MARKET ANALYSIS OF WHOLESALE (PHYSICAL) NETWORK INFRASTRUCTURE

152

Croatian Post and Electronic Communications Agency Jurišićeva 13 10000 Zagreb July 2009 MARKET ANALYSIS OF WHOLESALE (PHYSICAL) NETWORK INFRASTRUCTURE ACCESS (INCLUDING SHARED OR FULLY UNBUNDLED ACCESS) AT A FIXED LOCATION

Transcript of MARKET ANALYSIS OF WHOLESALE (PHYSICAL) NETWORK INFRASTRUCTURE

Croatian Post and Electronic Communications Agency

Jurišićeva 13

10000 Zagreb

July 2009

MARKET ANALYSIS OF WHOLESALE

(PHYSICAL) NETWORK

INFRASTRUCTURE ACCESS

(INCLUDING SHARED OR FULLY

UNBUNDLED ACCESS) AT A FIXED

LOCATION

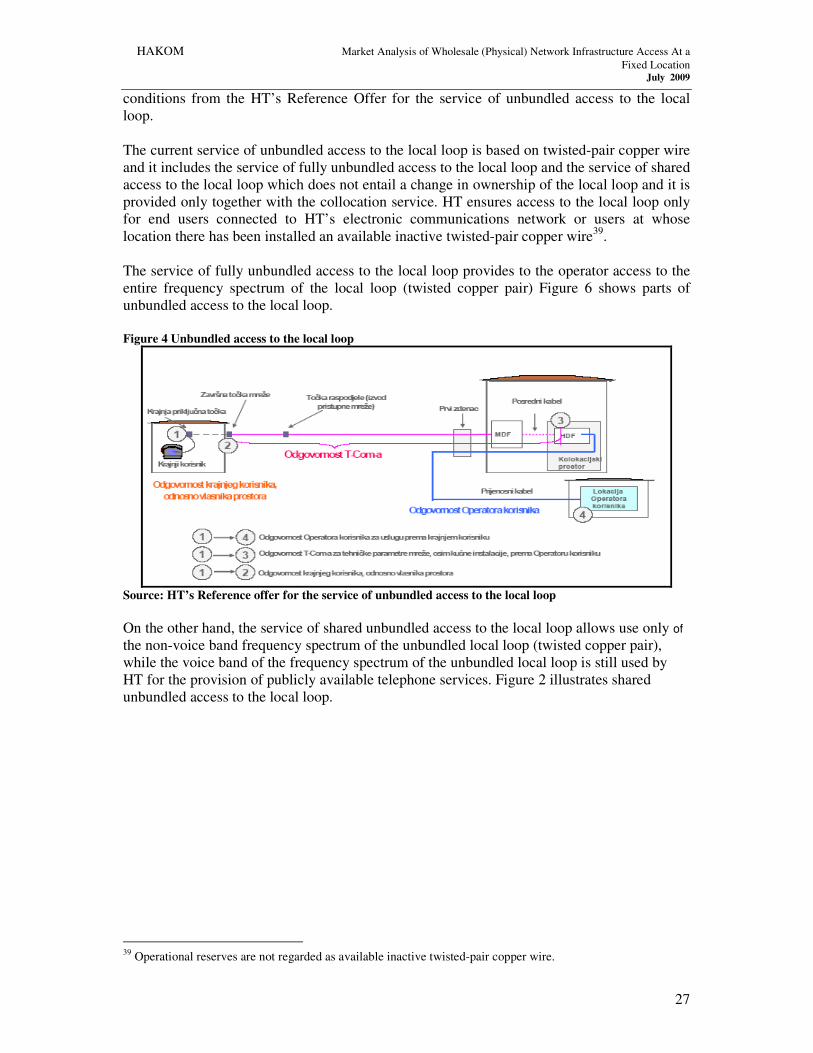

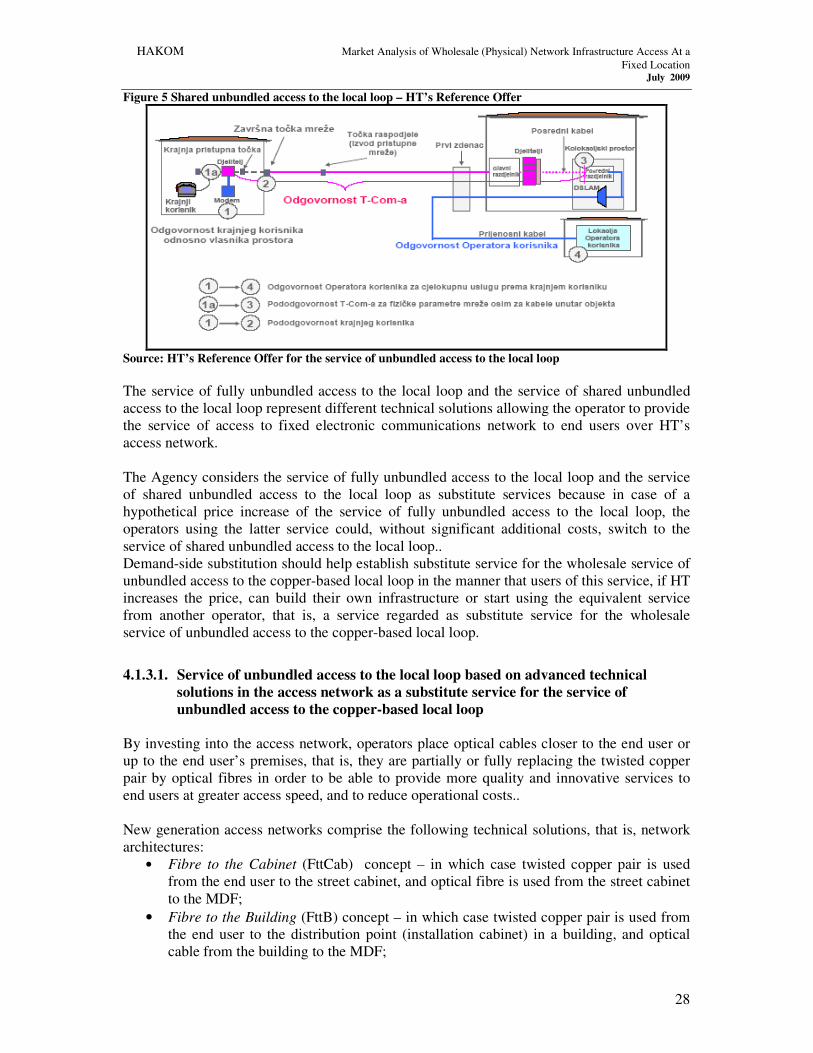

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

2

1. Executive Summary .....................................................................................................4

2. Introduction .................................................................................................................6 2.1. European Regulatory Framework for Electronic Communications ..............................6

2.2. Electronic Communications Act..................................................................................7

2.3. Chronology of activities..............................................................................................9

3. Identification of the Relevant Market.......................................................................11

4. Definition of a Relevant Market................................................................................12 4.1. Relevant market in the dimension of services............................................................12

4.1.1. Retail market of broadband Internet access ....................................................13

4.1.2. Demand-side substitution- retail level ............................................................13

4.1.2.1. xDSL access over twisted-pair copper wire ...........................................14

4.1.2.1.1 ADSL access over twisted-pair copper wire .........................................14

4.1.2.1.1 VDSL access over twisted-pair copper wire .........................................17

4.1.2.2. Access over mobile networks ................................................................18

4.1.2.3. Fixed wireless access.............................................................................21

4.1.2.3.1 Fixed wireless access over the Homebox service..................................21

4.1.2.3.2 Fixed wireless access over the WiMAX technology.............................22

4.1.2.3.3 Fixed wireless access over the HotSpot service....................................23

4.1.2.4. Access over cable networks ...................................................................23

4.1.2.5. Access over leased lines ........................................................................25

4.1.2.6. Access over optical fibre .......................................................................25

4.1.2.7. Conclusion ............................................................................................26

4.1.3. Demand-side substitution – wholesale level ...................................................26

4.1.3.1. Service of unbundled access to the local loop based on advanced

technical solutions in the access network as a substitute service for the

service of unbundled access to the copper-based local loop ...................28

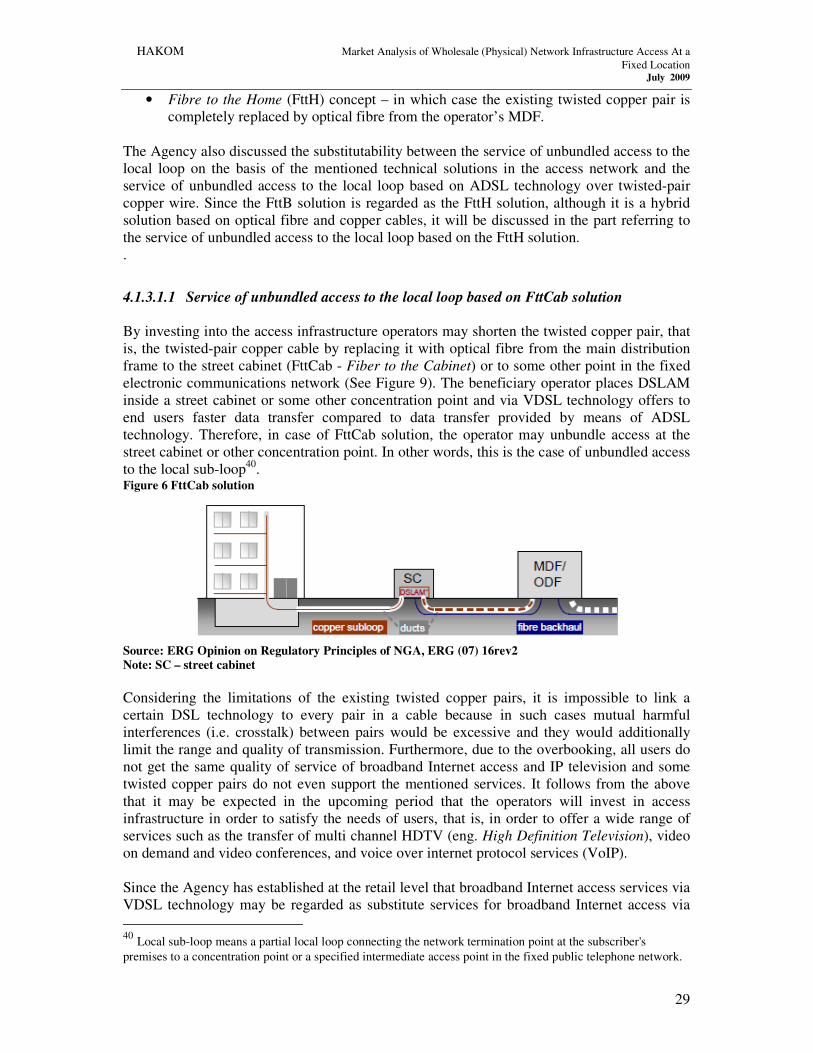

4.1.3.1.1 Service of unbundled access to the local loop based on FttCab solution29

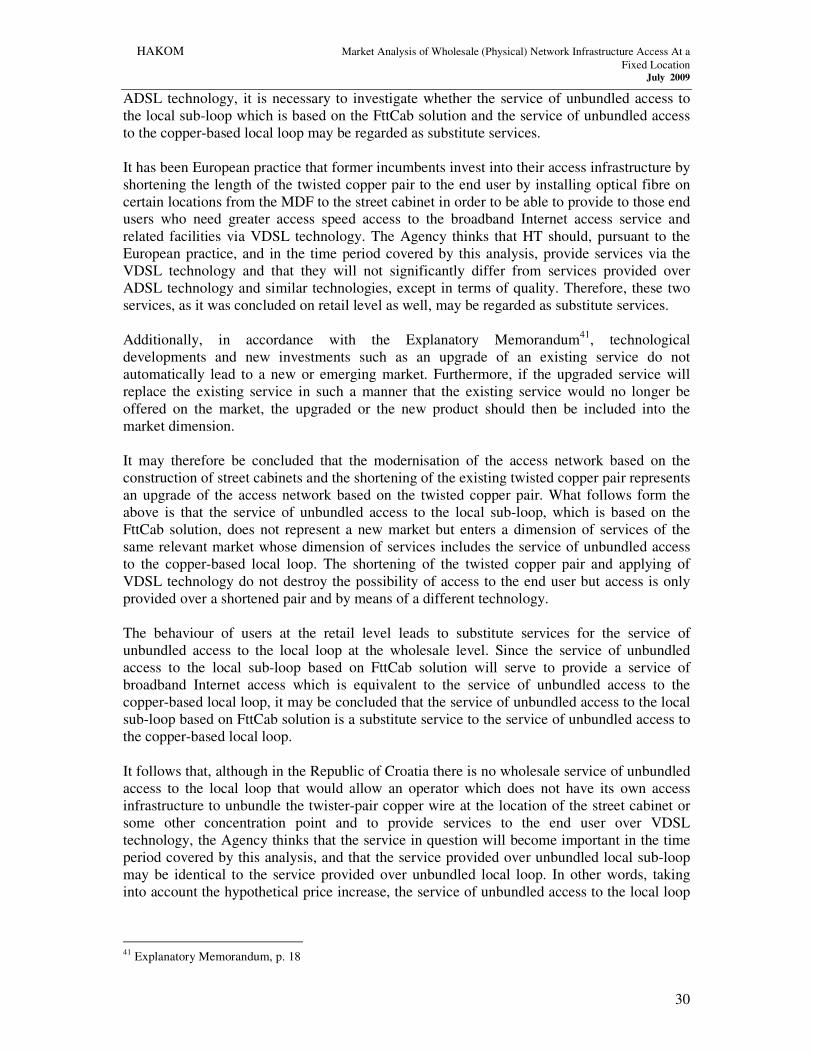

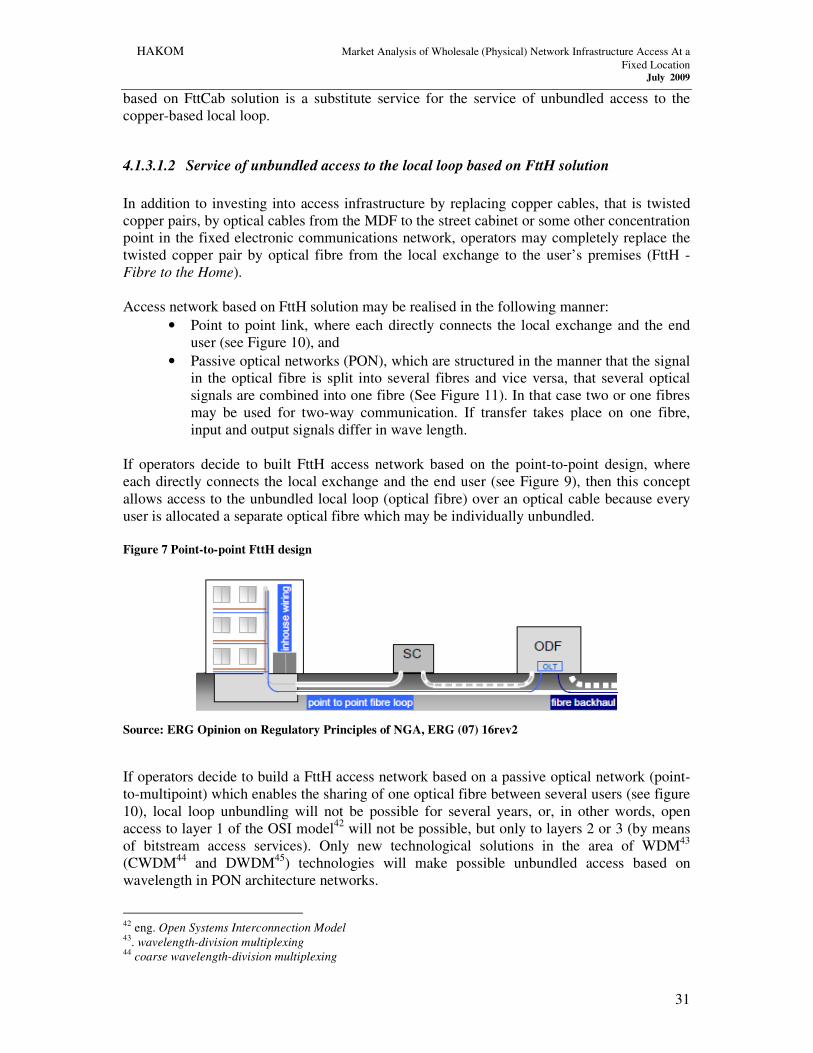

4.1.3.1.2 Service of unbundled access to the local loop based on FttH solution...31

4.1.3.2. Bitstream service as a substitute service for the service of unbundled

access to the local loop ..........................................................................34

4.1.3.3. Building own infrastructure as a substitute service for the service of

unbundled access to the local loop.........................................................36

4.1.3.4. Broadband Internet access service for self-supply as a substitute service

for the service of unbundled access to the local loop..............................36

4.1.4. Supply-side substitution.................................................................................38

4.1.5. Collocation service ........................................................................................38

4.1.6. Conclusion on the relevant market in the dimension of services.....................39

4.2. Relevant market in the geographical dimension.........................................................40

4.3. Opinion of the competent regulatory authority on the definition of the relevant market

.................................................................................................................................40

5. Objective and Subject of Market Analysis ...............................................................41 5.1. Market share of an operator on the relevant market ...................................................41

5.2. Control of infrastructure in case of significant problems for infrastructure competition

.................................................................................................................................43

5.3. Economies of scale ...................................................................................................44

5.4. Economies of scope ..................................................................................................44

5.5. Lack of countervailing buying power ........................................................................45

5.6. Level of vertical integration ......................................................................................45

5.7. Conclusion on the assessment of the existence of operators with significant market

power and the evaluation of effectiveness of competition .........................................46

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

3

6. Competition Problems ...............................................................................................47 6.1. Market dimension of competition problems ..............................................................48

6.1.1. Vertical leveraging ........................................................................................48

6.1.2. Horizontal leveraging ....................................................................................48

6.1.3. Single market dominance...............................................................................49

6.1.4. Call termination.............................................................................................49

6.2. Cause-and-effect type of dimension of competition problems....................................49

6.3. Overview of competition problems recognised in the European practice ...................50

6.4. Competition problems on the market of wholesale network infrastructure access

(including shared or fully unbundled access) at a fixed location................................51

6.4.1. Refusal to deal/denial of access......................................................................52

6.4.2. Leveraging by means of non-price variables ..................................................54

6.4.2.1. Discriminatory use or withholding of information .................................54

6.4.2.2. Delaying tactics.....................................................................................54

6.4.2.3. Undue requirements ..............................................................................55

6.4.2.4. Undue use of information about competitors..........................................56

6.4.2.5. Quality discrimination ...........................................................................56

6.4.2.6. Other types of discrimination currently defined in the Annex to the

Reference Offer for the service of unbundled access to the local loop....57

6.4.3. Leveraging by means of pricing.....................................................................57

6.4.3.1. Price discrimination...............................................................................57

6.4.3.2. Cross subsidisation ................................................................................59

7. Regulatory Obligations of the SMP Operator ..........................................................60 7.1. Regulatory obligations imposed on the SMP operator on the market of wholesale

(physical) network infrastructure access (including shared or fully unbundled access)

at a fixed location .....................................................................................................60

7.1.1. Obligation of access to, and use of, specific network facilities .......................61

7.1.2. Obligation of non-discrimination ...................................................................73

7.1.3. Obligation of transparency.............................................................................75

7.1.4. Price control and cost accounting obligation ..................................................81

7.1.5. Obligation of accounting separation...............................................................92

7.1.6. Other regulatory obligations that might be imposed by the Agency on the

market of wholesale (physical) network infrastructure access (including shared

or fully unbundled access) at a fixed location, pursuant to ECA.....................95

8. Annexes ...........................................................................................................................96 8.1 . Annex A – Opinion of the Croatian Competition Agency........................................96

8.2 Annex B – Comments on the market of wholesale (physical) network infrastructure

access (including shared or fully unbundled access) at a fixed location and the

Agency’s reply to the delivered comments................................................................98

8.2.1 Answers to comments made by HT-Hrvatske telekomunikacije d.d. ..............98

8.2.2 Answers to VIPnet’s comments ...................................................................131

8.2.3 Answers to comments made by H1 Telekom ...............................................136

8.2.4 Answers to comments made by OT-Optima Telekom ..................................143

8.2.5 The Agency’s comments..............................................................................150

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

4

1. Executive Summary

The European directives have been implemented into Croatian legislation through the

Electronic Communications Act1 which entered into force on 1 July 2008. The Electronic

Communications Act, among other things, lays down conditions for the provision of

electronic communications networks and services. Through the application of the provisions

of this Act, the Agency2 creates conditions for efficient competition, that is, it allows all

operators active in electronic communications markets to do their business under equal

conditions.

While carrying out the market analysis procedure provided for in Article 52 of the ECA, the

Agency paid particular attention to apply the relevant European Commission

Recommendation on Relevant Markets Susceptible to Ex-Ante Regulation3 and the relevant

European Commission guidelines on market analysis and assessment of significant market

power under the Community regulatory framework for electronic communications networks

and services4.

The main objective of the market analysis procedure is to establish the existence of efficient

competition in a certain market or whether there are one or more operators on that market

with single or joint significant market power. The results of the analysis will serve to impose,

alter, maintain or withdraw regulatory obligations laid down in Article 58 to 65 of the ECA.

Pursuant to Article 53, paragraph 1 of the ECA, the Agency has established the market of

wholesale (physical) network infrastructure access (including shared or fully unbundled

access) at a fixed location as a relevant market susceptible to ex-ante regulation. The

mentioned market is a part of the relevant European Commission Recommendation on

Relevant Markets Susceptible to Ex-Ante Regulation, which means that the European

Commission concluded that the three criteria referred to in Article 53, paragraph 2 of the ECA

have been cumulatively met in the relevant market.

The identification of the relevant market is a basis for market analysis which consists of the

definition of the relevant market and the assessment of the existence of one or more operators

with significant market power on this market followed by the imposition of regulatory

obligations on operators with significant market power.

The purpose of the process of the definition of a relevant market is to identify restrictions, that

is, problems faced by electronic communications networks operators on a certain market. In

the process of the definition of a relevant market, that is, of market boundaries, the Agency

has defined the dimension of services and the geographical dimension of the relevant market

and on the basis of the results of the conducted analysis it identified the above-mentioned

relevant market.

On the basis of the conducted analysis, the Agency has concluded that the relevant wholesale

broadband access market comprises the following:

1 Electronic Communications Act (OG 73/08)

2 Croatian Post and Electronic Communications Agency (HAKOM) 3 OJ L 344/65; 28 December 2007

4 OJ C 165/6; 11/7/ 2002

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

5

On the basis of the conducted analysis, the Agency has concluded that the relevant wholesale

(physical) network infrastructure access (including shared or fully unbundled access) at a

fixed location comprises the following services:

• Service of fully unbundled access to the copper-based local loop and the copper-based local sub-loop which enables the operator to use the entire frequency spectrum

of the local loop,

• Service of shared unbundled access to the copper-based local loop and the copper-based local sub-loop enables the operator to use only the non-voice band of

the frequency spectrum of the unbundled local loop or the local sub-loop (twisted

copper pair), while the voice band of frequency spectrum of the local loop or the local

sub-loop is still used by HT to provide publicly available telephone service,

• Service of unbundled access to the fibre local loop by means of point to point link,

• Service of access to network infrastructure provided by HT for self-supply regardless of whether access technology is based on twisted copper pair, a hybrid

solution including both twisted copper pair and optical fibre, or on the basis of optical

fibre;

• Collocation service, which includes physical, distant and virtual location.

The Agency has also determined that the relevant market of wholesale (physical) network

infrastructure access (including shared or fully unbundled access) at a fixed location in the

geographical dimension is the national territory of the Republic of Croatia.

After having identified the relevant market, the Agency has, on the basis of criteria necessary

for the assessment of significant market power of operators as laid down in Article 55,

paragraph 5 of the ECA, established the following:

• HT d.d. is an operator with significant market power on the market of wholesale

(physical) network infrastructure access (including shared or fully unbundled access)

at a fixed location.

After having identified HT as the operator with significant market power, the Agency has

imposed on HT as the SMP operator the following regulatory obligations in view of problems

that may appear in the market of wholesale (physical) network infrastructure access

(including shared or fully unbundled access) at a fixed location and in the downstream retail

market onto which the operator with significant market power may leverage its significant

market power:

• Obligation of access to, and use of, specific network facilities;

• Obligation of non-discrimination;

• Obligation of transparency and the obligation to publish the reference offer for the

service of unbundled access to the local loop and related facilities;

• Price control and cost-accounting obligations;

• Obligation of accounting separation.

Pursuant to Article 54, paragraph 5 of the ECA, the Agency asked for an opinion of the

Croatian Competition Agency on the manner in which the Agency has defined the relevant

market and designated the operator with significant market power on that market. The opinion

is enclosed to this document in Chapter 8.1 “Annex A” of this document.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

6

2. Introduction

2.1. European Regulatory Framework for Electronic Communications

In March 2002, the European Commission adopted four directives representing the 2002

Regulatory Framework for Electronic Communications Networks and Services, and the fifth

directive, which also represents the Regulatory Framework, was adopted in October 2002.

The previously mentioned directives are the following:

• Directive 2002/19/EC of the European Parliament and of the Council of 7 March 2002

on access to, and interconnection of, electronic communications networks and

associated facilities (Access Directive)

• Directive 2002/20/EC of the European Parliament and of the Council of 7 March

2002 on the authorisation of electronic communications networks and services

(Authorisation Directive)

• Directive 2002/21/EC of the European Parliament and of the Council of 7 March 2002

on a common regulatory framework for electronic communications networks and

services (Framework Directive)

• Directive 2002/22/EC of the European Parliament and of the Council of 7 March 2002

on universal service and users' rights relating to electronic communications networks

and services (Universal Service Directive)

• Directive 2002/58/EC of the European Parliament and of the Council of 12 July 2002

concerning the processing of personal data and the protection of privacy in the

electronic communications sector (Directive on privacy and electronic

communications)

The intention of the European Commission directives is to promote harmonisation in the field

of electronic communications in all Member States of the European Union.

On the basis of the first paragraph of Article 15 of the Framework Directive (Directive

2002/21/EC), the European Commission adopted the following:

• Recommendation 2003/311/EC of 11 February 2003 on relevant product and service

markets within the electronic communications sector susceptible to ex ante

regulation5, which was in force until December 2007 when it was replaced by

• Recommendation 2007/879/EC of 17 December 2007 on relevant product and service

markets within the electronic communications sector susceptible to ex ante regulation.

The relevant Recommendation from February 2003 recognised 18 markets susceptible to ex

ante regulation meaning that the European Commission concluded that three criteria were

cumulatively met in the relevant markets (The Three Criteria Test), and it thus concluded that

the relevant markets were susceptible to ex-ante regulation in the majority of the European

5 OJ L 114/45; 08/05/ 2003

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

7

Union Member States. The previous Recommendation on relevant markets was amended in

such a manner that the new Recommendation on relevant markets recognises 7 relevant

markets susceptible to ex ante regulation instead of the previous 18. Markets which are no

longer a constituent part of the Recommendation on relevant markets may still be regulated

by national regulatory authorities provided that they prove that the three criteria have been

cumulatively met on these markets (The Three Criteria Test).

The intention of the Recommendation on relevant markets is to promote harmonisation in the

electronic communications sector by making equivalent products and services subject to

market analysis in all Member States of the European Union. However, national regulatory

authorities of Member States are authorised to determine on their own that certain markets,

different from those on the list of markets in the valid Recommendation, are susceptible to ex

ante regulation, depending on the situation in each individual country provided that they

prove that three criteria have been cumulatively met in these markets (The Three Criteria

Test).

2.2. Electronic Communications Act

The previously mentioned directives have been implemented into Croatian legislation through

the ECA which, among other things, lays down the conditions for the provision of electronic

communications networks and services. By applying the provisions of ECA, the Agency

ensures conditions for efficient competition, that is, it allows all operators active in electronic

communications markets to operate under equal conditions.

While carrying out the market analysis procedure provided for in Article 52 of the ECA, the

Agency paid particular attention to apply the relevant European Commission

Recommendation on Relevant Markets Susceptible to Ex-Ante Regulation and the relevant

European Commission guidelines on market analysis and assessment of significant market

power under the Community regulatory framework for electronic communications networks

and services.

The main objective of the market analysis procedure is to establish the existence of efficient

competition in a certain market or whether there are one or more operators on that market

having single or joint significant market power. The results of the analysis or the Three

Criteria Test will serve to impose, alter, maintain or withdraw regulatory obligations laid

down in Articles 58 to 65 of the ECA.

The 2002 Regulatory Framework which has been implemented in the European Union

Member States and in Croatian legislation through the ECA, provides for a three-step market

analysis procedure:

1. The first step refers to the process of identification of relevant markets susceptible to ex

ante regulation pursuant to Article 53 of the ECA.

Pursuant to the first paragraph of Article 15 of the Framework Directive (Directive

2002/21/EC), the European Commission adopted Recommendation 2003/311/EC of 11

February 2003 on relevant product and service markets within the electronic

communications sector susceptible to ex ante regulation. The mentioned relevant

Recommendation recognised 18 markets susceptible to ex ante regulation meaning that

the European Commission concluded that three criteria were cumulatively met on the

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

8

relevant markets (The Three Criteria Test), and it thus concluded that the relevant markets

were susceptible to ex-ante regulation in the majority of the European Union Member

States.

On the basis of the new Recommendation of 17 December 2007 on relevant products and

service markets within the electronic communications sector susceptible to ex ante

regulation, the previous Recommendation was amended in such a manner instead of 18 it

recognises 7 relevant markets susceptible to ex ante regulation. Markets which are no

longer a constituent part of the Recommendation on relevant markets may still be

regulated by national regulatory authorities provided that they prove that the three criteria

have been cumulatively met in these markets (The Three Criteria Test).

The Electronic Communications Act entered into force in the Republic of Croatia on 1

July 2008, and Article 52, paragraph 4 of the ECA reads that the Agency shall, when

carrying out the procedures for identification of relevant markets susceptible to ex ante

regulation, take particular account of the application of the relevant Commission’s

Recommendation on relevant markets. Since the relevant Recommendation on relevant

markets in force is the one which entered into force on 28 December 2007 and which

recognises 7 markets susceptible to ex-ante regulation, the Agency may, without proving

the cumulative satisfaction of the three criteria (the Three Criteria Test), carry out ex ante

regulation only in these 7 markets.

At the same time, in accordance with Article 53, paragraph 2 of the ECA, the Agency may

adopt a decision establishing that other relevant markets, in addition to relevant markets

referred to in the European Commission recommendation, are susceptible to ex ante

regulation provided that the following three criteria have been cumulatively met in these

markets:

1. the presence of high and non-transitory market entry barriers of structural, legal or

regulatory nature;

2. market structure which does not aim towards the development of effective competition

within a certain time framework;

3. the application of relevant competition legislation alone does not make possible the

elimination of market entry failures concerned.

However, if all three criteria referred to in Article 53, paragraph 2 of the ECA have been

cumulatively satisfied, the Agency may carry out ex ante regulation of the remaining 11

markets that formed a constituent part of the old Recommendation on relevant markets.

The Agency also may also, provided that all three criteria referred to in Article 53,

paragraph 2 of the ECA have been cumulatively satisfied, regulate markets following

from the Telecommunications Act6 or any other markets which are specific for the

electronic communications networks and services sector in the Republic of Croatia but do

not follow from the old Recommendation on relevant markets or the Telecommunications

Act.

The market of „Wholesale (physical) network infrastructure access (including shared or

fully unbundled access) at a fixed location“, which is the subject of this document, was

6 The Telecommunications Act which was in force in the Republic of Croatia until 1 July 2008, and was based

on the 1998 Regulatory Framework. The mentioned Act recognised 4 relevant markets: interconnection market,

leased-lines market, fixed public telephone networks services market and market of public voice service in

mobile telecommunications networks.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

9

the 11th

of the 18 relevant markets mentioned in the old Recommendation on relevant

markets. In the new Recommendation on relevant markets the market in question in the 4th

of the 7 relevant markets mentioned in this Recommendation. In accordance with the

above, this market is still susceptible to ex ante regulation and the Agency may carry out

ex ante regulation of this market and thus identify the relevant market in question without

proving that the three criteria referred to in Article 53, paragraph 2 of the ECA have been

cumulatively met.

2. In the second step the Agency carries out a market analysis consisting of the definition

of the relevant market and the assessment of the existence of a single or multiple

operators with significant market power on that relevant market in order to assess the

effectiveness of competition on that relevant market pursuant to Article 54 of the ECA and

Article 55 of the ECA.

In order to establish the relevant market pursuant to Article 54 of the ECA, the Agency

shall determine the dimension of services and the geographical market dimension taking

into account the relevant European Commission Guidelines on market analysis and the

assessment of significant market power under the Community regulatory framework for

electronic communications networks and services and the relevant European Union acquis

communautaire in the competition protection sector.

After having identified the relevant market, the Agency shall, in cooperation with the

Croatian Competition Agency, asses the effectiveness of competition on that market.

After having assessed the efficiency of competition in this market, the Agency will, if

there is no effective competition and pursuant to Article 55 of the ECA, assess whether

there is, on this market, an operator with significant market power or operators with

significant market power.

If, on the basis of market analysis, the Agency establishes that there is no effective

competition on the relevant market, it shall, as part of the third step, adopt a decision

pursuant to Article 56 of the ECA on the designation of operators with significant market

power on that relevant market. By this decision the Agency will impose at least one

regulatory obligation referred to in Articles 58 to 65 of the ECA to every operator.

2.3. Chronology of activities

After the entry into force of the ECA on 1 July 2008, the Agency’s Council, on its session

held on 9 July 2008 adopted a decision7 determining operators who are obliged to submit all

data necessary for the definition and analysis of the market of wholesale (physical) network

infrastructure access (including shared or fully unbundled access) at a fixed location.

In the above-mentioned decision, the Agency’s Council determined that the following

operator is obliged to submit all necessary data:

• HT-Hrvatske telekomunikacije d.d., Savska cesta 32, 10000 Zagreb

7 Class: UP/I-344-01/08-01/1584; Reg. No. 376-11-08-01

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

10

In order to collect all the necessary data, the Agency prepared, on the basis of its own

assumptions and experiences from European Union Member States, a special questionnaire

for the market of wholesale (physical) network infrastructure access (including shared or fully

unbundled access) at a fixed location. The Agency prepared the questionnaire in such a

manner that it tried to cover all the peculiarities of the market in question while also taking

into account the best European practice. In order to get a quality questionnaire, the Agency

included HT in the preparation of the questionnaire at the meeting held on 3 July 2008. Data

requested in the above-mentioned questionnaire refer to the time period comprising the

second half of 2005, the whole of 2006 and 2007, and the first half of 2008.

In accordance with the decision of the Agency’s Council of 9 July 2008, the Agency sent the

questionnaire to HT on 16 July 2008. HT was asked to complete and return the questionnaire

to the Agency, both in written and electronic form, by 19 September 2008. HT returned the

completed questionnaire on 6 October 2008 after having asked the extension of the deadline

by an official letter of 18 September 2008.

Upon receipt of the questionnaire, the Agency initiated a detailed analysis of the relevant

market of wholesale (physical) network infrastructure access (including shared or fully

unbundled access) at a fixed location. Furthermore, after the receipt and the analysis of the

submitted data, bearing in mind the importance of the initiated procedure, and in order to

eliminate all possible ambiguities related to the submitted data, the Agency sent a memo on

13 November 20088 asking HT for additional clarifications and/or data which have not been

submitted but are important for further analysis of the relevant market. The set deadline was

28 November 2008.

The Agency took into account the delivered additional clarifications and/or data which had

not been delivered before and continued with the detailed analysis of the relevant market of

wholesale (physical) network infrastructure access (including shared or fully unbundled

access) at a fixed location.

For the purposes of analysis of this relevant market, the Agency also used data from the

questionnaire for broadband Internet access market.

8 Class: UP/I-344-01/08-01/1585; Reg.No: 376-11-08-25

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

11

3. Identification of the Relevant Market

The Croatian Post and Electronic Communications Agency is a national regulatory agency

carrying out regulatory and other tasks within the scope and competences laid down in the

Electronic Communications Act. Among other things, the Agency is competent for

competition in electronic communications, and, pursuant to Article 53, paragraphs 1 and 2 of

the ECA it adopts a decision identifying relevant markets susceptible to ex ante regulation.

On the basis of Article 53, paragraph 1 of the ECA, the Agency identifies relevant markets

susceptible to ex ante regulation while taking into account the relevant European Commission

Recommendation mentioned in Article 54, paragraph 4 of the ECA.

At the same time, in accordance with Article 53, paragraph 2 of the ECA, the Agency may

adopt a decision establishing that other relevant markets, in addition to relevant markets

referred to in the European Commission Recommendation, are susceptible to ex ante

regulation provided that the following three criteria have been cumulatively met in these

markets:

1. the presence of high and non-transitory market entry barriers of structural, legal or

regulatory nature;

2. market structure which does not aim towards the development of effective competition

within a certain time framework;

3. the application of relevant competition legislation alone does not make possible the

elimination of market entry failures concerned.

Pursuant to Article 53, paragraph 1 of the ECA, the Agency’s Council adopted a decision 9

identifying a relevant market of:

• Wholesale (physical) network infrastructure access (including shared or fully unbundled access) at a fixed location

10.

The mentioned market is a part of the recommendation in force, which means that the

European Commission concluded that the mentioned three criteria have been cumulatively

satisfied in the relevant market and thus established that the relevant market is susceptible to

ex ante regulation in the majority of EU Member States.

The identification of the relevant market is a basis for market analysis which consists in the

definition of the relevant market, the assessment of the existence of single or multiple

operators with significant market power in that market and the imposition of regulatory

obligations on SMP operators, which is described in detail in the following chapters.

9 Decision on relevant markets susceptible to ex ante regulation (Class: UP/I-344-01/08-01/1582; Reg. No: 376-

11-08-01) 10

Market No. 4 from the Annex to the European Commission Recommendation on relevant markets susceptible

to ex ante regulation

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

12

4. Definition of a Relevant Market

In order to define a relevant market, the Agency determines a dimension of services and a

geographical dimension of the relevant market taking into account the relevant European

Commission Guidelines on market analysis and the assessment of significant market power

and the relevant acquis communautaire in the competition sector.

According to the European Commission Guidelines, the assessment of behaviour of operators

on the market requires the taking into account of demand-side substitution and supply-side

substitution. In addition to the mentioned competition problems, it is necessary to assess the

existence of potential competition as well. The difference between potential competition and

supply-side substitution lies in the fact that supply-side substitution responds promptly to a

price increase whereas potential competitors may need more time before starting to supply the

market with the equivalent service. Furthermore, supply substitution involves no additional

significant costs whereas potential entry occurs at significant sunk costs11

.

Demand-side substitutability is used to establish services which are regarded as substitutes by

consumers whereas supply-side substitutability indicates the readiness of suppliers in the

immediate to short term offer the equivalent service without incurring significant additional

costs.

One possible way of assessing the existence of any demand and supply-side substitution is to

apply the so-called ‘hypothetical monopolist test12

. This test is used to study what would

happen in case of a small but significant, lasting increase in the price of a given product or

service, assuming that the prices of all other products or services remain constant whereby a

permanent price increase of between 5 and 10% is taken into account.

4.1. Relevant market in the dimension of services

Neither the Recommendation which is now in force nor the former one recognised the retail

broadband Internet market as a market susceptible to ex ante regulation. The European

Commission feels that efficient regulation at wholesale level may ensure competition at the

retail level.

However, since the demand for the service of wholesale (physical) network infrastructure

access (including shared or fully unbundled access) at a fixed location the Agency believed it

would be appropriate when determining the dimension of services of the relevant market of

wholesale (physical) network infrastructure access (including shared or fully unbundled

access) at a fixed location to define substitute services at the wholesale market by studying the

ways in which operators at the retail market provide the service of broadband internet access

to end users whilst taking into account future market development

.

For the purpose of providing broadband Internet access services at the retail level, operators

either have their own infrastructure or use wholesale services of other operators to ensure

access to the end user.

11

eng. sunk costs 12

SSNIP test – eng. small but significant non transitory increase in price

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

13

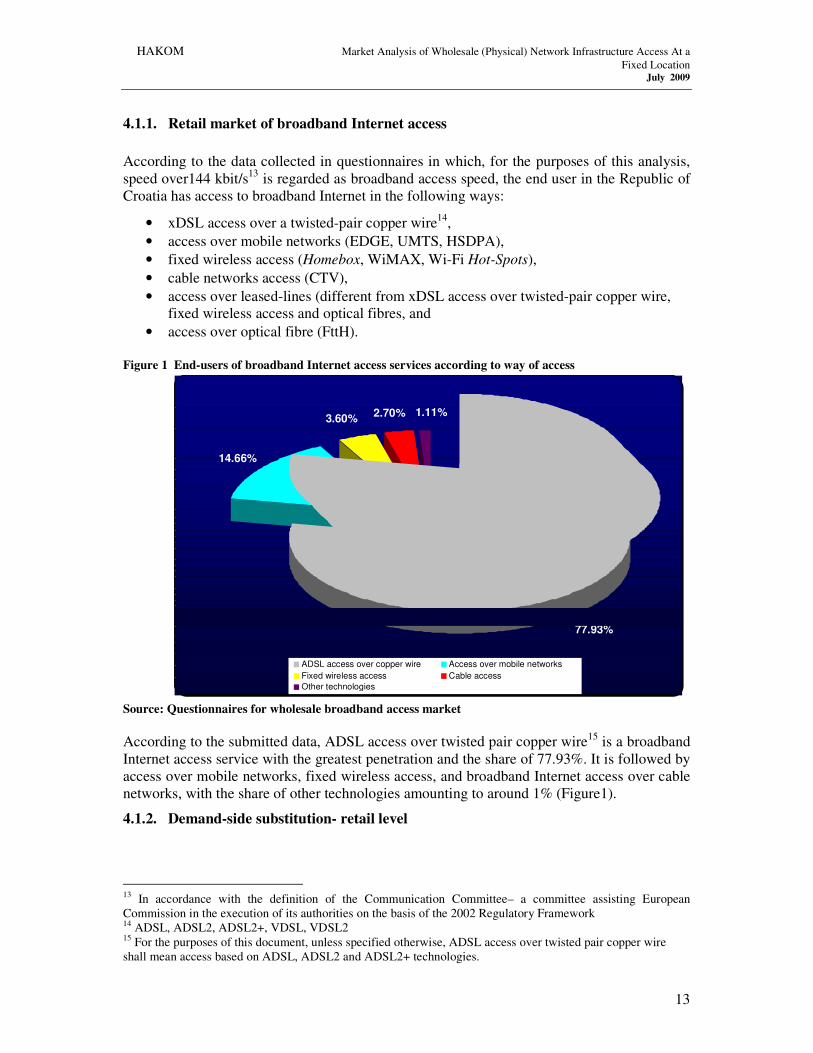

4.1.1. Retail market of broadband Internet access

According to the data collected in questionnaires in which, for the purposes of this analysis,

speed over144 kbit/s13

is regarded as broadband access speed, the end user in the Republic of

Croatia has access to broadband Internet in the following ways:

• xDSL access over a twisted-pair copper wire14

,

• access over mobile networks (EDGE, UMTS, HSDPA),

• fixed wireless access (Homebox, WiMAX, Wi-Fi Hot-Spots),

• cable networks access (CTV),

• access over leased-lines (different from xDSL access over twisted-pair copper wire,

fixed wireless access and optical fibres, and

• access over optical fibre (FttH).

Figure 1 End-users of broadband Internet access services according to way of access

Source: Questionnaires for wholesale broadband access market

According to the submitted data, ADSL access over twisted pair copper wire15

is a broadband

Internet access service with the greatest penetration and the share of 77.93%. It is followed by

access over mobile networks, fixed wireless access, and broadband Internet access over cable

networks, with the share of other technologies amounting to around 1% (Figure1).

4.1.2. Demand-side substitution- retail level

13

In accordance with the definition of the Communication Committee– a committee assisting European

Commission in the execution of its authorities on the basis of the 2002 Regulatory Framework 14 ADSL, ADSL2, ADSL2+, VDSL, VDSL2 15

For the purposes of this document, unless specified otherwise, ADSL access over twisted pair copper wire

shall mean access based on ADSL, ADSL2 and ADSL2+ technologies.

77.93%

14.66%

2.70% 1.11% 3.60%

ADSL access over copper wire Access over mobile networks

Fixed wireless access Cable access

Other technologies

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

14

Demand-side substitution implies the determination of services regarded by users as substitute

services. The Agency is of the opinion that the starting point for the establishment of services

that may be regarded as substitute services should be the service with greatest penetration.

Since services with the greatest penetration at the retail level of broadband Internet access are

services based on ADSL access over twisted-pair copper wire, the Agency aims at

determining whether there are at the retail level any services that could substitute ADSL

access over twisted-pair copper wire. Substitute services are those services to which

consumers could easily switch in case of a hypothetical price increase and thus satisfy their

equivalent need.

4.1.2.1. xDSL access over twisted-pair copper wire

4.1.2.1.1 ADSL access over twisted-pair copper wire

ADSL access over twisted-pair copper wire makes possible the downstream data transfer at a

higher speed and upstream data transfer at a lower speed, and it is adequate for high-speed

data transfer and access to related facilities whereby the transfer speed depends on the length

and type of the twisted- pair. ADSL technology at the retail level is more adequate for the use

of Internet and multimedia services requiring more speed towards the user and less speed in

the other direction.

The majority of twisted copper pairs in the Republic of Croatia are owned by the HT, which is

the incumbent and the owner of the public electronic communications network with

1.735.38616

active twisted copper pairs. The geographical accessibility/distribution is very

wide due to the fact that HT, as the universal service operator, must provide access to its

network to all users17

. HT’s access network was built during a long period of time while HT

was a public undertaking and a part of HPT18

and later while it enjoyed exclusive rights to this

network.

Broadband Internet access services based on ADSL access over twisted-pair copper wire are

supplied to end users by other operators as well, in the first place through HT’s wholesale

services in which case twisted-pair copper wire remains in HT’s ownership. The number of

users to whom they provide broadband Internet access via ADSL technology by means of

direct connection to their own network is negligible.

HT’s wholesale services used by other operators to provide broadband Internet access

services to its end users are the service of unbundled access to the local loop on one hand, and

on the other, the ADSL transport service and bitstream19

access.

What follows from the above-mentioned is that those end users in the Republic of Croatia

who access broadband Internet by means of ADSL access over twisted-pair copper wire may

be the users of the following:

16

Out of the total of 3,613,213 twisted-pairs in the access network. 17

In those parts of the republic of Croatia where there is no access infrastructure via twisted-pair copper wire,

the access to universal service is provided via fixed wireless access. (FGSM). 18

Croatian Post and Telecommunications 19

A service for which the operator uses the ADSL access service along with the ADSL transport service.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

15

• Other operators by means of the service of unbundled access to the local loop,

• Other operators by means of ADSL transport service, that is, the bitstream access

service, and

• Other operators by means of direct connection to that operator’s network20

.

Figure 2 End-users of broadband Internet access by means of ADSL access over twisted-pair copper wire

according to way of access

Source: Questionnaires for wholesale broadband access market

The majority of end users who access broadband Internet by means of ADSL access over

twisted-pair copper wire, namely 85.51% of them, are HT’s users (Figure 2).

During the time period covered by questionnaires HT offered in its tariff packages three

classes of access speeds among which the one with greatest penetration is the basic access

speed of 2 Mbit/s (Figure 3). A monthly fee for the basic download access speed in the entire

time period amounted to HRK 79.00 (excluding VAT).

20

In that case twisted-pair copper wire is not owned by HT.

86.51%

10.08% 0.17%3.24%

ADSL for self-supply - HTADSL via unbundled access to the local loopADSL transport and bitstreamADSL for self-supply - othersi

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

16

Figure 3 Classification of HT’s end users depending on access speed included in the tariff package

Source: Questionnaire for wholesale broadband access market –HT

Along with every access speed, HT offers to the end user a certain amount of traffic, that is,

data transfer. During the entire time period covered by questionnaires, HT offered the basic

data traffic package including 1 GB of traffic and unlimited traffic package, while the amount

of traffic included in the Super package changed over time21

. Table 1 shows the overview of

monthly fees for traffic within tariff packages currently offered by HT:

Table 1 Monthly fee for traffic within HT’s tariff packages

Name of package Price in HRK (VAT included)

MAXadsl Start 1GB 20.00

MAXadsl Super 59.00

Flat 99.00

Source: Questionnaire for wholesale broadband access market –HT

As it may be seen from Figure 4, HT’s end users most frequently use basic packages which

include 1 GB of traffic. However, with the increase in the selection of contents and needs of

end users and a reduction in the amount of the monthly fee for unlimited tariff packages,

together with the unaltered monthly fee for basic packages, in the last three time periods

covered by questionnaires the share of end users of the basic package has decreased with a

consequential increase in the share of users of unlimited tariff packages.

21

Super package included 2GB until 2006/2, 5 GB until 2008/1, and 10 GB in 2008/1.

90.58%

9.42%

92.49%

7.51%

94.32%

5.68%

95.10%

4.90%

95.56%

4.44%

95.91%

4.09%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005/2 2006/1 2006/2 2007/1 2007/2 2008/1

Other speed

Basic speed

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

17

Figure 4 Classification of HT’s end users depending on the traffic included in the tariff package

Source: Questionnaires for wholesale broadband access market

Note: * Start package includes 1GB of traffic.

** Super package included 2 GB until 2006/2, 5 GB until 2008/1 5 GB, and 10 GB in 2008/1.

In addition to the ADSL access over twisted-pair copper wire, HT also offers the service of

interactive television called MAXtv, which had 92,205 users at the end of the third quarter

of22

of 2008.

.

4.1.2.1.1 VDSL access over twisted-pair copper wire23

The increase in the selection of contents requiring broadband Internet access and the

increasing demand for the service of IP television led to the increase in the need of users for

more capacity, i.e. faster transfer speed of broadband Internet access. For that reason, ADSL

access over twisted-pair copper wire might prove to be insufifcient in situations requiring

simultaneous transmission of voice telephony, interactive video and high-speed data services

between end users and the main distribution frame.

By shortening the twisted copper pair, i.e., the cable with twisted pairs, in the manner that it is

replaced by an optical cable from the MDF to street cabinets or other concentration point in

the fixed electronic communications network and by installing DSLAM24

(Digital subscriber

line access multiplexer) in the street cabinet or some other concentration point, an operator

uses VDSL technology, in particular VDSL225

technology, to offer to end users quicker

22

T-HT- Results of the first nine months of 2008. 23

For the purposes of this document, unless indicated otherwise, DSL access over twisted-pair copper wire shall

include access on the basis of VDSL and VDSL2 technologies. 24 Digital subscriber line access multiplexer 25

VDSL2 is a symmetrical transfer technology supporting transfer speed from the theoretical 100 Mbit/s in both

directions, depending on the length and quality of the twisted-pair copper wire

79.87%

9.10%

11.03%

86.39%

9.88%

3.74%

79,42%

13.47%

7.10%

79.57%

13.60%

6.82%

77.87%

12.48%

9.65%

72.33%

15.11%

12.56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005/2 2006/1 2006/2 2007/1 2007/2 2008/1

MAXadsl Flat

MAXadsl Super **

MAXadsl Start*

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

18

transfer of data at shorter distances compared to data transfer based on ADSL technology.

VDSL2 was in the first place intended for the transfer of multi-channel HDTV (High

Definition Television), video on demand and videoconferences, and for Voice over the

Internet Protocol (VoIP). Therefore, VDSL2 is a good solution for triple play services26

.

Moreover, the Agency thinks that VDSL access over twisted-pair copper wire represents an

adequate substitute service for ADSL access over twisted-pair copper wire, that is, that the

users are likely, in case of a hypothetical increase in the price of the service based on ADSL

technology, to substitute this service with the service based on VDSL technology. In other

words, services based on VDSL technology will be substitutable with the already existing

services based on ADSL technology because this would satisfy the need of users for more

quality, faster and innovative services.

Consequently, the Agency believes that broadband Internet access services based on VDSL

access over twisted-pair copper wire will have a significant influence on competition at the

retail level. In other words, the mentioned services will be substitutable with broadband

Internet access services based on ADSL access over twisted-pair copper wire because this

would satisfy the need of users for more quality, faster and innovative services.

.

As a result, in the part of the analysis referring to wholesale demand-side substitution, the

Agency will take into account the influence of new generation access networks on the existing

wholesale services or, in this case, on the regulated wholesale service of unbundled access to

the local sub-loop over twisted-pair copper wire.

4.1.2.2. Access over mobile networks

Broadband Internet access over mobile networks has become the manner of Internet access

with greatest penetration after ADSL access over twisted-pair copper wire with a share of

14.66%.

The end user connects to the Internet via mobile networks by using a data card or a data

modem. The primary feature of broadband Internet access over mobile networks, which is

based on EDGE, UMTS and HSDPA technologies, is that the user is not exclusively tied to a

certain fixed location but may access Internet on his mobile phone or laptop from any

location, depending on the geographical coverage with EDGE, UMTS, or HSDPA signal.

EDGE technology makes possible the transfer of data up to 220 kbit/s, and UMTS technology

up to 384 kbit/s, which is significantly lower than access speeds offered by ADSL access over

twisted-pair copper wire. On the other hand, HDSPA technology allows transfer of data from

1.8 to 3.6 Mbit/s27

, which makes it comparable to ADSL Internet access technology in terms

of access speed. However, the speed with which the user accesses Internet via mobile

networks depends on the quality of signal reception (level or reception signal), that is, on the

closeness of the base station of the mobile operator and the number of users who are

accessing Internet at the same time, which may result in lower access speed and poorer

quality of service. In the usage of broadband data transfer via mobile technologies voice has

absolute priority over other services. This means that in case of network overload with voice

26

A service comprising broadband Internet access, IP television, and VoIP. 27

Theoretically up to 7,2 Mbit/s.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

19

calls (voice traffic), the fall in access speed is inevitable. Another restrictive factor in

broadband Internet access over mobile networks is population coverage with HSDPA signal

which amounts to 60% for all mobile network operators. It is therefore not possible in the

entire territory of the Republic of Croatia to achieve access over mobile networks at access

speed supported by HSDPA technology, which is comparable to access speed supported by

ADSL technology.

Because of the feature of mobility, the user is prepared to pay a higher price for the service of

broadband Internet access over mobile networks. More precisely, the monthly fee in mobile

tariff packages including 1GB of traffic 1 GB28

ranges from HRK 125.00 to 200,00 (see table

2), while the monthly fee for the equivalent tariff packages for ADSL access over twisted –

pair copper wire amounts to HRK 99.0029

.

Table 1 Internet access over mobile networks

Operator Name of package Price in HRK

(VAT included)

T-Mobile Mobile Internet 500 MB 100.00

T-Mobile Mobile Internet 1 GB 200.00

T-Mobile Mobile Internet 3 GB 300.00

VIP net Mobile Broadband 512 GB 91.00

VIP net Mobile Broadband 1 GB 191.00

VIP net Mobile Broadband 3 GB 291.00

VIP net Mobile Broadband Flat * 391.00

Tele2 Mobile Broadband 0 MB ** 0.00

Tele2 Mobile Broadband 500 MB 65.00

Tele2 Mobile Broadband 1 GB 125.00

Tele2 Mobile Broadband 3 GB 195.00

Table 2 Internet access over mobile networks

Operator Name of package Price in HRK

(VAT included)

T-Mobile Mobile Internet 500 MB 100.00

T-Mobile Mobile Internet 1 GB 200.00

T-Mobile Mobile Internet 3 GB 300.00

VIP net Mobile Broadband 512 GB 91.00

VIP net Mobile Broadband 1 GB 191.00

VIP net Mobile Broadband 3 GB 291.00

28 Broadband Internet access users mostly use packages including 1 GB of traffic. 29

The mentioned price refers to HT's tariff package within which access speed amounts to 2 Mbit/s, with

included 1 GB of traffic.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

20

VIP net Mobile Broadband Flat * 391.00

Tele2 Mobile Broadband 0 MB ** 0.00

Tele2 Mobile Broadband 500 MB 65.00

Tele2 Mobile Broadband 1 GB 125.00

Tele2 Mobile Broadband 3 GB 195.00

Source: official websites of operators T-Mobile, Vipnet and Tele2

Note: All subscribers of mobile Internet are charged a fee for the use of the radio frequency amounting to

HRK 10.00 per month.

* includes 10 GB of traffic

** does not include data transfer, charges per MB

Furthermore, any additional data transfer, that is, additional traffic30

, in mobile tariff

packages is charged per MB, ranging from 0.20 to 0.28 HRK/MB. Thus, the charge for an

additional GB of traffic in tariff packages based on access over mobile networks ranges from

HRK 204.80 to 286.72, while in tariff packages offered on the basis of ADSL access over

twisted-pair copper wire it amounts to HRK 20.0031

.

What follows from the above is that, if we take into account the retail price of mobile Internet

access services and Internet access services via ADSL access over twisted-pair copper wire,

in particular the fee for additional traffic, the hypothetic monopolist test shows that mobile

Internet access is not a substitute service of ADSL access over twisted-pair copper wire since

the increase in retail prices of tariff packages based on ADSL access over twisted-pair copper

wire between 5 and 10% will not influence the decision of end users to substitute the letter

service with the broadband Internet access service via mobile networks.

Furthermore, as opposed to tariff packages for ADSL access over twisted-pair copper wire,

the user of broadband Internet access over mobile network does not have the possibility to

choose a package with unlimited traffic32

. Considering the increasing share of users of basic

packages which include 1 GB and the increasing share of users of unlimited tariff packages

(Figure 4), the Agency does not consider the service of broadband Internet access over mobile

networks as a substitute service for ADSL access over twisted-pair copper wire.

Additionally, users of services of mobile Internet access are mostly corporate users who

appreciate mobility in the first place, as opposed to ADSL access over twisted-pair copper

wire which is primarily used by private users. Figure 5 shows the shares of private and

corporate users using broadband Internet access service over mobile networks from one of the

mobile operators. Precisely because of the fact that the majority of users of the above-

mentioned service are corporate users, and with the assumption that the above-mentioned

service is primarily needed for the purpose of mobility, it may be concluded that this service

does not represent a substitute service but a complementary service to services based on

ADSL access over twisted-pair copper wire.

30

Dana transfer, that is, traffic not included in the tariff package. 31 The price for additional GB of traffic within HT's tariff packages. 32

Although VIPnet does offer a tariff package Mobile Broadband Flat, this package does not include unlimited

traffic but 10 GB of traffic.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

21

Figure 5 Share of private and corporate users using broadband Internet access service over mobile

networks *

Source: Questionnaires for wholesale broadband access market

Note: * data from one of the mobile operators

As a result, the Agency is of the opinion that, considering its price and functional

characteristics, mobile Internet access does not represent a substitute service for ADSL access

over twisted-pair copper wire, and that these services will not be regarded as substitutable

services in the time period covered by this analysis. However, considering the increase in the

share of mobile Internet access in the total number of broadband Internet access users, the

Agency shall follow further development of the mentioned service and its influence on

broadband Internet access market.

4.1.2.3. Fixed wireless access

Fixed wireless access is achieved in the Republic of Croatia through the Homebox33

service,

WiMAX technology and the HotSpot service.The share of end users of broadband Internet

access service based on fixed wireless access is only 3.60%. From among the mentioned

services, Homebox service supplied by VIPnet has the largest number of users.

4.1.2.3.1 Fixed wireless access over the Homebox service

Homebox is a fixed wireless access service in the mobile electronic communications network

with the use of the radio-frequency spectrum. The mentioned service is based on EDGE,

UMTS and HSDPA technologies, and in areas covered by the HSDPA signal it enables

broadband Internet access with speed up to 1,8 Mbit/s, and in other areas with speed permitted

by UMTS and EDGE technologies. However, as it was already mentioned in relation to

mobile Internet access, access speed depends on the proximity of the base station of a mobile

network operator and the number of users accessing Internet at the same time, which may

result in lower access speed and poorer quality of service.

33

For the purposes of this document, the Homebox service shall include the Officebox service for corporate

users.

37.61%

62.39%

Corporate users Private users

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

22

Since the highest access speed allowing data transfer within the Homebox service is lower

even than the lowest access speed in tariff packages offered by HT, who has the biggest

number of end users, the Agency does not consider the Homebox service to be a substitute

service for ADSL access over twisted-pair copper wire. Furthermore, operators offer different

access speed within tariff packages based on ADSL access over twisted-pair copper wire,

while the user of the Homebox service who wants to increase access speed is limited with a

predetermined highest access speed up to 1.8 Mbit/s, which also depends on the coverage

with HSDPA signal.

A monthly fee for the Homebox service is HRK 150.00, and includes access to publicly

available telephone service, Internet access and 2 GB of traffic. Every additional data transfer

in tariff packages over mobile networks is charged HRK 0.20 per MB, that is, an additional

GB of traffic within the Homebox service amounts to HRK 204.80, while the same amount of

traffic in tariff packages offered on the basis of ADSL access over twisted-pair copper wire

amounts to HRK 20.00.

As opposed to tariff packages based on ADSL access over twisted-pair copper wire, the user

of the Homebox service may not chose another tariff package in terms of the amount of traffic

included in the monthly fee, except for the included 2 GB of traffic, not even the unlimited

tariff package. Taking into account the fact that the share of users of basic packages which

include 1 GB of traffic is decreasing, while the share of users of unlimited traffic packages is

increasing (see Figure 4), the Agency does not regard the Homebox services as a substitute

service for ADSL access over twisted-pair copper wire.

If one compares the monthly fee for the Homebox service and prices offered by HT for ADSL

access over twisted-pair copper wire and takes into account the monthly fee for the service of

access to a publicly available telephone service, a monthly fee for Internet access and Internet

traffic of 2 GB for which a user currently pays to HT the total price of HRK 192.20, the

hypothetical monopolist test might suggest that the mentioned services could be regarded as

substitute services. However, in case of the Homebox service, an additional GB of traffic,

which is not included in the tariff package for Homebox service, amounts to HRK 204.80. On

the other hand, in tariff packages offered on the basis of ADSL access over twisted-pair

copper wire, the additional GB amounts to HRK 20.00.

What follows from the above is that the Agency does not regard fixed wireless access over the

Homebox service and the service of ADSL access over twisted-pair copper wire as

substitutable services regardless of the fact that, in terms of the amount of the basic fee, the

Homebox service does represent a substitutable service for the HT’s service offered by means

of ADSL access over twisted-pair copper wire. However, if we take into account the price of

additional traffic, the two services may not be regarded as substitutable services. Therefore,

considering both the functional and price-related characteristics, and taking into account the

additional traffic and the share of users using the Homebox service, the Agency thinks that the

two services may not be regarded as substitute services in the time period covered by this

analysis. Nevertheless, the Agency shall follow further development of the mentioned service

and its influence on broadband Internet access market.

4.1.2.3.2 Fixed wireless access over the WiMAX technology

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

23

In late 2008 51 concessions for fixed wireless access over WiMAX technology34

were granted

in the Republic of Croatia. They were granted in all Croatian counties to the total of 8

operators. The only companies providing broadband Internet access over WiMAX technology

in certain counties are Novi-Net d.o.o., Optima Telekom d.d., and WiMAX Telecom d.o.o.

since the second half of 2008.

In the time periods covered by the questionnaire the number of end users of broadband

Internet access over WiMAX technology was negligible. The main reasons for the lack of

users of this technology in the provision of broadband Internet access are the lack of

standards, expensive terminal equipment and insufficient quality

Furthermore, some operators gave up the granted concessions35

. One operator mentions

problems encountered during implementation of the electronic communications system and

during commercial provision of the service. The problems were related to the usage of the

procured and installed equipment as well as to the fact that the service was not accepted on

the market, and the price of terminal equipment was too high. Since the mentioned reasons do

not allow the operator to provide the service in question on the basis of a long-term cost-

effective commercial model, the operator submitted a written request for the withdrawal of

the granted concessions.

As a result of the above, the Agency does not regard the mentioned technology to be a

substitute service for ADSL access over twisted-pair copper wire. Nevertheless, the Agency

shall observe the influence of the service in question on broadband Internet access market.

4.1.2.3.3 Fixed wireless access over the HotSpot service

The HotSpot service as a solution for wireless Internet access based on WLAN technology

may not be regarded as a substitute service because its price cannot compete with the price of

ADSL access over twisted-pair copper wire. For instance, T-Mobile measures Internet access

over the above-mentioned services in 15 minute intervals, and charges every interval at a

price of HRK 10.00. In other words, the service of Internet access over the Hot Spot service is

charged on the basis of duration, and not on the amount of transferred data as in the case of

broadband Internet access service based on ADSL access over twisted-pair copper wire.

HotSpot service also allows access at precisely designated locations such as city squares,

marinas, hotels and airports and it is not intended for usage in households and companies

which is why it does not represent a substitute for the service of ADSL access over twisted-

pair copper wire.

.

4.1.2.4. Access over cable networks

Access over cable networks is broadband Internet access allowing the user to connect by

using a coaxial cable (or over a hybrid fibre-coaxial network) which at the same time

broadcasts the cable television signal. Although the primary intention of the cable network is

to provide television contents, today, an increasing number of operators may, by means of

34

Some are for the territory of one county, and some for the territories of two or more neigthbouring counties. 35

Three operators gave up the total of 20 concessions.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

24

certain technical alterations on the networks, offer to their end users a publicly available

telephone service and data transfer.

Broadband Internet access over cable networks allows data transfer at an approximately

identical speed as ADSL access over twisted-pair copper wire. Internet access over cable

networks functions on the principle of bandwidth sharing. Cable modems are linked by

coaxial cables to the cable modem termination system (CMTS) which is a constituent part of

the CATV – local exchange of a cable network operator. Although this type of architecture

allows the broadcasting of the cable television signal to a large group of end users with a

relatively small number of cables, when using cable modems to access Internet, all users

linked with CMTS by means of a joint coaxial cable share the total transfer speed. In other

words, all users from the same or several neighbouring buildings share the same cable

connecting them to the central node and thus share the same frequency segment (bandwidth)

used by the cable modem. The result of this is that an individual user may not achieve

maximum speed at a certain moment or that transfer rate falls as a result of excessive overload

of the cable network.

The share of end users of broadband Internet access over cable networks in the Republic of

Croatia amounted 2.70% at the end of the first half of 2008.

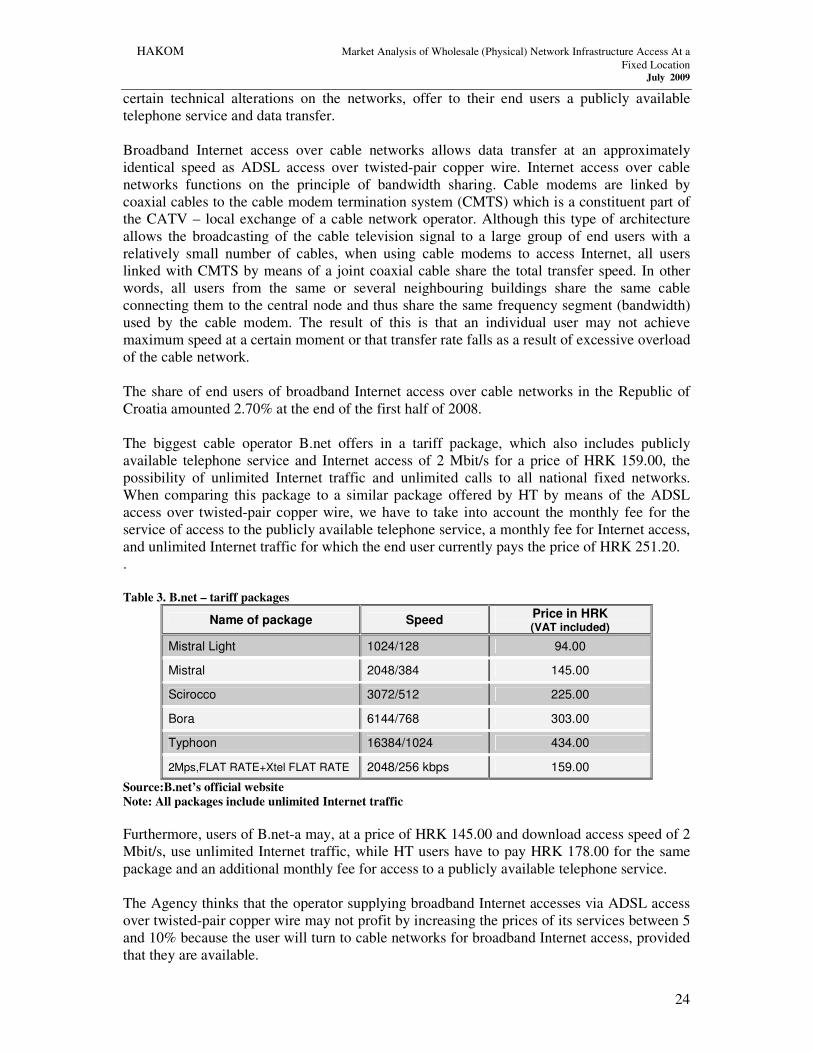

The biggest cable operator B.net offers in a tariff package, which also includes publicly

available telephone service and Internet access of 2 Mbit/s for a price of HRK 159.00, the

possibility of unlimited Internet traffic and unlimited calls to all national fixed networks.

When comparing this package to a similar package offered by HT by means of the ADSL

access over twisted-pair copper wire, we have to take into account the monthly fee for the

service of access to the publicly available telephone service, a monthly fee for Internet access,

and unlimited Internet traffic for which the end user currently pays the price of HRK 251.20.

.

Table 3. B.net – tariff packages

Name of package Speed Price in HRK (VAT included)

Mistral Light 1024/128 94.00

Mistral 2048/384 145.00

Scirocco 3072/512 225.00

Bora 6144/768 303.00

Typhoon 16384/1024 434.00

2Mps,FLAT RATE+Xtel FLAT RATE 2048/256 kbps 159.00

Source:B.net’s official website

Note: All packages include unlimited Internet traffic

Furthermore, users of B.net-a may, at a price of HRK 145.00 and download access speed of 2

Mbit/s, use unlimited Internet traffic, while HT users have to pay HRK 178.00 for the same

package and an additional monthly fee for access to a publicly available telephone service.

The Agency thinks that the operator supplying broadband Internet accesses via ADSL access

over twisted-pair copper wire may not profit by increasing the prices of its services between 5

and 10% because the user will turn to cable networks for broadband Internet access, provided

that they are available.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

25

Also, since prices of both technologies used for Internet access are similar, access over cable

exerts a certain price-related pressure at the retail level against retail prices of ADSL access

over twisted-pair copper wire. What follows from the above is that access over cable

networks, considering its characteristics in terms of price and functionality, represents a

substitute service for ADSL access over twisted-pair copper wire at the retail market of

broadband Internet access.

4.1.2.5. Access over leased lines

Broadband access line is intended for business entities and big companies whose business

communication is based on the need for constant Internet presence and for high-speed transfer

of data. The advantages of line access are high speed, safety, maximum reliability,

simultaneous Internet access for a large number of users and the possibility of a constant

connection of the computer system to the Internet.

Furthermore, the price of a leased HT line of 2 Mbit/s capacity amounts to HRK 3,375.0036

while Internet access at a speed of 2 Mbit/s by means of ADSL access over twisted-pair

copper wire, which includes unlimited Internet traffic, amounts to HRK183.7537

.

For that reason the above-mentioned service, considering its characteristics in terms of price

and functionality, does not represent an adequate substitute for ADSL access over twisted-pair

copper wire.

4.1.2.6. Access over optical fibre

In the period covered by questionnaires, a small number of end users, mostly business users,

used the service of broadband Internet access over optical fibre. However, with the increase of

the selection of contents requiring broadband Internet access and an increasing demand for the

service of IP television, users will need more capacity, that is, the demand for high-speed

broadband Internet access will grow.

Since optical fibre permits higher transfer speed than DSL technologies, which makes

possible the provision of high-quality services and supports advanced IP applications, such as,

for example, HDTV (High Definition Television), the Agency expects the number of users to

which operators will provide broadband Internet access service via optical fibre to increase,

that is, there will be more users who will be ready to pay a higher price for a service of a

higher quality.

As a result of the above, the Agency’s opinion is that broadband Internet access over optical

fibre will have a significant influence on competition at the retail level, that is, the mentioned

services will be substitutable with the already existing services based on ADSL technology

because this will satisfy the need of users for more quality, faster and innovative services.

36

VAT not included 37

VAT not included.

HAKOM Market Analysis of Wholesale (Physical) Network Infrastructure Access At a

Fixed Location July 2009

26

In conclusion, while analysing the substitutability of demand at the wholesale level, the

Agency will investigate the influence of new technology access networks on the existing

wholesale services, that is, in this case on the regulated wholesale service of unbundled access

to the copper-based local loop.

4.1.2.7. Conclusion

As a result, the Agency has concluded that the demand for the service of wholesale (physical)

network infrastructure access (including share or fully unbundled access) at a fixed location

access arises from broadband Internet access services provided at the retail level which are

based on:

• xDSL access over twisted-pair copper wire,

• access over cable networks, and

• access over optical fibre.

.

4.1.3. Demand-side substitution – wholesale level

Demand-side substitutability at wholesale level should serve to establish substitute services

for the currently valid service of wholesale (physical) network infrastructure access (including

share or fully unbundled access) at a fixed location, in the manner that the users of this

service, should the incumbent increase the price of the service, build their own access

infrastructure or start using some other wholesale service which will be regarded as equivalent