Molex Inc. - Texas Tech Universitymmoore.ba.ttu.edu/ValuationReports/Fall2008/Molex-Fall2008.pdf ·...

244

1 Molex Inc. Project Group Members: Johnnie Davis [email protected] Eric Gordon [email protected] Monica Longer [email protected] Katelyn Owens [email protected] Allina Pokorny [email protected]

Transcript of Molex Inc. - Texas Tech Universitymmoore.ba.ttu.edu/ValuationReports/Fall2008/Molex-Fall2008.pdf ·...

1

Molex Inc.

Project Group Members:

Johnnie Davis [email protected]

Eric Gordon [email protected]

Monica Longer [email protected]

Katelyn Owens [email protected]

Allina Pokorny [email protected]

2

Table of Contents

Executive Summary 12

Business and Industry Analysis 21

Company Overview 21

Industry Overview 22

Five Forces Model 25

Rivalry of Existing Firms 26

Industry Growth Rate 27

Concentration of Competitors 28

Differentiation 30

Switching Costs 30

Economies of Scale 31

Learning Economies 32

Exit Barriers 33

Conclusion 33

Threat of New Entrants 34

3

Economies of Scale 34

First Mover Advantage 36

Legal Barriers 36

Conclusion 37

Threat of Substitute Products 38

Relative Price and Performance 38

Customers’ Willingness to Switch 39

Conclusion 40

Bargaining Power of Customers 40

Switching Cost 41

Differentiation 41

Importance of Product for Cost and Quality 41

Number of Customers 42

Volume of Customers 42

Conclusion 43

Bargaining Power of Suppliers 43

Switching Cost 43

Differentiation 44

4

Importance of Product for Cost and Quality 44

Number of Suppliers 44

Volume of Suppliers 45

Conclusion 45

Customer and Supplier Bargaining Power Conclusion 45

Analysis of Key Success Factors for Value Creation in the Industry 46

Cost Leadership 46

Economies of Scale and Efficient Production 47

Lower Input Costs 48

Simpler Product Designs 48

Differentiation 49

Product Quality 49

Product Variety 50

Brand Image 51

Flexible Delivery 52

Customer Service 52

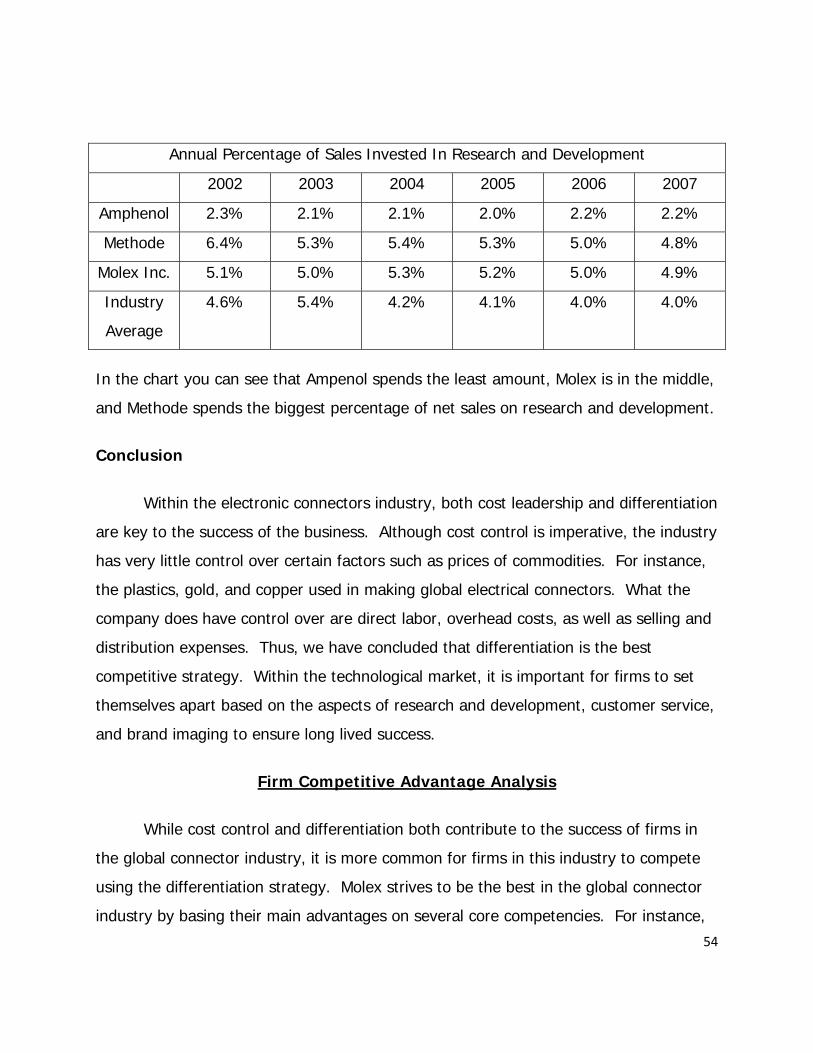

Research and Development 53

Conclusion 54

5

Firm Competitive Advantage Analysis 54

Product Quality and Brand Image 55

Product Variety 55

Customer Service 56

Flexible Delivery 56

Research and Development 57

Conclusion 58

Formal Accounting Analysis 58

Key Accounting Policies 59

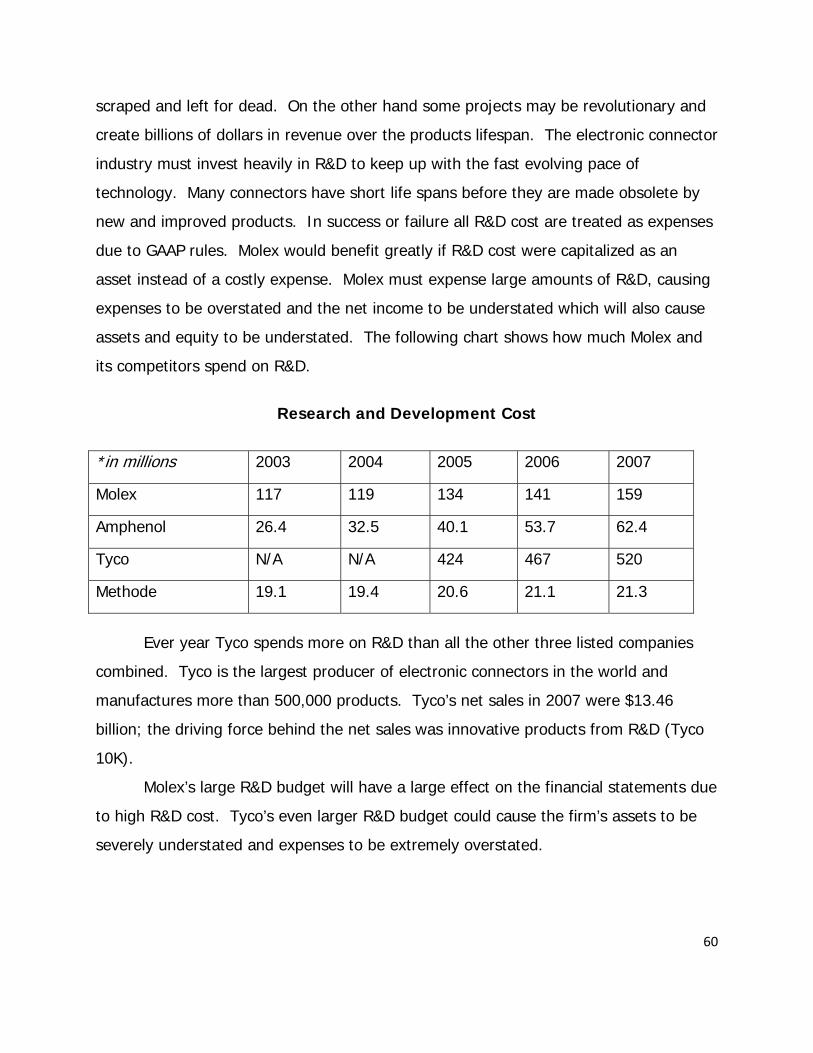

Research & Development 59

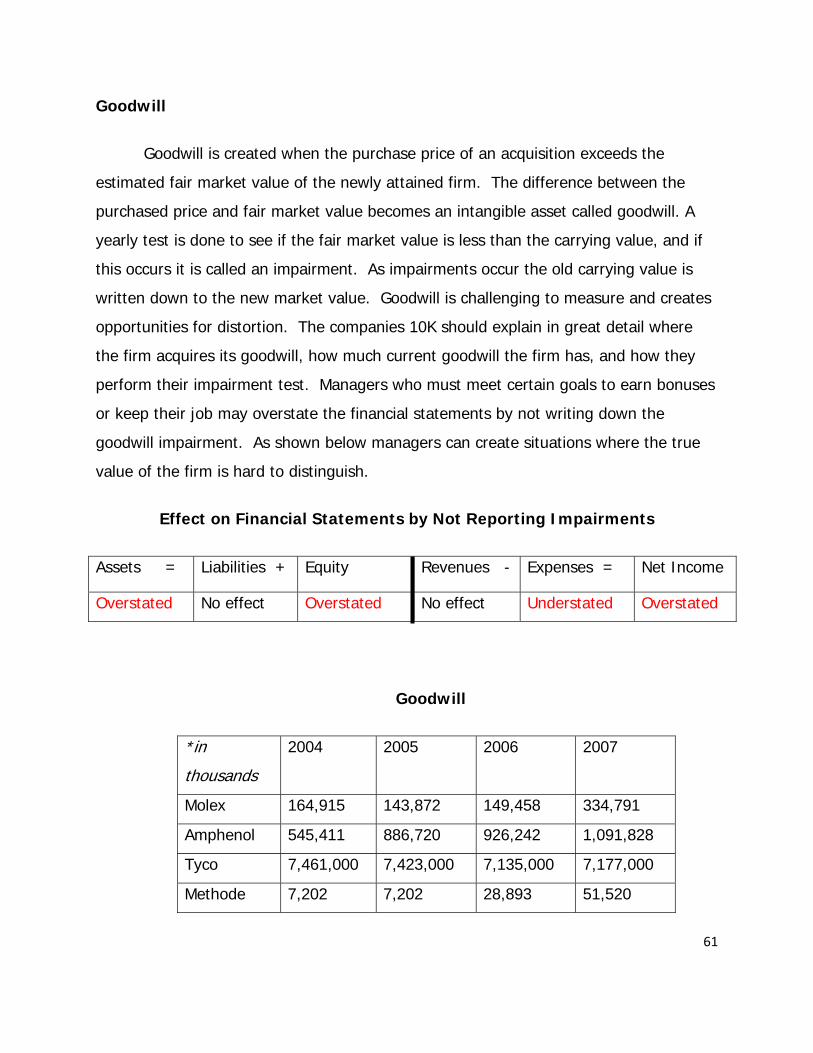

Goodwill 61

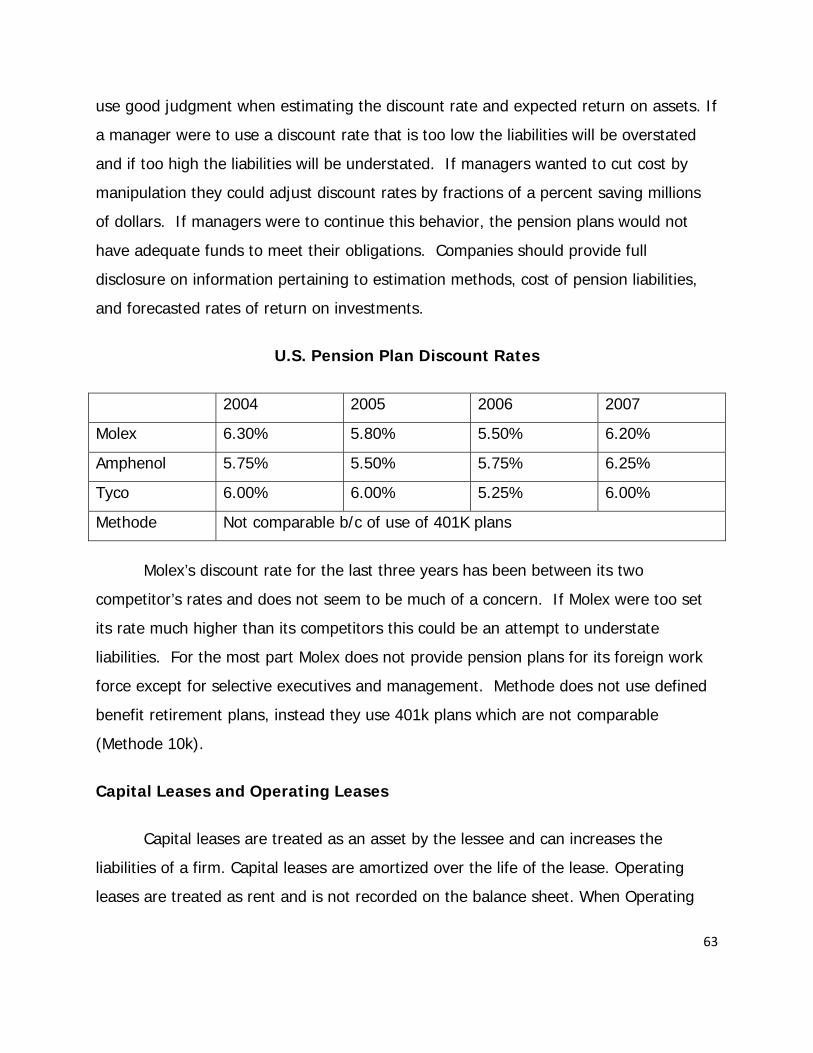

Pension Liabilities 62

Operating and Capital Leases 63

Currency Risk 64

Accounting Flexibility 65

Research & Development 65

Operating and Capital Leases 67

Pension Plans 68

6

Goodwill 69

Currency 70

Evaluate Accounting principles 71

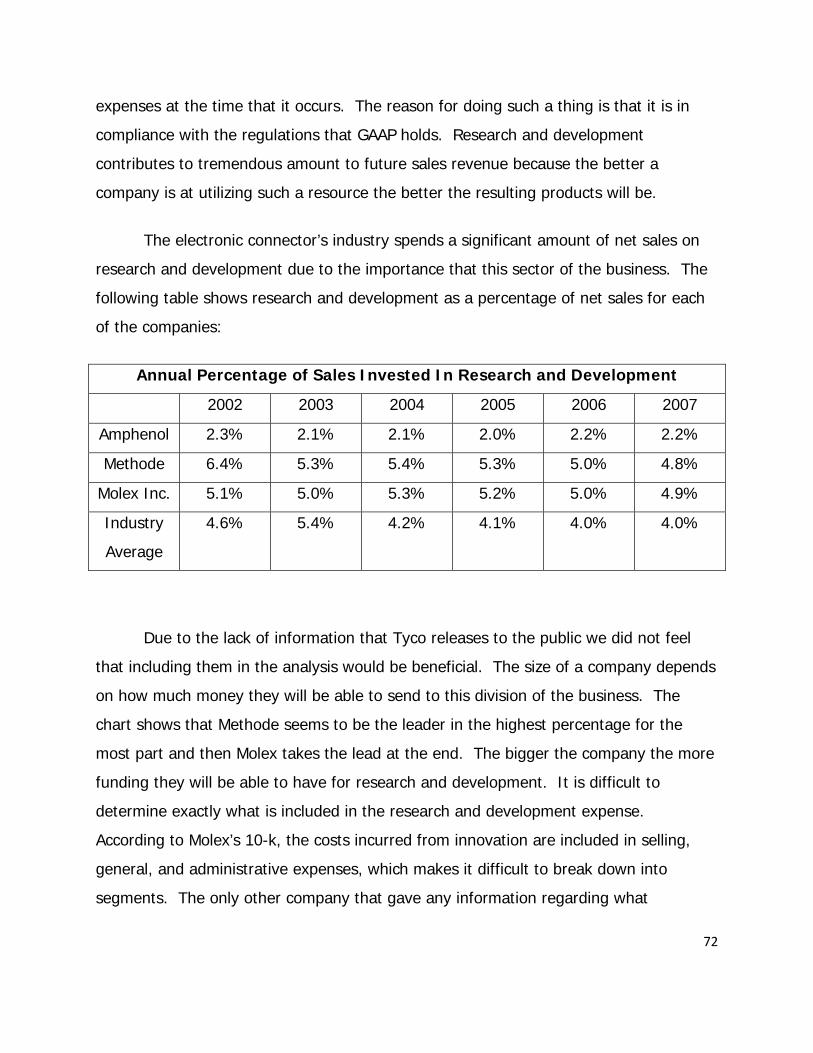

Research and Development 71

Operating and Capital Leases 73

Pension Plans 74

Goodwill 76

Currency 78

Qualitative Analysis 78

Research and Development 79

Operating and Capital Leases 80

Pensions 81

Goodwill 82

Currency 82

Quantitative Accounting Measures and Disclosure 83

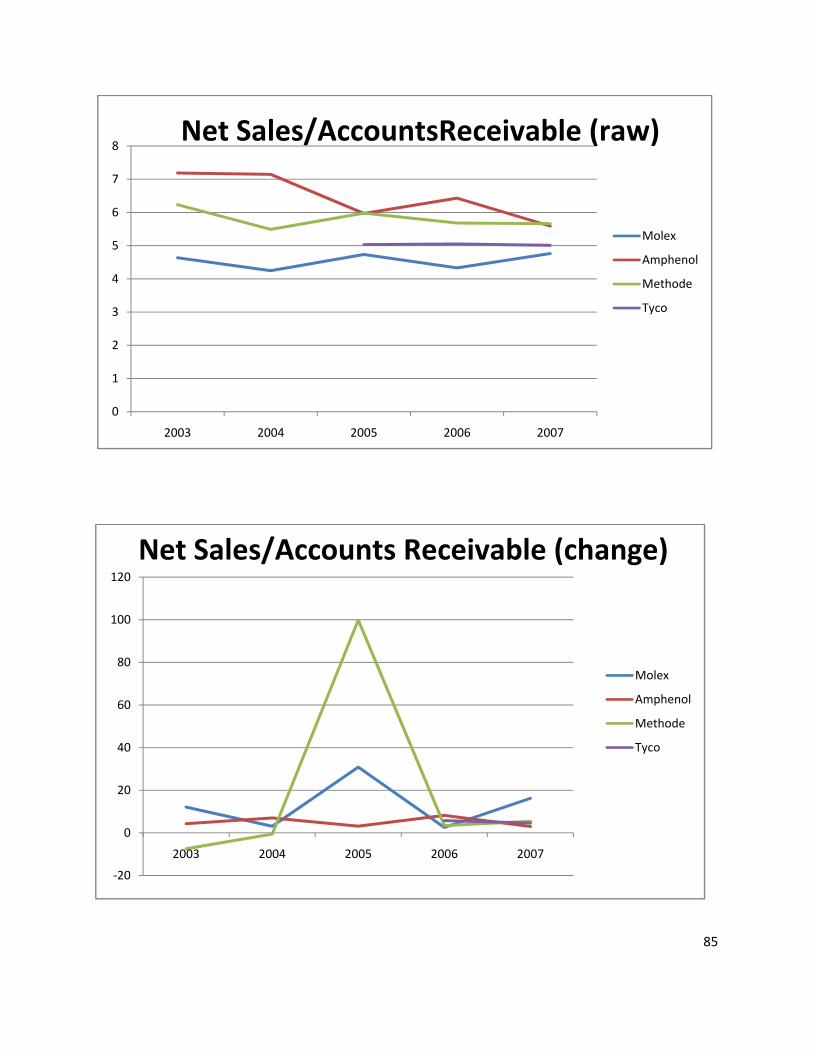

Sales Manipulation Diagnostic 84

Net Sales/Accounts Receivables 84

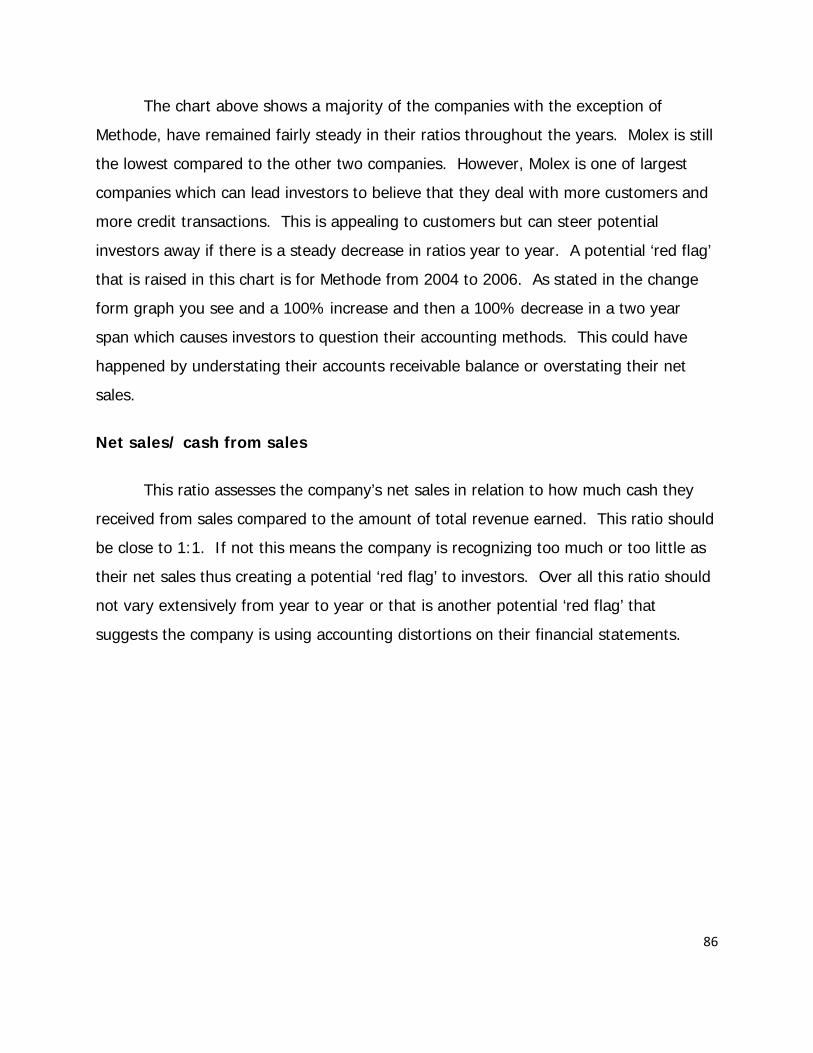

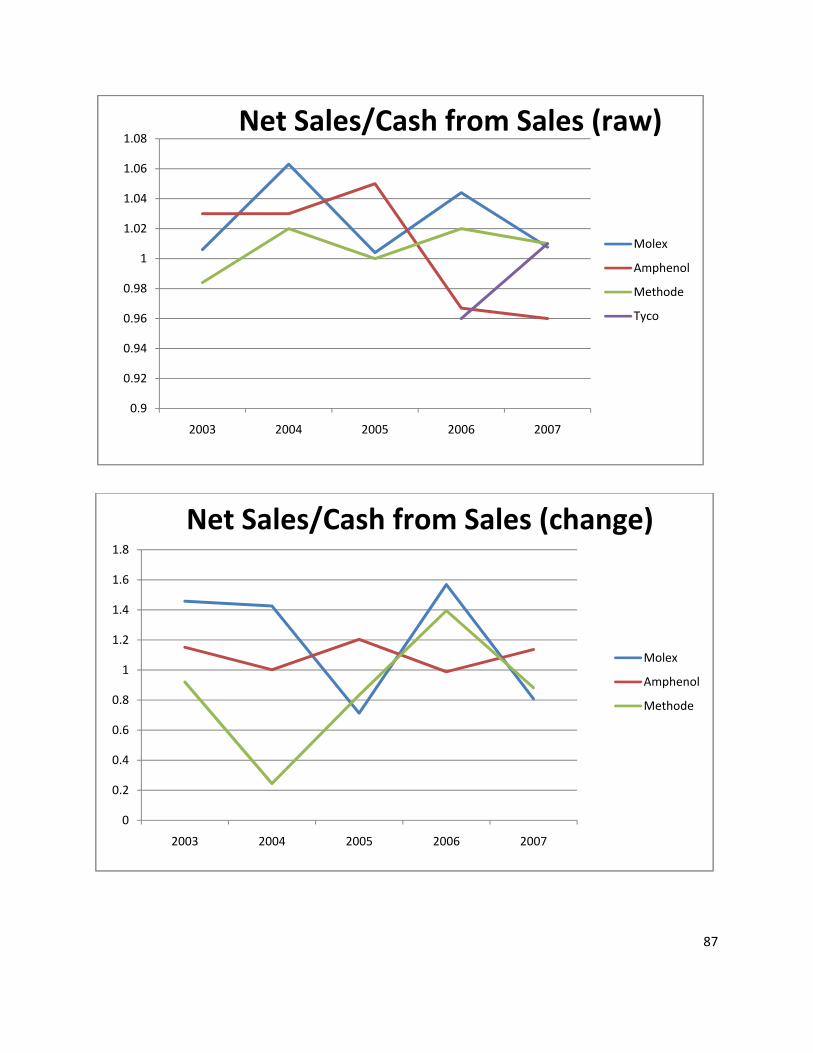

Net Sales/Cash from Sales 86

7

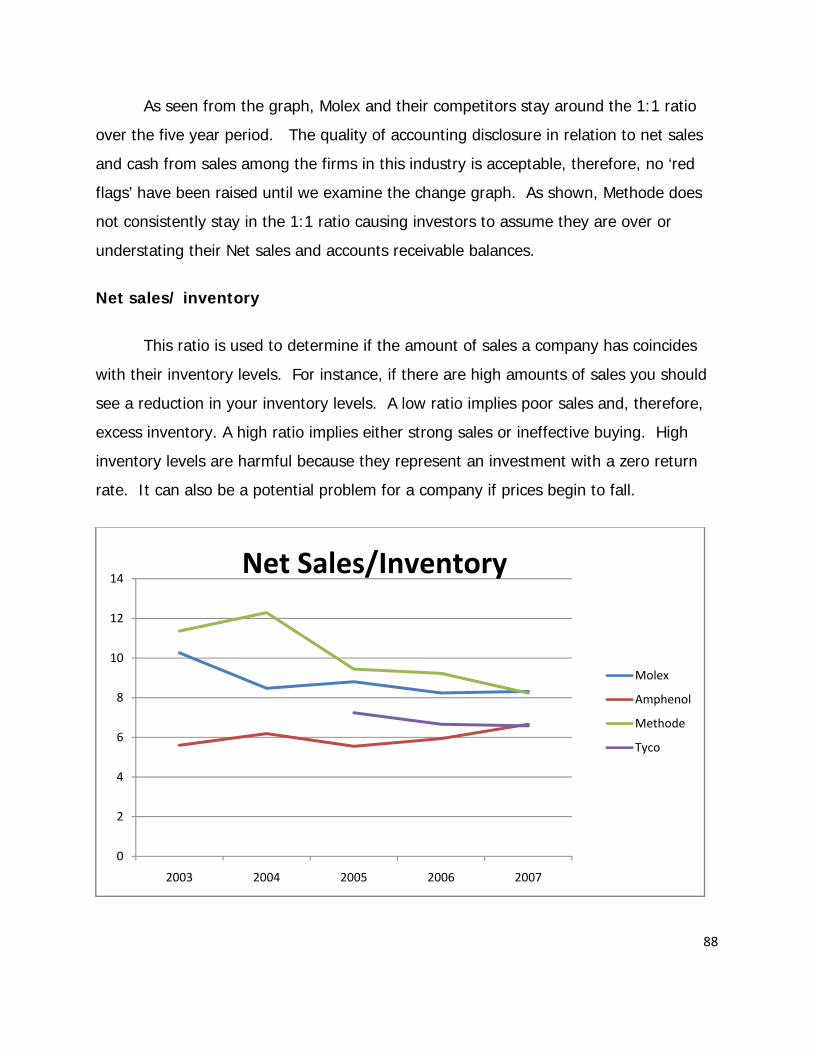

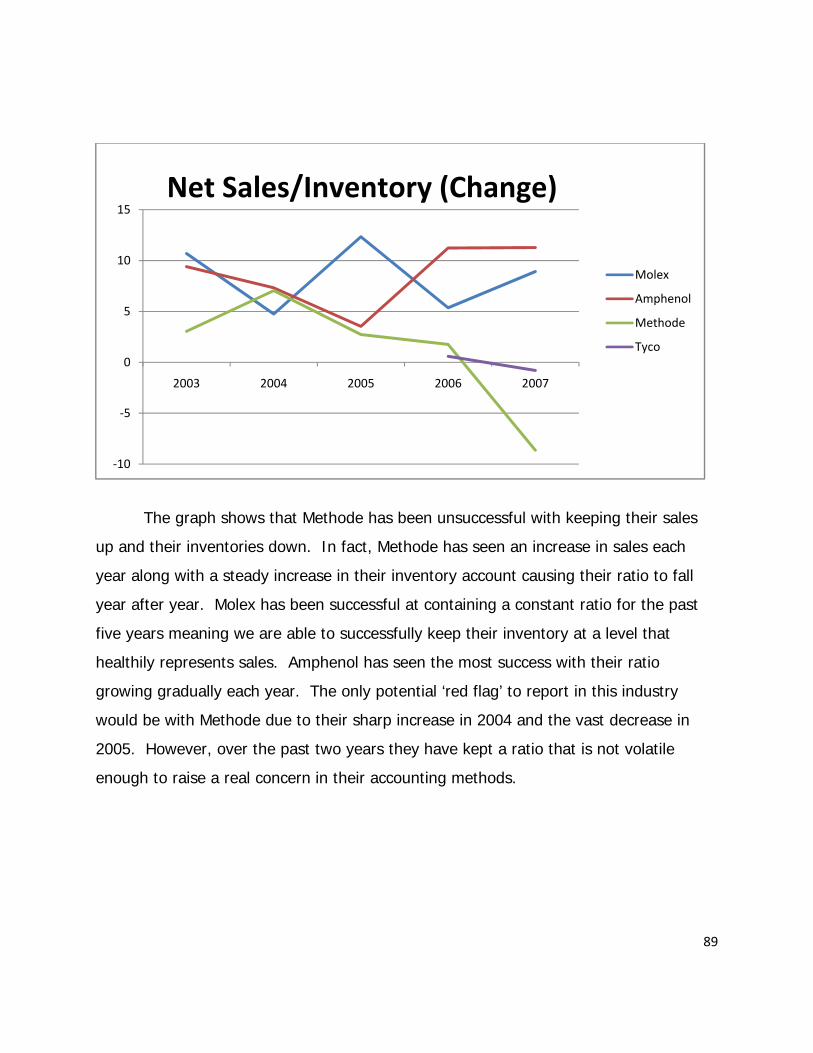

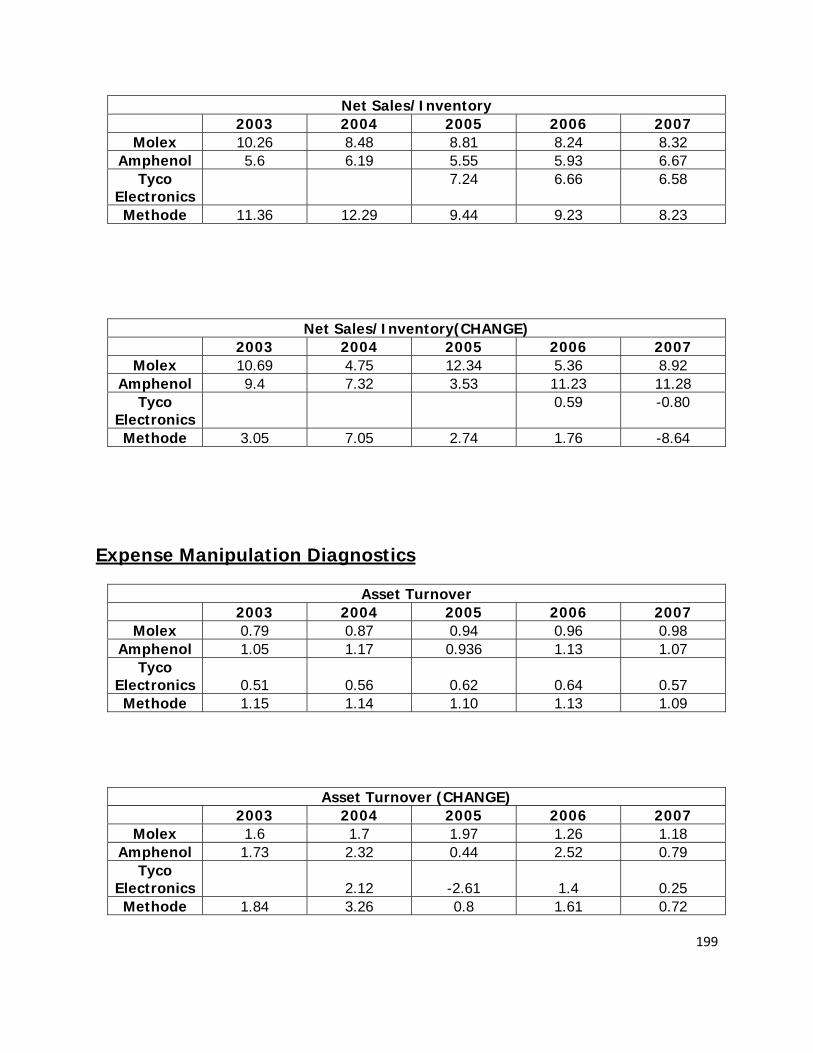

Net Sales/Inventory 88

Conclusion 90

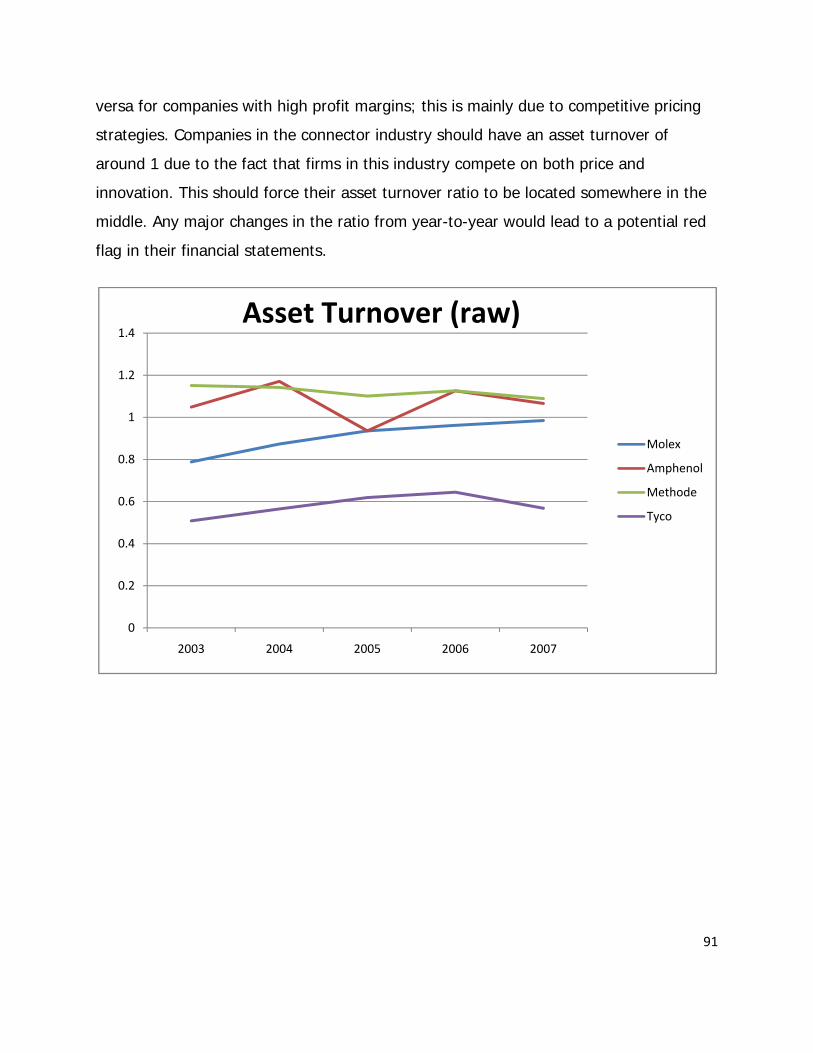

Expense Manipulation Diagnostic 90

Asset Turnover 90

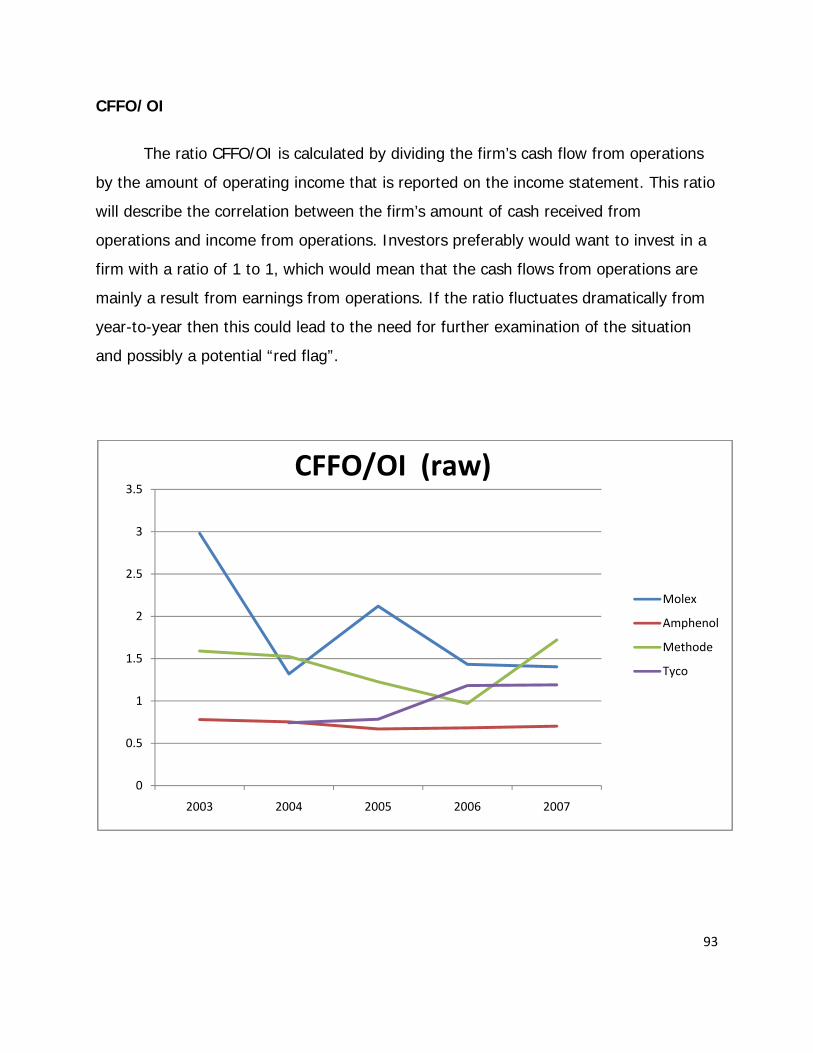

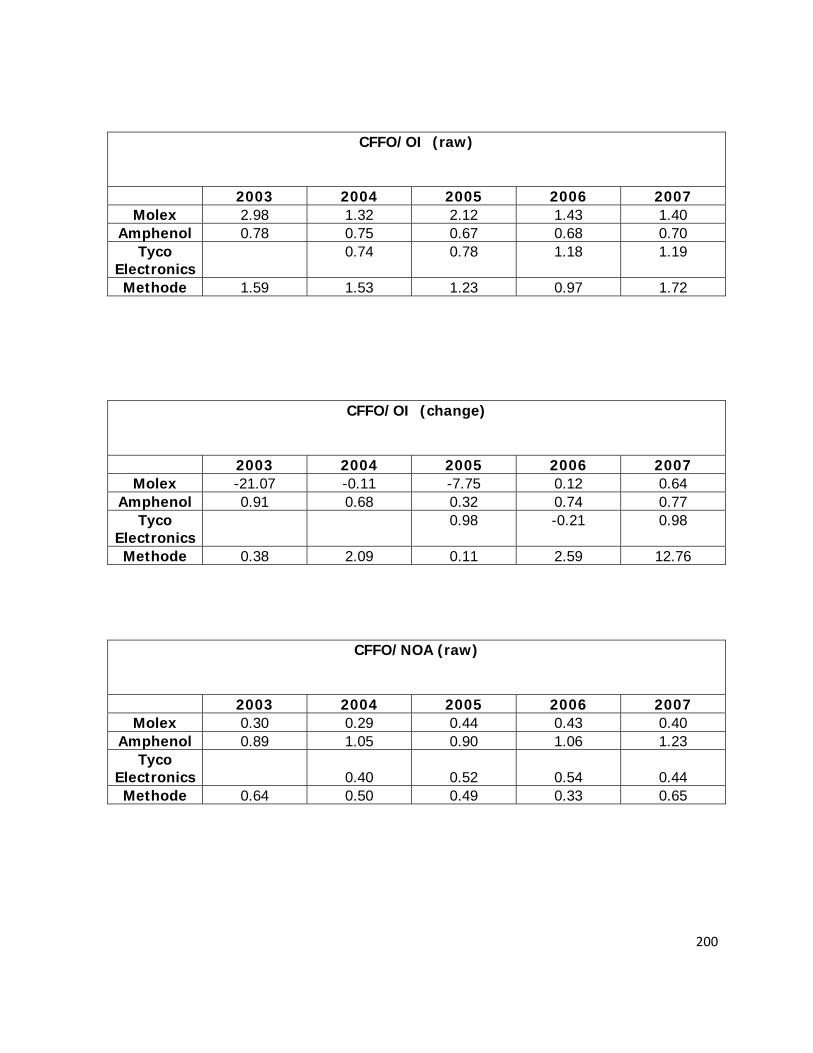

CFFO/OI 93

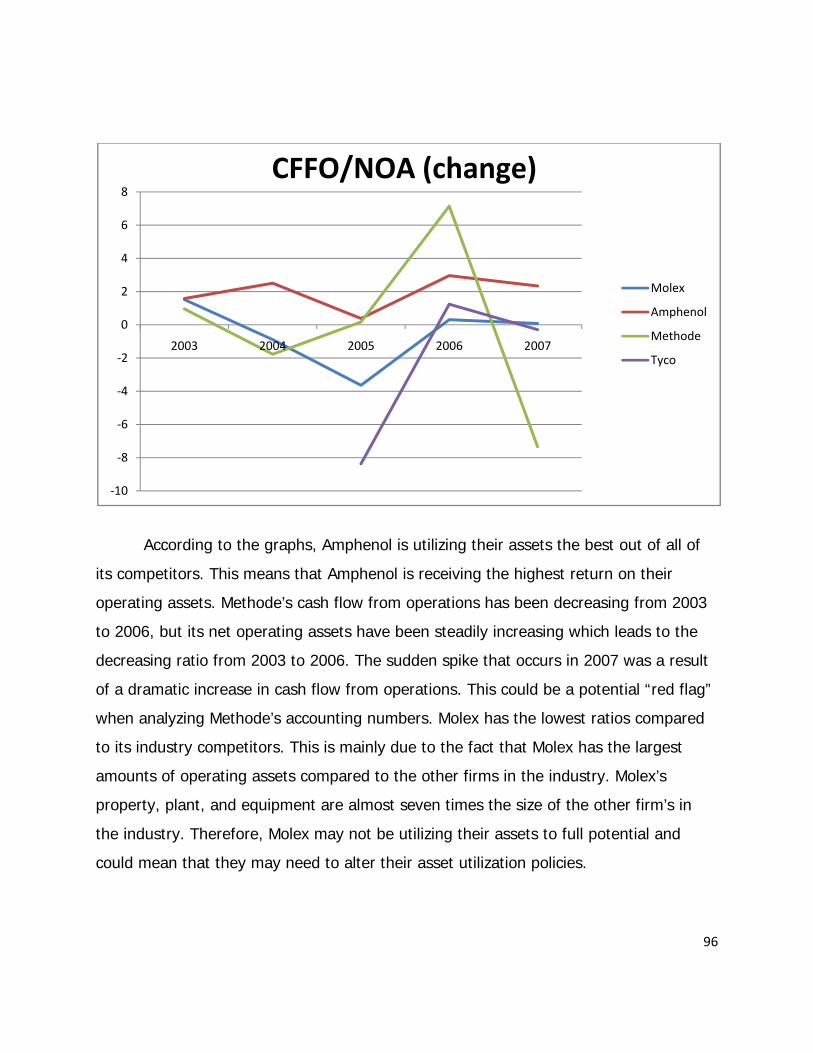

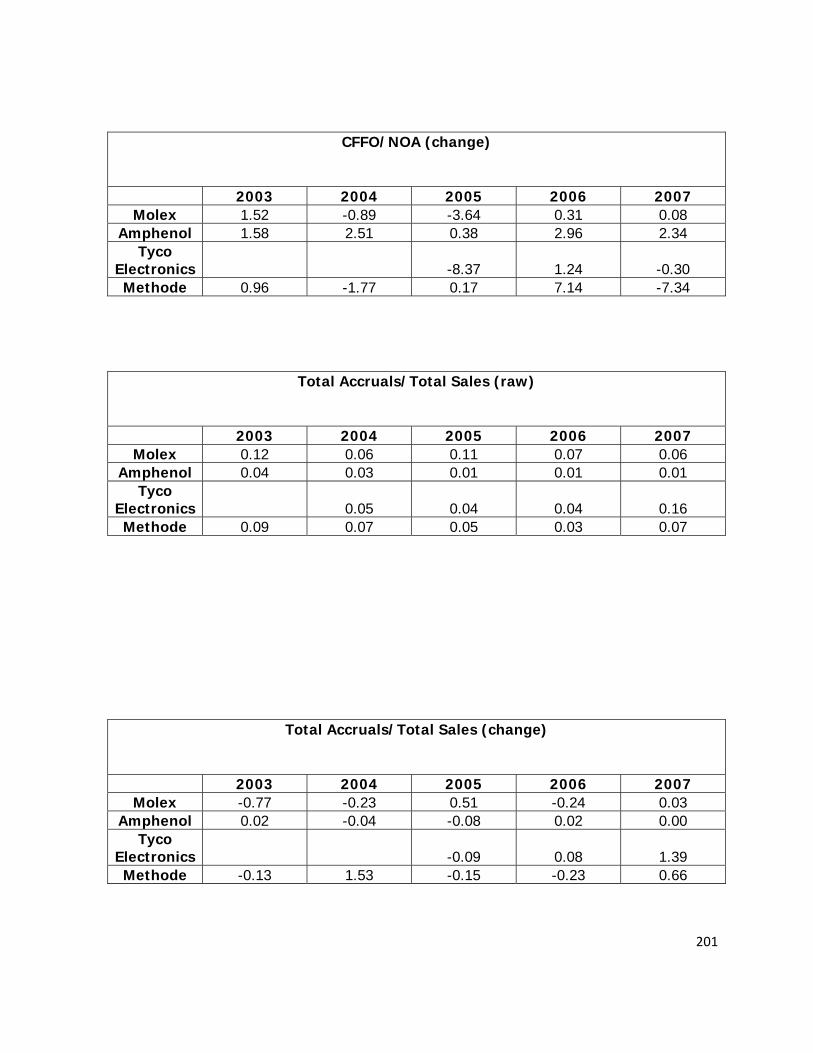

CFFO/NOA 95

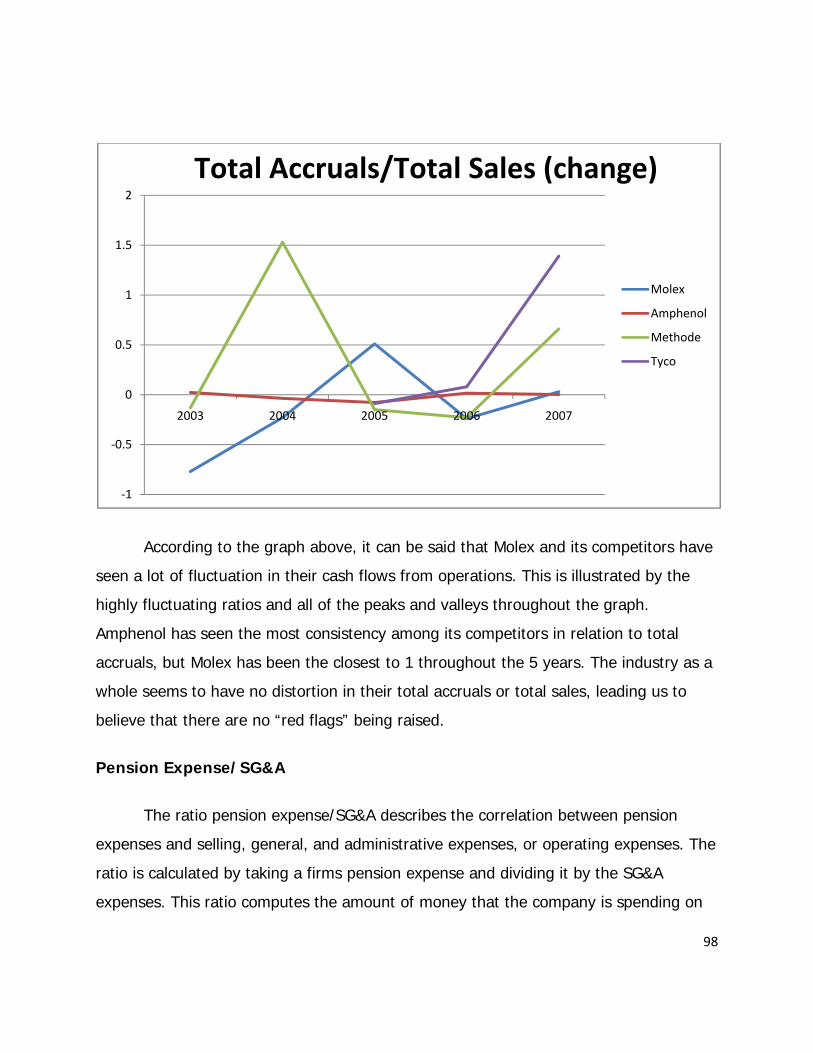

Total Accruals/Sales 97

Pension/SG&A 98

Conclusion 100

Potential Red Flags 101

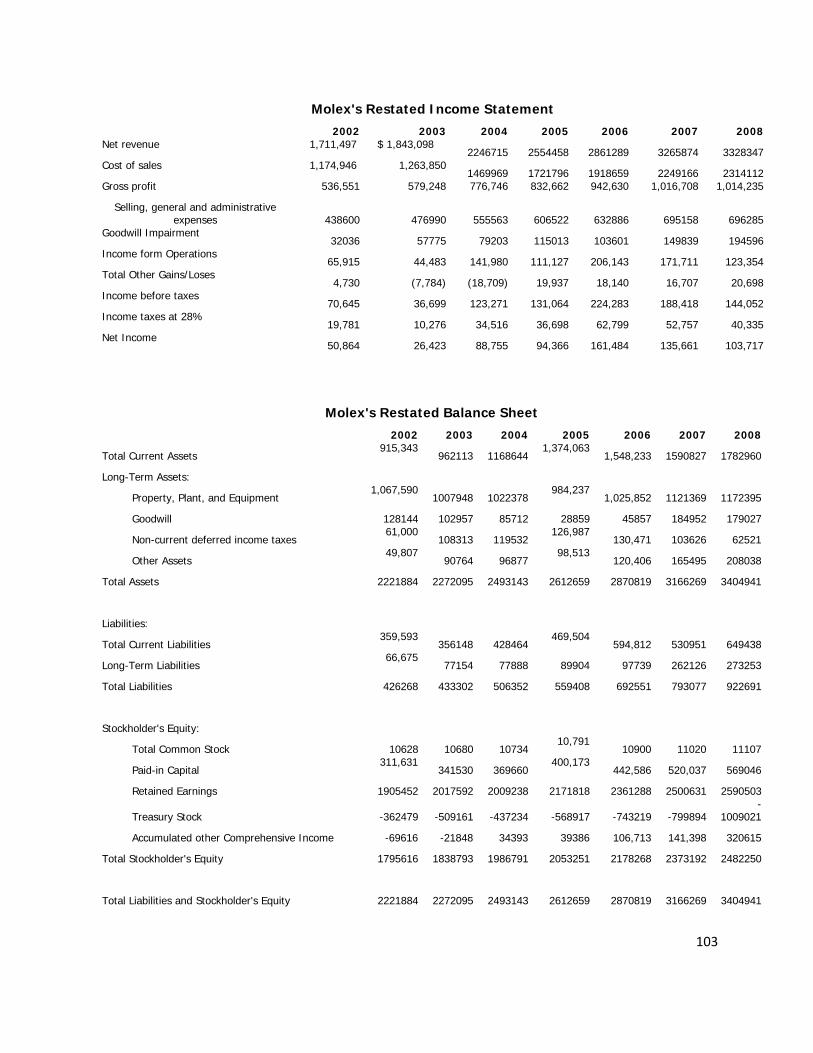

Undoing Accounting Distortion or Irregularities 102

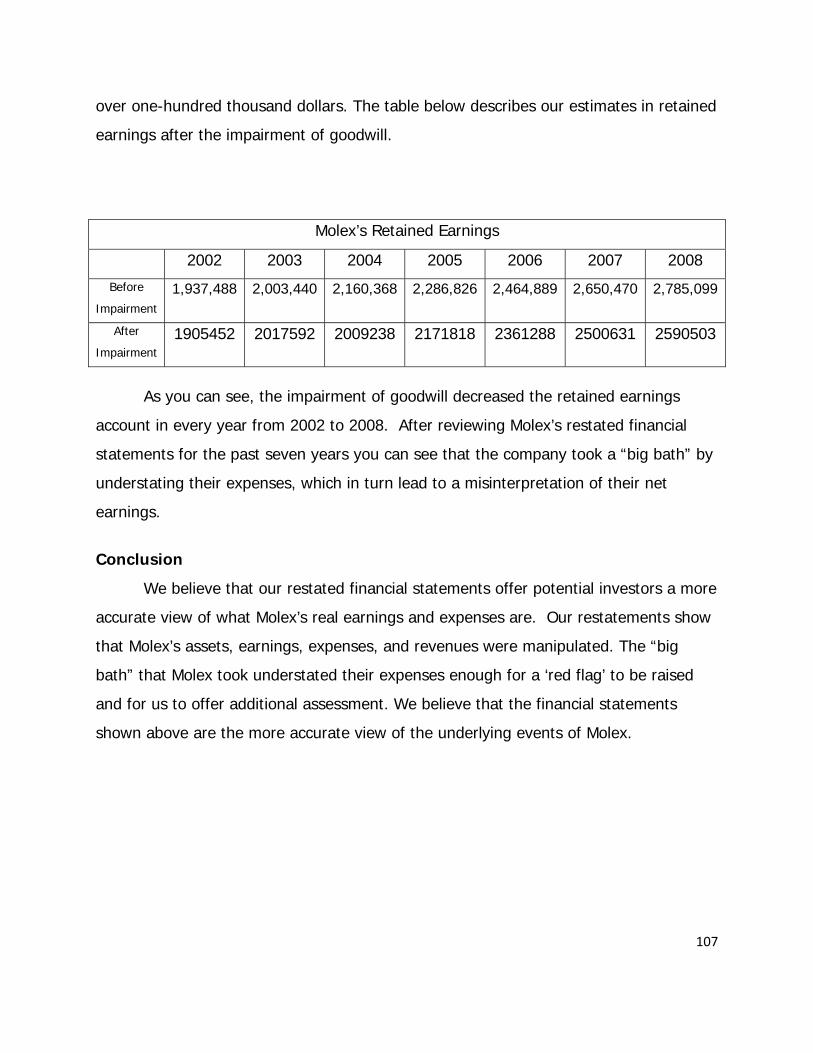

Goodwill 104

Conclusion 107

Financial Analysis Forecasting Financials and Cost of Capital Estimation 108

Financial Analysis 108

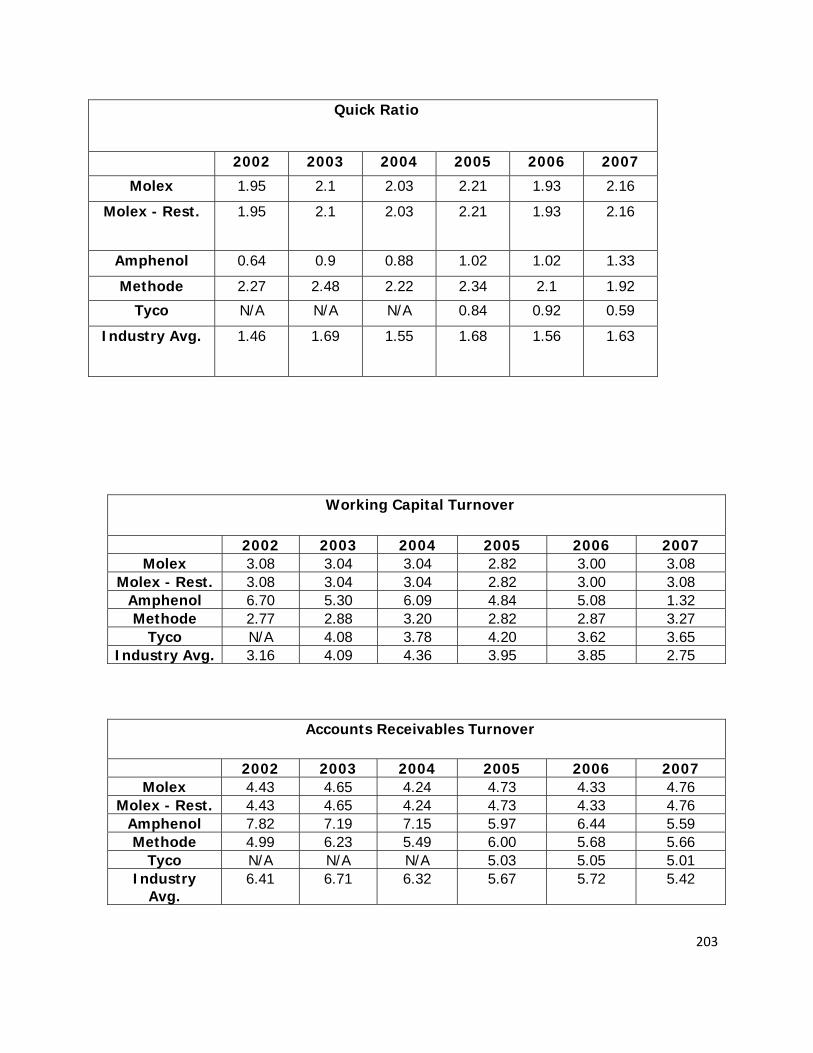

Liquidity Ratio Analysis 108

Current Ratio 109

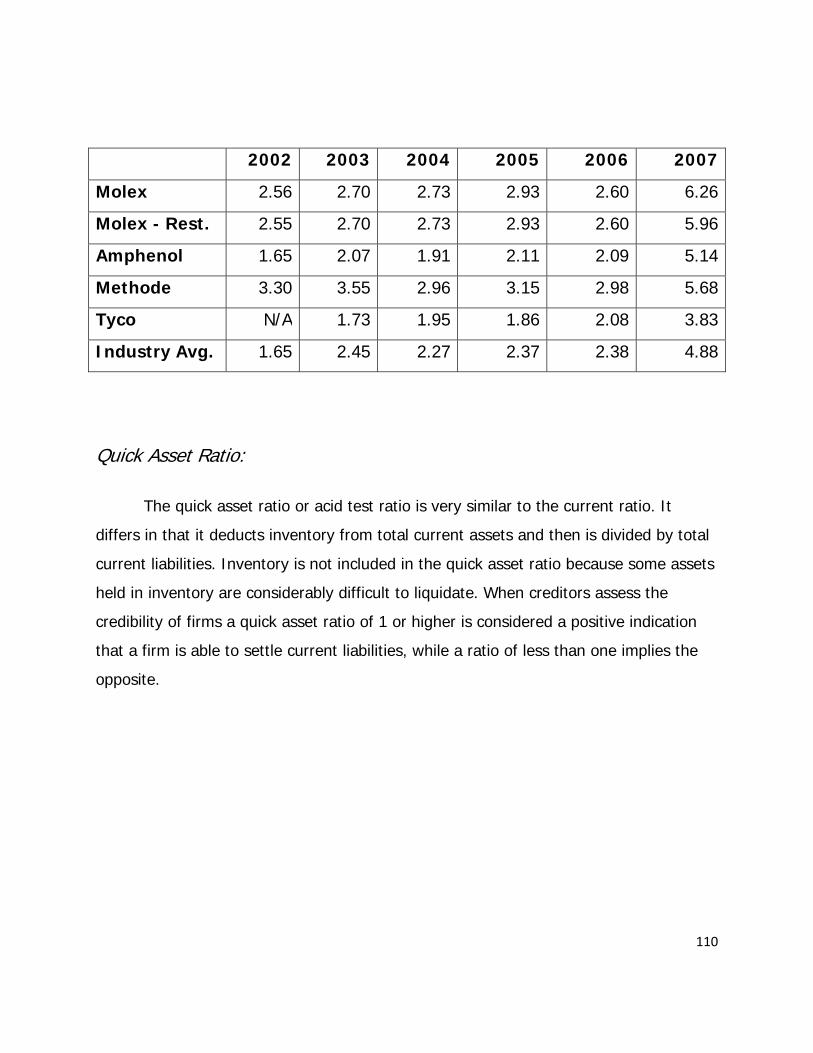

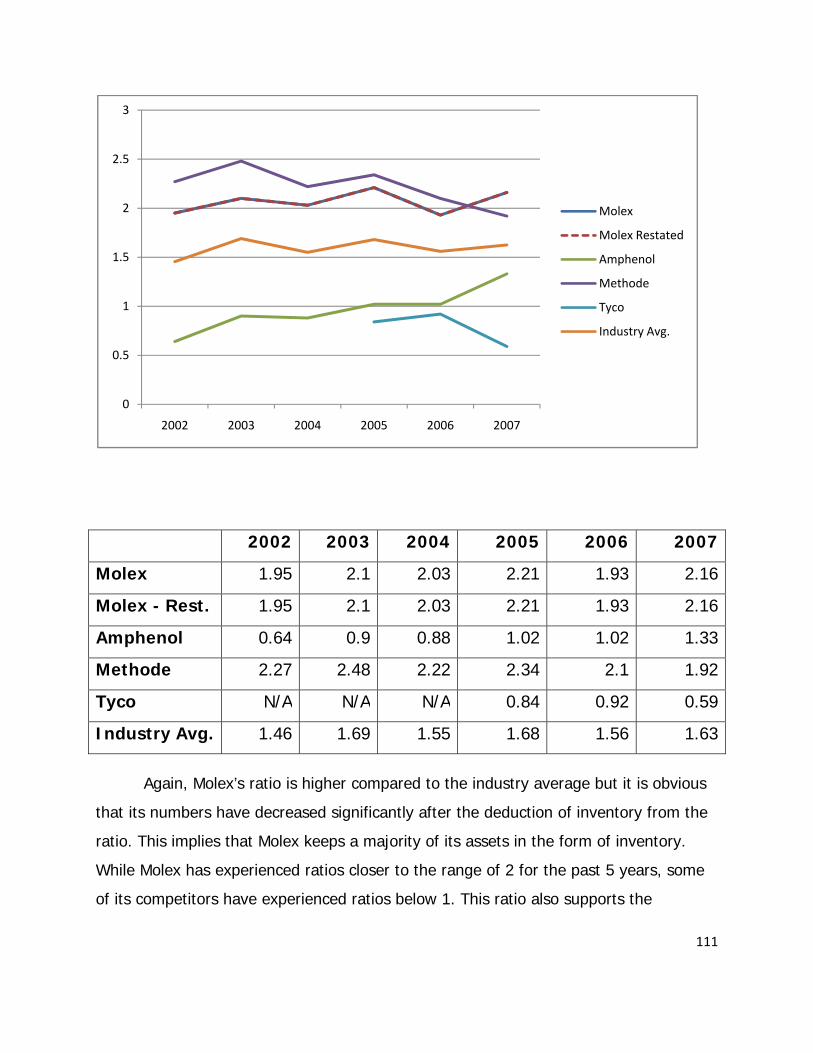

Quick Asset Ratio 110

8

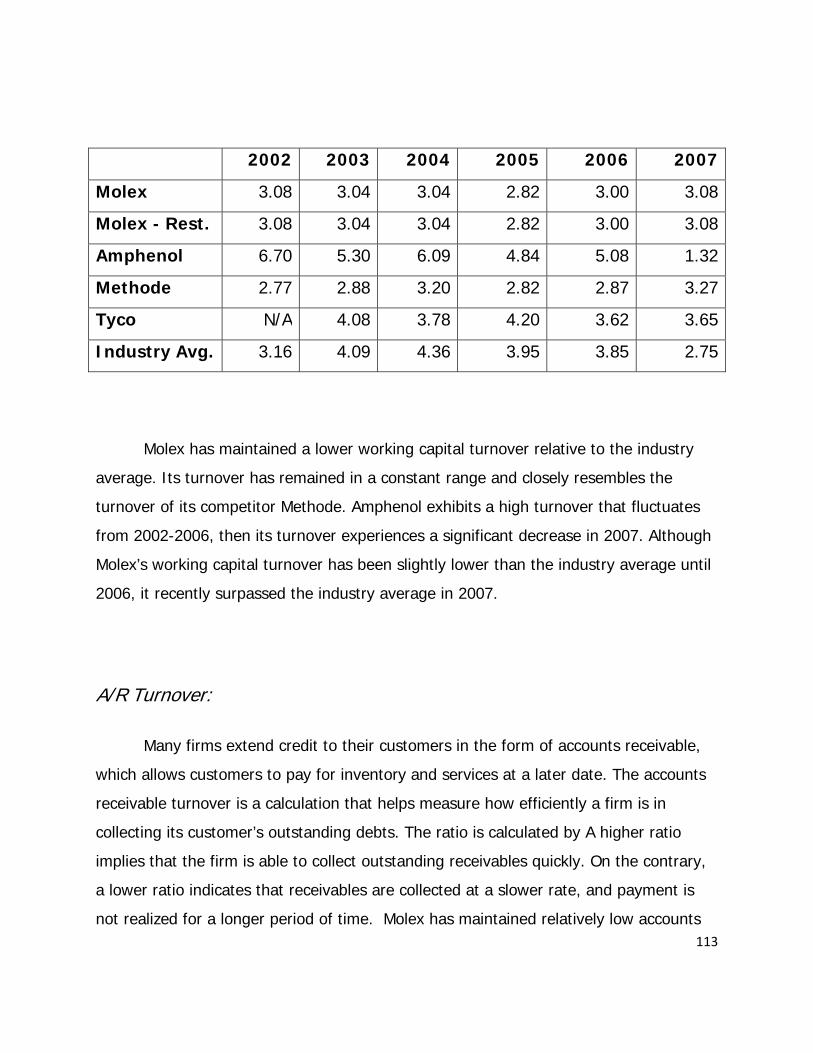

Working Capital Turnover 112

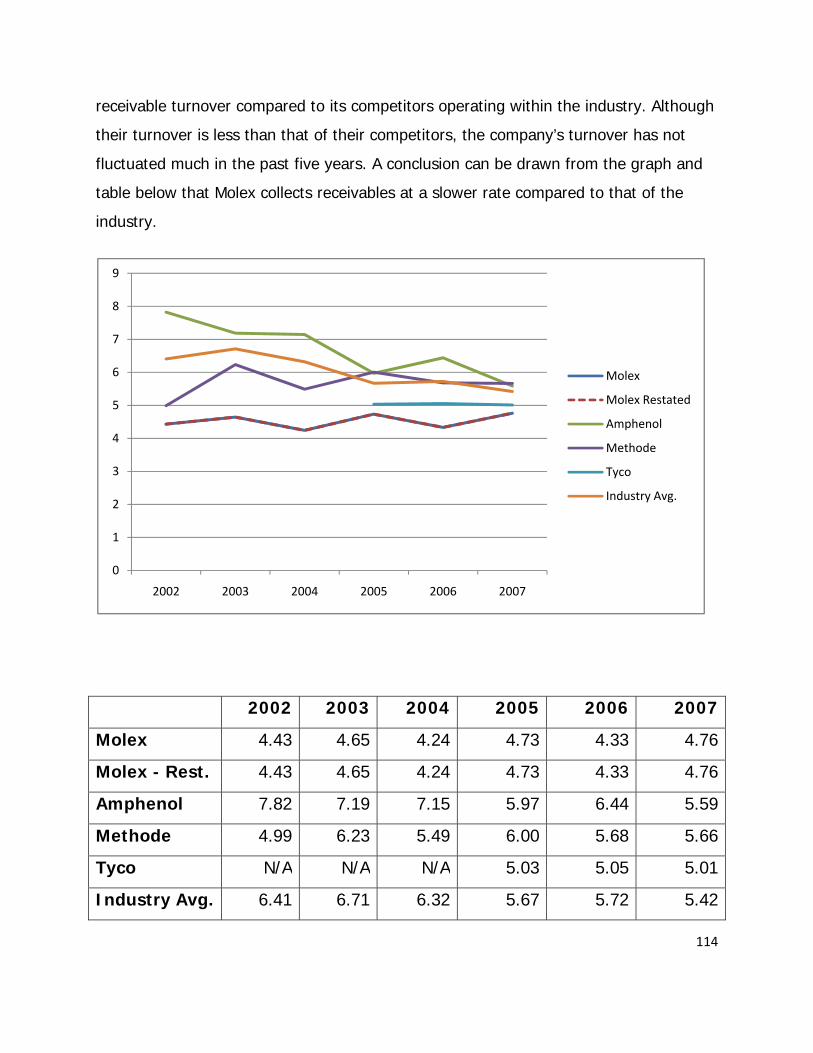

Accounts Receivables Turnover 113

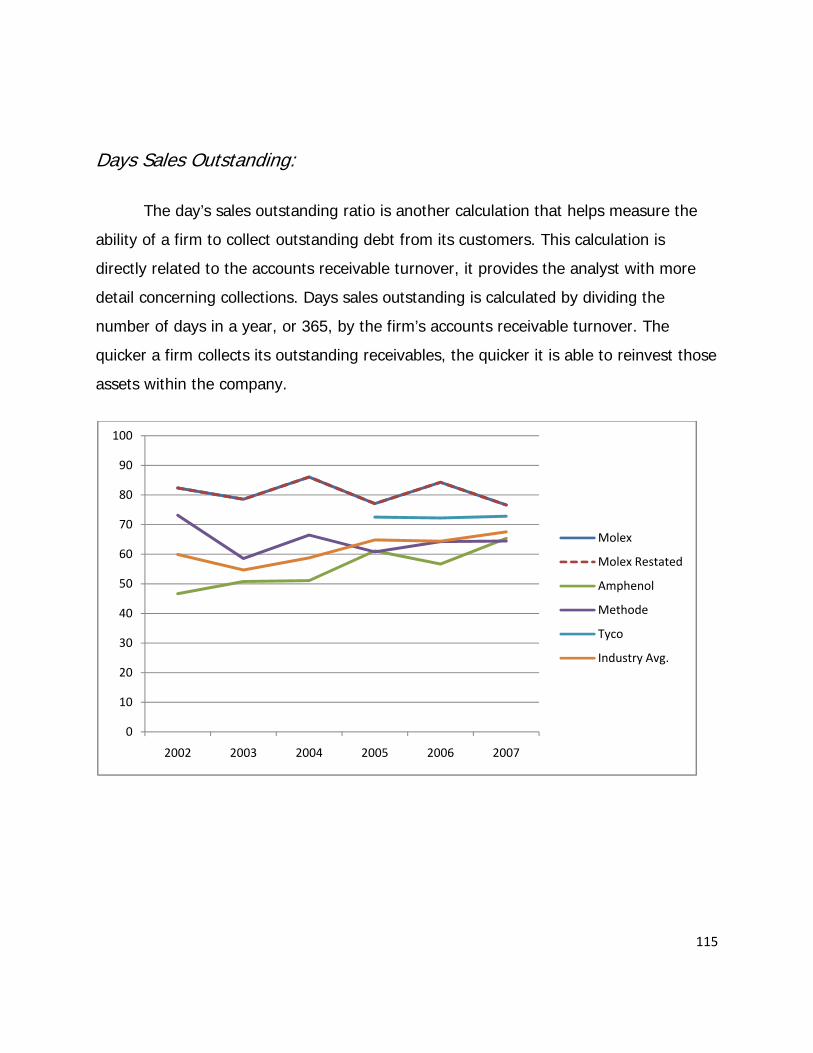

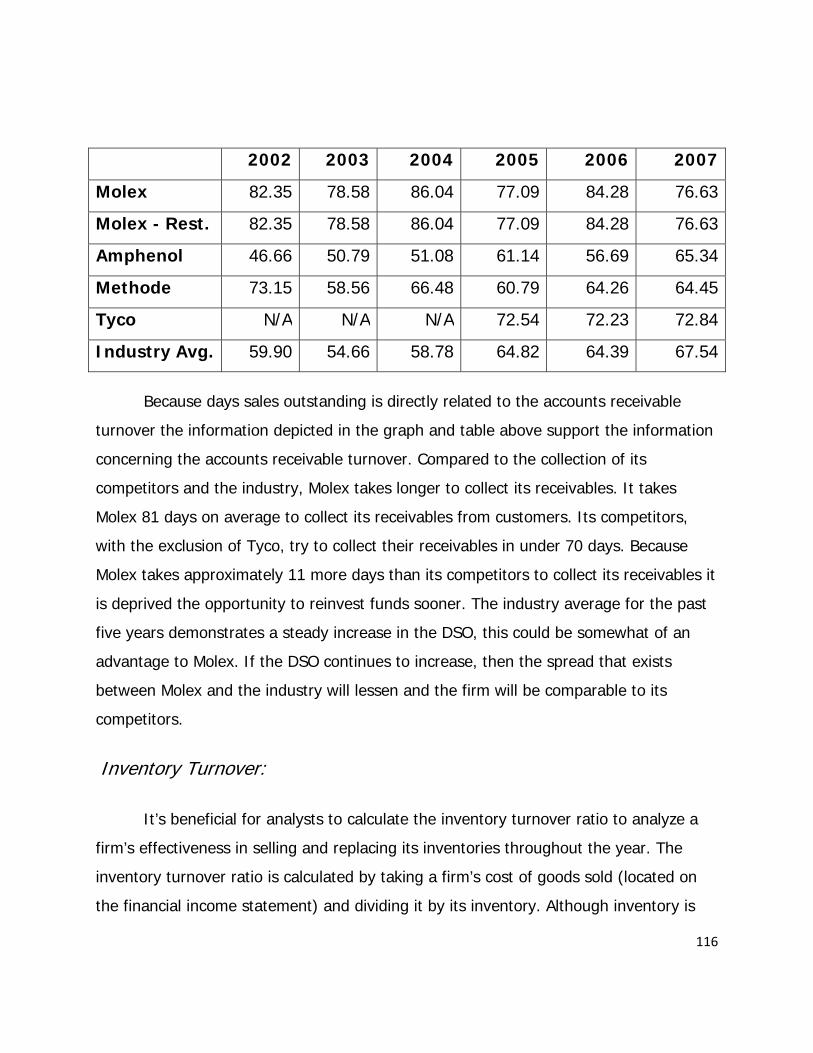

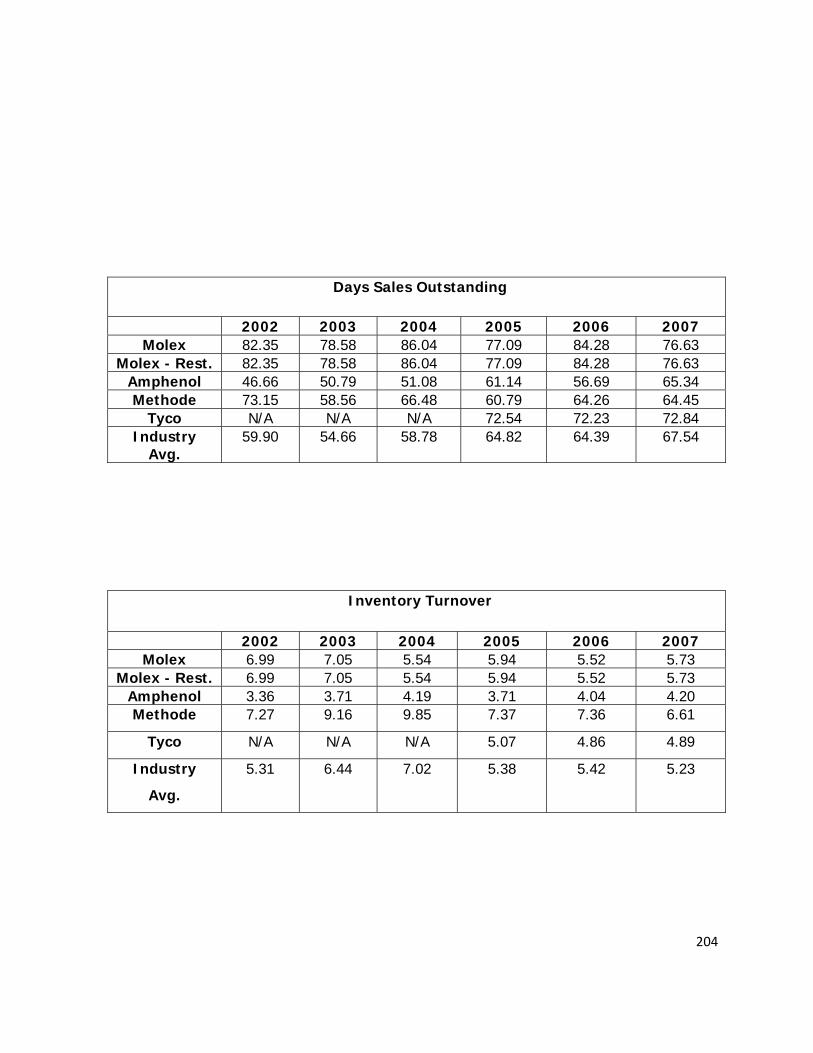

Days Sales Outstanding 115

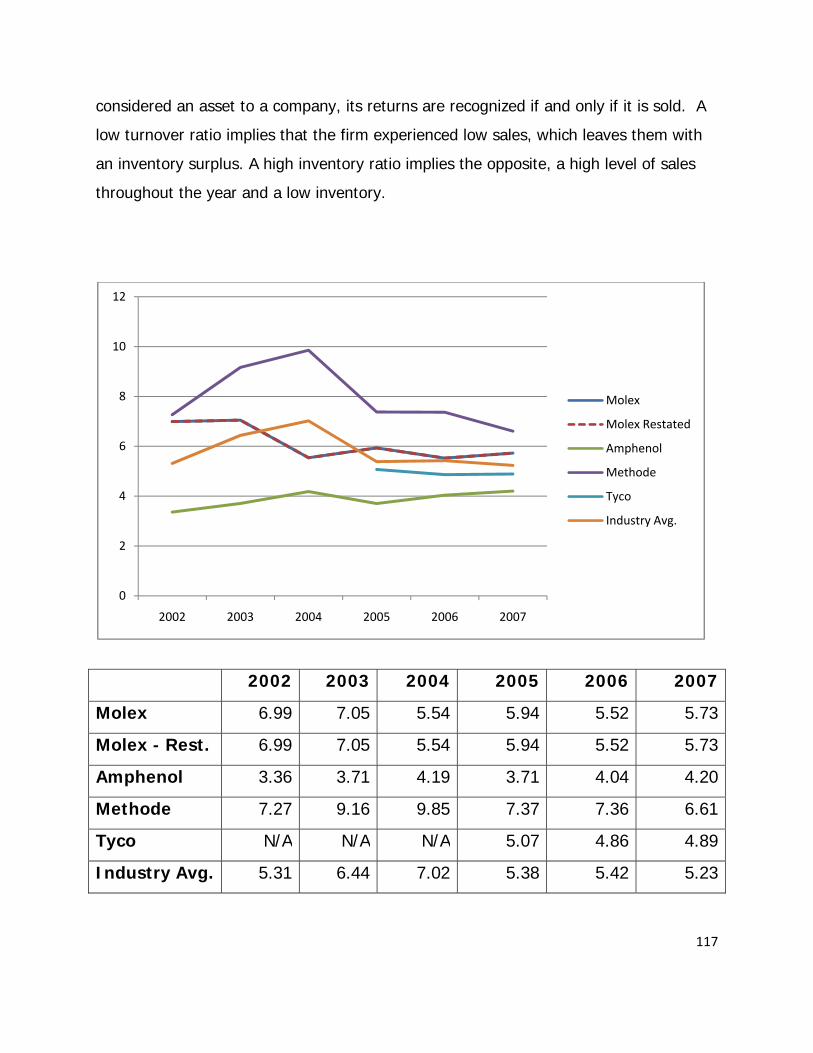

Inventory Turnover 116

Days Supply Inventory 118

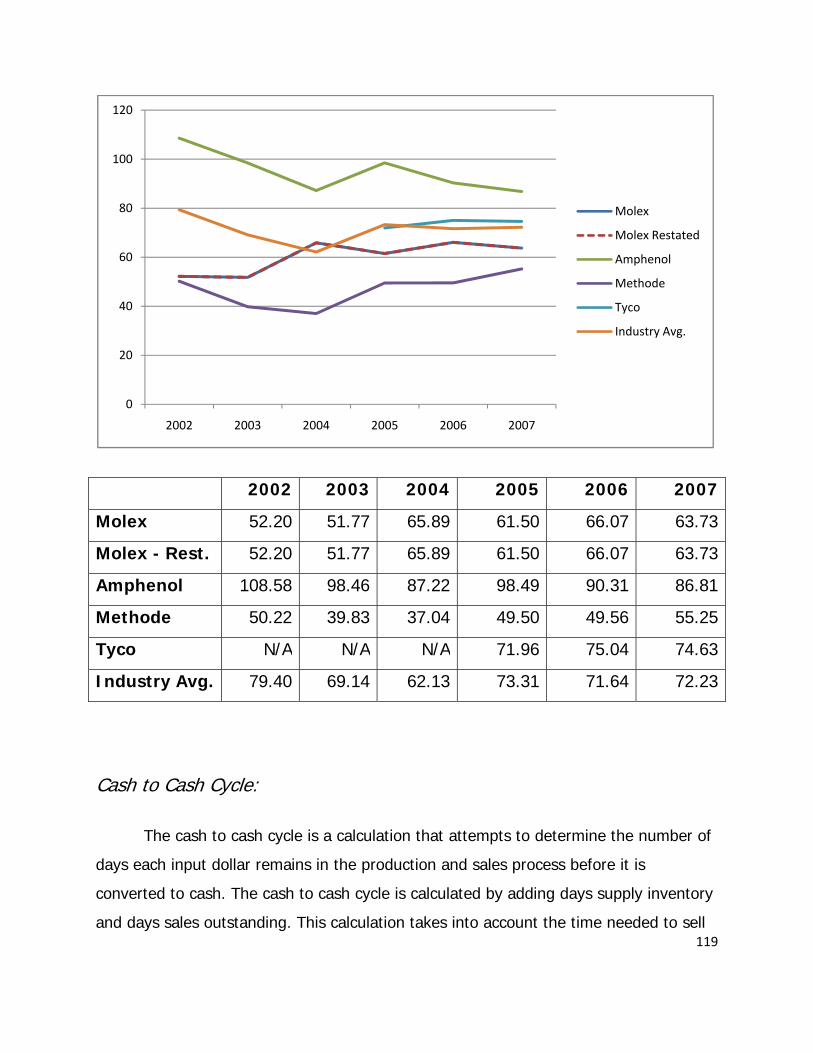

Cash to Cash Cycle 119

Conclusion 121

Profitability Analysis 122

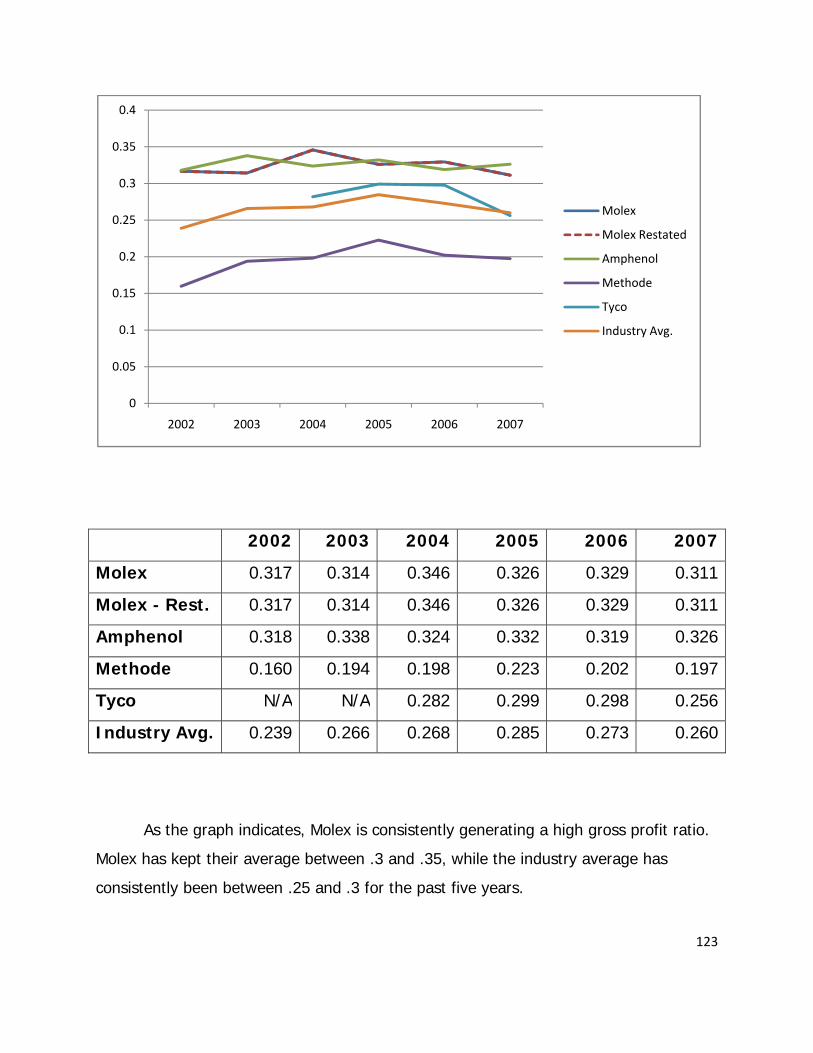

Gross Profit Margin 122

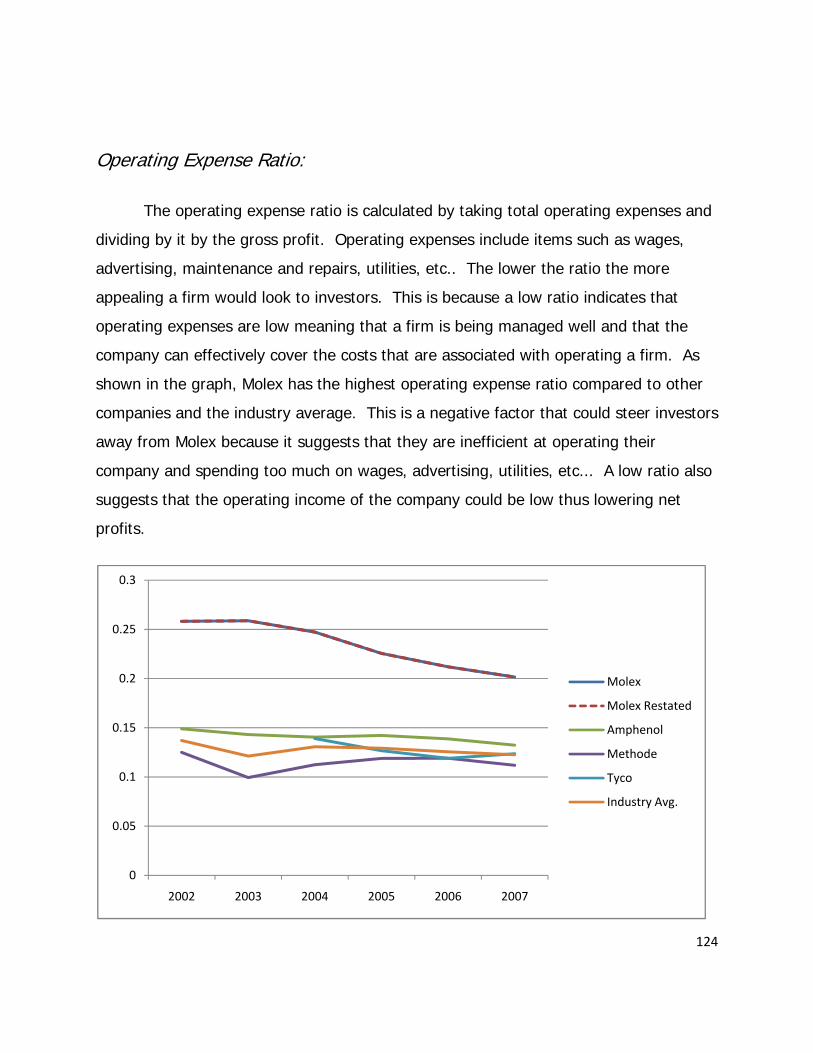

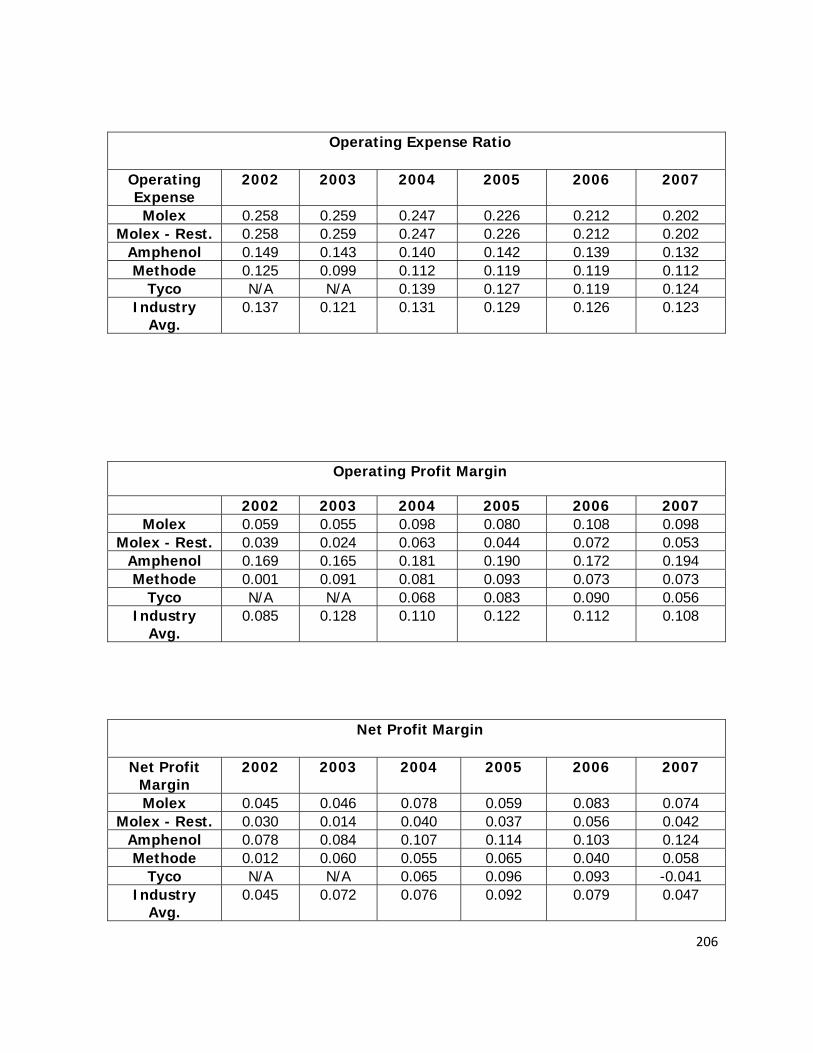

Operating Expense Ratio 124

Operating Profit Margin 125

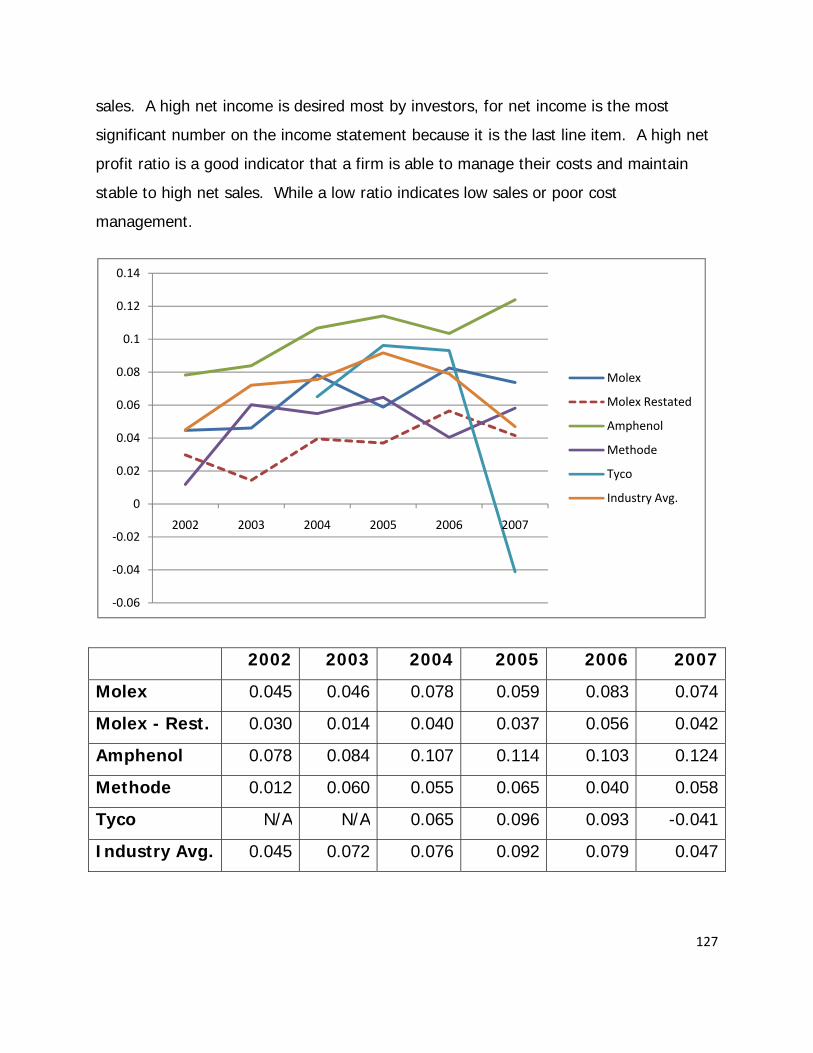

Net Profit Margin 126

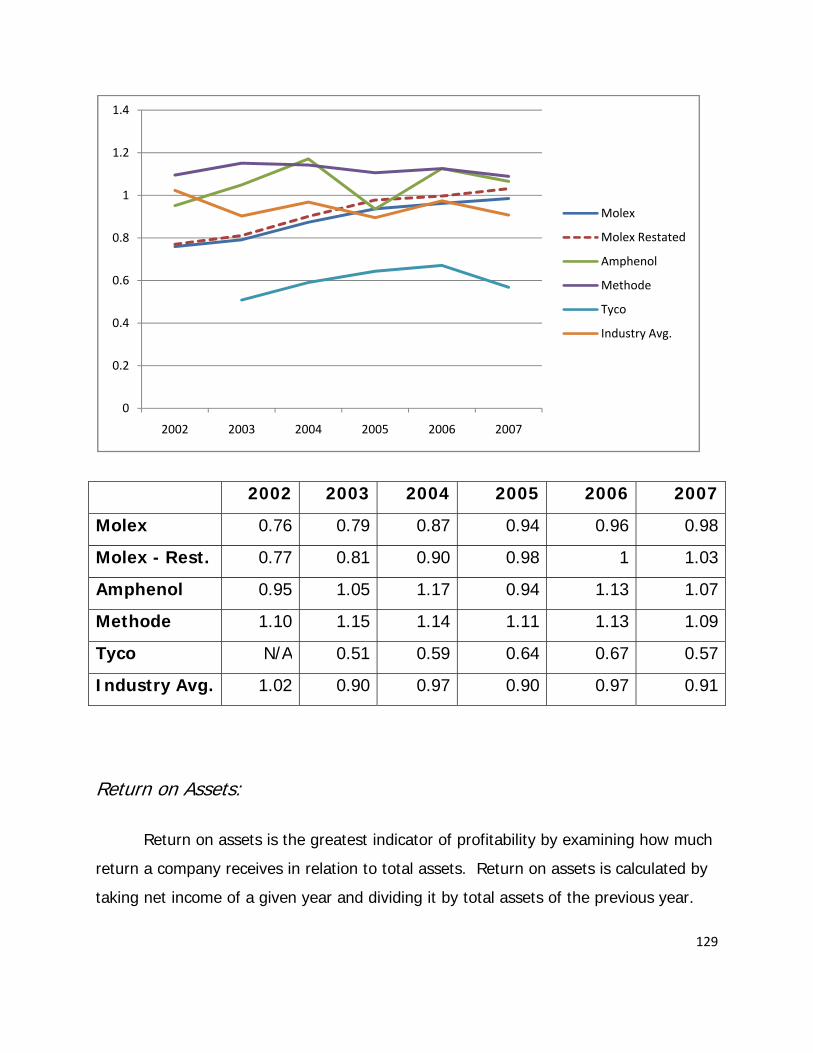

Asset Turnover 128

Return on Assets 129

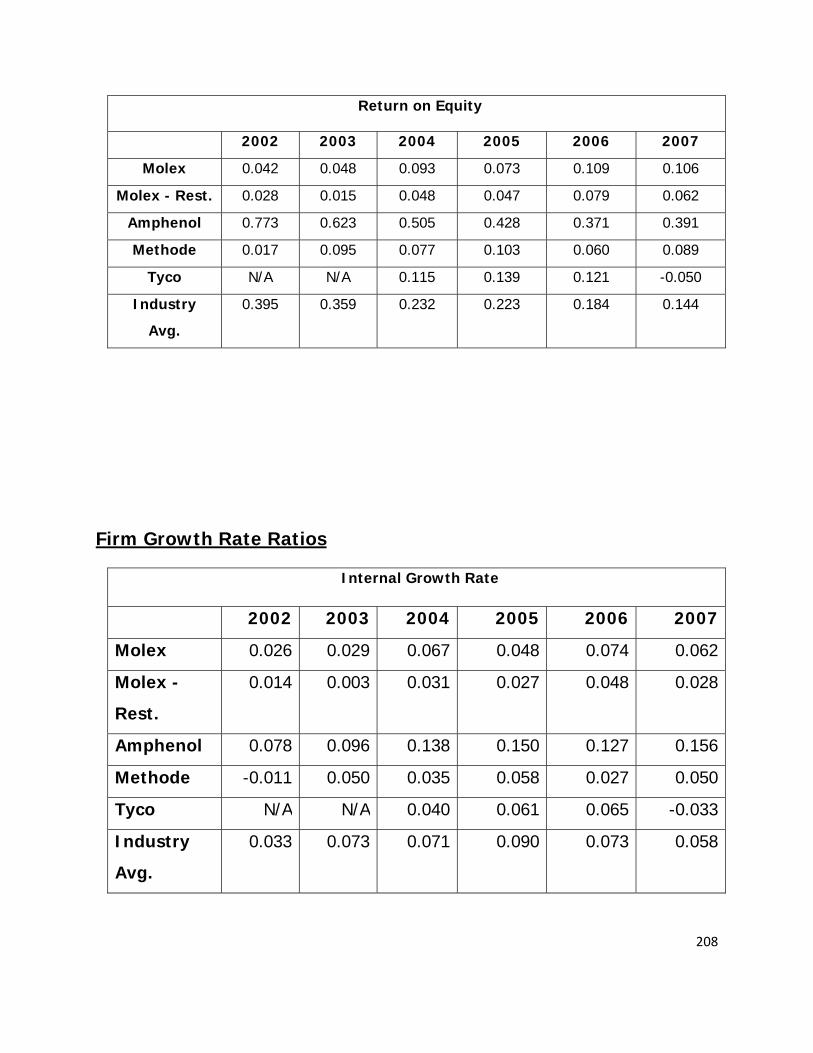

Return on Equity 131

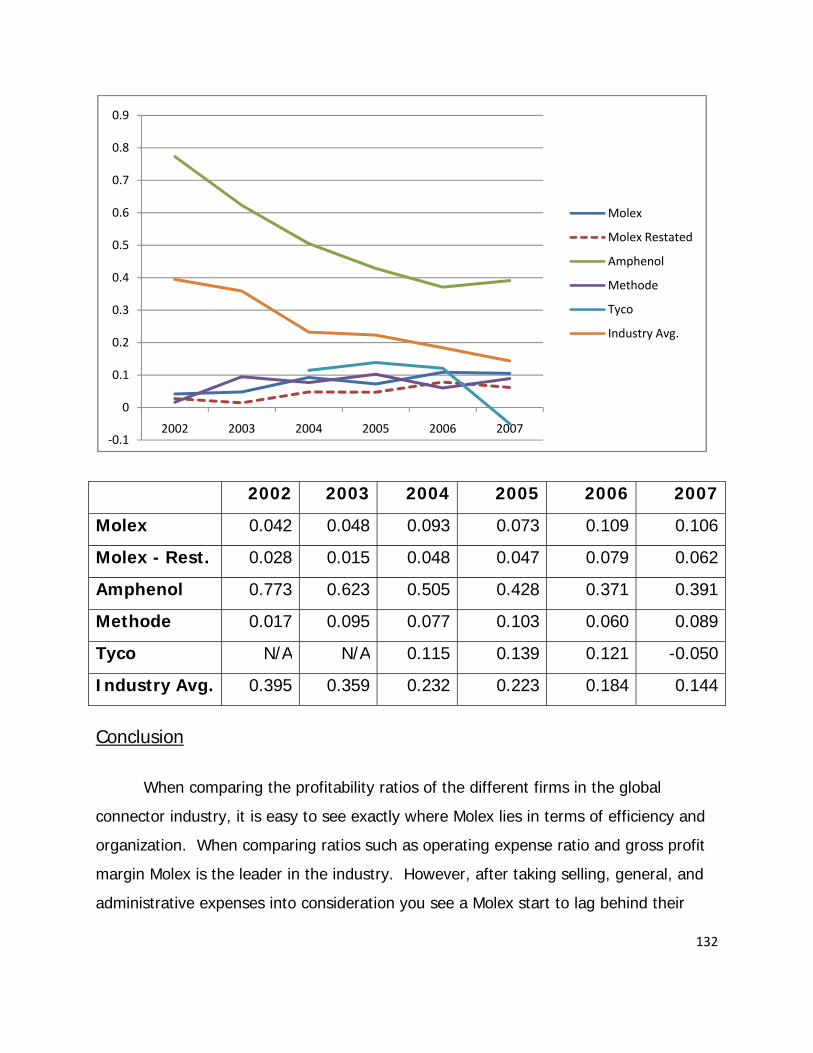

Conclusion 132

Firm Growth Rate Ratios 133

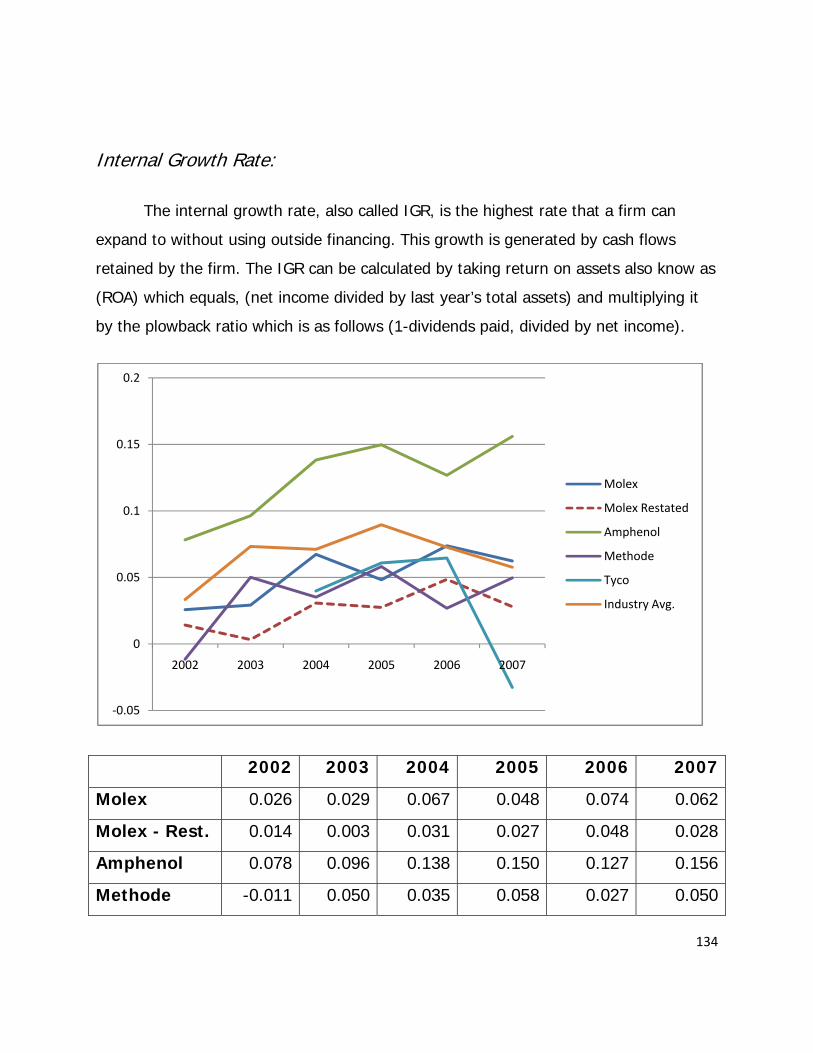

Internal Growth Rate 134

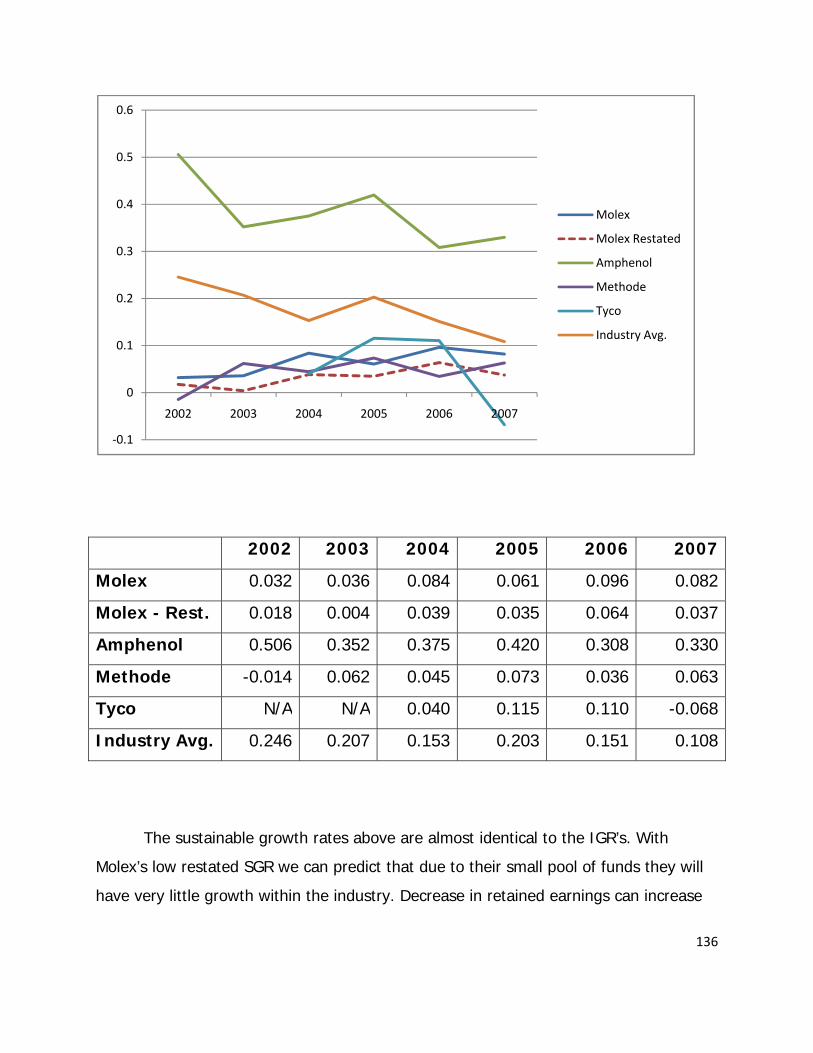

Sustainable Growth Rate 135

Conclusion 137

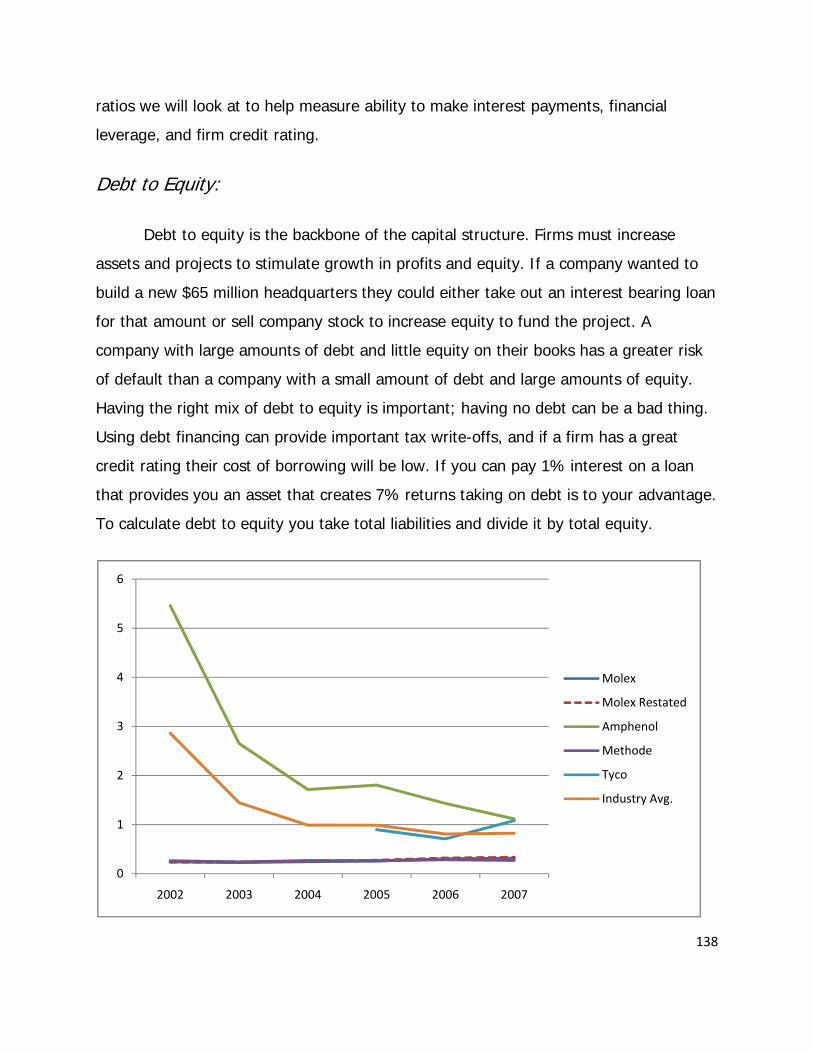

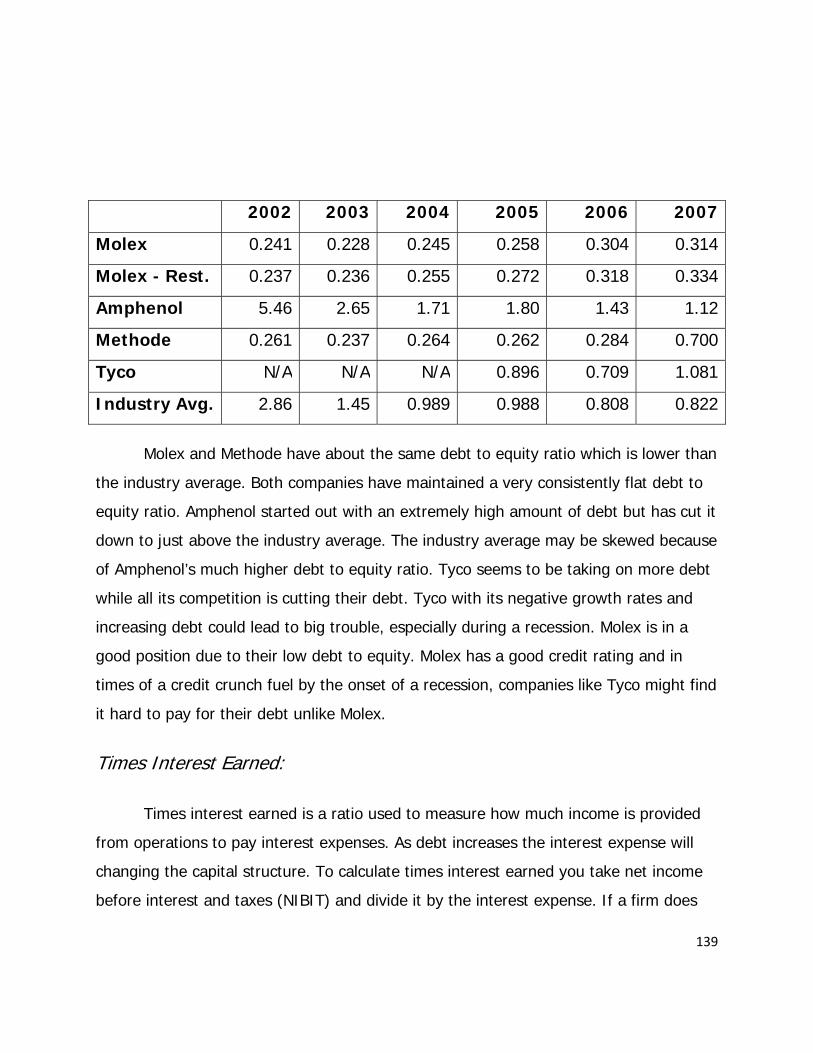

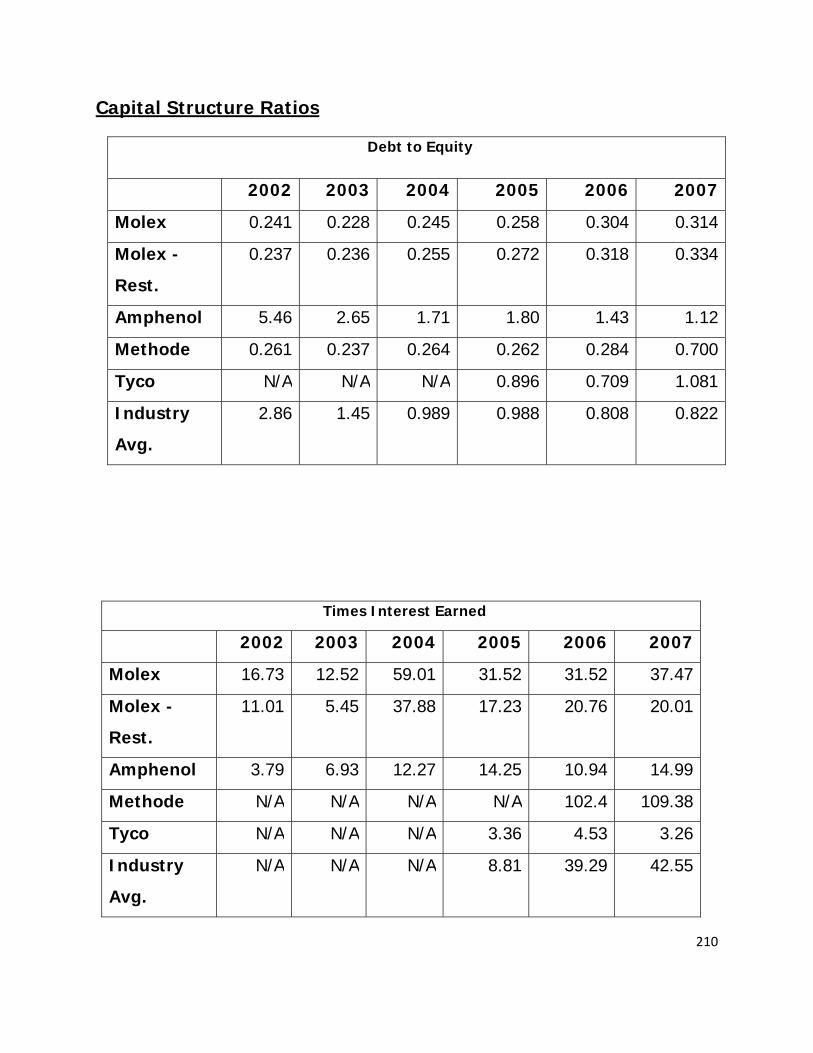

Capital Structure Analysis 137

Debt to Equity 138

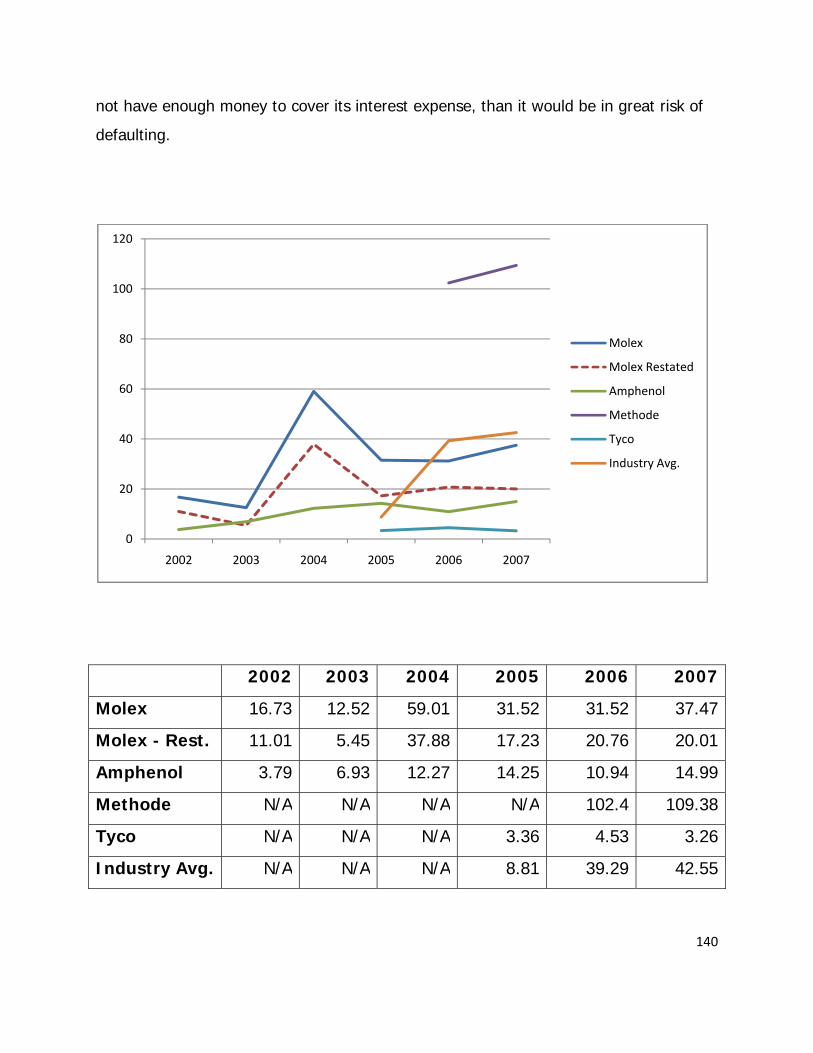

Times Interest Earned 139

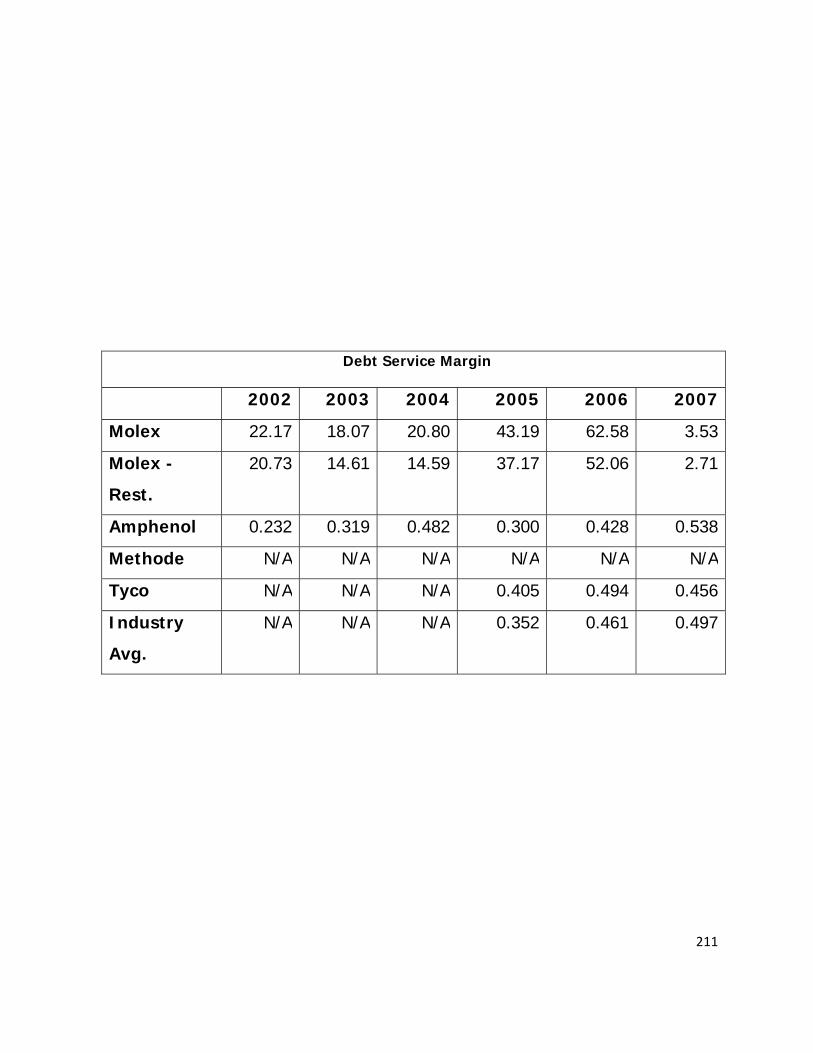

Debt Service Margin 141

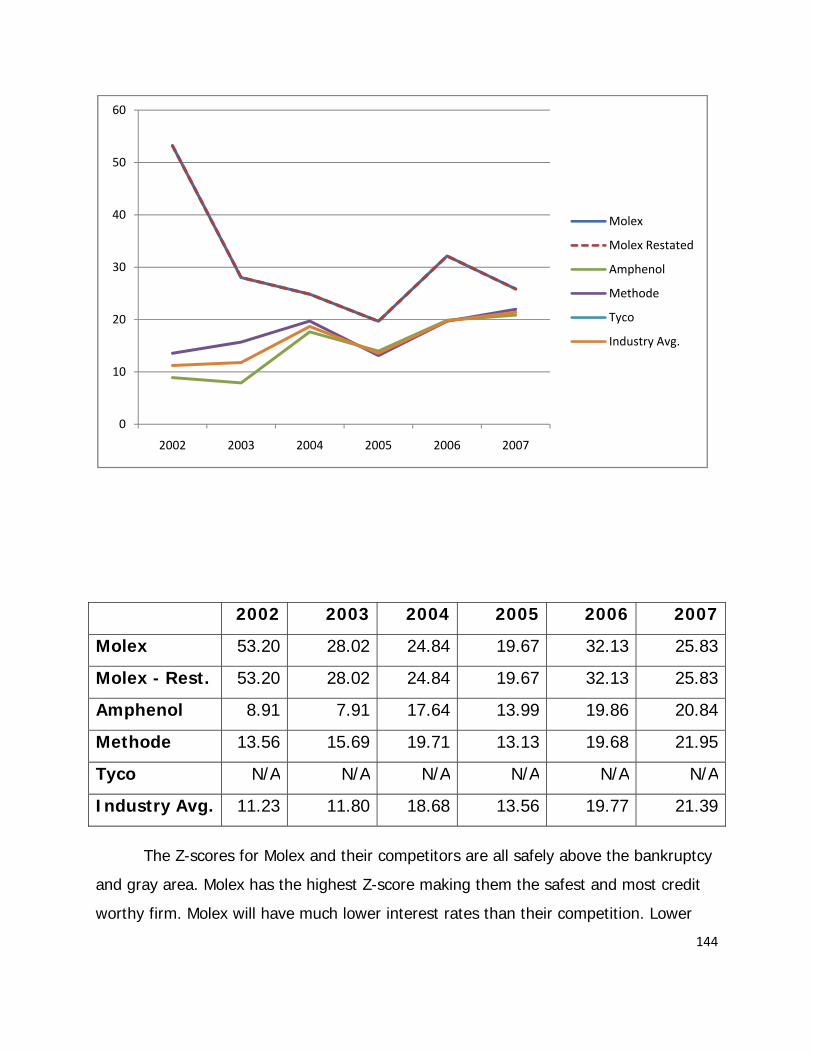

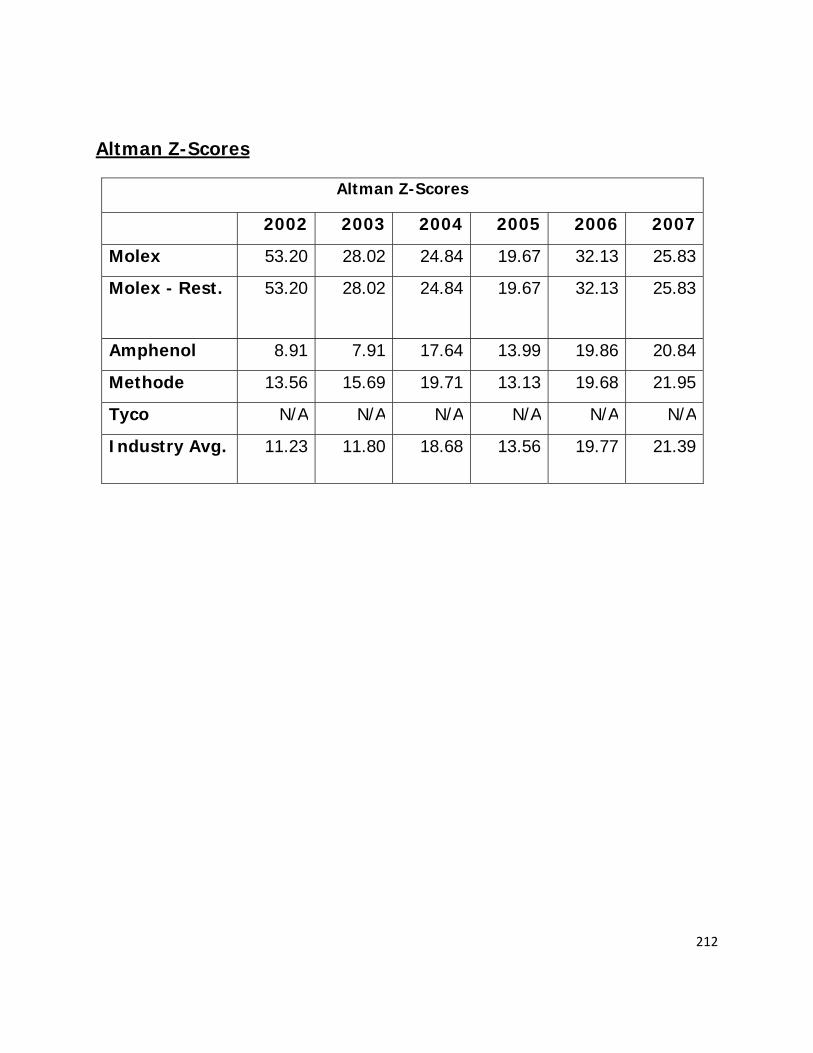

Z-scores 143

Conclusion 145

Estimating Cost of Capital 145

Cost of Equity 145

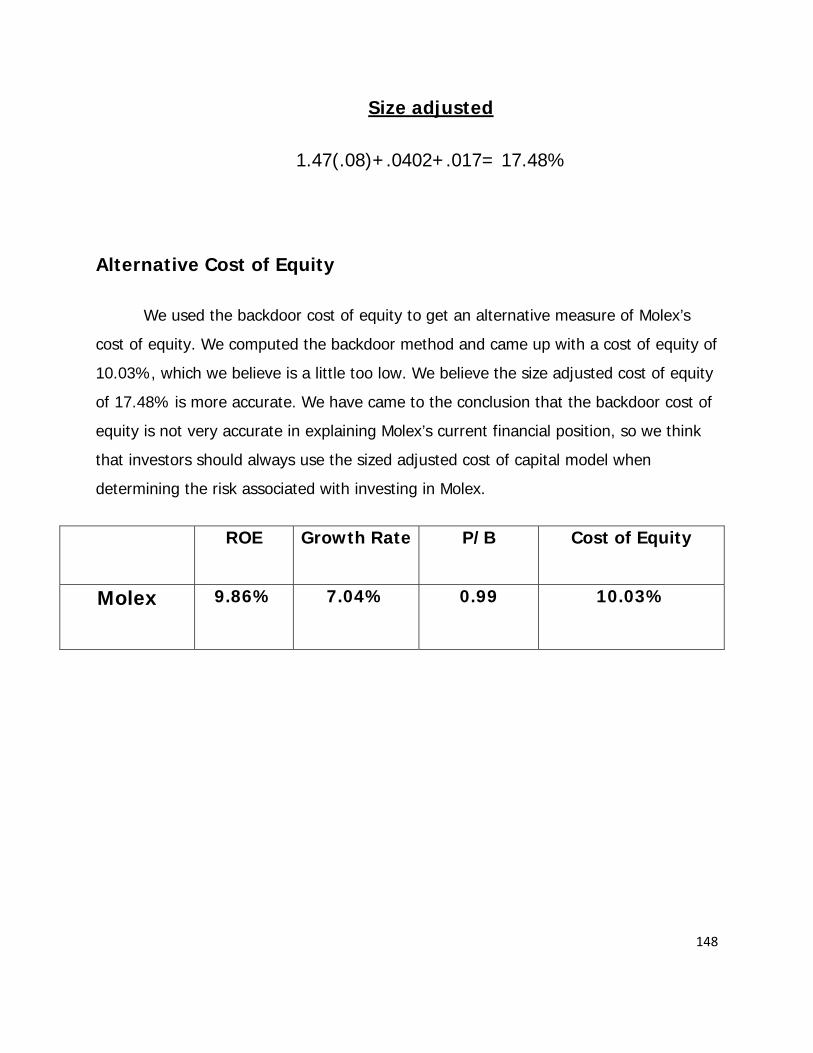

Size Adjusted 148

9

Alternative Cost of Equity 148

Cost of Debt 149

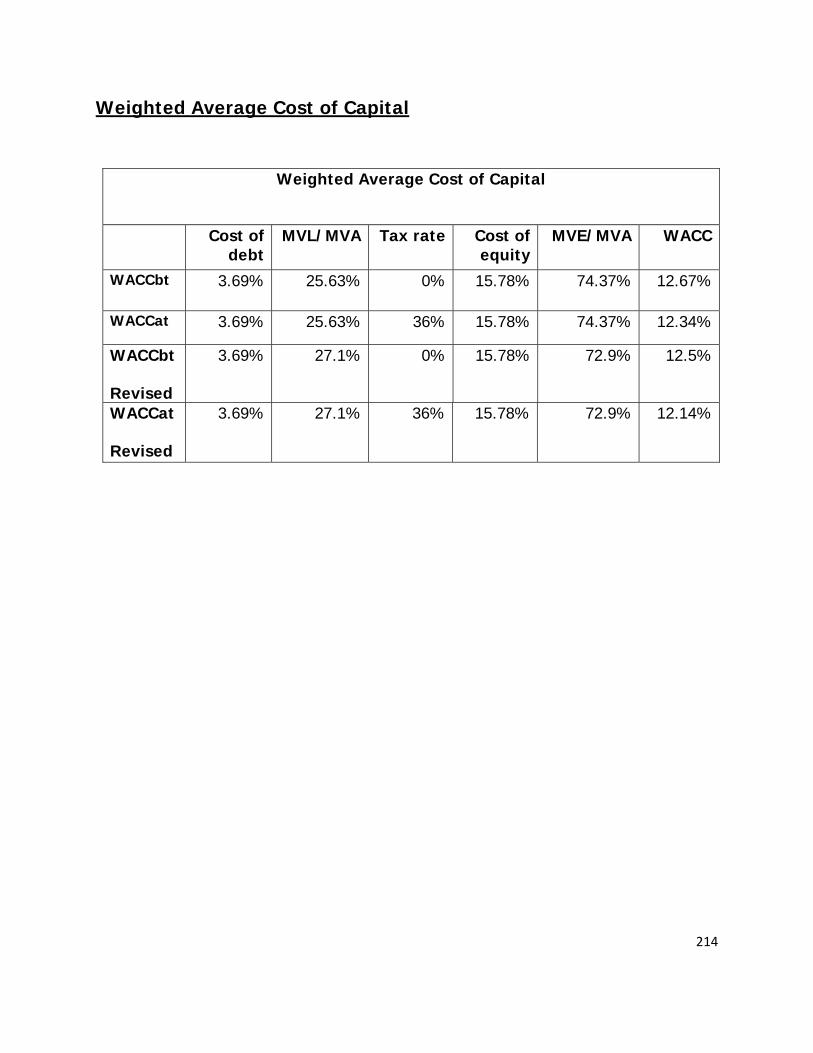

Weighted Average Cost of Capital 150

Financial Statement Forecasting 152

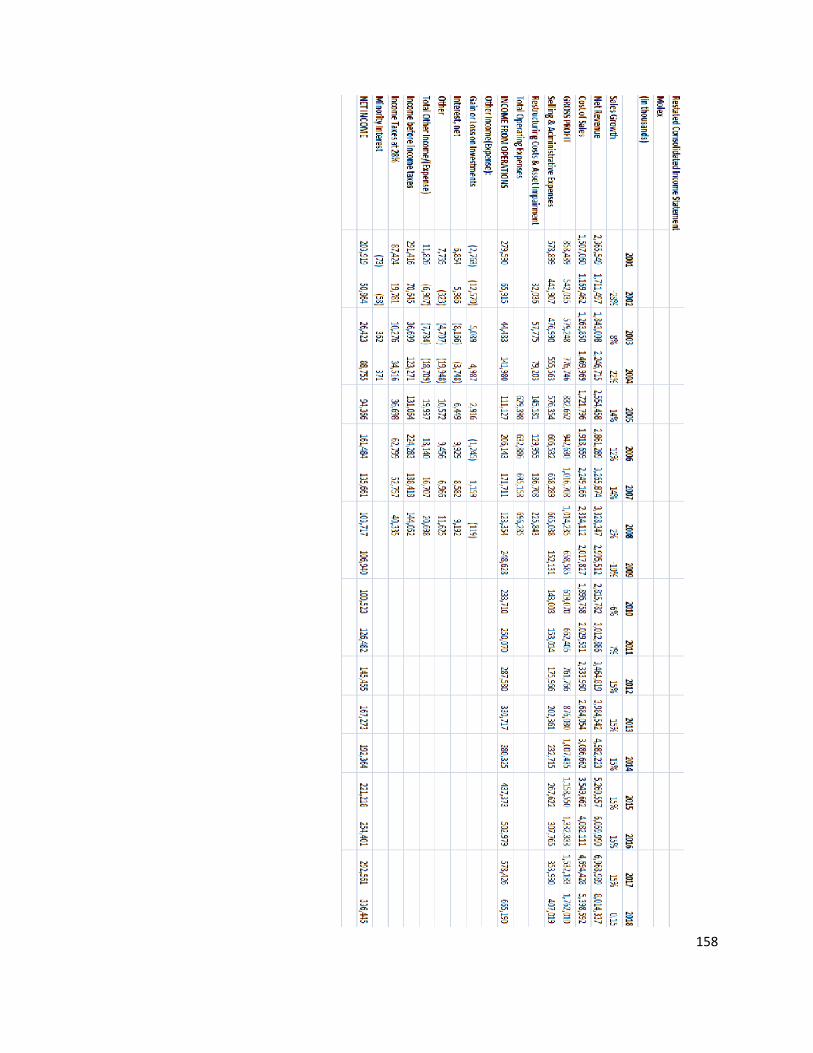

Income Statement 152

Income Statement (Restated) 157

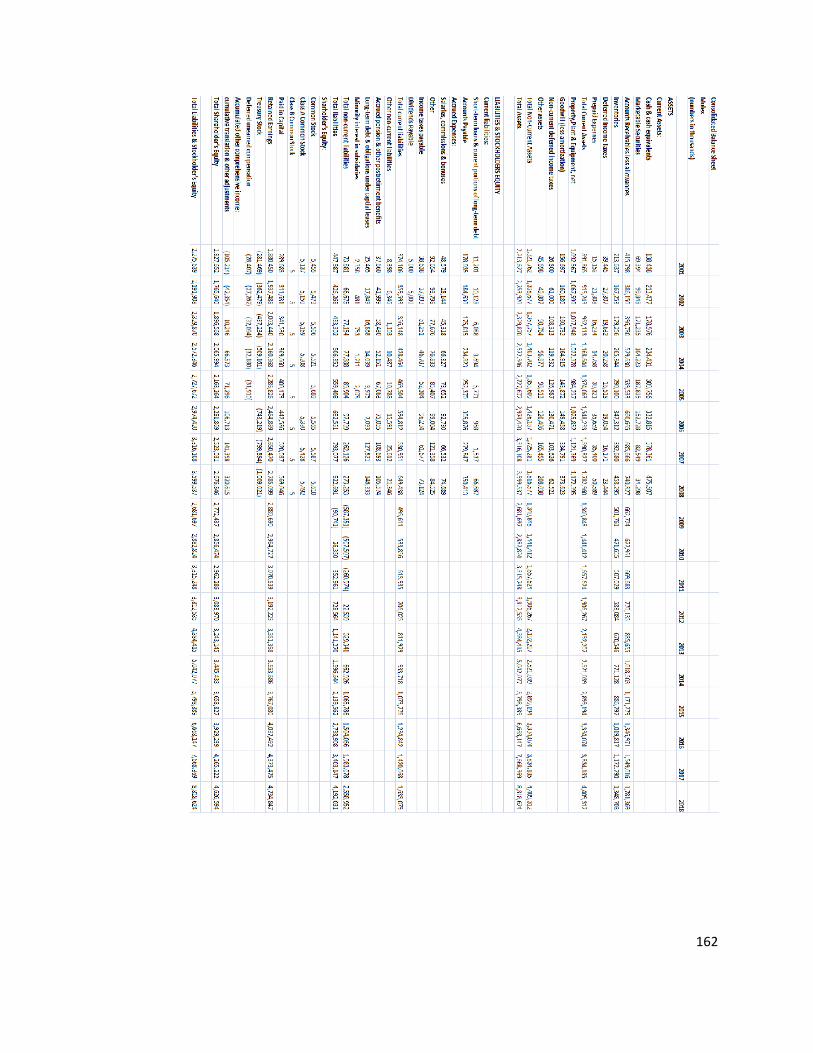

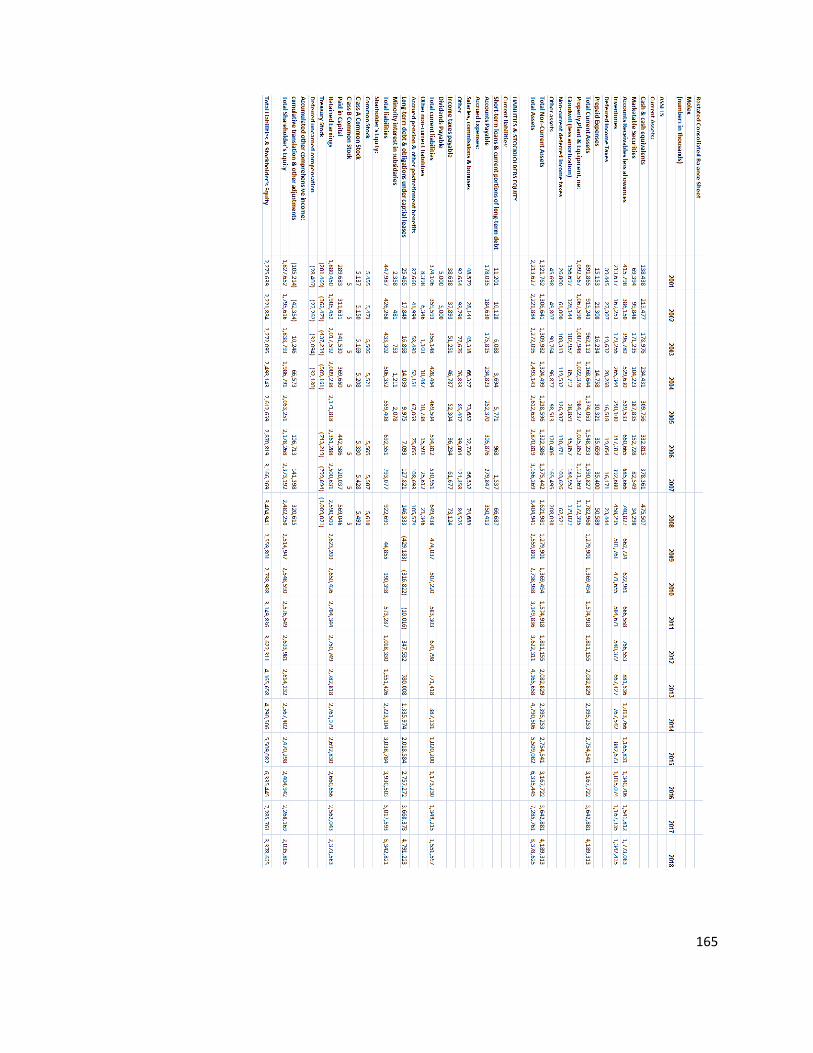

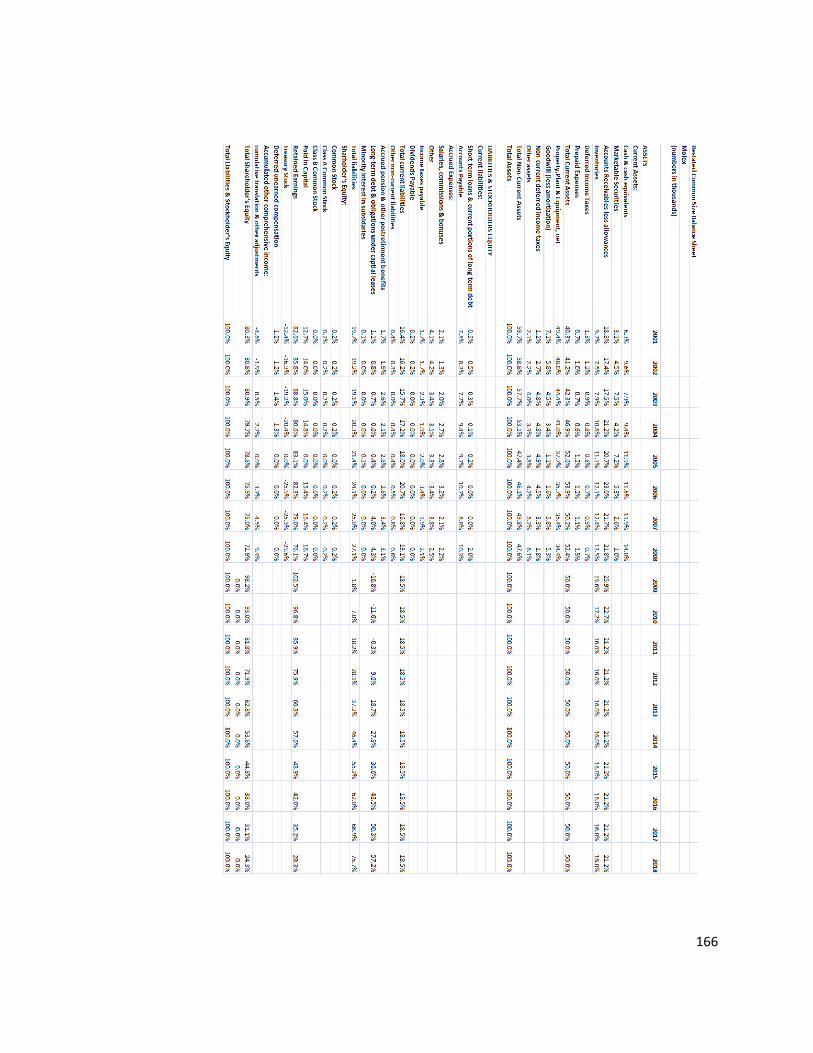

Balance Sheet 160

Balance Sheet (Restated) 164

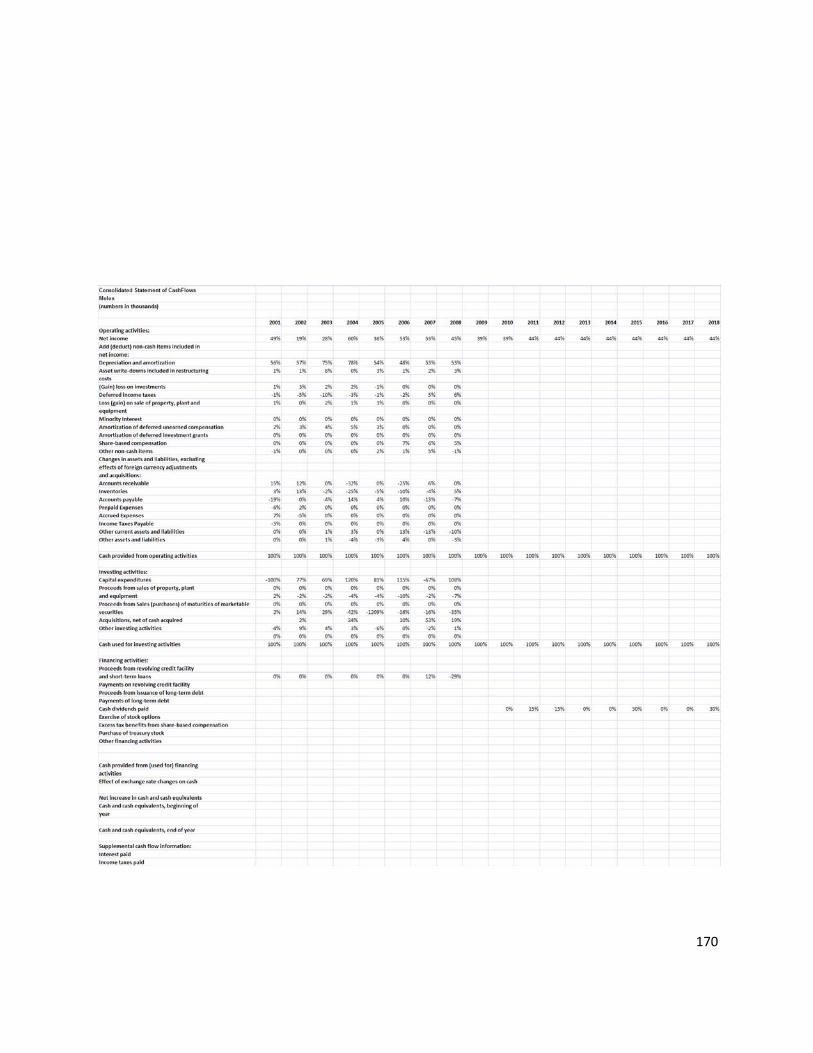

Statement of Cash Flows 167

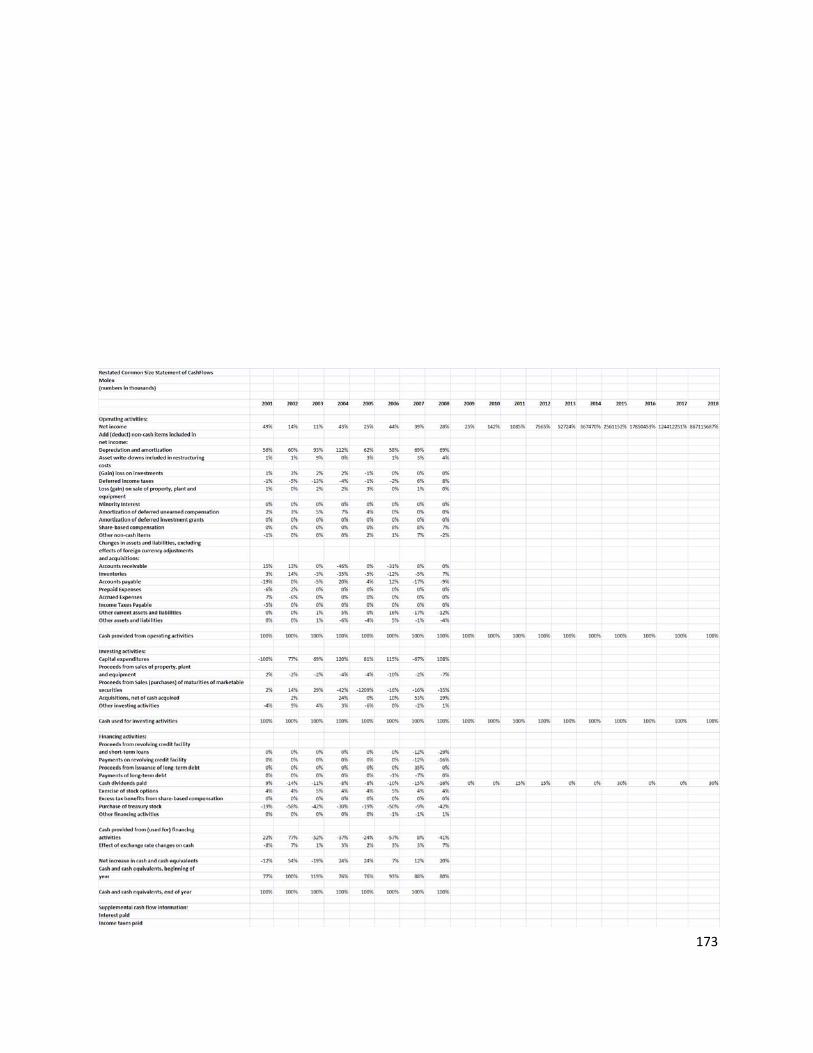

Statement of Cash Flows (Restated) 171

Valuation Analysis 174

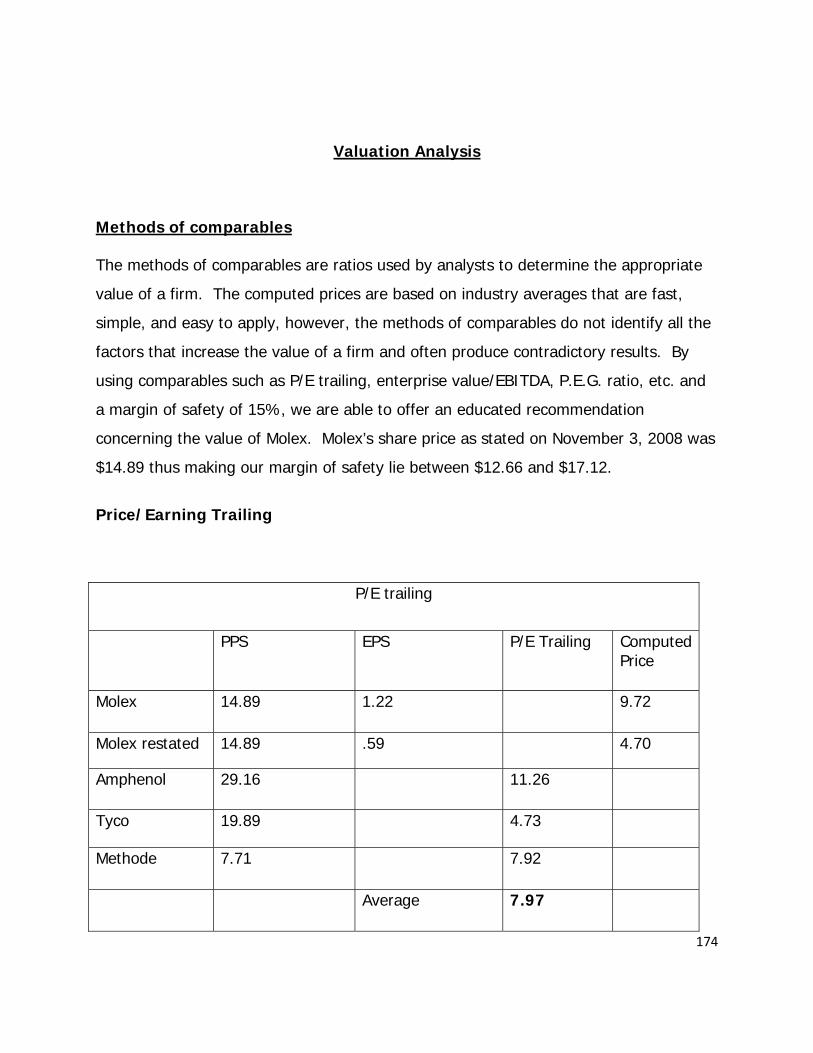

Method of Comparables 174

Price/Earnings Trailing 174

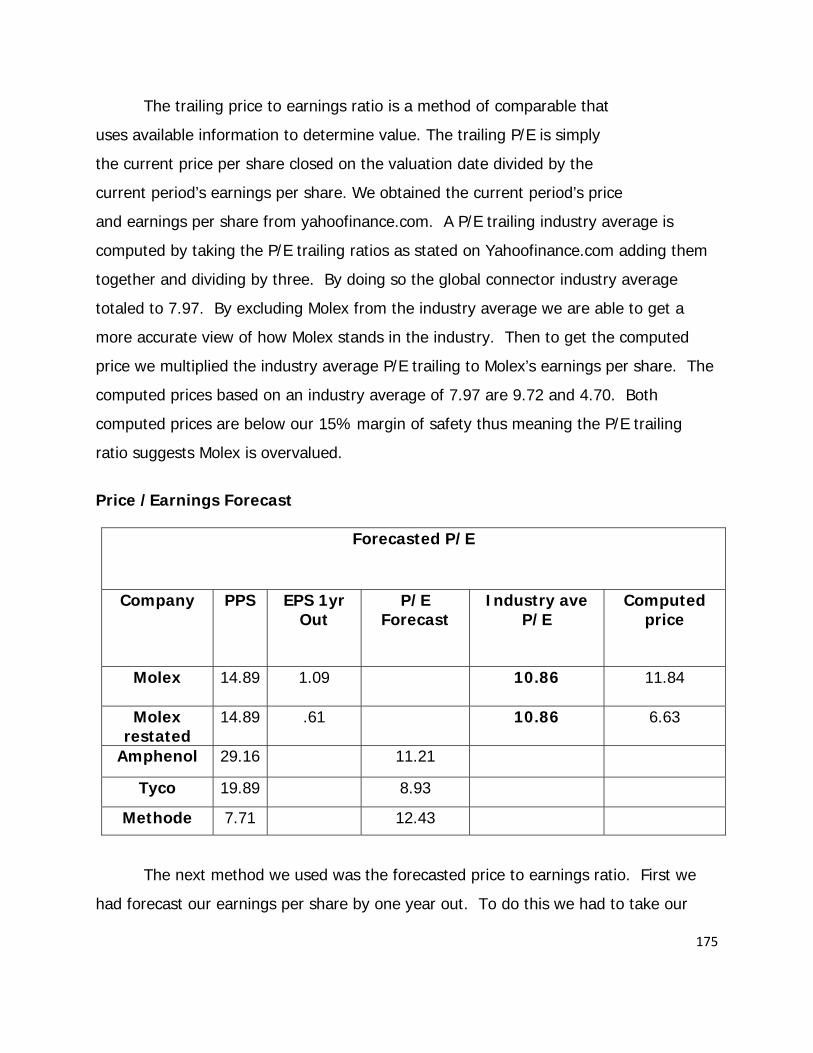

Price/Earnings Forecast 175

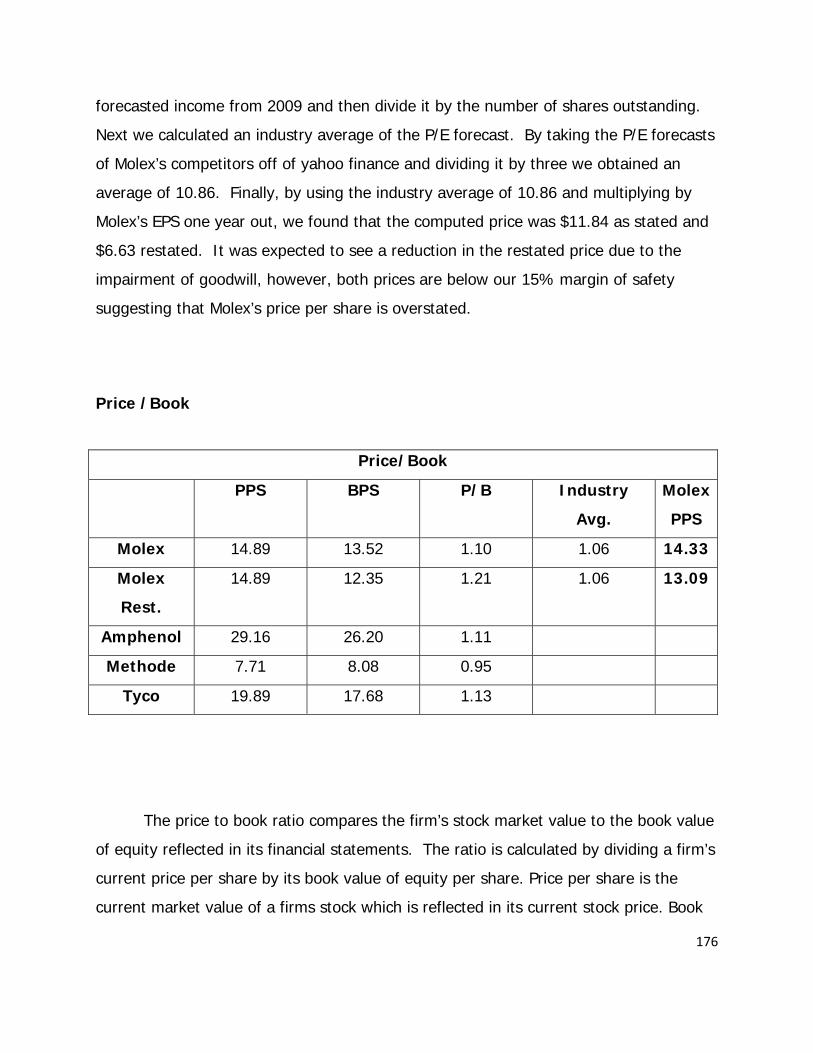

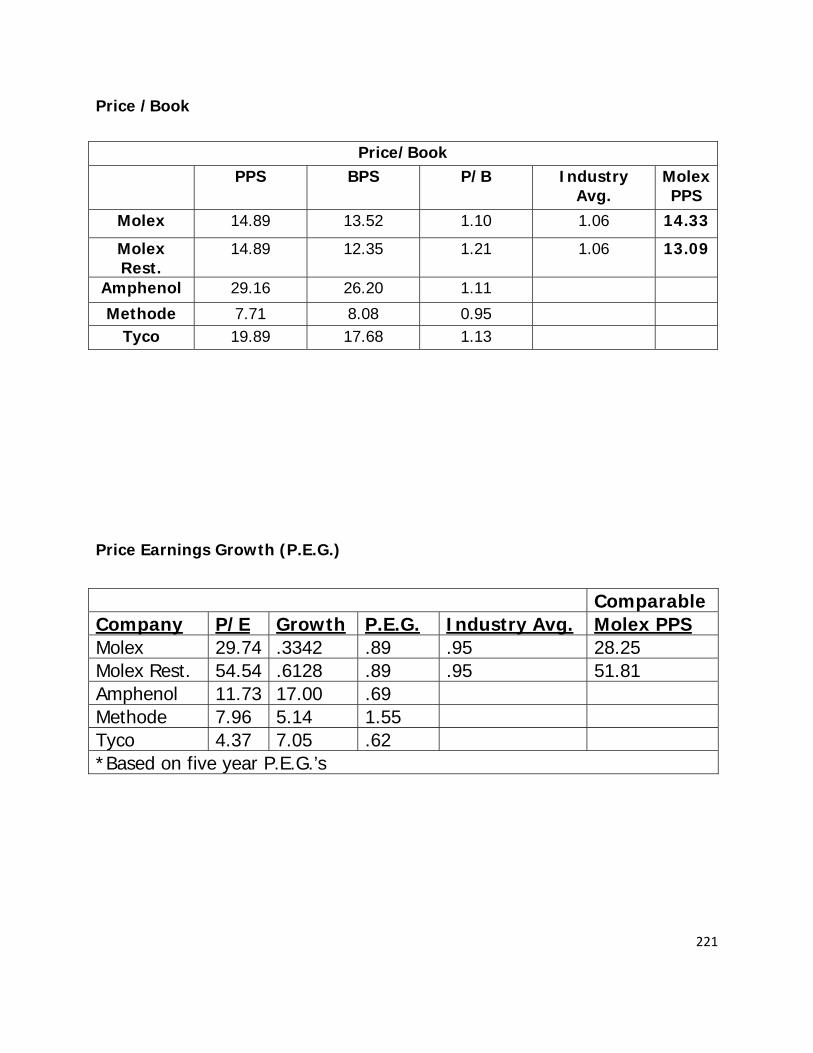

Price/Book 176

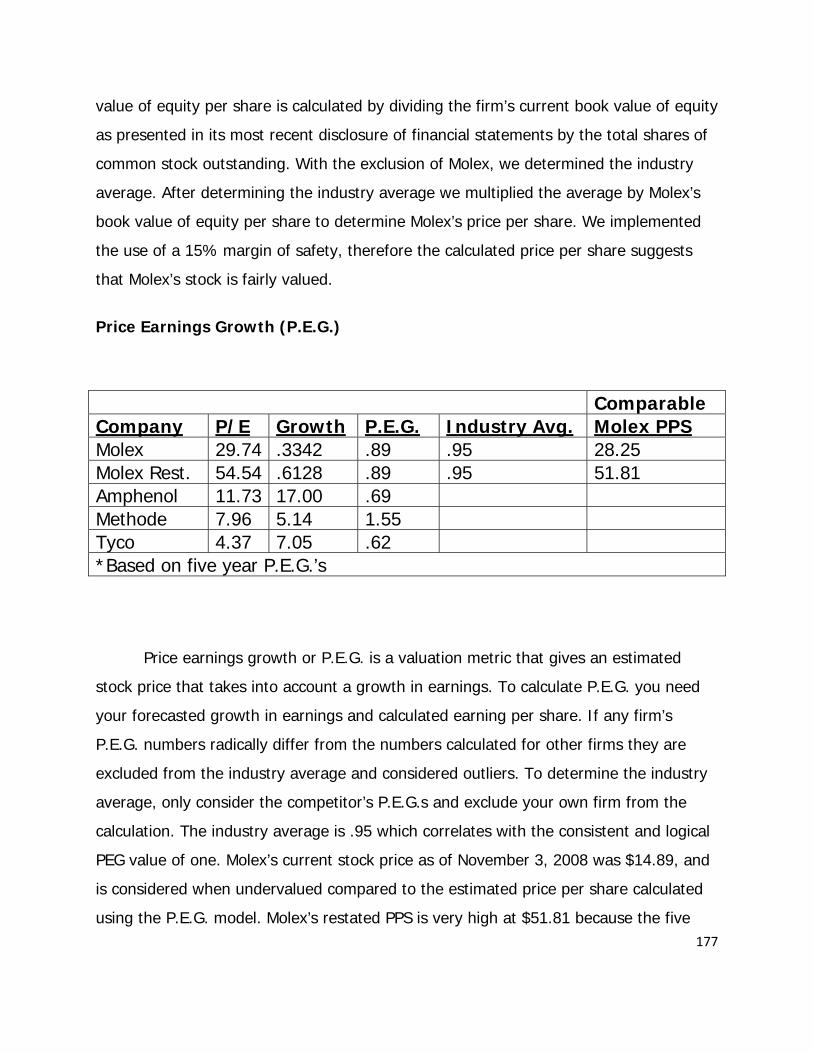

Price Earnings Growth (P.E.G.) 177

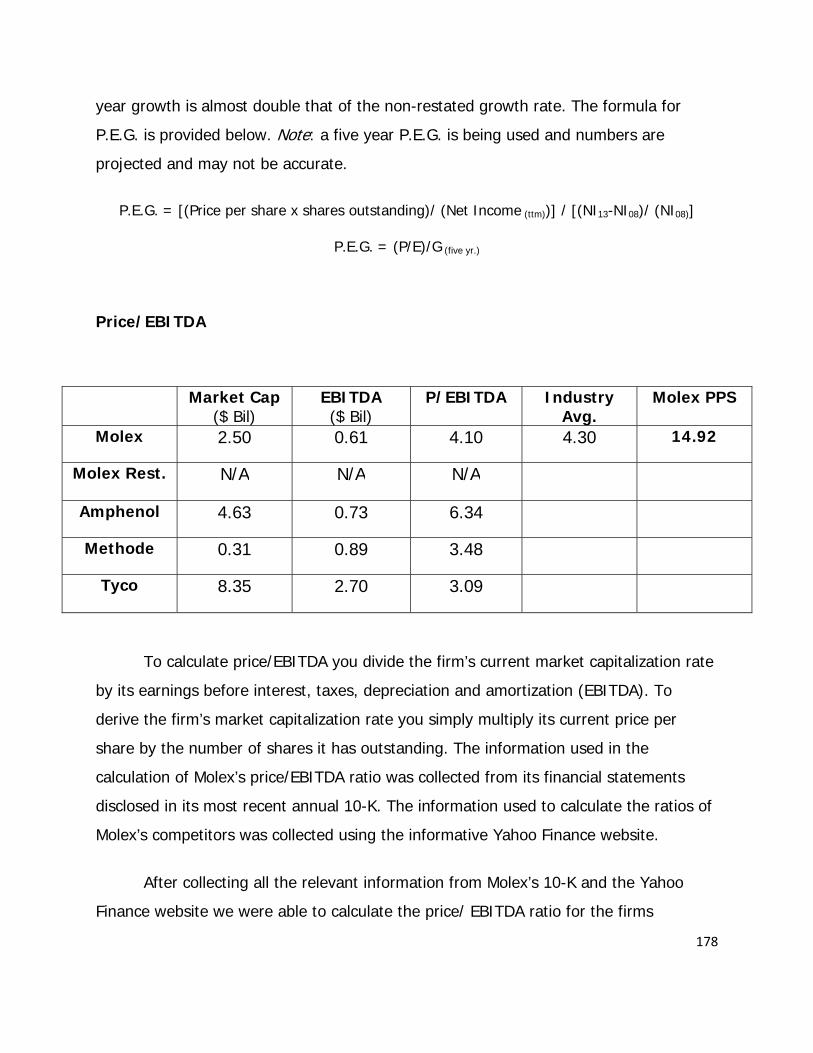

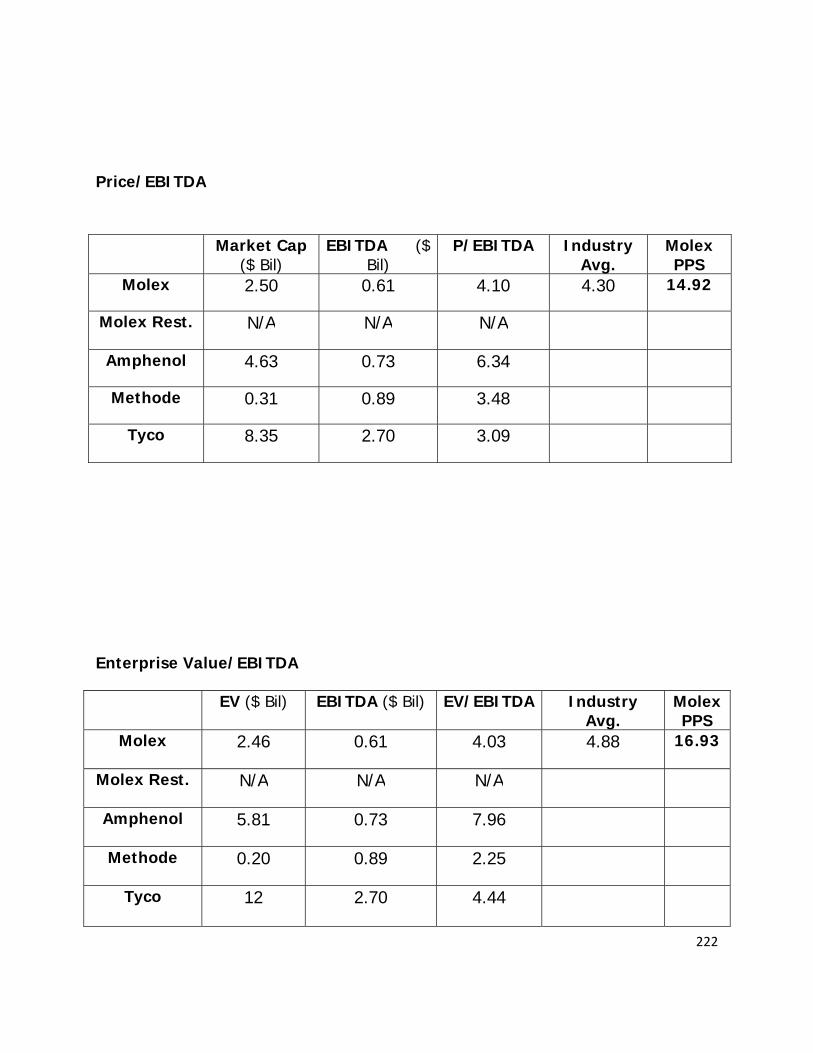

Price/EBITDA 178

Enterprise Value/EBITDA 179

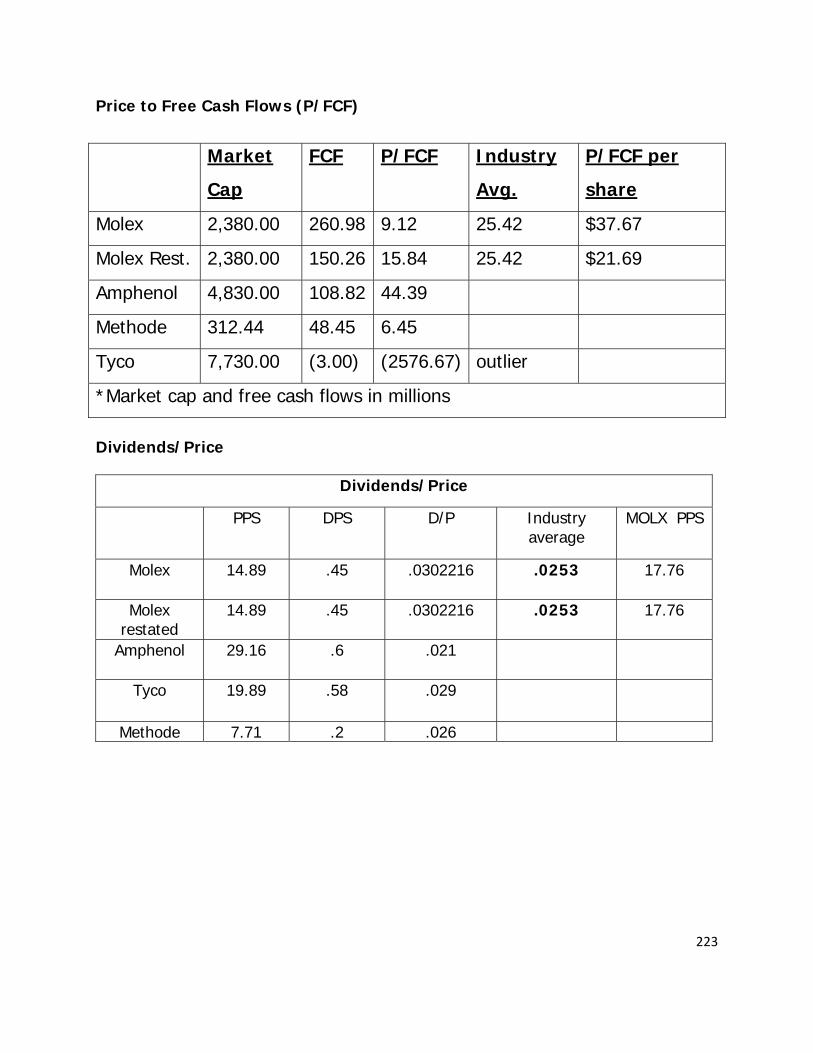

Price/Free Cash Flows 180

Dividends/Price 182

Conclusion 182

10

Intrinsic Valuation Models 183

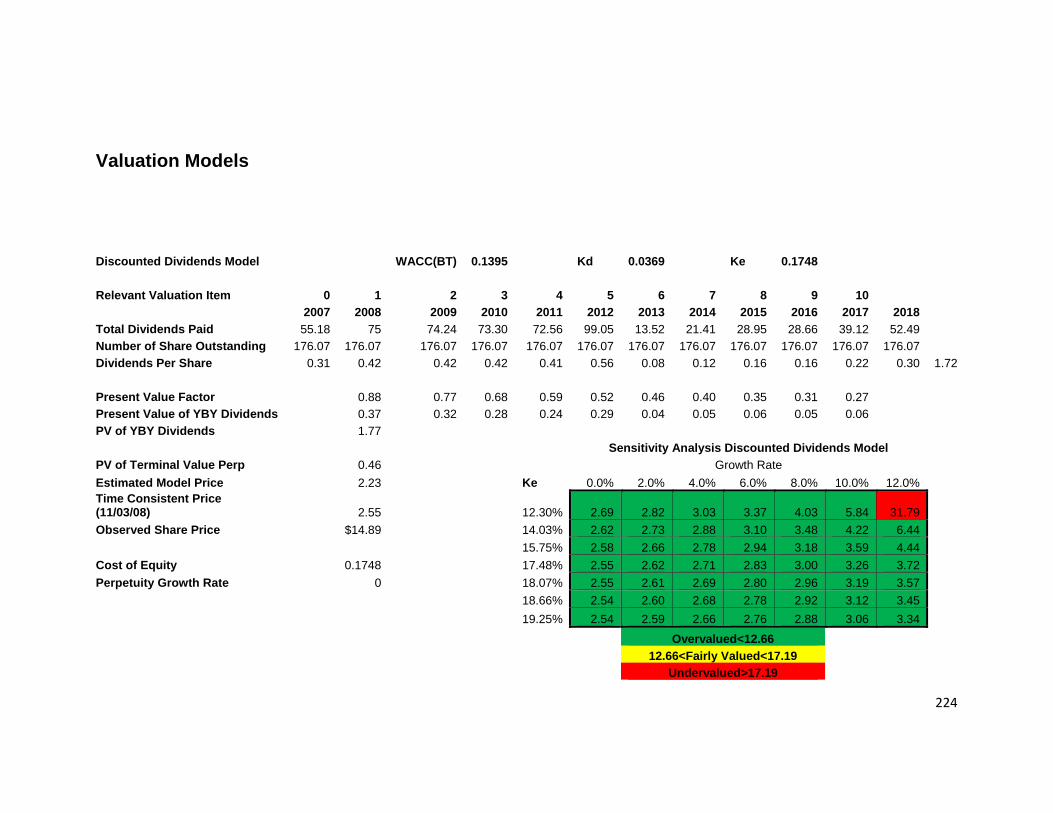

Discounted Dividends Model 183

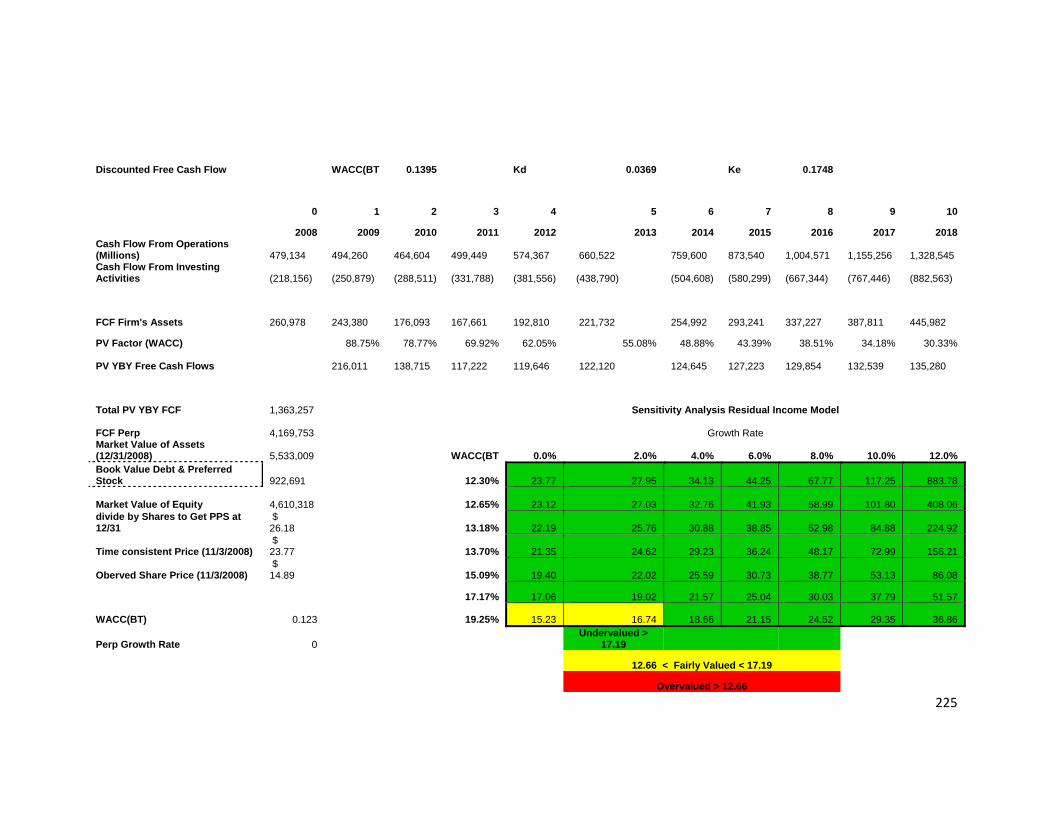

Discounted Free Cash Flows Model 185

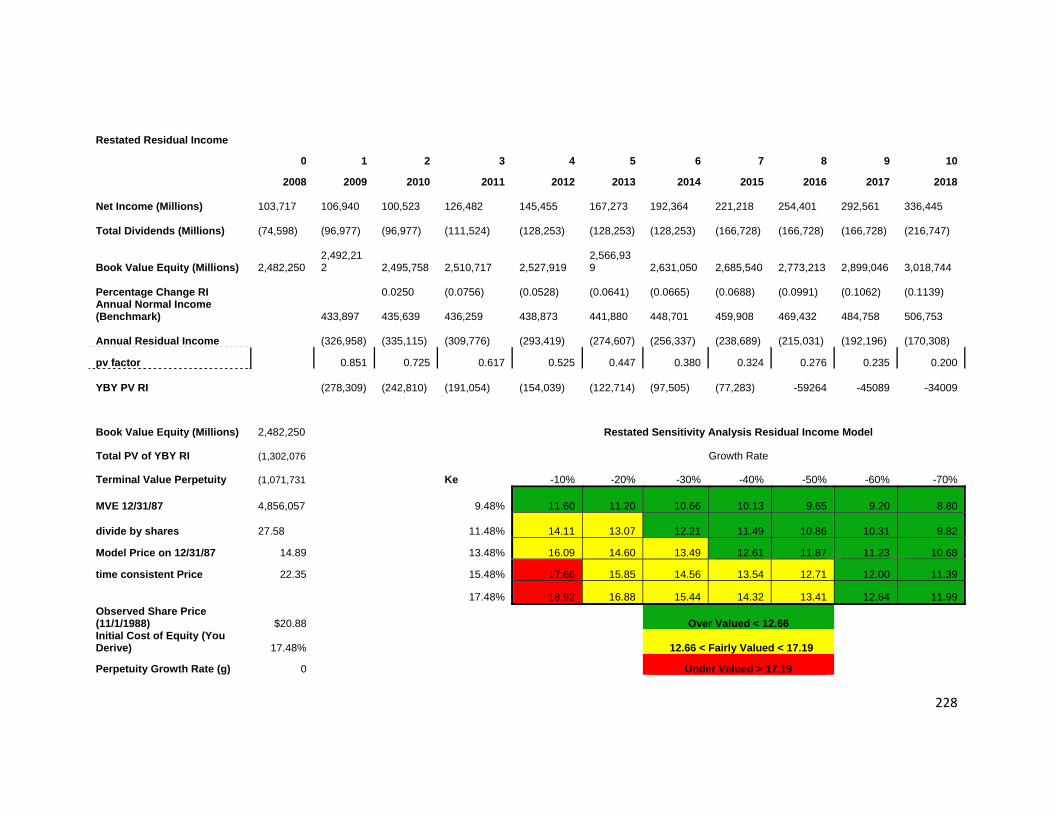

Residual Income Model 187

Abnormal Earnings Growth Model (A.E.G.) 190

Long Run Residual Income Model 192

Analyst Recommendations 196

Appendices 198

Sales Manipulation Diagnostic Ratios 198

Expense Manipulation Diagnostic Ratios 199

Liquidity Ratios 202

Profitability Ratios 205

Firm Growth Rate Ratios 208

Capital Structure Ratios 210

Altman Z-Scores 212

Cost of Debt 213

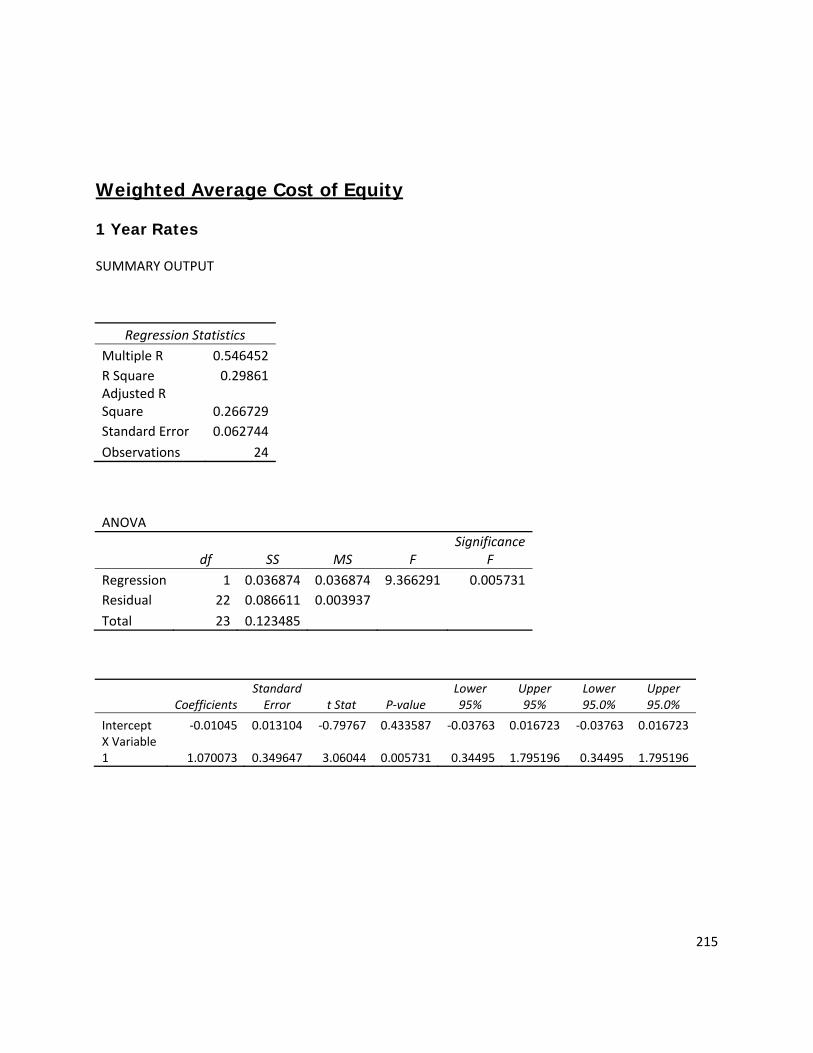

Weighted Average Cost of Capital 214

Weighted Average Cost of Equity 215

11

Year 1 Rates 215

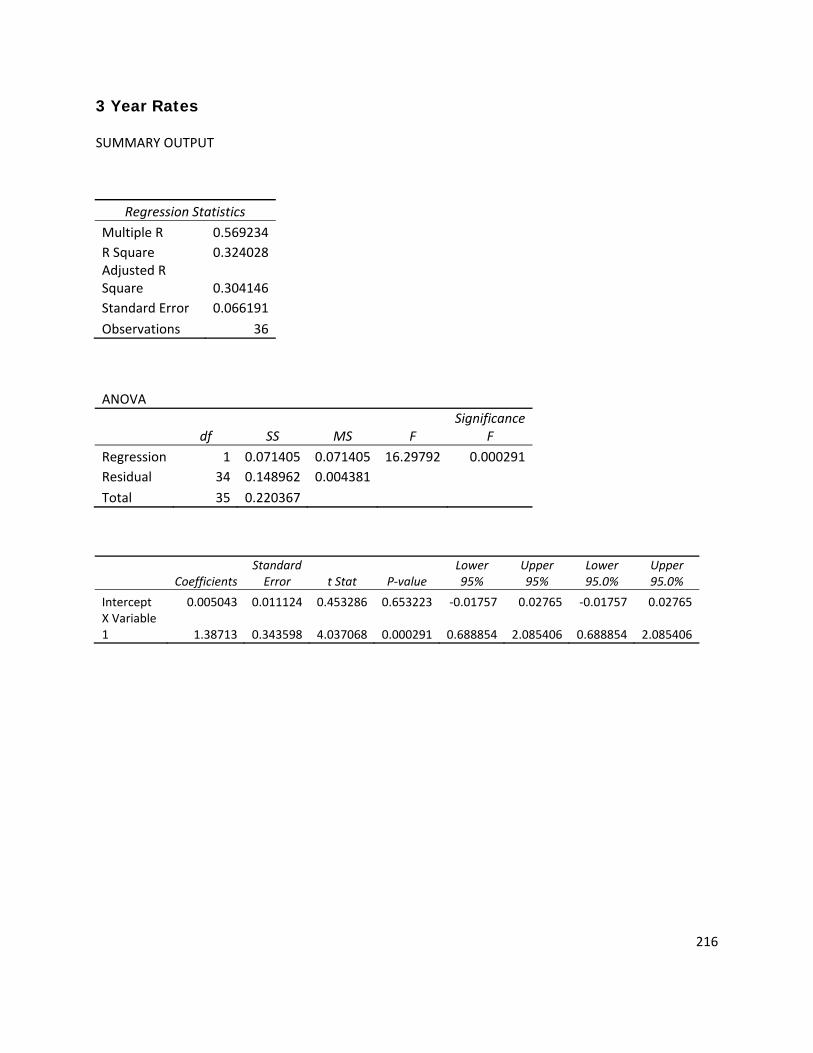

Year 3 Rates 216

Year 4 Rates 217

Year 5 Rates 218

Year 6 Rates 219

Methods of Comparables 220

Intrinsic Valuation Models 224

Works Cited 238

12

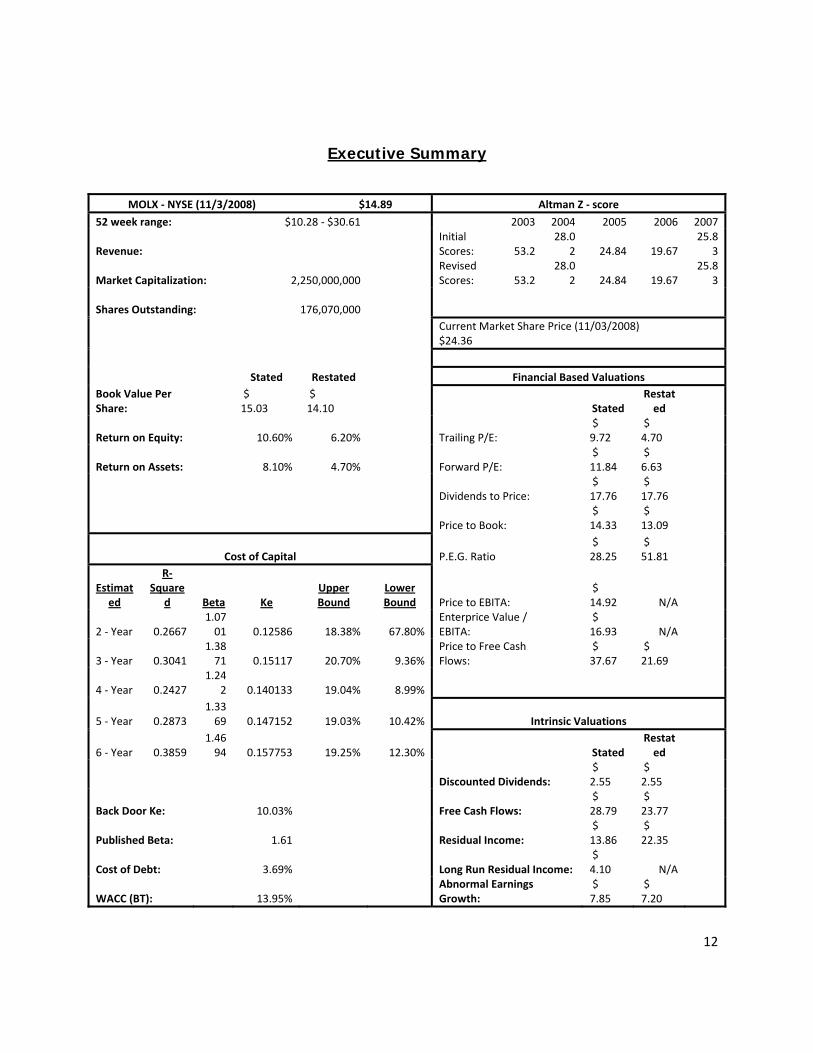

Executive Summary

MOLX ‐ NYSE (11/3/2008) $14.89 Altman Z ‐ score

52 week range: $10.28 ‐ $30.61 2003 2004 2005 2006 2007

Revenue: Initial Scores: 53.2

28.02 24.84 19.67

25.83

Market Capitalization: 2,250,000,000 Revised Scores: 53.2

28.02 24.84 19.67

25.83

Shares Outstanding:

176,070,000

Current Market Share Price (11/03/2008) $24.36

Stated Restated Financial Based Valuations Book Value Per Share:

$ 15.03

$ 14.10 Stated

Restated

Return on Equity: 10.60% 6.20% Trailing P/E: $ 9.72

$ 4.70

Return on Assets: 8.10% 4.70% Forward P/E: $ 11.84

$ 6.63

Dividends to Price: $ 17.76

$ 17.76

Price to Book: $ 14.33

$ 13.09

Cost of Capital P.E.G. Ratio $ 28.25

$ 51.81

Estimated

R‐Square

d Beta Ke Upper Bound

Lower Bound Price to EBITA:

$ 14.92 N/A

2 ‐ Year 0.2667 1.0701 0.12586 18.38% 67.80%

Enterprice Value / EBITA:

$ 16.93 N/A

3 ‐ Year 0.3041 1.3871 0.15117 20.70% 9.36%

Price to Free Cash Flows:

$ 37.67

$ 21.69

4 ‐ Year 0.2427 1.24

2 0.140133 19.04% 8.99%

5 ‐ Year 0.2873 1.3369 0.147152 19.03% 10.42% Intrinsic Valuations

6 ‐ Year 0.3859 1.4694 0.157753 19.25% 12.30% Stated

Restated

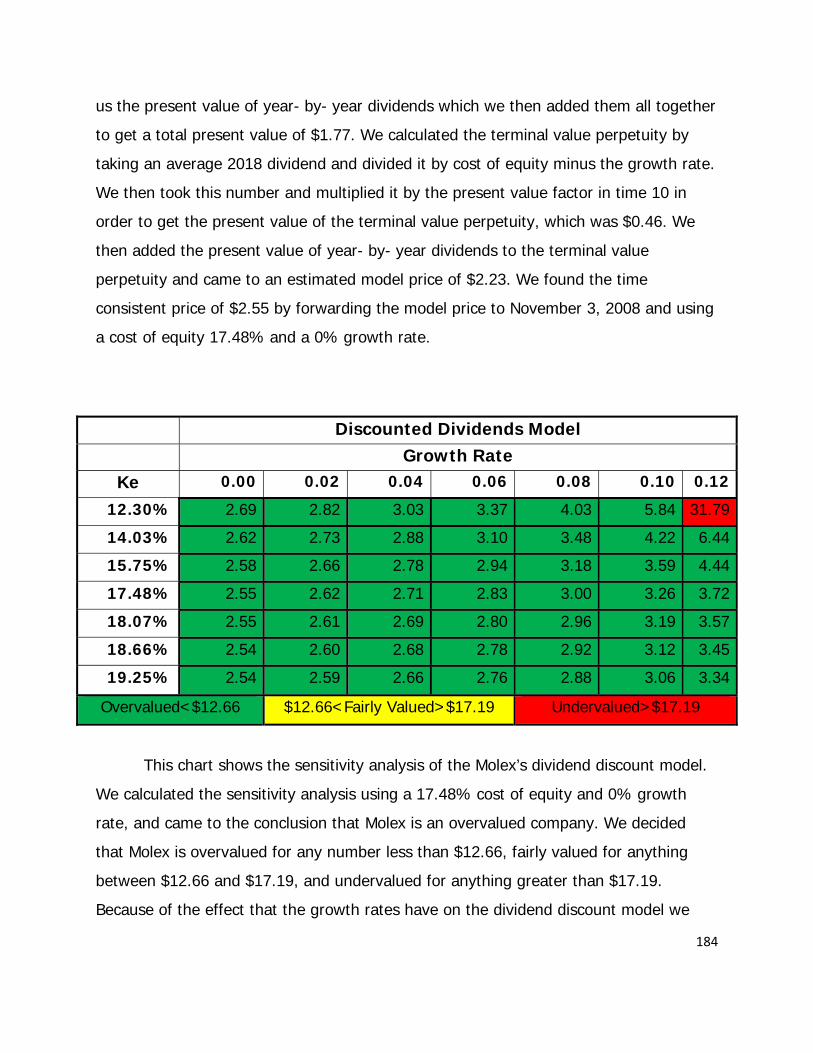

Discounted Dividends: $ 2.55

$ 2.55

Back Door Ke: 10.03% Free Cash Flows: $ 28.79

$ 23.77

Published Beta: 1.61 Residual Income: $ 13.86

$ 22.35

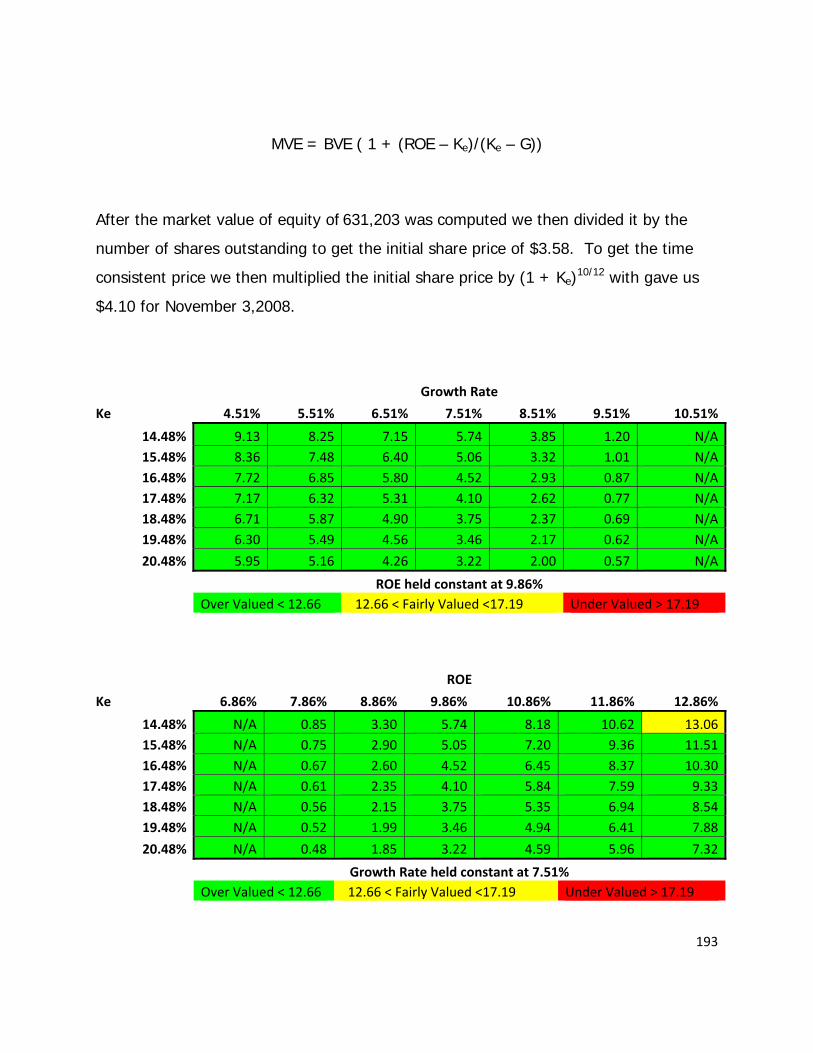

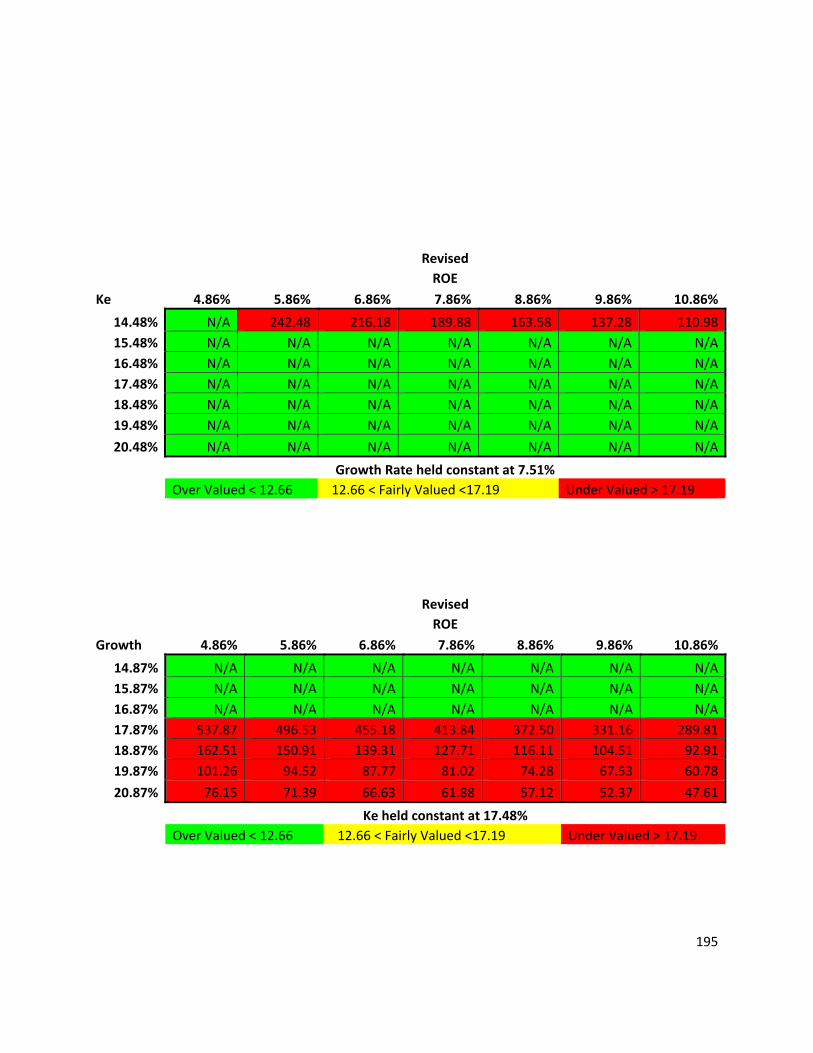

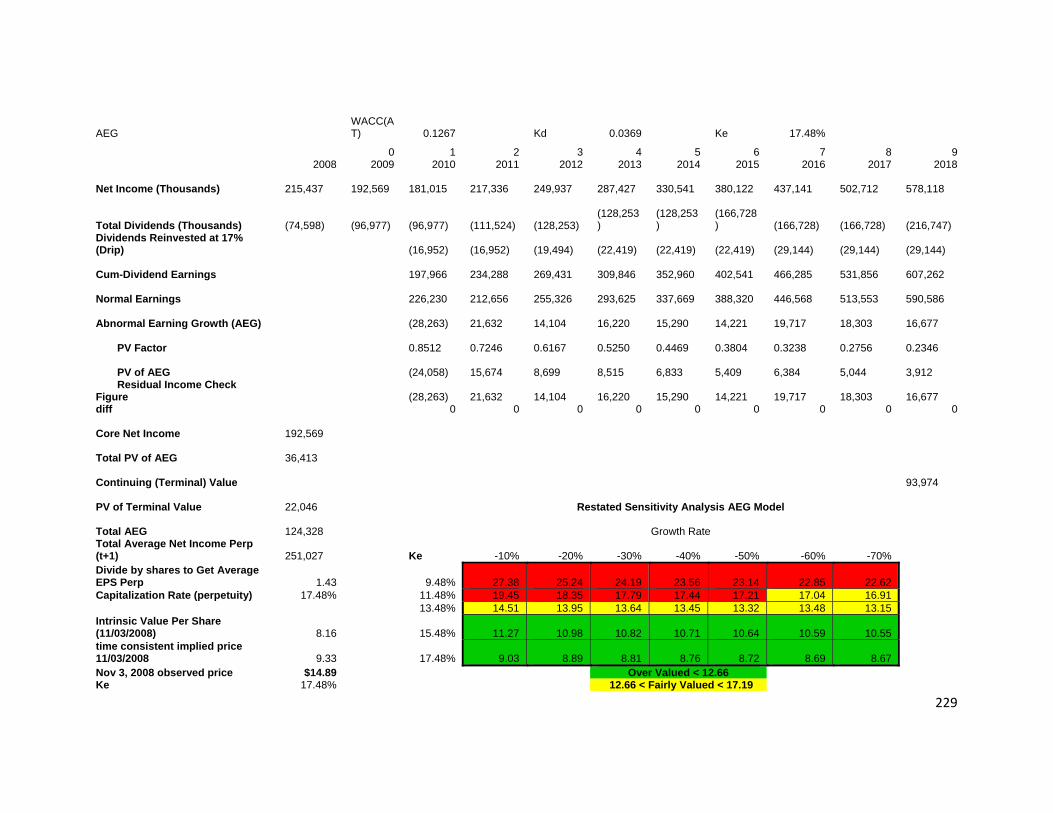

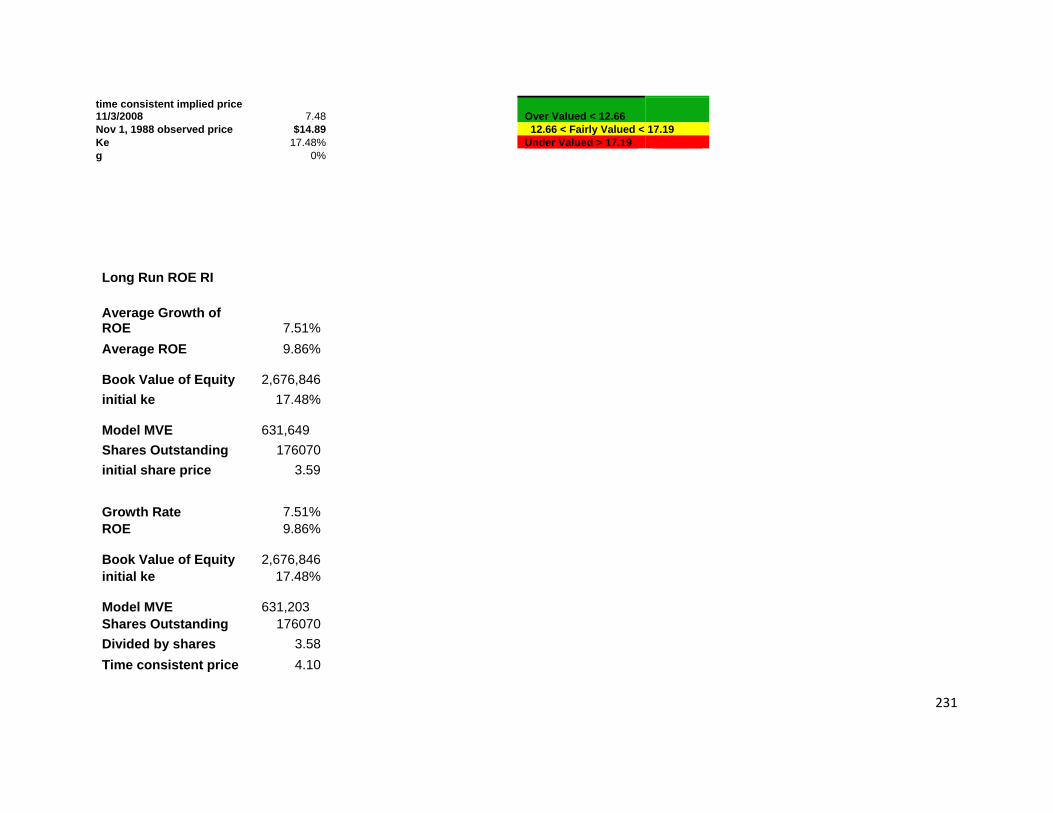

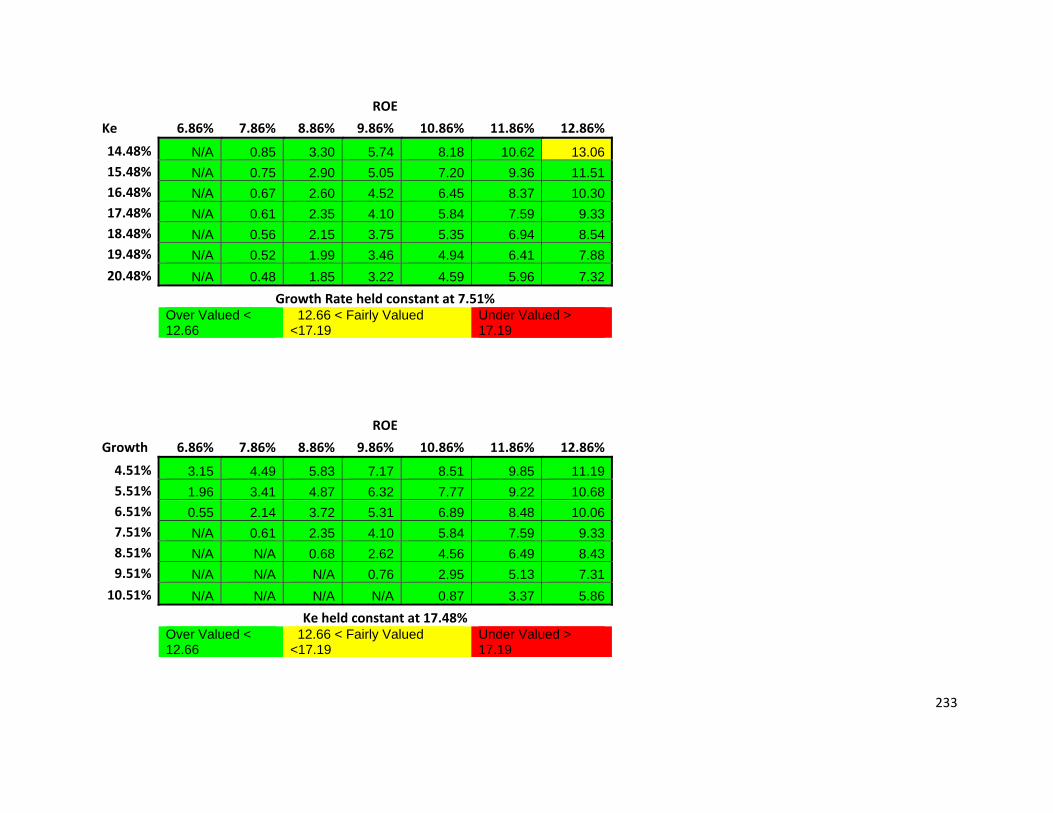

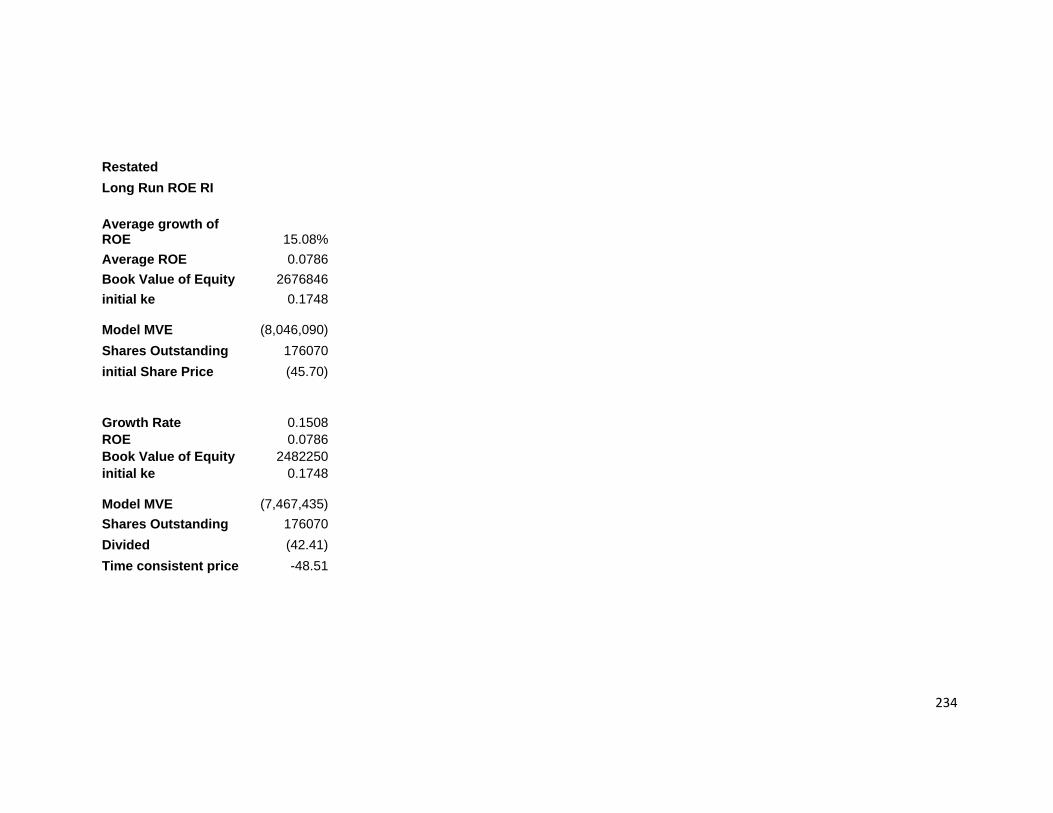

Cost of Debt: 3.69% Long Run Residual Income: $ 4.10 N/A

WACC (BT): 13.95% Abnormal Earnings Growth:

$ 7.85

$ 7.20

13

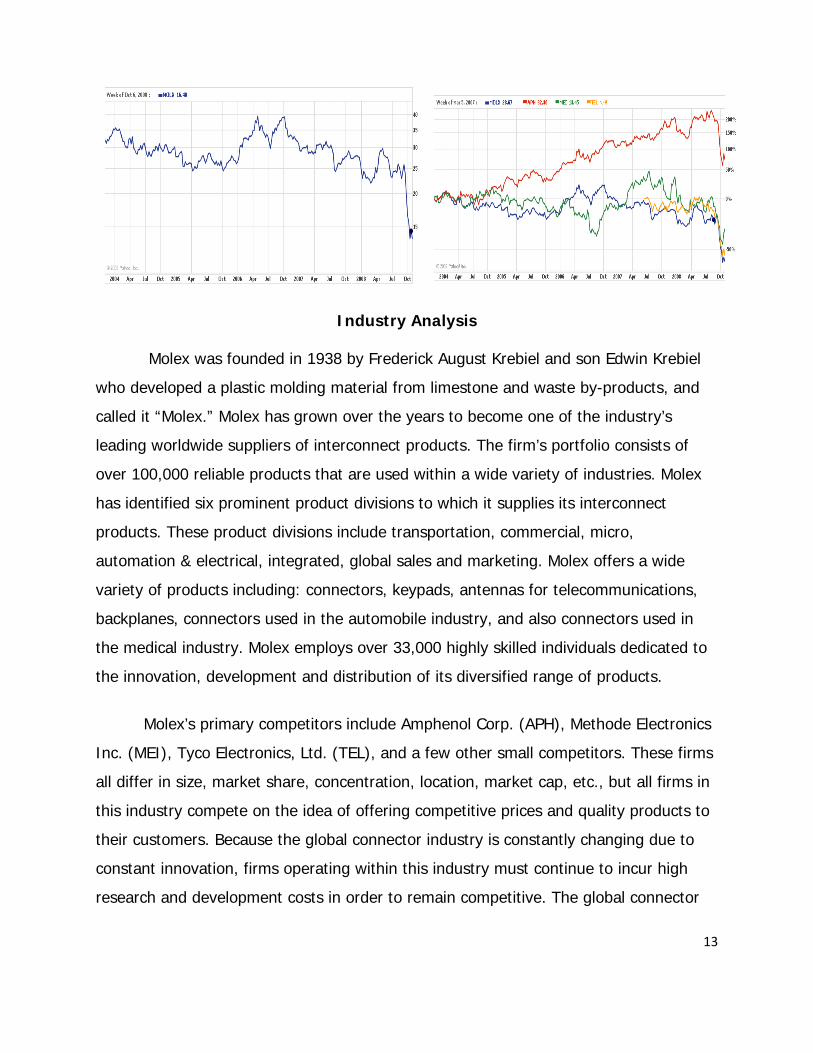

Industry Analysis

Molex was founded in 1938 by Frederick August Krebiel and son Edwin Krebiel

who developed a plastic molding material from limestone and waste by-products, and

called it “Molex.” Molex has grown over the years to become one of the industry’s

leading worldwide suppliers of interconnect products. The firm’s portfolio consists of

over 100,000 reliable products that are used within a wide variety of industries. Molex

has identified six prominent product divisions to which it supplies its interconnect

products. These product divisions include transportation, commercial, micro,

automation & electrical, integrated, global sales and marketing. Molex offers a wide

variety of products including: connectors, keypads, antennas for telecommunications,

backplanes, connectors used in the automobile industry, and also connectors used in

the medical industry. Molex employs over 33,000 highly skilled individuals dedicated to

the innovation, development and distribution of its diversified range of products.

Molex’s primary competitors include Amphenol Corp. (APH), Methode Electronics

Inc. (MEI), Tyco Electronics, Ltd. (TEL), and a few other small competitors. These firms

all differ in size, market share, concentration, location, market cap, etc., but all firms in

this industry compete on the idea of offering competitive prices and quality products to

their customers. Because the global connector industry is constantly changing due to

constant innovation, firms operating within this industry must continue to incur high

research and development costs in order to remain competitive. The global connector

14

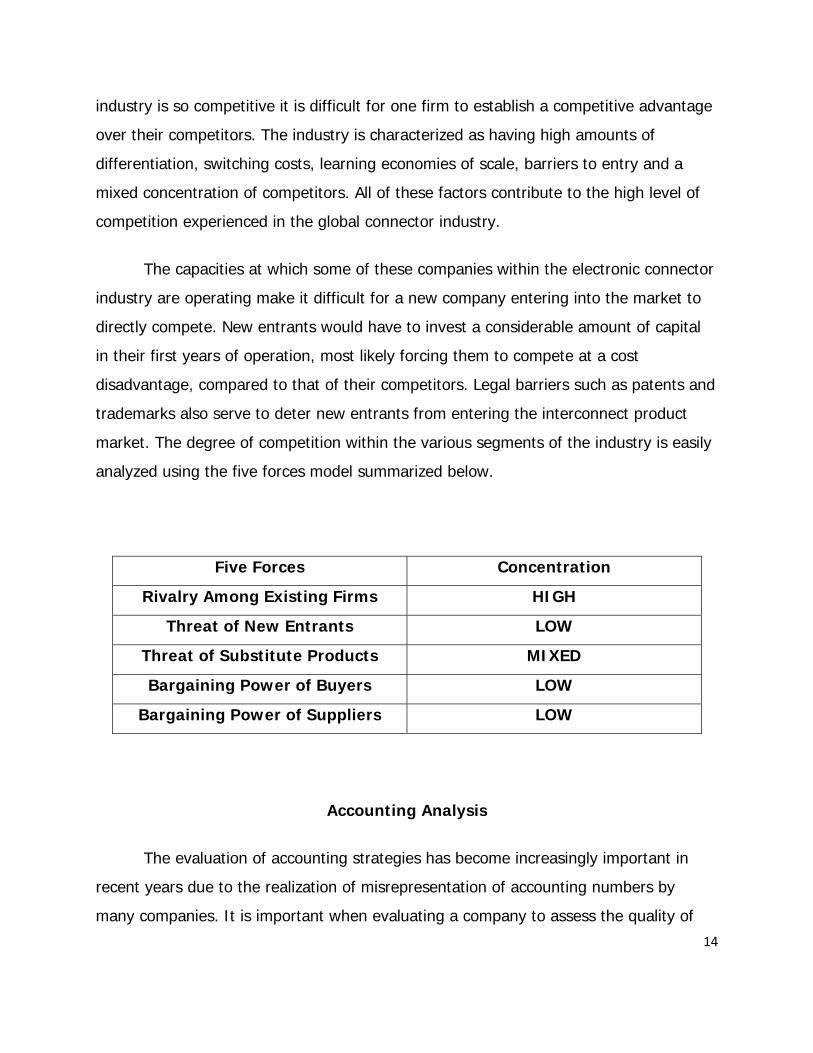

industry is so competitive it is difficult for one firm to establish a competitive advantage

over their competitors. The industry is characterized as having high amounts of

differentiation, switching costs, learning economies of scale, barriers to entry and a

mixed concentration of competitors. All of these factors contribute to the high level of

competition experienced in the global connector industry.

The capacities at which some of these companies within the electronic connector

industry are operating make it difficult for a new company entering into the market to

directly compete. New entrants would have to invest a considerable amount of capital

in their first years of operation, most likely forcing them to compete at a cost

disadvantage, compared to that of their competitors. Legal barriers such as patents and

trademarks also serve to deter new entrants from entering the interconnect product

market. The degree of competition within the various segments of the industry is easily

analyzed using the five forces model summarized below.

Five Forces Concentration

Rivalry Among Existing Firms HIGH

Threat of New Entrants LOW

Threat of Substitute Products MIXED

Bargaining Power of Buyers LOW

Bargaining Power of Suppliers LOW

Accounting Analysis

The evaluation of accounting strategies has become increasingly important in

recent years due to the realization of misrepresentation of accounting numbers by

many companies. It is important when evaluating a company to assess the quality of

15

disclosure within their financial statements and annual reports. High disclosure is

characterized by firm’s ability to represent thorough information regarding accounting

numbers, policies, and personal strategies implemented to the public. Low disclosure is

characterized by the hesitance of a company to provide thorough information to the

public, which makes them appear untrustworthy. Low disclosure can be a red flag to

investors, implicating the possibility of distortion within the firm’s financial statements.

The level of disclosure within the interconnector industry is generally high

concerning the disclosure of leases, pensions, goodwill, currency, and research and

development. Research and development continues to be a driving competitive factor

within this growing market, and while the majority of the firms in operation disclosed an

abundant amount of information one in particular chose not to. Molex and its

competitors Amphenol and Methode choose to implement a high level of disclosure in

reporting research and development, while Tyco Electronics chooses to simply

generalize. While comparing retirement benefits throughout the industry we concluded

that Methode had very low disclosure compared to its competitors, revealing limited if

not minimal information concerning its pension plans. On the other hand, the remaining

competitors within the industry disclosed a vast amount of information concerning their

specific pension, post-retirement, and defined contribution plans. The high level of

disclosure demonstrated by Molex is consistent with the levels established by its

competitors within the industry. A high level of disclosure suggests a firm’s willingness

to disclose thorough information regarding its accounting policies and strategies;

therefore implying the company is less likely to distort financial information.

Financial Analysis, Cost of Capital Estimation, and Forecasting

To successfully evaluate a company an analyst must complete a three step

process that includes ratio analysis, the forecasting of financials, and determining the

16

cost of capital of the company. Financial ratios produce easily comparable numbers so

that analysts, investors and creditors seeking information can identify relationships and

trends within the industry. Ratios were developed to measure the liquidity, profitability,

growth and capital structure of firms. The calculation of the liquidity ratios allows

analysts to measure the ability of a firm to meet its short-term financial obligations.

Molex’s current and quick ratio were significantly higher than their competitors, which

suggests a high level of liquidity. Molex demonstrated a low accounts receivable

turnover ratio compared to its competitors which we attributed to inefficiencies in debt

collections. After examining all the liquidity ratios we can see that many of Molex’s

competitors have comparably similar ratios, while some ratios including days supply in

inventory illustrate vast differences between firms. Profitability ratios measure the

ability of a firm to effectively generate revenues and cover expenses. By using sales

and income figures as the denominator in these ratios we can accurately view how

Molex successfully uses cost management to operate the firm. When viewing ratios

such as gross profit margin and operating expense ratio, Molex out performs the

industry average. We attribute this to Molex’s success in sales and gross profit.

However, when observing operating profit margin and net profit margin Molex performs

below the industry average. Our reasoning behind this factor is that Molex might have

significant expenses or poor cost management that overall negatively affects earnings.

When comparing Molex’s asset turnover to the industry we are the only company that is

able to maintain a stable and sound growth over a five year period thus suggesting that

Molex is effective at using assets to generate sales. When comparing Molex’s return on

assets to the rest of the industry, Molex initially appears to have a stable five year

growth, however, after restating Molex’s financials, Molex is below the industry

average. We attribute this drop to Molex acquiring two companies in 2006 and 2007.

The impairment of goodwill associated with the two acquisitions negatively affected

assets and therefore decreased the return on assets on the restatement. Finally, when

examining return on equity the industry trend is downward sloping. However, when

observing Molex we might fall below the industry average but we do not follow the

17

downward sloping trend. In fact Molex is the only company to maintain a steady growth

in the five year period. Overall when using profitability ratios to compare Molex to the

rest of the global connector industry it is obvious that Molex excels in sales and

generating revenue from assets, however, other ratios suggest that there could be

efficiency or cost management problems in the firm. This is an important factor to

consider when investing in Molex. Capital structure ratios are used to explain how a

firm finances their assets. Firms can use debt or equity to fund projects and assets.

Debt comes from loans or bonds while equity is from selling shares of company stock.

Capital structure ratios can measure the firm’s financial leverage, credit worthiness,

ability to make interest payments, and ability to pay off debt holders. A firm that has

little to no equity will have a poor credit rating which means high interest rates. A firm

with lots of equity can make its payments on debt with ease and do so with a low

interest rate. The three capital structure ratios used are debt to equity, times interest

earned, debt service margin.

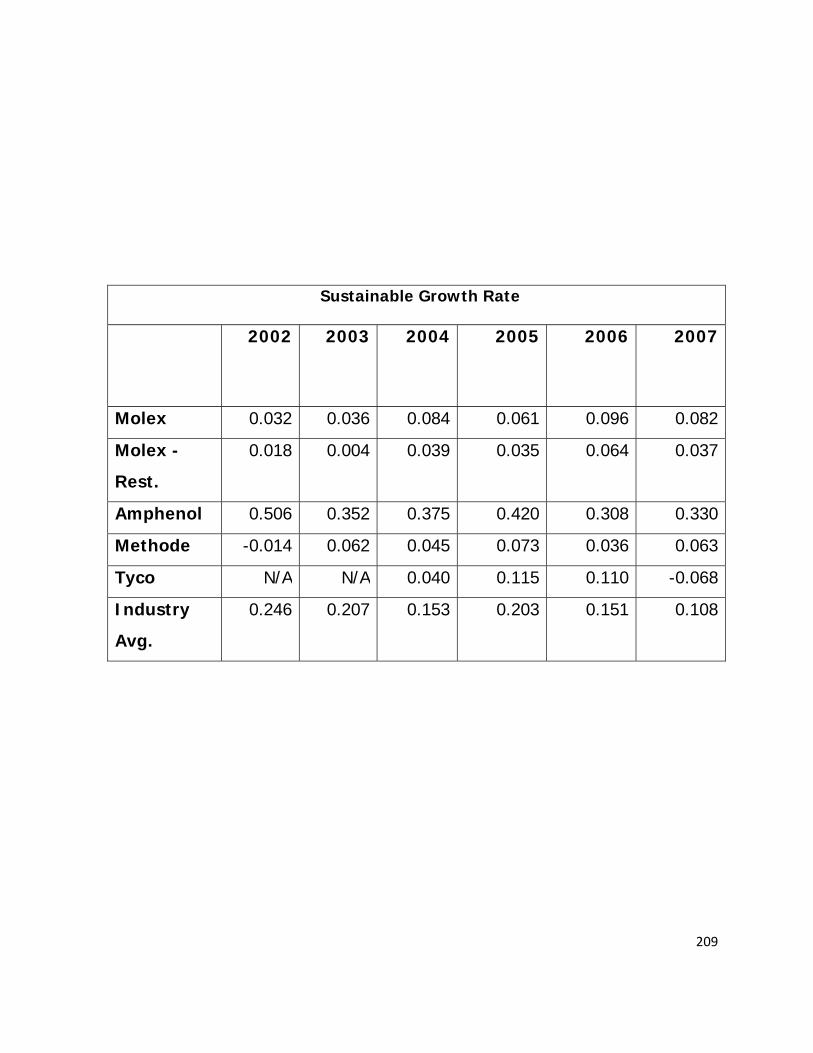

We also examined growth rates because they can help evaluate if a firm can

maintain its future increasing profits without the need of outside financing or changing

capital structure. The two growth rates used are the sustainable (SGR) and internal

growth rates (IGR). Graphing these two growth rates can help distinguish trends or

irregularities between the firm and the industry.

The next step in our prospective analysis was calculating the cost of capital. In

order to find the appropriate rate for our valuations, we had to find the

weighted average rates of both debt and equity financing. To find the cost of equity, we

first calculated beta from a series regression analysis. After deriving the 4.02% risk

free rate from the St. Louis Federal Reserve, a market risk premium of 8% and our beta

of 1.47, we used CAPM to calculate an initial cost of equity of 15.78%. However, when

computing CAPM it fails to account for the market value of the firm also known as the

“size effect”. Therefore, the appropriate cost of equity for Molex based on our market

value is 17.48%. When comparing our size adjusted cost of equity of 17.48% to our

18

backdoor cost of equity of 10.03%, we feel that the size adjusted cost of equity is a

more accurate representation of our company based on our explanatory power of

38.6% and our market value of 2.26 billion. Next we derived our cost of debt. By

using the three month financial AA grade commercial paper rating for the St. Louis

Federal Reserve, we were able to account for the debt associated with accounts

payable, salaries, bonuses, commissions and other accrued expenses. We then applied

the 10 year treasury yield for risk free rate as the interest rate for income taxes payable

and used the interest rates as stated in the 10-K to account for long term debt and debt

associated with short term loans, pensions and postretirement benefits. With our cost

of debt as 3.69% and our cost of equity of 17.48%, we found our weighted average

cost of capital before tax to be 13.95% as stated and 13.7% restated.

The final step and a key part in the valuation of the company in the financial

analysis is the forecasting of financial statements. The most vital part of the forecasting

is to foresee what net sales growth is going to be because the rest of the forecasting is

linked back to this growth rate. A major item that was taken into consideration is the

recession that the economy is currently in. Due to this we decided to use a negative

growth rate for the first two years and a slow positive growth rate for the third year.

The fourth year, 2012, is the year that we foresee the economy recovering and Molex

with have a stable 15% growth year for the flowing years. When forecasting many of

the entries in the financial statements we used the averages and results that came from

the profitability, liquidity, and capital structure ratios. For example, in the balance sheet

when we forecasted our current liabilities we used our already forecasted current assets

and divided by our current ratio of 2.7 to get the current liabilities for each year. This

method of uses ratios was used in many other lines in order to keep the numbers as

accurate as possible. One thing to keep in mind is that statement of cash flows would

be the least precise. We are certain that our numbers on the income statement and

balance sheet were done with accuracy, but the fact is that the statement of cash flows

is the most challenging for even the most talent analysis to forecast to the point that

19

one major part, the cash flows from financing activities, cannot even be reasonably

assumed. We feel that our forecasted numbers would very beneficial in an investor

that is looking at Molex.

Valuation

To accurately value a firm you must utilize both methods of comparables and

intrinsic methods of valuation. Methods of comparables are a set of eight ratios that

compute an estimated price per share which is then compared to a published stock

price to determine the value of a firm. Information is collected and used to calculate

these ratios for the industry competitors, which is then used in the calculation of the

industry average. The industry average, which excludes the data of Molex, was then

multiplied by a correlating factor to determine the implied price per share. We used a

15% margin of safety when comparing the implied price per share to Molex’s published

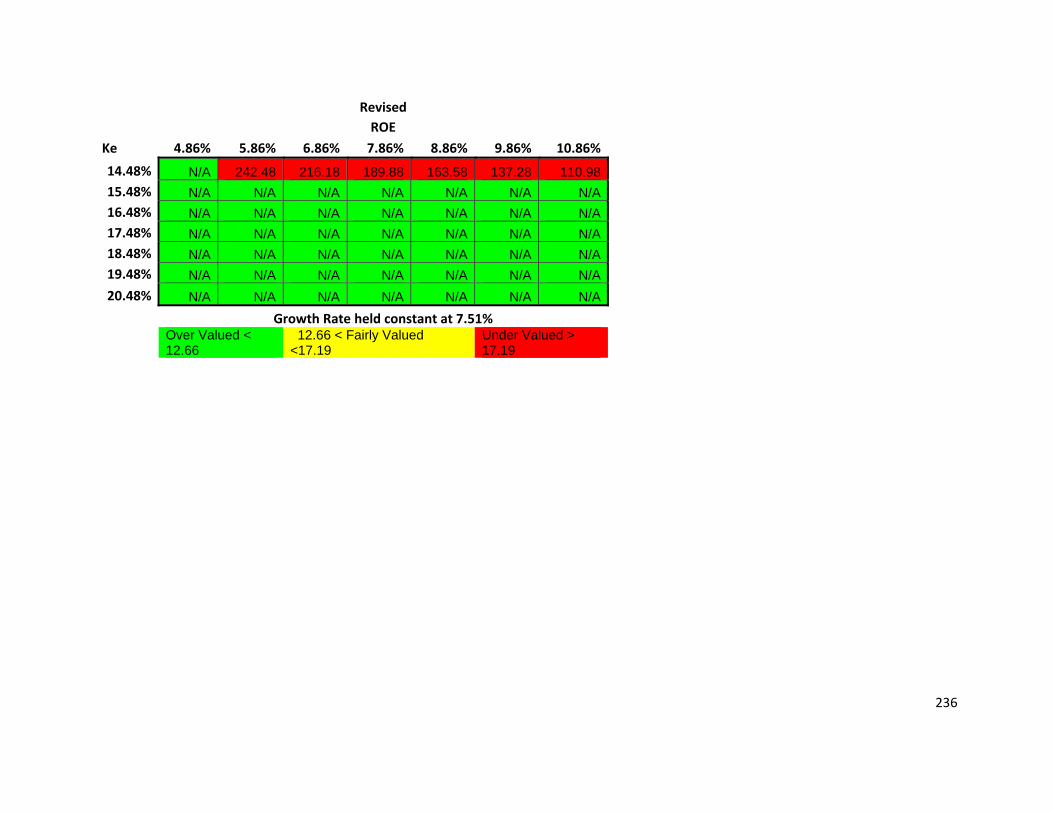

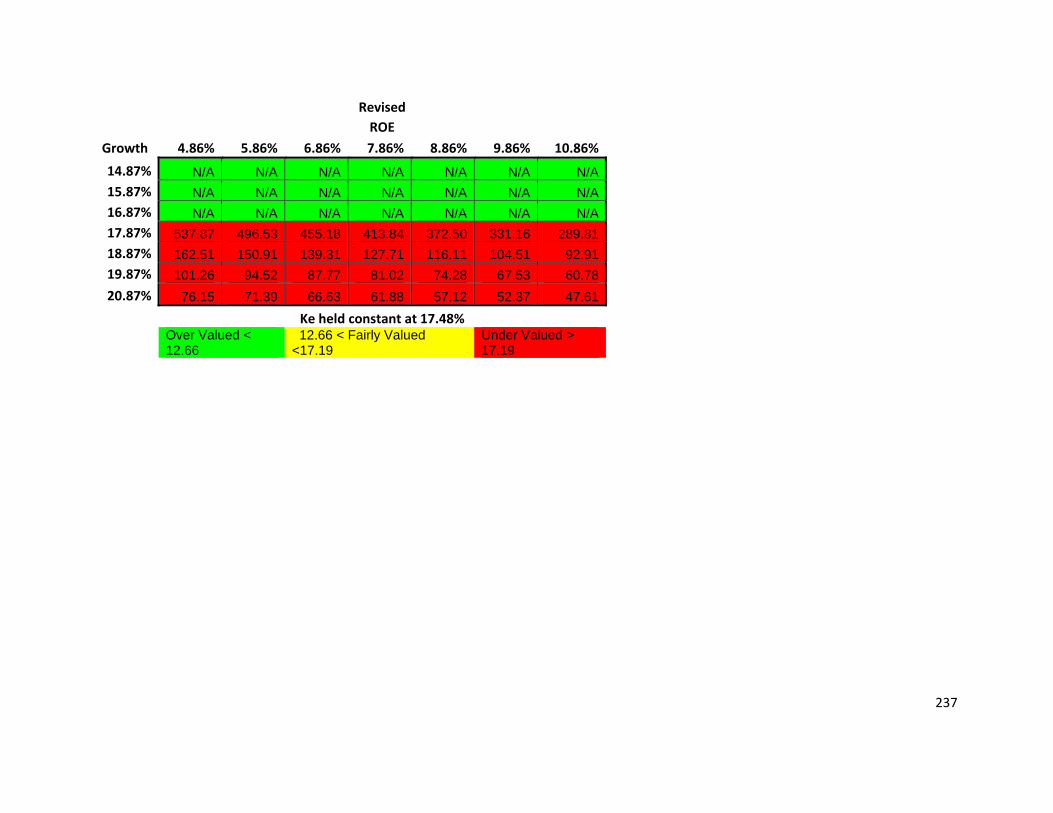

November 3, 2008 price of $14.89. If the price implied by the methods was below

$12.66 Molex was considered overvalued, and if the implied price was above $17.19

then it was considered undervalued. The results varied from each method of

comparable which suggests that these ratios offer limited to no reliability. The implied

price per share is dependent on the performance of Molex’s competitors, therefore

making the methods of comparables an inadequate method of valuation.

The intrinsic valuation methods are considered a more reliable form of valuation

compared to the methods of comparables. These models are supported by financial

theories which assure a higher level of explanatory power. The firm’s performance is

estimated by forecasting the financial statements of a firm. The financial statements

are forecasted to predict company performance, then discounted back into present day

values. The intrinsic valuation method consists of five models which include: discounted

dividends, discounted free cash flows, residual income, abnormal earnings growth , and

long-run residual income. Dividends are the most difficult item on the financials to

forecast, therefore the discounted dividends model yields the least amount of

20

explanatory power. Dividends are sensitive to growth rates, even the smallest changes

in growth dramatically affect the time consistent price based on the model. The

discounted free cash flows model is considered unreliable based on the inability to

accurately forecast future cash flows of a firm. As with the discounted dividend model,

the discounted free cash flow model is sensitive to increasing growth rates which

causes its prices to vary significantly. Molex’s estimated share price using WACCBT of

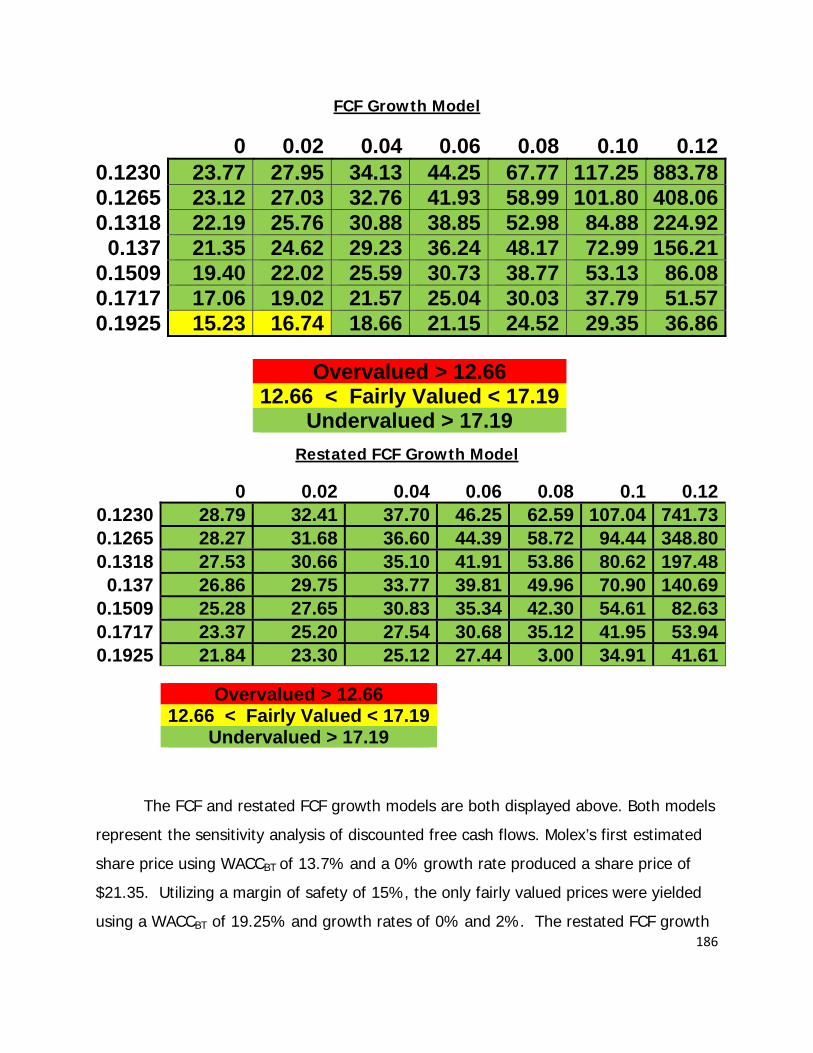

13.7% and a 0% growth rate produced a share price of $21.35, which assumes Molex

is undervalued. The residual income model can be considered a reliable factor when

valuing a firm because it offers one of the highest explanatory powers. This model

yielded an estimated price of $13.68 implying Molex is overvalued. The abnormal

earnings growth model directly correlates with the residual income model in that if you

subtract A.E.G. of any given year by residual income in that same year it should equal

zero. This implies that A.E.G offers the same amount of explanatory power as the

residual income model. A.E.G. produced an estimated share price of $9.33 which

suggests that Molex is considerably overvalued. The last intrinsic value model is the

long-run residual income model which is very solid is the direction of the company

being overvalued. The model has a good explanatory power which helps in the valuing

process. After conducting the various valuation models we consider Molex to be

overvalued.

21

Business and Industry Analysis

Company Overview

Molex was founded in 1938 by Frederick August Krebiel and son Edwin Krebiel

who developed a plastic molding material from limestone and waste by-products, and

called it “Molex.” They began using the Molex plastic material to make a variety of

products, including flower pots, toys, salt dispensers, clock cases, and insulators.

“Molex is the second-largest manufacturer of electronic connectors worldwide in terms

of revenue.” “Net revenue was $3.3 billion for fiscal 2008.” “Molex is a leading supplier

of connector products, with their core business being the manufacture and sale of over

100,000 different electronic components” (Molex 10-K). Molex is a top supplier of

connector components to telecommunications, computer, consumer, automotive and

industrial electronics markets. They offer a wide variety of products including:

connectors, keypads, antennas for telecommunications, backplanes, connectors used in

the automobile industry, and also connectors used in the medical industry. “Molex’s

products are essential to a large number of original equipment manufacturers

throughout the world.” “Molex’s headquarter is located in Lisle, Illinois with operating

locations in 17 different countries.” (Molex.com)

The company’s telecommunications division offers many products for mobile

phones and devices, networking equipment, and switches and transmission equipment.

Some of their products include high speed optical signal lines, backplane connectors,

keyboards, and antennas. These products are mainly produced for the mobile phone

industry. Molex also manufactures connectors for home and portable audio, CD and

DVD players, as well as plasma and LCD televisions. In addition to all of these

products, “they offer manufacturing services to integrate specific components into a

customer’s product” (Molex 10-K).

22

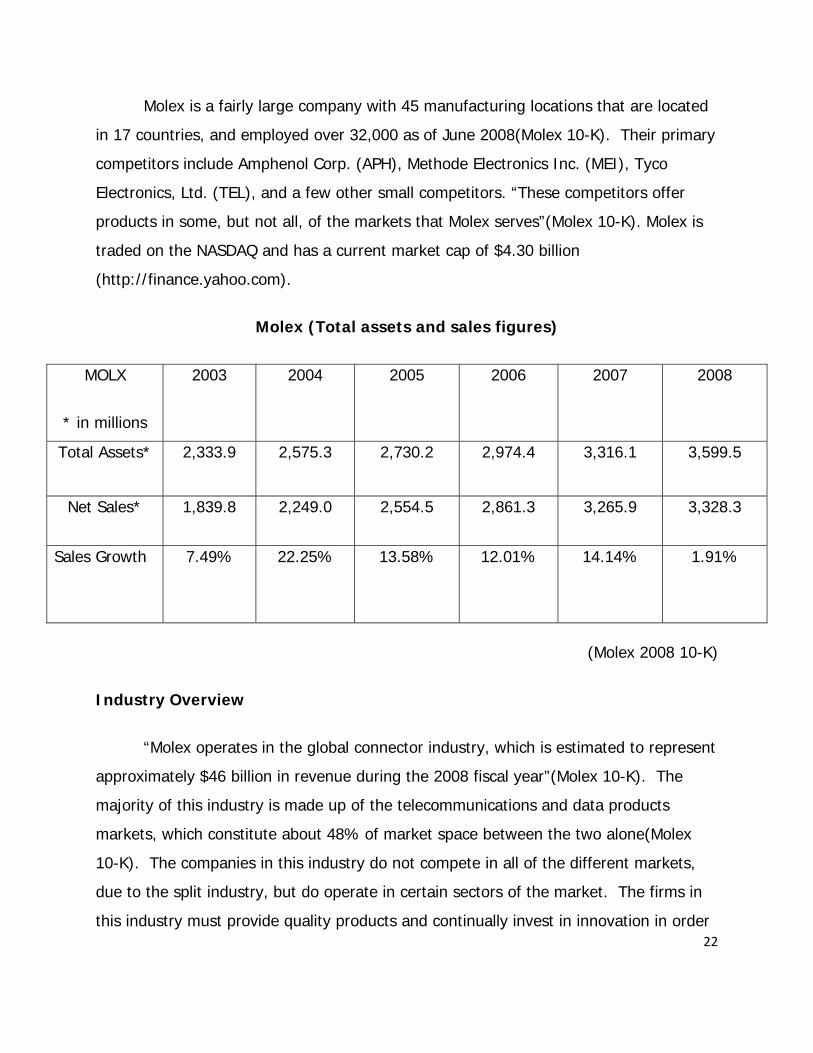

Molex is a fairly large company with 45 manufacturing locations that are located

in 17 countries, and employed over 32,000 as of June 2008(Molex 10-K). Their primary

competitors include Amphenol Corp. (APH), Methode Electronics Inc. (MEI), Tyco

Electronics, Ltd. (TEL), and a few other small competitors. “These competitors offer

products in some, but not all, of the markets that Molex serves”(Molex 10-K). Molex is

traded on the NASDAQ and has a current market cap of $4.30 billion

(http://finance.yahoo.com).

Molex (Total assets and sales figures)

MOLX

* in millions

2003 2004 2005 2006 2007 2008

Total Assets* 2,333.9 2,575.3 2,730.2 2,974.4 3,316.1 3,599.5

Net Sales* 1,839.8 2,249.0 2,554.5 2,861.3 3,265.9 3,328.3

Sales Growth 7.49% 22.25% 13.58% 12.01% 14.14%

1.91%

(Molex 2008 10-K)

Industry Overview

“Molex operates in the global connector industry, which is estimated to represent

approximately $46 billion in revenue during the 2008 fiscal year”(Molex 10-K). The

majority of this industry is made up of the telecommunications and data products

markets, which constitute about 48% of market space between the two alone(Molex

10-K). The companies in this industry do not compete in all of the different markets,

due to the split industry, but do operate in certain sectors of the market. The firms in

this industry must provide quality products and continually invest in innovation in order

23

for them to continually gain market share. The firms competing for market share in this

industry include Amphenol Corporation, Tyco Electronics, Ltd., Methode Electronics Inc.,

and many other small and large firms(Molex 10-K). These firms all differ in size, market

share, concentration, location, market cap, etc., but the one thing that all firms in this

industry compete on is the idea of offering competitive pricing and quality products to

their customers.

These companies must incur high research and development cost, in order to

compete in this very innovative industry. “We must continue to make investments in

research and development in order to continue to develop new products, enhance

existing products and achieve market acceptance for such products”(Molex 10-K).

In an industry where connectors and electronic devices are continually getting smaller

and smaller, and more technologically advanced, it is vital for a company in this market

to invest substantial amounts of revenue in research and development. Molex exceeds

the global connector industry average in terms of research and development expenses,

“Incurring costs of $164 million in 2008, and $159 million in 2007”; which is a lot higher

than the industry average of research and development costs(Molex 10-K).

Manufacturing costs within the connector industry are relatively high, but

companies are well compensated by the large amounts of profits that are received. The

industry, as a whole, has seen substantial amounts of growth during the last five-six

years due to the increasing demand throughout the telecommunications and data

markets. Most of the companies in this industry manufacture around 100,000 different

products, so the firms tend to differ in size, sales, total assets, etc. The four firms listed

below (shown with their net sales figures and total assets) are four of the main

competitors in the global connector industry.

24

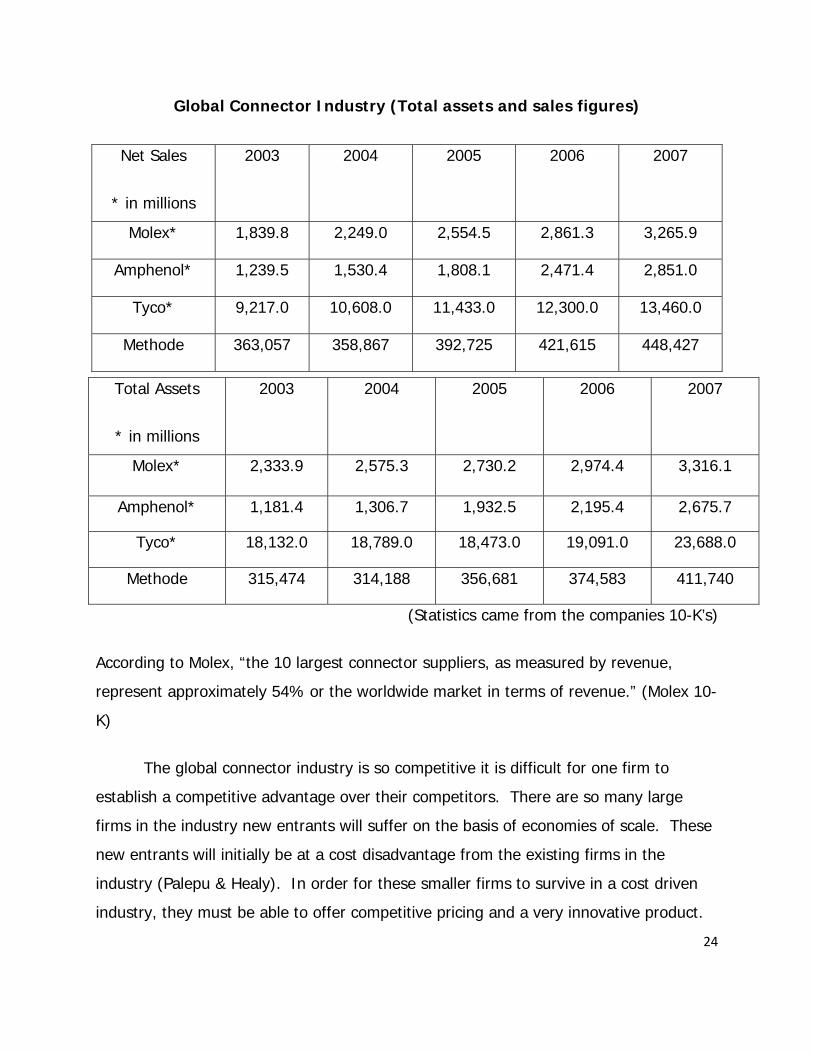

Global Connector Industry (Total assets and sales figures)

(Statistics came from the companies 10-K’s)

According to Molex, “the 10 largest connector suppliers, as measured by revenue,

represent approximately 54% or the worldwide market in terms of revenue.” (Molex 10-

K)

The global connector industry is so competitive it is difficult for one firm to

establish a competitive advantage over their competitors. There are so many large

firms in the industry new entrants will suffer on the basis of economies of scale. These

new entrants will initially be at a cost disadvantage from the existing firms in the

industry (Palepu & Healy). In order for these smaller firms to survive in a cost driven

industry, they must be able to offer competitive pricing and a very innovative product.

Net Sales

* in millions

2003 2004 2005 2006 2007

Molex* 1,839.8 2,249.0 2,554.5 2,861.3 3,265.9

Amphenol* 1,239.5 1,530.4 1,808.1 2,471.4 2,851.0

Tyco* 9,217.0 10,608.0 11,433.0 12,300.0 13,460.0

Methode 363,057 358,867 392,725 421,615 448,427

Total Assets

* in millions

2003 2004 2005 2006 2007

Molex* 2,333.9 2,575.3 2,730.2 2,974.4 3,316.1

Amphenol* 1,181.4 1,306.7 1,932.5 2,195.4 2,675.7

Tyco* 18,132.0 18,789.0 18,473.0 19,091.0 23,688.0

Methode 315,474 314,188 356,681 374,583 411,740

25

Lately, some of the firms in the industry have downsized their operations due to

the recent decline in the stock market. This has mainly been seen in the automotive

side of their operations because of the recent incline in gas prices. Tyco Electronics

stated, “That they plan to close three plants and consolidate production of its

automotive products in Europe…”. “They plan to take charges of $115 million in an

effort to streamline its portfolio and reallocate resources to core operations”

(online.wsj.com). Overall, the connector industry, as a whole, is experiencing nominal

growth rates and will continue to grow as long as we remain a technology based

economy.

Five Forces Model

When analyzing an industry it is important to thoroughly understand what issues

drive and power a business. In order to do so, you must be able to identify key success

factors that create value for the company. The five forces model is an analysis of how

five competitive factors can determine a company’s profitability and a firm’s success in

an industry. It is important to understand how these factors influence competition and

what issues can make or break a business. Porter’s five forces focus on rivalry amongst

existing firms, threat of new entrants, threat of substitute products, bargaining power

of buyers, and bargaining power of suppliers. The following is a table that reflects how

each force influences profitability and competition in our industry. We will discuss how

firms handle the five forces and how they successfully compete in the global connector

industry.

Five Forces Concentration

Rivalry Among Existing Firms HIGH

Threat of New Entrants LOW

Threat of Substitute Products MIXED

26

Bargaining Power of Buyers LOW

Bargaining Power of Suppliers LOW

Rivalry Among Existing Firms

When observing a particular industry you need to be able to evaluate the level of

competition that exists between operating firms. The level of competition within an

industry determines different strategies implemented by firms. If firms decide to

implement an aggressive pricing strategy they choose to push prices closer to marginal

cost. Another strategy is the coordination between competitors to compete with similar

prices, or in non-price dimensions. The technology industry is forever growing and

expanding, and as a result the firms operating in the production of electronic

connectors are forced to compete at a very high level. A number of factors including,

industry growth rate, concentration, differentiation, switching costs, scale economies,

learning economies, excess capacity and exit barriers are considered when determining

the level of competition within a particular industry.

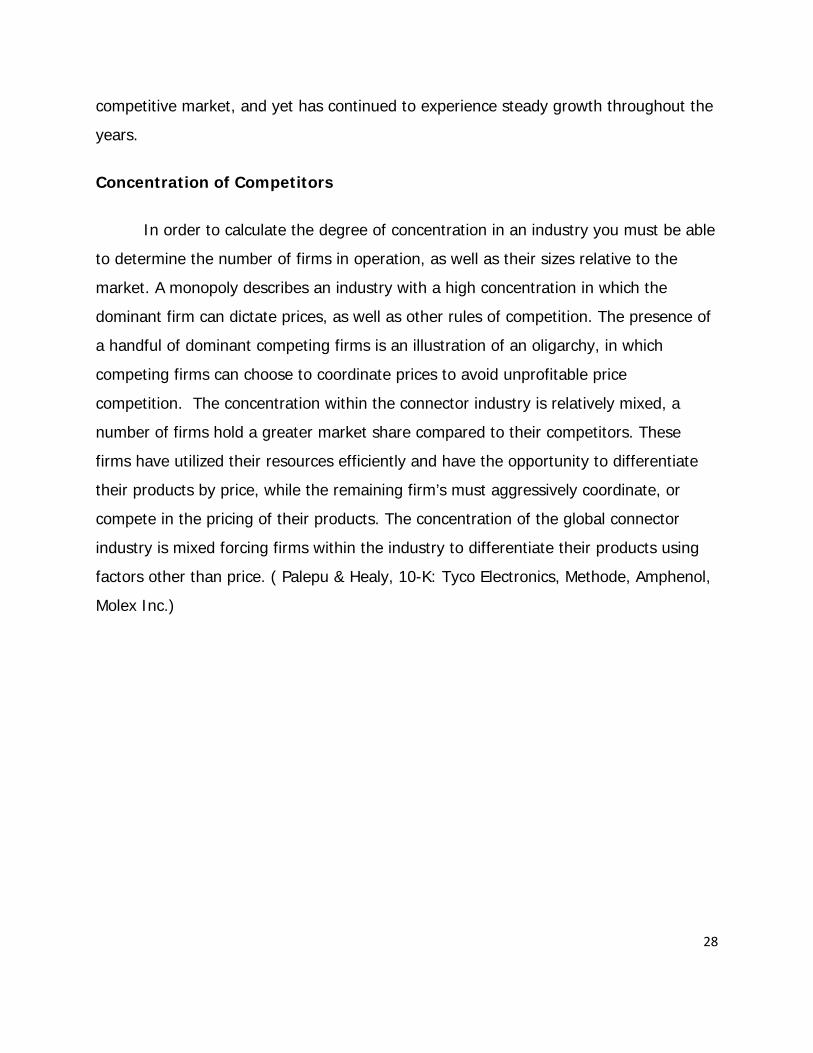

Industry Growth

27

In an industry like the one of electronic connectors, that is constantly innovating

and changing, it’s important to take into account the growth experienced by the

diversified electronics industry as a whole. Each of the companies operating within this

industry has experienced rapid growth as more and more of their products are needed

to operate both commercial and specialty items demanded by their customers (Refer to

graph above). This growth in the industry has lead to an increase in the functionality of

electrical connectors in products ranging from mobile phones to robotics. In terms of

industry growth, it’s not a priority of individual firms to concentrate on capturing a

greater percentage of market shares when the industry is growing constantly. But, price

wars will develop in an industry when it becomes sluggish, because competing with

other firms in the industry on price is the only way for the company to grow. A good

implication of growth is the comparison and calculation of percentage change in sales of

major firms operating within the industry. Commonly high percentage growth in the

industry suggests low competition, while low percentage suggests high competition.

This particular industry is an exception to this regularity in that it operates in a highly

00.020.040.060.080.10.120.140.160.18

2003 2004 2005 2006 2007

Industry Sales Growth

Industry Sales Growth

28

competitive market, and yet has continued to experience steady growth throughout the

years.

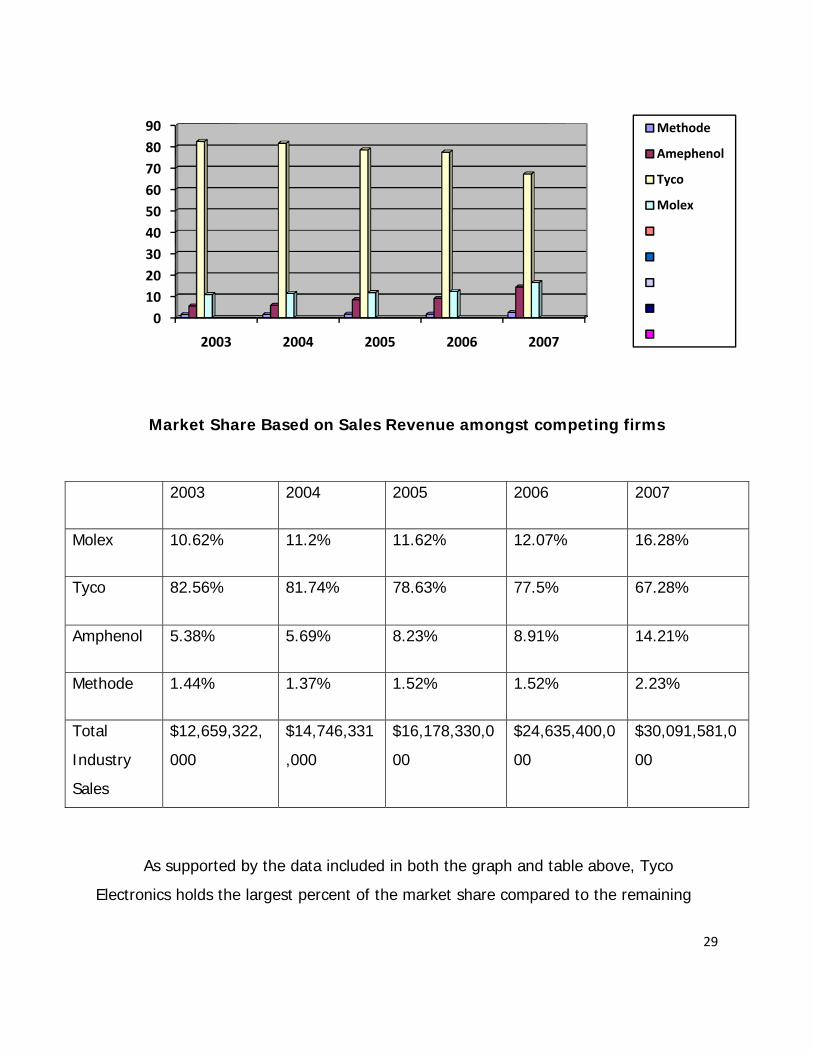

Concentration of Competitors

In order to calculate the degree of concentration in an industry you must be able

to determine the number of firms in operation, as well as their sizes relative to the

market. A monopoly describes an industry with a high concentration in which the

dominant firm can dictate prices, as well as other rules of competition. The presence of

a handful of dominant competing firms is an illustration of an oligarchy, in which

competing firms can choose to coordinate prices to avoid unprofitable price

competition. The concentration within the connector industry is relatively mixed, a

number of firms hold a greater market share compared to their competitors. These

firms have utilized their resources efficiently and have the opportunity to differentiate

their products by price, while the remaining firm’s must aggressively coordinate, or

compete in the pricing of their products. The concentration of the global connector

industry is mixed forcing firms within the industry to differentiate their products using

factors other than price. ( Palepu & Healy, 10-K: Tyco Electronics, Methode, Amphenol,

Molex Inc.)

29

Market Share Based on Sales Revenue amongst competing firms

As supported by the data included in both the graph and table above, Tyco

Electronics holds the largest percent of the market share compared to the remaining

0102030405060708090

2003 2004 2005 2006 2007

Methode

Amephenol

Tyco

Molex

2003 2004 2005 2006 2007

Molex 10.62% 11.2% 11.62% 12.07% 16.28%

Tyco 82.56% 81.74% 78.63% 77.5% 67.28%

Amphenol 5.38% 5.69% 8.23% 8.91% 14.21%

Methode 1.44% 1.37% 1.52% 1.52% 2.23%

Total

Industry

Sales

$12,659,322,

000

$14,746,331

,000

$16,178,330,0

00

$24,635,400,0

00

$30,091,581,0

00

30

firms operating within its industry. Although the remaining firms’ market shares are

minuscule in comparison to Tyco Electronics, each firm’s market share has been slowing

growing each year while Tyco Electronics has experienced decreases.

Differentiation

The attempt made by firms competing in highly competitive markets to set their

products apart from their competitors is referred to as differentiation. It is vital for firms

to differentiate their products as well as other business strategies in order to

accommodate the ever changing needs of consumers. Differentiation can be a detail as

insignificant as color or shape, but can help a product to appear unique when compared

to the products of a competitor. Limited opportunities to differentiate a product’s

physical attributes results in a firm’s focus on aspects such as customer service, brand

recognition, and quality. Firms competing in the global connector industry have

unlimited opportunities to differentiate their products. They are constantly innovating

and redesigning their products to appeal to the industry’s changing consumer. Firms

within the industry also make a valid effort to differentiate and improve the services

offered to their consumers. Differentiation of products within the market remains the

driving factor of success in the global connector industry (10-K : Molex Inc., Tyco

Electronics).

Switching Costs

The commitment firms have to their specific industry depends on the costs

associated with switching the labor of their resources into another market. There are

many risks a firm has to take into account with considering switching into a different

industry including: exit fees, search costs, and equipment costs. Although firms

producing global connectors operate within many diverse markets, the cost of

completely exiting the market and entering into a different industry would be very high.

Their manufacturing process consists of automated machines producing high numbers

31

of complex connectors; it would be difficult for the firms to use their pre-existing

resources for another type of production other than electronic connectors. Because of

the difficulty firms would face in trying to use their resources in another industry, we

would classify the industry as having high switching costs. (Wikipedia, 10-K: Molex Inc)

Economies of Scale

As the number of goods increases in production so must the efficiency as stated

in economies of scale. Larger companies that continue to reduce price per unit as

output increases, are able to use their resources to compete on a larger geographical

scale. Smaller firms are limited in their ability to grow and sometimes encounter

increases in production costs as output is also increased. Electronic connector firms

operate in many different markets, and own production facilities in numerous countries.

32

The amount of capital and resources at their disposal enables the firms to

compete at the level they do. To compete within the connector industry you must own

many production facilities, operate in a number of markets and generate considerable

revenues to own a large percentage of the total market share. Measuring and

comparing the total property, plant, and equipment owned and operated by firms

competing in the industry is a valuable way to support or disprove the assumption given

in the theory of economy of scales. Refer to the table above, most of the firms

competing in the global connector industry are able to achieve economies of scale due

to their individual size and total current assets. (investopedia.com, Answers.com,

molex.com, tycoelectronics.com)

Learning Economies

Firms operating within this industry spend a large percentage of yearly revenues

on the research and development of new products. By continuing to invest in research

and development these firms are serving as a catalyst in the development of new

products, as well as the improvement of products in existence. Because these firms

operate in an industry that is constantly changing and developing it’s paramount to

their existence to acquire highly innovative and intelligent personnel. Firms operating in

Total Assets 2003 2004 2005 2006 2007

Molex 2,333,854 2,575,286 2,730,162 2,974,420 3,316,108

Amphenol 1,181,384 1,306,711 1,932,540 2,195,397 2,675,733

Tyco 18,132,000 18,789,000 18,473,000 19,091,000 23,688,000

Methode 315,474 314,188 356,681 374,583 411,740

Total Assets:

Industry

21,962,712

22,985,185

23,492,383

24,635,400

30,091,581

33

the electronic connector industry continue to be very competitive in their search for

qualified engineers and technicians.

Exit Barriers

Exit Barriers refer to the consequences a company accepts when deciding to exit

the industry. Some important exit barriers to consider are the investment of specialized

equipment, specialized skills, and high fixed costs. If the company has a large amount

of asset worth in specialized equipment it faces a difficult exit barrier because the

equipment is not easily transferrable between markets. Property, plant and equipment

are considered assets of the company but they are not easily transferred into a liquid

asset such as cash or marketable securities, thus it will be harder for a company to

dispose of these assets without considerable time and effort. Skills that are exclusive to

your industry are also another asset that is difficult to transfer between markets, the

costs of retraining can be extremely costly in both time and money. Contracts entered

into by companies also serve as barriers to exit, in that they are obligated to perform

the said duties presented in contracts. In the global connector industry has high exit

barriers because its equipment and skills are highly specialized, making it difficult for

them to exit the industry without incurring significant costs. (10-k: Molex Inc.,

www.agmrc.org, Palepu & Healy)

Conclusion

The global connector industry is highly competitive as a result of its industry

growth rate, concentration of competitors, level of differentiation, switching costs, exit

barriers, economies and learning economies of scale. The industry continues to

experience steady growth year after year as a result of our innovative nature which

allows unlimited opportunities for growth within the industry. The concentration of

competitors within the industry is mixed, forcing firms with lower market share to

differentiate their products using factors other than price, like customer service, and

34

quality. Differentiation within the industry remains high, and important to the success of

any firm operating in the global connector market. Switching costs are high making it

difficult for existing firms to use their current resources in alternate industries. High

level of learning economies of scale force firms to compete aggressively when recruiting

personnel within the industry. High barriers to exit will force companies to remain and

compete within the market. All of these factors contribute to the high level of

competition experienced in the global connector industry.

Threat of New Entry

Firms operating within certain industries fear the threat of new entrants, and

new entrants and new products that may make their existing products obsolete. The

technology industry is constantly changing, forcing companies to constantly innovate

their products. The capacity at which some of these companies within the electronic

connector industry are operating make it difficult for a new company entering into the

market to directly compete. Factors such as, economies of scale, first mover advantage,

distribution access, relationships, and legal barriers act as deterrents to new entrants in

the electronic connector industry.

Economies of Scale

The size and resources of a company continue to be a significant barrier to entry

in the global connector industry. Firms operating within the connector industry have

large amounts of capital invested in property, plant & equipment as well as research

and development. Both of these assets are very important to the success of such

35

companies that supply their products to a number of industries and countries around

the world. Each company reports the reinvestment of at least 5% of their revenues

back into the company in the form of research and development. If a new firm were to

try to enter into the industry they would have to invest a large sum in both of these

areas to be able to compete on the same level as the companies in existence. The

graph below further illustrates the average assets available in the global connector

industry, without significant capital or property, plant and equipment a new entrant

would fail to successfully penetrate the market. New entrants would have to invest a

considerable amount of capital in their first years of operation, most likely forcing them

to compete at a cost disadvantage, compared to that of their competitors.

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

2003 2004 2005 2006 2007

Total Assets : Industry

Total Assets : Industry

36

First Mover Advantage

Early entrants into the industry can experience a number of advantages not

available to those entering at a later time. The earliest entrants have the opportunity to

develop relationships with suppliers, as well as the possibility of developing the

standards of the industry they operate in. Information reflected in many of the firms’

10-Ks has indicated that each individual firm chooses to purchase the raw materials

needed for their products from a limited number of suppliers in order to take advantage

of competitive pricing. The firms operating within the industry have recognized that the

raw materials that they use in the production of global connectors have continued in to

increase in price; therefore they remain faithful to a smaller pool of suppliers in order to

receive the best price. The relationships developed between supplier and firm can lead

to exclusive contracts in which the companies in agreement only deal with one another,

this can be disheartening to those firms entering the industry at a later time. The

opportunity for a firm to develop the industry standards is an incredible advantage to

those early entrants. This insures that all entrants from now on have to adhere to the

standards and regulations exemplified by these early entrants. Pre-existing firms within

the connector industry have been in existence as early as 1932, most starting out

producing simple products and growing throughout the years into intercontinental

production powerhouses. A company trying to enter into the electronic connector

industry would lack the experience, knowledge, and understanding already maintained

by firms in operation.

Legal Barriers

In a research intensive industry, like that of electronic connectors, legal barriers

such as patents, copyrights, contracts, and regulations limit the number of firms able to

enter. Many, if not all of the firms producing electronic connectors have patents on a

majority of their products, making it hard for new entrants to start production without

extensive research of existing patents held by competitors. Molex, one of the industry

37

competitors claims in its most recent annual 10-K to have received over 539 patents for

its products. While some firms like Tyco and Amphenol believe that the number of

patents it has doesn’t affect its overall competitive position, others like Methode believe

that its ability to compete within its industry depends on its ability to maintain the

propriety nature of their technology. The accumulation of patents a company considers

valued assets can serve as a major deterrent to firms trying to enter into the industry

because they would have to spend a large amount of time researching the competitor’s

products as not to infringe any legitimate patents. The firms operating within the

connector industry own production facilities around the globe, and as a result must

comply with regulations enforced by the different governments. Due to the recent focus

on environmental consciousness the European Union has enforced new regulations

involving environmental and equipment disposal within the connector industry. This

specific government has imposed RoHS, which stands for the “restriction of the use of

certain hazardous substances in electrical and electronic equipment”. This regulation

prohibits the production and selling of new electrical and electronic equipment

containing more than agreed levels of lead, cadmium, mercury, hexavalent chromium,

polybrominated biphenyl (PBB) and polybrominated diphenyl ether (PBDE) flame

retardants. New entrants considering opening production facilities must take into

account these newly enacted regulations. Barriers to entry for firms considering

entering a particular market in the future are very high due to the many patents in

effect, and the addition of environmental regulations.

Conclusion

Threat of new entrants into the electronic connector industry remains low. The

industry is constantly innovating and expanding across the globe and has made it

necessary for companies to have high amounts of capital, and revenues invested in

tangible assets as well as research and development. Existing companies can also utilize

the first mover advantage, by using their knowledge of the business, and recognition of

the industry standards. Firms wanting to enter into the connector industry must also

38

consider the many patents held by companies in existence. These potential new

entrants must also take into account the regulations regarding production within the

industry. These factors make it difficult for new entrants to compete or succeed in the

global connector industry without proper funding and planning.

Threat of Substitute Products

“The threat of substitute products depends on the price and performance of

competing products, as well as the customers’ willingness to substitute the product.”

(Palepu & Healy) Some of the firms in the industry do not supply the same products as

their competitors, but the industry as a whole, provides the same main product line

from company-to-company. Firms in the connector industry produce a lot of products

that can fairly easily be substituted by their competitors. So firms have lower bargaining

power and more incentive to offer competitive pricing among the existing firms in the

industry. But, since part of the industry deals with a lot of technology based products,

there is room for companies to compete on the basis of innovation and technology

advances throughout the market place. The threat of substitute products in the global

connector industry leads to competitive pricing and products for the consumer to

choose from.

Relative Price and Performance

One key factor associated with the threat of substitute products is the

competitors’ relative price and performance. “The threat of substitutes depends on the

relative price and performance of the competing products or services and on customers’

willingness to substitute.” (Palepu & Healy) “In an industry where there is low product

39

differentiation between suppliers, the buyer tends to have a relative high bargaining

power, leading to a high level of price competition among firms.”

The increasing competition among firms in the global connector industry is

constantly leading firms to create new innovative products. Our economy is continually

moving towards a more technology based world, and firms in the connector industry

are going to have to capitalize on this in order to succeed. Since firms are spending

around five percent of total revenue on R&D, prices are going to tend to move upward,

which in turn is going to lead to more product differentiation among firms in the

connector industry. The firms who decide to produce these more sophisticated products

will, in turn, separate themselves from their competitors. This will give the more

innovative companies an incentive to continually develop more profitable products.

These more advanced products are going to be used to substitute the cheaper

products, on the basis of quality and performance, but will not compete on price. Firms

in the industry must rely on their products to perform at a level higher than the overall

industry standard in order to succeed.

Customers’ Willingness to Switch

Another factor that deals with the threat of substitute products is the customers’

willingness to switch products. A small price difference in a product can create a

customers’ willingness to switch to a different product. So very competitive pricing is

needed in an industry where there is an absence of high switching costs. Brand loyalty

is also a factor than can lead a customer to switching to a more effective product.

The connector industry is an industry which experiences rapid change and

improvements on products as well as innovation. This makes firms stay up to date on

40

the latest technological improvements and advancements, and also have the latest, and

fastest products. In an industry where a customer has an incentive to do some research

on products and find out which firm produces the best, there are going to be some

moderate switching costs. Due to the fact, that it is very timely and costly to perform

this kind of research on so many companies and their products. Companies’ in this

industry want to create strong relationships with customers’ in order to build a powerful

brand image, and gain the “brand loyalty” that every firm seeks.

Conclusion

In an industry where there is a moderate amount of substitute products, firms

must compete on the basis of competitive pricing and quality products, in order to

create value for their customers’. In an industry where firms are spending adequate

amounts of their revenue on R&D the customer has a smaller a smaller incentive to look

around for substitute products. So overall, the threat of substitute products in the

industry is moderate.

Bargaining Power of Customers

In the competitive industry of electronic connectors competition is everywhere.

The largest customer’s in the industry are mega companies such as: Dell, Cisco, Ford,

GM, IBM, Motorola and Nokia. There are thousands of other companies who use

electrical connectors in their products. Electrical connectors are in almost every

electronic device in the World. Connectors are in high demand, but do the customers or

suppliers have the majority of bargaining power?

41

Switching Cost

The switching cost for customers depends on the connector they are using.

Some companies use generic, off-the-shelf connectors which require low switching

costs. Other companies have custom connectors made specifically for their products.

The custom-made connectors have to be designed to fit their manufacturing process.

To switch from one custom connector to another could cause the manufacturing

process to be reformatted thus increasing the cost of switching. With the use of the

internet manufactures can search for new products by the millions. Using a Google

search engine with the key word search of “electronic connectors” over 992,000 web

sites appear. Almost every large connector company has online catalogs that allow

manufactures to research products and compare prices. The convenience of this online

shopping saves time and money due to increased efficiency of switching products with

a push of a button.

Differentiation

Many connectors provide the same function as each other but there are multiple

factors that differentiate them for the others. The differences may be in size, wattage,

frequency, material, durability, and application. The customers have a wide range of

products to choose from. Many connectors are specifically made so that only like

connectors can be used and a competing brand cannot be substituted.

Importance of Product for Cost and quality

Electronic connectors are an inexpensive input into the final product. Due to

small fraction of cost to the end product, customers will not spend much effort

shopping for the lowest possible price. Large manufactures pay close attention to prices

especially when they are having financial troubles. According to the Wall Street Journal,

Dell Computers is cutting cost everywhere it can to save money and to increase profits.

Dell Computers puts pressure on their suppliers which includes the connector

42

companies to lower prices. A threat of switching suppliers can be enough to influence

the electronic connector supplier to lower their cost (Scheck, A1).

The quality of the electronic connector is essential for the final product. If a

connector is of poor quality it can cause the final product to malfunction. A faulty

connector in a line of computers can cause a malfunction creating a partial or full loss

of ability. Many repairs to replace a faulty connector require costly disassembly and

remanufacturing.

Number of Customers

The lists of customers are enormous. As mentioned before there are connectors

in almost every electronic device in the world. High competition between customers is

very common. The computer and telecommunication industry uses large amounts of

connectors compared the consumer product industry. A computer can have hundreds of

connectors when a washing machine may only have three or four. According to

(electronic-oems.com) they have over 1,526 electronic manufactures listed in their

index. There are thousands more that are unlisted that also use connectors in their

manufacturing processes.

Volume of Customers

Customers usually buy connectors in bulk orders with little lead time. The orders

of connectors could be in the million unit range or more. Long term contracts for

connectors are uncommon because of the rapid technology changes and the ever

changing trends in the electronics industry. Selling connectors in large orders creates

economies of scale because the costs are divided between millions of products lowering

manufacturing cost and transportation cost per unit. Customers tend to stock up

components before holidays such as Christmas to meet dramatically increased

demands.

43

Conclusion

Customers of electronic connectors can be classified as less price sensitive due

to differentiated connectors, the high switching cost due to reformatting the

manufacturing process, and the small cost of the connector to the final product.

Customers do not spend large amounts of efforts trying to shop for the lowest cost

connectors. Backwards integration is not a likely threat to the industry because the

connector industry is highly diversified. Owning your suppliers creates more risk and

would increase losses if the industry takes a downturn.

The customers do not hold as much price setting power as suppliers but they do

hold the power of demand. The customers create a large demand with their final

products such as HD TV’s or new cell phones causing the connector industry to

compete with innovated new products and low prices to influence customers to use

their products by the millions.

Bargaining Power of Suppliers

When suppliers have little competition and few substitutes they can become very

powerful. The materials sold by suppliers to make electronic connectors are palladium

salts, plastic resins, copper alloys, gold, and components. The price and availability of

these products play a critical role in the connector industry. Most of these commodities

have very few substitutes and a high level of competition.

Switching Cost

The switching cost for the connector industry to switch suppliers is very low due

to the large number of suppliers available. When switching from one brand of high

grade copper to another, it will not change anything within the manufacturing process

or end products; unless the copper comes in bars instead of wire spools or is of a lower

44

quality. Often manufactures order supplies from multiple suppliers because their orders

are two large to be filled by just one. Overall, switching suppliers is easy and very low

cost.

Differentiation

The undifferentiated products supplied by supplier’s causes them to lose some

power over the connector industry. High grade copper alloy from one supplier will be

physically identical to another’s. To distinguish a competitive advantage over other

copper suppliers the company may have great customer service, large inventories, and

fast delivery to satisfy the need of a large connector company. In overall product there

is no differentiation.

Importance of product for Cost and Quality

The cost of the raw supplies is the number one determining factor as to what

the connector industry will charge for their products. Many of the commodities listed

previously have volatile prices. For example, oil is the main ingredient for plastic, and as

the supply and price of oil fluctuates so does the price of plastic (How plastics are

made, 1). According to the Wall Street Journal light crude oil prices have increased27%

from September 12, 2007 to September 12, 2008 (Reuters, 1). If a commodity is in

short supply and high demand prices will skyrocket creating profit losses in the

connector industry. The quality of the product supplied will be very close if not

undistinguishable. Plastic resins may have slight chemical differences form one supplier

to another but the overall products are almost identical.

Number of Suppliers

There are thousands of suppliers in the global market for the connector industry.

Most of these suppliers provide their products to many various other industries not just

for connectors. Just a few examples of how raw copper can be used is to make pipe,

45

kitchen ware, or electronic connectors. According to (Copper.org) in the United States

there are more than 80 raw copper suppliers. Copper suppliers can be found

throughout the world not just the United States. The high level of competition among

suppliers will help keep prices down.

Volume of Suppliers

Suppliers sell in bulk orders to the connector industry. The commodities sold

have long shelf lives allowing the buyers to buy before anticipated price increases and

not having to worry about their inventories becoming obsolete. Commodities may be in

short demand and could even increase the value of a connector company’s inventory;

also the exact opposite could happen creating a loss in the value of inventory.

Conclusion

Suppliers are very price sensitive due to undifferentiated products and low

switching cost. Due to this price sensitive condition the connector industry will shop

around for the lowest cost product available. The lower they buy the commodities

needed the higher profits they will make. When commodity prices fluctuate the market

determines the price, the supplier then adds their cost of overhead, labor, and a small

spread of profit to determine the price for the buyers in the connector industry.

Customer and Supplier Bargaining Power Conclusion

Customer and supplier power over the connector industry does not produce a

clear cut winner. The huge customers like Dell, and IBM have a great amount of power

over demand and specifications of the products. The suppliers seem determine prices

due to the fluctuations in the commodities they sell. The connector industry is

comprised of customers and suppliers where no one force dominates over the other.

Both suppliers and customers do their part to set price and supply a demand.

46

Analysis of Key Success Factors for Value Creation in the Industry

Identifying and analyzing the key success factors of a firm’s given industry is vital

in determining a firm’s future profitability, industry standing, and best competitive

strategy. The most prominent and practiced of strategies are cost leadership and

differentiation. The cost leadership strategy attempts to gain a competitive advantage

primarily by reducing its economic costs below its competitors. For example, tight cost

controls, global sourcing, economies of scale and scope, and a simpler product design

that reduces manufacturing costs. The differentiation strategy seeks individuality within

an industry. Firms that compete applying the differentiation strategy use three

guidelines to be successful. First firms must define characteristics of a product or

service that the customers deem important and valuable. Then the firm must meet the

chosen customer need in a matchless way. Finally the firm must attain their

individuality at a cost that is lower than what the customer would want to pay. While

the global connector industry is a highly technological market that puts a huge

emphasis differentiation, it is also extremely important to consumers and investors that

a high quality product is made while also minimizing costs. Thus we will discuss how

both strategies are vital to the success of a firm in the global connector industry(Palepu,

Healy 2-9).

Cost Leadership

The global connector industry manufactures thousands of different types of

products. While most products created and manufactured in this industry are of a

highly differentiated nature, some products are considered commodities and can be

purchased from several different companies. Due to this situation, switching costs for

this industry are fair making the industry reasonably price competitive while still putting

the bulk of the emphasis on differentiation. A few examples of how the global

47

connector industry competes on cost are simpler product design, efficient production,

and economies of scale.

Economies of scale and efficient production

When working in an industry that is as highly competitive as that of global

connectors, it is not only important to set yourself apart from other competing firms by

differentiation, but by also making sure that the firm is able to make a product that is of

an impeccable quality and at the most affordable price. It is common in this industry to

mass produce products that create large volumes of inventory causing costs to

decrease thus driving down prices for consumers(Amphenol, Molex, Tyco 10ks). While

all firms in this industry follow this trend Molex describes the industry process very

thoroughly. “In the global connector industry firms analyze and design the

manufacturing patterns of the customers along with their own supply chain economics

to help ensure that the manufacturing operations are of sufficient scale and are located

strategically to minimize production costs and maximize customer service”(Molex 10K).

Another method that companies in the global connector industry use to expand and

become more efficient is by mergers and acquisitions of existing companies. From

1999 to 2007 Tyco, Molex, Amphenol, and Methode all acquired other companies in the

global connector industry. Companies in the global connector industry participate in

acquisitions in hope that as a company grows production increases thus lowering

production costs and improving production efficiency. In many cases acquisitions lower

costs but another reason why companies in the global connector industry participate in

acquisitions is because they can also diversify customer base thus increasing company

sales. Efficient production is an important factor to consider when analyzing the

connector industry because it ultimately creates more value for the company in terms of

cutting costs, ensuring customer satisfaction, and encouraging brand loyalty.

48

Lower input costs

While economies of scale and efficient production are some of the most common

ways to cut costs for firms in the global connector industry, lowering input costs such as

materials cost and outsourcing are other beneficial ways to control costs in this

competitive industry. For example, outsourcing is extremely common in any type of

technological business because it may be cheaper to design a product in China,

manufacture it in Taiwan, and sale it in the United States then it would be to design,

make, and sale a product in just one country. Another method of lowering input costs

is by having control over suppliers and obtaining the best quality materials at the lowest

cost. However, in the global connector industry a majority of products used such as

plastics, copper, and gold have experienced an over-all price increase in the past year

due to soaring petroleum prices and the increase of certain commodities. An example

of this situation is the automobile industry, an industry in which a majority of companies

in the global connector industry have as a customer base. According to The Wall Street

Journal, the automobile industry is suffering from huge sales declines. Rather than

cutting prices, some companies are being forced to increase them due to certain

increases in commodities(Takahashi 1). This is an excellent example of how firms in

certain industries cannot always control certain factors associated with costs and pricing

that ultimately drive down or damage a firm’s value. While the automobile industry

operates differently from the global connector industry they do correlate. Due to the

fact that the automobile industry is a primary customer of companies in the global

connector industry, a large decline in automobile sales could result in a large decline in

connector industry sales. This is an important factor to consider when investing in

companies in the global connector industry.

Simpler product designs

While the global connector industry is characterized by aggressive advances in

technology and innovative product development, some products are considered

49

commodities that require little originality and have a 25-30 year life span, for instance,

wiring and cables. Although a majority of firms in this industry spend more time and

money towards research and development, in the global connector industry it is

possible to create a simple approach to making certain products that are not only cost

effective but of a reputable quality. It is important to consider these factors in this

industry due to the broad variety of products each firm produces(Amphenol, Molex,

Tyco 10Ks).

Differentiation

When pursuing the differentiation strategy, a company must find a way to stand

out from their competitors in such a way that customers will value. Being unique in an

industry is the key for a company to distinguish themselves from others. It is crucial for

a company to determine what products are in demand, listen to their customers needs,

and then produce the best products based on that information. This will ensure that

the company will provide good customer service and maintain a positive image of the

company. In respect to the electronic connectors industry, this holds especially true

due to the heavy competition between companies like Molex Inc., Tyco Electronics,

Amphenol Corporation, and Methode Electronics. If another firm is doing a better job in

differentiating themselves then that company will receive a better competitor advantage

in the industry. An example of this would be if Tyco had a way of delivering products

to customers quicker than the others then they would be differentiating themselves and

gaining a competitor advantage. When a company stands out from their competitors is

when the company gains the differentiation and competitor advantage.

Product quality

Companies must produce high quality products in order to keep a competitive

edge. If a company’s product quality is not up to the standard of its competitors in the

market, then the company will surely fail. Most customers will be well informed about

50

the quality of all the products on the market and compare different companies to make

the best decision. For example, if Methode has many glitches in their connectors and

has a history of having problems, but Amphenol has never had any issues with their

products, any well informed customer would clearly choose Amphenol. In the electronic

connectors industry their many companies for customers to choose from; therefore, if

one of the companies were to start slacking off and having problems with products, like

a poor connection with the wires, then the other companies would start receive some of

their business and vice-versa. Maintaining the quality of all the products is imperative

to the success of a company; a firm never wants a customer to feel that they were let

down by their products. Word of mouth publicity can have a serious effect on a

company’s success.

Product variety

While preserving the quality of a product, it is also essential that a firm offers

more than one product for a customer to choose from, especially when it comes to

returning customers. Customers often develop brand loyalty quite easily, which can

ensure the success of a company for many years. In the electronic connectors industry

firms usually compete in more than one segment of the industry. For example,

according to Amphenol’s 10-k, Amphenol competes in three different markets which

are: information technology and communications, industrial and automotive, and

commercial aerospace and military. The main markets that Tyco competes in are

electronic components, network solutions, wireless systems (Tyco 10-k). Methode

mainly competes in the markets such as automotive, interconnect, and power products

(Methode 10-k). The company Molex participates in the telecommunications, data

products, automotive, consumer, and industrial markets (Molex 10-k). By a company

having more than just more product line it enable the company to offer more products

to their customers so that they have a variety of choices.

51

Brand Image

The way a consumer feels about a certain brand is referred to as brand imaging.

Brand imaging can be based on the quality of the company’s products, the customer

service that is offered, or personal experiences consumers have had with the company.

In the electronic connectors industry, it is very important for a firm to have a good