Netcare Limited HY 2012 results

26

UNAUDITED GROUP INTERIM RESULTS for the six months ended 31 March 2012 Netcare Limited

-

Upload

africanfinancials-investor-presentations -

Category

Investor Relations

-

view

152 -

download

0

Transcript of Netcare Limited HY 2012 results

UNAUDITED GROUP INTERIM RESULTSfor the six months ended 31 March 2012

Netcare Limited

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 1

Financial highlights

Revenue (R million)

+11.1%2012: R12 654 million 2011: R11 392 million

2010

11 038 11 39212 654

2011 2012

Adjusted1 headline earnings per share (cents)

+16.1%2010

42.9 44.7

51.9

2011 2012

2012: 51.9 cents 2011: 44.7 cents

1 Adjusted to exclude, inter alia, the effects of the ineffective portion of the interest rate swaps and the change in the UK tax rate.

2

Overview

A positive performance in South Africa (SA) was offset by weaker results in the United Kingdom (UK) primarily due to the challenging economic environment. Adjusted headline earnings per share (HEPS) increased 16.1% to 51.9 cents for the period under review. Operational efficiency and implementing business improvement plans were again key focus areas for the Group.

Commentary

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 3

Group financial review

Financial performanceRevenue in both SA and the UK grew in their

respective local currencies with total revenue

rising 11.1% to R12 654 million. Currency

conversion favourably impacted Group

revenue by R630 million. Group operating

profit increased 7.1% to R1 818 million, while

the operating profit margin declined from

14.9% to 14.4% due to lower margins in

the UK.

Net financial expenses increased R25 million

to R973 million. This was driven by the higher

average exchange rate on UK borrowing

costs, as well as a non-cash charge of

£8.1 million or R100 million (2011: £5.4 million

or R60 million) on the ineffective portion

of the fair value adjustment on UK interest

rate swaps. Cash-based net financial

expenses in the UK declined by £2.1 million

due to scheduled amortisation of debt

balances, and the settlement of debt

related to two hospital properties sold in

the prior year. In SA, net financial expenses

declined by R81 million and interest

cover improved to a healthy 11.8 times

(2011: 6.4 times).

Group tax of R164 million represented an

effective tax rate of 18.9% (2011: 7.2%)

and included R47 million of secondary tax

on companies (STC) arising from dividends

paid. No STC was paid in the comparative

period as distributions took the form of

capital reductions out of share premium.

The Group tax charge was favourably

impacted by a deferred tax release of

R163 million (2011: R155 million) in the

UK, after a 1% reduction in the UK tax

rate to 24%.

Financial position and cash flowDuring the period under review, Netcare

acquired a contractual economic interest

in the debt of the UK operating company

(OpCo). The transaction value of the affected

debt was at a 29.7% discount to its par

value of £64.7 million. The economic benefit

of the transaction totalling £25.3 million,

inclusive of interest receivable, will be

recognised in financial income over the

remaining debt term, with a benefit of

£3.8 million (R48 million) accounted for

in this reporting period.

Net debt rose to R25 974 million from

R25 689 million at 30 September 2011.

In SA, net debt increased to R4 218 million

from R3 303 million at 30 September 2011

due to the funding of normal seasonal working

capital requirements, capital expenditure,

tax and dividend payments, as well as

R582 million (£45.5 million) used to acquire

the economic interest in the UK OpCo

debt. In the UK, debt was lowered further

through scheduled debt amortisation

payments of £19.5 million. The UK’s

half-year cash balances of £123.1 million

(2011: £89.9 million) were a half-year record,

despite declining from £130.6 million at

30 September 2011 due to normal

seasonal cash requirements.

Cash generated from operations was

R212 million less than in the previous

period. This was mainly due to the settlement

of higher levels of payables on the statement

of financial position at 30 September 2011,

related to capital expenditure and the

economic interest in UK OpCo debt.

Debtor collections for the current period

were marginally affected by the close

of the period falling on a weekend.

4

Working capital remained tightly controlled across both geographies.

Capital expenditure was R570 million (including intangible assets), compared to R461 million in the prior period.

Divisional reviewSouth AfricaRevenue grew 7.9% to R6 983 million and operating profit rose 12.1% to R1 145 million. Earnings before interest, tax, depreciation and amortisation (EBITDA) margin increased to 19.6% from 18.7% in 2011. The EDITDA margin has increased 310 basis points from 16.5% in 2009. SA HEPS increased 18.4% to 54.1 cents.

Cash generated from operations, affected by higher seasonal working capital, fell from R949 million in the comparative period to R657 million for the current period. Capital expenditure including intangible assets totalled R378 million (2011: R242 million).

Our Public Private Partnership (PPP) with the Government of Lesotho is fully operational. The PPP will operate the newly built 425-bed Queen ‘Mamohato Hospital and four primary care clinics for 18 years. We are confident that this innovative integrated approach to healthcare delivery will deliver improved clinical outcomes and a sustainable operating performance.

Netcare was recognised at the Metropolitan Oliver Empowerment Awards for Supply Chain, Community Development and New Black Business Development. In the Financial Mail’s Top Empowerment Companies Survey for 2012, Netcare was ranked the most empowered company in the JSE’s healthcare sector for the fourth consecutive

year. Accelerating transformation is one of our

strategic pillars and we are humbled that our

efforts to assist in normalising our nation have

been so consistently recognised.

Hospitals and Emergency servicesRevenue from Hospitals and Emergency

services grew 8.3% to R6 327 million, and

EBITDA rose 11.2% to R1 324 million. The

division grew patient days by 1.8%, while

revenue per patient day increased 5.9%.

The total number of beds increased from

9 052 to 9 143 during the six months under

review. Major expansion projects completed

include building projects at Netcare Mulbarton

(30 surgical and six neo-natal intensive care

unit (ICU) beds), Netcare Kingsway

(23 medical and 12 surgical beds) and

Netcare The Bay (18 medical and 14 ICU

beds). Current projects include Netcare

Montana (46 beds) and Netcare Linmed

(31 beds). In addition to expanding our

ability to service the escalating demand for

healthcare, a portion of our capital investment

is focused on upgrading and replacing

existing equipment, in line with our

commitment to quality patient care.

According to Stats SA, hospital inflation

in 2010 and 2011 was 7.0% and 5.5%

respectively which compares favourably

with medical insurance inflation of 13.0%

and 10.3% respectively. This is evidence of

cost containment efforts by private hospital

operators such as Netcare.

Primary CareThe division delivered pleasing results for the

period, with revenue up 4.5% to R656 million.

The EBITDA margin has increased to 6.9% from

3.3% in 2011 underpinned by stringent cost

control measures and operational efficiencies,

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 5

as well as sound risk management in the managed care division. Operating profit rose to R31 million (2011: R8 million).

Medicross and Prime Cure is the largest private national network of group GP and dental practices. Primary care delivery is becoming increasingly more important in the delivery of sustainable and affordable healthcare.

United KingdomDespite a very difficult trading environment characterised by continuing recessionary pressures and ongoing NHS reforms, our UK operations delivered a robust performance for the period under review. Revenue rose by 2.5% to £456.8, although EBITDA declined 1.3% to £88.9 mainly due to the reduction in insured lives.

General Healthcare Group’s (GHG) overall caseload increased by 3.2% compared to the prior period, driven by NHS Choose & Book (C&B) growth, offset by a continued decline in Private Medical Insurance (PMI) volumes. High levels of unemployment and low levels of disposable income continued to cause the number of insured lives across the wider PMI market to contract. Self-pay volumes have recovered after two years of decline. This has been driven by NHS waiting times increasing further due to financial constraints and regulatory changes in the healthcare sector. Pleasingly, NHS activity has continued to increase and GHG has grown its market share in this segment to become the largest private hospital service provider to the NHS under C&B.

The EBITDA margin declined to 19.5% from 20.2% in the comparative period mainly as a result of the continued shift from private patient volumes to lower-margin NHS volumes and a

shift to more day cases. GHG’s operational

efficiency and cost rationalisation programmes

have however continued to offset this effect.

Net financial expenses were adversely

affected by an £8.1 million (2011: £5.4 million)

non-cash charge, representing the ineffective

portion of the movement in the fair value of

GHG’s interest rate swaps.

A tax benefit of £13.6 million

(2011: £14.0 million) was recognised for the

period, following a further 1% reduction in the

UK statutory company tax rate to 24%. GHG

recorded a loss after tax of £2.3 million

(2011: profit after tax of £7.1 million).

Capital expenditure (including intangible

assets) amounted to £15.1 million

(2011: £19.9 million), relating mainly to

projects initiated in the 2011 financial year

and spending on the existing asset base.

Net debt declined £9.0 million from

30 September 2011 to £1 776.4 million.

Working capital was tightly controlled and the

improvements of the prior year were sustained

during the period. Closing cash balances

remain high at £123.1 million compared to

£89.9 million in the comparative period.

GHG continues to meet all financial covenants

on both the OpCo and property-owning

companies (PropCo) debt facilities. PropCo

remains focused on achieving a solution to

the PropCo debt facility, which matures in

October 2013. Advisors have been appointed

and various options are being evaluated.

The PropCo debt is ring-fenced from the

OpCo and is also without recourse to

Netcare’s SA operations. Furthermore, in

terms of the long-term lease arrangements

in place (19 years remaining plus additional

6

extensions of 10 years), OpCo has the right

to ongoing use and occupation of the hospital

premises as long as it complies with its

contractual rental obligations to PropCo.

OutlookNetcare, in consultation with key stakeholders,

has completed an extensive scenario analysis

of the South African healthcare environment.

In every possible future scenario, healthcare

demand continues to expand. While this is

the basis for growth in health services, it also

poses a risk insofar as these demands may

not be met nationally by current healthcare

delivery systems or resources. The launch

of 10 NHI pilot sites is a significant step

forward in assessing the supply and demand

parameters of healthcare delivery. Netcare

is firmly committed to increasing access to

quality health care. We believe we can play

a meaningful role in assisting future NHI

delivery, in partnership with government

given our broad portfolio of healthcare

services and experience over the last

decade in the UK of working with the NHS

in public health delivery.

In the UK, a firm foundation has been set for

the remainder of the financial year, although

the challenges remain significant. These

include the economic headwinds and their

impact on personal incomes and the PMI

market, as well as government austerity

measures and changing dynamics within

the NHS. However, GHG continues to be

focused on its core businesses, ensuring

efficiency and quality, and being ready to

capitalise on the inevitable return to growth

of the private healthcare market.

Declaration of interim dividend number 6Notice is hereby given that on Thursday, 10 May 2012, the board of directors of Netcare Limited declared an interim gross dividend of 22.0 cents per ordinary share (18.7846 cents per ordinary share net of dividend withholding tax and STC credits) (2011: 22.0 cents), for the six months ended 31 March 2012. The board has determined that, taking all relevant factors into account, this dividend is appropriate in working towards a sustainable dividend policy of between 2.5 to 3.0 times cover over time. The board have confirmed by resolution that the solvency and liquidity test as contemplated by the Companies Act 71 of 2008 has been duly considered, applied and satisfied.

The dividend has been declared from income reserves.

In terms of the new Dividends Tax effective 1 April 2012, the following additional information is disclosed:

withholding tax at 15%. In determining dividend withholding tax, STC credits must be taken into account and the STC credits utilised as part of this dividend declaration amount to R8 178 401.

to 0.564 cents per share.

which results in a net dividend of 18.7846 cents per share to shareholders who are not exempt from dividends withholding tax.

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 7

of this declaration is 1 451 328 433

(inclusive of treasury shares) and the

Company’s tax reference number is

9999/581/71/4.

In accordance with the provisions of Strate,

the electronic settlement and custody system

used by the JSE Limited, the relevant dates

for the dividend are as follows:

Last day to trade cum dividend Friday, 13 July 2012

Trading ex dividend commences Monday, 16 July 2012

Record date Friday, 20 July 2012

Payment date Monday, 23 July 2012

Share certificates may not be dematerialised

nor rematerialised between Monday,

16 July 2012 and Friday, 20 July 2012,

both days inclusive.

On Monday, 23 July 2012, the dividend will be

electronically transferred to the bank accounts

of all certificated shareholders where this

facility is available. Where electronic funds

transfer is either not available or not elected

by the shareholder, cheques dated Monday,

23 July 2012 will be posted on that date.

Holders of dematerialised shares will have

their accounts credited at their participant

or broker on Monday, 23 July 2012.

On behalf of the Board

Jerry Vilakazi

Chairman

Richard Friedland

Chief Executive Officer

Keith Gibson

Chief Financial Officer

Sandton10 May 2012

8

Group income statement

Rm Notes

Unauditedsix months ended

% change

Auditedyear ended

31 March2012

31 March2011

30 September2011

Revenue 12 654 11 392 11.1 23 221 Cost of sales (7 359) (6 681) (13 513)

Gross profit 5 295 4 711 12.4 9 708 Other income 143 177 408 Administrative and other expenses (3 620) (3 190) (6 415)

Operating profit 3 1 818 1 698 7.1 3 701 Investment income 4 90 26 115 Financial expenses 5 (970) (904) (1 847)Other losses – net 6 (93) (70) (23)Attributable earnings of associates 25 3 23

Profit before taxation 870 753 15.5 1 969 Taxation (164) (54) (114)

Profit for the period 706 699 1.0 1 855

Attributable to:Owners of the parent 699 642 1 570 Preference shareholders 22 24 47

Profit attributable to shareholders 721 666 1 617 Non-controlling interest (15) 33 238

706 699 1 855

Earnings per share (cents)

Basic 53.6 50.2 6.8 122.1 Diluted 52.9 48.7 8.6 119.2

Dividend per share (cents) 22.0 22.0 53.0

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 9

Group statement of comprehensive income

Rm Note

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March*2011

30 September2011

Profit for the period 706 699 1 855 Other comprehensive (loss)/income, net of tax (172) 1 091 22

Actuarial losses on defined benefit plans (1)Effect of cash flow hedge accounting Change in the fair value of cash flow hedges (78) 1 130 (608) Reclassification of the cash flow hedge reserve 6 (9) 1 43

Effect of translation of foreign entities (85) (40) 588

Total comprehensive income for the period 534 1 790 1 877

Attributable to:Owners of the parent 594 1 210 1 605 Preference shareholders 22 24 47 Non-controlling interest (82) 556 225

534 1 790 1 877

* Restated refer to note 2.

10

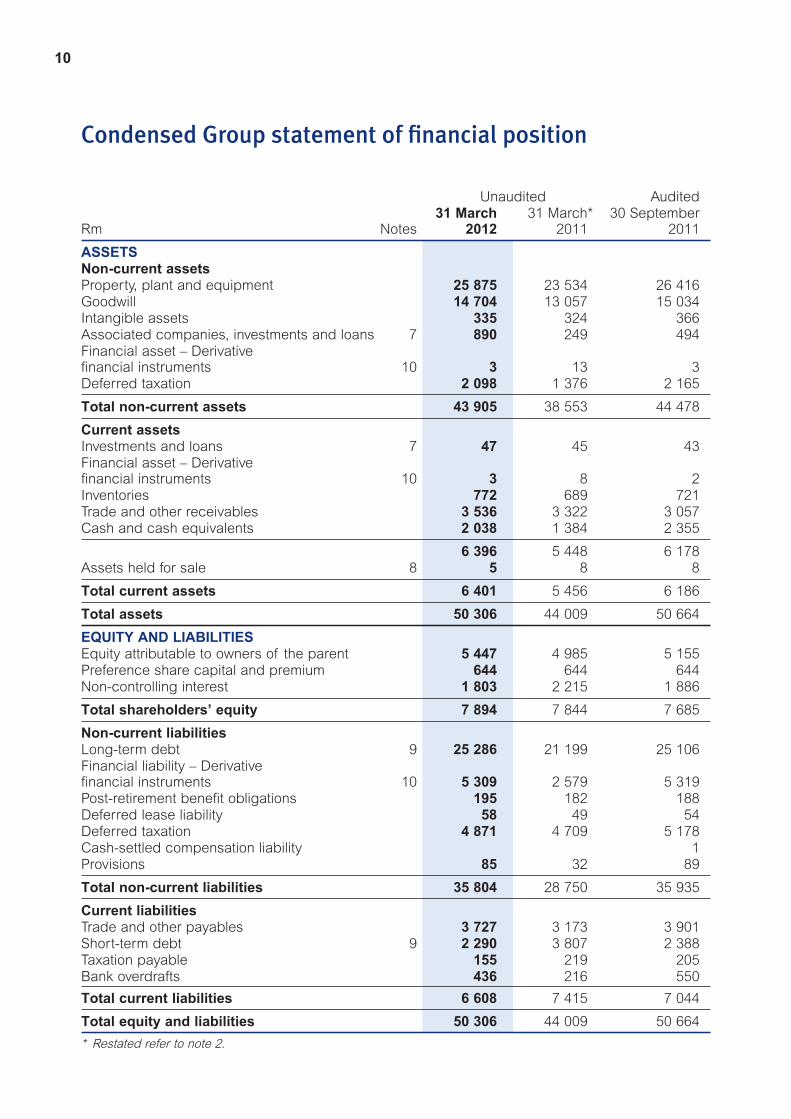

Condensed Group statement of financial position

Unaudited Audited

Rm Notes31 March

2012 31 March*

2011 30 September

2011

ASSETSNon-current assetsProperty, plant and equipment 25 875 23 534 26 416 Goodwill 14 704 13 057 15 034 Intangible assets 335 324 366 Associated companies, investments and loans 7 890 249 494 Financial asset – Derivative financial instruments 10 3 13 3 Deferred taxation 2 098 1 376 2 165

Total non-current assets 43 905 38 553 44 478

Current assetsInvestments and loans 7 47 45 43 Financial asset – Derivative financial instruments 10 3 8 2 Inventories 772 689 721 Trade and other receivables 3 536 3 322 3 057 Cash and cash equivalents 2 038 1 384 2 355

6 396 5 448 6 178 Assets held for sale 8 5 8 8

Total current assets 6 401 5 456 6 186

Total assets 50 306 44 009 50 664

EQUITY AND LIABILITIES Equity attributable to owners of the parent 5 447 4 985 5 155 Preference share capital and premium 644 644 644 Non-controlling interest 1 803 2 215 1 886

Total shareholders’ equity 7 894 7 844 7 685

Non-current liabilitiesLong-term debt 9 25 286 21 199 25 106 Financial liability – Derivative financial instruments 10 5 309 2 579 5 319 Post-retirement benefit obligations 195 182 188 Deferred lease liability 58 49 54 Deferred taxation 4 871 4 709 5 178 Cash-settled compensation liability 1 Provisions 85 32 89

Total non-current liabilities 35 804 28 750 35 935

Current liabilitiesTrade and other payables 3 727 3 173 3 901 Short-term debt 9 2 290 3 807 2 388 Taxation payable 155 219 205 Bank overdrafts 436 216 550

Total current liabilities 6 608 7 415 7 044

Total equity and liabilities 50 306 44 009 50 664

* Restated refer to note 2.

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 11

Group statement of cash flows

Rm

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March2011

30 September2011

Cash flows from operating activities

Cash received from customers 12 135 11 349 23 645 Cash paid to suppliers and employees (10 363) (9 365) (18 073)

Cash generated from operations 1 772 1 984 5 572 Interest paid (936) (902) (1 836)Taxation paid (427) (346) (674)Ordinary dividends paid by subsidiaries (1) (1) (3)Ordinary dividends paid (405) (269) (553)Preference dividends paid (22) (24) (47)Capital reductions paid (83) (83)Distributions to beneficiaries of the HPFL trusts (31) (38) (47)

Net cash from operating activities (50) 321 2 329

Cash flows from investing activities

Purchase of property, plant and equipment (561) (436) (1 327)Proceeds on disposal of property, plant and equipment 27 144 415 Additions to intangible assets (9) (25) (81)(Increase)/decrease in investments and loans (364) 85 (250)Interest received 54 26 115 Increase in equity interest in subsidiaries (11)

Net cash from investing activities (853) (206) (1 139)

Cash flows from financing activities

Proceeds from issue of ordinary shares 16 36 74 Proceeds on disposal of treasury shares 119 62 123 Equity premium on repurchase of convertible bond (10)Long-term liabilities raised/(repaid) 680 (286) 477 Short-term liabilities repaid (79) (37) (1 544)

Net cash from financing activities 736 (225) (880)

Net (decrease)/increase in cash and cash equivalents (167) (110) 310 Translation effects on cash and cash equivalents of foreign entities (36) (7) 210 Cash and cash equivalents at beginning of the period 1 805 1 285 1 285

Cash and cash equivalents at end of the period 1 602 1 168 1 805

Consisting of:

Cash on hand and balances with banks 2 038 1 384 2 355 Short-term money market borrowings and bank overdrafts (436) (216) (550)

1 602 1 168 1 805

12

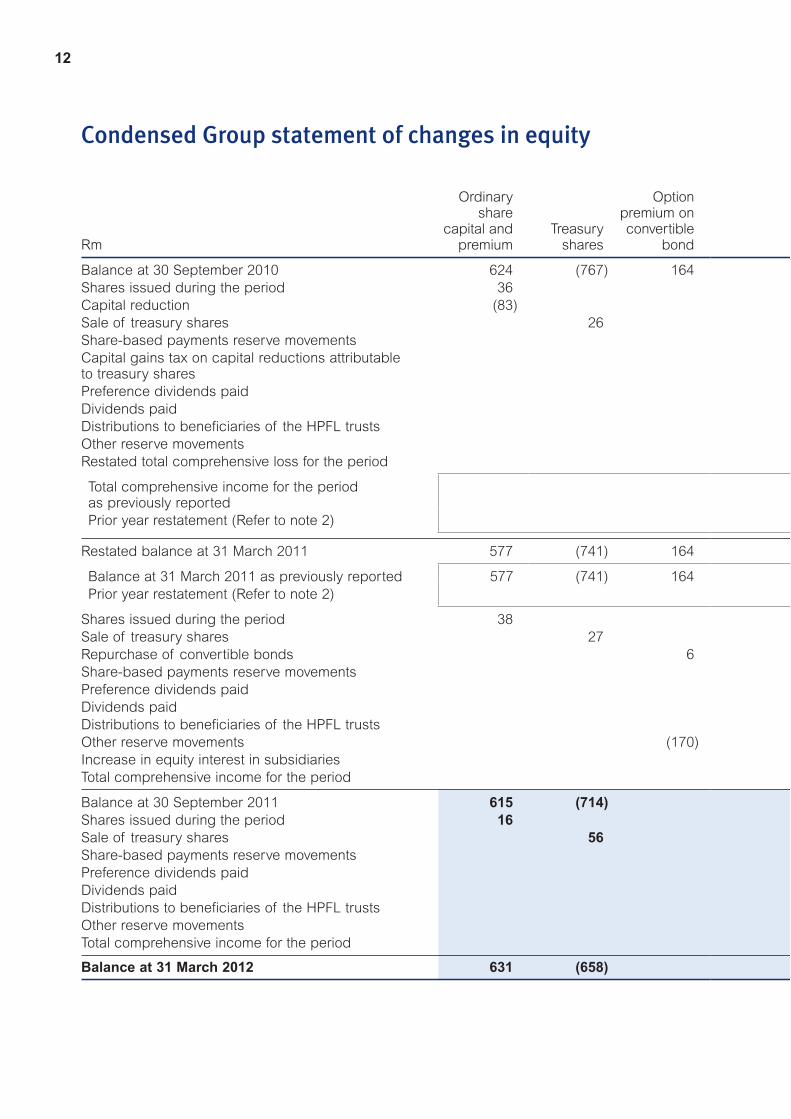

Condensed Group statement of changes in equity

Rm

Ordinary share

capital and premium

Treasury shares

Option premium onconvertible

bond

Balance at 30 September 2010 624 (767) 164 Shares issued during the period 36 Capital reduction (83)Sale of treasury shares 26 Share-based payments reserve movementsCapital gains tax on capital reductions attributable to treasury sharesPreference dividends paidDividends paid Distributions to beneficiaries of the HPFL trustsOther reserve movementsRestated total comprehensive loss for the period

Total comprehensive income for the period as previously reported

Prior year restatement (Refer to note 2)

Restated balance at 31 March 2011 577 (741) 164

Balance at 31 March 2011 as previously reported 577 (741) 164 Prior year restatement (Refer to note 2)

Shares issued during the period 38 Sale of treasury shares 27 Repurchase of convertible bonds 6 Share-based payments reserve movementsPreference dividends paidDividends paid Distributions to beneficiaries of the HPFL trustsOther reserve movements (170)Increase in equity interest in subsidiariesTotal comprehensive income for the period

Balance at 30 September 2011 615 (714)

Shares issued during the period 16

Sale of treasury shares 56

Share-based payments reserve movementsPreference dividends paidDividends paid Distributions to beneficiaries of the HPFL trustsOther reserve movementsTotal comprehensive income for the period

Balance at 31 March 2012 631 (658)

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 13

Cash flowhedge

accountingreserve

Foreigncurrency

translationreserve

Other reserves

Retained earnings

Equityattributable

to owners of the parent

Preferenceshare

capital andpremium

Non-controlling

interest

Totalshare-

holders’equity

(1 790) 769 551 4 518 4 069 644 1 645 6 358 36 36

(83) (83) 30 56 56

14 14 14

(1) (1) (1) (24) (24) (24)

(269) (269) (1) (270) (38) (38) (38)

19 (28) (9) 15 6 588 (20) 666 1 234 556 1 790

588 (21) 666 1 233 555 1 788 1 1 1 2

(1 202) 749 584 4 854 4 985 644 2 215 7 844

(1 202) 722 584 4 968 5 072 644 2 297 8 013 27 (114) (87) (82) (169)

38 38 25 52 52

(21) (15) (15) 9 9 9

(23) (23) (23) (284) (284) (2) (286)

(9) (9) (9) 104 80 14 (15) (1)

(30) (30) 19 (11) (889) 362 945 418 (331) 87

(2 091) 1 111 697 5 537 5 155 644 1 886 7 685

16 16

53 109 109

9 9 9

(22) (22) (22)

(405) (405) (1) (406)

(31) (31) (31)

5 (5)

(45) (60) 721 616 (82) 534

(2 136) 1 051 711 5 848 5 447 644 1 803 7 894

14

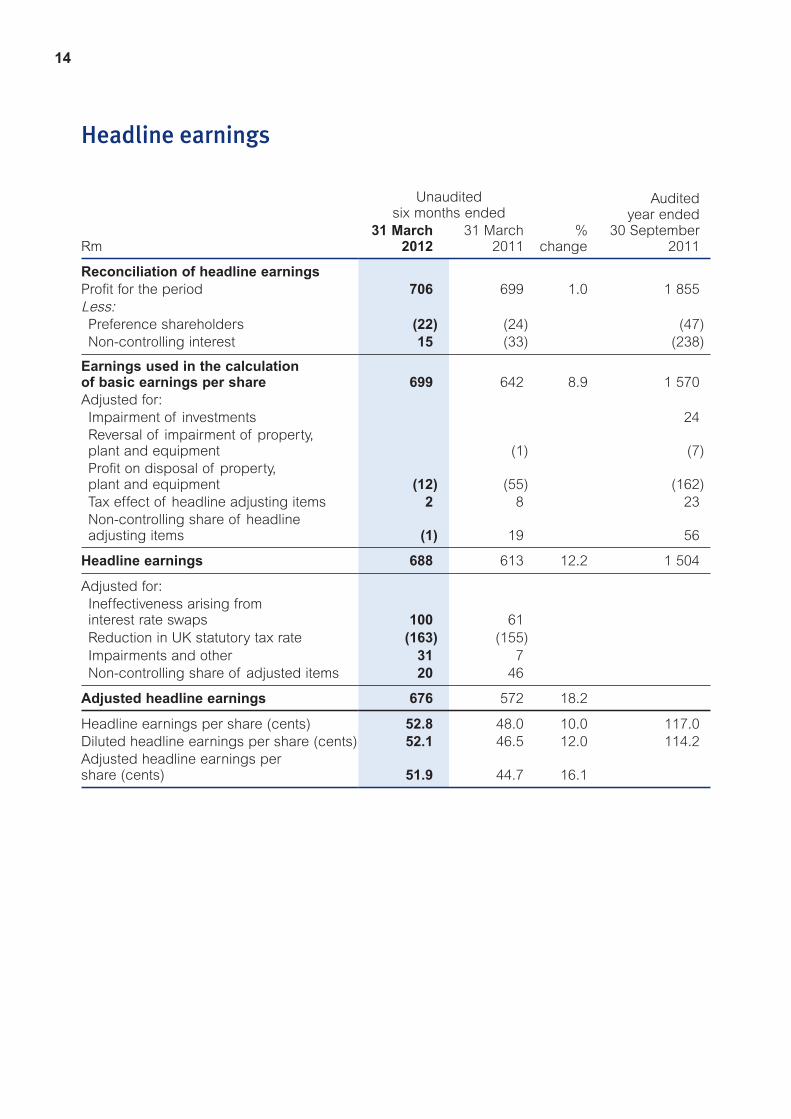

Headline earnings

Rm

Unauditedsix months ended

% change

Auditedyear ended

30 September2011

31 March2012

31 March2011

Reconciliation of headline earnings

Profit for the period 706 699 1.0 1 855 Less: Preference shareholders (22) (24) (47) Non-controlling interest 15 (33) (238)

Earnings used in the calculation of basic earnings per share 699 642 8.9 1 570 Adjusted for: Impairment of investments 24 Reversal of impairment of property, plant and equipment (1) (7)

Profit on disposal of property, plant and equipment (12) (55) (162)

Tax effect of headline adjusting items 2 8 23 Non-controlling share of headline adjusting items (1) 19 56

Headline earnings 688 613 12.2 1 504

Adjusted for: Ineffectiveness arising from interest rate swaps 100 61

Reduction in UK statutory tax rate (163) (155) Impairments and other 31 7 Non-controlling share of adjusted items 20 46

Adjusted headline earnings 676 572 18.2

Headline earnings per share (cents) 52.8 48.0 10.0 117.0 Diluted headline earnings per share (cents) 52.1 46.5 12.0 114.2Adjusted headline earnings per share (cents) 51.9 44.7 16.1

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 15

1. Basis of preparation and accounting policiesThe condensed financial statements for the six months ended 31 March 2012 have been prepared in accordance with International Financial Reporting Standards (IFRS) and comply with IAS 34 Interim Financial Reporting, the AC500 standards as issued by the Accounting Practices Board or its successor, the Listings Requirements of the JSE Limited and the South African Companies Act No 71 of 2008.

The accounting policies applied in the preparation of these condensed financial statements are consistent in all material respects with those applied in the audited financial statements for the year ended 30 September 2011.

A significant portion of the UK PropCo debt matures in October 2013, and the business is actively involved with its advisors in order to seek a solution. Whilst no formally committed plan currently exists, it is premature at this stage, with 17 months remaining before the maturity date, to conclude that a solution cannot be achieved. Furthermore, given the ring-fencing of the PropCo debt from the UK OpCo, and the non-recourse nature of this debt to Netcare’s SA operations, the directors are comfortable with the going concern assessment.

The interim results have not been audited by the Group’s independent external auditors, Grant Thornton.

The condensed financial statements have been prepared under the supervision of KN Gibson CA (SA), Chief Financial Officer of Netcare Limited.

2. Restatement of comparative informationThe annual financial statements for the year ended 30 September 2011 included a prior year restatement resulting from a change in GHG’s interpretation of IAS 12 Income taxes. This change related to the differences that arise on the straight-lining of lease rentals on operating leases between GHG’s wholly owned subsidiaries, BMI Healthcare Limited and other group property holding companies. In prior years, the differences were accounted for as permanent differences with no deferred tax being raised. Management concluded that fairer presentation would be achieved if these were treated as timing differences and the appropriate deferred tax liability raised. More details are provided in note 33 of the annual financial statements for the year ended 30 September 2011.

The March 2011 statement of financial position, statement of changes in equity and statement of comprehensive income have been restated to reflect the changes. The restatement did not result in any changes to earnings or headline earnings per share.

Condensed notes to the Group financial statements

16

2. Restatement of comparative information (continued)The effect of this change is summarised below:Group statement of financial position for the six months ended 31 March 2011

RmPreviously

reported Adjustment Restated

Non-current assets

Deferred taxation 1 071 305 1 376 Non-current liabilities

Deferred taxation (4 235) (474) (4 709)Equity

Foreign currency translation reserve (722) (27) (749)Retained earnings (4 968) 114 (4 854)Non-controlling interest (2 297) 82 (2 215)

Rm

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March2011

30 September2011

3. Operating profitAfter charging:Depreciation and amortisation 659 568 1 213 Operating lease charges 272 176 469

4. Investment incomeReturn on retirement benefit plan assets 49 Interest on bank accounts and other 90 26 66

90 26 115

5. Financial expensesAmortisation of arrangement fee 52 43 90 Interest on convertible bonds (liability portion) 73 140 Interest on promissory notes 121 84 166 Interest on preference shares classified as debt 1 3 4 Interest on bank loans and other 796 701 1 447

970 904 1 847

6. Other losses – netForeign exchange (losses)/gains (1) 5 Ineffectiveness (losses)/gains on cash flow hedges (100) (61) 43 Fair value loss on inflation rate swaps (not hedge accounted) (2)Fair value loss on derivative financial assets (not hedge accounted) (2) (7) (26)Amount reclassified from cash flow hedge reserve 9 (1) (43)

(93) (70) (23)

Condensed notes to the Group financial statements (continued)

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 17

Rm

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March2011

30 September2011

7. Associated companies, investments and loansNon-current

Associated companies 287 224 289 Available-for-sale investments 22 Loans and receivables 603 3 205

890 249 494

Current

Loans and receivables 47 45 43

937 294 537

The available-for-sale investment represents an 8% investment in Phoenix Hospital Limited, an unlisted group which comprises The Weymouth Clinic Limited and 9 Harley Street Limited in the United Kingdom. An impairment loss of R22 million was recognised during the prior year.

Included in loans and receivables is an investment of R584 million relating to the acquisition of a contractual economic interest in the debt of the UK OpCo.

8. Assets held for saleCertain land and buildings were classified as held for sale 5 8 8

18

Condensed notes to the Group financial statements (continued)

Rm

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March2011

30 September2011

9. DebtLong-term debt 25 286 21 199 25 106 Short-term debt 2 290 3 807 2 388

Total debt 27 576 25 006 27 494

Comprising:Debt in South African Rand

Finance leases 51 57 57 Redeemable cumulative preference shares 22 42 34 Convertible bonds (debt portion) 1 445 Promissory notes 4 039 1 910 3 180 Unsecured liabilities 200 452 200

4 312 3 906 3 471

Debt in foreign currency

Secured liabilities 22 927 20 903 23 563 Finance leases 153 111 154 Other 184 86 306

23 264 21 100 24 023

27 576 25 006 27 494

Maturity profile

Rm Total< 1

year1 – 2 years

2 – 3 years

3 – 4 years

> 4 years

31 March 2012

Debt in South African Rand 4 312 1 500 420 1 374 7 1 011 Debt in foreign currency 23 264 790 19 700 1 086 1 518 170

27 576 2 290 20 120 2 460 1 525 1 181

31 March 2011Debt in South African Rand 3 906 3 192 683 7 6 18 Debt in foreign currency 21 100 615 440 17 421 86 2 538

25 006 3 807 1 123 17 428 92 2 556

31 September 2011Debt in South African Rand 3 471 1 622 483 344 7 1 015 Debt in foreign currency 24 023 766 575 19 908 1 592 1 182

27 494 2 388 1 058 20 252 1 599 2 197

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 19

Rm

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March2011

30 September2011

10. Derivative financial instrumentsDerivative financial assets

European style call optionsSouth African Rand 3 21 5 Interest rate swapsSouth African Rand 3

6 21 5

Included in:Non-current assets 3 13 3 Current assets 3 8 2

6 21 5

Derivative financial liabilities

Interest rate swapsSouth African Rand 9 10 16 Foreign currency 5 297 2 569 5 300

5 306 2 579 5 316 Inflation rate swapsSouth African Rand 3 3

5 309 2 579 5 319

Included in:Non-current liabilities 5 309 2 579 5 319

The inter-bank rate used in the fair value calculations of the foreign currency interest rate swaps has been adjusted to take into account the credit risk to which the Group is exposed. The value of the foreign currency interest rate swaps excluding the counterparty valuation adjustment (CVA) at 31 March 2012 was R6 202 million.

20

Condensed notes to the Group financial statements (continued)

Rm

Unauditedsix months ended

Auditedyear ended

31 March2012

31 March2011

30 September2011

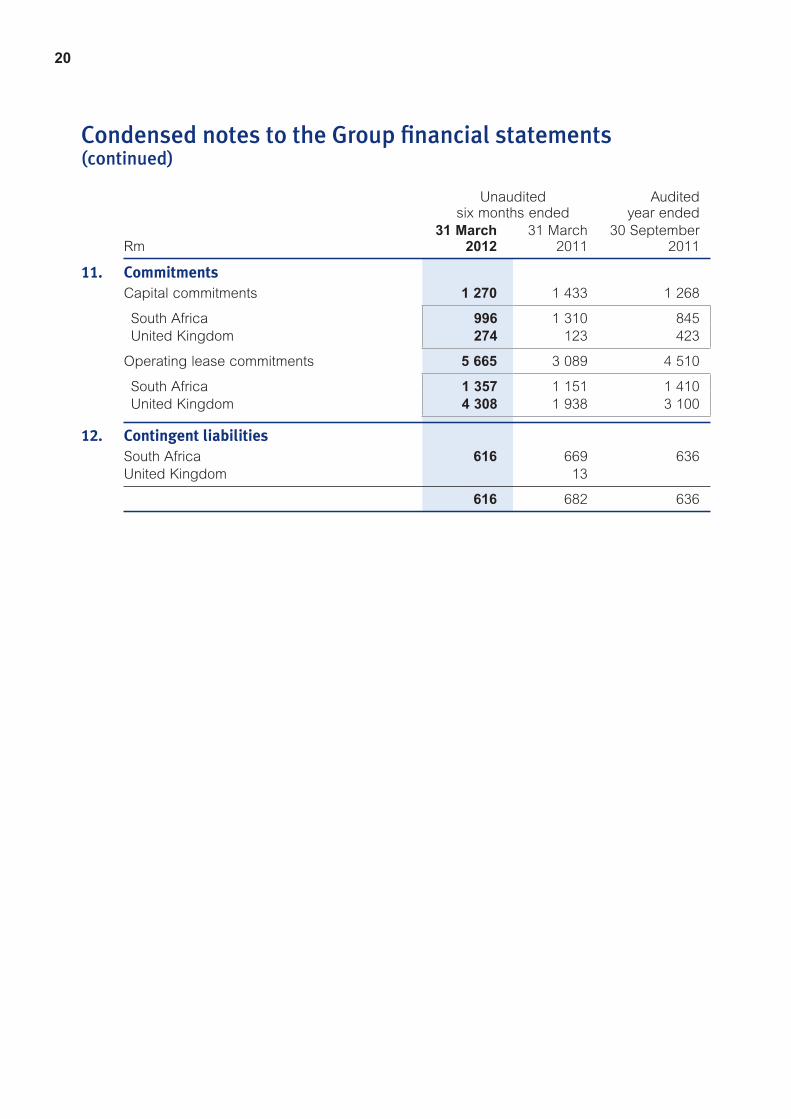

11. CommitmentsCapital commitments 1 270 1 433 1 268

South Africa 996 1 310 845 United Kingdom 274 123 423

Operating lease commitments 5 665 3 089 4 510

South Africa 1 357 1 151 1 410 United Kingdom 4 308 1 938 3 100

12. Contingent liabilitiesSouth Africa 616 669 636 United Kingdom 13

616 682 636

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 21

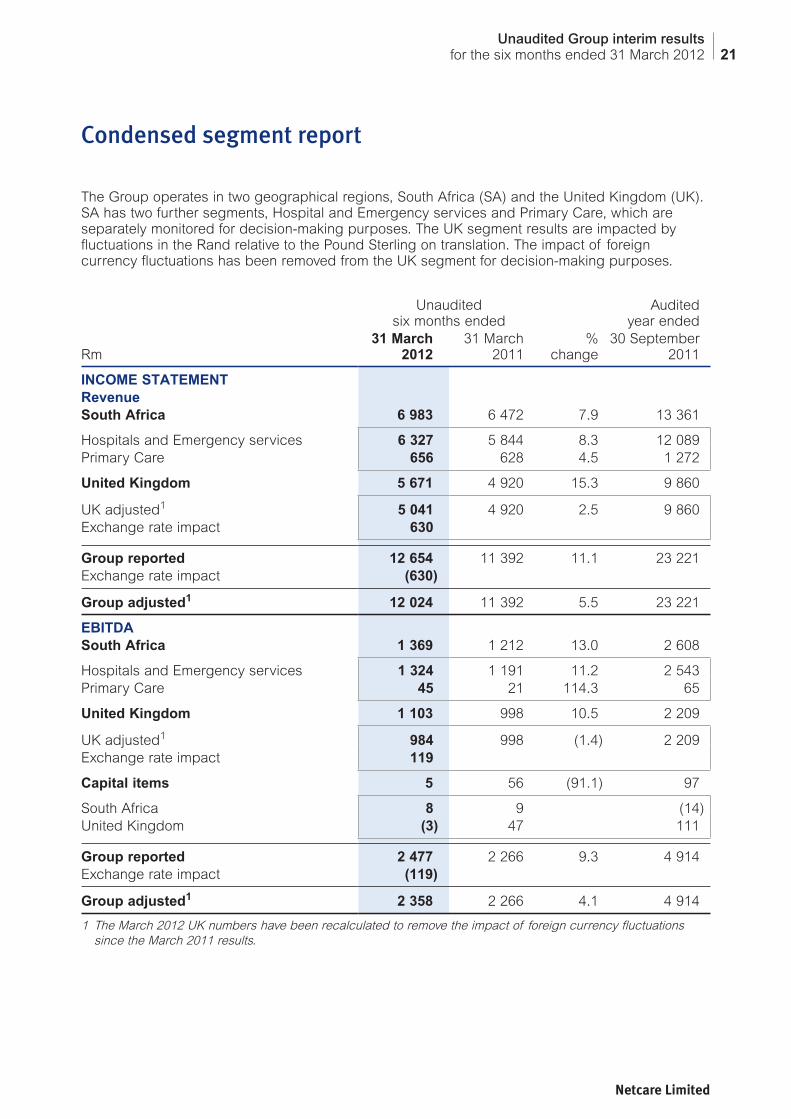

Condensed segment report

The Group operates in two geographical regions, South Africa (SA) and the United Kingdom (UK). SA has two further segments, Hospital and Emergency services and Primary Care, which are separately monitored for decision-making purposes. The UK segment results are impacted by fluctuations in the Rand relative to the Pound Sterling on translation. The impact of foreign currency fluctuations has been removed from the UK segment for decision-making purposes.

Rm

Unauditedsix months ended

% change

Auditedyear ended

31 March2012

31 March2011

30 September2011

INCOME STATEMENT

Revenue South Africa 6 983 6 472 7.9 13 361

Hospitals and Emergency services 6 327 5 844 8.3 12 089 Primary Care 656 628 4.5 1 272

United Kingdom 5 671 4 920 15.3 9 860

UK adjusted1 5 041 4 920 2.5 9 860 Exchange rate impact 630

Group reported 12 654 11 392 11.1 23 221 Exchange rate impact (630)

Group adjusted1 12 024 11 392 5.5 23 221

EBITDA

South Africa 1 369 1 212 13.0 2 608

Hospitals and Emergency services 1 324 1 191 11.2 2 543 Primary Care 45 21 114.3 65

United Kingdom 1 103 998 10.5 2 209

UK adjusted1 984 998 (1.4) 2 209 Exchange rate impact 119

Capital items 5 56 (91.1) 97

South Africa 8 9 (14)United Kingdom (3) 47 111

Group reported 2 477 2 266 9.3 4 914 Exchange rate impact (119)

Group adjusted1 2 358 2 266 4.1 4 914

1 The March 2012 UK numbers have been recalculated to remove the impact of foreign currency fluctuations since the March 2011 results.

22

Condensed segment report (continued)

Rm

Unauditedsix months ended

% change

Auditedyear ended

31 March2012

31 March2011

30 September2011

Operating profit

South Africa 1 145 1 021 12.1 2 220

Hospitals and Emergency services 1 114 1 013 10.0 2 182 Primary Care 31 8 287.5 38

United Kingdom 668 621 7.6 1 384

UK adjusted1 598 621 (3.7) 1 384 Exchange rate impact 70

Capital items 5 56 (91.1) 97

South Africa 8 9 (14)United Kingdom (3) 47 111

Group reported 1 818 1 698 7.1 3 701 Exchange rate impact (70)

Group adjusted1 1 748 1 698 2.9 3 701

Net interest expense

South Africa 98 162 39.5 327 United Kingdom 782 716 (9.2) 1 405

UK adjusted1 693 716 3.2 1 405 Exchange rate impact 89

Group reported 880 878 (0.2) 1 732 Exchange rate impact (89)

Group adjusted1 791 878 9.9 1 732

1 The March 2012 UK numbers have been recalculated to remove the impact of foreign currency fluctuations since the March 2011 results.

Netcare Limited

Unaudited Group interim results for the six months ended 31 March 2012 23

Rm

Unaudited%

change

Audited31 March

201231 March

201130 September

2011

STATEMENT OF FINANCIAL POSITION

Total assets2

South Africa 10 969 9 395 16.8 10 262 United Kingdom 39 337 34 614 13.6 40 402

UK adjusted1 34 832 34 614 0.6 40 402 Exchange rate impact (4 505)

Group reported 50 306 44 009 14.3 50 664 Exchange rate impact 4 505

Group adjusted1 45 801 44 009 4.1 50 664

Debt net of cash

South Africa 4 218 3 713 (13.6) 3 303 United Kingdom 21 756 20 125 (8.1) 22 386

UK adjusted1 19 264 20 125 4.3 22 386 Exchange rate impact 2 492

Group reported 25 974 23 838 (9.0) 25 689 Exchange rate impact (2 492)

Group adjusted1 23 482 23 838 1.5 25 689

1 The March 2012 UK numbers have been recalculated to remove the impact of foreign currency fluctuations since the March 2011 results.

2 Restated refer to note 2.

Salient features

Unaudited Audited31 March

2012 31 March

2011 30 September

2011

Share statistics

Ordinary sharesShares in issue (million) 1 448 1 441 1 446 Shares in issue net of treasury shares (million) 1 306 1 277 1 295 Weighted average number of shares (million) 1 303 1 279 1 286 Diluted weighted average number of shares (million) 1 321 1 318 1 317 Market price per share (cents) 1 423 1 450 1 305

Currency conversion guide (R:£)

Closing exchange rate 12.25 10.85 12.54 Average exchange rate for the period 12.42 11.02 11.09

Netcare Limited (“Netcare”, “the Company” or “the Group”)

Registration number: 1996/008242/06 (Incorporated in the Republic of South Africa)

JSE share code: NTC

ISIN code: ZAE000011953

����������� ���76 Maude Street (corner West Street), Sandton 2196, Private Bag X34, Benmore 2010

Executive directors: RH Friedland (Chief Executive Officer)KN Gibson (Chief Financial Officer)

Non-executive directors:SJ Vilakazi (Chairman)T BrewerAPH JammineJM KahnMJ KuscusHR LevinKD MorokaN Weltman

Company Secretary: L Bagwandeen

Sponsor: Nedbank Capital, a division of Nedbank Group Limited

Transfer secretaries: Link Market Services South Africa (Proprietary) Limited, 13th Floor, Rennie House, 19 Ameshoff Street, Braamfontein 2001

Investor relations: [email protected]

AdministrationDisclaimerNetcare has acted in good faith and has made every reasonable effort to ensure the accuracy and completeness of the information contained in this presentation, including all information that may be defined as ‘forward-looking statements’.

Forward-looking statements may be identified by words such as ‘believe’, ‘anticipate’, ‘expect’, ‘plan’,’estimate’, ‘intend’, ‘project’, ‘target’, ‘predict’ and ‘hope’. By their nature, forward-looking statements are inherently predictive, speculative and involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future, involve known and unknown risks, uncertainties and other facts or factors which may cause the actual results, performance or achievements of the Group, or its sector to be materially different from any results, performance or achievement expressed or implied by such forward-looking statements. Forward-looking statements are not guarantees of future performance and are based on assumptions regarding the Group’s present and future business strategies and the environments in which it operates now and in the future. No assurance can be given that forward-looking statements will prove to be correct and undue reliance should not be placed on such statements.

Netcare does not undertake to update any forward-looking statements contained in this document and does not assume responsibility for any loss or damage whatsoever and howsoever arising as a result of the reliance by any party thereon.