Mobilizing international resources for development: Foreign direct investment and other private...

24

Mobilizing international resources for development: Foreign direct investment and other private flows Mansoor Dailami New York February 15th, 2008 ager, International Finance, Development Prospects Group, World Ban

-

Upload

alivia-sheard -

Category

Documents

-

view

221 -

download

0

Transcript of Mobilizing international resources for development: Foreign direct investment and other private...

Mobilizing international resources for development: Foreign direct investment and other private

flows

Mansoor Dailami

New YorkFebruary 15th, 2008

Manager, International Finance, Development Prospects Group, World Bank

Summary and key issues

Private capital flows to developing countries have

been on a strong upward trend, supported by

domestic economic reforms and high growth

FDI continues to be the largest and most stable

capital flow with increasing focus on services

Private capital flows expected to decline somewhat

in the short term amid more moderate global

growth and tighter credit conditions

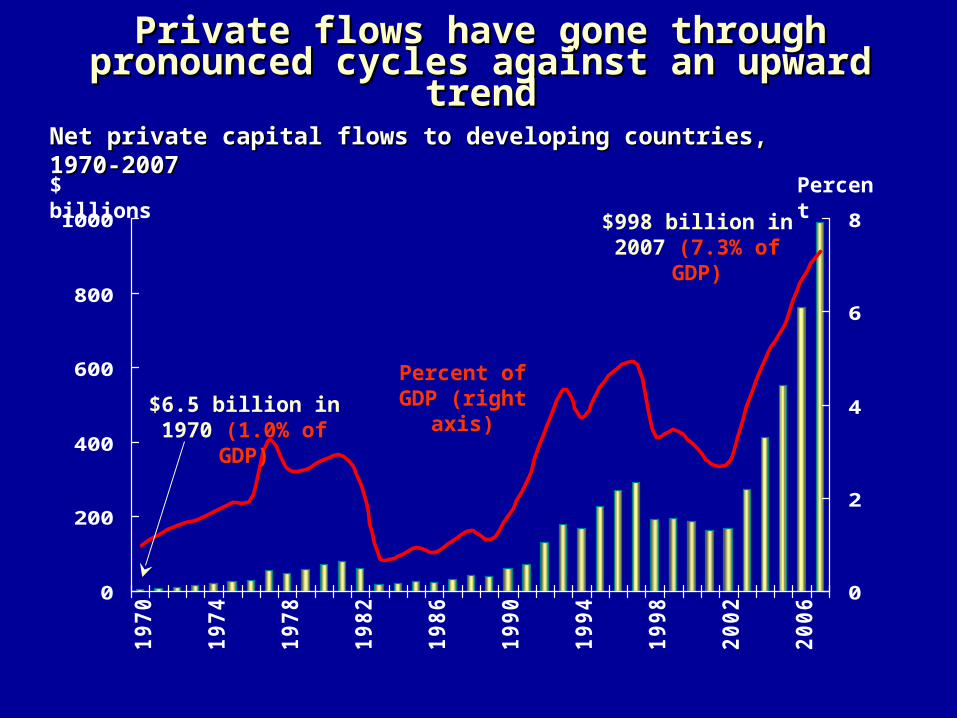

Private flows have gone through Private flows have gone through pronounced cycles against an upward pronounced cycles against an upward

trendtrend

$ billions

0

200

400

600

800

1000

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

0

2

4

6

8

Net private capital flows to developing countries, Net private capital flows to developing countries, 1970-20071970-2007

Percent of GDP (right

axis)

Percent$998 billion in

2007 (7.3% of GDP)

$6.5 billion in 1970 (1.0% of

GDP)

… … dominated by cycles in dominated by cycles in international bank lending…international bank lending…

Percent

-1

0

1

2

3

4

1970 1975 1980 1985 1990 1995 2000 2005

Net private debt flows to developing countries Net private debt flows to developing countries , , 1970-20071970-2007

Bonds

Bank loans

0

100

200

300

400

500

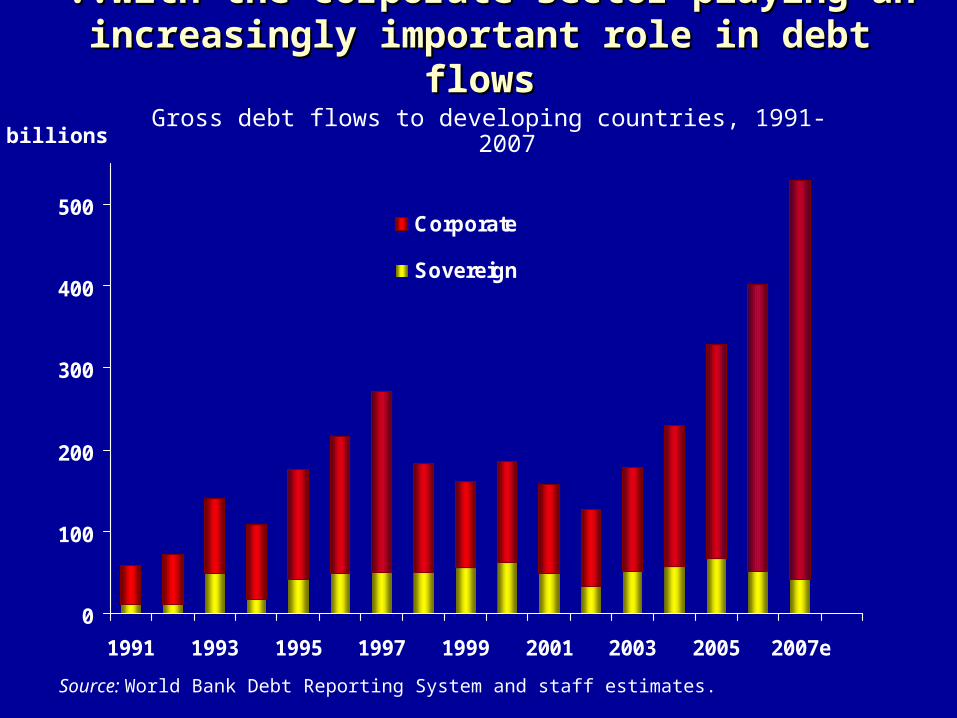

1991 1993 1995 1997 1999 2001 2003 2005 2007e

Corporate

Sovereign

$ billionsGross debt flows to developing countries, 1991-2007

..with the corporate sector playing an ..with the corporate sector playing an increasingly important role in debt flowsincreasingly important role in debt flows

Source: World Bank Debt Reporting System and staff estimates.

$ billions

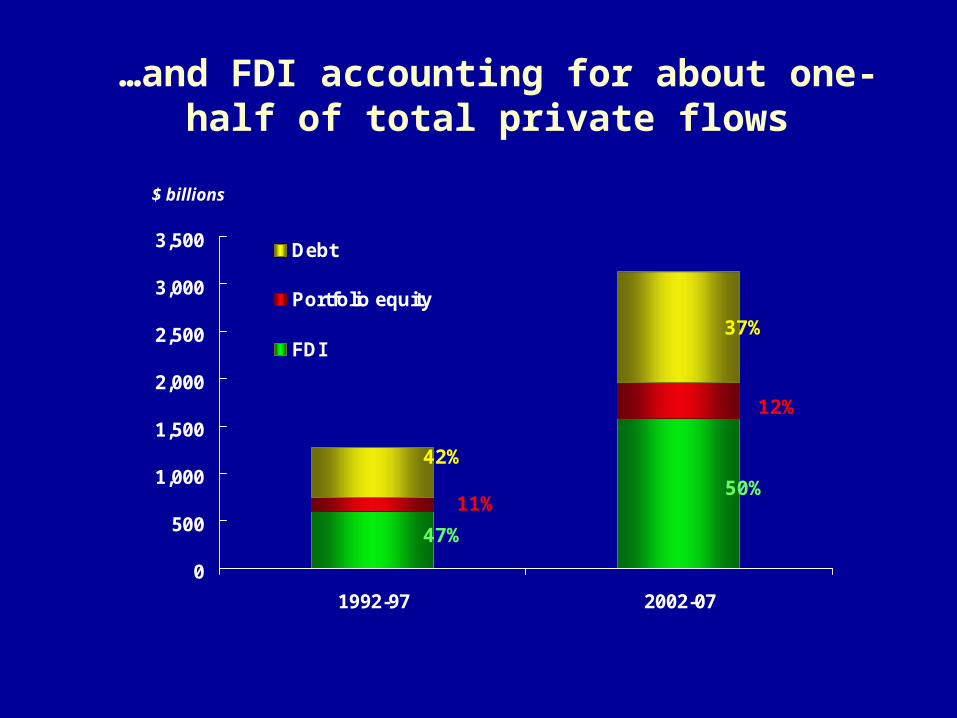

…and FDI accounting for about one-half of total private flows

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1992-97 2002-07

Debt

Portfolio equity

FDI

12%

37%

50%

42%

11%

47%

-2

0

2

4

6

8

10

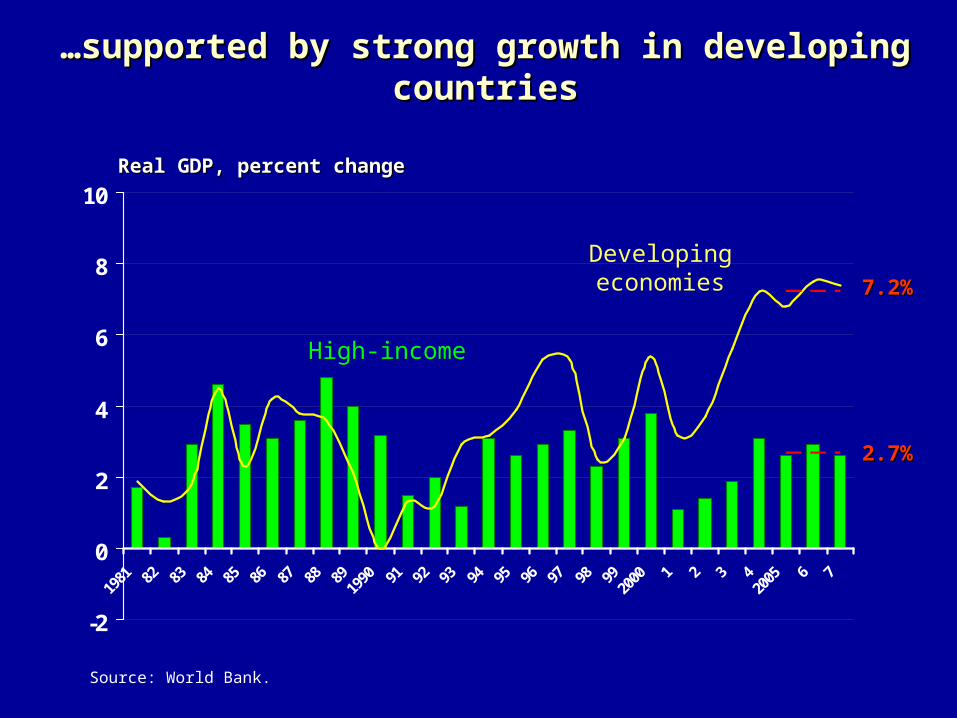

……supported by strong growth in developing supported by strong growth in developing countriescountries

Real GDP, percent changeReal GDP, percent change

Source: World Bank.

Developing economies

High-income

7.27.2%%

2.72.7%%

……and improved external payments and improved external payments positions positions

--current account surpluses in many --current account surpluses in many countriescountries

$ billions

- 3 0 0

- 1 5 0

0

1 5 0

3 0 0

4 5 0

1 9 9 0 1 9 9 2 1 9 9 4 1 9 9 6 1 9 9 8 2 0 0 0 2 0 0 2 2 0 0 4 2 0 0 6

- 4

- 3

- 2

- 1

0

1

2

3

4

Current account balance of developing countries

Percent of GDP (right

axis)

Percent$408 billion in $408 billion in

20072007

0

400

800

1200

1600

2000

2400

2800

3200

3600

4000

Oil-exportingcountries

Emerging Asia Developingcountries

1995199920052007

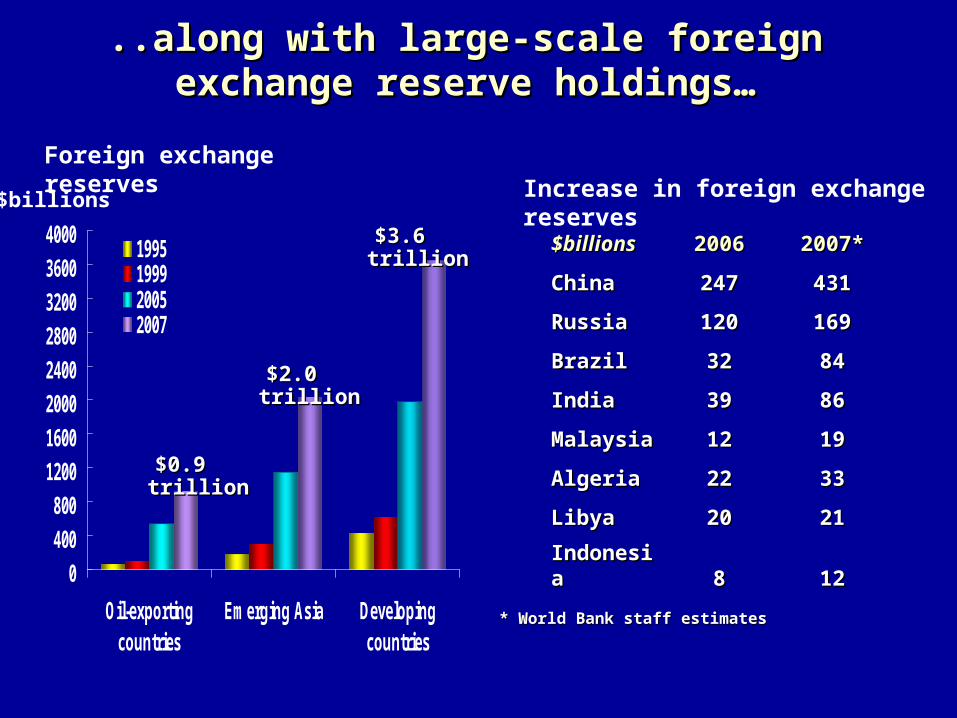

..along with large-scale foreign ..along with large-scale foreign exchange reserve holdings…exchange reserve holdings…

$billions

Foreign exchange reserves

$3.6 trillion$3.6 trillion

$2.0 trillion$2.0 trillion

$0.9 trillion$0.9 trillion

$billions$billions 20062006 2007*2007*

ChinaChina 247247 431431

RussiaRussia 120120 169169

BrazilBrazil 3232 8484

IndiaIndia 3939 8686

MalaysiaMalaysia 1212 1919

AlgeriaAlgeria 2222 3333

LibyaLibya 2020 2121

IndonesiIndonesiaa 88 1212

Increase in foreign exchange reserves

* World Bank staff estimates* World Bank staff estimates

……improved external financial policy…improved external financial policy…

Many developing countries have moved Many developing countries have moved to managed or free floating exchange to managed or free floating exchange rate regimesrate regimes

Mexico(1994), Indonesia(1997), Colombia(1999), Brazil(1999), Chile(1999), and Russian Federation(2002)...

Capital controls have been easedCapital controls have been easedBrazil, Chile, Hungary, Romania, and Slovak Republic...

Some have adopted inflation targetingSome have adopted inflation targetingBrazil, Chile, Colombia, Mexico, Peru, Philippines, South Africa, and Thailand...

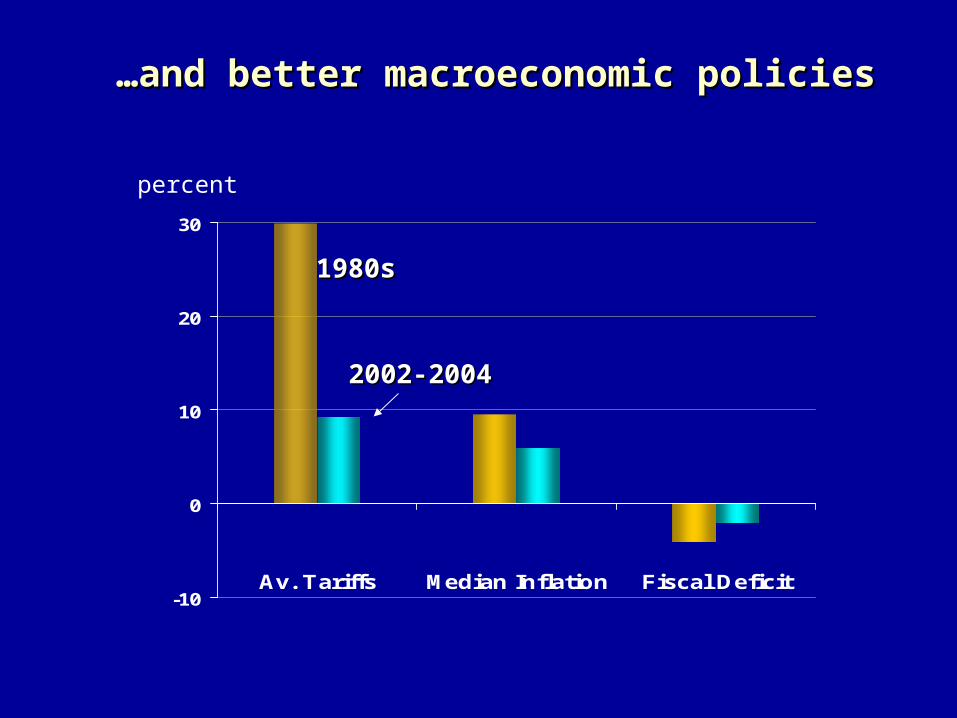

-10

0

10

20

30

Av. Tariffs Median Inflation Fiscal Deficit

……and better macroeconomic policiesand better macroeconomic policies

percent

1980s1980s

2002-20042002-2004

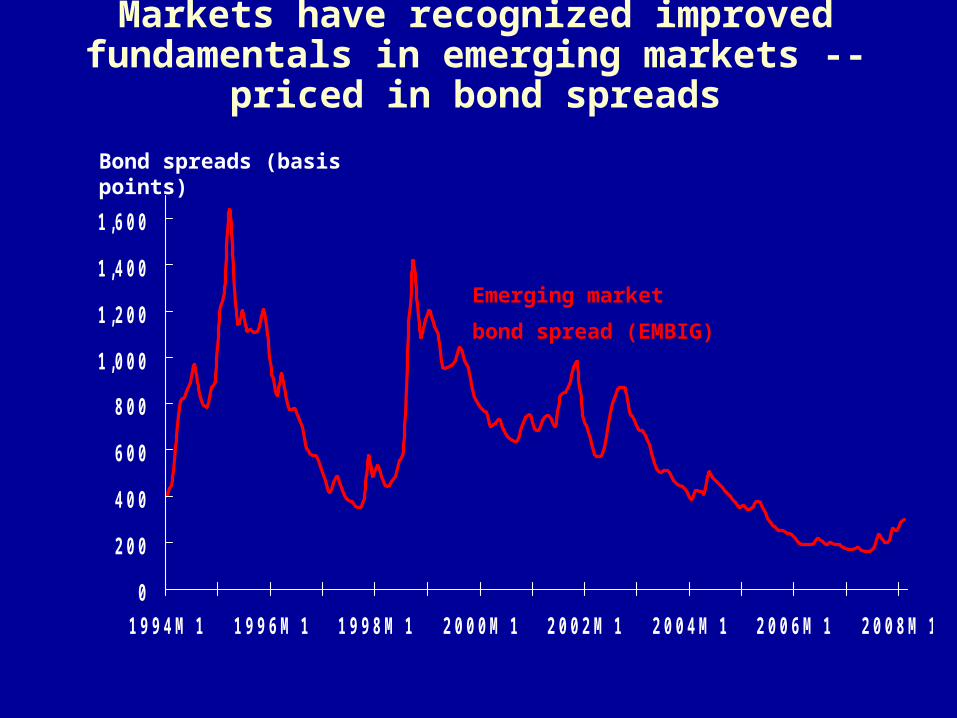

Markets have recognized improved fundamentals in emerging markets --

priced in bond spreads

0

2 0 0

4 0 0

6 0 0

8 0 0

1 , 0 0 0

1 , 2 0 0

1 , 4 0 0

1 , 6 0 0

1 9 9 4 M 1 1 9 9 6 M 1 1 9 9 8 M 1 2 0 0 0 M 1 2 0 0 2 M 1 2 0 0 4 M 1 2 0 0 6 M 1 2 0 0 8 M 1

Bond spreads (basis points)

Emerging market

bond spread (EMBIG)

Summary and key issues

Private capital flows to developing countries have

been on a strong upward trend, supported by

domestic economic reforms and high growth

FDI continues to be the largest and most stable

capital flow with increasing focus on services

Private capital flows expected to decline somewhat

in the short term amid more moderate global

growth and tighter credit conditions

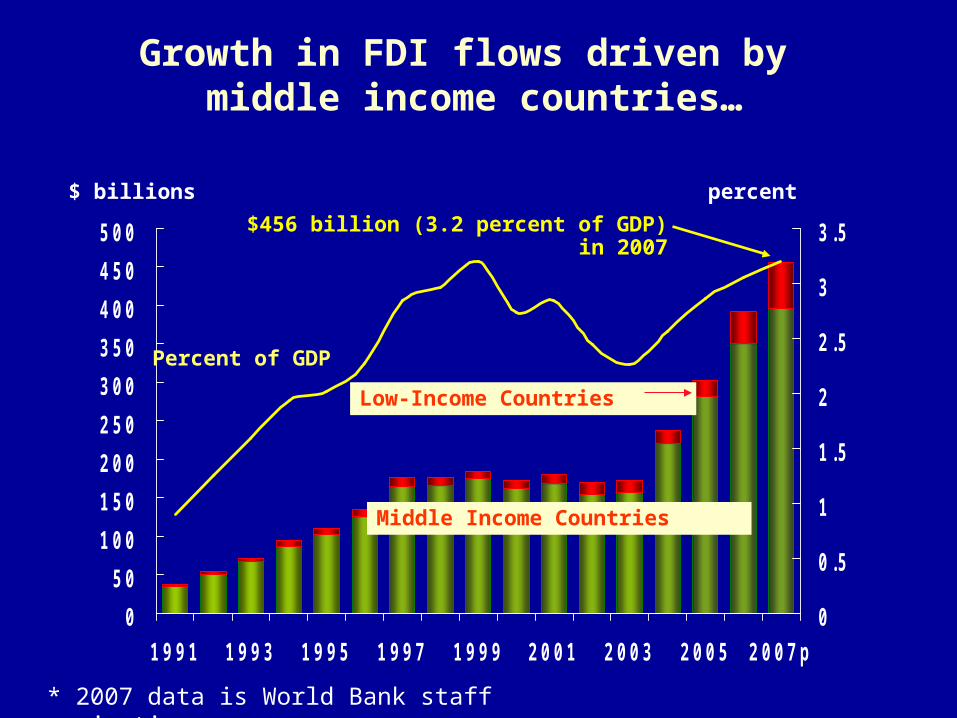

Growth in FDI flows driven by middle income countries…

0

5 0

1 0 0

1 5 0

2 0 0

2 5 0

3 0 0

3 5 0

4 0 0

4 5 0

5 0 0

1 9 9 1 1 9 9 3 1 9 9 5 1 9 9 7 1 9 9 9 2 0 0 1 2 0 0 3 2 0 0 5 2 0 0 7 p

0

0 . 5

1

1 . 5

2

2 . 5

3

3 . 5

$ billions percent

Percent of GDP

Middle Income Countries

Low-Income Countries

$456 billion (3.2 percent of GDP) in 2007

* 2007 data is World Bank staff projection

0

1 0 0

2 0 0

3 0 0

4 0 0

5 0 0

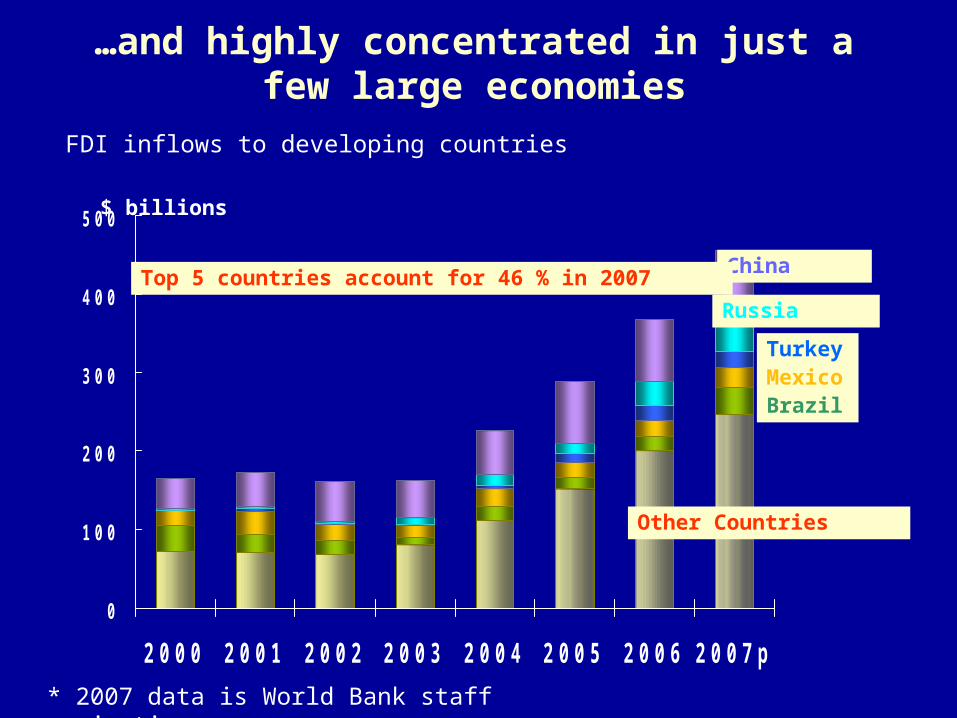

2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 p

$ billions

FDI inflows to developing countries

…and highly concentrated in just a few large economies

Other Countries

Russia

China

* 2007 data is World Bank staff projection

TurkeyMexic

o Brazil

Top 5 countries account for 46 % in 2007

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

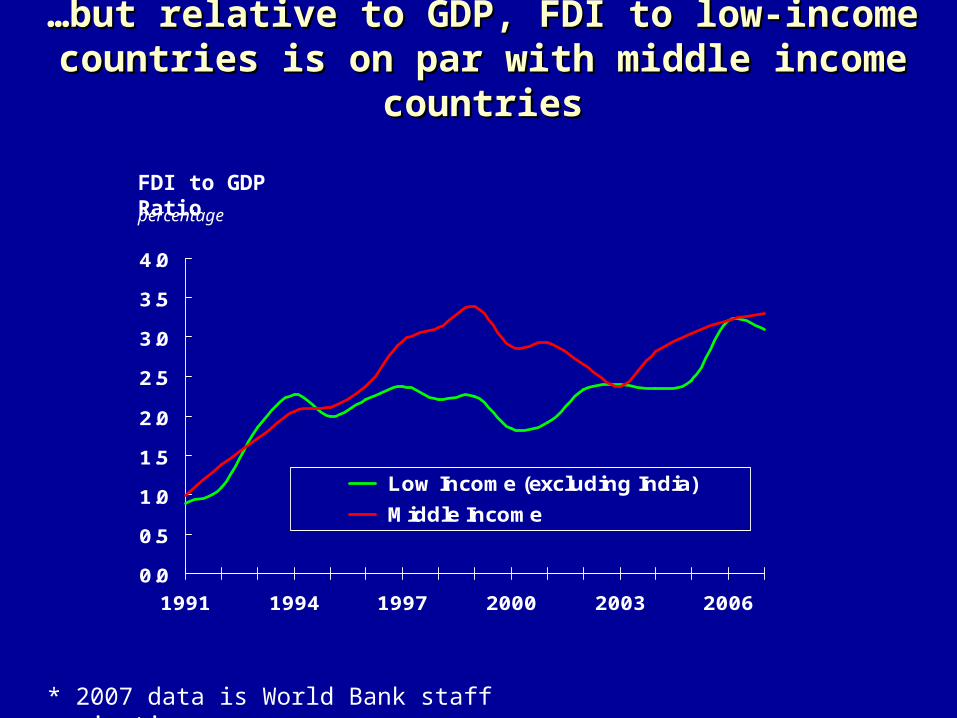

1991 1994 1997 2000 2003 2006

Low Income (excluding India)

Middle Income

percentage

FDI to GDP Ratio

……but relative to GDP, FDI to low-income but relative to GDP, FDI to low-income countries is on par with middle income countries is on par with middle income

countriescountries

* 2007 data is World Bank staff projection

FDI inflows are closely related to FDI inflows are closely related to income per capitaincome per capita

FDI per capita vs GDP per capita, 2001-06FDI per capita vs GDP per capita, 2001-06

y = 1.27x - 5.5

R2 = 0.69

-2

0

2

4

6

8

4 5 6 7 8 9 10

log(GDP per capita)

log(FDI per capita)China

Bolivia

Gambia

Azerbaijan

Equatorial Guinea

Zimbabwe

Iran

Venezuela

Oman

Chad

Romania

India

South Africa

MalawiRwanda

Central African Republic

Turkey

Congo, Dem. Rep.

Trinidad & Tobag

o

0

1 0

2 0

3 0

4 0

5 0

6 0

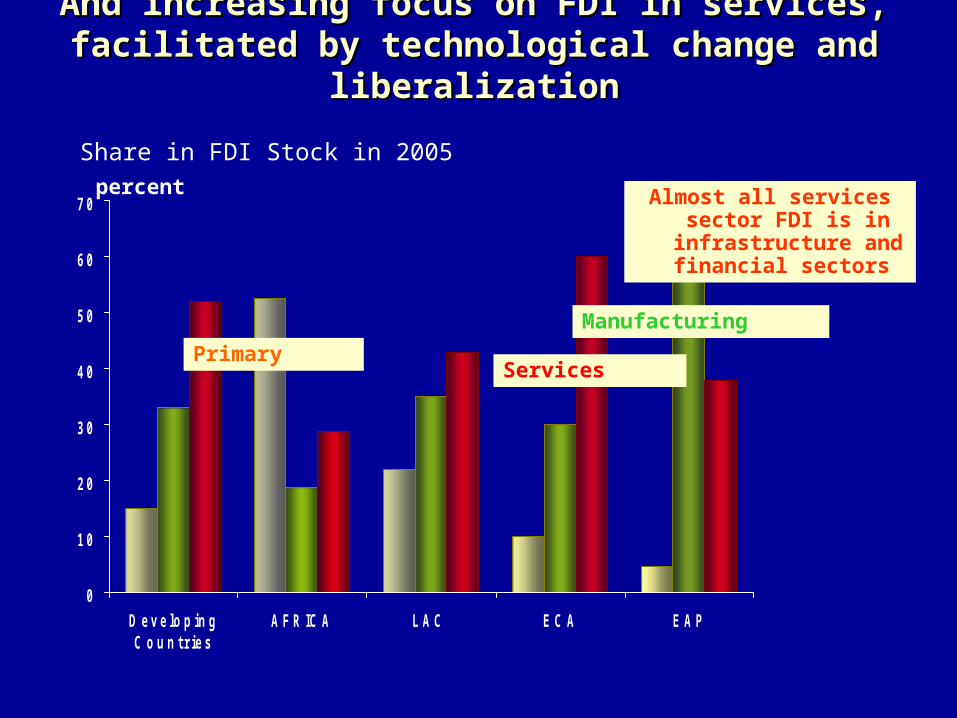

7 0

D e v e lo p in gC o u n t r ie s

A F R IC A L A C E C A E A P

percent

Share in FDI Stock in 2005

And increasing focus on FDI in services, And increasing focus on FDI in services, facilitated by technological change and facilitated by technological change and

liberalizationliberalization

Services

Manufacturing

Primary

Almost all services sector FDI is in

infrastructure and financial sectors

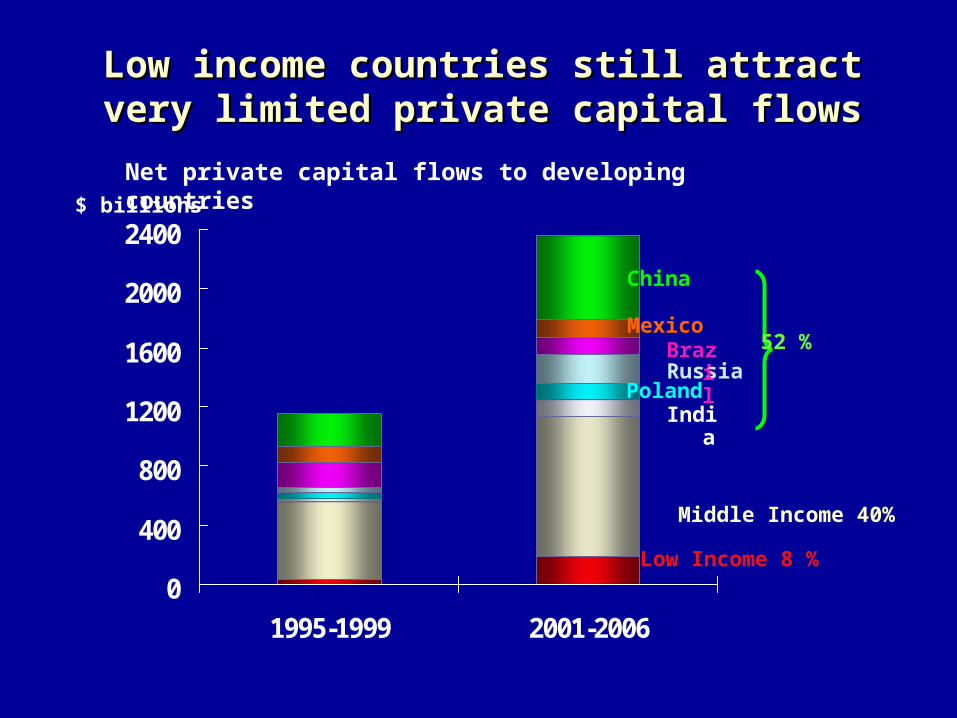

Low income countries still attract very Low income countries still attract very limited private capital flowslimited private capital flows

Russia

0

400

800

1200

1600

2000

2400

1995-1999 2001-2006

China

MexicoBraz

il

India

Middle Income 40%

Low Income 8 %

52 %

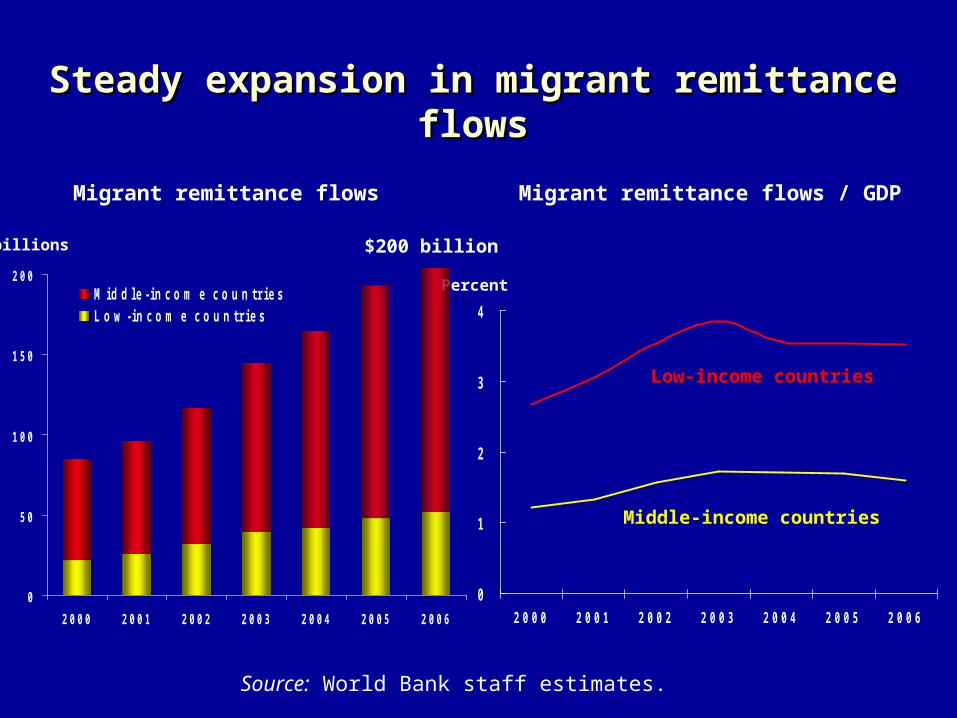

Net private capital flows to developing countries

Poland

$ billions

$ billions

0

1

2

3

4

2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

Percent

Migrant remittance flows Migrant remittance flows / GDP

Steady expansion in migrant remittance Steady expansion in migrant remittance flowsflows

0

5 0

1 0 0

1 5 0

2 0 0

2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

M i d d l e - i n c o m e c o u n t r i e sL o w - i n c o m e c o u n t r i e s

Low-income countries

Middle-income countries

$200 billion

Source: World Bank staff estimates.

Summary and key issues

Private capital flows to developing countries have

been on a strong upward trend, supported by

domestic economic reforms and high growth

FDI continues to be the largest and most stable

capital flow with increasing focus on services

Private capital flows expected to decline somewhat

in the short term amid more moderate global

growth and tighter credit conditions

Global financial conditions have Global financial conditions have worsened noticeably worsened noticeably

Moderate slowdown in global growth

Tighter credit conditions

Large losses in major financial institutions

More stringent credit standards

* Impact of financial turmoil on emerging markets limited so far…

Private capital flows expected to ease…

$ billions

0

2 0 0

4 0 0

6 0 0

8 0 0

1 0 0 0

1 9 9 1 1 9 9 3 1 9 9 5 1 9 9 7 1 9 9 9 2 0 0 1 2 0 0 3 2 0 0 5 2 0 0 7 e 2 0 0 9 P

0

2

4

6

8

Net private capital flows to developing countries

Percent of GDP (right

axis)

Percent

Projected 2008-09

$998 billion in 2007 (7.3% of

GDP)

5.25%

3.5% of GDP average 1990-

02

……but long-term prospects for but long-term prospects for increased capital flows remain positiveincreased capital flows remain positive

Developing countries’ favorable Developing countries’ favorable demographic profilesdemographic profiles About 84% of world Population reside in About 84% of world Population reside in

developing worlddeveloping world

Scope for increasing investment and Scope for increasing investment and growth (Per capita investment $500 in growth (Per capita investment $500 in 2006, compared to $6000 in developed 2006, compared to $6000 in developed countries )countries ) Less than 5% of global bonds issued in recent Less than 5% of global bonds issued in recent

years originated in developing countries.years originated in developing countries.

Further room for integration in the world Further room for integration in the world economy economy