Michael A. Hitt, Laszlo Tihanyi, Toyah Miller and - Sage Publications

38

http://jom.sagepub.com/ Journal of Management http://jom.sagepub.com/content/32/6/831 The online version of this article can be found at: DOI: 10.1177/0149206306293575 2006 32: 831 Journal of Management Michael A. Hitt, Laszlo Tihanyi, Toyah Miller and Brian Connelly International Diversification: Antecedents, Outcomes, and Moderators Published by: http://www.sagepublications.com On behalf of: Southern Management Association can be found at: Journal of Management Additional services and information for http://jom.sagepub.com/cgi/alerts Email Alerts: http://jom.sagepub.com/subscriptions Subscriptions: http://www.sagepub.com/journalsReprints.nav Reprints: http://www.sagepub.com/journalsPermissions.nav Permissions: http://jom.sagepub.com/content/32/6/831.refs.html Citations: at SAGE Publications on January 5, 2011 jom.sagepub.com Downloaded from

Transcript of Michael A. Hitt, Laszlo Tihanyi, Toyah Miller and - Sage Publications

http://jom.sagepub.com/Journal of Management

http://jom.sagepub.com/content/32/6/831The online version of this article can be found at:

DOI: 10.1177/0149206306293575

2006 32: 831Journal of ManagementMichael A. Hitt, Laszlo Tihanyi, Toyah Miller and Brian Connelly

International Diversification: Antecedents, Outcomes, and Moderators

Published by:

http://www.sagepublications.com

On behalf of:

Southern Management Association

can be found at:Journal of ManagementAdditional services and information for

http://jom.sagepub.com/cgi/alertsEmail Alerts:

http://jom.sagepub.com/subscriptionsSubscriptions:

http://www.sagepub.com/journalsReprints.navReprints:

http://www.sagepub.com/journalsPermissions.navPermissions:

http://jom.sagepub.com/content/32/6/831.refs.htmlCitations:

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

831

*Corresponding author. Tel.: 979-458-3393; fax: 979-845-9641.

E-mail address: [email protected]

Journal of Management, Vol. 32 No. 6, December 2006 831-867DOI: 10.1177/0149206306293575© 2006 Southern Management Association. All rights reserved.

International Diversification: Antecedents,Outcomes, and Moderators

Michael A. Hitt*Laszlo TihanyiToyah Miller

Brian ConnellyMays Business School, Texas A&M University, College Station, TX 77843

Pursuit of international markets and resources from foreign sources has increased dramaticallyduring the past two decades, and the academic study of international diversification has increasedconcurrently. Reviewing the literature in management and related disciplines, the authors discussrecent findings of research on international diversification. A conceptual model groups key rela-tionships, including antecedents, environmental factors, performance and process outcomes,moderators, and the characteristics of international diversification. The authors synthesize intel-lectual contributions, highlight unresolved issues, and provide recommendations for futureresearch.

Keywords: international diversification; internationalization; globalization; multinational

Developing strategies for the global marketplace and managing operations in diverse countrymarkets have become critical tasks for managers. At the same time, the international diversifi-cation process is accompanied by a great deal of uncertainty, with little agreement about theform it should take. Although several determinants of international diversification have beenexamined in prior research, the effects of firm, industry, and environmental factors have not beenfully specified (Gimeno, Hoskisson, Beal, & Wan, 2005). Similarly, the relationships betweentypes of international strategies and their performance outcomes remain complex (Geringer,

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

Beamish, & daCosta, 1989; Gomes & Ramaswamy, 1999). Not surprisingly, the extent of firms’international involvement—the scale and scope of their international diversification—hasincreasingly become a focus of research in management and its sister disciplines.

Two factors motivated this review and synthesis of the research stream on internationaldiversification. First, as scholars in the management domain continue to add new and diverseinsights to the already significant body of literature (Carpenter & Sanders, 2004; Nachum,2004; Tihanyi, Ellstrand, Daily, & Dalton, 2000; Wan, 2005; Werner, 2002; Zahra, Ireland,& Hitt, 2000), the field would benefit from an overview of the dominant relationships thatexist among important variables and emerging contexts of international diversification. Assuch, there is need for a comprehensive model to integrate the insights from prior researchand provide direction for future research.

Second, notable findings in international diversification research from related disciplines,such as finance (Riahi-Belkaoui & Alnajjar, 2002), accounting (Garrod & Rees, 1998), inter-national business (Ruigrok & Wagner, 2003), and marketing (Kotabe, Srinivasan, & Aulakh,2002), have not been integrated into the management literature. Findings from these alter-native disciplines offer unique perspectives on international diversification. Thus, we exam-ine recent developments and interpret gaps within and across disciplines. The goal of thisreview is to systematically examine the intellectual ground that has been covered during thepast 20 years, to identify diverse findings from multiple disciplines, to uncover discrepan-cies, and to suggest important areas of research that have yet to be explored.

“International diversification is a strategy through which a firm expands the sales of itsgoods or services across the borders of global regions and countries into different geo-graphic locations or markets” (Hitt, Ireland, & Hoskisson, 2007: 251). Studies using suchlabels as internationalization, geographic diversification, international expansion, global-ization, and multinationality tend to refer to the same strategic management construct andare included in our analysis. Although early international diversification research origi-nated from studies of capital flows (Caves, 1971), research on international diversificationin strategic management has focused on the portfolio of foreign direct investments involv-ing equity and control. Furthermore, strategic management researchers view internationaldiversification as more than a simple means of risk reduction (Geringer et al., 1989; Hitt,Hoskisson, & Ireland, 1994; ) embracing it, rather, as a strategy for gaining competitiveadvantage. Thus, the management literature provides significant attention to the relation-ship between international diversification and firm performance (Errunza & Senbet, 1984;Grant, 1987). Studies have also proposed a variety of antecedents (Sambharya, 1996;Tihanyi et al., 2000), and recent research on international diversification has increasinglyemphasized complex relationships and potential moderating effects (Thomas, 2005),process outcomes (Zahra et al., 2000), and the effects of the institutional environment(Wan, 2005). Herein, we derive a comprehensive model of international diversificationthat follows this general progression by examining research on the antecedents, modera-tors, and outcomes of international diversification research. We build a framework forexamining recent developments and considering gaps within and across disciplines. On thebasis of our review and critique of the literature, we outline a variety of suggestions forcontinuing research on international diversification.

832 Journal of Management / December 2006

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

Twenty Years of International Diversification Research

The international business environment has witnessed unprecedented change during thepast two decades, such that international diversification has become an increasingly impor-tant strategic option available to firms seeking sustained competitive advantage (Nachum &Zaheer, 2005). According to the World Investment Report (2005), leading multinationalenterprises (MNEs) in 2003 on average operated with 49.5% of their employees, 49.8% oftheir assets, and 54.1% of their sales outside their home countries. International diversifica-tion has significantly increased with developing country MNEs as well. For example, firmsbased in emerging market countries accounted for 12% or $849 billion of total foreign directinvestment (FDI) in 2002 (Hoskisson, Kim, White, & Tihanyi, 2004). An example of emerg-ing market firms’ international diversification is shown by Cemex S.A., a construction andmaterials company headquartered in Mexico. This company employs 66% of its workforceand operates 35 of its 48 subsidiaries outside its home country. Primarily since the late1980s, researchers have studied the phenomenon of international diversification by analyz-ing the share of foreign operations—sales, assets, subsidiaries, or profits—within the MNE.This line of research experienced rapid growth throughout the 1990s as scholars consideredhow firms could obtain new resources and transfer core competencies to new markets bydiversifying internationally, leading to higher performance and risk-adjusted returns. Arecent survey of articles published in the 20 top management journals indicates that interna-tional diversification has become one of the most popular research areas in internationalmanagement (Werner, 2002). Growth in international diversification research continues toincrease as research questions become richer, delving further into the complex relationshipwith performance and varied motivations that drive firms to expand internationally.

International Diversification as a Strategy of the Firm

International diversification has been studied from a broad range of theoretical perspectives,resulting in debates regarding its fundamental characteristics and appropriate measurement(Annavarjula & Beldona, 2000; Coviello & McAuley, 1999). Early studies in internationalbusiness list diverse strategic motives and explain several factors that affect the location ofmarkets where firms should compete, whether worldwide, regional, or domestic. Hymer(1976) was among the first to argue that the potential for enhanced returns spurs firms todiversify internationally and that firms experience cost trade-offs in doing business abroad. Inthis early account of FDI, firms retain control and create monopoly power by removing com-petition between subsidiaries, thereby exploiting subsidiary capabilities. Other theories con-centrated on transaction costs to explain why firms compete in foreign markets. Firms areprompted to enter international markets where transactions are not efficiently conducted in themarket (Hennart, 1982). Caves (1996) explained that there are high transaction costs whenoperating with intangible assets in some markets; therefore, transactions are taken inside thefirm to conduct business in those countries. Moving transactions within the firm improvescontrol, facilitates the dissemination of information, and offers means of dispute resolution.

Hitt et al. / International Diversification 833

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

Buckley and Casson (1976) argued that international markets are imperfect and that firmshave an incentive to internalize them.

From a strategic management perspective, “international business activity is a form of diver-sification” (Fouraker & Stopford, 1968: 48). The study of diversification across business unitsis one of the most influential literature streams of strategic management research (Bergh, 2001;Rumelt, Schendel, & Teece, 1994). Product diversification as a corporate strategy has beenconsidered more than a risk-reduction tool—it has been recognized as a means for increasedmarket power (Hitt et al., 1994), capitalizing on economies of scale (Teece, 1982), using excessresources (Penrose, 1959), and reducing transaction costs (Amit & Livnat, 1988).

International diversification, with its multiple objectives, is a complex corporate-levelstrategy that provides an effective alternative to product diversification and other strategies.Similar to firms that diversify their product portfolio, firms that diversify internationally havediverse motives, including economies of scale, access to new resources, cost reduction, exten-sion of innovative capabilities, knowledge acquisition, location advantages, and performanceimprovements (Hitt, Hoskisson, & Kim, 1997). In contrast to product diversification, how-ever, international diversification offers new means for value creation through access to for-eign stakeholders, resources, and institutions. Although doing business abroad increasesuncertainty, international diversification is increasingly preferred by firms because it allowsthem to accentuate their existing core competencies, gain unique knowledge, and access sub-stantial growth opportunities in the product markets of foreign countries. IKEA’s early inter-national entry illustrates the value creation potential from international diversification.Because of the limits to growth in its core furniture store business, IKEA considered differ-ent growth opportunities, including expanding its product lines to serve new customersegments in Sweden (i.e., product diversification) or by identifying and serving their existingcustomer base of young professionals and families in other countries (i.e., international diver-sification). International diversification allowed IKEA to cater to its customer base worldwideand become the international leader in its original market segment (Bartlett & Ghoshal, 1989).

Prior research from the strategic management perspective has focused on several importantcharacteristics of international diversification. The scale and scope of a firm’s internationaldiversification may help to explain the extent of its strategic intentions. A high level of inter-national diversification can indicate market power, access to abundant resources, or increasedpotential to more effectively use its resources. From a resource-based view, Oviatt andMcDougall (1994) emphasized the importance of resource utilization, defined as the numberof primary activities undertaken outside the home country. Beamish suggested that interna-tional diversification is “the process by which firms both increase their awareness of the directand indirect influence of international transactions on their future and establish and conducttransactions with other countries” (1990: 77). In addition to scale and scope characteristics,structural, performance, and attitudinal dimensions have been the subjects of previous studieson international diversification. Some researchers argue that international diversification doesnot always create value for the firm because of firms’ liability of foreignness (e.g., Zaheer,1995). Firms may face higher or lower liability of foreignness depending partly on the struc-tural dimensions of the markets represented by their international diversification, such as oper-ating in markets with different cultural values, levels of development, or institutions, and theirskills in managing entry into and operation in foreign markets. Some researchers suggest that

834 Journal of Management / December 2006

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

firms’ early international experience may be positive, but increases in scope augment the costsof coordination (Hitt et al., 1997). These researchers argue that a more complex relationshipexists between international diversification and firm performance than that suggested by priorwork.

In light of recent debate on, and interest in, the topic of international diversification, wereviewed key studies on the subject published in the past two decades in leading managementjournals, such as the Academy of Management Journal, the Academy of Management Review,Administrative Science Quarterly, the Journal of International Business Studies, the Journalof Management, Organization Science, and the Strategic Management Journal. We incorpo-rated insights from articles published in journals of related fields, including international busi-ness, finance, marketing, accounting, entrepreneurship, and economics. Our review resultedin the development of a framework (see Figure 1) that integrates the antecedents, environ-mental influences, process outcomes, moderators, and performance outcomes of internationaldiversification. Most previous literature focused on the effect of international diversificationrelative to a narrow set of constructs (e.g., firm performance) or debated measurement issues.Despite the important findings, several relevant constructs and their effects have been over-looked. Our framework offers assistance to researchers working in this area by presenting acomprehensive overview of a broad range of relevant constructs and based on prior research,identifying their dominant relationships with international diversification. In addition, wehave provided a short review of selected empirical articles on the relationships among thereviewed constructs in Table 1.

Antecedents: Relationship 1-2

A critical component of international diversification research concerns its antecedents.Early research considered the principal relationship of organizational size and structure withinternationalization (Wolf, 1977), and there has been renewed interest in exploring these firmcharacteristics in more detail. Prior research has shown that such variables as R&D intensity,size, performance, product diversification, and organizational age are positively associatedwith international diversification (Autio, Sapienza, & Almeida, 2000; Delios & Beamish,1999; Fiegenbaum, Shaver, & Yeung, 1997; Martin, Swaminathan, & Mitchell, 1998).Recent research on antecedents examined a number of strategic resources and organizationalprocesses as predictors of international diversification.

Drawing on theoretical rationale from Caves (1996) and Buckley and Casson (1976), onestream of research has sought to establish the relationship between intangible resourcesand international diversification (Delgado-Gomez, Ramirez-Aleson, & Espitia-Escuer, 2004;Nachum & Zaheer, 2005). These studies suggest that intangible resources provide ownershipadvantages that lend themselves to internal control and expansion to new locations. Findingsin this stream indicate that firms with higher endowments of intangible resources are morelikely to expand internationally (Delgado-Gomez et al., 2004). In this tradition, Hitt, Bierman,Uhlenbruck, and Shimizu (in press) found that firms holding stronger human capital and rela-tional capital with large corporate customers and with foreign governments have a higherprobability of entering international markets. Nachum and Zaheer (2005) considered not only

Hitt et al. / International Diversification 835

(text continues on p. 846)

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

2-3

2-3 (5)

4-2

2-4

2-4 (5)

3-4

2-4 (6)

5-2

1-2 (5)1-2

PR

OC

ES

S A

ND

OR

GA

NIZ

AT

ION

AL

OU

TC

OM

ES

(3)

-Inn

ovat

ion

-Lea

rnin

g-O

rgan

izat

iona

l Str

uctu

res

-Ope

ratin

g E

ffici

ency

-Ris

k-D

ebt

CH

AR

AC

TE

RIS

TIC

S O

FIN

TE

RN

AT

ION

AL

DIV

ER

SIF

ICA

TIO

N (

2)

-Sca

le-S

cope

-Dim

ensi

ons

(str

uctu

ral,

perf

orm

ance

,at

titud

inal

)

PE

RF

OR

MA

NC

EO

UT

CO

ME

S (

4)

-Acc

ount

ing

-Mar

ket

-Gro

wth

OT

HE

R M

OD

ER

AT

OR

S (

6)

-Pro

duct

Div

ersi

ficat

ion

-Org

aniz

atio

nal C

hara

cter

istic

s-T

MT

Exp

erie

nce

and

Div

ersi

ty

AN

TE

CE

DE

NT

S (

1)

-TM

T C

hara

cter

istic

s-B

oard

Com

posi

tion

-Org

aniz

atio

nal

Str

uctu

re a

nd S

ize

-Ow

ners

hip

Str

ateg

ic E

lem

ents

-Pro

cess

es a

nd R

esou

rces

EN

VIR

ON

ME

NTA

L FA

CTO

RS

(5)

-Hom

e, H

ost C

ount

ry R

esou

rces

-Inst

itutio

nal E

nviro

nmen

t-T

ask

Env

ironm

ent

-Indu

stry

Com

petit

ive

Env

ironm

ent

-Unc

erta

inty

Dire

ct R

elat

ions

hip,

e.g

., 2-

4

Mod

erat

ed R

elat

ions

hip,

e.g

., 2-

4 (5

)

Fig

ure

1A

Fra

mew

ork

for

Und

erst

andi

ng I

nter

nati

onal

Div

ersi

fica

tion

Res

earc

h

836

Not

e:T

MT

= to

p m

anag

emen

t tea

m

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

837

Tabl

e 1

Sum

mar

y of

Em

piri

cal R

esea

rch

on I

nter

nati

onal

Div

ersi

fica

tion

Pub

lishe

d Si

nce

1995

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:A

ntec

eden

ts

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

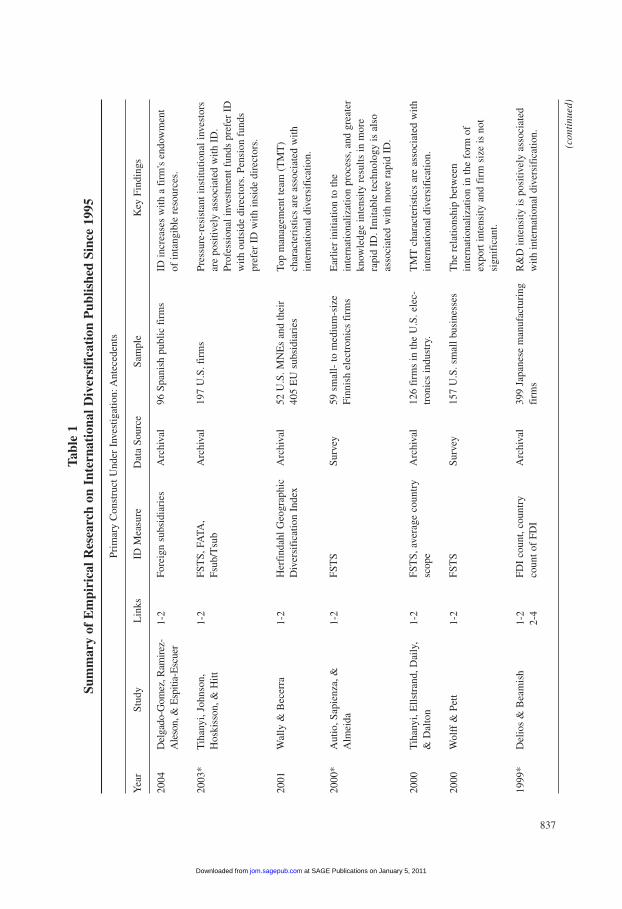

2004

2003

*

2001

2000

*

2000

2000

1999

*

1-2

1-2

1-2

1-2

1-2

1-2

1-2

2-4

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Surv

ey

Arc

hiva

l

Surv

ey

Arc

hiva

l

Del

gado

-Gom

ez,R

amir

ez-

Ale

son,

& E

spiti

a-E

scue

r

Tih

anyi

,Joh

nson

,H

oski

sson

,& H

itt

Wal

ly &

Bec

erra

Aut

io,S

apie

nza,

&A

lmei

da

Tih

anyi

,Ells

tran

d,D

aily

,&

Dal

ton

Wol

ff &

Pet

t

Del

ios

& B

eam

ish

Fore

ign

subs

idia

ries

FST

S,FA

TA,

Fsub

/Tsu

b

Her

find

ahl G

eogr

aphi

cD

iver

sifi

catio

n In

dex

FST

S

FST

S,av

erag

e co

untr

ysc

ope

FST

S

FDI

coun

t,co

untr

yco

unt o

f FD

I

96 S

pani

sh p

ublic

fir

ms

197

U.S

. fir

ms

52 U

.S. M

NE

s an

d th

eir

405

EU

sub

sidi

arie

s

59 s

mal

l- to

med

ium

-siz

eFi

nnis

h el

ectr

onic

s fi

rms

126

firm

s in

the

U.S

. ele

c-tr

onic

s in

dust

ry.

157

U.S

. sm

all b

usin

esse

s

399

Japa

nese

man

ufac

turi

ngfi

rms

ID in

crea

ses

with

a f

irm

's e

ndow

men

tof

inta

ngib

le r

esou

rces

.

Pres

sure

-res

ista

nt in

stitu

tiona

l inv

esto

rsar

e po

sitiv

ely

asso

ciat

ed w

ith I

D.

Prof

essi

onal

inve

stm

ent f

unds

pre

fer

IDw

ith o

utsi

de d

irec

tors

. Pen

sion

fun

dspr

efer

ID

with

insi

de d

irec

tors

.

Top

man

agem

ent t

eam

(T

MT

)ch

arac

teri

stic

s ar

e as

soci

ated

with

inte

rnat

iona

l div

ersi

fica

tion.

Ear

lier

initi

atio

n to

the

inte

rnat

iona

lizat

ion

proc

ess,

and

grea

ter

know

ledg

e in

tens

ity r

esul

ts in

mor

era

pid

ID. I

mita

ble

tech

nolo

gy is

als

oas

soci

ated

with

mor

e ra

pid

ID.

TM

T c

hara

cter

istic

s ar

e as

soci

ated

with

inte

rnat

iona

l div

ersi

fica

tion.

The

rel

atio

nshi

p be

twee

nin

tern

atio

naliz

atio

n in

the

form

of

expo

rt in

tens

ity a

nd f

irm

siz

e is

not

sign

ific

ant.

R&

D in

tens

ity is

pos

itive

ly a

ssoc

iate

dw

ith in

tern

atio

nal d

iver

sifi

catio

n.

(con

tinu

ed)

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

838

1998

*

1997

1996

2004

2003

*

1-2

1-2

1-2

2-4

2-4 (5)

2-4 (5)

Arc

hiva

l

Arc

hiva

l

Surv

ey &

arch

ival

Arc

hiva

l

Arc

hiva

l

Sand

ers

& C

arpe

nter

Fieg

enba

um,S

have

r,&

Yeu

ng

Sam

bhar

ya

Nac

hum

Wan

& H

oski

sson

FST

S,FA

TA,n

umbe

rof

cou

ntri

es w

ith

subs

idia

ries

FST

S

FST

S,FA

TA

Geo

grap

hic

Div

ersi

fica

tion

Inde

x

No.

of

coun

trie

s w

ithsu

bsid

iari

es

258

U.S

. fir

ms

from

the

S&P

500.

104

U.S

. Fir

ms

with

oper

atio

ns in

the

Mid

dle

Eas

t

54 U

.S. f

irm

s fr

om th

eFo

rtun

e In

dust

rial

500

345

firm

s fr

om d

evel

opin

gco

untr

ies

722

Wes

tern

Eur

opea

n fi

rms

Inte

rnat

iona

l div

ersi

fica

tion

ispo

sitiv

ely

rela

ted

to f

irm

per

form

ance

.

Hig

her

inte

rnat

iona

l div

ersi

fica

tion

isas

soci

ated

with

hig

her

CE

Oco

mpe

nsat

ion,

long

er te

rm C

EO

pay

,la

rger

TM

Ts,

and

sepa

ratio

n of

chai

rper

son

and

CE

O p

ositi

ons.

R&

D in

tens

ity is

pos

itive

ly r

elat

ed to

inte

rnat

iona

l div

ersi

fica

tion.

TM

Ts

with

gre

ater

inte

rnat

iona

lex

peri

ence

and

mor

e he

tero

gene

ity a

reas

soci

ated

with

hig

her

ID.

ID is

pos

itive

ly a

ssoc

iate

d w

ithpe

rfor

man

ce. T

his

rela

tions

hip

vari

esby

geo

grap

hic

regi

on.

Mun

ific

ence

in th

e ho

me

coun

try

mod

erat

es I

D-p

erfo

rman

ce r

elat

ions

hip

(it i

s po

sitiv

e in

mor

e m

unif

icen

ten

viro

nmen

ts,n

egat

ive

in le

ss)

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:C

ompe

titiv

e or

Cou

ntry

Env

iron

men

t

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

Tabl

e 1

(con

tinu

ed)

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:A

ntec

eden

ts

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

839

2002

*

2001

*

1999

1998

*

2004

*

2004

2-4

2-4 (6)

1-2 (5)

5-2

5-2

2-4

2-4 (6)

2-4

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Ver

meu

len

& B

arke

ma

Car

pent

er &

Fre

dric

kson

Sark

ar,C

avus

gil,

& A

ulak

h

Mar

tin,S

wam

inat

han,

&M

itche

ll

Lu

& B

eam

ish

Tho

mas

& E

den

No.

of

coun

trie

s,ex

pans

ion

per

year

FST

S,FA

TA,f

orei

gnsu

bsid

iari

es in

cul

tura

lzo

nes

FDI

coun

t,to

tal F

DI

Dum

my

vari

able

for

entr

y in

to N

orth

Am

eric

an m

arke

t

Fore

ign

subs

idia

ry,

no. o

f co

untr

ies

ente

red

FST

S,FA

TA,c

ount

rysc

ope

22 f

irm

s in

man

y in

dust

ries

over

26

year

s

207

U.S

. ind

ustr

ial f

irm

sfr

om th

e S&

P 50

0

19 la

rge

tele

com

mun

icat

ions

car

rier

sw

orld

wid

e.

547

Japa

nese

fir

ms

in th

eau

tom

obile

indu

stry

.

1,48

9 Ja

pane

se f

irm

s,19

86-

1997

151

U.S

. man

ufac

turi

ngfi

rms,

1990

-199

4

Spee

d of

inte

rnat

iona

lizat

ion,

spre

ad o

fth

e ge

ogra

phic

and

pro

duct

mar

kets

ente

red,

and

the

irre

gula

rity

of

the

expa

nsio

n pa

ttern

neg

ativ

ely

mod

erat

eID

-per

form

ance

rel

atio

nshi

p.

TM

T c

hara

cter

istic

s ar

e po

sitiv

ely

asso

ciat

ed w

ith I

D,b

ut th

e in

flue

nce

ofT

MT

tenu

re h

eter

ogen

eity

and

func

tiona

l het

erog

enei

ty a

re m

oder

ated

by e

nvir

onm

enta

l unc

erta

inty

.

Indu

stry

,net

wor

k,an

d en

try

cond

ition

sar

e po

sitiv

ely

asso

ciat

ed w

ith p

ace

and

mod

e of

ID

.

Supp

lier

ID in

crea

ses

at a

dec

reas

ing

rate

as

the

num

ber

of b

uyer

s th

at h

ave

inte

rnat

iona

lized

incr

ease

s. S

uppl

ier

IDin

itial

ly in

crea

ses,

then

dec

reas

es w

ithin

tern

atio

naliz

atio

n of

com

petit

ors.

The

re is

an

S-sh

aped

rel

atio

nshi

pbe

twee

n in

tern

atio

nal d

iver

sifi

catio

nan

d pe

rfor

man

ce. F

irm

s in

vest

ing

inin

tang

ible

ass

ets

achi

eve

grea

ter

gain

sfr

om in

tern

atio

nal d

iver

sifi

catio

n.

Thr

ee-s

tage

sig

moi

d re

latio

nshi

pbe

twee

n ID

and

per

form

ance

.

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:Fi

rm P

erfo

rman

ce

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

(con

tinue

d)

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

840

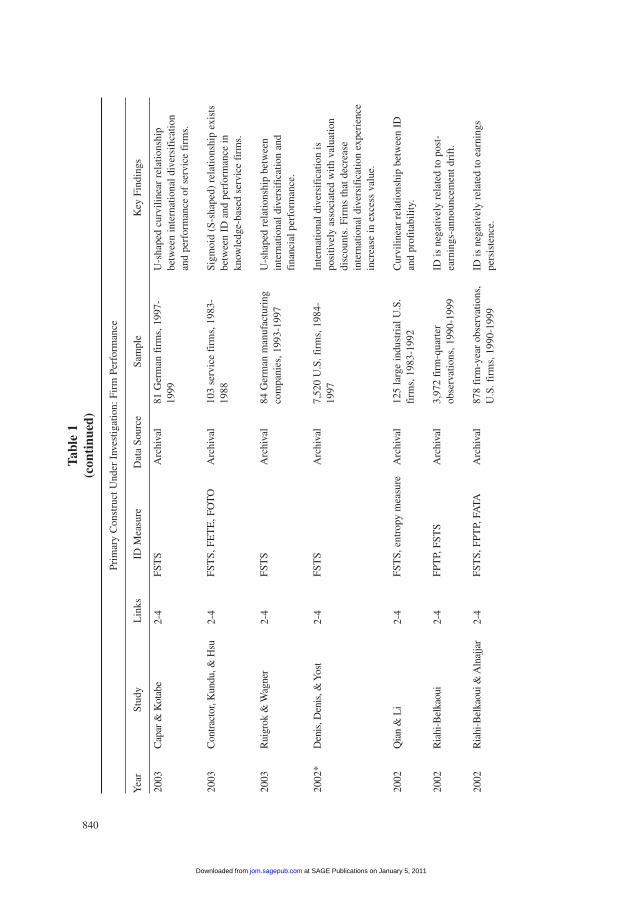

2003

2003

2003

2002

*

2002

2002

2002

2-4

2-4

2-4

2-4

2-4

2-4

2-4

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Cap

ar &

Kot

abe

Con

trac

tor,

Kun

du,&

Hsu

Rui

grok

& W

agne

r

Den

is,D

enis

,& Y

ost

Qia

n &

Li

Ria

hi-B

elka

oui

Ria

hi-B

elka

oui &

Aln

ajja

r

FST

S

FST

S,FE

TE

,FO

TO

FST

S

FST

S

FST

S,en

trop

y m

easu

re

FPT

P,FS

TS

FST

S,FP

TP,

FATA

81 G

erm

an f

irm

s,19

97-

1999

103

serv

ice

firm

s,19

83-

1988

84 G

erm

an m

anuf

actu

ring

com

pani

es,1

993-

1997

7,52

0 U

.S. f

irm

s,19

84-

1997

125

larg

e in

dust

rial

U.S

.fi

rms,

1983

-199

2

3,97

2 fi

rm-q

uart

erob

serv

atio

ns,1

990-

1999

878

firm

-yea

r ob

serv

atio

ns,

U.S

. fir

ms,

1990

-199

9

U-s

hape

d cu

rvili

near

rel

atio

nshi

pbe

twee

n in

tern

atio

nal d

iver

sifi

catio

nan

d pe

rfor

man

ce o

f se

rvic

e fi

rms.

Sigm

oid

(S-s

hape

d) r

elat

ions

hip

exis

tsbe

twee

n ID

and

per

form

ance

inkn

owle

dge-

base

d se

rvic

e fi

rms.

U-s

hape

d re

latio

nshi

p be

twee

nin

tern

atio

nal d

iver

sifi

catio

n an

dfi

nanc

ial p

erfo

rman

ce.

Inte

rnat

iona

l div

ersi

fica

tion

ispo

sitiv

ely

asso

ciat

ed w

ith v

alua

tion

disc

ount

s. F

irm

s th

at d

ecre

ase

inte

rnat

iona

l div

ersi

fica

tion

expe

rien

cein

crea

se in

exc

ess

valu

e.

Cur

vilin

ear

rela

tions

hip

betw

een

IDan

d pr

ofita

bilit

y.

ID is

neg

ativ

ely

rela

ted

to p

ost-

earn

ings

-ann

ounc

emen

t dri

ft.

ID is

neg

ativ

ely

rela

ted

to e

arni

ngs

pers

iste

nce.

Tabl

e 1

(con

tinu

ed)

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:Fi

rm P

erfo

rman

ce

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

841

2001

*

2001

1999

*

1998

1997

*

2005

2-4

2-4 (6)

2-4

2-4

2-3

2-4

2-4

2-4

(6)

2-4

(6)

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Lu

& B

eam

ish

Ram

irez

-Ale

son

& E

spiti

a-E

scue

r

Gom

es &

Ram

asw

amy

Ria

hi-B

elka

oui

Hitt

,Hos

kiss

on,&

Kim

J. L

i & Q

ian

No.

of

coun

trie

s,no

. of

10%

equ

ity F

DI

Div

ersi

fica

tion

inde

x,m

arke

t div

ersi

fica

tion

cate

gori

es

FST

S,FA

TA,

No.

of

coun

trie

sen

tere

d

FST

S

Ent

ropy

,by

4 pr

imar

yfo

reig

n m

arke

ts

FST

S,FA

TA,F

ET

E

164

Japa

nese

sm

all-

and

med

ium

-siz

e fi

rms,

1986

-199

7

103

Span

ish

firm

s,19

91-1

995

570

U.S

. man

ufac

turi

ngfi

rms,

1990

-199

5

100

U.S

. man

ufac

turi

ng a

ndse

rvic

e fi

rms,

1987

-199

3

295

U.S

. man

ufac

turi

ngfi

rms,

1988

-199

0

167

U.S

. fir

ms

from

the

Fort

une

500

The

re is

a U

-sha

ped

rela

tions

hip

betw

een

inte

rnat

iona

l div

ersi

fica

tion

and

firm

per

form

ance

. Exp

ortin

gne

gativ

ely

mod

erat

es th

is r

elat

ions

hip.

A p

ositi

ve r

elat

ions

hip

is f

ound

betw

een

mar

ket v

alue

and

inte

rnat

iona

ldi

vers

ific

atio

n.

The

re is

an

inve

rted

-U-s

hape

dre

latio

nshi

p be

twee

n in

tern

atio

nal

dive

rsif

icat

ion

and

oper

atin

gpe

rfor

man

ce,a

lso

betw

een

inte

rnat

iona

ldi

vers

ific

atio

n an

d fi

nanc

ial

perf

orm

ance

.

The

re is

an

S-sh

aped

rel

atio

nshi

pbe

twee

n ID

and

fir

m p

erfo

rman

ce.

The

re is

an

inve

rted

-U-s

hape

dre

latio

nshi

p be

twee

n in

tern

atio

nal

dive

rsif

icat

ion

and

perf

orm

ance

.Pr

oduc

t div

ersi

fica

tion

mod

erat

es th

isre

latio

nshi

p.

Reg

iona

l div

ersi

fica

tion

mod

erat

es I

D-

perf

orm

ance

rel

atio

nshi

p. I

D m

oder

ates

PD-p

erfo

rman

ce r

elat

ions

hip. (c

onti

nued

)

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:M

oder

ator

s

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

842

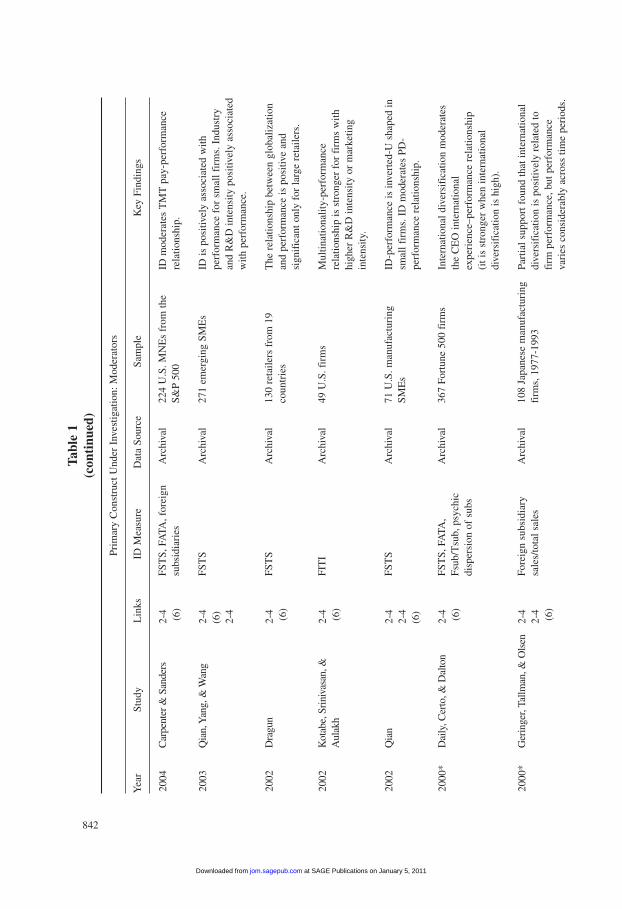

2004

2003

2002

2002

2002

2000

*

2000

*

2-4 (6)

2-4

(6)

2-4

2-4 (6)

2-4 (6)

2-4

2-4

(6)

2-4 (6)

2-4

2-4 (6)

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Car

pent

er &

San

ders

Qia

n,Y

ang,

& W

ang

Dra

gun

Kot

abe,

Srin

ivas

an,&

Aul

akh

Qia

n

Dai

ly,C

erto

,& D

alto

n

Ger

inge

r,Ta

llman

,& O

lsen

FST

S,FA

TA,f

orei

gnsu

bsid

iari

es

FST

S

FST

S

FIT

I

FST

S

FST

S,FA

TA,

Fsub

/Tsu

b,ps

ychi

cdi

sper

sion

of

subs

Fore

ign

subs

idia

rysa

les/

tota

l sal

es

224

U.S

. MN

Es

from

the

S&P

500

271

emer

ging

SM

Es

130

reta

ilers

fro

m 1

9co

untr

ies

49 U

.S. f

irm

s

71 U

.S. m

anuf

actu

ring

SME

s

367

Fort

une

500

firm

s

108

Japa

nese

man

ufac

turi

ngfi

rms,

1977

-199

3

ID m

oder

ates

TM

T p

ay-p

erfo

rman

cere

latio

nshi

p.

ID is

pos

itive

ly a

ssoc

iate

d w

ithpe

rfor

man

ce f

or s

mal

l fir

ms.

Ind

ustr

yan

d R

&D

inte

nsity

pos

itive

ly a

ssoc

iate

dw

ith p

erfo

rman

ce.

The

rel

atio

nshi

p be

twee

n gl

obal

izat

ion

and

perf

orm

ance

is p

ositi

ve a

ndsi

gnif

ican

t onl

y fo

r la

rge

reta

ilers

.

Mul

tinat

iona

lity-

perf

orm

ance

rela

tions

hip

is s

tron

ger

for

firm

s w

ithhi

gher

R&

D in

tens

ity o

r m

arke

ting

inte

nsity

.

ID-p

erfo

rman

ce is

inve

rted

-U s

hape

d in

smal

l fir

ms.

ID

mod

erat

es P

D-

perf

orm

ance

rel

atio

nshi

p.

Inte

rnat

iona

l div

ersi

fica

tion

mod

erat

esth

e C

EO

inte

rnat

iona

lex

peri

ence

–per

form

ance

rel

atio

nshi

p(i

t is

stro

nger

whe

n in

tern

atio

nal

dive

rsif

icat

ion

is h

igh)

.

Part

ial s

uppo

rt f

ound

that

inte

rnat

iona

ldi

vers

ific

atio

n is

pos

itive

ly r

elat

ed to

firm

per

form

ance

,but

per

form

ance

vari

es c

onsi

dera

bly

acro

ss ti

me

peri

ods.

Tabl

e 1

(con

tinu

ed)

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:M

oder

ator

s

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

843

1998

1996

*

1996

1996

*

1995

1995

2005

2-4

2-4

(6)

1-2

2-4

2-4

(6)

2-4

(6)

2-4

(6)

2-4

(6)

2-3

2-3-

4

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Surv

ey a

ndar

chiv

al

Arc

hiva

l

Surv

ey a

ndar

chiv

al

Surv

ey

Ria

hi-B

elka

oui &

Pic

ur

Blo

odgo

od,S

apie

nza,

&A

lmei

da

Ria

hi-B

elka

oui

Tallm

an &

Li

Ram

asw

amy

Sam

bhar

ya

Dib

rell,

Dav

is,&

Dan

skin

FST

S,FP

TP,

FATA

Perc

enta

ge o

f lo

gist

ics

outs

ide

the

U.S

.

FST

S

FST

S,no

. of

fore

ign

coun

trie

s

FATA

FST

S,FA

TA

FST

S,FE

TE

,FPT

P

80 U

.S. m

anuf

actu

ring

and

serv

ice

firm

s,19

87-1

992

61 f

irm

s th

at h

ad a

n IP

O in

1991

and

less

than

5 y

ears

old

31 F

renc

h M

NE

s

192

U.S

. man

ufac

turi

ngfi

rms

25 U

.S. M

NE

s in

phar

mac

eutic

als

53 U

.S. f

irm

s fr

om th

eFo

rtun

e In

dust

rial

500

85 f

irm

s in

pul

p an

d pa

per

ID is

pos

itive

ly a

ssoc

iate

d w

ithpe

rfor

man

ce (

rela

tions

hip

is s

tron

ger

with

mor

e di

vers

e in

vest

men

top

port

unity

set

).

Inte

rnat

iona

l div

ersi

fica

tion

is th

epr

oduc

t dif

fere

ntia

tion

as a

sou

rce

ofco

mpe

titiv

e ad

vant

age,

inte

rnat

iona

lex

peri

ence

of

the

BO

D,a

nd s

ize

at th

etim

e of

IPO

.

ID is

pos

itive

ly a

ssoc

iate

d w

ithpe

rfor

man

ce. P

erfo

rman

ce g

ains

fro

mID

are

mor

e lik

ely

with

unr

elat

eddi

vers

ific

atio

n.

Min

imal

rel

atio

nshi

p be

twee

n ID

-pe

rfor

man

ce. A

lso,

ID h

as o

nly

a w

eak

effe

ct o

n th

e re

latio

nshi

p be

twee

n PD

and

perf

orm

ance

.

Mul

tinat

iona

lity-

perf

orm

ance

rela

tions

hip

is s

tron

ger

for

grea

ter

amou

nts

of c

oord

inat

ion

and

cont

rol.

PD is

neg

ativ

ely

asso

ciat

ed w

ith I

D.

Nei

ther

lead

s to

impr

oved

per

form

ance

,bu

t the

inte

ract

ion

does

impr

ove

perf

orm

ance

.

ID p

ositi

vely

ass

ocia

ted

with

red

uctio

nin

cyc

le ti

mes

.

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:Pr

oces

s O

utco

mes

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

(con

tinu

ed)

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

844

Tabl

e 1

(con

tinu

ed)

Prim

ary

Con

stru

ct U

nder

Inv

estig

atio

n:Pr

oces

s O

utco

mes

Yea

rSt

udy

Lin

ksID

Mea

sure

Dat

a So

urce

Sam

ple

Key

Fin

ding

s

2004

*

2004

2004

2003

2000

*

2000

1998

2-3

2-3

(6)

2-3

2-3

2-4

2-3

2-3

3-4

2-3

2-4

2-3

Surv

ey

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Yeo

h

Low

& C

hen

Wag

ner

Hsu

& B

oggs

Zah

ra,I

rela

nd,&

Hitt

Kw

ok &

Ree

b

Han

,Lee

,& S

uk

FET

E,e

ntro

py

CIF

AR

inde

x

FST

S

FST

S,co

untr

y sc

ope

Num

ber

of c

ount

ries

,D

iver

sity

inde

x

FATA

FST

S

258

new

ven

ture

s in

the

U.S

.

232

indu

stri

al f

irm

s,19

86-1

990.

83 G

erm

an m

anuf

actu

ring

firm

s,19

93-1

997

118

U.S

. fir

ms,

1996

-199

8

321

high

-tec

h ne

w v

entu

res

in 1

993

1,32

0 fi

rms

in r

egul

ated

indu

stri

es,1

992-

1996

.

2,64

3 m

anuf

actu

ring

fir

ms

from

7 c

ount

ries

in 1

994

ID is

neg

ativ

ely

rela

ted

to te

chno

logi

cal

lear

ning

and

pos

itive

ly r

elat

ed to

soc

ial

lear

ning

,mod

erat

ed b

y cu

ltura

ldi

vers

ity a

nd T

MT

inte

rnat

iona

lex

peri

ence

.

ID n

egat

ivel

y as

soci

ated

with

le

vera

ge.

Inve

rted

-U-s

hape

d re

latio

nshi

p be

twee

nco

st e

ffic

ienc

y an

d in

tern

atio

naliz

atio

nsp

eed.

The

re is

an

inve

rted

-U-s

hape

dre

latio

nshi

p be

twee

n as

set t

urno

ver

and

ID a

nd b

etw

een

scop

e of

ID

and

perf

orm

ance

.

ID is

ass

ocia

ted

with

tech

nolo

gica

lle

arni

ng,w

hich

in tu

rn is

pos

itive

lyas

soci

ated

with

fir

m p

erfo

rman

ce.

Inte

rnat

iona

lizat

ion

is a

ssoc

iate

d w

ithde

bt r

educ

tion.

The

re is

no

cons

iste

nt p

ositi

ve e

ffec

t of

ID o

n pe

rfor

man

ce in

fir

ms

acro

ssco

untr

ies,

but I

D is

pos

itive

ly r

elat

ed to

com

pone

nts

of R

OE

.

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

845

Not

e:T

he t

able

inc

lude

s on

ly e

mpi

rica

l ar

ticle

s th

at o

pera

tiona

lize

inte

rnat

iona

l di

vers

ific

atio

n or

its

equ

ival

ent,

such

as

inte

rnat

iona

lizat

ion

or g

eogr

aphi

c ex

pans

ion.

*In

dica

tes

Web

of

Scie

nce

mos

t hig

hly

cite

d ar

ticle

s. I

D =

inte

rnat

iona

l div

ersi

fica

tion;

FST

S =

for

eign

sal

es/to

tal s

ales

; FA

TA =

for

eign

ass

ets/

tota

l ass

ets;

Fsu

b/T

sub

= f

orei

gn s

ubsi

diar

ies/

tota

l sub

sidi

arie

s;M

NE

= m

ultin

atio

nal e

nter

pris

e; F

DI

= f

orei

gn d

irec

t inv

estm

ent;

TM

T =

top

man

agem

ent t

eam

; FE

TE

= f

orei

gn e

xpor

ts/to

tal e

xpor

ts; F

OT

O =

for

eign

off

ices

/tota

l off

ices

; FPT

P =

for

eign

prof

its/to

tal p

rofi

ts; P

D =

pro

duct

div

ersi

fica

tion;

SM

E =

med

ium

-siz

e en

terp

rise

s; F

ITI =

fore

ign

inco

me/

tota

l inc

ome;

IPO

= in

itial

pub

lic o

ffer

; BO

D =

Boa

rd o

f Dir

ecto

rs; C

IFA

R =

Cen

ter

for I

nter

natio

nal F

inan

cial

Ana

lysi

s an

d R

esea

rch;

RO

E =

retu

rn o

n eq

uity

; FT

TT

= fo

reig

n ta

xes/

tota

l tax

es; M

NC

= m

ultin

atio

nal c

orpo

ratio

n; N

YSE

= N

ew Y

ork

Stoc

k E

xcha

nge;

S&

P =

Stan

dard

& P

oor’

s.

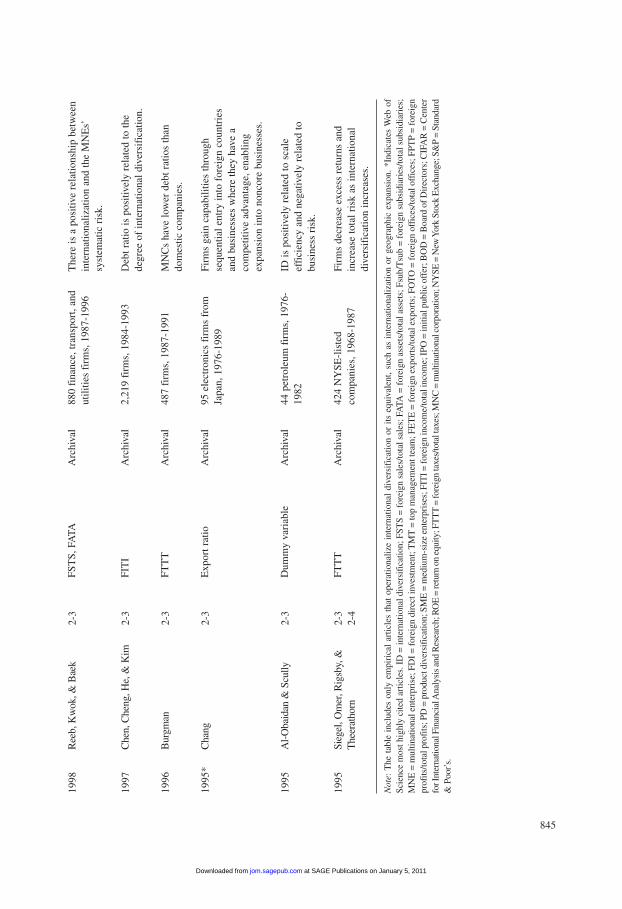

1998

1997

1996

1995

*

1995

1995

2-3

2-3

2-3

2-3

2-3

2-3

2-4

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Arc

hiva

l

Ree

b,K

wok

,& B

aek

Che

n,C

heng

,He,

& K

im

Bur

gman

Cha

ng

Al-

Oba

idan

& S

cully

Sieg

el,O

mer

,Rig

sby,

&T

heer

atho

rn

FST

S,FA

TA

FIT

I

FTT

T

Exp

ort r

atio

Dum

my

vari

able

FTT

T

880

fina

nce,

tran

spor

t,an

dut

ilitie

s fi

rms,

1987

-199

6

2,21

9 fi

rms,

1984

-199

3

487

firm

s,19

87-1

991

95 e

lect

roni

cs f

irm

s fr

omJa

pan,

1976

-198

9

44 p

etro

leum

fir

ms,

1976

-19

82

424

NY

SE-l

iste

dco

mpa

nies

,196

8-19

87

The

re is

a p

ositi

ve r

elat

ions

hip

betw

een

inte

rnat

iona

lizat

ion

and

the

MN

Es’

syst

emat

ic r

isk.

Deb

t rat

io is

pos

itive

ly r

elat

ed to

the

degr

ee o

f in

tern

atio

nal d

iver

sifi

catio

n.

MN

Cs

have

low

er d

ebt r

atio

s th

ando

mes

tic c

ompa

nies

.

Firm

s ga

in c

apab

ilitie

s th

roug

hse

quen

tial e

ntry

into

for

eign

cou

ntri

esan

d bu

sine

sses

whe

re th

ey h

ave

aco

mpe

titiv

e ad

vant

age,

enab

ling

expa

nsio

n in

to n

onco

re b

usin

esse

s.

ID is

pos

itive

ly r

elat

ed to

sca

leef

fici

ency

and

neg

ativ

ely

rela

ted

tobu

sine

ss r

isk.

Firm

s de

crea

se e

xces

s re

turn

s an

din

crea

se to

tal r

isk

as in

tern

atio

nal

dive

rsif

icat

ion

incr

ease

s.

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

the endowment of intangible resources but also the motivation of seeking intangible resourcesfrom the host country (e.g., intellectual capital). This resource-seeking motivation was foundto be most influential in information-intensive industries; market seeking and export seekingwere dominant motivations in less information-intensive industries. Araujo and Rezende(2003) considered path dependence and the influence of relational networks on internationaldiversification. The search for strategic resources and organizational processes that effectivelypredict international diversification is a recent phenomenon, and the research described hereinprovides the initial impetus toward more complete understanding.

Another line of research emphasizes the role of top executives in the decision to diversifyinternationally. Prior findings demonstrate that elite education, lower average age, and greaterinternational experience of the top management team (TMT) are positively associated withfirm international diversification (Eriksson & Johanson, 1997; Herrmann & Datta, 2005;Sambharya, 1996; Tihanyi et al., 2000; Wally & Becerra, 2001). These researchers reason thathigher education heightens managers’ awareness of international issues and that youngermanagers often have greater propensity toward risk taking. Furthermore, international expe-rience reduces the uncertainty associated with international expansion and creates socialcapital that can facilitate a firm’s plans to diversify internationally (Hitt et al., in press).International experience in the top management team (TMT) is also likely to increase thespeed of internationalization, particularly in small firms (Reuber & Fischer, 1997). The argu-ment that diversity within the TMT is likely to facilitate international diversification is con-sistent with findings that suggest larger (Sanders & Carpenter, 1998) and more heterogeneous(Sambharya, 1996) TMTs are associated with higher levels of international diversification.

Beyond the TMT, boards of directors and owners also influence organizational decisionsto diversify internationally. Tihanyi, Johnson, Hoskisson, and Hitt (2003) differentiated twotypes of pressure-resistant institutional investors, professional investment funds and pensionfunds, each with unique motivations for diversifying internationally. Ownership by eithergroup was found to be positively related to international diversification, but with a differenttheoretical rationale for each group’s behavior. Sanders and Carpenter (1998) used agencytheory to explain why the separation of chairperson and CEO positions is positively associ-ated with international diversification.

Environmental Factors: Relationships 1-2(5) and 2-4(5)

There are a variety of exogenous influences that shape when and how firms diversifyinternationally. Scholars have considered the effects of organizational task environments,institutional environments, and the natural environment. Discussion of the external environ-ment in the management literature is often focused on a firm’s task environment, includingcustomers, suppliers, and competitors (Castrogiovanni, 2002). In contrast, a multinationalfirm’s institutional environment is commonly considered in three domains: regulatory, cog-nitive, and normative institutions (Scott, 1995). The natural environment also has implica-tions for strategic decisions of the firm, although the intersection of the natural environmentand international diversification has not drawn appreciable research interest as yet (Starik &Marcus, 2000).

846 Journal of Management / December 2006

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

Several researchers have considered the effects of specific dimensions of the task environ-ment on international diversification decisions. For example, Martin and colleagues (1998)examined incentives and constraints on international expansion in relation to the firm’s buyersand suppliers. They found that the likelihood of international diversification increases at adecreasing rate with the number of internationally diverse buyers. Similarly, internationaldiversification of competitors leads to an initial increase and a subsequent decrease in supplierinternational involvement. In the telecommunications industry, researchers have found that thecompetitive structure of the industry and network characteristics of the firm are primary deter-minants of international diversification (Sarkar, Cavusgil, & Aulakh, 1999). In agreement withthese findings, Gimeno et al. (2005) compared competitive and institutional explanations formimicry in the international diversification process, finding the competitive rationale to havethe strongest influence.

Research has recently focused on institutional pressures—regulatory, cognitive, andnormative—as an important influence on a firm’s decisions regarding international diversifica-tion. Early research in this area found little relationship between host country regulatory indi-cators and international diversification decisions (Kobrin, 1976; Thunnel, 1977). Nigh (1985)suggested the lack of findings was due to methodological shortcomings, and more recentresearch has sought to rectify those problems. For example, Calof and Beamish (1995) foundthat the regulatory environment influences the mode of international diversification as well asmode changes. Acs, Morck, Shaver, and Yeung (1997) provided the theoretical basis for theimportant role of regulations and property rights in the host country, particularly in the case ofsmall- and medium-size firms seeking to internationalize. Others have focused on the influenceof economic institutions (Mascarenhas, 1992; Wan, 2005), suggesting that internationallydiversified firms first enter nations with lower bureaucratic costs, such as countries with liber-alized market economies. Although firms often find it easier to do business in countries wherethe social climate is similar to their own (Hitt et al., 1994), researchers have paid less attentionto normative and cognitive institutions in favor of studying the regulatory environment(Bergara, Henisz, & Spiller, 1998).

The host country resource endowment is an important consideration in firms’ choice of mar-kets for diversification. Firms may emphasize the market potential of the host country or thepotential for economies of scale in choosing target countries for diversification (Kochhar &Hitt, 1995). Nachum and Zaheer (2005) labeled these two motivations as market seeking andefficiency seeking, respectively, and added resource seeking, export seeking, and knowledgeseeking as additional motives, each of which value different resource endowments in the hostcountry. A topic of particular interest to researchers is how the composite level of technologi-cal sophistication and innovation capability of host countries influence market entry selections(Criscuolo, Narula, & Verspagen, 2005; Henisz & Macher, 2004). Although researchers haveconsidered home and host country endowments to be important (Buckley & Casson, 1998; Tse,Pan, & Au, 1997), most of this work is oriented specifically toward the entry mode decisionrather than international diversification in general (Werner, 2002).

Applying Dess and Beard’s (1984) model of environmental dimensions (e.g., complexity,munificence, and dynamism), Kostova and Zaheer (1999) suggested that complexity plays aprominent role in international diversification. Environmental complexity increases chal-lenges for organizational legitimacy more so for firms that are diversified internationally than

Hitt et al. / International Diversification 847

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

for primarily domestic firms. In other words, firms operating in multiple complex environ-ments experience more challenges than purely domestic firms operating in a single but com-plex domestic environment. Alternatively, Wan and Hoskisson (2003) found that munificenceof the home country environment functions as a moderator of the relationship between inter-national diversification and performance. Their results suggest that firms in more munificenthome country environments enjoy performance improvements when they diversify interna-tionally, whereas those in less munificent environments do not gain substantial performancebenefits. In addition, there is some evidence to suggest that dynamism may affect a firm’sdiversification strategy (Bergh & Lawless, 1998); international diversification researchershave examined the dynamism construct as a moderating variable (Carpenter & Fredrickson,2001; Rasheed, 2005). For example, Carpenter and Fredrickson (2001) found some evidencethat the relationship between TMT characteristics and international diversification may bestronger in highly uncertain environments. The authors explain that as firms diversify inter-nationally, TMT members are afforded greater discretion, which in turn increases demo-graphic effects on their strategic decisions.

Performance Outcomes: Relationships 2-4 and 4-2

The relationship between international diversification and firm performance has received themost attention in the literature, although findings have been mixed (Capar & Kotabe, 2003).Early research began by exploring differences in the performance of multinational and domes-tic firms (Brewer, 1981; Shaked, 1986; Vernon, 1971), but later studies focused on understand-ing the nature of the relationship. Vernon (1971) suggested that international diversification andperformance were positively related because of economies of scale and location-based advan-tages, prompting study of a positive linear relationship during the 1970s and 1980s (Errunza &Senbet, 1984; Grant, 1987; Grant, Jamine, & Thomas, 1988). Even recently, scholars (Delios &Beamish, 1999; Tallman & Li, 1996) have suggested that the scope of international diversifica-tion is positively related to firm profitability because it expands market opportunities, diversifiesrisk, and increases market power (Kim, Hwang, & Burgers, 1993; Kogut, 1985). Yet, other stud-ies have found a negative association and/or no association at all (Fatemi, 1984; Kumar, 1984;Siddharthan & Lall, 1982).

Currently, researchers posit a more complex relationship between international diversifica-tion and performance to reflect its costs as well as benefits, resembling U-shaped (Lu &Beamish, 2001; Ruigrok & Wagner, 2003), inverted-U-shaped (Gomes & Ramaswamy, 1999;Hitt et al., 1997), and S-shaped curves (Lu & Beamish, 2004; Thomas & Eden, 2004).Theoretical arguments suggesting an inverted-U relationship between the level of internationaldiversification and performance stress the positive effects of diversification up to a point, the“internationalization threshold,” where the costs of coordination among diverse operating unitsexceed the benefits of increased access to resources (Geringer et al., 1989; Sullivan, 1994b).Although prior work (Geringer et al., 1989; Hitt et al., 1994; Ramaswamy, 1995) hypothesizedthe possibility of an inverted-U relationship, Hitt et al. (1997) were among the first to provide amore solid theoretical foundation and employ a multidimensional measure of internationaldiversification. Exploring the stability of the relationship over time, Gomes and Ramaswamy

848 Journal of Management / December 2006

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from

(1999) supported the inverted-U relationship finding that increased international diversificationonly yields benefits up to a certain level and then declines because higher levels of diversifica-tion increase governance costs.

Still others report a U-shape relationship between international diversification and firmperformance, which is due to an interaction between initial governance costs and learningeffects (Lu & Beamish, 2001; Ruigrok & Wagner, 2003). Early on, international diversifica-tion may reduce firms’ profitability because of the complexity of an unrelated strategy.However, after a firm learns about the new environment, profitability begins to rise. Lu andBeamish (2001) found a U-shaped relationship in a sample of small- and medium-size enter-prises (SMEs) engaging in international diversification. In the initial stages of internationaldiversification, SMEs encounter performance declines as they deal with liabilities of for-eignness. However, performance improves with continued internationalization as newknowledge and capabilities are developed through learning and access to resources. In a lon-gitudinal study supporting the learning perspective, Ruigrok and Wagner (2003) found aU-shaped relationship between international diversification and performance, suggestingthat firms initially suffer declining performance but later learn and recover.

The differences in findings have been perplexing and have even led to more complex sig-moid models. Using FDI theory, Riahi-Belkaoui (1998) explained that entry into a newmarket is initially detrimental to performance. However, the positive effects arising frominternationalization occur at middle levels of diversification and decline again. Using a sim-ilar rationale, Contractor, Kundu, and Hsu (2003) found a sigmoid-shaped relationship inknowledge-based service firms. This S-curve relationship was again supported by Lu andBeamish (2004) and Thomas and Eden (2004). Lu and Beamish (2004) noted that as earlyliabilities and costs are reduced by experiential learning, firms profit from both scale andscope economies. However, as international diversification increases, governance and coor-dination costs associated with diversification increase and create more challenges for man-agement (Hitt et al., 1997). Consequently, Lu and Beamish (2004) found a horizontalS-curve, where the international diversification–performance relationship is negative at lowand high levels of international diversification, but positive at moderate levels.

Strategic management researchers investigating the international diversification-performance relationship have largely used accounting performance measures, but other dis-ciplines use market-based measures that may not yield the same results. In fact, Keats andHitt (1988) found that accounting and market-based measures of performance were nega-tively related. However, there is a lack of consensus about the international diversification-performance relationship even among those using market-based measures. A number ofstudies suggest that international diversification increases market value and reduces risks forinvestors (Brewer, 1981; Hughes & Sweeney, 1975; Kim et al., 1993). Some argue that inter-national diversification has negative effects on market value because it is more beneficial formanagers in search of prestige than it is for investors (Denis, Denis, & Yost, 2002; Fatemi,1984; Michel & Shaked, 1986). Others find higher valuation of multinational firms overdomestic firms, showing that increasing levels of diversification result in higher market value(Errunza & Senbet, 1984; Garrod & Rees, 1998; Ramirez-Aleson & Espitia-Escuer, 2001).

Regardless of the diverse performance measures used, findings remain inconclusive partlybecause of the examination of various industries, time periods, and motivations for international

Hitt et al. / International Diversification 849

at SAGE Publications on January 5, 2011jom.sagepub.comDownloaded from