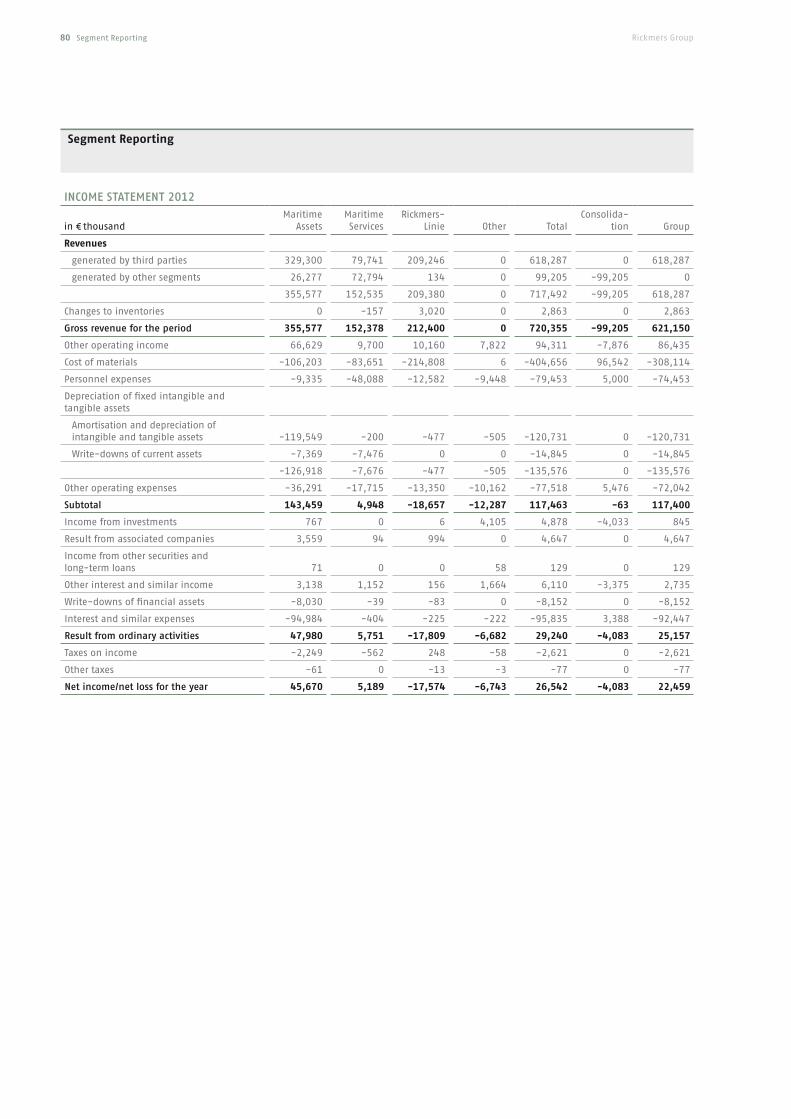

MaritiMe Values - Rickmers Group Values annual report 2012 our financial year 2012 Key performance...

113

MARITIME VALUES ANNUAL REPORT 2012

Transcript of MaritiMe Values - Rickmers Group Values annual report 2012 our financial year 2012 Key performance...

MaritiMe Valuesa n n u a l r e p o r t 2 0 1 2

our financial year 2012

Key performance indicators for the Rickmers Group 1

in € million 20122011

(pro forma)2012 vs 2011

(pro forma) 2011

(as reported)

revenues 618.3 574.3 7.7% 517.9

eBitDa 244.4 203.0 20.4% 152.6

eBit 114.7 90.5 26.7% 70.5

eBt 25.1 14.6 71.9% 15.2

net income 22.5 13.8 63.0% 14.4

Balance sheet total 2,765.0 2,989.0 -7.5% 2,060.0

equity 719.5 753.1 -4.5% 313.9

equity ratio in % 26.0 25.2 3.2% 15.2

net debt 1,768.8 1,926.2 -8.2% 1,564.4

Cash flow from operating activities 111.3 160.0 -30.4% 134.8

number of employees2 3,494 3,409 2.5% 3,409

Maritime Assets

in € million 20122011

(pro forma)2012 vs 2011

(pro forma)2011

(as reported)

revenues 355.6 309.4 14.9% 238.9

eBitDa 260.6 202.3 28.8% 151.8

eBit 139.7 91.8 52.2% 71.8

number of employees 39 110 -64.5% 110

Maritime Services

in € million 20122011

(pro forma)2012 vs 2011

(pro forma)2011

(as reported)

revenues 152.5 115.2 32.4% 115.2

eBitDa 12.7 8.6 47.7% 8.6

eBit 5.0 8.4 -40.5% 8.4

number of employees2 3,179 3,048 4.3% 3,048

Rickmers-Linie

in € million 20122011

(pro forma)2012 vs 2011

(pro forma)2011

(as reported)

revenues 209.4 218.3 -4.1% 218.3

eBitDa -17.2 -3.9 > -100% -3.9

eBit -17.8 -4.4 > -100% -4.4

number of employees 178 176 1.1% 176

1 Differences in significant items listed in the income statement and the balance sheet are shown in the comparison between the pro forma financial statements 2011 and the audited consolidated financial statements 2011. these differences are primarily attributable to the consolidation of rickmers Maritime.

2 including employees at sea from external crewing agencies.Rickmers Holding GmbH & Cie. KG

neumuehlen 1922763 HamburgGermanytel.: +49 40 38 91 77 - 0Fax: +49 40 38 91 77 - 500e-mail: [email protected] Ri

ckm

ers

Gro

upAn

nua

l Rep

ort

2012

Mobile

Middlesbrough

Yangoon

Ningbo

Port SudanAltamira

Manzanillo

Panama

Buenaventura

SantaMarta

Vancouver

Long Beach

San Diego Savannah

NorfolkMorehead City

Poti

Mersin

Iskenderun

Jizan

Djibouti

Brownsville

Buenos Aires

Santos

Rio de JaneiroVitória

Masan

Mokpo

Bogotá

Budapest

Mexico City

Prague

ShenzhenChangsha

Chengdu

Chongqing

Laem Chabang

Haiphong Kaohsiung

Ho Chi Minh City

Chennai

Chittagong

Kuala Lumpur

Jakarta

Jebel Ali

Abu Dhabi

Bahrain

Dammam

Urumqui

Raslaffan

Port Said

Cape Town

Lisbon

Zurich

ViennaKoper

London

Bergen

Copenhagen

Oslo

Tallinn

Gothenburg

HelsinkiSt.Petersburg

MoscowGdansk KlaipedaRiga

Philadelphia

Montoir

Istanbul

Kolkata

Toronto

New YorkChicago

San Francisco

Manila

KarachiMuscat

Aqaba

Jeddah

Bilbao

Umm Qasr

Kuwait

Colombo

Porto Marghera

Izmir

Mäntyluoto

Vejle

Port Kelang

Mumbai

Genoa

Houston

Düsseldorf

Douglas

Constanta

Limassol

Antwerp

Hamburg

Bejing

Shanghai

Yokohama

Hong Kong

Singapore

Dalian

SeoulTianjin & Xingang

Qingdao

New Orleans

Tokyo

KobeNagoya

Büro und/oder Hauptanlaufhafen Agentur und/oder Hauptanlaufhafen Agentur und bei Bedarf zu bedienender Hafen Auswahl von bei Bedarf zu bedienenden Häfen Round-the-World Pearl String Service Europa nach Mittelost und Indien Möglicher Vorlauftransport für Mittelost/Indien Dienst ab USA Indien und Mittelost nach Europa „NCS“-Dienst zur Nordküste Südamerikas Westbound Round-The-World Service Mögliche Vor- und Nachlauftransporte

Office and/or base port Agency and/or base port Agency and inducement port Selection of inducement ports Round-the-World Pearl String Service

Europe to Middle East and India Possible pre-carriage for Middle East/IndiaService

India and Middle East to Europe “NCS”-Service to North Coast South America Westbound Round-The-World Service Possible pre- or on-carriage transportation

• office and/or base port

• agency and/or base port

• agency and inducement port

• selection of inducement ports

• • • round-the-World pearl string service

• • • europe to Middle east and india

• • • possible pre-carriage for Middle east/india service from the usa

• • • india and Middle east to europe

• • • ‘nCs’-service to north Coast south america

• • • Westbound round-the-World service

• • • possible pre- or on-carriage transportation

represented internationally by more than 20 offices and over 50 sales agencies.

Rickmers Group the business activities of the rickmers Group and its three business segments cover a broad range of services in the shipping supply chain.

Competences Adaptability based on a 179-year long traditiona core competence of the company with its 179-year long history is adaptability. the rickmers Group has always known how to adapt to new circumstances inherent in the various stages of market develop-ment, and has exploited oppor-tunities as they arise. reliability, quality and efficiency are strengths our clients can rely on, strengths backed by the competences and an entrepreneurial mind-set of our employees.

Markets 90 percent market share of goods traded globally - dynamic growth and efficiency gains With the growth in the global economy and vigorously expand-ing international trade, shipping has grown dynamically because 90 percent of globally traded goods are transported by sea. the advantages for clients in terms of efficiency are thus immense. Com-pared with air freight, seaborne container freight is much more cost-effective and environmentally friendly.

Ships 109 ships operating around the world the rickmers fleet comprises 109 ships, including 83 container ships from small feeders to 13,100 teu, 15 multi-purpose carriers that transport breakbulk, heavy lift and project cargoes, six conbulk-ers, two bulk carriers and three car carriers. We are the sole owners of 53 of these ships, which on aver-age are six years old.

Clients A loyal client base and new client groupsthe rickmers Group has an impressive international client base, with client relationships cultivated over many years. We are the preferred shipping partner for many well-known global players. Besides our loyal long-stand-ing client base, we have also tapped new client groups. Drawing on our specific expertise in the market, we support institutional investors and banks in their efforts to exploit the opportunities in shipping.

Network Excellent relationships along the shipping supply chainWe have established a strong network that spans many sections of the ship-ping industry and a broad geographic coverage to serve the needs of our customers.

PresenceOffices and agencies aroundthe globetoday, the rickmers Grouphas offices and agencies aroundthe globe, offering a broad rangeof services in the shipping supplychain.

Maritime Assets plans, finances, acquires, and manages our assets as well as ships held in trust which are chartered out to liner operators.

Maritime Services provides pro-fessional ship management for rickmers ships and other leading companies in the shipping indus-try. services include technical and operational management, crewing and management of newbuilds.

Rickmers-Linie offers liner ser-vices for breakbulk, heavy lift and project cargoes, operating a fleet of multi-purpose carriers with heavy lift cranes. it also manages rickmers’ investment in a heavy lift/breakbulk terminal in Hamburg.

Mobile

Middlesbrough

Yangoon

Ningbo

Port SudanAltamira

Manzanillo

Panama

Buenaventura

SantaMarta

Vancouver

Long Beach

San Diego Savannah

NorfolkMorehead City

Poti

Mersin

Iskenderun

Jizan

Djibouti

Brownsville

Buenos Aires

Santos

Rio de JaneiroVitória

Masan

Mokpo

Bogotá

Budapest

Mexico City

Prague

ShenzhenChangsha

Chengdu

Chongqing

Laem Chabang

Haiphong Kaohsiung

Ho Chi Minh City

Chennai

Chittagong

Kuala Lumpur

Jakarta

Jebel Ali

Abu Dhabi

Bahrain

Dammam

Urumqui

Raslaffan

Port Said

Cape Town

Lisbon

Zurich

ViennaKoper

London

Bergen

Copenhagen

Oslo

Tallinn

Gothenburg

HelsinkiSt.Petersburg

MoscowGdansk KlaipedaRiga

Philadelphia

Montoir

Istanbul

Kolkata

Toronto

New YorkChicago

San Francisco

Manila

KarachiMuscat

Aqaba

Jeddah

Bilbao

Umm Qasr

Kuwait

Colombo

Porto Marghera

Izmir

Mäntyluoto

Vejle

Port Kelang

Mumbai

Genoa

Houston

Düsseldorf

Douglas

Constanta

Limassol

Antwerp

Hamburg

Bejing

Shanghai

Yokohama

Hong Kong

Singapore

Dalian

SeoulTianjin & Xingang

Qingdao

New Orleans

Tokyo

KobeNagoya

Büro und/oder Hauptanlaufhafen Agentur und/oder Hauptanlaufhafen Agentur und bei Bedarf zu bedienender Hafen Auswahl von bei Bedarf zu bedienenden Häfen Round-the-World Pearl String Service Europa nach Mittelost und Indien Möglicher Vorlauftransport für Mittelost/Indien Dienst ab USA Indien und Mittelost nach Europa „NCS“-Dienst zur Nordküste Südamerikas Westbound Round-The-World Service Mögliche Vor- und Nachlauftransporte

Office and/or base port Agency and/or base port Agency and inducement port Selection of inducement ports Round-the-World Pearl String Service

Europe to Middle East and India Possible pre-carriage for Middle East/IndiaService

India and Middle East to Europe “NCS”-Service to North Coast South America Westbound Round-The-World Service Possible pre- or on-carriage transportation

• office and/or base port

• agency and/or base port

• agency and inducement port

• selection of inducement ports

• • • round-the-World pearl string service

• • • europe to Middle east and india

• • • possible pre-carriage for Middle east/india service from the usa

• • • india and Middle east to europe

• • • ‘nCs’-service to north Coast south america

• • • Westbound round-the-World service

• • • possible pre- or on-carriage transportation

represented internationally by more than 20 offices and over 50 sales agencies.

Rickmers Group the business activities of the rickmers Group and its three business segments cover a broad range of services in the shipping supply chain.

Competences Adaptability based on a 179-year long traditiona core competence of the company with its 179-year long history is adaptability. the rickmers Group has always known how to adapt to new circumstances inherent in the various stages of market develop-ment, and has exploited oppor-tunities as they arise. reliability, quality and efficiency are strengths our clients can rely on, strengths backed by the competences and an entrepreneurial mind-set of our employees.

Markets 90 percent market share of goods traded globally - dynamic growth and efficiency gains With the growth in the global economy and vigorously expand-ing international trade, shipping has grown dynamically because 90 percent of globally traded goods are transported by sea. the advantages for clients in terms of efficiency are thus immense. Com-pared with air freight, seaborne container freight is much more cost-effective and environmentally friendly.

Ships 109 ships operating around the world the rickmers fleet comprises 109 ships, including 83 container ships from small feeders to 13,100 teu, 15 multi-purpose carriers that transport breakbulk, heavy lift and project cargoes, six conbulk-ers, two bulk carriers and three car carriers. We are the sole owners of 53 of these ships, which on aver-age are six years old.

Clients A loyal client base and new client groupsthe rickmers Group has an impressive international client base, with client relationships cultivated over many years. We are the preferred shipping partner for many well-known global players. Besides our loyal long-stand-ing client base, we have also tapped new client groups. Drawing on our specific expertise in the market, we support institutional investors and banks in their efforts to exploit the opportunities in shipping.

Network Excellent relationships along the shipping supply chainWe have established a strong network that spans many sections of the ship-ping industry and a broad geographic coverage to serve the needs of our customers.

PresenceOffices and agencies aroundthe globetoday, the rickmers Grouphas offices and agencies aroundthe globe, offering a broad rangeof services in the shipping supplychain.

Maritime Assets plans, finances, acquires, and manages our assets as well as ships held in trust which are chartered out to liner operators.

Maritime Services provides pro-fessional ship management for rickmers ships and other leading companies in the shipping indus-try. services include technical and operational management, crewing and management of newbuilds.

Rickmers-Linie offers liner ser-vices for breakbulk, heavy lift and project cargoes, operating a fleet of multi-purpose carriers with heavy lift cranes. it also manages rickmers’ investment in a heavy lift/breakbulk terminal in Hamburg.

MaritiMe Valuesa n n u a l r e p o r t 2 0 1 2

our financial year 2012

Key performance indicators for the Rickmers Group 1

in € million 20122011

(pro forma)2012 vs 2011

(pro forma) 2011

(as reported)

revenues 618.3 574.3 7.7% 517.9

eBitDa 244.4 203.0 20.4% 152.6

eBit 114.7 90.5 26.7% 70.5

eBt 25.1 14.6 71.9% 15.2

net income 22.5 13.8 63.0% 14.4

Balance sheet total 2,765.0 2,989.0 -7.5% 2,060.0

equity 719.5 753.1 -4.5% 313.9

equity ratio in % 26.0 25.2 3.2% 15.2

net debt 1,768.8 1,926.2 -8.2% 1,564.4

Cash flow from operating activities 111.3 160.0 -30.4% 134.8

number of employees2 3,494 3,409 2.5% 3,409

Maritime Assets

in € million 20122011

(pro forma)2012 vs 2011

(pro forma)2011

(as reported)

revenues 355.6 309.4 14.9% 238.9

eBitDa 260.6 202.3 28.8% 151.8

eBit 139.7 91.8 52.2% 71.8

number of employees 39 110 -64.5% 110

Maritime Services

in € million 20122011

(pro forma)2012 vs 2011

(pro forma)2011

(as reported)

revenues 152.5 115.2 32.4% 115.2

eBitDa 12.7 8.6 47.7% 8.6

eBit 5.0 8.4 -40.5% 8.4

number of employees2 3,179 3,048 4.3% 3,048

Rickmers-Linie

in € million 20122011

(pro forma)2012 vs 2011

(pro forma)2011

(as reported)

revenues 209.4 218.3 -4.1% 218.3

eBitDa -17.2 -3.9 > -100% -3.9

eBit -17.8 -4.4 > -100% -4.4

number of employees 178 176 1.1% 176

1 Differences in significant items listed in the income statement and the balance sheet are shown in the comparison between the pro forma financial statements 2011 and the audited consolidated financial statements 2011. these differences are primarily attributable to the consolidation of rickmers Maritime.

2 including employees at sea from external crewing agencies.Rickmers Holding GmbH & Cie. KG

neumuehlen 1922763 HamburgGermanytel.: +49 40 38 91 77 - 0Fax: +49 40 38 91 77 - 500e-mail: [email protected] Ri

ckm

ers

Gro

upAn

nua

l Rep

ort

2012

Contents

2 Chairman‘s Message

4 CEO‘s and Deputy CEO‘s Message

8 Extended Board Committee

10 Rickmers Group

12 Maritime Assets

20 Maritime Services

28 Rickmers-Linie

36 Corporate Governance

40 Group Management Report

71 Consolidated Financial Statements

101 Further Information

The Rickmers Group is an established international provider of services for the shipping industry with its business segments Maritime Assets, Maritime Services and Rickmers-Linie. We have a reputation for reliability, quality and efficiency. Adaptability and an entrepreneurial mind-set have been a tradition at Rickmers throughout its 179-year history.

We operate a fleet of 109 ships, with over 3,000 seafarers and currently around 480 staff ashore. We have 104 Group companies and seven minority holdings. Rickmers is internationally repre-sented through more than 20 offices and over 50 sales agencies. This network and a strong global management team secure the success of the company which remains true to its core values: Leadership. Passion. Responsibility.

We remain on course, even through turbulent seas. This is largely down to our adaptability - a distinction that is closely associated with our family shipping tradition, celebrating 180 years in 2014. A demanding financial environment, high operating costs and low freight rates - all these present the greatest challenges facing our industry. Nonetheless we remain optimistic. In 2012 we showed that even under the most difficult of circumstances we can still compete with the best. Although results in absolute terms are not as satisfactory as those we have produced over the last decade, it is still a respectable achievement to have remained profit-able in 2012.

The crisis in the shipping markets is an opportunity for us. Our prepara-tions for the new environment started at an early stage - remaining true to our ability to adapt. This is why we are not currently under pressure of having a huge pipeline of ships ordered at peak asset prices; our fleet is fully financed and our business is broadly diversified. We have begun addressing the energy efficiency of our ships, laying the foundation for increased earnings and strengthening our competitive position.

A good crew also needs good officers and not least a good captain: the Executive Board and our Extended Board reflect a high level of expertise in shipping, professional competence, an orientation towards the capital markets and management know-how. Ronald D. Widdows succeeded Jan B. Steffens as CEO effective 1 April 2012, to head the Rickmers Group and the Rickmers-Linie GmbH & Cie KG. He has more than 40 years’ ex-perience in shipping. For 31 of these years he was at American President Lines and Neptune Orient Lines, most recently as President and CEO. We are proud to have gained the services of Ron Widdows, who is currently Chairman of the World Shipping Council and one of the most experienced and talented top managers in the whole industry. Dr. Ignace Van Meenen, CFO of the Rickmers Group is deputy to Ron Widdows and has played a sig-nificant role in navigating our company safely through the last two years of the shipping crisis.

An experienced Advisory Board expertly supports our management team. Claus-Günther Budelmann, Jost Hellmann and Flemming R. Jacobs are valuable counsellors and we are grateful for their commitment. I would personally like to thank Jan B. Steffens, who left the Advisory Board of the Rickmers Group effective 30 June 2012, for the many years of friendship and successful collaboration.

2 Rickmers GroupChairman‘s Message

Bertram R. C. RickmersChairman Rickmers Group

Bertram R. C. Rickmers is the Chairman and owner of Rickmers Holding. As of 31 December 2012, he held 100 percent of the company‘s shares.

The Rickmers family can look back on 179 years‘ tradition in shipping. Bertram R. C. Rickmers set up MCC Marine Consulting & Contracting in 1982, the nucleus of the present-day Rickmers Group. With the re-vitalisation of Rickmers Reederei in 1984, the repurchase of Rickmers-Linie from Hapag-Lloyd and its introduction into the Group in 2000, he completed the current shipping and ship management activities of the Group.

Mr Rickmers has a degree in economics from the University of Freiburg.

The additional quality gained through our system of corporate leadership and control is clearly visible at all levels within the company. With our focus on Corporate Governance we have created organisational structures that are aligned with the requirements of the capital market. Rickmers has also implemented a compliance process across our company and is look-ing to set standards in compliance for our sector of the industry. Complete transparency towards banks, business partners and towards current and future investors has become a matter of course for us.

I am proud that we have created the essential requirements needed to make our company better prepared for the future. The staff, our manage-ment team, the organisation and the strategy all assure me that a stron-ger company will rise from the current market phase. We have developed the potential to actively shape the market in a demanding environment and to exploit the opportunities offered: a talent that sets us apart from the competition and places us in the position of continuing Rickmers’ his-tory by starting another successful chapter.

I would be pleased if we could continue this success story together under the nearly 180-year-old Rickmers flag.

Yours sincerely,

Bertram R. C. Rickmers

» We have developed the potential to actively shape the market in a demanding environment.«

3Annual Report 2012 Chairman‘s Message

Ladies and Gentlemen,Dear Friends of the Rickmers Group,

As shipping enters its fifth year of tough market conditions, it has become clear that not only to survive but also to prosper in this challenging environ-ment, a shipping company’s ability to change, to bring new capabilities and products to its customers and to differentiate its services from its competi-tion is crucial to its future prospects. Companies in a position to adapt to the new demands will emerge considerably stronger from the shipping crisis. At Rickmers, the transformation that began in 2010 continues.

The year 2012 was overshadowed by the continuing crisis in shipping, which had a firm hold on many companies: in Germany, as many as 150 single-ship KGs (limited partnerships) alone have filed for bankruptcy, and more than half of the 850 single-ship KGs are threatened with insolvency. Most sectors in shipping continue to sustain losses due to depressed freight rates, high operating costs and soft demand growth. The global supply of ships has in-creased dramatically in recent years due to the large number of deliveries of orders placed in past boom years: in 2013, container ship deliveries will reach a historic high, whilst charter rates for container tonnage and freight rates for container shipping as well as heavy lift, breakbulk and project cargoes remain at levels that are unsustainable. An example of just how challenging the shipping environment has become is to look at the Baltic Dry Index: in May 2008, this bulk cargo indicator stood at a record figure of 11,700 – by 3 February 2012 it had reached a historic low of 647 points, plummeting 94.5 percent. By the end of the year the index did not look much better, standing at 699 points. And the fuel price, which in the meantime accounts for more than three-quarters of vessel operating costs, has risen to well above $600 per ton, an almost fivefold increase since 2002.

These conditions, combined with the continuing turmoil in global financial markets, have also brought orders of new ships to a virtual standstill for most of the last two years. Shipyards have massive under-employment of their building capacity, competition for the few orders that have been placed is intense and the price for newbuilds has now reached an all-time low, having now dropped by more than 40 percent since 2008. The shipyards, who for most of the last decade were in a “sellers” market and were focused on optimising their production efficiency, now find themselves in a “buyers”

Ronald D. WiddowsCEO Rickmers Group and CEO Rickmers-Linie

Ronald D. Widdows has been CEO Rickmers Group and Rickmers-Linie since 1 April 2012. He has more than 40 years‘ experi-ence in shipping, 31 of these years at American President Lines and Neptune Orient Lines, most recently as President and CEO of Neptune Orient Lines. Currently he is also Chairman of the World Shipping Council in Washington D.C. and member of the Advisory Board of the International Transport Forum in Paris.

CEO‘s and Deputy CEO‘s Message

4 Rickmers GroupCEO‘s and Deputy CEO‘s Message

market and, in addition to competing heavily on price, they are beginning to focus proactively on developing much more fuel efficient ship designs and to respond more favourably to owners’ design requirements than was the case not very long ago. This opens the door to the development of the next generation of container ships with dramatically lower fuel consumption and emissions than the existing global fleet. As a result of low freight rates and high operating costs, our customers – the container shipping companies in particular – are desperately seeking means to lower their costs, reducing the fuel consumption of their existing fleet as well as beginning to plan to bring new ships which are substantially more fuel efficient and have significantly lower capital costs in to their fleet. Ad-ditionally, while the focus today is driven by an economic imperative, the industry knows that in the not too distant future, CO2, SOx and NOx emissions will become a significant issue and it must begin to move to a much more environmentally and cost efficient fleet. Against this background we initi-ated an energy efficiency programme in 2012, working closely with ABB to install new technology that will greatly assist our customers in managing fuel consumption. We are also making modifications to some vessels’ engines to enable more efficient slower steaming and are increasing our training of the ship management personnel to enhance their awareness with regards to fuel consumption. All these actions will lead to lower fuel costs for our customers as well as our own fleet in the heavy lift/breakbulk sector.

The transformation of Rickmers Group also aims to position us to take advantage of the uniquely favourable circumstances of historically low new-build prices. As the turmoil in global financial markets continues, traditional sources of equity and financing for new ship construction have dried up. German banks and the KG system that has built roughly 40 percent of the global supply of container ships over the last two decades are largely no longer supporting investment in shipping. Thus, sources of equity and debt financing will be quite different in the years ahead, and it has been clear to us for some time that in order to access these new sources of financing, Rickmers has needed to transform itself: from a family-owned German shipowner with a long, rich tradition into a more professionally-managed international shipping company that is geographically closer to its customers and sources of financ-ing. We believe that being prepared to access the capital markets as well as tapping other non-traditional sources of ship asset investment will be key

Dr. Ignace Van MeenenDeputy CEO and CFO

Dr. Ignace Van Meenen joined the Rickmers Group as Chief Financial Officer in October 2011, and was additionally appointed as Deputy CEO effective 1 April 2012. He is also a member of the Supervisory Board of Rickmers Maritime in Singapore.

After studying law in Ghent and Osna-brück, Dr. jur. Van Meenen started his career at Deutsche Bank AG where he held various positions in the finance sector in Germany and the USA. Later, he held leading management positions as finance director and CFO at the mining and chemi-cal group RAG AG, the international media company RTL Group S.A. and the real estate group DIC.

5Annual Report 2012 CEO‘s and Deputy CEO‘s Message

success factors and capabilities that will differentiate us from our competi-tion. Transparent financials, rigorous financial controls, corporate governance, compliance, and a stronger balance sheet will enable us to be successful in the new environment of shipping in the years ahead. In 2012 we made sig-nificant progress along this path of transformation.

In this demanding environment, our revenue rose by 7.7 percent to € 618.3 million compared to 2011. With an EBITDA of € 244.4 million (2011 pro forma: € 203.0 million), net income increased by 63 percent to € 22.5 mil-lion. With an equity ratio of 26.0 percent (2011 pro forma: 25.2 percent), we also have a solid financial base. Seen against the backdrop of the ongoing crisis in shipping, this is a positive development, which we have worked hard to achieve. However we are not resting on our laurels with this result and are committed to improving our financial performance in the years ahead.

Looking forward, we see many new opportunities for the Rickmers Group based on our existing strengths. Rickmers-Linie has established itself as a leader in the heavy lift/breakbulk sector with its reliable Round-the-World Liner service. We believe that the growth potential for scheduled routes from Asia to South America and for broadening our service capabil-ity within Asia and the Middle East are very promising. To take advantage of these developments, Rickmers-Linie is currently expanding its sales capability in the Americas, Asia and the Middle East. Furthermore, the company is growing a more considerable tramping capacity in developing project cargo markets. In addition to organic growth, we will continue to look for opportunities to grow through M&A and/or joint ventures.

Our Asset Management business is also in the process of a transformation of its own. We started to modernize our fleet with more efficient tonnage. On behalf of an independent owner we have signed contracts for two multi-purpose carriers (MPC) newbuilds that will be delivered in 2015 from the Houdong shipyard in China and join the Rickmers-Linie fleet. We have also begun to move a number of older, smaller container ships out of our fleet, a process that will continue in 2013.

As with our Asset Management business, we will grow our heavy lift, break-bulk and project cargo business organically and look for M&A opportunities in the German shipping business in 2013. To support our business growth, particularly related to newbuild projects, at the end of 2012 we established

6 Rickmers GroupCEO‘s and Deputy CEO‘s Message

a Capital Markets capability in Asia, based in Singapore. This will allow us to be more agile in working with financial institutions, export credit agencies and investors in the region of the world where most shipbuilding takes place.

Maritime Services’ expertise in technical and operational fleet management is being strengthened, particularly in Asia where we have increased our pres-ence to better serve the growing Asian shipping sector, where many of our customers and future business growth will come from. We see competitive advantage in our fuel conservation initiatives that are beginning to take hold and be embraced by our customers. These represent further growth oppor-tunities. Further, Rickmers has achieved an important milestone in China, becoming the first international company to obtain a licence for recruiting seafarers in China and has established its own crewing agency in Shanghai. We plan to increase the number of ships under our management through newbuild projects, acquiring additional third-party ship managment as well as consolidation activities the Group may embark upon over time.

We enter 2013 knowing that market conditions will continue to be very chal-lenging and that we will not likely see any market recovery for most of the next two years. The steps we continue to take to transform our company, to build more capability and to serve our customers better during these tough times, will help us to weather the near term challenges and position us to take advantage of improved industry conditions when they come in the future.

Our thanks go to our long-standing customers and business partners and to our employees ashore and at sea, without whom our successes in the past would not have been possible.

We look forward to guiding the Rickmers Group with you to further success in the future.

With best regards,

Ronald D. Widdows Dr. Ignace Van Meenen

7Annual Report 2012 CEO‘s and Deputy CEO‘s Message

Prof. Dr. Mark-Ken Erdmann PhDDeputy CFO (from 1 July 2012)

Prof. Mark-Ken Erdmann PhD was ap-pointed full-time Deputy CFO of the Rickmers Group effective 1 July 2012. In this function he is responsible, among other things, for the corporate divi-sions Mergers & Acquisitions, Financial Controlling, Accounting & Reporting, Tax, Legal Affairs, Human Resources, Organisation and IT. He was previously CEO of Bertelsmann Business Consulting, CIO of the Corporate Center and Senior Vice President for corporate financial reporting at Bertelsmann SE & Co. KGaA, latterly reporting to the group CEO. After graduat-ing in economics, he began his career at Ernst & Young AG in the assurance and advisory business services division. Fol-lowing executive education sojourns at INSEAD and the Harvard Business School, he has been visiting lecturer for the MBA programme at the Leipzig Graduate School of Management (HHL) since 2007 and has been a member of the Supervisory Board of Just Software AG since 2010.

Frank BünteChief Treasury & Risk Officer, Head of Capital Markets

Frank Bünte has been part of the man-agement of the Rickmers Group since 2011 and is head of the Treasury & Risk department. As from 1 April 2012, he is responsible for the Capital Markets division, where the Rickmers Group con-centrates its expertise in securing funding for its business segments. Previously, he held various positions in the lending department of HSH Nordbank, where he was latterly responsible for the domestic shipping market. Frank Bünte completed his bank training with the HSH Nordbank AG’s predecessor institution, Hamburgische Landesbank, in 1985 and then worked in the company’s various credit divi-sions. Following graduation in savings bank business management in 1994, he was responsible for parts of the bank’s international loan business from 1995 to 1999. In that year he switched to the HSH Nordbank Group’s shipping division.

The Deputy CFO, the Chief Treasury & Risk Officer, the Global Heads of the three business segments and the Chief Operating Officer of Rickmers-Linie make up the Extended Board Committee of the Rickmers Group.

Extended Board Committee

8 Rickmers GroupExtended Board Committee

Björn SprotteGlobal Head Maritime Services (from 10 January 2013)

Björn Sprotte joined Rickmers in May 2000 as a nautical officer. Following his career at sea, he held various management positions in the technical and commercial departments at Rickmers Reederei and in Rickmers Shipmanagement. In 2012 he was appointed Managing Director of Rickmers Shipmanagement (Singapore). On 10 January 2013 Björn Sprotte was also named Global Head of the Maritime Services business segment and Managing Director of Rickmers Shipmanagement in Hamburg.

Holger StrackGlobal Head Maritime Assets

After an apprenticeship as an industrial clerk, Holger Strack joined Rickmers Reederei in 1997 and worked in various departments and positions in account-ing and treasury. He has been Managing Director of Rickmers Reederei since 2010 and has been in charge of the newly cre-ated business segment Maritime Assets since 2011.

Rüdiger GerhardtGlobal Head Rickmers-Linie

Rüdiger Gerhardt began his training with Rickmers-Linie in 1978. Subsequently, he held various positions within the company in the areas of finance, controlling and personnel. In 2011 he was appointed Global Head of Rickmers-Linie and became Managing Director of Rickmers-Linie GmbH & Cie. KG.

Ulrich UlrichsCOO Rickmers-Linie (from 10 July 2012)

Ulrich Ulrichs joined Rickmers-Linie in 2005 and took over responsibility as General Manager Line Management, becoming a Director in 2008. From 1 July 2011, Mr Ulrichs has been Deputy Managing Director of Rickmers-Linie. In July 2012 he was appointed Chief Operating Officer and Managing Director.

9Annual Report 2012 Extended Board Committee

Rickmers Group

12 Maritime Assets

20 Maritime Services

28 Rickmers-Linie

36 Corporate Governance

Maritime Assets plans, finances, acquires, and manages our assets as well as ships held in trust which are chartered out to liner operators.

Maritime Services provides pro-fessional ship management for Rickmers ships and other leading companies in the shipping industry. Services include technical and op-erational management, crewing and management of newbuilds.

Rickmers-Linie offers liner services for breakbulk, heavy lift and project cargoes, operating a fleet of multi-purpose carriers with heavy lift cranes. It also manages Rickmers’ investment in a heavy lift/breakbulk terminal in Hamburg.

Rickmers Group The business activities of the Rickmers Group and its three business segments cover a broad range of services in the shipping supply chain.

Maritime Assets

Ships are considerable assets. As such, the core mission of asset management is not only to secure but also to maximise the capital invested in this asset category, exploiting the potential for long-term appreciation. In our opinion, this can only succeed by taking a holistic approach to the overall life-cycle of a vessel regarding its value creation and then preparing a dedicated investment strategy that takes account of investor expectations.

The service portfolio of asset management embraces every aspect of shipping – from financing, selection of proper ship type and design to realisation, optimisa-tion and chartering through to the final sale or scrapping of the vessel.

It’s expertise that counts

The Maritime Assets business segment focuses on container ships and multi-purpose carriers (MPC). We pursue a holistic, long-term strategy – long term in the sense that a shipping investment once undertaken is so sustainable that it can be successfully divested at the market place at any given time. However, the increasing impact of the capital market is creating new interfaces and with it ever more tasks with ever greater requirements. Our clients have divergent demands and these need to be analysed individually so we can derive the right course of action. Maritime Assets is facing up to this change. Fundamentally, we target a long-term relationship with our clients and are constantly on the look-out for ways to increase the value of the portfolio. But we are also capable of acting as trouble-shooters in acute problem situations. Often, time or financial emergencies can call for short-term measures.

For our clients: the best charterers in the shipping industry

By the end of 2012, around 83 percent of possible charter days in 2013 were fixed for the company’s own fleet of 53 vessels, for 2014 it was already 77 percent and for 2015 55 percent of our own capacity had already been contracted. Over 90 percent of Maritime Assets revenue is generated through its own fleet. With our worldwide network of brokers, Maritime Assets, together with our subsidiary Harper Petersen, is extremely successful in chartering out vessels and has been able to outperform the market significantly in the last years in various ship classes. Rickmers has charters to many of the leading companies in shipping: Maersk, MOL, MSC, OOCL, Evergreen, HMM and CMA CGM, to name but a few. Of the 103 ships in Asset Management, eleven are chartered out to the Rickmers-Linie.

Professional commercial management for owners: from financing and chartering out to sales

The capital market in general, but especially private equity and institutional in-vestors, all play an important role for the Rickmers Group. Together with Maritime Services, Maritime Assets leverages its expertise not only to design and order, but also to supervise the building of and to operate fuel-efficient, marketable vessels for the

14 Rickmers GroupMaritime Assets

investor. This enables Maritime Assets to develop an attractive portfolio that allows a maximum of fungibility on the capital market. Against this background, Maritime Assets set itself up to meet the increased requirements regarding reporting and con-trol systems. We are able to compile integrated reports at short notice for each ship and to monitor working capital and ship operating costs more efficiently. The value-oriented portfolio management is the key to successful investment. Furthermore, we support our clients with individual solutions to keep struggling KG companies’ ships in operation. This is what sets Maritime Assets apart – the ability to provide and implement solutions promptly.

» We are focused on building up lasting customer relationships and maximizing the value of the portfolio.« Holger Strack Global Head Maritime Assets

15Annual Report 2012 Maritime Assets

16 Rickmers GroupMaritime Assets

The right partner - even in special situations: developing values

The high level of interplay between a liner shipping company, asset management and technical ship management make the Group an excellent partner for institutional investors. For example, Maritime Assets made two construction contracts for multi-purpose ships marketable for an independent owner and the financing bank. Both ships were originally commissioned by a company that has since become insolvent. In collaboration with the Maritime Services segment, the ship design was significantly re-engineered to improve its long-term energy efficiency. With cuts in operating costs significantly increasing the competitiveness of both ships, Rickmers-Linie - as specialist in the project cargo business - will be able to operate the ships efficiently from spring 2015.

The fleet in asset management: 103 ships

At the centre of our fleet in asset management are the 77 container ships from smaller 900 TEU vessels to vessels with a capacity of 13,100 TEU. Maritime Assets also manages a fleet of 15 MPC ships with crane capacities of up to 640 tonnes (com-bined). The fleet also includes bulk carriers, conbulkers and car carriers. Maritime Assets currently manages a total of 103 ships. The Rickmers Group owns 53 of these ships. The company-owned vessels are on average six years old and have been fully financed until at least 2015.

Internationally well-positioned

Maritime Assets is well positioned internationally. The IPO of Rickmers Maritime in Singapore extended the presence of the Rickmers Group in Asia in 2007 and thereby created a new access to the capital market. Rickmers Maritime currently owns and operates 16 container ships ranging in size between 3,450 TEU and 5,060 TEU, most of which are chartered out to leading liner shipping companies on long-term contracts. With our focus on the Asian container shipping market, the Rickmers Group exploits the advantages presented by Singapore as a maritime base. The Trust is listed on the Mainboard of the Singapore Exchange Securities Trading Limited and included in the FTSE ST Maritime Index. The shareholders include the Rickmers Group with around 33.1 percent as well as institutional and private investors. Furthermore, besides Rickmers Reederei, as the principal asset management company, the Maritime Assets business segment also includes Polaris, EVT Elbe Vermögens Treuhand, Expert Shipping Service (since 1 January 2013) and Harper Petersen.

17Annual Report 2012 Maritime Assets

» As a specialised service provider, we are a strong team of experts. It’s a great help to me not only to know the commercial side, but also the nautical perspective from my time at sea.« Capt. Ralf Trützschler Senior Staff Surveyor & Head of Marine Consulting ExpErt Shipping SErvicE MaritiME aSSEtS

18 Rickmers GroupMaritime Assets

19Annual Report 2012 Maritime Assets

Maritime Services

The Maritime Services business segment provides professional ship management for Rickmers’ ships and other leading companies in the shipping industry. Services include technical and operational management, crewing and the management of newbuilds. Our competitive advantage lies in the skills of our employees. We attach great impor-tance to comprehensive training: an indispensable factor in securing safe and efficient ship operations. To the benefit of our customers, we not only focus on providing a high operational availability of the fleet at competitive cost, but also place great emphasis on defining best practice for fuel saving operations.

Strengthening the competitiveness of our clients

The Maritime Services segment combines client and industry-specific solutions to deliver safe and efficient technical and operational ship management. We also pay special attention to the selection, training and composition of crews. In addition, we have considerable expertise in planning ship newbuilds, retrofitting existing ships and carrying out regular dockings and maintenance. Our team of specialists use an integrated planning system to keep operational outages to a minimum. Our clients also benefit from our Group-wide cost-effective procurement of consumables, spare parts and services.

With fuel costs now accounting for over three-quarters of ship operating expenses, bunkers consumption is a vital factor in determining a ship’s profitability. We have initiated innovative projects to optimise energy efficiency and in January 2013 be-came the first German company to be accredited by GL Systems Certification in line with ISO 50001 (Energy Management System) for our offices in Hamburg and Sin-gapore and for the first ten ships. To achieve our goals, we have developed state-of-the-art technical systems in collaboration with renowned industrial partners. Professional services related to maritime insurance brokerage and worldwide claims management round off our portfolio.

Entrepreneurial thinking: ship-centric management

The long-term cost-efficiency of ship operations depends on a well-trained crew and professional on-board management that can guarantee high technical quality and high safety standards. Our concept of “ship-centric management” to optimise the operations of the Rickmers fleet is based on this conviction. According to this organ-isational principle a ship is regarded as a production unit within an organisation.

22 Rickmers GroupMaritime Services

The captain, officers and superintendent form the ship management team. This allows for a lean, efficient organisation and ensures that our high technical and safety stan-dards are adhered to on the ships. We run intensive interactive courses, which set international standards in terms of modern and responsible ship management, to

» We set standards: we are the first maritime company in Germany with a certified man-agement system for energy efficiency on board and the first international company with a crewing licence for China.« Björn Sprotte Global Head Maritime Services

23Annual Report 2012 Maritime Services

prepare our captains and officers for their management tasks. We train our on-board management in line with recognised techniques and methods tailored to meet the special requirements of operating at sea. Building on this, we have also developed special courses dealing with energy management.

24 Rickmers GroupMaritime Services

Worldwide crewing expertise

The recruiting and composition of on-board crews - the crewing - is another key element of our service. In order to further improve the future availability of highly qualified crews and officers for the Rickmers Group in the Far East, we have reor-ganised our crewing activities in a number of countries, including Cyprus and China. Rickmers is the first foreign company to receive a licence for recruiting seafarers on international ships in China and has set up a crewing agency in Shanghai, Rickmers Shipping (Shanghai).

Maritime Services sets standards, targeting growth in Europe and Asia

Our offices at strategically important centres in Hamburg, Singapore and Limassol coordinate our worldwide activities. As a global maritime service provider, our aim is to achieve sustained profitable growth and contribute to the economic success of our clients by means of safe, efficient operations and continual improvements to our internal processes. By certifying our services in accordance with international stan-dards and regulations, we create a reliable basis for collaboration with our clients that is founded on trust.

25Annual Report 2012 Maritime Services

26 Rickmers GroupMaritime Services

» Apart from the technical improvements, there are a large number of variable factors in the energy efficiency of a ship that the team can influence. At Rickmers we regularly compare notes on best practice.« Captain Doru Dragomir Master Mv ricKMErS antWErp MaritiME SErvicES

27Annual Report 2012 Maritime Services

Rickmers-Linie

Reliability, punctuality, safety and the highest levels of competence are what Rickmers-Linie is known for. With our Round-the-World Pearl String Service, we have established a liner service of unrivalled reliability in the heavy lift/breakbulk and project cargo sector and have built up a renowned, high-quality brand with excel-lent client relationships globally.

Prize-winning Maritime Logistics

Rickmers-Linie is a leading global specialist for the ocean transportation of break-bulk, heavy lift and project cargoes. Cargoes transported include transformers, gen-erators, pressure vessels, construction machinery, wind turbines, plant components for the chemical and petrochemical industries, breweries, cement plants, and even locomotives, sailing and motor yachts. In 2012, Rickmers-Linie was awarded ‘Best Shipping Line - Project Cargo’ at the Asian Freight & Supply Chain Awards, the ‘All India Maritime Logistics Award (MALA)’ and the ‘Gujarat Star Award’ for the premium quality of its services. Strengthened by these successes, Rickmers-Linie is looking to expand its sales network and add additional liner services for the high-growth project cargo trade flows of the world.

Liner services for breakbulk, heavy lift and project cargoes

For more than ten years, the Round-the-World Pearl String Service has been provid-ing fast transit times and a reliable schedule: in this liner service our multi-purpose carriers follow a fixed itinerary serving 16 ports around the globe on an eastbound route with two departures every month. The ports include Hamburg, Antwerp, Genoa, Singapore, Shanghai, Masan, Yokohama and Houston. Further ports of call along the main route may be added if there is sufficient demand. For clients of Rickmers-Linie, the Pearl String concept in practice also makes just-in-time deliver-ies possible, even in project cargo and heavy lift operations. Rickmers-Linie’s Round-the-world network of routes is complemented by liner services from Europe to the Middle East and India (and back), and the America-Asia service across the Pacific. Here, ships depart every three weeks. In 2013, Rickmers’ liner services will be further expanded to leverage our brand in the developing markets of Asia and Latin America.

Modern fleet for liner services

The Round-the-World Pearl String Service is operated with nine ships of the same type with a net tonnage of 30,000 dwt. Each ship has four cranes, the two largest of which (each 320 tonnes capacity) can be combined to lift up to 640 tonnes of cargo on board. Flexible tweendecks mean that the height of the cargo holds can be adapted to meet customer requirements. Dehumidification systems ensure improved air quality for moisture-sensitive cargoes.

30 Rickmers GroupRickmers-Linie

In its Middle East and India service, and across the Pacific from America to Asia, Rickmers-Linie operates long-term chartered tonnage. At present, Rickmers-Linie is extending its fleet to include two new multi-purpose ships which not only come equipped with high-performance cranes with a lifting capacity of twice 450 tonnes, at the same time they are considerably more energy efficient. It is anticipated that these new ships will be delivered in the spring of 2015.

» In 2013 Rickmers-Linie will be further expanding its liner services in the fastest growing regions of the world.« Rüdiger Gerhardt Global Head Rickmers-Linie

31Annual Report 2012 Rickmers-Linie

In-house cargo management system

The core business of Rickmers-Linie focuses on the ocean transportation of break-bulk, heavy lift and project cargoes from port to port. The portfolio also includes the door-to-door transportation from the factory to point of use. Here, Rickmers-Linie cooperates with reliable haulage partners in the respective country.

With the aid of the RICOSYS cargo management software developed by Rickmers in collaboration with its software partners, Rickmers-Linie advises its clients on how best to position and secure cargo.

Sea transportation of aircraft sections and even space equipment

As part of a long-term contract, since 2012 Rickmers-Linie has been transporting aircraft sections for the Airbus A350 from the USA to France. Another prime example from the past few years of the excellent competence and reputation of Rickmers- Linie in transporting sensitive loads is the transportation of the Kibo research module of the Japanese space agency Jaxa. Rickmers-Linie transported this module from Yo-kohama to Port Canaveral for onward transport by space shuttle to the International Space Station (ISS).

32 Rickmers GroupRickmers-Linie

Worldwide sales network: growth in key markets

Rickmers-Linie operates 16 branch offices worldwide including Hamburg, Antwerp, Houston, Shanghai, Tokyo and Seoul. In addition, this network is supported by 50 agencies that enhance Rickmers-Linie’s global presence. Rickmers-Linie will be further expanding its capabilities in attractive growth markets. It has already strengthened its sales organisation in China with new partner offices in Chongqing, Changsha, Shenzhen and Chengdu. These join Rickmers branch offices in; Beijing, Shanghai, Dalian, Hong Kong, Tianjin, Xingang, Qingdao. Rickmers also maintains a sales agency in Urumqi (Xinjiang). Rickmers-Linie’s commitment to China has a long tradition: the company opened the first ‘representative office’ in Tianjin in Septem-ber 1985.

To drive our expansion in Asia, Rickmers-Linie opened its own branch office in Sin-gapore at the beginning of 2013. Furthermore, Rickmers-Linie is also expanding its sales network in the Americas. Since December 2011, Rickmers has been offering sea transportation of project cargoes under the US flag and cooperates with Maersk Line, Limited a company headquartered in the USA, under the name ‘Maersk-Rickmers U.S. Flag Project Carrier’.

Responsibility for employees, the environment and safety

Rickmers-Linie takes its responsibilities in respect of its employees and the environ-ment very seriously. Together with Maritime Services, we work continually to reduce emissions from our ships. Slow steaming, special energy efficiency training and in-vestment in energy-saving technologies have resulted in lowering fuel consumption and emissions. As these measures also reduce ship operating costs, they also help to improve profitability. In order to ensure the best-possible protection for the ship and its cargo, Rickmers-Linie meets strict safety regulations. To not only strengthen but also to extend our leading market position for the future, the selection of the best people, together with their professional qualifications and on-going development and training, is one of the most important corporate policies. Also contributing to our client’s satisfaction, which has top priority, are an open, honest and cooperative approach on the part of Rickmers-Linie management and an orientation towards delivering high quality. It is therefore a matter of course for us that Rickmers-Linie is certified by Germanischer Lloyd in line with ISO 9001:2008, ISO 14001:2004 and OHSAS 18001:2007. In November 2012, Rickmers-Linie was successfully recertified for a period of three years.

33Annual Report 2012 Rickmers-Linie

» As supercargo, I coordinate the loading and discharge of our vessels on the spot. And that’s exciting, because at Rickmers we hardly ever transport one cargo that’s the same as the one before. We have to adjust to new requirements every day.« Valeriy Rokotyanskyy Supercargo ricKMErS-LiniE

34 Rickmers GroupRickmers-Linie

35Annual Report 2012 Rickmers-Linie

Corporate Governance

The Executive Board and the Advisory Board of Rickmers Holding are committed to securing the Company’s viability and to achieving a sustainable increase in enter-prise value through responsible long-term corporate governance and by endorsing the aims of the German Corporate Governance Code. Although Rickmers Holding is not listed, the framework of corporate governance at Rickmers widely follows the recommendations of the Code in the version dated 15 May 2012 primarily address-ing publicly listed companies.

Management

Rickmers Holding has a dual management system that distinguishes between the Executive Board as the managing body and the Advisory Board as the advising body.

The Executive Board of Rickmers Holding is responsible for the management of the company. Its responsibilities include determining company goals, defining the stra-tegic direction of the Group, managing the Group, corporate planning and Group financing. The Executive Board regularly reports to the Advisory Board in a timely and comprehensive manner on all issues relevant to the company, including business developments, the implementation of strategy, planning, cash flows and financial performance, and risk management. It ensures compliance with statutory provisions and internal Group regulations. The Chief Executive Officer coordinates cooperation with the Advisory Board and regularly consults with the Chairman of the Advisory Board.

The Advisory Board advises the Executive Board on strategic issues and important business transactions. The Executive Board and the Advisory Board have a close and mutually trusting working relationship to meet the requirement of quick, but dili-gent decision-making processes. Fundamental issues of corporate strategy and their implementation are openly discussed and deliberated at joint meetings.

36 Rickmers GroupCorporate Governance

Shareholders

After Bertram R. C. Rickmers acquired 4 percent of the limited partners’ shares in Rickmers Holding GbmH & Cie. KG from Jan B. Steffens on 1 July 2012, he is now the sole shareholder in the company. As the shareholder of Rickmers Holding he appoints the Executive Board and members of the Advisory Board.

Compliance

Rickmers Group and its business segments are active in many countries and various regulatory environments and are therefore subject to different cultural and national standards and legal provisions. It is therefore important that all employees at every level of the company understand the Group’s commitment to compliance and share the same values of integrity. Quintessential elements of the corporate culture at Rickmers are compliance with the law, incorruptibility and fair competition. Compli-ance with laws and internal regulations designed to avoid exposure to legal risks and their consequences has for this reason always enjoyed the highest priority at Rickmers and is now supported by a systematic process of training conducted by internal and external experts in the field.

Transparency

The core element of model corporate governance is the transparent presentation of developments and decisions within the enterprise. Constant and open dialogue with all stakeholders secures trust in the enterprise and its value creation.

In order to gain the trust of potential investors and maintain the esteem of the shareholder, Rickmers has embarked on a policy that ensures a high degree of trans-parency in financial communication. Shareholders, the Advisory Board, banks, inves-tors and business partners are actively provided with broad information to assess the company’s performance and financial strength.

Comprehensive information about Rickmers can also be found on our website at www.rickmers.com. The website contains current information about the business segments, direction and important business-related changes within the company.

37Annual Report 2012 Corporate Governance

Executive Board

Executive Bodies

Bertram R. C. Rickmers Chairman

Jan B. SteffensCEO (until 31 March 2012)

Ronald D. WiddowsCEO (from 1 April 2012) • Overall strategic, operational and com-

mercial responsibility of the Group• Corporate Communications

Dr. Ignace Van MeenenDeputy CEO und CFO• Accounting & Controlling• Corporate Finance• Human Resources• IT• Legal Affairs• M&A• Tax• Treasury & Risk

38 Rickmers GroupCorporate Governance

Advisory Board Bertram R. C. Rickmers ChairmanBertram R. C. Rickmers is the Chairman of the Advisory Board at, and sole shareholder in, Rickmers Holding. He set up MCC Marine Consulting & Contracting in 1982 and Rickmers Reederei in 1984 as the foundation for the current ship owing and ship management activities of the Group. In 2000 he purchased Rickmers-Linie back from Hapag-Lloyd.

Claus-Günther Budelmann Deputy ChairmanAfter his banking training and holding diverse positions at Bankhaus Joh. Berenberg, Gossler & Co. KG, Hamburg, Claus-Günther Budelmann was made General Manager of the bank in 1981. From 1988 to 2009 he was a general partner in the bank. Claus-Günther Budelmann is a member of various advisory boards.

Jost HellmannJost Hellmann is a law graduate. From 1982 he was responsible for setting up the international branches of the Hellmann Group. Since 1989 he has been Managing Partner of the Osnabrück-based group of companies Hellmann Worldwide Logistics GmbH & Co. KG. Jost Hellmann is a member of several advisory boards.

Flemming R. JacobsFrom 1960 to 1999 Flemming R. Jacobs worked for A.P. Moller-Maersk in various countries and posts, most recently from 1997 to 1999 as partner and CEO of Maersk Tankers. From 1999 to 2003 he was Group President and Chief Executive Officer and Director of the container shipping company Neptune Orient Lines, Ltd. and CEO of American President Lines (APL). He is currently a member of the supervisory and advisory boards of many companies.

Jan B. Steffens (from 1 April 2012 to 30 June 2012)Jan B. Steffens joined the Rickmers Group in 2002 as Managing Director of Rickmers-Linie. In 2005 he became CEO of Rickmers Holding and a partner in 2006. He left the Executive Board with effect 31 March 2012 and the Advisory Board effective 30 June 2012.

39Annual Report 2012 Corporate Governance

Group Management Report

42 The Rickmers Group

46 Economic Environment

50 Business Performance

53 Financial Performance

54 Cash Flows and Financial Position

57 Employees

60 Risk and Opportunity Report

67 Events after Reporting Date

68 Forecast

1 The Rickmers Group

1.1 Business operations

Business operations in the Rickmers Group are divided

into three segments: Maritime Assets, Maritime Services

and Rickmers-Linie (formerly: Logistics Services) and cover

a broad range of services in the shipping supply chain.

Maritime Assets plans, finances, acquires, and manages

our assets as well as ships held in trust which are chartered

out to liner operators.

Maritime Services provides professional ship management

for Rickmers ships and other leading companies in the

shipping industry. Services include technical and opera-

tional management, crewing and management of new-

builds.

Rickmers-Linie offers liner services for breakbulk, heavy

lift and project cargoes, operating a fleet of multi-purpose

freighters with heavy lift cranes. It also manages Rickmers’

investment in a heavy lift/breakbulk terminal in Hamburg.

As Group parent company, Rickmers Holding provides its

business segments with interdisciplinary services and

serves as a management holding company for the Group.

Amongst other things, this means acquiring, holding and

selling investments in other shipping companies and re-

lated maritime businesses. Moreover, Rickmers Holding

manages financing for the business segments.

1.2 Strategy and aims

The Rickmers Group has continued to develop its strategy

in the light of the on-going shipping crisis and the chal-

lenging situation on the capital market. Following up on

a detailed analysis of the shipping market, forecasts and

prevailing circumstances, Rickmers management has iden-

tified potential areas in which the company can achieve

profitable, sustainable growth.

Our strategy is based on the following assumptions:

1. Around 90 percent of goods traded globally are trans-

ported by sea. Consequently, clients stand to benefit from

reliability, safety, quality and low costs. Compared with

other transport modes, shipping’s significant advantages

based on economies of scale not only make it far much

more cost-efficient, it is also more environmentally friend-

ly, with much lower greenhouse gas emissions measured

per tonne. These benefits will also secure future growth in

shipping parallel to the development in world trade.

2. Ongoing tension in the shipping markets will continue

to add pressure in the industry to consolidate.

3. To meet the challenges of a demanding competitive en-

vironment and exploit the opportunities it presents, busi-

ness success hinges on a company’s standing on the capital

market and its particular shipping expertise - from asset

management and technical ship management through to

its liner shipping business.

4. In the future, the most significant impetus arising from

growth in international trade and the ensuing trade flows

will continue to come from Asia and South America.

Group Management Report

42 Rickmers GroupGroup Management Report

5. Capital investment in heavy industry and the construc-

tion of plant for power generation, the oil, gas and chemi-

cal industries, infrastructure and mining will grow world-

wide.

6. In the medium to long term, energy efficiency and re-

source-light shipping operations will grow in importance.

A fleet of low-cost vessels will be successful, even in a

market that remains plagued by over-capacity.

7. Besides the issues of energy and ecological efficiency,

qualities such as punctuality, cost efficiency and safe

transport will play an ever-greater role in future capital

goods logistics.

8. The recruiting and training of staff will become more

crucial determinants of competitiveness in the shipping

industry.

Rickmers has derived its strategy from just this scenario, a

strategy that aims to lead the company towards sustain-

able and profitable growth:

1. Meeting capital market requirements and tapping ad-

ditional sources of funds

In order to exploit market opportunities and to be able

to actively shape the anticipated consolidation, sound

corporate financing and access to the capital markets are

indispensable. The Rickmers Group is a soundly-financed

family-owned company whose financial structures and

reporting systems are aligned to meet the demands of

the international capital market. At the same time, the

ownership structure with its 179-year family tradition in

the shipping industry and experienced management team

guarantee sustainable management.

2. Reinforcing organic growth in the business segments

The Group’s three business segments, Maritime Assets,

Maritime Services and Rickmers-Linie cover a broad range

of services in the shipping supply chain and complement

each other supremely. Opportunities for growth are to be

had in all three business segments - either organically or

through active consolidation of the market. The aim of the

Rickmers Group is to set standards in its markets and to

offer clients premium services at very good performance

ratios. The fact that we cover a broad range of services in

the shipping supply chain enables us to have an excellent

understanding of our clients.

3. Expanding business in Asia and South America

The growth potential for trans-Pacific liner services, for

routes to South America and within Asia is highly promising,

which is why Rickmers-Linie is currently working intensely

to build up sales and new liner services in these areas.

The Maritime Services business segment has begun ac-

quiring new clients in Asia thanks to its skills in tech-

nical and operational fleet management. Maritime

Services is increasingly aiming to offer its services to

third-party companies and to gain additional cli-

ents, especially in Europe and Asia. On top of this, the

business segment is expanding its ability to recruit

new crew: Rickmers is the first international company

to hold a licence to crew seafarers from the People’s

Republic of China.

4. Creating added value as a service provider

Rickmers is an ideal partner for institutional investors

looking to exploit opportunities in the shipping market

and to control risks. In conjunction with the Maritime

Services business segment, Maritime Assets can coordinate

shipyard selection, newbuild design and supervision, and

the chartering out of ships to top-quality clients on be-

half of investors. It can also provide financial controlling,

reporting and accounting services and compile exit sce-

narios. Rickmers sees considerable potential in this service

business. Rickmers also offers to manage ships on behalf

of financing partners whose owners are no longer able

to cover on-going financing costs. As service providers to

these financers, Rickmers can significantly improve the

profitability of the ships by investing in measures such as

energy efficiency that have a relatively short payback peri-

od and by optimising operational processes. Rickmers also

offers solutions for special situations: in conjunction with

43Annual Report 2012 Group Management Report

Maritime Services, for example, Maritime Assets made two

construction contracts for multi-purpose carriers commer-

cially viable for an independent owner and the financing

bank. Both ships were originally commissioned by a com-

pany that has since become insolvent. The Rickmers Group

can significantly grow its services business and generate

high cash flows, all without having to tie up capital.

5. Exploiting energy-efficiency management to competi-

tive advantage

Through successful energy-efficiency management and

overall low ship operating costs, high capacity utilisation

at premium rates can still be achieved in a market char-

acterised by over-capacity. With fuel costs now accounting

for more than three-quarters of a ship’s operating costs,

charter clients much prefer fuel-saving vessels. This is

why we have initiated a comprehensive energy-efficiency

programme for our existing fleet. In terms of energy ef-

ficiency management, Rickmers is a global leader in the

shipping industry. Rickmers is the first German company

in the maritime industry to be certified in line with the

ISO 50001 energy management system standard.

6. Exploiting the low cost of newbuilds

The price of vessel newbuilds has today reached a historic

low, falling 40 percent since 2008. Moreover, vessels we

commission today will consume around 30 percent less

fuel than ships being delivered now. There are exciting op-

portunities in size classes over 5,000 TEU, especially in the

intra-Asian market and the trans-Pacific business which

make investing in newbuilds an attractive proposition even

in 2013 and beyond. However, other critical factors include

an intensive examination of terms offered by shipyards,

the energy efficiency of the vessels, the financial environ-

ment and the anticipated developments in the relevant

markets when decisions are made.

7. Managing ships analogous to a company production unit

The profit-oriented, commercially successful management

of ships is founded on the one hand on professional asset

management and, on the other, on entrepreneurial opera-

tional management. Rickmers achieves premium technical

quality, high safety standards and optimal vessel operating

costs through the concept of ‘ship-centric management’,

a system that handles a ship in a manner analogous to

a production unit within a company. Our ‘life cycle ap-

proach’ integrates best practices in all areas and ensures

cost-favourable, reliable operating procedures with pre-

dictable costs across the ship’s life cycle. This requires both

a well-trained crew and on-board management with an

entrepreneurial mind-set. For Rickmers, this business

management of a vessel is elementary to its corporate

strategy.

8. Investing in people

The Rickmers Group has recognised that employee train-

ing and development is crucial to the company’s achieve-

ment of its goals. This is why it has created a systematic

approach to personnel development and, in the Rickmers

Academy, created a central facility for learning and con-

tinuing education for our employees on shore. In interac-

tive courses our captains and officers are prepared for their

management tasks. For on-board teams, Rickmers provides

special courses focusing amongst other things on energy

management and on the provision of safe and appeal-

ing working and living conditions on board. Also, Rickmers

crewing programme has not only been developed for on-

board crews, but also as a key function for the professional

and targeted recruitment of employees within the holding

company.

1.3 Organisation and management structure

As well as Rickmers Holding GmbH & Cie. KG, the Rickmers

Group comprises 103 Group companies and seven consoli-

dated companies in which we have a non-controlling in-

terest. Rickmers Holding and its affiliated companies are

represented by over 20 branches in eleven countries (Ger-

many, Belgium, Isle of Man, Cyprus, Romania, Philippines,

China, Korea, Japan, Singapore, USA) and more than 50 sales

agencies.

Rickmers Holding is managed by a three-person Executive

Board - the Chairman, the CEO and the Deputy CEO & CFO.

Responsibility for the three business segments Maritime

Assets, Maritime Services and Rickmers-Linie lies with the

Global Heads of the respective business segments. As well

as Rickmers Holding, the main companies in the three seg-

ments are Rickmers Reederei (Maritime Assets), Rickmers

Shipmanagement (Maritime Services) and Rickmers-Linie

(Rickmers-Linie). The Deputy CFO, the Chief Treasury & Risk

Officer, the Global Heads of the three business segments

44 Rickmers GroupGroup Management Report

and the Chief Operating Officer of Rickmers-Linie make up

the Extended Board Committee of the Rickmers Group. In

this function, the Executive Board supports and advises the

Group in its work.

The Executive Board is also advised by an Advisory Board.

Effective controls and monitoring through competent

corporate governance

Rickmers Group corporate governance was further devel-

oped in 2012 and widely follows the “Deutsche Corporate

Governance Kodex” (German Corporate Governance Code).

As such, the company takes account of its special nature as

a family-owned enterprise and its legal form as a GmbH &

Cie. KG. In 2012, the Executive Board agreed a new ‘Chart

of Authority’ that defines decision-making authorities in

terms of financial amounts.

The Rickmers-Linie segment of the Rickmers Group, which

has a relatively larger client base, established a Code of

Conduct that is to be extended across the whole Group in

2013. Compliance programmes delivered worldwide raised

Rickmers-Linie employees’ awareness of critical issues. The

compliance seminars are to be continued across the whole

Rickmers Group.

Furthermore, Rickmers extended its legal department na-

tionally and internationally in 2012 and developed an IT-

Organisation of the Rickmers Group

Advisory Board

Bertram R. C. Rickmers

Ronald D. Widdows1

CEO

Corporate Communi-cations

Prof Dr Mark-Ken ErdmannDeputy CFO

Maritime AssetsHolger Strack, Global Head Maritime Assets

Rickmers ReedereiHamburg, Germany(100 %)

Rickmers ShipmanagementHamburg, Germany (100 %)

Rickmers-LinieHamburg, Germany (100 %)

PolarisDouglas, Isle of Man (100 %)

Global ManagementLimassol, Cyprus (100 %)

Rickmers-Linie (Singapore) Singapore, Singapore (100 %)

Rickmers Trust ManagementSingapore, Singapore (100 %)

Global Marine InsuranceBrokerage ServicesLimassol, Cyprus (50 %)

Rickmers (Korea)Seoul, South Korea (100 %)

Rickmers MaritimeSingapore, Singapore (33,1 %)3

Rickmers Shipping (Shanghai) Shanghai, China (80 %)

Rickmers Marine AgencyConstanta, Romania (100 %)

MCC Marine Consulting & Contracting Hamburg, Germany (100 %)

Maersk-Rickmers U.S. Flag Project CarrierDelaware, USA (50 %)

Harper PetersenHamburg, Germany (50 %)