Measuring Procurement's Performance

38

©ALL RIGHTS RESERVED - Confidential 1 Measuring Procurement’s Performance Peter Smith Wednesday October 17th 2012 Spend Matters UK/Europe

-

Upload

bravosolution -

Category

Business

-

view

10.521 -

download

1

Transcript of Measuring Procurement's Performance

©ALL RIGHTS RESERVED - Confidential 1

Measuring Procurement’s Performance

Peter Smith Wednesday October 17th 2012

Spend Matters UK/Europe

©ALL RIGHTS RESERVED - Confidential 2

• The Real World Sourcing Series is a series of 6 sessions covering hot topics for procurement professionals.

• The Real World Sourcing Series is promoted and supported by BravoSolution, and developed by Peter Smith (Spend Matters) and Guy Allen (4C Associates).

• Peter Smith started his procurement career with Mars Confectionery, then was CPO for Dun & Bradstreet Europe, the Department of Social Security and the NatWest Group. He is now a consultant, author, non-executive director and editor of the Spend Matters website. He was President of CIPS in 2002/3.

Spend Matters UK/Europe Spend Matters UK/Europe Spend Matters UK/Europe

Part 1 - Introduction

©ALL RIGHTS RESERVED - Confidential 3

Measuring Procurement’s Performance October 17th 2012

Agenda

1. Introduction

2. Measuring Savings

3. Other Measures

4. Conclusions

Spend Matters UK/Europe

©ALL RIGHTS RESERVED - Confidential 4

Hypothesis 1

Most organisations focus too strongly on “savings” as a measure of the procurement function’s effectiveness. But that’s a topic for another day really...

Today we will accept that reality

Part 2 – Measuring Savings

©ALL RIGHTS RESERVED - Confidential 5

Hypothesis 2

Procurement is worse than any other business function at measuring its performance in a objective, truthful and credible manner.

Even Marketing does it better!* They measure:

• Market share

• Response to adverts, websites etc.

• Consumer awareness – prompted / unprompted

• Brand equity

All pretty genuine measures. What are our equivalents?

(*Guy Allen disagrees!)

Part 2 – Measuring Savings

©ALL RIGHTS RESERVED - Confidential 6

Hypothesis 3

Most procurement functions deliberately deceive their bosses in terms of how they choose and apply the measurement methodology

There are many, many ways of doing this.

Here are just twelve......

Part 2 – Measuring Savings

©ALL RIGHTS RESERVED - Confidential 7

1. Carry forward savings from previous years to smooth the

profile.

2. Count the same savings year after year after year..

3. Move business to an outsourcer and claim ‘benchmarked’

savings against the market (even if prices are higher than those

you paid previously)!

4. Claim savings against your own market ‘benchmarks’, defined

as you choose.

5. Set a high commodity–specific inflation rate then beat it (e.g.

Facilities Management – assume 5% inflation; we only paid 3%, so

2% saving).

Falsifying Procurement Savings – part 1

©ALL RIGHTS RESERVED - Confidential 8

6. Take advantage of market prices naturally reducing e.g. most

technology (although this can be a genuine ‘saving’, it is passive,

not active.)

7. Claim sourcing savings even if more quantity bought and overall

spend rises (buy 1100 PCs at £800 instead of 800 at £1000 and

claim a ‘saving’ of 1100 x £200 = £220K although overall spend

has risen by £80K).

8. Claim demand management savings even if unit price and

therefore overall spend has increased (e.g. buy 800 printers at

£1100 rather than 1000 at £800 and claim a ‘saving’ of 200 x

£1100 = £220K although overall spend has risen by £80K again!)

Falsifying Procurement Savings – part 2

©ALL RIGHTS RESERVED - Confidential 9

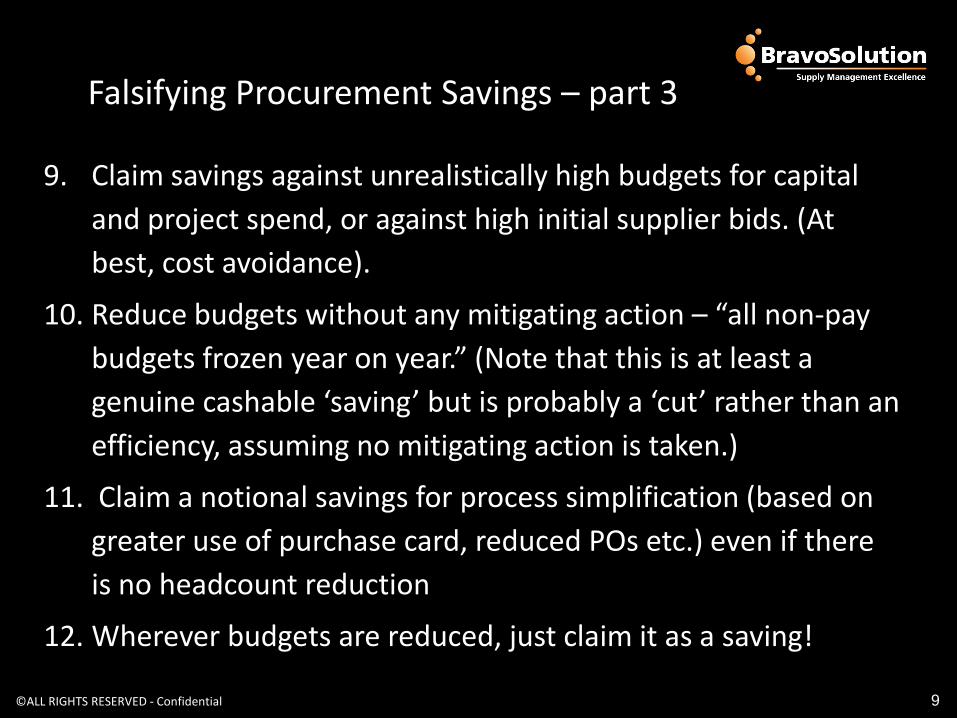

9. Claim savings against unrealistically high budgets for capital

and project spend, or against high initial supplier bids. (At

best, cost avoidance).

10. Reduce budgets without any mitigating action – “all non-pay

budgets frozen year on year.” (Note that this is at least a

genuine cashable ‘saving’ but is probably a ‘cut’ rather than an

efficiency, assuming no mitigating action is taken.)

11. Claim a notional savings for process simplification (based on

greater use of purchase card, reduced POs etc.) even if there

is no headcount reduction

12. Wherever budgets are reduced, just claim it as a saving!

Falsifying Procurement Savings – part 3

©ALL RIGHTS RESERVED - Confidential 10

What process will be used

Last year as the Category Manager I bought 50,000 standard

cartons at a total cost of £5000.

• This year we’ve found a new specification that uses 10% less

raw material.

• But the dollar (pulp is priced in $ on the world market)

appreciated 5% against the £

• The pulp market weakened by 20% because of global

recession

• We bought 100,000 cartons and our total cost was £8,000.

HOW DID I DO? HOW MUCH HAVE I “SAVED”?

Exercise

©ALL RIGHTS RESERVED - Confidential 11

• Different expenditure types should be treated

differently in terms of measuring and capturing

savings

• The two main dimensions are:

– Is it Capital Expenditure or Operating Expenditure

– Is it a recurring spend (i.e. basically the same year after

year) or a one-off spend?

Different types of Expenditure

©ALL RIGHTS RESERVED - Confidential 12

How do we choose which? Spend Types

Unique consulting projects “Emergency” activities

Direct materials Packaging Office supplies Facilities management Outsourced services

Construction projects Plant and equipment Major IT development

IT equipment “Repeat” construction Factory equipment

Opex

Capex

One-offs

Recurring

©ALL RIGHTS RESERVED - Confidential 13

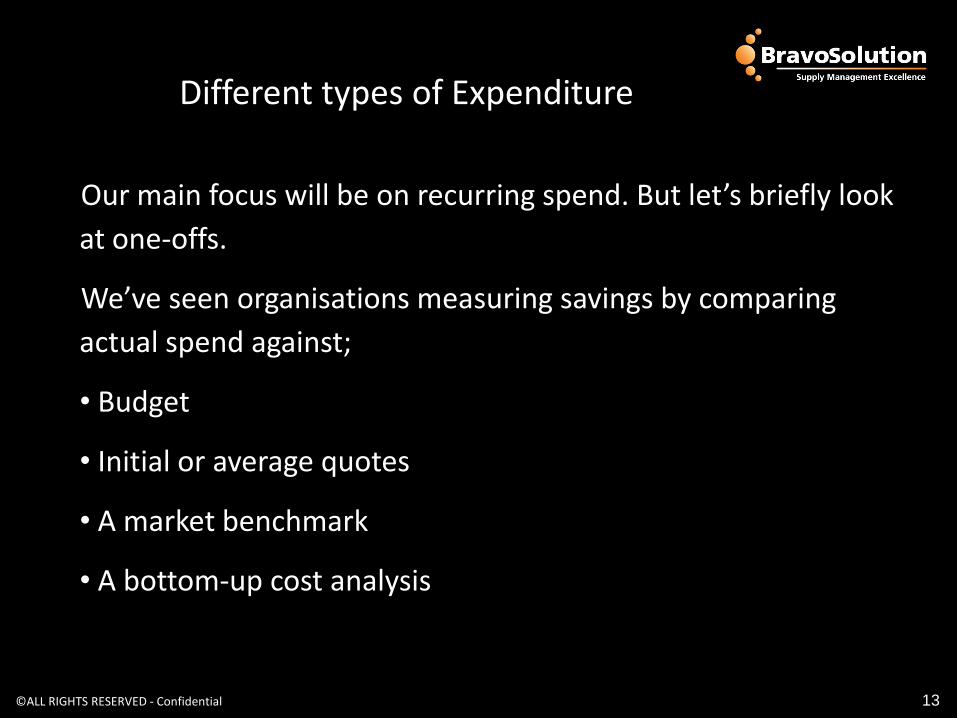

Our main focus will be on recurring spend. But let’s briefly look

at one-offs.

We’ve seen organisations measuring savings by comparing

actual spend against;

• Budget

• Initial or average quotes

• A market benchmark

• A bottom-up cost analysis

Different types of Expenditure

©ALL RIGHTS RESERVED - Confidential 14

Pros and Cons?

Comparing actual spend for one-offs against;

• Budget

• Initial or average quotes

• A market benchmark

• A bottom-up cost analysis

But all of these are essentially cost avoidance rather than

true “savings” – only the “budget” option, if it is at a

granular level and Opex, enables a saving to be tracked to

the P&L

Different types of Expenditure

©ALL RIGHTS RESERVED - Confidential 15

How do we choose which? Measuring “savings”

Track procurement “contribution” but not “savings” – cost avoidance

Feasible to measure procurement savings and identify in P&L

Track contribution against budget / benchmark, not traceable to P&L

Possible to measure procurement savings – but hard to trace in the P&L

Opex

Capex

One-offs

Recurring

©ALL RIGHTS RESERVED - Confidential 16

Recurring Spend

The issue here is not that we don’t have anything definite

to compare against – we do.

We have the previous cost (last month, last year) against

which we can measure the new cost.

The difficulty comes from isolating out the different

influences on the cost so we can see (if we want to) the

true “savings”.

What are those influences?

©ALL RIGHTS RESERVED - Confidential 17

Look at some examples

A number of “value drivers” are (usually) outside the control of

the procurement function. They are:

• Currency

• Volume (quantity used, NOT the economy of scale issue)

• Market movements

Spend data needs to be normalised to take these out of the

equation if we’re going to consider true “procurement savings”

Recurring Spend

©ALL RIGHTS RESERVED - Confidential 18

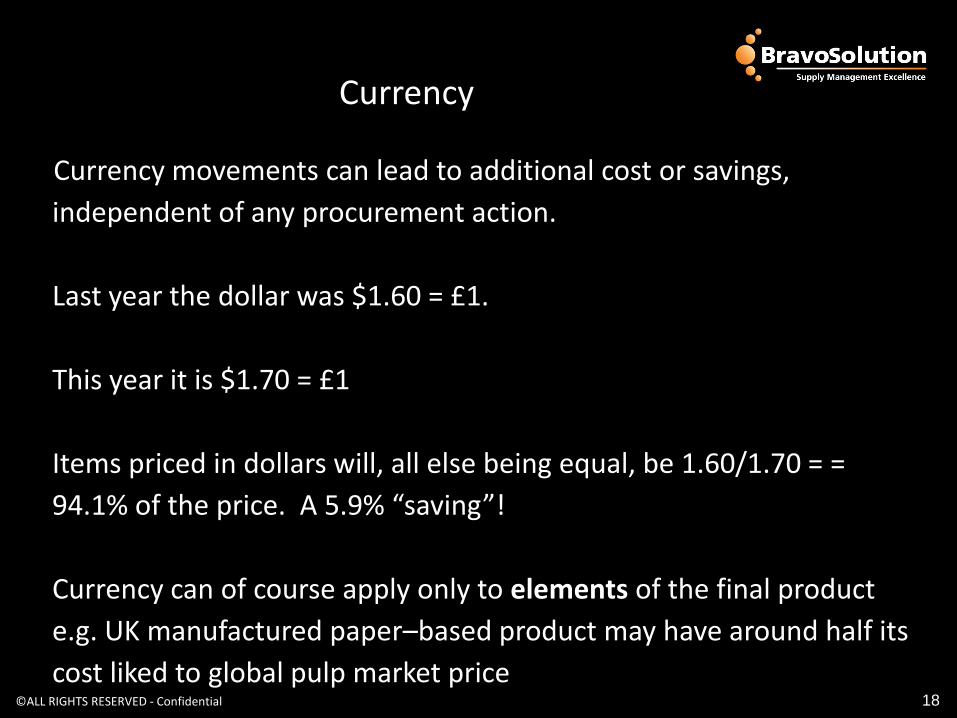

Currency movements can lead to additional cost or savings,

independent of any procurement action.

Last year the dollar was $1.60 = £1.

This year it is $1.70 = £1

Items priced in dollars will, all else being equal, be 1.60/1.70 = =

94.1% of the price. A 5.9% “saving”!

Currency can of course apply only to elements of the final product

e.g. UK manufactured paper–based product may have around half its

cost liked to global pulp market price

Currency

©ALL RIGHTS RESERVED - Confidential 19

OGC Procurement Capability Volume

Greater or less use of a commodity will lead to more or less

money being spent, all else being equal.

Last year we bought 1000 units at £1, so spend was £1000.

This year we bought 900 at £1, so total spend was £900.

The “saving” was 10%.

In terms of reporting, we would argue that a. we need to

know whether this saving affected the wider business and

b. whether the reduction was drive by business or

procurement action (e.g. “demand management”).

©ALL RIGHTS RESERVED - Confidential 20

OGC PCR Output Market

Market price movements will clearly have an affect on prices

and savings.

Last year, the market price for cocoa was (on average) £1500 /

Tonne. This year it is £1350.

Our costs have reduced by 10% - a saving, but one that had

nothing to do with procurement (or anyone else in the

business)

Note - the market price factor may only affect some of the cost

element of the item we’re buying (see currency example).

May still need procurement input to achieve market pricing!

©ALL RIGHTS RESERVED - Confidential 21

Normalisation

Last year we paid £10 per unit for widgets, and we bought 500

units.

The pound has depreciated (weakened) by 10% against the dollar –

widgets are made in Texas and priced in $ on the international

market.

We’ve bought 1000 widgets this year.

The market price of widgets has declined by 5%.

All else being equal, how much would you expect us to have spent

on widgets this year (total) ?

If this year we paid £9 per unit, what is the procurement saving?

©ALL RIGHTS RESERVED - Confidential 22

Normalisation

Last year we paid £10 per unit for widgets, and we bought 500

units. £5000 total spend

The pound has depreciated by 10% against the dollar –

widgets are made in Texas. Expect that to grow to £5500.

We’ve bought twice as many this year. So expect spend of

£11000.

The market price of widgets has declined by 5%. So £11000

would be reduced by 5% or £550

All else being equal, how much would you expect us to have

spent on widgets this year (total) ? £10450 (£11000 - £550)

©ALL RIGHTS RESERVED - Confidential 23

Normalisation

We actually spend 1000 x £9, so our “saving” is £10450 -

£9000 = £1450.

As a percentage of expected spend, that is

£1450 / £10450 = 13.8%

But that doesn't mean 13.8% is necessarily the procurement

contribution of course ....

And some of that may be down to an economy of scale effect

as volume went form 5000 to 10000 units.

©ALL RIGHTS RESERVED - Confidential 24

GOVERNANCE

STRATEGY & LADERSHIP

Commercial Factors

The saving on widgets (outside the normalised factors,

beyond our control) may have come from various actions by

procurement or the business (“strategic levers”):

• Changes in specification

• A change of supplier

• Aggregation or economy of scale

• Pure negotiation

• Other commercial factors

©ALL RIGHTS RESERVED - Confidential 25

Commercial Factors

Once we’ve identified the “real” savings, we might recognise

that they may be driven by procurement, the business,

another function or any combination of the above

So there is another question in terms of reporting – do you

try and allocate the savings across different people / areas?

That has some advantages, but may add another layer of

complexity

On the other hand, not doing so can lead to bad feeling –

“someone claiming credit for my work”!

©ALL RIGHTS RESERVED - Confidential 26

Part 3 – What Should We

Almost another whole topic in itself!

• But important – “what good are your procurement savings if I

can’t see them impacting the bottom line”?

• Less of an issue in a manufacturing (direct materials)

environment.

• Savings will generally come through to the bottom line however

the budgeting and tracking process is carried out (standard

pricing, etc).

Capturing the savings

©ALL RIGHTS RESERVED - Confidential 27

Strategy More challenging with services and discretionary spend.

How do we know the contracts we’ve agreed are actually being

used? (Internal compliance).

How do we know the suppliers are charging the prices and

offering the Ts and Cs we think we've negotiated? (External

compliance).

These factors mean “real” savings are often way out compared

to the procurement savings quoted which are based on

negotiated deals rather than actual spend.

Capturing the savings

©ALL RIGHTS RESERVED - Confidential 28

People

How do we make sure our negotiated savings get captured at

real spend level?

Several options:

• Don’t do anything

• Build savings into next year’s budget

• Real-time adjustment of budgets (in year)

• Build savings into current year (in advance of actual spend)

All of these have pros and cons .....

Capturing the savings

©ALL RIGHTS RESERVED - Confidential 29

Many leading organisations will take a “balanced business

scorecard” approach to measuring procurement, where savings

will just be one factor. Others may include:

• Service and quality factors

• Operational performance

• Added value

• People

Part 3 – Other Measures

©ALL RIGHTS RESERVED - Confidential 30

Governance

Service and quality factors

• Stakeholder satisfaction with procurement

• Quality of goods purchased

• Response to stakeholder queries, turn-around times

• Quality of supplier performance *

* a topic for next year’s Real World Sourcing Series, we suspect!

Other Measures

©ALL RIGHTS RESERVED - Confidential 31

Key processes (e.g. Contract

Operational performance

• Running the function within budget

• Speed and accuracy of processing activities

• Stockholding, delivery and logistics measures

• Invoices matching POs or similar P2P measures

Other Measures

©ALL RIGHTS RESERVED - Confidential 32

Added value

• Spend coverage

• Supplier satisfaction / improved relationships

• Innovation / contribution to top-line

• Risk management – avoidance of major incidents, strength of

process

Other Measures

©ALL RIGHTS RESERVED - Confidential 33

Time-Out: Discussion

People

• Training and development

• Professionalism – e.g. CIPS membership

• Retention

• Staff satisfaction / survey results

Other Measures

©ALL RIGHTS RESERVED - Confidential 34

Improvement Outcomes

Should procurement be judged on how well suppliers

perform?

That would incentivise the function to pay a lot more

attention to contract and supplier management.

A topic for next time – but you might like to reference

some of our thinking in this area.

Supplier Performance Measures

©ALL RIGHTS RESERVED - Confidential 35

Improvement Plans

• Given that measuring “savings” is such an important part of assessing procurement, we really should try and get better at it.

• That means

– different measures & reporting for one offs / recurring spend

– normalising to eliminate purely external factors

– looking to explain the internal strategic drivers

– ensuring savings are captured

• But we should also promote a wider balanced business scorecard approach to measuring procurement’s performance

Conclusions and key messages

©ALL RIGHTS RESERVED - Confidential 36

Conclusions and key

• Decide whether you REALLY want to measure savings

• If you do, make some effort to normalise the data and report in a reasonable manner

• Measure based on actual spend not theoretical “negotiated” prices

• Give the business credit where it is due

• Introduce a wider balanced business scorecard approach and look to reflect where procurement brings value to the organisation

• Move the focus away from purely “savings”

Recommendations

©ALL RIGHTS RESERVED - Confidential 37

• £2500 towards any procurement based training

• Log on to the BravoSolution Education Network with the details you’ll receive tomorrow

• Complete the certification programme

• Check your ranking!

• The winner will be announced at the Sourcing Experts dinner on 19 December

Spend Matters UK/Europe

Real World Sourcing Scholarship

©ALL RIGHTS RESERVED - Confidential 38

THANK YOU!

Please feel free to contact me on

Spend Matters UK/Europe