Merrill Lynch conference 2013

19

Merril Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 0 Bart De Smet CEO

-

Upload

ageas -

Category

Economy & Finance

-

view

180 -

download

2

Transcript of Merrill Lynch conference 2013

Merril Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 0

Bart De Smet CEO

1

Conclusion Ageas’s Investor Day 2012 It’s all about ….

6 Values

5 Choices

4 Targets

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

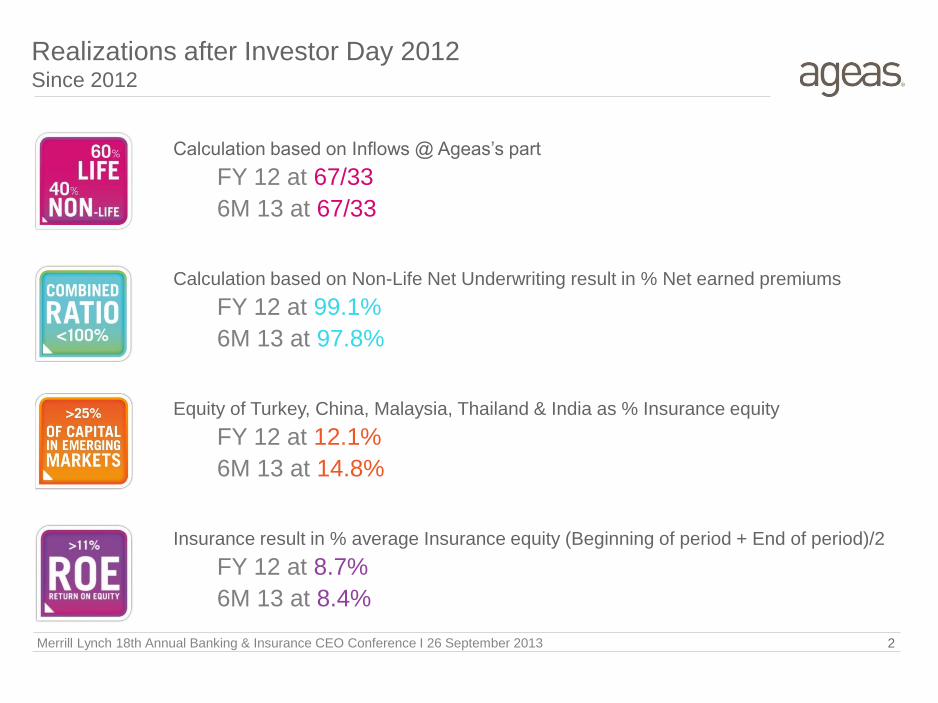

Realizations after Investor Day 2012 Since 2012

2

Calculation based on Inflows @ Ageas’s part

FY 12 at 67/33

6M 13 at 67/33

Calculation based on Non-Life Net Underwriting result in % Net earned premiums

FY 12 at 99.1%

6M 13 at 97.8%

Equity of Turkey, China, Malaysia, Thailand & India as % Insurance equity

FY 12 at 12.1%

6M 13 at 14.8%

Insurance result in % average Insurance equity (Beginning of period + End of period)/2

FY 12 at 8.7%

6M 13 at 8.4%

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

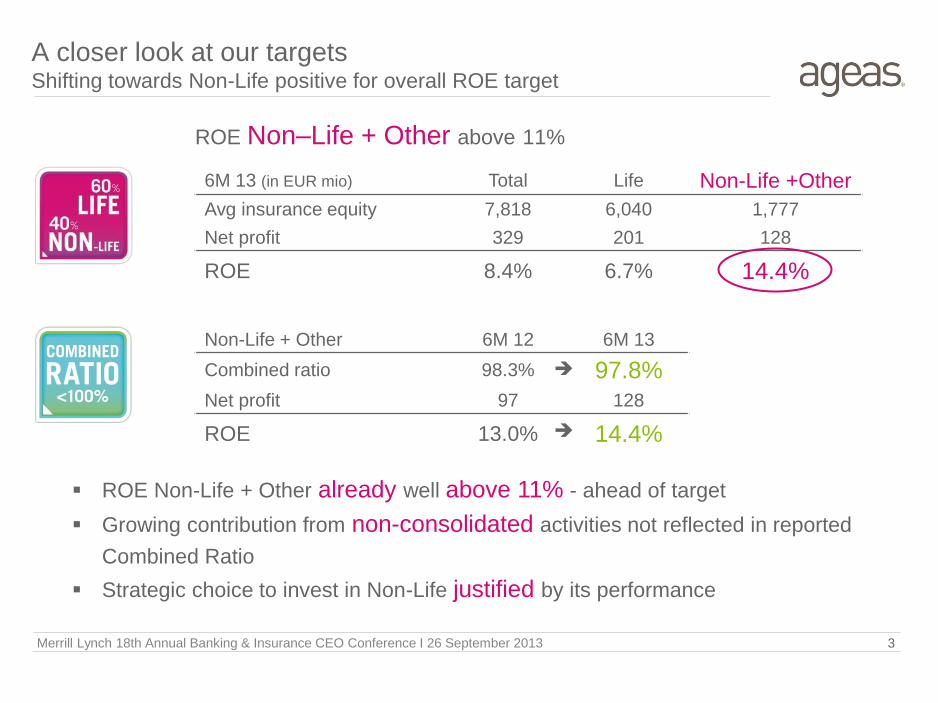

ROE Non–Life + Other above 11%

A closer look at our targets Shifting towards Non-Life positive for overall ROE target

6M 13 (in EUR mio) Total Life Non-Life +Other

Avg insurance equity 7,818 6,040 1,777

Net profit 329 201 128

ROE 8.4% 6.7% 14.4%

3

Non-Life + Other 6M 12 6M 13

Combined ratio 98.3% 97.8%

Net profit 97 128

ROE 13.0% 14.4%

ROE Non-Life + Other already well above 11% - ahead of target

Growing contribution from non-consolidated activities not reflected in reported

Combined Ratio

Strategic choice to invest in Non-Life justified by its performance

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

A closer look at our targets Shifting towards emerging markets positive for overall ROE target

Overall ROE < 11% - ROE emerging markets > 11%

6M 13 (in EUR mio) Total Belgium UK CEU Asia

Avg insurance equity 7,818 3,695 1,102 1,189 1,831

Net profit 329 160 58 46 66

ROE 8.4% 8.6% 10.5% 7.7% 7.2%

4

Emerging markets = Turkey, China, Thailand, India & Malaysia

Solid & increasing contribution from emerging markets to

Ageas’s net profit & ROE

Emerging markets 6M 12 6M 13

Avg insurance equity 964 1,054

Net profit * 67 76

ROE 13.9% 14.5%

*excluding regional costs

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

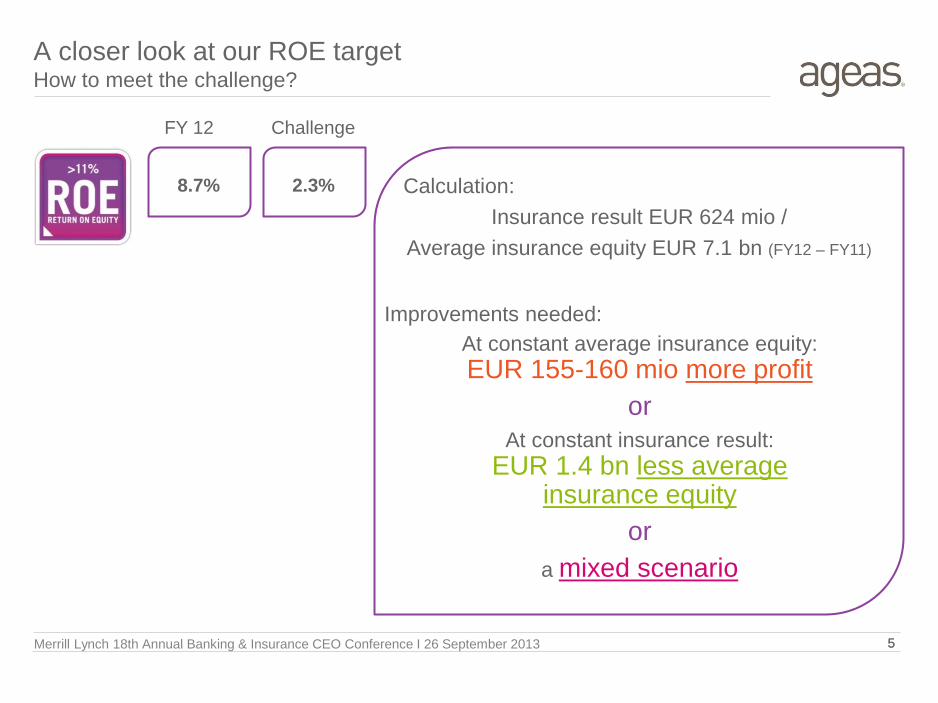

Challenge

2.3%

At constant average insurance equity:

EUR 155-160 mio more profit

or

At constant insurance result:

EUR 1.4 bn less average insurance equity

or

a mixed scenario

A closer look at our ROE target How to meet the challenge?

FY 12

8.7% Calculation:

Insurance result EUR 624 mio /

Average insurance equity EUR 7.1 bn (FY12 – FY11)

Improvements needed:

5 Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 5

How to reach Vision 2015 targets

The path towards realizing

the Vision 2015 targets

Focuses on:

1. ROE numerator : net profit

2. ROE denominator : insurance equity

Through:

1. Improving overall profitability

2. Gradually changing the company’s profile

6 Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 6

Active capital management

7

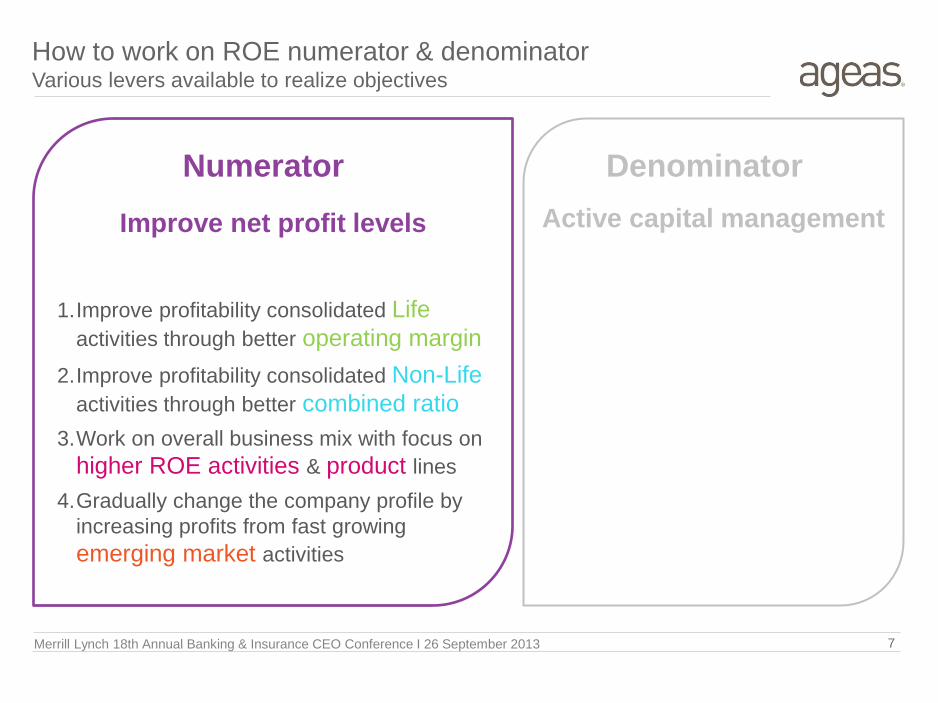

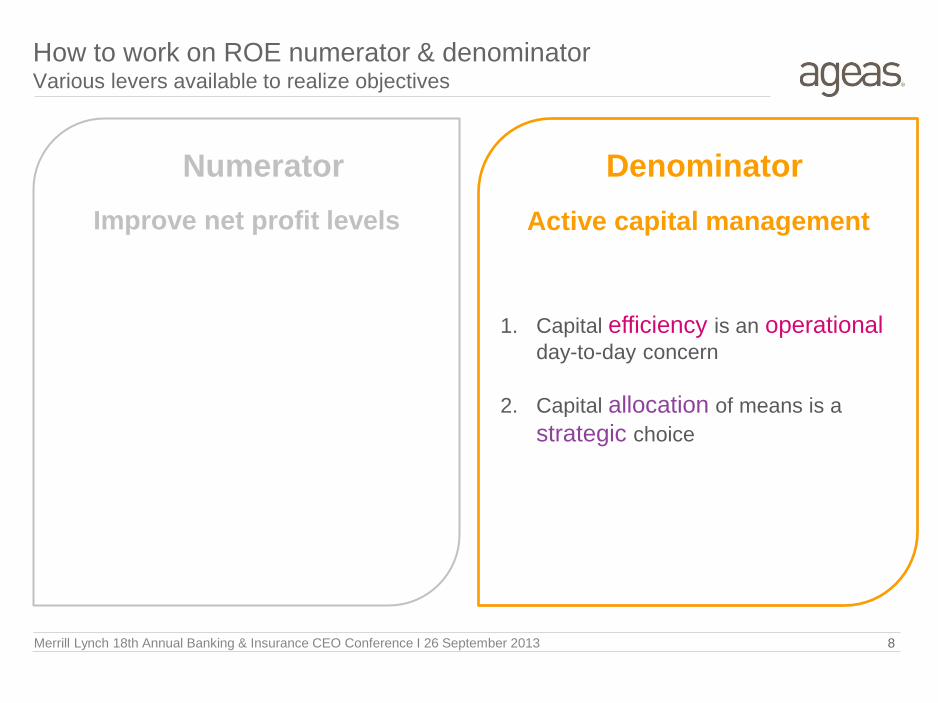

How to work on ROE numerator & denominator Various levers available to realize objectives

Improve net profit levels

1.Improve profitability consolidated Life

activities through better operating margin

2.Improve profitability consolidated Non-Life

activities through better combined ratio

3.Work on overall business mix with focus on

higher ROE activities & product lines

4.Gradually change the company profile by

increasing profits from fast growing

emerging market activities

Numerator Denominator

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

Active capital management

1. Capital efficiency is an operational day-to-day concern

2. Capital allocation of means is a

strategic choice

8

Improve net profit levels

Numerator Denominator

How to work on ROE numerator & denominator Various levers available to realize objectives

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

6M 13 net cash position General Account at EUR 2.1 bn

9

RPI transaction

share buy-back

capital reduction

In EUR mio

announced cash

movements

Expected cash in of EUR 0.2 bn from transactions RPI & BNPP Call option.

Expected cash out of EUR 0.4 bn in the coming months related to capital reduction & share buy-back

688

1,216

2,055340

827

144

(≈200)

(68) (77)(270)

(57)(≈200)

≈200

FY 11 FY 12 buy-back capitalinjection

TPL

paiddividend

upstreamopco's

RPI calloption

other 6M 13

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

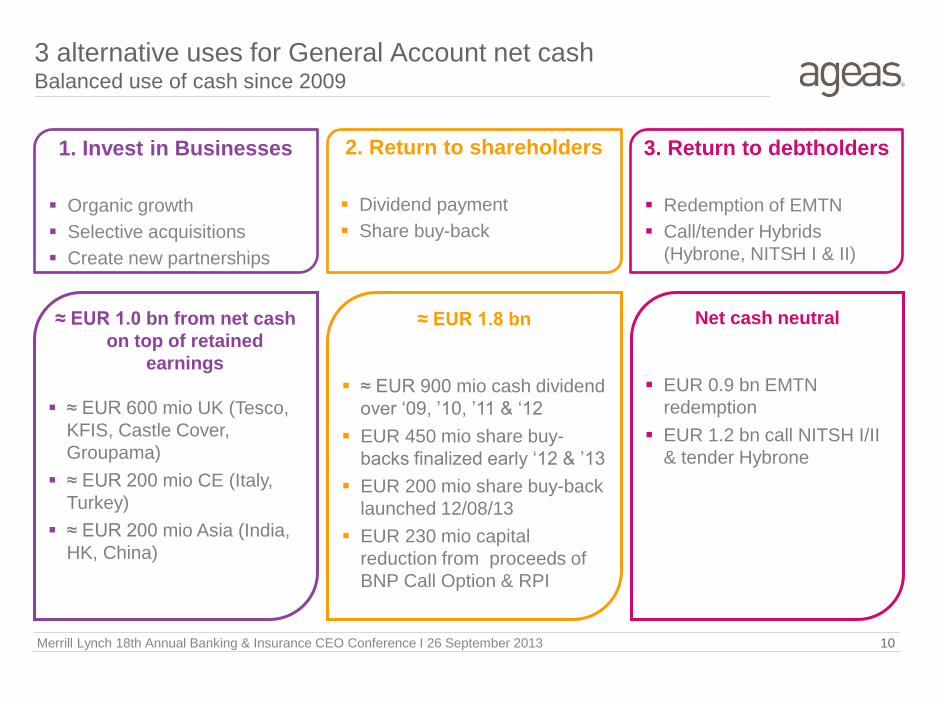

3 alternative uses for General Account net cash Balanced use of cash since 2009

3. Return to debtholders

Redemption of EMTN

Call/tender Hybrids

(Hybrone, NITSH I & II)

1. Invest in Businesses

Organic growth

Selective acquisitions

Create new partnerships

10

2. Return to shareholders

Dividend payment

Share buy-back

Net cash neutral

EUR 0.9 bn EMTN

redemption

EUR 1.2 bn call NITSH I/II

& tender Hybrone

≈ EUR 1.8 bn

≈ EUR 900 mio cash dividend

over ‘09, ’10, ’11 & ‘12

EUR 450 mio share buy-

backs finalized early ‘12 & ’13

EUR 200 mio share buy-back

launched 12/08/13

EUR 230 mio capital

reduction from proceeds of

BNP Call Option & RPI

≈ EUR 1.0 bn from net cash

on top of retained

earnings

≈ EUR 600 mio UK (Tesco,

KFIS, Castle Cover,

Groupama)

≈ EUR 200 mio CE (Italy,

Turkey)

≈ EUR 200 mio Asia (India,

HK, China)

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

Priority 1 : M&A : Focus on high ROE accretive activities New businesses need to pass the test on 3 key criteria

Critical size

Local presence should be

such that every entity can

compete effectively in its

market or niche

Critical size will ensure

each activity is able to

comply with Ageas’s

quality standards

Return in excess of

cost of equity

Return business will have

to exceed cost of equity

while taking into account

the business’ specificities

Return of growth business

will also take into

consideration the

expected value creation

Meaningful

contribution

Each activity should make

a meaningful contribution

to the insurance earnings

in the medium term

The contribution to the

insurance earnings should

be significant enough to

justify management time

11 Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

12

1. Priority to strengthen positions in existing markets

2. Clear preference for Non-Life. Expansion in Life

on a case by case basis

3. Further expansion in fast growing emerging markets while

respecting Ageas M&A criteria & overall financial

targets

continuing to build on a successful partnership

model

4. Flexibility for opportunities where Ageas believes

its expertise can create growth & improve the

business

Inorganic

growth

Priority 1 : M&A : Focus on high ROE accretive activities Disciplined approach will drive inorganic growth development

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

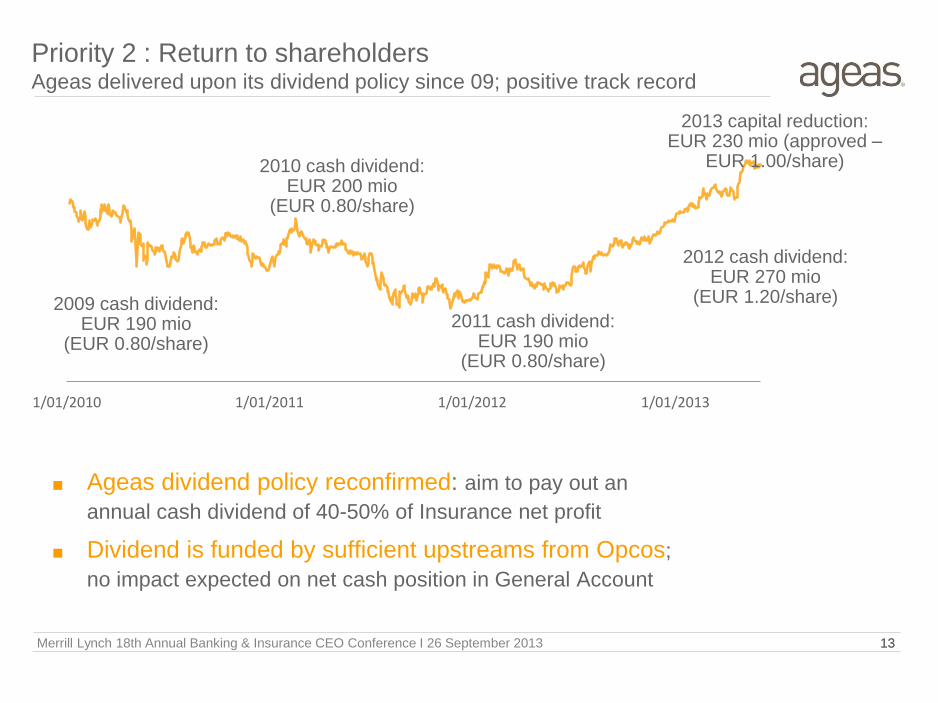

1/01/2010 1/01/2011 1/01/2012 1/01/2013

2009 cash dividend: EUR 190 mio

(EUR 0.80/share)

2010 cash dividend: EUR 200 mio

(EUR 0.80/share)

2011 cash dividend: EUR 190 mio

(EUR 0.80/share)

2012 cash dividend: EUR 270 mio

(EUR 1.20/share)

2013 capital reduction: EUR 230 mio (approved –

EUR 1.00/share)

■ Ageas dividend policy reconfirmed: aim to pay out an

annual cash dividend of 40-50% of Insurance net profit

■ Dividend is funded by sufficient upstreams from Opcos;

no impact expected on net cash position in General Account

13

Priority 2 : Return to shareholders Ageas delivered upon its dividend policy since 09; positive track record

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 13

Priority 2 : Return to shareholders Ageas started annual share buy-back programs in 2011

EUR 200 mio SBB - launched 08/2013

- on going

■ If no adequate M&A opportunities would arise, Ageas intends to

continue returning cash to shareholders in the most appropriate

way (share buy backs, dividends, capital reductions…)

14

EUR 200 mio SBB - launched 08/2012

- 3.8% shares cancelled

1/01/2010 1/01/2011 1/01/2012 1/01/2013

EUR 250 mio SBB - launched 08/2011

- 7.3% shares cancelled

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 14

15

Priority 3 : Return to debtholders No longer a priority

Recent initiatives returning cash to debtholders had no impact on

net cash position General Account

No intention to bid on FRESH financial instrument

No intention to raise new external hybrid debt

Optimizing debt levels in Opcos

Clear intention to lend on part of FRESH

Return cash to debtholders no longer a priority

From now on, Ageas will only report about 2 alternative uses of net cash

Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

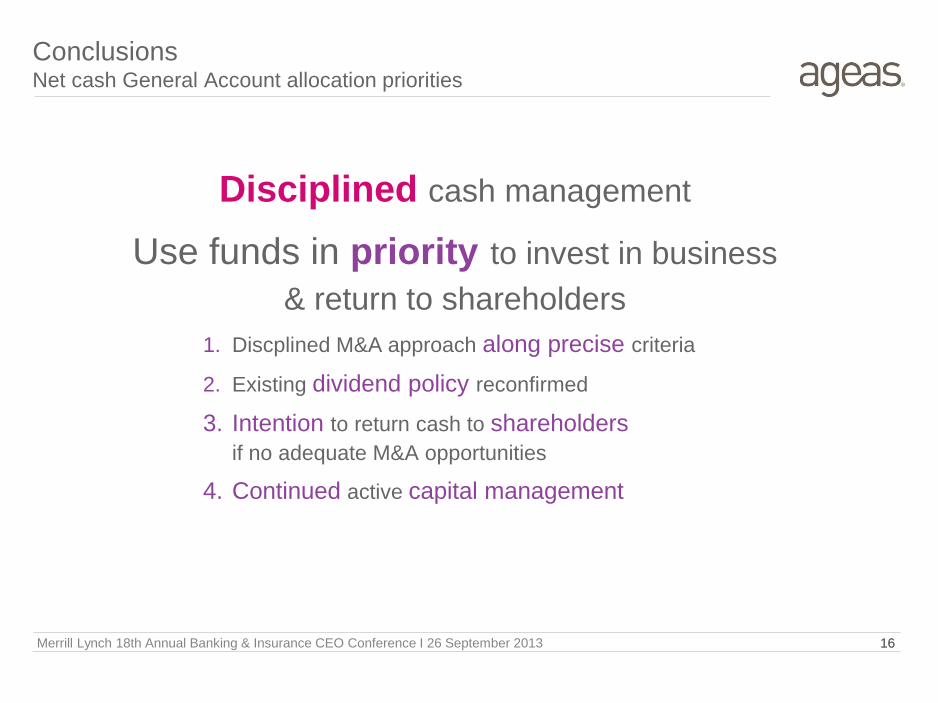

Conclusions Net cash General Account allocation priorities

Disciplined cash management

Use funds in priority to invest in business

& return to shareholders

1. Discplined M&A approach along precise criteria

2. Existing dividend policy reconfirmed

3. Intention to return cash to shareholders

if no adequate M&A opportunities

4. Continued active capital management

16 Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013 16

Insurance ROE target is leading & reconfirmed at 11%

The path to realize the 2015 target is clear & well defined

targets of 97%, 85-90 bps, 40-45 bps & capital optimization

Disciplined cash management rules all decisions

on the use of cash

Priority to first reinvest cash in business & return to shareholders if no

adequate M&A opportunities

No intention to bid on FRESH instrument

Continued active capital management going forward with focus on debt

optimization

Closing remarks

17 Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013

Disclaimer

18

Certain of the statements contained herein are statements of

future expectations and other forward-looking statements that

are based on management's current views and assumptions

and involve known and unknown risks and uncertainties that

could cause actual results, performance or events to differ

materially from those expressed or implied in such statements.

Future actual results, performance or events may differ

materially from those in such statements due to, without

limitation, (i) general economic conditions, including in particular

economic conditions in Ageas’s core markets, (ii) performance

of financial markets, (iii) the frequency and severity of insured

loss events, (iv) mortality and morbidity levels and trends, (v)

persistency levels, (vi) interest rate levels, (vii) currency

exchange rates, (viii) increasing levels of competition, (ix)

changes in laws and regulations, including monetary

convergence and the Economic and Monetary Union, (x)

changes in the policies of central banks and/or foreign

governments and (xi) general competitive factors, in each case

on a global, regional and/or national basis. In addition, the

financial information contained in this presentation, including the

pro forma information contained herein, is unaudited and is

provided for illustrative purposes only. It does not purport to be

indicative of what the actual results of operations or financial

condition of Ageas and its subsidiaries would have been had

these events occurred or transactions been consummated on or

as of the dates indicated, nor does it purport to be indicative of

the results of operations or financial condition that may be

achieved in the future. Merrill Lynch 18th Annual Banking & Insurance CEO Conference I 26 September 2013