Mobile Report - Custorapages.custora.com/.../Custora_E-commerce_Pulse_Mobile_Report.pdf · ON HIS...

12

1 CUSTORA JULY 2014 BROWSING FOR SANDALS ON AN IPHONE APP. PRETENDING SHE’S A MAGICAL DOLPHIN. READING A SUMMER SALE EMAIL FROM J CREW. UPPING HIS EBAY BID FOR A GUITAR ON A KINDLE. JUST BOUGHT A NEW SOFA ON HIS MOBILE BROWSER. Mobile Report

Transcript of Mobile Report - Custorapages.custora.com/.../Custora_E-commerce_Pulse_Mobile_Report.pdf · ON HIS...

1CUSTORA

J ULY 201 4

B R O W S I N G F O R S A N D A L S O N A N I P H O N E A P P.

P R E T E N D I N G S H E ’ S A M A G I C A L D O L P H I N .

R E A D I N G A S U M M E R S A L E E M A I L F R O M J C R E W .

U P P I N G H I S E B A Y B I D F O R A G U I T A R O N A K I N D L E .

J U S T B O U G H T A N E W S O F A O N H I S M O B I L E B R O W S E R .

MobileReport

2CUSTORA

T H E E V I D E N C E surrounds us, whether it’s

commuters immersed in their tablet on the

subway, toddlers with Sesame Street apps, or

a shopper buying toilet paper on her phone to

save a little and avoid the hassle of carrying it

home. Mobile computing is doing everything

except slowing down.

And while these anecdotes add up to some-

thing meaningful on their own, we wanted to

further explore this mobile shift and learn how

it’s impacting the way people shop online.

We analyzed US e-commerce data from over

100 retailers, 70 million consumers and $10B

in transaction revenue (read more about our

methodology on page 12), and reached some

compelling findings:

Additionally, we interviewed a few marketing

professionals who work for online retailers

excelling in mobile e-commerce. These

mobile pros share insights and advice based

on their experiences from the front lines. We

also spoke with a group of online shoppers

for their perspectives on the current state of

mobile e-commerce.

1 . M O B I L E I S B O O M I N G

2 . E M A I L ? Y E S , S O C I A L ? N O

3 . A P P L E L E A D S , B U T . . .

4 . C R O S S - D E V I C E I S C O M I N G

B O N U S ! D O W N L O A D O U R D A T A

I N T R O - D U C T I O N

I N T E R V I E W K E Y

CUSTORA

ONLINE SHOPPER

E-COMMERCE MARKETER

Mobile e-commerce is now a $40 billion market,

up from $2 billion in 2010. More than a third of

visits to online stores now come from mobile

devices, up from just 3% in 2010. (pg. 3)

Email marketing does surprisingly well driving

purchases on phones and tablets; social media —

not so much. (pg. 7)

iPad reigns with 80% of tablet orders, but Samsung

and a little startup called “Amazon” are nibbling

away at the Apple with 12% and 4% and of orders

respectively as of March, 2014. (pg. 6)

Cross-device shopping isn’t quite here yet. As of

Q1 2014, 88% of customers only use one device

to make purchases. (pg. 8)

We’ve made the complete data sets for the

findings within this report available at

custora.com/mobiledata

3CUSTORA

We use the internet in different ways now than we did four

years ago. Mobile internet is faster, hardware is better, and

it’s common to use a phone or tablet frequently and in

more settings.

These shifts are reflected in e-commerce browsing: at the

start of 2010, only 3.4% of total visits to e-commerce sites

came from mobile devices (phones and tablets). Now, four

years later, 36.9% of site visits are from tablets and phones.

Mobile’s meteoric riseIn the past four years, the percentage of traffic to e-commerce sites from mobile devices (phones and tablets) jumped from 3% to nearly 37%.

SHARE (%) OF E-COMMERCE SITE VISITS BY DEVICE, 2010- Q1 2014

GROWTH

100%

50%

24.5%

4-year total growth 2010-2013 4-Year CAGR (Compound Annual Growth Rate) 2010-2013

Note: These estimates are based on US Department of Commerce figures for total US e-commerce revenue, 2010-2014, and Custora’s estimates for the share of mobile e-commerce. Read more about our methodology on page 12.

12.4%

63.1%

11.4%

17.6%

9.3%

10.6%

3.4% 5.4%0%

2010 2011 2012 2013 2014 Q1

DESKTOP

PHONE

TABLET

84.1%88.7% 73.1%96.6%

CUSTORA E-COMMERCE PULSE _ MOBILE REPORT

CUSTORA E-COMMERCE PULSE _ MOBILE REPORT DOWNLOAD

DOWNLOAD THIS DATA AT CUSTORA.COM/MOBILEDATA

In the past four years, the US mobile e-commerce market

grew 19-fold: From $2.2 billion in 2010 to $42.8 billion in

2013. 2014 is off to a strong start with $12.2 billion in

mobile e-commerce sales in Q1 alone; it’s likely that

mobile e-commerce will hit $50 billion in sales in 2014.

US mobile e-commerce is a $40 billion market

US MOBILE E-COMMERCE REVENUE

2010-2013 ($ BILLION)

$50

$2.2$12.2

$42.8

$21.2$7.9

$25

02010 2011 2012 2013 2014 (Q1)1875% 111%

4CUSTORA

VISITS

ORDERS

REVENUE

FENG CHANG

DIRECTOR BUSINESS STRATEGY &

ANALYTICS, KARMALOOP

CUSTORA

ANTHONY MARINO

CMO, THRED UP

VISHAL AGARWAL

EVP & CMO, NOMORERACK

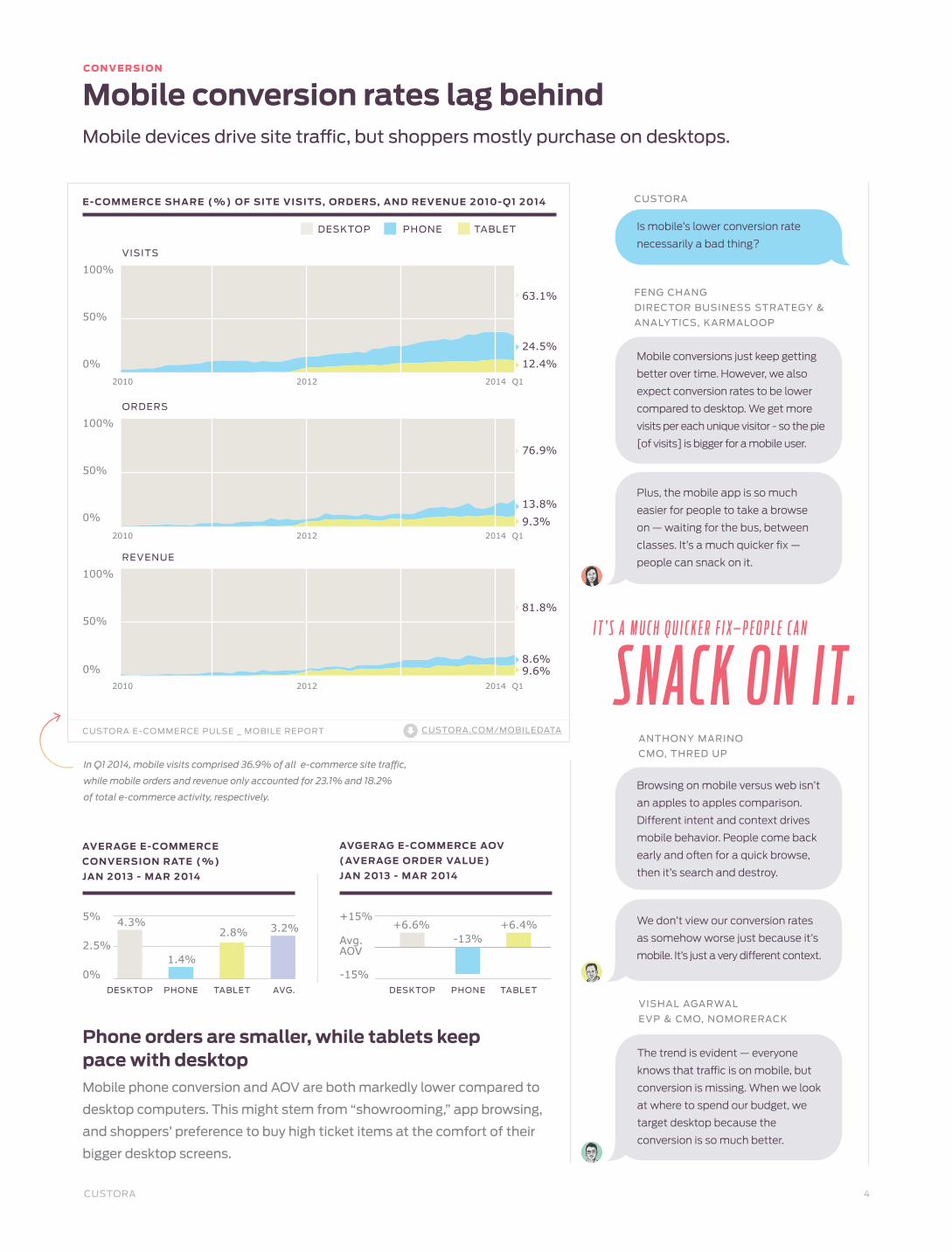

Mobile conversion rates lag behindMobile devices drive site traffic, but shoppers mostly purchase on desktops.

E-COMMERCE SHARE (%) OF SITE VISITS, ORDERS, AND REVENUE 2010-Q1 2014

In Q1 2014, mobile visits comprised 36.9% of all e-commerce site traffic,

while mobile orders and revenue only accounted for 23.1% and 18.2%

of total e-commerce activity, respectively.

Mobile phone conversion and AOV are both markedly lower compared to

desktop computers. This might stem from “showrooming,” app browsing,

and shoppers’ preference to buy high ticket items at the comfort of their

bigger desktop screens.

5% 4.3% 3.2%

1.4%

2.8%+15%

100%

100%

63.1%

76.9%

81.8%

24.5%

13.8%

8.6%

12.4%

9.3%

9.6%

100%

2.5% Avg.AOV

50%

50%

50%

0% -15%

0%

0%

0%

CONVERSION

Is mobile’s lower conversion rate

necessarily a bad thing?

Mobile conversions just keep getting

better over time. However, we also

expect conversion rates to be lower

compared to desktop. We get more

visits per each unique visitor - so the pie

[of visits] is bigger for a mobile user.

Browsing on mobile versus web isn’t

an apples to apples comparison.

Different intent and context drives

mobile behavior. People come back

early and often for a quick browse,

then it’s search and destroy.

We don’t view our conversion rates

as somehow worse just because it’s

mobile. It’s just a very different context.

The trend is evident — everyone

knows that traffic is on mobile, but

conversion is missing. When we look

at where to spend our budget, we

target desktop because the

conversion is so much better.

Plus, the mobile app is so much

easier for people to take a browse

on — waiting for the bus, between

classes. It’s a much quicker fix —

people can snack on it.

Phone orders are smaller, while tablets keep pace with desktop

2010

2010

2010

DESKTOP DESKTOP PHONE PHONETABLET TABLET AVG.

+6.6% +6.4%-13%

S N AC K O N I T.I T ’ S A M U C H Q U I C K E R F I X — P E O P L E C A N

CUSTORA E-COMMERCE PULSE _ MOBILE REPORT

AVERAGE E-COMMERCE

CONVERSION RATE (%)

JAN 2013 - MAR 2014

AVGERAG E-COMMERCE AOV

(AVERAGE ORDER VALUE)

JAN 2013 - MAR 2014

E-COMMERCE

AVG. AVERAGE ORDER VALUE (AOV)

COMPARISON 2013-Q1 2014

PHONEDESKTOP TABLET

CUSTORA.COM/MOBILEDATA

2012

2012

2012

2014 Q1

2014 Q1

2014 Q1

5CUSTORA

KHAI, AGE 27

BUSINESS DEVELOPMENT

NEW ORLEANS, LA

BEN, AGE 31

WEB DESIGNER

NEW YORK, NY

KAREN, AGE 52

RETIRED

MULLICA HILL, NJ

ERIK, AGE 46

DESIGNER

BOULDER, CO

NATASHA, AGE 32

SUSTAINABILITY CONSULTANT

BERKELEY, CA

How do you prefer to shop online?

Do you prefer shopping with

dedicated apps or in the broswer?

Do you ever shop online with your

phone? Why or why not?

Why?

I use my phone for price comparisons

when I’m in a brick and mortar store.

I’ll go to a lot of places knowing that it

will be cheaper online, but I just want

to see what it’s like in person.

Apps work better because the login

process on a mobile device is the

most frustrating part of the experi-

ence. If I can fire up the app, make

a quick purchase, without having to

login or input payment info I’ll do it.

I prefer to use my desktop computer

because of the big screen. If I am

buying something I bought before I

will use my tablet or phone because

I don’t need to see as much.

I usually don’t purchase from my

phone. For me it feels trivial and it

feels like I’m not being responsible

with my spending. Too spontaneous.

I’ve bought mainly clothing items on

my phone. Usually it’s something

I looked at on my laptop and was

trying to decide on, and then when

I’ve committed, purchased it.

Lack of familiarity with user inter-

face/company (I like to check out

reviews about the seller regarding

delivery, product returns, etc), and

I find it way easier to navigate that

information on my PC rather than

my phone.

However, my tablet is my at home

web browser and I do most of my

on-line shopping there. I’ve

purchased more things from my

tablet than I can remember.

And then there’s inputting personal

data into the system. I don’t want to

pull out my credit card on the train.

Once I’ve already purchased from

them [on a PC], it’s way easier to

purchase from them again.

I don’t think I’ve ever used my phone

to buy from a company I have never

purchased from before.

WORD ON THE STREET

What are shoppers saying about mobile commerce?

T H I N GS F R O M M Y TA B L E T R E M E M B E R.

M O R EI ’ V E P U R C H A S E D

T H A N I C A N

K

K

B N

N

E

6CUSTORA

GALAXY

NO

TE 2

iPhone and iPad dominate e-commerce. For now.

Apple’s mobile supremacy remains but continues to be challenged, most notably by Samsung and more recently, Amazon.

APPLE V. ALL

Over the last two years, Apple’s share of e-commerce

orders went down from 75.1% in January 2012 to 53.6% as of

March 2014. Samsung devices have more than quadrupled

their share of orders over the same time period — growing

from 6.9% in 2012 to 30.5% in 2014.

iPad still accounts for the biggest share of tablet

e-commerce orders, though share of orders made from

Samsung tablets increased substantially in the past year and

a half: from 1.9% in January 2012 to 12.4% as of March 2014.

Amazon has also quickly become a player, as purchases made

on Kindle Fire tablets account for 4.1% of all tablet orders.

SHARE (%) OF E-COMMERCE ORDERS BY BRAND, 2012-2014

PHONE

PHONE TABLET

TABLET

CUSTORA E-COMMERCE PULSE _ MOBILE REPORT

100%

100%

50%

50%

0%

0%2012

2012

SAMSUNG

SAMSUNG

APPLE

APPLE

OTHER

AMAZON GOOGLE OTHER

IPAD

MIN

I

IPAD

AIR

PRODUCT RELEASES

NEXU

S 7

KIND

LE

FIRE H

D

KIND

LE

FIRE H

DX

SURFACE 2

FIRE P

HO

NE

GALAXY S

4

NEXU

S 5

NEXU

S 4

GALAXY S

3

MO

TO X

IPH

ON

E 5

IPH

ON

E

5S,5C

SURFACE

30.5%

4.1%1.1%12.4%

15.9%

79.9%

2.5%

53.6%

WIN

DO

WS

PHO

NE 8

6.9%

1.9%

4.6%

93.6%

75.1%

18%

DOWNLOAD THIS DATA AT CUSTORA.COM/MOBILEDATA

2013 2014

2013 2014 Q1

Q1

7CUSTORA

Email marketing and direct traffic drive mobile purchases

Customers responding to email marketing and shoppers navigating directly to online stores (including app traffic) accounted for the highest share of purchases on phones.

MARKETING CHANNELS

When comparing the online marketing channels driving

purchases on mobile devices to those driving purchases on

desktop computers, the most notable differences are with

direct traffic, email marketing, and online search (both free/

organic and paid).

On mobile phones, email marketing generated 26.7% of

sales, compared to only 20.9% on desktop, and 23.1% on

tablet. This is a surprising data point considering the chal-

lenges of displaying email correctly on mobile devices, and

deep-linking into mobile apps.

Direct traffic also drove a larger share of purchases on mobile

phones, with a third (32.9%) of sales coming from shoppers

going straight to the source and bypassing search - organic

search drove 16% of phone sales compared to 23.5% of desktop

sales, and paid search (Search Engine Marketing / SEM) drove

13.35% of sales on phones, compared to 18% on desktop.

On tablets, however, paid search was the leading marketing

channel, driving 24.8% of sales. The difference between

SEM’s share of orders on different devices might stem from

many retailers not spending as much on mobile phone ads

and the phone’s small screen that displays a smaller number

of ads per search.

CATEGORY

AFFILIATE

PAID SEARCH (SEM)

DIRECT

DISPLAY

ORGANIC SEARCH

REFERRAL

SOCIAL

TOTAL

PHONE

0.6

13.35

32.9

0.35

26.7

16.0

9.5

0.6

100%

SHARE (%) OF CATEGORY

DESKTOP

1.15

18

21.3

1.15

20.9

23.5

13.7

0.3

100%

TABLET

1.3

24.8

22.5

0.4

23.1

15.4

12.3

0.2

100%

E-COMMERCE 2013

SHARE OF REVENUE BY CHANNEL AND PLATFORM

VISHAL

How does email marketing factor

into your mobile strategy?

We see a lot of the mobile clicks

coming from our daily emails – that

has driven traffic to the mobile web.

It’s been a very big contributor to our

mobile growth and success.

100% 100% 100%

CUSTORA E-COMMERCE PULSE _ MOBILE REPORT

I T ’ S M O R E I M PU L S I V E —W I T H M O B I L E

Y O U ’ R E O N T H E G O Y O U G E T A N E M A I L

A N D Y O U C L I C K A N D Y O U B U Y O R D O N ’ T B U Y.- V I S H A L

8CUSTORA

Cross-device shopping is coming

Only 12% of shoppers make purchases on more than one device type - but this segment is growing quickly

DESKTOP V. MOBILE

Despite the buzz around cross-device shopping and the idea that differ-

ent commerce experiences are converging, shoppers remain committed

to purchasing on just one particular device. As of Q1 2014, just 12% of

customers make purchases on more than one device type, and 76% of

customers make purchases using only their desktop.

However, these figures represent significant growth — at the

beginning of 2012, only 4% of shoppers had made purchases on more

than one device type.

FENG

What’s your current take on

cross-device shopping?

Everyone talks about it but the

data’s not there right now. There

needs to be more backend data

integration on the customer level.

We’re still looking to marry data

across mobile, desktop, and app.

There aren’t many companies that

can connect all the dots.

If we had clear data, we’d want to

know “Netta likes to be on her phone

in the evening, but checks the web

mid-day at work.” Then target her

based on her device and personalize.

For example, we’d send a push

notification in the evening, when

they’re on their phone, and then with

dynamic retargeting, retarget them

on the tablet at night.

A customer will shop on multiple

channels if they’re comfortable on

the site — the chances of someone

coming in from mobile and immedi-

ately purchasing is pretty small.

But first we’ll have to know they are

indeed that person and it’s really

hard to follow a particular customer

across platforms.

T H E DATA’ S N OT T H E R E R I G H T N OW.

E V E R Y O N E T A L K S A B O U T I T B U T

Another take on cross-device shopping

Many of the shoppers we interviewed feel more

comfortable making the first purchase with a

retailer on a desktop computer. Once trust has been

established after the first successful transaction,

they are more willing to make repeat purchases on

a mobile device. Maybe this is an early indicator of

more distributed purchasing across devices.

VISHAL

If someone has bought on desktop

they’re much more likely to convert

from mobile in the future. After a

desktop purchase, when you receive

an email on tablet or mobile you’re

much more likely to click and buy.

9CUSTORA

Mobile picks up on the weekend Desktop still leads for time on siteTIME OF WEEK HOW ABOUT TIME ON SITE?

2:13

3:39AVG. WEEKDAY

3:16AVG. WEEKEND DAY

00% 2:0050% 4:00100%

Untethered from the workweek and the presumed easy

access to a desktop computer, shoppers buy more on tablets

and phones once the weekend hits.

Another interesting usage snapshot is just looking at how

much time people spend on site with different platforms.

Desktop remains on top, with tablets close behind.

E-COMMERCE Q1 2014

SHARE OF MOBILE ORDERS COMPARISON

E-COMMERCE Q1 2014

AVERAGE CUSTOMER LIFETIME VALUE (CLV) COMPARISON

E-COMMERCE JAN 2013 - MAR 2014

AVERAGE TIME ON SITE (MINUTES) COMPARISON

22%

27%

DESKTOPPHONE/TABLET

Mobile shoppers are less valuable. At least for now.MOBILE CLV (CUSTOMER LIFETIME VALUE)

Shoppers who buy exclusively on desktop computers still

have the highest average CLV (Customer Lifetime Value).

The CLV of shoppers who buy exclusively on mobile phones

is 22% lower (mostly because their average order value is

lower) and the CLV of tablet shoppers is 5% lower (mostly

because they buy less frequently).

It’s also worth noting that the average CLV of cross-device

shoppers (defined as customers who have made at least one

purchase with a retailer on a desktop, phone and tablet) is

19% higher than average.

* Note: Correlation does not equal causation — the fact that

cross-device shoppers are more valuable does not necessarily

imply they are more valuable because they buy on multiple

devices. In fact, the most valuable shoppers (= those who

spend the most) make more purchases, thus increasing the

likelihood of them buying on more than one device. In other

words, shoppers who make more purchases and spend more

are more likely to be cross-device shoppers.

+30%

Avg CLV.

-30%

DESKTOP- ONLY

TABLET- ONLY

PHONE- ONLY

CROSS- DEVICE*

-5%

+19%

-2%

-22%

10CUSTORA

Advice for e-commerce retailers LOOKING AHEAD

Custora interviewed

marketers from

Nomorerack, Karmaloop,

and thredUp to collect

additional insights and

guiding principles geared

towards retailers looking to

get started with, expand,

or optimize mobile

e-commerce.

ANTHONY

ANTHONY

ANTHONY

VISHAL

FENG

VISHAL

FENG

FENG

What advice would you share with

marketers just getting started with

mobile commerce?

What’s your take: App? Mobile-only

site? Responsive design?

How do you measure success?

You just have to start. You have to

build your first product, get it into the

market, observe your users, look at

the data and then make fast changes.

Get to the core of what you want your

user to do, and then build to that. If it

doesn’t work, then rebuild. We just want to be where our users

are, which is on a range of platforms

for a range of user contexts. We add

thousands of new items every minute

to thredUP, and there are powerful

ways to showcase that unique part of

our offering on mobile.

We definitely measure Custora

metrics like CLV (customer lifetime

value), along with visits, average

order sizes (AOV), app downloads,

engagement metrics and how

those metrics change over time.

I wish I had known how important

the mobile site is. We did the

fancy route first with an iPhone

app. But for that, you have to drive

to installs. We found the day we

launched the mobile site our traffic

numbers jumped and you don’t

have to make any extra effort to

drive that traffic.

You need foresight into the under-

standing of “why we need to be here.”

For us, our core demographic is very

active on mobile and the market is

abundant with shopping apps. We

want our customer experience to be

seamless across platforms, whether

that’s mobile web, responsive, or

native apps.

Still, you need to really think to

yourself “What’s the value of a

mobile app? Why do we need an

app?” Then you need to give users

a reason to go to the app beyond

just shopping. It’s a very competitive

landscape.

Conversion is all that we judge —

we just look at dollars we spend

on a channel (in this case, mobile)

versus dollars customers spend on

that channel.

We primarily track sales and ROI in

the mobile channel.

Many people talk about “mobile

web,” “tablet app,” and others, but for

us the primary one is the mobile app.

CO N V E R S I O N I S A L LT H A T W E J U D G E

ANTHONY MARINO

CMO, THRED UP

FENG CHANG

DIRECTOR BUSINESS STRATEGY

& ANALYTICS, KARMALOOP

VISHAL AGARWAL

EVP & CMO, NOMORERACK

ILLUSTRATIONS BY SHYAMA GOLDEN

11CUSTORA

FENG

VISHAL

ANTHONY

FENG

ANTHONY

What has driven mobile wins? What’s next?

We have created mobile exclusive

sales events and products. We

incentivize shoppers to go to the

app because we looked at the data

and realized these shoppers and

sales are more valuable for us: both

for profitability and customer loyalty.

It’s common sense and the data

confirmed it.

It’s possible the sheer volume of

mobile traffic may overtake desktop

traffic so significantly that it could

negate the fact that conversions

are lower. This would make us

reevaluate our strategy and maybe

change our mobile offering.

We also constantly test and

optimize our mobile offerings and

have made big improvements on

conversion and engagement.

We are also looking into dynamic

retargeting, just like desktop –

desktop retention strategies are a

growing part of the mobile

marketing mix.

VISHAL

As of now we have mostly ridden

a wave. We haven’t tried to divert

customers to mobile; the strategy

has been to provide them a place to

interact organically.

Conversion has been so low we’d

rather focus our energy on desktop.

Advice for e-commerce retailers cont’d

We use it as a testing ground for

new features because it’s a smaller,

more engaged population.

Our goal is to continue optimizing

the mobile channel through

improving retention. We’ve also

started segmenting our push

notifications.

We want to understand channel

attribution across platform — track

at a user level what are they doing to

understand how they are interacting

across platforms.

W E US E I T A S A T EST I N G G R O U N D

F O R N E W F E A T U R E S

LOOKING AHEAD

12CUSTORA

The report’s findings are derived from data spanning over 70 million

anonymized shoppers, $10B in e-commerce revenue, and over 100

online retailers.

Mobile device, brand, and platform were obtained via the

deviceCategory, mobileDeviceBranding, and operatingSystem tags

in Google Analytics, respectively.

Desktop, mobile, and tablet users were defined as users who made

at least two orders and all of those orders were done with that

device. Cross-device users were defined as non-desktop, non-

mobile, and non-tablet users who made at least two orders. Conver-

sion rate is defined as number of orders divided by number of visits.

Customer Lifetime Value refers to the amount customers spent in

the two years after their initial purchase (initial purchase inclusive).

When customers made their first purchase less than two years prior

to data collection, their expected purchases for the remaining time

were projected using Custora’s statistical models and used in the

overall calculation. For marketing channel analysis, channel attri-

bution was set by each retailer; all retailers included in this report

used “last click” attribution.

Download the

complete data sets

for the findings

within this report at

custora.com/mobiledata

M E T H O D - O L O G Y

The Custora E-Commerce Pulse tracks key US e-commerce sta-

tistics and allows any retailer to benchmark their data in real time.

The Pulse is based on Custora’s analysis of over 70 million online

shoppers and over $10 billion in e-commerce revenue across over

100 US-based online retailers. The Pulse also leverages external

data points, such as the US Department of Commerce e-commerce

growth figures, to extrapolate growth trends within the Custora

data universe to arrive at predictions for the US industry at large.

Pulse research has been featured in The Wall Street Journal, USA

Today, Inc., Los Angeles Times, Bloomberg TV, McKinsey Insights,

AdAge, eMarketer, San Francisco Chronicle, and many other publica-

tions. Pulse data is part of the Bloomberg Professional® Platform.

A B O U T T H E P U L S E

Custora is a customer-centric marketing platform that helps

e-commerce teams acquire, retain, and segment their customers.

Custora uses best-in-class predictive analytics models to help

retailers answer questions like: What are our best performing

customer acquisition channels? How do we convert more members

to active customers? How do we increase repeat purchase rates?

How do we re-activate lost customers? What makes our most

valuable customers different? Where did I park the car?

We work with several leading e-commerce retailers, including Ann

Taylor LOFT, Bonobos, Crocs, Etsy, GUESS, Wine.com and many

more throughout Earth. To learn more about e-commerce marketing

analytics, check out Custora U for courses about segmentation,

lifecycle marketing, cohort analysis and more. Please direct inquires

A B O U T C U S T O R A

.XLS

R E Q U E S T A D E M O O F C U S T O R A

S I G N U P F O R P U L S E U P D AT E S