Mind Map: Power-Gen Africa #PGAfrica 2015 Conference David Lipschitz 15th July 2015 Day 1

1

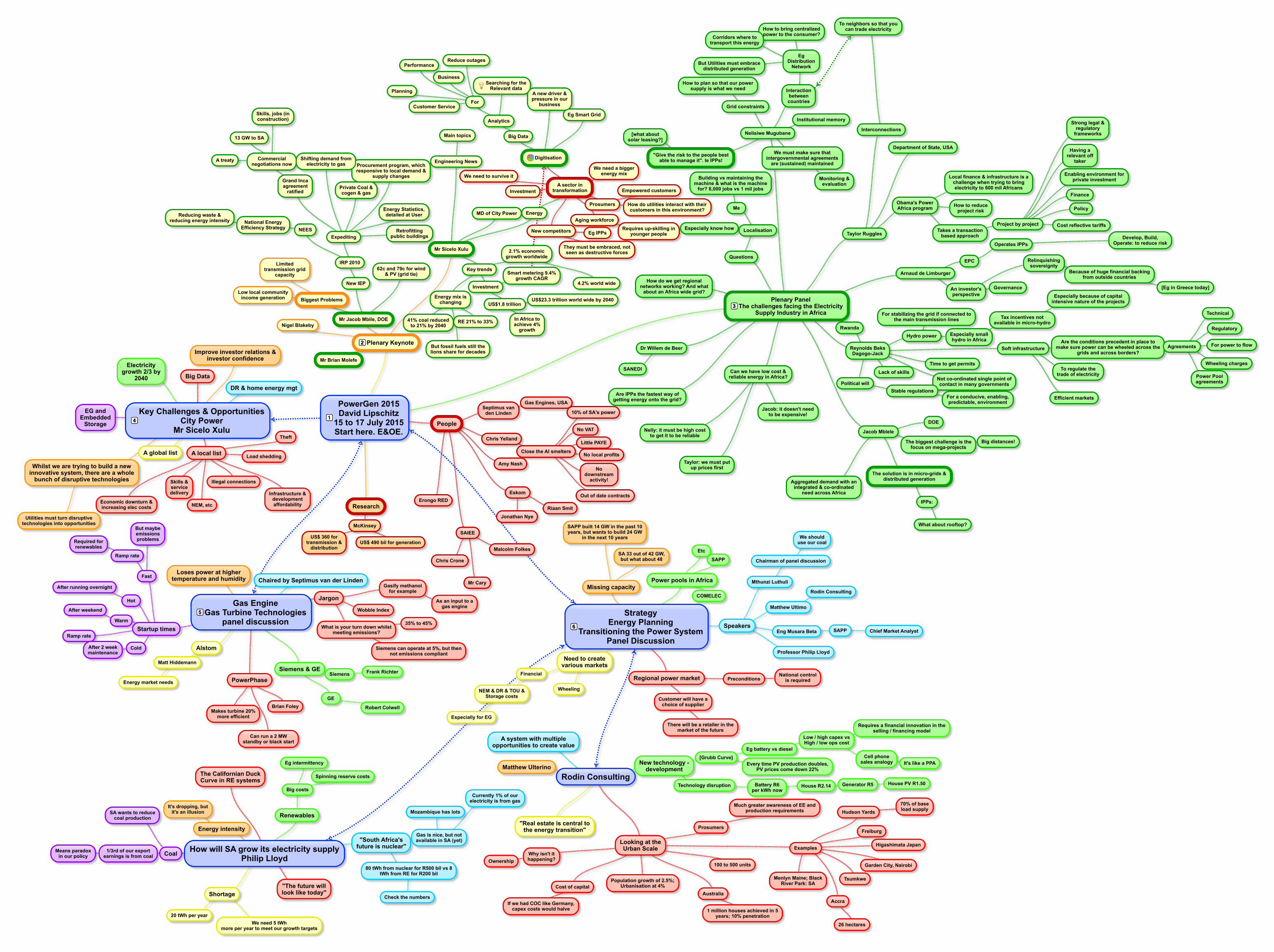

PowerGen 2015 David Lipschitz 15 to 17 July 2015 Start here. E&OE. People Septimus van den Linden Gas Engines, USA Chris Yelland Close the Al smelters No VAT Little PAYE No local profits No downstream activity! 10% of SA's power Out of date contracts SAIEE Chris Crone Malcolm Folkes Mr Cary Eskom Riaan Smit Jonathan Nye Erongo RED Amy Nash Research McKinsey US$ 490 bil for generation US$ 360 for transmission & distribution Plenary Keynote Mr Jacob Mbile, DOE New IEP IRP 2010 Expediting Private Coal & cogen & gas Procurement program, which responsive to local demand & supply changes Grand Inca agreement ratified Commercial negotiations now 13 GW to SA A treaty Skills, jobs (in construction) Energy Statistics, detailed at User Retrofitting public buildings Shifting demand from electricity to gas NEES National Energy Efficiency Strategy Reducing waste & reducing energy intensity 62c and 79c for wind & PV (grid tie) Biggest Problems Limited transmission grid capacity Low local community income generation Nigel Blakeby Mr Brian Molefe Mr Sicelo Xulu MD of City Power Energy A sector in transformation We need to survive it Investment We need a bigger energy mix Prosumers Empowered customers How do utilities interact with their customers in this environment? Digitisation Eg Smart Grid Big Data Analytics For Business Customer Service Reduce outages Performance Planning Searching for the Relevant data A new driver & pressure in our business New competitors Eg IPPs They must be embraced, not seen as destructive forces Aging workforce Requires up-skilling in younger people Key trends 2.1% economic growth worldwide 4.2% world wide Investment US$1.8 trillion In Africa to achieve 4% growth US$23.3 trillion world wide by 2040 Smart metering 9.4% growth CAGR Energy mix is changing 41% coal reduced to 21% by 2040 RE 21% to 33% But fossil fuels still the lions share for decades Engineering News Main topics Plenary Panel The challenges facing the Electricity Supply Industry in Africa Nelisiwe Mugubane Institutional memory Grid constraints How to plan so that our power supply is what we need Interaction between countries Eg Distribution Network How to bring centralized power to the consumer? But Utilities must embrace distributed generation Corridors where to transport this energy "Give the risk to the people best able to manage it". Ie IPPs! [what about solar leasing?] We must make sure that intergovernmental agreements are (sustained) maintained Monitoring & evaluation Dr Willem de Beer SANEDI Taylor Ruggles Department of State, USA Obama's Power Africa program Local finance & infrastructure is a challenge when trying to bring electricity to 600 mil Africans How to reduce project risk Takes a transaction based approach Project by project Finance Policy Enabling environment for private investment Cost reflective tariffs Having a relevant off taker Strong legal & regulatory frameworks Interconnections To neighbors so that you can trade electricity Arnaud de Limburger EPC Operates IPPs Develop, Build, Operate: to reduce risk An investor's perspective Governance Relinquishing sovereignty Because of huge financial backing from outside countries [Eg in Greece today] Reynolds Beks Dagogo-Jack Hydro power Especially small hydro in Africa Tax incentives not available in micro-hydro Especially because of capital intensive nature of the projects For stabilizing the grid if connected to the main transmission lines Time to get permits Not co-ordinated single point of contact in many governments Lack of skills Political will Stable regulations For a conducive, enabling, predictable, environment Soft infrastructure Are the conditions precedent in place to make sure power can be wheeled across the grids and across borders? Agreements Technical Regulatory For power to flow Wheeling charges Power Pool agreements To regulate the trade of electricity Efficient markets Rwanda Jacob Mblele The biggest challenge is the focus on mega-projects Big distances! DOE The solution is in micro-grids & distributed generation IPPs: What about rooftop? Aggregated demand with an integrated & co-ordinated need across Africa Are IPPs the fastest way of getting energy onto the grid? Can we have low cost & reliable energy in Africa? Nelly: it must be high cost to get it to be reliable Taylor: we must put up prices first Jacob: it doesn't need to be expensive! How do we get regional networks working? And what about an Africa wide grid? Questions Localisation Especially know how Me Building vs maintaining the machine & what is the machine for? 8,000 jobs vs 1 mil jobs Key Challenges & Opportunities City Power Mr Sicelo Xulu A local list Theft Load shedding Economic downturn & increasing elec costs Skills & service delivery Illegal connections Infrastructure & development affordability NEM, etc Whilst we are trying to build a new innovative system, there are a whole bunch of disruptive technologies Utilities must turn disruptive technologies into opportunities A global list Electricity growth 2/3 by 2040 DR & home energy mgt EG and Embedded Storage Big Data Improve investor relations & investor confidence Gas Engine Gas Turbine Technologies panel discussion PowerPhase Makes turbine 20% more efficient Brian Foley Can run a 2 MW standby or black start Loses power at higher temperature and humidity Alstom Matt Hiddemann Energy market needs Siemens & GE Siemens Frank Richter GE Robert Colwell Chaired by Septimus van der Linden Startup times Hot After running overnight Warm After weekend Cold After 2 week maintenance Fast Ramp rate Required for renewables But maybe emissions problems Ramp rate Jargon Wobble Index What is your turn down whilst meeting emissions? 35% to 45% Siemens can operate at 5%, but then not emissions compliant Gasify methanol for example As an input to a gas engine Strategy Energy Planning Transitioning the Power System Panel Discussion Regional power market Preconditions National control is required Customer will have a choice of supplier There will be a retailer in the market of the future Missing capacity SA 33 out of 42 GW, but what about 48 SAPP built 14 GW in the past 10 years, but wants to build 24 GW in the next 10 years Need to create various markets Financial NEM & DR & TOU & Storage costs Especially for EG Wheeling Power pools in Africa SAPP COMELEC Etc Speakers Eng Musara Beta SAPP Chief Market Analyst Matthew Ultimo Rodin Consulting Mthunzi Luthuli Chairman of panel discussion We should use our coal Professor Philip Lloyd Rodin Consulting Looking at the Urban Scale 100 to 500 units Prosumers Much greater awareness of EE and production requirements Population growth of 2.5%; Urbanisation at 4% Australia 1 million houses achieved in 5 years; 10% penetration Cost of capital If we had COC like Germany, capex costs would halve Examples Hudson Yards 70% of base load supply Freiburg Higashimata Japan Garden City, Nairobi Tsumkwe Menlyn Maine; Black River Park: SA Accra 26 hectares Why isn't it happening? Ownership Matthew Ulterino "Real estate is central to the energy transition" New technology - development [Grubb Curve] Eg battery vs diesel Low / high capex vs High / low ops cost Requires a financial innovation in the selling / financing model Cell phone sales analogy It's like a PPA Every time PV production doubles, PV prices come down 22% Technology disruption Battery R6 per kWh now House R2.14 Generator R5 House PV R1.50 A system with multiple opportunities to create value How will SA grow its electricity supply Philip Lloyd "The future will look like today" Energy intensity It's dropping, but it's an illusion Shortage 20 tWh per year We need 5 tWh more per year to meet our growth targets Renewables Big costs Eg intermittency Spinning reserve costs "South Africa's future is nuclear" Gas is nice, but not available in SA (yet) Mozambique has lots Currently 1% of our electricity is from gas 80 tWh from nuclear for R500 bil vs 8 tWh from RE for R200 bil Check the numbers Coal 1/3rd of our export earnings is from coal Means paradox in our policy SA wants to reduce coal production The Californian Duck Curve in RE systems

-

Upload

david-lipschitz -

Category

Technology

-

view

203 -

download

0

Transcript of Mind Map: Power-Gen Africa #PGAfrica 2015 Conference David Lipschitz 15th July 2015 Day 1

PowerGen 2015David Lipschitz

15 to 17 July 2015Start here. E&OE.

People

Septimus vanden Linden

Gas Engines, USA

Chris Yelland

Close the Al smelters

No VAT

Little PAYE

No local profits

Nodownstream

activity!

10% of SA's power

Out of date contracts

SAIEE

Chris Crone

Malcolm Folkes

Mr Cary

Eskom

Riaan SmitJonathan Nye

Erongo RED

Amy Nash

Research

McKinsey

US$ 490 bil for generationUS$ 360 for

transmission &distribution

Plenary Keynote

Mr Jacob Mbile, DOE

New IEP

IRP 2010

Expediting

Private Coal &cogen & gas

Procurement program, whichresponsive to local demand &

supply changesGrand Incaagreement

ratified

Commercialnegotiations now

13 GW to SA

A treaty

Skills, jobs (inconstruction)

Energy Statistics,detailed at User

Retrofittingpublic buildings

Shifting demand fromelectricity to gas

NEESNational Energy

Efficiency Strategy

Reducing waste &reducing energy intensity

62c and 79c for wind& PV (grid tie)

Biggest Problems

Limitedtransmission grid

capacity

Low local communityincome generation

Nigel Blakeby

Mr Brian Molefe

Mr Sicelo Xulu

MD of City Power Energy

A sector intransformation

We need to survive it

Investment

We need a biggerenergy mix

Prosumers

Empowered customers

How do utilities interact with theircustomers in this environment?

Digitisation

Eg Smart Grid

Big Data

Analytics

For

Business

Customer Service

Reduce outagesPerformance

PlanningSearching for the

Relevant dataA new driver &pressure in our

business

New competitors Eg IPPs

They must be embraced, notseen as destructive forces

Aging workforceRequires up-skilling in

younger people

Key trends

2.1% economicgrowth worldwide

4.2% world wideInvestment

US$1.8 trillion

In Africa toachieve 4%

growth

US$23.3 trillion world wide by 2040

Smart metering 9.4%growth CAGR

Energy mix ischanging

41% coal reducedto 21% by 2040

RE 21% to 33%

But fossil fuels still thelions share for decades

Engineering News

Main topics

Plenary PanelThe challenges facing the Electricity

Supply Industry in Africa

Nelisiwe Mugubane

Institutional memory

Grid constraints

How to plan so that our powersupply is what we need Interaction

betweencountries

EgDistribution

Network

How to bring centralizedpower to the consumer?

But Utilities must embracedistributed generation

Corridors where totransport this energy

"Give the risk to the people bestable to manage it". Ie IPPs!

[what aboutsolar leasing?]

We must make sure thatintergovernmental agreements

are (sustained) maintained

Monitoring &evaluation

Dr Willem de Beer

SANEDI

Taylor Ruggles

Department of State, USA

Obama's PowerAfrica program

Local finance & infrastructure is achallenge when trying to bringelectricity to 600 mil Africans

How to reduceproject risk

Takes a transactionbased approach

Project by project

Finance

Policy

Enabling environment forprivate investment

Cost reflective tariffs

Having arelevant off

taker

Strong legal ®ulatory

frameworksInterconnections

To neighbors so that youcan trade electricity

Arnaud de Limburger

EPC

Operates IPPsDevelop, Build,

Operate: to reduce risk

An investor'sperspective

Governance

Relinquishingsovereignty

Because of huge financial backingfrom outside countries

[Eg in Greece today]

Reynolds BeksDagogo-Jack

Hydro power Especially smallhydro in Africa

Tax incentives notavailable in micro-hydro

Especially because of capitalintensive nature of the projects

For stabilizing the grid if connected tothe main transmission lines

Time to get permits

Not co-ordinated single point ofcontact in many governments

Lack of skills

Political willStable regulations

For a conducive, enabling,predictable, environment

Soft infrastructureAre the conditions precedent in place to

make sure power can be wheeled across thegrids and across borders?

Agreements

Technical

Regulatory

For power to flow

Wheeling charges

Power Poolagreements

To regulate thetrade of electricity

Efficient markets

Rwanda

Jacob Mblele

The biggest challenge is thefocus on mega-projects

Big distances!

DOE

The solution is in micro-grids &distributed generation

IPPs:

What about rooftop?

Aggregated demand with anintegrated & co-ordinated

need across Africa

Are IPPs the fastest way ofgetting energy onto the grid?

Can we have low cost &reliable energy in Africa?

Nelly: it must be high costto get it to be reliable

Taylor: we must putup prices first

Jacob: it doesn't needto be expensive!

How do we get regionalnetworks working? And what

about an Africa wide grid?

Questions

LocalisationEspecially know how

Me

Building vs maintaining themachine & what is the machine

for? 8,000 jobs vs 1 mil jobs

Key Challenges & OpportunitiesCity Power

Mr Sicelo Xulu

A local list

Theft

Load shedding

Economic downturn &increasing elec costs

Skills &servicedelivery

Illegal connections

Infrastructure &developmentaffordabilityNEM, etc

Whilst we are trying to build a newinnovative system, there are a whole

bunch of disruptive technologies

Utilities must turn disruptivetechnologies into opportunities

A global list

Electricitygrowth 2/3 by

2040DR & home energy mgt

EG andEmbedded

Storage

Big Data

Improve investor relations &investor confidence

Gas EngineGas Turbine Technologies

panel discussion

PowerPhase

Makes turbine 20%more efficient

Brian Foley

Can run a 2 MWstandby or black start

Loses power at highertemperature and humidity

Alstom

Matt Hiddemann

Energy market needs

Siemens & GESiemens Frank Richter

GE

Robert Colwell

Chaired by Septimus van der Linden

Startup times

Hot

After running overnight

Warm

After weekend

ColdAfter 2 weekmaintenance

Fast

Ramp rate

Required forrenewables

But maybeemissionsproblems

Ramp rate

Jargon

Wobble Index

What is your turn down whilstmeeting emissions?

35% to 45%

Siemens can operate at 5%, but thennot emissions compliant

Gasify methanolfor example

As an input to agas engine

StrategyEnergy Planning

Transitioning the Power SystemPanel Discussion

Regional power market PreconditionsNational control

is required

Customer will have achoice of supplier

There will be a retailer in themarket of the future

Missing capacity

SA 33 out of 42 GW,but what about 48

SAPP built 14 GW in the past 10years, but wants to build 24 GW

in the next 10 years

Need to createvarious markets

Financial

NEM & DR & TOU &Storage costs

Especially for EG

Wheeling

Power pools in Africa

SAPP

COMELEC

Etc

SpeakersEng Musara Beta SAPP Chief Market Analyst

Matthew Ultimo

Rodin Consulting

Mthunzi Luthuli

Chairman of panel discussion

We shoulduse our coal

Professor Philip Lloyd

Rodin Consulting

Looking at theUrban Scale

100 to 500 units

Prosumers

Much greater awareness of EE andproduction requirements

Population growth of 2.5%;Urbanisation at 4%

Australia

1 million houses achieved in 5years; 10% penetration

Cost of capital

If we had COC like Germany,capex costs would halve

Examples

Hudson Yards70% of baseload supply

Freiburg

Higashimata Japan

Garden City, Nairobi

TsumkweMenlyn Maine; BlackRiver Park: SA

Accra

26 hectares

Why isn't ithappening?Ownership

Matthew Ulterino

"Real estate is central tothe energy transition"

New technology -development

[Grubb Curve]Eg battery vs diesel

Low / high capex vsHigh / low ops cost

Requires a financial innovation in theselling / financing model

Cell phonesales analogy It's like a PPAEvery time PV production doubles,

PV prices come down 22%

Technology disruption Battery R6per kWh now

House R2.14 Generator R5 House PV R1.50

A system with multipleopportunities to create value

How will SA grow its electricity supplyPhilip Lloyd

"The future willlook like today"

Energy intensity

It's dropping, butit's an illusion

Shortage

20 tWh per yearWe need 5 tWh

more per year to meet our growth targets

Renewables

Big costs

Eg intermittency

Spinning reserve costs

"South Africa'sfuture is nuclear"

Gas is nice, but notavailable in SA (yet)

Mozambique has lots

Currently 1% of ourelectricity is from gas

80 tWh from nuclear for R500 bil vs 8tWh from RE for R200 bil

Check the numbers

Coal1/3rd of our exportearnings is from coal

Means paradoxin our policy

SA wants to reducecoal production

The Californian DuckCurve in RE systems