST dataset. With the radar echo dataset, the

authors use several metrics for measuring the accuracy of a weather forecast, including the

22

rainfall mean squared error, critical success index, false alarm rate, probability of detection, and

correlation. The ConvLSTM outperforms both the FC-LSTM and the more conventional

ROVER forecasting method under all the rainfall metrics (Xingjian et al., 2015).

Time Series Forecasting with Stacked Autoencoders

An autoencoder is a neural network variation that seeks to learn a representation of the

input and then reconstruct the input as output. During training, a hidden layer learns features

within the data (Bao, Yue & Rao, 2017). In Zhao et al. (2017), the authors use a stacked

denoising autoencoder (SDAE) to forecast the price of crude oil. As described in the Relevance

and Significance section, a SDAE consists of more than one autoencoder stacked in layers. The

stacked autoencoder becomes denoising when noise is added to the input and trained against a

clean version of the data as a way to remove the noise (Zhao et al., 2017).

Zhao et al.’s (2017) work seeks to predict the price of West Texas Intermediate (WTI)

crude oil using a SDAE. To build a base dataset, the authors collect data from the Energy

Information Administration (EIA), the Federal Reserve Bank (FRB), and Yahoo! Finance. A

total of 198 features are gathered from these sources. Multiple related datasets are then created

from this base dataset using a technique known as bagging. Bagging, or bootstrap aggregation,

starts with a dataset of size N and creates new datasets also of size N by sampling with

replacement from the base dataset (Breiman., L. 1996).

The SDAE architecture is replicated, and multiple models are trained using the bagged

datasets. For prediction, the multiple models are used to generate a composite prediction with a

technique known as ensembling (Zhao et al., 2017). Ensembling leverages the predictive power

23

of multiple models to create a composite prediction that can have better performance than

individual models (Goodfellow et al., 2016).

To judge the effectiveness of this technique, the authors compare their model to several

other forecast models including a random walk, MRS (Markov Regime Switching), FNN

(Feedforward Neural Network), and a Support Vector Machine (SVR). The FNN and SVR are

also ensembled on a bagged dataset for comparison. The comparison of the models includes

metrics for prediction accuracy and statistical methods to test the model validity.

The metrics for prediction accuracy include directional accuracy, root mean squared error

(RMSE), and mean absolute percentage error (MAPE) (Zhao et al., 2017). Statistical methods

used to analyze the proposed method include the Wilcoxon signed rank test, the forecast

encompassing test, and the reality check. The Wilcoxon signed rank test is used to compare two

datasets that do not have to be normally distributed (Devore, J.L., 2011). The forecast

encompassing test is used to see if there is a statistically significant difference in the results of

the models (Harvey et al., 1998). Finally, the reality check looks for a false positive: given a

single dataset, if enough models are used to predict on it, there is the possibility of a model

showing a favorable result due to chance (White, H., 2000).

In Bao et al.’s (2017) publication, the researchers combine a wavelet transform, and two

neural networks: a stacked autoencoder and a LSTM network. Together, these components are

placed in a pipeline to create a composite model that is referred to as a WSAEs-LSTM (Bao et

al., 2017).

To generate a prediction, data is first passed through a wavelet transform as a way to

stabilize an irregular series such as financial data. Next, the data is passed through an

24

autoencoder in order to detect significant features. The data is then passed into a LSTM network

to generate a prediction (Bao et al., 2017).

This composite model is used to forecast the price of six separate stock market indices

including the Chinese CSI 300, the Indian Nifty 50, the Hang Seng from Hong Kong, Toyko’s

Nikkei 225, and the S&P 500 and Dow Jones Industrial Average from the United States. The

authors tested their novel architecture in multiple markets in order to see how well their model

would generalize across different time series. The authors sought indices from markets that can

be considered developing, developed, and a middle ground between the two in an effort to test

the robustness of their model (Bao et al., 2017).

To evaluate their model’s accuracy, Bao et al. (2017) used three primary metrics: MAPE,

the R correlation coefficient, and Theil’s inequality coefficient (Bao et al., 2017). Other models

were used as a basis for comparison to the WSAEs-LSTM; these include an RNN for a

performance benchmark, a LSTM, and a combination of wavelet transform and LSTM known as

the WLSTM. This last model was used to validate the efficacy of including an autoencoder as a

method of learning features in the data. The autoencoder as a means of learning features within

the data is what the authors view as their main contribution (Bao et al., 2017).

The study concluded by noting that their WSAEs-LSTM outperformed the other models

included in the study using all three of the aforementioned metrics. In addition, the authors note

that the models showed a correlation between the magnitude of their errors when the results were

compared by similar market development state. For example, the WSAE-LSTM had similar

errors when the S&P 500 and Dow index were measured, but the difference between the errors

was greater when the results of the S&P 500 and CSI 300 were compared (Bao et al., 2017).

25

Ensembling Multiple Models to Improve Prediction

In Zhao et al. (2017), ensembling is used to combine multiple independent model

predictions to increase the accuracy of a prediction. Ensembling a set of models can provide

more robust performance on out of sample data than a single model. While the most accurate

model in a set may outperform its ensemble, risk of using a poorly performing model on out of

sample data is reduced when an average prediction is taken (Polikar, R., 2006).

Ensembling is also a way to generate a composite prediction when the data is too large or

too complex to be accurately represented by a single model. For example, if the features are

radically different, such as a mix of image data, text data, and time series data, it is unlikely that

a single model can be trained to learn all of the features within the data (Polikar, R., 2006).

However, in such instances, it is possible to train a model on each class of data, and then

generate a composite prediction through ensembling. This is an example of data fusion (Polikar,

R., 2006).

Because of the noise and complexity inherent in most datasets, building a model with

perfect prediction accuracy is not realistic. However, it is possible to build a model that is correct

most of the time. With ensembling, the performance of such a model can be improved by adding

it to a group of other models (Polikar, R., 2006). To generate different models from a single

dataset, it is possible to use bagging, creating a new dataset from the original dataset by sampling

with replacement (Polikar, R., 2006; Zhao et al., 2017).

In Opitz & Maclin (1999), the researchers conducted an empirical study of ensembling

methods. The authors found that good ensembles are created when the models that compose the

ensemble make errors on different parts of the input. Citing earlier research, the authors state that

26

the best ensembles are composed of accurate models that otherwise disagree as much as possible

(Opitz & Maclin, 1999). One approach to having diverse but accurate models is to separate the

input into subtasks and then train models on these subtasks. These models are then combined

with a gating method to create a composite prediction (Opitz & Maclin, 1999).

Opitz & Maclin (1999) compare two variations on ensembling: bagging and boosting.

While bagging is generating a new dataset by sampling the original dataset with replacement,

boosting trains models serially where the training set of the next model is selected based on the

errors in the previous classifiers. Observations that the models have performed poorly on are

given more weight for new model training iterations. By doing this, boosting attempts to build

new models that strengthen currently poor performing areas (Opitz & Maclin, 1999).

The authors examine two forms of boosting, Arcing and Ada-boost, in addition to

bagging (Opitz & Maclin, 1999). The research demonstrated that bagging and boosting will

improve prediction results in most circumstances, when compared to a single model. However,

the authors note that in some instances boosting led to overfitting of the data by providing too

much weight to observations that were in actuality noise. In these instances, boosting hurt

accuracy (Opitz & Maclin, 1999).

Summary

This section started with a discussion of the challenges of time series forecasting: the

complex relationships in the data are hard to model. After the problem was introduced, the

literature review went into detail about different approaches to effectively modeling time series

data and using ensembling to improve model prediction. Chapter 3 will introduce the

methodology used in this study.

27

Chapter 3

Methodology

The goal of this dissertation was to develop and evaluate neural network-based models

for forecasting time series data, looking for improvements. This section describes the approach

that was taken to achieve this objective. Below is an outline of the steps that were taken as part

of the research. Each step will be expanded upon in turn:

1. Define the datasets

2. Create Random Walk and ARIMA models as a baseline

3. Create a SDAE model similar to Zhao et al. (2017)

4. Create neural network variations such as RNN variants, CNNs, and hybrid models then

compare them to extant methods on the selected time series

5. Model tuning

6. Use ensembling to improve model prediction

7. Compare the models using the performance analysis metrics

The Datasets

Zhao et al. (2017) focused their research on crude oil prices, specifically West Texas

Intermediate (WTI). The dataset consists of the monthly WTI price from January 1986 to May

2016. The data is sampled monthly for a total of 365 data points. There are 200 features in the

data including data related to crude oil production such as active rig count, road product

supplied, and aviation gasoline supplied. Financial indicators are also included as features. More

details about the dataset can be found in Appendix A. For Zhao et al.’s (2017) research, the first

28

80% of the data is used as a training set. The remaining 20% is used as test data. This dataset was

used for initial comparison of the SDAE model to the ARIMA and Random Walk baselines.

Because of the relatively limited number of observations available with the WTI and

related data, the study was broadened to compare the ARIMA and random walk baselines against

the SDAE and other neural networks on data found in the literature. This included a broad

market index, the SPX (Wiese et al., 2020; Borovykh et al., 2017), an interest rate (TNX) and

volatility index (VIX) (Borovykh et al., 2017) as well as the currency pairs EURUSD, EURJPY,

and USDJPY (Mayo, M., 2012). To facilitate a comparison with more observations, the daily

and weekly granularity was selected for each series bringing the total number of datasets to 12. A

total of 15 years of data was selected spanning the timeframe from 1/1/2005 to 1/1/2020. For the

weekly datasets, there are 783 observations per series. For the daily data, the observations vary

between 3740 and 4490 due to the different trading days of each series.

Zhao et al.’s (2017) research used 80% of the data for training and 20% of data as a test

set on which the metrics were calculated. This study took a similar approach, but varied the

proportions as follows: 70% of a dataset was used to train the model, 18% was used as a

validation set, and the remaining 12% was used as a test set to calculate model metrics. The

validation set was used to prevent overfitting. After each training epoch, the resulting model was

evaluated with the validation set using the loss function. If the model stopped improving based

on the validation set testing, training was ended. Metrics were then calculated on the test set.

Create Baseline Prediction Models

To determine the effectiveness of the models, baseline predictions were

generated. Several studies (Kaboudan, M.A, 2001; Morana, C., 2001; Mostafa & El-Masry,

29

2016; Zhao et al., 2017) use a random walk model as a baseline for comparison. Other research

uses the ARIMA model (Adhikari, R., 2015; Kardakos et al., 2013). Given their prevalence in

the literature, the random walk and ARIMA models were used as baselines in this study.

Create the SDAE Model

In the paper by Zhao et al. (2017), the architecture of the SDAE used in their

study is described. The model includes three hidden layers consisting of two Denoising

Autoencoders (DAEs) and a Feedfoward Neural Network (FNN). The number of neurons in each

layer are 200, 100, and 10, respectively. This study duplicated this structure to be used on each

dataset.

Create Neural Network Variations

Variations of neural networks were explored to look for improvements. This included

neural network variants such as CNNs, RNN variations, and hybrid models.

Long Short Term Memory Neural Networks

Given its success in previous forecast research, the LSTM was used in this study. The

LSTM model was built in Python using the Keras library for neural networks. The architecture

was similar to this pseudocode:

lstm = Sequential()

lstm.add(LSTM(units, input_shape(timesteps, feature_count)))

lstm.add(LSTM(units, activation=activation_type))

lstm.add(Dense(units, activation=activation_type))

lstm.compile(loss=loss_type, optimizer=optimizer_type, metrics = list_of_metrics)

Figure 2: Pseudocode for a LSTM model

30

The LSTM was tuned by adjusting the following parameters:

• The number of hidden layers

• The number of neurons per layer (‘units’ in the pseudocode above)

• The number of previous timesteps the model uses to make a prediction

(‘timesteps’ in the pseudocode)

• The activation function (‘activation_type’ in the pseudocode)

Gated Recurrent Unit Neural Networks

GRUs have been used for sequence prediction in works such as (Cho et al., 2014a; Chung

et al., 2014). Given their success with sequence prediction, they were used as part of the hybrid

models in this study.

Keras was also used for developing the GRUs. The models featuring GRUs were

constructed in a manner similar to the pseudocode below:

gru = Sequential()

gru.add(GRU(units, input_shape(timesteps, feature_count)))

gru.add(GRU(units, activation=activation_type))

gru.add(Dense(units, activation=activation_type))

gru.compile(loss=loss_type, optimizer=optimizer_type, metrics = list_of_metrics)

Figure 3: Pseudocode for a GRU model

In a manner similar to the LSTM, the GRU was tuned by adjusting the following

parameters:

• The number of hidden layers

• The number of neurons per layer (‘units’ in the pseudocode)

31

• The number of previous timesteps the model uses to make a prediction

(‘timesteps’ in the pseudocode)

• The activation function (‘activation_type’ in the pseudocode)

Convolutional Neural Networks

The CNN’s abilities to effectively extract features and recognize patterns have been

adapted to the problem of time series forecasting (Borovykh et al., 2017; Mittelman, R., 2015).

A key feature of the CNN is the convolutional layer, where one or more mathematical

operations are applied to the input in order to find features or patterns within the data. Originally

used for image recognition, convolutions in a CNN are two-dimensional matrices. As an

adaptation for time series prediction, the shape of the convolution is modified to one dimension,

which moves along the sequence of input data (Borovykh et al., 2017; Mittelman, R., 2015).

Using Keras, the CNNs were built similar to the pseudocode below:

cnn = Sequential()

cnn.add(Conv1D(filters=num_filters, kernel_size=kernel_sz, activation=cnn_activation,

input_shape(timesteps, feature_count)))

cnn.add(MaxPooling1D(pool_size=pool_sz))

cnn.add(Flatten())

cnn.add(Dense(units, activation=activation_type))

cnn.add(Dense(units, activation=activation_type))

cnn.add(Dense(units, activation=activation_type))

cnn.compile(loss=loss_type, optimizer=optimizer_type, metrics = list_of_metrics)

Figure 4: Pseudocode for a CNN model

The parameters for a CNN neural network are similar to those of other neural networks:

• The number of hidden layers

32

• The number of neurons per layer (‘units’ in the pseudocode)

• The number of previous timesteps the model uses to make a prediction

(‘timesteps’ in the pseudocode)

• The activation function (‘activation_type’ in the pseudocode)

In addition to the parameters common to other neural networks, CNNs will have the

following parameters for the convolutional layer that can be adjusted:

• The length of the convolutional filters (kernel_sz)

• The number of convolutional filters (num_filters)

• The activation function for the convolutional layer (cnn_activation)

Hybrid Model Variations

Hybrid models were also used in this study including the CNN-LSTM, and statistics-

LSTM variations.

As part of model tuning for the hybrid models, one of the hyperparameters was the neural

network type: LSTM or GRU.

Hybrid Model: Statistics – LSTM Model

Inspired by the Smyl (2020) paper describing the M4 competition winning algorithm, a

statistics-LSTM (or stat-LSTM) hybrid model was created to look for performance

improvements. However, the variation used in this research featured a level and seasonality

values that were chosen through hyperparameter optimization. The level and seasonality were

used as smoothing factors. Prior to the time series data being fed into the LSTM model as input,

the time series values were divided by the level and seasonality factors. As in Smyl’s (2020)

33

work, a logarithmic function was also applied as a preprocessing step. These steps were applied

in reverse order to unwind the preprocessing to obtain a final forecast value. As part of

hyperparameter tuning, the choice of RNN type: LSTM or GRU were variants that could be

selected.

Figure 5: stat-lstm architecture

CNN-LSTM Hybrid Model

Drawing inspiration from the Wavenet model in Borovykh et al. (2017), this work used

dilated convolutional layers as a way to detect features in the time series data and merged that

with the LSTM model network. The convolutional layers were a preprocessing step that served

34

to highlight significant features in the data prior to being fed into a LSTM model. As with the

stat-LSTM hybrid, as part of hyperparameter tuning, the choice of RNN type: LSTM or GRU

were variants that could be selected.

Figure 6: cnn-lstm architecture

Model Tuning

Most machine learning algorithms include configuration options known as

hyperparameters to adjust and optimize the functioning of the algorithm (Thornton, Hutter,

Hoos, & Leyton-Brown, 2013). Neural networks are no different. Typically, when applying a

machine learning algorithm to a problem, there are two selections that must be made: the

algorithm to be applied, and the configuration of the algorithm through hyperparameters. With

many models, there are a significant number of tunable parameters that create a large search

35

space. Finding the best configuration can be a daunting task. Using the default values can lead to

less than optimal results (Thornton et al., 2013). In the literature, methods of finding the best

parameter configuration range from an exhaustive grid search, random selection of

hyperparameter settings, to optimization algorithms (Bergstra & Bengio, 2012; Thornton et al.,

2013; van Stein, Wang, & Bäck, 2019).

Random Hyperparameter Search

A grid search through hyperparameter combinations is an exhaustive search through

every possible configuration combination. This has the advantage of being thorough but, is

subject to the curse of dimensionality as the number of possible combinations grows

exponentially with the number of possible hyperparameters (Bergstra & Bengio, 2012). With a

grid search, the size of the problem can be reduced by manually restricting the results to regions

in the space that appear to be promising, or by adjusting the resolution of the grid search so that

not every possible alternative is examined. This can make a prohibitively expensive grid search

tractable (Bergstra & Bengio, 2012). A more efficient alterative can be to use a random search

through the parameter space as an alternative to a grid search. Bergstra & Bengio (2012),

propose a random search that treats the configuration parameters as a uniform density from

which random samples are drawn. The authors state that this technique is a trade-off between

reduced efficiency in a low dimensional hyperparameter space with a significant improvement in

higher-dimensional spaces (Bergstra & Bengio, 2012).

In Bergstra & Bengio (2012), the authors conduct their comparison on several datasets

including the MNIST image classification dataset, variations on the MNIST dataset, and other

image classification datasets. A neural network is selected as the model with which to compare