Municipal Borrowing – Bonds or Bank Loans. Recent Experiences from Hungary Charles Jókay, Ph.D....

23

Municipal Borrowing – Bonds or Bank Loans. Recent Experiences from Hungary Charles Jókay, Ph.D. Visiting Professor of Public Policy, CEU, and Executive Director, IGE Consulting Limited, Budapest

Transcript of Municipal Borrowing – Bonds or Bank Loans. Recent Experiences from Hungary Charles Jókay, Ph.D....

Municipal Borrowing – Bonds or Bank Loans. Recent Experiences

from Hungary

Charles Jókay, Ph.D.

Visiting Professor of Public Policy, CEU, and Executive Director, IGE Consulting

Limited, Budapest

Elsewhere in Europe….

Most OECD and Council of Europe member states allow municipalities and other sub-national levels (provinces, counties etc.) to borrow for capital investment purposes

Some allow borrowing for liquidity purposes, but these loans have to be paid back by the end of a budget year

The definition of a legitimate „capital investment” varies by country. Some are strict in connecting „organic tasks” to investment, others give a free hand to municipal and other sub-national levels to „invest” as they see fit

DEBT CONTROL MECHANISMS USED ELSEWHERE IN EUROPE

The Policy Tools: Restrictions on volume of borrowing and/or debt

service ratios Restrictions on municipal guarantees Restrictions on collateral Restrictions on the legal sources of repayment Restrictions on the purposes for which borrowing is

allowed Administrative/review approval by higher levels Individual borrowing ceilings/purposes determined

by higher levels Legitimate lending sources, currencies can also be

regulated

Regulation of municipal borrowing in Hungary

Securities Law (2001) Law on Financial

Institutions (2006) Finance Ministry Decree on

Bonds (under review) Hungarian Financial

Supervisory Authority regulations (public offerings only)

Law on Local Self-Government (1990)

Law on State Budget System

Other laws re. Accounting, records etc.

“Buy side” regulations

Budapest Stock Exchange listing standards

Basel II

Prudency regulations regarding mandatory and voluntary private pension funds, insurance companies, investment funds and other investment vehicles

EU accession, cross-border finance, representation offices

Combined Debt Service and Source of Repayment Formula: Example of Hungary

Municipalilties may borrow for any capital investment purpose approved by the Local Council (no MOF involvement)

No restriction on currency or type of bank

Only property categorized as „non-essential” for performing public services may be used as collateral (the City Hall, school, main square, museum etc., are „protected” and may not be mortgaged)

Only 70% of „non budget revenue” (called own-source revenue in Hu) may be used in any given year to cover debt service.

Debt is defined as: bank loans, vendor loans, leasing, bond issues, guarantees, promissory notes and other long term commitments of public funds such as PPP arrangements

Long-term municipal debt in Hungary: 2003-2006

Type Amount HUF Amount HUF Amount HUF Amount HUF

2003 2004 2005 2006 2006/2003 index

Budapest City 80 472 412 000 90 301 023 000 97 926 574 000 136 805 067 000 170,00%

Budapest districts 10 431 030 000 10 406 940 000 15 834 371 000 22 407 583 000 214,82%

Cities w/county status 38 316 728 000 45 839 634 000 64 852 520 000 103 067 902 000 268,99%

Cities 40 412 857 000 50 643 258 000 64 004 648 000 86 123 196 000 213,11%

Villages 26 866 885 000 31 070 857 000 36 558 914 000 48 754 088 000 181,47%

Total 196 499 912 000 228 261 715 000 279 177 027 000 397 157 836 000 202,12%

End of year HUF/€ 262 HUF/€ 245 HUF/€ 252 HUF/€ 252 HUF/€

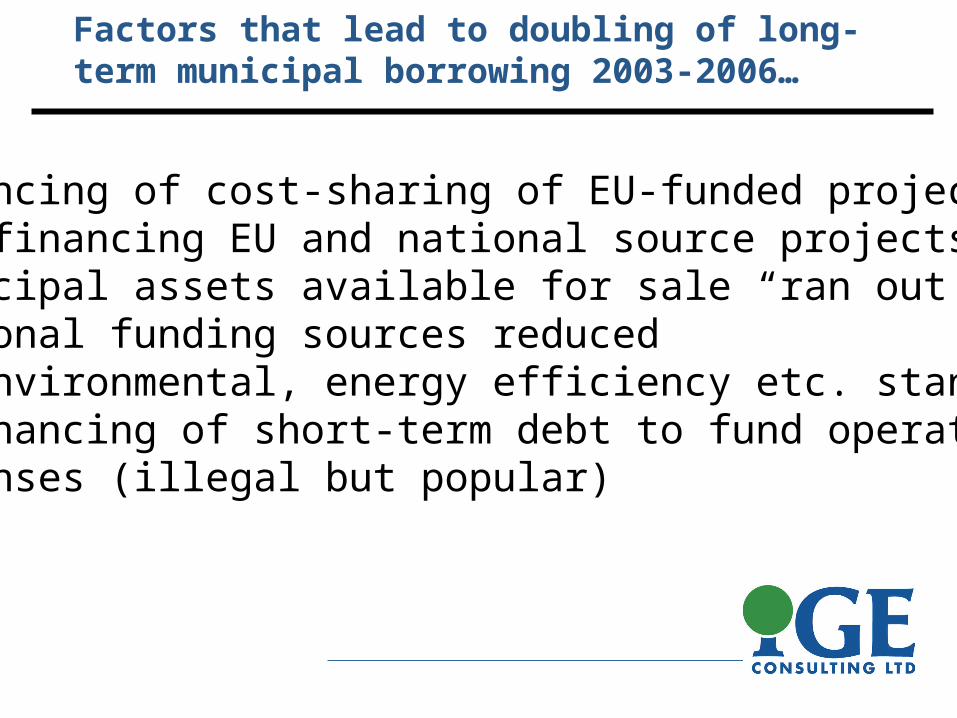

Factors that lead to doubling of long-term municipal borrowing 2003-2006…

•financing of cost-sharing of EU-funded projects•pre-financing EU and national source projects•municipal assets available for sale “ran out”•national funding sources reduced•EU environmental, energy efficiency etc. standards•Refinancing of short-term debt to fund operational expenses (illegal but popular)

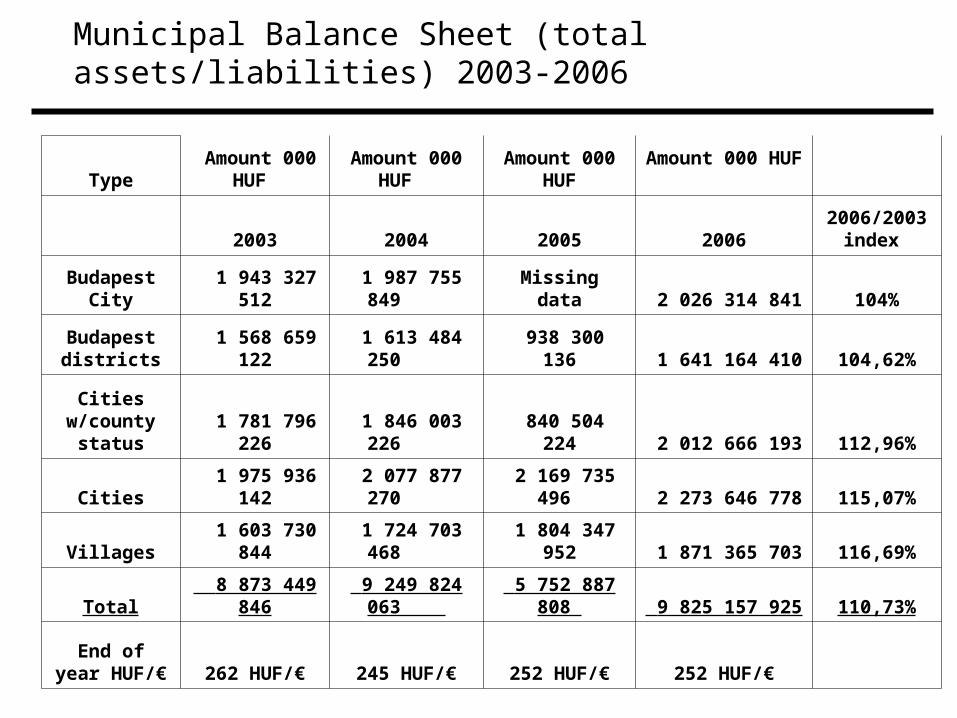

Municipal Balance Sheet (total assets/liabilities) 2003-2006

Type Amount 000

HUF Amount 000

HUF Amount 000

HUF Amount 000 HUF

2003 2004 2005 20062006/2003

index

Budapest City 1 943 327 512

1 987 755 849 Missing data 2 026 314 841 104%

Budapest districts 1 568 659 122

1 613 484 250 938 300 136 1 641 164 410 104,62%

Cities w/county

status 1 781 796 226 1 846 003 226

840 504 224 2 012 666 193 112,96%

Cities 1 975 936 142 2 077 877 270

2 169 735 496 2 273 646 778 115,07%

Villages 1 603 730 844 1 724 703 468

1 804 347 952 1 871 365 703 116,69%

Total 8 873 449 846 9 249 824 063

5 752 887 808 9 825 157 925 110,73%

End of year HUF/€ 262 HUF/€ 245 HUF/€ 252 HUF/€ 252 HUF/€

Municipal financial assets vs. Total debt (long term, short term, bank

loans and bonds issued) quarterly 2000 -2006 (thousand million HUF)

0

200

400

600

800

1 000

1 200

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2

2000 2001 2002 2003 2004 2005 2006

Pénzügyi eszközök

Kötelezettségek

Bank Loans made..stock figures, Financial Supervision data (2006-2007)

2006 End 9/2007 Change

€ % € %

businesses 22 000 000 000 41%24 000 000

000 39% 9,09%

households 16 800 000 000 31%20 000 000

000 33% 19,05%

municipalities 1 600 000 000 3% 1 648 000 000 3% 3,00%

other 13 448 000 000 25%15 080 000

000 25% 12,14%

Total Loans Made 53 848 000 000 100%61 000 000

000 100% 13,28%

Total Securities Held 9 940 000 000

14 950 000 000 50,40%

Total Bank Fin. Assets 63 788 000 000

75 950 000 000 19,07%

Minimal Exposure of Banking Sector....

Municipal Bank deposits and loans made to municipalties vs. Total deposits and total loans made to all sectors

2001 2002 2003 2004 2005 2006 2007.

June Municipal loans as a percentage of

total banking assets 0,08 1,12 1,12 1,22 1,37 1,66 1,68

Municipal Loans as a percentage of net loans made by banks

1,5 1,89 1,77 1,92 2,1 2,57 2,58

Municipal Deposits as percentage of all deposits

3,25 3,28 2,9 3,18 2,8 2,54 2,18

National Bank of Hungary, Financial Markets Supervision (András Vigvári’s calculations)

The shift towards bonds began in 2005 and continues

National Bank financial

accounts in €

Municipal Debt

Composition

Long term

bonds Long term loanstotal long

term debt% of LT in

bonds

end of 2003 22 800 000 730 000 000 752 800 000 3,03%

June, 2007 180 000

000 1 680 000 000 1 860 000 000 9,68%

author estimate Nov, 2007

260 000 000 2 000 000 000 2 260 000 000 11,50%

What caused the shift towards bonds?

longer maturities (15-20 years) longer grace periods (5 years!) “callable” bonds (at no cost) debt refinancing (active debt management) exemption from public procurement (EU Directive) debt limit measurement difficult to use in cash-

based accounting and budgeting system bonds in bank portfolios are liquid, do not have

reserve requirements

Municipality 2005 2006 2007*

Budapest XII. district 1.944

Budapest XXII. district 2.500

Cegléd 3.000

Debrecen 2.500 1.184

Edelény 300 300

Esztergom 700 1.000

Fejér County 700 1.600

Fonyód 900

Gárdony 1.100

Gödöllő 802

Gyöngyös 676

Gyömrő 445

Gyula 4 2.000

Hódmezővásárhely 10.862

Karcag 4.100

Kiskunfélegyháza 1.968

Marcali 1.000

Mohács 4.000

Ócsa 1.300

Oroszlány 150 150

Sopron 2.555

Somogy County 1.200

Székesfehérvár 1.345

Szerencs 1.000

Szolnok 8.700

Tolna 1.000

Total 3.657 22.119 34.713

Hindrances to public issues of bonds

•relatively small deal size

•banks (group members) buy entire issues and do not want to “securitize” their well-performing portfolios

•expense of disclosure, registration, advertising, market-making, stock market listing

•privately-placed bonds are essentially substitutes for bank loans

•Bank lending dominates corporate finance, few listed issues

Who are the key players?

Universal Banking services (accounts management) and lending dominated by:

OTP Bank and Raiffeisen Bank

Second tier: Erste, CIB (Intesa Gruppo), K & H (KBC Bank), Commerzbank, savings cooperatives, UniCredit

Rumors of Raiffeisen-Erste merger in Austria?

More key players…

Boutique players: NÖ Hypobank (cross-border), Dexia Kommunalkredit (portfolio, syndication)

Not active in municipal account management or lending: MKB (Bayerische Landesbank), Budapest Bank (GE

Moneybank), Citibank, Dresdner, Calyon, Oberbank, Sopron Bank, Deutsche Bank, Allianz Bank, BNP Paribas, ING Bank, Volksbank, WestLB etc.

Risks: Creditworthiness, default and debt adjustment

•very low default rate on municipal loans (few loans in higher risk category)

•Businesses are not „tough” on municipal clients

•Basel II treats municipal debt and debt of municipal companies favorably (statistics will soon show

exposure to corporatized municipal companies)

•-Act on Municipal Debt Adjustment (1996)

•PUCs („JKP”) were corporatized in 1991 and appear as commercial loans, i.e. are hidden

Lessons learned…

Municipalities are considered low risk despite slow and inaccurate information flow

Foreign currency lending now close to 40%

Competition is intense for accounts management and lending services

Lending has started to shift to private bond issues for reasons unrelated to cost

Accounts management and collateralized lending now not prerequisites (information monopoly)

Public procurement law distorts market

More...

Secondary regulations are critical

Banks prefer to retain municipal portfolios

Bond market developed 10 years after regulatory framework was in place

Non-bank financial institutions tend to ignore municipal lending market and do not buy municipal securities for their portfolios

If bonds are issued in great numbers for the wrong reason, regulators will overreact

Information Sources

National Bank of Hungary statistics:

http://english.mnb.hu

Hungarian Financial Markets Supervision:

http://english.pszaf.hu

Municipal bankruptcy case studies:

www.igeconsulting.com

EU Directives: 92/50/EEC listed financial services in Annex 1A; 2004/18/EC exempted bond issues and other securities from public procurement. Banking services, such as loans, are not exempt.

http://ec.europa.eu/internal_market/publicprocurement/legislation_en.htmstandard