Business Tax Reform and Economic Growth - … · Business Tax Reform and Economic Growth ... RICs...

20

Business Tax Reform and Economic Growth Jason Furman Chairman, Council of Economic Advisers September 22, 2014

Transcript of Business Tax Reform and Economic Growth - … · Business Tax Reform and Economic Growth ... RICs...

Business Tax Reform and Economic Growth

Jason Furman Chairman, Council of Economic Advisers

September 22, 2014

1

Economic Recovery and Economic Growth

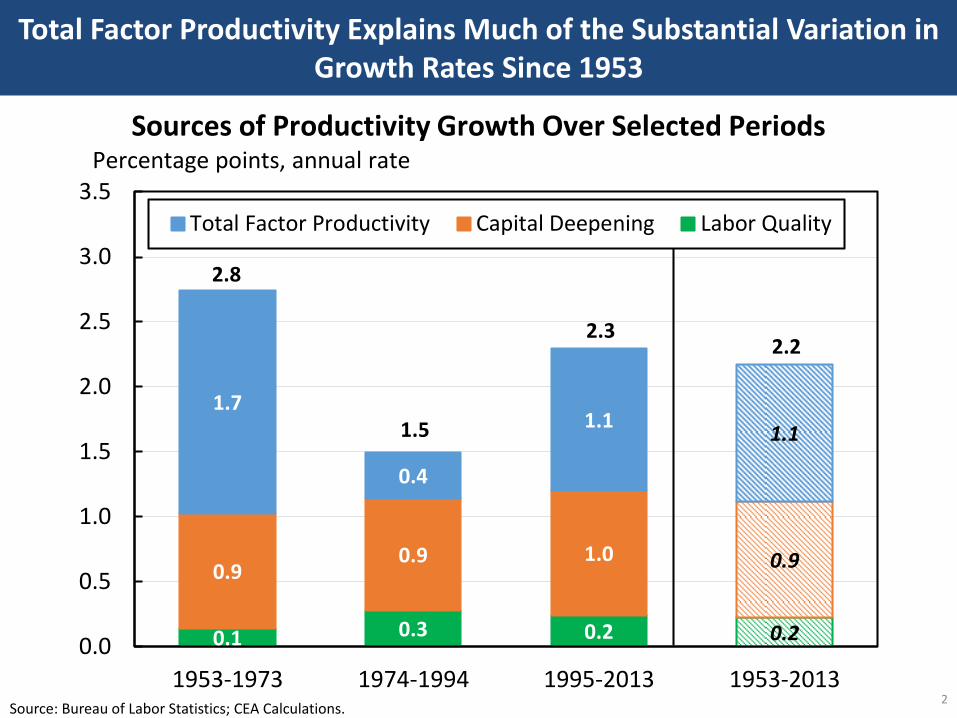

Total Factor Productivity Explains Much of the Substantial Variation in Growth Rates Since 1953

2

0.1 0.3 0.2 0.2

0.90.9 1.0 0.9

1.7

0.4

1.11.1

2.8

1.5

2.32.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1953-1973 1974-1994 1995-2013 1953-2013

Total Factor Productivity Capital Deepening Labor Quality

Sources of Productivity Growth Over Selected PeriodsPercentage points, annual rate

Source: Bureau of Labor Statistics; CEA Calculations.

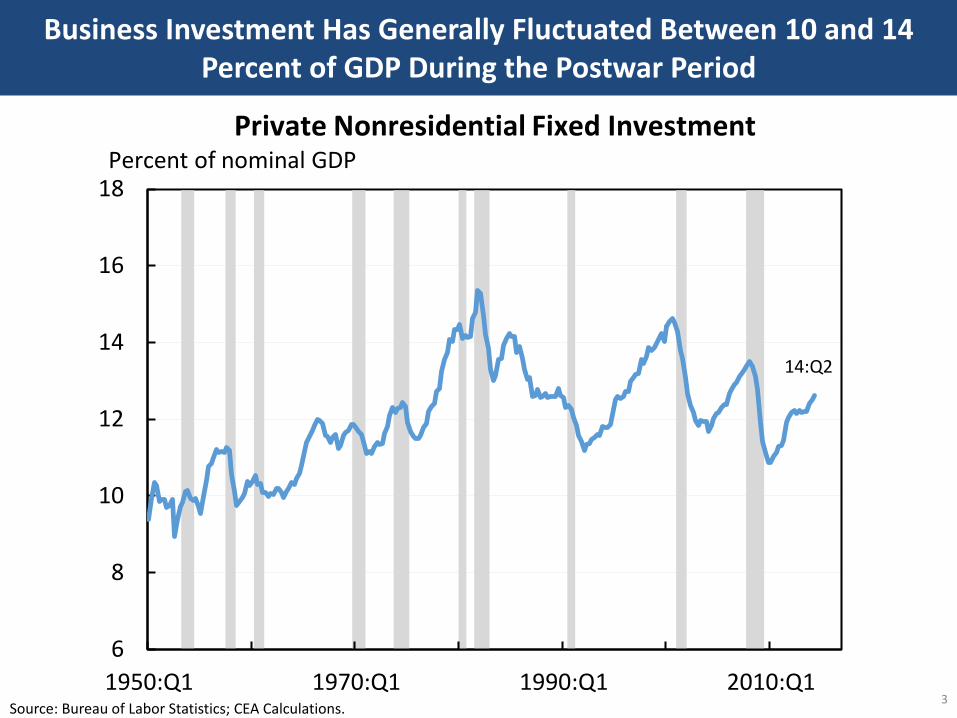

Business Investment Has Generally Fluctuated Between 10 and 14 Percent of GDP During the Postwar Period

3 Source: Bureau of Labor Statistics; CEA Calculations.

6

8

10

12

14

16

18

1950:Q1 1970:Q1 1990:Q1 2010:Q1

Private Nonresidential Fixed InvestmentPercent of nominal GDP

14:Q2

4

The Fundamental Underpinnings of Business Tax Reform

The Fundamental Underpinnings of Business Tax Reform

5

1.In general the tax system should strive for neutrality.

2. In carefully delineated specific cases, the tax system should deviate from neutrality to correct externalities.

3.The tax system should be simpler.

6

Shortcomings of the Current U.S. Business Tax System

The U.S. has Maintained a High Corporate Tax Rate Since the 1980s While Peer Countries Reduced Rates

7 Source: OECD.

25

30

35

40

45

50

55

1981 1985 1989 1993 1997 2001 2005 2009 2013

OECD Weighted Average (excluding U.S.)

United States

PercentStatutory Corporate Tax Rates in the U.S. and OECD

The U.S. has the Highest Corporate Tax Rate in the World

8

10

15

20

25

30

35

40

Irel

and

Slo

ven

ia

Cze

ch R

epu

blic

Hu

nga

ry

Po

lan

d

Ch

ile

Fin

lan

d

Icel

and

Turk

ey

Esto

nia

Un

ited

Kin

gdo

m

Swit

zerl

and

Slo

vak

Rep

ub

lic

Swed

en

Ko

rea

Den

mar

k

Au

stri

a

Net

her

lan

ds

Gre

ece

Can

ada

Isra

el

No

rway

Ital

y

New

Zea

lan

d

Luxe

mb

ou

rg

Au

stra

lia

Mex

ico

Spai

n

Ger

man

y

Po

rtu

gal

Bel

giu

m

Fran

ce

Jap

an

Un

ited

Sta

tes

Statutory Corporate Income Tax Rates, 2014Percent

OECD Weighted Average (excluding U.S.): 29.7

Source: OECD.

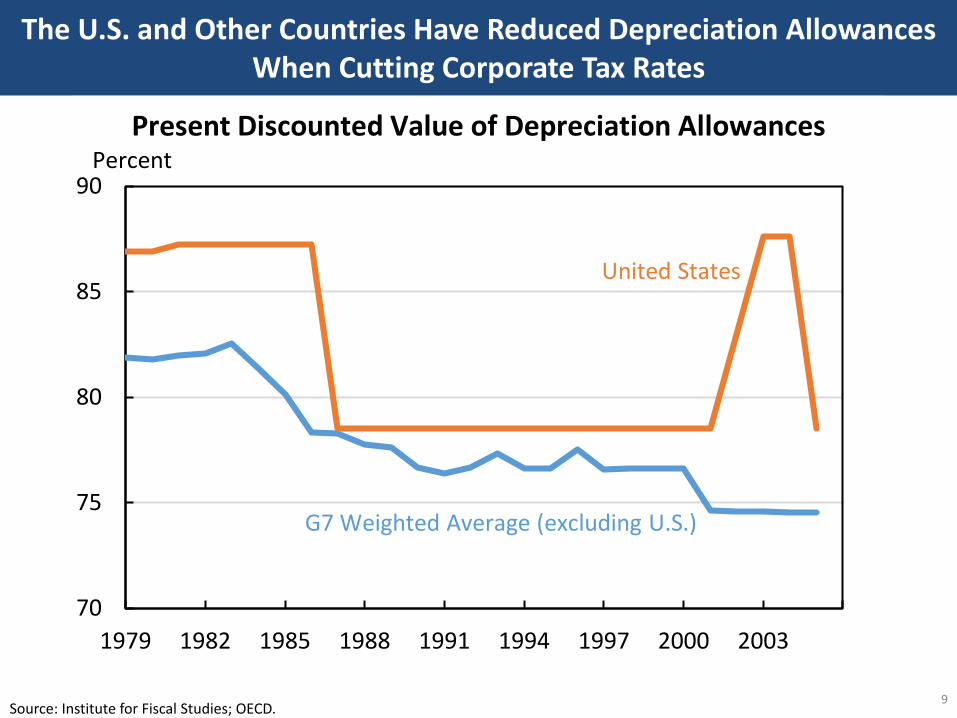

The U.S. and Other Countries Have Reduced Depreciation Allowances When Cutting Corporate Tax Rates

9

70

75

80

85

90

1979 1982 1985 1988 1991 1994 1997 2000 2003

Present Discounted Value of Depreciation AllowancesPercent

United States

G7 Weighted Average (excluding U.S.)

Source: Institute for Fiscal Studies; OECD.

U.S. Effective Marginal Tax Rates are in Line with Other G7 Countries

10 Source: U.S. Department of the Treasury; OECD.

2324

28 29

32 33

43

15

20

25

30

35

40

45

Germany Italy France UnitedStates

UnitedKingdom

Canada Japan

Effective Marginal Tax Rates, 2011

G7 Weighted Average(excluding U.S.):

31.7

Percent

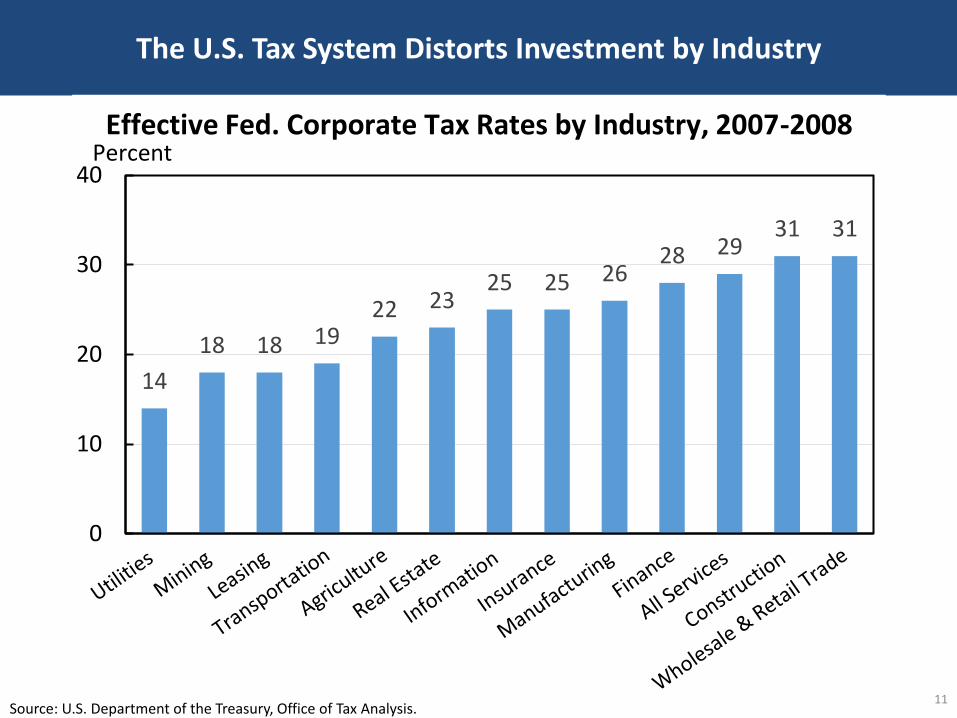

The U.S. Tax System Distorts Investment by Industry

11

14

18 18 1922 23

25 25 2628 29

31 31

0

10

20

30

40

Effective Fed. Corporate Tax Rates by Industry, 2007-2008Percent

Source: U.S. Department of the Treasury, Office of Tax Analysis.

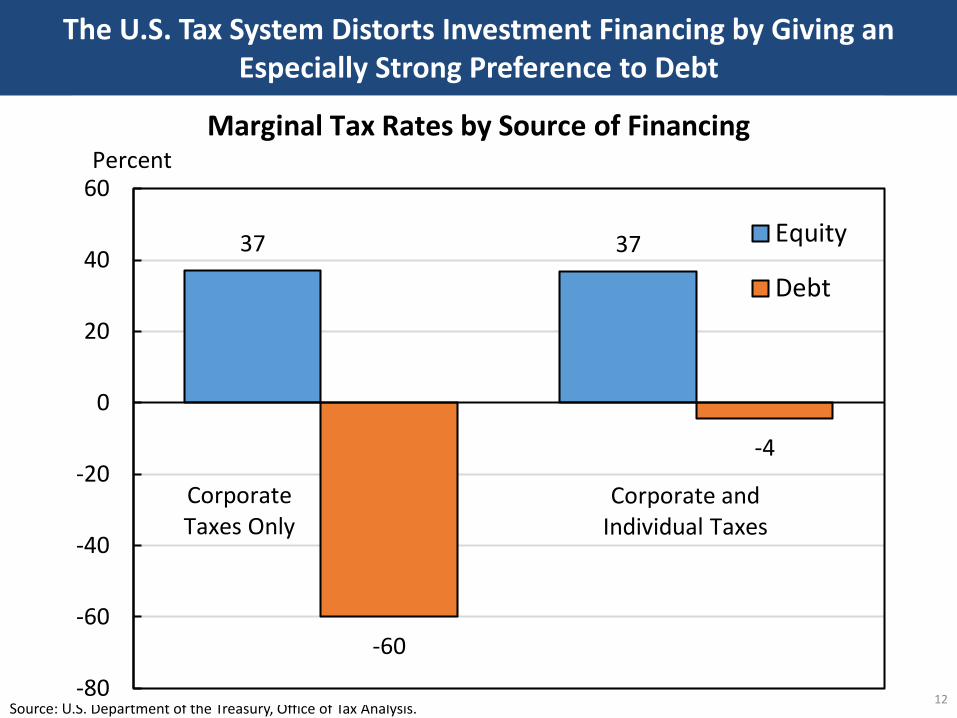

The U.S. Tax System Distorts Investment Financing by Giving an Especially Strong Preference to Debt

12 Source: U.S. Department of the Treasury, Office of Tax Analysis.

37 37

-60

-4

-80

-60

-40

-20

0

20

40

60

Equity

Debt

Marginal Tax Rates by Source of FinancingPercent

Corporate and Individual Taxes

CorporateTaxes Only

The U.S. Tax System Distorts the Form of Business by Disfavoring Large C Corporations

13

32

26

0

10

20

30

40

Effective Marginal Tax Rates on New Investment

Corporate Pass-through

Overall Business Tax Rate: 30.1

Percent

Source: U.S. Department of the Treasury, Office of Tax Analysis.

Business Receipts have Shifted Away from C Corporations

14

50

60

70

80

90

100

1980 1985 1990 1995 2000 2005 2010

C Corporation Share of Total Business ReceiptsPercent

Note: RICs and REITs excluded from both C corporation share and total. Source: IRS; CEA Calculations.

The U.S. Tax System Distorts the Location of Production and Profits

15 Source: IRS and United Nations; CEA Calculations.

Country

U.S. Controlled Foreign

Corporation Profits

Relative to GDP (2010)

Bahamas 104%

Bermuda 1,578%

British Virgin Islands 1,009%

Cayman Islands 1,430%

Cyprus 13%

Ireland 38%

Luxembourg 103%

Netherlands 15%

Netherlands Antilles 25%

16

The President’s Framework For Business Tax Reform

The President’s Framework For Business Tax Reform

17

• Cutting the corporate rate to 28 percent, paid for by closing loopholes and structural reforms.

• Making permanent, expanding and reforming key incentives.

• Establishing a hybrid international system with a minimum tax on the earnings of foreign subsidiaries.

• Simplifying and reducing taxes for small businesses.

• Funding immediate investments while being revenue neutral over the medium and long run.

18

Addressing Four Objections to the Approach to Tax Rates in the President’s

Framework For Business Tax Reform

The President’s Framework For Business Tax Reform: Addressing Four Objections

19

1. The Traditional Economist’s View: Tax Rate Reductions are a Windfall for Old Capital

2. The New Economist’s View: The Corporate Tax Rate Should be Zero

3. The Conservative View: The Top Individual Rate Needs to Be Cut with the Corporate Rate

4. The Progressive View: Corporate Loophole Closures Should Not Fund Rate Reductions