MOVING TOWARDS THE EUROPEAN DATA-AGILE ECONOMY The ...

61

The European Data Market Monitoring Tool Report 15th May 2020 MOVING TOWARDS THE EUROPEAN DATA-AGILE ECONOMY

Transcript of MOVING TOWARDS THE EUROPEAN DATA-AGILE ECONOMY The ...

The European Data Market Monitoring Tool Report

15th May 2020

MOVING TOWARDS THE EUROPEAN DATA-AGILE ECONOMY

UPDATE OF THE EUROPEAN DATA MARKET STUDY

SMART 2016/0063

D2.8 FINAL REPORT ON POLICY

CONCLUSIONS

IDC Italia S.r.l (Milan, IT) The Lisbon Council (Brussels, BE)

Prepared for:

Katalin IMREI

Policy Officer

European Commission – DG CONNECT

Unit G1 – Data Policy & Innovation

15th May 2020

Author(s) Gabriella Cattaneo, Giorgio Micheletti,Carla La Croce, Cristina Pepato, Alessandra Massaro, Irene Magnani (IDC)

Deliverable D2.8 Final Report on Policy Conclusions update

Date of delivery 15.05.2020

Version 2.1

Addressee officer Katalin IMREI

Policy Officer

European Commission, DG CONNECT

Unit G1 — Data Policy and Innovation

EUFO 1/265, L-2557 Luxembourg/Gasperich

Contract ref. N- 30-CE-0835309/00-96

5

Table of Contents

1. Introduction .................................................................................................................. 7

Considerations on COVID-19 Impact ............................................................................................. 8

2. THE EU DATA MARKET GROWTH IN 2019 .................................................................... 9

3. THE EU DATA MARKET AND ECONOMY POST-COVID SCENARIO ............................... 12

3.1 Introduction .......................................................................................................................... 12

3.2 The EU27 Data Market Post-COVID ...................................................................................... 12

3.3 The impact of COVID-19 on industries ................................................................................. 14

3.4 The EU27 Data Economy post-Covid .................................................................................... 15

4. THREE SCENARIOS FOR THE EUROPEAN DATA ECONOMY ......................................... 19

4.1 Baseline Scenario (Pre-COVID) ............................................................................................. 24

4.2 High-Growth Scenario (Pre-Covid) ........................................................................................ 27

4.3 Challenge Scenario (Pre-Covid) ............................................................................................. 30

5. A CHANGE OF PACE IN DATA POLICIES ....................................................................... 33

5.1 The new Data Policies and the EDM Monitoring Tool .......................................................... 33

5.2 The evolution of Data Ethics ................................................................................................. 35

5.3 Big Data as the lifeblood of the next innovation waves like AI ............................................. 36

5.3.1 AI paving the way for the Cognitive Revolution across European Utilities ........................ 36

5.3.2 Health Data and Data-driven Innovation in the European Healthcare Industry ................ 40

6. THE ROLE OF THE U.K. IN THE EUROPEAN DATA ECONOMY ...................................... 45

6.1 The U.K. - A Leading European Data Economy ...................................................................... 47

6.2 After Brexit: An initial policy perspective .............................................................................. 48

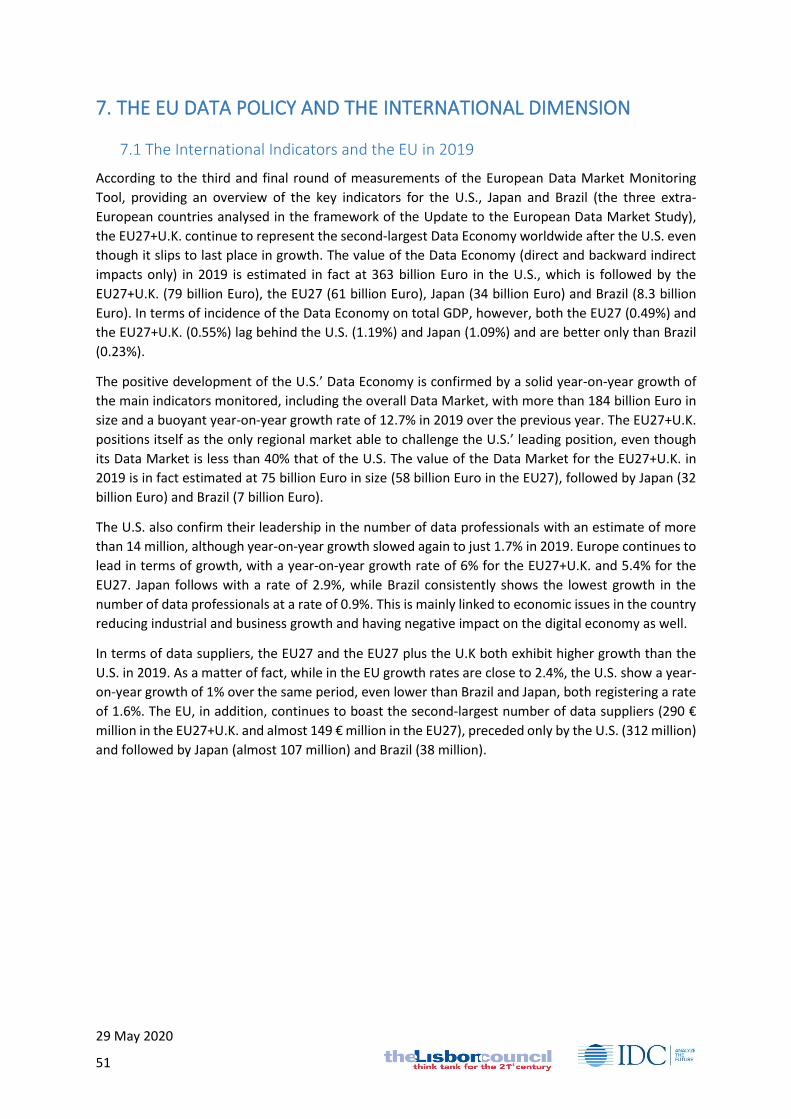

7. THE EU DATA POLICY AND THE INTERNATIONAL DIMENSION ................................... 51

7.1 The International Indicators and the EU in 2019 .................................................................. 51

7.2 What the International Indicators really say ......................................................................... 54

7.3 Europe on the international scene: looking for a recovered confidence ............................. 55

8. CONCLUSIONS ............................................................................................................ 56

8.1 Overview ............................................................................................................................... 56

8.2 Data Professionals ................................................................................................................ 57

8.3 Data Companies .................................................................................................................... 58

8.4 Data Market and Data Economy........................................................................................... 58

8.5 Concluding remarks .............................................................................................................. 60

29 May 2020

6

Table of Figures Figure 1: The European Data Market Monitoring Tool ........................................................................... 8

Figure 2 Top three use case for AI among European healthcare providers ......................................... 41

Figure 3 Digital Economy and Society Index (DESI) – 2019 Ranking ..................................................... 45

Figure 4 IMG World Digital Competitiveness Ranking 2019 ................................................................. 46

Figure 5 Data Professionals, Data Professionals’ Skills Gap, Data Suppliers and Data Users in the U.K.

(2019; 2025, 3 scenarios) ...................................................................................................................... 47

Figure 6 Data Suppliers’ Revenues, Data Market Value, Data Economy Value in the U.K. (2025, 3

scenarios) .............................................................................................................................................. 48

Figure 7 Adequacy vs. No-Deal ............................................................................................................. 50

Figure 8: The European Data Market Monitoring Tool: Interrelated Indicators and Building Blocks .. 56

Table of Tables Table 1 ICT spending by segment, 2019 and forecast 2020 ................................................................. 13

Table 2 Industries with the highest negative impact on IT spending from COVID-19, 2020 ................ 13

Table 3 EU27 Data Market, Post-Covid scenario, 2020 and 2025, 3 scenarios (€M)............................ 14

Table 4 EU27 Data Economy, Post-Covid Scenario, value and impact on GDP, 2019, 2020, 2025 (€

Million; %) ............................................................................................................................................. 16

Table 5 EU27 Data Economy, Post-Covid Forecast 2020 by type of impact (M€, %) ........................... 17

Table 6 EU27 Data Economy, Post-Covid Baseline scenario 2025, value and shares by type of impact

(€ Million; %) ......................................................................................................................................... 17

Table 7: Macroeconomic Assumptions ................................................................................................. 20

Table 8: Policy-Regulatory Assumptions ............................................................................................... 20

Table 9: Data Market Assumptions ....................................................................................................... 22

Table 10: Global Trends ........................................................................................................................ 23

29 May 2020

7

1. Introduction

Since 2013, the European Data Market Monitoring tool has traced the fast development of data-driven

innovation and its gradual diffusion across industries and user constituencies. What started as a

technology trend mostly relevant for business IT managers has quickly become a transformation

process of deep social as well as economic relevance, witnessed by the over 400 €B of value reached

by the European Data Economy in 2019, corresponding to 2.8% of the EU28 GDP. 2019 was also the

year when the emergence of Artificial Intelligence and related technologies became visible outside

the technology world. This created a new awareness about the power of data enabling all kinds of AI-

enabled decision-support systems, digital helpers in the work environment, robots, and drones,

generating new cultural as well as ethical and organizational challenges.

Today, in 2020, a more mature understanding of the complexity of the multi-dimensional

transformation driven by Big Data and AI has crystallised. The digital policy strategies presented in

February 2020 by the new Commission led by Ursula Von der Leyen recognize this and represent a

change of pace in data policies, both in breadth and boldness. The new European Data Strategy is a

cornerstone of the new Europe’s Digital Strategy and underline the ambition for Europe to become a

leading role model for a society empowered by data to make better decisions in business and the

public sector. A renewed ambition for Europe to become a global leader in the data-agile economy is

accompanied by the need to achieve “technological sovereignty” based on a resilient and independent

data infrastructure. The White Paper on Artificial Intelligence presented the same day suggests several

policy options to develop AI ecosystems of excellence and trust, reflecting the understanding of the

systemic impacts of technological innovation always promoted by this study.

As the centrality of data for European competitiveness is recognized at the highest level of the EU, the

results of the European Data Market (EDM) Monitoring Tool, presented in this report, provide relevant

insights and suggestions for the potential consequences of policy choices in the next years. The EDM

Monitoring Tool was designed by IDC, in collaboration with the Lisbon Council, to provide the

European Commission with a comprehensive view of the data-driven economy, through annual

reports. The methodology provides a unique perspective of the development of the data ecosystem

in Europe, through 6 main indicators measuring its key components (see Figure 1): the skills (the

number of data professionals and the gap between demand and supply of data skills); the enterprises

and their roles (both data suppliers and data user companies); the demand-side value (the market)

and the supply-side value (the data suppliers revenues); and finally the overall impacts on the

economic system, through the estimate of the European Data Economy as a share of EU GDP. This

report presents the main indicators for the year 2019 and the potential development paths of the

EU27 Data Market and Data Economy to 2025 under the three updated scenarios presented in the

Third Report on Facts and Figures1: Baseline scenario, High Growth scenario, and Challenge scenario.

These scenarios provide a snapshot of the range of magnitude of the potential economic gains or

missed opportunities facing the Data Economy.

Finally, the EDM Monitoring Tool measures a more limited set of indicators for three other

international economies, the U.S., Brazil and Japan. The report presents a snapshot of the indicators

and looks more closely at the U.S., examining the competitiveness implications. The full set of

indicators is available in the “Facts and Figures” report. Further results of the study are published on

the website www.datalandscape.eu.

1 Update of the European Data Market Study, SMART 2016/0063, D2.7 Third Report on Facts and Figures

29 May 2020

8

Considerations on COVID-19 Impact

As this report was being finalised in February 2020, the COVID-19 pandemic started its rampage across

the globe, endangering people and livelihoods, forcing governments to implement measures to

contain the virus, with unprecedented impacts on the European economy as well as the technology

market. While the EDM Monitoring tool data and analysis until 2019 remain valid, clearly our

estimates for 2020 are now off the mark and all forecasts to 2025 would need to be revised. Based on

IDC research carried out in March-April 2020, we provide an additional post-Covid-impact scenario

with estimates on the likely Data Market and Data Economy decline in 2020 and potential rebound

and impacts on the 2025 scenarios for the EU27. These estimates should be taken with caution

because of the extremely high level of uncertainty about the current damages to the economy and

the potential recovery paths. Unfortunately, there is insufficient evidence and time to revise the

estimate of all the other indicators of the EDM Monitoring too for 2020.

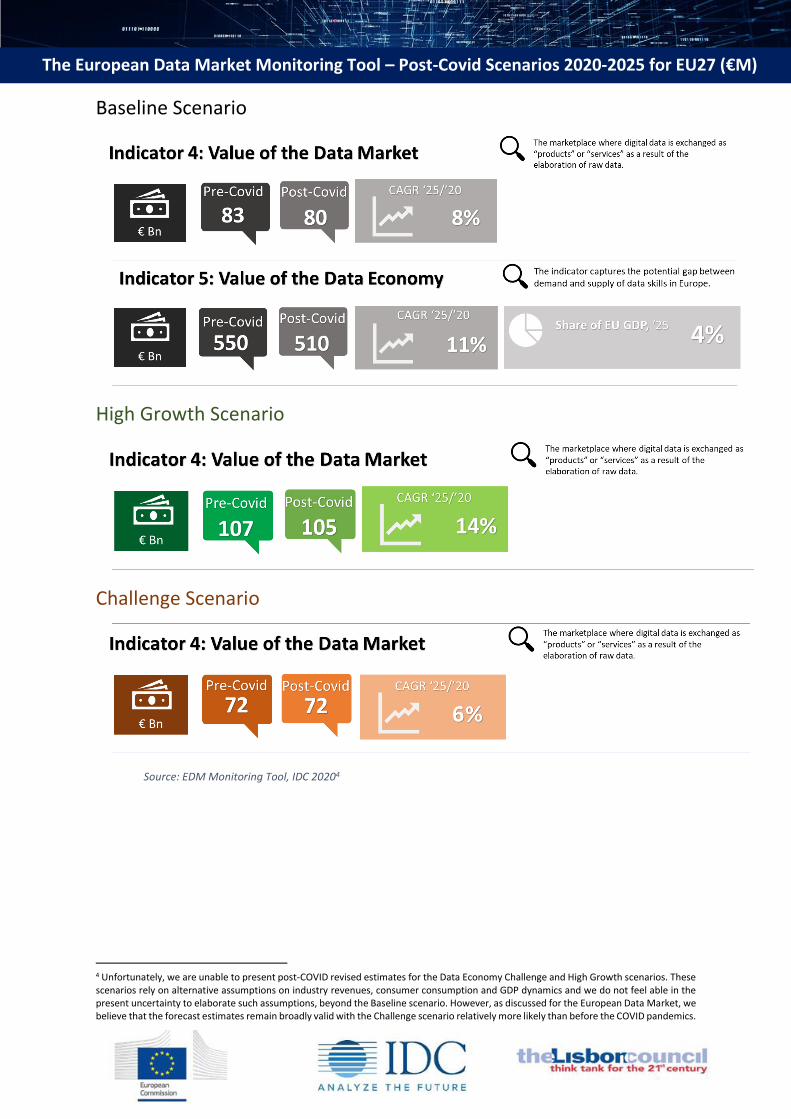

According to our post-COVID scenario estimates, the European Data Market should decrease by 7.1%

to 54 €B in 2020 (compared to 58 €B in 2019) and the Data Economy by 5.5% to 307 €B (compared to

325 €B in 2019). In our view, the powerful negative impact of the slow-down in 2020 will be followed

by a rebound and a likely return on the growth path in the next years. Many of the powerful drivers

of data-driven innovation are likely to prove resilient in the next years, particularly the willingness to

invest in digital technologies in order to re-launch services and create new products to stimulate

demand.

By 2025, the post-Covid Baseline scenario foresees strong growth rates resulting in a value of 80 €B

for the European Data Market (compared to 82.5 €B in the pre-Covid scenario) and 516 €B for the

Data Economy (compared to 550 €B in the pre-Covid scenario). However, the incidence of the

European Data Economy on the EU27 GDP will slightly increase from 4% (Pre-Covid scenario) to 4.04%

(post-Covid scenario) because GDP is also affected by the recession. The Challenge and High Growth

scenarios remain broadly valid, even though their degree of likeliness change; the Challenge scenario

is marginally more likely (if the recovery does not take off as hoped) while the High Growth scenario

assumptions, based on hyper-growth thanks to technology investments, seem now quite remote.

Figure 1: The European Data Market Monitoring Tool

29 May 2020

9

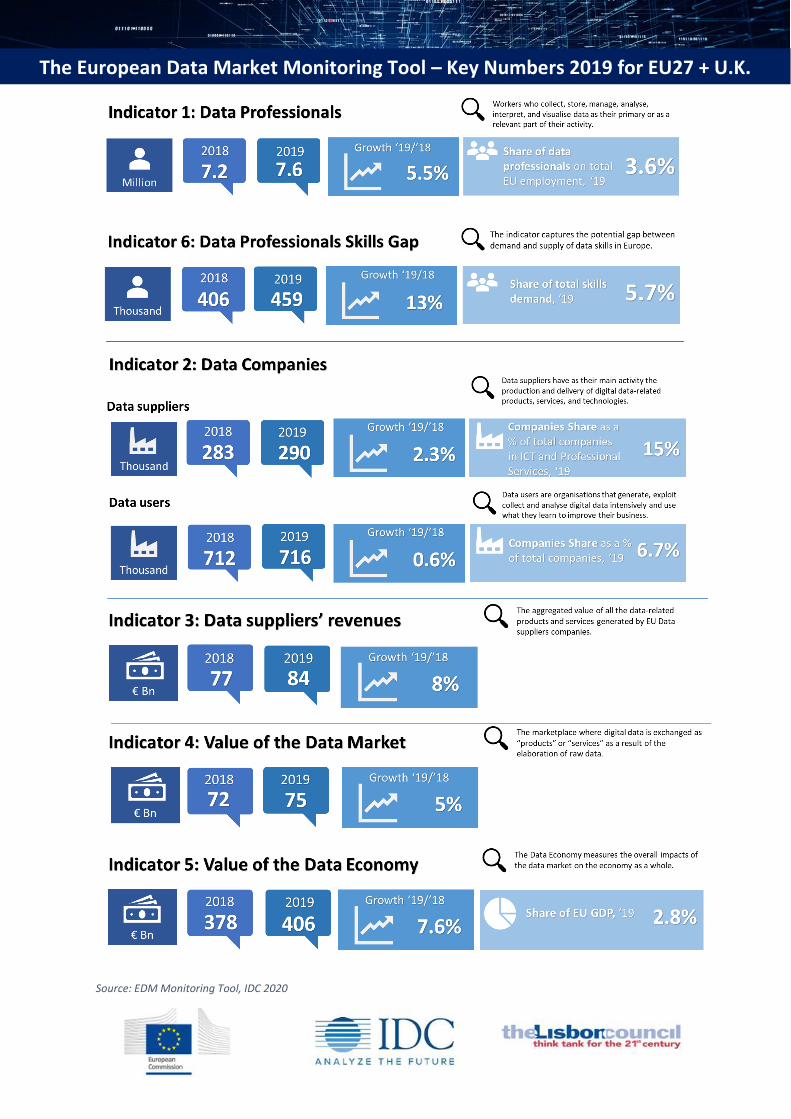

2. THE EU DATA MARKET GROWTH IN 2019

The value of the Data Economy, which measures the overall impacts of the Data Market on the

economy as a whole, exceeded the threshold of 400 Billion Euro in 2019 for the EU27 plus the United

Kingdom2, with a growth of 7.6% over the previous year. The positive trend in the growth of the Data

Economy is confirmed by the Data Market value in 2019 for the EU27+U.K., which is displaying a

growth rate above the one exhibited by the total IT spending, at 4.9% year-on-year, reaching 75 Billion

Euro. The size of the Data Market by Member State still correlates closely with the overall economic

strength of each country, as well as with their national spending on ICT - the U.K, Germany, France,

Italy, the Netherlands and Spain account for approximately three quarters of the Data Market for the

EU27+U.K. in 2019. Smaller economies, however, display higher-than-average shares of Data Market

on ICT Spending. This is notably the case of Estonia, and, to a lesser extent, Cyprus, Latvia and Lithuania

that have all fully embraced the process of digital transformation for some time. Aside from the

outliers, the spread of share of ICT spending taken by the Data Market is fairly narrow across most

Member States with the 16 middle Member States having a share between 10% and 13%.

As far as supply and demand are concerned, data suppliers are estimated at more than 290,000 units

in the EU27+U.K. for 2019, exhibiting a year-on-year growth of 2.3%. Data users, instead, remained

stable in 2019, amounting to nearly 716,000 units and registering a growth of 0.6% over the previous

year. Following increasing growth rates over the prior four years, these figures show a picture of

consolidation of data companies in the EU.

Revenues generated by data suppliers increased by 9% to reach almost 84 Billion Euro in the

EU27+U.K., with the U.K., still in the leading position, Germany, France and Italy showing the highest

share of data revenues per country - together accounting for two thirds (66%) of data revenues in the

European Union plus the U.K.

According to the latest estimates, the number of data professionals in the EU27+U.K. reached 7.6 €

million in 2019, corresponding to 3.6% of the total workforce, with an increase of 5.5% over the

previous year. However, the EDM Monitoring Tool continues to register an imbalance between the

demand and the supply of data skills in Europe as the estimated gap reached approximately 459,000

unfilled positions in the EU27+U.K., corresponding to 5.7% of total demand. The data skills gap is

forecast to continue in all the forecast scenarios as demand will continue to outpace supply.

2 Since Brexit is now definitive (as of May 2020), the authors provided an overview of data for EU27+U.K. until 2019, and for the remaining months data are displayed for EU27.

29 May 2020

10

Source: EDM Monitoring Tool, IDC 2020

The European Data Market Monitoring Tool – Key Numbers 2019 for EU27

29 May 2020

11

Source: EDM Monitoring Tool, IDC 2020

The European Data Market Monitoring Tool – Key Numbers 2019 for EU27 + U.K.

29 May 2020

12

3. THE EU DATA MARKET AND ECONOMY POST-COVID SCENARIO

3.1 Introduction

This section presents revised estimates of the EU27 Data Market and Data Economy value in 2020,

based on IDC revised ICT market estimates3 developed in the period March-April 2020, as well as a

forecast of the implications of these changes for the 2025 Baseline scenario. An analysis of the current

impacts by industry and the potential for rebound is also included. However, these estimates should

be considered with caution given the unprecedented nature of this pandemic and its economic impacts

and the high level of uncertainty about the potential consequences.

As COVID-19 sweeps across the globe, endangering people and livelihoods, forcing governments to

implement measures to contain the virus, Europe is facing a significant impact on people, the

economy, business, and investments. The impact of COVID-19 across European industries is significant

and is creating uncertainty in the technology market, with overall negative consequences ranging from

decreased customer demand and technology investment delays to supply-chain failures. Although

essential to contain the virus, lockdowns and restrictions on mobility are extracting a sizable toll on

economic activity.

As the IMF highlighted in the latest World Economic Outlook (April 2020), this crisis is like no other for

three main reasons: the first is that the shock is large, with an output loss that likely dwarfs the losses

that triggered the global financial crisis. Second, there is continued severe uncertainty about the

duration and intensity of the shock, similarly to what happens during a war or a political crisis. Third,

there is a very different role for economic policy, as differently that in normal crises, where

policymakers try to encourage economic activity in this case, the crisis is to a large extent the

consequence of needed containment measures. A partial recovery is projected for 2021, but the level

of GDP is likely to remain below the pre-virus forecast, also due to the considerable uncertainty about

the strength of the rebound.

3.2 The EU27 Data Market Post-COVID

The economic impact of the COVID-19 slow-down started to be understood only in March. IDC carries

out ongoing research and analysis of the impacts on ICT spending by industry, which is influenced by

contrasting trends: industries providing digitally-enabled (telecom, media) and critical services

(healthcare, government) are holding on or even growing, while others (tourism, transport services,

retail) are in free fall. This is clearly illustrated by Table 1 about forecasts of ICT spending by segment

in 2020, showing growth for infrastructures and software spending and reductions for devices and IT

services (correlated with business spending). The impact on the Data Market however is not identical,

because of the different mix of ICT components.

3 https://www.idc.com/misc/covid19

29 May 2020

13

Table 1 ICT spending by segment, 2019 and forecast 2020

Year on year growth (%)

2019 2020 2021

Devices 0.9% -8.8%

Infrastructure 8.8% 5.3%

Software 10.0% 1.7%

IT Services 3.9% -2.0%

Telecom Spending

1.0% 0.5% 1.0%

ICT Spending 3.5% -1.6% 3.4%

Source: IDC Worldwide ICT spending forecast Post-Covid, 21-Apr-2020

Industries see different effects on their ICT spending depending on their necessity to support the

population through the corona virus, and the industry’s interaction with workers. Some Member

States have imposed a lockdown, where the population must remain home in self isolation, but key

industry workers are exempt from this. Industries whose workers must be present at the workplace

are most affected, particularly consumer service industries, while the industries where remote work

is possible have been less impacted by the lockdown. While the Data Market is based on digital

technologies, many of the leading Big Data user industries are service industries severely affected by

the lockdown (e.g., Transport, Manufacturing, Retail and Wholesale). Table 2 shows the top industries

with the biggest revenues decline anticipated in 2020.

Table 2 Industries with the highest negative impact on IT spending from COVID-19, 2020

2019 2020 2021

Transport and Storage 4.7% -8.4% 0.0%

Mining, Manufacturing 5.6% -6.8% 0.4%

Home -0.1% -4.0% 0.1%

Retail & Wholesale 5.1% -3.3% 0.7%

Source: IDC Worldwide ICT spending forecast Post-Covid, 21-Apr-2020

All industries – except for Healthcare – are expected to decline in 2020, but most should return to

growth by 2021. According to IDC forecasts, several industries (Communications, Manufacturing,

Professional Services, and Retail) are likely to experience significant rebound in 2021, but not all

industries are expected to bounce back at the same rate, because of the disruption to the value chains

and the uncertainty about consumer and end user demand perspectives.

The estimated impact of Covid-19 on forecast growth in the European Data Market for 2019, and 2020,

is shown in Table 3. The turnaround in the market is dramatic: instead of a growth of +6.9% a fall of

7.1% in revenues. The four industries listed in Table 2 (Transport, Manufacturing, Retail and Home

consumer) account for nearly 90 percent of this fall.

However, as soon as the economy will start recovering, we expect the Data Market to pick up its

growth again. For example, Big Data and AI technologies have proven their value in managing the

COVID-19 pandemic and will likely continue to play a strong role in healthcare but also in many other

industries. Online interactions in education, remote working and media have increased and reached

new users as never before, hopefully overcoming once and for all old cultural barriers.

Overall, we estimate the cumulative average growth rate from 2020 to 2025 to increase from 5.8%

(pre-COVID baseline scenario) to 8.1% (post-COVID baseline scenario) leading the EU27 Data Market

to reach a value of 80 €B (Table 3). Even with this faster growth rate, the EU Data Market will not

reach the same value expected in the pre-COVID scenario but will be only slightly smaller, losing only

29 May 2020

14

3%. Symmetrically, this means that without this acceleration of growth it will not be possible to

recover the value burnt by the 2020 recession.

Extrapolating the same rationale to the other 2025 scenarios, we consider the Challenge scenario as

still valid in absolute terms, with a higher cumulative growth rate compared to the pre-Covid scenario,

because of a limited rebound effect. On the other hand, we consider the High Growth scenario post-

Covid as less likely, because of the difficulty to achieve very fast growth, and lower in value than the

pre-Covid estimate by 2%. In conclusion, based on these considerations, the most likely scenario

remains the Baseline, with the Challenge scenario as a possible alternative.

Table 3 EU27 Data Market, Post-Covid scenario, 2020 and 2025, 3 scenarios (€M)

EU27 Data Market

2019 2020 Forecast Growth rate 2020/2019

Baseline Scenario 2025

Forecast CAGR 2025/ 2020

Challenge Scenario 2025

Forecast CAGR 2025/ 2020

High Growth Scenario

2025

Forecast CAGR 2025/ 2020

Pre-COVID forecast

58,214 62,244 6.9% 82,564 5.8% 72,329 3.0% 107,139 11.5%

Post-COVID forecast

58,214 54,081 -7.1% 79,965 8.1% 72,329 6.0% 104,783 14.1%

Forecast variation

-8,163

-2,599

0

-2,355

% Variation -13%

-3%

0%

-2%

Variation on 2019

-4,133

% Variation -7%

Source: IDC European Data Monitoring Tool, April 2020

3.3 The impact of COVID-19 on industries

The impact of COVID-19 across European industries is significant and is creating uncertainty in the

technology market, with overall negative consequences ranging from decreased customer demand

and technology investment delays to supply-chain failures. IDC believes the IT spending pattern will

generally follow the direction of GDP, with some potential exceptions.

European industries that are the most negatively affected by the outbreak in terms of cash-flow and

overall business impact in this first phase are consumer facing, including transport and leisure and

retail. Moreover, severe challenges raised in the manufacturing space (lack of labour, supply chain,

and eventually demand) and oil and gas (demand, pricing).

Public sector organizations are in a special situation - they are under incredible duress but are also

expected to see more monetary support. The healthcare sector is expected to receive additional

emergency funding in many countries to cope with hospitalizations. Some of that funding will find its

way into ICT technologies in the mid-term.

If the overall impact on industries is negative, there are also some important "bright spots" for specific

solutions and use cases, through which technology can help make the difference and help businesses

and societies deal with the COVID-19 disruption. They are all enabled by data-driven innovation and

anticipate trends which are likely to drive the Data Market and the Data Economy back to growth.

29 May 2020

15

AI Enabled Solutions Will Support Healthcare Systems in Proactively Managing Outbreaks

Healthcare is the sector where organizations look at technology to predict the spread of disease more

accurately, and to proactively manage the pandemic. At this time, IT investments might undergo an

immediate increase, with hospitals expanding their digital infrastructure supporting ICUs and a surge

in capacity. But investments in population health analytics, AI-enabled solutions, remote patient

monitoring, and telemedicine will be also key in the broader response to the outbreak. The use of big

data and artificial intelligence were applied "to strengthen contact tracing and the management of

priority populations." Researchers have been starting to use deep learning techniques to support

COVID-19 detection when analysing CT scans and patient records. Remote health monitoring systems

can be used to observe and check the progress of less critical COVID-19 patients, and at the same time

keep the pressure off hospitals by managing patients affected by other pathologies at home or in other

care settings. IDC believes some of these patterns, albeit at a smaller scale, are already taking place in

Europe as well.

Online Shopping Triggering More Cloud Infrastructure Consumption

With restrictions and social distancing in place, online shopping is even more popular and consumers

who haven't relied on ecommerce, have been more likely to move online to buy food and household

items to avoid busy stores. These platforms and online marketplaces are experiencing an increase in

demand that could also be significant. In turn, this will increase cloud infrastructure consumption in

the short term.

Digital Advertising Will Help the Public Sector Raise COVID-19 Awareness

Safeguarding citizens' health will be among the top priorities for the public sector during these hard

times. Digital ads and social media campaigns to provide trusted, localized information to residents

regarding the spread and development of the outbreak are key to help societies in the fight against

the virus.

Chatbots Will Help Self-Isolating Customers Get Support

With stay-at-home measures in place, face-to-face customer support might be challenged, especially

for highly customer-facing industries such as finance, retail, and telecoms. These companies might

look at alternative ways to provide their customers the support they need without physical human

interaction needed. We see an increase of adoption of virtual assistants or digital customer service

agents (chatbots) to maintain customer relationships without human contact. Since these projects

require some incubation, IDC maintains that spending might take months or quarters to follow.

Intelligent Supply Chain Will Help Businesses Minimize Disruption

Another area that is deeply affected and is experiencing delays or shortages is the supply chain. This

is impacting many European automotive manufacturers as they are experiencing difficulties in

sourcing components from Chinese suppliers. In this scenario, manufacturing companies are looking

at use cases relying on artificial intelligence (AI) to minimize supply chain disruption. Intelligent supply

chain solutions might see an increase in demand as companies look at automation to improve visibility

of inventories, supply prediction, and adaption in order to minimize disruption. Backend changes

require long timeframes for implementation, so spending will take a quarter to follow.

3.4 The EU27 Data Economy post-Covid

This section presents our post-Covid scenario forecast for the Data Economy, building on the revised

estimates of the EU27 Data Market and on macroeconomic and industrial trends. To understand this

forecast it is important to remember the three main components of the Data Economy:

29 May 2020

16

• The direct impacts, which is the value of the goods and services sold in the Data Market;

• The indirect impacts, backwards (on the supply chain: gains made by industries providing

goods and services to data users) and forwards: revenues gained by user industries thanks to

data innovation;

• The induced impacts on the general economy, thanks to additional spending and consumption

driven by the value of the direct and indirect impacts.

Therefore, the post-COVID Data Economy reflects the decline of the Data Market, the fall in revenues

of the industries affected by the lock-down, and the steep decrease of consumer demand and overall

consumption.

As shown in Table 4, according to our new estimates the EU27 Data Economy is expected to decrease

by 5.5% in 2020, contrasting with a healthy growth of 7.7% in 2019. This means a reduction of 18 €B

on the previous year and a loss of 48 €B of potential growth, compared with the pre-Covid forecast

for the 2020 Data Economy. The value of the Data Economy as a share of GDP is stable compared to

2019 because the EU GDP is decreasing sharply too.

Table 4 EU27 Data Economy, Post-Covid Scenario, value and impact on GDP, 2019, 2020, 2025 (€ Million; %)

EU 27 Data Economy

2019 Impact on GDP

2019

2020 Forecast Growth rate 2020/2019

Impact on GDP

2020

Baseline Scenario

2025

CAGR 2025/2020

Impact on GDP 2025

Pre-COVID forecast

324,858 2.60% 355,109 9.30% 2.80% 549,783 9.10% 4.00%

Post-COVID forecast

324,858 2.60% 306,926 -5.50% 2.60% 509,851 10.70% 3.90%

Forecast variation

0.0% -48,183 -15% -0.20% -39,932 2% -0.10%

% Variation

-13.6%

-7.3%

Variation on 2019

-17,932

% Variation

-5.5%

Source: IDC European Data Monitoring Tool, April 2020

Breaking down the type of impacts provides new light on the dynamics of this fall of the Data Economy

(Table 5). The direct impacts decrease by 7% compared to the previous year, on a par with the Data

Market. The indirect impacts decrease only by 3% and therefore represent a higher share of the Data

Economy. As explained above, the indirect impacts are the B2B component of the Data Economy,

which is suffering from the disruption of value chains but is also more resilient, since some critical

industries remained active during lockdown and others such as healthcare see spending going up, not

down. Digital supply chains were disrupted, but less so than physical supply chains: consider for

example online shopping which during lockdown is increasing, even if facing delivery problems for

physical goods. Finally, the biggest loss concerns the induced impacts, a decrease of 8.5% on 2019,

reflecting the steep drop of consumer spending, tight financial conditions, and the rise of

unemployment. These effects lead to a decrease in the share of induced impacts from 33% in 2019 to

32% in 2020.

29 May 2020

17

Table 5 EU27 Data Economy, Post-Covid Forecast 2020 by type of impact (M€, %)

EU27 Data Economy, 2019-2020

Direct

Impacts Share of total %

Indirect Impacts

Share of total %

Induced Impacts

Share of total %

Values 2019 58,214 17.92% 158,586 48.8% 108,058 33%

Post-COVID forecast 2020 54,081 17.60% 153,992 50.20% 98,853 32.20%

Variation 2020 on 2019 -4,133 -0.3% -4,594 1.4% -9,205 -1.1%

% Variation 2020 on 2019 -7% -2% -3% 3% -8.5% -3%

Pre-COVID forecast 2020 62,244 17.50% 170,753 48.10% 122,113 34.40%

Source: IDC European Data Monitoring Tool, April 2020

Finally, in the post-COVID baseline scenario the EU27 Data Economy is expected to reach 516 €B by

2025, corresponding to 4% of GDP, same share as in the pre-COVID scenario. This means we expect

similar growth dynamics for the Data Economy and GDP. As already observed concerning the Data

Market, the recovery is expected to be quick, with the Data Economy returning to a healthy growth

rate already from 2021. However, because of the 2020 decline, the value by 2025 is estimated to be

33 €B lower than in the previous forecast. In the new forecast we expect direct and indirect impacts

to recover faster than induced impacts (Table 6) because the damages to consumer demand and the

labour market will take longer to be overcome.

Unfortunately, we are unable to present post-COVID revised estimates for the Data Economy

Challenge and High Growth scenarios. These scenarios rely on alternative assumptions on industry

revenues, consumer consumption and GDP dynamics and we do not feel able in the present

uncertainty to elaborate such assumptions, beyond the Baseline scenario. However, as discussed for

the European Data Market, we believe that the forecast estimates remain broadly valid with the

Challenge scenario relatively more likely than before the COVID pandemics.

Table 6 EU27 Data Economy, Post-Covid Baseline scenario 2025, value and shares by type of impact (€ Million; %)

EU27 Data Economy, Baseline scenario, 2025

Direct Impacts Share of total %

Indirect Impacts

Share of total %

Induced Impacts

Share of total %

Pre-COVID forecast 2025

82,564 15% 235,613 42.90% 231,606 42.10%

Post-COVID forecast 2025

79,965 15.50% 220,915 42.80% 214,992 41.70%

Variation Forecast

-2,599 0.5% -14,698 -0.1% -16,685 -0.4%

% Variation Forecast

-3% -6.2% -7.2%

Source: IDC European Data Monitoring Tool, April 2020

29 May 2020

18

Baseline Scenario

High Growth Scenario

Challenge Scenario

Source: EDM Monitoring Tool, IDC 20204

4 Unfortunately, we are unable to present post-COVID revised estimates for the Data Economy Challenge and High Growth scenarios. These scenarios rely on alternative assumptions on industry revenues, consumer consumption and GDP dynamics and we do not feel able in the present uncertainty to elaborate such assumptions, beyond the Baseline scenario. However, as discussed for the European Data Market, we believe that the forecast estimates remain broadly valid with the Challenge scenario relatively more likely than before the COVID pandemics.

The European Data Market Monitoring Tool – Post-Covid Scenarios 2020-2025 for EU27 (€M)

29 May 2020

19

4. THREE SCENARIOS FOR THE EUROPEAN DATA ECONOMY

The new European Data strategy outlines the ambition for Europe to become a leading role model for

a society empowered by data to make better decisions in business and the public sector and a global

leader in the data-agile economy. Our 2025 scenarios outline different pathways of evolution of the

European Data Market (EDM) and Data Economy in the next years, exploring the different mix of

factors and policy choices which may lead to achieve this ambition or instead to fail it. In the past years

we have monitored the fast growth of the Data Market and Data Economy and have witnessed the

evolution of supply and demand dynamics in Europe. Today, as we look at the main driving trends for

the next years, we notice that the role of policies has increased in relevance: as data-driven innovation

has become widespread across all industry sectors and user constituencies, the scope of the

regulations and framework conditions to be adapted has considerably grown. At the same time, the

emergence of disruptive technologies such as AI has increased the need for policy intervention to

manage emerging social, economic and ethical risks. Therefore, the 2025 scenario presented in this

report are strongly influenced by multiple policy assumptions shaped by the Data Strategy and

European Digital Strategy recently published by the new Commission.

Given this context, we have updated the description of the two main focal issues (axes) around which

we have developed our 2025 scenarios, as follows:

• the high or low pace of diffusion of data-driven innovation, driven by demand-supply

dynamics, and its impact on economic growth. This year we add to this perspective the pace

of multiple innovation adoption, where data is at the core of a multiple technology

environment powered by AI.

• the social and economic data governance model enabling a fair and competitive economy,

as indicated by the new European Data Strategy. Today the term “data governance” has grown

from its original narrow definition as an approach to data management, to a much broader

concept of a policy and conceptual framework establishing the norms, practices and principles

covering all aspects of data dynamics in the society and the economy. Essentially, the data

governance framework which is the first pillar of the new European Data Strategy recognizes

the need to deal with data as a strategic asset influencing power dynamics in the socio-

economic system.

At one extreme, we foresee a society where a few actors, such as leading online platforms,

governments, large businesses, dominate the main data assets and therefore capture a

disproportionately high share of data innovation benefits, increasing social inequality (highly

centralized model). The polar opposite of this scenario would be a society characterised by an open,

transparent and participatory approach to data governance, where both citizens and organisations

are able to control and extract value from their data. This would result in a wider social distribution of

data innovation benefits, decreasing social inequality. Trustworthiness and respect of data ethics

principles are other important characteristics of this ideal model.

This analysis highlights the critical turning points to be faced in the next years by governments,

businesses and social actors in the development of the European Data Economy. The combination of

alternative social and economic trends results in the following scenarios:

• The Baseline scenario is characterised by a healthy growth of data innovation, a moderate

concentration of power by dominant data owners with a data governance model protecting

29 May 2020

20

personal data rights, and an uneven but rather wide distribution of data innovation benefits in the

society. This is considered the most likely scenario.

• The High Growth scenario is characterised by a high level of data innovation, low data power

concentration, an open and transparent data governance model with high data sharing, and a

wide distribution of the benefits of data innovation in the society;

• The Challenge scenario is characterised by a low level of data innovation, a moderate level of data

power concentration due to digital markets fragmentation, and an uneven distribution of data

innovation benefits in the society.

The scenarios explore the drivers and framework conditions which may lead to maximise the benefits

of a balanced Data Economy and to avoid the risks of an unbalanced one, highlighting the

consequences of policy actions.

Table 7: Macroeconomic Assumptions

MACROECONOMIC

ASSUMPTIONS Baseline Scenario High Growth Scenario Challenge Scenario

Economy trends Moderate GDP growth

trends under 2% continue

after a slow down in 2020

Moderate GDP growth in

2020-2021 gradually

accelerates to healthy

growth by the end of the

forecast period.

Trade wars, political conflicts, and

unexpected events such as the

Coronavirus pandemic reduce

cumulative GDP growth rates over the

period to 1%

EU27 GDP growth CAGR 2019-

2025 1.5% 2.0% 1.0%

EU27 ICT spending growth CAGR

2019-2025 1.7% 2.2% 1.2%

EU27 Data Market CAGR 2019-

2025 6.0% 10.7% 3.7%

EU27 Data Market as a share of

ICT spending,2025 14.3% 18.0% 12.9%

Source: European Data Market Monitoring Tool, IDC February 2020

Table 8: Policy-Regulatory Assumptions

POLICY-REGULATORY

ASSUMPTIONS

Baseline Scenario High Growth Scenario Challenge Scenario

Digital Strategy/ Achieving

European technological

sovereignty

Europe makes progress in the

development of data

infrastructures and digital

resources, plays a strong role in

shaping global digital

governance rules building on

GDPR but does not quite

dominate AI-led developments

Strong investments and MS

cooperation help Europe to

develop fully independent data

infrastructures and digital

resources, to shape global digital

governance rules with EU values,

becoming a leader in the Big

Data-AI space

Uneven development of

European data infrastructures

and digital resources, continuing

dependency from global

platforms, fails in taking the lead

in global digital governance,

Europe struggles to keep up with

competition particularly for AI

Data Strategy-make

Europe a global leader in

the data-agile economy

The EU's gradually builds a single

market for data and attracts a

growing share of the global Data

Economy

The EU's share of the global Data

Economy well on the way to

become equal to its economic

weight by 2030 thanks to a

genuine single market for data

The EU market for data remains

fragmented with uneven data

sharing and the EU share of the

global Data Economy does not

grow on a par of its economy

Data Strategy -

Development of an

effective data governance

framework

Progress in the development of

the new regulatory framework

enhance data access and sharing

in time but main effects

deployed at the end of the

forecast period, the single

Fast progress with new Data Act,

Digital Services and Competition

framework enhance data access,

sharing and re-use, achieve fair

playing field and contribute to

effective single market for data

EU efforts to renew the digital

services and data governance

regulation fail or achieve only

minimal changes, barriers and

stakeholder’s reluctance to data

sharing remain high, only high

29 May 2020

21

market for data gradually

emerges

performing enterprises and

regions make progress

Data Strategy-

empowering individuals-

data and privacy

protection

GDPR implementation continues

successfully but further progress

on personal data portability and

control is slow and unevenly

applied across Europe, slow

progress in sharing data for

social good

GDPR and new measures ensure

people control of their data,

improve willingness to share

data for social good (healthcare),

barriers to data sharing removed

GDPR compliance only formal -

many Europeans become

careless about it and enterprises

learn to get around it - this

hinders the willingness to share

and reuse personal and non-

personal data for social good

Data Strategy/ investments

in EU data capabilities,

infrastructures,

standardization and

interoperability

EU High impact projects make

progress in the development of

data sharing and interoperable

architectures. Gradual

deployment of an EU cloud

infrastructure and cloud services

marketplace

EU High impact projects

successfully catalyse private

investment to develop data

sharing and interoperable

architectures. Successful

deployment of an EU cloud

infrastructure and cloud services

marketplace satisfies industry/

SMEs needs

EU High Impact projects

insufficient to catalyse

investments in EU data

infrastructures, European cloud

offerings grow but remain

marginal in the market and do

not break the dominance of

foreign suppliers-

Data Strategy/ developing

the skills for the Data

Economy

DEP programme5 slow to start

but delivers boost to

development of advanced digital

and data skills - uneven

distribution across the EU of

skills supply

DEP programme delivers boost

to development of advanced

digital and data skills - revised

Digital Education act drives

digital skills for digital

transformation

DEP Programme slow to start

with low impacts on advanced

digital skills supply, while

demand is hindered by weak

economic growth

Data strategy (Common

European data spaces

The development of common EU

data spaces is faster and more

successful in some sectors with

strong innovation demand

(manufacturing, agriculture) but

meets with barriers and low

demand in others failing to

achieve economies of scale.

Improvement of the single Data

Market and of data exploitation

by EU industries.

Successful development of

common EU data spaces

achieves economies of scale and

delivers strong boost to data

single market and data

exploitation by EU industries

The development of common EU

data spaces is slow and does not

deliver the expected boost to

industries across Europe, failing

to generate economies of scale

and therefore to fight the Data

Market fragmentation.

Data strategy and Digital

Strategy/ Europe as a

global player

EU makes progress towards a

Global Digital Cooperation

strategy and promoting the EU

digital transformation approach

- EU more proactive in

development and adoption of

standards and interoperable

technologies with mixed success

on the global scene

EU develops successfully a

Global Digital Cooperation

strategy becoming a leader in

promoting the EU digital

transformation approach -

defends and successfully

promotes EU standards and

interoperability choices

The EU fails in developing an

effective Global Digital

Cooperation strategy and

remains strongly dependent

from international standards and

interoperability choices

Digital Strategy/

Development of a

legislative framework for

trustworthy AI

The EU makes progress in

defining requirements for high-

risk AI particularly for training

data, human oversight, specific

applications such as remote

biometric identification (face

recognition) but fails to lead in

overall AI development

regulation

Europe develops a flexible

legislation based on the risk

management principle not

hindering technology progress

and becomes a successful global

leader of AI governance

principles

Fast AI technology progress in

other world regions supersedes

EU legislative proposals forcing

EU to revise its approach or risk

to weaken EU industry

competitiveness

White Paper on AI/ Development of an ecosystem of excellence for AI

Slow but secure improvement of EU AI research and innovation capabilities through HE, DEP and CEF2 programmes

HE, DEP and CEF2 programmes deliver a strong boost to European AI research and innovation capabilities building an ecosystem capable of global leadership

Slow start of HE, DEP and CEF2 programmes and insufficient investments hinder the development of European AI capabilities and research-innovation ecosystem

5 DE: Digital Europe Programme, HE: Horizon Europe Programme, CEF2: Connecting Europe Facility.

29 May 2020

22

Digital strategy/ European Cybersecurity, Gigabit connectivity, interoperability and standardization, Quantum. Blockchain and HPC

Increased investments accelerate deployment of 5G and blockchain infrastructures, provide basis for fast innovation adoption, progress accelerates at the end of the forecast period

Strong investment and MS collaboration drives boost to data infrastructures also providing basis for fast adoption of AI

Insufficient investments and difficulty in solving technology challenges hinder the development of EU digital capabilities and infrastructures

Digital Strategy/ Develop fair and effective regulation for the digital economy (competition, taxation, digital finance, consumer empowerment...)

Progress towards creating favourable conditions for the digital economy fighting new power imbalances

Fast progress in the adaptation of the market regulatory framework creating a fair playing field especially for SMEs and traditional industries

Insufficient progress towards creating favourable conditions for the digital economy - new power imbalances remain creating difficulties for SMEs and many traditional industries

Digital Strategy/ Develop a sustainable Data Economy

Partially successful policy initiatives supporting the ICT and electronic industry transition to fully climate-neutral, sustainability and energy efficiency

Successful policy initiatives supporting the ICT and electronic industry transition to fully climate-neutral, sustainability and energy efficiency

Policy initiatives fail to drive the ICT and electronic industry fully towards climate neutrality and sustainability by the end of the period

Source: European Data Market Monitoring Tool, IDC February 2020

Table 9: Data Market Assumptions

DATA MARKET

ASSUMPTIONS

Baseline Scenario High Growth Scenario Challenge Scenario

Data technologies

supply-demand

dynamics

Data industry drives technology

innovation, lower costs, data

holders gradually increase demand.

The adoption of big data

technologies spreads beyond

pioneers to mainstream users; a

fully developed data ecosystem

powers a positive demand-supply

growth cycle – boost by the DEP

European innovation forces

become lost in a maze of digital

barriers (incomplete Digital Single

Market). Only the best

enterprises and the richest regions

keep pace with the technology

race

Development of the

data ecosystem in

Europe

Emergence of multiple vertical/

horizontal industrial and personal

data platforms providing secure

data sharing and trading

environments for data industry and

data owners

The industrial and personal data

platforms converge in

interoperable EU infrastructures

with clear governance models,

fostering participation of SMEs

Insufficient development of the

data ecosystem, limited diffusion

of data sharing platforms

Rate of diffusion of

digital

transformation and

data-driven

business models

Fast adoption by large companies

and innovative SMEs; public sector

gradually catches up during the

period; slower adoption by

traditional SMEs

Widespread diffusion of digital

transformation, EU SMEs learn to

adopt data monetization

solutions; successful impact of

DEP and other policies supporting

fast digital transformation

Slower adoption of digital

transformation and data-driven

business models hindered by

lower private investments, lower

expectation of take-up of

innovative services, lack of trust

and confidence in data sharing

Managing data ethics and AI business risks

Guidelines and data ethics principles multiply – enterprises need time to find a balance between business interests and ethics but eventually succeed – in some areas European enterprises able to use their ethics as a competitive advantage

Europe develops a coherent system of data ethics guidelines balancing EU values and business interests which becomes a global reference point and a competitive advantage for EU businesses

Guidelines and data ethics principles multiply – European enterprises struggle to develop skills and capability to manage risks – many enterprises refrain from data-driven innovation for fear of business risks

Deployment of 5G

infrastructures

Commercial deployment starts

around 2020, uneven diffusion

across Europe

5G networks and services

deployment accelerated and fully

interoperable across Europe by

2025

Slow deployment of 5G networks

and services undermine IoT/

advanced services diffusion

Source: European Data Market Monitoring Tool, IDC February 2020

29 May 2020

23

Table 10: Global Trends

Global Trends Baseline Scenario High Growth Scenario Challenge Scenario

Multiple innovation:

enterprise ability to

adopt and combine

multiple technologies

enabled by data

Fast diffusion of technologies

drives multiple innovation, for

example leveraging AI software

for technology and process

innovation. By 2025 the take-up

of AI, Big Data, IoT, and

robotics reach over 60% of

medium-large EU enterprises.

But SMEs and enterprises from

traditional industries in some

regions (where for example 5G

diffusion is slower) struggle to

keep pace.

Take-up of multiple technologies and

multiple innovation grow even faster

than in the baseline scenario including

a large share of SMEs and all EU

regions.

Only leading enterprises succeed in

adopting multiple innovation, many

enterprises lag behind suffering from

insufficient investments in digital

infrastructures (missing 5G for

example) resources and skills

Rise of the platform

economy

(collaborative

connected, data-

centric environments

used to develop

multiple innovation) at

various levels: global

(mega platforms),

applications-specific or

industry specific.

European industries develop

industry platforms to harness

multiplied innovation and build

ecosystem-based value. For

example, by 2025 the majority

of manufacturers will use IoT

platforms with digital innovation

platforms to operate networks

of asset, product, and process

digital twins for a 25% reduction

in cost of quality.

European industries exploit platforms

to combine data with AI and machine

learning, spreading intelligence from

the core to the edge of their networks

turning data into action and action

into value.

European industries struggle to adapt

to the platform economy and to

develop cross-border ecosystems.

Markets fragmentation, data-sharing

obstacles. Insufficient interoperability

and standardization hinder

collaboration and innovation.

Deep transformation

of the work

environment

Driven by demographic and

technology trends, European

enterprises multiply the use of

"digital co-workers" (using

intelligent process automation

and AR/VR to

support/complement human

workers) reducing repetitive

tasks, improving productivity

and security and managing

digital transformation.

Besides automation, enterprises

engage in "augmentation" of human

resources providing technologies

enhancing their physical and

intelligence capabilities.

Technology-driven automation and

augmentation are badly managed and

create a negative reaction by the

human workforce slowing down

acceptance and digital transformation.

Emergence of new work culture and contracting models to create and manage an agile, borderless and reconfigurable workforce.

Organizations improve their capability to manage, retrain and upskill the existing workforce but they face problems of digital skills gap, resistance and need to access new talent sources. Change management and HR management are critical success factors. But substantial groups of workers are unhappy or displaced by the new way of working.

Organizations succeed in managing the transformation of the work culture for digital transformation through a combination of incentives, intensive training investments, identifying appropriate job roles and tasks in open ecosystems.

European organizations struggle to adapt to the new work environment and to motivate the workforce. Fragmented ecosystems and insufficient investments in re-training and re-skilling increase the skills gap and slow down digital transformation, while leaving many workers unhappy or displaced

29 May 2020

24

4.1 Baseline Scenario (Pre-COVID)

This scenario predicts a healthy growth of data-driven innovation and increase of investments in the

new wave of digital technologies, pioneered by the most advanced, competitive and innovative

enterprises, medium and large (both as technology providers and users) with a share of competitive

SMEs, savvy in the use of ICTs. By 2025 we expect the take-up of AI, Big Data, IoT, and robotics to

reach over 60% of medium-large EU enterprises (IDC survey on Advanced Technologies for Industry,

2019), while other technologies such as 5G, AR/VR, blockchain, new materials and industrial

biotechnologies will also make strong progress. This will force enterprises to engage in multiple

innovation, adopting and combining multiple technologies: this convergence is enabled and powered

by data and intelligence. A key driver of innovation will be the interplay and convergence between

cloud-enabled AI, Robotics and 5G, extensively supported by edge computing, which will require deep

re-organization and restructuring of business processes and value chains. In this scenario, competition

is powered by platforms and ecosystems where network effects and innovations feed off themselves.

In this scenario, the EU27 GDP cumulative growth average in the period 2019-2025 (+1.5%) will sustain

the investments in the digital economy and consumer willingness to spend. As a result, the Data

Market is forecast to reach 82.5 billion Euro in the EU27, with a compound annual growth rate of 5.8%.

The Data Economy will grow faster than the Data Market, because the investments in data

technologies have direct and indirect impacts on the economy with a multiplier effect, reaching a

value of 550 billion Euro in the EU27, with a steep increase of its incidence on EU from 2.6% in 2019

to 4% in 2025. Enterprises will add 3.2 € million data professionals’ positions between 2019 and 2025,

bringing the total to 9.3 € million jobs. However, this will increase the potential data professionals’

skills gap to approximately 759,000 unfilled positions in the EU27, corresponding to 8.2% of total data

skills demand. The lack of skills may become a bottleneck for some enterprises or regions, creating

competition between enterprises for the most skilled professionals. In this scenario, Europe makes

progress in the investment and deployment of independent data infrastructures and digital resources,

also leveraging the new Horizon Europe and Digital Europe Programs. This means Europe reaches a

better, but not quite complete, technological sovereignty. We expect Europe to play a strong role in

shaping global digital governance rules building on GDPR, but without quite dominating AI-led

developments. There is a good chance that Europe will play an important role in defining requirements

for high-risk AI, particularly for training data and human oversight. However, since this will take some

time, it will be difficult to bring under control ex-ante specific applications such as remote biometric

identification (facial recognition) which are already in the market. We foresee a scenario where

Europe will bring ex post some order and respect of ethical principles to applications such as facial

recognition.

The new digital policy strategies will empower Europe to play a stronger role in the global scene,

leveraging the GDPR success as a global standard. Not only Europe, but also many other international

governments are now conscious of the downside and risks of global platforms dominance and control

of global data flows and will work together towards achieving a more balanced playing field. Progress

will be made in terms of fair and effective regulation of competition in the digital economy, digital

finance and consumer empowerment. This scenario therefore is positioned between the two

extremes of high and low concentration of power and data control. The development of an effective

regulatory framework of data governance, as foreseen by the Data strategy, will enhance

stakeholders’ willingness and capability to manage data sharing and improves data access and re-use,

even though the main effects are seen at the end of the forecast period. The single market for data

gradually emerges as fragmentation is overcome, and this enables Europe to attract a growing share

of the global Data Economy, in terms of capability of data processing and management. The

29 May 2020

25

development of common EU data spaces is faster and more successful in some sectors with strong

innovation demand (manufacturing, agriculture) but meets with barriers and low demand in others,

failing to achieve economies of scale.

The rise of the platform economy (collaborative connected, data-centric environments used to

develop multiple innovation) at various levels: global (mega platforms), applications-specific or

industry specific will reshape the competitive environment. European industries will develop industry

platforms to harness multiplied innovation and build ecosystem-based value. For example, by 2025

the majority of manufacturers will use IoT platforms with digital innovation platforms to operate

networks of asset, product, and process digital twins for a 25% reduction in cost of quality. The market

is not yet mature and because of the arising of a new wave of innovation driven by the exploitation of

data by AI and Machine learning technologies, the dominant model is still technology push and so will

be for a few years more.

To enable digital transformation, this scenario is accompanied by the emergence of new work culture

and contracting models to create and manage an agile, borderless and reconfigurable workforce.

Driven by demographic and technology trends, European enterprises multiply the use of "digital co-

workers" (using intelligent process automation and AR/VR to support/complement human workers)

reducing repetitive tasks, improving productivity and security. To achieve this, European organizations

improve their capability to manage, retrain and upskill the workforce but also face problems of

motivation and resistance. A substantial minority of workers however may be unhappy or displaced.

Europe will make progress towards a sustainable Data Economy, with policy initiatives promoting the

ICT and electronic industry full transformation to climate-neutral and energy efficiency practices. In

this scenario we foresee progress towards a Global Digital Cooperation strategy led by the EU and a

more proactive European role in the development and adoption of standards and interoperable

technologies on the global scene, leveraging the power of the single internal market.

29 May 2020

26

Source: EDM Monitoring Tool, IDC 2020

The European Data Market Monitoring Tool – Baseline Scenario 2025 for EU27

29 May 2020

27

4.2 High-Growth Scenario (Pre-Covid)

This scenario foresees a faster growth trajectory of the Data Market and economy, boosted by

favourable economic conditions, by strong investment, proactive policies, and effective collaboration

between the MS at the EU level. By 2025 we expect a higher take-up of multiple technologies than in

the baseline scenario (AI, Big Data, IoT, robotics, 5G, new materials, blockchain…) with European

enterprises fully embracing multiple innovation and the power of data. In this scenario, business

competitiveness is enabled by platforms and ecosystems where innovation and network effects (each

additional user multiplies benefits for all users, increasing the attractiveness of the platform) create a

positive feedback loop, reinforcing the positive impacts. All industries will keep pace, also the public

sector, even though the intensity of data innovation will grow faster in Finance, Manufacturing,

Professional services, ICT and Media. European industries will exploit platforms to combine data with

AI and machine learning, spreading intelligence from the core to the edge of their networks, turning

data into action and action into value. The supply-demand dynamics will become more balanced

between technology-push and demand pull, with a fully developed ecosystem generating positive

feed-back loops between data companies and users. Horizon Europe, Digital Europe and Connecting

Europe Facility programmes deliver a strong boost to European AI research and innovation capabilities

building an ecosystem capable of global leadership. To achieve the benefits of this scenario, Europe

must fully capture the AI opportunity.

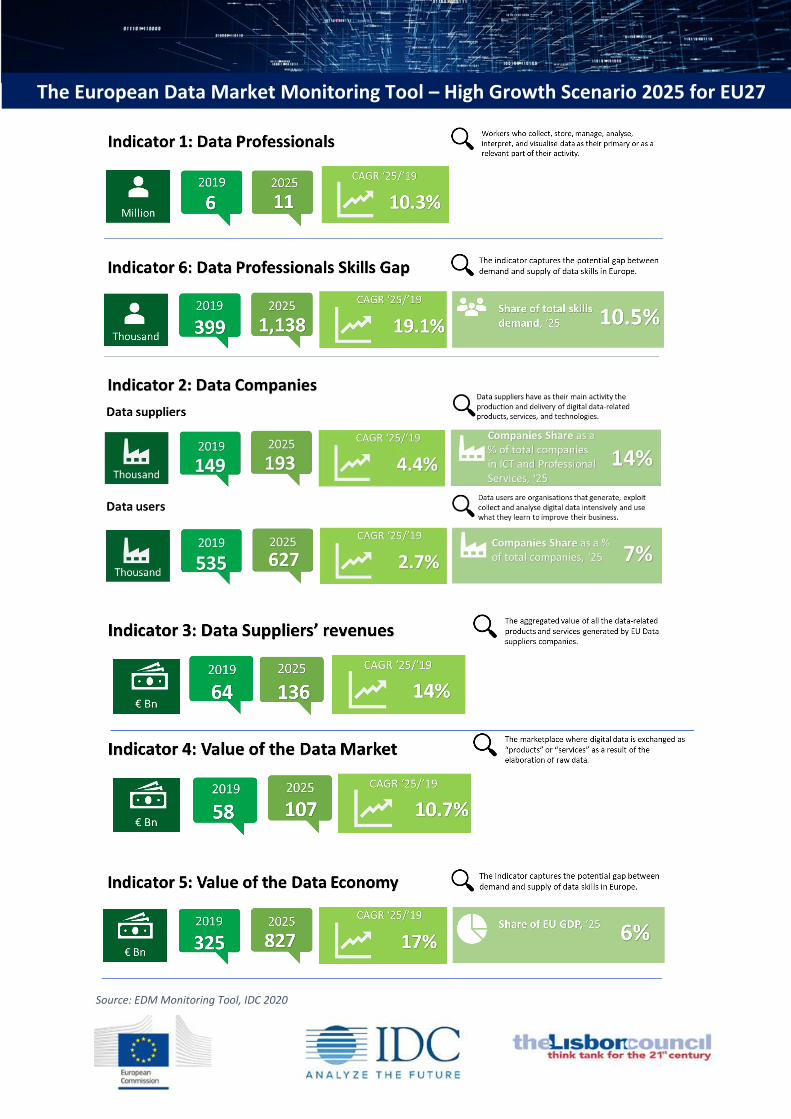

In this scenario, the EU27 GDP compound annual growth rate in the period 2019-2025 (+2.0%) will be

1.5 times higher than in the Challenge scenario and 40% higher than in the Baseline scenario. This will

accelerate the investments in the digital economy and consumer willingness to spend. In the European

Union public and private investments will accelerate in Artificial Intelligence, advanced robotics,

automation as well as new skills. As a result, the Data Market is forecast to reach 107 billion Euro in

the EU27, with a compound annual growth rate of 10.7% between 2019 and 2025. The Data Economy

will grow faster than the Data Market, reaching a value of 827 billion Euro in the EU27, with an

incidence on EU GDP of 5.9%, against the 4.0% of the Baseline scenario. Enterprises will add 4.8 €

million data professionals’ positions between 2019 and 2025 (compared to 3.2 € million in the

previous scenario).

Given the acceleration of technology trends, this scenario foresees a deep transformation of business

processes and the work culture, where change management and HR management become critical

success factors. As in the Baseline scenario, European enterprises multiply the use of "digital co-

workers" (using intelligent process automation and AR/VR to support/complement human workers)

reducing repetitive tasks, improving productivity and security and managing digital transformation.

Besides automation, enterprises engage in "augmentation" of human resources providing

technologies enhancing their physical and intelligence capabilities. Organizations succeed in managing

the transformation of the work culture for digital transformation through a combination of incentives,

intensive training investments, identifying appropriate job roles and tasks in open ecosystems. On the

other hand, initiatives to develop digital skills are successful: the Digital Europe Programmes delivers

a boost to the supply of advanced digital and data skills, the revised Digital Education act helps to

improve digital learning, and the networks of Digital Innovation Hubs play their role in providing

internships, training and experimental spaces for companies to learn about new technologies.

In this scenario, strong investments and MS cooperation help Europe to develop fully independent

data infrastructures and digital resources, to shape global digital governance rules with EU values,

becoming a leader in the Big Data-AI space. As foreseen by the digital and data strategies, Europe

succeeds in achieving technological sovereignty. Europe’s share of the global Data Economy is well on

29 May 2020

28

the way to become equal to its economic weight by 2030 thanks to a successful single market for data.

The new Horizon Europe and Digital Europe Programmes as well as the EU High impact projects

successfully catalyze private investment to develop data sharing and interoperable architectures. The

successful deployment of an EU cloud infrastructure and cloud services marketplace satisfies industry

and SMEs needs. The successful development of common EU data spaces in most sectors achieves

economies of scale and supports the rise of the platform economy, enabling companies to deal with

multiple innovation.

By developing a flexible legislation based on the risk management principle, but not hindering

technology progress. Europe becomes a successful global leader of trustworthy AI governance.

However, since this will take some time, it will be difficult to bring under control ex-ante specific

applications such as remote biometric identification (facial recognition) which are already in the

market. We foresee a scenario where Europe will bring ex post some order and respect of ethical

principles to applications such as facial recognition. Fast progress with a new Data Act, Digital Services

and Competition framework enhance data access, sharing and re-use, achieve fair playing field and

build the basis for the effective single market for data.

29 May 2020

29

Source: EDM Monitoring Tool, IDC 2020

The European Data Market Monitoring Tool – High Growth Scenario 2025 for EU27

29 May 2020

30

4.3 Challenge Scenario (Pre-Covid)

In the Challenge scenario, a combination of economic, social and technology threats overcome

European innovation forces, which become lost in a maze of barriers, resulting in much slower Data

Market and Data Economy growth. This scenario examines the main fault points and critical issues

which may drag down Europe’s potential for innovation and growth, to be able to anticipate and fight

them.

The first threat is lower GDP growth, estimated at a compound annual growth rate in the period 2019-

2025 of 1%, substantially lower than in the other scenarios. Trade wars, political conflicts, and

unexpected events such as the Coronavirus pandemic are the main drivers of this growth slow-down.

Lower GDP growth means lower overall investments and consumers’ willingness to spend. Even

though research and innovation investments are partially countercyclical and in a low-interest rate

world, so that public investments are easier to make, in this scenario governments have many other

demands on their budgets and private enterprises have less resources. So, investments inevitably slow

down.

The second main threat is if the digital Europe and data strategies are not implemented successfully

and fail to achieve many of their objectives. This may happen if a combination of insufficient

investments and lack of collaboration at EU level lead to an uneven development of data

infrastructures and digital resources. Without an effective data governance framework and incentives

for stakeholders to increase data sharing, there is a risk that the Data Market will remain fragmented.

Europe fails to achieve technological sovereignty and the lack of widespread European cloud

infrastructures and services results in dependency of EU industries, particularly SMEs, on global

platforms, with the risk to have low control of European datasets. In this scenario it is possible that,

notwithstanding the GDPR, many Europeans have no visibility and very little control on the use of their

personal data: this hinders the willingness to share and reuse personal and non- personal data for

social good. If the development of common data spaces is slow and does not deliver the expected

boost to industries across Europe, this may hinder the rise of the platform economy, miss the

development of economies of scale and reduce the incentives to fight market fragmentation for

innovative services.

In this context and missing public support, European enterprises struggle to manage multiple

innovation and adapt to the platform economy, losing competitiveness in the global market.

Guidelines and data ethics principles multiply, but European enterprises struggle to develop skills and

capability to manage risks and in many cases refrain from data-driven innovation for fear of business

risks. Insufficient interoperability and standardization hinder collaboration and innovation. European

organizations struggle to adapt to the new work environment and to motivate the workforce.

Fragmented ecosystems and insufficient investments in re-training and re-skilling increase the skills

gap and slow down digital transformation, while leaving many workers unhappy or displaced.

Technology-driven automation and augmentation are badly managed and create a negative reaction

by the human workforce slowing down acceptance and digital transformation.

This scenario foresees a negative self-reinforcing circle, where less positive global economic conditions

discourage investments and weaken global demand with a negative impact on European growth. A

slower pace of digital innovation deprives the economy of the boost to growth potentially given by

data-driven services and products, while enterprises find competing in international markets more

difficult.

29 May 2020

31

As a result, in this scenario the Data Market is forecast to reach 72 billion Euro in the EU27 with a

compound annual growth rate of 3.7% between 2019 and 2025. In the same context, the Data

Economy will reach a value of 432 billion Euro in the EU27 with an incidence on GDP of 3.3%, compared

to 4% in the Baseline scenario 2025.

The number of data professionals will still increase to 8.4 € million in the EU27 by 2025, adding 2.4 €

million data professionals’ positions in the period 2019-2025. We estimate a potential data skills gap