Modern REITs and the Corporate Tax - University of …ˆ’ REITs, like RICs, allow small investors...

71

Modern REITs and the Corporate Tax Participant Version (A “Cliffs Notes” Version of the Paper) November 6, 2015 68 th Annual Federal Tax Conference at the University of Chicago Dave Levy, Todd Maynes, Ana O’Brien, and Julanne Allen* *Neither Ms. Allen nor any other IRS employee participated in the preparation of this presentation or any material accompanying it.

Transcript of Modern REITs and the Corporate Tax - University of …ˆ’ REITs, like RICs, allow small investors...

68th Annual Federal Tax Conference

Modern REITs and the Corporate Tax

Participant Version (A “Cliffs Notes” Version of the Paper)

November 6, 2015

68th Annual Federal Tax Conference at the University of Chicago

Dave Levy, Todd Maynes, Ana O’Brien, and Julanne Allen*

*Neither Ms. Allen nor any other IRS employee participated in the preparation of this presentation or any material accompanying it.

68th Annual Federal Tax Conference

Table of Contents

1. The recent debate: Why is everyone talking about REITs?

2. Framing the debate: It’s all about the premises

3. The thesis (a/k/a “Don Quixote becomes a tax guy”)

4. Overview of REITs

5. History of REIT operations and taxation: 18th century through 1935

6. History of the corporate tax and REITs’ place in it

7. The impact of Morrissey and history: Why are we using discredited and

discarded authorities to frame the current debate on the proper taxation of

REITs?

8. REIT legislative changes: 1960 through today

9. Modern developments in the REIT space and their tax policy implications

10.Policy recommendations

68th Annual Federal Tax Conference

The recent debate: Why is

everyone talking about REITs? 1

68th Annual Federal Tax Conference 4

Why is everyone talking about REITs?

• REITs have garnered tremendous attention in recent years in the media, tax press, and

government

• Key drivers of the attention

− Capital markets developments—have encouraged the formation of new types of REITs, the

conversion of C corporations into REITs, and the distribution of REIT shares by C corporations

» Mandatory distributions mean that REIT shares provide attractive yields in a low-interest-rate

environment

» GAAP treatment of “leased real estate” is far more company-friendly than GAAP treatment of

“owned real estate”

» Certain non-traditional asset classes either—

> did not exist in the past (e.g., cell towers and data centers) or

> for historical reasons were owned and used by the same person but can now be owned by a stand-alone REIT (e.g., a power

producer need not own its transmission system)

» Corporate trends toward specialization and away from vertical integration and the conglomerate

form

− Poor optics—REITs are perceived by some commentators as enjoying an unjustified “exemption”

from the corporate tax

− Complexity—participants in the debate do not appreciate the extent to which tax benefits enjoyed at

the REIT entity level are offset by higher taxes imposed on REIT shareholders

68th Annual Federal Tax Conference 5

What types of attention have REITs been receiving?

• “Regular media” and “Tax press”

− Criticism of IRS attempts to “expand” the definition of real estate

− General theme that the REIT regime is an unjustified tax break

− General disdain for non-traditional REITs, C-to-REIT conversions, and REIT spinoffs

» Viewed by the press as tax-motivated transactions lacking in business purpose

• Government

− Congress—the Camp Proposal

» C-to-REIT conversions and REIT spinoffs would become cost prohibitive

> Immediate corporate tax on built-in gains

> Requirement to distribute C corporation’s E&P in cash

» Non-traditional REITs become more difficult because the definition of real estate would be

restricted to assets with at least a 27.5-year depreciation schedule

− IRS no-rule policy on REIT spinoffs

• Scholarly works

− Many of the works have been one-sided attacks on the REIT regime as it currently exists

− Notable exceptions to the negative coverage

» Professor Borden’s work on the impact of C-to-REIT conversions and REIT spinoffs on the fisc

» Richard Nugent’s work on REIT spinoffs

68th Annual Federal Tax Conference

Framing the debate: It’s all

about the premises 2

68th Annual Federal Tax Conference 7

This debate is only as productive as its premises

• Premise 1: REITs should have been subject to the corporate tax in the first instance,

meaning that the REIT regime is a narrow “exception” to the corporate tax

• Premise 2: Recent developments in the REIT space are a material and inappropriate drain

on the fisc

68th Annual Federal Tax Conference

The thesis (a/k/a “Don Quixote

becomes a tax guy”) 3

68th Annual Federal Tax Conference 9

Thesis: Both premises underlying the current debate are false

• We focus on Premise 1—the idea that REITs should be subject to the corporate tax in the first instance

− In light of the policy objectives underlying the corporate tax, Premise 1 is false

» Because REITs operate in a way that does not implicate the policy objectives underlying the corporate tax, REITs

should never have been subject to the corporate tax

» REITs behave in a way that helps advance the policy objectives of the corporate tax, so curtailing the REIT

regime is inconsistent with the policy objectives underlying the corporate tax

− Recent developments in the REIT space do not undercut this conclusion

• Premise 2—the idea that recent REIT developments are a material and inappropriate drain on the fisc—

has been addressed by Professor Borden and shown to be false

− Professor Borden undertook a quantitative analysis of the net effect on the fisc of C-to-REIT conversions

and REIT spinoffs, taking into account—

» The additional taxes paid by REIT shareholders,

» The requirement that a REIT distribute at least 90% of its taxable income, and

» The requirement that a REIT distribute all of its C corporation E&P

− Professor Borden shows that these three features of the REIT regime reduce significantly the net effect on

the fisc of C-to-REIT conversions and REIT spinoffs

» Main wild cards are the extent to which REIT shares are owned by tax-exempt organizations and foreign

governments

• Because it is based on false premises, the entire debate on the proper taxation of REITs,

although extremely consequential from a public-relations and political perspective, has been

misguided and unproductive from a tax-policy perspective since the beginning

68th Annual Federal Tax Conference 10

Moving past false premises: Resetting the debate

• Although the current debate is framed in terms of whether REITs should be “exempt” from

the corporate tax, the debate should really be about the proper way to think about

collective investment vehicles such as REITs

• Based on an examination of first principles—

− REITs should never have been subject to the corporate tax

− Legislative changes to the 1960 REIT regime do not alter that conclusion

− Developments in the REIT space since 1960 do not alter that conclusion

• The real problem with the REIT regime is that it applies to too narrow a set of assets

− REITs, by distributing their earnings annually, operate in a way that does not implicate the policy

objectives underlying the corporate tax

− REITs, like RICs, allow small investors to pool their resources in order to gain exposure to asset

classes that would otherwise be unavailable to them

» This type of activity has historically not been punished by the corporate tax

− REITs, by owning or financing assets that are held in corporate form, help further the goals of the

corporate tax by inhibiting the growth of corporate retained earnings

− The REIT regime ought to be extended to include any asset that can be owned outside of corporate

solution and leased to a corporate user without either impinging on the regulatory objectives of the

corporate tax or creating an unfair competitive landscape for taxable corporations

68th Annual Federal Tax Conference 11

Our approach

• What are REITs and how do they work?

• Should REITs have been subject to the corporate tax in the first instance?

• If not, do recent developments in the REIT space change that conclusion?

• If REITs are only one form of collective investment, should other forms of collective

investment be included in the REIT regime?

12 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates 68th Annual Federal Tax Conference

Overview of Real Estate

Investment Trusts (REITs) 4

68th Annual Federal Tax Conference 13

Typical REIT structure with non-customary services

REIT

Real

Property

Third Party

Lessee

Taxable

REIT

Subsidiary

Lease of Real

Property

Rent

Payment

for Services

Non-Customary

Services

68th Annual Federal Tax Conference 14

REITs as compared to RICs

RICs REITs

Legal authority for treating as

corporation, outside of

statutory “exemption”

Morrissey v.

Commissioner (1935);

Kintner Regulations

(1960)

Morrissey v.

Commissioner (1935);

Kintner Regulations

(1960)

Statutory regime Subchapter M

(Sections 851-855, 860)

Subchapter M

(Sections 856-860)

Means by which no corporate

tax is paid Dividends-paid deduction Dividends-paid deduction

Asset class Stocks and securities Real property

Income class Dividends, interest, and

capital gains

Rent, mortgage interest,

corporate dividends and

interest, and capital gains

Ability to own wholly– or

partially–owned subsidiaries? Yes Yes

68th Annual Federal Tax Conference 15

Dividends-paid deduction

• Unlike a C corporation, a REIT generally is entitled to an income tax deduction for the

amount of dividends it distributes to shareholders

• By contrast, a C corporation is subject to tax on its own income, and the shareholders pay

tax again on the dividends they receive

C Corporation REIT

Income $100 $100

Corporate tax ($35) (35%) ($0) (n/a)

Dividend $65 $100

Tax on U.S. Individual Shareholders ($15.47) (20% + 3.8%) ($43.40) (39.6% + 3.8%)

Shareholders’ After-Tax Distribution $49.5 $56.60

Difference: $7.07

Intuition suggests that this number

would be much larger. The difference is

smaller than anticipated because the tax

rate on REIT dividends is higher than

the tax rate on C corporation dividends.

68th Annual Federal Tax Conference 16

Key REIT rules from a policy perspective

• Annual distribution requirement of at least 90% of taxable income

• No C corporation E&P at the end of any REIT year

• 10-year built-in gains tax on any BIG inherited from a C corporation

• Other Rules

− Asset and income tests to ensure focus on real estate

− Allowed to own wholly– or partially–owned “taxable REIT subsidiaries” (TRSs) that can provide non-

customary tenant services and earn non-qualifying income

68th Annual Federal Tax Conference 17

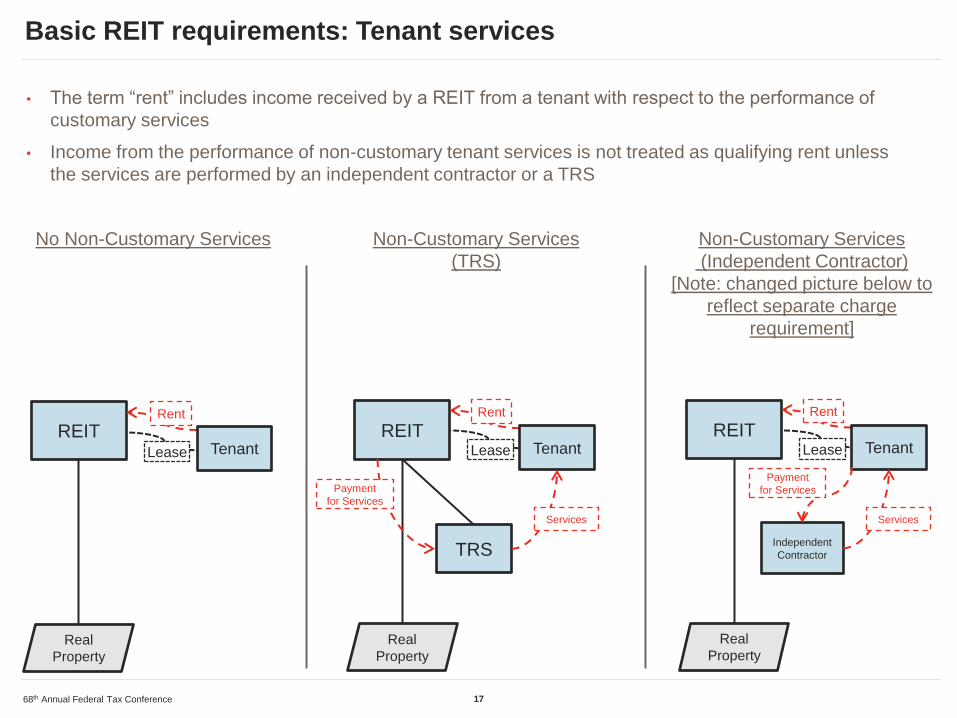

Basic REIT requirements: Tenant services

• The term “rent” includes income received by a REIT from a tenant with respect to the performance of

customary services

• Income from the performance of non-customary tenant services is not treated as qualifying rent unless

the services are performed by an independent contractor or a TRS

REIT

Real

Property

TRS

Lease

Rent

Payment

for Services

REIT

Real

Property

Lease

Rent

Tenant Tenant

No Non-Customary Services Non-Customary Services

(TRS)

Non-Customary Services

(Independent Contractor)

[Note: changed picture below to

reflect separate charge

requirement]

REIT

Real

Property

Independent

Contractor

Lease

Rent

Tenant

Payment

for Services

Services Services

68th Annual Federal Tax Conference 18

Basic REIT requirements: Related party rent

• Related party rent does not qualify under either of the income tests

− Rent received from a person of which the REIT owns 10% or more of the vote or value

− Prevents earnings stripping amongst related parties

• “RIDEA” structures

− Allow REIT to lease property to a TRS and treat the rent as qualifying rent if—

» The property is a qualified healthcare or lodging facility; and

» The property is managed by an eligible independent contractor

REIT

Real

Property

Tenant

Lease

Non-

Qualifying

Rent

>10%

Eligible

Independent

Contractor

Management

Contract

Management

Fee

Non-Qualifying Rent Illustration RIDEA Structure

REIT

Real Property

(Healthcare/

Lodging)

TRS

Lease

Qualifying

Rent

68th Annual Federal Tax Conference 19

Basic REIT requirements: Limitations on the use of TRSs

• The value of TRS securities, together with all other non-real estate assets (including

equipment), may not exceed 25% of the REIT’s assets

• Dividends and non-mortgage interest paid by a TRS to a REIT do not qualify under the

75% income test

• Interest paid by a TRS to a REIT is subject to the Section 163(j) limitation

• 100% excise tax on certain non-arm’s–length arrangements between a REIT and a TRS

• TRSs cannot manage or operate healthcare or lodging facilities

68th Annual Federal Tax Conference 20

REIT shareholder-level treatment

• Although REITs are generally treated as corporations under the Code, there are a number

of rules that subject REIT shareholders to different tax treatment than they would have

received had they invested in stock of a C corporation

• Differences in tax treatment between an investment in a REIT and an investment in a C

corporation can reduce the net impact on the fisc of C-to-REIT conversions and REIT

spinoffs

• This was one of the primary areas of focus of Professor Borden’s work

68th Annual Federal Tax Conference 21

REIT shareholder-level treatment: General

• Distributions from REITs to tax-exempt shareholders are generally not treated as unrelated

business taxable income (UBTI)

− Distributions from “pension-held” REITs may be treated as UBTI (see next slide)

• Distributions to non-U.S. persons are generally not treated as effectively connected

income (ECI)

− Distributions on REIT stock in excess of basis may be treated as a disposition of REIT stock, gains

from which may be treated as ECI under the Foreign Investment in Real Property Tax Act of 1980

(FIRPTA)

− Distributions on REIT stock attributable to the REIT’s disposition of United States Real Property

Interests (USRPIs) may be treated as ECI under FIRPTA

» Also subject to the branch profits tax in the case of a non-U.S. corporate shareholder

• Distributions to sovereign wealth funds are generally not subject to tax, provided certain

requirements under Section 892 are satisfied

− Exception for distributions attributable to asset sales by the REIT

68th Annual Federal Tax Conference 22

REIT shareholder-level treatment: Tax drawbacks

• Asset sale and forward merger exits for non-U.S. shareholders are complicated by certain FIRPTA rules

− Distributions on REIT stock attributable to the REIT’s disposition of USRPIs may be treated as ECI under FIRPTA

and subject to the branch profits tax in the case of a non-U.S. corporate shareholder

− REITs are not eligible for FIRPTA’s “cleansing exception,” which allows a corporation which is not a REIT to sell its

USRPIs and make a liquidating distribution of the proceeds without implicating FIRPTA at the shareholder level

• REIT dividends are not “qualifying dividends” for U.S. individual shareholders

− Non-qualifying dividends are subject to tax at ordinary income rates, while qualifying dividends are subject to tax at

capital gains rates

• REIT dividends generally receive less favorable treatment than C corporation dividends under tax

treaties

− C corporation dividends are often taxed under treaties at rates as low as 0% or 5%

− REIT dividends are generally taxed at 30% under tax treaties, and may be taxed at 15% if the REIT complies with

certain complex requirements relating to asset diversification and shareholder ownership

• Distributions received by a pension fund that owns 10% or more of a “pension-held” REIT constitute

UBTI to the extent income earned by the REIT would have been UBTI if earned directly by the pension

fund

− A “pension-held” REIT is a REIT in which either (i) a pension fund owns more than 25% of the REIT or (ii) one or

more pension funds, each of which owns more than 10% of the REIT, own more than 50% of the REIT in aggregate

68th Annual Federal Tax Conference 23

Illustrating the net impact of the REIT drawbacks

C Corporation REIT REIT (if REIT dividends were

eligible for C Corp dividend rates)

Income $100 $100 $100

Corporate tax ($35) (35%) ($0) (n/a) ($0) (n/a)

Dividend $65 $100 $100

Tax on U.S. Individual

Shareholders ($15.47) (20% + 3.8%) ($43.40) (39.6% + 3.8%) ($23.80) (20%+3.8%)

Shareholders’ after-

tax distribution $49.50 $56.60 $72.20

REIT dividends are not eligible for the 20% QDI rate

C Corporation

(0% treaty rate on

dividends)

C Corporation

(5% treaty rate on

dividends)

REIT

(15% treaty rate on

dividends)

REIT

(30% treaty rate on

dividends)

Income $100 $100 $100 $100

Corporate tax ($35) (35%) ($35) (35%) ($0) (n/a) ($0) (n/a)

Dividend $65 $65 $100 $100

Withholding tax on non-

U.S. shareholders ($0) (0%) ($3.25) (5%) ($15) (15%) ($30) (30%)

Shareholders’ after-tax

distribution $65 $62.75 $85 $70

REIT dividends distributed to foreign shareholders are generally not eligible for treaty rates as low as C corporation dividends

68th Annual Federal Tax Conference

History of REIT operations:

19th century through 1935 5

68th Annual Federal Tax Conference 25

Historic development of REITs

• REITs have been used in this country since the late 18th century and became very popular

during the 19th century

− Provided real estate owners and developers/sponsors with access to a large pool of non-bank

investors

− Provided investors with exposure to real estate assets and sometimes diversified pools of real estate

− REITs funded the development of Boston and many of the cities in the Midwest (Chicago, St. Louis,

St. Paul, Minneapolis) during the 19th and early 20th centuries

• REITs preceded RICs

• Examples of the early REITs

− Boston Pier or Long Wharf (1772): wharf property in Boston Harbor

− Fifty Associates (1820): office space in St. Louis and commercial buildings in Boston

− Boston Wharf Company (1836): loft and industrial property, downtown Boston

− Chicago Real Estate Trustees (1890): three commercial buildings in downtown Chicago

− Second Duluth Real Estate Associates (1899): commercial buildings in Duluth

68th Annual Federal Tax Conference 26

Historic development of REITs (cont'd)

• Form of entity

− Some early REITs were formed as state law corporations, but this structure proved difficult, as many

corporations were only permitted to own real estate in their own name if the state legislature specially

approved

− The “Massachusetts Trust” became popular in the REIT and RIC areas in the 19th century after they were

given the statutory right to own real property and securities in their own name

• Key operational features of the Massachusetts Trust

» Used to hold real estate or securities in the name of the trust for the production of income

» Income generally distributed to the beneficiaries on at least an annual basis

» Generally no retained earnings

• Tax profile

− Between 1909 and 1936, no Federal income tax distinction between REITs and RICs

» REITs and RICs took the position that they were subject to tax as trusts, meaning that their income

was not subject to the corporate level tax to the extent distributed to beneficiaries

− In 1935, the Supreme Court decided Morrissey (described below), which classified REITs and RICs as

“associations” that were subject to the corporate tax

68th Annual Federal Tax Conference

History of the corporate tax

and REITs’ place in it 6

68th Annual Federal Tax Conference 28

Corporate income tax: The history of the lead-up

• Congress’ desire to enact the corporate tax was driven by structural changes in our

economy during the last half of the 19th century

− During the Industrial Revolution, many large corporations consolidated into mega-firms, first

underneath a single trust and later underneath a single holding corporation

• Key drivers behind the use of the corporate form

− Limited liability for shareholders

− Centralized management

» Managers ran the corporation without input or consent from shareholders

» Managers had the ability to retain earnings and deploy those earnings without input or consent from shareholders

• Retained earnings

− Provided significant power to corporate managers

− Permitted the acquisition of assets or competing businesses

− Enabled corporations to engage in price wars in order to achieve market domination

− The anti-competitive activities of some of the early industrial trusts—particularly Standard Oil and the

American Sugar Refining Company—led to the Sherman Antitrust Act of 1890 and a movement

inside government to reconsider the tariff regime that shielded the industrial trusts from foreign

competition

68th Annual Federal Tax Conference 29

Corporate income tax: The history of the lead-up (cont'd)

• As the industrial trusts (and, after 1896, the large holding company corporations) began to

exert power over both society (through monopoly pricing and restraints on trade) and

government, people began to re-evaluate how they thought about corporations

• During the period from the 1850s to the 1880s, corporations were generally viewed as

aggregates of their shareholders, much the same way as a general partnership might be

viewed today

− The corporations themselves were usually closely held

− A corporation was generally managed by its owners, or a subset of its owners

• Once corporations grew to encompass entire industries and management became

separated from ownership, people began to think about corporations as separate from

their owners

• This new way of thinking about corporations as separate from their shareholders helped

our government get comfortable with the idea of imposing a tax on a corporation separate

from any tax imposed on shareholders

68th Annual Federal Tax Conference 30

Corporate income tax: Justification and scope

• By the early 1900s, Congress and the executive branch came under significant pressure

to enact legislation to regulate the large monopolies

• Federal power over business was extremely limited at this time in our history

• Congress and President Theodore Roosevelt relied on two sources of federal power to

regulate the monopolies—

− Commerce clause (which gave Congress the authority to enact the Sherman Antitrust Act of 1890)

− Power to tax

• The corporate tax in 1909 can be thought of as the legislative answer to a two-part

question:

− Could an entity be thought of as separate from its owners for tax purposes?

− If so, should that entity be taxed?

• The thought process on whether an entity could be subject to tax separately from its

owners appears to have been driven by the same factors that had already driven

government to change its view of corporations from an “aggregate” of owners to an “entity”

separate from owners

• The analysis of whether an entity should be subject to tax was part of a broader policy

discussion on the role of the federal government in regulating corporations

68th Annual Federal Tax Conference 31

Corporate income tax: Justification and scope (cont'd)

• The “regulatory view” of the corporate tax

− Restricts the ability of large businesses to accumulate retained earnings, which could be used to

create monopoly power or otherwise restrain trade

» The interest deduction has been justified on the theory that debt service payments inhibit the accumulation of

retained earnings

− Renders corporate books transparent to the public through the publication of tax return information

• The “capital lock-in view” (a/k/a anti-deferral)

− Congress originally enacted the corporate tax in order to get at shareholder-level income

− Struggle ensued between government and corporate managers over managers’ ability to retain

earnings and the extent to which government would either tax retained earnings as a proxy for

shareholder-level taxation or compel their distribution through confiscatory taxation

− Struggle ended in what can be thought of as a settlement between government and corporate

managers –

» Corporate tax was increased to a level that the government was happy with

» Managers retained power of after-tax earnings at the corporate level

» Corporate tax functions as a crude anti-deferral mechanism (conceptually similar to the PFIC regime)

» Shareholders experience agency cost issues

− Corporate tax rate is basically a reflection of the negotiated cost that corporate managers pay in

order to keep control over shareholders’ money

• Both views are all about retained earnings

68th Annual Federal Tax Conference 32

Corporate income tax: Justification and scope (cont'd)

• We have been unable to locate in any of the amendments to the corporate tax any evidence of

Congressional intent to expand the policy objectives underlying the corporate tax beyond the focus on

retained earnings

• The corporate tax originally applied to “joint stock companies” and “associations,” which were not

defined by statute

− Congress’ “punt” on these definitions was likely attributable to the debate over the “natural” vs. “artificial” entity

theories of the corporation

• Shortly following the 1913 corporate tax legislation, Treasury began issuing a series of regulations to

bring into the corporate tax base as “associations” a number of unincorporated entities that did not

historically retain their earnings and did not historically tend toward monopoly, including REITs and

RICs

− Under Treasury’s early approach, any entity that resembled a corporation was treated as an “association” that was

subject to the corporate tax

− Conceptually speaking, as Congress laid out the corporate tax, the question of whether an unincorporated entity

should be subject to the corporate tax should have been viewed as the outcome of a two–part analysis—

» Could the entity be subject to tax separately from its owners?

» If so, should the entity be taxed?

− The first question goes to whether the entity can be viewed as existing separate from its owners, while the second

question goes to whether the entity is operating in a way that implicates the policy objectives underlying the corporate

tax

− Treasury seems to have focused solely on the first part of the analysis, taking the view that any entity which could be

taxed must be taxed, regardless of whether the entity implicated the policy objectives underlying the corporate tax

− The series of regulations were quite confusing and seemed to change from cycle year to the text, and the courts

often complained about Treasury having created massive confusion

68th Annual Federal Tax Conference 33

Supreme Court approach to “associations”

• Early on, the Supreme Court rejected Treasury’s attempts to subject REITs and RICs to the corporate

tax base, concluding that the corporate tax was not intended to apply either to REITs because, as

entities that distributed their earnings, they were trusts at common law, or to RICs, because a RIC’s

non-controlling interest in a portfolio company was not monopolistic

− Crocker v. Malley, 249 U.S. 223, 232 and 234 (1919).

• The Court was not always clear on its rationale and left the door open to a corporate resemblance

approach, under which an entity would be subject to the corporate tax if it sufficiently resembled a

corporation

− A trust is a taxable association if its trustees are “associated together in much the same manner as the directors in a

corporation for the purpose of carrying on business enterprises.” Hecht v. Malley, 265 U.S. 144, 161 (1924).

• This “corporate resemblance” approach was first adopted by the Service in Reg. 65, Art. 1504 under

the Revenue Act of 1924, and updated several times through 1934; Reg. 86, Section 801-2

under the Revenue Act of 1934, which defined an association as any organization with continuity of

life and centralized management, was blessed by the Court in Morrissey

• The Court in Morrissey, deferring to Treasury’s definition in Regulation Section 801-2 (1934), held that a

real estate investment trust could be taxed as a corporation because its organizational documents were

sufficiently analogous to the corporate form

− The Court’s opinion relies heavily on deference to Treasury

− Unclear to what extent the Court was influenced by ongoing animosity between it and the Roosevelt administration over the

Court’s view toward other New Deal legislation

68th Annual Federal Tax Conference 34

The fallout from Morrissey

• Morrissey was decided in 1935 and applied equally to RICs and REITs, meaning that the

country’s two most popular collective investment vehicles would be taxed as corporations

− Perceived negative impact on middle class investors

− Would severely dilute investment returns and make collective investment prohibitively expensive for

small investors

• The RIC industry approached Congress for relief for small investors, which Congress

granted in 1936

• Although the RIC industry was surviving the Great Depression, the REIT industry was still

on its back

− Commentators suggest that the REIT industry did not request relief from Morrissey because the

general feeling was that the industry was awash in tax losses and that real estate values would

never recover

68th Annual Federal Tax Conference 35

The fallout from Morrissey (cont'd)

• Interesting aspects of the 1936 RIC Legislation

− Enacted less than nine months after Morrissey was decided, as part of the Revenue Act of 1936

− Legislative history indicates that RICs were never intended to be subject to the corporate tax

− The definition of RIC in the 1936 RIC Legislation reads like an ad hoc description of the organizational and

operational profile of those Massachusetts Trusts that focused on securities

− The 1936 RIC Legislation was not designed to mitigate the double taxation of corporate dividends

» The legislation allowed RICs to earn interest income and capital gains without being subject to the corporate tax

» Indicates Congressional intent not to impose the corporate tax on collective investment

− Additional safeguards to carry out corporate tax policy

» RIC diversification requirement

> Originally, RICs could not own more than 10% of any one corporation

> Designed to prevent RICs from engaging in the monopolistic business practices that led to the adoption of the corporate tax in 1909

> Most pre-Morrissey Massachusetts Trust RICs satisfied this standard and therefore were not affected by these new tests

> RICs were allowed to operate as they always had, but as a precaution, they could not concentrate their assets in a way that could

be used to create a monopoly

» Undistributed profits tax—the Revenue Act of 1936 imposed a tax on the undistributed profits of C corporations in order deal with

the perceived problem of “corporate cash hoarding”

− The inclusion of the RIC legislation and the undistributed profits tax in the same legislation, combined with the

operational safeguards designed to prevent RICs from engaging in monopolistic behavior—

» Illustrate Congress’ continued policy focus on corporate retained earnings, and

» Provide evidence that the corporate resemblance approach upheld by the Court in Morrissey was inappropriate

68th Annual Federal Tax Conference 36

From Morrissey to the Kintner Regulations

• Morrissey’s corporate resemblance test ultimately gave way to the “Kintner Regulations,” under which an entity’s

classification as a corporation—and thus its status as taxable—was determined based on whether the entity had certain

corporate-like “characteristics”:

− associates

− an objective to carry on business and divide the gains

therefrom

− continuity of life

− centralization of management

− liability for corporate debts limited to corporate property

− free transferability of interests

• These characteristics were basically a restatement of the characteristics relied upon by scholars to support the view that

a corporation was a “natural entity” with the same rights as a person under the law (as contrasted with an artificial entity

which had only those rights bestowed by the state)

• These characteristics did not shed any light on how a corporation should be treated, as a matter of policy, under the law

in general or under the tax law in particular

• The Kintner Regulations were widely criticized as simplistic and inadequate to the function of entity classification

• In 1997, the check-the-box regulations were finalized and the Kintner Regulations were discarded

68th Annual Federal Tax Conference 37

Timeline: From the antitrust movement to Kintner to check-the-box

• 1880–1904: Corporations grow into mega firms where management and ownership are separated from one another;

monopolies arise throughout the economy and accumulate massive amounts of retained earnings at the corporate level

• 1890: Sherman Antitrust Act enacted amid concern over large “industrial trusts” and anti-competitive behavior

• 1909/1913: Enactment of the corporate tax and its successor as a regulatory effort to limit anti-competitive behavior by--

− Limiting the accumulation of retained earnings

− Publicizing corporate activity through publication of tax returns

• 1913–1935: Treasury drafts and re-drafts regulations on “associations” that attempt to draw into the corporate tax a wide

variety of unincorporated entities that did not operate in a way that implicated the policy objectives underlying the

corporate tax

• 1911–1924: Supreme Court rules that REITs did not operate in a way that implicated the policy objectives underlying the

corporate tax and should not be taxed as corporations

• 1929-1939: Onset of Great Depression and widespread destruction of value in the real estate sector; many RICs were

done in by the stock market crash, but many continued to earn interest income and gains on stock sales

• 1935: The Supreme Court decides Morrissey based on deference to Treasury regulations that adopted a “corporate

resemblance” approach to the classification of unincorporated entities

• 1936: Congress overrules Morrissey with respect to RICs by enacting the 1936 RIC Legislation

− Ad-hoc description of the pre-Morrissey Massachusetts Trust/RIC operational model

− Asset concentration provisions guard against monopolistic behavior

− Undistributed profits tax on C corporations prevent accumulation of retained earnings

• 1960: 1960 REIT Legislation is adopted, essentially adopting an ad hoc description of the 19th century Massachusetts

REIT organizational and operational model

• 1997: Kintner Regulations are discarded in favor of the check-the-box approach

68th Annual Federal Tax Conference 38

Should REITs have been subject to the corporate tax?

• Given the policy objectives underlying the corporate tax, REITs should never have been subject to the

corporate tax

− REITs historically distributed all of their earnings and therefore could not accumulate earnings

− Real estate is not an industry that is prone to monopolistic or similar trade-restraining behavior

• The corporate resemblance test did not advance any tax policy objective, in that Congress was

concerned with how corporations operated and not how they looked on paper

− The characteristics of corporate personality helped establish whether corporations could be taxed but said nothing

as to whether they should be taxed

• The corporate resemblance test undercut the policy objectives underlying the corporate tax by

preventing REITs from acting in a manner similar to lenders

− Debt service payments limit the accumulation of retained earnings and advance the policy objectives underlying the

corporate tax

− Rent payments limit the accumulation of retained earnings every bit as much as interest payments

• The authorities under which a REIT was historically subject to the corporate tax have been discredited

and discarded

− The corporate resemblance test was ultimately embodied in the Kintner Regulations, which were both discredited and

discarded by the government in 1997

− Morrissey is no longer relevant

• Although the intellectual foundation for subjecting REITs to the corporate tax has been

discredited and discarded, the premise that REITs should be subject to the corporate tax in the

first instance continues to frame the modern debate

68th Annual Federal Tax Conference

The impact of Morrissey and

history: Why are we using

discredited and discarded

authorities to frame the

current debate on the proper

taxation of REITs?

7

68th Annual Federal Tax Conference 40

Why do we rely on discredited and discarded authorities?

• If the authorities that led to REITs being subject to the corporate tax have been discredited and

discarded, why are we continuing to rely on them to frame a modern tax policy debate on the proper

taxation of REITs?

• The answer is ultimately unknowable and is likely to differ from one person to another, but at a high

level we think the answer has to do with how we are trained to think about technical and policy issues

and how historical events have influenced our thinking

• Things that might have influenced our thinking

» Although RICs and REITs look alike and are subject to the same statutory scheme, because our collective

memory tends not to extend past 1939, it is easy for us to form the impression that RICs have “always” been

exempt from the corporate tax while REITs have “always” been subject to the corporate tax

» The 1936 RIC Legislation, coming less than a year after Morrissey was decided, helps create both an inference

that RICs ought never have been subject to the corporate tax and a corresponding negative inference that REITs

should have always been subject to the corporate tax

> This is unfortunate, as neither RICs nor REITs historically operated in a way that implicated the policies underlying the

corporate tax and REITs preceded RICs as investment vehicles

> Query how the current debate would be framed, or if it would be occurring at all, had the initial REIT legislation

been adopted in 1936 rather than 1960

» The 1960 REIT Legislation is drafted as an exception to the corporate tax

> This should not be determinative, as REITs and RICs are subject to the same statutory scheme

» Treasury was historically hostile toward REITs

> Restrictive regulations following adoption of the 1960 REIT Legislation

> Comparison to GM in the late 1950s

68th Annual Federal Tax Conference 41

Why do we rely on discredited and discarded authorities? (cont'd)

• Evidence that our thinking on a critical tax policy issue has been influenced by historical

developments that have nothing to do with tax policy

− Our entire profession seems to assume without further examination that RICs are “naturally” exempt

from the corporate tax while REITs are “naturally” subject to the corporate tax and therefore require a

narrowly construed exemption to operate as they do

− We have been unable to locate any suggestion that RICs should be subject to the corporate tax,

even in the obvious case of a RIC that holds debt of corporate issuers

− The recent REIT tax policy discussions, whether pro-REIT or anti-REIT, seem to start from the

position that REITs should be subject to the corporate tax in the first instance

• It seems as though our training as lawyers has led us to create in our minds a

“presumption of non-taxation” for RICs and a “presumption of taxation” for REITs,

and these presumptions are skewing the entire debate around the proper way to

think about both RICs and REITs

68th Annual Federal Tax Conference

REIT legislative

developments: 1960 through

today 8

68th Annual Federal Tax Conference 43

The 1960 REIT Legislation

• The 1960 REIT Legislation reads in many ways like an ad hoc description of 19th century REIT structures

− REIT had to be organized as a trust

− REIT had to be subject to tax as a corporation

− REIT had to be managed by trustees

− REIT’s shares had to be freely transferable

− REIT had to be held by at least 100 beneficiaries

• Policy objectives of the 1960 REIT Legislation

− Populist goals: provide small investors with access to real estate portfolio investments that were otherwise available only to

wealthy and institutional investors

− Capital markets goals: provide a new source of capital to real estate owners and developers who were otherwise facing tight

capital markets conditions

» Post WWII rebuilding efforts in Europe and Japan; military spending on Cold War and Korean War; domestic infrastructure

projects such as the interstate highway system, air transportation, etc.

• Perhaps as a result of the hostility with which Treasury regarded REITs, the 1960 REIT Legislation contained a number

of restrictions on a REIT’s ability to earn income

− These restrictions were purportedly designed to ensure that REITs remained “passive,” a term that has never been defined but

has nonetheless caused endless confusion in the REIT space

− It appears that the term “passive” was first used in connection with the 1936 RIC Legislation and was used in the context of anti-

trust concerns

» Congress thought that non-controlling interests in C corporations were “passive” investments because they could not lead to

monopolistic behavior on the part of the RIC, whereas controlling interests were, by definition, “active”

− Commentators viewed these restrictions as unworkable in the long run, but a necessary nuisance in the short run

» The idea was to get the REIT concept back into the law and return to Congress later for amendments to make the concept

workable in practice

68th Annual Federal Tax Conference 44

The 1960 REIT Legislation (cont'd)

• Examples of severe operating restrictions in the 1960 REIT Legislation

− Any amount received from real property was “bad” income if the REIT provided any services (even

customary services), unless it hired an independent contractor to do so

− REIT that owned any inventory property would lose its REIT status (even if it did not recognize gain

from sale of the property)

» Some REITs worried that a REIT-owned vending machine in an apartment building might violate this requirement

− REIT could not derive more than 30% of its income from either (i) the sale of securities held for six

months or less or (ii) the sale of real estate held for four years or less

68th Annual Federal Tax Conference 45

REIT legislative developments: 1960 through today

• The restrictions imposed on REITs in the 1960 REIT Legislation—especially those prohibiting the

provision of any services—initially hampered REITs’ ability to carry out the populist and capital markets

goals that the legislation was intended to achieve

− The REIT regime has been amended several times by Congress between 1960 and 1986 in order to address this

shortcoming and enable REITs to achieve Congress’ policy objectives

− The REIT regime has been amended several times between 1986 and today in order to enable REITs to

simultaneously carry out those policy objectives while adapting to changes in the marketplace

• REIT legislative developments most important to the current debate:

− Tax Reform Act of 1976: allowed REITS to receive separately stated charges for customary services provided by an

independent contractor (separate charges were prohibited under prior regulations); allowed “rents” to include small

amounts from the rental of personal property; allowed REITs to organize as corporations under state law

− Tax Reform Act of 1986: allowed REITs to furnish customary services directly (rather than through an independent

contractor) and to provide an enhanced set of non-customary services through independent contractors

− REIT Simplification Act of 1997: expanded a REIT’s ability to provide non-customary services to tenants through

independent contractors

− REIT Modernization Act of 1999:

» Allowed REITs to form TRSs, which can engage in non-REIT businesses and provide non-customary services to REIT

tenants

» Allowed REITs to lease hotel property to TRS so long as the TRS engaged an eligible independent contractor to operate the

property

− REIT Investment and Diversification Act (RIDEA) of 2007: allowed healthcare REITs to employ similar TRS structure

used by hotel REITs

68th Annual Federal Tax Conference 46

Key take-aways from the REIT legislative changes

• These changes were needed in order to enable REITs to carry out the populist and capital

markets policies underlying the 1960 REIT Legislation

− These changes should be viewed as expressions of how Congress’ original legislative intent ought to

have been implemented in the first place, rather than expansions of a regime beyond its original

intent

• Congress has retained the two requirements which establish that REITs ought never have

been subject to the corporate tax—

− The requirement to distribute substantially all taxable income on an annual basis

− The requirement to distribute all C corporation E&P

• If the changes are advancing the policies underlying the 1960 REIT Legislation

without running afoul of the policy objectives underlying the corporate tax, the

changes cannot have an adverse policy impact as a whole

68th Annual Federal Tax Conference

Modern developments in the

REIT space and their tax

policy implications 9

68th Annual Federal Tax Conference 48

Modern REIT developments driving the current debate

• The Key Developments

− Use of TRSs

» Wholly– or partially–owned TRSs engaging in non-REIT businesses

» TRSs providing tenant services

− Development of non-traditional REITs

− C-to-REIT conversions and REIT spinoffs

• Summary of policy implications

− None of these developments undercuts the conclusion that REITs should not be subject to the corporate tax

» REITs are still required to distribute their earnings

» REITs are still prohibited from retaining C corporation E&P

» REITs still operate in a way that furthers the policy objectives underlying the corporate tax by limiting the ability of

corporations to accumulate retained earnings

− Curtailing these developments would undercut the policy objectives underlying the 1960 REIT Legislation

» Populist goals would be thwarted by denying small investors a vehicle through which they could gain exposure to

commercial real estate on terms similar to those available in the private (i.e., pass-through) market

» Capital markets goals would be thwarted because real estate owners and developers would not have access to the public

capital markets and would have to rely on private (i.e., pass-through) investors for capital

− Curtailing these developments does not serve any other tax policy goal that has been articulated by Congress

68th Annual Federal Tax Conference 49

Increased use of TRSs

• TRSs conducting non-REIT businesses

− In this situation, the REIT is essentially acting like a RIC, and all equity RICs by definition own interests in C

corporations that earn non-RIC income

− Given that corporate tax is being paid by the TRS and no one is suggesting curtailing the RIC regime, this should be

a non-issue

• TRSs providing tenant services

− Tenants are going to demand varying levels of service, and all service is driven by tenant demands

− With high-touch buildings where tenants demand lots of services, there are three choices:

» Force REITs to exit the high-touch market

> Undercuts both the populist and capital markets policies underlying the 1960 REIT Legislation

> Does not advance any policy goal articulated by Congress

> Does not advance the policy objectives of the corporate tax

» Allow REITs to stay in the high-touch market, but force them to rely on independent contractors to provide services

> Proven by history to be unworkable

> Undercuts the populist and capital markets policies underlying the 1960 REIT Legislation, as REIT investors would be forced to

either abandon the high-touch market or surrender to a third party the profits on services

> Because corporate tax is being paid by the TRS, this approach does not advance any corporate tax or other policy objective

» Allow REITs to provide services through TRSs, which is what current law does

> Services income is subject to corporate tax

> Advances the populist and capital markets policies underlying the 1960 REIT Legislation by providing small investors and real estate

owners/sponsors with access to one another

> Size limit on TRSs ensures REITs stay focused primarily on real estate

68th Annual Federal Tax Conference 50

Non-traditional REITs

• Consistent application of the term “real estate”

• Key Drivers of non-traditional REIT development

− Changes in regulatory and capital markets

» Assets that traditionally were owned together (e.g., power generation and transmission lines) may now be owned separately

» Infrastructure assets that had historically been owned by a government might now be owned privately

» Increased lender/capital markets comfort with businesses that own parts of another businesses’ value chains

− Trend toward specialization

» As tenants become more specialized in their real estate needs, property owners need to develop properties that are more

and more specialized

» Specialization amongst tenants tends to create specialized property owners

− Technological change

» Some of the newer non-traditional assets did not exist in 1960

> Cell towers

> Fiber optic networks and data centers

> Electronic billboards

» Some of these assets are “direct” technological successors to older assets that were clearly real estate

» The remainder of these assets are real estate under the 1962 regulations

• Policy implications

− REITs are acting in a way that advances the policy objectives underlying the corporate tax

− Curtailing these activities would undercut the populist and capital markets objectives underlying the 1960 REIT Legislation, and

not advance any other policy objective articulated by Congress

68th Annual Federal Tax Conference 51

C-to-REIT conversions and spinoffs

• Key drivers

− Capital markets factors

» Companies’ desire to operate on a “capital light” basis

» Investors’ desire for yielding securities in a low-yield environment

> Increases the value of yielding securities

> Leads to higher multiples for REIT shares as compared with C corporation shares

> Leads to reduced cost of equity capital for REITs

» Financial statement metrics punish non-real estate companies that own their real estate, creating

an incentive for companies to sell or spinoff their real estate

− Specialization

» Businesses tend to focus on doing a smaller number of things really well

> Increased business specialization can increase demands for specialized real estate

» Conglomerate structures and vertical integration are becoming disfavored for business and

capital markets reasons, creating an incentive for companies to sell or spinoff their real estate

» Some companies start off as non-real estate companies that own their real estate and morph over

time into real estate companies that do other things

> If the non-real estate business is small enough to fit inside a TRS, the entire company may

convert to REIT status in order to access REIT capital markets and enhanced valuations

> If the non-real estate business is too big for a TRS, it might be spun off or sold

68th Annual Federal Tax Conference 52

C-to-REIT conversions and spinoffs (cont'd)

• Policy implications

− C-to-REIT conversions and REIT spinoffs do not, in and of themselves, undercut the policy

objectives underlying the corporate tax and can actually advance those policy objectives by—

» triggering the immediate distribution of historic C corporation E&P and

» preventing the accumulation of future earnings through—

> rental payments from the distributing company to the real estate company, in the case of an opco/propco spinoff, and

> The REIT distribution requirement imposed on the REIT

− These transactions also advance the policy objectives underlying the 1960 REIT Legislation by—

» providing investors with enhanced access to yielding real estate assets, and

» enabling a formerly bundled real estate business greater capital markets access

− Curtailing C-to-REIT conversions and REIT spinoffs would put older firms at an unfair disadvantage

to newly formed REITs

» Older firms that are restructuring or re-aligning their business goals and skill sets should not be permanently

locked into C corporation status when they might have to compete with newly formed REITs

68th Annual Federal Tax Conference 53

Illustrative REIT spinoffs—“OpCo/PropCo”

C Corp

Real

Property

Contribution

of Real

Property

Operations

Newly

Formed

“PropCo”

REIT

Shareholders

• Step 1: C Corp forms a new “PropCo REIT” by contributing its historic real estate assets

• Step 2: C Corp distributes PropCo REIT stock to its shareholders in a tax-free transaction under Section 355

• Step 3: C Corp (now an “OpCo”) enters into an arm's-length lease with the PropCo REIT for the use of the real property

C Corp

Real

Property Operations

Shareholders

PropCo

REIT

Distribution

of PropCo

REIT Stock

C Corp

(OpCo)

Real

Property Operations

Shareholders

PropCo

REIT

Arm’s-length

lease of real

property

Step 1 Step 2 Step 3

68th Annual Federal Tax Conference 54

Illustrative REIT spinoffs—sale-leaseback

• Step 1: C Corp sells its real property to an existing REIT or newly formed REIT

• Step 2: C Corp (now an “OpCo”) enters into an arm's-length lease with the REIT for the use of the Real Property

C Corp

Real

Property Operations

REIT C Corp

Real

Property Operations

REIT

Arm’s-length

lease of real

property

Step 1 Step 2

Sale of Real

Property

Shareholders Shareholders Shareholders Shareholders

Cash

68th Annual Federal Tax Conference 55

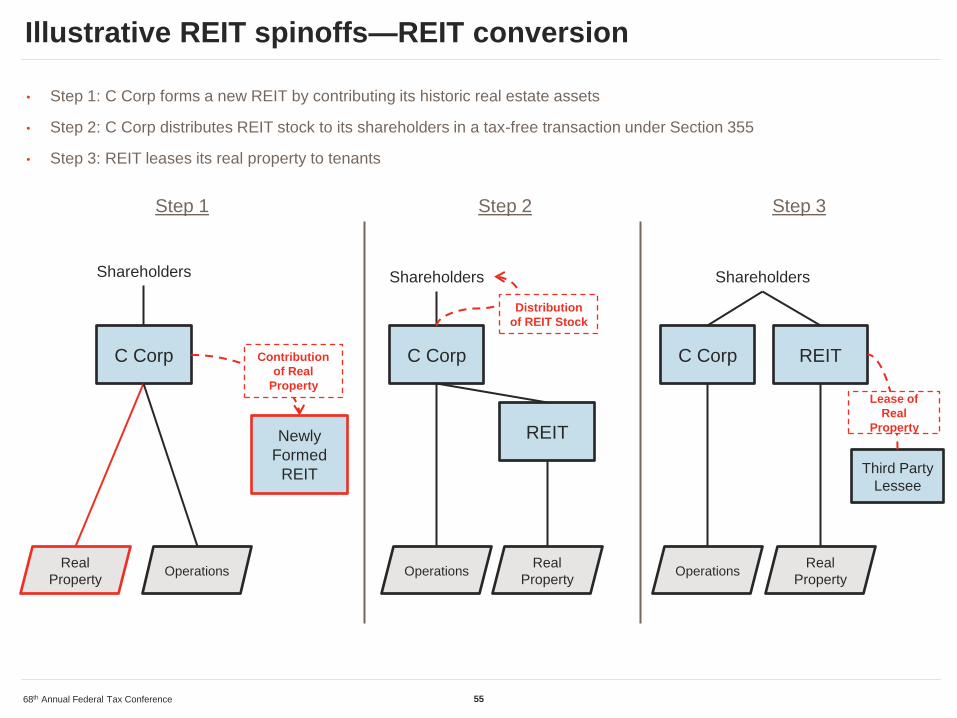

Illustrative REIT spinoffs—REIT conversion

C Corp

Real

Property

Contribution

of Real

Property

Operations

Newly

Formed

REIT

Shareholders

• Step 1: C Corp forms a new REIT by contributing its historic real estate assets

• Step 2: C Corp distributes REIT stock to its shareholders in a tax-free transaction under Section 355

• Step 3: REIT leases its real property to tenants

C Corp

Real

Property Operations

Shareholders

REIT

Distribution

of REIT Stock

C Corp

Real

Property Operations

Shareholders

REIT

Step 1 Step 2 Step 3

Third Party

Lessee

Lease of

Real

Property

68th Annual Federal Tax Conference 56

Tax-revenue effects of REIT spinoffs (adapted from Professor Borden’s work)*

*Examples adapted from Bradley Borden, “Counterintuitive Tax-Revenue Effect of REIT Spinoffs,” 146 Tax Notes 381 (Jan. 19, 2015).

• While REIT spinoffs may reduce corporate tax revenue, the overall tax effect may be slight because (i) REITs tend to pay

out a greater share of their earnings as taxable dividends than C corporations and (ii) REIT dividends are not “qualifying

dividends” and thus are taxed at a higher rate than C corporation dividends

• If the C corporation has a 65% dividend payout ratio (i.e., distributes 100% of its after-tax income), and the REIT

distributes 100% of its income, under the assumptions below, a REIT spinoff decreases total tax revenue by just 7%,

assuming that the REIT’s shareholders are fully taxable

• If the C corporation has a 50% dividend payout ratio, a REIT spinoff decreases total tax revenue by just 3.7%, again,

assuming the REIT’s shareholders are fully taxable

• If the C corporation has a 25% dividend payout ratio—the national average—a REIT spinoff actually increases total tax

revenue by 3%, again, assuming the REIT’s shareholders are fully taxable

• Even in cases where the REIT spinoff results in a net tax benefit, it may take many years (as illustrated on following

slides) in order for this benefit to exceed the up-front tax paid on the “purging” distribution of the REIT’s share of the C

corporation’s historical earnings and profits at the time of the spinoff

− The effect of the purging distribution in the following slides is calculated based on the following assumptions:

» The C corporation’s total earnings and profits are various multiples of its yearly undistributed taxable income (i.e., 10 years,

20 years, and 30 years)

» The REIT’s share of the C corporation’s earnings and profits are 10%, 20%, 30%, 40%, or 50%

» The tax rate on the purging distribution is 23.8%

• Revenue effects of “sale-leaseback transactions” are similar, except—

− The tax on a purging distribution is replaced by capital gains tax on the sale of real estate to a REIT

− The C corporation retains the proceeds of the sale (unlike the purging distribution in a spinoff, which is distributed to

shareholders)

− The purchasing REIT is able to take a larger depreciation deduction because of a stepped-up tax basis in the real estate

68th Annual Federal Tax Conference 57

Tax Effects of REIT Spinoff Assuming 65% C Corporation Dividend Payout Ratio and No E&P Purging Distribution†

Tax Paid On Purging Dividend†

n/a

Years Before Tax Benefit of REIT Spinoff Exceeds Tax on Purging Dividend†

n/a

*Chart adapted from Borden, “Counterintuitive Tax-Revenue Effect of REIT Spinoffs.”

Tax-revenue effects of REIT spinoffs (cont'd)

†Assumption: if the C corporation historically paid out 65% of its taxable income (i.e., 100% of its after-tax income), it will have no accumulated earnings and profits

Without Spinoff* With Spinoff

Corporation Corporation REIT

Gross income $ 100,000 Gross income $ 100,000 Gross income $ 70,000

Depreciation deduction $ 40,000 Rent deduction $ 70,000 Depreciation $ 40,000

Taxable income $ 60,000 Taxable income $ 30,000 Taxable income $ 30,000

Tax rate 35% Tax rate 35% Tax rate 0%

Corporate tax $ 21,000 Corporate tax $ 10,500 Corporate tax $ -

Distribution $ 39,000 Distribution $ 19,500 Distribution $ 30,000

Shareholder tax rate 23.8% Shareholder tax rate 23.8% Shareholder tax rate 43.4%

Shareholder tax $ 9,282 Shareholder tax $ 4,641 Shareholder tax $ 13,020

Total tax $ 30,282 Total tax $ 15,141 Total tax $ 13,020

Without Spinoff total tax $ 30,282 C Corporation Dividend Payout Ratio

as a Proportion of Taxable Income

65% With Spinoff total tax $ 28,161

Difference ($) $ (2,121)

Difference (%) -7.0%

68th Annual Federal Tax Conference 58

Tax Effects of REIT Spinoff Assuming 50% C Corporation Dividend Payout Ratio with E&P Purging Distribution

*Chart adapted from Borden, “Counterintuitive Tax-Revenue Effect of REIT Spinoffs.”

Tax-revenue effects of REIT spinoffs (cont'd)

Depending on the amount of the REIT’s

share of the C corporation’s historic

E&P, it may take many years for the

spinoff to reduce overall tax revenue.

Without Spinoff* With Spinoff

Corporation Corporation REIT

Gross income $ 100,000 Gross income $ 100,000 Gross income $ 70,000

Depreciation deduction $ 40,000 Rent deduction $ 70,000 Depreciation $ 40,000

Taxable income $ 60,000 Taxable income $ 30,000 Taxable income $ 30,000

Tax rate 35% Tax rate 35% Tax rate 0%

Corporate tax $ 21,000 Corporate tax $ 10,500 Corporate tax $ -

Distribution $ 30,000 Distribution $ 15,000 Distribution $ 30,000

Shareholder tax rate 23.8% Shareholder tax rate 23.8% Shareholder tax rate 43.4%

Shareholder tax $ 7,140 Shareholder tax $ 3,570 Shareholder tax $ 13,020

Total tax $ 28,140 Total tax $ 14,070 Total tax $ 13,020

Without Spinoff total tax $ 28,140 C Corporation Dividend Payout Ratio as a

Proportion of Taxable Income

50% With Spinoff total tax $ 27,090

Difference ($) $ (1,050)

Difference (%) -3.7%

Tax Paid On Purging Dividend

REIT's Share of C Corporation's Historical E&P

10% 20% 30% 40% 50%

Years' Worth of Undistributed

E&P

10 $ 2,142 $ 4,284 $ 6,426 $ 8,568 $ 10,710

20 $ 4,284 $ 8,568 $ 12,852 $ 17,136 $ 21,420

30 $ 6,426 $ 12,852 $ 19,278 $ 25,704 $ 32,130

Years Before Tax Benefit of REIT Spinoff Exceeds Tax on Purging Dividend

REIT's Share of C Corporation's Historical E&P

10% 20% 30% 40% 50%

Years' Worth of Undistributed

E&P

10 2.0 4.1 6.1 8.2 10.2

20 4.1 8.2 12.2 16.3 20.4

30 6.1 12.2 18.4 24.5 30.6

68th Annual Federal Tax Conference 59

Tax Effects of REIT Spinoff Assuming 25% C Corporation Dividend Payout Ratio with E&P Purging Distribution

Years Before Tax Benefit of REIT Spinoff Exceeds Tax on Purging Dividend

Never

*Chart adapted from Borden, “Counterintuitive Tax-Revenue Effect of REIT Spinoffs.”

Tax-revenue effects of REIT spinoffs (cont'd)

If the C corporation’s dividend payout

ratio is sufficiently low, a spinoff may

actually increase net tax revenue

(assuming the REIT’s shareholders pay

tax on distributions)

Tax Paid On Purging Dividend

REIT's Share of C Corporation's Historical E&P

10% 20% 30% 40% 50%

Years' Worth of Undistributed

E&P

10 $ 5,712 $ 11,424 $ 17,136 $ 22,848 $ 28,560

20 $ 11,424 $ 22,848 $ 34,272 $ 45,696 $ 57,120

30 $ 17,136 $ 34,272 $ 51,408 $ 68,544 $ 85,680

Without Spinoff* With Spinoff

Corporation Corporation REIT

Gross income $ 100,000 Gross income $ 100,000 Gross income $ 70,000

Depreciation deduction $ 40,000 Rent deduction $ 70,000 Depreciation $ 40,000

Taxable income $ 60,000 Taxable income $ 30,000 Taxable income $ 30,000

Tax rate 35% Tax rate 35% Tax rate 0%

Corporate tax $ 21,000 Corporate tax $ 10,500 Corporate tax $ -

Distribution $ 15,000 Distribution $ 7,500 Distribution $ 30,000

Shareholder tax rate 23.8% Shareholder tax rate 23.8% Shareholder tax rate 43.4%

Shareholder tax $ 3,570 Shareholder tax $ 1,785 Shareholder tax $ 13,020

Total tax $ 24,570 Total tax $ 12,285 Total tax $ 13,020

Without Spinoff total tax $ 24,570 C Corporation Dividend Payout Ratio as a

Proportion of Taxable Income

25% With Spinoff total tax $ 25,305

Difference ($) $ 735

Difference (%) 3.0%

68th Annual Federal Tax Conference

Policy recommendations 10

68th Annual Federal Tax Conference 61

Key questions for the policy discussion

• Should collective investment vehicles be subject to the corporate tax?

• What types of income should collective investment vehicles be allowed to receive?

• What operating model should the tax system adopt if we are to expand the collective

investment vehicle concept to other asset classes?

• What other tax law changes should be adopted in order to enable the collective

investment system to function properly?

68th Annual Federal Tax Conference 62

Should collective investment vehicles be subject to the corporate tax?

• Collective investment vehicles do not implicate the policy objectives underlying the corporate tax

− Annual distributions of taxable income prevent the accumulation of retained earnings

− Asset classes that are appropriate for collective investment vehicles tend not to be prone to monopoly

• Collective investment vehicles can help advance the policy objectives underlying the corporate tax by

loaning money to corporations or leasing capital assets to corporations, and in each case charging

interest or rent

− Rent payments made by a corporate user of capital to a collective investment vehicle prevent the accumulation of

retained earnings

» In this sense, rent payments made by a corporate user of capital to a collective investment vehicle function as a tax imposed

on the corporate sector by the private sector

• Collective investment can advance socially desirable outcomes

− Provides small investors with exposure to asset classes normally available only to wealthy or institutional investors

− Encourages investors to set aside money for future commitments

» Individuals: college, housing, retirement, etc.

» Corporations: pension obligations

» Insurance companies: future claims

− Helps build a bridge between smaller savers and users of capital, who might otherwise be able to find one another

only through the banking system

» Eliminating the banking system as an intermediary between savers and users of capital can increase investors’ returns

while also reducing users’ cost of capital

68th Annual Federal Tax Conference 63

• Aside from false premises, one of the key shortcomings of the current debate concerns the use of words such as

“passive” and “active”

− Congress intended REITs to be “passive” without providing a definition

− The term “passive” seems to have been used in the context of the 1936 RIC Legislation to ensure that—

» RICs could not be used to obtain control over corporations which could create monopolies, and

» Banks could not use externally managed RICs to exert control over industries

− The “passive” concept seemed to be satisfied through the 10% concentration limitation imposed on RICs and did not focus on

the actions the RIC was able to take in order to earn money

• We should stop using the terms “passive” and “active” to distinguish between those entities which should be subject to

the corporate tax and those which should not

− The term “passive” has never been relevant to delineate the types of activities that should or should not be subject to the

corporate tax

» The corporate tax was designed to limit the accumulation of retained earnings that could be used to engage in monopolistic or

other economically harmful behavior

» The distinction between “passive” and “active” has nothing to do with this policy objective

− The use of the terms “passive” and “active” to distinguish between “passive” RICs that should be outside the corporate tax base

and REITs whose TRSs “do things” (e.g., provide non-customary services or earn non-REIT income) is a fundamentally flawed

approach, because many RICs “do things” that would appear to be “active”

» At the very least, most non-index RICs are engaged in the trade or business of trading in securities

» Many equity RICs actively monitor and engage with the companies in which they invest on a regular basis

» Most debt-focused RICs are engaged in a loan origination business

» BDC RICs are basically non-deposit banking institutions

What types of income should collective investment vehicles be allowed to receive?

68th Annual Federal Tax Conference 64

What should replace the active/passive distinction?

• Although it has used the terms “passive” and “active,” what Congress has really been focused on is the type of income

being earned and the reason it is being earned

• Collective investment is all about using saved money to earn more money in order to fund future consumption

• If we want to encourage collective investment as a socially desirable activity that should not be punished by the

corporate tax, and if we want collective investment vehicles to be able to make money by allowing other people to use

our savings for a while, then we should allow collective investment vehicles to do whatever they need to do in order to

earn returns in the nature of—

− dividends, rent, interest, royalties, and

− gains from assets that produce these types of returns

• Requires us to acknowledge that—

− Rent and interest are economically the same thing—income received by an owner of capital as compensation for allowing

someone else to use that capital—and should be treated the same way

− In terms of distinguishing between collective investment vehicles that should not be subject to the corporate tax and those

entities that should be subject to the corporate tax, the things that must be done in order to earn rent and interest should not

affect the analysis

» Lenders must “do things” in order to earn interest—loan negotiation, structuring, and restructuring; overseeing the board and

management (in the case of loans coupled with conversion features or equity kickers); determining whether to advance new loans

in the case of a revolving loan

» Property owners must likewise do things in order to earn rent—building repair and maintenance; provision of utilities; provision of

services that tenants demand in order to occupy the property

− The main focus should be on whether—

» The entity operates in a way that does not run afoul of the policy objectives underlying the corporate tax, and

» Can help advance those policy objectives where the counterparty is a corporation

68th Annual Federal Tax Conference 65

What types of assets could a collective investment vehicle own?

• Tangible assets: any asset that can be owned by one party and used by another in exchange for rent or a usage fee

− Infrastructure, including power plants, airports, bridges, tunnels, etc.

− Plant, equipment, and machinery

• Intangible assets present a tougher question

− Intangible assets that require no further development and can be licensed for a fee should be treated the same as tangible

property

» Movies, music, books, syndicated television shows

» Patents for products that do not require further development

− Intangible assets that require further development raise tough questions regarding who handles the development

» Development work could be handled through a TRS in order to avoid unfair competition with taxable technology companies

» Can rely on the additional safeguards described below

• Manufacturers of personal property raise tricky questions

− The manufacturing function should likely be subject to the corporate tax through the use of a TRS—

» Manufacturing and leasing of personal property is the type of activity that can tend toward monopoly

» Allowing collective investment vehicles to engage in manufacturing activities free of the corporate tax can create an unfair

competitive advantage

− Can rely on the additional safeguards described below

68th Annual Federal Tax Conference 66

What types of assets could a collective investment vehicle own? (cont'd)

• Additional safeguards—

− TRS size limit can help prevent collective investment vehicles from competing unfairly with taxable

manufacturing and technology companies

− 163(j) limits earnings stripping out of the TRS

− Prohibition on related party rent can prevent earnings stripping between a collective investment

vehicle and a related corporation

− 100% penalty tax on non-arm's length arrangements between the collective investment vehicle and

the TRS prevents abuse

− 100% penalty tax on sale of dealer property by the collective investment vehicle or its subsidiaries

(would lock manufacturer/sellers out of collective investment vehicle status)

− Distribution requirement can be imposed on the TRS as well as the collective investment vehicle to

ensure against the accumulation of retained earnings

68th Annual Federal Tax Conference 67

• Existing Models

− Subchapter M: RICs and REITs

− Grantor trusts

− REMICs

− MLPs

• Key attributes that a collective investment vehicle should possess

− Capital markets acceptance

» Flexible capital structure

» Flexible and familiar corporate governance structure

» Investor–friendly tax reporting

> ECI, UBTI, state tax filings

− Ability to own and transfer a variety of assets

• On these attributes, the Subchapter M entities win the debate hands down

− Subchapter M entities provide—

» Flexible capital structure and corporate governance

» Investor–friendly tax reporting (no ECI, UBTI, or state tax filings)

− Grantor trusts and REMICs are too limited

» Set-and-forget vehicles are too limited for broad asset classes

» Rigid capital structure requirements make grantor trusts unsuitable for public capital markets

− MLPs are flexible but unfriendly for individual, tax-exempt, and foreign investors

What operating model should the tax system adopt if we are to expand the

collective investment vehicle concept to other asset classes?

68th Annual Federal Tax Conference 68

• Create disincentives for the corporate ownership of assets that could be owned by a collective investment vehicle and

leased to a corporation

− Having corporations rent their assets reduces retained earnings and thereby advances the policy objectives underlying the

corporate tax

− In order to discourage corporations from owning their assets (and using asset ownership as a way to accumulate earnings),

consider eliminating accelerated depreciation for assets that could be held by a collective investment vehicle

• MLP migration

− The expansion of Subchapter M may enable collective investment vehicles to do things that MLPs are allowed to do

− This could place MLPs at a competitive disadvantage to the new collective investment vehicle structure, as MLPs are less

capital markets and investor friendly than Subchapter M entities

− Possible changes

» Allow MLPs to migrate to the new collective investment vehicle format on a tax–free basis

> Need recapture mechanism for negative tax capital of MLP unitholders

» Modify MLP reporting system to conform as closely as possible to the tax reporting and treatment of the new collective investment

vehicle structure

> Eliminate UBTI and ECI for tax-exempt and foreign MLP investors

> Eliminate creation of additional negative tax capital

> Provide simplified net income reporting on Form 1099

> Permit treaty withholding under RIC rules

» Allow C corporations to convert to MLP status, subject to E&P distribution requirement, Section 1374, etc.

What other tax law changes should be adopted in order to enable the

collective investment system to function properly?

68th Annual Federal Tax Conference 69

• Further considerations—