Mudit Mittal Project Report

104

A SUMMER TRAINING PROJECT REPORT ON “Financial Analysis” AT DUSS LIMITED, MORADABAD IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR BBA DEGREE Submitted To, Submitted By. Mr. Syed Md. Faisal Ali khan Mudit Mittal Faculty Management BBA 5 th Sem. 1

-

Upload

sujeet-kumar -

Category

Documents

-

view

417 -

download

16

Transcript of Mudit Mittal Project Report

ASUMMER TRAINING PROJECT REPORT

ON

“Financial Analysis”

AT

DUSS LIMITED, MORADABAD

IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR BBA DEGREE

Submitted To,Submitted By.

Mr. Syed Md. Faisal Ali khanMudit Mittal

Faculty Management BBA 5th

Sem.

(2008-2011)

1

SARASWATI INSTITUTE OF MANAGEMENT &

TECHNOLOGY

Affiliated to Kumaun University, Nanital

12 Km on Rudrapur- Gadarpur Road, P.O. Prem Nagar via Gadarpur (U.S. Nagar) Uttarakhand

Website: www.simtrdr.org , E-mail: [email protected]

COLLEGE CERTIFICATE

2

COMPANY’S LETTER

3

STUDENT DECLARATION

This project has been undertaken as a partial fulfilment of the

requirements for the award of the Degree of Bachelor of Business

Administration from Kumaun University, Nanital.

This project was executed during the IVth semester under the

supervision of Mr. Syed Md. Faisal Ali Khan, Faculty Management

Department.

Further, I declare that this project is my original work and analysis

and findings are for academic purpose only. This project has not been

presented in any seminar or submitted elsewhere for the award of any

degree or diploma.

4

Supervisor Signature Student Signature

MR. SYED MD. FAISAL AlI KHAN MUDIT MITTAL

Dep’t of Management BBA IVth sem.

HOD Signature

Mrs. PUJA JHORI

ACKNOWLEDGEMENT

It is a matter of great pride to my summer training in the prestigious Dugdh

Utpadak Sahkari Sangh Limited (DUSS Ltd.) "PARAG" Dalpatpur, Distt.

Moradabad, under its Finance Department.

I have no word to express my gratitude towards General Manager Sri

Mr. PRASADI LAL, who allowed me to carry on my summer training at

"PARAG" Dalpatpur. There is a great sense of indebtness toward Finance In

charge Mr. SARVESH KUMAR SAXENA, Who has also

supervised my report and spared his valuable time for timely suggestion and

help.

My reverenced teacher, Director Dr. MOHD. ALI, S.G.I. whose

guidance is of great importance in the completion of this report.

I am thankful to Mrs. PUJA JHORI (H.O.D.), of Management

dep’t., for the help rendered by them time to time.

5

I also express my sincere thanks to Mr. SYED MD. FAISAL

ALI KHAN my Project Guide, who had make the concepts of Finance so

clear that the project had become very easy to understand and make.

My most sincere and greatest gratitude towards my parents who enabled

me with all their resources, love and guidance.

Last but not the least I want express my regards all the staff members of

Parag, my teachers and my friends who helped me in every possible manner to

present this treatise in this form.

Mudit Mittal

PREFACE

PREFACE

Indian economy has undergone a radical transformation in the last three

decades. The discoveries and inventions in various fields of life is perhaps

being the reasons for this transformation. The marketing strategy in India,

which has practiced in the olden days, has either changed or been refined so

as to adjust with the dynamic world. If we consider the early years of the

development of our economy. The report help us to understand the

followings:

(i) To know the Earning Capacity or Profitability.

(ii) To know the Solvency.

(iii) To know the Financial Strength.

(iv) To make comparative study with other firms.

6

(v) To know the capability of payment of interest and dividend.

(vi) To know the trend of the business.

(vii) To know the efficiency of management.

(viii) To provide useful information's to the Management.

7

8

Table of Contents

Title Page no.

College Certificate (2)

Company Letter (3)

Student Declaration (4)

Acknowledgement (5)

Preface (6)

Chapter No.

1. Introduction to topic 8

2. Introduction to company 9

3. Objective of study 26

4. Scope and Importance

5. Research Methodology 28

6. Data analysis 33

7. Findings and Analysis

8. Conclusion

9. Recommendations

10. Limitations

Bibliography …..

9

Annexure …..

INTRODUCTION TO TOPIC

My project is based on facts and survey conducted under the guidance of the

people of Moradabad Dugdh Utpadak Sahkari Sangh Limited, who had been

very helpful at all times.

10

INTRODUCTION TO COMPANY

Uttar Pradesh milk co-operatives are contributing immensely to the Indian dairy

industry, the highest milk producer in the world. The impact of Uttar Pradesh

milk co-operatives can be ascertained from their role in the private and co-

operative systems. With the launch of innovative technologies Uttar Pradesh is

now being able to enhance their milk production acutely. The merging of the

rural and the urban contribution to the dairy production in Uttar Pradesh forms

the Uttar Pradesh milk co-operative union. This induces rapid growth and

development in the dairy production. The Uttar Pradesh milk co-operatives are

significantly engaged in the production, procurement, processing and marketing

of milk. The Pradeshik Co-operative Dairy Federation in Lucknow facilitates

the marketing and distribution of milk in Uttar Pradesh.

Moradabad Sahkari Milk Board Ltd., Dalpatpur, was established in 1968

with the joint planning of INDIAN GOVERNMENT & UNICEF. The

“UNICEF” with assistance from freedom from hunger campaign committee for

the benefits of poor and malnourished population in India and it was a belief

that this dairy may serve as a living monument of international co-operation.

The main objective to set up the Moradabad Sahkari Milk Board is

collecting the milk from the villages. Through co-operative societies and

distribute pure, fresh milk and milk products after pasteurization in Moradabad

on fair prices. This was the planning of state govt. which is now successfully

running under the PRADESIK CO-OPERATIVE DAIRY FEDERATION.

11

The dairy was started in 1968. The capacity of plant at that time is 50,000

liter per day. The organization was manufacturing its product under brand

“PARAG” but due to some reason in June 1993 again this organization

started working under two schemes. This aid was given by NATIONAL

DAIRY DEVELOPMENT BOARD, NEW DELHI to PRADESHIK CO-

OPERATIVE DAIRY FEDERATION LTD.

In the year 1993 the name of organization changed and new name was

assigned MORADABAD DUGDH UTPADAK SAHKARI SANGH LTD.

(DUSS Ltd.) DALPATPUR, MORADABAD and the brand name of

product is “PARAG”.

Parag the brand name of Pradeshik Co-operative Dairy Federation

is given by the general public and accepted by Pradeshik Co-operative Dairy

Federation. It is a symbol of “PARAG” which is found in the flowers on pollen

grains.

Milk procurement by the Uttar Pradesh

Milk co-operativesIn 1999-2000 Uttar Pradesh procured milk of 7.19 Lakh kg Per Day to 7.09

Lakh kg Per Day. According to an authentic source it procured 15, 943 tonne

thousand milk in the year 2003-2004 as against 2.89 lakh tonnes in 2000-2001.

Estimates of Milk Production

State 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05 05-06 06-07 07-08 08-09

12

Uttar Pradesh 12934 13618 14152 13857 14648 15288 15943 16512 17356 18095 18861 19537

*Production in lakh liters.

CORPORATE PROFILE

It is the project of Indian government established in 23 state of India from the

name of “state dairy cooperative federation.” It is running is various 23 states in

India from the name of “state cooperative dairy federation” under the

supervision of central government running by state government dairy

cooperative all over country are allowing the small dairy farmers to take

initiative in moulding their own destiny. They serve more then 10 million

former in over 80,000 villages. Here is a list of dairy co-operatives in India state

wise.

STATE COOPERATIVE DAIRY FEDERATIONS

ANDAMAN & NICOBAR:

Andaman & Nicobar Island Integrated Development Corporation Ltd.

(ANIIDCO),

Port Blair - 744101.

ANDHRA PRADESH:

Andhra Pradesh Dairy Development Cooperative Federation Ltd.

Lalapet, Hyderabad - 500017

13

Brand name: Vijaya.

BIHAR

Bihar State Cooperative Milk Producers’ Federation Ltd.

Dairy Development Complex, PO Bihar Veterinary College, Patna - 800014

Brand Name: Sudha.

GOA:

Goa State Cooperative Milk Producers’ Union Ltd.

Curti, Ponda - 403401, Goa

Brand Name: Goadairy.

GUJARAT:

Gujarat Cooperative Milk Marketing Federation Ltd. (GCMMF)

Amul Dairy Rd, Anand - 388001

Brand Names: Amul, Sagar.

HARYANA:

Haryana Dairy Development Cooperative Federation Ltd.

SCO No 127-128, Sector 17-C, Chandigarh - 160017

Brand Name: Vita.

HIMACHAL PRADESH:

Himachal Pradesh State Cooperative Milk Producers’ Federation Ltd.

Totu, shimla – 171011

JAMMU & KASHMIR:

Jammu Cooperative Milk Producers’ Federation Ltd. (JCMPF)

14

Jammu cantt - 180003

Brand name: Jamfed .

Kashmir Valley Milk Producers’ Cooperative Federation Ltd.

Srinagar - 19001

KARNATAKA:

Karnataka Cooperative Milk Producers’ federation Ltd.

Bangalore - 560029

Brand name: Nandini.

KERALA:

Kerala Cooperative Milk marketing federation Ltd.

Thiruvananthapuram - 695004

Brand Name: Milma .

MADHYA PRADESH:

Madhya Pradesh State Cooperative Dairy federation Ltd.

Bhopal - 462011

Brand Name: Sanchi, Shakti, Sneha.

MAHARASTRA:

Maharashtra Rajya Sahkari Dugdh Mahasangh Maryadit

Mumbai - 400020

Brand Name: Mahanan.

15

MANIPUR:

Manipur State Cooperation Milk Processing & Marketing federation Ltd.

Imphal – 795001

NAGALAND:

Kohima Dist Cooperative Milk Producers Union Ltd.

Dimapur - 797112

Brand Name: Kevi.

ORISSA:

Orissa state cooperative milk producers’ federation Ltd.

Bhubaneswar - 751007

Brand Name: Omfed.

PONDICHERRY:

Pondicherry Cooperative Milk Producers Union Ltd.

Pondicherry - 605009

Brand Name: Ponlait.

PUNJAB:

Punjab State Cooperative Milk Producers’ federation Ltd.

Chandigarh - 160022

Brand Name: Verka.

16

RAJASTHAN:

Rajasthan Cooperative Dairy federation Ltd.

Jaipur 302017

Brand Nam: Saras .

SIKKIM:

Sikkim Cooperative Milk Producers Union Ltd.

Gangtok - 737102

Brand Name: Sikkimilk.

TAMIL NADU:

Tamil Nadu Cooperative Milk Producers Federation Ltd.

Chennai - 600051

Brand Name: Aavin.

TRIPURA:

Tripura Cooperative Milk Producers Union Ltd.

Agartala - 799006

Brand Name: Gomati.

UTTAR PRADESH:

Pradeshik Cooperative Dairy Federation Ltd.

Lucknow - 226001

Brand Name: Parag.

17

WEST BENGAL:

West Bengal Cooperative Milk Producers Federation Ltd.

Calcutta - 700091

Brand Name: Benmilk.

PROFILE OF PARAG U.P.

Established in 3/Jan/1967 Pradesh Corporative Dairy Federation Ltd. (Parag) is

the largest FMCG and manufacture enterprise of its kind in India today. The

company is engaged in manufacture of wide variety of milk products and

FMCG product, transmission and utilization of milk food product.

Placed among the top 4 manufacture of milk product & milk, PARAG provides

products, services for milk products, Ghee, Butter, Milk, Power, Ice Cream etc.

In each of these sectors, PARAG offer total service to its customers on turnkey

basis.

The first plant of PARAG was set up in Lucknow, which signalled the dawn the

milk food industry in India. It has 26 major plant were set up in U.P. &

Uttarakhand.

PARAG business broadly covers conversions, transmission, utilization and

conservation of food products in core sectors of economy that fulfil vital

infrastructure needs of the country. Its products have established and enviable

reputation of high quality and reliability, which is largely due to emphasis

placed all along on contemporary companies. Parag has consistently upgraded

its design and manufacturing facilities to National standards acquiring and

assimilating some of the best technologies of the India from the leading

companies in all over India from its own R & D Centres.

18

Headquarters at Lucknow, the company now has 26 manufacture divisions,

more than 100 service centres and 4 regional centres besides project sites spread

all over India and effective service to customers in India. PARAG has more

than 30,000 employees comprising trained engineers, technicians & skilled

artisans supporting technical staff and management staff. The company

registered a turnover of Rs.100000 cr during the year 2006-2007.

MANUFACTURING UNITS OF PARAG

PRADESHIK CO-OPERATION DAIRY

FEDERATION LTD.

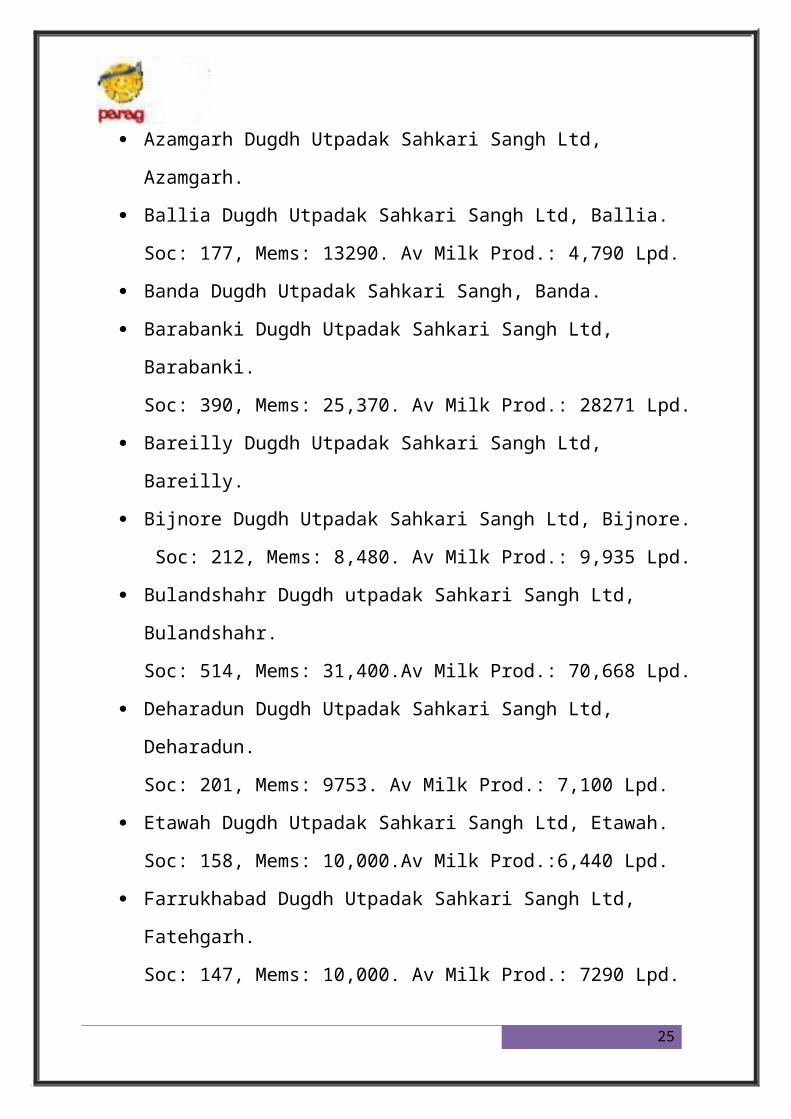

Agra Dugdh Utpadak Sahkari Sangh Ltd., Agra.

Allahabad Dugdh Utpadak Sahkari Sangh Ltd, Allahabad.

Soc: 360, Mems: 20,000. Av Milk Prod.: 30,000 Lpd.

Almora Dugdh Utpadak Sahkari Sangh Ltd. Almora.

Soc: 151, Mems: 7020. Av Milk Prod.: 4,5 61 Lpd.

Azamgarh Dugdh Utpadak Sahkari Sangh Ltd, Azamgarh.

Ballia Dugdh Utpadak Sahkari Sangh Ltd, Ballia.

Soc: 177, Mems: 13290. Av Milk Prod.: 4,790 Lpd.

Banda Dugdh Utpadak Sahkari Sangh, Banda.

Barabanki Dugdh Utpadak Sahkari Sangh Ltd, Barabanki.

Soc: 390, Mems: 25,370. Av Milk Prod.: 28271 Lpd.

Bareilly Dugdh Utpadak Sahkari Sangh Ltd, Bareilly.

Bijnore Dugdh Utpadak Sahkari Sangh Ltd, Bijnore.

Soc: 212, Mems: 8,480. Av Milk Prod.: 9,935 Lpd.

Bulandshahr Dugdh utpadak Sahkari Sangh Ltd, Bulandshahr.

Soc: 514, Mems: 31,400.Av Milk Prod.: 70,668 Lpd.

19

Deharadun Dugdh Utpadak Sahkari Sangh Ltd, Deharadun.

Soc: 201, Mems: 9753. Av Milk Prod.: 7,100 Lpd.

Etawah Dugdh Utpadak Sahkari Sangh Ltd, Etawah.

Soc: 158, Mems: 10,000.Av Milk Prod.:6,440 Lpd.

Farrukhabad Dugdh Utpadak Sahkari Sangh Ltd, Fatehgarh.

Soc: 147, Mems: 10,000. Av Milk Prod.: 7290 Lpd.

Fatehpur Dugdh Utpadak Sahkari Sangh Ltd, Fatehpur.

Soc: 304, Mems: 18,000.Av Milk Prod.: 24,000 Lpd.

Firozabad Dugdh Utpadak Sahkari Sangh Ltd, Sheikhabad.

Gangol Sahkari Dugdh Utpadak Sangh Ltd, Meerut.

Soc: 449, Mems: 27,971.Av Milk Prod.: 48,066lpd.

Ghaziabad Dugdh Utpadak Sahkari Sangh Ltd, Hapur.

Ghazipur Dugdh Utpadak Sahkari Sangh Ltd, Ghazipur.

Gonda Dugdh Utpadak Sahkari Sangh Ltd, Gonda.

Soc: 146, Mems: 5,451.Av Milk Prod.: 4,100 Lpd.

Gorakhpur Dugdh Utpadak Sahkari Sangh Ltd, Gorakhpur.

Soc: 211, Mems: 12975.Av Milk Prod.: 4,331 Lpd.

Hamirpur Dugdh Utpadak Sahkari Sangh Ltd. Hamirpur.

Hardoi Dugdh Utpadak Sahkari Sangh Ltd, Hardoi.

Av Milk Prod.: 17,000.Lpd.

Jalaun Dugdh Utpadak Sahkari Sangh Ltd, Hardoi.

Av Milk Prod.: 11,381 Lpd.

Jaunpur Dugdh Utpadak Sahkari Sangh Ltd, Jaunpur.

Soc: 102, Mems: 4,700. Av Milk Prod.: 2,700 Lpd.

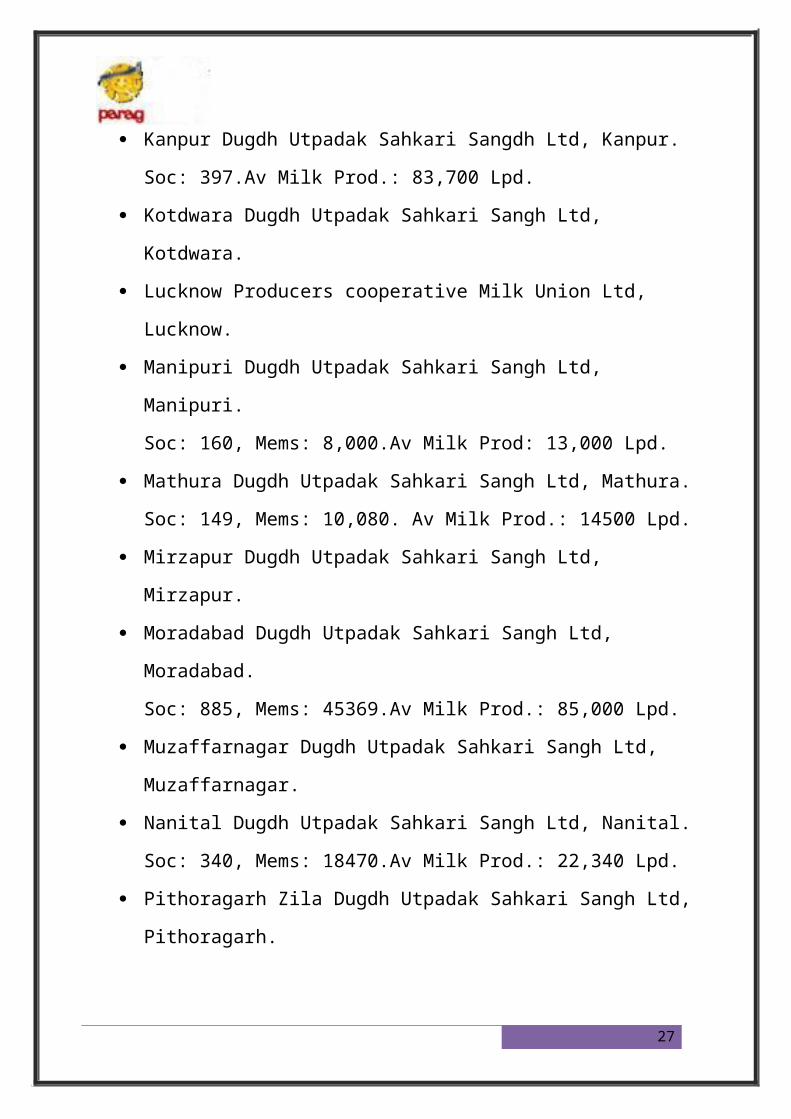

Kanpur Dugdh Utpadak Sahkari Sangdh Ltd, Kanpur.

Soc: 397.Av Milk Prod.: 83,700 Lpd.

Kotdwara Dugdh Utpadak Sahkari Sangh Ltd, Kotdwara.

Lucknow Producers cooperative Milk Union Ltd, Lucknow.

20

Manipuri Dugdh Utpadak Sahkari Sangh Ltd, Manipuri.

Soc: 160, Mems: 8,000.Av Milk Prod: 13,000 Lpd.

Mathura Dugdh Utpadak Sahkari Sangh Ltd, Mathura.

Soc: 149, Mems: 10,080. Av Milk Prod.: 14500 Lpd.

Mirzapur Dugdh Utpadak Sahkari Sangh Ltd, Mirzapur.

Moradabad Dugdh Utpadak Sahkari Sangh Ltd, Moradabad.

Soc: 885, Mems: 45369.Av Milk Prod.: 85,000 Lpd.

Muzaffarnagar Dugdh Utpadak Sahkari Sangh Ltd, Muzaffarnagar.

Nanital Dugdh Utpadak Sahkari Sangh Ltd, Nanital.

Soc: 340, Mems: 18470.Av Milk Prod.: 22,340 Lpd.

Pithoragarh Zila Dugdh Utpadak Sahkari Sangh Ltd, Pithoragarh.

Rae Bareilly Dugdh Utpadak Sahkari Sangh Ltd, Rae Bareilly.

Soc: 126, Mems: 12,970.Av Milk Prod.: 5,930 Lpd.

Saharanpur Dugdh Utpadak Sahkari Sangh Ltd, Saharanpur.

Soc: 213, Mems: 11,310.Av Milk Prod.: 12,370 Lpd.

Shahjahanpur Dugdh Utpadak Sahkari Sangh Ltd, Shahjahanpur.

Soc: 104, Mems: 4,715. Av Milk Prod.: 3,255 Lpd.

Sitapur Dugdh Utpadak Sahkari Sangh Ltd, Sitapur.

Soc: 130, Mems: 6,490.Av Milk Prod.: 12,456 Lpd.

Sultanpur Dugdh Utpadak Sahkari Sangh Ltd, Sitapur.

Soc: 292, Mems: 14,720. Av Milk Prod.: 12,456 Lpd.

Uttar Kashi Dugdh Utpadak Sahkari Sangh, Uttar Kashi.

Varanasi Dugdh Utpadak Sahkari Sangh Ltd, Varanasi.

Soc: 248, Mems: 11,495.Av Milk Prod.: 16,657 Lpd.

21

GROWTH AND DEVELOPMENT OF

THE ORGANISATION

MORADABAD DUDGH SAHKARI SANGH LTD. Was started in Nov. 1968

with the capacity of 150000 lit. Per day.

This aid was given by NATIONAL DAIRY DEVELOPMENT BOARD,

NEW DELHI to PRADESIK CO-OPERATIVE DAIRY DEDERATION LTD.

LUCKNOW in year 1983 organization starts selling of milk in Polly pack. At

that time it was the only organization who sale the milk in Polly pack in

Moradabad Mahanager.

The table represents the growth rate of milk from the beginning of this

organization in Polly pack.

Sales Report of Liquid Milk

Year Sale/Lit. Day Decline/Increase

in%

1999-2000 16359 -------------

2000-2001 18838 15.153%

22

2001-2002 17038 9.55%

2002-2003 15479 9.15%

2003-2004 12109 21.77%

2004-2005 11040 8.8%

2005-2006 12700 13.70%

2006-2007 11005 13.34%

2007-2008 10959 .41%

2008-2009 11162 1.85%

Above sales report presents fluctuation in the sale of Parag polypack milk. With

the compare of 1997-98, in 2007-08 the sale of Parag has been declined

31.76%g downward due to coming of similar other companies in similar field.

Present sale is concentrated on 9-10 thousand lit. /Day.

Moradabad Dugdh Sangh has increased the capacity of its doing from 50,000 to

1,50,000 Liters. The efficiency of Akbarpur chilling center has been accelerated

from 10,000 liter to 90,000 liter per day another chilling plant has been

established at Bijnor.

During 1992-93 the organization faced a loose of Rs. 3.31 Crores while in

93-94 organization earned a profit of Rs. 6.60 lakhs with all dedication & hard

work of management and employees of organization and in 1994-95

organization earned a profit of Rs. 888.94 Lakhs, the company reaped a profit of

Rs. 2 crore approximately in Year2003-2004.

23

SOCIETY AND THEIR PROCUREMENT

REPORT

Society and their Procurement Report

Year No. of Society No. of member Procurement of

Milk(Liters/Day)

2000-01 727 49390 46737

01-02 684 43652 46552

02-03 707 40956 67049

03-04 749 41214 71617

04-05 859 44470 67385

05-06 1054 4889 102060

06-07 1008 48975 65074

07-08 871 43199 70652

08-09 645 42675 40817

24

At present the company is making all possible effort for increasing the sale of

liquid milk and milk products. About 1 milk bar is operating in Moradabad

Mahanager and a large no. of agents involved in selling of milk and product.

There are more than 200 commission agents of milk and milk product in

Moradabad Mahanager. At present Moradabad Dugdh Sahkari Sangh Ltd. Deals

in so many milk products as Pasteurized Standardised Milk, Double toned milk,

Sterilized flavour milk, Simple Mattha, Salted Mattha, Milk cake, Parag kheer,

pure ghee etc.

Over all Parag is the market leader due to their quality, Brand image,

operating efficiency and approachability from last thirty years.

PRESENT STATUS OF THE

ORGANISATION

Moradabad Mahanagar Parag is the market leader in Polypack milk. Before two

year percentage sale of Parag Polypack milk is near about 90% but due to

coming of similar other companies their percentage came down by 26.6%. Now

total percentage of consumption of milk in Moradabad is near about 56% in

poly pack industry. At present Parag milk board sale is concentrates nine

thousand liters/day.

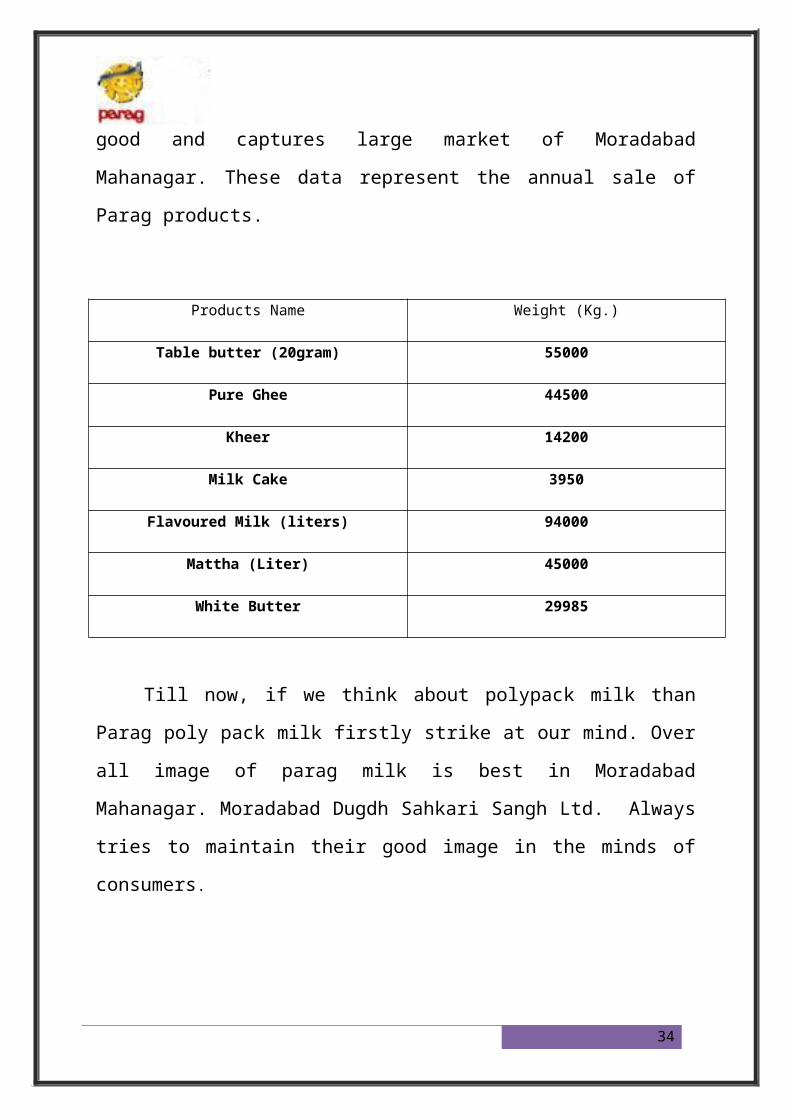

Over all Parag polypack milk is the market leader. The sale of their other

products is also very good and captures large market of Moradabad Mahanagar.

These data represent the annual sale of Parag products.

Products Name Weight (Kg.)

Table butter (20gram) 55000

25

Pure Ghee 44500

Kheer 14200

Milk Cake 3950

Flavoured Milk (liters) 94000

Mattha (Liter) 45000

White Butter 29985

Till now, if we think about polypack milk than Parag poly pack milk

firstly strike at our mind. Over all image of parag milk is best in Moradabad

Mahanagar. Moradabad Dugdh Sahkari Sangh Ltd. Always tries to maintain

their good image in the minds of consumers.

PRODUCT PROFILE

26

27

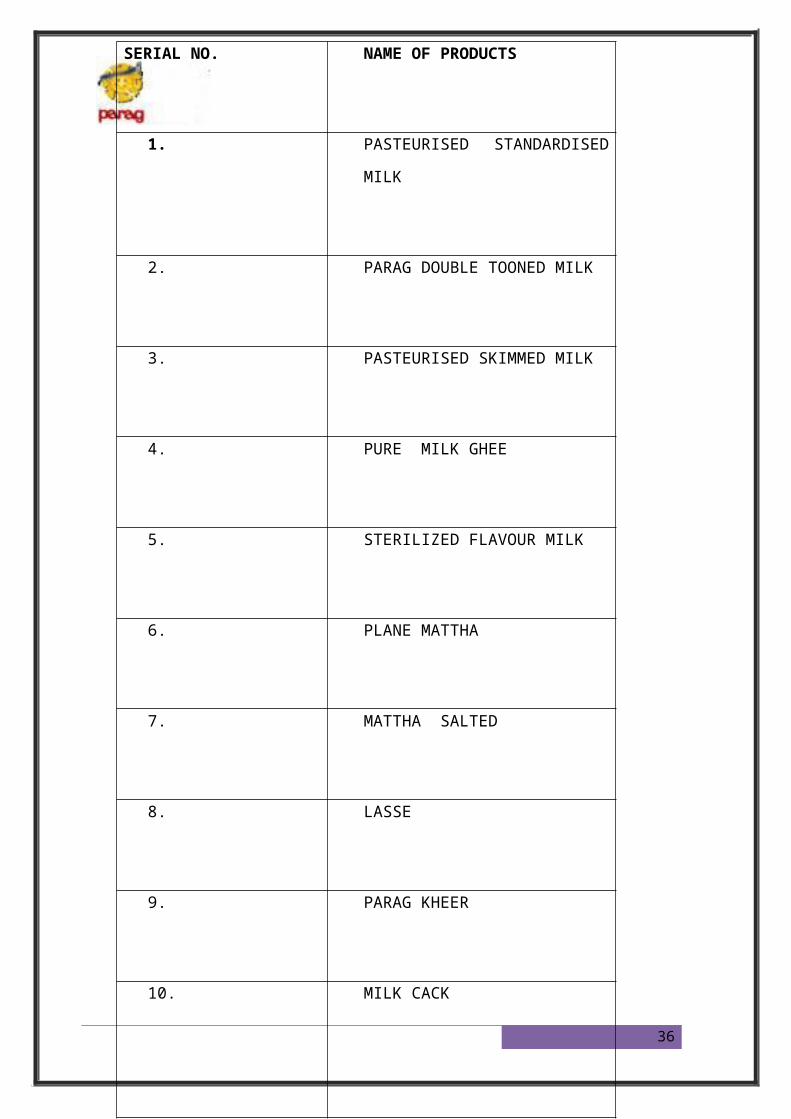

SERIAL NO. NAME OF PRODUCTS

1. PASTEURISED STANDARDISED

MILK

2. PARAG DOUBLE TOONED MILK

3. PASTEURISED SKIMMED MILK

4. PURE MILK GHEE

5. STERILIZED FLAVOUR MILK

6. PLANE MATTHA

7. MATTHA SALTED

8. LASSE

9. PARAG KHEER

10. MILK CACK

OBJECTIVES

PARAG’S VISION

VISION OF PARAG (DALPATPUR) MORADABAD:

Word class, innovative, competitive, cost effective & Profitable productive

enterprise committed to quality, learning, growth, stake-holders and customer

enrichment

CORPORATE VISION:

Total Business Solutions.

World class, Innovative,

Competitive &Profitable

Hygienic food products providing

COMPANY’S BUSINESS MISSION

BUSINESS MISSION:

To maintain a leading position as suppliers of quality products, and services in

the field of conversion of milk, for application in the areas of food products.

Utilize company’s capabilities and resources to expand business into allied

areas and other priority sectors of the economy.

BUSINESS OBJECTIVES:

1. GROWTH:-

28

To ensure a steady growth by enhancing the competitive edge of PARAG in

existing business, new areas and India leading operations so as to fulfil national

expectation from PARAG.

2. PROFITABILITY:-

To provide a reasonable and adequate return on capital employed, primarily

through improvements in operational efficiency, capacity utilization and

productivity and generate adequate internal resources to finance the company

growth.

3. CUSTOMER FOCUS:-

To build a high degree of customer confidence by providing increased value for

his money through international standards of product quality, performance and

superior service.

4. PEOPLE ORIENTATION:-

To enable each employee to archive his potential, improve his capabilities,

perceive his role and responsibilities and participate and contribute positively to

the growth and success of the company. To invest in human resources

continuously and alive to their needs.

5. IMAGE:-

To fulfil the expectation which stake holders like Government as owner,

employee, customer and the country at large have from PARAG.

29

RESEARCH

METHODOLO

GY

RESEARCH METHODOLOGY30

After recession with my locality member. I choose the project of working

capital management. I discussed the project with my instructor and coordinator

Mr. Sarvesh Kumar, account of books & budget section at PARAG Moradabad.

He approved the project. After that a simple course of action has been

followed for working on this project. That entire information and data were

gathered from the respective annual report of PARAG, Moradabad. All the

figures are taken from their balance sheet, profit & loss account of the

respective years and the other internal documents, which were personally shown

by the members of company in our interest.

A great help was provided by our instructor Sarvesh Kumar in

understanding the facts and figures Mr. Sarvesh Kumar it possible to us to ask

our quarry from that person who can answer it best than anybody else in the

company. Although it has been a difficult task but the availability of proper data

and timely guidance give by Mr. Sarvesh Kumar and my efforts made it a little

simpler of completed this project.

The study is based on Exploratory research and then the descriptive research.

31

SWOT ANALYSIS

Every organization is a part of an industry. All most all the organization faces

competition either directly or indirectly. Thus the industry and competition are

vital considerations in making of strategic choice.

Business firms undertake S.W.O.T. analysis to understand the central and

internal environment. S.W.O.T. analysis stands for strength, weakness,

opportunity and threats. It is also known as WOTS- UP analysis. With the help

of S.W.O.T.

Analysis the strength and existing within an organization can be matched with

the opportunities and threats operating in the environment so that an effective

strategy is one that capitalizes on the opportunities through the use of strength

and neutralizes the threats by minimizing the impact of weaknesses.

S.W.O.T. analysis involves matching of internal capabilities with the

environmental opportunity and threats matching strengths and weakness with

opportunities and threats requires that a firm should direct its strength towards

and threats requires that a firm should direct its strength towards exploiting

opportunities and blacking threats white minimizing exposure of its weakness at

the same time. S.W.O.T. analysis of PARAG is as:

STRENGTHS (S):

1. The company has a strong image and strong brand image.

2. PARAG has excellent distribution network.

3. The company has a competent sale force.

4. It has a long experience.

32

5. The company has a strong market reputation.

6. The visibility of Parag in Moradabad polypack market is very high as

compare to the other brand.

7. Parag Sangh is a Semi-Government Sector.

WEAKNESSES (W):

1. Inability to provide project financing.

2. The promotional budget of the PARAG is less than their competitors.

3. Rate of PARAG polypack is higher than their competitors.

4. The company is somewhat over confident.

OPPORTUNITITIES (O):

1. High expected growth in food sector.

2. The polypack market is growing at a steady phase of 5 to 7%.

3. The total market of polypack milk is near about 15000 liters per day.

4. Opportunity to promote by using various sales promotion methods.

THREATS (T):

1. The threat to the PARAG Company is by the entry of competitors.

Namely by Gopalji, Amul, Nandan, Mother dairy.

2. Their promotional budget is very low in comparison to their other budget.

3. Total percentage of loose milk is near about 80-83% in Moradabad

Mahanagar.

4. The market there of Parag polypack milk is declined by 25%.

33

NATURE AND SCOPE OF STUDY

The basic purpose of Financial Analysis of Parag milk factory and Comparison

with two year Balance Sheet in Parag milk factory and Maintain equitable

wages and salary structure. Wages and Salary Administration refers to the

establishment and implementation of sound policies and practices of employee

compensation. It includes such areas as job evaluation survey of wages and

salary analysis or relevant organization problem development and maintenance

of wage structure, establishing rules for administrating wages, wages payment,

incentives, profit changing and adjustment, supplementary payments, control on

compensation costs and other related items.

The wages and salary administration is concerned with the financial aspect

needs, motivation of needs, motivation and rewards of the organization, analysis

and interpret the needs of their employee so that rewards can be individually

designed to satisfy these needs.

FINANCIAL ANALYSIS34

Meaning of Financial Analysis is to classify the data in simple form given in

financial statements and to compare with each other to find out the strong points

and weakness of the business and to take decisions for future. For instance, if all

items relating to current assets are placed in one group while all items relating

to current liabilities are placed in another group, the comparison between the

two groups will provide useful information. Actually the figures given in

financial statements do not speak anything themselves. The analysis of these

figures helps the interested reader by giving tongue to these mute heaps of

figures.

In the words of Finney and Miller:

“Financial analysis consists in separating facts according to some definite

plan, arranging them in groups according to certain circumstances and then

presenting them in a convenient and easily read and understandable form.”

In the words of John N. Myres:

“Financial statement analysis is largely a study of relationships among the

various financial factors in a business, as disclosed by a single set of statements

and a study of the trends of these factors as shown in a series of statements.”

OBJECTS OR PURPOSE OF FINANCIAL ANALYSIS

35

The purpose of financial analysis depends on the needs of the person who is

analyzing these statements. These varying needs may be :—

(i) To know the Earning Capacity or Profitability.

(ii) To know the Solvency.

(iii) To know the Financial Strength.

(iv) To make comparative study with other firms.

(v) To know the capability of payment of interest and dividend.

(vi) To know the trend of the business.

(vii) To know the efficiency of management.

(viii) To provide useful information's to the Management.

FINANCE FUNTIONS

COST SECTION:

36

Cost-section of the company is divided into following two sections viz,

PRODUCT COST & CENTRAL COST and these deals with the following

functions:-

Determination of periodic profits including inventory valuation.

Determination of pricing policy of the company.

Work relates to capital expenditures of the company.

Developing variance management information report for different

parts of management for purpose of cost control and reduction.

Valuation of work in progress and finished goods.

Interaction with management of top management link for achieving

cost control and cost reduction and thereby improving bottom line of the

company.

Preparation of cost sheet of different product and their analysis for

future planning.

SALES SECTION:

Sales accounts section will deal mainly with the following:-

Scrutiny and vetting of estimates / quotation for sale of products /

services, whenever financial concurrence is required.

Scrutiny and vetting of agreements for sales of products and

services.

Invoicing for sale / advance or progressive payment / erection income and

other.

Maintenance of subsidiary records like sale journals / sales day book, sundry

debtor’s ledgers’ advances from customer ledger etc.

Payments, recovery and accounting of sale tax, excise duty.

37

Accounting of claims on carries/ insurance companies for missing items /

damages on outward consignments.

Scrutiny, payments and accounting of bills of carriers and insurers and other

miscellaneous claims relating to them outwards consignments.

Review and in coordination Reconciliation as well as follow up of recovery

of outstanding dues from the customers Calculation and scrutiny of data for

payments of royalties to the collaborators.

STORES SECTION:

For the conveniences of performance of various functions it is divided in to

further three sections which are as follows:-

a) Stores bills.

b) Store review

. They deal mainly with the following items of works:-

i) Payment of supplier’s bill including bill for advances indigenous.

ii) Pricing of stores receipt vouchers including fixed assets vouchers and fixed

assets receipt vouchers.

iii) Maintenance of accounts of advances to suppliers, claims

recoverable, claims for short suppliers, rejections and rectifications to materials

and sundry creditors.

iv) Opening of letter of credit and arranging payment to suppliers

under credit / deferred payment agreements.

v) Payment of bills for ocean freight, port trust dues, custom duty, local agents

commission and clearing agents bills, transit insurance bills, bills of contractors

for transport / handling etc. and accounting of such payments are made at

regional offices.

38

vi) Maintenance of account of accounts of material issued on loan

and materials issued to subcontractors.

vii) Keeping account of earnest money and security deposits

received from tender and suppliers.

viii) Adjustment of stores in transit to be made at the close of the

year.

BOOKS AND BUDGET SECTION:

i) Preparation of operating budget for the company as a whole.

ii) Co-ordination with various function of organization with regard to generation

and submission of important MIR’s to corporate office.

iii) Preparation of annual accounts to the company.

iv) Coordination with company auditors with regard to company

accounts.

v) Maintenance and accounting of fixed assets accounts.

Preparation of long term profit plans based on broad objectives of the

company.

PAYROLL SECTION:

This section deals mainly with the following functions:-

i) Preparation of monthly wages bill.

ii) All account work related to personal payment and discloses profit and

loss account of the company.

iii) Dealing with income tax authority with regard to personal taxation of

employee.

39

iv) Dealing with other statutory authority such as P.F. Commissioner, ESI

(Employee state insurance).

v) To ensure correct payment of salary and wages and other benefits to

employees in line with policies.

vi) Payments and accounting of all miscellaneous expenditures incurred

on post and telegraph, telephone and miscellaneous payments.

CASH SECTION:

The cash section shall responsible for banking of all money or money’s

worth received by the company and the disbursement of all authorized

payments on behalf of the company and also for the safe custody of all cash

and other valuable as may be entrusted to that section. The broad functions

are:

i) Receipt of money in the form of cash, cheque, bank draft, and postal

orders etc.on behalf of the company. Payment of money to the

suppliers, contractors etc. on behalf of the company and disbursement

of salaries, wages and other personal payments of employees.

ii) Handling and custody of cash, cheque etc. till disbursement or deposit

in bank and custody of other valuables like govt. and other paper

securities, share certificates, bank guarantees etc.

iii) Accounting of all receipt and payments on behalf of the company in

cash / bank books, maintenance of registers and other record

incidental to and for the efficient dispatch of the responsibilities of the

section.

iv) Arrangement / operation of cash credit facility with banks.

v) Preparation of cash flow statement forecasts etc.40

Note: - The function of arrangements of cash credit facility specified at item

(IV) above is now discharged centrally by the cash management section of

the corporate office. However the division concerned will also keep proper

liaisons with all the local members, bank consortium to ensure the smooth

functioning of the centralized cash credit system.

WORKS SECTION:

Work section of the company is dealing with the following functions:-

i) Payments of contractors bill including bills for advance.

ii) Maintenance of accounts of contractors with regard to security

deposits, earnest money, progressive payments.

iii) 215 maintenance of accounts of materials issued on loans to

contractors.

iv) All accounting work related to capital expenditure in progress on

erection of plant & machinery and building.

v) All other miscellaneous. Work relating to hiring of various facilities.

vi) Payments and accounting of all expenditure related to revenue

particularly with regard to expenditure related to revenue particularly

with regard to expenditure incurred on repair and maintenance of plant

machinery, building and roads.

41

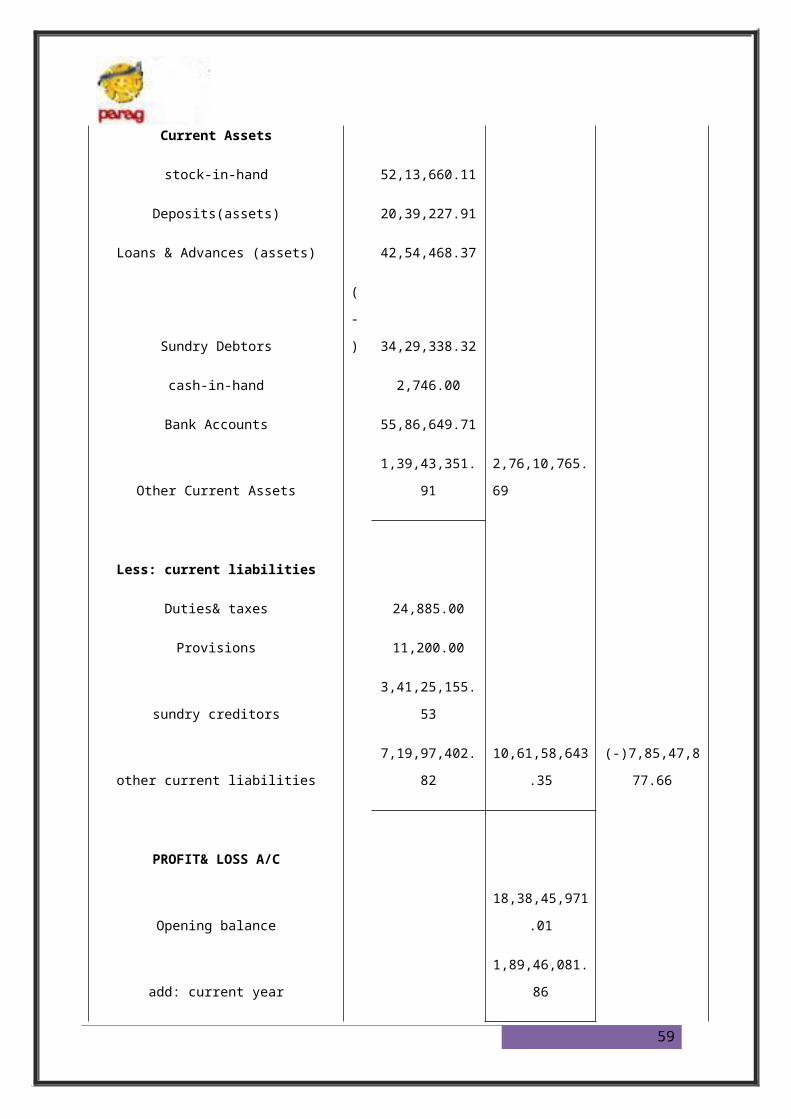

Status of DUSS Ltd. Moradabad showing

balance sheet

Balance sheet of 2007-08

PARTICULARS AMOUNT AMOUNT

Sources of Funds:-

Capital account 3,69,71,020.61

Loans (Liability)

secured loans 6,29,78,457.05

unsecured loans 1,37,60,018.19 7,67,38,475.24

Branch / Divisions 4,02,98,483.91

GRAND TOTAL 15,40,07,979.76

Application of Fund:-

2,57,17,108.19

Fixed Assets

Investment 17,65,774.85

42

Working capital

Current Assets

stock-in-hand 52,13,660.11

Deposits(assets) 20,39,227.91

Loans & Advances (assets) 42,54,468.37

Sundry Debtors (-) 34,29,338.32

cash-in-hand 2,746.00

Bank Accounts 55,86,649.71

Other Current Assets 1,39,43,351.91 2,76,10,765.69

Less: current liabilities

Duties& taxes 24,885.00

Provisions 11,200.00

sundry creditors 3,41,25,155.53

other current liabilities 7,19,97,402.82 10,61,58,643.35

(-)7,85,47,877.6

6

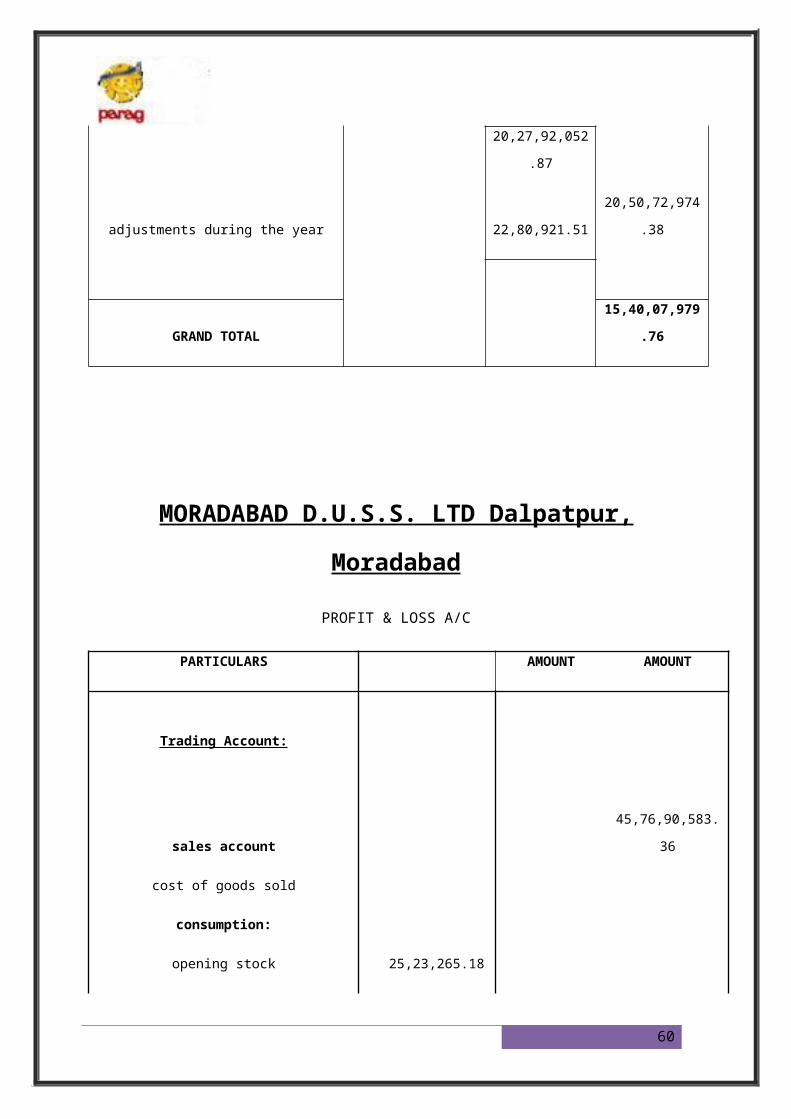

PROFIT& LOSS A/C

Opening balance 18,38,45,971.01

add: current year 1,89,46,081.86

20,27,92,052.87

adjustments during the year 22,80,921.51 20,50,72,974.38

GRAND TOTAL 15,40,07,979.76

43

MORADABAD D.U.S.S. LTD Dalpatpur,

Moradabad

PROFIT & LOSS A/C

PARTICULARS AMOUNT AMOUNT

Trading Account:

sales account 45,76,90,583.36

cost of goods sold

consumption:

opening stock 25,23,265.18

purchase account 37,66,55,503.45

37,91,78,768.63

Less: closing stock 52,13,660.11 37,39,65,108.52

Expenses (Direct) 6,53,25,407.77 43,92,90,516.29

Gross profit 1,84,00,067.06

Income Statement :

44

income (Revenue) 6,01,545.79

Sub-total 1,90,01,612.85

Less : Expenses

Expenses ( indirect) 3,79,47,694.71 3,79,47,694.71

Net Profit (-)1,89,46,081.86

45

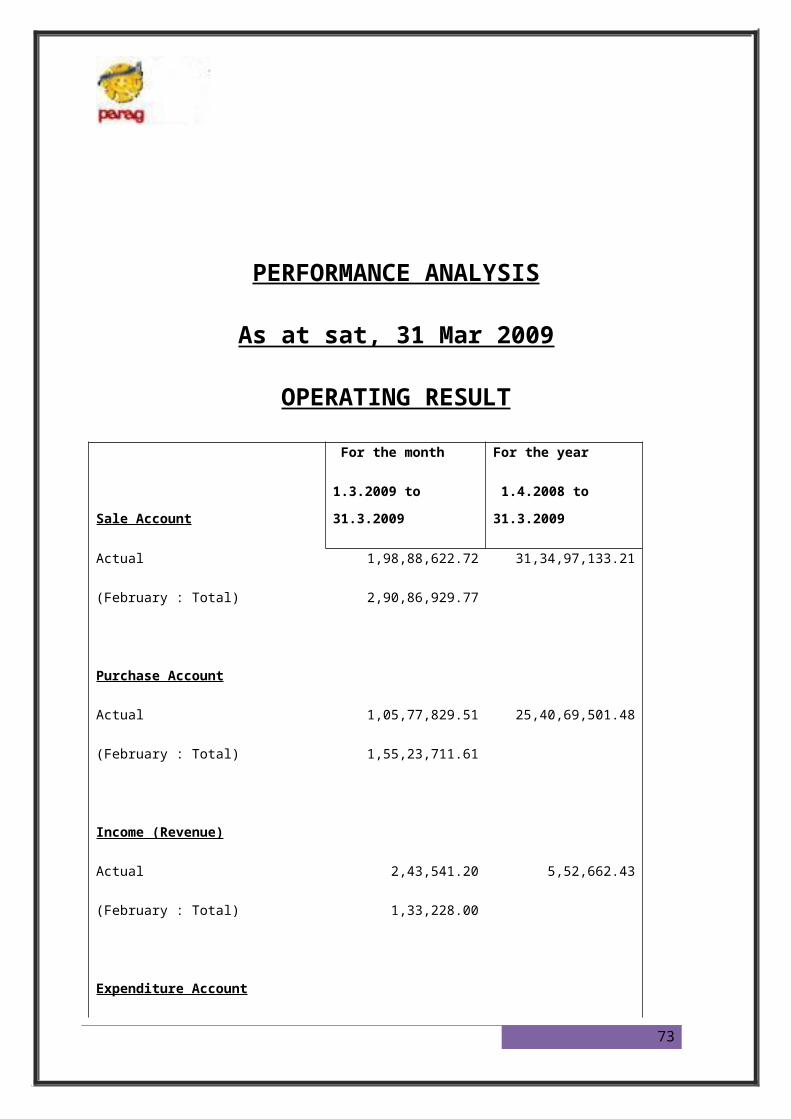

PERFORMANCE ANALYSIS

As at sat, 31 Mar 2008

OPERATING RESULT

For the month For the year

Sale Account 1.3.2008to31.3.2008 1.4.2007to31.3.2008

Actual 11,29,163,915.60 45,76,90,583.35

(February : Total) 2,45,33,288.04

Purchase Account

Actual 9,54,02,454.77 37,66,55,503.45

(February : Total) 4,56,69,888.86

Income (Revenue)

Actual 48,168.54 6,01,545.79

(February : Total) 11,605.00

Expenditure Account

Actual 4,05,99,953.68 10,32,73,102.48

(February : Total) 75,58,099.98

46

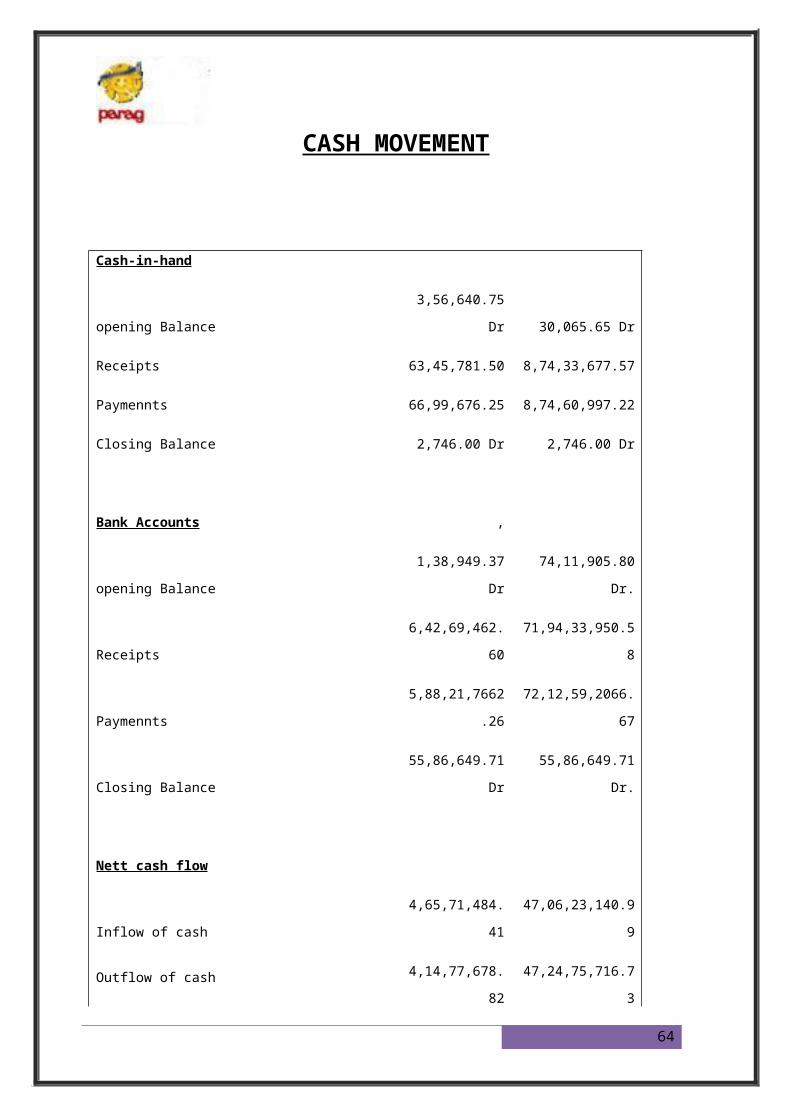

CASH MOVEMENT

Cash-in-hand

opening Balance 3,56,640.75 Dr 30,065.65 Dr

Receipts 63,45,781.50 8,74,33,677.57

Paymennts 66,99,676.25 8,74,60,997.22

Closing Balance 2,746.00 Dr 2,746.00 Dr

Bank Accounts ,

opening Balance 1,38,949.37 Dr 74,11,905.80 Dr.

Receipts 6,42,69,462.60 71,94,33,950.58

Paymennts 5,88,21,7662.26 72,12,59,2066.67

Closing Balance 55,86,649.71 Dr 55,86,649.71 Dr.

Nett cash flow

Inflow of cash 4,65,71,484.41 47,06,23,140.99

Outflow of cash 4,14,77,678.82 47,24,75,716.73

(net inflow of cash) 50,93,805.59 (-)18,52,575.74

47

RATIO ANALYSIS OF DUSS Ltd. Moradabad

ON THE YEAR OF 2008

for the month for the year

1.3.2008 to

31.3.2008

1.4.2007 to

31.3.2008

PROFITABILITY RATIOS

Sales Account 11,29,13,915.60 45,76,90,593.35

Gross Profit (-)1,20,64,020.96 1,84,00,067.06

Gross Profit % (-)10.68% 4.02%

Net Profit (-)3,11,38,397.36 (-)1,89,46,081.86

Net Profit % (-)27.58% (-)4.14%

Operating Cost % 127.58% 104.14%

Current Ratio

A. Current Assets 2,76,765.69

B. Current Liabilities 10,61,586,43.35

A:B 0.26:1

( at the end of February) 0.77:1

48

Quick Ratio

(without stock-in-hand)

A. Liquid Assets 2,23,97,105.58

B. Current Liabilities 10,61,58,643.35

A:B 0.21:1

(at the end of February) 0.61:1

Debt / Equity Ratio

A. Loans (Liability) 7,67,38,475.24

B. Net Capital Account (-)16,81,01,953.77

A:B (not calculable)

Working Capital Turnover

A. Sales Account 45,76,90,583.35

B. Working Capital (-)7,85,47,877.66

A / B (not calculable)

Receivables Turnover

(avg. credit on sales)

A. Sundry Debtors (-)34,29,338.32

B. Sales Account 45,76,90,583.35

(A / B) * no. of wkg days (not calculable)

49

Present Status of DUSS Ltd. Moradabad

showing balance sheet

Balance sheet of 2008-09

PARTICULARS AMOUNT AMOUNT

Sources of Funds:-

capital account 3,69,79,745.61

Loans (Liability)

secured loans 6,31,86,202.05

unsecured loans 1,37,60,018.19 769,46,220.24

Branch / Divisions 6,85,60,178.06

GRAND TOTAL 18,24,86,143.91

Application of Fund:-

Fixed Assets 2,31,84,266.30

Investment 13,89,196.85

working capital

50

Current Assets

stock-in-hand 10,97,881.13

Deposits(assets) 20,39,227.91

Loans & Advances (assets) 12,79,449.55

Sundry Debtors (-) 30,40,668.25

cash-in-hand 22,886.75

Bank Accounts 3,20,13,258.85

Other Current Assets 1,27,58,957.22 4,61,70,993.1666

Less: current liabilities

Provisions 11,200.00

Duties& taxes 18,343.00

sundry creditors 4,60,19,234.89

other current liabilities 7,91,09,037.02 12,51,57,823.91 (-)7,89,86,830.75

PROFIT& LOSS A/C

opening balance 20,50,72,974.38

add: current year 3,20,45,623.98

23,71,18,598.36

adjustments during the year (-)2,19,086.85 23,68,99,511.51

GRAND TOTAL 18,24,86,143.91

51

MORADABAD D.U.S.S. LTD Dalpatpur,

Moradabad

PROFIT & LOSS A/C

PARTICULARS AMOUNT AMOUNT

Trading Account:

sales account 31,34,97,133.21

cost of goods sold

consumption:

opening stock 52,13,660.11

purchase account 25,40,69,501.48

25,92,83,161.59

Less: closing stock 10,97,881.13 25,81,85,280.46

Expenses (Direct) 5,63,10,031.57 31,44,95,312.03

Gross profit (-)9,98,178.82

Income Statement :

income (Revenue) 5,52,662.43

52

sub-total (-)4,45,516.39

Less : Expenses

Expenses ( indirect) 3,16,00,107.59

Other revenue accounts - 3,16,00,107.59

Net Profit (-)3,20,45,623.98

PERFORMANCE ANALYSIS

As at sat, 31 Mar 2009

53

OPERATING RESULT

For the month For the year

Sale Account 1.3.2009 to 31.3.2009 1.4.2008 to 31.3.2009

Actual 1,98,88,622.72 31,34,97,133.21

(February : Total) 2,90,86,929.77

Purchase Account

Actual 1,05,77,829.51 25,40,69,501.48

(February : Total) 1,55,23,711.61

Income (Revenue)

Actual 2,43,541.20 5,52,662.43

(February : Total) 1,33,228.00

Expenditure Account

Actual 3,43,52,271.97 8,79,10,139.16

(February : Total) 30,97,126.11

CASH MOVEMENT

54

Cash-in-hand

opening Balance 35,351.05 Dr 2,748.00 Dr

Receipts 63,45,781.50 9,21,78,543.97

Payments 66,99,676.25 9,21,58,403.22

Closing Balance 22,886.75 Dr 22,886.75 Dr

Bank Accounts

opening Balance 2,36,24,857.45 Dr 55,86,649.71 Dr.

Receipts 1,91,78,807.00 50,02,82,511.00

Payments 5,88,21,7662.26 47,38,55,901.86

Closing Balance 55,86,649.71 Dr 3,20,13,258.85 Dr.

Net cash flow

Inflow of cash 2,15,62,113.25 37,12,14,707.01

Outflow of cash 1,31,86,176.15 34,47,67,957.12

(net inflow of cash) 83,75,937.10 2,64,46,749.89

RATIO ANALYSIS OF DUSS Ltd. Moradabad

ON THE YEAR OF 2009

55

for the month for the year

1.3.2008 to

31.3.2008 1.4.2007to31.3.2008

PROFITABILITY RATIOS

Sales Account 1,98,88,622.72 31,34,97,133.21

Gross Profit (-)1,58,69,732.01 (-)9,98,178.82

Gross Profit % (-)79.79% (-)0.32%

Net Profit (-)2,70,17,247.67 (-)3,20,45,623.98

Net Profit % (-)135.84% (-)10.22%

Operating Cost % 235.84% 110.22%

Current Ratio

A. Current Assets 4,61,70,993.16

B. Current Liabilities 12,51,57,823.91

A:B 0.37:1

( at the end of February) 0.47:1

Quick Ratio

(without stock-in-hand)

A. Liquid Assets 4,50,73,112.03

56

B. Current Liabilities 12,51,57,823.91

A:B 0.36:1

(at the end of February) 0.43:1

Debt / Equity Ratio

A. Loans (Liability) 7,69,46,220.24

B. Net Capital Account (-)19,99,19,765.90

A:B (not calculable)

Working Capital Turnover

A. Sales Account 31,34,97,133.21

B. Working Capital (-)7,89,86,830.75

A / B (not calculable)

Receivables Turnover

(avg. credit on sales)

A. Sundry Debtors (-)30,40,668.25

B. Sales Account 31,34,97,133.21

(A / B) * no. of wkg days (not calculable)

WAGES & SALARY ADMINISRATION

57

The basic purpose of wages and salary administration is to establish and

maintain an equitable wages and salary. It is not so simple to developed or

maintain the wages and salary structure in an structure in an organization. So

wages and administration should be controlled by some proper agency. This

responsibility may be entrusted to the personnel department or general company

organization, or to some job executive. Since the problem of wages salary is

very dedicated and complicated. I usually entrusted to a committee of high

ranking executives representing major line organization. The major functions of

much committee are:-

1. Approval and / or recommendation to management on the job evaluation

methods and finding.

2. Review and recommendation of basic wages and salary structure.

3. Help in the formulation of wages policies.

4. Co-ordination and review of departmental rates to ensure conformity.

5. Review of budget estimates for wages and salary adjustments and increase.

This committee should be supported by the advise of the

technical staff; such committee may be for job evaluation; job description meant

rating wages salary survey in an industry and for a review of present wages rate

procedure and policies.

Alternative the overall plan is first presented by the personnel

manager in consultation and discussions with senior members of other

department. It is then committed for final approval of the top executives. Once

he has given his approval for the wages and salary structure and the rules for

administration its implementation becomes a joint effort of all heads of the

departments. The actual appraisal of the performance of subordinates is carried

out by the various managers, who is turn submit their recommendations to

58

ensure compliance with established rules to administration in unusual cases of

serious disagreement the president makes the final decision.

(a) MEANING

A wages (or pay) is the remuneration paid, for the service of labour in

production to on employee/worker. Wages usually refers to the hourly rate paid

to such groups as production and maintenance of employees (blue caller

worker). On the other side, salary normally refers to the weekly or monthly

rates paid to clerical administrative and professional employees (white caller

worker). Every organization has a unique wages and salary structure if its own,

while framing the wages and salary police the top management ensure that the

wages structure is attractive and the compensation package provides a

reasonable standard of living for its employees.

According to the plan, it first prepared by the personnel manager and

discussion with senior members of other departments. After this it is submitted

for final approval of the top executive organization, a sound wages policy is to

adopt a job evaluation, depending upon the contents of the job.

(b)PRINCIPAL

The generally accepted principles governing the fixation of wages and salary

are:-

i) The plan should carefully distinguish between jobs and

employees.

ii) Equal pay for equal worker.

iii) There should be a well defined and clear cut procedure

for hearing the wages complaint and redressed of these grievances.

iv) All the wages and trade union members should be fully

aware of the existing wages rates and grievances redressed procedure about

wages complaints.59

v) The wages and salary structure should be flexible so that

changing condition can be easily met.

vi) The wages and salary payment must fulfill a wide variety

of human need for self actualization.

vii) For revision of wages

FACTORS:

The factor usually taken into consideration for wages and salary administration.

i) The firm’s capacity to pay

The main factor of wages and salary

administration is the capacity of firm’s to pay. Firm’s enjoying higher profits,

higher rate of return over investment gives higher wages than those firms’s

which are running into losses are enjoying lesser profit.

ii) Demand and supply of labour

If the demand of labour is more than its

supply the labour wanted higher wages and if the demand of labour is less then

its supply the labour wanted lesser wages.

iii) Prevailing market rate

To attract the sufficient and maintain the quality

and quantity of manpower, a firm gives the wages to its employee, according to

the industry or other firm’s.

60

iv) The cost of living

When the cost of living increasing, the worker demand

increases for real wages.

v) Job requirement

Wages is also depending upon skills, responsibility and

job condition required. Those employees who have higher responsibility get

more wages then the employees which have lower skill and responsibility.

vi) Production of labour

Productivity measures the contribution of all the

resource factors men, method, material and management.

vii) Managerial attitudes

Job management’s desire to maintain or enhance

the company’s prestige has been a major factor in the wages policy of number

of firms. Desire to improve or maintain moral to attract high-caliber employees,

to reduce turnover and to provide as possible wages policy decisions.

WAGES DETERMINATION PROCESS

The element of these diagrams is explained below:

a) Job Analysis

61

The process is done, after the deciding that how many persons would be needed.

It is a written document. It records the detail of training, skill, qualification,

abilities, experience, responsibilities etc.

Job Description and Specification

These are the structure of job analysis. Job description

mean to describe the job that, what’s responsibilities, authority given to the

people where as, job specification tells that what kind of person to recruit and

what qualities are present for doing the particular job.

c) Job Evaluation

In these processes, there is a comparison between the

different type of work and the workers which are doing this work.

d) Wages Survey

After the job evaluation the actual amount to be paid to

worker must be determined. This is done by making wages or salary survey.

Such surveys are given the answers the questions like, what are other firms

paying? What is the level of pay offered by firms for similar occupation? etc.

such wages survey provide may be kinds of useful information about

differences in wages level for particular kinds of occupation. this can have a

great influence on an organization compensation policy.

e) Wages Structure

The next step is to determine the wages structure. For this

several decisions need to taken such as:-

62

i) Where the organization wishes or able pay amount above,

below or equal to averages in the industry.

ii) Where wages range should be provide for merit increase or

whether their should be single rate.

iii) The number and width of the payment grade and extent to

overlap.

iv) Which jobs are to be placed in each of the pay grade.

There are though no hard and fast rule for making such

decision and procedure.

f) Rules of Administration

Wages & Salary administration should be

controlled by some proper agency. This responsibility may be entrusted to

personal department or, some job executive. For controlling the wages and

salary administration a committee is formed for the formulation of wages

policies. According to the rules of administration the wages and salary is paid to

the worker / employees.

g) Wages Payment

Method of wages payment is different in different

organization. Different industry applied different method for the payment of

wages. But the three most common methods which have provide a basis for all

these systems of wages are payment by time, by piece and debt. These systems

are generally termed as:-

a) Time Wages Payment System

63

As the name suggested under this

system time is the basis of payment. Remuneration of is the directly calculated

on the basis of time spent by him on the work. This system is simplest historical

and oldest method of wages payment. Under this system if a worker is paid 5

rupees per hour and work for 8 hours.

They will get 5x8=40 rupee

* Time wages=T x R

T = Time spent at the work place.

R = Rate of wages per unit of time.]

This system enjoys the following payoffs:-

1) This method is simple to operate and easy to understand.

2) Understand the method any sickness and lazy cannot cut the payment of

worker.

3) It is accept by trade unions.

4) Eliminated wastage.

5) Illiterate worker also can not cheated by employees.

Pitfalls:-

1) Increase cost of production.

2) No distraction between good and bad workers.

3) Decline in efficiency.

64

b) Piece Wages Payment System

This system is also very old, but

it is only recently that it has begun to be windily used. Under this system

workers are paid according to the quality of goods products not on the

basis of payment.

When the result or output is zero, then quite obviously the pay

will be zero.

Piece wages = N x R

N = Number of pieces are produced by the workers.

R = Rate per piece

This system enjoys the following payoffs:-

1) It provides greater incentive it the worker.

2) It distinguishes skilled and semiskilled work.

3) Easy estimation of labour cost.

Pitfalls:-

1) This method is harmful for worker.

2) Heavy wastage during the highly wages.

65

3) Under this system minimum wages are not fix.

c) Balance Method

The methods also know as debt method. This is a

combination of time and piece rates. The worker is guaranteed an hourly or a

daily with an alternative piece rate. If the earning of a worker calculated at the

piece rates, the worker is guaranteed an hourly or daily rate with an alternative

piece rate. If the earning of a worker calculated at the piece rate exceeds the

amount which he would have earned means, if the paid on the time basis he get

credit for the balance, i.e. , if his price rate earning are equal to his time rate

earnings the question of excess payment dose not arise. Where piece rate

earning are less than time rate earning he is paid on the basis of the time rate;

but the excess which he is paid is carried forward as a debt against him to

recovered from any future balance of piece work earning over time work

earning over time earnings. This system presupposes the fixation of time and

piece rate on a scientific basis.

All the wages payment system has discussed, but in PARAG time

wages payment system is going on, because other wages payment system is

impossible.

ALLOWANCES AND DEDUCTIONS

I) ALLOWANCES:

1. DEARENESS ALLOWANCE (D.A.)

The payment of these allowances

will be regulated in accordance with the orders issued by the company from

66

time to time. It will be regulated by Head Office of Government of U.P. in

Lucknow. Dearness allowance will be computed on the basis pay of each

employee. Dearness allowance (DA) will be admissible during leave provided

leave salary is payable. It will not be admissible during extra ordinary leave or

leave without apply.

- At present Dearness Allowance is 41.8% on Basic Pay.

2. HOUSE RENT ALLOWANCE (HRA)

The payment of these allowances

will be regulated to those employees who never uses the company quarters and

they live in there own quarters. House Rent Allowance (HRA) is also payable in

leave period. For these purpose leave means total leave of all kinds not

exceeding 120 days of the leave period of holidays are combined with leave, the

entire period of holidays and leave should be taken as one spell of leave.

- At present House Rent Allowance is 10% on Basic Pay and Special

Allowances.

3. OVERTIME ALLOWANCE (OT)

When a worker, who comes in

factories act, 1948, works beyond the prescribed hours on any day, he is entitled

to payment of Overtime Allowance. This is worked out at a single rate i.e.

(1/208 of pay, Basic Pay, Special Allowance, Dearness Allowance) for each

hour on a working day. When a worker works more than 9 hours on a day or

more than 48 hours a week. Overtime Allowance is calculated at double the rate

mentioned above.

OT = BP + SA + DA \ 208 X 1 Hr.

67

In the cause of staff not covered by factories Act, the overtime

allowance will be claimed in accordance with rules and rates fixed by the

Management.

4. CONVEYANCE ALLOWANCE

Conveyance allowance / cycle allowance

will be paid as per the rules framed by the company from time to time.

5. LATE NIGHT SNACK ALLOWANCE (LNSA)

All employees who

work in night shifts extending beyond midnight are paid LNSA. This allowance

is also paid to temporary employees who working against regular employees.

- At present LNSA is Rs. 30/- per night

6. WASHING ALLOWANCE

Payment of washing allowance is to be

regulated as per orders/circulars issued by personnel department in this regard

from time to time.

- At present Washing Allowance is Rs. 70/-per month

II) SUBSCRIPTOIN TO CONTRIBUTORY POVIDEND FUND:

On receipt of office order of joining from personal dept., the data is sent

to computer for deduction of CPF. The particulars are noted in the individual

salary/wages record and further recoveries are affected every month at the rate

prescribed from time to time.

- At present the rate of recovery of subscription towards cpf is 12% wages/salary.

III) RECOVERY OF CYCLE/SCOTER/MOPED/CAR ADVANCE:

68

When payment of cycle/motorcycle/scooter/moped/car advance is made,

the particulars of the number of installment recoverable will be noted in the

individual salary/wages record and the recovery effected every month

accordingly. Just after the last installment of the principle amount is recovered,

interest due will calculated be and also be noted for recovery.

IV) LIFE INSURANCE PREMUM:

The concerned office of the life insurance

Corporation intimates the rate of Premia and policy numbers in respect of

employees covered by Life Insurance Corporation’s Salary savings scheme.

This will be noted in the individual salary/wages record and recoveries affected

every month accordingly.

V) HOSPITAL AND DIET CHARGES:

A statement of hospital and diet

charges recoverable from various employees is received every month from the

chief medical officer in charge of the hospital either directly or through the

Revenue Accounts section. A note of the amount due for recovery will be kept

in the individual wages/salary record and recoveries will be affected

accordingly.

- At present the rate of Hospital and Diet Charge is Rs.30/-per day.

VI) CLUB SUBSCRIPTIONS:

The list employees joining the clubs as well as

those who have discontinued the subscription of the club are received from the

secretaries of the clubs every month. With reference to these advice recoveries

will be affected by the establishment Accounts Section.

69

- At present the rate of Club Subscription is Rs.50/-per month.

VII) INCOME TAX:

At the beginning of the year, the total anticipated income

assessable to income tax is worked out with reference to details available in the

establishment.

Accounts section and the installments of deductions are fixed accordingly. In

the month of August or September a declaration is obtained from each

employee assessable to income tax showing the detail of annual income, Life

Insurance Premium paid, subscription to provident fund, Recurring Deposit

Scheme and other relevant particulars for the calculation of income tax in terms

of financial act of the year. A statement of deductions on account of income tax

deduction at source will also be supplied to the employees concerned by 30

April every year.

For the purpose of calculations of income tax recoverable from salaries of

company employees, the salaries earned and paid from the period from April to

March are taken into account. However, in case of deputations the basis adopted

while in government service of namely, salaries earned during the period March

to February, will be continued in the company so long as they continue on

deputation with the company.

70

JOURNAL ENTRY OF EARNINGS AND DEDUCTIONS

DESCRIPTION DR CR

BASIC PAY xxx

DEARNESS ALLOWANCE xxx

HOUSE RENT ALLOWANCE xxx

OVERTIME ALLOWANCE xxx

LATE NIGHT SNACK ALLOWANCE xxx

WASHING ALLOWANCE xxx

SPECIAL ALLOWANCE xxx

OTHER ALLOWANCE xxx

RENT COMPANY QUARTERS xxx

ELECTRICITY CHARGES xxx

WATER AND GARDEN CHARGES xxx

SUBSCRIPTION TO CONTRIBUTION PROVIDENT FUNDxxx

RECOVERY OF CYCLE/MOTOR CYCLE/ CAR ADVANCExxx

LIFE INSURANCE PREMIUM xxx

HOSPITAL AND DIET CHARGES xxx

CLUB SUBSCRIPTION xxx

OTHER RECOVERIES xxx

71

FINDINGS

To find out the financial position of Parag will decrease day by day.

After analyzing the ratio in two year balance sheet we found that the ratio

has decreased in comparison to last year balance sheet.

The existing pay structure should be regularly revised. This will make job

evaluation program mere acceptable to employees.

Wages and salary structure must be such that which help to maintain

harmonious relation between employers and employees.

Regional difference in wages should invariably be maintained.

To find out satisfaction level of employees related to salary.

To find out employees grade in parag milk factory.

72

Employees Grade

73

SUGGESTION

The company should create a system to evaluate the financial position of

the company.

Ensure that training contributes to competitive strategy of the firm.

Different strategies need different financial skill for implementation.

There should be making leaning one of the fundamental values of the

company. Let this philosophy percolate down to all employees in the

organization.

There should be a comprehensible and systematic approach to training

exits, and training and re-training are done at all levels on a continuous

and ongoing basis.

There should be a proper linkage among organizational and individual

training needs.

CONCLUSION

74

1. Pay fixation on age revision in PARAG is not point to point due to which

pay annually arises.

2. There is no efficiency bar system in PARAG.

3. Both the inefficient and efficient persons get equal wages, hence efficient

workers lose their enthusiasm for work.

BIBLIOGRAPHY

1. Understanding financial position of Parag.

2. Financial dept. of PARAG.

3. Establishment of Accounts in PARAG, Moradabad.

4. Intranet of PARAG, Moradabad.

5. www.indiandairy.com

6. www.paragmilk.com

7. E-mail: [email protected]

75

![Mudit [Recovered]](https://static.fdocuments.in/doc/165x107/55cf8557550346484b8cf2fd/mudit-recovered.jpg)