Monthly Outlook - CIBCWM.comresearch.cibcwm.com/economic_public/download/dec06.pdf · Monthly...

22

European Economic Research CIBC World Markets PLC London, England SE1 2QL Tel: +44 207 234-6000 Fax: +44 207 234-6234 www.cibcwm.com Monthly Outlook The securities mentioned in this report are speculative in nature and involve risk to principal and interest payments. This document and the recommendations included herein are for informational purposes only and intended for distribution solely to Qualified Institutional Buyers under Rule 144A. CIBC World Markets Corp. 425 Lexington Avenue, New York, NY 10017. Tel: +1 (212) 885-4646, Fax: +1 (212) 885-4936. December 2006 Audrey Childe-Freeman Senior European Economist +44 207 234-6666 [email protected]k Jodie Saul European Economist +44 207 234-7325 [email protected] € £ £

Transcript of Monthly Outlook - CIBCWM.comresearch.cibcwm.com/economic_public/download/dec06.pdf · Monthly...

European Economic Research CIBC World Markets PLC London, England SE1 2QL

Tel: +44 207 234-6000 Fax: +44 207 234-6234 www.cibcwm.com

Monthly Outlook

The securities mentioned in this report are speculative in nature and involve risk to principal and interest payments. This document and the recommendations included herein are for informational purposes only and intended for distribution solely to Qualified Institutional Buyers under Rule 144A.

CIBC World Markets Corp. 425 Lexington Avenue, New York, NY 10017. Tel: +1 (212) 885-4646, Fax: +1 (212) 885-4936.

December 2006

Audrey Childe-FreemanSenior European Economist

+44 207 [email protected]

Jodie SaulEuropean Economist

+44 207 [email protected]

€

£

£

European Economic Research Monthly Outlook

2 December 2006

Blank Inside Cover

European Economic Research Monthly Outlook

December 2006 3

Table of Contents

European Economic Research Monthly Outlook 4

Quote of the Month 4

An outperforming Eurozone Economy… 5

Conclusion 6

Monthly Indicators 7

Eurozone 7

United Kingdom 9

Recent Monetary Policy History 11

Central Bank Watch 12

Key Official Central Bank Rates 12

Monetary Policy Outlook 13

European Central Bank 13

Bank of England 14

Interest Rates & Currency Forecasts 15

Market Outlook 16

Eurozone 16

United Kingdom 16

Technical Update 17

European Economic Research Monthly Outlook

4 December 2006

European Economic Research Monthly Outlook

It is still all good news from the Eurozone economy at this stage of the cycle, with Germany’s IFO index beating expectations and climbing to a new 15 year high in November, all boding well for a strong Euro Q4 GDP growth performance. A stronger euro is not too much of an issue, for now anyway.

The weaker oil price environment has contributed to keeping the Eurozone headline HICP below target for the third consecutive month in November (at +1.8%) but an upward bias persists: we still expect headline inflation back above the 2% mark next year.

A continuation in the rate normalisation process is a “fait accomplit” at this month’s ECB Governing Council Meeting and expect the monetary authorities to keep all options open for 2007, despite the recent euro appreciation.

It is the same old story from the UK economy at this stage of the cycle, with a buoyant housing sector continuing to make the headlines but the retail and manufacturing sectors failing to impress and an unemployment that is still on the rise.

Little news on the inflation front, with a CPI y/y rate unchanged (at +2.4%) but the latest easing in average earnings will come as a relief to inflation hawks on the MPC.

After having just hiked interest rates by 25bp at the November MPC Meeting, we expect the BoE to wait and see in December. The medium term monetary policy outlook remains relatively open but we remain of the view that the case for further BoE rate hikes will become less and less convincing into 2007.

Quote of the Month

“I am not concerned” (about the strength of the euro)

ECB’s Wellink, 28th November 2006

European Economic Research Monthly Outlook

December 2006 5

Monthly Issue

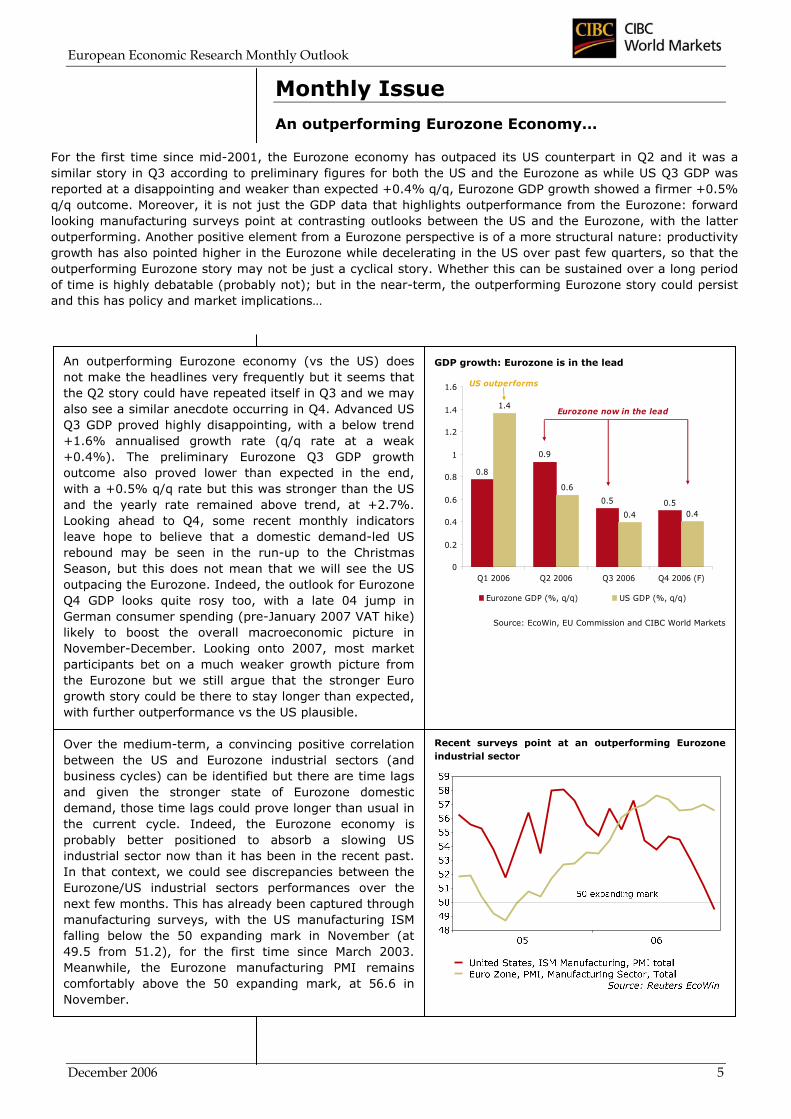

An outperforming Eurozone Economy…

GDP growth: Eurozone is in the lead

0.8

0.9

0.5 0.5

1.4

0.6

0.4 0.4

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Q1 2006 Q2 2006 Q3 2006 Q4 2006 (F)

Eurozone GDP (%, q/q) US GDP (%, q/q)

Eurozone now in the lead

US outperforms

Source: EcoWin, EU Commission and CIBC World Markets

Recent surveys point at an outperforming Eurozone industrial sector

An outperforming Eurozone economy (vs the US) does not make the headlines very frequently but it seems that the Q2 story could have repeated itself in Q3 and we may also see a similar anecdote occurring in Q4. Advanced US Q3 GDP proved highly disappointing, with a below trend +1.6% annualised growth rate (q/q rate at a weak +0.4%). The preliminary Eurozone Q3 GDP growth outcome also proved lower than expected in the end, with a +0.5% q/q rate but this was stronger than the US and the yearly rate remained above trend, at +2.7%. Looking ahead to Q4, some recent monthly indicators leave hope to believe that a domestic demand-led US rebound may be seen in the run-up to the Christmas Season, but this does not mean that we will see the US outpacing the Eurozone. Indeed, the outlook for Eurozone Q4 GDP looks quite rosy too, with a late 04 jump in German consumer spending (pre-January 2007 VAT hike) likely to boost the overall macroeconomic picture in November-December. Looking onto 2007, most market participants bet on a much weaker growth picture from the Eurozone but we still argue that the stronger Euro growth story could be there to stay longer than expected, with further outperformance vs the US plausible.

Over the medium-term, a convincing positive correlation between the US and Eurozone industrial sectors (and business cycles) can be identified but there are time lags and given the stronger state of Eurozone domestic demand, those time lags could prove longer than usual in the current cycle. Indeed, the Eurozone economy is probably better positioned to absorb a slowing US industrial sector now than it has been in the recent past. In that context, we could see discrepancies between the Eurozone/US industrial sectors performances over the next few months. This has already been captured through manufacturing surveys, with the US manufacturing ISM falling below the 50 expanding mark in November (at 49.5 from 51.2), for the first time since March 2003. Meanwhile, the Eurozone manufacturing PMI remains comfortably above the 50 expanding mark, at 56.6 in November.

For the first time since mid-2001, the Eurozone economy has outpaced its US counterpart in Q2 and it was a similar story in Q3 according to preliminary figures for both the US and the Eurozone as while US Q3 GDP was reported at a disappointing and weaker than expected +0.4% q/q, Eurozone GDP growth showed a firmer +0.5% q/q outcome. Moreover, it is not just the GDP data that highlights outperformance from the Eurozone: forward looking manufacturing surveys point at contrasting outlooks between the US and the Eurozone, with the latter outperforming. Another positive element from a Eurozone perspective is of a more structural nature: productivity growth has also pointed higher in the Eurozone while decelerating in the US over past few quarters, so that the outperforming Eurozone story may not be just a cyclical story. Whether this can be sustained over a long period of time is highly debatable (probably not); but in the near-term, the outperforming Eurozone story could persist and this has policy and market implications…

European Economic Research Monthly Outlook

6 December 2006

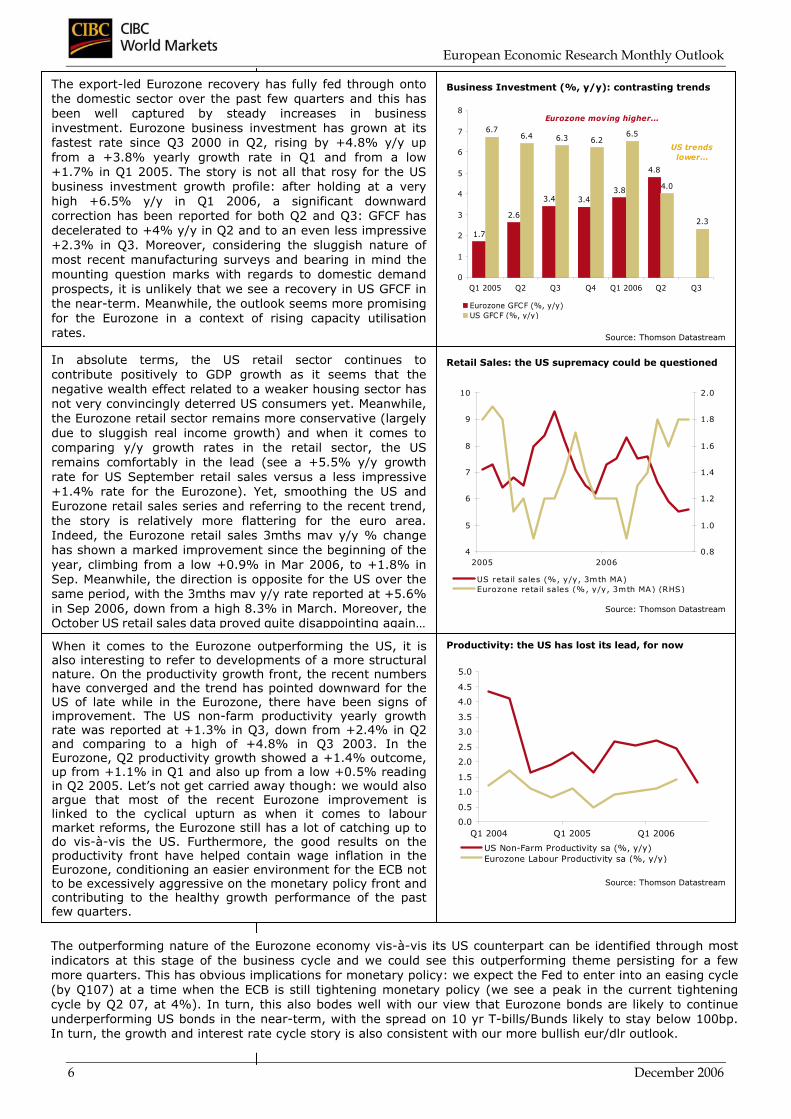

Retail Sales: the US supremacy could be questioned

4

5

6

7

8

9

10

2005 20060.8

1.0

1.2

1.4

1.6

1.8

2.0

US retail sales (%, y/y, 3mth MA)Eurozone retail sales (%, y/y, 3mth MA) (RHS)

Source: Thomson Datastream

Productivity: the US has lost its lead, for now

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q1 2004 Q1 2005 Q1 2006

US Non-Farm Productivity sa (%, y/y)Eurozone Labour Productivity sa (%, y/y)

Source: Thomson Datastream

In absolute terms, the US retail sector continues to contribute positively to GDP growth as it seems that the negative wealth effect related to a weaker housing sector has not very convincingly deterred US consumers yet. Meanwhile, the Eurozone retail sector remains more conservative (largely due to sluggish real income growth) and when it comes to comparing y/y growth rates in the retail sector, the US remains comfortably in the lead (see a +5.5% y/y growth rate for US September retail sales versus a less impressive +1.4% rate for the Eurozone). Yet, smoothing the US and Eurozone retail sales series and referring to the recent trend, the story is relatively more flattering for the euro area. Indeed, the Eurozone retail sales 3mths mav y/y % change has shown a marked improvement since the beginning of the year, climbing from a low +0.9% in Mar 2006, to +1.8% in Sep. Meanwhile, the direction is opposite for the US over the same period, with the 3mths mav y/y rate reported at +5.6% in Sep 2006, down from a high 8.3% in March. Moreover, the October US retail sales data proved quite disappointing again…

When it comes to the Eurozone outperforming the US, it is also interesting to refer to developments of a more structural nature. On the productivity growth front, the recent numbers have converged and the trend has pointed downward for the US of late while in the Eurozone, there have been signs of improvement. The US non-farm productivity yearly growth rate was reported at +1.3% in Q3, down from +2.4% in Q2 and comparing to a high of +4.8% in Q3 2003. In the Eurozone, Q2 productivity growth showed a +1.4% outcome, up from +1.1% in Q1 and also up from a low +0.5% reading in Q2 2005. Let’s not get carried away though: we would also argue that most of the recent Eurozone improvement is linked to the cyclical upturn as when it comes to labour market reforms, the Eurozone still has a lot of catching up to do vis-à-vis the US. Furthermore, the good results on the productivity front have helped contain wage inflation in the Eurozone, conditioning an easier environment for the ECB not to be excessively aggressive on the monetary policy front and contributing to the healthy growth performance of the past few quarters.

The outperforming nature of the Eurozone economy vis-à-vis its US counterpart can be identified through most indicators at this stage of the business cycle and we could see this outperforming theme persisting for a few more quarters. This has obvious implications for monetary policy: we expect the Fed to enter into an easing cycle (by Q107) at a time when the ECB is still tightening monetary policy (we see a peak in the current tightening cycle by Q2 07, at 4%). In turn, this also bodes well with our view that Eurozone bonds are likely to continue underperforming US bonds in the near-term, with the spread on 10 yr T-bills/Bunds likely to stay below 100bp. In turn, the growth and interest rate cycle story is also consistent with our more bullish eur/dlr outlook.

The export-led Eurozone recovery has fully fed through onto the domestic sector over the past few quarters and this has been well captured by steady increases in business investment. Eurozone business investment has grown at its fastest rate since Q3 2000 in Q2, rising by +4.8% y/y up from a +3.8% yearly growth rate in Q1 and from a low +1.7% in Q1 2005. The story is not all that rosy for the US business investment growth profile: after holding at a very high +6.5% y/y in Q1 2006, a significant downward correction has been reported for both Q2 and Q3: GFCF has decelerated to +4% y/y in Q2 and to an even less impressive +2.3% in Q3. Moreover, considering the sluggish nature of most recent manufacturing surveys and bearing in mind the mounting question marks with regards to domestic demand prospects, it is unlikely that we see a recovery in US GFCF in the near-term. Meanwhile, the outlook seems more promising for the Eurozone in a context of rising capacity utilisation rates.

Business Investment (%, y/y): contrasting trends

1.7

2.6

3.4 3.43.8

4.8

6.76.4 6.3 6.2

6.5

4.0

2.3

0

1

2

3

4

5

6

7

8

Q1 2005 Q2 Q3 Q4 Q1 2006 Q2 Q3

Eurozone GFCF (%, y/y)US GFCF (%, y/y)

Eurozone moving higher...

US trends lower...

Source: Thomson Datastream

European Economic Research Monthly Outlook

December 2006 7

Monthly Indicators

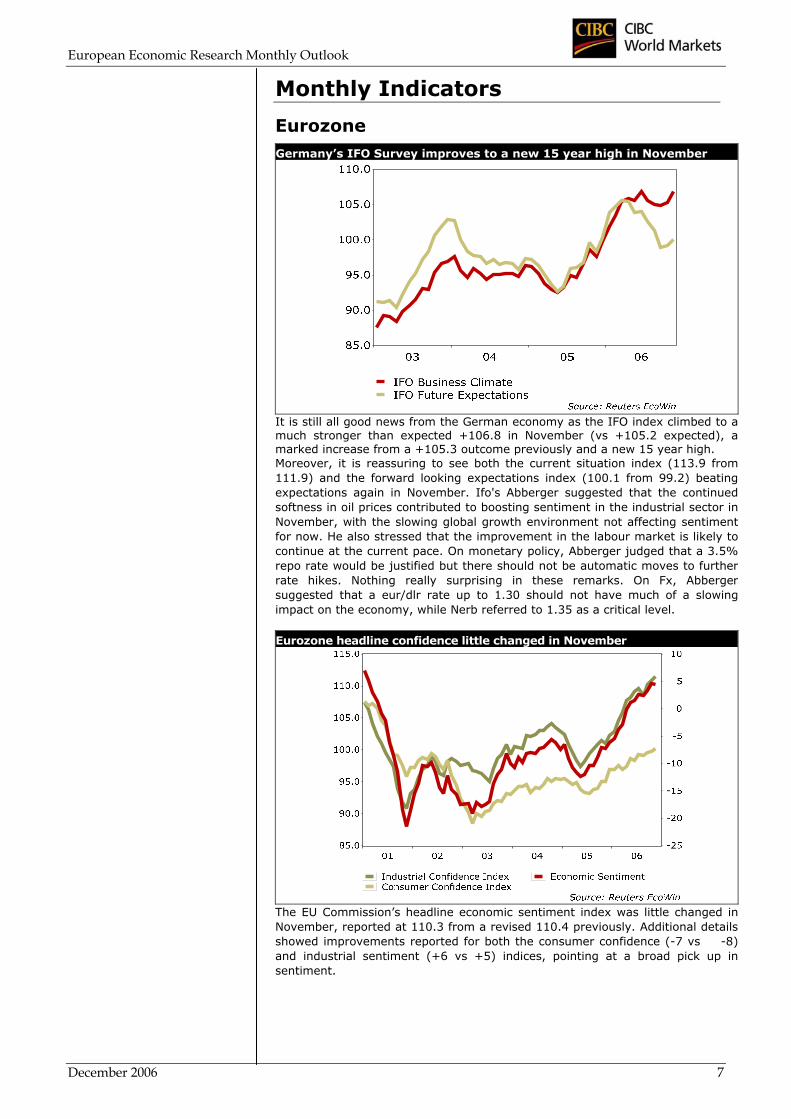

Eurozone Germany’s IFO Survey improves to a new 15 year high in November

It is still all good news from the German economy as the IFO index climbed to amuch stronger than expected +106.8 in November (vs +105.2 expected), amarked increase from a +105.3 outcome previously and a new 15 year high. Moreover, it is reassuring to see both the current situation index (113.9 from111.9) and the forward looking expectations index (100.1 from 99.2) beatingexpectations again in November. Ifo's Abberger suggested that the continuedsoftness in oil prices contributed to boosting sentiment in the industrial sector inNovember, with the slowing global growth environment not affecting sentimentfor now. He also stressed that the improvement in the labour market is likely tocontinue at the current pace. On monetary policy, Abberger judged that a 3.5%repo rate would be justified but there should not be automatic moves to furtherrate hikes. Nothing really surprising in these remarks. On Fx, Abbergersuggested that a eur/dlr rate up to 1.30 should not have much of a slowingimpact on the economy, while Nerb referred to 1.35 as a critical level.

Eurozone headline confidence little changed in November

The EU Commission’s headline economic sentiment index was little changed inNovember, reported at 110.3 from a revised 110.4 previously. Additional detailsshowed improvements reported for both the consumer confidence (-7 vs -8)and industrial sentiment (+6 vs +5) indices, pointing at a broad pick up insentiment.

European Economic Research Monthly Outlook

8 December 2006

Monthly Indicators Eurozone Eurozone HICP Yearly Rate below the ECB’s 2% ceiling, again

The softer oil price environment helped sustain a sub 2% reading on Eurozoneheadline inflation in October for the second month in a row. Consumer priceswere 0.1% higher on the month, corresponding to a yearly rate at 1.6%(unchanged from the first estimate) vs 1.7% in September. Core inflation wasreported at 1.5%, the same outcome as in September. The data breakdown showed monthly rises in the prices of clothing (+2.9%),household equipment (+0.2%), health (+0.1%), education (+1.1%) andhousing (+0.1%). Energy prices were 1.8% lower in October, while transportprices were off by 1.1%. Lower oil prices may have helped headline inflation ease in recent months, butsub 2% readings are likely to prove unsustainable; this report does not alterthe near term monetary policy outlook at the ECB. Eurozone Money Supply (M3 Yearly & 3 Months Average, %)

M3 monetary growth in the Eurozone expanded at a slightly slower thanexpected 8.5% y/y in October (vs 8.7% expected), the same outcome asSeptember, but obviously still significantly higher than the ECB's 4.5%reference value. That took the three month moving average to 8.4% from8.2% previously. Additional details showed still strong annual growth of loans to the privatesector (+11.2% from +11.4%), while private credit growth was reported at12% y/y. The strength of the housing market was highlighted by double digitgrowth in loans for home purchases (+10.4%). Headline M3 money supply may have been unchanged but the three month MAedged higher and both remain significantly above the ECB's non-inflationaryreference value - hence the ECB will be keeping a close eye on liquidity levelsin the Eurozone.

European Economic Research Monthly Outlook

December 2006 9

Monthly Indicators United Kingdom Industrial & Manufacturing Output (Yearly % Change)

Industrial production rose by a softer than expected 0.2% in September andcame after the August reading was revised lower to unchanged vs +0.1%,with the y/y rate at 0.5% from 0.6%. Manufacturing output did not fair anybetter, posting an unchanged outcome, its weakest reading since April, afterthe 0.3% rise previously, but the y/y rate rose to its highest level since June2004, to 2% from 1.4%. The quarterly rate of industrial output was reportedat +0.1% vs -0.1% and manufacturing output expanded at +0.6% on thequarter, the same outcome as previously. Additional details showed oil and gas extraction rising by 3.1% in Septemberfrom -2.1% in August, while utilities output remained in the red, at -0.3%from -0.7%. All in all, this report confirms that the manufacturing sector remains sluggishand still the weakest link for the UK economy. Unemployment & Average Earnings

Further soft news emerged from the UK labour market in October: risingunemployment and softening earnings growth. Indeed, the number ofunemployed rose by 1,200 in October (not quite as bad as the expected 5krise) and coming after the 8.3k rise in September, leaving the unemploymentrate unchanged at 3%. On an ILO basis, the number of unemployed rose by27k in the three months to September, with that unemployment rate rising toits highest level since March-May 2000, to 5.6%. On the earnings front, there was little inflation concern in September, withheadline average earnings softening to a weaker than expected 3.9% from4.2% previously, the weakest reading since January. The ex bonus rate alsosoftened, to 3.5% from 3.6%. So a soft UK labour market was confirmed in October: unemployment remainson the rise and the softer earnings growth reinforces our view that underlyingwage growth remains under control in the UK.

European Economic Research Monthly Outlook

10 December 2006

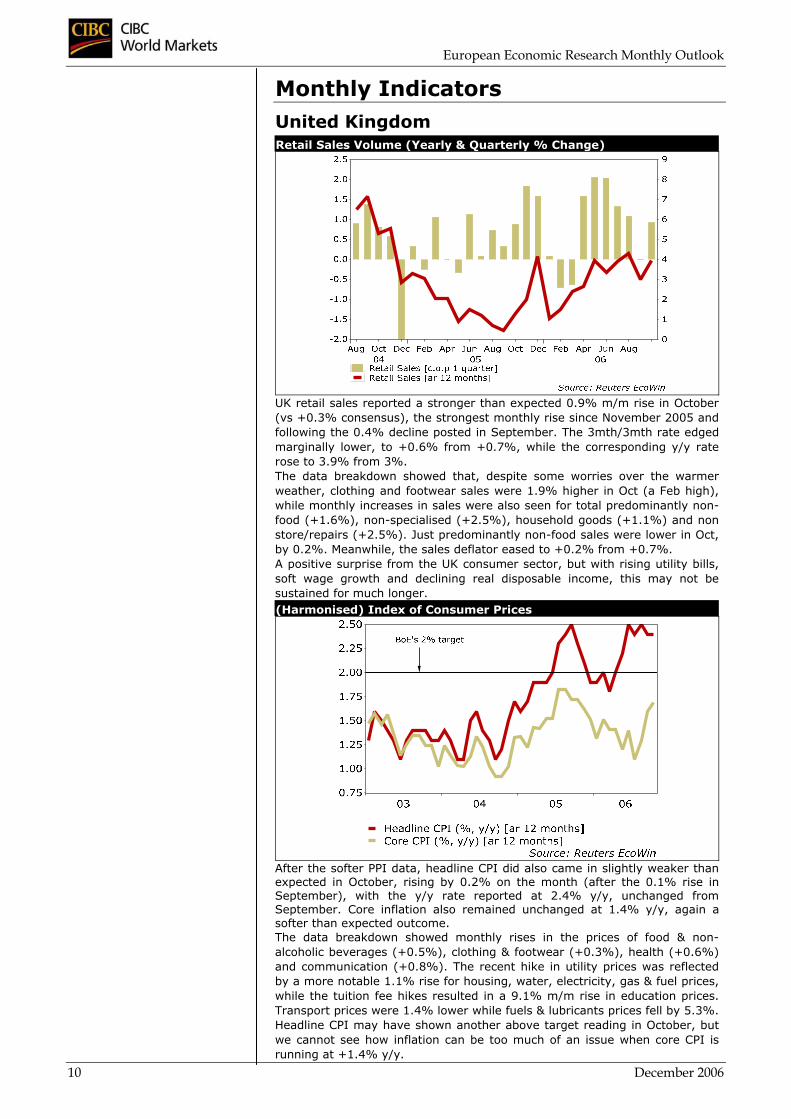

Monthly Indicators United Kingdom Retail Sales Volume (Yearly & Quarterly % Change)

UK retail sales reported a stronger than expected 0.9% m/m rise in October(vs +0.3% consensus), the strongest monthly rise since November 2005 andfollowing the 0.4% decline posted in September. The 3mth/3mth rate edgedmarginally lower, to +0.6% from +0.7%, while the corresponding y/y raterose to 3.9% from 3%. The data breakdown showed that, despite some worries over the warmerweather, clothing and footwear sales were 1.9% higher in Oct (a Feb high),while monthly increases in sales were also seen for total predominantly non-food (+1.6%), non-specialised (+2.5%), household goods (+1.1%) and nonstore/repairs (+2.5%). Just predominantly non-food sales were lower in Oct,by 0.2%. Meanwhile, the sales deflator eased to +0.2% from +0.7%. A positive surprise from the UK consumer sector, but with rising utility bills,soft wage growth and declining real disposable income, this may not besustained for much longer. (Harmonised) Index of Consumer Prices

After the softer PPI data, headline CPI did also came in slightly weaker thanexpected in October, rising by 0.2% on the month (after the 0.1% rise inSeptember), with the y/y rate reported at 2.4% y/y, unchanged fromSeptember. Core inflation also remained unchanged at 1.4% y/y, again asofter than expected outcome. The data breakdown showed monthly rises in the prices of food & non-alcoholic beverages (+0.5%), clothing & footwear (+0.3%), health (+0.6%)and communication (+0.8%). The recent hike in utility prices was reflectedby a more notable 1.1% rise for housing, water, electricity, gas & fuel prices,while the tuition fee hikes resulted in a 9.1% m/m rise in education prices.Transport prices were 1.4% lower while fuels & lubricants prices fell by 5.3%.Headline CPI may have shown another above target reading in October, butwe cannot see how inflation can be too much of an issue when core CPI isrunning at +1.4% y/y.

European Economic Research Monthly Outlook

December 2006 11

Recent Monetary Policy History United States: Fed Funds Rate & S&P 500

Eurozone: Repo Rate & Dax Index

United Kingdom: FTSE 100 & Base Rates

European Economic Research Monthly Outlook

12 December 2006

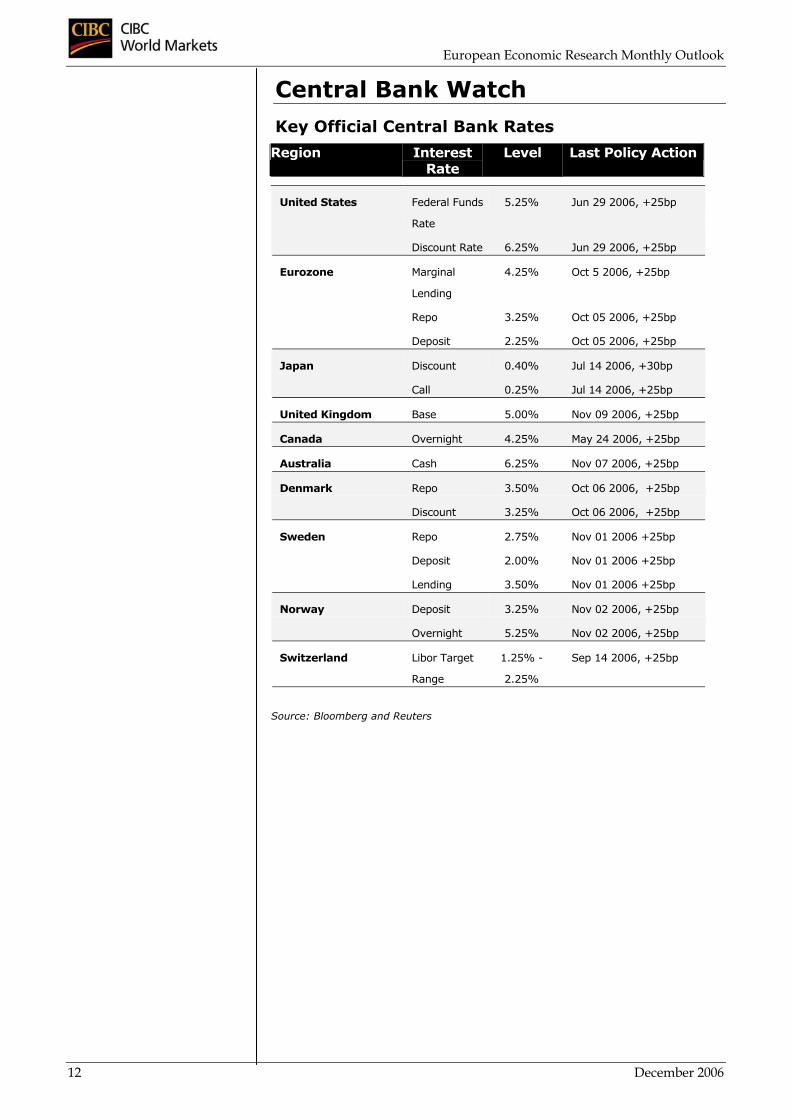

Central Bank Watch

Key Official Central Bank Rates

Region Interest Rate

Level Last Policy Action

United States Federal Funds

Rate

5.25% Jun 29 2006, +25bp

Discount Rate 6.25% Jun 29 2006, +25bp

Eurozone Marginal

Lending

4.25% Oct 5 2006, +25bp

Repo 3.25% Oct 05 2006, +25bp

Deposit 2.25% Oct 05 2006, +25bp

Japan Discount 0.40% Jul 14 2006, +30bp

Call 0.25% Jul 14 2006, +25bp

United Kingdom Base 5.00% Nov 09 2006, +25bp

Canada Overnight 4.25% May 24 2006, +25bp

Australia Cash 6.25% Nov 07 2006, +25bp

Denmark Repo 3.50% Oct 06 2006, +25bp

Discount 3.25% Oct 06 2006, +25bp

Sweden Repo 2.75% Nov 01 2006 +25bp

Deposit 2.00% Nov 01 2006 +25bp

Lending 3.50% Nov 01 2006 +25bp

Norway Deposit 3.25% Nov 02 2006, +25bp

Overnight 5.25% Nov 02 2006, +25bp

Switzerland Libor Target

Range

1.25% -

2.25%

Sep 14 2006, +25bp

Source: Bloomberg and Reuters

European Economic Research Monthly Outlook

December 2006 13

Monetary Policy Outlook

European Central Bank European Central Bank Latest Macroeconomic Projections (Sep 2006) (Average Annual % Change)* 2006 2007 Real GDP +2.2% - +2.8% +1.6% - +2.6%HICP * +2.3% - +2.5% +1.9% - +2.9% Source: European Central Bank * Harmonised Index of Consumer Prices. For each variable and horizon, ranges are based on the average absolute difference between the actual outcome and past projections by euro central banks.

Monthly Economic Report The ECB’s November economic bulletin stated that, “the information that had become available since the Governing Council’s decision of 5 October to increase interest rates…confirmed that strong vigilance remains of the essence so as to ensure that medium to longer-term inflation expectations in the euro area remain solidly anchored at levels consistent with price stability”. Additionally, and rather importantly, “if the Governing Council’s assumptions and baseline scenario continue to be confirmed, it will remain warranted to further withdraw monetary accommodation”. As for growth, the report states that, “the conditions remain in place for the euro area economy to grow at solid rates around potential, although some volatility in the quarterly growth rates is likely to emerge”. The risks to the growth outlook are said to be “broadly balanced over the shorter term” and “continue to lie to the downside” over the longer term. With regards to inflation, the ECB expects “a high degree of volatility in the annual HICP inflation rate”, but looking through this volatility, “HICP inflation will remain elevated at a level above 2% on average in 2006 and is likely to remain so in 2007”. The risks to the outlook for price stability remain “clearly on the upside”. In summing up, the ECB states that, “annual inflation rates are projected to remain elevated in 2006 and 2007, with risks to this outlook remaining clearly on the upside…If the Governing Council’s assumptions and baseline scenario continue to be confirmed, it will remain warranted to further withdraw monetary accommodation. Acting in a firm and timely manner remains essential to ensuring price stability over the medium term. The Governing Council will therefore exercise strong vigilance”.

Near-Term Monetary Policy Outlook Coming Interest Rate Announcement: December 7th We expect the ECB to hike its main marginal lending, repo and deposit rates by 25bp at the December Governing Council Meeting, to 4.50%, 3.50% and 2.50% respectively. This would take the cumulative rate rises to 150bp since the beginning of the rate normalisation process (last December) and we expect a further 50bp rate rises early next year, with a repo rate likely to peak at 4%. A 25bp rate rise could prove to be a bit of a non-event for the market as ECB’s officials have clearly flagged at an imminent policy action at the November post Meeting press conference, switching from a ‘close monitoring’ to a ‘strongly vigilant’ approach with regards to upside inflation risks. The strength observed in a majority of recent Euro indicators would also have strengthened the ECB hawks’ case. In particular, the German IFO index – which is a highly reliable indicator when it comes to predicting growth in Euroland – has surprised to the upside again in November, with a main index at a 15 year high. The sharp decline in Germany’s November unemployment was also very good news and pointed at a likely rebound in GDP growth in Q4 after the softer performance observed in Q3. As for inflation, there has not been anything unexpected of late: November CPI was reported below the 2% ceiling for the third consecutive month but this is unlikely to prove sustained into 2007. Supposedly, since the November Meeting, the key news for the ECB to digest has been a stronger Euro: the euro has appreciated by roughly 4% against the dollar and by about 2% on a trade weighted index basis since November. This is a tightening of monetary policy, but the Eurozone economy is in a much better position to absorb a stronger euro now than it was in December 2004: concluding that a higher euro means that the ECB will not hike rates could prove misjudged and the recent verbal intervention from some EU officials is unlikely to have much impact. The ECB’s tolerance level is likely to be much higher in terms of euro actual levels, yet the ECB may reiterate that ‘excess Fx moves are unwelcome’…

We expect the ECB to hike its main marginal lending, repo and deposit rates by 25bp at the December Governing Council Meeting, to 4.50%, 3.50% and 2.50% respect-tively...and we expect a further 50bp rate rises early next year, with a repo rate likely to peak at 4%.

A 25bp rate rise could prove to be a bit of a non-event for the market.

…the key news for the ECB to digest has been a stronger Euro…

…but the Eurozone economy is in a much better position to absorb a stronger euro now than it was in December 2004

European Economic Research Monthly Outlook

14 December 2006

Monetary Policy Outlook

Bank of England Bank of England Monetary Policy Committee Members’ Recent Voting Records Nov 2006 Oct 2006 Sep 2006 Aug 2006

King +25bp Unch Unch +25bp

Lomax Unch Unch Unch +25bp

Bean +25bp Unch Unch +25bp

Tucker +25bp Unch Unch +25bp

Barker +25bp Unch Unch +25bp

Gieve +25bp Unch Unch +25bp

Blanchflower Unch Unch Unch Unch

Besley +25bp +25bp Unch n/a

Sentance +25bp +25bp n/a n/a Source: CIBC World Markets plc

Focus on the Latest MPC Meeting Minutes As we suspected, the Bank of England’s decision to hike interest rates by 25bp, to 5%, at the November MPC meeting was not taken unanimously, however, the surprise effect came from dove Blanchflower being joined by Deputy Governor Lomax in the no change camp. The doves presented their case for voting for unchanged rates: the current spike in inflation was mainly related to large gas and electricity price increases, so once their immediate impact had dissipated, CPI inflation was likely to fall back sharply next year; meanwhile the August rate rise had not yet fully been felt and the downside risks from the world, especially the US, were greater than implied by the Inflation Report. For the majority of the Committee, the balance of risks suggested that CPI inflation would exceed the 2% target in the medium term if the Bank rate was maintained at 4.75% - hence an immediate increase of 25bp was necessary to return inflation to target. The factors posing upside risks to inflation were cited as the risk that employees would seek to negotiate higher wages in order to resist the erosion of their purchasing power; the prospect for further strength in nominal domestic demand and also the risk that if inflation continued above target for much longer, that might come to be reflected in inflation expectations.

Near-Term Monetary Policy Outlook After the 25bp November rate hike, we expect the BoE to maintain its repo rate unchanged (at 5%) at the December MPC Meeting. While a no-change monetary policy outcome is a done deal this month, the near-term monetary policy outlook remains uncertain. Indeed, we are still of the view that the BoE will not have to raise interest rates again early next year but this is far from being a unanimous view in the market and we also acknowledge that the BoE’s recent policy language does not totally rule out future rate hikes. Referring to recent MPC members’ remarks, the January pay rounds will prove crucial in determining whether another interest rate hike is on the agenda. At a time when unemployment is clearly on the rise (UK ILO unemployment rate is at a 6½ year high) and considering a rising labour force, we identify limited upward pressure on underlying wage growth going forward. Headline average earnings may jump as record high city bonuses feed through in Q107 while ex-bonus average earnings should remain well behaved. There are varying levels of hawkishness within the MPC at present but we’d expect this month’s decision to leave rates on hold to be taken unanimously. Indeed, recent economic indicators have shown no pressing need for the MPC to pull the trigger on interest rates again. On the domestic front, recent data have failed to impress. The hawks on the MPC may mention continued strength in the housing sector as a continued source for concern but a tighter monetary policy environment may not do much to ease house price inflation as this as much of a supply than a demand problem. Internationally, it has been a mixed bag: a weaker than expected performance from the US but a Eurozone economy that continues to surprise to the upside. As for the recent Cable rally, it is a touch premature to conclude on implications for monetary policy but if sustained, a stronger pound should reinforce the doves’ case going forward. In that context, a wait and see approach to monetary policy is most appropriate at the December MPC Meeting. Thereafter, the debate remains relatively open….

After the 25bp November rate hike, we expect the BoE to maintain its repo rate unchanged (at 5%) at the December MPC Meeting. While a no-change monetary policy outcome is a done deal this month, the near-term monetary policy outlook remains uncertain. Referring to recent MPC members’ remarks, the January pay rounds will prove crucial in determining whether another interest rate hike is on the agenda. …we’d expect this month’s decision to leave rates on hold to be taken unanimously. Indeed, recent economic indicators have shown no pressing need for the MPC to pull the trigger on interest rates again.

European Economic Research Monthly Outlook

December 2006 15

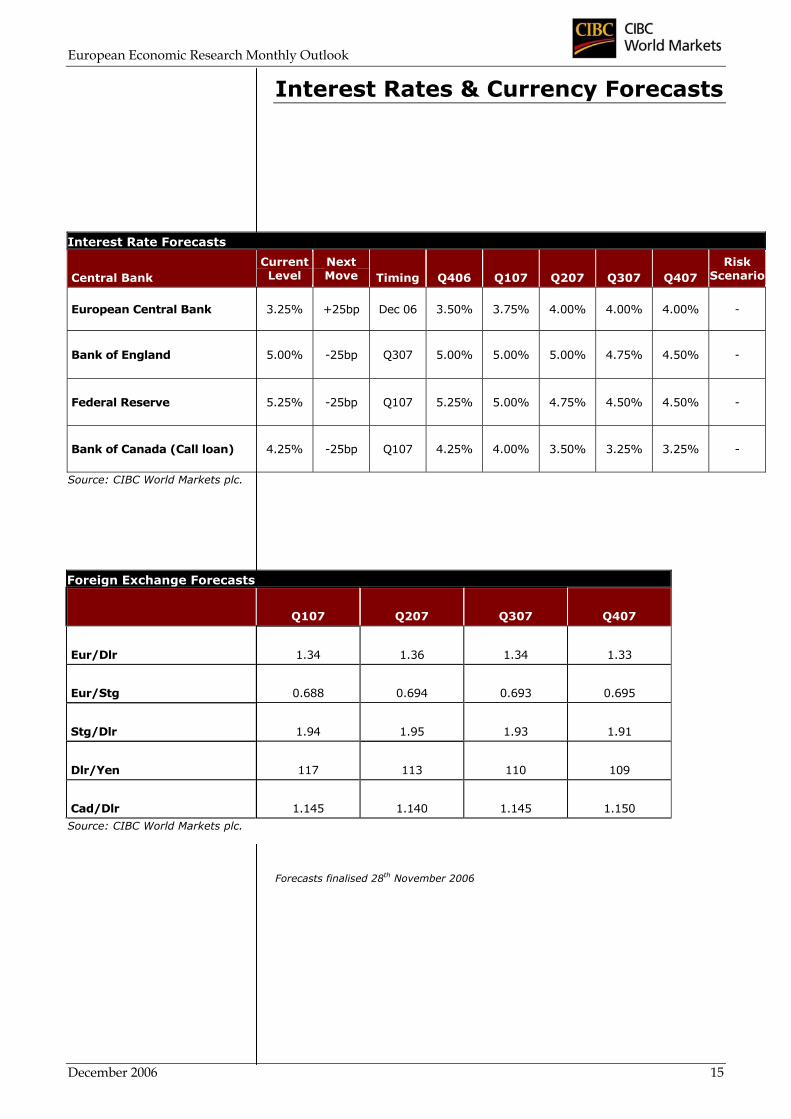

Interest Rates & Currency Forecasts

Interest Rate Forecasts

Central Bank Current Level

Next Move Timing Q406 Q107 Q207 Q307 Q407

Risk Scenario

European Central Bank 3.25% +25bp Dec 06 3.50% 3.75% 4.00% 4.00% 4.00% -

Bank of England 5.00% -25bp Q307 5.00% 5.00% 5.00% 4.75% 4.50% -

Federal Reserve 5.25% -25bp Q107 5.25% 5.00% 4.75% 4.50% 4.50% -

Bank of Canada (Call loan) 4.25% -25bp Q107 4.25% 4.00% 3.50% 3.25% 3.25% -

Source: CIBC World Markets plc.

Foreign Exchange Forecasts

Q107 Q207 Q307 Q407

Eur/Dlr 1.34 1.36 1.34 1.33

Eur/Stg 0.688 0.694 0.693 0.695

Stg/Dlr 1.94 1.95 1.93 1.91

Dlr/Yen 117 113 110 109

Cad/Dlr 1.145 1.140 1.145 1.150

Source: CIBC World Markets plc.

Forecasts finalised 28th November 2006

European Economic Research Monthly Outlook

16 December 2006

Market Outlook Finalised on November 27th • The dollar bear story has materialized (at last) and even

though the initial move was favored by a holiday, thin volumes trading environment, we see the move as sustainable and consistent with our bearish 2007 dollar outlook.

• It is premature to speculate on a less hard-nosed ECB monetary policy outlook in the wake of the recent euro rally but expect verbal intervention to become more frequent among EU officials in the next few weeks. However, we see the ECB’s tolerance level higher than in the previous euro strength cycle.

• Uncertainty with regard to the UK near-term monetary policy outlook continues to dominate in a context of mixed economic news. We stick to a more dovish BoE monetary policy outlook, leaving a more favourable outlook for Gilts than for their Eurozone counterpart. Currency wise, Cable looks like a one way upward trade while eur/stg is a good buy on the dips.

Eurozone A strengthening euro has made the headlines of late, raising question marks about the possible dragging effects that this could have on Eurozone GDP growth and on the implications for the ECB near-term monetary policy outlook. All this may provide a welcome short-term relief to a struggling Eurozone bond market, which we see as a good selling opportunity (especially versus the US Treasury market). Not that Fx levels do not matter when it comes to economic (or monetary policy) forecasting but it is probably premature to jump to conclusions at this stage of the cycle. The moves are still relatively recent and given the current strong upward momentum in the Eurozone economy (in domestic demand in particular), the economy is better positioned to absorb a stronger euro than it was in December 2004. EU MoF verbal intervention is likely to become more frequent over the next few weeks but we believe that the ECB’s tolerance level is likely to have gone up compared to December 2004 - the recent euro appreciation is unlikely to deter an ECB rate hike scenario at the December Governing Council Meeting. Looking ahead, we expect this stronger euro story to prevail into 2007: we have pencilled in a high of 1.36 by H207 on eur/dlr, with a Q407 target at 1.33. Note that in the wake of the recent moves, there may also be scope for upward revisions to those forecasts. Indeed, whether it is on structural, cyclical, Fx diversification concerns or ‘the time of the year’ grounds (December has often proven to be a bad month for the dollar), it is looking rather shaky for the greenback...

United Kingdom These are uncertain times for the UK markets, with a mixed set of economic news for market participants to digest and different lines of thoughts emerging from within the MPC all leaving a hesitant mood in the Gilts and Short-Sterling markets. We remain of the view that the BoE will not have to raise interest rates again in 2007, so the 25bp rate rise priced in the Short-Sterling market by the end of Q1 2007 is excessive. In fact, it is rate cut talks that could resurface in H2 2007, but it will take a lot more weakness from the domestic data for the market to ‘buy’ into our more dovish UK rate story. Moreover, our ECB/BoE rate outlook also points at likely outperformance of Gilts versus Bunds. On the currency front, it is all about dollar weakness these days, with Cable becoming a one-way upward trade of late. However, we left our eur/stg targets (0.69 remains a credible target) little changed, with the euro likely to outperform as it becomes more obvious that it is far from an all clear for the UK economy…

European Economic Research Monthly Outlook

December 2006 17

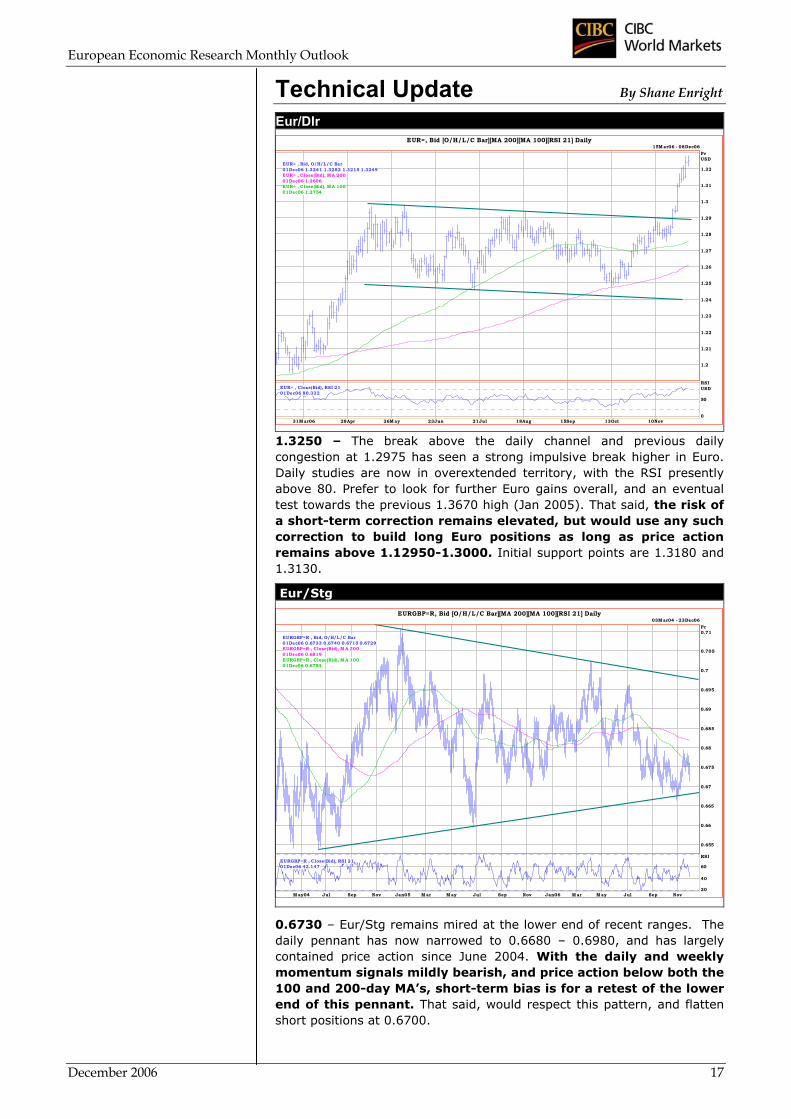

Technical Update By Shane Enright

Eur/Dlr EUR=, Bid [O/H/L/C Bar][MA 200][MA 100][RSI 21] Daily

15M ar06 - 08Dec06

31M ar06 28Apr 26M ay 23Jun 21Jul 18Aug 15Sep 13Oct 10Nov

PrUSD

1.2

1.21

1.22

1.23

1.24

1.25

1.26

1.27

1.28

1.29

1.3

1.31

1.32EUR= , Bid, O/H/L/C Bar01Dec06 1.3241 1.3282 1.3215 1.3249EUR= , Close(Bid), M A 20001Dec06 1.2606EUR= , Close(Bid), M A 10001Dec06 1.2754

RSIUSD

0

50

EUR= , Close(Bid), RSI 2101Dec06 80.332

1.3250 – The break above the daily channel and previous daily congestion at 1.2975 has seen a strong impulsive break higher in Euro. Daily studies are now in overextended territory, with the RSI presently above 80. Prefer to look for further Euro gains overall, and an eventual test towards the previous 1.3670 high (Jan 2005). That said, the risk of a short-term correction remains elevated, but would use any such correction to build long Euro positions as long as price action remains above 1.12950-1.3000. Initial support points are 1.3180 and 1.3130.

Eur/Stg

EURGBP=R, Bid [O/H/L/C Bar][MA 200][MA 100][RSI 21] Daily03M ar04 - 23Dec06

M ay04 Jul Sep Nov Jan05 M ar M ay Jul Sep Nov Jan06 M ar M ay Jul Sep Nov

Pr

0.655

0.66

0.665

0.67

0.675

0.68

0.685

0.69

0.695

0.7

0.705

0.71EURGBP=R , Bid, O/H/L/C Bar01Dec06 0.6733 0.6740 0.6715 0.6729EURGBP=R , Close(Bid), M A 20001Dec06 0.6819EURGBP=R , Close(Bid), M A 10001Dec06 0.6754

RSI

20

40

60EURGBP=R , Close(Bid), RSI 2101Dec06 43.147

0.6730 – Eur/Stg remains mired at the lower end of recent ranges. The daily pennant has now narrowed to 0.6680 – 0.6980, and has largely contained price action since June 2004. With the daily and weekly momentum signals mildly bearish, and price action below both the 100 and 200-day MA’s, short-term bias is for a retest of the lower end of this pennant. That said, would respect this pattern, and flatten short positions at 0.6700.

European Economic Research Monthly Outlook

18 December 2006

Dlr/Yen

JPY=, Bid [O/H/L/C Bar][MA 200][MA 100][RSI 21] Daily05M ay06 - 07Dec06

Jun06 Jul Aug Sep Oct Nov Dec

Pr/ USD

109

110

111

112

113

114

115

116

117

118

119

JPY= , Bid, O/H/L/C Bar01Dec06 115.78 116.38 115.46 116.08JPY= , Close(Bid), M A 20001Dec06 116.12JPY= , Close(Bid), M A 10001Dec06 117.12

RSI/ USD

20

40

JPY= , Close(Bid), RSI 2101Dec06 38.460

116.10 – Favored Yen strength from last month eventuated, although Yen has been a relative underperformer next to major European currencies like GBP and Euro. Solid initial resistance is now expected at the 117.00 level, with the 100-day MA at 117.12, and the neckline of a broken head and shoulder pattern at 117.20. Price objective of the head and shoulders break is close to the July low (113.30), with initial support at 115.45 (price congestion), and 115.00 (daily channel base). Continue to prefer long Yen positions overall, and would add on any correction towards 117.00.

Gbp/Dlr

GBP=, Bid [O/H/L/C Bar][MA 200][MA 100][RSI 21] Daily16Jun06 - 06Dec06

26Jun06 10Jul 24Jul 07Aug 21Aug 04Sep 18Sep 02Oct 16Oct 30Oct 13Nov 27Nov

PrUSD

1.78

1.79

1.8

1.81

1.82

1.83

1.84

1.85

1.86

1.87

1.88

1.89

1.9

1.91

1.92

1.93

1.94

1.95

1.96

GBP= , Bid, O/H/L/C Bar01Dec06 1.9661 1.9748 1.9632 1.9690GBP= , Close(Bid), M A 20001Dec06 1.8487GBP= , Close(Bid), M A 10001Dec06 1.8879

RSIUSD

40

60

GBP= , Close(Bid), RSI 2101Dec06 80.555

1.9690 – A 700 point appreciation in GBP since this commentary was written 4-weeks ago represents this currency’s best monthly performance since May. With current price action through the top of daily, weekly, and monthly Bollinger bands, Sterling is clearly in dangerously overbought territory in the short-term. Previous major cycle highs of 2.0050 (Mar 1991) and 2.0115 (Sept 1992) appear to be vulnerable in coming weeks, but for now, prefer short GBP positions, looking for some of these overbought conditions to be relieved in the initial part of December. Support levels to watch are 1.9540, 1.9420, and 1.9340.

European Economic Research Monthly Outlook

December 2006 19

[This page left intentionally blank]

CIBC World Markets PLC Cottons Centre, Cottons Lane

London, England SE1 2QL Tel: +44 207 234-7890 Fax: +44 207 234-7851

www.cibcwm.com

The securities mentioned in this report are speculative in nature and involve risk to principal and interest payments. This document and the recommendations included herein are for informational purposes only and intended for distribution solely to Qualified Institutional Buyers under Rule 144A.

This report is issued by (i) in the US, CIBC World Markets Corp., a member of the NYSE and SIPC, (ii) in Canada, CIBC World Markets Inc., a member of the IDA and CIPF, and (iii) in the UK, CIBC World Markets plc, regulated by the FSA. Any questions should be directed to your sales representative.

Every state in the United States, province in Canada and most countries throughout the world have their own laws regulating the types of securities and other investment products which may be offered to their residents, as well as the process for doing so. As a result, some of the securities discussed in this report may not be available to every interested investor. Accordingly, this report is provided for informational purposes only, and does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such would be prohibited. No part of any report may be reproduced in any manner without the prior written permission of CIBC World Markets.

The information and any statistical data contained herein have been obtained from sources which we believe to be reliable, but we do not represent that they are accurate or complete, and they should not be relied upon as such. All opinions expressed and data provided herein are subject to change without notice. A CIBC World Markets company or its shareholders, directors, officers and/or employees, may have a long or short position or deal as principal in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. A CIBC World Markets company may have acted as initial purchaser or placement agent for a private placement of any of the securities of any company mentioned in this report, may from time to time solicit from or perform financial advisory, investment banking or other services for such company, or have lending or other credit relationships with the same. The securities mentioned in this report may not be suitable for all types of investors; their prices, value and/or income they produce may fluctuate and/or be adversely affected by exchange rates. Since the levels and bases of taxation can change, any reference in this report to the impact of taxation should not be construed as offering tax advice; as with any transaction having potential tax implications, clients should consult with their own tax advisors. Past performance is no guarantee of future results.

This document and any of the products and information contained herein are not intended for the use of private investors in the UK. Such investors will not be able to enter into agreements or purchase products mentioned herein from CIBC World Markets plc.

Although each company issuing this report is a wholly owned subsidiary of Canadian Imperial Bank of Commerce (“CIBC”), each is solely responsible for its contractual obligations and commitments, and any securities products offered or recommended to or purchased or sold in any client accounts (i) will not be insured by the Federal Deposit Insurance Corporation, the Canada Deposit Insurance Corporation or other similar deposit insurance, (ii) will not be deposits or other obligations of CIBC, (iii) will not be endorsed or guaranteed by CIBC, and (iv) will be subject to investment risks, including possible loss of the principal invested. The CIBC trademark is used under license.

©2002 CIBC World Markets Corp. and CIBC World Markets Inc. All rights reserved.

Global Economic Research

Europe

Audrey Childe-Freeman Tel. +44 20-7234-6666 [email protected]

Jodie Saul Tel. +44 20-7234-7325 [email protected]

North America

Jeffrey Rubin Tel. 416-594-7357 [email protected]

Avery Shenfeld Tel. 416-594-7356 [email protected]

Peter Buchanan Tel. 416-594-7354 [email protected]

Warren Lovely Tel. 416-594-7359 [email protected]

Benjamin Tal Tel: 416-956-3698 [email protected]

David Bezic Tel. 416-956-3219 [email protected]

Colleen Curran Tel. 416-594-7355 [email protected]

![Outlook 2007 - calendarOffice 2007 [OUTLOOK 2007 - CALENDAR] 2 OUTLOOK 2007 CALENDAR FOLDER Outlook 2007 Calendar Window The Outlook 2007 Calendar Folder provides easy viewing of appointments,](https://static.fdocuments.in/doc/165x107/5f4d6a371177844bdc7827e3/outlook-2007-office-2007-outlook-2007-calendar-2-outlook-2007-calendar-folder.jpg)