Net Operating Losses - Spidell Publishing, Inc. · · 2015-11-06NET OPERATING LOSSES . ... •...

63

Net Operating Losses

Transcript of Net Operating Losses - Spidell Publishing, Inc. · · 2015-11-06NET OPERATING LOSSES . ... •...

Net Operating Losses

This publication is distributed with the understanding that the authors and publisher are not engaged in rendering legal, accounting or other professional advice and assume no liability in connection with its use. Tax laws are constantly changing and are subject to differing interpretation. In addition, the facts and circumstances in your particular situation may not be the same as those presented here. Therefore, we urge you to do additional research and ensure that you are fully informed before using the information contained in this publication. Federal law prohibits unauthorized reproduction of the material in Spidell’s Net Operating Losses manual. All reproduction must be approved in writing by Spidell Publishing, Inc.®

This is not a free publication. Purchase of this electronic publication entitles the buyer to keep one copy on his/her computer and to print out one copy only. Printing out more than one copy — and any electronic distribution of this publication — is prohibited by international and United States copyright laws and treaties. Illegal distribution of this publication will subject the purchaser to penalties of up to $100,000 per copy distributed.

NET OPERATING LOSSES

Course objectives: The purpose of this course is to provide a guide to essential information for net operating losses. Topics addressed include: calculating statutory loss, nonbusiness vs. business capital losses, computing NOLs for business taxpayers, NOL filing details, the alternative minimum tax NOL, modified taxable income, and much more.

After completing this course, you will be able to:

• Determine how to calculate a net operating loss when making a nonbusiness capital loss modification

• Choose what is allocable to a taxpayer’s business when calculating statutory loss • Identify the appropriate carryback period for qualified disaster losses • Select the itemized deductions that require recalculation when determining tax liability for a

carryback year • Recall how much of a net operating loss can be absorbed • Identify adjustments when calculating an alternative minimum tax NOL

Category: Taxes Recommended CPE Hours: CPAs/PAs — 2

EAs/CRTPs — 2 Federal Tax Law Level: Basic Prerequisite: None Advanced Preparation: None Expiration Date: November 2016

Net Operating Losses

©2015 Spidell Publishing, Inc.®

TABLE OF CONTENTS

Introduction .............................................................................................................................................. Page 1 Part I — Compute Current Year Net Operating Losses ..................................................................... Page 1 Statutory Loss .................................................................................................................................... Page 1 Example: Form 1045 (2011) Schedule A - NOL— Barry Berry ................................................... Page 6 IRC Section 172 (d) illustrated on Form 1045 Schedule A ........................................................... Page 9 Example: Form 1045 (2014) Schedule A - NOL— Carl McGallo .............................................. Page 11 Individual NOL Quick Worksheet ............................................................................................... Page 12 Part II — Determine the Carryback and Carryover Periods for the Net Operating Loss ............ Page 14

Standard Carryback Period ........................................................................................................... Page 14 Waiving the Carryback Period ...................................................................................................... Page 17 Sample Election Statements ........................................................................................................... Page 18 Carryover Period ............................................................................................................................. Page 21

Part III — Compute the Net Operating Loss Absorption in a Carryback Year and Intervening Years .................................................................................................................................................................. Page 21

Example: Form 1045 (2014) Application for Tentative Refund ................................................ Page 29 How is the NOL Carried Back? ..................................................................................................... Page 34

Part IV — Special Issues with Join and Separate Tax Returns, Deceased Spouses & Divorced Taxpayers ......................................................................................................................................... Page 36

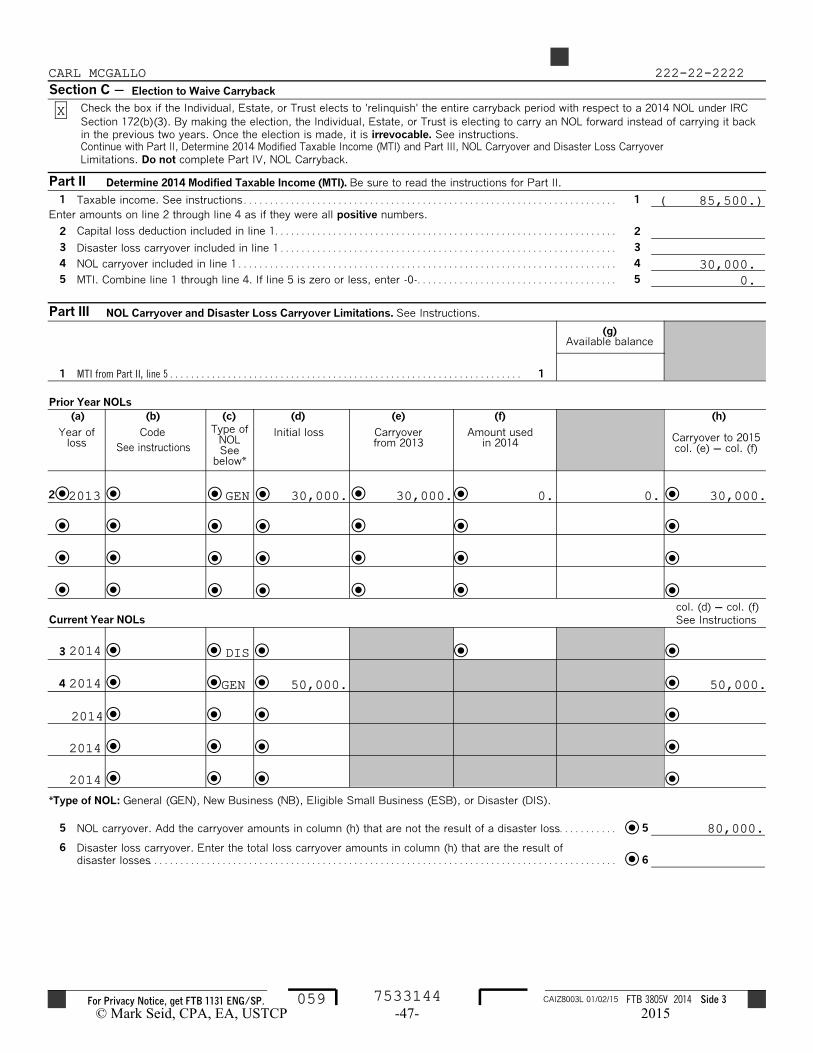

Part V — Getting the Carryback Claim Accepted By the IRS the First Time ................................ Page 40 Part VI — Alternative Minimum Tax Considerations ...................................................................... Page 44 Part VII — California ............................................................................................................................. Page 46 Example: Form 3805V Section C – Election to Waive Carryback ............................................. Page 47 Example of California NOL Use ................................................................................................... Page 50

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 1 - 2015

INTRODUCTION This course is designed to provide a guide to federal and California net operating losses. The materials will cover the computation of a current year net operating loss, determination of the property carryback and carryover periods, absorption of a net operating loss (NOL) in carryback and intervening years, issues created by separate and joint NOLs, and California conformity issues. IRC §172 – Net Operating Loss Deduction. Subsection Titles. IRC §172(a) – Deduction Allowed IRC §172(b) – Net Operating Loss Carrybacks and Carryovers IRC §172(c) – Net Operating Loss Defined IRC §172(d) – Modifications IRC §172(e) – Law Applicable to Computations IRC §172(f) – Rules Relating to Specified Liability Losses IRC §172(g) – Rules Relating to Bad Debt Losses of Commercial Banks IRC §172(h) – Corporate Equity Reduction Interest Losses IRC §172(i) – Rules Relating to Farming Losses IRC §172(j) – Rules Relating to Qualified Disaster Losses IRC §172(k) – Cross References

PART I – COMPUTE CURRENT YEAR NET OPERATING LOSS STATUTORY LOSS The starting point for calculating a net operating loss is the “statutory loss.” Statutory loss is defined in IRC §172(c).

IRC §172(c) Net Operating Loss Defined. – For purposes of this section, the term “net operating loss” means the excess of the deductions allowed by this chapter over the gross income. Such excess shall be computed with the modifications specified in subsection (d).

“Deductions allowed by this chapter” IRC §172 is located in: Title 26 – Internal Revenue Code

Subtitle A – Income Taxes Chapter 1 – Normal Taxes and Surtaxes (§§1-1400U)

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 2 - 2015

“Gross income” Gross income is defined in IRC §61 – “Except as otherwise provided in this subtitle, gross income means all income from whatever source derived…” “Modifications specified in subsection (d)” No deduction is allowed for a net operating loss deduction. §172(d)(1). No deduction is allowed for capital losses. §172(d)(2)(A). No exclusion is allowed for gains on small business stock. §172(d)(2)(B). No deduction is allowed for personal exemptions. §172(d)(3). No nonbusiness deductions in excess of nonbusiness income. §172(d)(4). o No taxable income limitation on dividends received deduction if the full deduction results

in a loss. §172(d)(5). o No adjustments to REIT taxable income for adjustments in §857(b)(2). §172(d)(6). No manufacturing deduction (domestic production activities deduction) is allowed.

§172(d)(7). §172(d)(1) Modification – Net Operating Loss Deductions To calculate the statutory loss no deduction is allowed for a net operating loss deduction. A net operating loss deduction is either a carryover from a prior year or a carryback from subsequent year. §172(d)(2)(A) Modification – Capital Losses (nonbusiness) To calculate the statutory loss, no deduction is allowed for capital losses. Capital gains and losses need to be divided into two classes in order to make this calculation: (1) business capital gains and losses and (2) nonbusiness capital gains and losses. Business capital gains cannot be offset by nonbusiness capital losses.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 3 - 2015

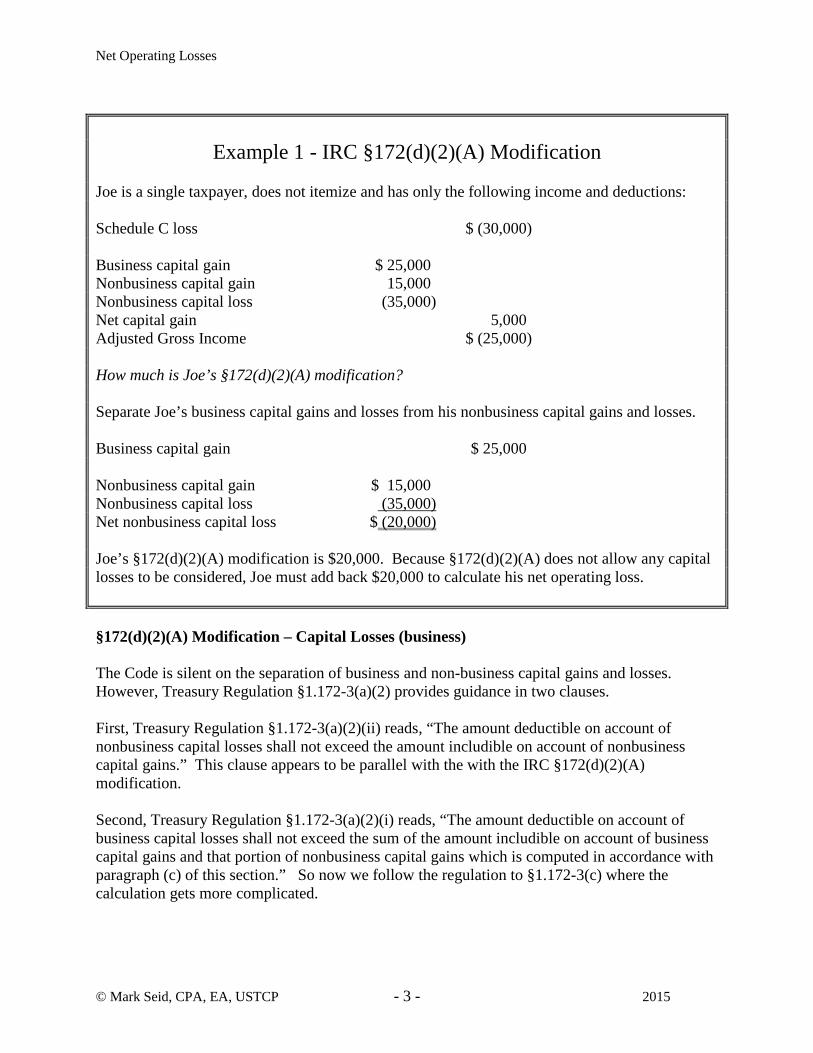

Example 1 - IRC §172(d)(2)(A) Modification Joe is a single taxpayer, does not itemize and has only the following income and deductions: Schedule C loss $ (30,000) Business capital gain $ 25,000 Nonbusiness capital gain 15,000 Nonbusiness capital loss (35,000) Net capital gain 5,000 Adjusted Gross Income $ (25,000) How much is Joe’s §172(d)(2)(A) modification? Separate Joe’s business capital gains and losses from his nonbusiness capital gains and losses. Business capital gain $ 25,000 Nonbusiness capital gain $ 15,000 Nonbusiness capital loss (35,000) Net nonbusiness capital loss $ (20,000) Joe’s §172(d)(2)(A) modification is $20,000. Because §172(d)(2)(A) does not allow any capital losses to be considered, Joe must add back $20,000 to calculate his net operating loss. §172(d)(2)(A) Modification – Capital Losses (business) The Code is silent on the separation of business and non-business capital gains and losses. However, Treasury Regulation §1.172-3(a)(2) provides guidance in two clauses. First, Treasury Regulation §1.172-3(a)(2)(ii) reads, “The amount deductible on account of nonbusiness capital losses shall not exceed the amount includible on account of nonbusiness capital gains.” This clause appears to be parallel with the with the IRC §172(d)(2)(A) modification. Second, Treasury Regulation §1.172-3(a)(2)(i) reads, “The amount deductible on account of business capital losses shall not exceed the sum of the amount includible on account of business capital gains and that portion of nonbusiness capital gains which is computed in accordance with paragraph (c) of this section.” So now we follow the regulation to §1.172-3(c) where the calculation gets more complicated.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 4 - 2015

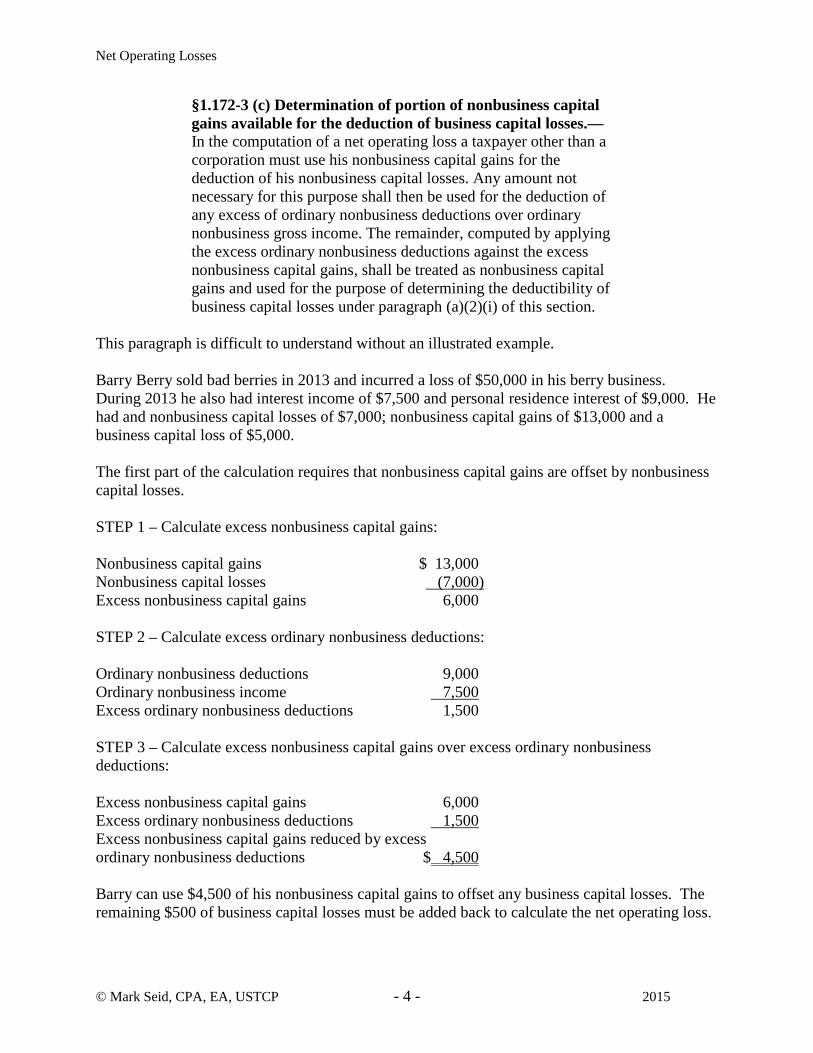

§1.172-3 (c) Determination of portion of nonbusiness capital gains available for the deduction of business capital losses.— In the computation of a net operating loss a taxpayer other than a corporation must use his nonbusiness capital gains for the deduction of his nonbusiness capital losses. Any amount not necessary for this purpose shall then be used for the deduction of any excess of ordinary nonbusiness deductions over ordinary nonbusiness gross income. The remainder, computed by applying the excess ordinary nonbusiness deductions against the excess nonbusiness capital gains, shall be treated as nonbusiness capital gains and used for the purpose of determining the deductibility of business capital losses under paragraph (a)(2)(i) of this section.

This paragraph is difficult to understand without an illustrated example. Barry Berry sold bad berries in 2013 and incurred a loss of $50,000 in his berry business. During 2013 he also had interest income of $7,500 and personal residence interest of $9,000. He had and nonbusiness capital losses of $7,000; nonbusiness capital gains of $13,000 and a business capital loss of $5,000. The first part of the calculation requires that nonbusiness capital gains are offset by nonbusiness capital losses. STEP 1 – Calculate excess nonbusiness capital gains: Nonbusiness capital gains $ 13,000 Nonbusiness capital losses (7,000) Excess nonbusiness capital gains 6,000 STEP 2 – Calculate excess ordinary nonbusiness deductions: Ordinary nonbusiness deductions 9,000 Ordinary nonbusiness income 7,500 Excess ordinary nonbusiness deductions 1,500 STEP 3 – Calculate excess nonbusiness capital gains over excess ordinary nonbusiness deductions: Excess nonbusiness capital gains 6,000 Excess ordinary nonbusiness deductions 1,500 Excess nonbusiness capital gains reduced by excess ordinary nonbusiness deductions $ 4,500 Barry can use $4,500 of his nonbusiness capital gains to offset any business capital losses. The remaining $500 of business capital losses must be added back to calculate the net operating loss.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 5 - 2015

Both the IRS and most commercial tax preparation software have modified the above formula found in Treasury Regulation §1.172-3(c). The alternative calculation arrives at the same answer, but follows a more logical path. STEP 1 – Calculate excess nonbusiness capital gains. Nonbusiness capital gains $ 13,000 Nonbusiness capital losses (7,000) Excess nonbusiness capital gains 6,000 STEP 2 – Combine ordinary nonbusiness income and excess nonbusiness capital gains. Ordinary nonbusiness income 7,500 Excess nonbusiness capital gains 6,000 Step 2 subtotal 13,500 STEP 3 – Subtract ordinary nonbusiness deductions from Step 2 result (but not below zero). Step 2 subtotal 13,500 Ordinary nonbusiness deductions (9,000) Step 3 subtotal 4,500 STEP 4 – Reduce business capital gains by Step 3 result (but not below zero). Business capital gains 5,000 Step 3 subtotal (4,500) Business capital gains not offset by deductions 500

Schedule A ' NOL (see instructions)

1 Enter the amount from your 2011 Form 1040, line 41, or Form 1040NR, line 39. Estates and trusts, entertaxable income increased by the total of the charitable deduction, income distribution deduction, andexemption amount. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Nonbusiness capital losses before limitation. Enter as a positive number . . . . . . . 2

3 Nonbusiness capital gains (without regard to any section 1202 exclusion). . . . . . . 3

4 If line 2 is more than line 3, enter the difference. Otherwise, enter -0-. . . . . . . . . . 4

5 If line 3 is more than line 2, enter the difference.Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

6 Nonbusiness deductions (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Nonbusiness income other than capital gains(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Add lines 5 and 7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

9 If line 6 is more than line 8, enter the difference. Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

10 If line 8 is more than line 6, enter the difference.Otherwise, enter -0-. But do not enter more thanline 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Business capital losses before limitation. Enter as a positive number. . . . . . . . . . . 11

12 Business capital gains (without regard to anysection 1202 exclusion). . . . . . . . . . . . . . . . . . . . . . . . . . . 12

13 Add lines 10 and 12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 Subtract line 13 from line 11. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . 14

15 Add lines 4 and 14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

16 Enter the loss, if any, from line 16 of your 2011 Schedule D (Form 1040).(Estates and trusts, enter the loss, if any, from line 15, column (3), of ScheduleD (Form 1041).) Enter as a positive number. If you do not have a loss on thatline (and do not have a section 1202 exclusion), skip lines 16 through 21 andenter on line 22 the amount from line 15 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

FDIA2302L 08/08/11

Form 1045 (2011) Page 2

17 Section 1202 exclusion. Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18 Subtract line 17 from line 16. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . 18

19 Enter the loss, if any, from line 21 of your 2011 Schedule D (Form 1040).(Estates and trusts, enter the loss, if any, from line 16 of Schedule D (Form1041).) Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

20 If line 18 is more than line 19, enter the difference. Otherwise, enter -0-. . . . . . . . 20

21 If line 19 is more than line 18, enter the difference. Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

22 Subtract line 20 from line 15. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

23 Domestic production activities deduction from your 2011 Form 1040, line 35, or Form 1040NR, line 34 (orincluded on Form 1041, line 15a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

24 NOL deduction for losses from other years. Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

25 NOL. Combine lines 1, 9, 17, and 21 through 24. If the result is less than zero, enter it here and on page 1,line 1a. If the result is zero or more, you do not have an NOL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

BAA Form 1045 (2011)

BARRY BERRY 123-45-6789

-80,500.7,000.

13,000.0.

6,000.9,000.

7,500.13,500.

0.

4,500.5,000.

4,500.500.500.

500.

30,000.

-50,000.

© Mark Seid, CPA, EA, USTCP -6- 2015

Mark Seid

Text Box

IRC 172(d)(3) No deduction for personal exemptions.

Mark Seid

Text Box

IRC 172(d)(2) No deduction for capital losses. Business capital losses can be offset

Mark Seid

Text Box

by excess of nonbusiness capital gains over excess ordinary nonbusiness deductions.

Mark Seid

Text Box

IRC 172(d)(1) No deduction for net operating loss deduction.

Mark Seid

Text Box

AA

Mark Seid

Text Box

AA

Mark Seid

Text Box

BB

Mark Seid

Text Box

BB

Mark Seid

Text Box

BB

Mark Seid

Text Box

CC

Mark Seid

Text Box

CC

Mark Seid

Line

Mark Seid

Line

Mark Seid

Line

Mark Seid

Line

Mark Seid

Line

Mark Seid

Line

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 7 - 2015

§172(d)(2)(B) Modification – IRC §1202 Exclusion The exclusion allowed for gain on the sale or exchange of qualified small business stock under IRC §1202 is disregarded and the entire gain must be included in the calculation of a net operating loss. IRC §1202 allows and individual to exclude a percentage of gain on the sale or exchange of qualified small business stock held for more than five years. The exclusion percentage is 50% (60% for empowerment zone business stock); 75% for stock acquired after February 17, 2009 and before September 28, 2010; and 100% for stock acquired after September 27, 2010 and before January 1, 2015. §172(d)(3) Modification – Personal Exemptions To calculate the statutory loss no deduction is allowed for personal exemptions or any amounts allowed in lieu of personal exemptions. §172(d)(4) Modification – Nonbusiness Deductions To calculate the statutory loss nonbusiness deductions are allowed only to the extent of nonbusiness income. This paragraph defines certain items of income and deduction as belonging in either the business or nonbusiness category. There are only three items of income and deductions that are differentiated in this subsection as either business or nonbusiness.

1. Gain or loss from the disposition of any depreciable or real property used in a taxpayer’s trade or business is considered attributable to such business. §172(d)(4)(A).

2. Deductions of casualty or theft losses under IRC §165(c)(2) or (c)(3) are considered as

arising from the taxpayer’s trade or business. IRC §165(c)(2) losses are those losses “incurred in any transaction entered into for profit, though not connected with a trade or business.” IRC §165(c)(3) losses are losses that “arise from fire, storm, shipwreck, or other casualty, or from theft.” §172(d)(4)(C).

3. Deductions for Individual Retirement Accounts (IRC §408) and any deduction allowed

under IRC §404 (Keogh, SEP, SIMPLE IRA) to the extent allocable to a self-employed person are not considered attributable to the individual’s trade or business. §172(d)(4)(D).

Treasury Regulation §1.172-3(a)(3)(i) provides one additional categorization: “Wages and salary constitute income attributable to the taxpayer’s trade or business.”

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 8 - 2015

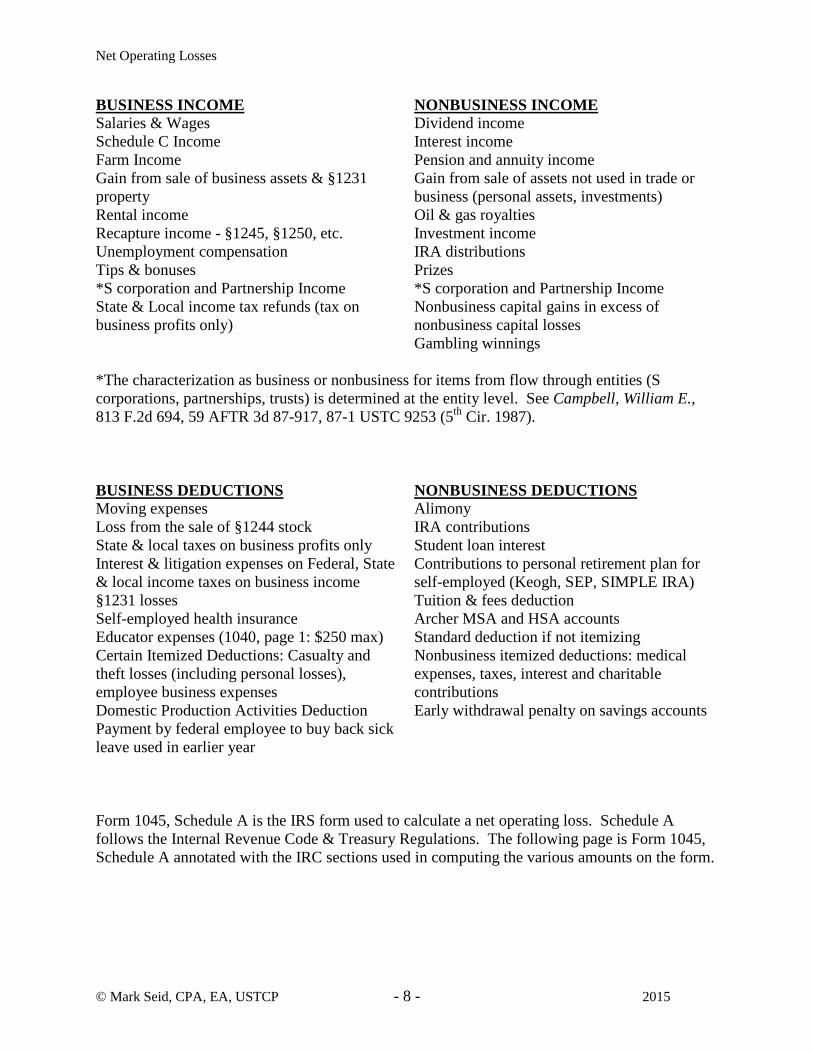

BUSINESS INCOME NONBUSINESS INCOME Salaries & Wages Dividend income Schedule C Income Interest income Farm Income Pension and annuity income Gain from sale of business assets & §1231 property

Gain from sale of assets not used in trade or business (personal assets, investments)

Rental income Oil & gas royalties Recapture income - §1245, §1250, etc. Investment income Unemployment compensation IRA distributions Tips & bonuses Prizes *S corporation and Partnership Income *S corporation and Partnership Income State & Local income tax refunds (tax on business profits only)

Nonbusiness capital gains in excess of nonbusiness capital losses

Gambling winnings *The characterization as business or nonbusiness for items from flow through entities (S corporations, partnerships, trusts) is determined at the entity level. See Campbell, William E., 813 F.2d 694, 59 AFTR 3d 87-917, 87-1 USTC 9253 (5th Cir. 1987). BUSINESS DEDUCTIONS NONBUSINESS DEDUCTIONS Moving expenses Alimony Loss from the sale of §1244 stock IRA contributions State & local taxes on business profits only Student loan interest Interest & litigation expenses on Federal, State & local income taxes on business income

Contributions to personal retirement plan for self-employed (Keogh, SEP, SIMPLE IRA)

§1231 losses Tuition & fees deduction Self-employed health insurance Archer MSA and HSA accounts Educator expenses (1040, page 1: $250 max) Standard deduction if not itemizing Certain Itemized Deductions: Casualty and theft losses (including personal losses), employee business expenses

Nonbusiness itemized deductions: medical expenses, taxes, interest and charitable contributions

Domestic Production Activities Deduction Early withdrawal penalty on savings accounts Payment by federal employee to buy back sick leave used in earlier year

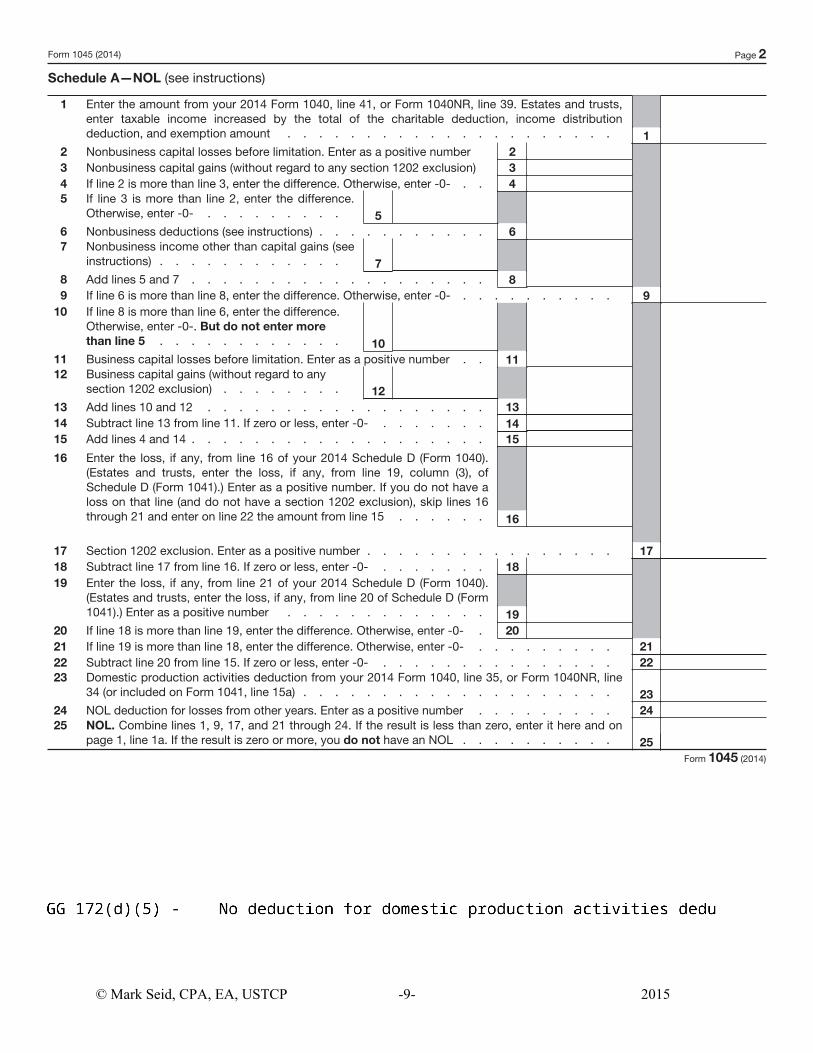

Form 1045, Schedule A is the IRS form used to calculate a net operating loss. Schedule A follows the Internal Revenue Code & Treasury Regulations. The following page is Form 1045, Schedule A annotated with the IRC sections used in computing the various amounts on the form.

Form 1045 (2014) Page 2

Schedule A—NOL (see instructions)

1

Enter the amount from your 2014 Form 1040, line 41, or Form 1040NR, line 39. Estates and trusts, enter taxable income increased by the total of the charitable deduction, income distributiondeduction, and exemption amount . . . . . . . . . . . . . . . . . . . . . 1

2 Nonbusiness capital losses before limitation. Enter as a positive number 2 3 Nonbusiness capital gains (without regard to any section 1202 exclusion) 3 4 If line 2 is more than line 3, enter the difference. Otherwise, enter -0- . . 4 5 If line 3 is more than line 2, enter the difference.

Otherwise, enter -0- . . . . . . . . . 5 6 Nonbusiness deductions (see instructions) . . . . . . . . . . . 6 7 Nonbusiness income other than capital gains (see

instructions) . . . . . . . . . . . . 7 8 Add lines 5 and 7 . . . . . . . . . . . . . . . . . . . 8 9 If line 6 is more than line 8, enter the difference. Otherwise, enter -0- . . . . . . . . . . 9

10

If line 8 is more than line 6, enter the difference. Otherwise, enter -0-. But do not enter more than line 5 . . . . . . . . . . . . 10

11 Business capital losses before limitation. Enter as a positive number . . 11 12 Business capital gains (without regard to any

section 1202 exclusion) . . . . . . . . 12 13 Add lines 10 and 12 . . . . . . . . . . . . . . . . . . 13 14 Subtract line 13 from line 11. If zero or less, enter -0- . . . . . . . 14 15 Add lines 4 and 14 . . . . . . . . . . . . . . . . . . . 15

16

Enter the loss, if any, from line 16 of your 2014 Schedule D (Form 1040). (Estates and trusts, enter the loss, if any, from line 19, column (3), ofSchedule D (Form 1041).) Enter as a positive number. If you do not have a loss on that line (and do not have a section 1202 exclusion), skip lines 16 through 21 and enter on line 22 the amount from line 15 . . . . . . 16

17 Section 1202 exclusion. Enter as a positive number . . . . . . . . . . . . . . . . 17 18 Subtract line 17 from line 16. If zero or less, enter -0- . . . . . . . 18 19

Enter the loss, if any, from line 21 of your 2014 Schedule D (Form 1040). (Estates and trusts, enter the loss, if any, from line 20 of Schedule D (Form1041).) Enter as a positive number . . . . . . . . . . . . . 19

20 If line 18 is more than line 19, enter the difference. Otherwise, enter -0- . 20 21 If line 19 is more than line 18, enter the difference. Otherwise, enter -0- . . . . . . . . . 21 22 Subtract line 20 from line 15. If zero or less, enter -0- . . . . . . . . . . . . . . . 22 23 Domestic production activities deduction from your 2014 Form 1040, line 35, or Form 1040NR, line

34 (or included on Form 1041, line 15a) . . . . . . . . . . . . . . . . . . . . 23 24 NOL deduction for losses from other years. Enter as a positive number . . . . . . . . . 24 25 NOL. Combine lines 1, 9, 17, and 21 through 24. If the result is less than zero, enter it here and on

page 1, line 1a. If the result is zero or more, you do not have an NOL . . . . . . . . . . 25Form 1045 (2014)

© Mark Seid, CPA, EA, USTCP -9- 2015

Mark Seid

Text Box

IRC Section 172(d) illustrated on Form 1045 Schedule A

Mark Seid

Text Box

EE

Mark Seid

Text Box

CC

Mark Seid

Text Box

FF

Mark Seid

Text Box

FF

Mark Seid

Text Box

FF

Mark Seid

Text Box

BB

Mark Seid

Text Box

BB

Mark Seid

Text Box

BB

Mark Seid

Text Box

DD

Mark Seid

Text Box

GG

Mark Seid

Text Box

AA

Mark Seid

Typewritten Text

AA 172(d)(1) - No deduction for NOLD BB 172(d)(2)(A) - No deduction for capital losses - business CC 172(d)(2)(A) - No deduction for capital losses - nonbusiness DD 172(d)(2)(B) - No deduction for IRC Section 1202 gains EE 172(d)(3) - No deduction for personal exemptions FF 172(d)(4) - No nonbusiness deductions in excess of nonbusiness income GG 172(d)(5) - No deduction for domestic production activities deduction

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 10 - 2015

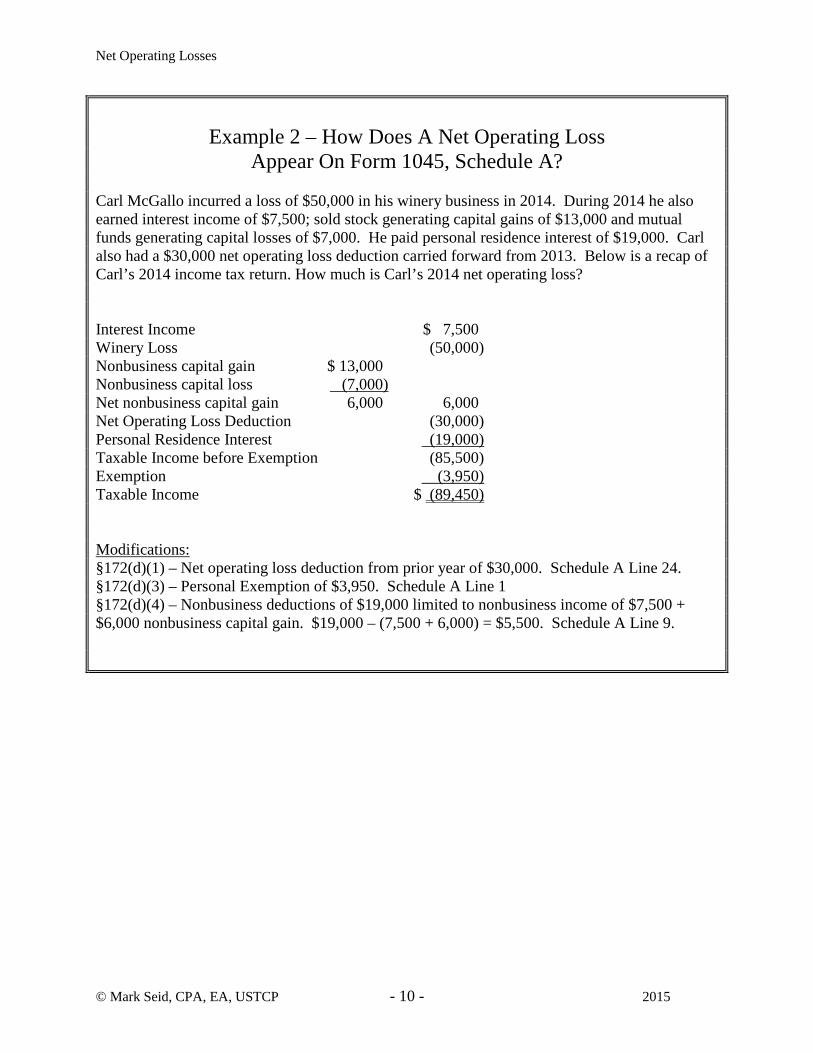

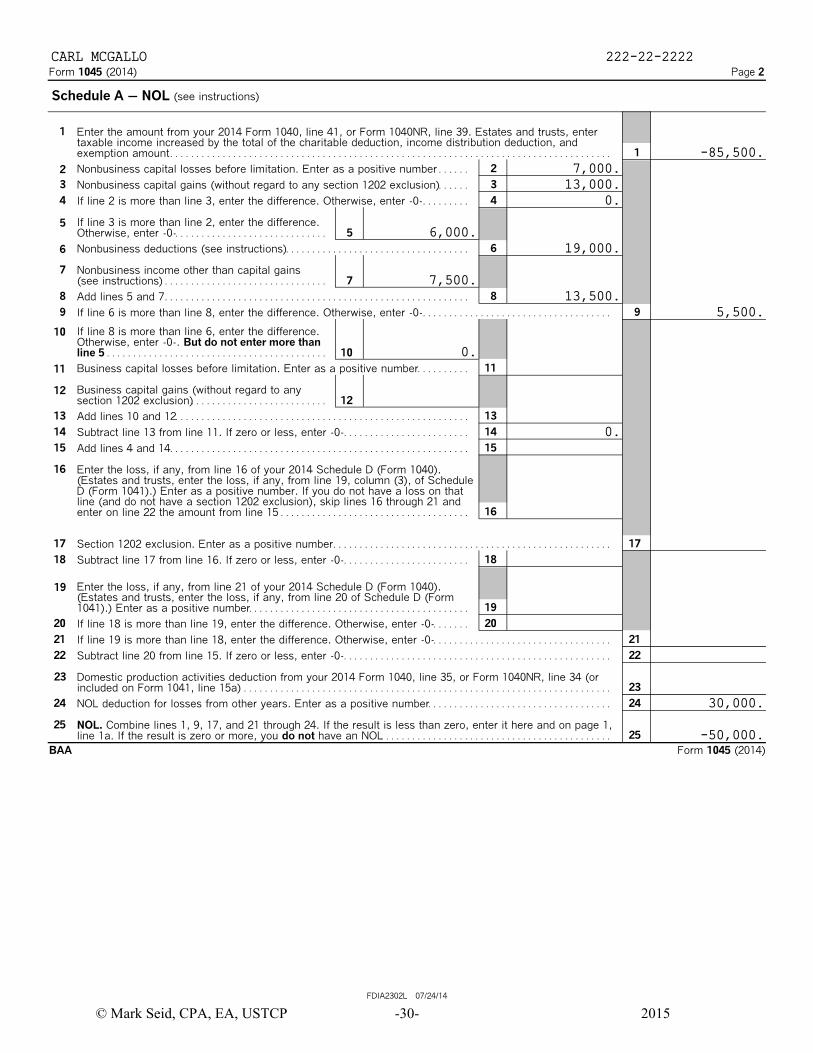

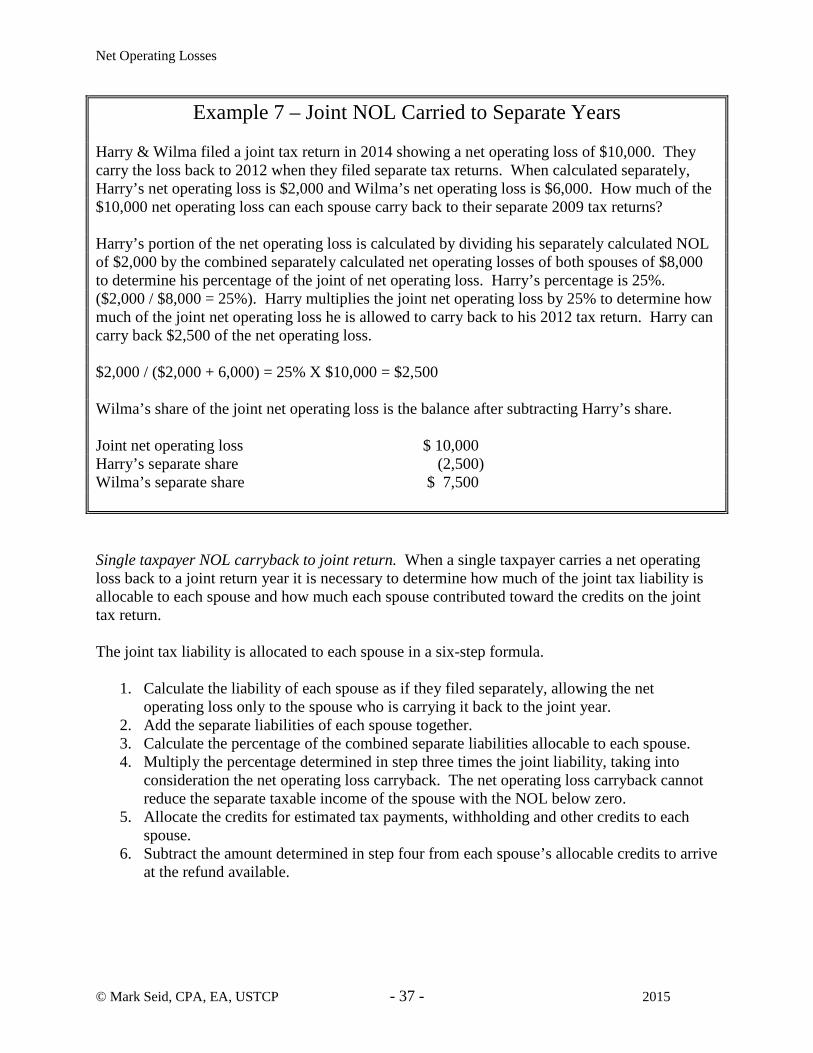

Example 2 – How Does A Net Operating Loss

Appear On Form 1045, Schedule A? Carl McGallo incurred a loss of $50,000 in his winery business in 2014. During 2014 he also earned interest income of $7,500; sold stock generating capital gains of $13,000 and mutual funds generating capital losses of $7,000. He paid personal residence interest of $19,000. Carl also had a $30,000 net operating loss deduction carried forward from 2013. Below is a recap of Carl’s 2014 income tax return. How much is Carl’s 2014 net operating loss? Interest Income $ 7,500 Winery Loss (50,000) Nonbusiness capital gain $ 13,000 Nonbusiness capital loss (7,000) Net nonbusiness capital gain 6,000 6,000 Net Operating Loss Deduction (30,000) Personal Residence Interest (19,000) Taxable Income before Exemption (85,500) Exemption (3,950) Taxable Income $ (89,450) Modifications: §172(d)(1) – Net operating loss deduction from prior year of $30,000. Schedule A Line 24. §172(d)(3) – Personal Exemption of $3,950. Schedule A Line 1 §172(d)(4) – Nonbusiness deductions of $19,000 limited to nonbusiness income of $7,500 + $6,000 nonbusiness capital gain. $19,000 – (7,500 + 6,000) = $5,500. Schedule A Line 9.

Form 1045 (2014) Page 2

Schedule A ' NOL (see instructions)

1 Enter the amount from your 2014 Form 1040, line 41, or Form 1040NR, line 39. Estates and trusts, entertaxable income increased by the total of the charitable deduction, income distribution deduction, and

1exemption amount. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2Nonbusiness capital losses before limitation. Enter as a positive number . . . . . . 2

3 3Nonbusiness capital gains (without regard to any section 1202 exclusion). . . . . .

4 4If line 2 is more than line 3, enter the difference. Otherwise, enter -0-. . . . . . . . .

If line 3 is more than line 2, enter the difference.55Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6Nonbusiness deductions (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Nonbusiness income other than capital gains7(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8 8Add lines 5 and 7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 9If line 6 is more than line 8, enter the difference. Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If line 8 is more than line 6, enter the difference.10Otherwise, enter -0-. But do not enter more than

10line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11Business capital losses before limitation. Enter as a positive number. . . . . . . . . . 11

Business capital gains (without regard to any1212section 1202 exclusion). . . . . . . . . . . . . . . . . . . . . . . . . .

13 13Add lines 10 and 12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

14 14Subtract line 13 from line 11. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . .

15 15Add lines 4 and 14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

16 Enter the loss, if any, from line 16 of your 2014 Schedule D (Form 1040).(Estates and trusts, enter the loss, if any, from line 19, column (3), of ScheduleD (Form 1041).) Enter as a positive number. If you do not have a loss on thatline (and do not have a section 1202 exclusion), skip lines 16 through 21 and

16enter on line 22 the amount from line 15 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17 17Section 1202 exclusion. Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

18 18Subtract line 17 from line 16. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . .

Enter the loss, if any, from line 21 of your 2014 Schedule D (Form 1040).19(Estates and trusts, enter the loss, if any, from line 20 of Schedule D (Form

191041).) Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20 20If line 18 is more than line 19, enter the difference. Otherwise, enter -0-. . . . . . .

21 21If line 19 is more than line 18, enter the difference. Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2222 Subtract line 20 from line 15. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

23 Domestic production activities deduction from your 2014 Form 1040, line 35, or Form 1040NR, line 34 (or23included on Form 1041, line 15a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

24 24NOL deduction for losses from other years. Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

25 NOL. Combine lines 1, 9, 17, and 21 through 24. If the result is less than zero, enter it here and on page 1,25line 1a. If the result is zero or more, you do not have an NOL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

BAA Form 1045 (2014)

FDIA2302L 07/24/14

CARL MCGALLO 222-22-2222

-85,500.7,000.

13,000.0.

6,000.19,000.

7,500.13,500.

5,500.

0.

0.

30,000.

-50,000.

© Mark Seid, CPA, EA, USTCP -11- 2015

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 12 - 2015

INDIVIDUAL NOL QUICK WORKSHEET

(No business capital gains or losses) a. Taxable Income before Exemptions $(_______)

Modifications:

b. Net Operating Loss Deduction $_______

c. Capital Losses * _______

d. IRC §1202 exclusion _______

Excess Nonbusiness Deductions

e. Nonbusiness Deductions $_______

f. Nonbusiness Income (_______)

g. Excess Nonbusiness Deductions (e-f) _______

h. DPAD _______

i. Total Modifications (b+c+d+g+h) ________

j. Net Operating Loss (a + i) $________

* Separate business and nonbusiness capital gains and losses. Business capital losses can only be offset by excess of sum of (1) nonbusiness capital gains and (2) nonbusiness ordinary income over nonbusiness deductions. See example earlier for a detailed example of how business capital losses impact the calculation of a net operating loss.

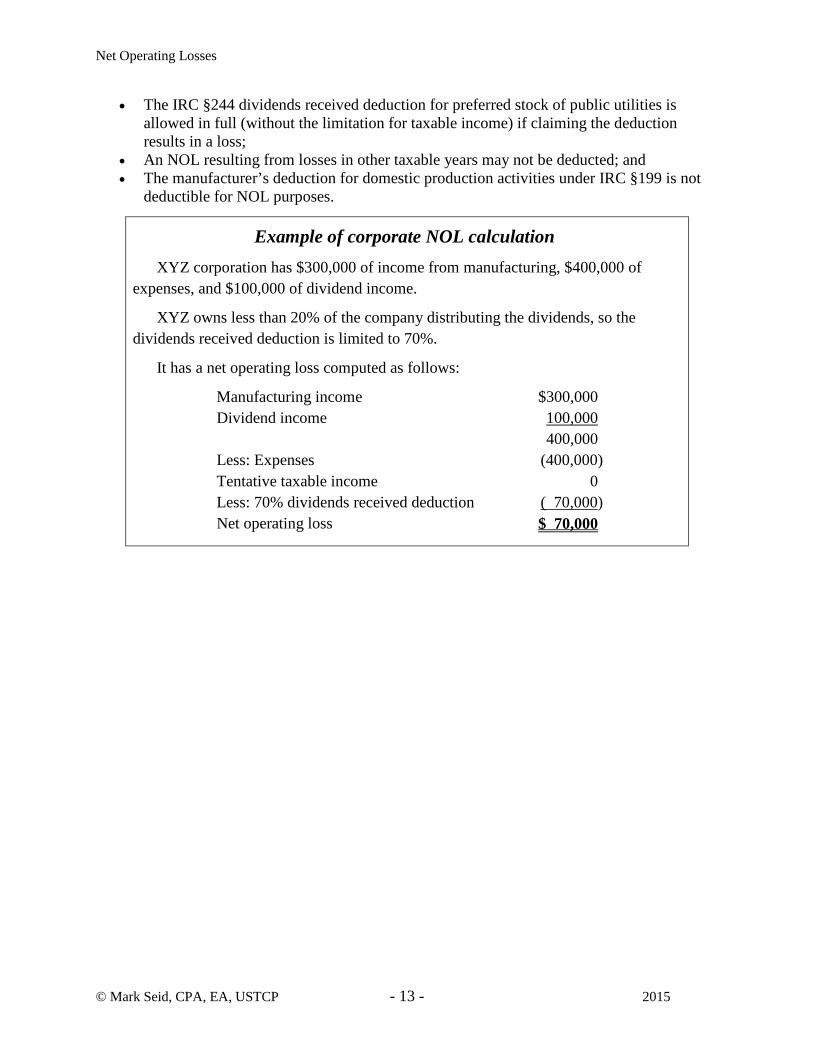

Computing NOLs for corporate taxpayers The NOL of a corporate taxpayer is calculated by taking the excess of deductions over gross

income, with some adjustments. (IRC §172(a)–(c)) The adjustments are:

• A dividends received deduction is allowed in full if claiming the deduction results in a loss. A corporation owning less than 20% of the distributing corporation may deduct 70% of the dividends received or accrued. The deduction is increased to 80% for a corporation owning at least 80% of the distributing corporation;

• A deduction for dividends paid on certain preferred stock of public utilities is allowed in full without regard to the limitations under IRC §247;

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 13 - 2015

• The IRC §244 dividends received deduction for preferred stock of public utilities is allowed in full (without the limitation for taxable income) if claiming the deduction results in a loss;

• An NOL resulting from losses in other taxable years may not be deducted; and • The manufacturer’s deduction for domestic production activities under IRC §199 is not

deductible for NOL purposes.

Example of corporate NOL calculation XYZ corporation has $300,000 of income from manufacturing, $400,000 of

expenses, and $100,000 of dividend income.

XYZ owns less than 20% of the company distributing the dividends, so the dividends received deduction is limited to 70%.

It has a net operating loss computed as follows:

Manufacturing income $300,000 Dividend income 100,000

400,000 Less: Expenses (400,000) Tentative taxable income 0 Less: 70% dividends received deduction ( 70,000) Net operating loss $ 70,000

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 14 - 2015

PART II – DETERMINE THE CARRYBACK AND CARRYOVER PERIODS FOR A NET OPERATING LOSS

STANDARD CARRYBACK PERIOD The carryback and carryover periods for a net operating loss are governed under IRC §172(b)(1).

172(b)(1)(A)General rule.— Except as otherwise provided in this paragraph, a net operating loss for any taxable year:

172(b)(1)(A)(i) shall be a net operating loss carryback to each of the 2 taxable years preceding the taxable year of such loss, and 172(b)(1)(A)(ii) shall be a net operating loss carryover to each of the 20 taxable years following the taxable year of the loss.

A net operating loss is first carried back two (2) years and then forward twenty (20) years. For a net operating loss incurred in 2014 the first carryback year is 2012. A net operating loss that is not fully absorbed in the carryback or intervening year(s) will be carried forward twenty (20) years past the loss year. For a net operating loss incurred in 2014 the carryover period is 2015 through 2034. Any portion of a net operating loss not absorbed by the year 2034 will expire and is lost forever.

Example 3 – Net Operating Loss Carryback and Carryover

Sarah started a new business in 2014 making chewing gum from fish flavors: Juicy Jellyfish, Blowfish Bubble, Sweet Salmon and Luscious Lungfish were her favorites. Sarah’s business did not do well its first year and she generated a net operating loss of $50,000 on her 2014 tax return. Sarah does not live in a federally declared disaster area. Q: In what years will Sarah be able to utilize her 2014 net operating loss? A: Sarah can carryback her net operating loss to 2012. If her loss is not fully absorbed in 2012 Sarah will carry the remaining portion of her loss to 2013. If her loss is still not fully absorbed after carrying back to both 2012 and 2013, Sarah will carry her loss forward to 2015 and subsequent years for the next 20 years. If Sarah’s loss is not fully absorbed by 2034 (20 years after the original loss year) it will expire.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 15 - 2015

Periods of less than twelve (12) months. Any taxable period that contains less than 12 months is considered to be a full taxable year for purposes of determining the number of years a net operating loss is carried to under IRC §172(b)(1). Treasury Regulation §1.172-4(a)(2). A short taxable year in the year of a taxpayer’s birth or death is considered a full taxable year for purposes of determining the carryback or carryover years. Other Carryback Periods Taxpayer Relief Act of 1997 changed the carryback period from three (3) years to two (2) years and the carryover period from fifteen (15) years to twenty (20) years. This change to the carryback and carryover periods was effective for tax years beginning after August 5, 1997. Three-Year Carryback A 3-year carryback period is required in certain cases. IRC §172(b)(1)(F) requires a taxpayer to carry a net operating loss back three years rather than two years required under IRC §172(b)(1)(A). There are three categories of individuals that are required to use the 3-year carryback.

1. Individuals with losses arising from fire, storm, shipwreck, or other casualty, or from theft,

2. Small businesses with net operating losses attributable to federally declared disasters. The term “federally declared disaster” means and disaster that the President of the United States has determined to warrant assistance under the Robert T. Stafford Disaster Relief and Emergency Assistance Act. A list of presidentially declared disasters is available on the IRS website at http://www.irs.gov/newsroom/article/0,,id=98936,00.html. The list is organized by state.

3. For taxpayers engaged in the trade or business of farming (defined below), net operating losses attributable to federally declared disasters.

For purposes of #2 above, a small business is a sole proprietorship or partnership whose average annual gross receipts were $5 million or less in the three-year period ending with the year of the net operating loss. Five-Year Carryback Qualified disaster losses. The carryback period for a qualified disaster loss is five years. Qualified disaster losses are only available for federally declared disasters occurring before January 1, 2010. Such losses are limited to the amounts allowed as casualty losses under IRC §165 plus the deductions allowed for qualified disaster expenses under IRC §198A. The losses must be attributable to a federally declared disaster and cannot otherwise exceed the regular net operating loss.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 16 - 2015

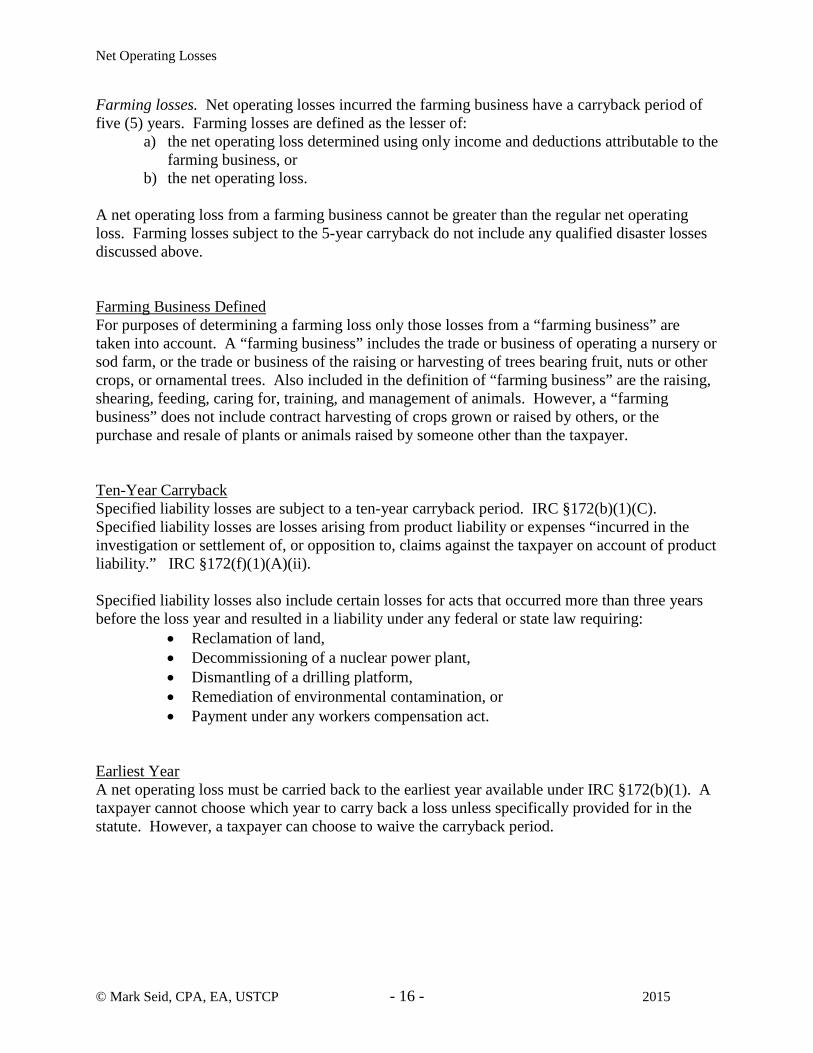

Farming losses. Net operating losses incurred the farming business have a carryback period of five (5) years. Farming losses are defined as the lesser of:

a) the net operating loss determined using only income and deductions attributable to the farming business, or

b) the net operating loss. A net operating loss from a farming business cannot be greater than the regular net operating loss. Farming losses subject to the 5-year carryback do not include any qualified disaster losses discussed above. Farming Business Defined For purposes of determining a farming loss only those losses from a “farming business” are taken into account. A “farming business” includes the trade or business of operating a nursery or sod farm, or the trade or business of the raising or harvesting of trees bearing fruit, nuts or other crops, or ornamental trees. Also included in the definition of “farming business” are the raising, shearing, feeding, caring for, training, and management of animals. However, a “farming business” does not include contract harvesting of crops grown or raised by others, or the purchase and resale of plants or animals raised by someone other than the taxpayer. Ten-Year Carryback Specified liability losses are subject to a ten-year carryback period. IRC §172(b)(1)(C). Specified liability losses are losses arising from product liability or expenses “incurred in the investigation or settlement of, or opposition to, claims against the taxpayer on account of product liability.” IRC §172(f)(1)(A)(ii). Specified liability losses also include certain losses for acts that occurred more than three years before the loss year and resulted in a liability under any federal or state law requiring:

• Reclamation of land, • Decommissioning of a nuclear power plant, • Dismantling of a drilling platform, • Remediation of environmental contamination, or • Payment under any workers compensation act.

Earliest Year A net operating loss must be carried back to the earliest year available under IRC §172(b)(1). A taxpayer cannot choose which year to carry back a loss unless specifically provided for in the statute. However, a taxpayer can choose to waive the carryback period.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 17 - 2015

WAIVING THE CARRYBACK PERIOD Taxpayers may elect to waive the carryback. Any taxpayer may relinquish the entire carryback period with a timely election. Once made, the election is irrevocable for that year. IRC §172(b)(3). Elections to waive carryback period must be timely. An election to waive the carryback period, or multiple carryback periods, must be made by the due date of the tax return (including extensions). If a taxpayer files their original tax return by the unextended due date and later decides that they want to waive the carryback period, there is a brief window of opportunity available to secure the election. For timely filed returns without extensions, an amended return can be filed electing to waive the carryback period. The amended return must be filed within six (6) months of the due date of the original return (excluding extensions). At the top of the statement electing to waive the carryback period, enter the phrase “Filed pursuant to section 301.9100-2.” Multiple carryback periods available. If a taxpayer is eligible for more than one carryback period, separate elections to waive each carryback period are required. For example, if a taxpayer is eligible to carry back a net operating loss 5 years due to a qualified disaster loss, both an election not to claim the 5-year carryback and an election not to claim the regular 2-year carryback must be made. Merely carrying a loss back two years is not an effective election to waive the 5-year carryback period. Relinquishing the carryback period does not extend the carryover period. Both the carryback period and the carryover period are absolute. Relinquishing any number of years in a carryback period does not add that number of years to the carryover period. Regular Tax & Alternative Minimum Tax Net Operating Losses. Waiving a carryback period is effective for both regular income tax and alternative minimum tax. Separate waivers are not permissible. Rev. Rul. 87-44, 1987-1 CB 3. Multiple taxpayers have attempted to make elections to waive the carryback of their regular tax net operating loss but not their alternative tax net operating loss. Miller v. Commissioner, 96-2 USTC ¶50,614, 99 F3d 1042 (CA-11, 1996); Plumb v. Commissioner 97 T.C. 632 (1991). Failure to make election. When an election to waive a carryback period is not made, the net operating loss must be carried back. If the statute of limitations for making the carryback has expired, the net operating loss carryover must still be adjusted as if it had been carried back. See “How is the NOL Carried Back” later.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 18 - 2015

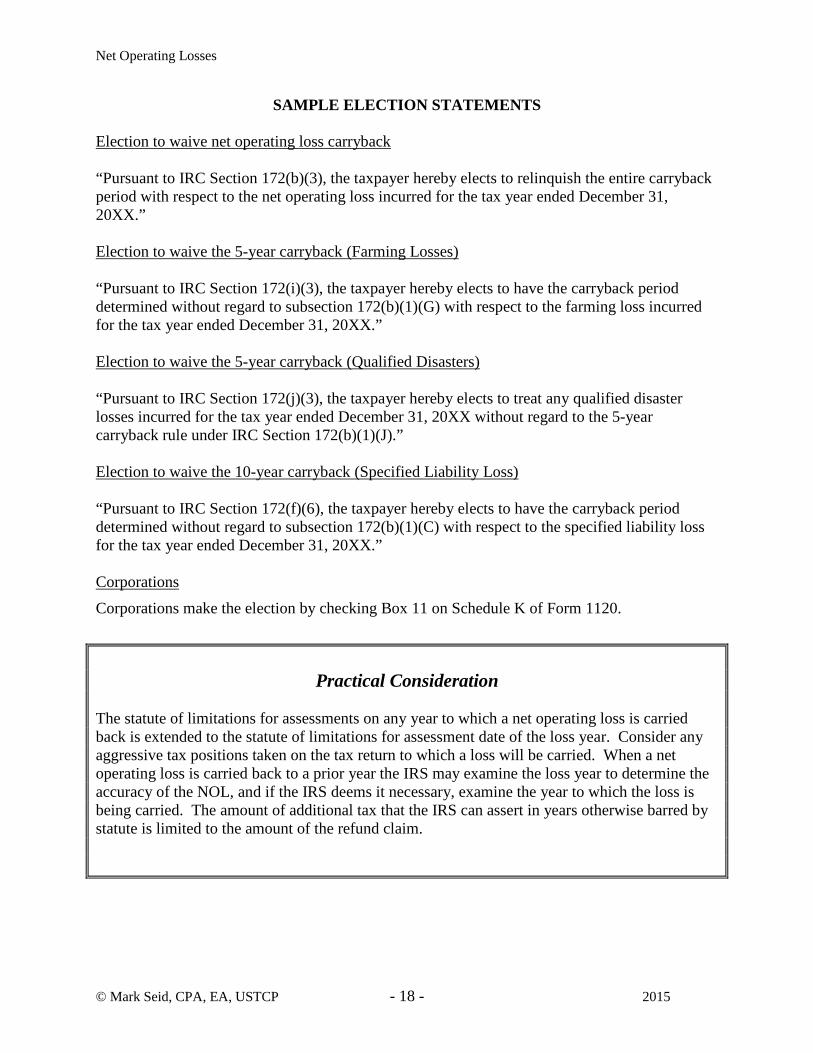

SAMPLE ELECTION STATEMENTS Election to waive net operating loss carryback “Pursuant to IRC Section 172(b)(3), the taxpayer hereby elects to relinquish the entire carryback period with respect to the net operating loss incurred for the tax year ended December 31, 20XX.” Election to waive the 5-year carryback (Farming Losses) “Pursuant to IRC Section 172(i)(3), the taxpayer hereby elects to have the carryback period determined without regard to subsection 172(b)(1)(G) with respect to the farming loss incurred for the tax year ended December 31, 20XX.” Election to waive the 5-year carryback (Qualified Disasters) “Pursuant to IRC Section 172(j)(3), the taxpayer hereby elects to treat any qualified disaster losses incurred for the tax year ended December 31, 20XX without regard to the 5-year carryback rule under IRC Section 172(b)(1)(J).” Election to waive the 10-year carryback (Specified Liability Loss) “Pursuant to IRC Section 172(f)(6), the taxpayer hereby elects to have the carryback period determined without regard to subsection 172(b)(1)(C) with respect to the specified liability loss for the tax year ended December 31, 20XX.” Corporations

Corporations make the election by checking Box 11 on Schedule K of Form 1120.

Practical Consideration The statute of limitations for assessments on any year to which a net operating loss is carried back is extended to the statute of limitations for assessment date of the loss year. Consider any aggressive tax positions taken on the tax return to which a loss will be carried. When a net operating loss is carried back to a prior year the IRS may examine the loss year to determine the accuracy of the NOL, and if the IRS deems it necessary, examine the year to which the loss is being carried. The amount of additional tax that the IRS can assert in years otherwise barred by statute is limited to the amount of the refund claim.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 19 - 2015

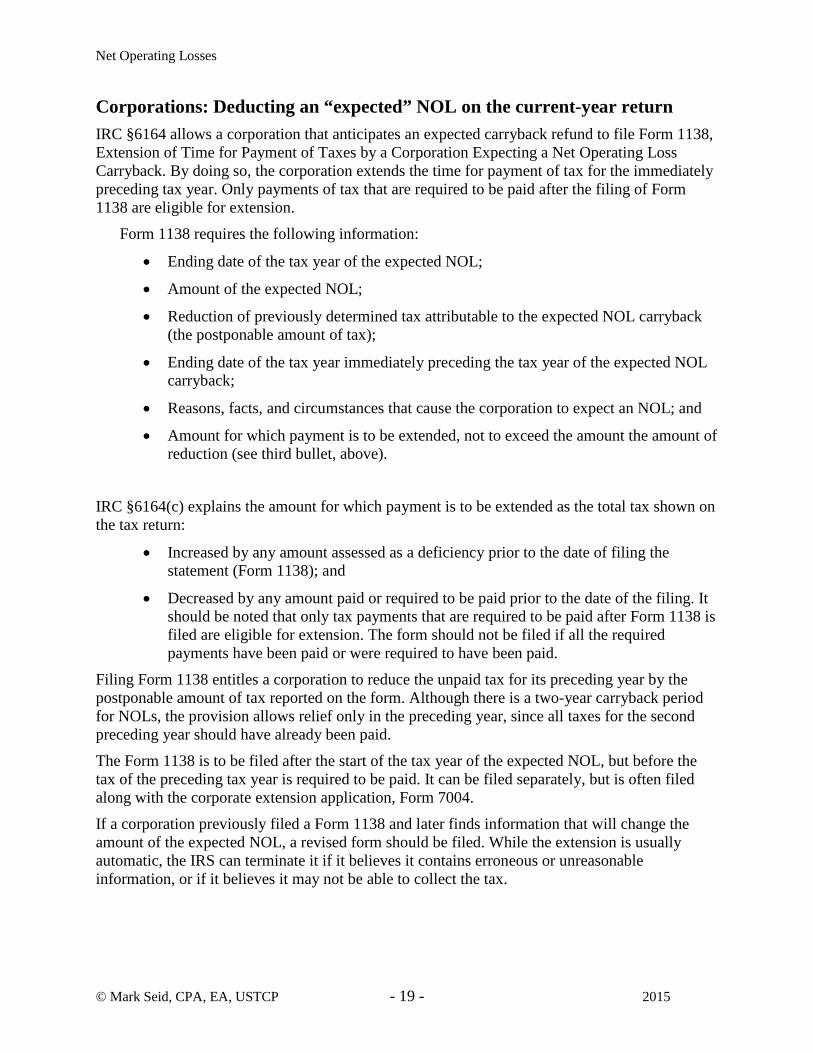

Corporations: Deducting an “expected” NOL on the current-year return IRC §6164 allows a corporation that anticipates an expected carryback refund to file Form 1138, Extension of Time for Payment of Taxes by a Corporation Expecting a Net Operating Loss Carryback. By doing so, the corporation extends the time for payment of tax for the immediately preceding tax year. Only payments of tax that are required to be paid after the filing of Form 1138 are eligible for extension.

Form 1138 requires the following information:

• Ending date of the tax year of the expected NOL;

• Amount of the expected NOL;

• Reduction of previously determined tax attributable to the expected NOL carryback (the postponable amount of tax);

• Ending date of the tax year immediately preceding the tax year of the expected NOL carryback;

• Reasons, facts, and circumstances that cause the corporation to expect an NOL; and

• Amount for which payment is to be extended, not to exceed the amount the amount of reduction (see third bullet, above).

IRC §6164(c) explains the amount for which payment is to be extended as the total tax shown on the tax return:

• Increased by any amount assessed as a deficiency prior to the date of filing the statement (Form 1138); and

• Decreased by any amount paid or required to be paid prior to the date of the filing. It should be noted that only tax payments that are required to be paid after Form 1138 is filed are eligible for extension. The form should not be filed if all the required payments have been paid or were required to have been paid.

Filing Form 1138 entitles a corporation to reduce the unpaid tax for its preceding year by the postponable amount of tax reported on the form. Although there is a two-year carryback period for NOLs, the provision allows relief only in the preceding year, since all taxes for the second preceding year should have already been paid.

The Form 1138 is to be filed after the start of the tax year of the expected NOL, but before the tax of the preceding tax year is required to be paid. It can be filed separately, but is often filed along with the corporate extension application, Form 7004.

If a corporation previously filed a Form 1138 and later finds information that will change the amount of the expected NOL, a revised form should be filed. While the extension is usually automatic, the IRS can terminate it if it believes it contains erroneous or unreasonable information, or if it believes it may not be able to collect the tax.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 20 - 2015

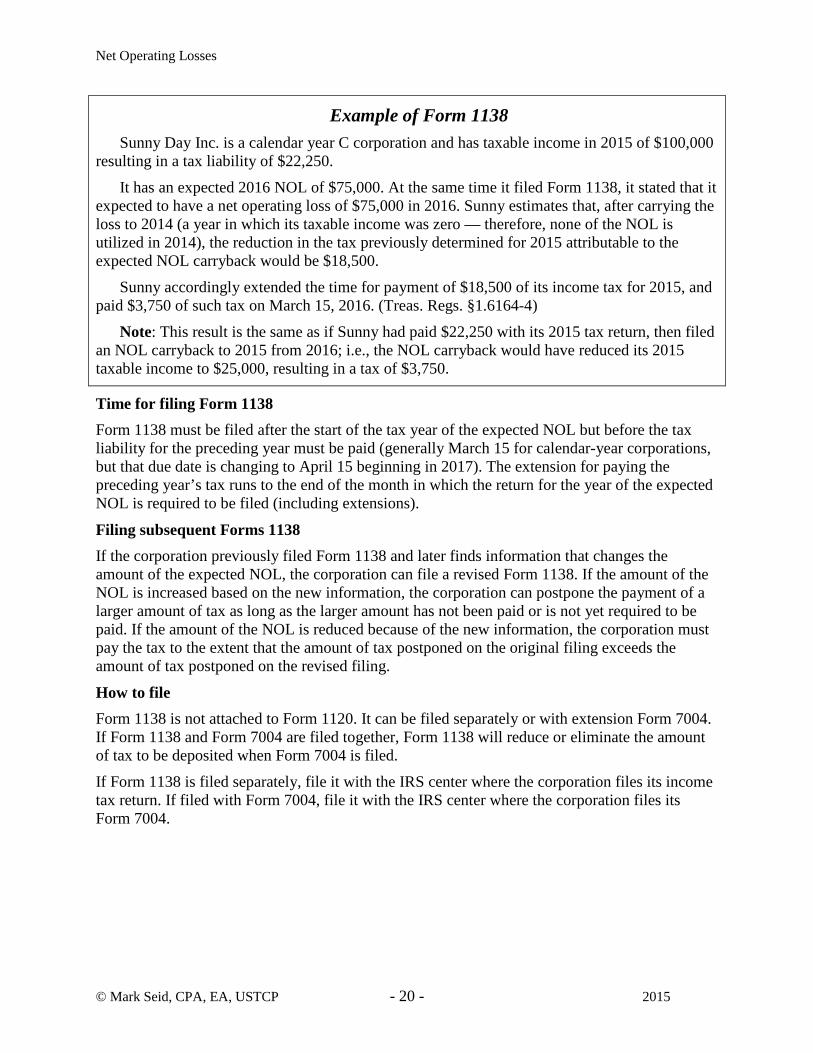

Example of Form 1138 Sunny Day Inc. is a calendar year C corporation and has taxable income in 2015 of $100,000

resulting in a tax liability of $22,250.

It has an expected 2016 NOL of $75,000. At the same time it filed Form 1138, it stated that it expected to have a net operating loss of $75,000 in 2016. Sunny estimates that, after carrying the loss to 2014 (a year in which its taxable income was zero — therefore, none of the NOL is utilized in 2014), the reduction in the tax previously determined for 2015 attributable to the expected NOL carryback would be $18,500.

Sunny accordingly extended the time for payment of $18,500 of its income tax for 2015, and paid $3,750 of such tax on March 15, 2016. (Treas. Regs. §1.6164-4)

Note: This result is the same as if Sunny had paid $22,250 with its 2015 tax return, then filed an NOL carryback to 2015 from 2016; i.e., the NOL carryback would have reduced its 2015 taxable income to $25,000, resulting in a tax of $3,750.

Time for filing Form 1138 Form 1138 must be filed after the start of the tax year of the expected NOL but before the tax liability for the preceding year must be paid (generally March 15 for calendar-year corporations, but that due date is changing to April 15 beginning in 2017). The extension for paying the preceding year’s tax runs to the end of the month in which the return for the year of the expected NOL is required to be filed (including extensions).

Filing subsequent Forms 1138 If the corporation previously filed Form 1138 and later finds information that changes the amount of the expected NOL, the corporation can file a revised Form 1138. If the amount of the NOL is increased based on the new information, the corporation can postpone the payment of a larger amount of tax as long as the larger amount has not been paid or is not yet required to be paid. If the amount of the NOL is reduced because of the new information, the corporation must pay the tax to the extent that the amount of tax postponed on the original filing exceeds the amount of tax postponed on the revised filing.

How to file Form 1138 is not attached to Form 1120. It can be filed separately or with extension Form 7004. If Form 1138 and Form 7004 are filed together, Form 1138 will reduce or eliminate the amount of tax to be deposited when Form 7004 is filed.

If Form 1138 is filed separately, file it with the IRS center where the corporation files its income tax return. If filed with Form 7004, file it with the IRS center where the corporation files its Form 7004.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 21 - 2015

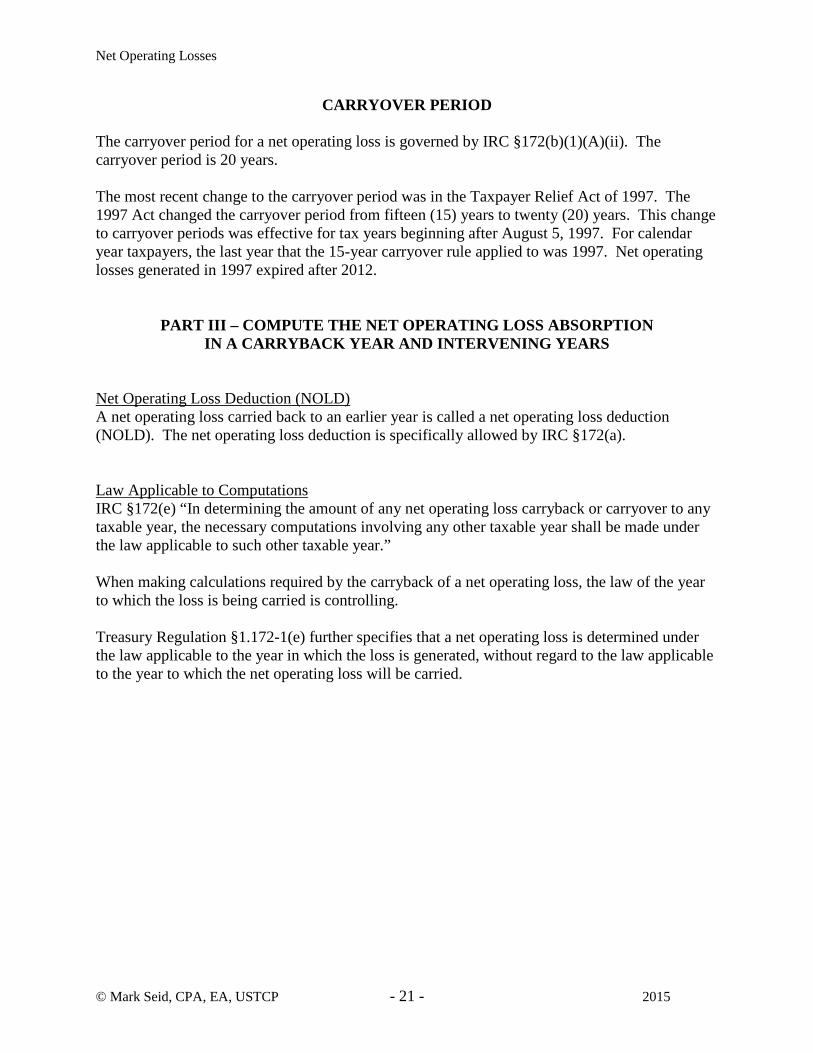

CARRYOVER PERIOD The carryover period for a net operating loss is governed by IRC §172(b)(1)(A)(ii). The carryover period is 20 years. The most recent change to the carryover period was in the Taxpayer Relief Act of 1997. The 1997 Act changed the carryover period from fifteen (15) years to twenty (20) years. This change to carryover periods was effective for tax years beginning after August 5, 1997. For calendar year taxpayers, the last year that the 15-year carryover rule applied to was 1997. Net operating losses generated in 1997 expired after 2012.

PART III – COMPUTE THE NET OPERATING LOSS ABSORPTION IN A CARRYBACK YEAR AND INTERVENING YEARS

Net Operating Loss Deduction (NOLD) A net operating loss carried back to an earlier year is called a net operating loss deduction (NOLD). The net operating loss deduction is specifically allowed by IRC §172(a). Law Applicable to Computations IRC §172(e) “In determining the amount of any net operating loss carryback or carryover to any taxable year, the necessary computations involving any other taxable year shall be made under the law applicable to such other taxable year.” When making calculations required by the carryback of a net operating loss, the law of the year to which the loss is being carried is controlling. Treasury Regulation §1.172-1(e) further specifies that a net operating loss is determined under the law applicable to the year in which the loss is generated, without regard to the law applicable to the year to which the net operating loss will be carried.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 22 - 2015

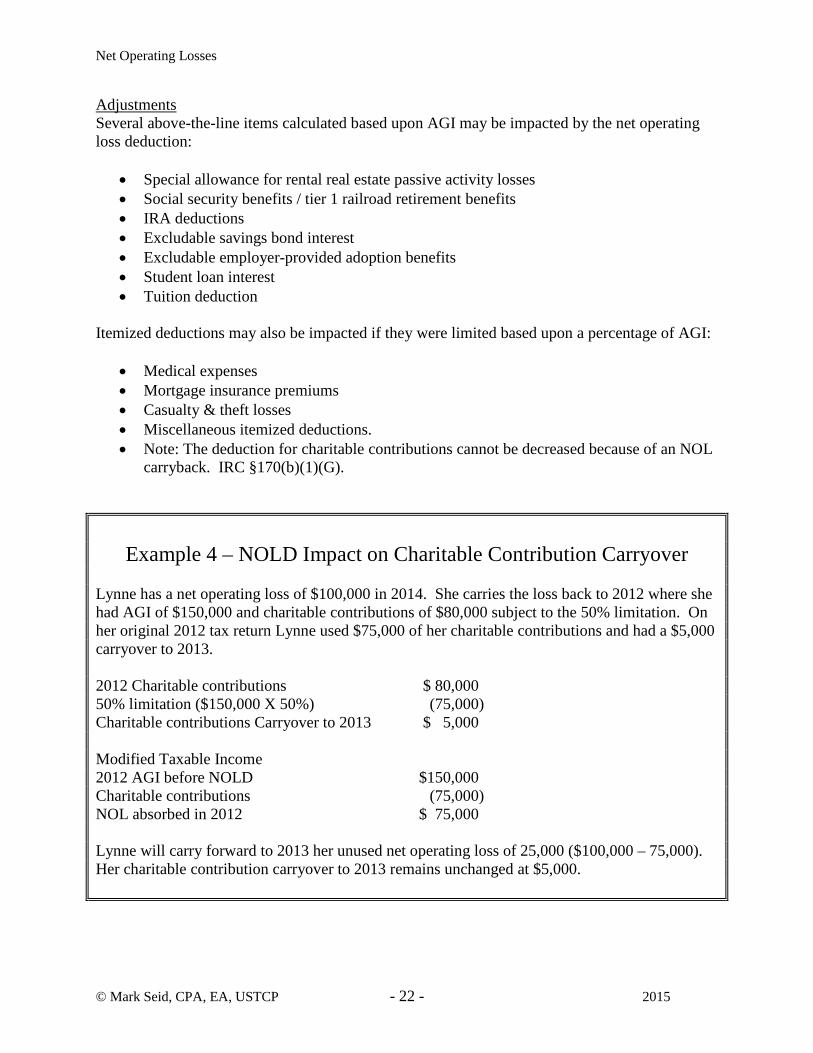

Adjustments Several above-the-line items calculated based upon AGI may be impacted by the net operating loss deduction:

• Special allowance for rental real estate passive activity losses • Social security benefits / tier 1 railroad retirement benefits • IRA deductions • Excludable savings bond interest • Excludable employer-provided adoption benefits • Student loan interest • Tuition deduction

Itemized deductions may also be impacted if they were limited based upon a percentage of AGI:

• Medical expenses • Mortgage insurance premiums • Casualty & theft losses • Miscellaneous itemized deductions. • Note: The deduction for charitable contributions cannot be decreased because of an NOL

carryback. IRC §170(b)(1)(G).

Example 4 – NOLD Impact on Charitable Contribution Carryover

Lynne has a net operating loss of $100,000 in 2014. She carries the loss back to 2012 where she had AGI of $150,000 and charitable contributions of $80,000 subject to the 50% limitation. On her original 2012 tax return Lynne used $75,000 of her charitable contributions and had a $5,000 carryover to 2013. 2012 Charitable contributions $ 80,000 50% limitation ($150,000 X 50%) (75,000) Charitable contributions Carryover to 2013 $ 5,000 Modified Taxable Income 2012 AGI before NOLD $150,000 Charitable contributions (75,000) NOL absorbed in 2012 $ 75,000 Lynne will carry forward to 2013 her unused net operating loss of 25,000 ($100,000 – 75,000). Her charitable contribution carryover to 2013 remains unchanged at $5,000.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 23 - 2015

Phase-outs in the carryback year may be impacted when the net operating loss deduction is taken into consideration:

• Pease limitation on overall itemized deductions • Phase-out of personal Exemptions

Credits in the carryback year may be impacted by the net operating loss deduction:

• Education credits • Retirement Saver’s credit • First-time homebuyer credit • Child and dependent care credit • Credit for the elderly and disabled

Note: Credits that carryover to prior and succeeding years may be impacted by a change in tax liability. In cases where credits are freed up, taxpayers may be required to file amended tax returns for years other than the carryback year. Credits affected by the decrease in tax liability include the foreign tax credit, general business credit and alternative minimum tax credit. The amount of the net operating loss carryback and carryover is determined under IRC §172(b)(2).

172(b)(2)Amount of carrybacks and carryovers.— The entire amount of the net operating loss for any taxable year (hereinafter in this section referred to as the “loss year”) shall be carried to the earliest of the taxable years to which (by reason of paragraph (1)) such loss may be carried. The portion of such loss which shall be carried to each of the other taxable years shall be the excess, if any, of the amount of such loss over the sum of the taxable income for each of the prior taxable years to which such loss may be carried. For purposes of the preceding sentence, the taxable income for any such prior taxable year shall be computed:

172(b)(2)(A) with the modifications specified in subsection (d) other than paragraphs (1), (4), and (5) thereof, and 172(b)(2)(B) by determining the amount of the net operating loss deduction without regard to the net operating loss for the loss year or for any taxable year thereafter,

and the taxable income so computed shall not be considered to be less than zero.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 24 - 2015

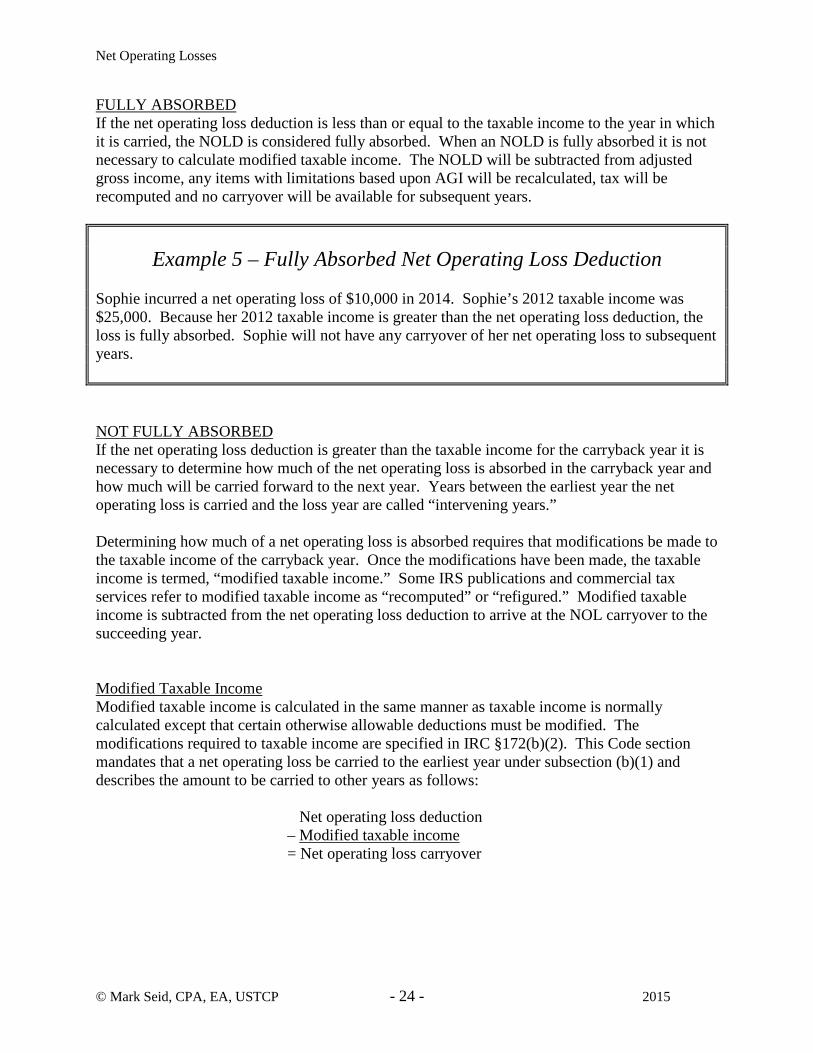

FULLY ABSORBED If the net operating loss deduction is less than or equal to the taxable income to the year in which it is carried, the NOLD is considered fully absorbed. When an NOLD is fully absorbed it is not necessary to calculate modified taxable income. The NOLD will be subtracted from adjusted gross income, any items with limitations based upon AGI will be recalculated, tax will be recomputed and no carryover will be available for subsequent years.

Example 5 – Fully Absorbed Net Operating Loss Deduction

Sophie incurred a net operating loss of $10,000 in 2014. Sophie’s 2012 taxable income was $25,000. Because her 2012 taxable income is greater than the net operating loss deduction, the loss is fully absorbed. Sophie will not have any carryover of her net operating loss to subsequent years. NOT FULLY ABSORBED If the net operating loss deduction is greater than the taxable income for the carryback year it is necessary to determine how much of the net operating loss is absorbed in the carryback year and how much will be carried forward to the next year. Years between the earliest year the net operating loss is carried and the loss year are called “intervening years.” Determining how much of a net operating loss is absorbed requires that modifications be made to the taxable income of the carryback year. Once the modifications have been made, the taxable income is termed, “modified taxable income.” Some IRS publications and commercial tax services refer to modified taxable income as “recomputed” or “refigured.” Modified taxable income is subtracted from the net operating loss deduction to arrive at the NOL carryover to the succeeding year. Modified Taxable Income Modified taxable income is calculated in the same manner as taxable income is normally calculated except that certain otherwise allowable deductions must be modified. The modifications required to taxable income are specified in IRC §172(b)(2). This Code section mandates that a net operating loss be carried to the earliest year under subsection (b)(1) and describes the amount to be carried to other years as follows:

Net operating loss deduction – Modified taxable income = Net operating loss carryover

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 25 - 2015

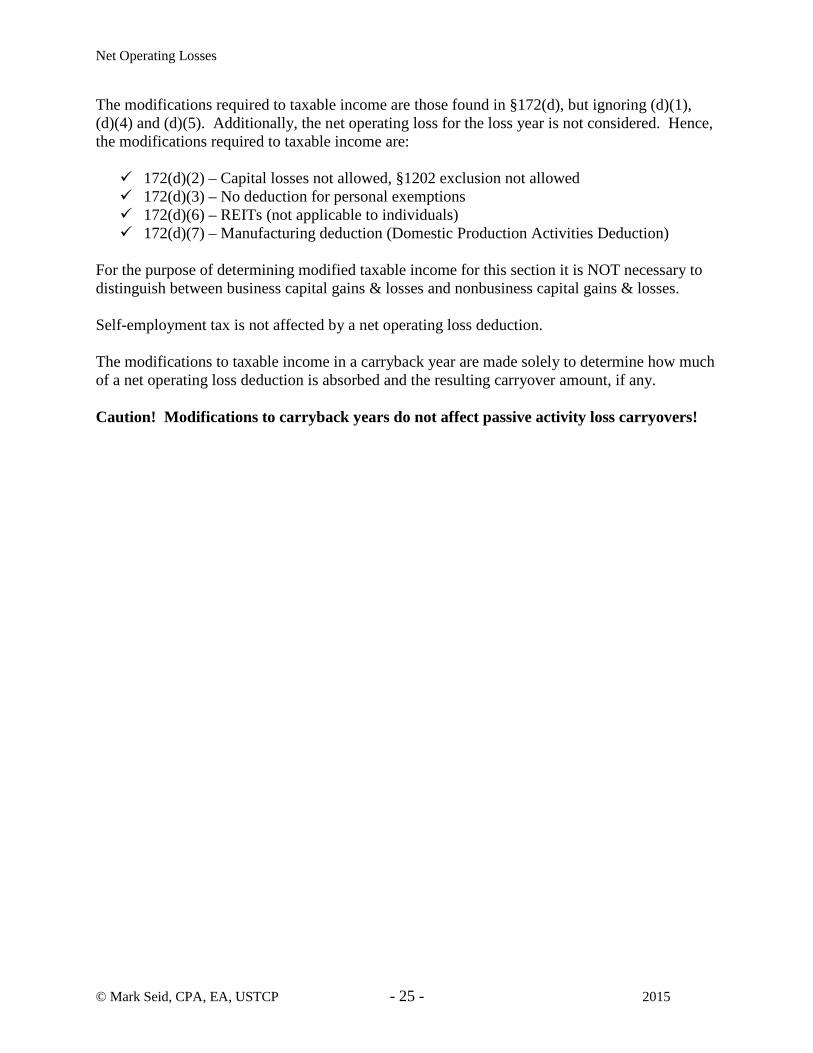

The modifications required to taxable income are those found in §172(d), but ignoring (d)(1), (d)(4) and (d)(5). Additionally, the net operating loss for the loss year is not considered. Hence, the modifications required to taxable income are: 172(d)(2) – Capital losses not allowed, §1202 exclusion not allowed 172(d)(3) – No deduction for personal exemptions 172(d)(6) – REITs (not applicable to individuals) 172(d)(7) – Manufacturing deduction (Domestic Production Activities Deduction)

For the purpose of determining modified taxable income for this section it is NOT necessary to distinguish between business capital gains & losses and nonbusiness capital gains & losses. Self-employment tax is not affected by a net operating loss deduction. The modifications to taxable income in a carryback year are made solely to determine how much of a net operating loss deduction is absorbed and the resulting carryover amount, if any. Caution! Modifications to carryback years do not affect passive activity loss carryovers!

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 26 - 2015

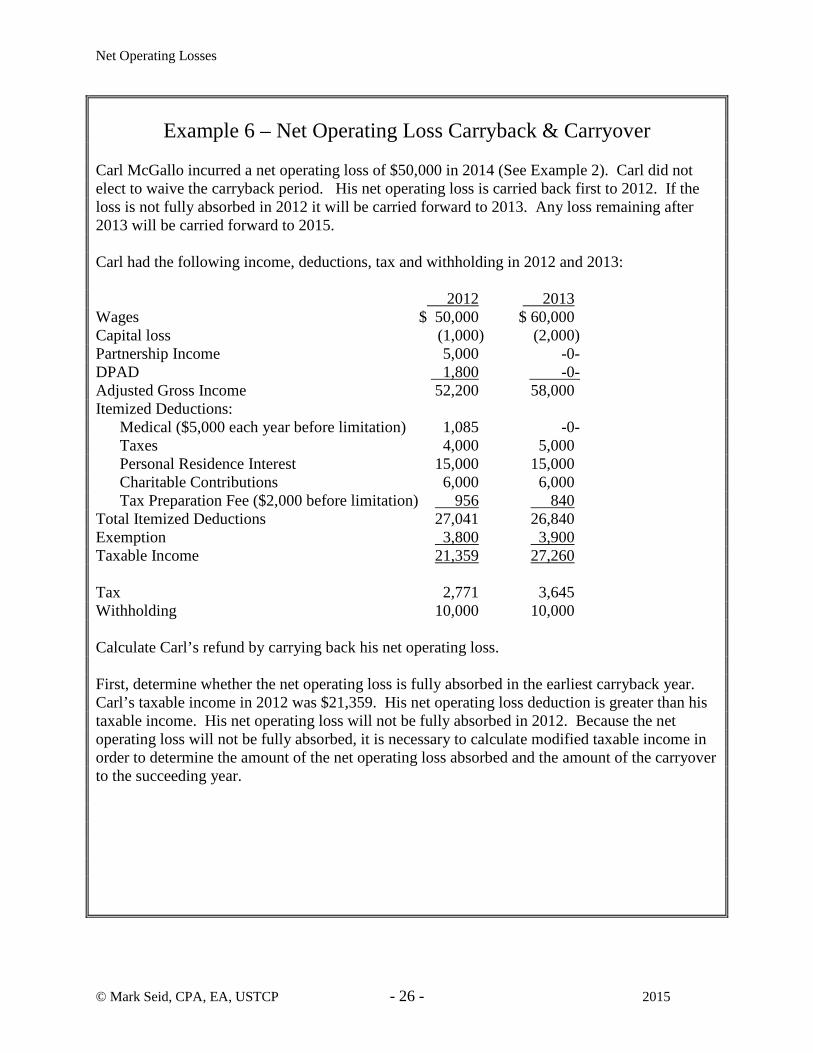

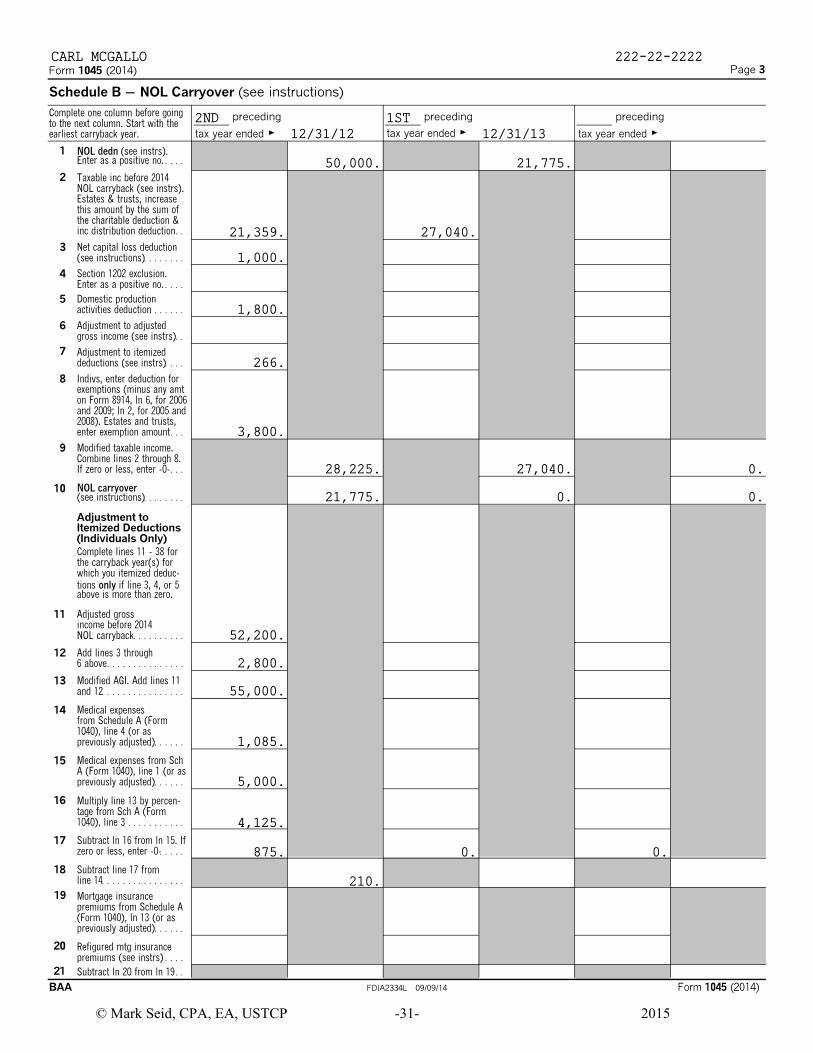

Example 6 – Net Operating Loss Carryback & Carryover

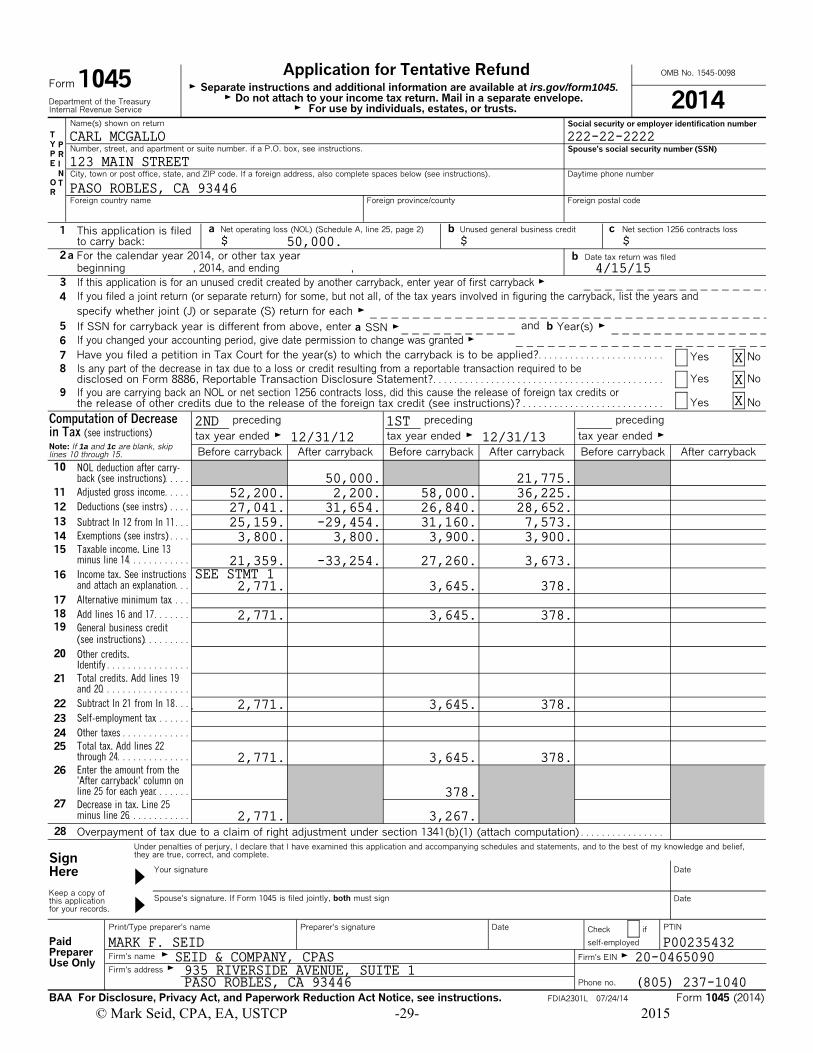

Carl McGallo incurred a net operating loss of $50,000 in 2014 (See Example 2). Carl did not elect to waive the carryback period. His net operating loss is carried back first to 2012. If the loss is not fully absorbed in 2012 it will be carried forward to 2013. Any loss remaining after 2013 will be carried forward to 2015. Carl had the following income, deductions, tax and withholding in 2012 and 2013: 2012 2013 Wages $ 50,000 $ 60,000 Capital loss (1,000) (2,000) Partnership Income 5,000 -0- DPAD 1,800 -0- Adjusted Gross Income 52,200 58,000 Itemized Deductions: Medical ($5,000 each year before limitation) 1,085 -0- Taxes 4,000 5,000 Personal Residence Interest 15,000 15,000 Charitable Contributions 6,000 6,000 Tax Preparation Fee ($2,000 before limitation) 956 840 Total Itemized Deductions 27,041 26,840 Exemption 3,800 3,900 Taxable Income 21,359 27,260 Tax 2,771 3,645 Withholding 10,000 10,000 Calculate Carl’s refund by carrying back his net operating loss. First, determine whether the net operating loss is fully absorbed in the earliest carryback year. Carl’s taxable income in 2012 was $21,359. His net operating loss deduction is greater than his taxable income. His net operating loss will not be fully absorbed in 2012. Because the net operating loss will not be fully absorbed, it is necessary to calculate modified taxable income in order to determine the amount of the net operating loss absorbed and the amount of the carryover to the succeeding year.

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 27 - 2015

Example 6 - Continued Second, if Carl has a net capital loss, a §1202 exclusion or a DPAD deduction, then recompute the 2012 adjusted gross income with the modifications required by IRC §172(b). Adjusted Gross Income $ 52,200 Capital loss 1,000 DPAD 1,800 Recomputed adjusted gross income 55,000 Refigure the itemized deductions using the recomputed adjusted gross income. Gross medical expenses $ 5,000 Limitation ($55,000 x 7.5%) (4,125) Refigured medical expenses (not less than $0) 875 Allowable medical expenses on original return 1,085 Refigured medical expenses (not less than $0) (875) Medical Expense Adjustment 210 Gross miscellaneous itemized deductions $ 2,000 Limitation ($55,000 X 2%) (1,100) Refigured miscellaneous itemized deductions 900 Allowable misc. deductions on original return 956 Refigured miscellaneous itemized deductions 900 Miscellaneous Deductions Adjustment 56 Calculate modified taxable income: 2012 taxable income before NOLD $ 21,359 Add capital loss 1,000 Add DPAD 1,800 Add itemized deduction adjustments 266 Add personal exemptions 3,800 Modified Taxable Income 28,225 Calculate NOLD carryover to succeeding year: Net operating loss deduction $ 50,000 Less Modified Taxable Income (28,225) NOLD carryover to 2013 21,775

Net Operating Losses

© Mark Seid, CPA, EA, USTCP - 28 - 2015

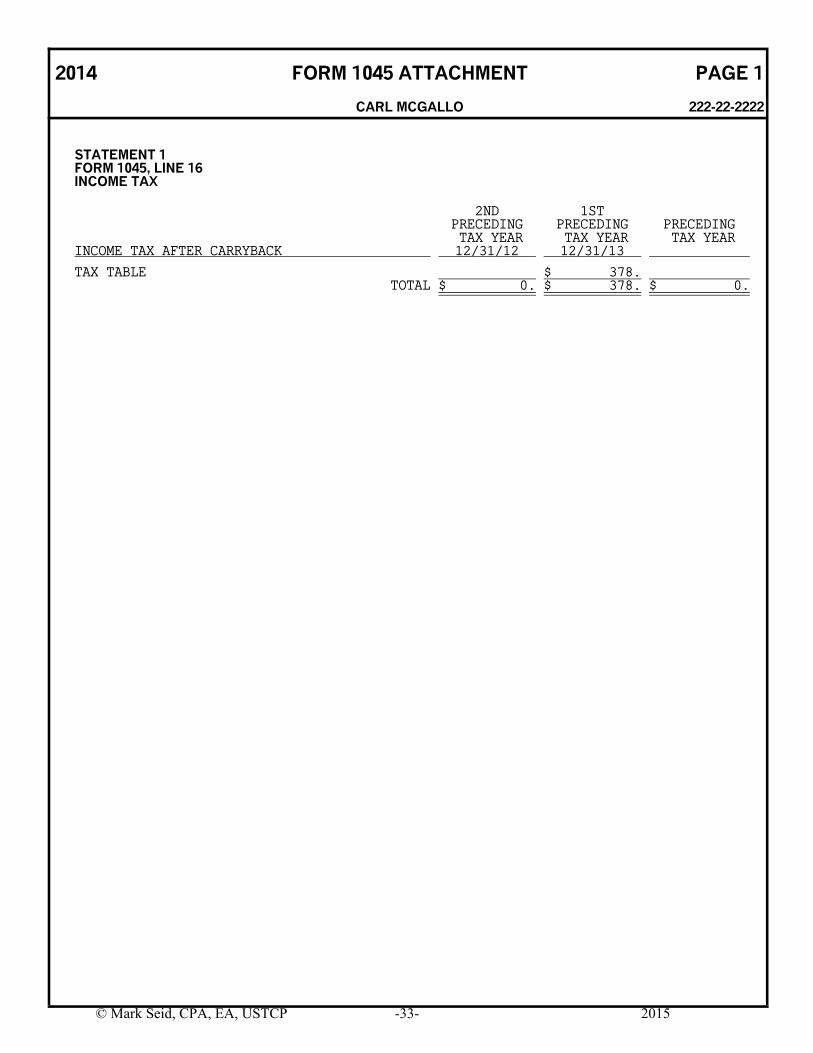

Example 6 – Continued Now that Carl’s net operating loss deduction carryover to 2013 has been calculated, repeat the first step – determine whether the net operating loss is fully absorbed. Carl’s taxable income in 2013 was $27,260. His 2013 taxable income is greater than the net operating loss deduction. The net operating loss deduction is fully absorbed in 2013. Because the net operating loss is fully absorbed in 2013 it will not be necessary to calculate modified taxable income. The net operating loss deduction will be subtracted from adjusted gross income, any items with limitations based upon AGI will be recalculated, and tax will be recomputed. 2013 Adjusted Gross Income $ 58,000 Net operating loss deduction carryover (21,775) 2013 AGI after NOLD 36,225 36,225 Itemized deductions: Medical [$5,000 – (36,225 X 10%)] 1,377 Taxes 5,000 Personal Residence Interest 15,000 Charitable Contributions 6,000 Miscellaneous [$2,000 – (36,225 X 2%) $ 1,275 Total Itemized Deductions 28,652 (28,652) Personal Exemption (3,900) 2013 Taxable income after NOLD $ 3,673 Tax calculation and refunds are shown on accompanying Form 1045, page 1.

Application for Tentative Refund OMB No. 1545-0098

Form 1045 G Separate instructions and additional information are available at irs.gov/form1045.G Do not attach to your income tax return. Mail in a separate envelope.Department of the Treasury 2014G For use by individuals, estates, or trusts.Internal Revenue Service

Name(s) shown on return Social security or employer identification number

TY P Number, street, and apartment or suite number. if a P.O. box, see instructions. Spouse's social security number (SSN)P RE I

N City, town or post office, state, and ZIP code. If a foreign address, also complete spaces below (see instructions). Daytime phone numberO TR

Foreign country name Foreign province/county Foreign postal code

Net operating loss (NOL) (Schedule A, line 25, page 2) Unused general business credit Net section 1256 contracts lossa b c1 This application is filed$ $ $to carry back:

2 a For the calendar year 2014, or other tax year Date tax return was filedbbeginning , 2014, and ending ,

3 If this application is for an unused credit created by another carryback, enter year of first carryback G

If you filed a joint return (or separate return) for some, but not all, of the tax years involved in figuring the carryback, list the years and4

specify whether joint (J) or separate (S) return for each G

and b5 If SSN for carryback year is different from above, enter Year(s) Ga SSN GIf you changed your accounting period, give date permission to change was granted G6

Have you filed a petition in Tax Court for the year(s) to which the carryback is to be applied?. . . . . . . . . . . . . . . . . . . . . . . . 7 Yes No8 Is any part of the decrease in tax due to a loss or credit resulting from a reportable transaction required to be

Yes Nodisclosed on Form 8886, Reportable Transaction Disclosure Statement?. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 If you are carrying back an NOL or net section 1256 contracts loss, did this cause the release of foreign tax credits orYes Nothe release of other credits due to the release of the foreign tax credit (see instructions)? . . . . . . . . . . . . . . . . . . . . . . . . . . .

Computation of Decrease preceding preceding precedingin Tax (see instructions) tax year ended G tax year ended G tax year ended GNote: If 1a and 1c are blank, skip

Before carryback After carryback Before carryback After carryback Before carryback After carrybacklines 10 through 15.

10 NOL deduction after carry-back (see instructions). . . . .

Adjusted gross income. . . . . 11

Deductions (see instrs). . . . . 12

13 Subtract ln 12 from ln 11. . .

Exemptions (see instrs) . . . . 14Taxable income. Line 1315minus line 14. . . . . . . . . . . .

Income tax. See instructions16and attach an explanation. . .

Alternative minimum tax. . . . 17

18 Add lines 16 and 17. . . . . . .

19 General business credit(see instructions). . . . . . . . .

20 Other credits.Identify . . . . . . . . . . . . . . . .

Total credits. Add lines 1921and 20. . . . . . . . . . . . . . . . .

Subtract ln 21 from ln 18. . . 22

Self-employment tax. . . . . . . 23

Other taxes . . . . . . . . . . . . . 24Total tax. Add lines 2225through 24. . . . . . . . . . . . . . Enter the amount from the26'After carryback' column online 25 for each year. . . . . . .

27 Decrease in tax. Line 25minus line 26. . . . . . . . . . . .

28 Overpayment of tax due to a claim of right adjustment under section 1341(b)(1) (attach computation) . . . . . . . . . . . . . . . .

Under penalties of perjury, I declare that I have examined this application and accompanying schedules and statements, and to the best of my knowledge and belief,they are true, correct, and complete.Sign

Your signature DateHere AKeep a copy of

Spouse's signature. If Form 1045 is filed jointly, both must sign Datethis applicationfor your records. A

Print/Type preparer's name Preparer's signature Date PTINCheck if

Paid self-employed

Preparer GFirm's name Firm's EIN GUse Only

Firm's address GPhone no.

FDIA2301L 07/24/14 Form 1045 (2014)BAA For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see instructions.

CARL MCGALLO 222-22-2222

123 MAIN STREET

PASO ROBLES, CA 93446

50,000.

4/15/15

X

X

X

2ND 1ST12/31/12 12/31/13

50,000. 21,775.52,200. 2,200. 58,000. 36,225.27,041. 31,654. 26,840. 28,652.25,159. -29,454. 31,160. 7,573.3,800. 3,800. 3,900. 3,900.

21,359. -33,254. 27,260. 3,673.

2,771. 3,645. 378.

2,771. 3,645. 378.

2,771. 3,645. 378.

2,771. 3,645. 378.

378.

2,771. 3,267.

P00235432SEID & COMPANY, CPAS 20-0465090935 RIVERSIDE AVENUE, SUITE 1PASO ROBLES, CA 93446 (805) 237-1040

MARK F. SEID

SEE STMT 1

© Mark Seid, CPA, EA, USTCP -29- 2015

Form 1045 (2014) Page 2

Schedule A ' NOL (see instructions)

1 Enter the amount from your 2014 Form 1040, line 41, or Form 1040NR, line 39. Estates and trusts, entertaxable income increased by the total of the charitable deduction, income distribution deduction, and

1exemption amount. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2Nonbusiness capital losses before limitation. Enter as a positive number . . . . . . 2

3 3Nonbusiness capital gains (without regard to any section 1202 exclusion). . . . . .

4 4If line 2 is more than line 3, enter the difference. Otherwise, enter -0-. . . . . . . . .

If line 3 is more than line 2, enter the difference.55Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6Nonbusiness deductions (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Nonbusiness income other than capital gains7(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8 8Add lines 5 and 7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 9If line 6 is more than line 8, enter the difference. Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If line 8 is more than line 6, enter the difference.10Otherwise, enter -0-. But do not enter more than

10line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11Business capital losses before limitation. Enter as a positive number. . . . . . . . . . 11

Business capital gains (without regard to any1212section 1202 exclusion). . . . . . . . . . . . . . . . . . . . . . . . . .

13 13Add lines 10 and 12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

14 14Subtract line 13 from line 11. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . .

15 15Add lines 4 and 14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

16 Enter the loss, if any, from line 16 of your 2014 Schedule D (Form 1040).(Estates and trusts, enter the loss, if any, from line 19, column (3), of ScheduleD (Form 1041).) Enter as a positive number. If you do not have a loss on thatline (and do not have a section 1202 exclusion), skip lines 16 through 21 and

16enter on line 22 the amount from line 15 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17 17Section 1202 exclusion. Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

18 18Subtract line 17 from line 16. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . .

Enter the loss, if any, from line 21 of your 2014 Schedule D (Form 1040).19(Estates and trusts, enter the loss, if any, from line 20 of Schedule D (Form

191041).) Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20 20If line 18 is more than line 19, enter the difference. Otherwise, enter -0-. . . . . . .

21 21If line 19 is more than line 18, enter the difference. Otherwise, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2222 Subtract line 20 from line 15. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

23 Domestic production activities deduction from your 2014 Form 1040, line 35, or Form 1040NR, line 34 (or23included on Form 1041, line 15a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

24 24NOL deduction for losses from other years. Enter as a positive number. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

25 NOL. Combine lines 1, 9, 17, and 21 through 24. If the result is less than zero, enter it here and on page 1,25line 1a. If the result is zero or more, you do not have an NOL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

BAA Form 1045 (2014)

FDIA2302L 07/24/14

CARL MCGALLO 222-22-2222

-85,500.7,000.

13,000.0.

6,000.19,000.

7,500.13,500.

5,500.

0.

0.

30,000.

-50,000.

© Mark Seid, CPA, EA, USTCP -30- 2015

Page 3Form 1045 (2014)

Schedule B ' NOL Carryover (see instructions)

Complete one column before going preceding preceding precedingto the next column. Start with the

tax year ended Gtax year ended G tax year ended Gearliest carryback year.

1 NOL dedn (see instrs).Enter as a positive no. . . . .

2 Taxable inc before 2014NOL carryback (see instrs).Estates & trusts, increasethis amount by the sum ofthe charitable deduction &inc distribution deduction. .

Net capital loss deduction3(see instructions). . . . . . . .

Section 1202 exclusion.4Enter as a positive no. . . . .

Domestic production5activities deduction. . . . . . .

Adjustment to adjusted6gross income (see instrs). .

7 Adjustment to itemizeddeductions (see instrs). . . .

Indivs, enter deduction for8exemptions (minus any amton Form 8914, ln 6, for 2006and 2009; ln 2, for 2005 and2008). Estates and trusts,enter exemption amount. . .

Modified taxable income.9Combine lines 2 through 8.If zero or less, enter -0-. . .

NOL carryover10(see instructions). . . . . . . .

Adjustment toItemized Deductions(Individuals Only)Complete lines 11 - 38 forthe carryback year(s) forwhich you itemized deduc-tions only if line 3, 4, or 5above is more than zero.

Adjusted gross11income before 2014NOL carryback. . . . . . . . . .

Add lines 3 through126 above. . . . . . . . . . . . . . .

Modified AGI. Add lines 1113and 12. . . . . . . . . . . . . . . .

Medical expenses14from Schedule A (Form1040), line 4 (or aspreviously adjusted). . . . . .

Medical expenses from Sch15A (Form 1040), line 1 (or aspreviously adjusted). . . . . .

16 Multiply line 13 by percen-tage from Sch A (Form1040), line 3. . . . . . . . . . . .

Subtract ln 16 from ln 15. If17zero or less, enter -0-. . . . .

Subtract line 17 from18line 14. . . . . . . . . . . . . . . .

19 Mortgage insurancepremiums from Schedule A(Form 1040), ln 13 (or aspreviously adjusted). . . . . .

20 Refigured mtg insurancepremiums (see instrs) . . . .

21 Subtract ln 20 from ln 19. .

FDIA2334L 09/09/14 Form 1045 (2014)BAA

CARL MCGALLO 222-22-2222

2ND 1ST12/31/12 12/31/13

50,000. 21,775.

21,359. 27,040.

1,000.

1,800.

266.

3,800.

28,225. 27,040. 0.

21,775. 0. 0.

52,200.

2,800.

55,000.

1,085.

5,000.

4,125.

875. 0. 0.

210.

© Mark Seid, CPA, EA, USTCP -31- 2015

Form 1045 (2014) Page 4

Schedule B ' NOL Carryover (Continued)Complete one column before going preceding preceding precedingto the next column. Start with the

G G Gtax year ended tax year ended tax year endedearliest carryback year.

22 Modified AGI from line 13on page 3 of the form. . . . .

Enter as a positive number23any NOL carryback from ayear before 2014 that wasdeducted to figure line 11on page 3 of the form. . . . .

24 Add lines 22 and 23. . . . . .

Charitable contributions25from Sch A (Form 1040),line 19 (line 18 for 2004 -2006), or Sch A (Form1040NR), line 5 (line 7 for2004 through 2010), or aspreviously adjusted . . . . . .

Refigured charitable26contributions (seeinstructions). . . . . . . . .

Subtract ln 26 from ln 25. . 27

28 Casualty and theft lossesfrom Form 4684, line 18(line 23 for 2008; line 21 for2009; line 20 for 2005, 2006and 2010) . . . . . . . . . . . . .